IV. Markov-switching models

|

|

|

- Kristina Elizabeth Harmon

- 5 years ago

- Views:

Transcription

1 IV. Markov-switching models A. Introduction to Markov-switching models Many economic series exhibit dramatic breaks: - recessions - financial panics - currency crises Questions to be addressed: - how handle econometrically - how incorporate into economic theory

2 Economic recessions as changes in regime y t real GDP growth in quarter t s t 1 when economy is in expansion s t 2 when economy is in recesion y t m st t t N0, 2 Probs t j s t1 i, s t2 k,..., y t1, y t2,... p ij

3 y t m st t If s t is observed, m st AR(1) m st a m st1 v t a p 21 m 1 p 12 m 2 p 11 p 21 v t martingale difference sequence

4 If only t y t, y t1,..., y 1 is observed, Probs t 1 t is nonlinear in t. Given Probs t1 j t1, can calculate Probs t j t (and likelihood fy t t1 recursively:

5 Probs t j t1 p 1j Probs t1 1 t1 p 2j Probs t1 2 t1 2 fy t t1 Probs t i t1 fy t s t i, t1 i1 Probs t j t Probs tj t1 fy t s t j, t1 fy t t1

6 Could choose population parameters m 1, m 2,, p 11, p 22 by maximizing likelihood.

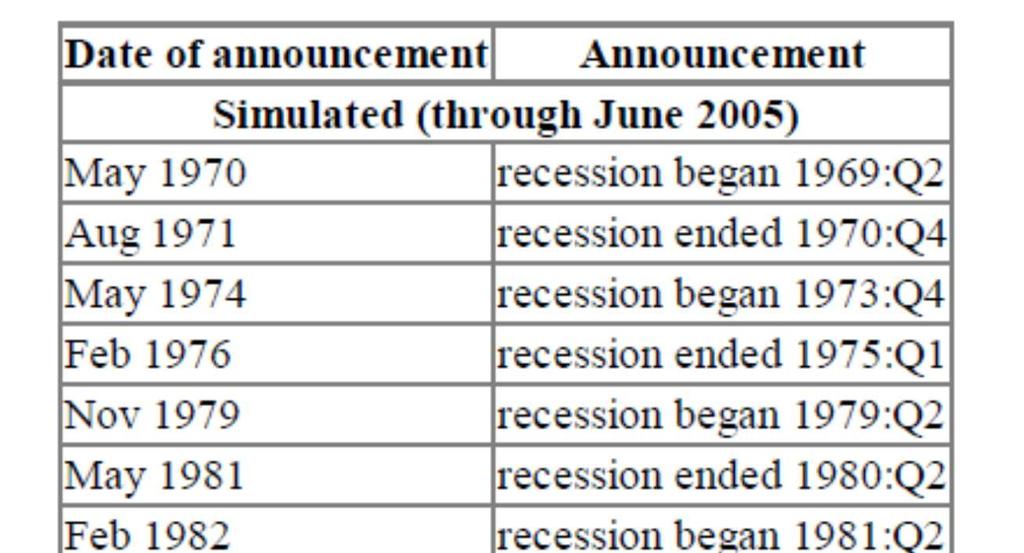

7 Plot of Prob(s t 2 t1, t1 with simulated real-time inference (historical real-time data sets from ALFRED) through Plot of actual real-time inference (announced publicly at each date t 1 since 2005.

8

9

10 Another example of change in regime Dollar-denominated minus Peso-denominated (in logs)

11 Model of structural change: y t 1 y t1 1 t t t 0 y t 2 y t1 2 t t t 0

12 Questions: 1) How forecast with this model? 2) What caused change at t 0? 3) What is probability law for {y t }?

13 s t 1 t 1,2,..,t 0 s t 2 t t 0 1, t 0 2,... y t s y t t1 st1 t Need: probability law for s t

14 Markov chain: Ps t j s t1 i,s t2 k,... Ps t j s t1 i p ij Transition from 1 to 2 is permanent p 21 0

15 In general, if s t is a Markov chain taking on one of the values s t 1,2,...,N, let p ij Ps t j s t1 i. Collect in matrix P p ji p 11 p 21 p N1 P p 12 p 22 p N2 p 1N p 2N p NN

16 In general, if s t is a Markov chain taking on one of the values s t 1,2,...,N, let p ij Ps t j s t1 i. Collect in matrix P p ji p 11 p 21 p N1 P p 12 p 22 p N2 p 1N p 2N p NN

17 Let t e i (the ith column of I N when s t i. Then Ps t1 1 s t i E t1 t e i Ps t1 2 s t i Ps t1 N s t i Pe i P t

18 Suppose we had a set of observations t y t, y t1,..., y 1 that gave us an imperfect inference about s t summarized as Ps t 1 t t t E t t Ps t 2 t Ps t N t

19 Then t1 t E t1 t P t t (e.g., row j states that Ps t1 j t p 1j Ps t 1 t p 2j Ps t 2 t p Nj Ps t N t

20 Return to original example of interest: y t s y t t1 st1 t t ~ i.i.d. N0, 2 Ps t j s t1 i p ij i, j 1,2 s t T t1 independent of t T t1 t y t,y t1,...,y 1

21 Implication: y t t1,s t,s t1 ~ N y st t1 s, 2 t1

22 Convenient to summarize s t,s t1 with a single Markov chain: s t 1 s t 2 s t 3 s t 4 if s t 1 and s t1 1 if s t 2 and s t1 1 if s t 1 and s t1 2 if s t 2 and s t1 2

23 t e i (ith column of I 4 ) when s t i t1 t P t t p 11 0 p 11 0 P p 12 0 p p 21 0 p 21 0 p 22 0 p 22

24 py t s t 3, t1 py t s t 1, st1 2, t1 1 2 exp y t 1 y t

25 Collect the densities that might be associated with each of the N 4 states in an N1 vector py t s t 1, t1 t py t s t 2, t1 py t s t N, t1

26 Recall that Ps t 1 t1 P t1 t1 Ps t 2 t1 Ps t N t1

27 Thus t P t1 t1 py t s t 1, t1 Ps t 1 t1 py t s t 2, t1 Ps t 2 t1 py t s t N, t1 Ps t N t1

28 Summing the elements of this vector gives 1 t P t1 t1 N j1 py t t1, py t, s t j t1 the conditional likelihood of tth observation.

29 The result of dividing the jth element of t P t1 t1 by the conditional likelihood is py t, s t j t1 py t t1 Ps t j y t, t1 t P t1 t1 1 t P t1 t1 t t

30 t P t1 t1 1 t t t P t1 t1 Iterative algorithm similar to Kalman filter: Input for step t: t1 t1 (an N1vector whose jth element is Ps t j y t,y t1,...,y 1 ). Output for step t: t t

31 Options for initial value 0 0 : (1) If Markov chain is ergodic, use ergodic probabilities 0 0 A A 1 A e N1 A N1N I N P 1

32 (2) Set 0 0, a vector of free parameters to be estimated by maximum likelihood or Bayesian methods along with the other parameters.

33 (3) Set 0 0 N 1 1. (4) Set 0 0 based on prior beliefs.

34 Above assumed we knew parameters appearing in t py t s t j, t1 ;N j1 (in this case, 1, 2, 2 ) and p appearing in P (in this case p p 11,p 22 ).

35 However, as byproduct of step t of iteration we ended up calculating py t t ;,p and so we ve calculated log likelihood,p T t1 logpy t t ;,p which can be maximized numerically with respect to and p by numerical methods.

36 Note during numerical search we d want to be choosing 11 and 22 rather than p 11 and p 22 where p p

37 General case: py t s t 1, t1 t py t s t 2, t1 py t s t N, t1 py t t1 1 t P t1 t1 y,...,y ; T 1 T t1 log py t t1

38 IV. Markov-switching models A. Introduction to Markov-switching models B. Economic theory and changes in regime

39 B.1. Closed-form solution of DSGE s and asset-pricing implications Lucas tree model with CRRA utility: P t price of stock D t dividend coefficient of relative risk aversion P t D t k1 k 1 E t D tk

40 Cecchetti, Lam and Mark (1990): log D t log D t1 m st t P t st D t

41 B.2. Linear rational expectations models with changes in regime A st Ey t1 t, s t, s t1,..., s 1 d st B st y t C st x t A j n y n y matrix of parameters when s t j.

42 Davig and Leeper (2007): Let y jt value of y t when s t j Y t Nn y 1 y 1t n y 1 y Nt n y 1

43 N Ey t1 s t i, t j1 Hence when s t i, Ey t1 s t1 j, s t i, t p ij A st Ey t1 s t, t p i A i EY t1 Y t

44 p 1 1N A 1 n y n y d 1 n y 1 A Nn y Nn y p N 1N A N n y n y d Nn y 1 d N n y 1

45 B Nn y Nn y B B B N C Nn y n x C 1 n y n x C N n y n x

46 Consider non-regime-changing system AEY t1 Y t d BY t Cx t If we can find a stable solution of the form Y t h Nn y 1 Nn y 1 then the ith block y t h st n y 1 n y 1 H x t Nn y n x n x 1 H st x t n y n x n x 1 is a stable solution to our original equation of interest.

47 However, even if we find a unique stable solution to the invariant system, there may be other stable solutions to the original system - Farmer, Waggoner, and Zha (2010)

48 B.3. Multiple equilibria Multiplicity of stable equilibria could itself be of interest - Coordination externalities (Cooper and John, 1988; Cooper, 1994) - Equilibria indexed by expectations (Kurz and Motolese, 2001) Regime-switching model could describe transitions between equilibria - Kirman (1993); Chamley (1999)

49 B.4. Tipping points and financial crises In other models, there is a unique equilibrium, but small change in fundamentals can cause big change in outcome - Acemoglu and Scott (1997); Moore and Schaller (2002); Guo, Miao, and Morelle (2005); Veldkamp (2005); Startz (1998); Hong, Stein, and Yu (2007); Branch and Evans (2010) Financial crises - Brunnermeier and Sannikov (2014); Hamilton (2005); Asea and Blomberg (1998); Hubrich and Tetlow (2013)

50 B.5. Currency crises and sovereign debt crises Currency crises - Jeanne and Masson (2000); Peria (2002); Cerra and Saxena (2005) Sovereign debt crises - Greenlaw, et. al. (2013); Davig, Leeper and Walker (2011); Bi (2012)

51 B.6. Changes in policy as the source of changes in regime Monetary policy: hawks vs. doves Owyang and Ramey (2004); Schorfheide (2005); Liu, Waggoner, and Zha (2011); Bianchi (2013) Unsustainable fiscal policy and inflation Ruge-Murcia (1995, 1999)

52 IV. Markov-switching models A. Introduction to Markov-switching models B. Economic theory and changes in regime C. Extensions

53 C.1. Selecting the number of regimes Smith, Naik and Tsai (2006): y t x t st st t T i T t1 Probs t i T ; MLE MSC 2 N MLE i1 T i T i Nk T i Nk2

54 Calculate nonstandard properties of likelihood ratio test - Hansen (1992) - Garcia (1998) Use general specification tests of null of N regimes that have power against N +1 - Hamilton (1996) - Carrasco, Hu and Ploberger (2014)

55 C.2. Chib s multiple change-point model P p p 11 p p 22 p p N1,N p N1,N1 1

56 C.3. Allowing any parameters of distribution to change py t s t 1, t1 t py t s t 2, t1 py t s t N, t1 py t t1 1 t P t1 t1 y,...,y ; T 1 T t1 log py t t1

57 Example: Dueker (JBES, 1997). AR(1) with Student t innovations whose degrees of freedom change with regime: py t s t j, t1 ; j 1/2 j 1/2 j /2 1 y t c y t1 2 j c,,, 1, 2 j 1/2

58 Example: Krolzig (Markov-Switching Vector Autoregressions, Springer 1997): Gaussian VAR(1) with lag coefficients changing: py t s t j, t1, 2 n/2 1/2 exp1/2y t c j j y t1 1 c 1, c 2 y t c j j y t1,vec 1,vec 2,vech

59 Can also allow transition probabilities to be parametric function of exogenous or lagged dependent variables z t : P Ps t j s t1 i, z t ; p N i,j1. Example: P p, exp z t 1exp z t 1 1exp z t 1 1exp z t exp z t 1exp z t

60 What can t we do? Models where y t depends on a growing number of states: py t t1,s t,s t1,...,s 1 ; Example: ARMA process y t t st1 t1 y t t st1 y t1 st1 st2 y t2 y st1 st2 st3 t3

61 Example: GARCH process: y t h t t h t s y2 t t1 h t1 y2 st t1 y 2 st1 t2 2 s y 2 t2 t3

62 Solution: numerical Bayesian methods

63 IV. Markov-switching models A. Introduction to Markov-switching models B. Economic theory and changes in regime C. Extensions D. Bayesian analysis of Markov-switching models

64 Example: y t s x t t t t ~ i.i.d. N0, 2 Ps t j s t1 i p ij i,j 1, 2 (does not depend on x tk, tk, s tk1 for k 0,1, 2,...)

65 Gibbs sampler: 1, 2, 3, , 2 3 p 11,p 22 4 s 1,s 2,...,s T

66 (1) Generating 1 2 from p 1 2, 3, 4, Y, X. Prior: 2 ~N, Conditioning on 2, 3, 4, Y, X is equivalent to observing t T t1 t y t st Posterior: x t for 2 2, 3, 4,Y, X ~N T, S S T 2 t1 t

67 (2) Generating 2 1 p 2 1, 3, 4,Y, X. Priors:, 2 from i 2 ~ Nm i, 2 M i i 1,2 (independent of each other) Posterior: Conditioning on s t T t1, only those observations t for which s t 1 are relevant for posterior distribution of 1.

68 i 1, 3, 4,Y, X ~ Nm i, 2 M i M i M 1 T i t1 x t x t st i 1 m i M i M 1 i m i T t1 x t y t s ti

69 Label-switching problem: If switch 1 with 2 and p 11 with p 22, value of likelihood py X, 1, 2, 3 is identical. Implication: if priors for i and p ii are same for i 1,2, then true posterior distribution is bimodal and perfectly symmetric around the two modes.

70 Presume we have interpretive (as opposed to numerical) labels for regimes. E.g., regime 2 recession, should have faster GDP growth, so that, say, 1 1, first element of 1, should be bigger 2 1, the first element of 2.

71 Strategy (1): Intentionally use symmetric priors for regimes 1 and 2 and intentionally randomly perturb parameter draw j to switch across modes so as to get multimodal posterior distribution, and apply normalization rule to this.

72 Strategy (2): Impose normalization requirement at every draw. Drawback to (2): not clear it s same distribution as (1).

73 Drawback to either approach: Even though normalized posterior distribution has unique global mode, may still have local modes resulting from label switching. Recommendation: plot posterior distributions to check for this.

74 (3) Generating 3 p 11,p 22 from p 3 1, 2, 4,Y, X. Priors: A variable x is said to have a beta distribution with parameters 0 and 0, denoted x ~ Beta,, if px, x1 1x 1 for 0 x 1 and px, 0 elsewhere.

75 Ex Vx 2 1

76 Beta distribution p(x) ==0.5 ==1 ==6 == x

77 Beta distribution p(x) =1.5,=0.5 =3,=1 =6,=2 =18,= x

78 Priors: p ii ~ Beta i, i i 1, 2 (independent of each other)

79 Posterior: Observation of 1, 2, 4, Y, X only affects inference about p ii through 4 s 1, s 2,...,s T. Assume that initial probability Ps 1 1 does not depend on p ii (don t use ergodic probabilities).

80 Suppose that in the sequence 4 s 1,s 2,...,s T state s t 1 is observed to be followed by s t1 1 a total of n 11 times, whereas state s t 1 is followed by s t1 2 a total of n 12 times.

81 Then, for purposes of inference about p 11, can view the data 1, 2, 4, Y, X solely as a sample of n 11 n 12 observations from a Bernoulli variable with probability of success p 11 : n p 1, 2, 4,Y, X 3 p p 11 n 12

82 data: n p 1, 2, 4, Y, X 3 p p 11 n 12 prior: p ii ~ Beta i, i p 3 p p posterior: p ii ~ Beta i, i 1 1 n n n n 21

83 (4) Generating 4 s 1, s 2,...,s T from p 4 1, 2, 3, Y, X. Calculate Ps T 1 1, 2, 3,Y, X from first element of T T. Generate U T ~ U0,1 and set S T 1 if U T e 1 T T.

84 Consider PS t i S t1 j,s t2 k,...,s T z, 1, 2, 3, Y, X PS t i S t1 j, 1, 2, 3, t for t y t, y t1,...,y 1, x t, x t1,...,x 1

85 PS t i S t1 j, 1, 2, 3, t PS t i,s t1 j 1, 2, 3, t PS t1 j 1, 2, 3, t PS t1 j S t ips t i 1, 2, 3, t PS t1 j 1, 2, 3, t p ije i t t e j P t t

86 Iterating backwards t T 1, T 2,... we generate the sequence 4 s 1,s 2,...,s T from p 4 1, 2, 3, Y, X.

87 Generalization: N-state Markov chain. x ~ Beta 1, 2 px 1, x 11 1 x 21 0 x 1

88 x 1, x 2,..., x N ~ Dirichlet 1, 2,..., N px 1,..., N 1 N 1 N x x N 1 N 0 x i 1 x 1 x N 1 i 0

89 prior: p 11,p 12,...,p 1N ~ Dirichlet 11, 12,..., 1N data: n 1j number of times s t 1 is followed by s t1 j posterior: p 11,p 12,...,p 1N 1, 2, 3,Y, X ~ Dirichlet 11 n 11,..., 1N n 1N

90 Generalization: time-dependent transition probabilities: Ps t j s t1 i,x t x t predetermined at t

91 Convenient framework for Gibbs sampling: latent variable z t z t 0 s t1 x t u t u t ~ N0, 1 s t 1 if z t 0 2 if z t 0

92 Gibbs sampler: 1, 2, 3, , s 1,s 2,...,s T, z 1,z 2,...,z T 4 0,

93 Draws from p 1 2, 3, 4, Y,X and p 2 1, 3, 4, Y, X same as before (conditioning onz t adds no information beyond that ins t ).

94 Will draw 3 using p 3 1, 2, 4, Y, X ps 1,...,s T 1, 2, 4,Y,X pz 1,...,z T s 1,...,s T, 1, 2, 4, Y, X (a) To draw from ps 1,...,s T 1, 2, 4,Y,X use modification of filter for time-varying probabilities

95 Recall filter with constant probabilities: jth element of : t jt py t s t j, t1 jth element of t t1 P t1 t1 : ps t j t1 jth element of t t t1 : py t, s t j t1 t t t t t1 1 t t t1

96 Filter with time-varying probabilities: z t 0 s t1 x t u t u t N0, 1 s t 1 if z t 0

97 ps t 1 t1 ps t 1 s t1 1, t1 ps t1 1 t1 ps t 1 s t1 2, t1 ps t1 2 t1 p 0 x t u t 0ps t1 1 t1 p2 0 x t u t 0ps t1 2 t1 0 x t ps t1 1 t1 2 0 x t ps t1 2 t1

98 So we just replace t t1 P t1 t1 in the regular filter with t t1 ps t 1 t1 ps t 2 t1 t t t t t1 1 t t t1

99 (i) Run through filter to calculate t t, t t1 T t1 (ii) Generate s T 1 with probability e 1 T T and s T 2 with probability e 2 T T. (iii) To get s t for t T1,T2,... use modification of earlier smoothing algorithm:

100 PS t i S t1 j, 1, 2, 4, t PS t i,s t1 j 1, 2, 4, t PS t1 j 1, 2, 4, t PS t1 j S t ips t i 1, 2, 4, t PS t1 j 1, 2, 4, t 0 i x t e i t t e 1 t1 t if j i x t e i t t e 2 t1 t if j 2

101 p 3 1, 2, 4,Y,X ps 1,...,s T 1, 2, 4,Y,X pz 1,...,z T s 1,...,s T, 1, 2, 4,Y,X (b) To draw from pz 1,...,z T s 1,...,s T, 1, 2, 4,Y,X z t 0 s t1 x t u t Generate z t N 0 s t1 x t,1 keep if signz t signs t 1.5 otherwise draw new z t

102 Finally, to generate a value for 4 0, given 1, 2, 3, Y, X, notice that conditional on having observed s t1, z t T t1, generating 4 is standard regression problem: z t 0 s t1 x t u t

103 IV. Markov-switching models A. Introduction to Markov-switching models B. Economic theory and changes in regime C. Extensions D. Bayesian analysis of Markov-switching models E. State-space models with Markov switching

104 t1 F s t t v t1 y t A s t x t H st Ps t1 j s t i p ij Ev t1 v t1 Q st t w t Ew t w t R s t s t,v t,w t independent x t predetermined exogenous

105 1 unknown elements of Q 1, Q 2,R 1,R 2 2 unknown elements of F 1, F 2, A 1, A 2, H 1,H 2 3 p 11,p 22 4 s 0,s 1,s 2,...,s T 5 unknown elements of 0, 1,..., T

106 (1) Generating 1 Q 1, Q 2,R 1,R 2 given Y, X, 2, 3, 4, 5. t1 F s t t v t1 Ev t1 v t1 Q st

107 Notice for purposes of estimating Q 1, the likelihood satisfies py X, 2, 3, 4, 5 T Q t1 s 1/2 t1 exp 1/2 T t1 t F s t 1 t1 Q 1 st1 t F st 1 t1 T t1 Q 1 1/2 s t1 1 exp 1/2 T t1 t F s t 1 t1 Q 1 1 t F st 1 t1 st1 1

108 prior: Q 1 1 ~ WN Q 1, Q1 posterior: Q 1 1 2, 3, 4, 5, Y,X ~ WN Q1 T 1, Q1 S Q1 T 1 T t1 S T Q1 t1 st1 1 v t v t v t t F st 1 t1 s t1 1

109 (2) Generating 2 F 1, F 2,A 1, A 2,H 1, H 2 given Y,X, 1, 3, 4, 5. t1 F s t t v t1 Ev t1 v t1 Q st

110 prior: f 2 Q 2 ~ Nm F2, Q 2 M F2 posterior: f 2 Y, X, 1, 3, 4, 5 ~ Nm,Q F2 2 M F2 M F2 M 1 T F2 t1 t1 t1 s t1 2 1

111 m I F2 r M M 1 m F2 F2 F2 I r M T F2 t1 t1 t1 st1 2 f 2 f 2 vecf 2 F 2 T t1 t1 t1 st1 2 1 T t1 t1 t st1 2

112 (3) Generating 3 p 11, p 22 given Y, X, 1, 2, 4, 5. (4) Generating 4 s 0, s 1,s 2,...,s T given Y,X, 1, 2, 3, 5. Exactly same as for other Markovswitching models.

113 (5) Generating 5 0, 1,..., T given Y, X, 1, 2, 3, 4. t1 F s t t v t1 y t A s t x t H st Ev t1 v t1 Q st t w t Ew t w t R s t Conditional on s 0, s 1,...,s T, this is just a Kalman filter problem where we use different F, Q, A, H, R for different dates.

114 P t1 t F s tp t t F st Q s t P t1 t1 P t1 t P t1 t H st1 H st1 t1 t F s t t t P t1 t H R 1 H st1 st1 st1 P t1 t

115 t1 t y t1 A x st1 t1 H st1 t1 t t1 t1 t1 t P t1 t H st1 H st1 P t1 t H st1 R st1 1 t1 t

116 T Y,X, 1, 2, 3, 4 ~ N T T, P T T t t1, Y,X, 1, 2, 3, 4 ~ N t t,p t t J t P t t F P 1 st t1 t P t t P t t J t F P st t t

Business cycles and changes in regime. 1. Motivating examples 2. Econometric approaches 3. Incorporating into theoretical models

Business cycles and changes in regime 1. Motivating examples 2. Econometric approaches 3. Incorporating into theoretical models 1 1. Motivating examples Many economic series exhibit dramatic breaks: -

Business cycles and changes in regime 1. Motivating examples 2. Econometric approaches 3. Incorporating into theoretical models 1 1. Motivating examples Many economic series exhibit dramatic breaks: -

New meeting times for Econ 210D Mondays 8:00-9:20 a.m. in Econ 300 Wednesdays 11:00-12:20 in Econ 300

New meeting times for Econ 210D Mondays 8:00-9:20 a.m. in Econ 300 Wednesdays 11:00-12:20 in Econ 300 1 Identification using nonrecursive structure, long-run restrictions and heteroskedasticity 2 General

New meeting times for Econ 210D Mondays 8:00-9:20 a.m. in Econ 300 Wednesdays 11:00-12:20 in Econ 300 1 Identification using nonrecursive structure, long-run restrictions and heteroskedasticity 2 General

Inference when identifying assumptions are doubted. A. Theory. Structural model of interest: B 1 y t1. u t. B m y tm. u t i.i.d.

Inference when identifying assumptions are doubted A. Theory B. Applications Structural model of interest: A y t B y t B m y tm nn n i.i.d. N, D D diagonal A. Theory Bayesian approach: Summarize whatever

Inference when identifying assumptions are doubted A. Theory B. Applications Structural model of interest: A y t B y t B m y tm nn n i.i.d. N, D D diagonal A. Theory Bayesian approach: Summarize whatever

Inference when identifying assumptions are doubted. A. Theory B. Applications

Inference when identifying assumptions are doubted A. Theory B. Applications 1 A. Theory Structural model of interest: A y t B 1 y t1 B m y tm u t nn n1 u t i.i.d. N0, D D diagonal 2 Bayesian approach:

Inference when identifying assumptions are doubted A. Theory B. Applications 1 A. Theory Structural model of interest: A y t B 1 y t1 B m y tm u t nn n1 u t i.i.d. N0, D D diagonal 2 Bayesian approach:

Modeling conditional distributions with mixture models: Theory and Inference

Modeling conditional distributions with mixture models: Theory and Inference John Geweke University of Iowa, USA Journal of Applied Econometrics Invited Lecture Università di Venezia Italia June 2, 2005

Modeling conditional distributions with mixture models: Theory and Inference John Geweke University of Iowa, USA Journal of Applied Econometrics Invited Lecture Università di Venezia Italia June 2, 2005

I. Bayesian econometrics

I. Bayesian econometrics A. Introduction B. Bayesian inference in the univariate regression model C. Statistical decision theory D. Large sample results E. Diffuse priors F. Numerical Bayesian methods

I. Bayesian econometrics A. Introduction B. Bayesian inference in the univariate regression model C. Statistical decision theory D. Large sample results E. Diffuse priors F. Numerical Bayesian methods

The Kalman filter, Nonlinear filtering, and Markov Chain Monte Carlo

NBER Summer Institute Minicourse What s New in Econometrics: Time Series Lecture 5 July 5, 2008 The Kalman filter, Nonlinear filtering, and Markov Chain Monte Carlo Lecture 5, July 2, 2008 Outline. Models

NBER Summer Institute Minicourse What s New in Econometrics: Time Series Lecture 5 July 5, 2008 The Kalman filter, Nonlinear filtering, and Markov Chain Monte Carlo Lecture 5, July 2, 2008 Outline. Models

Time-Varying Vector Autoregressive Models with Structural Dynamic Factors

Time-Varying Vector Autoregressive Models with Structural Dynamic Factors Paolo Gorgi, Siem Jan Koopman, Julia Schaumburg http://sjkoopman.net Vrije Universiteit Amsterdam School of Business and Economics

Time-Varying Vector Autoregressive Models with Structural Dynamic Factors Paolo Gorgi, Siem Jan Koopman, Julia Schaumburg http://sjkoopman.net Vrije Universiteit Amsterdam School of Business and Economics

THE CONSEQUENCES OF AN UNKNOWN DEBT TARGET

THE CONSEQUENCES OF AN UNKNOWN DEBT TARGET Alexander W. Richter Auburn University Nathaniel A. Throckmorton College of William & Mary MOTIVATION Agreement on benefits of central bank communication No consensus

THE CONSEQUENCES OF AN UNKNOWN DEBT TARGET Alexander W. Richter Auburn University Nathaniel A. Throckmorton College of William & Mary MOTIVATION Agreement on benefits of central bank communication No consensus

Chapter 6. Maximum Likelihood Analysis of Dynamic Stochastic General Equilibrium (DSGE) Models

Models") Chapter 6. Maximum Likelihood Analysis of Dynamic Stochastic General Equilibrium (DSGE) Models Fall 22 Contents Introduction 2. An illustrative example........................... 2.2 Discussion...................................

Chapter 6. Maximum Likelihood Analysis of Dynamic Stochastic General Equilibrium (DSGE) Models Fall 22 Contents Introduction 2. An illustrative example........................... 2.2 Discussion...................................

ECO 513 Fall 2009 C. Sims HIDDEN MARKOV CHAIN MODELS

ECO 513 Fall 2009 C. Sims HIDDEN MARKOV CHAIN MODELS 1. THE CLASS OF MODELS y t {y s, s < t} p(y t θ t, {y s, s < t}) θ t = θ(s t ) P[S t = i S t 1 = j] = h ij. 2. WHAT S HANDY ABOUT IT Evaluating the

ECO 513 Fall 2009 C. Sims HIDDEN MARKOV CHAIN MODELS 1. THE CLASS OF MODELS y t {y s, s < t} p(y t θ t, {y s, s < t}) θ t = θ(s t ) P[S t = i S t 1 = j] = h ij. 2. WHAT S HANDY ABOUT IT Evaluating the

Non-Markovian Regime Switching with Endogenous States and Time-Varying State Strengths

Non-Markovian Regime Switching with Endogenous States and Time-Varying State Strengths January 2004 Siddhartha Chib Olin School of Business Washington University chib@olin.wustl.edu Michael Dueker Federal

Non-Markovian Regime Switching with Endogenous States and Time-Varying State Strengths January 2004 Siddhartha Chib Olin School of Business Washington University chib@olin.wustl.edu Michael Dueker Federal

A. Recursively orthogonalized. VARs

Orthogonalized VARs A. Recursively orthogonalized VAR B. Variance decomposition C. Historical decomposition D. Structural interpretation E. Generalized IRFs 1 A. Recursively orthogonalized Nonorthogonal

Orthogonalized VARs A. Recursively orthogonalized VAR B. Variance decomposition C. Historical decomposition D. Structural interpretation E. Generalized IRFs 1 A. Recursively orthogonalized Nonorthogonal

Unit roots in vector time series. Scalar autoregression True model: y t 1 y t1 2 y t2 p y tp t Estimated model: y t c y t1 1 y t1 2 y t2

Unit roots in vector time series A. Vector autoregressions with unit roots Scalar autoregression True model: y t y t y t p y tp t Estimated model: y t c y t y t y t p y tp t Results: T j j is asymptotically

Unit roots in vector time series A. Vector autoregressions with unit roots Scalar autoregression True model: y t y t y t p y tp t Estimated model: y t c y t y t y t p y tp t Results: T j j is asymptotically

Bayesian Inference for DSGE Models. Lawrence J. Christiano

Bayesian Inference for DSGE Models Lawrence J. Christiano Outline State space-observer form. convenient for model estimation and many other things. Bayesian inference Bayes rule. Monte Carlo integation.

Bayesian Inference for DSGE Models Lawrence J. Christiano Outline State space-observer form. convenient for model estimation and many other things. Bayesian inference Bayes rule. Monte Carlo integation.

Indeterminacy and Sunspots in Macroeconomics

Indeterminacy and Sunspots in Macroeconomics Friday September 8 th : Lecture 10 Gerzensee, September 2017 Roger E. A. Farmer Warwick University and NIESR Topics for Lecture 10 Tying together the pieces

Indeterminacy and Sunspots in Macroeconomics Friday September 8 th : Lecture 10 Gerzensee, September 2017 Roger E. A. Farmer Warwick University and NIESR Topics for Lecture 10 Tying together the pieces

Switching Regime Estimation

Switching Regime Estimation Series de Tiempo BIrkbeck March 2013 Martin Sola (FE) Markov Switching models 01/13 1 / 52 The economy (the time series) often behaves very different in periods such as booms

Switching Regime Estimation Series de Tiempo BIrkbeck March 2013 Martin Sola (FE) Markov Switching models 01/13 1 / 52 The economy (the time series) often behaves very different in periods such as booms

Dynamic models. Dependent data The AR(p) model The MA(q) model Hidden Markov models. 6 Dynamic models

model The MA(q) model Hidden Markov models. 6 Dynamic models") 6 Dependent data The AR(p) model The MA(q) model Hidden Markov models Dependent data Dependent data Huge portion of real-life data involving dependent datapoints Example (Capture-recapture) capture histories

6 Dependent data The AR(p) model The MA(q) model Hidden Markov models Dependent data Dependent data Huge portion of real-life data involving dependent datapoints Example (Capture-recapture) capture histories

Financial Econometrics

Financial Econometrics Nonlinear time series analysis Gerald P. Dwyer Trinity College, Dublin January 2016 Outline 1 Nonlinearity Does nonlinearity matter? Nonlinear models Tests for nonlinearity Forecasting

Financial Econometrics Nonlinear time series analysis Gerald P. Dwyer Trinity College, Dublin January 2016 Outline 1 Nonlinearity Does nonlinearity matter? Nonlinear models Tests for nonlinearity Forecasting

Basic math for biology

Basic math for biology Lei Li Florida State University, Feb 6, 2002 The EM algorithm: setup Parametric models: {P θ }. Data: full data (Y, X); partial data Y. Missing data: X. Likelihood and maximum likelihood

Basic math for biology Lei Li Florida State University, Feb 6, 2002 The EM algorithm: setup Parametric models: {P θ }. Data: full data (Y, X); partial data Y. Missing data: X. Likelihood and maximum likelihood

... Econometric Methods for the Analysis of Dynamic General Equilibrium Models

... Econometric Methods for the Analysis of Dynamic General Equilibrium Models 1 Overview Multiple Equation Methods State space-observer form Three Examples of Versatility of state space-observer form:

... Econometric Methods for the Analysis of Dynamic General Equilibrium Models 1 Overview Multiple Equation Methods State space-observer form Three Examples of Versatility of state space-observer form:

Research Division Federal Reserve Bank of St. Louis Working Paper Series

Research Division Federal Reserve Bank of St Louis Working Paper Series Kalman Filtering with Truncated Normal State Variables for Bayesian Estimation of Macroeconomic Models Michael Dueker Working Paper

Research Division Federal Reserve Bank of St Louis Working Paper Series Kalman Filtering with Truncated Normal State Variables for Bayesian Estimation of Macroeconomic Models Michael Dueker Working Paper

Multivariate Markov Switching With Weighted Regime Determination: Giving France More Weight than Finland

Multivariate Markov Switching With Weighted Regime Determination: Giving France More Weight than Finland November 2006 Michael Dueker Federal Reserve Bank of St. Louis P.O. Box 442, St. Louis, MO 63166

Multivariate Markov Switching With Weighted Regime Determination: Giving France More Weight than Finland November 2006 Michael Dueker Federal Reserve Bank of St. Louis P.O. Box 442, St. Louis, MO 63166

STA 4273H: Statistical Machine Learning

STA 4273H: Statistical Machine Learning Russ Salakhutdinov Department of Statistics! rsalakhu@utstat.toronto.edu! http://www.utstat.utoronto.ca/~rsalakhu/ Sidney Smith Hall, Room 6002 Lecture 11 Project

STA 4273H: Statistical Machine Learning Russ Salakhutdinov Department of Statistics! rsalakhu@utstat.toronto.edu! http://www.utstat.utoronto.ca/~rsalakhu/ Sidney Smith Hall, Room 6002 Lecture 11 Project

Vector Auto-Regressive Models

Vector Auto-Regressive Models Laurent Ferrara 1 1 University of Paris Nanterre M2 Oct. 2018 Overview of the presentation 1. Vector Auto-Regressions Definition Estimation Testing 2. Impulse responses functions

Vector Auto-Regressive Models Laurent Ferrara 1 1 University of Paris Nanterre M2 Oct. 2018 Overview of the presentation 1. Vector Auto-Regressions Definition Estimation Testing 2. Impulse responses functions

VAR Models and Applications

VAR Models and Applications Laurent Ferrara 1 1 University of Paris West M2 EIPMC Oct. 2016 Overview of the presentation 1. Vector Auto-Regressions Definition Estimation Testing 2. Impulse responses functions

VAR Models and Applications Laurent Ferrara 1 1 University of Paris West M2 EIPMC Oct. 2016 Overview of the presentation 1. Vector Auto-Regressions Definition Estimation Testing 2. Impulse responses functions

Point, Interval, and Density Forecast Evaluation of Linear versus Nonlinear DSGE Models

Point, Interval, and Density Forecast Evaluation of Linear versus Nonlinear DSGE Models Francis X. Diebold Frank Schorfheide Minchul Shin University of Pennsylvania May 4, 2014 1 / 33 Motivation The use

Point, Interval, and Density Forecast Evaluation of Linear versus Nonlinear DSGE Models Francis X. Diebold Frank Schorfheide Minchul Shin University of Pennsylvania May 4, 2014 1 / 33 Motivation The use

MA Advanced Macroeconomics: Solving Models with Rational Expectations

MA Advanced Macroeconomics: Solving Models with Rational Expectations Karl Whelan School of Economics, UCD February 6, 2009 Karl Whelan (UCD) Models with Rational Expectations February 6, 2009 1 / 32 Moving

MA Advanced Macroeconomics: Solving Models with Rational Expectations Karl Whelan School of Economics, UCD February 6, 2009 Karl Whelan (UCD) Models with Rational Expectations February 6, 2009 1 / 32 Moving

Markov Switching Models

Applications with R Tsarouchas Nikolaos-Marios Supervisor Professor Sophia Dimelis A thesis presented for the MSc degree in Business Mathematics Department of Informatics Athens University of Economics

Applications with R Tsarouchas Nikolaos-Marios Supervisor Professor Sophia Dimelis A thesis presented for the MSc degree in Business Mathematics Department of Informatics Athens University of Economics

Web Appendix for The Dynamics of Reciprocity, Accountability, and Credibility

Web Appendix for The Dynamics of Reciprocity, Accountability, and Credibility Patrick T. Brandt School of Economic, Political and Policy Sciences University of Texas at Dallas E-mail: pbrandt@utdallas.edu

Web Appendix for The Dynamics of Reciprocity, Accountability, and Credibility Patrick T. Brandt School of Economic, Political and Policy Sciences University of Texas at Dallas E-mail: pbrandt@utdallas.edu

Do Markov-Switching Models Capture Nonlinearities in the Data? Tests using Nonparametric Methods

Do Markov-Switching Models Capture Nonlinearities in the Data? Tests using Nonparametric Methods Robert V. Breunig Centre for Economic Policy Research, Research School of Social Sciences and School of

Do Markov-Switching Models Capture Nonlinearities in the Data? Tests using Nonparametric Methods Robert V. Breunig Centre for Economic Policy Research, Research School of Social Sciences and School of

Generalized Autoregressive Score Models

Generalized Autoregressive Score Models by: Drew Creal, Siem Jan Koopman, André Lucas To capture the dynamic behavior of univariate and multivariate time series processes, we can allow parameters to be

Generalized Autoregressive Score Models by: Drew Creal, Siem Jan Koopman, André Lucas To capture the dynamic behavior of univariate and multivariate time series processes, we can allow parameters to be

ECO 513 Fall 2008 C.Sims KALMAN FILTER. s t = As t 1 + ε t Measurement equation : y t = Hs t + ν t. u t = r t. u 0 0 t 1 + y t = [ H I ] u t.

![ECO 513 Fall 2008 C.Sims KALMAN FILTER. s t = As t 1 + ε t Measurement equation : y t = Hs t + ν t. u t = r t. u 0 0 t 1 + y t = [ H I ] u t.](/thumbs/87/95887004.jpg "ECO 513 Fall 2008 C.Sims KALMAN FILTER. s t = As t 1 + ε t Measurement equation : y t = Hs t + ν t. u t = r t. u 0 0 t 1 + y t = [ H I ] u t.") ECO 513 Fall 2008 C.Sims KALMAN FILTER Model in the form 1. THE KALMAN FILTER Plant equation : s t = As t 1 + ε t Measurement equation : y t = Hs t + ν t. Var(ε t ) = Ω, Var(ν t ) = Ξ. ε t ν t and (ε t,

ECO 513 Fall 2008 C.Sims KALMAN FILTER Model in the form 1. THE KALMAN FILTER Plant equation : s t = As t 1 + ε t Measurement equation : y t = Hs t + ν t. Var(ε t ) = Ω, Var(ν t ) = Ξ. ε t ν t and (ε t,

ECONOMICS 7200 MODERN TIME SERIES ANALYSIS Econometric Theory and Applications

ECONOMICS 7200 MODERN TIME SERIES ANALYSIS Econometric Theory and Applications Yongmiao Hong Department of Economics & Department of Statistical Sciences Cornell University Spring 2019 Time and uncertainty

ECONOMICS 7200 MODERN TIME SERIES ANALYSIS Econometric Theory and Applications Yongmiao Hong Department of Economics & Department of Statistical Sciences Cornell University Spring 2019 Time and uncertainty

Bayesian Inference for DSGE Models. Lawrence J. Christiano

Bayesian Inference for DSGE Models Lawrence J. Christiano Outline State space-observer form. convenient for model estimation and many other things. Bayesian inference Bayes rule. Monte Carlo integation.

Bayesian Inference for DSGE Models Lawrence J. Christiano Outline State space-observer form. convenient for model estimation and many other things. Bayesian inference Bayes rule. Monte Carlo integation.

Predicting bond returns using the output gap in expansions and recessions

Erasmus university Rotterdam Erasmus school of economics Bachelor Thesis Quantitative finance Predicting bond returns using the output gap in expansions and recessions Author: Martijn Eertman Studentnumber:

Erasmus university Rotterdam Erasmus school of economics Bachelor Thesis Quantitative finance Predicting bond returns using the output gap in expansions and recessions Author: Martijn Eertman Studentnumber:

DSGE MODELS WITH STUDENT-t ERRORS

Econometric Reviews, 33(1 4):152 171, 2014 Copyright Taylor & Francis Group, LLC ISSN: 0747-4938 print/1532-4168 online DOI: 10.1080/07474938.2013.807152 DSGE MODELS WITH STUDENT-t ERRORS Siddhartha Chib

Econometric Reviews, 33(1 4):152 171, 2014 Copyright Taylor & Francis Group, LLC ISSN: 0747-4938 print/1532-4168 online DOI: 10.1080/07474938.2013.807152 DSGE MODELS WITH STUDENT-t ERRORS Siddhartha Chib

Combining Macroeconomic Models for Prediction

Combining Macroeconomic Models for Prediction John Geweke University of Technology Sydney 15th Australasian Macro Workshop April 8, 2010 Outline 1 Optimal prediction pools 2 Models and data 3 Optimal pools

Combining Macroeconomic Models for Prediction John Geweke University of Technology Sydney 15th Australasian Macro Workshop April 8, 2010 Outline 1 Optimal prediction pools 2 Models and data 3 Optimal pools

Empirical Market Microstructure Analysis (EMMA)

") Empirical Market Microstructure Analysis (EMMA) Lecture 3: Statistical Building Blocks and Econometric Basics Prof. Dr. Michael Stein michael.stein@vwl.uni-freiburg.de Albert-Ludwigs-University of Freiburg

Empirical Market Microstructure Analysis (EMMA) Lecture 3: Statistical Building Blocks and Econometric Basics Prof. Dr. Michael Stein michael.stein@vwl.uni-freiburg.de Albert-Ludwigs-University of Freiburg

STA 414/2104: Machine Learning

STA 414/2104: Machine Learning Russ Salakhutdinov Department of Computer Science! Department of Statistics! rsalakhu@cs.toronto.edu! http://www.cs.toronto.edu/~rsalakhu/ Lecture 9 Sequential Data So far

STA 414/2104: Machine Learning Russ Salakhutdinov Department of Computer Science! Department of Statistics! rsalakhu@cs.toronto.edu! http://www.cs.toronto.edu/~rsalakhu/ Lecture 9 Sequential Data So far

Dynamic Factor Models and Factor Augmented Vector Autoregressions. Lawrence J. Christiano

Dynamic Factor Models and Factor Augmented Vector Autoregressions Lawrence J Christiano Dynamic Factor Models and Factor Augmented Vector Autoregressions Problem: the time series dimension of data is relatively

Dynamic Factor Models and Factor Augmented Vector Autoregressions Lawrence J Christiano Dynamic Factor Models and Factor Augmented Vector Autoregressions Problem: the time series dimension of data is relatively

Katsuhiro Sugita Faculty of Law and Letters, University of the Ryukyus. Abstract

Bayesian analysis of a vector autoregressive model with multiple structural breaks Katsuhiro Sugita Faculty of Law and Letters, University of the Ryukyus Abstract This paper develops a Bayesian approach

Bayesian analysis of a vector autoregressive model with multiple structural breaks Katsuhiro Sugita Faculty of Law and Letters, University of the Ryukyus Abstract This paper develops a Bayesian approach

The Metropolis-Hastings Algorithm. June 8, 2012

The Metropolis-Hastings Algorithm June 8, 22 The Plan. Understand what a simulated distribution is 2. Understand why the Metropolis-Hastings algorithm works 3. Learn how to apply the Metropolis-Hastings

The Metropolis-Hastings Algorithm June 8, 22 The Plan. Understand what a simulated distribution is 2. Understand why the Metropolis-Hastings algorithm works 3. Learn how to apply the Metropolis-Hastings

The Particle Filter. PD Dr. Rudolph Triebel Computer Vision Group. Machine Learning for Computer Vision

The Particle Filter Non-parametric implementation of Bayes filter Represents the belief (posterior) random state samples. by a set of This representation is approximate. Can represent distributions that

The Particle Filter Non-parametric implementation of Bayes filter Represents the belief (posterior) random state samples. by a set of This representation is approximate. Can represent distributions that

Outline. Binomial, Multinomial, Normal, Beta, Dirichlet. Posterior mean, MAP, credible interval, posterior distribution

Outline A short review on Bayesian analysis. Binomial, Multinomial, Normal, Beta, Dirichlet Posterior mean, MAP, credible interval, posterior distribution Gibbs sampling Revisit the Gaussian mixture model

Outline A short review on Bayesian analysis. Binomial, Multinomial, Normal, Beta, Dirichlet Posterior mean, MAP, credible interval, posterior distribution Gibbs sampling Revisit the Gaussian mixture model

Markov Chain Monte Carlo Methods for Stochastic Optimization

Markov Chain Monte Carlo Methods for Stochastic Optimization John R. Birge The University of Chicago Booth School of Business Joint work with Nicholas Polson, Chicago Booth. JRBirge U of Toronto, MIE,

Markov Chain Monte Carlo Methods for Stochastic Optimization John R. Birge The University of Chicago Booth School of Business Joint work with Nicholas Polson, Chicago Booth. JRBirge U of Toronto, MIE,

STA 4273H: Statistical Machine Learning

STA 4273H: Statistical Machine Learning Russ Salakhutdinov Department of Computer Science! Department of Statistical Sciences! rsalakhu@cs.toronto.edu! h0p://www.cs.utoronto.ca/~rsalakhu/ Lecture 7 Approximate

STA 4273H: Statistical Machine Learning Russ Salakhutdinov Department of Computer Science! Department of Statistical Sciences! rsalakhu@cs.toronto.edu! h0p://www.cs.utoronto.ca/~rsalakhu/ Lecture 7 Approximate

Particle Filtering Approaches for Dynamic Stochastic Optimization

Particle Filtering Approaches for Dynamic Stochastic Optimization John R. Birge The University of Chicago Booth School of Business Joint work with Nicholas Polson, Chicago Booth. JRBirge I-Sim Workshop,

Particle Filtering Approaches for Dynamic Stochastic Optimization John R. Birge The University of Chicago Booth School of Business Joint work with Nicholas Polson, Chicago Booth. JRBirge I-Sim Workshop,

Markov Chain Monte Carlo Methods for Stochastic

Markov Chain Monte Carlo Methods for Stochastic Optimization i John R. Birge The University of Chicago Booth School of Business Joint work with Nicholas Polson, Chicago Booth. JRBirge U Florida, Nov 2013

Markov Chain Monte Carlo Methods for Stochastic Optimization i John R. Birge The University of Chicago Booth School of Business Joint work with Nicholas Polson, Chicago Booth. JRBirge U Florida, Nov 2013

Infering the Number of State Clusters in Hidden Markov Model and its Extension

Infering the Number of State Clusters in Hidden Markov Model and its Extension Xugang Ye Department of Applied Mathematics and Statistics, Johns Hopkins University Elements of a Hidden Markov Model (HMM)

Infering the Number of State Clusters in Hidden Markov Model and its Extension Xugang Ye Department of Applied Mathematics and Statistics, Johns Hopkins University Elements of a Hidden Markov Model (HMM)

Open Economy Macroeconomics: Theory, methods and applications

Open Economy Macroeconomics: Theory, methods and applications Lecture 4: The state space representation and the Kalman Filter Hernán D. Seoane UC3M January, 2016 Today s lecture State space representation

Open Economy Macroeconomics: Theory, methods and applications Lecture 4: The state space representation and the Kalman Filter Hernán D. Seoane UC3M January, 2016 Today s lecture State space representation

I. Bayesian econometrics

I. Bayesian econometrics A. Introduction B. Bayesian inference in the univariate regression model C. Statistical decision theory Question: once we ve calculated the posterior distribution, what do we do

I. Bayesian econometrics A. Introduction B. Bayesian inference in the univariate regression model C. Statistical decision theory Question: once we ve calculated the posterior distribution, what do we do

High-dimensional Problems in Finance and Economics. Thomas M. Mertens

High-dimensional Problems in Finance and Economics Thomas M. Mertens NYU Stern Risk Economics Lab April 17, 2012 1 / 78 Motivation Many problems in finance and economics are high dimensional. Dynamic Optimization:

High-dimensional Problems in Finance and Economics Thomas M. Mertens NYU Stern Risk Economics Lab April 17, 2012 1 / 78 Motivation Many problems in finance and economics are high dimensional. Dynamic Optimization:

Online appendix to On the stability of the excess sensitivity of aggregate consumption growth in the US

Online appendix to On the stability of the excess sensitivity of aggregate consumption growth in the US Gerdie Everaert 1, Lorenzo Pozzi 2, and Ruben Schoonackers 3 1 Ghent University & SHERPPA 2 Erasmus

Online appendix to On the stability of the excess sensitivity of aggregate consumption growth in the US Gerdie Everaert 1, Lorenzo Pozzi 2, and Ruben Schoonackers 3 1 Ghent University & SHERPPA 2 Erasmus

Impulse-Response Analysis in Markov Switching Vector Autoregressive Models

Impulse-Response Analysis in Markov Switching Vector Autoregressive Models Hans-Martin Krolzig Economics Department, University of Kent, Keynes College, Canterbury CT2 7NP October 16, 2006 Abstract By

Impulse-Response Analysis in Markov Switching Vector Autoregressive Models Hans-Martin Krolzig Economics Department, University of Kent, Keynes College, Canterbury CT2 7NP October 16, 2006 Abstract By

Warwick Business School Forecasting System. Summary. Ana Galvao, Anthony Garratt and James Mitchell November, 2014

Warwick Business School Forecasting System Summary Ana Galvao, Anthony Garratt and James Mitchell November, 21 The main objective of the Warwick Business School Forecasting System is to provide competitive

Warwick Business School Forecasting System Summary Ana Galvao, Anthony Garratt and James Mitchell November, 21 The main objective of the Warwick Business School Forecasting System is to provide competitive

Stochastic process for macro

Stochastic process for macro Tianxiao Zheng SAIF 1. Stochastic process The state of a system {X t } evolves probabilistically in time. The joint probability distribution is given by Pr(X t1, t 1 ; X t2,

Stochastic process for macro Tianxiao Zheng SAIF 1. Stochastic process The state of a system {X t } evolves probabilistically in time. The joint probability distribution is given by Pr(X t1, t 1 ; X t2,

Estimating Markov-switching regression models in Stata

Estimating Markov-switching regression models in Stata Ashish Rajbhandari Senior Econometrician StataCorp LP Stata Conference 2015 Ashish Rajbhandari (StataCorp LP) Markov-switching regression Stata Conference

Estimating Markov-switching regression models in Stata Ashish Rajbhandari Senior Econometrician StataCorp LP Stata Conference 2015 Ashish Rajbhandari (StataCorp LP) Markov-switching regression Stata Conference

Ambiguous Business Cycles: Online Appendix

Ambiguous Business Cycles: Online Appendix By Cosmin Ilut and Martin Schneider This paper studies a New Keynesian business cycle model with agents who are averse to ambiguity (Knightian uncertainty). Shocks

Ambiguous Business Cycles: Online Appendix By Cosmin Ilut and Martin Schneider This paper studies a New Keynesian business cycle model with agents who are averse to ambiguity (Knightian uncertainty). Shocks

Computer Vision Group Prof. Daniel Cremers. 10a. Markov Chain Monte Carlo

Group Prof. Daniel Cremers 10a. Markov Chain Monte Carlo Markov Chain Monte Carlo In high-dimensional spaces, rejection sampling and importance sampling are very inefficient An alternative is Markov Chain

Group Prof. Daniel Cremers 10a. Markov Chain Monte Carlo Markov Chain Monte Carlo In high-dimensional spaces, rejection sampling and importance sampling are very inefficient An alternative is Markov Chain

Timevarying VARs. Wouter J. Den Haan London School of Economics. c Wouter J. Den Haan

Timevarying VARs Wouter J. Den Haan London School of Economics c Wouter J. Den Haan Time-Varying VARs Gibbs-Sampler general idea probit regression application (Inverted Wishart distribution Drawing from

Timevarying VARs Wouter J. Den Haan London School of Economics c Wouter J. Den Haan Time-Varying VARs Gibbs-Sampler general idea probit regression application (Inverted Wishart distribution Drawing from

Modeling conditional distributions with mixture models: Applications in finance and financial decision-making

Modeling conditional distributions with mixture models: Applications in finance and financial decision-making John Geweke University of Iowa, USA Journal of Applied Econometrics Invited Lecture Università

Modeling conditional distributions with mixture models: Applications in finance and financial decision-making John Geweke University of Iowa, USA Journal of Applied Econometrics Invited Lecture Università

Non-Markovian Regime Switching with Endogenous States and Time-Varying State Strengths

WORKING PAPER SERIES Non-Markovian Regime Switching with Endogenous States and Time-Varying State Strengths Siddhartha Chib and Michael Dueker Working Paper 2004-030A http://research.stlouisfed.org/wp/2004/2004-030.pdf

WORKING PAPER SERIES Non-Markovian Regime Switching with Endogenous States and Time-Varying State Strengths Siddhartha Chib and Michael Dueker Working Paper 2004-030A http://research.stlouisfed.org/wp/2004/2004-030.pdf

X t = a t + r t, (7.1)

") Chapter 7 State Space Models 71 Introduction State Space models, developed over the past 10 20 years, are alternative models for time series They include both the ARIMA models of Chapters 3 6 and the Classical

Chapter 7 State Space Models 71 Introduction State Space models, developed over the past 10 20 years, are alternative models for time series They include both the ARIMA models of Chapters 3 6 and the Classical

FEDERAL RESERVE BANK of ATLANTA

FEDERAL RESERVE BANK of ATLANTA Understanding Markov-Switching Rational Expectations Models Roger E.A. Farmer, Daniel F. Waggoner, and Tao Zha Working Paper 2009-5 March 2009 WORKING PAPER SERIES FEDERAL

FEDERAL RESERVE BANK of ATLANTA Understanding Markov-Switching Rational Expectations Models Roger E.A. Farmer, Daniel F. Waggoner, and Tao Zha Working Paper 2009-5 March 2009 WORKING PAPER SERIES FEDERAL

Motivation Non-linear Rational Expectations The Permanent Income Hypothesis The Log of Gravity Non-linear IV Estimation Summary.

Econometrics I Department of Economics Universidad Carlos III de Madrid Master in Industrial Economics and Markets Outline Motivation 1 Motivation 2 3 4 5 Motivation Hansen's contributions GMM was developed

Econometrics I Department of Economics Universidad Carlos III de Madrid Master in Industrial Economics and Markets Outline Motivation 1 Motivation 2 3 4 5 Motivation Hansen's contributions GMM was developed

IMPLIED DISTRIBUTIONS IN MULTIPLE CHANGE POINT PROBLEMS

IMPLIED DISTRIBUTIONS IN MULTIPLE CHANGE POINT PROBLEMS J. A. D. ASTON 1,2, J. Y. PENG 3 AND D. E. K. MARTIN 4 1 CENTRE FOR RESEARCH IN STATISTICAL METHODOLOGY, WARWICK UNIVERSITY 2 INSTITUTE OF STATISTICAL

IMPLIED DISTRIBUTIONS IN MULTIPLE CHANGE POINT PROBLEMS J. A. D. ASTON 1,2, J. Y. PENG 3 AND D. E. K. MARTIN 4 1 CENTRE FOR RESEARCH IN STATISTICAL METHODOLOGY, WARWICK UNIVERSITY 2 INSTITUTE OF STATISTICAL

Bayesian Dynamic Linear Modelling for. Complex Computer Models

Bayesian Dynamic Linear Modelling for Complex Computer Models Fei Liu, Liang Zhang, Mike West Abstract Computer models may have functional outputs. With no loss of generality, we assume that a single computer

Bayesian Dynamic Linear Modelling for Complex Computer Models Fei Liu, Liang Zhang, Mike West Abstract Computer models may have functional outputs. With no loss of generality, we assume that a single computer

Federal Reserve Bank of Chicago

Federal Reserve Bank of Chicago Modeling the Evolution of Expectations and Uncertainty in General Equilibrium Francesco Bianchi and Leonardo Melosi September 2013 WP 2013-12 Modeling the Evolution of Expectations

Federal Reserve Bank of Chicago Modeling the Evolution of Expectations and Uncertainty in General Equilibrium Francesco Bianchi and Leonardo Melosi September 2013 WP 2013-12 Modeling the Evolution of Expectations

STAT Financial Time Series

STAT 6104 - Financial Time Series Chapter 4 - Estimation in the time Domain Chun Yip Yau (CUHK) STAT 6104:Financial Time Series 1 / 46 Agenda 1 Introduction 2 Moment Estimates 3 Autoregressive Models (AR

STAT 6104 - Financial Time Series Chapter 4 - Estimation in the time Domain Chun Yip Yau (CUHK) STAT 6104:Financial Time Series 1 / 46 Agenda 1 Introduction 2 Moment Estimates 3 Autoregressive Models (AR

Constructing Turning Point Chronologies with Markov Switching Vector Autoregressive Models: the Euro Zone Business Cycle

Constructing Turning Point Chronologies with Markov Switching Vector Autoregressive Models: the Euro Zone Business Cycle Hans Martin Krolzig Department of Economics and Nuffield College, Oxford University.

Constructing Turning Point Chronologies with Markov Switching Vector Autoregressive Models: the Euro Zone Business Cycle Hans Martin Krolzig Department of Economics and Nuffield College, Oxford University.

Assessing Structural VAR s

... Assessing Structural VAR s by Lawrence J. Christiano, Martin Eichenbaum and Robert Vigfusson Zurich, September 2005 1 Background Structural Vector Autoregressions Address the Following Type of Question:

... Assessing Structural VAR s by Lawrence J. Christiano, Martin Eichenbaum and Robert Vigfusson Zurich, September 2005 1 Background Structural Vector Autoregressions Address the Following Type of Question:

Bayesian Inference for DSGE Models. Lawrence J. Christiano

Bayesian Inference for DSGE Models Lawrence J. Christiano Outline State space-observer form. convenient for model estimation and many other things. Preliminaries. Probabilities. Maximum Likelihood. Bayesian

Bayesian Inference for DSGE Models Lawrence J. Christiano Outline State space-observer form. convenient for model estimation and many other things. Preliminaries. Probabilities. Maximum Likelihood. Bayesian

Statistical Inference and Methods

Department of Mathematics Imperial College London d.stephens@imperial.ac.uk http://stats.ma.ic.ac.uk/ das01/ 31st January 2006 Part VI Session 6: Filtering and Time to Event Data Session 6: Filtering and

Department of Mathematics Imperial College London d.stephens@imperial.ac.uk http://stats.ma.ic.ac.uk/ das01/ 31st January 2006 Part VI Session 6: Filtering and Time to Event Data Session 6: Filtering and

1. The Multivariate Classical Linear Regression Model

Business School, Brunel University MSc. EC550/5509 Modelling Financial Decisions and Markets/Introduction to Quantitative Methods Prof. Menelaos Karanasos (Room SS69, Tel. 08956584) Lecture Notes 5. The

Business School, Brunel University MSc. EC550/5509 Modelling Financial Decisions and Markets/Introduction to Quantitative Methods Prof. Menelaos Karanasos (Room SS69, Tel. 08956584) Lecture Notes 5. The

Program. The. provide the. coefficientss. (b) References. y Watson. probability (1991), "A. Stock. Arouba, Diebold conditions" based on monthly

References. y Watson. probability (1991), A. Stock. Arouba, Diebold conditions based on monthly") Macroeconomic Forecasting Topics October 6 th to 10 th, 2014 Banco Central de Venezuela Caracas, Venezuela Program Professor: Pablo Lavado The aim of this course is to provide the basis for short term

Macroeconomic Forecasting Topics October 6 th to 10 th, 2014 Banco Central de Venezuela Caracas, Venezuela Program Professor: Pablo Lavado The aim of this course is to provide the basis for short term

Seoul National University Mini-Course: Monetary & Fiscal Policy Interactions II

Seoul National University Mini-Course: Monetary & Fiscal Policy Interactions II Eric M. Leeper Indiana University July/August 2013 Linear Analysis Generalize policy behavior with a conventional parametric

Seoul National University Mini-Course: Monetary & Fiscal Policy Interactions II Eric M. Leeper Indiana University July/August 2013 Linear Analysis Generalize policy behavior with a conventional parametric

Confronting Model Misspecification in Macroeconomics

FEDERAL RESERVE BANK of ATLANTA WORKING PAPER SERIES Confronting Model Misspecification in Macroeconomics Daniel F. Waggoner and Tao Zha Working Paper 2010-18a February 2012 Abstract: We estimate a Markov-switching

FEDERAL RESERVE BANK of ATLANTA WORKING PAPER SERIES Confronting Model Misspecification in Macroeconomics Daniel F. Waggoner and Tao Zha Working Paper 2010-18a February 2012 Abstract: We estimate a Markov-switching

Markov Switching Regular Vine Copulas

Int. Statistical Inst.: Proc. 58th World Statistical Congress, 2011, Dublin (Session CPS057) p.5304 Markov Switching Regular Vine Copulas Stöber, Jakob and Czado, Claudia Lehrstuhl für Mathematische Statistik,

Int. Statistical Inst.: Proc. 58th World Statistical Congress, 2011, Dublin (Session CPS057) p.5304 Markov Switching Regular Vine Copulas Stöber, Jakob and Czado, Claudia Lehrstuhl für Mathematische Statistik,

State-space Model. Eduardo Rossi University of Pavia. November Rossi State-space Model Financial Econometrics / 49

State-space Model Eduardo Rossi University of Pavia November 2013 Rossi State-space Model Financial Econometrics - 2013 1 / 49 Outline 1 Introduction 2 The Kalman filter 3 Forecast errors 4 State smoothing

State-space Model Eduardo Rossi University of Pavia November 2013 Rossi State-space Model Financial Econometrics - 2013 1 / 49 Outline 1 Introduction 2 The Kalman filter 3 Forecast errors 4 State smoothing

Econ 623 Econometrics II Topic 2: Stationary Time Series

1 Introduction Econ 623 Econometrics II Topic 2: Stationary Time Series In the regression model we can model the error term as an autoregression AR(1) process. That is, we can use the past value of the

1 Introduction Econ 623 Econometrics II Topic 2: Stationary Time Series In the regression model we can model the error term as an autoregression AR(1) process. That is, we can use the past value of the

Lecture 9: Markov Switching Models

Lecture 9: Markov Switching Models Prof. Massimo Guidolin 20192 Financial Econometrics Winter/Spring 2018 Overview Defining a Markov Switching VAR model Structure and mechanics of Markov Switching: from

Lecture 9: Markov Switching Models Prof. Massimo Guidolin 20192 Financial Econometrics Winter/Spring 2018 Overview Defining a Markov Switching VAR model Structure and mechanics of Markov Switching: from

ARIMA Modelling and Forecasting

ARIMA Modelling and Forecasting Economic time series often appear nonstationary, because of trends, seasonal patterns, cycles, etc. However, the differences may appear stationary. Δx t x t x t 1 (first

ARIMA Modelling and Forecasting Economic time series often appear nonstationary, because of trends, seasonal patterns, cycles, etc. However, the differences may appear stationary. Δx t x t x t 1 (first

An estimate of the long-run covariance matrix, Ω, is necessary to calculate asymptotic

Chapter 6 ESTIMATION OF THE LONG-RUN COVARIANCE MATRIX An estimate of the long-run covariance matrix, Ω, is necessary to calculate asymptotic standard errors for the OLS and linear IV estimators presented

Chapter 6 ESTIMATION OF THE LONG-RUN COVARIANCE MATRIX An estimate of the long-run covariance matrix, Ω, is necessary to calculate asymptotic standard errors for the OLS and linear IV estimators presented

9) Time series econometrics

Time series econometrics") 30C00200 Econometrics 9) Time series econometrics Timo Kuosmanen Professor Management Science http://nomepre.net/index.php/timokuosmanen 1 Macroeconomic data: GDP Inflation rate Examples of time series

30C00200 Econometrics 9) Time series econometrics Timo Kuosmanen Professor Management Science http://nomepre.net/index.php/timokuosmanen 1 Macroeconomic data: GDP Inflation rate Examples of time series

Asset Pricing. Question: What is the equilibrium price of a stock? Defn: a stock is a claim to a future stream of dividends. # X E β t U(c t ) t=0

t=0") Asset Pricing 1 Lucas (1978, Econometrica) Question: What is the equilibrium price of a stock? Defn: a stock is a claim to a future stream of dividends. 1.1 Environment Tastes: " # X E β t U( ) t=0 Technology:

Asset Pricing 1 Lucas (1978, Econometrica) Question: What is the equilibrium price of a stock? Defn: a stock is a claim to a future stream of dividends. 1.1 Environment Tastes: " # X E β t U( ) t=0 Technology:

Sequential Monte Carlo Methods (for DSGE Models)

") Sequential Monte Carlo Methods (for DSGE Models) Frank Schorfheide University of Pennsylvania, PIER, CEPR, and NBER October 23, 2017 Some References These lectures use material from our joint work: Tempered

Sequential Monte Carlo Methods (for DSGE Models) Frank Schorfheide University of Pennsylvania, PIER, CEPR, and NBER October 23, 2017 Some References These lectures use material from our joint work: Tempered

Bayesian Modeling of Conditional Distributions

Bayesian Modeling of Conditional Distributions John Geweke University of Iowa Indiana University Department of Economics February 27, 2007 Outline Motivation Model description Methods of inference Earnings

Bayesian Modeling of Conditional Distributions John Geweke University of Iowa Indiana University Department of Economics February 27, 2007 Outline Motivation Model description Methods of inference Earnings

Structural Interpretation of Vector Autoregressions with Incomplete Identification: Revisiting the Role of Oil Supply and Demand Shocks

Structural Interpretation of Vector Autoregressions with Incomplete Identification: Revisiting the Role of Oil Supply and Demand Shocks Christiane Baumeister, University of Notre Dame James D. Hamilton,

Structural Interpretation of Vector Autoregressions with Incomplete Identification: Revisiting the Role of Oil Supply and Demand Shocks Christiane Baumeister, University of Notre Dame James D. Hamilton,

Structural VAR Models and Applications

Structural VAR Models and Applications Laurent Ferrara 1 1 University of Paris Nanterre M2 Oct. 2018 SVAR: Objectives Whereas the VAR model is able to capture efficiently the interactions between the different

Structural VAR Models and Applications Laurent Ferrara 1 1 University of Paris Nanterre M2 Oct. 2018 SVAR: Objectives Whereas the VAR model is able to capture efficiently the interactions between the different

Machine Learning 4771

Machine Learning 4771 Instructor: ony Jebara Kalman Filtering Linear Dynamical Systems and Kalman Filtering Structure from Motion Linear Dynamical Systems Audio: x=pitch y=acoustic waveform Vision: x=object

Machine Learning 4771 Instructor: ony Jebara Kalman Filtering Linear Dynamical Systems and Kalman Filtering Structure from Motion Linear Dynamical Systems Audio: x=pitch y=acoustic waveform Vision: x=object

Financial Factors in Economic Fluctuations. Lawrence Christiano Roberto Motto Massimo Rostagno

Financial Factors in Economic Fluctuations Lawrence Christiano Roberto Motto Massimo Rostagno Background Much progress made on constructing and estimating models that fit quarterly data well (Smets-Wouters,

Financial Factors in Economic Fluctuations Lawrence Christiano Roberto Motto Massimo Rostagno Background Much progress made on constructing and estimating models that fit quarterly data well (Smets-Wouters,

Identifying the Monetary Policy Shock Christiano et al. (1999)

") Identifying the Monetary Policy Shock Christiano et al. (1999) The question we are asking is: What are the consequences of a monetary policy shock a shock which is purely related to monetary conditions

Identifying the Monetary Policy Shock Christiano et al. (1999) The question we are asking is: What are the consequences of a monetary policy shock a shock which is purely related to monetary conditions

Labor-Supply Shifts and Economic Fluctuations. Technical Appendix

Labor-Supply Shifts and Economic Fluctuations Technical Appendix Yongsung Chang Department of Economics University of Pennsylvania Frank Schorfheide Department of Economics University of Pennsylvania January

Labor-Supply Shifts and Economic Fluctuations Technical Appendix Yongsung Chang Department of Economics University of Pennsylvania Frank Schorfheide Department of Economics University of Pennsylvania January

Session 5B: A worked example EGARCH model

Session 5B: A worked example EGARCH model John Geweke Bayesian Econometrics and its Applications August 7, worked example EGARCH model August 7, / 6 EGARCH Exponential generalized autoregressive conditional

Session 5B: A worked example EGARCH model John Geweke Bayesian Econometrics and its Applications August 7, worked example EGARCH model August 7, / 6 EGARCH Exponential generalized autoregressive conditional

Y t = log (employment t )

") Advanced Macroeconomics, Christiano Econ 416 Homework #7 Due: November 21 1. Consider the linearized equilibrium conditions of the New Keynesian model, on the slide, The Equilibrium Conditions in the handout,

Advanced Macroeconomics, Christiano Econ 416 Homework #7 Due: November 21 1. Consider the linearized equilibrium conditions of the New Keynesian model, on the slide, The Equilibrium Conditions in the handout,

Machine Learning. Gaussian Mixture Models. Zhiyao Duan & Bryan Pardo, Machine Learning: EECS 349 Fall

Machine Learning Gaussian Mixture Models Zhiyao Duan & Bryan Pardo, Machine Learning: EECS 349 Fall 2012 1 The Generative Model POV We think of the data as being generated from some process. We assume

Machine Learning Gaussian Mixture Models Zhiyao Duan & Bryan Pardo, Machine Learning: EECS 349 Fall 2012 1 The Generative Model POV We think of the data as being generated from some process. We assume

Postestimation commands predict estat Remarks and examples Stored results Methods and formulas

Title stata.com mswitch postestimation Postestimation tools for mswitch Postestimation commands predict estat Remarks and examples Stored results Methods and formulas References Also see Postestimation

Title stata.com mswitch postestimation Postestimation tools for mswitch Postestimation commands predict estat Remarks and examples Stored results Methods and formulas References Also see Postestimation

Assessing Structural Convergence between Romanian Economy and Euro Area: A Bayesian Approach

Vol. 3, No.3, July 2013, pp. 372 383 ISSN: 2225-8329 2013 HRMARS www.hrmars.com Assessing Structural Convergence between Romanian Economy and Euro Area: A Bayesian Approach Alexie ALUPOAIEI 1 Ana-Maria

Vol. 3, No.3, July 2013, pp. 372 383 ISSN: 2225-8329 2013 HRMARS www.hrmars.com Assessing Structural Convergence between Romanian Economy and Euro Area: A Bayesian Approach Alexie ALUPOAIEI 1 Ana-Maria

Bayesian Methods for Machine Learning

Bayesian Methods for Machine Learning CS 584: Big Data Analytics Material adapted from Radford Neal s tutorial (http://ftp.cs.utoronto.ca/pub/radford/bayes-tut.pdf), Zoubin Ghahramni (http://hunch.net/~coms-4771/zoubin_ghahramani_bayesian_learning.pdf),

Bayesian Methods for Machine Learning CS 584: Big Data Analytics Material adapted from Radford Neal s tutorial (http://ftp.cs.utoronto.ca/pub/radford/bayes-tut.pdf), Zoubin Ghahramni (http://hunch.net/~coms-4771/zoubin_ghahramani_bayesian_learning.pdf),