Time Series Analysis -- An Introduction -- AMS 586

|

|

|

- Marian Griffin

- 5 years ago

- Views:

Transcription

1 Time Series Analysis -- An Introduction -- AMS 586 1

2 Objectives of time series analysis Data description Data interpretation Modeling Control Prediction & Forecasting 2

3 Time-Series Data Numerical data obtained at regular time intervals The time intervals can be annually, quarterly, monthly, weekly, daily, hourly, etc. Example: Year: Sales:

4 Inflation Rate (%) Time Plot A time-series plot (time plot) is a twodimensional plot of time series data the vertical axis measures the variable of interest the horizontal axis corresponds to the time periods U.S. Inflation Rate 4 Year

5 Time-Series Components Time Series Trend Component Seasonal Component Cyclical Component Irregular /Random Component Overall, persistent, longterm movement Regular periodic fluctuations, usually within a 12-month period Repeating swings or movements over more than one year Erratic or residual fluctuations 5

6 Trend Component Long-run increase or decrease over time (overall upward or downward movement) Data taken over a long period of time Sales 6 Time

7 Trend Component (continued) Trend can be upward or downward Trend can be linear or non-linear Sales Sales Downward linear trend Time Upward nonlinear trend Time 7

8 Seasonal Component Short-term regular wave-like patterns Observed within 1 year Often monthly or quarterly Sales Winter Summer Winter Spring Summer Fall Spring Fall 8 Time (Quarterly)

9 Cyclical Component Long-term wave-like patterns Regularly occur but may vary in length Often measured peak to peak or trough to trough 1 Cycle Sales 9 Year

10 Irregular/Random Component Unpredictable, random, residual fluctuations Noise in the time series The truly irregular component may not be estimated however, the more predictable random component can be estimated and is usually the emphasis of time series analysis via the usual stationary time series models such as AR, MA, ARMA etc after we filter out the trend, seasonal and other cyclical components 10

11 Two simplified time series models In the following, we present two classes of simplified time series models 1. Non-seasonal Model with Trend 2. Classical Decomposition Model with Trend and Seasonal Components The usual procedure is to first filter out the trend and seasonal component then fit the random component with a stationary time series model to capture the correlation structure in the time series If necessary, the entire time series (with seasonal, trend, and random components) can be re-analyzed for better estimation, modeling and prediction. 11

12 Non-seasonal Models with Trend X t = m t + Y t Stochastic process trend random noise 12

13 Classical Decomposition Model with Trend and Season X t = m t + s t + Y t Stochastic process trend seasonal component random noise 13

14 Non-seasonal Models with Trend There are two basic methods for estimating/eliminating trend: Method 1: Trend estimation (first we estimate the trend either by moving average smoothing or regression analysis then we remove it) Method 2: Trend elimination by differencing 14

15 Method 1: Trend Estimation by Regression Analysis Estimate a trend line using regression analysis Year Time Period (t) Sales (X) Use time (t) as the independent variable: In least squares linear, non-linear, and exponential modeling, time periods are numbered starting with 0 and increasing by 1 for each time period

16 sales Least Squares Regression Without knowing the exact time series random error correlation structure, one often resorts to the ordinary least squares regression method, not optimal but practical. Year Time Period (t) Sales (X) The estimated linear trend equation is: Sales trend Year

17 sales Linear Trend Forecasting One can even performs trend forecasting at this point but bear in mind that the forecasting may not be optimal. Forecast for time period 6 (2010): Year Time Period (t) Sales (X) ?? Sales trend Year 17

18 Method 2: Trend Elimination by Differencing 18

19 Trend Elimination by Differencing If the operator is applied to a linear trend function: Then we obtain the constant function: In the same way any polynomial trend of degree k can be removed by the operator: 19

20 Classical Decomposition Model (Seasonal Model) with trend and season where 20

21 Classical Decomposition Model Method 1: Filtering: First we estimate and remove the trend component by using moving average method; then we estimate and remove the seasonal component by using suitable periodic averages. Method 2: Differencing: First we remove the seasonal component by differencing. We then remove the trend by differencing as well. Method 3: Joint-fit method: Alternatively, we can fit a combined polynomial linear regression and harmonic functions to estimate and then remove the trend and seasonal component simultaneously as the following: 21

22 Method 1: Filtering (1). We first estimate the trend by the moving average: If d = 2q (even), we use: If d = 2q+1 (odd), we use: (2). Then we estimate the seasonal component by using the average, k = 1,, d, of the de-trended data: To ensure: we further subtract the mean of (3). One can also re-analyze the trend from the de-seasonalized data in order to obtain a polynomial linear regression equation for modeling and prediction 22 purposes.

23 Method 2: Differencing Define the lag-d differencing operator as: We can transform a seasonal model to a non-seasonal model: Differencing method can then be further applied to eliminate the trend component. 23

24 Method 3: Joint Modeling As shown before, one can also fit a joint model to analyze both components simultaneously: 24

25 Detrended series 25 P. J. Brockwell, R. A. Davis, Introduction to Time Series and Forecasting, Springer, 1987

26 Time series Realization of a stochastic process {X t } is a stochastic time series if each component takes a value according to a certain probability distribution function. A time series model specifies the joint distribution of the sequence of random variables. 26

27 White noise - example of a time series model 27

28 28 Gaussian white noise

29 Stochastic properties of the process STATIONARITY Once we have removed the seasonal and trend.1 components of a time series (as in the classical decomposition model), the remainder (random) component the residual, can often be modeled by a stationary time series. * System does not change its properties in time * Well-developed analytical methods of signal analysis and stochastic processes 29

30 WHEN A STOCHASTIC PROCESS IS STATIONARY? {X t } is a strictly stationary time series if f(x 1,...,X n )= f(x 1+h,...,X n+h ), where n 1, h integer Properties: * The random variables are identically distributed. * An idependent identically distributed (iid) sequence is strictly stationary. 30

31 Weak stationarity {X t } is a weakly stationary time series if EX t = and Var(X t ) = 2 are independent of time t Cov(X s, X r ) depends on (s-r) only, independent of t 31

32 32 Autocorrelation function (ACF)

33 33 ACF for Gaussian WN

34 ARMA models Time series is an ARMA(p,q) process if X t is stationary and if for every t: X t 1 X t-1... p X t-p = Z t + 1 Z t p Z t-p where Z t represents white noise with mean 0 and variance 2 The Left side of the equation represents the Autoregressive AR(p) part, and the right side the Moving Average MA(q) component. 34

35 35 Examples

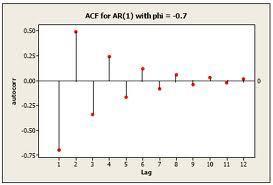

36 Exponential decay of ACF MA(1) sample ACF AR(1) 36

37 37 More examples of ACF

38 Reference Box, George and Jenkins, Gwilym (1970) Time series analysis: Forecasting and control, San Francisco: Holden-Day. Brockwell, Peter J. and Davis, Richard A. (1991). Time Series: Theory and Methods. Springer-Verlag. Brockwell, Peter J. and Davis, Richard A. (1987, 2002). Introduction to Time Series and Forecasting. Springer. We also thank various on-line open resources for time series analysis. 38

Statistics of stochastic processes

Introduction Statistics of stochastic processes Generally statistics is performed on observations y 1,..., y n assumed to be realizations of independent random variables Y 1,..., Y n. 14 settembre 2014

Introduction Statistics of stochastic processes Generally statistics is performed on observations y 1,..., y n assumed to be realizations of independent random variables Y 1,..., Y n. 14 settembre 2014

Time Series and Forecasting

Time Series and Forecasting Introduction to Forecasting n What is forecasting? n Primary Function is to Predict the Future using (time series related or other) data we have in hand n Why are we interested?

Time Series and Forecasting Introduction to Forecasting n What is forecasting? n Primary Function is to Predict the Future using (time series related or other) data we have in hand n Why are we interested?

Lesson 13: Box-Jenkins Modeling Strategy for building ARMA models

Lesson 13: Box-Jenkins Modeling Strategy for building ARMA models Facoltà di Economia Università dell Aquila umberto.triacca@gmail.com Introduction In this lesson we present a method to construct an ARMA(p,

Lesson 13: Box-Jenkins Modeling Strategy for building ARMA models Facoltà di Economia Università dell Aquila umberto.triacca@gmail.com Introduction In this lesson we present a method to construct an ARMA(p,

Time Series and Forecasting

Time Series and Forecasting Introduction to Forecasting n What is forecasting? n Primary Function is to Predict the Future using (time series related or other) data we have in hand n Why are we interested?

Time Series and Forecasting Introduction to Forecasting n What is forecasting? n Primary Function is to Predict the Future using (time series related or other) data we have in hand n Why are we interested?

Part II. Time Series

Part II Time Series 12 Introduction This Part is mainly a summary of the book of Brockwell and Davis (2002). Additionally the textbook Shumway and Stoffer (2010) can be recommended. 1 Our purpose is to

Part II Time Series 12 Introduction This Part is mainly a summary of the book of Brockwell and Davis (2002). Additionally the textbook Shumway and Stoffer (2010) can be recommended. 1 Our purpose is to

Econometría 2: Análisis de series de Tiempo

Econometría 2: Análisis de series de Tiempo Karoll GOMEZ kgomezp@unal.edu.co http://karollgomez.wordpress.com Segundo semestre 2016 II. Basic definitions A time series is a set of observations X t, each

Econometría 2: Análisis de series de Tiempo Karoll GOMEZ kgomezp@unal.edu.co http://karollgomez.wordpress.com Segundo semestre 2016 II. Basic definitions A time series is a set of observations X t, each

Forecasting. Simon Shaw 2005/06 Semester II

Forecasting Simon Shaw s.c.shaw@maths.bath.ac.uk 2005/06 Semester II 1 Introduction A critical aspect of managing any business is planning for the future. events is called forecasting. Predicting future

Forecasting Simon Shaw s.c.shaw@maths.bath.ac.uk 2005/06 Semester II 1 Introduction A critical aspect of managing any business is planning for the future. events is called forecasting. Predicting future

at least 50 and preferably 100 observations should be available to build a proper model

III Box-Jenkins Methods 1. Pros and Cons of ARIMA Forecasting a) need for data at least 50 and preferably 100 observations should be available to build a proper model used most frequently for hourly or

III Box-Jenkins Methods 1. Pros and Cons of ARIMA Forecasting a) need for data at least 50 and preferably 100 observations should be available to build a proper model used most frequently for hourly or

Time Series I Time Domain Methods

Astrostatistics Summer School Penn State University University Park, PA 16802 May 21, 2007 Overview Filtering and the Likelihood Function Time series is the study of data consisting of a sequence of DEPENDENT

Astrostatistics Summer School Penn State University University Park, PA 16802 May 21, 2007 Overview Filtering and the Likelihood Function Time series is the study of data consisting of a sequence of DEPENDENT

Stochastic Processes

Stochastic Processes Stochastic Process Non Formal Definition: Non formal: A stochastic process (random process) is the opposite of a deterministic process such as one defined by a differential equation.

Stochastic Processes Stochastic Process Non Formal Definition: Non formal: A stochastic process (random process) is the opposite of a deterministic process such as one defined by a differential equation.

Econ 424 Time Series Concepts

Econ 424 Time Series Concepts Eric Zivot January 20 2015 Time Series Processes Stochastic (Random) Process { 1 2 +1 } = { } = sequence of random variables indexed by time Observed time series of length

Econ 424 Time Series Concepts Eric Zivot January 20 2015 Time Series Processes Stochastic (Random) Process { 1 2 +1 } = { } = sequence of random variables indexed by time Observed time series of length

ESSE Mid-Term Test 2017 Tuesday 17 October :30-09:45

ESSE 4020 3.0 - Mid-Term Test 207 Tuesday 7 October 207. 08:30-09:45 Symbols have their usual meanings. All questions are worth 0 marks, although some are more difficult than others. Answer as many questions

ESSE 4020 3.0 - Mid-Term Test 207 Tuesday 7 October 207. 08:30-09:45 Symbols have their usual meanings. All questions are worth 0 marks, although some are more difficult than others. Answer as many questions

Basics: Definitions and Notation. Stationarity. A More Formal Definition

Basics: Definitions and Notation A Univariate is a sequence of measurements of the same variable collected over (usually regular intervals of) time. Usual assumption in many time series techniques is that

Basics: Definitions and Notation A Univariate is a sequence of measurements of the same variable collected over (usually regular intervals of) time. Usual assumption in many time series techniques is that

Some Time-Series Models

Some Time-Series Models Outline 1. Stochastic processes and their properties 2. Stationary processes 3. Some properties of the autocorrelation function 4. Some useful models Purely random processes, random

Some Time-Series Models Outline 1. Stochastic processes and their properties 2. Stationary processes 3. Some properties of the autocorrelation function 4. Some useful models Purely random processes, random

Applied time-series analysis

Robert M. Kunst robert.kunst@univie.ac.at University of Vienna and Institute for Advanced Studies Vienna October 18, 2011 Outline Introduction and overview Econometric Time-Series Analysis In principle,

Robert M. Kunst robert.kunst@univie.ac.at University of Vienna and Institute for Advanced Studies Vienna October 18, 2011 Outline Introduction and overview Econometric Time-Series Analysis In principle,

{ } Stochastic processes. Models for time series. Specification of a process. Specification of a process. , X t3. ,...X tn }

Stochastic processes Time series are an example of a stochastic or random process Models for time series A stochastic process is 'a statistical phenomenon that evolves in time according to probabilistic

Stochastic processes Time series are an example of a stochastic or random process Models for time series A stochastic process is 'a statistical phenomenon that evolves in time according to probabilistic

Time Series Outlier Detection

Time Series Outlier Detection Tingyi Zhu July 28, 2016 Tingyi Zhu Time Series Outlier Detection July 28, 2016 1 / 42 Outline Time Series Basics Outliers Detection in Single Time Series Outlier Series Detection

Time Series Outlier Detection Tingyi Zhu July 28, 2016 Tingyi Zhu Time Series Outlier Detection July 28, 2016 1 / 42 Outline Time Series Basics Outliers Detection in Single Time Series Outlier Series Detection

3. ARMA Modeling. Now: Important class of stationary processes

3. ARMA Modeling Now: Important class of stationary processes Definition 3.1: (ARMA(p, q) process) Let {ɛ t } t Z WN(0, σ 2 ) be a white noise process. The process {X t } t Z is called AutoRegressive-Moving-Average

3. ARMA Modeling Now: Important class of stationary processes Definition 3.1: (ARMA(p, q) process) Let {ɛ t } t Z WN(0, σ 2 ) be a white noise process. The process {X t } t Z is called AutoRegressive-Moving-Average

2. An Introduction to Moving Average Models and ARMA Models

. An Introduction to Moving Average Models and ARMA Models.1 White Noise. The MA(1) model.3 The MA(q) model..4 Estimation and forecasting of MA models..5 ARMA(p,q) models. The Moving Average (MA) models

. An Introduction to Moving Average Models and ARMA Models.1 White Noise. The MA(1) model.3 The MA(q) model..4 Estimation and forecasting of MA models..5 ARMA(p,q) models. The Moving Average (MA) models

STAT 443 Final Exam Review. 1 Basic Definitions. 2 Statistical Tests. L A TEXer: W. Kong

STAT 443 Final Exam Review L A TEXer: W Kong 1 Basic Definitions Definition 11 The time series {X t } with E[X 2 t ] < is said to be weakly stationary if: 1 µ X (t) = E[X t ] is independent of t 2 γ X

STAT 443 Final Exam Review L A TEXer: W Kong 1 Basic Definitions Definition 11 The time series {X t } with E[X 2 t ] < is said to be weakly stationary if: 1 µ X (t) = E[X t ] is independent of t 2 γ X

Classic Time Series Analysis

Classic Time Series Analysis Concepts and Definitions Let Y be a random number with PDF f Y t ~f,t Define t =E[Y t ] m(t) is known as the trend Define the autocovariance t, s =COV [Y t,y s ] =E[ Y t t

Classic Time Series Analysis Concepts and Definitions Let Y be a random number with PDF f Y t ~f,t Define t =E[Y t ] m(t) is known as the trend Define the autocovariance t, s =COV [Y t,y s ] =E[ Y t t

Minitab Project Report - Assignment 6

.. Sunspot data Minitab Project Report - Assignment Time Series Plot of y Time Series Plot of X y X 7 9 7 9 The data have a wavy pattern. However, they do not show any seasonality. There seem to be an

.. Sunspot data Minitab Project Report - Assignment Time Series Plot of y Time Series Plot of X y X 7 9 7 9 The data have a wavy pattern. However, they do not show any seasonality. There seem to be an

Chapter 3: Regression Methods for Trends

Chapter 3: Regression Methods for Trends Time series exhibiting trends over time have a mean function that is some simple function (not necessarily constant) of time. The example random walk graph from

Chapter 3: Regression Methods for Trends Time series exhibiting trends over time have a mean function that is some simple function (not necessarily constant) of time. The example random walk graph from

LECTURES 2-3 : Stochastic Processes, Autocorrelation function. Stationarity.

LECTURES 2-3 : Stochastic Processes, Autocorrelation function. Stationarity. Important points of Lecture 1: A time series {X t } is a series of observations taken sequentially over time: x t is an observation

LECTURES 2-3 : Stochastic Processes, Autocorrelation function. Stationarity. Important points of Lecture 1: A time series {X t } is a series of observations taken sequentially over time: x t is an observation

MODELING INFLATION RATES IN NIGERIA: BOX-JENKINS APPROACH. I. U. Moffat and A. E. David Department of Mathematics & Statistics, University of Uyo, Uyo

Vol.4, No.2, pp.2-27, April 216 MODELING INFLATION RATES IN NIGERIA: BOX-JENKINS APPROACH I. U. Moffat and A. E. David Department of Mathematics & Statistics, University of Uyo, Uyo ABSTRACT: This study

Vol.4, No.2, pp.2-27, April 216 MODELING INFLATION RATES IN NIGERIA: BOX-JENKINS APPROACH I. U. Moffat and A. E. David Department of Mathematics & Statistics, University of Uyo, Uyo ABSTRACT: This study

3 Time Series Regression

3 Time Series Regression 3.1 Modelling Trend Using Regression Random Walk 2 0 2 4 6 8 Random Walk 0 2 4 6 8 0 10 20 30 40 50 60 (a) Time 0 10 20 30 40 50 60 (b) Time Random Walk 8 6 4 2 0 Random Walk 0

3 Time Series Regression 3.1 Modelling Trend Using Regression Random Walk 2 0 2 4 6 8 Random Walk 0 2 4 6 8 0 10 20 30 40 50 60 (a) Time 0 10 20 30 40 50 60 (b) Time Random Walk 8 6 4 2 0 Random Walk 0

Problem Set 2 Solution Sketches Time Series Analysis Spring 2010

Problem Set 2 Solution Sketches Time Series Analysis Spring 2010 Forecasting 1. Let X and Y be two random variables such that E(X 2 ) < and E(Y 2 )

Problem Set 2 Solution Sketches Time Series Analysis Spring 2010 Forecasting 1. Let X and Y be two random variables such that E(X 2 ) < and E(Y 2 )

A time series is called strictly stationary if the joint distribution of every collection (Y t

5 Time series A time series is a set of observations recorded over time. You can think for example at the GDP of a country over the years (or quarters) or the hourly measurements of temperature over a

5 Time series A time series is a set of observations recorded over time. You can think for example at the GDP of a country over the years (or quarters) or the hourly measurements of temperature over a

Empirical Market Microstructure Analysis (EMMA)

") Empirical Market Microstructure Analysis (EMMA) Lecture 3: Statistical Building Blocks and Econometric Basics Prof. Dr. Michael Stein michael.stein@vwl.uni-freiburg.de Albert-Ludwigs-University of Freiburg

Empirical Market Microstructure Analysis (EMMA) Lecture 3: Statistical Building Blocks and Econometric Basics Prof. Dr. Michael Stein michael.stein@vwl.uni-freiburg.de Albert-Ludwigs-University of Freiburg

Module 3. Descriptive Time Series Statistics and Introduction to Time Series Models

Module 3 Descriptive Time Series Statistics and Introduction to Time Series Models Class notes for Statistics 451: Applied Time Series Iowa State University Copyright 2015 W Q Meeker November 11, 2015

Module 3 Descriptive Time Series Statistics and Introduction to Time Series Models Class notes for Statistics 451: Applied Time Series Iowa State University Copyright 2015 W Q Meeker November 11, 2015

Stat 248 Lab 2: Stationarity, More EDA, Basic TS Models

Stat 248 Lab 2: Stationarity, More EDA, Basic TS Models Tessa L. Childers-Day February 8, 2013 1 Introduction Today s section will deal with topics such as: the mean function, the auto- and cross-covariance

Stat 248 Lab 2: Stationarity, More EDA, Basic TS Models Tessa L. Childers-Day February 8, 2013 1 Introduction Today s section will deal with topics such as: the mean function, the auto- and cross-covariance

Lecture 3: Autoregressive Moving Average (ARMA) Models and their Practical Applications

Models and their Practical Applications") Lecture 3: Autoregressive Moving Average (ARMA) Models and their Practical Applications Prof. Massimo Guidolin 20192 Financial Econometrics Winter/Spring 2018 Overview Moving average processes Autoregressive

Lecture 3: Autoregressive Moving Average (ARMA) Models and their Practical Applications Prof. Massimo Guidolin 20192 Financial Econometrics Winter/Spring 2018 Overview Moving average processes Autoregressive

FORECASTING SUGARCANE PRODUCTION IN INDIA WITH ARIMA MODEL

FORECASTING SUGARCANE PRODUCTION IN INDIA WITH ARIMA MODEL B. N. MANDAL Abstract: Yearly sugarcane production data for the period of - to - of India were analyzed by time-series methods. Autocorrelation

FORECASTING SUGARCANE PRODUCTION IN INDIA WITH ARIMA MODEL B. N. MANDAL Abstract: Yearly sugarcane production data for the period of - to - of India were analyzed by time-series methods. Autocorrelation

Stochastic Processes: I. consider bowl of worms model for oscilloscope experiment:

Stochastic Processes: I consider bowl of worms model for oscilloscope experiment: SAPAscope 2.0 / 0 1 RESET SAPA2e 22, 23 II 1 stochastic process is: Stochastic Processes: II informally: bowl + drawing

Stochastic Processes: I consider bowl of worms model for oscilloscope experiment: SAPAscope 2.0 / 0 1 RESET SAPA2e 22, 23 II 1 stochastic process is: Stochastic Processes: II informally: bowl + drawing

The autocorrelation and autocovariance functions - helpful tools in the modelling problem

The autocorrelation and autocovariance functions - helpful tools in the modelling problem J. Nowicka-Zagrajek A. Wy lomańska Institute of Mathematics and Computer Science Wroc law University of Technology,

The autocorrelation and autocovariance functions - helpful tools in the modelling problem J. Nowicka-Zagrajek A. Wy lomańska Institute of Mathematics and Computer Science Wroc law University of Technology,

Time Series Analysis - Part 1

Time Series Analysis - Part 1 Dr. Esam Mahdi Islamic University of Gaza - Department of Mathematics April 19, 2017 1 of 189 What is a Time Series? Fundamental concepts Time Series Decomposition Estimating

Time Series Analysis - Part 1 Dr. Esam Mahdi Islamic University of Gaza - Department of Mathematics April 19, 2017 1 of 189 What is a Time Series? Fundamental concepts Time Series Decomposition Estimating

AR, MA and ARMA models

AR, MA and AR by Hedibert Lopes P Based on Tsay s Analysis of Financial Time Series (3rd edition) P 1 Stationarity 2 3 4 5 6 7 P 8 9 10 11 Outline P Linear Time Series Analysis and Its Applications For

AR, MA and AR by Hedibert Lopes P Based on Tsay s Analysis of Financial Time Series (3rd edition) P 1 Stationarity 2 3 4 5 6 7 P 8 9 10 11 Outline P Linear Time Series Analysis and Its Applications For

Prof. Dr. Roland Füss Lecture Series in Applied Econometrics Summer Term Introduction to Time Series Analysis

Introduction to Time Series Analysis 1 Contents: I. Basics of Time Series Analysis... 4 I.1 Stationarity... 5 I.2 Autocorrelation Function... 9 I.3 Partial Autocorrelation Function (PACF)... 14 I.4 Transformation

Introduction to Time Series Analysis 1 Contents: I. Basics of Time Series Analysis... 4 I.1 Stationarity... 5 I.2 Autocorrelation Function... 9 I.3 Partial Autocorrelation Function (PACF)... 14 I.4 Transformation

STAT 520: Forecasting and Time Series. David B. Hitchcock University of South Carolina Department of Statistics

David B. University of South Carolina Department of Statistics What are Time Series Data? Time series data are collected sequentially over time. Some common examples include: 1. Meteorological data (temperatures,

David B. University of South Carolina Department of Statistics What are Time Series Data? Time series data are collected sequentially over time. Some common examples include: 1. Meteorological data (temperatures,

MCMC analysis of classical time series algorithms.

MCMC analysis of classical time series algorithms. mbalawata@yahoo.com Lappeenranta University of Technology Lappeenranta, 19.03.2009 Outline Introduction 1 Introduction 2 3 Series generation Box-Jenkins

MCMC analysis of classical time series algorithms. mbalawata@yahoo.com Lappeenranta University of Technology Lappeenranta, 19.03.2009 Outline Introduction 1 Introduction 2 3 Series generation Box-Jenkins

A SEASONAL TIME SERIES MODEL FOR NIGERIAN MONTHLY AIR TRAFFIC DATA

www.arpapress.com/volumes/vol14issue3/ijrras_14_3_14.pdf A SEASONAL TIME SERIES MODEL FOR NIGERIAN MONTHLY AIR TRAFFIC DATA Ette Harrison Etuk Department of Mathematics/Computer Science, Rivers State University

www.arpapress.com/volumes/vol14issue3/ijrras_14_3_14.pdf A SEASONAL TIME SERIES MODEL FOR NIGERIAN MONTHLY AIR TRAFFIC DATA Ette Harrison Etuk Department of Mathematics/Computer Science, Rivers State University

Analysis. Components of a Time Series

Module 8: Time Series Analysis 8.2 Components of a Time Series, Detection of Change Points and Trends, Time Series Models Components of a Time Series There can be several things happening simultaneously

Module 8: Time Series Analysis 8.2 Components of a Time Series, Detection of Change Points and Trends, Time Series Models Components of a Time Series There can be several things happening simultaneously

Time Series 4. Robert Almgren. Oct. 5, 2009

Time Series 4 Robert Almgren Oct. 5, 2009 1 Nonstationarity How should you model a process that has drift? ARMA models are intrinsically stationary, that is, they are mean-reverting: when the value of

Time Series 4 Robert Almgren Oct. 5, 2009 1 Nonstationarity How should you model a process that has drift? ARMA models are intrinsically stationary, that is, they are mean-reverting: when the value of

Gaussian processes. Basic Properties VAG002-

Gaussian processes The class of Gaussian processes is one of the most widely used families of stochastic processes for modeling dependent data observed over time, or space, or time and space. The popularity

Gaussian processes The class of Gaussian processes is one of the most widely used families of stochastic processes for modeling dependent data observed over time, or space, or time and space. The popularity

Based on the original slides from Levine, et. all, First Edition, Prentice Hall, Inc

Based on the original slides from Levine, et. all, First Edition, Prentice Hall, Inc Process of predicting a future event Underlying basis of all business decisions Production Inventory Personnel Facilities

Based on the original slides from Levine, et. all, First Edition, Prentice Hall, Inc Process of predicting a future event Underlying basis of all business decisions Production Inventory Personnel Facilities

11. Further Issues in Using OLS with TS Data

11. Further Issues in Using OLS with TS Data With TS, including lags of the dependent variable often allow us to fit much better the variation in y Exact distribution theory is rarely available in TS applications,

11. Further Issues in Using OLS with TS Data With TS, including lags of the dependent variable often allow us to fit much better the variation in y Exact distribution theory is rarely available in TS applications,

TIME SERIES DATA PREDICTION OF NATURAL GAS CONSUMPTION USING ARIMA MODEL

International Journal of Information Technology & Management Information System (IJITMIS) Volume 7, Issue 3, Sep-Dec-2016, pp. 01 07, Article ID: IJITMIS_07_03_001 Available online at http://www.iaeme.com/ijitmis/issues.asp?jtype=ijitmis&vtype=7&itype=3

International Journal of Information Technology & Management Information System (IJITMIS) Volume 7, Issue 3, Sep-Dec-2016, pp. 01 07, Article ID: IJITMIS_07_03_001 Available online at http://www.iaeme.com/ijitmis/issues.asp?jtype=ijitmis&vtype=7&itype=3

Estimation and application of best ARIMA model for forecasting the uranium price.

Estimation and application of best ARIMA model for forecasting the uranium price. Medeu Amangeldi May 13, 2018 Capstone Project Superviser: Dongming Wei Second reader: Zhenisbek Assylbekov Abstract This

Estimation and application of best ARIMA model for forecasting the uranium price. Medeu Amangeldi May 13, 2018 Capstone Project Superviser: Dongming Wei Second reader: Zhenisbek Assylbekov Abstract This

1. Fundamental concepts

. Fundamental concepts A time series is a sequence of data points, measured typically at successive times spaced at uniform intervals. Time series are used in such fields as statistics, signal processing

. Fundamental concepts A time series is a sequence of data points, measured typically at successive times spaced at uniform intervals. Time series are used in such fields as statistics, signal processing

V3: Circadian rhythms, time-series analysis (contd )

") V3: Circadian rhythms, time-series analysis (contd ) Introduction: 5 paragraphs (1) Insufficient sleep - Biological/medical relevance (2) Previous work on effects of insufficient sleep in rodents (dt.

V3: Circadian rhythms, time-series analysis (contd ) Introduction: 5 paragraphs (1) Insufficient sleep - Biological/medical relevance (2) Previous work on effects of insufficient sleep in rodents (dt.

Lecture 19 Box-Jenkins Seasonal Models

Lecture 19 Box-Jenkins Seasonal Models If the time series is nonstationary with respect to its variance, then we can stabilize the variance of the time series by using a pre-differencing transformation.

Lecture 19 Box-Jenkins Seasonal Models If the time series is nonstationary with respect to its variance, then we can stabilize the variance of the time series by using a pre-differencing transformation.

5 Autoregressive-Moving-Average Modeling

5 Autoregressive-Moving-Average Modeling 5. Purpose. Autoregressive-moving-average (ARMA models are mathematical models of the persistence, or autocorrelation, in a time series. ARMA models are widely

5 Autoregressive-Moving-Average Modeling 5. Purpose. Autoregressive-moving-average (ARMA models are mathematical models of the persistence, or autocorrelation, in a time series. ARMA models are widely

Time Series: Theory and Methods

Peter J. Brockwell Richard A. Davis Time Series: Theory and Methods Second Edition With 124 Illustrations Springer Contents Preface to the Second Edition Preface to the First Edition vn ix CHAPTER 1 Stationary

Peter J. Brockwell Richard A. Davis Time Series: Theory and Methods Second Edition With 124 Illustrations Springer Contents Preface to the Second Edition Preface to the First Edition vn ix CHAPTER 1 Stationary

Econ 300/QAC 201: Quantitative Methods in Economics/Applied Data Analysis. 17th Class 7/1/10

Econ 300/QAC 201: Quantitative Methods in Economics/Applied Data Analysis 17th Class 7/1/10 The only function of economic forecasting is to make astrology look respectable. --John Kenneth Galbraith show

Econ 300/QAC 201: Quantitative Methods in Economics/Applied Data Analysis 17th Class 7/1/10 The only function of economic forecasting is to make astrology look respectable. --John Kenneth Galbraith show

γ 0 = Var(X i ) = Var(φ 1 X i 1 +W i ) = φ 2 1γ 0 +σ 2, which implies that we must have φ 1 < 1, and γ 0 = σ2 . 1 φ 2 1 We may also calculate for j 1

= Var(φ 1 X i 1 +W i ) = φ 2 1γ 0 +σ 2, which implies that we must have φ 1 < 1, and γ 0 = σ2 . 1 φ 2 1 We may also calculate for j 1") 4.2 Autoregressive (AR) Moving average models are causal linear processes by definition. There is another class of models, based on a recursive formulation similar to the exponentially weighted moving

4.2 Autoregressive (AR) Moving average models are causal linear processes by definition. There is another class of models, based on a recursive formulation similar to the exponentially weighted moving

Time Series Models and Inference. James L. Powell Department of Economics University of California, Berkeley

Time Series Models and Inference James L. Powell Department of Economics University of California, Berkeley Overview In contrast to the classical linear regression model, in which the components of the

Time Series Models and Inference James L. Powell Department of Economics University of California, Berkeley Overview In contrast to the classical linear regression model, in which the components of the

Introduction to Stochastic processes

Università di Pavia Introduction to Stochastic processes Eduardo Rossi Stochastic Process Stochastic Process: A stochastic process is an ordered sequence of random variables defined on a probability space

Università di Pavia Introduction to Stochastic processes Eduardo Rossi Stochastic Process Stochastic Process: A stochastic process is an ordered sequence of random variables defined on a probability space

Reliability and Risk Analysis. Time Series, Types of Trend Functions and Estimates of Trends

Reliability and Risk Analysis Stochastic process The sequence of random variables {Y t, t = 0, ±1, ±2 } is called the stochastic process The mean function of a stochastic process {Y t} is the function

Reliability and Risk Analysis Stochastic process The sequence of random variables {Y t, t = 0, ±1, ±2 } is called the stochastic process The mean function of a stochastic process {Y t} is the function

Exercises - Time series analysis

Descriptive analysis of a time series (1) Estimate the trend of the series of gasoline consumption in Spain using a straight line in the period from 1945 to 1995 and generate forecasts for 24 months. Compare

Descriptive analysis of a time series (1) Estimate the trend of the series of gasoline consumption in Spain using a straight line in the period from 1945 to 1995 and generate forecasts for 24 months. Compare

EASTERN MEDITERRANEAN UNIVERSITY ECON 604, FALL 2007 DEPARTMENT OF ECONOMICS MEHMET BALCILAR ARIMA MODELS: IDENTIFICATION

ARIMA MODELS: IDENTIFICATION A. Autocorrelations and Partial Autocorrelations 1. Summary of What We Know So Far: a) Series y t is to be modeled by Box-Jenkins methods. The first step was to convert y t

ARIMA MODELS: IDENTIFICATION A. Autocorrelations and Partial Autocorrelations 1. Summary of What We Know So Far: a) Series y t is to be modeled by Box-Jenkins methods. The first step was to convert y t

Time series analysis of activity and temperature data of four healthy individuals

Time series analysis of activity and temperature data of four healthy individuals B.Hadj-Amar N.Cunningham S.Ip March 11, 2016 B.Hadj-Amar, N.Cunningham, S.Ip Time Series Analysis March 11, 2016 1 / 26

Time series analysis of activity and temperature data of four healthy individuals B.Hadj-Amar N.Cunningham S.Ip March 11, 2016 B.Hadj-Amar, N.Cunningham, S.Ip Time Series Analysis March 11, 2016 1 / 26

Discrete time processes

Discrete time processes Predictions are difficult. Especially about the future Mark Twain. Florian Herzog 2013 Modeling observed data When we model observed (realized) data, we encounter usually the following

Discrete time processes Predictions are difficult. Especially about the future Mark Twain. Florian Herzog 2013 Modeling observed data When we model observed (realized) data, we encounter usually the following

Time-Series Analysis. Dr. Seetha Bandara Dept. of Economics MA_ECON

Time-Series Analysis Dr. Seetha Bandara Dept. of Economics MA_ECON Time Series Patterns A time series is a sequence of observations on a variable measured at successive points in time or over successive

Time-Series Analysis Dr. Seetha Bandara Dept. of Economics MA_ECON Time Series Patterns A time series is a sequence of observations on a variable measured at successive points in time or over successive

Time Series 2. Robert Almgren. Sept. 21, 2009

Time Series 2 Robert Almgren Sept. 21, 2009 This week we will talk about linear time series models: AR, MA, ARMA, ARIMA, etc. First we will talk about theory and after we will talk about fitting the models

Time Series 2 Robert Almgren Sept. 21, 2009 This week we will talk about linear time series models: AR, MA, ARMA, ARIMA, etc. First we will talk about theory and after we will talk about fitting the models

Modelling Monthly Rainfall Data of Port Harcourt, Nigeria by Seasonal Box-Jenkins Methods

International Journal of Sciences Research Article (ISSN 2305-3925) Volume 2, Issue July 2013 http://www.ijsciences.com Modelling Monthly Rainfall Data of Port Harcourt, Nigeria by Seasonal Box-Jenkins

International Journal of Sciences Research Article (ISSN 2305-3925) Volume 2, Issue July 2013 http://www.ijsciences.com Modelling Monthly Rainfall Data of Port Harcourt, Nigeria by Seasonal Box-Jenkins

Ross Bettinger, Analytical Consultant, Seattle, WA

ABSTRACT DYNAMIC REGRESSION IN ARIMA MODELING Ross Bettinger, Analytical Consultant, Seattle, WA Box-Jenkins time series models that contain exogenous predictor variables are called dynamic regression

ABSTRACT DYNAMIC REGRESSION IN ARIMA MODELING Ross Bettinger, Analytical Consultant, Seattle, WA Box-Jenkins time series models that contain exogenous predictor variables are called dynamic regression

Autoregressive Moving Average (ARMA) Models and their Practical Applications

Models and their Practical Applications") Autoregressive Moving Average (ARMA) Models and their Practical Applications Massimo Guidolin February 2018 1 Essential Concepts in Time Series Analysis 1.1 Time Series and Their Properties Time series:

Autoregressive Moving Average (ARMA) Models and their Practical Applications Massimo Guidolin February 2018 1 Essential Concepts in Time Series Analysis 1.1 Time Series and Their Properties Time series:

Lesson 9: Autoregressive-Moving Average (ARMA) models

models") Lesson 9: Autoregressive-Moving Average (ARMA) models Dipartimento di Ingegneria e Scienze dell Informazione e Matematica Università dell Aquila, umberto.triacca@ec.univaq.it Introduction We have seen

Lesson 9: Autoregressive-Moving Average (ARMA) models Dipartimento di Ingegneria e Scienze dell Informazione e Matematica Università dell Aquila, umberto.triacca@ec.univaq.it Introduction We have seen

ITSM-R Reference Manual

ITSM-R Reference Manual George Weigt February 11, 2018 1 Contents 1 Introduction 3 1.1 Time series analysis in a nutshell............................... 3 1.2 White Noise Variance.....................................

ITSM-R Reference Manual George Weigt February 11, 2018 1 Contents 1 Introduction 3 1.1 Time series analysis in a nutshell............................... 3 1.2 White Noise Variance.....................................

Review Session: Econometrics - CLEFIN (20192)

") Review Session: Econometrics - CLEFIN (20192) Part II: Univariate time series analysis Daniele Bianchi March 20, 2013 Fundamentals Stationarity A time series is a sequence of random variables x t, t =

Review Session: Econometrics - CLEFIN (20192) Part II: Univariate time series analysis Daniele Bianchi March 20, 2013 Fundamentals Stationarity A time series is a sequence of random variables x t, t =

STAT 248: EDA & Stationarity Handout 3

STAT 248: EDA & Stationarity Handout 3 GSI: Gido van de Ven September 17th, 2010 1 Introduction Today s section we will deal with the following topics: the mean function, the auto- and crosscovariance

STAT 248: EDA & Stationarity Handout 3 GSI: Gido van de Ven September 17th, 2010 1 Introduction Today s section we will deal with the following topics: the mean function, the auto- and crosscovariance

Univariate, Nonstationary Processes

Univariate, Nonstationary Processes Jamie Monogan University of Georgia March 20, 2018 Jamie Monogan (UGA) Univariate, Nonstationary Processes March 20, 2018 1 / 14 Objectives By the end of this meeting,

Univariate, Nonstationary Processes Jamie Monogan University of Georgia March 20, 2018 Jamie Monogan (UGA) Univariate, Nonstationary Processes March 20, 2018 1 / 14 Objectives By the end of this meeting,

Lecture 1: Fundamental concepts in Time Series Analysis (part 2)

") Lecture 1: Fundamental concepts in Time Series Analysis (part 2) Florian Pelgrin University of Lausanne, École des HEC Department of mathematics (IMEA-Nice) Sept. 2011 - Jan. 2012 Florian Pelgrin (HEC)

Lecture 1: Fundamental concepts in Time Series Analysis (part 2) Florian Pelgrin University of Lausanne, École des HEC Department of mathematics (IMEA-Nice) Sept. 2011 - Jan. 2012 Florian Pelgrin (HEC)

Simple Descriptive Techniques

Simple Descriptive Techniques Outline 1 Types of variation 2 Stationary Time Series 3 The Time Plot 4 Transformations 5 Analysing Series that Contain a Trend 6 Analysing Series that Contain Seasonal Variation

Simple Descriptive Techniques Outline 1 Types of variation 2 Stationary Time Series 3 The Time Plot 4 Transformations 5 Analysing Series that Contain a Trend 6 Analysing Series that Contain Seasonal Variation

Design of Time Series Model for Road Accident Fatal Death in Tamilnadu

Volume 109 No. 8 2016, 225-232 ISSN: 1311-8080 (printed version); ISSN: 1314-3395 (on-line version) url: http://www.ijpam.eu ijpam.eu Design of Time Series Model for Road Accident Fatal Death in Tamilnadu

Volume 109 No. 8 2016, 225-232 ISSN: 1311-8080 (printed version); ISSN: 1314-3395 (on-line version) url: http://www.ijpam.eu ijpam.eu Design of Time Series Model for Road Accident Fatal Death in Tamilnadu

7 Introduction to Time Series

Econ 495 - Econometric Review 1 7 Introduction to Time Series 7.1 Time Series vs. Cross-Sectional Data Time series data has a temporal ordering, unlike cross-section data, we will need to changes some

Econ 495 - Econometric Review 1 7 Introduction to Time Series 7.1 Time Series vs. Cross-Sectional Data Time series data has a temporal ordering, unlike cross-section data, we will need to changes some

Introduction to Time Series Analysis. Lecture 11.

Introduction to Time Series Analysis. Lecture 11. Peter Bartlett 1. Review: Time series modelling and forecasting 2. Parameter estimation 3. Maximum likelihood estimator 4. Yule-Walker estimation 5. Yule-Walker

Introduction to Time Series Analysis. Lecture 11. Peter Bartlett 1. Review: Time series modelling and forecasting 2. Parameter estimation 3. Maximum likelihood estimator 4. Yule-Walker estimation 5. Yule-Walker

NANYANG TECHNOLOGICAL UNIVERSITY SEMESTER II EXAMINATION MAS451/MTH451 Time Series Analysis TIME ALLOWED: 2 HOURS

NANYANG TECHNOLOGICAL UNIVERSITY SEMESTER II EXAMINATION 2012-2013 MAS451/MTH451 Time Series Analysis May 2013 TIME ALLOWED: 2 HOURS INSTRUCTIONS TO CANDIDATES 1. This examination paper contains FOUR (4)

NANYANG TECHNOLOGICAL UNIVERSITY SEMESTER II EXAMINATION 2012-2013 MAS451/MTH451 Time Series Analysis May 2013 TIME ALLOWED: 2 HOURS INSTRUCTIONS TO CANDIDATES 1. This examination paper contains FOUR (4)

Lesson 4: Stationary stochastic processes

Dipartimento di Ingegneria e Scienze dell Informazione e Matematica Università dell Aquila, umberto.triacca@univaq.it Stationary stochastic processes Stationarity is a rather intuitive concept, it means

Dipartimento di Ingegneria e Scienze dell Informazione e Matematica Università dell Aquila, umberto.triacca@univaq.it Stationary stochastic processes Stationarity is a rather intuitive concept, it means

Lecture 2: ARMA(p,q) models (part 2)

models (part 2)") Lecture 2: ARMA(p,q) models (part 2) Florian Pelgrin University of Lausanne, École des HEC Department of mathematics (IMEA-Nice) Sept. 2011 - Jan. 2012 Florian Pelgrin (HEC) Univariate time series Sept.

Lecture 2: ARMA(p,q) models (part 2) Florian Pelgrin University of Lausanne, École des HEC Department of mathematics (IMEA-Nice) Sept. 2011 - Jan. 2012 Florian Pelgrin (HEC) Univariate time series Sept.

Lesson 2: Analysis of time series

Lesson 2: Analysis of time series Time series Main aims of time series analysis choosing right model statistical testing forecast driving and optimalisation Problems in analysis of time series time problems

Lesson 2: Analysis of time series Time series Main aims of time series analysis choosing right model statistical testing forecast driving and optimalisation Problems in analysis of time series time problems

CHAPTER 8 FORECASTING PRACTICE I

CHAPTER 8 FORECASTING PRACTICE I Sometimes we find time series with mixed AR and MA properties (ACF and PACF) We then can use mixed models: ARMA(p,q) These slides are based on: González-Rivera: Forecasting

CHAPTER 8 FORECASTING PRACTICE I Sometimes we find time series with mixed AR and MA properties (ACF and PACF) We then can use mixed models: ARMA(p,q) These slides are based on: González-Rivera: Forecasting

FinQuiz Notes

Reading 9 A time series is any series of data that varies over time e.g. the quarterly sales for a company during the past five years or daily returns of a security. When assumptions of the regression

Reading 9 A time series is any series of data that varies over time e.g. the quarterly sales for a company during the past five years or daily returns of a security. When assumptions of the regression

A Data-Driven Model for Software Reliability Prediction

A Data-Driven Model for Software Reliability Prediction Author: Jung-Hua Lo IEEE International Conference on Granular Computing (2012) Young Taek Kim KAIST SE Lab. 9/4/2013 Contents Introduction Background

A Data-Driven Model for Software Reliability Prediction Author: Jung-Hua Lo IEEE International Conference on Granular Computing (2012) Young Taek Kim KAIST SE Lab. 9/4/2013 Contents Introduction Background

MGR-815. Notes for the MGR-815 course. 12 June School of Superior Technology. Professor Zbigniew Dziong

Modeling, Estimation and Control, for Telecommunication Networks Notes for the MGR-815 course 12 June 2010 School of Superior Technology Professor Zbigniew Dziong 1 Table of Contents Preface 5 1. Example

Modeling, Estimation and Control, for Telecommunication Networks Notes for the MGR-815 course 12 June 2010 School of Superior Technology Professor Zbigniew Dziong 1 Table of Contents Preface 5 1. Example

Modeling and forecasting global mean temperature time series

Modeling and forecasting global mean temperature time series April 22, 2018 Abstract: An ARIMA time series model was developed to analyze the yearly records of the change in global annual mean surface

Modeling and forecasting global mean temperature time series April 22, 2018 Abstract: An ARIMA time series model was developed to analyze the yearly records of the change in global annual mean surface

Applied Time Series Topics

Applied Time Series Topics Ivan Medovikov Brock University April 16, 2013 Ivan Medovikov, Brock University Applied Time Series Topics 1/34 Overview 1. Non-stationary data and consequences 2. Trends and

Applied Time Series Topics Ivan Medovikov Brock University April 16, 2013 Ivan Medovikov, Brock University Applied Time Series Topics 1/34 Overview 1. Non-stationary data and consequences 2. Trends and

Lecture 2: Univariate Time Series

Lecture 2: Univariate Time Series Analysis: Conditional and Unconditional Densities, Stationarity, ARMA Processes Prof. Massimo Guidolin 20192 Financial Econometrics Spring/Winter 2017 Overview Motivation:

Lecture 2: Univariate Time Series Analysis: Conditional and Unconditional Densities, Stationarity, ARMA Processes Prof. Massimo Guidolin 20192 Financial Econometrics Spring/Winter 2017 Overview Motivation:

UNIVARIATE TIME SERIES ANALYSIS BRIEFING 1970

UNIVARIATE TIME SERIES ANALYSIS BRIEFING 1970 Joseph George Caldwell, PhD (Statistics) 1432 N Camino Mateo, Tucson, AZ 85745-3311 USA Tel. (001)(520)222-3446, E-mail jcaldwell9@yahoo.com (File converted

UNIVARIATE TIME SERIES ANALYSIS BRIEFING 1970 Joseph George Caldwell, PhD (Statistics) 1432 N Camino Mateo, Tucson, AZ 85745-3311 USA Tel. (001)(520)222-3446, E-mail jcaldwell9@yahoo.com (File converted

Econ 623 Econometrics II Topic 2: Stationary Time Series

1 Introduction Econ 623 Econometrics II Topic 2: Stationary Time Series In the regression model we can model the error term as an autoregression AR(1) process. That is, we can use the past value of the

1 Introduction Econ 623 Econometrics II Topic 2: Stationary Time Series In the regression model we can model the error term as an autoregression AR(1) process. That is, we can use the past value of the

Statistical Methods for Forecasting

Statistical Methods for Forecasting BOVAS ABRAHAM University of Waterloo JOHANNES LEDOLTER University of Iowa John Wiley & Sons New York Chichester Brisbane Toronto Singapore Contents 1 INTRODUCTION AND

Statistical Methods for Forecasting BOVAS ABRAHAM University of Waterloo JOHANNES LEDOLTER University of Iowa John Wiley & Sons New York Chichester Brisbane Toronto Singapore Contents 1 INTRODUCTION AND

ARIMA Models. Jamie Monogan. January 16, University of Georgia. Jamie Monogan (UGA) ARIMA Models January 16, / 27

ARIMA Models January 16, / 27") ARIMA Models Jamie Monogan University of Georgia January 16, 2018 Jamie Monogan (UGA) ARIMA Models January 16, 2018 1 / 27 Objectives By the end of this meeting, participants should be able to: Argue why

ARIMA Models Jamie Monogan University of Georgia January 16, 2018 Jamie Monogan (UGA) ARIMA Models January 16, 2018 1 / 27 Objectives By the end of this meeting, participants should be able to: Argue why

Time Series Analysis. James D. Hamilton PRINCETON UNIVERSITY PRESS PRINCETON, NEW JERSEY

Time Series Analysis James D. Hamilton PRINCETON UNIVERSITY PRESS PRINCETON, NEW JERSEY & Contents PREFACE xiii 1 1.1. 1.2. Difference Equations First-Order Difference Equations 1 /?th-order Difference

Time Series Analysis James D. Hamilton PRINCETON UNIVERSITY PRESS PRINCETON, NEW JERSEY & Contents PREFACE xiii 1 1.1. 1.2. Difference Equations First-Order Difference Equations 1 /?th-order Difference

Problem Set 1 Solution Sketches Time Series Analysis Spring 2010

Problem Set 1 Solution Sketches Time Series Analysis Spring 2010 1. Construct a martingale difference process that is not weakly stationary. Simplest e.g.: Let Y t be a sequence of independent, non-identically

Problem Set 1 Solution Sketches Time Series Analysis Spring 2010 1. Construct a martingale difference process that is not weakly stationary. Simplest e.g.: Let Y t be a sequence of independent, non-identically

The Art of Forecasting

Time Series The Art of Forecasting Learning Objectives Describe what forecasting is Explain time series & its components Smooth a data series Moving average Exponential smoothing Forecast using trend models

Time Series The Art of Forecasting Learning Objectives Describe what forecasting is Explain time series & its components Smooth a data series Moving average Exponential smoothing Forecast using trend models

A Diagnostic for Seasonality Based Upon Autoregressive Roots

A Diagnostic for Seasonality Based Upon Autoregressive Roots Tucker McElroy (U.S. Census Bureau) 2018 Seasonal Adjustment Practitioners Workshop April 26, 2018 1 / 33 Disclaimer This presentation is released

A Diagnostic for Seasonality Based Upon Autoregressive Roots Tucker McElroy (U.S. Census Bureau) 2018 Seasonal Adjustment Practitioners Workshop April 26, 2018 1 / 33 Disclaimer This presentation is released

Dynamic Time Series Regression: A Panacea for Spurious Correlations

International Journal of Scientific and Research Publications, Volume 6, Issue 10, October 2016 337 Dynamic Time Series Regression: A Panacea for Spurious Correlations Emmanuel Alphonsus Akpan *, Imoh

International Journal of Scientific and Research Publications, Volume 6, Issue 10, October 2016 337 Dynamic Time Series Regression: A Panacea for Spurious Correlations Emmanuel Alphonsus Akpan *, Imoh

Marcel Dettling. Applied Time Series Analysis SS 2013 Week 05. ETH Zürich, March 18, Institute for Data Analysis and Process Design

Marcel Dettling Institute for Data Analysis and Process Design Zurich University of Applied Sciences marcel.dettling@zhaw.ch http://stat.ethz.ch/~dettling ETH Zürich, March 18, 2013 1 Basics of Modeling

Marcel Dettling Institute for Data Analysis and Process Design Zurich University of Applied Sciences marcel.dettling@zhaw.ch http://stat.ethz.ch/~dettling ETH Zürich, March 18, 2013 1 Basics of Modeling

ARIMA Models. Richard G. Pierse

ARIMA Models Richard G. Pierse 1 Introduction Time Series Analysis looks at the properties of time series from a purely statistical point of view. No attempt is made to relate variables using a priori

ARIMA Models Richard G. Pierse 1 Introduction Time Series Analysis looks at the properties of time series from a purely statistical point of view. No attempt is made to relate variables using a priori

Ch 4. Models For Stationary Time Series. Time Series Analysis

This chapter discusses the basic concept of a broad class of stationary parametric time series models the autoregressive moving average (ARMA) models. Let {Y t } denote the observed time series, and {e

This chapter discusses the basic concept of a broad class of stationary parametric time series models the autoregressive moving average (ARMA) models. Let {Y t } denote the observed time series, and {e