OBJECTIVES OF TIME SERIES ANALYSIS

|

|

|

- Cornelius Lynch

- 5 years ago

- Views:

Transcription

1

2 OBJECTIVES OF TIME SERIES ANALYSIS Undersanding he dynamic or imedependen srucure of he observaions of a single series (univariae analysis) Forecasing of fuure observaions Asceraining he leading, lagging and feedback relaionships among several series (mulivariae analysis) 2

3 STEPS IN TIME SERIES ANALYSIS Model Idenificaion Time Series plo of he series Check for he exisence of a rend or seasonaliy Check for he sharp changes in behavior Check for possible ouliers Remove he rend and he seasonal componen o ge saionary residuals. Esimaion MME MLE Diagnosic Checking Normaliy of error erms Independency of error erms Consan error variance (Homoscedasiciy) Forecasing Exponenial smoohing mehods Minimum MSE forecasing 3

4 CHARACTERISTICS OF A SERIES For a ime series THE MEAN FUNCTION: E Exiss iff EY. THE VARIANCE FUNCTION: 2 0 Y, 0,, 2, Y The expeced value of he process a ime. Var Y E Y E Y 0 0 4

5 CHARACTERISTICS OF A SERIES THE AUTOCOVARIANCE FUNCTION:, s Cov E Y, Y YY ;, s 0,, 2, s THE AUTOCORRELATION FUNCTION:, s s Corr Y, Ys,, s E s Y Y s Covariance beween he value a ime and he value a ime s of a sochasic process Y., s s The correlaion of he series wih iself s 5

6 EXAMPLE Moving average process: Le i.i.d.(0, ), and X =

7 EXAMPLE RANDOM WALK: Le e,e 2, be a sequence of i.i.d. rvs wih 0 mean and variance. The observed ime series is obained as 7 2 e n Y,,2,, e Y Y e e Y e Y Y e e e Y e Y Y e e Y e Y

8 STATIONARITY The mos vial and common assumpion in ime series analysis. The basic idea of saionariy is ha he probabiliy laws governing he process do no change wih ime. The process is in saisical equilibrium. 8

9

10

11

12 TYPES OF STATIONARITY STRICT (STRONG OR COMPLETE) STATIONARY PROCESS: Consider a finie se of r.v.s. Y, Y,, Y from a sochasic process 2 n Y w, ; 0,, 2,. The n-dimensional disribuion funcion is defined by F y y,, y P w: Y y,, Y Y y, Y,, Y, 2 n 2 n where y i, i=, 2,, n are any real numbers. n n 2

13 STRONG STATIONARITY A process is said o be firs order saionary in disribuion, if is one dimensional disribuion funcion is ime-invarian, i.e., y F y for any and k. FY Y k Second order saionary in disribuion if y, y F y y for any, and k. FY, Y 2 Y, Y, 2 k k n-h order saionary in disribuion if F y, y F y, y for any,, and k. Y,, Y, n Y,, Y, n k n k n n 3

14 STRONG STATIONARITY n-h order saionariy in disribuion = srong saionariy Shifing he ime origin by an amoun k has no effec on he join disribuion, which mus herefore depend only on ime inervals beween, 2,, n, no on absolue ime,. 4

15

16 STRONG STATIONARITY So, for a srong saionary process i) ii) iii) iv) 6 y y f y y f n Y Y n Y Y k n k n,,,,,,,, k E Y Y E k k,, Expeced value of a series is consan over ime, no a funcion of ime k Y Var Y Var k k,, The variance of a series is consan over ime, homoscedasic. h k s k s k s k s k s k s k Y Cov Y Y Cov Y,,,,,, No consan, no depend on ime, depends on ime inerval, which we call lag, k

17 STRONG STATIONARITY Y Y Y 3 Y 2 Y n ) ( ,,,,, Y Y Cov Y Y Cov Y Y Cov Y Y Cov Y Y Cov n n n n Affeced from ime lag, k...

18 STRONG STATIONARITY v) Le =-k and s=, I is usually impossible o verify a disribuion paricularly a join disribuion funcion from an observed ime series. So, we use weaker sense of saionariy. 8 h k s k s k s k s k s k s k Y Y Corr Y Y Corr,,,,,, k k k k,,,,

19 WEAK STATIONARITY WEAK (COVARIANCE) STATIONARITY OR STATIONARITY IN WIDE SENSE: A ime series is said o be covariance saionary if is firs and second order momens are unaffeced by a change of ime origin. Tha is, we have consan mean and variance wih covariance and correlaion beings funcions of he ime difference only. 9

20 WEAK STATIONARITY E Y Var Cov Corr Y Y,, Y, Y, Y, k 2 k, From, now on, when we say saionary, we imply weak saionariy. k k 20

21

22

23 EXAMPLE Consider a ime series {Y } where Y =e and e i.i.d.(0, 2 ). Is he process saionary? 23

24 EXAMPLE MOVING AVERAGE: Suppose ha {Y } is consruced as Y e e 2 and e i.i.d.(0, 2 ). Is he process {Y } saionary? 24

25 EXAMPLE RANDOM WALK Y e e 2 e where e i.i.d.(0, 2 ). Is he process {Y } saionary? 25

26 EXAMPLE Suppose ha ime series has he form Y a b e where a and b are consans and {e } is a weakly saionary process wih mean 0 and auocovariance funcion k. Is {Y } saionary? 26

27 EXAMPLE where e i.i.d.(0, 2 ). Is he process {Y } saionary? Y e 27

28 STRONG VERSUS WEAK STATIONARITY Sric saionariy means ha he join disribuion only depends on he difference h, no he ime (,..., k ). Finie variance is no assumed in he definiion of srong saionariy, herefore, sric saionariy does no necessarily imply weak saionariy. For example, processes like i.i.d. Cauchy is sricly saionary bu no weak saionary. A nonlinear funcion of a sric saionary variable is sill sricly saionary, bu his is no rue for weak saionary. For example, he square of a covariance saionary process may no have finie variance. Weak saionariy usually does no imply sric saionariy as higher momens of he process may depend on ime. 28

29 STRONG VERSUS WEAK STATIONARITY If process {X } is a Gaussian ime series, which means ha he disribuion funcions of {X } are all mulivariae Normal, weak saionary also implies sric saionary. This is because a mulivariae Normal disribuion is fully characerized by is firs wo momens. 29

30 STRONG VERSUS WEAK STATIONARITY For example, a whie noise is saionary bu may no be sric saionary, bu a Gaussian whie noise is sric saionary. Also, general whie noise only implies uncorrelaion while Gaussian whie noise also implies independence. Because if a process is Gaussian, uncorrelaion implies independence. Therefore, a Gaussian whie noise is jus i.i.d. N(0, 2 ). 30

31 STATIONARITY AND NONSTATIONARITY Saionary and nonsaionary processes are very differen in heir properies, and hey require differen inference procedures. 3

32

33 Noe he difference beween he (log-) price and he reurn of he S&P500.. The laer is mean-revering around zero, he former is no

34

35

36

37

38

39 F( B) X = m +Q( B)e B is he backward operaor(also denoed as L, lag operaor)

40 BX = X - B 2 X = B(BX ) = BX - = X -2 B k X = X -k

41

k")

42 D k = ( - B) k

43

44

45

46

47

48

49

50

51

52

53

54 Expeced value of MA(q) q q y E E Variance of MA(q) q q q y y Var Var Auocovariance of MA(q) q k q k q k q k k q q y q q k k k E k.,,2,, 0, 2 Auocorelaion of MA(q) q k q k y y y q q q k k k k k.,,2,, / 0, ε whie noise

55 Firs Order Moving Average Process MA() q= y = m +e -q e - e whie noise Auocovariance of MA(q) g y (0) = s 2 2 ( +q ) g y () = -q s 2 g y (k) = 0, k > Auocorelaion of MA(q) y 2 ( k) 0, k y y

56 Second Order Moving Average MA(2) process y B B Auocovariance of MA(q) g y (0) = s 2 +q 2 2 ( +q 2 ) g y () = s 2 (-q +q q 2 ) g y (2) = s 2 (-q 2 ) g y (k) = 0, k > 2 Auocorelaion of MA(q) r y ( ) = -q +q q 2 +q 2 2 +q 2 r y ( 2) = -q 2 +q 2 +q 2 2 r y (k) = 0, k > 2 56

57 Inveribiliy of MA models Inverible moving average process: The MA(q) process k k P is inverible if i has an absolue summable infinie AR represenaion k I can be shown: The infinie AR represenaion for MA(q) y i y i i, i i 57

58

59

60

61

62

63

64

65

66

67

68

69

70

71

72

73

74

75

76

77

78

79

80

81 Firs order exponenial smoohing Firs-order exponenial smoohing: linear combinaion of he curren observaion & he smoohed observaion a he previous ime uni ~ y y T ~ y T ~ y y T ( ) ~ y T Discoun facor : weigh on he las observaion ( ) : weigh on he smoohed value of he previous observaions

82 ~ The iniial value y 0 2 commonly used esimaes of ~ y 0 ~ y y 0 If he changes in he process are expeced o occur early & fas ~ y0 y If he process a he beginning is consan

83 The value of As ges closer o, & more emphasis is given in he las observaions : he smoohed values follow he original values more closely 0: ~ y ~ T y : ~ yt y T 0 The smoohed values equal o a consan The leas smoohed version of he original ime series Values recommended Choice of he smoohing consan: Subjecive: depending of willingness o have fas adapiviy or more rigidiy. 2 Choice advocaed by Brown (invenor of he mehod): λ = Objecive: consan chosen o minimize he sum of squared forecas errors

84 Use exponenial smoohers for forecasing A ime T, we wish o forecas observaion a ime T+, or a ime T + ˆ y T T sep ahead forecas Consan Process y 0 0 Can be esimaed by he firs-order exponenial smooher Forecas : y ˆ ( T ) ~ T y T A ime T+ ˆ T y T y T y ~ yˆ ( ) yˆ T yt T T yˆ ˆ () ˆ T ( T) yt yt yt yˆ () e () T T e ( ) y ˆ T T yt ( T) One-sep-ahead forecas error

85 yˆ ˆ () ˆ T ( T) yt yt yt yˆ () e () T T Our forecas for he nex observaion is our previous forecas for he curren observaion plus a fracion of he forecas error we made in forecasing he curren observaion

86 Hol s Exponenial smoohing Hol s wo parameer exponenial smoohing mehod is an exension of simple exponenial smoohing. I adds a growh facor (or rend facor) o he smoohing equaion as a way of adjusing for he rend.

87 Hol s Exponenial smoohing Three equaions and wo smoohing consans are used in he model. The exponenially smoohed series or curren level esimae. L y The rend esimae. ( )( L b ) b ( L L ) ( ) b Forecas m periods ino he fuure. F m L mb

88 Hol s Exponenial smoohing Three equaions and wo smoohing consans are used in he model. The exponenially smoohed series or curren level esimae. L y The rend esimae. ( )( L b ) b ( L L ) ( ) b Forecas m periods ino he fuure. F m L mb

89 Hol s Exponenial smoohing L = Esimae of he level of he series a ime = smoohing consan for he daa. y = new observaion or acual value of series in period. = smoohing consan for rend esimae b = esimae of he slope of he series a ime m = periods o be forecas ino he fuure.

90 Hol s Exponenial smoohing The weigh and can be seleced subjecively or by minimizing a measure of forecas error such as RMSE. Large weighs resul in more rapid changes in he componen. Small weighs resul in less rapid changes.

91 Hol s Exponenial smoohing The iniializaion process for Hol s linear exponenial smoohing requires wo esimaes: One o ge he firs smoohed value for L The oher o ge he rend b. One alernaive is o se L = y and b or b or b y y y y

Diebold, Chapter 7. Francis X. Diebold, Elements of Forecasting, 4th Edition (Mason, Ohio: Cengage Learning, 2006). Chapter 7. Characterizing Cycles

. Chapter 7. Characterizing Cycles") Diebold, Chaper 7 Francis X. Diebold, Elemens of Forecasing, 4h Ediion (Mason, Ohio: Cengage Learning, 006). Chaper 7. Characerizing Cycles Afer compleing his reading you should be able o: Define covariance

Diebold, Chaper 7 Francis X. Diebold, Elemens of Forecasing, 4h Ediion (Mason, Ohio: Cengage Learning, 006). Chaper 7. Characerizing Cycles Afer compleing his reading you should be able o: Define covariance

Smoothing. Backward smoother: At any give T, replace the observation yt by a combination of observations at & before T

Smoohing Consan process Separae signal & noise Smooh he daa: Backward smooher: A an give, replace he observaion b a combinaion of observaions a & before Simple smooher : replace he curren observaion wih

Smoohing Consan process Separae signal & noise Smooh he daa: Backward smooher: A an give, replace he observaion b a combinaion of observaions a & before Simple smooher : replace he curren observaion wih

14 Autoregressive Moving Average Models

14 Auoregressive Moving Average Models In his chaper an imporan parameric family of saionary ime series is inroduced, he family of he auoregressive moving average, or ARMA, processes. For a large class

14 Auoregressive Moving Average Models In his chaper an imporan parameric family of saionary ime series is inroduced, he family of he auoregressive moving average, or ARMA, processes. For a large class

- The whole joint distribution is independent of the date at which it is measured and depends only on the lag.

Saionary Processes Sricly saionary - The whole join disribuion is indeenden of he dae a which i is measured and deends only on he lag. - E y ) is a finie consan. ( - V y ) is a finie consan. ( ( y, y s

Saionary Processes Sricly saionary - The whole join disribuion is indeenden of he dae a which i is measured and deends only on he lag. - E y ) is a finie consan. ( - V y ) is a finie consan. ( ( y, y s

Types of Exponential Smoothing Methods. Simple Exponential Smoothing. Simple Exponential Smoothing

M Business Forecasing Mehods Exponenial moohing Mehods ecurer : Dr Iris Yeung Room No : P79 Tel No : 788 8 Types of Exponenial moohing Mehods imple Exponenial moohing Double Exponenial moohing Brown s

M Business Forecasing Mehods Exponenial moohing Mehods ecurer : Dr Iris Yeung Room No : P79 Tel No : 788 8 Types of Exponenial moohing Mehods imple Exponenial moohing Double Exponenial moohing Brown s

Stationary Time Series

3-Jul-3 Time Series Analysis Assoc. Prof. Dr. Sevap Kesel July 03 Saionary Time Series Sricly saionary process: If he oin dis. of is he same as he oin dis. of ( X,... X n) ( X h,... X nh) Weakly Saionary

3-Jul-3 Time Series Analysis Assoc. Prof. Dr. Sevap Kesel July 03 Saionary Time Series Sricly saionary process: If he oin dis. of is he same as he oin dis. of ( X,... X n) ( X h,... X nh) Weakly Saionary

State-Space Models. Initialization, Estimation and Smoothing of the Kalman Filter

Sae-Space Models Iniializaion, Esimaion and Smoohing of he Kalman Filer Iniializaion of he Kalman Filer The Kalman filer shows how o updae pas predicors and he corresponding predicion error variances when

Sae-Space Models Iniializaion, Esimaion and Smoohing of he Kalman Filer Iniializaion of he Kalman Filer The Kalman filer shows how o updae pas predicors and he corresponding predicion error variances when

Vectorautoregressive Model and Cointegration Analysis. Time Series Analysis Dr. Sevtap Kestel 1

Vecorauoregressive Model and Coinegraion Analysis Par V Time Series Analysis Dr. Sevap Kesel 1 Vecorauoregression Vecor auoregression (VAR) is an economeric model used o capure he evoluion and he inerdependencies

Vecorauoregressive Model and Coinegraion Analysis Par V Time Series Analysis Dr. Sevap Kesel 1 Vecorauoregression Vecor auoregression (VAR) is an economeric model used o capure he evoluion and he inerdependencies

Linear Gaussian State Space Models

Linear Gaussian Sae Space Models Srucural Time Series Models Level and Trend Models Basic Srucural Model (BSM Dynamic Linear Models Sae Space Model Represenaion Level, Trend, and Seasonal Models Time Varying

Linear Gaussian Sae Space Models Srucural Time Series Models Level and Trend Models Basic Srucural Model (BSM Dynamic Linear Models Sae Space Model Represenaion Level, Trend, and Seasonal Models Time Varying

Exponential Smoothing

Exponenial moohing Inroducion A simple mehod for forecasing. Does no require long series. Enables o decompose he series ino a rend and seasonal effecs. Paricularly useful mehod when here is a need o forecas

Exponenial moohing Inroducion A simple mehod for forecasing. Does no require long series. Enables o decompose he series ino a rend and seasonal effecs. Paricularly useful mehod when here is a need o forecas

Chapter 15. Time Series: Descriptive Analyses, Models, and Forecasting

Chaper 15 Time Series: Descripive Analyses, Models, and Forecasing Descripive Analysis: Index Numbers Index Number a number ha measures he change in a variable over ime relaive o he value of he variable

Chaper 15 Time Series: Descripive Analyses, Models, and Forecasing Descripive Analysis: Index Numbers Index Number a number ha measures he change in a variable over ime relaive o he value of he variable

Section 4 NABE ASTEF 232

Secion 4 NABE ASTEF 3 APPLIED ECONOMETRICS: TIME-SERIES ANALYSIS 33 Inroducion and Review The Naure of Economic Modeling Judgemen calls unavoidable Economerics an ar Componens of Applied Economerics Specificaion

Secion 4 NABE ASTEF 3 APPLIED ECONOMETRICS: TIME-SERIES ANALYSIS 33 Inroducion and Review The Naure of Economic Modeling Judgemen calls unavoidable Economerics an ar Componens of Applied Economerics Specificaion

Licenciatura de ADE y Licenciatura conjunta Derecho y ADE. Hoja de ejercicios 2 PARTE A

Licenciaura de ADE y Licenciaura conjuna Derecho y ADE Hoja de ejercicios PARTE A 1. Consider he following models Δy = 0.8 + ε (1 + 0.8L) Δ 1 y = ε where ε and ε are independen whie noise processes. In

Licenciaura de ADE y Licenciaura conjuna Derecho y ADE Hoja de ejercicios PARTE A 1. Consider he following models Δy = 0.8 + ε (1 + 0.8L) Δ 1 y = ε where ε and ε are independen whie noise processes. In

Methodology. -ratios are biased and that the appropriate critical values have to be increased by an amount. that depends on the sample size.

Mehodology. Uni Roo Tess A ime series is inegraed when i has a mean revering propery and a finie variance. I is only emporarily ou of equilibrium and is called saionary in I(0). However a ime series ha

Mehodology. Uni Roo Tess A ime series is inegraed when i has a mean revering propery and a finie variance. I is only emporarily ou of equilibrium and is called saionary in I(0). However a ime series ha

Lecture 3: Exponential Smoothing

NATCOR: Forecasing & Predicive Analyics Lecure 3: Exponenial Smoohing John Boylan Lancaser Cenre for Forecasing Deparmen of Managemen Science Mehods and Models Forecasing Mehod A (numerical) procedure

NATCOR: Forecasing & Predicive Analyics Lecure 3: Exponenial Smoohing John Boylan Lancaser Cenre for Forecasing Deparmen of Managemen Science Mehods and Models Forecasing Mehod A (numerical) procedure

Distribution of Estimates

Disribuion of Esimaes From Economerics (40) Linear Regression Model Assume (y,x ) is iid and E(x e )0 Esimaion Consisency y α + βx + he esimaes approach he rue values as he sample size increases Esimaion

Disribuion of Esimaes From Economerics (40) Linear Regression Model Assume (y,x ) is iid and E(x e )0 Esimaion Consisency y α + βx + he esimaes approach he rue values as he sample size increases Esimaion

ECON 482 / WH Hong Time Series Data Analysis 1. The Nature of Time Series Data. Example of time series data (inflation and unemployment rates)

") ECON 48 / WH Hong Time Series Daa Analysis. The Naure of Time Series Daa Example of ime series daa (inflaion and unemploymen raes) ECON 48 / WH Hong Time Series Daa Analysis The naure of ime series daa

ECON 48 / WH Hong Time Series Daa Analysis. The Naure of Time Series Daa Example of ime series daa (inflaion and unemploymen raes) ECON 48 / WH Hong Time Series Daa Analysis The naure of ime series daa

Lecture Notes 2. The Hilbert Space Approach to Time Series

Time Series Seven N. Durlauf Universiy of Wisconsin. Basic ideas Lecure Noes. The Hilber Space Approach o Time Series The Hilber space framework provides a very powerful language for discussing he relaionship

Time Series Seven N. Durlauf Universiy of Wisconsin. Basic ideas Lecure Noes. The Hilber Space Approach o Time Series The Hilber space framework provides a very powerful language for discussing he relaionship

Quarterly ice cream sales are high each summer, and the series tends to repeat itself each year, so that the seasonal period is 4.

Seasonal models Many business and economic ime series conain a seasonal componen ha repeas iself afer a regular period of ime. The smalles ime period for his repeiion is called he seasonal period, and

Seasonal models Many business and economic ime series conain a seasonal componen ha repeas iself afer a regular period of ime. The smalles ime period for his repeiion is called he seasonal period, and

Institute for Mathematical Methods in Economics. University of Technology Vienna. Singapore, May Manfred Deistler

MULTIVARIATE TIME SERIES ANALYSIS AND FORECASTING Manfred Deisler E O S Economerics and Sysems Theory Insiue for Mahemaical Mehods in Economics Universiy of Technology Vienna Singapore, May 2004 Inroducion

MULTIVARIATE TIME SERIES ANALYSIS AND FORECASTING Manfred Deisler E O S Economerics and Sysems Theory Insiue for Mahemaical Mehods in Economics Universiy of Technology Vienna Singapore, May 2004 Inroducion

Nature Neuroscience: doi: /nn Supplementary Figure 1. Spike-count autocorrelations in time.

Supplemenary Figure 1 Spike-coun auocorrelaions in ime. Normalized auocorrelaion marices are shown for each area in a daase. The marix shows he mean correlaion of he spike coun in each ime bin wih he spike

Supplemenary Figure 1 Spike-coun auocorrelaions in ime. Normalized auocorrelaion marices are shown for each area in a daase. The marix shows he mean correlaion of he spike coun in each ime bin wih he spike

Unit Root Time Series. Univariate random walk

Uni Roo ime Series Univariae random walk Consider he regression y y where ~ iid N 0, he leas squares esimae of is: ˆ yy y y yy Now wha if = If y y hen le y 0 =0 so ha y j j If ~ iid N 0, hen y ~ N 0, he

Uni Roo ime Series Univariae random walk Consider he regression y y where ~ iid N 0, he leas squares esimae of is: ˆ yy y y yy Now wha if = If y y hen le y 0 =0 so ha y j j If ~ iid N 0, hen y ~ N 0, he

Elements of Stochastic Processes Lecture II Hamid R. Rabiee

Sochasic Processes Elemens of Sochasic Processes Lecure II Hamid R. Rabiee Overview Reading Assignmen Chaper 9 of exbook Furher Resources MIT Open Course Ware S. Karlin and H. M. Taylor, A Firs Course

Sochasic Processes Elemens of Sochasic Processes Lecure II Hamid R. Rabiee Overview Reading Assignmen Chaper 9 of exbook Furher Resources MIT Open Course Ware S. Karlin and H. M. Taylor, A Firs Course

Linear Combinations of Volatility Forecasts for the WIG20 and Polish Exchange Rates

Eliza Buszkowska Universiy of Poznań, Poland Linear Combinaions of Volailiy Forecass for he WIG0 and Polish Exchange Raes Absrak. As is known forecas combinaions may be beer forecass hen forecass obained

Eliza Buszkowska Universiy of Poznań, Poland Linear Combinaions of Volailiy Forecass for he WIG0 and Polish Exchange Raes Absrak. As is known forecas combinaions may be beer forecass hen forecass obained

Financial Econometrics Jeffrey R. Russell Midterm Winter 2009 SOLUTIONS

Name SOLUTIONS Financial Economerics Jeffrey R. Russell Miderm Winer 009 SOLUTIONS You have 80 minues o complee he exam. Use can use a calculaor and noes. Try o fi all your work in he space provided. If

Name SOLUTIONS Financial Economerics Jeffrey R. Russell Miderm Winer 009 SOLUTIONS You have 80 minues o complee he exam. Use can use a calculaor and noes. Try o fi all your work in he space provided. If

Properties of Autocorrelated Processes Economics 30331

Properies of Auocorrelaed Processes Economics 3033 Bill Evans Fall 05 Suppose we have ime series daa series labeled as where =,,3, T (he final period) Some examples are he dail closing price of he S&500,

Properies of Auocorrelaed Processes Economics 3033 Bill Evans Fall 05 Suppose we have ime series daa series labeled as where =,,3, T (he final period) Some examples are he dail closing price of he S&500,

STAD57 Time Series Analysis. Lecture 5

STAD57 Time Series Analysis Lecure 5 1 Exploraory Daa Analysis Check if given TS is saionary: µ is consan σ 2 is consan γ(s,) is funcion of h= s If no, ry o make i saionary using some of he mehods below:

STAD57 Time Series Analysis Lecure 5 1 Exploraory Daa Analysis Check if given TS is saionary: µ is consan σ 2 is consan γ(s,) is funcion of h= s If no, ry o make i saionary using some of he mehods below:

Chapter 5. Heterocedastic Models. Introduction to time series (2008) 1

1") Chaper 5 Heerocedasic Models Inroducion o ime series (2008) 1 Chaper 5. Conens. 5.1. The ARCH model. 5.2. The GARCH model. 5.3. The exponenial GARCH model. 5.4. The CHARMA model. 5.5. Random coefficien

Chaper 5 Heerocedasic Models Inroducion o ime series (2008) 1 Chaper 5. Conens. 5.1. The ARCH model. 5.2. The GARCH model. 5.3. The exponenial GARCH model. 5.4. The CHARMA model. 5.5. Random coefficien

Kriging Models Predicting Atrazine Concentrations in Surface Water Draining Agricultural Watersheds

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 Kriging Models Predicing Arazine Concenraions in Surface Waer Draining Agriculural Waersheds Paul L. Mosquin, Jeremy Aldworh, Wenlin Chen Supplemenal Maerial Number

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 Kriging Models Predicing Arazine Concenraions in Surface Waer Draining Agriculural Waersheds Paul L. Mosquin, Jeremy Aldworh, Wenlin Chen Supplemenal Maerial Number

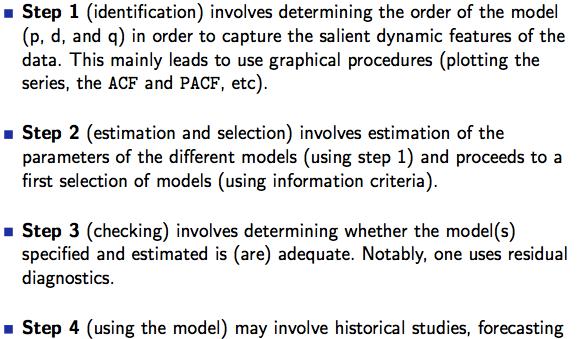

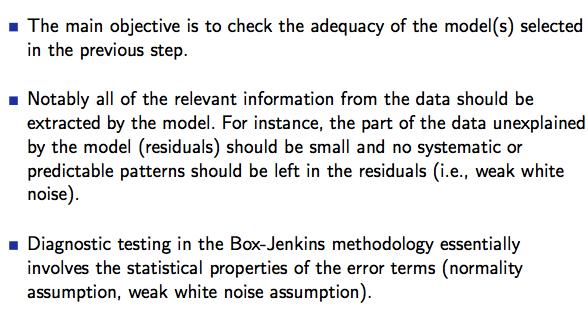

Chapter 3, Part IV: The Box-Jenkins Approach to Model Building

Chaper 3, Par IV: The Box-Jenkins Approach o Model Building The ARMA models have been found o be quie useful for describing saionary nonseasonal ime series. A parial explanaion for his fac is provided

Chaper 3, Par IV: The Box-Jenkins Approach o Model Building The ARMA models have been found o be quie useful for describing saionary nonseasonal ime series. A parial explanaion for his fac is provided

R t. C t P t. + u t. C t = αp t + βr t + v t. + β + w t

Exercise 7 C P = α + β R P + u C = αp + βr + v (a) (b) C R = α P R + β + w (c) Assumpions abou he disurbances u, v, w : Classical assumions on he disurbance of one of he equaions, eg. on (b): E(v v s P,

Exercise 7 C P = α + β R P + u C = αp + βr + v (a) (b) C R = α P R + β + w (c) Assumpions abou he disurbances u, v, w : Classical assumions on he disurbance of one of he equaions, eg. on (b): E(v v s P,

Introduction D P. r = constant discount rate, g = Gordon Model (1962): constant dividend growth rate.

: constant dividend growth rate.") Inroducion Gordon Model (1962): D P = r g r = consan discoun rae, g = consan dividend growh rae. If raional expecaions of fuure discoun raes and dividend growh vary over ime, so should he D/P raio. Since

Inroducion Gordon Model (1962): D P = r g r = consan discoun rae, g = consan dividend growh rae. If raional expecaions of fuure discoun raes and dividend growh vary over ime, so should he D/P raio. Since

Generalized Least Squares

Generalized Leas Squares Augus 006 1 Modified Model Original assumpions: 1 Specificaion: y = Xβ + ε (1) Eε =0 3 EX 0 ε =0 4 Eεε 0 = σ I In his secion, we consider relaxing assumpion (4) Insead, assume

Generalized Leas Squares Augus 006 1 Modified Model Original assumpions: 1 Specificaion: y = Xβ + ε (1) Eε =0 3 EX 0 ε =0 4 Eεε 0 = σ I In his secion, we consider relaxing assumpion (4) Insead, assume

Cointegration and Implications for Forecasting

Coinegraion and Implicaions for Forecasing Two examples (A) Y Y 1 1 1 2 (B) Y 0.3 0.9 1 1 2 Example B: Coinegraion Y and coinegraed wih coinegraing vecor [1, 0.9] because Y 0.9 0.3 is a saionary process

Coinegraion and Implicaions for Forecasing Two examples (A) Y Y 1 1 1 2 (B) Y 0.3 0.9 1 1 2 Example B: Coinegraion Y and coinegraed wih coinegraing vecor [1, 0.9] because Y 0.9 0.3 is a saionary process

BOX-JENKINS MODEL NOTATION. The Box-Jenkins ARMA(p,q) model is denoted by the equation. pwhile the moving average (MA) part of the model is θ1at

model is denoted by the equation. pwhile the moving average (MA) part of the model is θ1at") BOX-JENKINS MODEL NOAION he Box-Jenkins ARMA(,q) model is denoed b he equaion + + L+ + a θ a L θ a 0 q q. () he auoregressive (AR) ar of he model is + L+ while he moving average (MA) ar of he model is

BOX-JENKINS MODEL NOAION he Box-Jenkins ARMA(,q) model is denoed b he equaion + + L+ + a θ a L θ a 0 q q. () he auoregressive (AR) ar of he model is + L+ while he moving average (MA) ar of he model is

ST4064. Time Series Analysis. Lecture notes

ST4064 Time Series Analysis ST4064 Time Series Analysis Lecure noes ST4064 Time Series Analysis Ouline I II Inroducion o ime series analysis Saionariy and ARMA modelling. Saionariy a. Definiions b. Sric

ST4064 Time Series Analysis ST4064 Time Series Analysis Lecure noes ST4064 Time Series Analysis Ouline I II Inroducion o ime series analysis Saionariy and ARMA modelling. Saionariy a. Definiions b. Sric

Estimation Uncertainty

Esimaion Uncerainy The sample mean is an esimae of β = E(y +h ) The esimaion error is = + = T h y T b ( ) = = + = + = = = T T h T h e T y T y T b β β β Esimaion Variance Under classical condiions, where

Esimaion Uncerainy The sample mean is an esimae of β = E(y +h ) The esimaion error is = + = T h y T b ( ) = = + = + = = = T T h T h e T y T y T b β β β Esimaion Variance Under classical condiions, where

Distribution of Least Squares

Disribuion of Leas Squares In classic regression, if he errors are iid normal, and independen of he regressors, hen he leas squares esimaes have an exac normal disribuion, no jus asympoic his is no rue

Disribuion of Leas Squares In classic regression, if he errors are iid normal, and independen of he regressors, hen he leas squares esimaes have an exac normal disribuion, no jus asympoic his is no rue

Econ107 Applied Econometrics Topic 7: Multicollinearity (Studenmund, Chapter 8)

") I. Definiions and Problems A. Perfec Mulicollineariy Econ7 Applied Economerics Topic 7: Mulicollineariy (Sudenmund, Chaper 8) Definiion: Perfec mulicollineariy exiss in a following K-variable regression

I. Definiions and Problems A. Perfec Mulicollineariy Econ7 Applied Economerics Topic 7: Mulicollineariy (Sudenmund, Chaper 8) Definiion: Perfec mulicollineariy exiss in a following K-variable regression

Lesson 2, page 1. Outline of lesson 2

Lesson 2, page Ouline of lesson 2 Inroduce he Auocorrelaion Coefficien Undersand and define saionariy Discuss ransformaion Discuss rend and rend removal C:\Kyrre\sudier\drgrad\Kurs\series\lecure 02 03022.doc,

Lesson 2, page Ouline of lesson 2 Inroduce he Auocorrelaion Coefficien Undersand and define saionariy Discuss ransformaion Discuss rend and rend removal C:\Kyrre\sudier\drgrad\Kurs\series\lecure 02 03022.doc,

Solutions to Odd Number Exercises in Chapter 6

1 Soluions o Odd Number Exercises in 6.1 R y eˆ 1.7151 y 6.3 From eˆ ( T K) ˆ R 1 1 SST SST SST (1 R ) 55.36(1.7911) we have, ˆ 6.414 T K ( ) 6.5 y ye ye y e 1 1 Consider he erms e and xe b b x e y e b

1 Soluions o Odd Number Exercises in 6.1 R y eˆ 1.7151 y 6.3 From eˆ ( T K) ˆ R 1 1 SST SST SST (1 R ) 55.36(1.7911) we have, ˆ 6.414 T K ( ) 6.5 y ye ye y e 1 1 Consider he erms e and xe b b x e y e b

Γ(h)=0 h 0. Γ(h)=cov(X 0,X 0-h ). A stationary process is called white noise if its autocovariance

=0 h 0. Γ(h)=cov(X 0,X 0-h ). A stationary process is called white noise if its autocovariance") A family, Z,of random vecors : Ω R k defined on a probabiliy space Ω, A,P) is called a saionary process if he mean vecors E E =E M = M k E and he auocovariance marices are independen of. k cov, -h )=E

A family, Z,of random vecors : Ω R k defined on a probabiliy space Ω, A,P) is called a saionary process if he mean vecors E E =E M = M k E and he auocovariance marices are independen of. k cov, -h )=E

3.1.3 INTRODUCTION TO DYNAMIC OPTIMIZATION: DISCRETE TIME PROBLEMS. A. The Hamiltonian and First-Order Conditions in a Finite Time Horizon

3..3 INRODUCION O DYNAMIC OPIMIZAION: DISCREE IME PROBLEMS A. he Hamilonian and Firs-Order Condiions in a Finie ime Horizon Define a new funcion, he Hamilonian funcion, H. H he change in he oal value of

3..3 INRODUCION O DYNAMIC OPIMIZAION: DISCREE IME PROBLEMS A. he Hamilonian and Firs-Order Condiions in a Finie ime Horizon Define a new funcion, he Hamilonian funcion, H. H he change in he oal value of

Summer Term Albert-Ludwigs-Universität Freiburg Empirische Forschung und Okonometrie. Time Series Analysis

Summer Term 2009 Alber-Ludwigs-Universiä Freiburg Empirische Forschung und Okonomerie Time Series Analysis Classical Time Series Models Time Series Analysis Dr. Sevap Kesel 2 Componens Hourly earnings:

Summer Term 2009 Alber-Ludwigs-Universiä Freiburg Empirische Forschung und Okonomerie Time Series Analysis Classical Time Series Models Time Series Analysis Dr. Sevap Kesel 2 Componens Hourly earnings:

3.1 More on model selection

3. More on Model selecion 3. Comparing models AIC, BIC, Adjused R squared. 3. Over Fiing problem. 3.3 Sample spliing. 3. More on model selecion crieria Ofen afer model fiing you are lef wih a handful of

3. More on Model selecion 3. Comparing models AIC, BIC, Adjused R squared. 3. Over Fiing problem. 3.3 Sample spliing. 3. More on model selecion crieria Ofen afer model fiing you are lef wih a handful of

Zürich. ETH Master Course: L Autonomous Mobile Robots Localization II

Roland Siegwar Margaria Chli Paul Furgale Marco Huer Marin Rufli Davide Scaramuzza ETH Maser Course: 151-0854-00L Auonomous Mobile Robos Localizaion II ACT and SEE For all do, (predicion updae / ACT),

Roland Siegwar Margaria Chli Paul Furgale Marco Huer Marin Rufli Davide Scaramuzza ETH Maser Course: 151-0854-00L Auonomous Mobile Robos Localizaion II ACT and SEE For all do, (predicion updae / ACT),

Time series Decomposition method

Time series Decomposiion mehod A ime series is described using a mulifacor model such as = f (rend, cyclical, seasonal, error) = f (T, C, S, e) Long- Iner-mediaed Seasonal Irregular erm erm effec, effec,

Time series Decomposiion mehod A ime series is described using a mulifacor model such as = f (rend, cyclical, seasonal, error) = f (T, C, S, e) Long- Iner-mediaed Seasonal Irregular erm erm effec, effec,

L07. KALMAN FILTERING FOR NON-LINEAR SYSTEMS. NA568 Mobile Robotics: Methods & Algorithms

L07. KALMAN FILTERING FOR NON-LINEAR SYSTEMS NA568 Mobile Roboics: Mehods & Algorihms Today s Topic Quick review on (Linear) Kalman Filer Kalman Filering for Non-Linear Sysems Exended Kalman Filer (EKF)

L07. KALMAN FILTERING FOR NON-LINEAR SYSTEMS NA568 Mobile Roboics: Mehods & Algorihms Today s Topic Quick review on (Linear) Kalman Filer Kalman Filering for Non-Linear Sysems Exended Kalman Filer (EKF)

20. Applications of the Genetic-Drift Model

0. Applicaions of he Geneic-Drif Model 1) Deermining he probabiliy of forming any paricular combinaion of genoypes in he nex generaion: Example: If he parenal allele frequencies are p 0 = 0.35 and q 0

0. Applicaions of he Geneic-Drif Model 1) Deermining he probabiliy of forming any paricular combinaion of genoypes in he nex generaion: Example: If he parenal allele frequencies are p 0 = 0.35 and q 0

Økonomisk Kandidateksamen 2005(II) Econometrics 2. Solution

Econometrics 2. Solution") Økonomisk Kandidaeksamen 2005(II) Economerics 2 Soluion his is he proposed soluion for he exam in Economerics 2. For compleeness he soluion gives formal answers o mos of he quesions alhough his is no always

Økonomisk Kandidaeksamen 2005(II) Economerics 2 Soluion his is he proposed soluion for he exam in Economerics 2. For compleeness he soluion gives formal answers o mos of he quesions alhough his is no always

Vector autoregression VAR. Case 1

Vecor auoregression VAR So far we have focused mosl on models where deends onl on as. More generall we migh wan o consider oin models ha involve more han one variable. There are wo reasons: Firs, we migh

Vecor auoregression VAR So far we have focused mosl on models where deends onl on as. More generall we migh wan o consider oin models ha involve more han one variable. There are wo reasons: Firs, we migh

2 Univariate Stationary Processes

Univariae Saionary Processes As menioned in he inroducion, he publicaion of he exbook by GEORGE E.P. BOX and GWILYM M. JENKINS in 97 opened a new road o he analysis of economic ime series. This chaper

Univariae Saionary Processes As menioned in he inroducion, he publicaion of he exbook by GEORGE E.P. BOX and GWILYM M. JENKINS in 97 opened a new road o he analysis of economic ime series. This chaper

Forecasting optimally

I) ile: Forecas Evaluaion II) Conens: Evaluaing forecass, properies of opimal forecass, esing properies of opimal forecass, saisical comparison of forecas accuracy III) Documenaion: - Diebold, Francis

I) ile: Forecas Evaluaion II) Conens: Evaluaing forecass, properies of opimal forecass, esing properies of opimal forecass, saisical comparison of forecas accuracy III) Documenaion: - Diebold, Francis

ACE 562 Fall Lecture 4: Simple Linear Regression Model: Specification and Estimation. by Professor Scott H. Irwin

ACE 56 Fall 005 Lecure 4: Simple Linear Regression Model: Specificaion and Esimaion by Professor Sco H. Irwin Required Reading: Griffihs, Hill and Judge. "Simple Regression: Economic and Saisical Model

ACE 56 Fall 005 Lecure 4: Simple Linear Regression Model: Specificaion and Esimaion by Professor Sco H. Irwin Required Reading: Griffihs, Hill and Judge. "Simple Regression: Economic and Saisical Model

References are appeared in the last slide. Last update: (1393/08/19)

") SYSEM IDEIFICAIO Ali Karimpour Associae Professor Ferdowsi Universi of Mashhad References are appeared in he las slide. Las updae: 0..204 393/08/9 Lecure 5 lecure 5 Parameer Esimaion Mehods opics o be

SYSEM IDEIFICAIO Ali Karimpour Associae Professor Ferdowsi Universi of Mashhad References are appeared in he las slide. Las updae: 0..204 393/08/9 Lecure 5 lecure 5 Parameer Esimaion Mehods opics o be

Box-Jenkins Modelling of Nigerian Stock Prices Data

Greener Journal of Science Engineering and Technological Research ISSN: 76-7835 Vol. (), pp. 03-038, Sepember 0. Research Aricle Box-Jenkins Modelling of Nigerian Sock Prices Daa Ee Harrison Euk*, Barholomew

Greener Journal of Science Engineering and Technological Research ISSN: 76-7835 Vol. (), pp. 03-038, Sepember 0. Research Aricle Box-Jenkins Modelling of Nigerian Sock Prices Daa Ee Harrison Euk*, Barholomew

Regression with Time Series Data

Regression wih Time Series Daa y = β 0 + β 1 x 1 +...+ β k x k + u Serial Correlaion and Heeroskedasiciy Time Series - Serial Correlaion and Heeroskedasiciy 1 Serially Correlaed Errors: Consequences Wih

Regression wih Time Series Daa y = β 0 + β 1 x 1 +...+ β k x k + u Serial Correlaion and Heeroskedasiciy Time Series - Serial Correlaion and Heeroskedasiciy 1 Serially Correlaed Errors: Consequences Wih

Dynamic Models, Autocorrelation and Forecasting

ECON 4551 Economerics II Memorial Universiy of Newfoundland Dynamic Models, Auocorrelaion and Forecasing Adaped from Vera Tabakova s noes 9.1 Inroducion 9.2 Lags in he Error Term: Auocorrelaion 9.3 Esimaing

ECON 4551 Economerics II Memorial Universiy of Newfoundland Dynamic Models, Auocorrelaion and Forecasing Adaped from Vera Tabakova s noes 9.1 Inroducion 9.2 Lags in he Error Term: Auocorrelaion 9.3 Esimaing

How to Deal with Structural Breaks in Practical Cointegration Analysis

How o Deal wih Srucural Breaks in Pracical Coinegraion Analysis Roselyne Joyeux * School of Economic and Financial Sudies Macquarie Universiy December 00 ABSTRACT In his noe we consider he reamen of srucural

How o Deal wih Srucural Breaks in Pracical Coinegraion Analysis Roselyne Joyeux * School of Economic and Financial Sudies Macquarie Universiy December 00 ABSTRACT In his noe we consider he reamen of srucural

Recent Developments in the Unit Root Problem for Moving Averages

Recen Developmens in he Uni Roo Problem for Moving Averages Richard A. Davis Colorado Sae Universiy Mei-Ching Chen Chaoyang Insiue of echnology homas Miosch Universiy of Groningen Non-inverible MA() Model

Recen Developmens in he Uni Roo Problem for Moving Averages Richard A. Davis Colorado Sae Universiy Mei-Ching Chen Chaoyang Insiue of echnology homas Miosch Universiy of Groningen Non-inverible MA() Model

Testing the Random Walk Model. i.i.d. ( ) r

r") he random walk heory saes: esing he Random Walk Model µ ε () np = + np + Momen Condiions where where ε ~ i.i.d he idea here is o es direcly he resricions imposed by momen condiions. lnp lnp µ ( lnp lnp

he random walk heory saes: esing he Random Walk Model µ ε () np = + np + Momen Condiions where where ε ~ i.i.d he idea here is o es direcly he resricions imposed by momen condiions. lnp lnp µ ( lnp lnp

EXERCISES FOR SECTION 1.5

1.5 Exisence and Uniqueness of Soluions 43 20. 1 v c 21. 1 v c 1 2 4 6 8 10 1 2 2 4 6 8 10 Graph of approximae soluion obained using Euler s mehod wih = 0.1. Graph of approximae soluion obained using Euler

1.5 Exisence and Uniqueness of Soluions 43 20. 1 v c 21. 1 v c 1 2 4 6 8 10 1 2 2 4 6 8 10 Graph of approximae soluion obained using Euler s mehod wih = 0.1. Graph of approximae soluion obained using Euler

Vehicle Arrival Models : Headway

Chaper 12 Vehicle Arrival Models : Headway 12.1 Inroducion Modelling arrival of vehicle a secion of road is an imporan sep in raffic flow modelling. I has imporan applicaion in raffic flow simulaion where

Chaper 12 Vehicle Arrival Models : Headway 12.1 Inroducion Modelling arrival of vehicle a secion of road is an imporan sep in raffic flow modelling. I has imporan applicaion in raffic flow simulaion where

Wisconsin Unemployment Rate Forecast Revisited

Wisconsin Unemploymen Rae Forecas Revisied Forecas in Lecure Wisconsin unemploymen November 06 was 4.% Forecass Poin Forecas 50% Inerval 80% Inerval Forecas Forecas December 06 4.0% (4.0%, 4.0%) (3.95%,

Wisconsin Unemploymen Rae Forecas Revisied Forecas in Lecure Wisconsin unemploymen November 06 was 4.% Forecass Poin Forecas 50% Inerval 80% Inerval Forecas Forecas December 06 4.0% (4.0%, 4.0%) (3.95%,

ACE 562 Fall Lecture 8: The Simple Linear Regression Model: R 2, Reporting the Results and Prediction. by Professor Scott H.

ACE 56 Fall 5 Lecure 8: The Simple Linear Regression Model: R, Reporing he Resuls and Predicion by Professor Sco H. Irwin Required Readings: Griffihs, Hill and Judge. "Explaining Variaion in he Dependen

ACE 56 Fall 5 Lecure 8: The Simple Linear Regression Model: R, Reporing he Resuls and Predicion by Professor Sco H. Irwin Required Readings: Griffihs, Hill and Judge. "Explaining Variaion in he Dependen

Modeling Economic Time Series with Stochastic Linear Difference Equations

A. Thiemer, SLDG.mcd, 6..6 FH-Kiel Universiy of Applied Sciences Prof. Dr. Andreas Thiemer e-mail: andreas.hiemer@fh-kiel.de Modeling Economic Time Series wih Sochasic Linear Difference Equaions Summary:

A. Thiemer, SLDG.mcd, 6..6 FH-Kiel Universiy of Applied Sciences Prof. Dr. Andreas Thiemer e-mail: andreas.hiemer@fh-kiel.de Modeling Economic Time Series wih Sochasic Linear Difference Equaions Summary:

Nonstationarity-Integrated Models. Time Series Analysis Dr. Sevtap Kestel 1

Nonsaionariy-Inegraed Models Time Series Analysis Dr. Sevap Kesel 1 Diagnosic Checking Residual Analysis: Whie noise. P-P or Q-Q plos of he residuals follow a normal disribuion, he series is called a Gaussian

Nonsaionariy-Inegraed Models Time Series Analysis Dr. Sevap Kesel 1 Diagnosic Checking Residual Analysis: Whie noise. P-P or Q-Q plos of he residuals follow a normal disribuion, he series is called a Gaussian

I. Return Calculations (20 pts, 4 points each)

") Universiy of Washingon Spring 015 Deparmen of Economics Eric Zivo Econ 44 Miderm Exam Soluions This is a closed book and closed noe exam. However, you are allowed one page of noes (8.5 by 11 or A4 double-sided)

Universiy of Washingon Spring 015 Deparmen of Economics Eric Zivo Econ 44 Miderm Exam Soluions This is a closed book and closed noe exam. However, you are allowed one page of noes (8.5 by 11 or A4 double-sided)

Robust estimation based on the first- and third-moment restrictions of the power transformation model

h Inernaional Congress on Modelling and Simulaion, Adelaide, Ausralia, 6 December 3 www.mssanz.org.au/modsim3 Robus esimaion based on he firs- and hird-momen resricions of he power ransformaion Nawaa,

h Inernaional Congress on Modelling and Simulaion, Adelaide, Ausralia, 6 December 3 www.mssanz.org.au/modsim3 Robus esimaion based on he firs- and hird-momen resricions of he power ransformaion Nawaa,

Lecture 5. Time series: ECM. Bernardina Algieri Department Economics, Statistics and Finance

Lecure 5 Time series: ECM Bernardina Algieri Deparmen Economics, Saisics and Finance Conens Time Series Modelling Coinegraion Error Correcion Model Two Seps, Engle-Granger procedure Error Correcion Model

Lecure 5 Time series: ECM Bernardina Algieri Deparmen Economics, Saisics and Finance Conens Time Series Modelling Coinegraion Error Correcion Model Two Seps, Engle-Granger procedure Error Correcion Model

Volatility. Many economic series, and most financial series, display conditional volatility

Volailiy Many economic series, and mos financial series, display condiional volailiy The condiional variance changes over ime There are periods of high volailiy When large changes frequenly occur And periods

Volailiy Many economic series, and mos financial series, display condiional volailiy The condiional variance changes over ime There are periods of high volailiy When large changes frequenly occur And periods

Exponential Weighted Moving Average (EWMA) Chart Under The Assumption of Moderateness And Its 3 Control Limits

Chart Under The Assumption of Moderateness And Its 3 Control Limits") DOI: 0.545/mjis.07.5009 Exponenial Weighed Moving Average (EWMA) Char Under The Assumpion of Moderaeness And Is 3 Conrol Limis KALPESH S TAILOR Assisan Professor, Deparmen of Saisics, M. K. Bhavnagar Universiy,

DOI: 0.545/mjis.07.5009 Exponenial Weighed Moving Average (EWMA) Char Under The Assumpion of Moderaeness And Is 3 Conrol Limis KALPESH S TAILOR Assisan Professor, Deparmen of Saisics, M. K. Bhavnagar Universiy,

Forecasting. Summary. Sample StatFolio: tsforecast.sgp. STATGRAPHICS Centurion Rev. 9/16/2013

STATGRAPHICS Cenurion Rev. 9/16/2013 Forecasing Summary... 1 Daa Inpu... 3 Analysis Opions... 5 Forecasing Models... 9 Analysis Summary... 21 Time Sequence Plo... 23 Forecas Table... 24 Forecas Plo...

STATGRAPHICS Cenurion Rev. 9/16/2013 Forecasing Summary... 1 Daa Inpu... 3 Analysis Opions... 5 Forecasing Models... 9 Analysis Summary... 21 Time Sequence Plo... 23 Forecas Table... 24 Forecas Plo...

BOOTSTRAP PREDICTION INTERVALS FOR TIME SERIES MODELS WITH HETROSCEDASTIC ERRORS. Department of Statistics, Islamia College, Peshawar, KP, Pakistan 2

Pak. J. Sais. 017 Vol. 33(1), 1-13 BOOTSTRAP PREDICTIO ITERVAS FOR TIME SERIES MODES WITH HETROSCEDASTIC ERRORS Amjad Ali 1, Sajjad Ahmad Khan, Alamgir 3 Umair Khalil and Dos Muhammad Khan 1 Deparmen of

Pak. J. Sais. 017 Vol. 33(1), 1-13 BOOTSTRAP PREDICTIO ITERVAS FOR TIME SERIES MODES WITH HETROSCEDASTIC ERRORS Amjad Ali 1, Sajjad Ahmad Khan, Alamgir 3 Umair Khalil and Dos Muhammad Khan 1 Deparmen of

On Measuring Pro-Poor Growth. 1. On Various Ways of Measuring Pro-Poor Growth: A Short Review of the Literature

On Measuring Pro-Poor Growh 1. On Various Ways of Measuring Pro-Poor Growh: A Shor eview of he Lieraure During he pas en years or so here have been various suggesions concerning he way one should check

On Measuring Pro-Poor Growh 1. On Various Ways of Measuring Pro-Poor Growh: A Shor eview of he Lieraure During he pas en years or so here have been various suggesions concerning he way one should check

Forecasting models for economic and environmental applications

Universiy of Souh Florida Scholar Commons Graduae Theses and Disseraions Graduae School 008 Forecasing models for economic and environmenal applicaions Shou Hsing Shih Universiy of Souh Florida Follow

Universiy of Souh Florida Scholar Commons Graduae Theses and Disseraions Graduae School 008 Forecasing models for economic and environmenal applicaions Shou Hsing Shih Universiy of Souh Florida Follow

Derived Short-Run and Long-Run Softwood Lumber Demand and Supply

Derived Shor-Run and Long-Run Sofwood Lumber Demand and Supply Nianfu Song and Sun Joseph Chang School of Renewable Naural Resources Louisiana Sae Universiy Ouline Shor-run run and long-run implied by

Derived Shor-Run and Long-Run Sofwood Lumber Demand and Supply Nianfu Song and Sun Joseph Chang School of Renewable Naural Resources Louisiana Sae Universiy Ouline Shor-run run and long-run implied by

The Brock-Mirman Stochastic Growth Model

c December 3, 208, Chrisopher D. Carroll BrockMirman The Brock-Mirman Sochasic Growh Model Brock and Mirman (972) provided he firs opimizing growh model wih unpredicable (sochasic) shocks. The social planner

c December 3, 208, Chrisopher D. Carroll BrockMirman The Brock-Mirman Sochasic Growh Model Brock and Mirman (972) provided he firs opimizing growh model wih unpredicable (sochasic) shocks. The social planner

Robust critical values for unit root tests for series with conditional heteroscedasticity errors: An application of the simple NoVaS transformation

WORKING PAPER 01: Robus criical values for uni roo ess for series wih condiional heeroscedasiciy errors: An applicaion of he simple NoVaS ransformaion Panagiois Manalos ECONOMETRICS AND STATISTICS ISSN

WORKING PAPER 01: Robus criical values for uni roo ess for series wih condiional heeroscedasiciy errors: An applicaion of he simple NoVaS ransformaion Panagiois Manalos ECONOMETRICS AND STATISTICS ISSN

hen found from Bayes rule. Specically, he prior disribuion is given by p( ) = N( ; ^ ; r ) (.3) where r is he prior variance (we add on he random drif

= N( ; ^ ; r ) (.3) where r is he prior variance (we add on he random drif") Chaper Kalman Filers. Inroducion We describe Bayesian Learning for sequenial esimaion of parameers (eg. means, AR coeciens). The updae procedures are known as Kalman Filers. We show how Dynamic Linear

Chaper Kalman Filers. Inroducion We describe Bayesian Learning for sequenial esimaion of parameers (eg. means, AR coeciens). The updae procedures are known as Kalman Filers. We show how Dynamic Linear

CH Sean Han QF, NTHU, Taiwan BFS2010. (Joint work with T.-Y. Chen and W.-H. Liu)

") CH Sean Han QF, NTHU, Taiwan BFS2010 (Join work wih T.-Y. Chen and W.-H. Liu) Risk Managemen in Pracice: Value a Risk (VaR) / Condiional Value a Risk (CVaR) Volailiy Esimaion: Correced Fourier Transform

CH Sean Han QF, NTHU, Taiwan BFS2010 (Join work wih T.-Y. Chen and W.-H. Liu) Risk Managemen in Pracice: Value a Risk (VaR) / Condiional Value a Risk (CVaR) Volailiy Esimaion: Correced Fourier Transform

Richard A. Davis Colorado State University Bojan Basrak Eurandom Thomas Mikosch University of Groningen

Mulivariae Regular Variaion wih Applicaion o Financial Time Series Models Richard A. Davis Colorado Sae Universiy Bojan Basrak Eurandom Thomas Mikosch Universiy of Groningen Ouline + Characerisics of some

Mulivariae Regular Variaion wih Applicaion o Financial Time Series Models Richard A. Davis Colorado Sae Universiy Bojan Basrak Eurandom Thomas Mikosch Universiy of Groningen Ouline + Characerisics of some

Chapter 11. Heteroskedasticity The Nature of Heteroskedasticity. In Chapter 3 we introduced the linear model (11.1.1)

") Chaper 11 Heeroskedasiciy 11.1 The Naure of Heeroskedasiciy In Chaper 3 we inroduced he linear model y = β+β x (11.1.1) 1 o explain household expendiure on food (y) as a funcion of household income (x).

Chaper 11 Heeroskedasiciy 11.1 The Naure of Heeroskedasiciy In Chaper 3 we inroduced he linear model y = β+β x (11.1.1) 1 o explain household expendiure on food (y) as a funcion of household income (x).

Estimation of Poses with Particle Filters

Esimaion of Poses wih Paricle Filers Dr.-Ing. Bernd Ludwig Chair for Arificial Inelligence Deparmen of Compuer Science Friedrich-Alexander-Universiä Erlangen-Nürnberg 12/05/2008 Dr.-Ing. Bernd Ludwig (FAU

Esimaion of Poses wih Paricle Filers Dr.-Ing. Bernd Ludwig Chair for Arificial Inelligence Deparmen of Compuer Science Friedrich-Alexander-Universiä Erlangen-Nürnberg 12/05/2008 Dr.-Ing. Bernd Ludwig (FAU

PROC NLP Approach for Optimal Exponential Smoothing Srihari Jaganathan, Cognizant Technology Solutions, Newbury Park, CA.

PROC NLP Approach for Opimal Exponenial Smoohing Srihari Jaganahan, Cognizan Technology Soluions, Newbury Park, CA. ABSTRACT Esimaion of smoohing parameers and iniial values are some of he basic requiremens

PROC NLP Approach for Opimal Exponenial Smoohing Srihari Jaganahan, Cognizan Technology Soluions, Newbury Park, CA. ABSTRACT Esimaion of smoohing parameers and iniial values are some of he basic requiremens

12: AUTOREGRESSIVE AND MOVING AVERAGE PROCESSES IN DISCRETE TIME. Σ j =

1: AUTOREGRESSIVE AND MOVING AVERAGE PROCESSES IN DISCRETE TIME Moving Averages Recall ha a whie noise process is a series { } = having variance σ. The whie noise process has specral densiy f (λ) = of

1: AUTOREGRESSIVE AND MOVING AVERAGE PROCESSES IN DISCRETE TIME Moving Averages Recall ha a whie noise process is a series { } = having variance σ. The whie noise process has specral densiy f (λ) = of

Outline. lse-logo. Outline. Outline. 1 Wald Test. 2 The Likelihood Ratio Test. 3 Lagrange Multiplier Tests

Ouline Ouline Hypohesis Tes wihin he Maximum Likelihood Framework There are hree main frequenis approaches o inference wihin he Maximum Likelihood framework: he Wald es, he Likelihood Raio es and he Lagrange

Ouline Ouline Hypohesis Tes wihin he Maximum Likelihood Framework There are hree main frequenis approaches o inference wihin he Maximum Likelihood framework: he Wald es, he Likelihood Raio es and he Lagrange

1. Consider a pure-exchange economy with stochastic endowments. The state of the economy

Answer 4 of he following 5 quesions. 1. Consider a pure-exchange economy wih sochasic endowmens. The sae of he economy in period, 0,1,..., is he hisory of evens s ( s0, s1,..., s ). The iniial sae is given.

Answer 4 of he following 5 quesions. 1. Consider a pure-exchange economy wih sochasic endowmens. The sae of he economy in period, 0,1,..., is he hisory of evens s ( s0, s1,..., s ). The iniial sae is given.

5. Stochastic processes (1)

") Lec05.pp S-38.45 - Inroducion o Teleraffic Theory Spring 2005 Conens Basic conceps Poisson process 2 Sochasic processes () Consider some quaniy in a eleraffic (or any) sysem I ypically evolves in ime randomly

Lec05.pp S-38.45 - Inroducion o Teleraffic Theory Spring 2005 Conens Basic conceps Poisson process 2 Sochasic processes () Consider some quaniy in a eleraffic (or any) sysem I ypically evolves in ime randomly

ACE 562 Fall Lecture 5: The Simple Linear Regression Model: Sampling Properties of the Least Squares Estimators. by Professor Scott H.

ACE 56 Fall 005 Lecure 5: he Simple Linear Regression Model: Sampling Properies of he Leas Squares Esimaors by Professor Sco H. Irwin Required Reading: Griffihs, Hill and Judge. "Inference in he Simple

ACE 56 Fall 005 Lecure 5: he Simple Linear Regression Model: Sampling Properies of he Leas Squares Esimaors by Professor Sco H. Irwin Required Reading: Griffihs, Hill and Judge. "Inference in he Simple

Ready for euro? Empirical study of the actual monetary policy independence in Poland VECM modelling

Macroeconomerics Handou 2 Ready for euro? Empirical sudy of he acual moneary policy independence in Poland VECM modelling 1. Inroducion This classes are based on: Łukasz Goczek & Dagmara Mycielska, 2013.

Macroeconomerics Handou 2 Ready for euro? Empirical sudy of he acual moneary policy independence in Poland VECM modelling 1. Inroducion This classes are based on: Łukasz Goczek & Dagmara Mycielska, 2013.

13.3 Term structure models

13.3 Term srucure models 13.3.1 Expecaions hypohesis model - Simples "model" a) shor rae b) expecaions o ge oher prices Resul: y () = 1 h +1 δ = φ( δ)+ε +1 f () = E (y +1) (1) =δ + φ( δ) f (3) = E (y +)

13.3 Term srucure models 13.3.1 Expecaions hypohesis model - Simples "model" a) shor rae b) expecaions o ge oher prices Resul: y () = 1 h +1 δ = φ( δ)+ε +1 f () = E (y +1) (1) =δ + φ( δ) f (3) = E (y +)

Math 10B: Mock Mid II. April 13, 2016

Name: Soluions Mah 10B: Mock Mid II April 13, 016 1. ( poins) Sae, wih jusificaion, wheher he following saemens are rue or false. (a) If a 3 3 marix A saisfies A 3 A = 0, hen i canno be inverible. True.

Name: Soluions Mah 10B: Mock Mid II April 13, 016 1. ( poins) Sae, wih jusificaion, wheher he following saemens are rue or false. (a) If a 3 3 marix A saisfies A 3 A = 0, hen i canno be inverible. True.

2017 3rd International Conference on E-commerce and Contemporary Economic Development (ECED 2017) ISBN:

ISBN:") 7 3rd Inernaional Conference on E-commerce and Conemporary Economic Developmen (ECED 7) ISBN: 978--6595-446- Fuures Arbirage of Differen Varieies and based on he Coinegraion Which is under he Framework

7 3rd Inernaional Conference on E-commerce and Conemporary Economic Developmen (ECED 7) ISBN: 978--6595-446- Fuures Arbirage of Differen Varieies and based on he Coinegraion Which is under he Framework

A Bayesian Approach to Spectral Analysis

Chirped Signals A Bayesian Approach o Specral Analysis Chirped signals are oscillaing signals wih ime variable frequencies, usually wih a linear variaion of frequency wih ime. E.g. f() = A cos(ω + α 2

Chirped Signals A Bayesian Approach o Specral Analysis Chirped signals are oscillaing signals wih ime variable frequencies, usually wih a linear variaion of frequency wih ime. E.g. f() = A cos(ω + α 2

Applied Time Series Notes White noise: e t mean 0, variance 5 2 uncorrelated Moving Average

Applied Time Series Noes Whie noise: e mean 0, variance 5 uncorrelaed Moving Average Order 1: (Y. ) œ e ) 1e -1 all Order q: (Y. ) œ e ) e â ) e all 1-1 q -q ( 14 ) Infinie order: (Y. ) œ e ) 1e -1 ) e

Applied Time Series Noes Whie noise: e mean 0, variance 5 uncorrelaed Moving Average Order 1: (Y. ) œ e ) 1e -1 all Order q: (Y. ) œ e ) e â ) e all 1-1 q -q ( 14 ) Infinie order: (Y. ) œ e ) 1e -1 ) e

Modeling and Forecasting Volatility Autoregressive Conditional Heteroskedasticity Models. Economic Forecasting Anthony Tay Slide 1

Modeling and Forecasing Volailiy Auoregressive Condiional Heeroskedasiciy Models Anhony Tay Slide 1 smpl @all line(m) sii dl_sii S TII D L _ S TII 4,000. 3,000.1.0,000 -.1 1,000 -. 0 86 88 90 9 94 96 98

Modeling and Forecasing Volailiy Auoregressive Condiional Heeroskedasiciy Models Anhony Tay Slide 1 smpl @all line(m) sii dl_sii S TII D L _ S TII 4,000. 3,000.1.0,000 -.1 1,000 -. 0 86 88 90 9 94 96 98

Georey E. Hinton. University oftoronto. Technical Report CRG-TR February 22, Abstract

Parameer Esimaion for Linear Dynamical Sysems Zoubin Ghahramani Georey E. Hinon Deparmen of Compuer Science Universiy oftorono 6 King's College Road Torono, Canada M5S A4 Email: zoubin@cs.orono.edu Technical

Parameer Esimaion for Linear Dynamical Sysems Zoubin Ghahramani Georey E. Hinon Deparmen of Compuer Science Universiy oftorono 6 King's College Road Torono, Canada M5S A4 Email: zoubin@cs.orono.edu Technical

Stochastic Model for Cancer Cell Growth through Single Forward Mutation

Journal of Modern Applied Saisical Mehods Volume 16 Issue 1 Aricle 31 5-1-2017 Sochasic Model for Cancer Cell Growh hrough Single Forward Muaion Jayabharahiraj Jayabalan Pondicherry Universiy, jayabharahi8@gmail.com

Journal of Modern Applied Saisical Mehods Volume 16 Issue 1 Aricle 31 5-1-2017 Sochasic Model for Cancer Cell Growh hrough Single Forward Muaion Jayabharahiraj Jayabalan Pondicherry Universiy, jayabharahi8@gmail.com

Wednesday, November 7 Handout: Heteroskedasticity

Amhers College Deparmen of Economics Economics 360 Fall 202 Wednesday, November 7 Handou: Heeroskedasiciy Preview Review o Regression Model o Sandard Ordinary Leas Squares (OLS) Premises o Esimaion Procedures

Amhers College Deparmen of Economics Economics 360 Fall 202 Wednesday, November 7 Handou: Heeroskedasiciy Preview Review o Regression Model o Sandard Ordinary Leas Squares (OLS) Premises o Esimaion Procedures