Chapter 7. Hypothesis Tests and Confidence Intervals in Multiple Regression

|

|

|

- Jasmin George

- 6 years ago

- Views:

Transcription

1 Chapter 7 Hypothesis Tests and Confidence Intervals in Multiple Regression

2 Outline 1. Hypothesis tests and confidence intervals for a single coefficie. Joint hypothesis tests on multiple coefficients 3. Other types of hypotheses involving multiple coefficients 4. How to decide what variables to include in a regression model

3 3 Hypothesis Tests and Confidence Intervals for a Single Coefficient in Multiple Regression (SW Section 7.1) ˆ β E( ˆ β ) var( ˆ β ) is approximately distributed N(0,1) (CLT). Thus hypotheses on β 1 can be tested using the usual t-statistic, and confidence intervals are constructed as { ˆ β 1 ± 1.96 SE( ˆ β 1 )}. So too for β,, β k. ˆ β 1 and ˆ β are generally not independently distributed so neither are their t-statistics (more on this later).

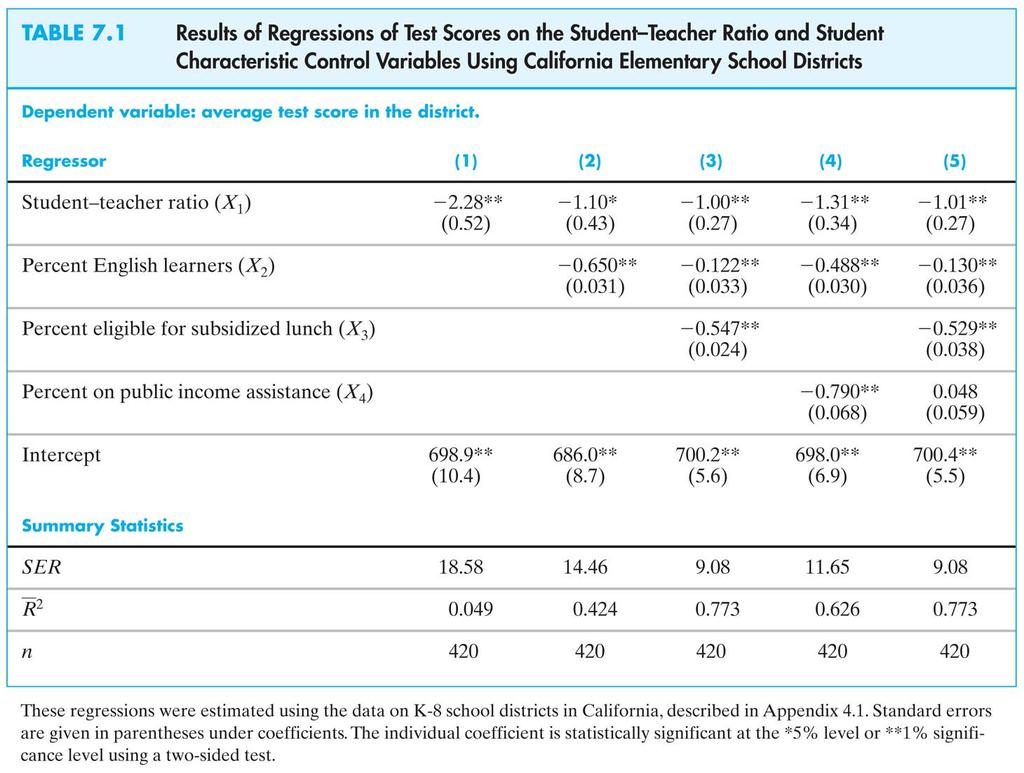

4 Example: The California class size data (1) TestScore = STR (10.4) (0.5) () TestScore = STR 0.650PctEL (8.7) (0.43) (0.031) The coefficient on STR in () is the effect on TestScores of a unit change in STR, holding constant the percentage of English Learners in the district The coefficient on STR falls by one-half The 95% confidence interval for coefficient on STR in () is { 1.10 ± } = ( 1.95, 0.6) The t-statistic testing β STR = 0 is t = 1.10/0.43 =.54, so we reject the hypothesis at the 5% significance level 4

5 Standard errors in multiple regression in STATA reg testscr str pctel, robust; Regression with robust standard errors Number of obs = 40 F(, 417) = 3.8 Prob > F = R-squared = Root MSE = Robust testscr Coef. Std. Err. t P> t [95% Conf. Interval] str pctel _cons TestScore = STR 0.650PctEL (8.7) (0.43) (0.031) We use heteroskedasticity-robust standard errors for exactly the same reason as in the case of a single regressor. 5

6 6 Tests of Joint Hypotheses (SW Section 7.) Let Expn = expenditures per pupil and consider the population regression model: TestScore i = β 0 + β 1 STR i + β Expn i + β 3 PctEL i + u i The null hypothesis that school resources don t matter, and the alternative that they do, corresponds to: H 0 : β 1 = 0 and β = 0 vs. H 1 : either β 1 0 or β 0 or both TestScore i = β 0 + β 1 STR i + β Expn i + β 3 PctEL i + u i

7 7 Tests of joint hypotheses, ctd. H 0 : β 1 = 0 and β = 0 vs. H 1 : either β 1 0 or β 0 or both A joint hypothesis specifies a value for two or more coefficients, that is, it imposes a restriction on two or more coefficients. In general, a joint hypothesis will involve q restrictions. In the example above, q =, and the two restrictions are β 1 = 0 and β = 0. A common sense idea is to reject if either of the individual t-statistics exceeds 1.96 in absolute value. But this one at a time test isn t valid: the resulting test rejects too often under the null hypothesis (more than 5%)!

8 Why can t we just test the coefficients one at a time? Because the rejection rate under the null isn t 5%. We ll calculate the probability of incorrectly rejecting the null using the common sense test based on the two individual t-statistics. To simplify the calculation, suppose that ˆ β 1 and ˆ β are independently distributed. Let t 1 and t be the t-statistics: ˆ β1 0 ˆ β 0 t 1 = and t SE( ˆ = β ) SE( ˆ β ) The one at time test is: reject H 0 : β 1 = β = 0 if t 1 > 1.96 and/or t > What is the probability that this one at a time test rejects H 0, when H 0 is actually true? (It should be 5%.) 8

9 Suppose t 1 and t are independent (for this calculation). The probability of incorrectly rejecting the null hypothesis using the one at a time test = Pr H [ t 1 > 1.96 and/or t > 1.96] = = 0 Pr H [ t 0 1 > 1.96, t > 1.96] + Pr H [ t 0 1 > 1.96, t 1.96] + Pr H [ t , t > 1.96] (disjoint events) 0 Pr H [ t 0 1 > 1.96] + + Pr H [ t 0 1 > 1.96] Pr H [ t 0 > 1.96] Pr H [ t ] Pr H [ t ] Pr H [ t 0 > 1.96] (t 1, t are independent by assumption) = =.0975 = 9.75% which is not the desired 5%!! 9

10 10 The size of a test is the actual rejection rate under the null hypothesis. The size of the common sense test isn t 5%! In fact, its size depends on the correlation between t 1 and t (and thus on the correlation between ˆ β 1 and ˆ β ). Two Solutions: Use a different critical value in this procedure not 1.96 (this is the Bonferroni method see SW App. 7.1) (this method is rarely used in practice however) Use a different test statistic that test both β 1 and β at once: the F- statistic (this is common practice)

11 The F-statistic The F-statistic tests all parts of a joint hypothesis at once. Formula for the special case of the joint hypothesis β 1 = β 1,0 and β = β,0 in a regression with two regressors: 1 t + t ˆ ρt 1 ttt F = 1 ˆ ρt 1, t 1, 1 where ρ estimates the correlation between t 1 and t. ˆt, t 1 Reject when F is large (how large?) 11

12 1 The F-statistic testing β 1 and β : 1 t + t ˆ ρt 1 ttt F = 1 ˆ ρt 1, t 1, 1 The F-statistic is large when t 1 and/or t is large The F-statistic corrects (in just the right way) for the correlation between t 1 and t. The formula for more than two β s is nasty unless you use matrix algebra. This gives the F-statistic a nice large-sample approximate distribution, which is

13 13 Large-sample distribution of the F-statistic Consider special case that t 1 and t are independent, so in large samples the formula becomes ρ p 0; ˆt, t 1 1 t + t ˆ ρt 1 ttt F = 1 ˆ ρt 1, t 1, 1 1 ( ) 1 t + t Under the null, t 1 and t have standard normal distributions that, in this special case, are independent The large-sample distribution of the F-statistic is the distribution of the average of two independently distributed squared standard normal random variables.

14 14 The chi-squared distribution with q degrees of freedom ( χ ) is defined to be the distribution of the sum of q independent squared standard normal random variables. q In large samples, F is distributed as χ q /q. Selected large-sample critical values of χ q /q q 5% critical value (why?) 3.00 (the case q= above)

15 15 Computing the p-value using the F-statistic: p-value = tail probability of the χ q /q distribution beyond the F-statistic actually computed. Implementation in STATA Use the test command after the regression Example: Test the joint hypothesis that the population coefficients on STR and expenditures per pupil (expn_stu) are both zero, against the alternative that at least one of the population coefficients is nonzero.

16 F-test example, California class size data: reg testscr str expn_stu pctel, r; Regression with robust standard errors Number of obs = 40 F( 3, 416) = Prob > F = R-squared = Root MSE = Robust testscr Coef. Std. Err. t P> t [95% Conf. Interval] str expn_stu pctel _cons NOTE test str expn_stu; The test command follows the regression ( 1) str = 0.0 There are q= restrictions being tested ( ) expn_stu = 0.0 F(, 416) = 5.43 The 5% critical value for q= is 3.00 Prob > F = Stata computes the p-value for you 16

17 17 More on F-statistics: a simple F-statistic formula that is easy to understand (it is only valid if the errors are homoskedastic, but it might help intuition). The homoskedasticity-only F-statistic When the errors are homoskedastic, there is a simple formula for computing the homoskedasticity-only F-statistic: Run two regressions, one under the null hypothesis (the restricted regression) and one under the alternative hypothesis (the unrestricted regression). Compare the fits of the regressions the R s if the unrestricted model fits sufficiently better, reject the null

18 18 The restricted and unrestricted regressions Example: are the coefficients on STR and Expn zero? Unrestricted population regression (under H 1 ): TestScore i = β 0 + β 1 STR i + β Expn i + β 3 PctEL i + u i Restricted population regression (that is, under H 0 ): TestScore i = β 0 + β 3 PctEL i + u i (why?) The number of restrictions under H 0 is q = (why?). The fit will be better (R will be higher) in the unrestricted regression (why?) By how much must the R increase for the coefficients on Expn and PctEL to be judged statistically significant?

19 Simple formula for the homoskedasticity-only F-statistic: where: F = ( Runrestricted Rrestricted )/ q unrestricted unrestricted (1 R ) /( n k 1) R restricted = the R for the restricted regression R unrestricted = the R for the unrestricted regression q = the number of restrictions under the null k unrestricted = the number of regressors in the unrestricted regression. The bigger the difference between the restricted and unrestricted R s the greater the improvement in fit by adding the variables in question the larger is the homoskedasticity-only F. 19

20 Example: Restricted regression: TestScore = PctEL, (1.0) (0.03) Unrestricted regression: R restricted = TestScore = STR Expn 0.656PctEL (15.5) (0.48) (1.59) (0.03) R unrestricted = , k unrestricted = 3, q = ( Runrestricted Rrestricted )/ q so F = (1 Runrestricted ) /( n kunrestricted 1) ( ) / = = 8.01 (1.4366) /(40 3 1) Note: Heteroskedasticity-robust F =

21 1 The homoskedasticity-only F-statistic summary F = ( Runrestricted Rrestricted )/ q unrestricted unrestricted (1 R ) /( n k 1) The homoskedasticity-only F-statistic rejects when adding the two variables increased the R by enough that is, when adding the two variables improves the fit of the regression by enough If the errors are homoskedastic, then the homoskedasticity- only F-statistic has a large-sample distribution that is χ q /q. But if the errors are heteroskedastic, the large-sample distribution is a mess and is not χ /q q

22 Digression: The F distribution Your regression printouts might refer to the F distribution. If the four multiple regression LS assumptions hold and: 5. u i is homoskedastic, that is, var(u X 1,,X k ) does not depend on X s 6. u 1,,u n are normally distributed then the homoskedasticity-only F-statistic has the F q,n-k 1 distribution, where q = the number of restrictions and k = the number of regressors under the alternative (the unrestricted model). The F distribution is to the χ q /q distribution what the t n 1 distribution is to the N(0,1) distribution

23 The F q,n k 1 distribution: The F distribution is tabulated many places As n, the F q,n-k 1 distribution asymptotes to the distribution: χ q /q The F q, and χ q /q distributions are the same. For q not too big and n 100, the F q,n k 1 distribution and the χ q /q distribution are essentially identical. Many regression packages (including STATA) compute p- values of F-statistics using the F distribution You will encounter the F distribution in published empirical work. 3

24 4 Another digression: A little history of statistics The theory of the homoskedasticity-only F-statistic and the F q,n k 1 distributions rests on implausibly strong assumptions (are earnings normally distributed?) These statistics dates to the early 0 th century back in the days when data sets were small and computers were people The F-statistic and F q,n k 1 distribution were major breakthroughs: an easily computed formula; a single set of tables that could be published once, then applied in many settings; and a precise, mathematically elegant justification.

25 5 A little history of statistics, ctd The strong assumptions seemed a minor price for this breakthrough. But with modern computers and large samples we can use the heteroskedasticity-robust F-statistic and the F q, distribution, which only require the four least squares assumptions (not assumptions #5 and #6) This historical legacy persists in modern software, in which homoskedasticity-only standard errors (and F-statistics) are the default, and in which p-values are computed using the F q,n k 1 distribution.

26 6 Summary: the homoskedasticity-only F- statistic and the F distribution These are justified only under very strong conditions stronger than are realistic in practice. Yet, they are widely used. You should use the heteroskedasticity-robust F-statistic, with χ q /q (that is, F q, ) critical values. For n 100, the F-distribution essentially is the distribution. χ q /q For small n, sometimes researchers use the F distribution because it has larger critical values and in this sense is more conservative.

27 7 Summary: testing joint hypotheses The one at a time approach of rejecting if either of the t- statistics exceeds 1.96 rejects more than 5% of the time under the null (the size exceeds the desired significance level) The heteroskedasticity-robust F-statistic is built in to STATA ( test command); this tests all q restrictions at once. For n large, the F-statistic is distributed χ q /q (= F q, ) The homoskedasticity-only F-statistic is important historically (and thus in practice), and can help intuition, but isn t valid when there is heteroskedasticity

28 8 Testing Single Restrictions on Multiple Coefficients (SW Section 7.3) Y i = β 0 + β 1 X 1i + β X i + u i, i = 1,,n Consider the null and alternative hypothesis, H 0 : β 1 = β vs. H 1 : β 1 β This null imposes a single restriction (q = 1) on multiple coefficients it is not a joint hypothesis with multiple restrictions (compare with β 1 = 0 and β = 0).

29 Testing single restrictions on multiple coefficients, ctd. Here are two methods for testing single restrictions on multiple coefficients: 1. Rearrange ( transform ) the regression Rearrange the regressors so that the restriction becomes a restriction on a single coefficient in an equivalent regression; or,. Perform the test directly Some software, including STATA, lets you test restrictions using multiple coefficients directly 9

30 30 Method 1: Rearrange ( transform ) the regression Y i = β 0 + β 1 X 1i + β X i + u i H 0 : β 1 = β vs. H 1 : β 1 β Add and subtract β X 1i : Y i = β 0 + (β 1 β ) X 1i + β (X 1i + X i ) + u i or Y i = β 0 + γ 1 X 1i + β W i + u i where γ 1 = β 1 β W i = X 1i + X i

31 31 Rearrange the regression, ctd. (a) Original system: Y i = β 0 + β 1 X 1i + β X i + u i H 0 : β 1 = β vs. H 1 : β 1 β (b) Rearranged ( transformed ) system: Y i = β 0 + γ 1 X 1i + β W i + u i where γ 1 = β 1 β and W i = X 1i + X i so H 0 : γ 1 = 0 vs. H 1 : γ 1 0 The testing problem is now a simple one: test whether γ 1 = 0 in specification (b).

32 3 Method : Perform the test directly Y i = β 0 + β 1 X 1i + β X i + u i H 0 : β 1 = β vs. H 1 : β 1 β Example: TestScore i = β 0 + β 1 STR i + β Expn i + β 3 PctEL i + u i In STATA, to test β 1 = β vs. β 1 β (two-sided): regress testscore str expn pctel, r test str=expn The details of implementing this method are software-specific.

33 33 Confidence Sets for Multiple Coefficients (SW Section 7.4) Y i = β 0 + β 1 X 1i + β X i + + β k X ki + u i, i = 1,,n What is a joint confidence set for β 1 and β? A 95% joint confidence set is: A set-valued function of the data that contains the true parameter(s) in 95% of hypothetical repeated samples. The set of parameter values that cannot be rejected at the 5% significance level. You can find a 95% confidence set as the set of (β 1, β ) that cannot be rejected at the 5% level using an F-test (why not just combine the two 95% confidence intervals?).

34 34 Joint confidence sets ctd. Let F(β 1,0,β,0 ) be the (heteroskedasticity-robust) F-statistic testing the hypothesis that β 1 = β 1, 0 and β = β,0 : 95% confidence set = {β 1,0, β,0 : F(β 1,0, β,0 ) < 3.00} 3.00 is the 5% critical value of the F, distribution This set has coverage rate 95% because the test on which it is based (the test it inverts ) has size of 5% 5% of the time, the test incorrectly rejects the null when the null is true, so 95% of the time it does not; therefore the confidence set constructed as the nonrejected values contains the true value 95% of the time (in 95% of all samples).

35 35 The confidence set based on the F-statistic is an ellipse 1 t + t ˆ ρt 1 ttt {β 1, β : F = 1 ˆ ρt 1, t Now 1 F = t1 + t ˆ ρt 1, ttt 1 (1 ˆ ρ ) t, t 1 1 = (1 ˆ ρ ) t, t 1 1, } ˆ β β ˆ,0 β1 β ˆ ˆ 1,0 β1 β 1,0 β β,0 ˆt 1, t ˆ + ˆ + ρ SE( β ˆ ˆ ) SE( β1) SE( β1) SE( β) This is a quadratic form in β 1,0 and β,0 thus the boundary of the set F = 3.00 is an ellipse.

36 36 Confidence set based on inverting the F-statistic

37 An example of a multiple regression analysis and how to decide which variables to include in a regression A Closer Look at the Test Score Data (SW Sections 7.5 and 7.6) We want to get an unbiased estimate of the effect on test scores of changing class size, holding constant student and school characteristics (but not necessarily holding constant the budget (why?)). To do this we need to think about what variables to include and what regressions to run and we should do this before we actually sit down at the computer. This entails thinking beforehand about your model specification. 37

38 38 A general approach to variable selection and model specification Specify a base or benchmark model. Specify a range of plausible alternative models, which include additional candidate variables. Does a candidate variable change the coefficient of interest (β 1 )? Is a candidate variable statistically significant? Use judgment, not a mechanical recipe Don t just try to maximize R!

39 39 Digression about measures of fit It is easy to fall into the trap of maximizing the R and R but this loses sight of our real objective, an unbiased estimator of the class size effect. A high R (or R ) means that the regressors explain the variation in Y. A high R (or R ) does not mean that you have eliminated omitted variable bias. A high R (or R ) does not mean that you have an unbiased estimator of a causal effect (β 1 ). A high R (or R ) does not mean that the included variables are statistically significant this must be determined using hypotheses tests.

40 40 Back to the test score application: What variables would you want ideally to estimate the effect on test scores of STR using school district data? Variables actually in the California class size data set: student-teacher ratio (STR) percent English learners in the district (PctEL) school expenditures per pupil name of the district (so we could look up average rainfall, for example) percent eligible for subsidized/free lunch percent on public income assistance average district income Which of these variables would you want to include?

41 More California data 41

42 Digression on presentation of regression results We have a number of regressions and we want to report them. It is awkward and difficult to read regressions written out in equation form, so instead it is conventional to report them in a table. A table of regression results should include: estimated regression coefficients standard errors measures of fit number of observations relevant F-statistics, if any Any other pertinent information. Find this information in the following table: 4

43 43

44 44 Summary: Multiple Regression Multiple regression allows you to estimate the effect on Y of a change in X 1, holding X constant. If you can measure a variable, you can avoid omitted variable bias from that variable by including it. There is no simple recipe for deciding which variables belong in a regression you must exercise judgment. One approach is to specify a base model relying on a- priori reasoning then explore the sensitivity of the key estimate(s) in alternative specifications.

Hypothesis Tests and Confidence Intervals in Multiple Regression

Hypothesis Tests and Confidence Intervals in Multiple Regression (SW Chapter 7) Outline 1. Hypothesis tests and confidence intervals for one coefficient. Joint hypothesis tests on multiple coefficients

Hypothesis Tests and Confidence Intervals in Multiple Regression (SW Chapter 7) Outline 1. Hypothesis tests and confidence intervals for one coefficient. Joint hypothesis tests on multiple coefficients

Hypothesis Tests and Confidence Intervals. in Multiple Regression

ECON4135, LN6 Hypothesis Tests and Confidence Intervals Outline 1. Why multipple regression? in Multiple Regression (SW Chapter 7) 2. Simpson s paradox (omitted variables bias) 3. Hypothesis tests and

ECON4135, LN6 Hypothesis Tests and Confidence Intervals Outline 1. Why multipple regression? in Multiple Regression (SW Chapter 7) 2. Simpson s paradox (omitted variables bias) 3. Hypothesis tests and

Introduction to Econometrics. Multiple Regression

Introduction to Econometrics The statistical analysis of economic (and related) data STATS301 Multiple Regression Titulaire: Christopher Bruffaerts Assistant: Lorenzo Ricci 1 OLS estimate of the TS/STR

Introduction to Econometrics The statistical analysis of economic (and related) data STATS301 Multiple Regression Titulaire: Christopher Bruffaerts Assistant: Lorenzo Ricci 1 OLS estimate of the TS/STR

Introduction to Econometrics. Multiple Regression (2016/2017)

") Introduction to Econometrics STAT-S-301 Multiple Regression (016/017) Lecturer: Yves Dominicy Teaching Assistant: Elise Petit 1 OLS estimate of the TS/STR relation: OLS estimate of the Test Score/STR relation:

Introduction to Econometrics STAT-S-301 Multiple Regression (016/017) Lecturer: Yves Dominicy Teaching Assistant: Elise Petit 1 OLS estimate of the TS/STR relation: OLS estimate of the Test Score/STR relation:

The F distribution. If: 1. u 1,,u n are normally distributed; and 2. X i is distributed independently of u i (so in particular u i is homoskedastic)

") The F distribution If: 1. u 1,,u n are normally distributed; and. X i is distributed independently of u i (so in particular u i is homoskedastic) then the homoskedasticity-only F-statistic has the F q,n-k

The F distribution If: 1. u 1,,u n are normally distributed; and. X i is distributed independently of u i (so in particular u i is homoskedastic) then the homoskedasticity-only F-statistic has the F q,n-k

Applied Statistics and Econometrics

Applied Statistics and Econometrics Lecture 7 Saul Lach September 2017 Saul Lach () Applied Statistics and Econometrics September 2017 1 / 68 Outline of Lecture 7 1 Empirical example: Italian labor force

Applied Statistics and Econometrics Lecture 7 Saul Lach September 2017 Saul Lach () Applied Statistics and Econometrics September 2017 1 / 68 Outline of Lecture 7 1 Empirical example: Italian labor force

ECON Introductory Econometrics. Lecture 7: OLS with Multiple Regressors Hypotheses tests

ECON4150 - Introductory Econometrics Lecture 7: OLS with Multiple Regressors Hypotheses tests Monique de Haan (moniqued@econ.uio.no) Stock and Watson Chapter 7 Lecture outline 2 Hypothesis test for single

ECON4150 - Introductory Econometrics Lecture 7: OLS with Multiple Regressors Hypotheses tests Monique de Haan (moniqued@econ.uio.no) Stock and Watson Chapter 7 Lecture outline 2 Hypothesis test for single

Recall that a measure of fit is the sum of squared residuals: where. The F-test statistic may be written as:

1 Joint hypotheses The null and alternative hypotheses can usually be interpreted as a restricted model ( ) and an model ( ). In our example: Note that if the model fits significantly better than the restricted

1 Joint hypotheses The null and alternative hypotheses can usually be interpreted as a restricted model ( ) and an model ( ). In our example: Note that if the model fits significantly better than the restricted

Nonlinear Regression Functions

Nonlinear Regression Functions (SW Chapter 8) Outline 1. Nonlinear regression functions general comments 2. Nonlinear functions of one variable 3. Nonlinear functions of two variables: interactions 4.

Nonlinear Regression Functions (SW Chapter 8) Outline 1. Nonlinear regression functions general comments 2. Nonlinear functions of one variable 3. Nonlinear functions of two variables: interactions 4.

Applied Statistics and Econometrics

Applied Statistics and Econometrics Lecture 6 Saul Lach September 2017 Saul Lach () Applied Statistics and Econometrics September 2017 1 / 53 Outline of Lecture 6 1 Omitted variable bias (SW 6.1) 2 Multiple

Applied Statistics and Econometrics Lecture 6 Saul Lach September 2017 Saul Lach () Applied Statistics and Econometrics September 2017 1 / 53 Outline of Lecture 6 1 Omitted variable bias (SW 6.1) 2 Multiple

Regression with a Single Regressor: Hypothesis Tests and Confidence Intervals

Regression with a Single Regressor: Hypothesis Tests and Confidence Intervals (SW Chapter 5) Outline. The standard error of ˆ. Hypothesis tests concerning β 3. Confidence intervals for β 4. Regression

Regression with a Single Regressor: Hypothesis Tests and Confidence Intervals (SW Chapter 5) Outline. The standard error of ˆ. Hypothesis tests concerning β 3. Confidence intervals for β 4. Regression

Linear Regression with Multiple Regressors

Linear Regression with Multiple Regressors (SW Chapter 6) Outline 1. Omitted variable bias 2. Causality and regression analysis 3. Multiple regression and OLS 4. Measures of fit 5. Sampling distribution

Linear Regression with Multiple Regressors (SW Chapter 6) Outline 1. Omitted variable bias 2. Causality and regression analysis 3. Multiple regression and OLS 4. Measures of fit 5. Sampling distribution

Chapter 6: Linear Regression With Multiple Regressors

Chapter 6: Linear Regression With Multiple Regressors 1-1 Outline 1. Omitted variable bias 2. Causality and regression analysis 3. Multiple regression and OLS 4. Measures of fit 5. Sampling distribution

Chapter 6: Linear Regression With Multiple Regressors 1-1 Outline 1. Omitted variable bias 2. Causality and regression analysis 3. Multiple regression and OLS 4. Measures of fit 5. Sampling distribution

Applied Statistics and Econometrics

Applied Statistics and Econometrics Lecture 13 Nonlinearities Saul Lach October 2018 Saul Lach () Applied Statistics and Econometrics October 2018 1 / 91 Outline of Lecture 13 1 Nonlinear regression functions

Applied Statistics and Econometrics Lecture 13 Nonlinearities Saul Lach October 2018 Saul Lach () Applied Statistics and Econometrics October 2018 1 / 91 Outline of Lecture 13 1 Nonlinear regression functions

ECON Introductory Econometrics. Lecture 5: OLS with One Regressor: Hypothesis Tests

ECON4150 - Introductory Econometrics Lecture 5: OLS with One Regressor: Hypothesis Tests Monique de Haan (moniqued@econ.uio.no) Stock and Watson Chapter 5 Lecture outline 2 Testing Hypotheses about one

ECON4150 - Introductory Econometrics Lecture 5: OLS with One Regressor: Hypothesis Tests Monique de Haan (moniqued@econ.uio.no) Stock and Watson Chapter 5 Lecture outline 2 Testing Hypotheses about one

Applied Statistics and Econometrics

Applied Statistics and Econometrics Lecture 5 Saul Lach September 2017 Saul Lach () Applied Statistics and Econometrics September 2017 1 / 44 Outline of Lecture 5 Now that we know the sampling distribution

Applied Statistics and Econometrics Lecture 5 Saul Lach September 2017 Saul Lach () Applied Statistics and Econometrics September 2017 1 / 44 Outline of Lecture 5 Now that we know the sampling distribution

Linear Regression with Multiple Regressors

Linear Regression with Multiple Regressors (SW Chapter 6) Outline 1. Omitted variable bias 2. Causality and regression analysis 3. Multiple regression and OLS 4. Measures of fit 5. Sampling distribution

Linear Regression with Multiple Regressors (SW Chapter 6) Outline 1. Omitted variable bias 2. Causality and regression analysis 3. Multiple regression and OLS 4. Measures of fit 5. Sampling distribution

Introduction to Econometrics Third Edition James H. Stock Mark W. Watson The statistical analysis of economic (and related) data

data") Introduction to Econometrics Third Edition James H. Stock Mark W. Watson The statistical analysis of economic (and related) data 1/2/3-1 1/2/3-2 Brief Overview of the Course Economics suggests important

Introduction to Econometrics Third Edition James H. Stock Mark W. Watson The statistical analysis of economic (and related) data 1/2/3-1 1/2/3-2 Brief Overview of the Course Economics suggests important

Lecture 5. In the last lecture, we covered. This lecture introduces you to

Lecture 5 In the last lecture, we covered. homework 2. The linear regression model (4.) 3. Estimating the coefficients (4.2) This lecture introduces you to. Measures of Fit (4.3) 2. The Least Square Assumptions

Lecture 5 In the last lecture, we covered. homework 2. The linear regression model (4.) 3. Estimating the coefficients (4.2) This lecture introduces you to. Measures of Fit (4.3) 2. The Least Square Assumptions

Introduction to Econometrics. Review of Probability & Statistics

1 Introduction to Econometrics Review of Probability & Statistics Peerapat Wongchaiwat, Ph.D. wongchaiwat@hotmail.com Introduction 2 What is Econometrics? Econometrics consists of the application of mathematical

1 Introduction to Econometrics Review of Probability & Statistics Peerapat Wongchaiwat, Ph.D. wongchaiwat@hotmail.com Introduction 2 What is Econometrics? Econometrics consists of the application of mathematical

Econometrics Midterm Examination Answers

Econometrics Midterm Examination Answers March 4, 204. Question (35 points) Answer the following short questions. (i) De ne what is an unbiased estimator. Show that X is an unbiased estimator for E(X i

Econometrics Midterm Examination Answers March 4, 204. Question (35 points) Answer the following short questions. (i) De ne what is an unbiased estimator. Show that X is an unbiased estimator for E(X i

Chapter 11. Regression with a Binary Dependent Variable

Chapter 11 Regression with a Binary Dependent Variable 2 Regression with a Binary Dependent Variable (SW Chapter 11) So far the dependent variable (Y) has been continuous: district-wide average test score

Chapter 11 Regression with a Binary Dependent Variable 2 Regression with a Binary Dependent Variable (SW Chapter 11) So far the dependent variable (Y) has been continuous: district-wide average test score

ECON Introductory Econometrics. Lecture 6: OLS with Multiple Regressors

ECON4150 - Introductory Econometrics Lecture 6: OLS with Multiple Regressors Monique de Haan (moniqued@econ.uio.no) Stock and Watson Chapter 6 Lecture outline 2 Violation of first Least Squares assumption

ECON4150 - Introductory Econometrics Lecture 6: OLS with Multiple Regressors Monique de Haan (moniqued@econ.uio.no) Stock and Watson Chapter 6 Lecture outline 2 Violation of first Least Squares assumption

Multiple Regression Analysis: Estimation. Simple linear regression model: an intercept and one explanatory variable (regressor)

") 1 Multiple Regression Analysis: Estimation Simple linear regression model: an intercept and one explanatory variable (regressor) Y i = β 0 + β 1 X i + u i, i = 1,2,, n Multiple linear regression model:

1 Multiple Regression Analysis: Estimation Simple linear regression model: an intercept and one explanatory variable (regressor) Y i = β 0 + β 1 X i + u i, i = 1,2,, n Multiple linear regression model:

2. Linear regression with multiple regressors

2. Linear regression with multiple regressors Aim of this section: Introduction of the multiple regression model OLS estimation in multiple regression Measures-of-fit in multiple regression Assumptions

2. Linear regression with multiple regressors Aim of this section: Introduction of the multiple regression model OLS estimation in multiple regression Measures-of-fit in multiple regression Assumptions

(a) Briefly discuss the advantage of using panel data in this situation rather than pure crosssections

Briefly discuss the advantage of using panel data in this situation rather than pure crosssections") Answer Key Fixed Effect and First Difference Models 1. See discussion in class.. David Neumark and William Wascher published a study in 199 of the effect of minimum wages on teenage employment using a

Answer Key Fixed Effect and First Difference Models 1. See discussion in class.. David Neumark and William Wascher published a study in 199 of the effect of minimum wages on teenage employment using a

ECON Introductory Econometrics. Lecture 17: Experiments

ECON4150 - Introductory Econometrics Lecture 17: Experiments Monique de Haan (moniqued@econ.uio.no) Stock and Watson Chapter 13 Lecture outline 2 Why study experiments? The potential outcome framework.

ECON4150 - Introductory Econometrics Lecture 17: Experiments Monique de Haan (moniqued@econ.uio.no) Stock and Watson Chapter 13 Lecture outline 2 Why study experiments? The potential outcome framework.

Linear Regression with 1 Regressor. Introduction to Econometrics Spring 2012 Ken Simons

Linear Regression with 1 Regressor Introduction to Econometrics Spring 2012 Ken Simons Linear Regression with 1 Regressor 1. The regression equation 2. Estimating the equation 3. Assumptions required for

Linear Regression with 1 Regressor Introduction to Econometrics Spring 2012 Ken Simons Linear Regression with 1 Regressor 1. The regression equation 2. Estimating the equation 3. Assumptions required for

Linear Regression with one Regressor

1 Linear Regression with one Regressor Covering Chapters 4.1 and 4.2. We ve seen the California test score data before. Now we will try to estimate the marginal effect of STR on SCORE. To motivate these

1 Linear Regression with one Regressor Covering Chapters 4.1 and 4.2. We ve seen the California test score data before. Now we will try to estimate the marginal effect of STR on SCORE. To motivate these

Lab 11 - Heteroskedasticity

Lab 11 - Heteroskedasticity Spring 2017 Contents 1 Introduction 2 2 Heteroskedasticity 2 3 Addressing heteroskedasticity in Stata 3 4 Testing for heteroskedasticity 4 5 A simple example 5 1 1 Introduction

Lab 11 - Heteroskedasticity Spring 2017 Contents 1 Introduction 2 2 Heteroskedasticity 2 3 Addressing heteroskedasticity in Stata 3 4 Testing for heteroskedasticity 4 5 A simple example 5 1 1 Introduction

ECO220Y Simple Regression: Testing the Slope

ECO220Y Simple Regression: Testing the Slope Readings: Chapter 18 (Sections 18.3-18.5) Winter 2012 Lecture 19 (Winter 2012) Simple Regression Lecture 19 1 / 32 Simple Regression Model y i = β 0 + β 1 x

ECO220Y Simple Regression: Testing the Slope Readings: Chapter 18 (Sections 18.3-18.5) Winter 2012 Lecture 19 (Winter 2012) Simple Regression Lecture 19 1 / 32 Simple Regression Model y i = β 0 + β 1 x

4. Nonlinear regression functions

4. Nonlinear regression functions Up to now: Population regression function was assumed to be linear The slope(s) of the population regression function is (are) constant The effect on Y of a unit-change

4. Nonlinear regression functions Up to now: Population regression function was assumed to be linear The slope(s) of the population regression function is (are) constant The effect on Y of a unit-change

6. Assessing studies based on multiple regression

6. Assessing studies based on multiple regression Questions of this section: What makes a study using multiple regression (un)reliable? When does multiple regression provide a useful estimate of the causal

6. Assessing studies based on multiple regression Questions of this section: What makes a study using multiple regression (un)reliable? When does multiple regression provide a useful estimate of the causal

Assessing Studies Based on Multiple Regression

Assessing Studies Based on Multiple Regression Outline 1. Internal and External Validity 2. Threats to Internal Validity a. Omitted variable bias b. Functional form misspecification c. Errors-in-variables

Assessing Studies Based on Multiple Regression Outline 1. Internal and External Validity 2. Threats to Internal Validity a. Omitted variable bias b. Functional form misspecification c. Errors-in-variables

Introduction to Econometrics

Introduction to Econometrics STAT-S-301 Introduction to Time Series Regression and Forecasting (2016/2017) Lecturer: Yves Dominicy Teaching Assistant: Elise Petit 1 Introduction to Time Series Regression

Introduction to Econometrics STAT-S-301 Introduction to Time Series Regression and Forecasting (2016/2017) Lecturer: Yves Dominicy Teaching Assistant: Elise Petit 1 Introduction to Time Series Regression

Multivariate Regression: Part I

Topic 1 Multivariate Regression: Part I ARE/ECN 240 A Graduate Econometrics Professor: Òscar Jordà Outline of this topic Statement of the objective: we want to explain the behavior of one variable as a

Topic 1 Multivariate Regression: Part I ARE/ECN 240 A Graduate Econometrics Professor: Òscar Jordà Outline of this topic Statement of the objective: we want to explain the behavior of one variable as a

Multiple Regression Analysis

Multiple Regression Analysis y = β 0 + β 1 x 1 + β 2 x 2 +... β k x k + u 2. Inference 0 Assumptions of the Classical Linear Model (CLM)! So far, we know: 1. The mean and variance of the OLS estimators

Multiple Regression Analysis y = β 0 + β 1 x 1 + β 2 x 2 +... β k x k + u 2. Inference 0 Assumptions of the Classical Linear Model (CLM)! So far, we know: 1. The mean and variance of the OLS estimators

Binary Dependent Variable. Regression with a

Beykent University Faculty of Business and Economics Department of Economics Econometrics II Yrd.Doç.Dr. Özgür Ömer Ersin Regression with a Binary Dependent Variable (SW Chapter 11) SW Ch. 11 1/59 Regression

Beykent University Faculty of Business and Economics Department of Economics Econometrics II Yrd.Doç.Dr. Özgür Ömer Ersin Regression with a Binary Dependent Variable (SW Chapter 11) SW Ch. 11 1/59 Regression

The Simple Linear Regression Model

The Simple Linear Regression Model Lesson 3 Ryan Safner 1 1 Department of Economics Hood College ECON 480 - Econometrics Fall 2017 Ryan Safner (Hood College) ECON 480 - Lesson 3 Fall 2017 1 / 77 Bivariate

The Simple Linear Regression Model Lesson 3 Ryan Safner 1 1 Department of Economics Hood College ECON 480 - Econometrics Fall 2017 Ryan Safner (Hood College) ECON 480 - Lesson 3 Fall 2017 1 / 77 Bivariate

Statistical Inference with Regression Analysis

Introductory Applied Econometrics EEP/IAS 118 Spring 2015 Steven Buck Lecture #13 Statistical Inference with Regression Analysis Next we turn to calculating confidence intervals and hypothesis testing

Introductory Applied Econometrics EEP/IAS 118 Spring 2015 Steven Buck Lecture #13 Statistical Inference with Regression Analysis Next we turn to calculating confidence intervals and hypothesis testing

Binary Dependent Variables

Binary Dependent Variables In some cases the outcome of interest rather than one of the right hand side variables - is discrete rather than continuous Binary Dependent Variables In some cases the outcome

Binary Dependent Variables In some cases the outcome of interest rather than one of the right hand side variables - is discrete rather than continuous Binary Dependent Variables In some cases the outcome

Contest Quiz 3. Question Sheet. In this quiz we will review concepts of linear regression covered in lecture 2.

Updated: November 17, 2011 Lecturer: Thilo Klein Contact: tk375@cam.ac.uk Contest Quiz 3 Question Sheet In this quiz we will review concepts of linear regression covered in lecture 2. NOTE: Please round

Updated: November 17, 2011 Lecturer: Thilo Klein Contact: tk375@cam.ac.uk Contest Quiz 3 Question Sheet In this quiz we will review concepts of linear regression covered in lecture 2. NOTE: Please round

8. Nonstandard standard error issues 8.1. The bias of robust standard errors

8.1. The bias of robust standard errors Bias Robust standard errors are now easily obtained using e.g. Stata option robust Robust standard errors are preferable to normal standard errors when residuals

8.1. The bias of robust standard errors Bias Robust standard errors are now easily obtained using e.g. Stata option robust Robust standard errors are preferable to normal standard errors when residuals

Empirical Application of Simple Regression (Chapter 2)

") Empirical Application of Simple Regression (Chapter 2) 1. The data file is House Data, which can be downloaded from my webpage. 2. Use stata menu File Import Excel Spreadsheet to read the data. Don t forget

Empirical Application of Simple Regression (Chapter 2) 1. The data file is House Data, which can be downloaded from my webpage. 2. Use stata menu File Import Excel Spreadsheet to read the data. Don t forget

The Application of California School

The Application of California School Zheng Tian 1 Introduction This tutorial shows how to estimate a multiple regression model and perform linear hypothesis testing. The application is about the test scores

The Application of California School Zheng Tian 1 Introduction This tutorial shows how to estimate a multiple regression model and perform linear hypothesis testing. The application is about the test scores

Heteroskedasticity. (In practice this means the spread of observations around any given value of X will not now be constant)

") Heteroskedasticity Occurs when the Gauss Markov assumption that the residual variance is constant across all observations in the data set so that E(u 2 i /X i ) σ 2 i (In practice this means the spread

Heteroskedasticity Occurs when the Gauss Markov assumption that the residual variance is constant across all observations in the data set so that E(u 2 i /X i ) σ 2 i (In practice this means the spread

1: a b c d e 2: a b c d e 3: a b c d e 4: a b c d e 5: a b c d e. 6: a b c d e 7: a b c d e 8: a b c d e 9: a b c d e 10: a b c d e

Economics 102: Analysis of Economic Data Cameron Spring 2016 Department of Economics, U.C.-Davis Final Exam (A) Tuesday June 7 Compulsory. Closed book. Total of 58 points and worth 45% of course grade.

Economics 102: Analysis of Economic Data Cameron Spring 2016 Department of Economics, U.C.-Davis Final Exam (A) Tuesday June 7 Compulsory. Closed book. Total of 58 points and worth 45% of course grade.

Problem Set #5-Key Sonoma State University Dr. Cuellar Economics 317- Introduction to Econometrics

Problem Set #5-Key Sonoma State University Dr. Cuellar Economics 317- Introduction to Econometrics C1.1 Use the data set Wage1.dta to answer the following questions. Estimate regression equation wage =

Problem Set #5-Key Sonoma State University Dr. Cuellar Economics 317- Introduction to Econometrics C1.1 Use the data set Wage1.dta to answer the following questions. Estimate regression equation wage =

Chapter 8 Conclusion

1 Chapter 8 Conclusion Three questions about test scores (score) and student-teacher ratio (str): a) After controlling for differences in economic characteristics of different districts, does the effect

1 Chapter 8 Conclusion Three questions about test scores (score) and student-teacher ratio (str): a) After controlling for differences in economic characteristics of different districts, does the effect

Lecture 5: Hypothesis testing with the classical linear model

Lecture 5: Hypothesis testing with the classical linear model Assumption MLR6: Normality MLR6 is not one of the Gauss-Markov assumptions. It s not necessary to assume the error is normally distributed

Lecture 5: Hypothesis testing with the classical linear model Assumption MLR6: Normality MLR6 is not one of the Gauss-Markov assumptions. It s not necessary to assume the error is normally distributed

Economics 326 Methods of Empirical Research in Economics. Lecture 14: Hypothesis testing in the multiple regression model, Part 2

Economics 326 Methods of Empirical Research in Economics Lecture 14: Hypothesis testing in the multiple regression model, Part 2 Vadim Marmer University of British Columbia May 5, 2010 Multiple restrictions

Economics 326 Methods of Empirical Research in Economics Lecture 14: Hypothesis testing in the multiple regression model, Part 2 Vadim Marmer University of British Columbia May 5, 2010 Multiple restrictions

ECON2228 Notes 7. Christopher F Baum. Boston College Economics. cfb (BC Econ) ECON2228 Notes / 41

ECON2228 Notes / 41") ECON2228 Notes 7 Christopher F Baum Boston College Economics 2014 2015 cfb (BC Econ) ECON2228 Notes 6 2014 2015 1 / 41 Chapter 8: Heteroskedasticity In laying out the standard regression model, we made

ECON2228 Notes 7 Christopher F Baum Boston College Economics 2014 2015 cfb (BC Econ) ECON2228 Notes 6 2014 2015 1 / 41 Chapter 8: Heteroskedasticity In laying out the standard regression model, we made

Quantitative Methods Final Exam (2017/1)

") Quantitative Methods Final Exam (2017/1) 1. Please write down your name and student ID number. 2. Calculator is allowed during the exam, but DO NOT use a smartphone. 3. List your answers (together with

Quantitative Methods Final Exam (2017/1) 1. Please write down your name and student ID number. 2. Calculator is allowed during the exam, but DO NOT use a smartphone. 3. List your answers (together with

ECON3150/4150 Spring 2015

ECON3150/4150 Spring 2015 Lecture 3&4 - The linear regression model Siv-Elisabeth Skjelbred University of Oslo January 29, 2015 1 / 67 Chapter 4 in S&W Section 17.1 in S&W (extended OLS assumptions) 2

ECON3150/4150 Spring 2015 Lecture 3&4 - The linear regression model Siv-Elisabeth Skjelbred University of Oslo January 29, 2015 1 / 67 Chapter 4 in S&W Section 17.1 in S&W (extended OLS assumptions) 2

Heteroskedasticity. Occurs when the Gauss Markov assumption that the residual variance is constant across all observations in the data set

Heteroskedasticity Occurs when the Gauss Markov assumption that the residual variance is constant across all observations in the data set Heteroskedasticity Occurs when the Gauss Markov assumption that

Heteroskedasticity Occurs when the Gauss Markov assumption that the residual variance is constant across all observations in the data set Heteroskedasticity Occurs when the Gauss Markov assumption that

Essential of Simple regression

Essential of Simple regression We use simple regression when we are interested in the relationship between two variables (e.g., x is class size, and y is student s GPA). For simplicity we assume the relationship

Essential of Simple regression We use simple regression when we are interested in the relationship between two variables (e.g., x is class size, and y is student s GPA). For simplicity we assume the relationship

Econometrics I KS. Module 2: Multivariate Linear Regression. Alexander Ahammer. This version: April 16, 2018

Econometrics I KS Module 2: Multivariate Linear Regression Alexander Ahammer Department of Economics Johannes Kepler University of Linz This version: April 16, 2018 Alexander Ahammer (JKU) Module 2: Multivariate

Econometrics I KS Module 2: Multivariate Linear Regression Alexander Ahammer Department of Economics Johannes Kepler University of Linz This version: April 16, 2018 Alexander Ahammer (JKU) Module 2: Multivariate

Lecture notes to Stock and Watson chapter 8

Lecture notes to Stock and Watson chapter 8 Nonlinear regression Tore Schweder September 29 TS () LN7 9/9 1 / 2 Example: TestScore Income relation, linear or nonlinear? TS () LN7 9/9 2 / 2 General problem

Lecture notes to Stock and Watson chapter 8 Nonlinear regression Tore Schweder September 29 TS () LN7 9/9 1 / 2 Example: TestScore Income relation, linear or nonlinear? TS () LN7 9/9 2 / 2 General problem

ECON Introductory Econometrics. Lecture 11: Binary dependent variables

ECON4150 - Introductory Econometrics Lecture 11: Binary dependent variables Monique de Haan (moniqued@econ.uio.no) Stock and Watson Chapter 11 Lecture Outline 2 The linear probability model Nonlinear probability

ECON4150 - Introductory Econometrics Lecture 11: Binary dependent variables Monique de Haan (moniqued@econ.uio.no) Stock and Watson Chapter 11 Lecture Outline 2 The linear probability model Nonlinear probability

Autocorrelation. Think of autocorrelation as signifying a systematic relationship between the residuals measured at different points in time

Autocorrelation Given the model Y t = b 0 + b 1 X t + u t Think of autocorrelation as signifying a systematic relationship between the residuals measured at different points in time This could be caused

Autocorrelation Given the model Y t = b 0 + b 1 X t + u t Think of autocorrelation as signifying a systematic relationship between the residuals measured at different points in time This could be caused

Introduction to Econometrics

Introduction to Econometrics STAT-S-301 Panel Data (2016/2017) Lecturer: Yves Dominicy Teaching Assistant: Elise Petit 1 Regression with Panel Data A panel dataset contains observations on multiple entities

Introduction to Econometrics STAT-S-301 Panel Data (2016/2017) Lecturer: Yves Dominicy Teaching Assistant: Elise Petit 1 Regression with Panel Data A panel dataset contains observations on multiple entities

Econ 423 Lecture Notes

Econ 423 Lecture Notes (hese notes are modified versions of lecture notes provided by Stock and Watson, 2007. hey are for instructional purposes only and are not to be distributed outside of the classroom.)

Econ 423 Lecture Notes (hese notes are modified versions of lecture notes provided by Stock and Watson, 2007. hey are for instructional purposes only and are not to be distributed outside of the classroom.)

ECON Introductory Econometrics. Lecture 16: Instrumental variables

ECON4150 - Introductory Econometrics Lecture 16: Instrumental variables Monique de Haan (moniqued@econ.uio.no) Stock and Watson Chapter 12 Lecture outline 2 OLS assumptions and when they are violated Instrumental

ECON4150 - Introductory Econometrics Lecture 16: Instrumental variables Monique de Haan (moniqued@econ.uio.no) Stock and Watson Chapter 12 Lecture outline 2 OLS assumptions and when they are violated Instrumental

Longitudinal Data Analysis Using Stata Paul D. Allison, Ph.D. Upcoming Seminar: May 18-19, 2017, Chicago, Illinois

Longitudinal Data Analysis Using Stata Paul D. Allison, Ph.D. Upcoming Seminar: May 18-19, 217, Chicago, Illinois Outline 1. Opportunities and challenges of panel data. a. Data requirements b. Control

Longitudinal Data Analysis Using Stata Paul D. Allison, Ph.D. Upcoming Seminar: May 18-19, 217, Chicago, Illinois Outline 1. Opportunities and challenges of panel data. a. Data requirements b. Control

ECON3150/4150 Spring 2016

ECON3150/4150 Spring 2016 Lecture 6 Multiple regression model Siv-Elisabeth Skjelbred University of Oslo February 5th Last updated: February 3, 2016 1 / 49 Outline Multiple linear regression model and

ECON3150/4150 Spring 2016 Lecture 6 Multiple regression model Siv-Elisabeth Skjelbred University of Oslo February 5th Last updated: February 3, 2016 1 / 49 Outline Multiple linear regression model and

WISE MA/PhD Programs Econometrics Instructor: Brett Graham Spring Semester, Academic Year Exam Version: A

WISE MA/PhD Programs Econometrics Instructor: Brett Graham Spring Semester, 2016-17 Academic Year Exam Version: A INSTRUCTIONS TO STUDENTS 1 The time allowed for this examination paper is 2 hours. 2 This

WISE MA/PhD Programs Econometrics Instructor: Brett Graham Spring Semester, 2016-17 Academic Year Exam Version: A INSTRUCTIONS TO STUDENTS 1 The time allowed for this examination paper is 2 hours. 2 This

LECTURE 10. Introduction to Econometrics. Multicollinearity & Heteroskedasticity

LECTURE 10 Introduction to Econometrics Multicollinearity & Heteroskedasticity November 22, 2016 1 / 23 ON PREVIOUS LECTURES We discussed the specification of a regression equation Specification consists

LECTURE 10 Introduction to Econometrics Multicollinearity & Heteroskedasticity November 22, 2016 1 / 23 ON PREVIOUS LECTURES We discussed the specification of a regression equation Specification consists

WISE MA/PhD Programs Econometrics Instructor: Brett Graham Spring Semester, Academic Year Exam Version: A

WISE MA/PhD Programs Econometrics Instructor: Brett Graham Spring Semester, 2016-17 Academic Year Exam Version: A INSTRUCTIONS TO STUDENTS 1 The time allowed for this examination paper is 2 hours. 2 This

WISE MA/PhD Programs Econometrics Instructor: Brett Graham Spring Semester, 2016-17 Academic Year Exam Version: A INSTRUCTIONS TO STUDENTS 1 The time allowed for this examination paper is 2 hours. 2 This

Chapter 9: Assessing Studies Based on Multiple Regression. Copyright 2011 Pearson Addison-Wesley. All rights reserved.

Chapter 9: Assessing Studies Based on Multiple Regression 1-1 9-1 Outline 1. Internal and External Validity 2. Threats to Internal Validity a) Omitted variable bias b) Functional form misspecification

Chapter 9: Assessing Studies Based on Multiple Regression 1-1 9-1 Outline 1. Internal and External Validity 2. Threats to Internal Validity a) Omitted variable bias b) Functional form misspecification

Review of Econometrics

Review of Econometrics Zheng Tian June 5th, 2017 1 The Essence of the OLS Estimation Multiple regression model involves the models as follows Y i = β 0 + β 1 X 1i + β 2 X 2i + + β k X ki + u i, i = 1,...,

Review of Econometrics Zheng Tian June 5th, 2017 1 The Essence of the OLS Estimation Multiple regression model involves the models as follows Y i = β 0 + β 1 X 1i + β 2 X 2i + + β k X ki + u i, i = 1,...,

Problem Set #3-Key. wage Coef. Std. Err. t P> t [95% Conf. Interval]

![Problem Set #3-Key. wage Coef. Std. Err. t P> t [95% Conf. Interval]](/thumbs/84/90891969.jpg "Problem Set #3-Key. wage Coef. Std. Err. t P> t [95% Conf. Interval]") Problem Set #3-Key Sonoma State University Economics 317- Introduction to Econometrics Dr. Cuellar 1. Use the data set Wage1.dta to answer the following questions. a. For the regression model Wage i =

Problem Set #3-Key Sonoma State University Economics 317- Introduction to Econometrics Dr. Cuellar 1. Use the data set Wage1.dta to answer the following questions. a. For the regression model Wage i =

Econ 836 Final Exam. 2 w N 2 u N 2. 2 v N

1) [4 points] Let Econ 836 Final Exam Y Xβ+ ε, X w+ u, w N w~ N(, σi ), u N u~ N(, σi ), ε N ε~ Nu ( γσ, I ), where X is a just one column. Let denote the OLS estimator, and define residuals e as e Y X.

1) [4 points] Let Econ 836 Final Exam Y Xβ+ ε, X w+ u, w N w~ N(, σi ), u N u~ N(, σi ), ε N ε~ Nu ( γσ, I ), where X is a just one column. Let denote the OLS estimator, and define residuals e as e Y X.

ECON2228 Notes 2. Christopher F Baum. Boston College Economics. cfb (BC Econ) ECON2228 Notes / 47

ECON2228 Notes / 47") ECON2228 Notes 2 Christopher F Baum Boston College Economics 2014 2015 cfb (BC Econ) ECON2228 Notes 2 2014 2015 1 / 47 Chapter 2: The simple regression model Most of this course will be concerned with

ECON2228 Notes 2 Christopher F Baum Boston College Economics 2014 2015 cfb (BC Econ) ECON2228 Notes 2 2014 2015 1 / 47 Chapter 2: The simple regression model Most of this course will be concerned with

Recent Advances in the Field of Trade Theory and Policy Analysis Using Micro-Level Data

Recent Advances in the Field of Trade Theory and Policy Analysis Using Micro-Level Data July 2012 Bangkok, Thailand Cosimo Beverelli (World Trade Organization) 1 Content a) Classical regression model b)

Recent Advances in the Field of Trade Theory and Policy Analysis Using Micro-Level Data July 2012 Bangkok, Thailand Cosimo Beverelli (World Trade Organization) 1 Content a) Classical regression model b)

Econ 423 Lecture Notes

Econ 423 Lecture Notes (These notes are slightly modified versions of lecture notes provided by Stock and Watson, 2007. They are for instructional purposes only and are not to be distributed outside of

Econ 423 Lecture Notes (These notes are slightly modified versions of lecture notes provided by Stock and Watson, 2007. They are for instructional purposes only and are not to be distributed outside of

Econometrics 1. Lecture 8: Linear Regression (2) 黄嘉平

黄嘉平") Econometrics 1 Lecture 8: Linear Regression (2) 黄嘉平 中国经济特区研究中 心讲师 办公室 : 文科楼 1726 E-mail: huangjp@szu.edu.cn Tel: (0755) 2695 0548 Office hour: Mon./Tue. 13:00-14:00 The linear regression model The linear

Econometrics 1 Lecture 8: Linear Regression (2) 黄嘉平 中国经济特区研究中 心讲师 办公室 : 文科楼 1726 E-mail: huangjp@szu.edu.cn Tel: (0755) 2695 0548 Office hour: Mon./Tue. 13:00-14:00 The linear regression model The linear

Practice exam questions

Practice exam questions Nathaniel Higgins nhiggins@jhu.edu, nhiggins@ers.usda.gov 1. The following question is based on the model y = β 0 + β 1 x 1 + β 2 x 2 + β 3 x 3 + u. Discuss the following two hypotheses.

Practice exam questions Nathaniel Higgins nhiggins@jhu.edu, nhiggins@ers.usda.gov 1. The following question is based on the model y = β 0 + β 1 x 1 + β 2 x 2 + β 3 x 3 + u. Discuss the following two hypotheses.

Handout 12. Endogeneity & Simultaneous Equation Models

Handout 12. Endogeneity & Simultaneous Equation Models In which you learn about another potential source of endogeneity caused by the simultaneous determination of economic variables, and learn how to

Handout 12. Endogeneity & Simultaneous Equation Models In which you learn about another potential source of endogeneity caused by the simultaneous determination of economic variables, and learn how to

2.1. Consider the following production function, known in the literature as the transcendental production function (TPF).

.") CHAPTER Functional Forms of Regression Models.1. Consider the following production function, known in the literature as the transcendental production function (TPF). Q i B 1 L B i K i B 3 e B L B K 4 i

CHAPTER Functional Forms of Regression Models.1. Consider the following production function, known in the literature as the transcendental production function (TPF). Q i B 1 L B i K i B 3 e B L B K 4 i

Regression with a Binary Dependent Variable (SW Ch. 9)

") Regression with a Binary Dependent Variable (SW Ch. 9) So far the dependent variable (Y) has been continuous: district-wide average test score traffic fatality rate But we might want to understand the

Regression with a Binary Dependent Variable (SW Ch. 9) So far the dependent variable (Y) has been continuous: district-wide average test score traffic fatality rate But we might want to understand the

Homework Set 2, ECO 311, Fall 2014

Homework Set 2, ECO 311, Fall 2014 Due Date: At the beginning of class on October 21, 2014 Instruction: There are twelve questions. Each question is worth 2 points. You need to submit the answers of only

Homework Set 2, ECO 311, Fall 2014 Due Date: At the beginning of class on October 21, 2014 Instruction: There are twelve questions. Each question is worth 2 points. You need to submit the answers of only

Business Statistics. Lecture 10: Course Review

Business Statistics Lecture 10: Course Review 1 Descriptive Statistics for Continuous Data Numerical Summaries Location: mean, median Spread or variability: variance, standard deviation, range, percentiles,

Business Statistics Lecture 10: Course Review 1 Descriptive Statistics for Continuous Data Numerical Summaries Location: mean, median Spread or variability: variance, standard deviation, range, percentiles,

Multiple Regression Analysis: Heteroskedasticity

Multiple Regression Analysis: Heteroskedasticity y = β 0 + β 1 x 1 + β x +... β k x k + u Read chapter 8. EE45 -Chaiyuth Punyasavatsut 1 topics 8.1 Heteroskedasticity and OLS 8. Robust estimation 8.3 Testing

Multiple Regression Analysis: Heteroskedasticity y = β 0 + β 1 x 1 + β x +... β k x k + u Read chapter 8. EE45 -Chaiyuth Punyasavatsut 1 topics 8.1 Heteroskedasticity and OLS 8. Robust estimation 8.3 Testing

Introduction to Econometrics. Assessing Studies Based on Multiple Regression

Introduction to Econometrics The statistical analysis of economic (and related) data STATS301 Assessing Studies Based on Multiple Regression Titulaire: Christopher Bruffaerts Assistant: Lorenzo Ricci 1

Introduction to Econometrics The statistical analysis of economic (and related) data STATS301 Assessing Studies Based on Multiple Regression Titulaire: Christopher Bruffaerts Assistant: Lorenzo Ricci 1

F Tests and F statistics

F Tests and F statistics Testing Linear estrictions F Stats and F Tests F Distributions F stats (w/ ) F Stats and tstat s eported F Stat's in OLS Output Example I: Bodyfat Babies and Bathwater F Stats,

F Tests and F statistics Testing Linear estrictions F Stats and F Tests F Distributions F stats (w/ ) F Stats and tstat s eported F Stat's in OLS Output Example I: Bodyfat Babies and Bathwater F Stats,

Econ 1123: Section 2. Review. Binary Regressors. Bivariate. Regression. Omitted Variable Bias

Contact Information Elena Llaudet Sections are voluntary. My office hours are Thursdays 5pm-7pm in Littauer Mezzanine 34-36 (Note room change) You can email me administrative questions to ellaudet@gmail.com.

Contact Information Elena Llaudet Sections are voluntary. My office hours are Thursdays 5pm-7pm in Littauer Mezzanine 34-36 (Note room change) You can email me administrative questions to ellaudet@gmail.com.

Final Exam. Question 1 (20 points) 2 (25 points) 3 (30 points) 4 (25 points) 5 (10 points) 6 (40 points) Total (150 points) Bonus question (10)

2 (25 points) 3 (30 points) 4 (25 points) 5 (10 points) 6 (40 points) Total (150 points) Bonus question (10)") Name Economics 170 Spring 2004 Honor pledge: I have neither given nor received aid on this exam including the preparation of my one page formula list and the preparation of the Stata assignment for the

Name Economics 170 Spring 2004 Honor pledge: I have neither given nor received aid on this exam including the preparation of my one page formula list and the preparation of the Stata assignment for the

1 Independent Practice: Hypothesis tests for one parameter:

1 Independent Practice: Hypothesis tests for one parameter: Data from the Indian DHS survey from 2006 includes a measure of autonomy of the women surveyed (a scale from 0-10, 10 being the most autonomous)

1 Independent Practice: Hypothesis tests for one parameter: Data from the Indian DHS survey from 2006 includes a measure of autonomy of the women surveyed (a scale from 0-10, 10 being the most autonomous)

OSU Economics 444: Elementary Econometrics. Ch.10 Heteroskedasticity

OSU Economics 444: Elementary Econometrics Ch.0 Heteroskedasticity (Pure) heteroskedasticity is caused by the error term of a correctly speciþed equation: Var(² i )=σ 2 i, i =, 2,,n, i.e., the variance

OSU Economics 444: Elementary Econometrics Ch.0 Heteroskedasticity (Pure) heteroskedasticity is caused by the error term of a correctly speciþed equation: Var(² i )=σ 2 i, i =, 2,,n, i.e., the variance

Multiple Regression: Inference

Multiple Regression: Inference The t-test: is ˆ j big and precise enough? We test the null hypothesis: H 0 : β j =0; i.e. test that x j has no effect on y once the other explanatory variables are controlled

Multiple Regression: Inference The t-test: is ˆ j big and precise enough? We test the null hypothesis: H 0 : β j =0; i.e. test that x j has no effect on y once the other explanatory variables are controlled

8. Instrumental variables regression

8. Instrumental variables regression Recall: In Section 5 we analyzed five sources of estimation bias arising because the regressor is correlated with the error term Violation of the first OLS assumption

8. Instrumental variables regression Recall: In Section 5 we analyzed five sources of estimation bias arising because the regressor is correlated with the error term Violation of the first OLS assumption

Econometrics -- Final Exam (Sample)

") Econometrics -- Final Exam (Sample) 1) The sample regression line estimated by OLS A) has an intercept that is equal to zero. B) is the same as the population regression line. C) cannot have negative and

Econometrics -- Final Exam (Sample) 1) The sample regression line estimated by OLS A) has an intercept that is equal to zero. B) is the same as the population regression line. C) cannot have negative and

2) For a normal distribution, the skewness and kurtosis measures are as follows: A) 1.96 and 4 B) 1 and 2 C) 0 and 3 D) 0 and 0

For a normal distribution, the skewness and kurtosis measures are as follows: A) 1.96 and 4 B) 1 and 2 C) 0 and 3 D) 0 and 0") Introduction to Econometrics Midterm April 26, 2011 Name Student ID MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. (5,000 credit for each correct

Introduction to Econometrics Midterm April 26, 2011 Name Student ID MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. (5,000 credit for each correct

Economics 471: Econometrics Department of Economics, Finance and Legal Studies University of Alabama

Economics 471: Econometrics Department of Economics, Finance and Legal Studies University of Alabama Course Packet The purpose of this packet is to show you one particular dataset and how it is used in

Economics 471: Econometrics Department of Economics, Finance and Legal Studies University of Alabama Course Packet The purpose of this packet is to show you one particular dataset and how it is used in

Introduction to Econometrics. Regression with Panel Data

Introduction to Econometrics The statistical analysis of economic (and related) data STATS301 Regression with Panel Data Titulaire: Christopher Bruffaerts Assistant: Lorenzo Ricci 1 Regression with Panel

Introduction to Econometrics The statistical analysis of economic (and related) data STATS301 Regression with Panel Data Titulaire: Christopher Bruffaerts Assistant: Lorenzo Ricci 1 Regression with Panel

5. Let W follow a normal distribution with mean of μ and the variance of 1. Then, the pdf of W is

Practice Final Exam Last Name:, First Name:. Please write LEGIBLY. Answer all questions on this exam in the space provided (you may use the back of any page if you need more space). Show all work but do

Practice Final Exam Last Name:, First Name:. Please write LEGIBLY. Answer all questions on this exam in the space provided (you may use the back of any page if you need more space). Show all work but do

Review of Statistics 101

Review of Statistics 101 We review some important themes from the course 1. Introduction Statistics- Set of methods for collecting/analyzing data (the art and science of learning from data). Provides methods

Review of Statistics 101 We review some important themes from the course 1. Introduction Statistics- Set of methods for collecting/analyzing data (the art and science of learning from data). Provides methods

Econometrics Homework 1

Econometrics Homework Due Date: March, 24. by This problem set includes questions for Lecture -4 covered before midterm exam. Question Let z be a random column vector of size 3 : z = @ (a) Write out z

Econometrics Homework Due Date: March, 24. by This problem set includes questions for Lecture -4 covered before midterm exam. Question Let z be a random column vector of size 3 : z = @ (a) Write out z

ECO321: Economic Statistics II

ECO321: Economic Statistics II Chapter 6: Linear Regression a Hiroshi Morita hmorita@hunter.cuny.edu Department of Economics Hunter College, The City University of New York a c 2010 by Hiroshi Morita.

ECO321: Economic Statistics II Chapter 6: Linear Regression a Hiroshi Morita hmorita@hunter.cuny.edu Department of Economics Hunter College, The City University of New York a c 2010 by Hiroshi Morita.

Correlation and Simple Linear Regression

Correlation and Simple Linear Regression Sasivimol Rattanasiri, Ph.D Section for Clinical Epidemiology and Biostatistics Ramathibodi Hospital, Mahidol University E-mail: sasivimol.rat@mahidol.ac.th 1 Outline

Correlation and Simple Linear Regression Sasivimol Rattanasiri, Ph.D Section for Clinical Epidemiology and Biostatistics Ramathibodi Hospital, Mahidol University E-mail: sasivimol.rat@mahidol.ac.th 1 Outline