LECTURE 9: GENTLE INTRODUCTION TO

|

|

|

- Oscar Joseph

- 5 years ago

- Views:

Transcription

1 LECTURE 9: GENTLE INTRODUCTION TO REGRESSION WITH TIME SERIES

2 From random variables to random processes (cont d) 2 in cross-sectional regression, we were making inferences about the whole population based on a small sample a crucial assumption: random sampling the bridge between population characteristics (distribution of wages in a country) and the probabilistic machinery of random variables (distribution of a wage of a randomly drawn person) unfortunately, with time series, random sampling makes no sense: year GDP inflation unemp , , what would the underlying population be?

3 From random variables to random processes (cont d) 3 random sampling makes the characteristics of different individuals independent it is difficult to imagine that GDP in 2004 is independent of that in 2005 therefore, we will have to switch to a more advanced theoretical vehicle: random processes those who had taken courses in random processes would tell you it was difficult we will omit many mathematical details, and focus on the intuition

4 New issues with time series 4 good news: everything we learnt with cross-sectional data will be used in time-series analysis, too bad news: many new pitfalls that can spoil the analysis 1. trends and seasonality: can result in spurious regression (see next slide) 2. lags in economic behaviour: government s expenditure cuts will slowly percolate through the economy lagged effect (the effect of today s cuts will spread over quarters or even years) 3. persistence in time series: governments expenditure itself cannot change too dramatically from one year to another most real-life time series persistent, but the degree differs strong persistence of time series can again produce spurious regression (stationarity, unit-root issues) weak persistence problematic only if applies to u (serial correlation, or autocorrelation of u)

5 Spurious regression problem 5 both y and x both exhibit a monotonous trend, we will find a relationship even though they have nothing in common Example: Norwegian salmon production vs GDP in the U.S. the data in salmon.gdt contain two annual time series ( ) annual salmon production in Norway GDP in the U.S. (bln. of 2005 dollars) do you think that there is a strong causal relationship? estimated equation in Gretl: ^gdp = 1.34e *salmon (713) ( ) T = 29, R-squared = (standard errors in parentheses) Quizz: is salmon significant at the 5 % level? And how about 1 %?

6 Let s look at the time series first: 6

7 Fitted values are calculated as: 13,

8 Accounting for trends in the regressions 8 Option 1 detrend all time series, i.e. create new variables where the linear trends have been subtracted two steps involved: (1) regress x t on t (time, values 1,2,,n) (2) save residuals (this is the detrended x t ) salmon series and its linear trend detrended salmon series

9 Accounting for trends in the regressions (cont d) 9 Option 2: add variable t (time) to the estimated equation Option 1: results ^gdp_detrended = 1.46e *salmon_detrended (52.7) ( ) T = 29, R-squared = (standard errors in parentheses) Option 2: results ^gdp = 5.14e *salmon + 295*time (304) ( ) (9.90) T = 29, R-squared = (standard errors in parentheses) salmon coefficient identical, std. errors nearly identical can use both R-squareds different, but most variation explained by time in Option 2 use detrended dependent variable for the R-squared!

10 10 Frisch-Waugh-Lovell theorem ===================================================================== Dependent variable: gdp gdp_detrended gdp (1) (2) (3) (4) year *** * ( ) ( ) salmon ** ** ( ) ( ) salmon_detrended ** ( ) ( ) Constant -578, *** -38, * (19, ) (19, ) Observations R =====================================================================

11 Using dummies to account for specific events 11 Example: fertility equation frequency: annual data, gfr = the number of births per 1000 women aged ww2 = 1 for years , = 0 otherwise expected fertility β 0 β 1 gfr ww u t 0 1 2t t WW2 period time

12

13

14 Using dummies to account for specific events (cont d) 14 Example: fertility equation 2 pill = 0 before 1963, = 1 afterwards expected fertility β 0 β 1 gfr pill u t 0 1 t t contraceptive pill introduced time

15

16 16 gfr β β ww2 β pill u t 0 1 t 2 t t

17 Seasonality 17 seasonal patterns are noticeable with quarterly, monthly, or daily data note that many time series in the online databases are seasonally adjusted, meaning that specialized algorithms have been used to even out the differences between seasons these series can be used without further ado when using a seasonally unadjusted series, we can still use a simple fix that accounts for the seasonal variation: periodic dummies, i.e. dummy variables that identify individual periods Example: durable goods open durgoods.gdt in Gretl change dataset structure to a quarterly time series (Data Dataset structure) add periodic dummies (Add Periodic dummies) this creates variables dq1,, dq4 (dq1 stands for dummy for quarter 1 )

18 18

19 values of the periodic dummies 19

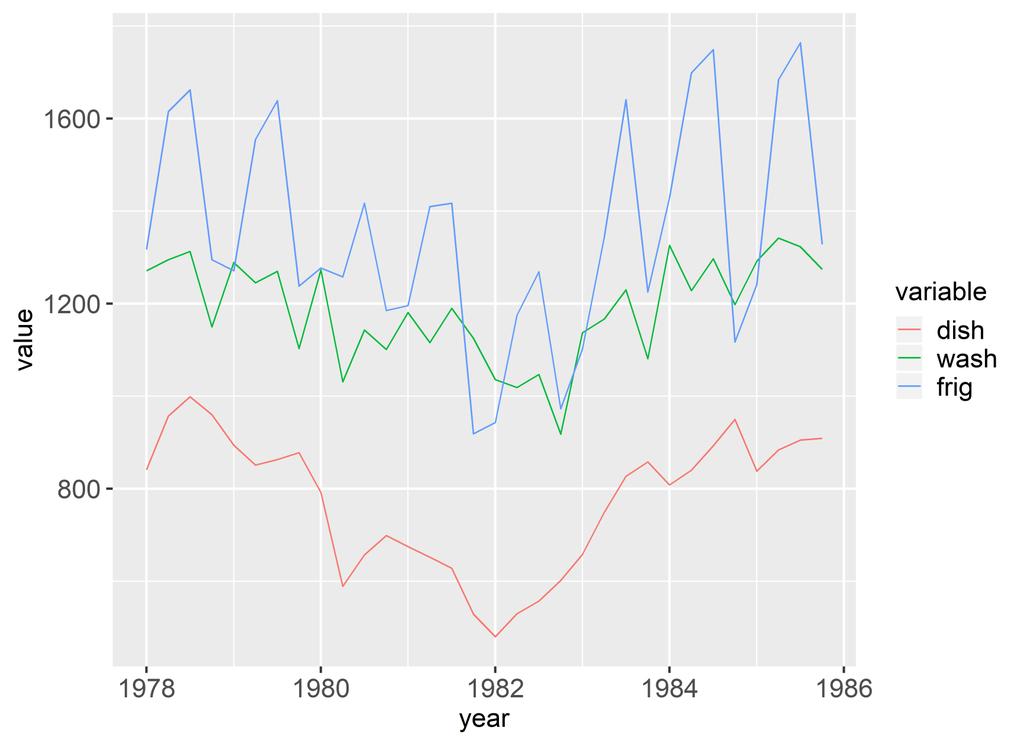

20 Seasonality (cont d) 20 to describe the seasonal pattern in dishwasher sales, run the regression dish dq1 dq2 dq3 u t 0 1 t 2 t 3 t t the dishwasher time series and the fitted values are shown below, F-test for joint significance: p-value = 0.89 no statistical evidence of seasonality

21 Seasonality (cont d) 21 with refrigerator series, that s a different story: joint significance: p-value = , strong evidence of seasonality (i.e. we reject the null of no seasonal pattern)

22 Seasonality (cont d) 22 interpretation: just as with other category dummies we omitted dq4 quarter 4 is the base period e.g., the coefficient on dq1 tells us that in quarter 1, sales are higher by 62,125 than in quarter 4 (on average) Model 2: OLS, using observations 1978:1-1985:4 (T = 32) Dependent variable: frig coefficient std. error t-ratio p-value const e-018 *** dq dq *** dq e-05 *** Mean dependent var S.D. dependent var Sum squared resid S.E. of regression R-squared Adjusted R-squared F(3, 28) P-value(F)

23 Seasonality (cont d) 23 conclusion: with seasonally unadjusted data, it makes sense to add both a time trend and periodic dummies in addition to your independent variables of interest note that this can be done also in case the dependent variable is logged, only the interpretation changes: ^l_frig = *dq *dq *dq3 (0.0458)(0.0647) (0.0647) (0.0647) T = 32, R-squared = (standard errors in parentheses) results imply that in quarter 1, sales increase by 5.3 % compared with the baseline level of quarter 4

24 ^l_frig = *dq *dq *dq *time *sq_time (0.0590)(0.0470) (0.0471) (0.0473) ( ) ( ) T = 32, R-squared = Null hypothesis: the regression parameters are zero for the variables dq2, dq3, dq4 Test statistic: F(3, 26) = , p-value e-007

25 Finite distributed lag (FDL) model 25 Example: fertility equation 3 pe = real dollar value of personal tax exemption gfr pe pe pe pe u t 0 0 t 1 t1 2 t2 3 t3 t here, δ 0 is the impact propensity (= immediate effect) of a unit increase in pe the δ parameters capture the effect of a temporary increase in pe: assume that pe equals c except for period 0, where it increases to c + 1: pe t c time

26

27 pe t 1 c pe t 1 1 c pe t 2 pe t 3 c c 1 1 a temporary change in pe occurs in subsequent periods in lagged versions of pe gfr t d δ 0 δ 1 δ 2 δ 3 the effect of a temporary change in pe, or the lag distribution time 27

28

29 Finite distributed lag (FDL) model (cont d) 29 long-run propensity (LRP): the effect of a permanent unit increase in pe LRP pe t 1 c gfr t d δ 0 δ 1 δ 2 δ 3 the effect of a permanent change in pe, or long-run propensity time

30

31 gfr β β ww2 β pill β t δ pe δ pe δ pe δ pe u t 0 1 t 2 t 3 0 t 1 t 1 2 t 2 3 t 3 t

32 Finite distributed lag (FDL) model (cont d) 32 Estimating LRP a natural estimator of LRP is LRP ˆ ˆ ˆ ˆ so we just add up the coefficients on pe and its lags more work is required in case we need std. errors or 95% CI for LRP we ll use a simple trick: the equation can be rewritten as follows gfr pe pe pe pe u t 0 0 t 1 t1 2 t2 3 t3 t LRP pe ( pe pe ) ( pe pe ) ( pe pe ) u 0 t 1 t1 t 2 t2 t 3 t3 t t A B C this gives us the following procedure: 1. Create variables A, B, and C. in Gretl: Add Define new variable A = pe( 1) pe etc. 2. Regress gfr on pe, A, B and C; now, LRP is the coefficient on pe, and we can read off its std. error and calculate the 95% CI if needed.

33 LECTURE 9: GENTLE INTRODUCTION TO REGRESSION WITH TIME SERIES

Outline. 11. Time Series Analysis. Basic Regression. Differences between Time Series and Cross Section

Outline I. The Nature of Time Series Data 11. Time Series Analysis II. Examples of Time Series Models IV. Functional Form, Dummy Variables, and Index Basic Regression Numbers Read Wooldridge (2013), Chapter

Outline I. The Nature of Time Series Data 11. Time Series Analysis II. Examples of Time Series Models IV. Functional Form, Dummy Variables, and Index Basic Regression Numbers Read Wooldridge (2013), Chapter

7 Introduction to Time Series Time Series vs. Cross-Sectional Data Detrending Time Series... 15

Econ 495 - Econometric Review 1 Contents 7 Introduction to Time Series 3 7.1 Time Series vs. Cross-Sectional Data............ 3 7.2 Detrending Time Series................... 15 7.3 Types of Stochastic

Econ 495 - Econometric Review 1 Contents 7 Introduction to Time Series 3 7.1 Time Series vs. Cross-Sectional Data............ 3 7.2 Detrending Time Series................... 15 7.3 Types of Stochastic

7 Introduction to Time Series

Econ 495 - Econometric Review 1 7 Introduction to Time Series 7.1 Time Series vs. Cross-Sectional Data Time series data has a temporal ordering, unlike cross-section data, we will need to changes some

Econ 495 - Econometric Review 1 7 Introduction to Time Series 7.1 Time Series vs. Cross-Sectional Data Time series data has a temporal ordering, unlike cross-section data, we will need to changes some

Multiple Regression. Midterm results: AVG = 26.5 (88%) A = 27+ B = C =

A = 27+ B = C =") Economics 130 Lecture 6 Midterm Review Next Steps for the Class Multiple Regression Review & Issues Model Specification Issues Launching the Projects!!!!! Midterm results: AVG = 26.5 (88%) A = 27+ B =

Economics 130 Lecture 6 Midterm Review Next Steps for the Class Multiple Regression Review & Issues Model Specification Issues Launching the Projects!!!!! Midterm results: AVG = 26.5 (88%) A = 27+ B =

Introduction to Econometrics

Introduction to Econometrics STAT-S-301 Introduction to Time Series Regression and Forecasting (2016/2017) Lecturer: Yves Dominicy Teaching Assistant: Elise Petit 1 Introduction to Time Series Regression

Introduction to Econometrics STAT-S-301 Introduction to Time Series Regression and Forecasting (2016/2017) Lecturer: Yves Dominicy Teaching Assistant: Elise Petit 1 Introduction to Time Series Regression

LECTURE 11. Introduction to Econometrics. Autocorrelation

LECTURE 11 Introduction to Econometrics Autocorrelation November 29, 2016 1 / 24 ON PREVIOUS LECTURES We discussed the specification of a regression equation Specification consists of choosing: 1. correct

LECTURE 11 Introduction to Econometrics Autocorrelation November 29, 2016 1 / 24 ON PREVIOUS LECTURES We discussed the specification of a regression equation Specification consists of choosing: 1. correct

Basic Regression Analysis with Time Series Data

Basic Regression Analysis with Time Series Data Ping Yu School of Economics and Finance The University of Hong Kong Ping Yu (HKU) Basic Time Series 1 / 50 The Nature of Time Series Data The Nature of Time

Basic Regression Analysis with Time Series Data Ping Yu School of Economics and Finance The University of Hong Kong Ping Yu (HKU) Basic Time Series 1 / 50 The Nature of Time Series Data The Nature of Time

Economics Introduction to Econometrics - Fall 2007 Final Exam - Answers

Student Name: Economics 4818 - Introduction to Econometrics - Fall 2007 Final Exam - Answers SHOW ALL WORK! Evaluation: Problems: 3, 4C, 5C and 5F are worth 4 points. All other questions are worth 3 points.

Student Name: Economics 4818 - Introduction to Econometrics - Fall 2007 Final Exam - Answers SHOW ALL WORK! Evaluation: Problems: 3, 4C, 5C and 5F are worth 4 points. All other questions are worth 3 points.

LECTURE 10: MORE ON RANDOM PROCESSES

LECTURE 10: MORE ON RANDOM PROCESSES AND SERIAL CORRELATION 2 Classification of random processes (cont d) stationary vs. non-stationary processes stationary = distribution does not change over time more

LECTURE 10: MORE ON RANDOM PROCESSES AND SERIAL CORRELATION 2 Classification of random processes (cont d) stationary vs. non-stationary processes stationary = distribution does not change over time more

The multiple regression model; Indicator variables as regressors

The multiple regression model; Indicator variables as regressors Ragnar Nymoen University of Oslo 28 February 2013 1 / 21 This lecture (#12): Based on the econometric model specification from Lecture 9

The multiple regression model; Indicator variables as regressors Ragnar Nymoen University of Oslo 28 February 2013 1 / 21 This lecture (#12): Based on the econometric model specification from Lecture 9

Applied Economics. Panel Data. Department of Economics Universidad Carlos III de Madrid

Applied Economics Panel Data Department of Economics Universidad Carlos III de Madrid See also Wooldridge (chapter 13), and Stock and Watson (chapter 10) 1 / 38 Panel Data vs Repeated Cross-sections In

Applied Economics Panel Data Department of Economics Universidad Carlos III de Madrid See also Wooldridge (chapter 13), and Stock and Watson (chapter 10) 1 / 38 Panel Data vs Repeated Cross-sections In

10. Time series regression and forecasting

10. Time series regression and forecasting Key feature of this section: Analysis of data on a single entity observed at multiple points in time (time series data) Typical research questions: What is the

10. Time series regression and forecasting Key feature of this section: Analysis of data on a single entity observed at multiple points in time (time series data) Typical research questions: What is the

Making sense of Econometrics: Basics

Making sense of Econometrics: Basics Lecture 4: Qualitative influences and Heteroskedasticity Egypt Scholars Economic Society November 1, 2014 Assignment & feedback enter classroom at http://b.socrative.com/login/student/

Making sense of Econometrics: Basics Lecture 4: Qualitative influences and Heteroskedasticity Egypt Scholars Economic Society November 1, 2014 Assignment & feedback enter classroom at http://b.socrative.com/login/student/

Wooldridge, Introductory Econometrics, 2d ed. Chapter 10: Basic regression analysis with time series data We now turn to the analysis of time series

Wooldridge, Introductory Econometrics, 2d ed. Chapter 10: Basic regression analysis with time series data We now turn to the analysis of time series data. One of the key assumptions underlying our analysis

Wooldridge, Introductory Econometrics, 2d ed. Chapter 10: Basic regression analysis with time series data We now turn to the analysis of time series data. One of the key assumptions underlying our analysis

Exercises (in progress) Applied Econometrics Part 1

Applied Econometrics Part 1") Exercises (in progress) Applied Econometrics 2016-2017 Part 1 1. De ne the concept of unbiased estimator. 2. Explain what it is a classic linear regression model and which are its distinctive features.

Exercises (in progress) Applied Econometrics 2016-2017 Part 1 1. De ne the concept of unbiased estimator. 2. Explain what it is a classic linear regression model and which are its distinctive features.

7. Integrated Processes

7. Integrated Processes Up to now: Analysis of stationary processes (stationary ARMA(p, q) processes) Problem: Many economic time series exhibit non-stationary patterns over time 226 Example: We consider

7. Integrated Processes Up to now: Analysis of stationary processes (stationary ARMA(p, q) processes) Problem: Many economic time series exhibit non-stationary patterns over time 226 Example: We consider

Time Series. Chapter Time Series Data

Chapter 10 Time Series 10.1 Time Series Data The main difference between time series data and cross-sectional data is the temporal ordering. To emphasize the proper ordering of the observations, Table

Chapter 10 Time Series 10.1 Time Series Data The main difference between time series data and cross-sectional data is the temporal ordering. To emphasize the proper ordering of the observations, Table

7. Integrated Processes

7. Integrated Processes Up to now: Analysis of stationary processes (stationary ARMA(p, q) processes) Problem: Many economic time series exhibit non-stationary patterns over time 226 Example: We consider

7. Integrated Processes Up to now: Analysis of stationary processes (stationary ARMA(p, q) processes) Problem: Many economic time series exhibit non-stationary patterns over time 226 Example: We consider

Covers Chapter 10-12, some of 16, some of 18 in Wooldridge. Regression Analysis with Time Series Data

Covers Chapter 10-12, some of 16, some of 18 in Wooldridge Regression Analysis with Time Series Data Obviously time series data different from cross section in terms of source of variation in x and y temporal

Covers Chapter 10-12, some of 16, some of 18 in Wooldridge Regression Analysis with Time Series Data Obviously time series data different from cross section in terms of source of variation in x and y temporal

LECTURE 5. Introduction to Econometrics. Hypothesis testing

LECTURE 5 Introduction to Econometrics Hypothesis testing October 18, 2016 1 / 26 ON TODAY S LECTURE We are going to discuss how hypotheses about coefficients can be tested in regression models We will

LECTURE 5 Introduction to Econometrics Hypothesis testing October 18, 2016 1 / 26 ON TODAY S LECTURE We are going to discuss how hypotheses about coefficients can be tested in regression models We will

Exercise sheet 6 Models with endogenous explanatory variables

Exercise sheet 6 Models with endogenous explanatory variables Note: Some of the exercises include estimations and references to the data files. Use these to compare them to the results you obtained with

Exercise sheet 6 Models with endogenous explanatory variables Note: Some of the exercises include estimations and references to the data files. Use these to compare them to the results you obtained with

EC408 Topics in Applied Econometrics. B Fingleton, Dept of Economics, Strathclyde University

EC408 Topics in Applied Econometrics B Fingleton, Dept of Economics, Strathclyde University Applied Econometrics What is spurious regression? How do we check for stochastic trends? Cointegration and Error

EC408 Topics in Applied Econometrics B Fingleton, Dept of Economics, Strathclyde University Applied Econometrics What is spurious regression? How do we check for stochastic trends? Cointegration and Error

Lecture 8a: Spurious Regression

Lecture 8a: Spurious Regression 1 2 Old Stuff The traditional statistical theory holds when we run regression using stationary variables. For example, when we regress one stationary series onto another

Lecture 8a: Spurious Regression 1 2 Old Stuff The traditional statistical theory holds when we run regression using stationary variables. For example, when we regress one stationary series onto another

Solutions to Problem Set 6 (Due December 8) Maximum number of points for Problem set 8 is: 220. Problem 10.6

Maximum number of points for Problem set 8 is: 220. Problem 10.6") Solutions to Problem Set 6 (Due December 8) EC 228 02, Fall 2010 Prof. Baum, Ms Hristakeva Maximum number of points for Problem set 8 is: 220 Problem 10.6 (i) (5 pts) Given the formula for δ j = γ 0 +

Solutions to Problem Set 6 (Due December 8) EC 228 02, Fall 2010 Prof. Baum, Ms Hristakeva Maximum number of points for Problem set 8 is: 220 Problem 10.6 (i) (5 pts) Given the formula for δ j = γ 0 +

ECON3150/4150 Spring 2016

ECON3150/4150 Spring 2016 Lecture 4 - The linear regression model Siv-Elisabeth Skjelbred University of Oslo Last updated: January 26, 2016 1 / 49 Overview These lecture slides covers: The linear regression

ECON3150/4150 Spring 2016 Lecture 4 - The linear regression model Siv-Elisabeth Skjelbred University of Oslo Last updated: January 26, 2016 1 / 49 Overview These lecture slides covers: The linear regression

Lecture 8a: Spurious Regression

Lecture 8a: Spurious Regression 1 Old Stuff The traditional statistical theory holds when we run regression using (weakly or covariance) stationary variables. For example, when we regress one stationary

Lecture 8a: Spurious Regression 1 Old Stuff The traditional statistical theory holds when we run regression using (weakly or covariance) stationary variables. For example, when we regress one stationary

Statistics and Quantitative Analysis U4320. Segment 10 Prof. Sharyn O Halloran

Statistics and Quantitative Analysis U4320 Segment 10 Prof. Sharyn O Halloran Key Points 1. Review Univariate Regression Model 2. Introduce Multivariate Regression Model Assumptions Estimation Hypothesis

Statistics and Quantitative Analysis U4320 Segment 10 Prof. Sharyn O Halloran Key Points 1. Review Univariate Regression Model 2. Introduce Multivariate Regression Model Assumptions Estimation Hypothesis

Autoregressive models with distributed lags (ADL)

") Autoregressive models with distributed lags (ADL) It often happens than including the lagged dependent variable in the model results in model which is better fitted and needs less parameters. It can be

Autoregressive models with distributed lags (ADL) It often happens than including the lagged dependent variable in the model results in model which is better fitted and needs less parameters. It can be

Testing methodology. It often the case that we try to determine the form of the model on the basis of data

Testing methodology It often the case that we try to determine the form of the model on the basis of data The simplest case: we try to determine the set of explanatory variables in the model Testing for

Testing methodology It often the case that we try to determine the form of the model on the basis of data The simplest case: we try to determine the set of explanatory variables in the model Testing for

Decision 411: Class 7

Decision 411: Class 7 Confidence limits for sums of coefficients Use of the time index as a regressor The difficulty of predicting the future Confidence intervals for sums of coefficients Sometimes the

Decision 411: Class 7 Confidence limits for sums of coefficients Use of the time index as a regressor The difficulty of predicting the future Confidence intervals for sums of coefficients Sometimes the

9) Time series econometrics

Time series econometrics") 30C00200 Econometrics 9) Time series econometrics Timo Kuosmanen Professor Management Science http://nomepre.net/index.php/timokuosmanen 1 Macroeconomic data: GDP Inflation rate Examples of time series

30C00200 Econometrics 9) Time series econometrics Timo Kuosmanen Professor Management Science http://nomepre.net/index.php/timokuosmanen 1 Macroeconomic data: GDP Inflation rate Examples of time series

Econ 423 Lecture Notes: Additional Topics in Time Series 1

Econ 423 Lecture Notes: Additional Topics in Time Series 1 John C. Chao April 25, 2017 1 These notes are based in large part on Chapter 16 of Stock and Watson (2011). They are for instructional purposes

Econ 423 Lecture Notes: Additional Topics in Time Series 1 John C. Chao April 25, 2017 1 These notes are based in large part on Chapter 16 of Stock and Watson (2011). They are for instructional purposes

LECTURE 2: SIMPLE REGRESSION I

LECTURE 2: SIMPLE REGRESSION I 2 Introducing Simple Regression Introducing Simple Regression 3 simple regression = regression with 2 variables y dependent variable explained variable response variable

LECTURE 2: SIMPLE REGRESSION I 2 Introducing Simple Regression Introducing Simple Regression 3 simple regression = regression with 2 variables y dependent variable explained variable response variable

Lectures 5 & 6: Hypothesis Testing

Lectures 5 & 6: Hypothesis Testing in which you learn to apply the concept of statistical significance to OLS estimates, learn the concept of t values, how to use them in regression work and come across

Lectures 5 & 6: Hypothesis Testing in which you learn to apply the concept of statistical significance to OLS estimates, learn the concept of t values, how to use them in regression work and come across

UNIVERSIDAD CARLOS III DE MADRID ECONOMETRICS FINAL EXAM (Type B) 2. This document is self contained. Your are not allowed to use any other material.

2. This document is self contained. Your are not allowed to use any other material.") DURATION: 125 MINUTES Directions: UNIVERSIDAD CARLOS III DE MADRID ECONOMETRICS FINAL EXAM (Type B) 1. This is an example of a exam that you can use to self-evaluate about the contents of the course Econometrics

DURATION: 125 MINUTES Directions: UNIVERSIDAD CARLOS III DE MADRID ECONOMETRICS FINAL EXAM (Type B) 1. This is an example of a exam that you can use to self-evaluate about the contents of the course Econometrics

Exercise Sheet 5: Solutions

Exercise Sheet 5: Solutions R.G. Pierse 2. Estimation of Model M1 yields the following results: Date: 10/24/02 Time: 18:06 C -1.448432 0.696587-2.079327 0.0395 LPC -0.306051 0.272836-1.121740 0.2640 LPF

Exercise Sheet 5: Solutions R.G. Pierse 2. Estimation of Model M1 yields the following results: Date: 10/24/02 Time: 18:06 C -1.448432 0.696587-2.079327 0.0395 LPC -0.306051 0.272836-1.121740 0.2640 LPF

Announcements. J. Parman (UC-Davis) Analysis of Economic Data, Winter 2011 February 8, / 45

Analysis of Economic Data, Winter 2011 February 8, / 45") Announcements Solutions to Problem Set 3 are posted Problem Set 4 is posted, It will be graded and is due a week from Friday You already know everything you need to work on Problem Set 4 Professor Miller

Announcements Solutions to Problem Set 3 are posted Problem Set 4 is posted, It will be graded and is due a week from Friday You already know everything you need to work on Problem Set 4 Professor Miller

ECON3150/4150 Spring 2015

ECON3150/4150 Spring 2015 Lecture 3&4 - The linear regression model Siv-Elisabeth Skjelbred University of Oslo January 29, 2015 1 / 67 Chapter 4 in S&W Section 17.1 in S&W (extended OLS assumptions) 2

ECON3150/4150 Spring 2015 Lecture 3&4 - The linear regression model Siv-Elisabeth Skjelbred University of Oslo January 29, 2015 1 / 67 Chapter 4 in S&W Section 17.1 in S&W (extended OLS assumptions) 2

Topic 4 Unit Roots. Gerald P. Dwyer. February Clemson University

Topic 4 Unit Roots Gerald P. Dwyer Clemson University February 2016 Outline 1 Unit Roots Introduction Trend and Difference Stationary Autocorrelations of Series That Have Deterministic or Stochastic Trends

Topic 4 Unit Roots Gerald P. Dwyer Clemson University February 2016 Outline 1 Unit Roots Introduction Trend and Difference Stationary Autocorrelations of Series That Have Deterministic or Stochastic Trends

E 4101/5101 Lecture 9: Non-stationarity

E 4101/5101 Lecture 9: Non-stationarity Ragnar Nymoen 30 March 2011 Introduction I Main references: Hamilton Ch 15,16 and 17. Davidson and MacKinnon Ch 14.3 and 14.4 Also read Ch 2.4 and Ch 2.5 in Davidson

E 4101/5101 Lecture 9: Non-stationarity Ragnar Nymoen 30 March 2011 Introduction I Main references: Hamilton Ch 15,16 and 17. Davidson and MacKinnon Ch 14.3 and 14.4 Also read Ch 2.4 and Ch 2.5 in Davidson

INTRODUCTION TO BASIC LINEAR REGRESSION MODEL

INTRODUCTION TO BASIC LINEAR REGRESSION MODEL 13 September 2011 Yogyakarta, Indonesia Cosimo Beverelli (World Trade Organization) 1 LINEAR REGRESSION MODEL In general, regression models estimate the effect

INTRODUCTION TO BASIC LINEAR REGRESSION MODEL 13 September 2011 Yogyakarta, Indonesia Cosimo Beverelli (World Trade Organization) 1 LINEAR REGRESSION MODEL In general, regression models estimate the effect

Inference with Simple Regression

1 Introduction Inference with Simple Regression Alan B. Gelder 06E:071, The University of Iowa 1 Moving to infinite means: In this course we have seen one-mean problems, twomean problems, and problems

1 Introduction Inference with Simple Regression Alan B. Gelder 06E:071, The University of Iowa 1 Moving to infinite means: In this course we have seen one-mean problems, twomean problems, and problems

Introduction to Regression Analysis. Dr. Devlina Chatterjee 11 th August, 2017

Introduction to Regression Analysis Dr. Devlina Chatterjee 11 th August, 2017 What is regression analysis? Regression analysis is a statistical technique for studying linear relationships. One dependent

Introduction to Regression Analysis Dr. Devlina Chatterjee 11 th August, 2017 What is regression analysis? Regression analysis is a statistical technique for studying linear relationships. One dependent

13. Time Series Analysis: Asymptotics Weakly Dependent and Random Walk Process. Strict Exogeneity

Outline: Further Issues in Using OLS with Time Series Data 13. Time Series Analysis: Asymptotics Weakly Dependent and Random Walk Process I. Stationary and Weakly Dependent Time Series III. Highly Persistent

Outline: Further Issues in Using OLS with Time Series Data 13. Time Series Analysis: Asymptotics Weakly Dependent and Random Walk Process I. Stationary and Weakly Dependent Time Series III. Highly Persistent

In order to carry out a study on employees wages, a company collects information from its 500 employees 1 as follows:

INTRODUCTORY ECONOMETRICS Dpt of Econometrics & Statistics (EA3) University of the Basque Country UPV/EHU OCW Self Evaluation answers Time: 21/2 hours SURNAME: NAME: ID#: Specific competences to be evaluated

INTRODUCTORY ECONOMETRICS Dpt of Econometrics & Statistics (EA3) University of the Basque Country UPV/EHU OCW Self Evaluation answers Time: 21/2 hours SURNAME: NAME: ID#: Specific competences to be evaluated

Question 1 [17 points]: (ch 11)

![Question 1 [17 points]: (ch 11)](/thumbs/95/123686850.jpg "Question 1 [17 points]: (ch 11)") Question 1 [17 points]: (ch 11) A study analyzed the probability that Major League Baseball (MLB) players "survive" for another season, or, in other words, play one more season. They studied a model of

Question 1 [17 points]: (ch 11) A study analyzed the probability that Major League Baseball (MLB) players "survive" for another season, or, in other words, play one more season. They studied a model of

TESTING FOR CO-INTEGRATION

Bo Sjö 2010-12-05 TESTING FOR CO-INTEGRATION To be used in combination with Sjö (2008) Testing for Unit Roots and Cointegration A Guide. Instructions: Use the Johansen method to test for Purchasing Power

Bo Sjö 2010-12-05 TESTING FOR CO-INTEGRATION To be used in combination with Sjö (2008) Testing for Unit Roots and Cointegration A Guide. Instructions: Use the Johansen method to test for Purchasing Power

L6: Regression II. JJ Chen. July 2, 2015

L6: Regression II JJ Chen July 2, 2015 Today s Plan Review basic inference based on Sample average Difference in sample average Extrapolate the knowledge to sample regression coefficients Standard error,

L6: Regression II JJ Chen July 2, 2015 Today s Plan Review basic inference based on Sample average Difference in sample average Extrapolate the knowledge to sample regression coefficients Standard error,

Decision 411: Class 3

Decision 411: Class 3 Discussion of HW#1 Introduction to seasonal models Seasonal decomposition Seasonal adjustment on a spreadsheet Forecasting with seasonal adjustment Forecasting inflation Poor man

Decision 411: Class 3 Discussion of HW#1 Introduction to seasonal models Seasonal decomposition Seasonal adjustment on a spreadsheet Forecasting with seasonal adjustment Forecasting inflation Poor man

Oil price and macroeconomy in Russia. Abstract

Oil price and macroeconomy in Russia Katsuya Ito Fukuoka University Abstract In this note, using the VEC model we attempt to empirically investigate the effects of oil price and monetary shocks on the

Oil price and macroeconomy in Russia Katsuya Ito Fukuoka University Abstract In this note, using the VEC model we attempt to empirically investigate the effects of oil price and monetary shocks on the

Basic econometrics. Tutorial 3. Dipl.Kfm. Johannes Metzler

Basic econometrics Tutorial 3 Dipl.Kfm. Introduction Some of you were asking about material to revise/prepare econometrics fundamentals. First of all, be aware that I will not be too technical, only as

Basic econometrics Tutorial 3 Dipl.Kfm. Introduction Some of you were asking about material to revise/prepare econometrics fundamentals. First of all, be aware that I will not be too technical, only as

THE SEASONAL UNIT ROOTS IN DEMOGRAPHIC TIME SERIES ANDTHE POSSIBILITIES OF ITS EXACT TESTING

THE SEASONAL UNIT ROOTS IN DEMOGRAPHIC TIME SERIES ANDTHE POSSIBILITIES OF ITS EXACT TESTING Ondřej Šimpach, Petra Dotlačilová University of Economics in Prague ondrej.simpach@vse.cz, xdotp00@vse.cz Key

THE SEASONAL UNIT ROOTS IN DEMOGRAPHIC TIME SERIES ANDTHE POSSIBILITIES OF ITS EXACT TESTING Ondřej Šimpach, Petra Dotlačilová University of Economics in Prague ondrej.simpach@vse.cz, xdotp00@vse.cz Key

LECTURE 10. Introduction to Econometrics. Multicollinearity & Heteroskedasticity

LECTURE 10 Introduction to Econometrics Multicollinearity & Heteroskedasticity November 22, 2016 1 / 23 ON PREVIOUS LECTURES We discussed the specification of a regression equation Specification consists

LECTURE 10 Introduction to Econometrics Multicollinearity & Heteroskedasticity November 22, 2016 1 / 23 ON PREVIOUS LECTURES We discussed the specification of a regression equation Specification consists

FinQuiz Notes

Reading 9 A time series is any series of data that varies over time e.g. the quarterly sales for a company during the past five years or daily returns of a security. When assumptions of the regression

Reading 9 A time series is any series of data that varies over time e.g. the quarterly sales for a company during the past five years or daily returns of a security. When assumptions of the regression

ARDL Cointegration Tests for Beginner

ARDL Cointegration Tests for Beginner Tuck Cheong TANG Department of Economics, Faculty of Economics & Administration University of Malaya Email: tangtuckcheong@um.edu.my DURATION: 3 HOURS On completing

ARDL Cointegration Tests for Beginner Tuck Cheong TANG Department of Economics, Faculty of Economics & Administration University of Malaya Email: tangtuckcheong@um.edu.my DURATION: 3 HOURS On completing

In this chapter, we begin to study the properties of OLS for estimating linear regression

C h a p t e r Ten Basic Regression Analysis with Time Series Data In this chapter, we begin to study the properties of OLS for estimating linear regression models using time series data. In Section 10.1,

C h a p t e r Ten Basic Regression Analysis with Time Series Data In this chapter, we begin to study the properties of OLS for estimating linear regression models using time series data. In Section 10.1,

Time Series Analysis -- An Introduction -- AMS 586

Time Series Analysis -- An Introduction -- AMS 586 1 Objectives of time series analysis Data description Data interpretation Modeling Control Prediction & Forecasting 2 Time-Series Data Numerical data

Time Series Analysis -- An Introduction -- AMS 586 1 Objectives of time series analysis Data description Data interpretation Modeling Control Prediction & Forecasting 2 Time-Series Data Numerical data

Econ 444, class 11. Robert de Jong 1. Monday November 6. Ohio State University. Econ 444, Wednesday November 1, class Department of Economics

Econ 444, class 11 Robert de Jong 1 1 Department of Economics Ohio State University Monday November 6 Monday November 6 1 Exercise for today 2 New material: 1 dummy variables 2 multicollinearity Exercise

Econ 444, class 11 Robert de Jong 1 1 Department of Economics Ohio State University Monday November 6 Monday November 6 1 Exercise for today 2 New material: 1 dummy variables 2 multicollinearity Exercise

REED TUTORIALS (Pty) LTD ECS3706 EXAM PACK

LTD ECS3706 EXAM PACK") REED TUTORIALS (Pty) LTD ECS3706 EXAM PACK 1 ECONOMETRICS STUDY PACK MAY/JUNE 2016 Question 1 (a) (i) Describing economic reality (ii) Testing hypothesis about economic theory (iii) Forecasting future

REED TUTORIALS (Pty) LTD ECS3706 EXAM PACK 1 ECONOMETRICS STUDY PACK MAY/JUNE 2016 Question 1 (a) (i) Describing economic reality (ii) Testing hypothesis about economic theory (iii) Forecasting future

Applied Econometrics. Professor Bernard Fingleton

Applied Econometrics Professor Bernard Fingleton Regression A quick summary of some key issues Some key issues Text book JH Stock & MW Watson Introduction to Econometrics 2nd Edition Software Gretl Gretl.sourceforge.net

Applied Econometrics Professor Bernard Fingleton Regression A quick summary of some key issues Some key issues Text book JH Stock & MW Watson Introduction to Econometrics 2nd Edition Software Gretl Gretl.sourceforge.net

EMERGING MARKETS - Lecture 2: Methodology refresher

EMERGING MARKETS - Lecture 2: Methodology refresher Maria Perrotta April 4, 2013 SITE http://www.hhs.se/site/pages/default.aspx My contact: maria.perrotta@hhs.se Aim of this class There are many different

EMERGING MARKETS - Lecture 2: Methodology refresher Maria Perrotta April 4, 2013 SITE http://www.hhs.se/site/pages/default.aspx My contact: maria.perrotta@hhs.se Aim of this class There are many different

Time Series Methods. Sanjaya Desilva

Time Series Methods Sanjaya Desilva 1 Dynamic Models In estimating time series models, sometimes we need to explicitly model the temporal relationships between variables, i.e. does X affect Y in the same

Time Series Methods Sanjaya Desilva 1 Dynamic Models In estimating time series models, sometimes we need to explicitly model the temporal relationships between variables, i.e. does X affect Y in the same

Estimates of the Sticky-Information Phillips Curve for the USA with the General to Specific Method

MPRA Munich Personal RePEc Archive Estimates of the Sticky-Information Phillips Curve for the USA with the General to Specific Method Antonio Paradiso and B. Bhaskara Rao and Marco Ventura 12. February

MPRA Munich Personal RePEc Archive Estimates of the Sticky-Information Phillips Curve for the USA with the General to Specific Method Antonio Paradiso and B. Bhaskara Rao and Marco Ventura 12. February

UNIVERSIDAD CARLOS III DE MADRID ECONOMETRICS Academic year 2009/10 FINAL EXAM (2nd Call) June, 25, 2010

June, 25, 2010") UNIVERSIDAD CARLOS III DE MADRID ECONOMETRICS Academic year 2009/10 FINAL EXAM (2nd Call) June, 25, 2010 Very important: Take into account that: 1. Each question, unless otherwise stated, requires a complete

UNIVERSIDAD CARLOS III DE MADRID ECONOMETRICS Academic year 2009/10 FINAL EXAM (2nd Call) June, 25, 2010 Very important: Take into account that: 1. Each question, unless otherwise stated, requires a complete

Will it float? The New Keynesian Phillips curve tested on OECD panel data

Phillips curve Roger Bjørnstad 1 2 1 Research Department Statistics Norway 2 Department of Economics University of Oslo 31 October 2006 Outline Outline Outline Outline Outline The debatable The hybrid

Phillips curve Roger Bjørnstad 1 2 1 Research Department Statistics Norway 2 Department of Economics University of Oslo 31 October 2006 Outline Outline Outline Outline Outline The debatable The hybrid

Eco and Bus Forecasting Fall 2016 EXERCISE 2

ECO 5375-701 Prof. Tom Fomby Eco and Bus Forecasting Fall 016 EXERCISE Purpose: To learn how to use the DTDS model to test for the presence or absence of seasonality in time series data and to estimate

ECO 5375-701 Prof. Tom Fomby Eco and Bus Forecasting Fall 016 EXERCISE Purpose: To learn how to use the DTDS model to test for the presence or absence of seasonality in time series data and to estimate

Decision 411: Class 3

Decision 411: Class 3 Discussion of HW#1 Introduction to seasonal models Seasonal decomposition Seasonal adjustment on a spreadsheet Forecasting with seasonal adjustment Forecasting inflation Poor man

Decision 411: Class 3 Discussion of HW#1 Introduction to seasonal models Seasonal decomposition Seasonal adjustment on a spreadsheet Forecasting with seasonal adjustment Forecasting inflation Poor man

ECON 497 Midterm Spring

ECON 497 Midterm Spring 2009 1 ECON 497: Economic Research and Forecasting Name: Spring 2009 Bellas Midterm You have three hours and twenty minutes to complete this exam. Answer all questions and explain

ECON 497 Midterm Spring 2009 1 ECON 497: Economic Research and Forecasting Name: Spring 2009 Bellas Midterm You have three hours and twenty minutes to complete this exam. Answer all questions and explain

Econ 423 Lecture Notes

Econ 423 Lecture Notes (These notes are slightly modified versions of lecture notes provided by Stock and Watson, 2007. They are for instructional purposes only and are not to be distributed outside of

Econ 423 Lecture Notes (These notes are slightly modified versions of lecture notes provided by Stock and Watson, 2007. They are for instructional purposes only and are not to be distributed outside of

Time-Series Analysis. Dr. Seetha Bandara Dept. of Economics MA_ECON

Time-Series Analysis Dr. Seetha Bandara Dept. of Economics MA_ECON Time Series Patterns A time series is a sequence of observations on a variable measured at successive points in time or over successive

Time-Series Analysis Dr. Seetha Bandara Dept. of Economics MA_ECON Time Series Patterns A time series is a sequence of observations on a variable measured at successive points in time or over successive

in the time series. The relation between y and x is contemporaneous.

9 Regression with Time Series 9.1 Some Basic Concepts Static Models (1) y t = β 0 + β 1 x t + u t t = 1, 2,..., T, where T is the number of observation in the time series. The relation between y and x

9 Regression with Time Series 9.1 Some Basic Concepts Static Models (1) y t = β 0 + β 1 x t + u t t = 1, 2,..., T, where T is the number of observation in the time series. The relation between y and x

Lecture 6a: Unit Root and ARIMA Models

Lecture 6a: Unit Root and ARIMA Models 1 2 Big Picture A time series is non-stationary if it contains a unit root unit root nonstationary The reverse is not true. For example, y t = cos(t) + u t has no

Lecture 6a: Unit Root and ARIMA Models 1 2 Big Picture A time series is non-stationary if it contains a unit root unit root nonstationary The reverse is not true. For example, y t = cos(t) + u t has no

Autocorrelation. Think of autocorrelation as signifying a systematic relationship between the residuals measured at different points in time

Autocorrelation Given the model Y t = b 0 + b 1 X t + u t Think of autocorrelation as signifying a systematic relationship between the residuals measured at different points in time This could be caused

Autocorrelation Given the model Y t = b 0 + b 1 X t + u t Think of autocorrelation as signifying a systematic relationship between the residuals measured at different points in time This could be caused

Problem Set #6: OLS. Economics 835: Econometrics. Fall 2012

Problem Set #6: OLS Economics 835: Econometrics Fall 202 A preliminary result Suppose we have a random sample of size n on the scalar random variables (x, y) with finite means, variances, and covariance.

Problem Set #6: OLS Economics 835: Econometrics Fall 202 A preliminary result Suppose we have a random sample of size n on the scalar random variables (x, y) with finite means, variances, and covariance.

CHAPTER 21: TIME SERIES ECONOMETRICS: SOME BASIC CONCEPTS

CHAPTER 21: TIME SERIES ECONOMETRICS: SOME BASIC CONCEPTS 21.1 A stochastic process is said to be weakly stationary if its mean and variance are constant over time and if the value of the covariance between

CHAPTER 21: TIME SERIES ECONOMETRICS: SOME BASIC CONCEPTS 21.1 A stochastic process is said to be weakly stationary if its mean and variance are constant over time and if the value of the covariance between

CHAPTER 6: SPECIFICATION VARIABLES

Recall, we had the following six assumptions required for the Gauss-Markov Theorem: 1. The regression model is linear, correctly specified, and has an additive error term. 2. The error term has a zero

Recall, we had the following six assumptions required for the Gauss-Markov Theorem: 1. The regression model is linear, correctly specified, and has an additive error term. 2. The error term has a zero

Introduction to Econometrics. Review of Probability & Statistics

1 Introduction to Econometrics Review of Probability & Statistics Peerapat Wongchaiwat, Ph.D. wongchaiwat@hotmail.com Introduction 2 What is Econometrics? Econometrics consists of the application of mathematical

1 Introduction to Econometrics Review of Probability & Statistics Peerapat Wongchaiwat, Ph.D. wongchaiwat@hotmail.com Introduction 2 What is Econometrics? Econometrics consists of the application of mathematical

Econ 300/QAC 201: Quantitative Methods in Economics/Applied Data Analysis. 17th Class 7/1/10

Econ 300/QAC 201: Quantitative Methods in Economics/Applied Data Analysis 17th Class 7/1/10 The only function of economic forecasting is to make astrology look respectable. --John Kenneth Galbraith show

Econ 300/QAC 201: Quantitative Methods in Economics/Applied Data Analysis 17th Class 7/1/10 The only function of economic forecasting is to make astrology look respectable. --John Kenneth Galbraith show

Exercise sheet 3 The Multiple Regression Model

Exercise sheet 3 The Multiple Regression Model Note: In those problems that include estimations and have a reference to a data set the students should check the outputs obtained with Gretl. 1. Let the

Exercise sheet 3 The Multiple Regression Model Note: In those problems that include estimations and have a reference to a data set the students should check the outputs obtained with Gretl. 1. Let the

Univariate linear models

Univariate linear models The specification process of an univariate ARIMA model is based on the theoretical properties of the different processes and it is also important the observation and interpretation

Univariate linear models The specification process of an univariate ARIMA model is based on the theoretical properties of the different processes and it is also important the observation and interpretation

STOCKHOLM UNIVERSITY Department of Economics Course name: Empirical Methods Course code: EC40 Examiner: Lena Nekby Number of credits: 7,5 credits Date of exam: Saturday, May 9, 008 Examination time: 3

STOCKHOLM UNIVERSITY Department of Economics Course name: Empirical Methods Course code: EC40 Examiner: Lena Nekby Number of credits: 7,5 credits Date of exam: Saturday, May 9, 008 Examination time: 3

Ordinary Least Squares Regression Explained: Vartanian

Ordinary Least Squares Regression Explained: Vartanian When to Use Ordinary Least Squares Regression Analysis A. Variable types. When you have an interval/ratio scale dependent variable.. When your independent

Ordinary Least Squares Regression Explained: Vartanian When to Use Ordinary Least Squares Regression Analysis A. Variable types. When you have an interval/ratio scale dependent variable.. When your independent

The Multiple Regression Model Estimation

Lesson 5 The Multiple Regression Model Estimation Pilar González and Susan Orbe Dpt Applied Econometrics III (Econometrics and Statistics) Pilar González and Susan Orbe OCW 2014 Lesson 5 Regression model:

Lesson 5 The Multiple Regression Model Estimation Pilar González and Susan Orbe Dpt Applied Econometrics III (Econometrics and Statistics) Pilar González and Susan Orbe OCW 2014 Lesson 5 Regression model:

E 4160 Autumn term Lecture 9: Deterministic trends vs integrated series; Spurious regression; Dickey-Fuller distribution and test

E 4160 Autumn term 2016. Lecture 9: Deterministic trends vs integrated series; Spurious regression; Dickey-Fuller distribution and test Ragnar Nymoen Department of Economics, University of Oslo 24 October

E 4160 Autumn term 2016. Lecture 9: Deterministic trends vs integrated series; Spurious regression; Dickey-Fuller distribution and test Ragnar Nymoen Department of Economics, University of Oslo 24 October

Lecture on State Dependent Government Spending Multipliers

Lecture on State Dependent Government Spending Multipliers Valerie A. Ramey University of California, San Diego and NBER February 25, 2014 Does the Multiplier Depend on the State of Economy? Evidence suggests

Lecture on State Dependent Government Spending Multipliers Valerie A. Ramey University of California, San Diego and NBER February 25, 2014 Does the Multiplier Depend on the State of Economy? Evidence suggests

Economtrics of money and finance Lecture six: spurious regression and cointegration

Economtrics of money and finance Lecture six: spurious regression and cointegration Zongxin Qian School of Finance, Renmin University of China October 21, 2014 Table of Contents Overview Spurious regression

Economtrics of money and finance Lecture six: spurious regression and cointegration Zongxin Qian School of Finance, Renmin University of China October 21, 2014 Table of Contents Overview Spurious regression

Chapter 7. Testing Linear Restrictions on Regression Coefficients

Chapter 7 Testing Linear Restrictions on Regression Coefficients 1.F-tests versus t-tests In the previous chapter we discussed several applications of the t-distribution to testing hypotheses in the linear

Chapter 7 Testing Linear Restrictions on Regression Coefficients 1.F-tests versus t-tests In the previous chapter we discussed several applications of the t-distribution to testing hypotheses in the linear

Applied Economics. Regression with a Binary Dependent Variable. Department of Economics Universidad Carlos III de Madrid

Applied Economics Regression with a Binary Dependent Variable Department of Economics Universidad Carlos III de Madrid See Stock and Watson (chapter 11) 1 / 28 Binary Dependent Variables: What is Different?

Applied Economics Regression with a Binary Dependent Variable Department of Economics Universidad Carlos III de Madrid See Stock and Watson (chapter 11) 1 / 28 Binary Dependent Variables: What is Different?

Multiple Regression Analysis

Chapter 4 Multiple Regression Analysis The simple linear regression covered in Chapter 2 can be generalized to include more than one variable. Multiple regression analysis is an extension of the simple

Chapter 4 Multiple Regression Analysis The simple linear regression covered in Chapter 2 can be generalized to include more than one variable. Multiple regression analysis is an extension of the simple

Inference. ME104: Linear Regression Analysis Kenneth Benoit. August 15, August 15, 2012 Lecture 3 Multiple linear regression 1 1 / 58

Inference ME104: Linear Regression Analysis Kenneth Benoit August 15, 2012 August 15, 2012 Lecture 3 Multiple linear regression 1 1 / 58 Stata output resvisited. reg votes1st spend_total incumb minister

Inference ME104: Linear Regression Analysis Kenneth Benoit August 15, 2012 August 15, 2012 Lecture 3 Multiple linear regression 1 1 / 58 Stata output resvisited. reg votes1st spend_total incumb minister

where Female = 0 for males, = 1 for females Age is measured in years (22, 23, ) GPA is measured in units on a four-point scale (0, 1.22, 3.45, etc.

GPA is measured in units on a four-point scale (0, 1.22, 3.45, etc.") Notes on regression analysis 1. Basics in regression analysis key concepts (actual implementation is more complicated) A. Collect data B. Plot data on graph, draw a line through the middle of the scatter

Notes on regression analysis 1. Basics in regression analysis key concepts (actual implementation is more complicated) A. Collect data B. Plot data on graph, draw a line through the middle of the scatter

Ref.: Spring SOS3003 Applied data analysis for social science Lecture note

SOS3003 Applied data analysis for social science Lecture note 05-2010 Erling Berge Department of sociology and political science NTNU Spring 2010 Erling Berge 2010 1 Literature Regression criticism I Hamilton

SOS3003 Applied data analysis for social science Lecture note 05-2010 Erling Berge Department of sociology and political science NTNU Spring 2010 Erling Berge 2010 1 Literature Regression criticism I Hamilton

Multiple Regression Analysis

Multiple Regression Analysis y = β 0 + β 1 x 1 + β 2 x 2 +... β k x k + u 2. Inference 0 Assumptions of the Classical Linear Model (CLM)! So far, we know: 1. The mean and variance of the OLS estimators

Multiple Regression Analysis y = β 0 + β 1 x 1 + β 2 x 2 +... β k x k + u 2. Inference 0 Assumptions of the Classical Linear Model (CLM)! So far, we know: 1. The mean and variance of the OLS estimators

Chapter 7: Correlation and regression

Slide 7.1 Chapter 7: Correlation and regression Correlation and regression techniques examine the relationships between variables, e.g. between the price of doughnuts and the demand for them. Such analyses

Slide 7.1 Chapter 7: Correlation and regression Correlation and regression techniques examine the relationships between variables, e.g. between the price of doughnuts and the demand for them. Such analyses

Applied Econometrics. From Analysis of Economic Data, Gary Koop

Applied Econometrics From Analysis of Economic Data, Gary Koop 1 OLS Assumptions But OLS is the best estimator under certain assumptions Regression is linear in parameters 2. Error term has zero population

Applied Econometrics From Analysis of Economic Data, Gary Koop 1 OLS Assumptions But OLS is the best estimator under certain assumptions Regression is linear in parameters 2. Error term has zero population

Are Forecast Updates Progressive?

MPRA Munich Personal RePEc Archive Are Forecast Updates Progressive? Chia-Lin Chang and Philip Hans Franses and Michael McAleer National Chung Hsing University, Erasmus University Rotterdam, Erasmus University

MPRA Munich Personal RePEc Archive Are Forecast Updates Progressive? Chia-Lin Chang and Philip Hans Franses and Michael McAleer National Chung Hsing University, Erasmus University Rotterdam, Erasmus University

Describing Associations, Covariance, Correlation, and Causality. Interest Rates and Inflation. Data & Scatter Diagram. Lecture 4

Describing Associations, Covariance, Correlation, and Causality Lecture Reading: Chapter 6 & SW11 ( Readings in portal) 1 Interest Rates and Inflation At the heart of Canada s monetary policy framework

Describing Associations, Covariance, Correlation, and Causality Lecture Reading: Chapter 6 & SW11 ( Readings in portal) 1 Interest Rates and Inflation At the heart of Canada s monetary policy framework

Lecture 5: Omitted Variables, Dummy Variables and Multicollinearity

Lecture 5: Omitted Variables, Dummy Variables and Multicollinearity R.G. Pierse 1 Omitted Variables Suppose that the true model is Y i β 1 + β X i + β 3 X 3i + u i, i 1,, n (1.1) where β 3 0 but that the

Lecture 5: Omitted Variables, Dummy Variables and Multicollinearity R.G. Pierse 1 Omitted Variables Suppose that the true model is Y i β 1 + β X i + β 3 X 3i + u i, i 1,, n (1.1) where β 3 0 but that the

Practice exam questions

Practice exam questions Nathaniel Higgins nhiggins@jhu.edu, nhiggins@ers.usda.gov 1. The following question is based on the model y = β 0 + β 1 x 1 + β 2 x 2 + β 3 x 3 + u. Discuss the following two hypotheses.

Practice exam questions Nathaniel Higgins nhiggins@jhu.edu, nhiggins@ers.usda.gov 1. The following question is based on the model y = β 0 + β 1 x 1 + β 2 x 2 + β 3 x 3 + u. Discuss the following two hypotheses.

10) Time series econometrics

Time series econometrics") 30C00200 Econometrics 10) Time series econometrics Timo Kuosmanen Professor, Ph.D. 1 Topics today Static vs. dynamic time series model Suprious regression Stationary and nonstationary time series Unit

30C00200 Econometrics 10) Time series econometrics Timo Kuosmanen Professor, Ph.D. 1 Topics today Static vs. dynamic time series model Suprious regression Stationary and nonstationary time series Unit