ARDL Cointegration Tests for Beginner

|

|

|

- Julia Gaines

- 5 years ago

- Views:

Transcription

1 ARDL Cointegration Tests for Beginner Tuck Cheong TANG Department of Economics, Faculty of Economics & Administration University of Malaya DURATION: 3 HOURS On completing this workshop you should be able to: understand the concepts of cointegration and its application as well. perform cointegration tests by using EViews software; and interpret the outputs and estimates. 1. UNIT ROOT TEST An estimate of OLS (ordinary least squared) regression model can spurious from regressing nonstationary series with no long-run relationship (or no cointegration) (Engle and Granger, 1987). Stationary a series fluctuates around a mean value with a tendency to converge to the mean. For example:- 20 Malaysia: Consumer price index: Inflation rate %pa Non-statioanry a series wanders widely without any tendency to converge; it is relatively smooth. For example:- 1

2 140 Malaysia: Consumer price index 1995= Conventional tests for examining series stationarity:- Type of tests 1. Augmented Dickey-Fuller (ADF) 2. Phillips-Perron (PP) 3. Kwiatkowski, Phillips, Schmidt, and Shin (KPSS) Null hypothesis a unit root a unit root trend stationary or level stationary Other types of tests are Dickey-Fuller Test with GLS Detrending (DFGLS), Elliot, Rothenberg, and Stock Point Optimal (ERS) Test, and Ng and Perron (NP) Tests I(0) -> stationary in levels I(1) -> non stationary in levels but it becomes stationary after differencing once. 2. COINTEGRATION From econometric point of view, it is a solution to the problems that arise as a result of the presence of non-stationary data (OLS estimates), that is to avoid the problems associated with spurious regression. In practice, it is more appropriate to test a theory. Economic theory often suggests certain variables are cointegrated with know (or unknown) cointegrating vector. In order words, we use to test for the presence of an equilibrium relationship between the variables suggested by economic theory. Because: - Evan though an economic time series may wander over time there may exist a linear combination of the variables that converges to an equilibrium, that is, the variables are cointegrated. How: - Engle and Granger (1987) pointed out that a linear combination of two or more non-stationary series may be stationary. If such a stationary linear combination exists, the non-stationary time series are said to be cointegrated. 2

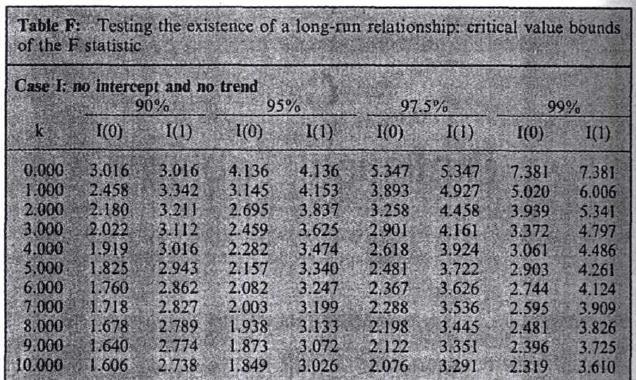

3 ARDL APPROACH FOR COINTEGRATION SINGLE EQUATION APPROACH The main advantage of this testing and estimation strategy (ARDL procedure) lies in the fact that it can be applied irrespective of the regressors are I(0) or I(1), and this avoids the pre-testing problems associated with standard cointegration analysis which requires the classification of the variables into I(1) and I(0) (Pesaran and Pesaran, 1997, p ). Also see, Jenkinson (1986) for ARDL model for cointegration analysis. ARDL (autoregressive-distributed lag) approach for cointegration by Pesaran, Shin and Smith (2001) can be performed via the error correction version of the ARDL model as: p1 p (1) y c y x b y b x u t 0 t1 1 t1 1i ti 2i ti t i1 i1 In testing for a long run relationship between y and x, we test H0: (nonexistence of the long run relationship) against HA: 0 0, 1 0 (a long run relationship) by running an usual F-test. If the computed F-statistic falls outside the band (the values for I(0) and I(1) in the Table F), a conclusive decision can be made. 1) if the computed F-statistic exceeds the upper bound of the critical value band (denote I(1) in the Table F), the null hypothesis can be rejected and then support cointegration, and 2) if the computed F-statistic falls well below the lower bound of the critical value band (denote I(0) in the Table F), and hence the null hypothesis cannot be rejected no cointegration. If the computed statistic falls within the critical value band, the result of the inference is inconclusive and depends on whether the underlying variables are I(0) or I(1). It is at this stage in the analysis that the researcher may have to carry out unit rot tests on the variables. The long run coefficient (or elasticity) of x, that is, = -( 1 / 0 ) (see equation 1) (Pesaran, et al., 2001,p. 294). 3

4 4

The critical value bounds reported in Table F above are computed using stochastic simulation for T = 500")

5 Source: Pesaran and Pesaran (1997) p.478 Appendices. Notes: k is the number of the forcing variables (regressors) The critical value bounds reported in Table F above are computed using stochastic simulation for T = 500 and 20,000 replications in the case of Wald and F statistics for testing the joint null hypothesis that the coefficients of the level variables are zero (i.e. there exists no long-run relationship between them). Further reading: Pesaran et al. (2001) Eviews by hands Investigate the presence of a long run relationship among m, y and rp with ARDL(lag length of 4, quarterly data) (assume an intercept and no trend). Step 1:- OLS estimation for ARDL 5

=C(2)=C(3)=0 The critical values at 0.10 level are 3.182 (lower bound) and 4.126 (upper bound) (k = 2, Case II: intercept and no trend case).")

6 D(M) M(-1) Y(-1) RP(-1) D(Y(-1)) D(Y(-2)) D(Y(-3)) D(Y(-4)) D(RP(-1)) D(RP(-2)) D(RP(-3)) D(RP(-4)) D(M(-1)) D(M(-2)) D(M(-3)) D(M(-4)) C Step 2:- Wald test (F-statistic) for restrictions. C(1)=C(2)=C(3)=0 The critical values at 0.10 level are (lower bound) and (upper bound) (k = 2, Case II: intercept and no trend case). :- inconclusive (within the critical value band) The 0.05 level critical values are (lower bound) and (upper bound) :- no cointegration (below the lower bound) Sensitivity check ARDL(8) and ARDL(12). Computed F-statistic is for ARDL(8), and for ARDL(12). Both F- statistics are below the lower bound, (10%), there for no cointegration among m, y and rp. 6

7 by default Step 1:- Select the variables the first selected is dependent variable. M RP Y Go to <Equation Estimation> Select <ARDL > from [Method:] Determine the MAXIMUM lag length under <Specification> Go to <Options> if necessary. 7

Dynamic regressors (4 lags, automatic): RP Y Fixed regressors: C Number of models evalulated: 100 Selected Model: ARDL(4, 0, 0) Variable Coefficient Std.")

8 Dependent Variable: M Method: ARDL Date: 07/29/16 Time: 15:44 Sample (adjusted): 1974Q1 2000Q4 Included observations: 108 after adjustments Maximum dependent lags: 4 (Automatic selection) Model selection method: Akaike info criterion (AIC) Dynamic regressors (4 lags, automatic): RP Y Fixed regressors: C Number of models evalulated: 100 Selected Model: ARDL(4, 0, 0) Variable Coefficient Std. Error t-statistic Prob.* M(-1) M(-2) M(-3) M(-4) RP Y C R-squared Mean dependent var Adjusted R-squared S.D. dependent var *Note: p-values and any subsequent tests do not account for model selection. Step 2:- To run Bounds testing for cointegration, go to <View>, and select <Coefficient Diagnostics>. You will see <Bounds Test> 8

9 ARDL Bounds Test Date: 07/29/16 Time: 15:43 Sample: 1974Q1 2000Q4 Included observations: 108 Null Hypothesis: No long-run relationships exist Test Statistic Value k F-statistic Critical Value Bounds Significance I0 Bound I1 Bound 10% % % % Test Equation: Dependent Variable: D(M) Method: Least Squares Date: 07/29/16 Time: 15:43 Sample: 1974Q1 2000Q4 Included observations: 108 Variable Coefficient Std. Error t-statistic Prob. D(M(-1)) D(M(-2)) D(M(-3)) C RP(-1) Y(-1) M(-1) R-squared Mean dependent var Adjusted R-squared S.D. dependent var S.E. of regression Akaike info criterion Sum squared resid Schwarz criterion Log likelihood Hannan-Quinn criter F-statistic Durbin-Watson stat Prob(F-statistic) Unrestricted Error-Correction Model - ARDL(4, 0, 0) for (M RP Y), see Equation (1). <= short-run (first differenced) <= unrestricted error-correction term (level in one year lag). It is only to generate the bounds test statistic. Step 3:- Long-run and short run estimates:- Click <Coefficient diagnostics> then go to <Cointegration and Long Run Form> 9

Date: 07/29/16 Time: 15:48 Sample: 1973Q1 2000Q4 Included observations: 108 Cointegrating Form Variable Coefficient Std. Error t-statistic Prob. D(M(-1)) 0.")

10 ARDL Cointegrating And Long Run Form Original dep. variable: M Selected Model: ARDL(4, 0, 0) Date: 07/29/16 Time: 15:48 Sample: 1973Q1 2000Q4 Included observations: 108 Cointegrating Form Variable Coefficient Std. Error t-statistic Prob. D(M(-1)) D(M(-2)) D(M(-3)) D(RP) D(Y) CointEq(-1) Cointeq = M - ( *RP *Y ) Error-Correction Model, ECM <= short-run (first differenced) <= Error-correction term i.e. lagged one period residuals, actual M minus estimated M. Long Run Coefficients Variable Coefficient Std. Error t-statistic Prob. RP Y C

11 Diagnostics Check Confidence Ellipse Serial Correlation LM Test Recursive Estimates 11

12 Selected Readings [1] Davidson, R. and MacKinnon, J. G Estimation and inference in econometrics. New York: Oxford University Press. [2] Engle, R. F., and Granger, C. W. J., Co-integration and error correction: representation, estimation, and testing, Econometrica, 55, [3] Granger, C.W. J., Some recent development in a concept of causality. Journal of Econometrics. 39: [4] Granger, C. W. J., Investigating causal relations by econometric models and cross-spectral methods, Econometrica, 37, [5] Hamilton, J.D Time series analysis, New Jersey: Princeton University Press. [6] Jenkinson, T. J., Testing neo-classical theories of labour demand: an application of cointegration techniques, Oxford Bulletin of Economics and Statistics, 48, [7] Johansen, Søren and Juselius, K., Maximum likelihood estimation and inferences on cointegration-with applications to the demand for money, Oxford Bulletin of Economics and Statistics, 52, [8] MacKinnon, James G Critical values for cointegration tests, Chapter 13 in R. F. Engle and C. W. J. Granger (eds.), Long-run Economic Relationships: Readings in Cointegration, Oxford: Oxford University Press. [9] Sims, C. A., Money, income, and causality, American Economic Review, 62, [10] Toda, H. Y. and Yamamoto, T. 1995, Statistical inference in vector autoregressions with possibly integrated processes, Journal of Econometrics, 66, [11] Pesaran, M. H., and Pesaran, B.,1997. Working with Microfit 4.0 interactive econometric anlaysis. Oxford: Oxford University Press. [12] Pesaran, M. H.., Shin, y., and Smith, R. J Bounds testing approaches to the analysis of level relationships, Journal of Applied Econometrics, 16,

13 APPENDIX CASE FOR APPLICATION Aggregate Import Demand Function for Japan The existing literature has empirically approached standard formulation of import demand equation that relating the quantity of import demanded to domestic real income and relative price of imports. This specification of imports demand corresponds to that of the imperfect substitute model, which implies the existence of imports and domestic production as well as intra-industry trade. By assuming zero degree homogeneity, and of the supply elasticity is infinite or at least large, single equation of imports demand (equation 1) can be consistently estimated. Mt = f (Yt, RPt) where M is the desired quantity of imports demanded at period t, Y is the real income (domestic real activity). RP is the relative price of imports that is the ratio of import price to domestic price level. And the double-log linear form of data-driven import demand regression is given in equation below. LnMt = a1 +a1lnyt + a2lnrpt +et Data The data for the candidate variables are from OECD Main Economic Indicators. The quarterly data covers the sample period 1973:1-2000:4 (in indexes and in 1995 prices). All variables are in natural logarithm form. m = log of aggregated imports demand (in 1995 prices, index) y = log of real Gross Domestic Product, GDP (in 1995 prices, index) rp = log of ratio of import price to domestic price level (proxied by GDP deflator) (in 1995 prices, index) EViews work file japan importdd.wf1 13

Government expense, Consumer Price Index and Economic Growth in Cameroon

MPRA Munich Personal RePEc Archive Government expense, Consumer Price Index and Economic Growth in Cameroon Ngangue NGWEN and Claude Marius AMBA OYON and Taoufiki MBRATANA Department of Economics, University

MPRA Munich Personal RePEc Archive Government expense, Consumer Price Index and Economic Growth in Cameroon Ngangue NGWEN and Claude Marius AMBA OYON and Taoufiki MBRATANA Department of Economics, University

7. Integrated Processes

7. Integrated Processes Up to now: Analysis of stationary processes (stationary ARMA(p, q) processes) Problem: Many economic time series exhibit non-stationary patterns over time 226 Example: We consider

7. Integrated Processes Up to now: Analysis of stationary processes (stationary ARMA(p, q) processes) Problem: Many economic time series exhibit non-stationary patterns over time 226 Example: We consider

7. Integrated Processes

7. Integrated Processes Up to now: Analysis of stationary processes (stationary ARMA(p, q) processes) Problem: Many economic time series exhibit non-stationary patterns over time 226 Example: We consider

7. Integrated Processes Up to now: Analysis of stationary processes (stationary ARMA(p, q) processes) Problem: Many economic time series exhibit non-stationary patterns over time 226 Example: We consider

Oil price and macroeconomy in Russia. Abstract

Oil price and macroeconomy in Russia Katsuya Ito Fukuoka University Abstract In this note, using the VEC model we attempt to empirically investigate the effects of oil price and monetary shocks on the

Oil price and macroeconomy in Russia Katsuya Ito Fukuoka University Abstract In this note, using the VEC model we attempt to empirically investigate the effects of oil price and monetary shocks on the

1 Quantitative Techniques in Practice

1 Quantitative Techniques in Practice 1.1 Lecture 2: Stationarity, spurious regression, etc. 1.1.1 Overview In the rst part we shall look at some issues in time series economics. In the second part we

1 Quantitative Techniques in Practice 1.1 Lecture 2: Stationarity, spurious regression, etc. 1.1.1 Overview In the rst part we shall look at some issues in time series economics. In the second part we

Brief Sketch of Solutions: Tutorial 3. 3) unit root tests

unit root tests") Brief Sketch of Solutions: Tutorial 3 3) unit root tests.5.4.4.3.3.2.2.1.1.. -.1 -.1 -.2 -.2 -.3 -.3 -.4 -.4 21 22 23 24 25 26 -.5 21 22 23 24 25 26.8.2.4. -.4 - -.8 - - -.12 21 22 23 24 25 26 -.2 21 22

Brief Sketch of Solutions: Tutorial 3 3) unit root tests.5.4.4.3.3.2.2.1.1.. -.1 -.1 -.2 -.2 -.3 -.3 -.4 -.4 21 22 23 24 25 26 -.5 21 22 23 24 25 26.8.2.4. -.4 - -.8 - - -.12 21 22 23 24 25 26 -.2 21 22

Stationarity and cointegration tests: Comparison of Engle - Granger and Johansen methodologies

MPRA Munich Personal RePEc Archive Stationarity and cointegration tests: Comparison of Engle - Granger and Johansen methodologies Faik Bilgili Erciyes University, Faculty of Economics and Administrative

MPRA Munich Personal RePEc Archive Stationarity and cointegration tests: Comparison of Engle - Granger and Johansen methodologies Faik Bilgili Erciyes University, Faculty of Economics and Administrative

Response surface models for the Elliott, Rothenberg, Stock DF-GLS unit-root test

Response surface models for the Elliott, Rothenberg, Stock DF-GLS unit-root test Christopher F Baum Jesús Otero Stata Conference, Baltimore, July 2017 Baum, Otero (BC, U. del Rosario) DF-GLS response surfaces

Response surface models for the Elliott, Rothenberg, Stock DF-GLS unit-root test Christopher F Baum Jesús Otero Stata Conference, Baltimore, July 2017 Baum, Otero (BC, U. del Rosario) DF-GLS response surfaces

10. Time series regression and forecasting

10. Time series regression and forecasting Key feature of this section: Analysis of data on a single entity observed at multiple points in time (time series data) Typical research questions: What is the

10. Time series regression and forecasting Key feature of this section: Analysis of data on a single entity observed at multiple points in time (time series data) Typical research questions: What is the

An Econometric Modeling for India s Imports and exports during

Inter national Journal of Pure and Applied Mathematics Volume 113 No. 6 2017, 242 250 ISSN: 1311-8080 (printed version); ISSN: 1314-3395 (on-line version) url: http://www.ijpam.eu ijpam.eu An Econometric

Inter national Journal of Pure and Applied Mathematics Volume 113 No. 6 2017, 242 250 ISSN: 1311-8080 (printed version); ISSN: 1314-3395 (on-line version) url: http://www.ijpam.eu ijpam.eu An Econometric

THE LONG-RUN DETERMINANTS OF MONEY DEMAND IN SLOVAKIA MARTIN LUKÁČIK - ADRIANA LUKÁČIKOVÁ - KAROL SZOMOLÁNYI

92 Multiple Criteria Decision Making XIII THE LONG-RUN DETERMINANTS OF MONEY DEMAND IN SLOVAKIA MARTIN LUKÁČIK - ADRIANA LUKÁČIKOVÁ - KAROL SZOMOLÁNYI Abstract: The paper verifies the long-run determinants

92 Multiple Criteria Decision Making XIII THE LONG-RUN DETERMINANTS OF MONEY DEMAND IN SLOVAKIA MARTIN LUKÁČIK - ADRIANA LUKÁČIKOVÁ - KAROL SZOMOLÁNYI Abstract: The paper verifies the long-run determinants

MEXICO S INDUSTRIAL ENGINE OF GROWTH: COINTEGRATION AND CAUSALITY

NÚM. 126, MARZO-ABRIL DE 2003, PP. 34-41. MEXICO S INDUSTRIAL ENGINE OF GROWTH: COINTEGRATION AND CAUSALITY ALEJANDRO DÍAZ BAUTISTA* Abstract The present study applies the techniques of cointegration and

NÚM. 126, MARZO-ABRIL DE 2003, PP. 34-41. MEXICO S INDUSTRIAL ENGINE OF GROWTH: COINTEGRATION AND CAUSALITY ALEJANDRO DÍAZ BAUTISTA* Abstract The present study applies the techniques of cointegration and

Bristol Business School

Bristol Business School Module Leader: Module Code: Title of Module: Paul Dunne UMEN3P-15-M Econometrics Academic Year: 07/08 Examination Period: January 2008 Examination Date: 16 January 2007 Examination

Bristol Business School Module Leader: Module Code: Title of Module: Paul Dunne UMEN3P-15-M Econometrics Academic Year: 07/08 Examination Period: January 2008 Examination Date: 16 January 2007 Examination

Financial Time Series Analysis: Part II

Department of Mathematics and Statistics, University of Vaasa, Finland Spring 2017 1 Unit root Deterministic trend Stochastic trend Testing for unit root ADF-test (Augmented Dickey-Fuller test) Testing

Department of Mathematics and Statistics, University of Vaasa, Finland Spring 2017 1 Unit root Deterministic trend Stochastic trend Testing for unit root ADF-test (Augmented Dickey-Fuller test) Testing

11/18/2008. So run regression in first differences to examine association. 18 November November November 2008

Time Series Econometrics 7 Vijayamohanan Pillai N Unit Root Tests Vijayamohan: CDS M Phil: Time Series 7 1 Vijayamohan: CDS M Phil: Time Series 7 2 R 2 > DW Spurious/Nonsense Regression. Integrated but

Time Series Econometrics 7 Vijayamohanan Pillai N Unit Root Tests Vijayamohan: CDS M Phil: Time Series 7 1 Vijayamohan: CDS M Phil: Time Series 7 2 R 2 > DW Spurious/Nonsense Regression. Integrated but

Response surface models for the Elliott, Rothenberg, Stock DF-GLS unit-root test

Response surface models for the Elliott, Rothenberg, Stock DF-GLS unit-root test Christopher F Baum Jesús Otero UK Stata Users Group Meetings, London, September 2017 Baum, Otero (BC, U. del Rosario) DF-GLS

Response surface models for the Elliott, Rothenberg, Stock DF-GLS unit-root test Christopher F Baum Jesús Otero UK Stata Users Group Meetings, London, September 2017 Baum, Otero (BC, U. del Rosario) DF-GLS

Exercise Sheet 6: Solutions

Exercise Sheet 6: Solutions R.G. Pierse 1. (a) Regression yields: Dependent Variable: LC Date: 10/29/02 Time: 18:37 Sample(adjusted): 1950 1985 Included observations: 36 after adjusting endpoints C 0.244716

Exercise Sheet 6: Solutions R.G. Pierse 1. (a) Regression yields: Dependent Variable: LC Date: 10/29/02 Time: 18:37 Sample(adjusted): 1950 1985 Included observations: 36 after adjusting endpoints C 0.244716

Time Series Analysis. James D. Hamilton PRINCETON UNIVERSITY PRESS PRINCETON, NEW JERSEY

Time Series Analysis James D. Hamilton PRINCETON UNIVERSITY PRESS PRINCETON, NEW JERSEY & Contents PREFACE xiii 1 1.1. 1.2. Difference Equations First-Order Difference Equations 1 /?th-order Difference

Time Series Analysis James D. Hamilton PRINCETON UNIVERSITY PRESS PRINCETON, NEW JERSEY & Contents PREFACE xiii 1 1.1. 1.2. Difference Equations First-Order Difference Equations 1 /?th-order Difference

OUTWARD FDI, DOMESTIC INVESTMENT AND INFORMAL INSTITUTIONS: EVIDENCE FROM CHINA WAQAR AMEER & MOHAMMED SAUD M ALOTAISH

International Journal of Economics, Commerce and Research (IJECR) ISSN(P): 2250-0006; ISSN(E): 2319-4472 Vol. 7, Issue 1, Feb 2017, 25-30 TJPRC Pvt. Ltd. OUTWARD FDI, DOMESTIC INVESTMENT AND INFORMAL INSTITUTIONS:

International Journal of Economics, Commerce and Research (IJECR) ISSN(P): 2250-0006; ISSN(E): 2319-4472 Vol. 7, Issue 1, Feb 2017, 25-30 TJPRC Pvt. Ltd. OUTWARD FDI, DOMESTIC INVESTMENT AND INFORMAL INSTITUTIONS:

APPLIED MACROECONOMETRICS Licenciatura Universidade Nova de Lisboa Faculdade de Economia. FINAL EXAM JUNE 3, 2004 Starts at 14:00 Ends at 16:30

APPLIED MACROECONOMETRICS Licenciatura Universidade Nova de Lisboa Faculdade de Economia FINAL EXAM JUNE 3, 2004 Starts at 14:00 Ends at 16:30 I In Figure I.1 you can find a quarterly inflation rate series

APPLIED MACROECONOMETRICS Licenciatura Universidade Nova de Lisboa Faculdade de Economia FINAL EXAM JUNE 3, 2004 Starts at 14:00 Ends at 16:30 I In Figure I.1 you can find a quarterly inflation rate series

CHAPTER 21: TIME SERIES ECONOMETRICS: SOME BASIC CONCEPTS

CHAPTER 21: TIME SERIES ECONOMETRICS: SOME BASIC CONCEPTS 21.1 A stochastic process is said to be weakly stationary if its mean and variance are constant over time and if the value of the covariance between

CHAPTER 21: TIME SERIES ECONOMETRICS: SOME BASIC CONCEPTS 21.1 A stochastic process is said to be weakly stationary if its mean and variance are constant over time and if the value of the covariance between

The causal relationship between energy consumption and GDP in Turkey

The causal relationship between energy consumption and GDP in Turkey Huseyin Kalyoncu1, Ilhan Ozturk2, Muhittin Kaplan1 1Meliksah University, Faculty of Economics and Administrative Sciences, 38010, Kayseri,

The causal relationship between energy consumption and GDP in Turkey Huseyin Kalyoncu1, Ilhan Ozturk2, Muhittin Kaplan1 1Meliksah University, Faculty of Economics and Administrative Sciences, 38010, Kayseri,

The Causal Relation between Savings and Economic Growth: Some Evidence. from MENA Countries. Bassam AbuAl-Foul

The Causal Relation between Savings and Economic Growth: Some Evidence from MENA Countries Bassam AbuAl-Foul (babufoul@aus.edu) Abstract This paper examines empirically the long-run relationship between

The Causal Relation between Savings and Economic Growth: Some Evidence from MENA Countries Bassam AbuAl-Foul (babufoul@aus.edu) Abstract This paper examines empirically the long-run relationship between

Bristol Business School

Bristol Business School Academic Year: 10/11 Examination Period: January Module Leader: Module Code: Title of Module: John Paul Dunne Econometrics UMEN3P-15-M Examination Date: 12 January 2011 Examination

Bristol Business School Academic Year: 10/11 Examination Period: January Module Leader: Module Code: Title of Module: John Paul Dunne Econometrics UMEN3P-15-M Examination Date: 12 January 2011 Examination

Stationarity and Cointegration analysis. Tinashe Bvirindi

Stationarity and Cointegration analysis By Tinashe Bvirindi tbvirindi@gmail.com layout Unit root testing Cointegration Vector Auto-regressions Cointegration in Multivariate systems Introduction Stationarity

Stationarity and Cointegration analysis By Tinashe Bvirindi tbvirindi@gmail.com layout Unit root testing Cointegration Vector Auto-regressions Cointegration in Multivariate systems Introduction Stationarity

Time Series Analysis. James D. Hamilton PRINCETON UNIVERSITY PRESS PRINCETON, NEW JERSEY

Time Series Analysis James D. Hamilton PRINCETON UNIVERSITY PRESS PRINCETON, NEW JERSEY PREFACE xiii 1 Difference Equations 1.1. First-Order Difference Equations 1 1.2. pth-order Difference Equations 7

Time Series Analysis James D. Hamilton PRINCETON UNIVERSITY PRESS PRINCETON, NEW JERSEY PREFACE xiii 1 Difference Equations 1.1. First-Order Difference Equations 1 1.2. pth-order Difference Equations 7

Econ 423 Lecture Notes: Additional Topics in Time Series 1

Econ 423 Lecture Notes: Additional Topics in Time Series 1 John C. Chao April 25, 2017 1 These notes are based in large part on Chapter 16 of Stock and Watson (2011). They are for instructional purposes

Econ 423 Lecture Notes: Additional Topics in Time Series 1 John C. Chao April 25, 2017 1 These notes are based in large part on Chapter 16 of Stock and Watson (2011). They are for instructional purposes

Economtrics of money and finance Lecture six: spurious regression and cointegration

Economtrics of money and finance Lecture six: spurious regression and cointegration Zongxin Qian School of Finance, Renmin University of China October 21, 2014 Table of Contents Overview Spurious regression

Economtrics of money and finance Lecture six: spurious regression and cointegration Zongxin Qian School of Finance, Renmin University of China October 21, 2014 Table of Contents Overview Spurious regression

13. Time Series Analysis: Asymptotics Weakly Dependent and Random Walk Process. Strict Exogeneity

Outline: Further Issues in Using OLS with Time Series Data 13. Time Series Analysis: Asymptotics Weakly Dependent and Random Walk Process I. Stationary and Weakly Dependent Time Series III. Highly Persistent

Outline: Further Issues in Using OLS with Time Series Data 13. Time Series Analysis: Asymptotics Weakly Dependent and Random Walk Process I. Stationary and Weakly Dependent Time Series III. Highly Persistent

G. S. Maddala Kajal Lahiri. WILEY A John Wiley and Sons, Ltd., Publication

G. S. Maddala Kajal Lahiri WILEY A John Wiley and Sons, Ltd., Publication TEMT Foreword Preface to the Fourth Edition xvii xix Part I Introduction and the Linear Regression Model 1 CHAPTER 1 What is Econometrics?

G. S. Maddala Kajal Lahiri WILEY A John Wiley and Sons, Ltd., Publication TEMT Foreword Preface to the Fourth Edition xvii xix Part I Introduction and the Linear Regression Model 1 CHAPTER 1 What is Econometrics?

The Effects of Unemployment on Economic Growth in Greece. An ARDL Bound Test Approach.

53 The Effects of Unemployment on Economic Growth in Greece. An ARDL Bound Test Approach. Nikolaos Dritsakis 1 Pavlos Stamatiou 2 The aim of this paper is to investigate the relationship between unemployment

53 The Effects of Unemployment on Economic Growth in Greece. An ARDL Bound Test Approach. Nikolaos Dritsakis 1 Pavlos Stamatiou 2 The aim of this paper is to investigate the relationship between unemployment

Contents. Part I Statistical Background and Basic Data Handling 5. List of Figures List of Tables xix

Contents List of Figures List of Tables xix Preface Acknowledgements 1 Introduction 1 What is econometrics? 2 The stages of applied econometric work 2 Part I Statistical Background and Basic Data Handling

Contents List of Figures List of Tables xix Preface Acknowledgements 1 Introduction 1 What is econometrics? 2 The stages of applied econometric work 2 Part I Statistical Background and Basic Data Handling

A Horse-Race Contest of Selected Economic Indicators & Their Potential Prediction Abilities on GDP

A Horse-Race Contest of Selected Economic Indicators & Their Potential Prediction Abilities on GDP Tahmoures Afshar, Woodbury University, USA ABSTRACT This paper empirically investigates, in the context

A Horse-Race Contest of Selected Economic Indicators & Their Potential Prediction Abilities on GDP Tahmoures Afshar, Woodbury University, USA ABSTRACT This paper empirically investigates, in the context

10) Time series econometrics

Time series econometrics") 30C00200 Econometrics 10) Time series econometrics Timo Kuosmanen Professor, Ph.D. 1 Topics today Static vs. dynamic time series model Suprious regression Stationary and nonstationary time series Unit

30C00200 Econometrics 10) Time series econometrics Timo Kuosmanen Professor, Ph.D. 1 Topics today Static vs. dynamic time series model Suprious regression Stationary and nonstationary time series Unit

THE INFLUENCE OF FOREIGN DIRECT INVESTMENTS ON MONTENEGRO PAYMENT BALANCE

Preliminary communication (accepted September 12, 2013) THE INFLUENCE OF FOREIGN DIRECT INVESTMENTS ON MONTENEGRO PAYMENT BALANCE Ana Gardasevic 1 Abstract: In this work, with help of econometric analysis

Preliminary communication (accepted September 12, 2013) THE INFLUENCE OF FOREIGN DIRECT INVESTMENTS ON MONTENEGRO PAYMENT BALANCE Ana Gardasevic 1 Abstract: In this work, with help of econometric analysis

Economic modelling and forecasting. 2-6 February 2015

Economic modelling and forecasting 2-6 February 2015 Bank of England 2015 Ole Rummel Adviser, CCBS at the Bank of England ole.rummel@bankofengland.co.uk Philosophy of my presentations Everything should

Economic modelling and forecasting 2-6 February 2015 Bank of England 2015 Ole Rummel Adviser, CCBS at the Bank of England ole.rummel@bankofengland.co.uk Philosophy of my presentations Everything should

The Role of "Leads" in the Dynamic Title of Cointegrating Regression Models. Author(s) Hayakawa, Kazuhiko; Kurozumi, Eiji

Hayakawa, Kazuhiko; Kurozumi, Eiji") he Role of "Leads" in the Dynamic itle of Cointegrating Regression Models Author(s) Hayakawa, Kazuhiko; Kurozumi, Eiji Citation Issue 2006-12 Date ype echnical Report ext Version publisher URL http://hdl.handle.net/10086/13599

he Role of "Leads" in the Dynamic itle of Cointegrating Regression Models Author(s) Hayakawa, Kazuhiko; Kurozumi, Eiji Citation Issue 2006-12 Date ype echnical Report ext Version publisher URL http://hdl.handle.net/10086/13599

Cointegration and Tests of Purchasing Parity Anthony Mac Guinness- Senior Sophister

Cointegration and Tests of Purchasing Parity Anthony Mac Guinness- Senior Sophister Most of us know Purchasing Power Parity as a sensible way of expressing per capita GNP; that is taking local price levels

Cointegration and Tests of Purchasing Parity Anthony Mac Guinness- Senior Sophister Most of us know Purchasing Power Parity as a sensible way of expressing per capita GNP; that is taking local price levels

Existence of Export-Import Cointegration: A Study on Indonesia and Malaysia

Existence of Export-Import Cointegration: A Study on Indonesia and Malaysia Mohammad Zillur Rahman Assistant Professor, School of Business Studies Southeast University, Plot 64-B, Road#18-B, Banani, Dhaka,

Existence of Export-Import Cointegration: A Study on Indonesia and Malaysia Mohammad Zillur Rahman Assistant Professor, School of Business Studies Southeast University, Plot 64-B, Road#18-B, Banani, Dhaka,

Aviation Demand and Economic Growth in the Czech Republic: Cointegration Estimation and Causality Analysis

Analyses Aviation Demand and Economic Growth in the Czech Republic: Cointegration Estimation and Causality Analysis Bilal Mehmood 1 Government College University, Lahore, Pakistan Amna Shahid 2 Government

Analyses Aviation Demand and Economic Growth in the Czech Republic: Cointegration Estimation and Causality Analysis Bilal Mehmood 1 Government College University, Lahore, Pakistan Amna Shahid 2 Government

Practice Questions for the Final Exam. Theoretical Part

Brooklyn College Econometrics 7020X Spring 2016 Instructor: G. Koimisis Name: Date: Practice Questions for the Final Exam Theoretical Part 1. Define dummy variable and give two examples. 2. Analyze the

Brooklyn College Econometrics 7020X Spring 2016 Instructor: G. Koimisis Name: Date: Practice Questions for the Final Exam Theoretical Part 1. Define dummy variable and give two examples. 2. Analyze the

Testing for non-stationarity

20 November, 2009 Overview The tests for investigating the non-stationary of a time series falls into four types: 1 Check the null that there is a unit root against stationarity. Within these, there are

20 November, 2009 Overview The tests for investigating the non-stationary of a time series falls into four types: 1 Check the null that there is a unit root against stationarity. Within these, there are

This chapter reviews properties of regression estimators and test statistics based on

Chapter 12 COINTEGRATING AND SPURIOUS REGRESSIONS This chapter reviews properties of regression estimators and test statistics based on the estimators when the regressors and regressant are difference

Chapter 12 COINTEGRATING AND SPURIOUS REGRESSIONS This chapter reviews properties of regression estimators and test statistics based on the estimators when the regressors and regressant are difference

Cointegration Analysis of Exports and Imports: The Case of Pakistan Economy

MPRA Munich Personal RePEc Archive Cointegration Analysis of Exports and Imports: The Case of Pakistan Economy Sharafat Ali Government Postgraduate College Kot Sultan District Layyah, Pakistan August 2013

MPRA Munich Personal RePEc Archive Cointegration Analysis of Exports and Imports: The Case of Pakistan Economy Sharafat Ali Government Postgraduate College Kot Sultan District Layyah, Pakistan August 2013

BCT Lecture 3. Lukas Vacha.

BCT Lecture 3 Lukas Vacha vachal@utia.cas.cz Stationarity and Unit Root Testing Why do we need to test for Non-Stationarity? The stationarity or otherwise of a series can strongly influence its behaviour

BCT Lecture 3 Lukas Vacha vachal@utia.cas.cz Stationarity and Unit Root Testing Why do we need to test for Non-Stationarity? The stationarity or otherwise of a series can strongly influence its behaviour

9) Time series econometrics

Time series econometrics") 30C00200 Econometrics 9) Time series econometrics Timo Kuosmanen Professor Management Science http://nomepre.net/index.php/timokuosmanen 1 Macroeconomic data: GDP Inflation rate Examples of time series

30C00200 Econometrics 9) Time series econometrics Timo Kuosmanen Professor Management Science http://nomepre.net/index.php/timokuosmanen 1 Macroeconomic data: GDP Inflation rate Examples of time series

Darmstadt Discussion Papers in Economics

Darmstadt Discussion Papers in Economics The Effect of Linear Time Trends on Cointegration Testing in Single Equations Uwe Hassler Nr. 111 Arbeitspapiere des Instituts für Volkswirtschaftslehre Technische

Darmstadt Discussion Papers in Economics The Effect of Linear Time Trends on Cointegration Testing in Single Equations Uwe Hassler Nr. 111 Arbeitspapiere des Instituts für Volkswirtschaftslehre Technische

Bootstrapping the Grainger Causality Test With Integrated Data

Bootstrapping the Grainger Causality Test With Integrated Data Richard Ti n University of Reading July 26, 2006 Abstract A Monte-carlo experiment is conducted to investigate the small sample performance

Bootstrapping the Grainger Causality Test With Integrated Data Richard Ti n University of Reading July 26, 2006 Abstract A Monte-carlo experiment is conducted to investigate the small sample performance

Econometrics Lab Hour Session 6

Econometrics Lab Hour Session 6 Agustín Bénétrix benetria@tcd.ie Office hour: Wednesday 4-5 Room 3021 Martin Schmitz schmitzm@tcd.ie Office hour: Monday 5-6 Room 3021 Outline Importing the dataset Time

Econometrics Lab Hour Session 6 Agustín Bénétrix benetria@tcd.ie Office hour: Wednesday 4-5 Room 3021 Martin Schmitz schmitzm@tcd.ie Office hour: Monday 5-6 Room 3021 Outline Importing the dataset Time

International Monetary Policy Spillovers

International Monetary Policy Spillovers Dennis Nsafoah Department of Economics University of Calgary Canada November 1, 2017 1 Abstract This paper uses monthly data (from January 1997 to April 2017) to

International Monetary Policy Spillovers Dennis Nsafoah Department of Economics University of Calgary Canada November 1, 2017 1 Abstract This paper uses monthly data (from January 1997 to April 2017) to

Introduction to Modern Time Series Analysis

Introduction to Modern Time Series Analysis Gebhard Kirchgässner, Jürgen Wolters and Uwe Hassler Second Edition Springer 3 Teaching Material The following figures and tables are from the above book. They

Introduction to Modern Time Series Analysis Gebhard Kirchgässner, Jürgen Wolters and Uwe Hassler Second Edition Springer 3 Teaching Material The following figures and tables are from the above book. They

Univariate linear models

Univariate linear models The specification process of an univariate ARIMA model is based on the theoretical properties of the different processes and it is also important the observation and interpretation

Univariate linear models The specification process of an univariate ARIMA model is based on the theoretical properties of the different processes and it is also important the observation and interpretation

Volume 30, Issue 1. EUAs and CERs: Vector Autoregression, Impulse Response Function and Cointegration Analysis

Volume 30, Issue 1 EUAs and CERs: Vector Autoregression, Impulse Response Function and Cointegration Analysis Julien Chevallier Université Paris Dauphine Abstract EUAs are European Union Allowances traded

Volume 30, Issue 1 EUAs and CERs: Vector Autoregression, Impulse Response Function and Cointegration Analysis Julien Chevallier Université Paris Dauphine Abstract EUAs are European Union Allowances traded

Christopher Dougherty London School of Economics and Political Science

Introduction to Econometrics FIFTH EDITION Christopher Dougherty London School of Economics and Political Science OXFORD UNIVERSITY PRESS Contents INTRODU CTION 1 Why study econometrics? 1 Aim of this

Introduction to Econometrics FIFTH EDITION Christopher Dougherty London School of Economics and Political Science OXFORD UNIVERSITY PRESS Contents INTRODU CTION 1 Why study econometrics? 1 Aim of this

Lecture 8a: Spurious Regression

Lecture 8a: Spurious Regression 1 2 Old Stuff The traditional statistical theory holds when we run regression using stationary variables. For example, when we regress one stationary series onto another

Lecture 8a: Spurious Regression 1 2 Old Stuff The traditional statistical theory holds when we run regression using stationary variables. For example, when we regress one stationary series onto another

Introduction to Eco n o m et rics

2008 AGI-Information Management Consultants May be used for personal purporses only or by libraries associated to dandelon.com network. Introduction to Eco n o m et rics Third Edition G.S. Maddala Formerly

2008 AGI-Information Management Consultants May be used for personal purporses only or by libraries associated to dandelon.com network. Introduction to Eco n o m et rics Third Edition G.S. Maddala Formerly

Inflation Revisited: New Evidence from Modified Unit Root Tests

1 Inflation Revisited: New Evidence from Modified Unit Root Tests Walter Enders and Yu Liu * University of Alabama in Tuscaloosa and University of Texas at El Paso Abstract: We propose a simple modification

1 Inflation Revisited: New Evidence from Modified Unit Root Tests Walter Enders and Yu Liu * University of Alabama in Tuscaloosa and University of Texas at El Paso Abstract: We propose a simple modification

Questions and Answers on Unit Roots, Cointegration, VARs and VECMs

Questions and Answers on Unit Roots, Cointegration, VARs and VECMs L. Magee Winter, 2012 1. Let ɛ t, t = 1,..., T be a series of independent draws from a N[0,1] distribution. Let w t, t = 1,..., T, be

Questions and Answers on Unit Roots, Cointegration, VARs and VECMs L. Magee Winter, 2012 1. Let ɛ t, t = 1,..., T be a series of independent draws from a N[0,1] distribution. Let w t, t = 1,..., T, be

Applied Econometrics. Applied Econometrics Second edition. Dimitrios Asteriou and Stephen G. Hall

Applied Econometrics Second edition Dimitrios Asteriou and Stephen G. Hall MULTICOLLINEARITY 1. Perfect Multicollinearity 2. Consequences of Perfect Multicollinearity 3. Imperfect Multicollinearity 4.

Applied Econometrics Second edition Dimitrios Asteriou and Stephen G. Hall MULTICOLLINEARITY 1. Perfect Multicollinearity 2. Consequences of Perfect Multicollinearity 3. Imperfect Multicollinearity 4.

OLS Assumptions Violation and Its Treatment: An Empirical Test of Gross Domestic Product Relationship with Exchange Rate, Inflation and Interest Rate

J. Appl. Environ. Biol. Sci., 6(5S)43-54, 2016 2016, TextRoad Publication ISSN: 2090-4274 Journal of Applied Environmental and Biological Sciences www.textroad.com OLS Assumptions Violation and Its Treatment:

J. Appl. Environ. Biol. Sci., 6(5S)43-54, 2016 2016, TextRoad Publication ISSN: 2090-4274 Journal of Applied Environmental and Biological Sciences www.textroad.com OLS Assumptions Violation and Its Treatment:

This is a repository copy of The Error Correction Model as a Test for Cointegration.

This is a repository copy of The Error Correction Model as a Test for Cointegration. White Rose Research Online URL for this paper: http://eprints.whiterose.ac.uk/9886/ Monograph: Kanioura, A. and Turner,

This is a repository copy of The Error Correction Model as a Test for Cointegration. White Rose Research Online URL for this paper: http://eprints.whiterose.ac.uk/9886/ Monograph: Kanioura, A. and Turner,

DEPARTMENT OF ECONOMICS AND FINANCE COLLEGE OF BUSINESS AND ECONOMICS UNIVERSITY OF CANTERBURY CHRISTCHURCH, NEW ZEALAND

DEPARTMENT OF ECONOMICS AND FINANCE COLLEGE OF BUSINESS AND ECONOMICS UNIVERSITY OF CANTERBURY CHRISTCHURCH, NEW ZEALAND Testing For Unit Roots With Cointegrated Data NOTE: This paper is a revision of

DEPARTMENT OF ECONOMICS AND FINANCE COLLEGE OF BUSINESS AND ECONOMICS UNIVERSITY OF CANTERBURY CHRISTCHURCH, NEW ZEALAND Testing For Unit Roots With Cointegrated Data NOTE: This paper is a revision of

A multivariate cointegration analysis of the role of energy in the US macroeconomy

Ž. Energy Economics 22 2000 267 283 A multivariate cointegration analysis of the role of energy in the US macroeconomy David I. Stern Centre for Resource and En ironmental Studies, Australian National

Ž. Energy Economics 22 2000 267 283 A multivariate cointegration analysis of the role of energy in the US macroeconomy David I. Stern Centre for Resource and En ironmental Studies, Australian National

Lecture 8a: Spurious Regression

Lecture 8a: Spurious Regression 1 Old Stuff The traditional statistical theory holds when we run regression using (weakly or covariance) stationary variables. For example, when we regress one stationary

Lecture 8a: Spurious Regression 1 Old Stuff The traditional statistical theory holds when we run regression using (weakly or covariance) stationary variables. For example, when we regress one stationary

Research Center for Science Technology and Society of Fuzhou University, International Studies and Trade, Changle Fuzhou , China

2017 3rd Annual International Conference on Modern Education and Social Science (MESS 2017) ISBN: 978-1-60595-450-9 An Analysis of the Correlation Between the Scale of Higher Education and Economic Growth

2017 3rd Annual International Conference on Modern Education and Social Science (MESS 2017) ISBN: 978-1-60595-450-9 An Analysis of the Correlation Between the Scale of Higher Education and Economic Growth

Nonstationary Time Series:

Nonstationary Time Series: Unit Roots Egon Zakrajšek Division of Monetary Affairs Federal Reserve Board Summer School in Financial Mathematics Faculty of Mathematics & Physics University of Ljubljana September

Nonstationary Time Series: Unit Roots Egon Zakrajšek Division of Monetary Affairs Federal Reserve Board Summer School in Financial Mathematics Faculty of Mathematics & Physics University of Ljubljana September

EXCHANGE RATE PASS-THROUGH: THE CASE OF BRAZILIAN EXPORTS OF MANUFACTURES

EXCHANGE RATE PASS-THROUGH: THE CASE OF BRAZILIAN EXPORTS OF MANUFACTURES Afonso Ferreira Departamento de Economia - Universidade Federal de Minas Gerais (UFMG) and Centro de Pesquisa em Economia Internacional,

EXCHANGE RATE PASS-THROUGH: THE CASE OF BRAZILIAN EXPORTS OF MANUFACTURES Afonso Ferreira Departamento de Economia - Universidade Federal de Minas Gerais (UFMG) and Centro de Pesquisa em Economia Internacional,

Modelling Electricity Demand in New Zealand

Modelling Electricity Demand in New Zealand Market performance enquiry 14 April 2014 Market Performance Version control Version Date amended Comments 1.0 15 April 2014 1 st draft i 20 March 2015 12.39

Modelling Electricity Demand in New Zealand Market performance enquiry 14 April 2014 Market Performance Version control Version Date amended Comments 1.0 15 April 2014 1 st draft i 20 March 2015 12.39

2. Linear regression with multiple regressors

2. Linear regression with multiple regressors Aim of this section: Introduction of the multiple regression model OLS estimation in multiple regression Measures-of-fit in multiple regression Assumptions

2. Linear regression with multiple regressors Aim of this section: Introduction of the multiple regression model OLS estimation in multiple regression Measures-of-fit in multiple regression Assumptions

CO INTEGRATION: APPLICATION TO THE ROLE OF INFRASTRUCTURES ON ECONOMIC DEVELOPMENT IN NIGERIA

CO INTEGRATION: APPLICATION TO THE ROLE OF INFRASTRUCTURES ON ECONOMIC DEVELOPMENT IN NIGERIA Alabi Oluwapelumi Department of Statistics Federal University of Technology, Akure Olarinde O. Bolanle Department

CO INTEGRATION: APPLICATION TO THE ROLE OF INFRASTRUCTURES ON ECONOMIC DEVELOPMENT IN NIGERIA Alabi Oluwapelumi Department of Statistics Federal University of Technology, Akure Olarinde O. Bolanle Department

Testing for Unit Roots with Cointegrated Data

Discussion Paper No. 2015-57 August 19, 2015 http://www.economics-ejournal.org/economics/discussionpapers/2015-57 Testing for Unit Roots with Cointegrated Data W. Robert Reed Abstract This paper demonstrates

Discussion Paper No. 2015-57 August 19, 2015 http://www.economics-ejournal.org/economics/discussionpapers/2015-57 Testing for Unit Roots with Cointegrated Data W. Robert Reed Abstract This paper demonstrates

THE IMPACT OF REAL EXCHANGE RATE CHANGES ON SOUTH AFRICAN AGRICULTURAL EXPORTS: AN ERROR CORRECTION MODEL APPROACH

THE IMPACT OF REAL EXCHANGE RATE CHANGES ON SOUTH AFRICAN AGRICULTURAL EXPORTS: AN ERROR CORRECTION MODEL APPROACH D. Poonyth and J. van Zyl 1 This study evaluates the long run and short run effects of

THE IMPACT OF REAL EXCHANGE RATE CHANGES ON SOUTH AFRICAN AGRICULTURAL EXPORTS: AN ERROR CORRECTION MODEL APPROACH D. Poonyth and J. van Zyl 1 This study evaluates the long run and short run effects of

Title. Description. Quick start. Menu. stata.com. xtcointtest Panel-data cointegration tests

Title stata.com xtcointtest Panel-data cointegration tests Description Quick start Menu Syntax Options Remarks and examples Stored results Methods and formulas References Also see Description xtcointtest

Title stata.com xtcointtest Panel-data cointegration tests Description Quick start Menu Syntax Options Remarks and examples Stored results Methods and formulas References Also see Description xtcointtest

TESTING FOR CO-INTEGRATION

Bo Sjö 2010-12-05 TESTING FOR CO-INTEGRATION To be used in combination with Sjö (2008) Testing for Unit Roots and Cointegration A Guide. Instructions: Use the Johansen method to test for Purchasing Power

Bo Sjö 2010-12-05 TESTING FOR CO-INTEGRATION To be used in combination with Sjö (2008) Testing for Unit Roots and Cointegration A Guide. Instructions: Use the Johansen method to test for Purchasing Power

A TIME SERIES PARADOX: UNIT ROOT TESTS PERFORM POORLY WHEN DATA ARE COINTEGRATED

A TIME SERIES PARADOX: UNIT ROOT TESTS PERFORM POORLY WHEN DATA ARE COINTEGRATED by W. Robert Reed Department of Economics and Finance University of Canterbury, New Zealand Email: bob.reed@canterbury.ac.nz

A TIME SERIES PARADOX: UNIT ROOT TESTS PERFORM POORLY WHEN DATA ARE COINTEGRATED by W. Robert Reed Department of Economics and Finance University of Canterbury, New Zealand Email: bob.reed@canterbury.ac.nz

Volume 29, Issue 1. Price and Wage Setting in Japan: An Empirical Investigation

Volume 29, Issue 1 Price and Wage Setting in Japan: An Empirical Investigation Shigeyuki Hamori Kobe University Junya Masuda Mitsubishi Research Institute Takeshi Hoshikawa Kinki University Kunihiro Hanabusa

Volume 29, Issue 1 Price and Wage Setting in Japan: An Empirical Investigation Shigeyuki Hamori Kobe University Junya Masuda Mitsubishi Research Institute Takeshi Hoshikawa Kinki University Kunihiro Hanabusa

A Non-Parametric Approach of Heteroskedasticity Robust Estimation of Vector-Autoregressive (VAR) Models

Models") Journal of Finance and Investment Analysis, vol.1, no.1, 2012, 55-67 ISSN: 2241-0988 (print version), 2241-0996 (online) International Scientific Press, 2012 A Non-Parametric Approach of Heteroskedasticity

Journal of Finance and Investment Analysis, vol.1, no.1, 2012, 55-67 ISSN: 2241-0988 (print version), 2241-0996 (online) International Scientific Press, 2012 A Non-Parametric Approach of Heteroskedasticity

Exercise Sheet 5: Solutions

Exercise Sheet 5: Solutions R.G. Pierse 2. Estimation of Model M1 yields the following results: Date: 10/24/02 Time: 18:06 C -1.448432 0.696587-2.079327 0.0395 LPC -0.306051 0.272836-1.121740 0.2640 LPF

Exercise Sheet 5: Solutions R.G. Pierse 2. Estimation of Model M1 yields the following results: Date: 10/24/02 Time: 18:06 C -1.448432 0.696587-2.079327 0.0395 LPC -0.306051 0.272836-1.121740 0.2640 LPF

Cointegration tests of purchasing power parity

MPRA Munich Personal RePEc Archive Cointegration tests of purchasing power parity Frederick Wallace Universidad de Quintana Roo 1. October 2009 Online at http://mpra.ub.uni-muenchen.de/18079/ MPRA Paper

MPRA Munich Personal RePEc Archive Cointegration tests of purchasing power parity Frederick Wallace Universidad de Quintana Roo 1. October 2009 Online at http://mpra.ub.uni-muenchen.de/18079/ MPRA Paper

Romanian Economic and Business Review Vol. 3, No. 3 THE EVOLUTION OF SNP PETROM STOCK LIST - STUDY THROUGH AUTOREGRESSIVE MODELS

THE EVOLUTION OF SNP PETROM STOCK LIST - STUDY THROUGH AUTOREGRESSIVE MODELS Marian Zaharia, Ioana Zaheu, and Elena Roxana Stan Abstract Stock exchange market is one of the most dynamic and unpredictable

THE EVOLUTION OF SNP PETROM STOCK LIST - STUDY THROUGH AUTOREGRESSIVE MODELS Marian Zaharia, Ioana Zaheu, and Elena Roxana Stan Abstract Stock exchange market is one of the most dynamic and unpredictable

Lecture 5: Unit Roots, Cointegration and Error Correction Models The Spurious Regression Problem

Lecture 5: Unit Roots, Cointegration and Error Correction Models The Spurious Regression Problem Prof. Massimo Guidolin 20192 Financial Econometrics Winter/Spring 2018 Overview Stochastic vs. deterministic

Lecture 5: Unit Roots, Cointegration and Error Correction Models The Spurious Regression Problem Prof. Massimo Guidolin 20192 Financial Econometrics Winter/Spring 2018 Overview Stochastic vs. deterministic

A PANIC Attack on Unit Roots and Cointegration. July 31, Preliminary and Incomplete

A PANIC Attack on Unit Roots and Cointegration Jushan Bai Serena Ng July 3, 200 Preliminary and Incomplete Abstract his paper presents a toolkit for Panel Analysis of Non-stationarity in Idiosyncratic

A PANIC Attack on Unit Roots and Cointegration Jushan Bai Serena Ng July 3, 200 Preliminary and Incomplete Abstract his paper presents a toolkit for Panel Analysis of Non-stationarity in Idiosyncratic

On Consistency of Tests for Stationarity in Autoregressive and Moving Average Models of Different Orders

American Journal of Theoretical and Applied Statistics 2016; 5(3): 146-153 http://www.sciencepublishinggroup.com/j/ajtas doi: 10.11648/j.ajtas.20160503.20 ISSN: 2326-8999 (Print); ISSN: 2326-9006 (Online)

American Journal of Theoretical and Applied Statistics 2016; 5(3): 146-153 http://www.sciencepublishinggroup.com/j/ajtas doi: 10.11648/j.ajtas.20160503.20 ISSN: 2326-8999 (Print); ISSN: 2326-9006 (Online)

Exports and Economic Growth in Asian Developing Countries: Cointegration and Error-Correction Models

Volume 24, Number 2, December 1999 Exports and Economic Growth in Asian Developing Countries: Cointegration and Error-Correction Models E.M. Ekanayake * 1 This paper uses cointegration and error-correction

Volume 24, Number 2, December 1999 Exports and Economic Growth in Asian Developing Countries: Cointegration and Error-Correction Models E.M. Ekanayake * 1 This paper uses cointegration and error-correction

Population Growth and Economic Development: Test for Causality

The Lahore Journal of Economics 11 : 2 (Winter 2006) pp. 71-77 Population Growth and Economic Development: Test for Causality Khalid Mushtaq * Abstract This paper examines the existence of a long-run relationship

The Lahore Journal of Economics 11 : 2 (Winter 2006) pp. 71-77 Population Growth and Economic Development: Test for Causality Khalid Mushtaq * Abstract This paper examines the existence of a long-run relationship

Relationship between Energy Consumption and GDP in Iran

Relationship between Energy Consumption and GDP in Iran Gudarzi Farahani, Yazdan 1 Soheli Ghasemi, Banafshe 2 * 1. M.A. student in Economics, University of Tehran, Faculty of economics, Shomali Kargar,

Relationship between Energy Consumption and GDP in Iran Gudarzi Farahani, Yazdan 1 Soheli Ghasemi, Banafshe 2 * 1. M.A. student in Economics, University of Tehran, Faculty of economics, Shomali Kargar,

CAN ECONOMIC GROWTH LAST? SERIOUSLY.

THE 6TH INTERNATIONAL CONFERENCE THE CHANGING ECONOMIC LANDSCAPE: ISSUES, IMPLICATIONS AND POLICY OPTIONS ISSN1331 677X (UDK 338) May 30 th - June 1 st 2013 Saša Stjepanović a a Ph.d. Saša Stjepanović,

THE 6TH INTERNATIONAL CONFERENCE THE CHANGING ECONOMIC LANDSCAPE: ISSUES, IMPLICATIONS AND POLICY OPTIONS ISSN1331 677X (UDK 338) May 30 th - June 1 st 2013 Saša Stjepanović a a Ph.d. Saša Stjepanović,

ICT AND CAUSALITY IN THE NEW ZEALAND ECONOMY. Nancy Chu, Les Oxley and Ken Carlaw

Proceedings of the 2005 International Conference on Simulation and Modelling V. Kachitvichyanukul, U. Purintrapiban, P. Utayopas, Chu, Oxley eds. and Carlaw ICT AND CAUSALITY IN THE NEW ZEALAND ECONOMY

Proceedings of the 2005 International Conference on Simulation and Modelling V. Kachitvichyanukul, U. Purintrapiban, P. Utayopas, Chu, Oxley eds. and Carlaw ICT AND CAUSALITY IN THE NEW ZEALAND ECONOMY

1 Regression with Time Series Variables

1 Regression with Time Series Variables With time series regression, Y might not only depend on X, but also lags of Y and lags of X Autoregressive Distributed lag (or ADL(p; q)) model has these features:

1 Regression with Time Series Variables With time series regression, Y might not only depend on X, but also lags of Y and lags of X Autoregressive Distributed lag (or ADL(p; q)) model has these features:

Estimates of the Sticky-Information Phillips Curve for the USA with the General to Specific Method

MPRA Munich Personal RePEc Archive Estimates of the Sticky-Information Phillips Curve for the USA with the General to Specific Method Antonio Paradiso and B. Bhaskara Rao and Marco Ventura 12. February

MPRA Munich Personal RePEc Archive Estimates of the Sticky-Information Phillips Curve for the USA with the General to Specific Method Antonio Paradiso and B. Bhaskara Rao and Marco Ventura 12. February

Simultaneous Equation Models Learning Objectives Introduction Introduction (2) Introduction (3) Solving the Model structural equations

Introduction (3) Solving the Model structural equations") Simultaneous Equation Models. Introduction: basic definitions 2. Consequences of ignoring simultaneity 3. The identification problem 4. Estimation of simultaneous equation models 5. Example: IS LM model

Simultaneous Equation Models. Introduction: basic definitions 2. Consequences of ignoring simultaneity 3. The identification problem 4. Estimation of simultaneous equation models 5. Example: IS LM model

Trends and Unit Roots in Greek Real Money Supply, Real GDP and Nominal Interest Rate

European Research Studies Volume V, Issue (3-4), 00, pp. 5-43 Trends and Unit Roots in Greek Real Money Supply, Real GDP and Nominal Interest Rate Karpetis Christos & Varelas Erotokritos * Abstract This

European Research Studies Volume V, Issue (3-4), 00, pp. 5-43 Trends and Unit Roots in Greek Real Money Supply, Real GDP and Nominal Interest Rate Karpetis Christos & Varelas Erotokritos * Abstract This

The GARCH Analysis of YU EBAO Annual Yields Weiwei Guo1,a

2nd Workshop on Advanced Research and Technology in Industry Applications (WARTIA 2016) The GARCH Analysis of YU EBAO Annual Yields Weiwei Guo1,a 1 Longdong University,Qingyang,Gansu province,745000 a

2nd Workshop on Advanced Research and Technology in Industry Applications (WARTIA 2016) The GARCH Analysis of YU EBAO Annual Yields Weiwei Guo1,a 1 Longdong University,Qingyang,Gansu province,745000 a

Financial Deepening and Economic Growth in Nigeria: an Application of Cointegration and Causality Analysis

Financial Deepening and Economic Growth in Nigeria: an Application of Cointegration and Causality Analysis Torruam, J.T., Chiawa, M.A. and Abur, C.C. Abstract The study investigates the impact of financial

Financial Deepening and Economic Growth in Nigeria: an Application of Cointegration and Causality Analysis Torruam, J.T., Chiawa, M.A. and Abur, C.C. Abstract The study investigates the impact of financial

Frequency Forecasting using Time Series ARIMA model

Frequency Forecasting using Time Series ARIMA model Manish Kumar Tikariha DGM(O) NSPCL Bhilai Abstract In view of stringent regulatory stance and recent tariff guidelines, Deviation Settlement mechanism

Frequency Forecasting using Time Series ARIMA model Manish Kumar Tikariha DGM(O) NSPCL Bhilai Abstract In view of stringent regulatory stance and recent tariff guidelines, Deviation Settlement mechanism

in the time series. The relation between y and x is contemporaneous.

9 Regression with Time Series 9.1 Some Basic Concepts Static Models (1) y t = β 0 + β 1 x t + u t t = 1, 2,..., T, where T is the number of observation in the time series. The relation between y and x

9 Regression with Time Series 9.1 Some Basic Concepts Static Models (1) y t = β 0 + β 1 x t + u t t = 1, 2,..., T, where T is the number of observation in the time series. The relation between y and x

Goce Delcev University-Stip, Goce Delcev University-Stip

MPRA Munich Personal RePEc Archive The causal relationship between patent growth and growth of GDP with quarterly data in the G7 countries: cointegration, ARDL and error correction models Dushko Josheski

MPRA Munich Personal RePEc Archive The causal relationship between patent growth and growth of GDP with quarterly data in the G7 countries: cointegration, ARDL and error correction models Dushko Josheski

IS THERE A COINTEGRATION RELATIONSHIP BETWEEN ENERGY CONSUMPTION AND GDP IN IRAN?

IS THERE A COINTEGRATION RELATIONSHIP BETWEEN ENERGY CONSUMPTION AND GDP IN IRAN? Aliasghar Sadeghimojarad- Sina Mehrabirad Abstract This paper tries to unfold the linkage between energy consumption and

IS THERE A COINTEGRATION RELATIONSHIP BETWEEN ENERGY CONSUMPTION AND GDP IN IRAN? Aliasghar Sadeghimojarad- Sina Mehrabirad Abstract This paper tries to unfold the linkage between energy consumption and

Multivariate Time Series: Part 4

Multivariate Time Series: Part 4 Cointegration Gerald P. Dwyer Clemson University March 2016 Outline 1 Multivariate Time Series: Part 4 Cointegration Engle-Granger Test for Cointegration Johansen Test

Multivariate Time Series: Part 4 Cointegration Gerald P. Dwyer Clemson University March 2016 Outline 1 Multivariate Time Series: Part 4 Cointegration Engle-Granger Test for Cointegration Johansen Test

Applied Econometrics. Professor Bernard Fingleton

Applied Econometrics Professor Bernard Fingleton Regression A quick summary of some key issues Some key issues Text book JH Stock & MW Watson Introduction to Econometrics 2nd Edition Software Gretl Gretl.sourceforge.net

Applied Econometrics Professor Bernard Fingleton Regression A quick summary of some key issues Some key issues Text book JH Stock & MW Watson Introduction to Econometrics 2nd Edition Software Gretl Gretl.sourceforge.net