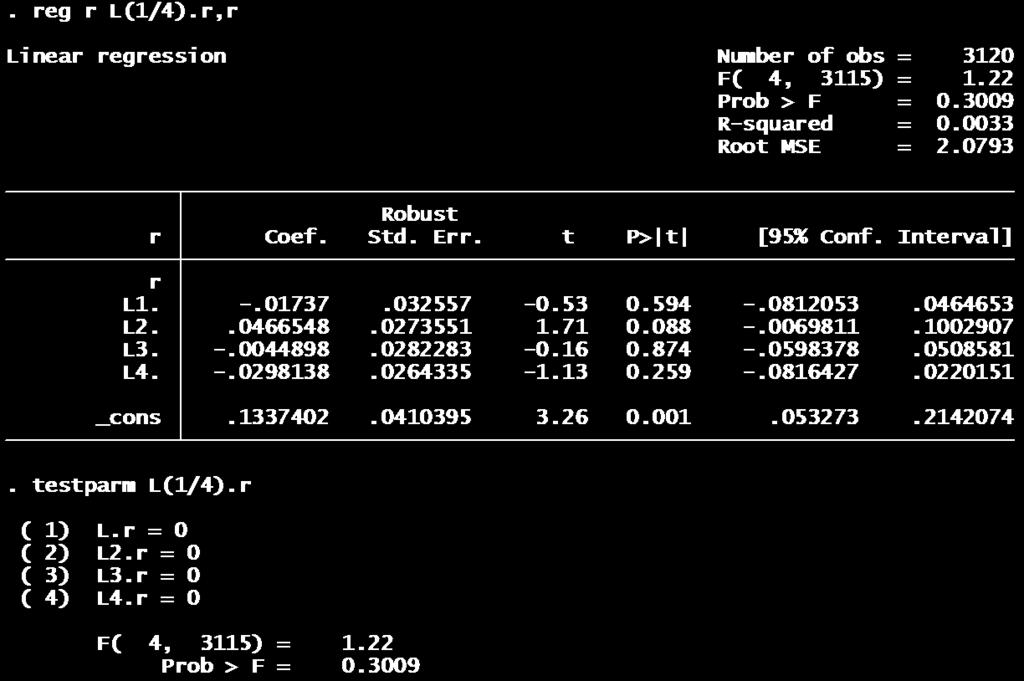

Volatility. Many economic series, and most financial series, display conditional volatility

|

|

|

- Edward Wheeler

- 6 years ago

- Views:

Transcription

1 Volailiy Many economic series, and mos financial series, display condiional volailiy The condiional variance changes over ime There are periods of high volailiy When large changes frequenly occur And periods of low volailiy When large changes are less frequen

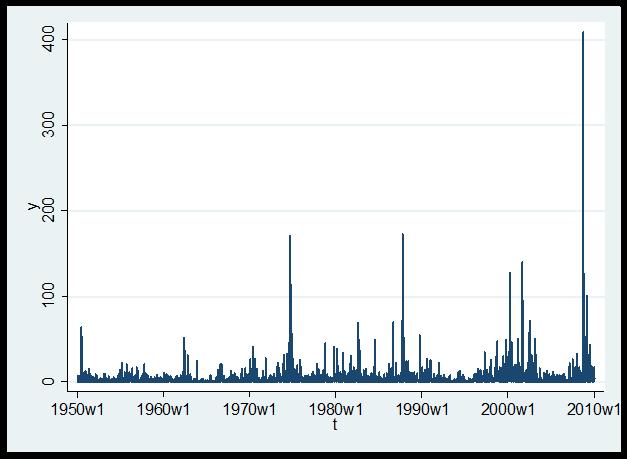

2 Weekly Sock Prices Levels and Reurns

3 Condiional Mean The condiional mean of y is E ( ) Ω 1 The regression error is mean zero and unforecasable E y ( ) = 1 0 e Ω

4 Condiional Variance The condiional variance of y is The squared regression error can be forecasable ( ) ( ) ( ) ( ) ( ) var Ω = Ω Ω = Ω e E y E y E y

5 Forecasable Condiional Variance If he squared error is forecasable, hen he condiional variance is ime varying and correlaed. The magniude of changes is predicable The sign is no predicable

6 Sock reurns are unpredicable

7 Squared Reurns are predicable

8 Squared Reurns

9 ARCH Rober Engle (198) proposed a model for he condiional variance AuoRegressive Condiional Heeroskedasiciy ARCH now describes volailiy models Nobel Prize 003

10 y σ ARCH(1) Model = ω > α = μ + e var 0 0 ( e Ω ) α>0 means ha he condiional variance is high when he lagged squared error is high Large errors (eiher sign) oday mean high expeced errors (in magniude) omorrow. Small magniude errors forecas nex period small magniude errors. 1 = ω + αe 1

11 Uncondiional variance A propery of expecaions is ha expeced (average) condiional expecaions are uncondiional expecaions. So he average condiional variance is he average variance he variance of he regression error. ( ) ( ) σ = E σ = ω + αe e 1 = ω + ασ Solving for he variance: ω σ = 1 α

12 Rewriing, his implies ω = σ 1 ( α ) Subsiuing ino ARCH(1) equaion ( ) σ = α σ + αe or σ σ + α σ = e ( ) This shows ha he condiional variance is a combinaion of he uncondiional variance, and he deviaion of he squared error from is average value.

13 ARCH(1) as AR(1) in squares The model var ( ) ( ) e Ω E e ω αe 1 implies he regression = Ω = = ω αe 1 e + + u where u is whie noise Thus e squared is an AR(1)

")

14 .arch r, arch(1) Esimaion

15 Variance Forecas Given he parameer esimaes, he esimaed condiional variance for period is ˆ σ ˆ ˆˆ = ω + αe 1 = ω + α 1 ˆ ˆ ( y ˆ μ) The forecased ou of sample variance is ˆ σ ˆ ( y μ) ˆ n+ 1 = ω + α n ˆ

16 Forecas Inerval for he mean You can use he esimaed condiional sandard deviaion o obain forecas inervals for he mean y Z σ ˆ ˆ n+ 1 n ± α / n+ 1 These forecas inervals will vary in widh depending on he esimaed condiional variance. Wider in periods of high volailiy More narrow in periods of low volailiy

17 ARCH(p) model Allow p lags of squared errors Similar o AR(p) in squares Esimaion: ARCH(8).arch r, arch(1/8) ARCH model wih lags 1 hrough p p e e e e y = + = α α α ω σ μ L

")

18 .arch r, arch(1/8) ARCH(8) Esimaes

19 ARCH needs many lags Noice ha we included 8 lags, and all appeared significan. This is commonly observed in esimaed ARCH models The condiional variance appears o be a funcion of many lagged pas squares

20 GARCH Model Tim Bollerslev (1986) A suden of Engle Curren faculy a Duke proposed he GARCH model o simplify his problem σ ω + βσ + αe β > ω > α =

21 GARCH(1,1) This makes he variance a funcion of all pas lags: I is also smooher han an ARCH model wih a small number of lags ( ) = + = + + = j j j e e α ω β α βσ ω σ

22 GARCH(p,q) p lags of squared error q lags of condiional variance σ = ω + β σ α e L+ βqσ q + α1e 1 + L+ p p GARCH(1,1):.arch r, arch(1) garch(1) GARCH(3,):.arch r, arch(1/3) garch(1/)

")

23 GARCH(1,1) Common GARCH feaures Lagged variance has large coefficien Sum of wo coefficiens very close o (bu less han) one

24 GARCH(,) for Sock Reurns

25 GARCH(1,1) The GARCH(1,1) ofen fis well, and is a useful benchmark. Daily, weekly, or monhly asse reurns, exchange raes, or ineres raes

26 Exensions There are many exensions of he basic GARCH model, developed o handle a variey of siuaions Asymmeric Response Garch in mean Explanaory variables in variance Non normal errors

27 Threshold GARCH σ Asymeric GARCH = ω + βσ 1 + αe 1 + γe 11 1 ( e > 0) The las ern is dummy variable for posiive lagged errors This model specifies ha he ARCH effec depends on wheher he error was posiive or negaive If he error is negaive, he effec is α If he error is posiive, he full effec is α+γ

28 TARCH esimaion.arch r, arch(1) arch(1) garch(1) Negaive errors have coefficien of 0.19 Posiive errors have coefficien of 0.05 Negaive reurns increase volailiy much more han posiive reurns

29 Leverage Effec This model describes wha is called he leverage effec A negaive shock o equiy increases he raio deb/equiy of invesors This increases he leverage of heir porfolios This increases risk, and he condiional variance Negaive shocks have sronger effec on variance han posiive shocks

30 GARCH in mean If invesors are risk averse, risky asses will earn higher reurns (a risk premium) in marke equilibrium If asses have varying volailiy (risk), heir expeced reurn will vary wih his volailiy Expeced reurn should be posiively correlaed wih volailiy

31 GARCH M model y σ = β + β σ 1 1 = ω + βσ e + αe 1.arch arch(1) garch(1) archm

32 GARCH M for Sock Reurns Marginally posiive effec

arch(1) garch(1) archm archm")

33 TARCH and GARCH M.arch arch(1) arch(1) garch(1) archm archm erm appears insignifican

34 Esimaed sandard deviaion Esimaed TARCH model.predic v, variance.gen s=sqr(v) Uncondiional variance is.1

35 S&P, reurns, and sandard deviaion

DEPARTMENT OF ECONOMICS AND FINANCE COLLEGE OF BUSINESS AND ECONOMICS UNIVERSITY OF CANTERBURY CHRISTCHURCH, NEW ZEALAND

DEPARTMENT OF ECONOMICS AND FINANCE COLLEGE OF BUSINESS AND ECONOMICS UNIVERSITY OF CANTERBURY CHRISTCHURCH, NEW ZEALAND Asymmery and Leverage in Condiional Volailiy Models Michael McAleer WORKING PAPER

DEPARTMENT OF ECONOMICS AND FINANCE COLLEGE OF BUSINESS AND ECONOMICS UNIVERSITY OF CANTERBURY CHRISTCHURCH, NEW ZEALAND Asymmery and Leverage in Condiional Volailiy Models Michael McAleer WORKING PAPER

Financial Econometrics Jeffrey R. Russell Midterm Winter 2009 SOLUTIONS

Name SOLUTIONS Financial Economerics Jeffrey R. Russell Miderm Winer 009 SOLUTIONS You have 80 minues o complee he exam. Use can use a calculaor and noes. Try o fi all your work in he space provided. If

Name SOLUTIONS Financial Economerics Jeffrey R. Russell Miderm Winer 009 SOLUTIONS You have 80 minues o complee he exam. Use can use a calculaor and noes. Try o fi all your work in he space provided. If

Chapter 5. Heterocedastic Models. Introduction to time series (2008) 1

1") Chaper 5 Heerocedasic Models Inroducion o ime series (2008) 1 Chaper 5. Conens. 5.1. The ARCH model. 5.2. The GARCH model. 5.3. The exponenial GARCH model. 5.4. The CHARMA model. 5.5. Random coefficien

Chaper 5 Heerocedasic Models Inroducion o ime series (2008) 1 Chaper 5. Conens. 5.1. The ARCH model. 5.2. The GARCH model. 5.3. The exponenial GARCH model. 5.4. The CHARMA model. 5.5. Random coefficien

Introduction D P. r = constant discount rate, g = Gordon Model (1962): constant dividend growth rate.

: constant dividend growth rate.") Inroducion Gordon Model (1962): D P = r g r = consan discoun rae, g = consan dividend growh rae. If raional expecaions of fuure discoun raes and dividend growh vary over ime, so should he D/P raio. Since

Inroducion Gordon Model (1962): D P = r g r = consan discoun rae, g = consan dividend growh rae. If raional expecaions of fuure discoun raes and dividend growh vary over ime, so should he D/P raio. Since

R t. C t P t. + u t. C t = αp t + βr t + v t. + β + w t

Exercise 7 C P = α + β R P + u C = αp + βr + v (a) (b) C R = α P R + β + w (c) Assumpions abou he disurbances u, v, w : Classical assumions on he disurbance of one of he equaions, eg. on (b): E(v v s P,

Exercise 7 C P = α + β R P + u C = αp + βr + v (a) (b) C R = α P R + β + w (c) Assumpions abou he disurbances u, v, w : Classical assumions on he disurbance of one of he equaions, eg. on (b): E(v v s P,

Modeling and Forecasting Volatility Autoregressive Conditional Heteroskedasticity Models. Economic Forecasting Anthony Tay Slide 1

Modeling and Forecasing Volailiy Auoregressive Condiional Heeroskedasiciy Models Anhony Tay Slide 1 smpl @all line(m) sii dl_sii S TII D L _ S TII 4,000. 3,000.1.0,000 -.1 1,000 -. 0 86 88 90 9 94 96 98

Modeling and Forecasing Volailiy Auoregressive Condiional Heeroskedasiciy Models Anhony Tay Slide 1 smpl @all line(m) sii dl_sii S TII D L _ S TII 4,000. 3,000.1.0,000 -.1 1,000 -. 0 86 88 90 9 94 96 98

Asymmetry and Leverage in Conditional Volatility Models*

Asymmery and Leverage in Condiional Volailiy Models* Micael McAleer Deparmen of Quaniaive Finance Naional Tsing Hua Universiy Taiwan and Economeric Insiue Erasmus Scool of Economics Erasmus Universiy Roerdam

Asymmery and Leverage in Condiional Volailiy Models* Micael McAleer Deparmen of Quaniaive Finance Naional Tsing Hua Universiy Taiwan and Economeric Insiue Erasmus Scool of Economics Erasmus Universiy Roerdam

Linear Combinations of Volatility Forecasts for the WIG20 and Polish Exchange Rates

Eliza Buszkowska Universiy of Poznań, Poland Linear Combinaions of Volailiy Forecass for he WIG0 and Polish Exchange Raes Absrak. As is known forecas combinaions may be beer forecass hen forecass obained

Eliza Buszkowska Universiy of Poznań, Poland Linear Combinaions of Volailiy Forecass for he WIG0 and Polish Exchange Raes Absrak. As is known forecas combinaions may be beer forecass hen forecass obained

Distribution of Least Squares

Disribuion of Leas Squares In classic regression, if he errors are iid normal, and independen of he regressors, hen he leas squares esimaes have an exac normal disribuion, no jus asympoic his is no rue

Disribuion of Leas Squares In classic regression, if he errors are iid normal, and independen of he regressors, hen he leas squares esimaes have an exac normal disribuion, no jus asympoic his is no rue

Distribution of Estimates

Disribuion of Esimaes From Economerics (40) Linear Regression Model Assume (y,x ) is iid and E(x e )0 Esimaion Consisency y α + βx + he esimaes approach he rue values as he sample size increases Esimaion

Disribuion of Esimaes From Economerics (40) Linear Regression Model Assume (y,x ) is iid and E(x e )0 Esimaion Consisency y α + βx + he esimaes approach he rue values as he sample size increases Esimaion

Vectorautoregressive Model and Cointegration Analysis. Time Series Analysis Dr. Sevtap Kestel 1

Vecorauoregressive Model and Coinegraion Analysis Par V Time Series Analysis Dr. Sevap Kesel 1 Vecorauoregression Vecor auoregression (VAR) is an economeric model used o capure he evoluion and he inerdependencies

Vecorauoregressive Model and Coinegraion Analysis Par V Time Series Analysis Dr. Sevap Kesel 1 Vecorauoregression Vecor auoregression (VAR) is an economeric model used o capure he evoluion and he inerdependencies

Estimation Uncertainty

Esimaion Uncerainy The sample mean is an esimae of β = E(y +h ) The esimaion error is = + = T h y T b ( ) = = + = + = = = T T h T h e T y T y T b β β β Esimaion Variance Under classical condiions, where

Esimaion Uncerainy The sample mean is an esimae of β = E(y +h ) The esimaion error is = + = T h y T b ( ) = = + = + = = = T T h T h e T y T y T b β β β Esimaion Variance Under classical condiions, where

Diebold, Chapter 7. Francis X. Diebold, Elements of Forecasting, 4th Edition (Mason, Ohio: Cengage Learning, 2006). Chapter 7. Characterizing Cycles

. Chapter 7. Characterizing Cycles") Diebold, Chaper 7 Francis X. Diebold, Elemens of Forecasing, 4h Ediion (Mason, Ohio: Cengage Learning, 006). Chaper 7. Characerizing Cycles Afer compleing his reading you should be able o: Define covariance

Diebold, Chaper 7 Francis X. Diebold, Elemens of Forecasing, 4h Ediion (Mason, Ohio: Cengage Learning, 006). Chaper 7. Characerizing Cycles Afer compleing his reading you should be able o: Define covariance

Time series Decomposition method

Time series Decomposiion mehod A ime series is described using a mulifacor model such as = f (rend, cyclical, seasonal, error) = f (T, C, S, e) Long- Iner-mediaed Seasonal Irregular erm erm effec, effec,

Time series Decomposiion mehod A ime series is described using a mulifacor model such as = f (rend, cyclical, seasonal, error) = f (T, C, S, e) Long- Iner-mediaed Seasonal Irregular erm erm effec, effec,

OBJECTIVES OF TIME SERIES ANALYSIS

OBJECTIVES OF TIME SERIES ANALYSIS Undersanding he dynamic or imedependen srucure of he observaions of a single series (univariae analysis) Forecasing of fuure observaions Asceraining he leading, lagging

OBJECTIVES OF TIME SERIES ANALYSIS Undersanding he dynamic or imedependen srucure of he observaions of a single series (univariae analysis) Forecasing of fuure observaions Asceraining he leading, lagging

Wisconsin Unemployment Rate Forecast Revisited

Wisconsin Unemploymen Rae Forecas Revisied Forecas in Lecure Wisconsin unemploymen November 06 was 4.% Forecass Poin Forecas 50% Inerval 80% Inerval Forecas Forecas December 06 4.0% (4.0%, 4.0%) (3.95%,

Wisconsin Unemploymen Rae Forecas Revisied Forecas in Lecure Wisconsin unemploymen November 06 was 4.% Forecass Poin Forecas 50% Inerval 80% Inerval Forecas Forecas December 06 4.0% (4.0%, 4.0%) (3.95%,

ECON 482 / WH Hong Time Series Data Analysis 1. The Nature of Time Series Data. Example of time series data (inflation and unemployment rates)

") ECON 48 / WH Hong Time Series Daa Analysis. The Naure of Time Series Daa Example of ime series daa (inflaion and unemploymen raes) ECON 48 / WH Hong Time Series Daa Analysis The naure of ime series daa

ECON 48 / WH Hong Time Series Daa Analysis. The Naure of Time Series Daa Example of ime series daa (inflaion and unemploymen raes) ECON 48 / WH Hong Time Series Daa Analysis The naure of ime series daa

Econ Autocorrelation. Sanjaya DeSilva

Econ 39 - Auocorrelaion Sanjaya DeSilva Ocober 3, 008 1 Definiion Auocorrelaion (or serial correlaion) occurs when he error erm of one observaion is correlaed wih he error erm of any oher observaion. This

Econ 39 - Auocorrelaion Sanjaya DeSilva Ocober 3, 008 1 Definiion Auocorrelaion (or serial correlaion) occurs when he error erm of one observaion is correlaed wih he error erm of any oher observaion. This

Econ107 Applied Econometrics Topic 7: Multicollinearity (Studenmund, Chapter 8)

") I. Definiions and Problems A. Perfec Mulicollineariy Econ7 Applied Economerics Topic 7: Mulicollineariy (Sudenmund, Chaper 8) Definiion: Perfec mulicollineariy exiss in a following K-variable regression

I. Definiions and Problems A. Perfec Mulicollineariy Econ7 Applied Economerics Topic 7: Mulicollineariy (Sudenmund, Chaper 8) Definiion: Perfec mulicollineariy exiss in a following K-variable regression

Vector autoregression VAR. Case 1

Vecor auoregression VAR So far we have focused mosl on models where deends onl on as. More generall we migh wan o consider oin models ha involve more han one variable. There are wo reasons: Firs, we migh

Vecor auoregression VAR So far we have focused mosl on models where deends onl on as. More generall we migh wan o consider oin models ha involve more han one variable. There are wo reasons: Firs, we migh

Forecasting optimally

I) ile: Forecas Evaluaion II) Conens: Evaluaing forecass, properies of opimal forecass, esing properies of opimal forecass, saisical comparison of forecas accuracy III) Documenaion: - Diebold, Francis

I) ile: Forecas Evaluaion II) Conens: Evaluaing forecass, properies of opimal forecass, esing properies of opimal forecass, saisical comparison of forecas accuracy III) Documenaion: - Diebold, Francis

Tourism forecasting using conditional volatility models

Tourism forecasing using condiional volailiy models ABSTRACT Condiional volailiy models are used in ourism demand sudies o model he effecs of shocks on demand volailiy, which arise from changes in poliical,

Tourism forecasing using condiional volailiy models ABSTRACT Condiional volailiy models are used in ourism demand sudies o model he effecs of shocks on demand volailiy, which arise from changes in poliical,

Modeling the Volatility of Shanghai Composite Index

Modeling he Volailiy of Shanghai Composie Index wih GARCH Family Models Auhor: Yuchen Du Supervisor: Changli He Essay in Saisics, Advanced Level Dalarna Universiy Sweden Modeling he volailiy of Shanghai

Modeling he Volailiy of Shanghai Composie Index wih GARCH Family Models Auhor: Yuchen Du Supervisor: Changli He Essay in Saisics, Advanced Level Dalarna Universiy Sweden Modeling he volailiy of Shanghai

V Time Varying Covariance and Correlation

V Time Varying Covariance and Correlaion DEFINITION OF CONDITIONAL CORRELATIONS. ARE THEY TIME VARYING? WHY DO WE NEED THEM? FACTOR MODELS DYNAMIC CONDITIONAL CORRELATIONS Are correlaions/covariances ime

V Time Varying Covariance and Correlaion DEFINITION OF CONDITIONAL CORRELATIONS. ARE THEY TIME VARYING? WHY DO WE NEED THEM? FACTOR MODELS DYNAMIC CONDITIONAL CORRELATIONS Are correlaions/covariances ime

Solutions to Odd Number Exercises in Chapter 6

1 Soluions o Odd Number Exercises in 6.1 R y eˆ 1.7151 y 6.3 From eˆ ( T K) ˆ R 1 1 SST SST SST (1 R ) 55.36(1.7911) we have, ˆ 6.414 T K ( ) 6.5 y ye ye y e 1 1 Consider he erms e and xe b b x e y e b

1 Soluions o Odd Number Exercises in 6.1 R y eˆ 1.7151 y 6.3 From eˆ ( T K) ˆ R 1 1 SST SST SST (1 R ) 55.36(1.7911) we have, ˆ 6.414 T K ( ) 6.5 y ye ye y e 1 1 Consider he erms e and xe b b x e y e b

Testing for a Single Factor Model in the Multivariate State Space Framework

esing for a Single Facor Model in he Mulivariae Sae Space Framework Chen C.-Y. M. Chiba and M. Kobayashi Inernaional Graduae School of Social Sciences Yokohama Naional Universiy Japan Faculy of Economics

esing for a Single Facor Model in he Mulivariae Sae Space Framework Chen C.-Y. M. Chiba and M. Kobayashi Inernaional Graduae School of Social Sciences Yokohama Naional Universiy Japan Faculy of Economics

Regression with Time Series Data

Regression wih Time Series Daa y = β 0 + β 1 x 1 +...+ β k x k + u Serial Correlaion and Heeroskedasiciy Time Series - Serial Correlaion and Heeroskedasiciy 1 Serially Correlaed Errors: Consequences Wih

Regression wih Time Series Daa y = β 0 + β 1 x 1 +...+ β k x k + u Serial Correlaion and Heeroskedasiciy Time Series - Serial Correlaion and Heeroskedasiciy 1 Serially Correlaed Errors: Consequences Wih

The Real Exchange Rate, Real Interest Rates, and the Risk Premium. Charles Engel University of Wisconsin

The Real Exchange Rae, Real Ineres Raes, and he Risk Premium Charles Engel Universiy of Wisconsin How does exchange rae respond o ineres rae changes? In sandard open economy New Keynesian model, increase

The Real Exchange Rae, Real Ineres Raes, and he Risk Premium Charles Engel Universiy of Wisconsin How does exchange rae respond o ineres rae changes? In sandard open economy New Keynesian model, increase

Unit Root Time Series. Univariate random walk

Uni Roo ime Series Univariae random walk Consider he regression y y where ~ iid N 0, he leas squares esimae of is: ˆ yy y y yy Now wha if = If y y hen le y 0 =0 so ha y j j If ~ iid N 0, hen y ~ N 0, he

Uni Roo ime Series Univariae random walk Consider he regression y y where ~ iid N 0, he leas squares esimae of is: ˆ yy y y yy Now wha if = If y y hen le y 0 =0 so ha y j j If ~ iid N 0, hen y ~ N 0, he

1 Answers to Final Exam, ECN 200E, Spring

1 Answers o Final Exam, ECN 200E, Spring 2004 1. A good answer would include he following elemens: The equiy premium puzzle demonsraed ha wih sandard (i.e ime separable and consan relaive risk aversion)

1 Answers o Final Exam, ECN 200E, Spring 2004 1. A good answer would include he following elemens: The equiy premium puzzle demonsraed ha wih sandard (i.e ime separable and consan relaive risk aversion)

Chapter 14 Wiener Processes and Itô s Lemma. Options, Futures, and Other Derivatives, 9th Edition, Copyright John C. Hull

Chaper 14 Wiener Processes and Iô s Lemma Copyrigh John C. Hull 014 1 Sochasic Processes! Describes he way in which a variable such as a sock price, exchange rae or ineres rae changes hrough ime! Incorporaes

Chaper 14 Wiener Processes and Iô s Lemma Copyrigh John C. Hull 014 1 Sochasic Processes! Describes he way in which a variable such as a sock price, exchange rae or ineres rae changes hrough ime! Incorporaes

Asymmetry and Leverage in Conditional Volatility Models

Economerics 04,, 45-50; doi:0.3390/economerics03045 OPEN ACCESS economerics ISSN 5-46 www.mdpi.com/journal/economerics Aricle Asymmery and Leverage in Condiional Volailiy Models Micael McAleer,,3,4 Deparmen

Economerics 04,, 45-50; doi:0.3390/economerics03045 OPEN ACCESS economerics ISSN 5-46 www.mdpi.com/journal/economerics Aricle Asymmery and Leverage in Condiional Volailiy Models Micael McAleer,,3,4 Deparmen

Asymmetric Conditional Volatility on the Romanian Stock Market - DISSERTATION PAPER-

ACADEMY OF ECONOMIC STUDIES DOCTORAL SCHOOL OF FINANCE AND BANKING Asymmeric Condiional Volailiy on he Romanian Sock Marke - DISSERTATION PAPER- MSc Suden: STANCIU FLORIN AURELIAN Coordinaor: Professor

ACADEMY OF ECONOMIC STUDIES DOCTORAL SCHOOL OF FINANCE AND BANKING Asymmeric Condiional Volailiy on he Romanian Sock Marke - DISSERTATION PAPER- MSc Suden: STANCIU FLORIN AURELIAN Coordinaor: Professor

Lecture 5. Time series: ECM. Bernardina Algieri Department Economics, Statistics and Finance

Lecure 5 Time series: ECM Bernardina Algieri Deparmen Economics, Saisics and Finance Conens Time Series Modelling Coinegraion Error Correcion Model Two Seps, Engle-Granger procedure Error Correcion Model

Lecure 5 Time series: ECM Bernardina Algieri Deparmen Economics, Saisics and Finance Conens Time Series Modelling Coinegraion Error Correcion Model Two Seps, Engle-Granger procedure Error Correcion Model

Title: GARCH modelling applied to the Index of Industrial Production in Ireland

Tile: GARCH modelling applied o he Index of Indusrial Producion in Ireland Candidae: Aoife Healy Masers projec Universiy Name: Naional Universiy of Ireland, Galway Supervisor: Dr. Damien Fay Monh and Year

Tile: GARCH modelling applied o he Index of Indusrial Producion in Ireland Candidae: Aoife Healy Masers projec Universiy Name: Naional Universiy of Ireland, Galway Supervisor: Dr. Damien Fay Monh and Year

Chapter 15. Time Series: Descriptive Analyses, Models, and Forecasting

Chaper 15 Time Series: Descripive Analyses, Models, and Forecasing Descripive Analysis: Index Numbers Index Number a number ha measures he change in a variable over ime relaive o he value of he variable

Chaper 15 Time Series: Descripive Analyses, Models, and Forecasing Descripive Analysis: Index Numbers Index Number a number ha measures he change in a variable over ime relaive o he value of he variable

Applied Econometrics GARCH Models - Extensions. Roman Horvath Lecture 2

Applied Economerics GARCH Models - Exensions Roman Horva Lecre Conens GARCH EGARCH, GARCH-M Mlivariae GARCH Sylized facs in finance Unpredicabiliy Volailiy Fa ails Efficien markes Time-varying (rblen vs.

Applied Economerics GARCH Models - Exensions Roman Horva Lecre Conens GARCH EGARCH, GARCH-M Mlivariae GARCH Sylized facs in finance Unpredicabiliy Volailiy Fa ails Efficien markes Time-varying (rblen vs.

The Brock-Mirman Stochastic Growth Model

c December 3, 208, Chrisopher D. Carroll BrockMirman The Brock-Mirman Sochasic Growh Model Brock and Mirman (972) provided he firs opimizing growh model wih unpredicable (sochasic) shocks. The social planner

c December 3, 208, Chrisopher D. Carroll BrockMirman The Brock-Mirman Sochasic Growh Model Brock and Mirman (972) provided he firs opimizing growh model wih unpredicable (sochasic) shocks. The social planner

UNIVERSITY OF OSLO DEPARTMENT OF ECONOMICS

UNIVERSITY OF OSLO DEPARTMENT OF ECONOMICS Exam: ECON4325 Moneary Policy Dae of exam: Tuesday, May 24, 206 Grades are given: June 4, 206 Time for exam: 2.30 p.m. 5.30 p.m. The problem se covers 5 pages

UNIVERSITY OF OSLO DEPARTMENT OF ECONOMICS Exam: ECON4325 Moneary Policy Dae of exam: Tuesday, May 24, 206 Grades are given: June 4, 206 Time for exam: 2.30 p.m. 5.30 p.m. The problem se covers 5 pages

Cointegration and Implications for Forecasting

Coinegraion and Implicaions for Forecasing Two examples (A) Y Y 1 1 1 2 (B) Y 0.3 0.9 1 1 2 Example B: Coinegraion Y and coinegraed wih coinegraing vecor [1, 0.9] because Y 0.9 0.3 is a saionary process

Coinegraion and Implicaions for Forecasing Two examples (A) Y Y 1 1 1 2 (B) Y 0.3 0.9 1 1 2 Example B: Coinegraion Y and coinegraed wih coinegraing vecor [1, 0.9] because Y 0.9 0.3 is a saionary process

1. Consider a pure-exchange economy with stochastic endowments. The state of the economy

Answer 4 of he following 5 quesions. 1. Consider a pure-exchange economy wih sochasic endowmens. The sae of he economy in period, 0,1,..., is he hisory of evens s ( s0, s1,..., s ). The iniial sae is given.

Answer 4 of he following 5 quesions. 1. Consider a pure-exchange economy wih sochasic endowmens. The sae of he economy in period, 0,1,..., is he hisory of evens s ( s0, s1,..., s ). The iniial sae is given.

Exponential Smoothing

Exponenial moohing Inroducion A simple mehod for forecasing. Does no require long series. Enables o decompose he series ino a rend and seasonal effecs. Paricularly useful mehod when here is a need o forecas

Exponenial moohing Inroducion A simple mehod for forecasing. Does no require long series. Enables o decompose he series ino a rend and seasonal effecs. Paricularly useful mehod when here is a need o forecas

20. Applications of the Genetic-Drift Model

0. Applicaions of he Geneic-Drif Model 1) Deermining he probabiliy of forming any paricular combinaion of genoypes in he nex generaion: Example: If he parenal allele frequencies are p 0 = 0.35 and q 0

0. Applicaions of he Geneic-Drif Model 1) Deermining he probabiliy of forming any paricular combinaion of genoypes in he nex generaion: Example: If he parenal allele frequencies are p 0 = 0.35 and q 0

13.3 Term structure models

13.3 Term srucure models 13.3.1 Expecaions hypohesis model - Simples "model" a) shor rae b) expecaions o ge oher prices Resul: y () = 1 h +1 δ = φ( δ)+ε +1 f () = E (y +1) (1) =δ + φ( δ) f (3) = E (y +)

13.3 Term srucure models 13.3.1 Expecaions hypohesis model - Simples "model" a) shor rae b) expecaions o ge oher prices Resul: y () = 1 h +1 δ = φ( δ)+ε +1 f () = E (y +1) (1) =δ + φ( δ) f (3) = E (y +)

1 Consumption and Risky Assets

Soluions o Problem Se 8 Econ 0A - nd Half - Fall 011 Prof David Romer, GSI: Vicoria Vanasco 1 Consumpion and Risky Asses Consumer's lifeime uiliy: U = u(c 1 )+E[u(c )] Income: Y 1 = Ȳ cerain and Y F (

Soluions o Problem Se 8 Econ 0A - nd Half - Fall 011 Prof David Romer, GSI: Vicoria Vanasco 1 Consumpion and Risky Asses Consumer's lifeime uiliy: U = u(c 1 )+E[u(c )] Income: Y 1 = Ȳ cerain and Y F (

Linear Gaussian State Space Models

Linear Gaussian Sae Space Models Srucural Time Series Models Level and Trend Models Basic Srucural Model (BSM Dynamic Linear Models Sae Space Model Represenaion Level, Trend, and Seasonal Models Time Varying

Linear Gaussian Sae Space Models Srucural Time Series Models Level and Trend Models Basic Srucural Model (BSM Dynamic Linear Models Sae Space Model Represenaion Level, Trend, and Seasonal Models Time Varying

Problem Set 5. Graduate Macro II, Spring 2017 The University of Notre Dame Professor Sims

Problem Se 5 Graduae Macro II, Spring 2017 The Universiy of Nore Dame Professor Sims Insrucions: You may consul wih oher members of he class, bu please make sure o urn in your own work. Where applicable,

Problem Se 5 Graduae Macro II, Spring 2017 The Universiy of Nore Dame Professor Sims Insrucions: You may consul wih oher members of he class, bu please make sure o urn in your own work. Where applicable,

The Brock-Mirman Stochastic Growth Model

c November 20, 207, Chrisopher D. Carroll BrockMirman The Brock-Mirman Sochasic Growh Model Brock and Mirman (972) provided he firs opimizing growh model wih unpredicable (sochasic) shocks. The social

c November 20, 207, Chrisopher D. Carroll BrockMirman The Brock-Mirman Sochasic Growh Model Brock and Mirman (972) provided he firs opimizing growh model wih unpredicable (sochasic) shocks. The social

CH Sean Han QF, NTHU, Taiwan BFS2010. (Joint work with T.-Y. Chen and W.-H. Liu)

") CH Sean Han QF, NTHU, Taiwan BFS2010 (Join work wih T.-Y. Chen and W.-H. Liu) Risk Managemen in Pracice: Value a Risk (VaR) / Condiional Value a Risk (CVaR) Volailiy Esimaion: Correced Fourier Transform

CH Sean Han QF, NTHU, Taiwan BFS2010 (Join work wih T.-Y. Chen and W.-H. Liu) Risk Managemen in Pracice: Value a Risk (VaR) / Condiional Value a Risk (CVaR) Volailiy Esimaion: Correced Fourier Transform

State-Space Models. Initialization, Estimation and Smoothing of the Kalman Filter

Sae-Space Models Iniializaion, Esimaion and Smoohing of he Kalman Filer Iniializaion of he Kalman Filer The Kalman filer shows how o updae pas predicors and he corresponding predicion error variances when

Sae-Space Models Iniializaion, Esimaion and Smoohing of he Kalman Filer Iniializaion of he Kalman Filer The Kalman filer shows how o updae pas predicors and he corresponding predicion error variances when

Dynamic Econometric Models: Y t = + 0 X t + 1 X t X t k X t-k + e t. A. Autoregressive Model:

Dynamic Economeric Models: A. Auoregressive Model: Y = + 0 X 1 Y -1 + 2 Y -2 + k Y -k + e (Wih lagged dependen variable(s) on he RHS) B. Disribued-lag Model: Y = + 0 X + 1 X -1 + 2 X -2 + + k X -k + e

Dynamic Economeric Models: A. Auoregressive Model: Y = + 0 X 1 Y -1 + 2 Y -2 + k Y -k + e (Wih lagged dependen variable(s) on he RHS) B. Disribued-lag Model: Y = + 0 X + 1 X -1 + 2 X -2 + + k X -k + e

23.2. Representing Periodic Functions by Fourier Series. Introduction. Prerequisites. Learning Outcomes

Represening Periodic Funcions by Fourier Series 3. Inroducion In his Secion we show how a periodic funcion can be expressed as a series of sines and cosines. We begin by obaining some sandard inegrals

Represening Periodic Funcions by Fourier Series 3. Inroducion In his Secion we show how a periodic funcion can be expressed as a series of sines and cosines. We begin by obaining some sandard inegrals

AN APPLICATION OF THE GARCH-t MODEL ON CENTRAL EUROPEAN STOCK RETURNS

AN APPLICATION OF THE GARCH- MODEL ON CENTRAL EUROPEAN STOCK RETURNS Miloslav VOŠVRDA, Filip ŽIKEŠ * Absrac: The purpose of his paper is o invesigae he ime-series and disribuional properies of Cenral European

AN APPLICATION OF THE GARCH- MODEL ON CENTRAL EUROPEAN STOCK RETURNS Miloslav VOŠVRDA, Filip ŽIKEŠ * Absrac: The purpose of his paper is o invesigae he ime-series and disribuional properies of Cenral European

Licenciatura de ADE y Licenciatura conjunta Derecho y ADE. Hoja de ejercicios 2 PARTE A

Licenciaura de ADE y Licenciaura conjuna Derecho y ADE Hoja de ejercicios PARTE A 1. Consider he following models Δy = 0.8 + ε (1 + 0.8L) Δ 1 y = ε where ε and ε are independen whie noise processes. In

Licenciaura de ADE y Licenciaura conjuna Derecho y ADE Hoja de ejercicios PARTE A 1. Consider he following models Δy = 0.8 + ε (1 + 0.8L) Δ 1 y = ε where ε and ε are independen whie noise processes. In

Methodology. -ratios are biased and that the appropriate critical values have to be increased by an amount. that depends on the sample size.

Mehodology. Uni Roo Tess A ime series is inegraed when i has a mean revering propery and a finie variance. I is only emporarily ou of equilibrium and is called saionary in I(0). However a ime series ha

Mehodology. Uni Roo Tess A ime series is inegraed when i has a mean revering propery and a finie variance. I is only emporarily ou of equilibrium and is called saionary in I(0). However a ime series ha

Properties of Autocorrelated Processes Economics 30331

Properies of Auocorrelaed Processes Economics 3033 Bill Evans Fall 05 Suppose we have ime series daa series labeled as where =,,3, T (he final period) Some examples are he dail closing price of he S&500,

Properies of Auocorrelaed Processes Economics 3033 Bill Evans Fall 05 Suppose we have ime series daa series labeled as where =,,3, T (he final period) Some examples are he dail closing price of he S&500,

Comparing Means: t-tests for One Sample & Two Related Samples

Comparing Means: -Tess for One Sample & Two Relaed Samples Using he z-tes: Assumpions -Tess for One Sample & Two Relaed Samples The z-es (of a sample mean agains a populaion mean) is based on he assumpion

Comparing Means: -Tess for One Sample & Two Relaed Samples Using he z-tes: Assumpions -Tess for One Sample & Two Relaed Samples The z-es (of a sample mean agains a populaion mean) is based on he assumpion

FORECASTS GENERATING FOR ARCH-GARCH PROCESSES USING THE MATLAB PROCEDURES

FORECASS GENERAING FOR ARCH-GARCH PROCESSES USING HE MALAB PROCEDURES Dušan Marček, Insiue of Comuer Science, Faculy of Philosohy and Science, he Silesian Universiy Oava he Faculy of Managemen Science

FORECASS GENERAING FOR ARCH-GARCH PROCESSES USING HE MALAB PROCEDURES Dušan Marček, Insiue of Comuer Science, Faculy of Philosohy and Science, he Silesian Universiy Oava he Faculy of Managemen Science

Smoothing. Backward smoother: At any give T, replace the observation yt by a combination of observations at & before T

Smoohing Consan process Separae signal & noise Smooh he daa: Backward smooher: A an give, replace he observaion b a combinaion of observaions a & before Simple smooher : replace he curren observaion wih

Smoohing Consan process Separae signal & noise Smooh he daa: Backward smooher: A an give, replace he observaion b a combinaion of observaions a & before Simple smooher : replace he curren observaion wih

Policy regimes Theory

Advanced Moneary Theory and Policy EPOS 2012/13 Policy regimes Theory Giovanni Di Barolomeo giovanni.dibarolomeo@uniroma1.i The moneary policy regime The simple model: x = - s (i - p e ) + x e + e D p

Advanced Moneary Theory and Policy EPOS 2012/13 Policy regimes Theory Giovanni Di Barolomeo giovanni.dibarolomeo@uniroma1.i The moneary policy regime The simple model: x = - s (i - p e ) + x e + e D p

Box-Jenkins Modelling of Nigerian Stock Prices Data

Greener Journal of Science Engineering and Technological Research ISSN: 76-7835 Vol. (), pp. 03-038, Sepember 0. Research Aricle Box-Jenkins Modelling of Nigerian Sock Prices Daa Ee Harrison Euk*, Barholomew

Greener Journal of Science Engineering and Technological Research ISSN: 76-7835 Vol. (), pp. 03-038, Sepember 0. Research Aricle Box-Jenkins Modelling of Nigerian Sock Prices Daa Ee Harrison Euk*, Barholomew

Affine term structure models

Affine erm srucure models A. Inro o Gaussian affine erm srucure models B. Esimaion by minimum chi square (Hamilon and Wu) C. Esimaion by OLS (Adrian, Moench, and Crump) D. Dynamic Nelson-Siegel model (Chrisensen,

Affine erm srucure models A. Inro o Gaussian affine erm srucure models B. Esimaion by minimum chi square (Hamilon and Wu) C. Esimaion by OLS (Adrian, Moench, and Crump) D. Dynamic Nelson-Siegel model (Chrisensen,

The Real Exchange Rate, Real Interest Rates, and the Risk Premium. Charles Engel University of Wisconsin

The Real Exchange Rae, Real Ineres Raes, an he Risk Premium Charles Engel Universiy of Wisconsin 1 Define he excess reurn or risk premium on Foreign s.. bons: λ i + Es+ 1 s i = r + Eq+ 1 q r The famous

The Real Exchange Rae, Real Ineres Raes, an he Risk Premium Charles Engel Universiy of Wisconsin 1 Define he excess reurn or risk premium on Foreign s.. bons: λ i + Es+ 1 s i = r + Eq+ 1 q r The famous

Macroeconomic Theory Ph.D. Qualifying Examination Fall 2005 ANSWER EACH PART IN A SEPARATE BLUE BOOK. PART ONE: ANSWER IN BOOK 1 WEIGHT 1/3

Macroeconomic Theory Ph.D. Qualifying Examinaion Fall 2005 Comprehensive Examinaion UCLA Dep. of Economics You have 4 hours o complee he exam. There are hree pars o he exam. Answer all pars. Each par has

Macroeconomic Theory Ph.D. Qualifying Examinaion Fall 2005 Comprehensive Examinaion UCLA Dep. of Economics You have 4 hours o complee he exam. There are hree pars o he exam. Answer all pars. Each par has

A Dynamic Model of Economic Fluctuations

CHAPTER 15 A Dynamic Model of Economic Flucuaions Modified for ECON 2204 by Bob Murphy 2016 Worh Publishers, all righs reserved IN THIS CHAPTER, OU WILL LEARN: how o incorporae dynamics ino he AD-AS model

CHAPTER 15 A Dynamic Model of Economic Flucuaions Modified for ECON 2204 by Bob Murphy 2016 Worh Publishers, all righs reserved IN THIS CHAPTER, OU WILL LEARN: how o incorporae dynamics ino he AD-AS model

Testing the Random Walk Model. i.i.d. ( ) r

r") he random walk heory saes: esing he Random Walk Model µ ε () np = + np + Momen Condiions where where ε ~ i.i.d he idea here is o es direcly he resricions imposed by momen condiions. lnp lnp µ ( lnp lnp

he random walk heory saes: esing he Random Walk Model µ ε () np = + np + Momen Condiions where where ε ~ i.i.d he idea here is o es direcly he resricions imposed by momen condiions. lnp lnp µ ( lnp lnp

Solutions to Exercises in Chapter 12

Chaper in Chaper. (a) The leas-squares esimaed equaion is given by (b)!i = 6. + 0.770 Y 0.8 R R = 0.86 (.5) (0.07) (0.6) Boh b and b 3 have he expeced signs; income is expeced o have a posiive effec on

Chaper in Chaper. (a) The leas-squares esimaed equaion is given by (b)!i = 6. + 0.770 Y 0.8 R R = 0.86 (.5) (0.07) (0.6) Boh b and b 3 have he expeced signs; income is expeced o have a posiive effec on

ACE 562 Fall Lecture 8: The Simple Linear Regression Model: R 2, Reporting the Results and Prediction. by Professor Scott H.

ACE 56 Fall 5 Lecure 8: The Simple Linear Regression Model: R, Reporing he Resuls and Predicion by Professor Sco H. Irwin Required Readings: Griffihs, Hill and Judge. "Explaining Variaion in he Dependen

ACE 56 Fall 5 Lecure 8: The Simple Linear Regression Model: R, Reporing he Resuls and Predicion by Professor Sco H. Irwin Required Readings: Griffihs, Hill and Judge. "Explaining Variaion in he Dependen

BOOTSTRAP PREDICTION INTERVALS FOR TIME SERIES MODELS WITH HETROSCEDASTIC ERRORS. Department of Statistics, Islamia College, Peshawar, KP, Pakistan 2

Pak. J. Sais. 017 Vol. 33(1), 1-13 BOOTSTRAP PREDICTIO ITERVAS FOR TIME SERIES MODES WITH HETROSCEDASTIC ERRORS Amjad Ali 1, Sajjad Ahmad Khan, Alamgir 3 Umair Khalil and Dos Muhammad Khan 1 Deparmen of

Pak. J. Sais. 017 Vol. 33(1), 1-13 BOOTSTRAP PREDICTIO ITERVAS FOR TIME SERIES MODES WITH HETROSCEDASTIC ERRORS Amjad Ali 1, Sajjad Ahmad Khan, Alamgir 3 Umair Khalil and Dos Muhammad Khan 1 Deparmen of

The Simple Linear Regression Model: Reporting the Results and Choosing the Functional Form

Chaper 6 The Simple Linear Regression Model: Reporing he Resuls and Choosing he Funcional Form To complee he analysis of he simple linear regression model, in his chaper we will consider how o measure

Chaper 6 The Simple Linear Regression Model: Reporing he Resuls and Choosing he Funcional Form To complee he analysis of he simple linear regression model, in his chaper we will consider how o measure

Richard A. Davis Colorado State University Bojan Basrak Eurandom Thomas Mikosch University of Groningen

Mulivariae Regular Variaion wih Applicaion o Financial Time Series Models Richard A. Davis Colorado Sae Universiy Bojan Basrak Eurandom Thomas Mikosch Universiy of Groningen Ouline + Characerisics of some

Mulivariae Regular Variaion wih Applicaion o Financial Time Series Models Richard A. Davis Colorado Sae Universiy Bojan Basrak Eurandom Thomas Mikosch Universiy of Groningen Ouline + Characerisics of some

Essential Microeconomics : OPTIMAL CONTROL 1. Consider the following class of optimization problems

Essenial Microeconomics -- 6.5: OPIMAL CONROL Consider he following class of opimizaion problems Max{ U( k, x) + U+ ( k+ ) k+ k F( k, x)}. { x, k+ } = In he language of conrol heory, he vecor k is he vecor

Essenial Microeconomics -- 6.5: OPIMAL CONROL Consider he following class of opimizaion problems Max{ U( k, x) + U+ ( k+ ) k+ k F( k, x)}. { x, k+ } = In he language of conrol heory, he vecor k is he vecor

Dynamic Models, Autocorrelation and Forecasting

ECON 4551 Economerics II Memorial Universiy of Newfoundland Dynamic Models, Auocorrelaion and Forecasing Adaped from Vera Tabakova s noes 9.1 Inroducion 9.2 Lags in he Error Term: Auocorrelaion 9.3 Esimaing

ECON 4551 Economerics II Memorial Universiy of Newfoundland Dynamic Models, Auocorrelaion and Forecasing Adaped from Vera Tabakova s noes 9.1 Inroducion 9.2 Lags in he Error Term: Auocorrelaion 9.3 Esimaing

Recursive Modelling of Symmetric and Asymmetric Volatility in the Presence of Extreme Observations *

Recursive Modelling of Symmeric and Asymmeric in he Presence of Exreme Observaions * Hock Guan Ng Deparmen of Accouning and Finance Universiy of Wesern Ausralia Michael McAleer Deparmen of Economics Universiy

Recursive Modelling of Symmeric and Asymmeric in he Presence of Exreme Observaions * Hock Guan Ng Deparmen of Accouning and Finance Universiy of Wesern Ausralia Michael McAleer Deparmen of Economics Universiy

Estocástica FINANZAS Y RIESGO

Sochasic discoun facor for Mexico and Chile... Esocásica Sochasic discoun facor for Mexico and Chile, a coninuous updaing esimaion approach Humbero Valencia Herrera Fecha de recepción: 2 de diciembre de

Sochasic discoun facor for Mexico and Chile... Esocásica Sochasic discoun facor for Mexico and Chile, a coninuous updaing esimaion approach Humbero Valencia Herrera Fecha de recepción: 2 de diciembre de

I. Return Calculations (20 pts, 4 points each)

") Universiy of Washingon Spring 015 Deparmen of Economics Eric Zivo Econ 44 Miderm Exam Soluions This is a closed book and closed noe exam. However, you are allowed one page of noes (8.5 by 11 or A4 double-sided)

Universiy of Washingon Spring 015 Deparmen of Economics Eric Zivo Econ 44 Miderm Exam Soluions This is a closed book and closed noe exam. However, you are allowed one page of noes (8.5 by 11 or A4 double-sided)

Types of Exponential Smoothing Methods. Simple Exponential Smoothing. Simple Exponential Smoothing

M Business Forecasing Mehods Exponenial moohing Mehods ecurer : Dr Iris Yeung Room No : P79 Tel No : 788 8 Types of Exponenial moohing Mehods imple Exponenial moohing Double Exponenial moohing Brown s

M Business Forecasing Mehods Exponenial moohing Mehods ecurer : Dr Iris Yeung Room No : P79 Tel No : 788 8 Types of Exponenial moohing Mehods imple Exponenial moohing Double Exponenial moohing Brown s

ADVANCED MATHEMATICS FOR ECONOMICS /2013 Sheet 3: Di erential equations

ADVANCED MATHEMATICS FOR ECONOMICS - /3 Shee 3: Di erenial equaions Check ha x() =± p ln(c( + )), where C is a posiive consan, is soluion of he ODE x () = Solve he following di erenial equaions: (a) x

ADVANCED MATHEMATICS FOR ECONOMICS - /3 Shee 3: Di erenial equaions Check ha x() =± p ln(c( + )), where C is a posiive consan, is soluion of he ODE x () = Solve he following di erenial equaions: (a) x

Sample Autocorrelations for Financial Time Series Models. Richard A. Davis Colorado State University Thomas Mikosch University of Copenhagen

Sample Auocorrelaions for Financial Time Series Models Richard A. Davis Colorado Sae Universiy Thomas Mikosch Universiy of Copenhagen Ouline Characerisics of some financial ime series IBM reurns NZ-USA

Sample Auocorrelaions for Financial Time Series Models Richard A. Davis Colorado Sae Universiy Thomas Mikosch Universiy of Copenhagen Ouline Characerisics of some financial ime series IBM reurns NZ-USA

C. Theoretical channels 1. Conditions for complete neutrality Suppose preferences are E t. Monetary policy at the zero lower bound: Theory 11/22/2017

//7 Moneary policy a he zero lower bound: Theory A. Theoreical channels. Condiions for complee neuraliy (Eggersson and Woodford, ). Marke fricions. Preferred habia and risk-bearing (Hamilon and Wu, ) B.

//7 Moneary policy a he zero lower bound: Theory A. Theoreical channels. Condiions for complee neuraliy (Eggersson and Woodford, ). Marke fricions. Preferred habia and risk-bearing (Hamilon and Wu, ) B.

GDP Advance Estimate, 2016Q4

GDP Advance Esimae, 26Q4 Friday, Jan 27 Real gross domesic produc (GDP) increased a an annual rae of.9 percen in he fourh quarer of 26. The deceleraion in real GDP in he fourh quarer refleced a downurn

GDP Advance Esimae, 26Q4 Friday, Jan 27 Real gross domesic produc (GDP) increased a an annual rae of.9 percen in he fourh quarer of 26. The deceleraion in real GDP in he fourh quarer refleced a downurn

Modeling Economic Time Series with Stochastic Linear Difference Equations

A. Thiemer, SLDG.mcd, 6..6 FH-Kiel Universiy of Applied Sciences Prof. Dr. Andreas Thiemer e-mail: andreas.hiemer@fh-kiel.de Modeling Economic Time Series wih Sochasic Linear Difference Equaions Summary:

A. Thiemer, SLDG.mcd, 6..6 FH-Kiel Universiy of Applied Sciences Prof. Dr. Andreas Thiemer e-mail: andreas.hiemer@fh-kiel.de Modeling Economic Time Series wih Sochasic Linear Difference Equaions Summary:

Økonomisk Kandidateksamen 2005(II) Econometrics 2. Solution

Econometrics 2. Solution") Økonomisk Kandidaeksamen 2005(II) Economerics 2 Soluion his is he proposed soluion for he exam in Economerics 2. For compleeness he soluion gives formal answers o mos of he quesions alhough his is no always

Økonomisk Kandidaeksamen 2005(II) Economerics 2 Soluion his is he proposed soluion for he exam in Economerics 2. For compleeness he soluion gives formal answers o mos of he quesions alhough his is no always

Lecture Notes 3: Quantitative Analysis in DSGE Models: New Keynesian Model

Lecure Noes 3: Quaniaive Analysis in DSGE Models: New Keynesian Model Zhiwei Xu, Email: xuzhiwei@sju.edu.cn The moneary policy plays lile role in he basic moneary model wihou price sickiness. We now urn

Lecure Noes 3: Quaniaive Analysis in DSGE Models: New Keynesian Model Zhiwei Xu, Email: xuzhiwei@sju.edu.cn The moneary policy plays lile role in he basic moneary model wihou price sickiness. We now urn

TIME DEPENDENT CONDITIONAL HETEROSKEDASTICITY

TIME DEPENDENT CONDITIONAL HETEROSKEDASTICITY Professor Richard Baillie, (March 004 Iniially ime series economeric work emphasized modeling and esing relaionships in he condiional mean of a variable. However,

TIME DEPENDENT CONDITIONAL HETEROSKEDASTICITY Professor Richard Baillie, (March 004 Iniially ime series economeric work emphasized modeling and esing relaionships in he condiional mean of a variable. However,

Lecture #31, 32: The Ornstein-Uhlenbeck Process as a Model of Volatility

Saisics 441 (Fall 214) November 19, 21, 214 Prof Michael Kozdron Lecure #31, 32: The Ornsein-Uhlenbeck Process as a Model of Volailiy The Ornsein-Uhlenbeck process is a di usion process ha was inroduced

Saisics 441 (Fall 214) November 19, 21, 214 Prof Michael Kozdron Lecure #31, 32: The Ornsein-Uhlenbeck Process as a Model of Volailiy The Ornsein-Uhlenbeck process is a di usion process ha was inroduced

Exchange Rates and Interest Rates: Levels and Changes of the Price of Foreign Currency

Exchange Raes and Ineres Raes: Levels and Changes of he Price of Foreign Currency Charles Engel Universiy of Wisconsin Conference in Honor of James Hamilon, Federal Reserve Bank of San Francisco, Sepember

Exchange Raes and Ineres Raes: Levels and Changes of he Price of Foreign Currency Charles Engel Universiy of Wisconsin Conference in Honor of James Hamilon, Federal Reserve Bank of San Francisco, Sepember

ESTIMATION OF DYNAMIC PANEL DATA MODELS WHEN REGRESSION COEFFICIENTS AND INDIVIDUAL EFFECTS ARE TIME-VARYING

Inernaional Journal of Social Science and Economic Research Volume:02 Issue:0 ESTIMATION OF DYNAMIC PANEL DATA MODELS WHEN REGRESSION COEFFICIENTS AND INDIVIDUAL EFFECTS ARE TIME-VARYING Chung-ki Min Professor

Inernaional Journal of Social Science and Economic Research Volume:02 Issue:0 ESTIMATION OF DYNAMIC PANEL DATA MODELS WHEN REGRESSION COEFFICIENTS AND INDIVIDUAL EFFECTS ARE TIME-VARYING Chung-ki Min Professor

ACE 562 Fall Lecture 5: The Simple Linear Regression Model: Sampling Properties of the Least Squares Estimators. by Professor Scott H.

ACE 56 Fall 005 Lecure 5: he Simple Linear Regression Model: Sampling Properies of he Leas Squares Esimaors by Professor Sco H. Irwin Required Reading: Griffihs, Hill and Judge. "Inference in he Simple

ACE 56 Fall 005 Lecure 5: he Simple Linear Regression Model: Sampling Properies of he Leas Squares Esimaors by Professor Sco H. Irwin Required Reading: Griffihs, Hill and Judge. "Inference in he Simple

3.1.3 INTRODUCTION TO DYNAMIC OPTIMIZATION: DISCRETE TIME PROBLEMS. A. The Hamiltonian and First-Order Conditions in a Finite Time Horizon

3..3 INRODUCION O DYNAMIC OPIMIZAION: DISCREE IME PROBLEMS A. he Hamilonian and Firs-Order Condiions in a Finie ime Horizon Define a new funcion, he Hamilonian funcion, H. H he change in he oal value of

3..3 INRODUCION O DYNAMIC OPIMIZAION: DISCREE IME PROBLEMS A. he Hamilonian and Firs-Order Condiions in a Finie ime Horizon Define a new funcion, he Hamilonian funcion, H. H he change in he oal value of

dy dx = xey (a) y(0) = 2 (b) y(1) = 2.5 SOLUTION: See next page

y(0) = 2 (b) y(1) = 2.5 SOLUTION: See next page") Assignmen 1 MATH 2270 SOLUTION Please wrie ou complee soluions for each of he following 6 problems (one more will sill be added). You may, of course, consul wih your classmaes, he exbook or oher resources,

Assignmen 1 MATH 2270 SOLUTION Please wrie ou complee soluions for each of he following 6 problems (one more will sill be added). You may, of course, consul wih your classmaes, he exbook or oher resources,

Kriging Models Predicting Atrazine Concentrations in Surface Water Draining Agricultural Watersheds

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 Kriging Models Predicing Arazine Concenraions in Surface Waer Draining Agriculural Waersheds Paul L. Mosquin, Jeremy Aldworh, Wenlin Chen Supplemenal Maerial Number

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 Kriging Models Predicing Arazine Concenraions in Surface Waer Draining Agriculural Waersheds Paul L. Mosquin, Jeremy Aldworh, Wenlin Chen Supplemenal Maerial Number

Financial Econometrics Introduction to Realized Variance

Financial Economerics Inroducion o Realized Variance Eric Zivo May 16, 2011 Ouline Inroducion Realized Variance Defined Quadraic Variaion and Realized Variance Asympoic Disribuion Theory for Realized Variance

Financial Economerics Inroducion o Realized Variance Eric Zivo May 16, 2011 Ouline Inroducion Realized Variance Defined Quadraic Variaion and Realized Variance Asympoic Disribuion Theory for Realized Variance

Problem Set on Differential Equations

Problem Se on Differenial Equaions 1. Solve he following differenial equaions (a) x () = e x (), x () = 3/ 4. (b) x () = e x (), x (1) =. (c) xe () = + (1 x ()) e, x () =.. (An asse marke model). Le p()

Problem Se on Differenial Equaions 1. Solve he following differenial equaions (a) x () = e x (), x () = 3/ 4. (b) x () = e x (), x (1) =. (c) xe () = + (1 x ()) e, x () =.. (An asse marke model). Le p()

Vehicle Arrival Models : Headway

Chaper 12 Vehicle Arrival Models : Headway 12.1 Inroducion Modelling arrival of vehicle a secion of road is an imporan sep in raffic flow modelling. I has imporan applicaion in raffic flow simulaion where

Chaper 12 Vehicle Arrival Models : Headway 12.1 Inroducion Modelling arrival of vehicle a secion of road is an imporan sep in raffic flow modelling. I has imporan applicaion in raffic flow simulaion where

Wednesday, November 7 Handout: Heteroskedasticity

Amhers College Deparmen of Economics Economics 360 Fall 202 Wednesday, November 7 Handou: Heeroskedasiciy Preview Review o Regression Model o Sandard Ordinary Leas Squares (OLS) Premises o Esimaion Procedures

Amhers College Deparmen of Economics Economics 360 Fall 202 Wednesday, November 7 Handou: Heeroskedasiciy Preview Review o Regression Model o Sandard Ordinary Leas Squares (OLS) Premises o Esimaion Procedures

Chapter 11. Heteroskedasticity The Nature of Heteroskedasticity. In Chapter 3 we introduced the linear model (11.1.1)

") Chaper 11 Heeroskedasiciy 11.1 The Naure of Heeroskedasiciy In Chaper 3 we inroduced he linear model y = β+β x (11.1.1) 1 o explain household expendiure on food (y) as a funcion of household income (x).

Chaper 11 Heeroskedasiciy 11.1 The Naure of Heeroskedasiciy In Chaper 3 we inroduced he linear model y = β+β x (11.1.1) 1 o explain household expendiure on food (y) as a funcion of household income (x).

Quarterly ice cream sales are high each summer, and the series tends to repeat itself each year, so that the seasonal period is 4.

Seasonal models Many business and economic ime series conain a seasonal componen ha repeas iself afer a regular period of ime. The smalles ime period for his repeiion is called he seasonal period, and

Seasonal models Many business and economic ime series conain a seasonal componen ha repeas iself afer a regular period of ime. The smalles ime period for his repeiion is called he seasonal period, and

The consumption-based determinants of the term structure of discount rates: Corrigendum. Christian Gollier 1 Toulouse School of Economics March 2012

The consumpion-based deerminans of he erm srucure of discoun raes: Corrigendum Chrisian Gollier Toulouse School of Economics March 0 In Gollier (007), I examine he effec of serially correlaed growh raes

The consumpion-based deerminans of he erm srucure of discoun raes: Corrigendum Chrisian Gollier Toulouse School of Economics March 0 In Gollier (007), I examine he effec of serially correlaed growh raes

Smooth Transition Autoregressive-GARCH Model in Forecasting Non-linear Economic Time Series Data

Journal of Saisical and conomeric Mehods, vol., no., 03, -9 ISSN: 05-5057 (prin version), 05-5065(online) Scienpress d, 03 Smooh Transiion Auoregressive-GARCH Model in Forecasing Non-linear conomic Time

Journal of Saisical and conomeric Mehods, vol., no., 03, -9 ISSN: 05-5057 (prin version), 05-5065(online) Scienpress d, 03 Smooh Transiion Auoregressive-GARCH Model in Forecasing Non-linear conomic Time