Chapter 11. Regression with a Binary Dependent Variable

|

|

|

- Jerome Waters

- 5 years ago

- Views:

Transcription

1 Chapter 11 Regression with a Binary Dependent Variable

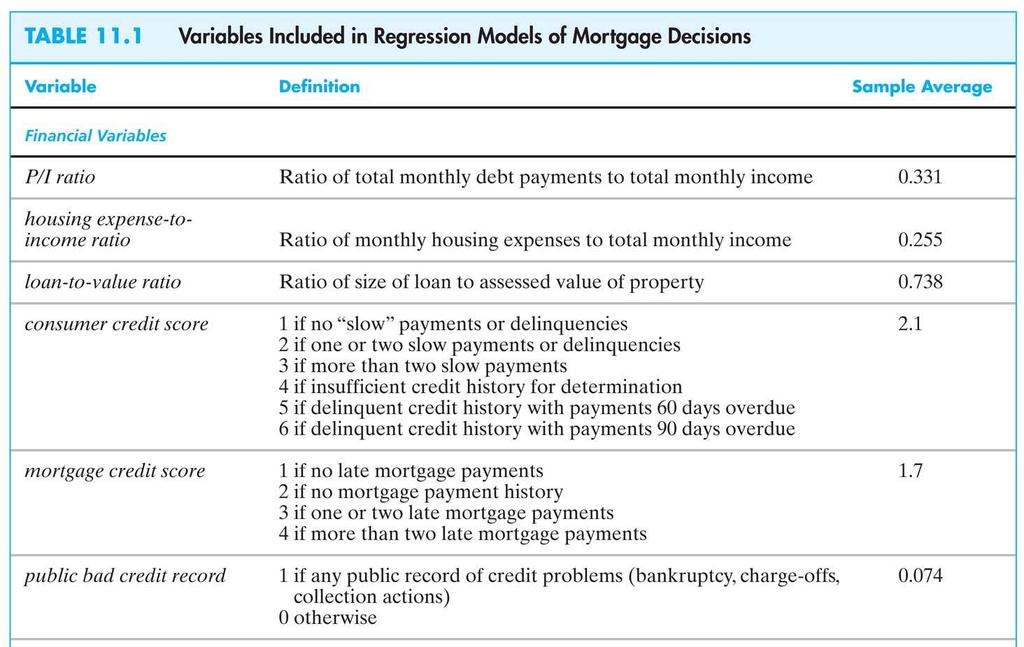

2 2 Regression with a Binary Dependent Variable (SW Chapter 11) So far the dependent variable (Y) has been continuous: district-wide average test score traffic fatality rate What if Y is binary? Y = get into college, or not; X = years of education Y = person smokes, or not; X = income Y = mortgage application is accepted, or not; X = income, house characteristics, marital status, race

3 Example: Mortgage denial and race The Boston Fed HMDA data set Individual applications for single-family mortgages made in 1990 in the greater Boston area 2380 observations, collected under Home Mortgage Disclosure Act (HMDA) Variables Dependent variable: Is the mortgage denied or accepted? Independent variables: income, wealth, employment status other loan, property characteristics race of applicant 3

4 4 The Linear Probability Model (SW Section 11.1) A natural starting point is the linear regression model with a single regressor: Y i = β 0 + β 1 X i + u i But: ΔY What does β 1 mean when Y is binary? Is β 1 = Δ X? What does the line β 0 + β 1 X mean when Y is binary? What does the predicted value Y ˆ mean when Y is binary? For example, what does Y ˆ = 0.26 mean?

5 5 The linear probability model, ctd. Y i = β 0 + β 1 X i + u i Recall assumption #1: E(u i X i ) = 0, so E(Y i X i ) = E(β 0 + β 1 X i + u i X i ) = β 0 + β 1 X i When Y is binary, E(Y) = 1 Pr(Y=1) + 0 Pr(Y=0) = Pr(Y=1) so E(Y X) = Pr(Y=1 X)

6 The linear probability model, ctd. When Y is binary, the linear regression model Y i = β 0 + β 1 X i + u i is called the linear probability model. The predicted value is a probability: E(Y X=x) = Pr(Y=1 X=x) = prob. that Y = 1 given x Y ˆ = the predicted probability that Y i = 1, given X β 1 = change in probability that Y = 1 for a given Δx: Pr( 1 ) Pr( 1 ) β 1 = Y = X = x +Δ x Y = X = x Δx 6

7 7 Example: linear probability model, HMDA data Mortgage denial v. ratio of debt payments to income (P/I ratio) in the HMDA data set (subset)

8 8 Linear probability model: HMDA data, ctd. deny = P/I ratio (n = 2380) (.032) (.098) What is the predicted value for P/I ratio =.3? Pr( deny = 1 P / Iratio =.3) = =.151 Calculating effects: increase P/I ratio from.3 to.4: Pr( deny = 1 P / Iratio =.4) = =.212 The effect on the probability of denial of an increase in P/I ratio from.3 to.4 is to increase the probability by.061, that is, by 6.1 percentage points (what?).

9 9 Linear probability model: HMDA data, ctd Next include black as a regressor: deny = P/I ratio +.177black (.032) (.098) (.025) Predicted probability of denial: for black applicant with P/I ratio =.3: Pr( deny = 1) = =.254 for white applicant, P/I ratio =.3: Pr( deny = 1) = =.077 difference =.177 = 17.7 percentage points Coefficient on black is significant at the 5% level Still plenty of room for omitted variable bias

10 10 The linear probability model: Summary Models Pr(Y=1 X) as a linear function of X Advantages: simple to estimate and to interpret inference is the same as for multiple regression (need heteroskedasticity-robust standard errors) Disadvantages: Does it make sense that the probability should be linear in X? Predicted probabilities can be <0 or >1! These disadvantages can be solved by using a nonlinear probability model: probit and logit regression

11 11 Probit and Logit Regression (SW Section 11.2) The problem with the linear probability model is that it models the probability of Y=1 as being linear: Pr(Y = 1 X) = β 0 + β 1 X Instead, we want: 0 Pr(Y = 1 X) 1 for all X Pr(Y = 1 X) to be increasing in X (for β 1 >0) This requires a nonlinear functional form for the probability. How about an S-curve

12 12 The probit model satisfies these conditions: 0 Pr(Y = 1 X) 1 for all X Pr(Y = 1 X) to be increasing in X (for β 1 >0)

13 13 Probit regression models the probability that Y=1 using the cumulative standard normal distribution function, evaluated at z = β 0 + β 1 X: Pr(Y = 1 X) = Φ(β 0 + β 1 X) Φ is the cumulative normal distribution function. z = β 0 + β 1 X is the z-value or z-index of the probit model. Example: Suppose β 0 = -2, β 1 = 3, X =.4, so Pr(Y = 1 X=.4) = Φ( ) = Φ(-0.8) Pr(Y = 1 X=.4) = area under the standard normal density to left of z = -.8, which is

=.2119")

14 Pr(Z -0.8) =

15 15 Probit regression, ctd. Why use the cumulative normal probability distribution? The S-shape gives us what we want: 0 Pr(Y = 1 X) 1 for all X Pr(Y = 1 X) to be increasing in X (for β 1 >0) Easy to use the probabilities are tabulated in the cumulative normal tables Relatively straightforward interpretation: z-value = β 0 + β 1 X ˆ β 0 + ˆ β 1 X is the predicted z-value, given X β 1 is the change in the z-value for a unit change in X

16 STATA Example: HMDA data. probit deny p_irat, r; Iteration 0: log likelihood = Iteration 1: log likelihood = Iteration 2: log likelihood = Iteration 3: log likelihood = We ll discuss this later Probit estimates Number of obs = 2380 Wald chi2(1) = Prob > chi2 = Log likelihood = Pseudo R2 = Robust deny Coef. Std. Err. z P> z [95% Conf. Interval] p_irat _cons Pr( deny = 1 P / Iratio) = Φ( P/I ratio) (.16) (.47) 16

17 STATA Example: HMDA data, ctd. Pr( deny = 1 P / Iratio) = Φ( P/I ratio) (.16) (.47) Positive coefficient: does this make sense? Standard errors have the usual interpretation Predicted probabilities: Pr( deny = 1 P / Iratio =.3) = Φ( ) = Φ(-1.30) =.097 Effect of change in P/I ratio from.3 to.4: Pr( deny = 1 P / Iratio =.4) = Φ( ) =.159 Predicted probability of denial rises from.097 to

18 18 Probit regression with multiple regressors Pr(Y = 1 X 1, X 2 ) = Φ(β 0 + β 1 X 1 + β 2 X 2 ) Φ is the cumulative normal distribution function. z = β 0 + β 1 X 1 + β 2 X 2 is the z-value or z-index of the probit model. β 1 is the effect on the z-score of a unit change in X 1, holding constant X 2

19 19 STATA Example: HMDA data. probit deny p_irat black, r; Iteration 0: log likelihood = Iteration 1: log likelihood = Iteration 2: log likelihood = Iteration 3: log likelihood = Probit estimates Number of obs = 2380 Wald chi2(2) = Prob > chi2 = Log likelihood = Pseudo R2 = Robust deny Coef. Std. Err. z P> z [95% Conf. Interval] p_irat black _cons We ll go through the estimation details later

20 STATA Example, ctd.: predicted probit probabilities. probit deny p_irat black, r; Probit estimates Number of obs = 2380 Wald chi2(2) = Prob > chi2 = Log likelihood = Pseudo R2 = Robust deny Coef. Std. Err. z P> z [95% Conf. Interval] p_irat black _cons sca z1 = _b[_cons]+_b[p_irat]*.3+_b[black]*0;. display "Pred prob, p_irat=.3, white: " normprob(z1); Pred prob, p_irat=.3, white: NOTE _b[_cons] is the estimated intercept ( ) _b[p_irat] is the coefficient on p_irat ( ) sca creates a new scalar which is the result of a calculation display prints the indicated information to the screen 20

21 21 STATA Example, ctd. Pr( deny = 1 P / I, black) = Φ( P/I ratio +.71 black) (.16) (.44) (.08) Is the coefficient on black statistically significant? Estimated effect of race for P/I ratio =.3: Pr( deny = 1.3,1) = Φ( ) =.233 Pr( deny = 1.3,0) = Φ( ) =.075 Difference in rejection probabilities =.158 (15.8 percentage points) Still plenty of room still for omitted variable bias

22 Logit Regression Logit regression models the probability of Y=1 as the cumulative standard logistic distribution function, evaluated at z = β 0 + β 1 X: Pr(Y = 1 X) = F(β 0 + β 1 X) F is the cumulative logistic distribution function: F(β 0 + β 1 X) = 1+ 1 ( 0 1X ) e β + β 22

23 Logit regression, ctd. Pr(Y = 1 X) = F(β 0 + β 1 X) where F(β 0 + β 1 X) = 1+ 1 ( 0 1X ) e β + β. Example: β 0 = -3, β 1 = 2, X =.4, so β 0 + β 1 X = = -2.2 so Pr(Y = 1 X=.4) = 1/(1+e ( 2.2) ) =.0998 Why bother with logit if we have probit? Historically, logit is more convenient computationally In practice, logit and probit are very similar 23

24 24 STATA Example: HMDA data. logit deny p_irat black, r; Iteration 0: log likelihood = Later Iteration 1: log likelihood = Iteration 2: log likelihood = Iteration 3: log likelihood = Iteration 4: log likelihood = Logit estimates Number of obs = 2380 Wald chi2(2) = Prob > chi2 = Log likelihood = Pseudo R2 = Robust deny Coef. Std. Err. z P> z [95% Conf. Interval] p_irat black _cons dis "Pred prob, p_irat=.3, white: " > 1/(1+exp(-(_b[_cons]+_b[p_irat]*.3+_b[black]*0))); Pred prob, p_irat=.3, white: NOTE: the probit predicted probability is

25 Predicted probabilities from estimated probit and logit models usually are (as usual) very close in this application. 25

26 26 Example for class discussion: Characterizing the Background of Hezbollah Militants Source: Alan Krueger and Jitka Maleckova, Education, Poverty and Terrorism: Is There a Causal Connection? Journal of Economic Perspectives, Fall 2003, Logit regression: 1 = died in Hezbollah military event Table of logit results:

27 27

28 28

29 29 Hezbollah militants example, ctd. Compute the effect of schooling by comparing predicted probabilities using the logit regression in column (3): Pr(Y=1 secondary = 1, poverty = 0, age = 20) Pr(Y=0 secondary = 0, poverty = 0, age = 20): Pr(Y=1 secondary = 1, poverty = 0, age = 20) = 1/[1+e ( ) ] = 1/[1 + e ] = does this make sense? Pr(Y=1 secondary = 0, poverty = 0, age = 20) = 1/[1+e ( ) ] = 1/[1 + e ] = does this make sense?

30 30 Predicted change in probabilities: Pr(Y=1 secondary = 1, poverty = 0, age = 20) Pr(Y=1 secondary = 1, poverty = 0, age = 20) = = Both these statements are true: The probability of being a Hezbollah militant increases by percentage points, if secondary school is attended. The probability of being a Hezbollah militant increases by 32%, if secondary school is attended ( / =.32). These sound so different! what is going on?

31 31 Estimation and Inference in Probit (and Logit) Models (SW Section 11.3) Probit model: Pr(Y = 1 X) = Φ(β 0 + β 1 X) Estimation and inference How can we estimate β 0 and β 1? What is the sampling distribution of the estimators? Why can we use the usual methods of inference? First motivate via nonlinear least squares Then discuss maximum likelihood estimation (what is actually done in practice)

32 Probit estimation by nonlinear least squares Recall OLS: n min [ Y ( b + b X )] b0, b1 i 0 1 i i= 1 The result is the OLS estimators ˆ β 0 and ˆ β 1 Nonlinear least squares estimator of probit coefficients: n min [ Y Φ ( b + b X )] b0, b1 i 0 1 i i= 1 How to solve this minimization problem? Calculus doesn t give and explicit solution. Solved numerically using the computer(specialized minimization algorithms) In practice, nonlinear least squares isn t used because it isn t efficient an estimator with a smaller variance is

33 33 Probit estimation by maximum likelihood The likelihood function is the conditional density of Y 1,,Y n given X 1,,X n, treated as a function of the unknown parameters β 0 and β 1. The maximum likelihood estimator (MLE) is the value of (β 0, β 1 ) that maximize the likelihood function. The MLE is the value of (β 0, β 1 ) that best describe the full distribution of the data. In large samples, the MLE is: consistent normally distributed efficient (has the smallest variance of all estimators)

34 34 Special case: the probit MLE with no X Y = 1 with probability p 0 with probability 1 p (Bernoulli distribution) Data: Y 1,,Y n, i.i.d. Derivation of the likelihood starts with the density of Y 1 : so Pr(Y 1 = 1) = p and Pr(Y 1 = 0) = 1 p y1 1 y1 Pr(Y 1 = y 1 ) = p (1 p) (verify this for y 1 =0, 1!)

35 35 Joint density of (Y 1,Y 2 ): Because Y 1 and Y 2 are independent, Pr(Y 1 = y 1,Y 2 = y 2 ) = Pr(Y 1 = y 1 ) Pr(Y 2 = y 2 ) y1 1 y1 = [ p (1 p) y2 1 y2 ] [ p (1 p) ] = Joint density of (Y 1,..,Y n ): p ( y + y ) [ 2 ( y + y )] (1 p) Pr(Y 1 = y 1,Y 2 = y 2,,Y n = y n ) y1 1 y1 = [ p (1 p) y2 1 y2 ] [ p (1 p) ] [ n n y ( n y 1 i ) i 1 i i = p = = (1 p) p y n (1 ) 1 yn p ]

36 36 The likelihood is the joint density, treated as a function of the unknown parameters, which here is p: ( ) n n Y n Y 1 i i 1 i i f(p;y 1,,Y n ) = p = = (1 p) The MLE maximizes the likelihood. Its easier to work with the logarithm of the likelihood, ln[f(p;y 1,,Y n )]: ln[f(p;y 1,,Y n )] = ( n ) ( n ) i i Y ln( p) + n Y ln(1 p) i= 1 i= 1 Maximize the likelihood by setting the derivative = 0: dln f( p; Y1,..., Y n ) = ( n ) 1 ( n ) 1 Y i 1 i + n Y = i= 1 i dp p 1 p Solving for p yields the MLE; that is, p ˆ MLE satisfies, = 0

37 37 or or or MLE pˆ 1 pˆ ( n ) ( n Y ) 1 i n Y i= MLE i= 1 i = pˆ 1 pˆ ( n ) ( n Y ) 1 i = n Y i= MLE i= 1 i Y pˆ = 1 Y 1 pˆ MLE MLE MLE ˆ MLE p = Y = fraction of 1 s whew a lot of work to get back to the first thing you would think of using but the nice thing is that this whole approach generalizes to more complicated models...

38 38 The MLE in the no-x case (Bernoulli distribution), ctd.: ˆ MLE p = Y = fraction of 1 s For Y i i.i.d. Bernoulli, the MLE is the natural estimator of p, the fraction of 1 s, which is Y We already know the essentials of inference: In large n, the sampling distribution of p ˆ MLE = Y is normally distributed Thus inference is as usual: hypothesis testing via t- statistic, confidence interval as ± 1.96SE

39 39 The MLE in the no-x case (Bernoulli distribution), ctd: The theory of maximum likelihood estimation says that p ˆ MLE is the most efficient estimator of p of all possible estimators at least for large n. (Much stronger than the Gauss-Markov theorem). This is why people use the MLE. STATA note: to emphasize requirement of large-n, the printout calls the t-statistic the z-statistic; instead of the F- statistic, the chi-squared statistic (= q F). Now we extend this to probit in which the probability is conditional on X the MLE of the probit coefficients.

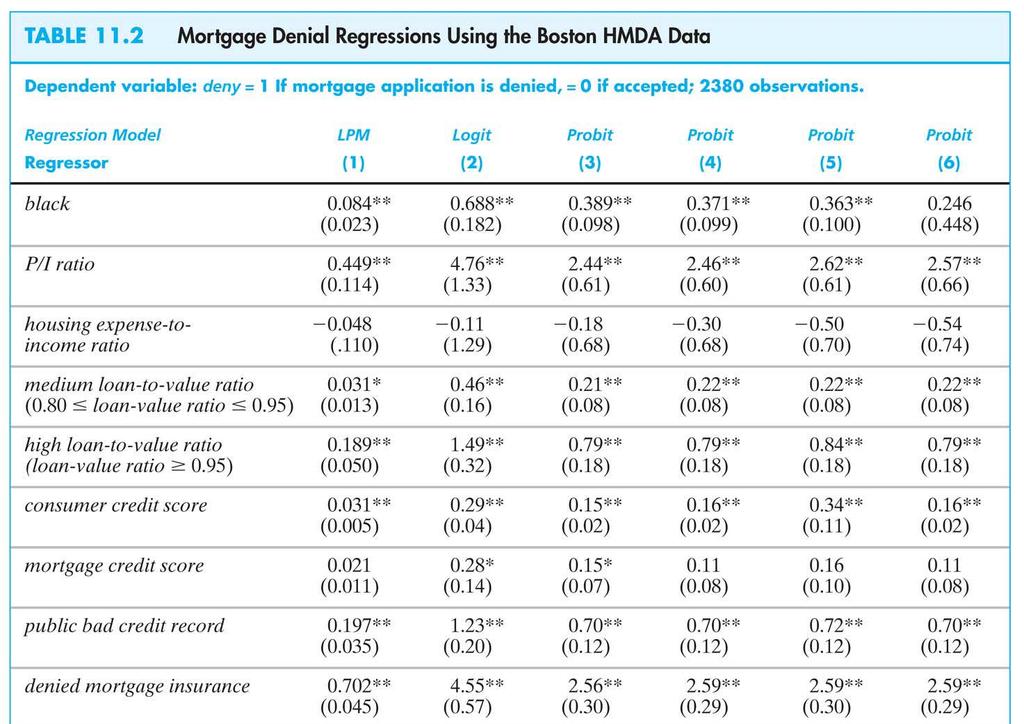

40 40 The probit likelihood with one X The derivation starts with the density of Y 1, given X 1 : Pr(Y 1 = 1 X 1 ) = Φ(β 0 + β 1 X 1 ) Pr(Y 1 = 0 X 1 ) = 1 Φ(β 0 + β 1 X 1 ) so y1 1 y1 Pr(Y 1 = y 1 X 1 ) = Φ ( β + β X ) [1 Φ ( β + β X )] The probit likelihood function is the joint density of Y 1,,Y n given X 1,,X n, treated as a function of β 0, β 1 : f(β 0,β 1 ; Y 1,,Y n X 1,,X n ) Y1 1 = { ( ) [1 ( )] 1 Y Φ β + β X Φ β + β X } Yn 1 Yn { Φ ( β + β X ) [1 Φ ( β + β X )] } 0 1 n 0 1 n

41 41 The probit likelihood function: f(β 0,β 1 ; Y 1,,Y n X 1,,X n ) Y1 1 Y1 = { Φ ( β + β X ) [1 Φ ( β + β X )] } Yn 1 Yn { Φ ( β + β X ) [1 Φ ( β + β X )] } 0 1 n 0 1 Can t solve for the maximum explicitly Must maximize using numerical methods As in the case of no X, in large samples: ˆ MLE 0 ˆ MLE 0 ˆ MLE 0 ˆ MLE β, β 1 are consistent β, ˆ β MLE 1 are normally distributed β, ˆ β MLE 1 are asymptotically efficient among all estimators (assuming the probit model is the correct model) n

42 42 The Probit MLE, ctd. Standard errors of ˆ β MLE 0, ˆ β MLE 1 are computed automatically Testing, confidence intervals proceeds as usual For multiple X s, see SW App. 11.2

43 43 The logit likelihood with one X The only difference between probit and logit is the functional form used for the probability: Φ is replaced by the cumulative logistic function. Otherwise, the likelihood is similar; for details see SW App As with probit, ˆ β MLE 0, ˆ β MLE 1 are consistent ˆ β MLE 0, ˆ β MLE 1 are normally distributed Their standard errors can be computed Testing, confidence intervals proceeds as usual

44 44 Measures of fit for logit and probit The R 2 2 and R don t make sense here (why?). So, two other specialized measures are used: 1. The fraction correctly predicted = fraction of Y s for which predicted probability is >50% (if Y i =1) or is <50% (if Y i =0). 2. The pseudo-r 2 measure the fit using the likelihood function: measures the improvement in the value of the log likelihood, relative to having no X s (see SW App. 11.2). This simplifies to the R 2 in the linear model with normally distributed errors.

45 45 Application to the Boston HMDA Data (SW Section 11.4) Mortgages (home loans) are an essential part of buying a home. Is there differential access to home loans by race? If two otherwise identical individuals, one white and one black, applied for a home loan, is there a difference in the probability of denial?

46 46 The HMDA Data Set Data on individual characteristics, property characteristics, and loan denial/acceptance The mortgage application process circa : Go to a bank or mortgage company Fill out an application (personal+financial info) Meet with the loan officer Then the loan officer decides by law, in a race-blind way. Presumably, the bank wants to make profitable loans, and the loan officer doesn t want to originate defaults.

47 47 The loan officer s decision Loan officer uses key financial variables: P/I ratio housing expense-to-income ratio loan-to-value ratio personal credit history The decision rule is nonlinear: loan-to-value ratio > 80% loan-to-value ratio > 95% (what happens in default?) credit score

48 48 Regression specifications Pr(deny=1 black, other X s) = linear probability model probit Main problem with the regressions so far: potential omitted variable bias. All these (i) enter the loan officer decision function, all (ii) are or could be correlated with race: wealth, type of employment credit history family status The HMDA data set is very rich

49 49

50 50

51 51

52 Table 11.2, ctd. 52

53 Table 11.2, ctd. 53

54 54 Summary of Empirical Results Coefficients on the financial variables make sense. Black is statistically significant in all specifications Race-financial variable interactions aren t significant. Including the covariates sharply reduces the effect of race on denial probability. LPM, probit, logit: similar estimates of effect of race on the probability of denial. Estimated effects are large in a real world sense.

55 55 Remaining threats to internal, external validity Internal validity 1. omitted variable bias what else is learned in the in-person interviews? 2. functional form misspecification (no ) 3. measurement error (originally, yes; now, no ) 4. selection random sample of loan applications define population to be loan applicants 5. simultaneous causality (no) External validity This is for Boston in What about today?

56 56 Summary (SW Section 11.5) If Y i is binary, then E(Y X) = Pr(Y=1 X) Three models: linear probability model (linear multiple regression) probit (cumulative standard normal distribution) logit (cumulative standard logistic distribution) LPM, probit, logit all produce predicted probabilities Effect of ΔX is change in conditional probability that Y=1. For logit and probit, this depends on the initial X Probit and logit are estimated via maximum likelihood Coefficients are normally distributed for large n Large-n hypothesis testing, conf. intervals is as usual

Binary Dependent Variable. Regression with a

Beykent University Faculty of Business and Economics Department of Economics Econometrics II Yrd.Doç.Dr. Özgür Ömer Ersin Regression with a Binary Dependent Variable (SW Chapter 11) SW Ch. 11 1/59 Regression

Beykent University Faculty of Business and Economics Department of Economics Econometrics II Yrd.Doç.Dr. Özgür Ömer Ersin Regression with a Binary Dependent Variable (SW Chapter 11) SW Ch. 11 1/59 Regression

Regression with a Binary Dependent Variable (SW Ch. 9)

") Regression with a Binary Dependent Variable (SW Ch. 9) So far the dependent variable (Y) has been continuous: district-wide average test score traffic fatality rate But we might want to understand the

Regression with a Binary Dependent Variable (SW Ch. 9) So far the dependent variable (Y) has been continuous: district-wide average test score traffic fatality rate But we might want to understand the

ECON Introductory Econometrics. Lecture 11: Binary dependent variables

ECON4150 - Introductory Econometrics Lecture 11: Binary dependent variables Monique de Haan (moniqued@econ.uio.no) Stock and Watson Chapter 11 Lecture Outline 2 The linear probability model Nonlinear probability

ECON4150 - Introductory Econometrics Lecture 11: Binary dependent variables Monique de Haan (moniqued@econ.uio.no) Stock and Watson Chapter 11 Lecture Outline 2 The linear probability model Nonlinear probability

Applied Economics. Regression with a Binary Dependent Variable. Department of Economics Universidad Carlos III de Madrid

Applied Economics Regression with a Binary Dependent Variable Department of Economics Universidad Carlos III de Madrid See Stock and Watson (chapter 11) 1 / 28 Binary Dependent Variables: What is Different?

Applied Economics Regression with a Binary Dependent Variable Department of Economics Universidad Carlos III de Madrid See Stock and Watson (chapter 11) 1 / 28 Binary Dependent Variables: What is Different?

2. We care about proportion for categorical variable, but average for numerical one.

Probit Model 1. We apply Probit model to Bank data. The dependent variable is deny, a dummy variable equaling one if a mortgage application is denied, and equaling zero if accepted. The key regressor is

Probit Model 1. We apply Probit model to Bank data. The dependent variable is deny, a dummy variable equaling one if a mortgage application is denied, and equaling zero if accepted. The key regressor is

Regression with a Single Regressor: Hypothesis Tests and Confidence Intervals

Regression with a Single Regressor: Hypothesis Tests and Confidence Intervals (SW Chapter 5) Outline. The standard error of ˆ. Hypothesis tests concerning β 3. Confidence intervals for β 4. Regression

Regression with a Single Regressor: Hypothesis Tests and Confidence Intervals (SW Chapter 5) Outline. The standard error of ˆ. Hypothesis tests concerning β 3. Confidence intervals for β 4. Regression

Chapter 9 Regression with a Binary Dependent Variable. Multiple Choice. 1) The binary dependent variable model is an example of a

The binary dependent variable model is an example of a") Chapter 9 Regression with a Binary Dependent Variable Multiple Choice ) The binary dependent variable model is an example of a a. regression model, which has as a regressor, among others, a binary variable.

Chapter 9 Regression with a Binary Dependent Variable Multiple Choice ) The binary dependent variable model is an example of a a. regression model, which has as a regressor, among others, a binary variable.

Chapter 7. Hypothesis Tests and Confidence Intervals in Multiple Regression

Chapter 7 Hypothesis Tests and Confidence Intervals in Multiple Regression Outline 1. Hypothesis tests and confidence intervals for a single coefficie. Joint hypothesis tests on multiple coefficients 3.

Chapter 7 Hypothesis Tests and Confidence Intervals in Multiple Regression Outline 1. Hypothesis tests and confidence intervals for a single coefficie. Joint hypothesis tests on multiple coefficients 3.

Econometrics Honor s Exam Review Session. Spring 2012 Eunice Han

Econometrics Honor s Exam Review Session Spring 2012 Eunice Han Topics 1. OLS The Assumptions Omitted Variable Bias Conditional Mean Independence Hypothesis Testing and Confidence Intervals Homoskedasticity

Econometrics Honor s Exam Review Session Spring 2012 Eunice Han Topics 1. OLS The Assumptions Omitted Variable Bias Conditional Mean Independence Hypothesis Testing and Confidence Intervals Homoskedasticity

Hypothesis Tests and Confidence Intervals in Multiple Regression

Hypothesis Tests and Confidence Intervals in Multiple Regression (SW Chapter 7) Outline 1. Hypothesis tests and confidence intervals for one coefficient. Joint hypothesis tests on multiple coefficients

Hypothesis Tests and Confidence Intervals in Multiple Regression (SW Chapter 7) Outline 1. Hypothesis tests and confidence intervals for one coefficient. Joint hypothesis tests on multiple coefficients

Nonlinear Regression Functions

Nonlinear Regression Functions (SW Chapter 8) Outline 1. Nonlinear regression functions general comments 2. Nonlinear functions of one variable 3. Nonlinear functions of two variables: interactions 4.

Nonlinear Regression Functions (SW Chapter 8) Outline 1. Nonlinear regression functions general comments 2. Nonlinear functions of one variable 3. Nonlinear functions of two variables: interactions 4.

ECONOMETRICS HONOR S EXAM REVIEW SESSION

ECONOMETRICS HONOR S EXAM REVIEW SESSION Eunice Han ehan@fas.harvard.edu March 26 th, 2013 Harvard University Information 2 Exam: April 3 rd 3-6pm @ Emerson 105 Bring a calculator and extra pens. Notes

ECONOMETRICS HONOR S EXAM REVIEW SESSION Eunice Han ehan@fas.harvard.edu March 26 th, 2013 Harvard University Information 2 Exam: April 3 rd 3-6pm @ Emerson 105 Bring a calculator and extra pens. Notes

Econ 371 Problem Set #6 Answer Sheet. deaths per 10,000. The 90% confidence interval for the change in death rate is 1.81 ±

Econ 371 Problem Set #6 Answer Sheet 10.1 This question focuses on the regression model results in Table 10.1. a. The first part of this question asks you to predict the number of lives that would be saved

Econ 371 Problem Set #6 Answer Sheet 10.1 This question focuses on the regression model results in Table 10.1. a. The first part of this question asks you to predict the number of lives that would be saved

Econometrics Problem Set 10

Econometrics Problem Set 0 WISE, Xiamen University Spring 207 Conceptual Questions Dependent variable: P ass Probit Logit LPM Probit Logit LPM Probit () (2) (3) (4) (5) (6) (7) Experience 0.03 0.040 0.006

Econometrics Problem Set 0 WISE, Xiamen University Spring 207 Conceptual Questions Dependent variable: P ass Probit Logit LPM Probit Logit LPM Probit () (2) (3) (4) (5) (6) (7) Experience 0.03 0.040 0.006

Introduction to Econometrics

Introduction to Econometrics T H I R D E D I T I O N Global Edition James H. Stock Harvard University Mark W. Watson Princeton University Boston Columbus Indianapolis New York San Francisco Upper Saddle

Introduction to Econometrics T H I R D E D I T I O N Global Edition James H. Stock Harvard University Mark W. Watson Princeton University Boston Columbus Indianapolis New York San Francisco Upper Saddle

Logit regression Logit regression

Logit regressio Logit regressio models the probability of Y= as the cumulative stadard logistic distributio fuctio, evaluated at z = β 0 + β X: Pr(Y = X) = F(β 0 + β X) F is the cumulative logistic distributio

Logit regressio Logit regressio models the probability of Y= as the cumulative stadard logistic distributio fuctio, evaluated at z = β 0 + β X: Pr(Y = X) = F(β 0 + β X) F is the cumulative logistic distributio

Binary Dependent Variables

Binary Dependent Variables In some cases the outcome of interest rather than one of the right hand side variables - is discrete rather than continuous Binary Dependent Variables In some cases the outcome

Binary Dependent Variables In some cases the outcome of interest rather than one of the right hand side variables - is discrete rather than continuous Binary Dependent Variables In some cases the outcome

Extensions to the Basic Framework II

Topic 7 Extensions to the Basic Framework II ARE/ECN 240 A Graduate Econometrics Professor: Òscar Jordà Outline of this topic Nonlinear regression Limited Dependent Variable regression Applications of

Topic 7 Extensions to the Basic Framework II ARE/ECN 240 A Graduate Econometrics Professor: Òscar Jordà Outline of this topic Nonlinear regression Limited Dependent Variable regression Applications of

Lecture 12: Effect modification, and confounding in logistic regression

Lecture 12: Effect modification, and confounding in logistic regression Ani Manichaikul amanicha@jhsph.edu 4 May 2007 Today Categorical predictor create dummy variables just like for linear regression

Lecture 12: Effect modification, and confounding in logistic regression Ani Manichaikul amanicha@jhsph.edu 4 May 2007 Today Categorical predictor create dummy variables just like for linear regression

Linear Regression with Multiple Regressors

Linear Regression with Multiple Regressors (SW Chapter 6) Outline 1. Omitted variable bias 2. Causality and regression analysis 3. Multiple regression and OLS 4. Measures of fit 5. Sampling distribution

Linear Regression with Multiple Regressors (SW Chapter 6) Outline 1. Omitted variable bias 2. Causality and regression analysis 3. Multiple regression and OLS 4. Measures of fit 5. Sampling distribution

Binomial Model. Lecture 10: Introduction to Logistic Regression. Logistic Regression. Binomial Distribution. n independent trials

Lecture : Introduction to Logistic Regression Ani Manichaikul amanicha@jhsph.edu 2 May 27 Binomial Model n independent trials (e.g., coin tosses) p = probability of success on each trial (e.g., p =! =

Lecture : Introduction to Logistic Regression Ani Manichaikul amanicha@jhsph.edu 2 May 27 Binomial Model n independent trials (e.g., coin tosses) p = probability of success on each trial (e.g., p =! =

Lecture 10: Introduction to Logistic Regression

Lecture 10: Introduction to Logistic Regression Ani Manichaikul amanicha@jhsph.edu 2 May 2007 Logistic Regression Regression for a response variable that follows a binomial distribution Recall the binomial

Lecture 10: Introduction to Logistic Regression Ani Manichaikul amanicha@jhsph.edu 2 May 2007 Logistic Regression Regression for a response variable that follows a binomial distribution Recall the binomial

Homework Solutions Applied Logistic Regression

Homework Solutions Applied Logistic Regression WEEK 6 Exercise 1 From the ICU data, use as the outcome variable vital status (STA) and CPR prior to ICU admission (CPR) as a covariate. (a) Demonstrate that

Homework Solutions Applied Logistic Regression WEEK 6 Exercise 1 From the ICU data, use as the outcome variable vital status (STA) and CPR prior to ICU admission (CPR) as a covariate. (a) Demonstrate that

Statistical Inference with Regression Analysis

Introductory Applied Econometrics EEP/IAS 118 Spring 2015 Steven Buck Lecture #13 Statistical Inference with Regression Analysis Next we turn to calculating confidence intervals and hypothesis testing

Introductory Applied Econometrics EEP/IAS 118 Spring 2015 Steven Buck Lecture #13 Statistical Inference with Regression Analysis Next we turn to calculating confidence intervals and hypothesis testing

Nonlinear Econometric Analysis (ECO 722) : Homework 2 Answers. (1 θ) if y i = 0. which can be written in an analytically more convenient way as

: Homework 2 Answers. (1 θ) if y i = 0. which can be written in an analytically more convenient way as") Nonlinear Econometric Analysis (ECO 722) : Homework 2 Answers 1. Consider a binary random variable y i that describes a Bernoulli trial in which the probability of observing y i = 1 in any draw is given

Nonlinear Econometric Analysis (ECO 722) : Homework 2 Answers 1. Consider a binary random variable y i that describes a Bernoulli trial in which the probability of observing y i = 1 in any draw is given

Applied Statistics and Econometrics

Applied Statistics and Econometrics Lecture 6 Saul Lach September 2017 Saul Lach () Applied Statistics and Econometrics September 2017 1 / 53 Outline of Lecture 6 1 Omitted variable bias (SW 6.1) 2 Multiple

Applied Statistics and Econometrics Lecture 6 Saul Lach September 2017 Saul Lach () Applied Statistics and Econometrics September 2017 1 / 53 Outline of Lecture 6 1 Omitted variable bias (SW 6.1) 2 Multiple

ECON Introductory Econometrics. Lecture 5: OLS with One Regressor: Hypothesis Tests

ECON4150 - Introductory Econometrics Lecture 5: OLS with One Regressor: Hypothesis Tests Monique de Haan (moniqued@econ.uio.no) Stock and Watson Chapter 5 Lecture outline 2 Testing Hypotheses about one

ECON4150 - Introductory Econometrics Lecture 5: OLS with One Regressor: Hypothesis Tests Monique de Haan (moniqued@econ.uio.no) Stock and Watson Chapter 5 Lecture outline 2 Testing Hypotheses about one

Linear Regression with one Regressor

1 Linear Regression with one Regressor Covering Chapters 4.1 and 4.2. We ve seen the California test score data before. Now we will try to estimate the marginal effect of STR on SCORE. To motivate these

1 Linear Regression with one Regressor Covering Chapters 4.1 and 4.2. We ve seen the California test score data before. Now we will try to estimate the marginal effect of STR on SCORE. To motivate these

Sociology 362 Data Exercise 6 Logistic Regression 2

Sociology 362 Data Exercise 6 Logistic Regression 2 The questions below refer to the data and output beginning on the next page. Although the raw data are given there, you do not have to do any Stata runs

Sociology 362 Data Exercise 6 Logistic Regression 2 The questions below refer to the data and output beginning on the next page. Although the raw data are given there, you do not have to do any Stata runs

Introduction to Econometrics. Multiple Regression

Introduction to Econometrics The statistical analysis of economic (and related) data STATS301 Multiple Regression Titulaire: Christopher Bruffaerts Assistant: Lorenzo Ricci 1 OLS estimate of the TS/STR

Introduction to Econometrics The statistical analysis of economic (and related) data STATS301 Multiple Regression Titulaire: Christopher Bruffaerts Assistant: Lorenzo Ricci 1 OLS estimate of the TS/STR

Introduction to Econometrics. Multiple Regression (2016/2017)

") Introduction to Econometrics STAT-S-301 Multiple Regression (016/017) Lecturer: Yves Dominicy Teaching Assistant: Elise Petit 1 OLS estimate of the TS/STR relation: OLS estimate of the Test Score/STR relation:

Introduction to Econometrics STAT-S-301 Multiple Regression (016/017) Lecturer: Yves Dominicy Teaching Assistant: Elise Petit 1 OLS estimate of the TS/STR relation: OLS estimate of the Test Score/STR relation:

Introduction to Econometrics Third Edition James H. Stock Mark W. Watson The statistical analysis of economic (and related) data

data") Introduction to Econometrics Third Edition James H. Stock Mark W. Watson The statistical analysis of economic (and related) data 1/2/3-1 1/2/3-2 Brief Overview of the Course Economics suggests important

Introduction to Econometrics Third Edition James H. Stock Mark W. Watson The statistical analysis of economic (and related) data 1/2/3-1 1/2/3-2 Brief Overview of the Course Economics suggests important

Exam ECON3150/4150: Introductory Econometrics. 18 May 2016; 09:00h-12.00h.

Exam ECON3150/4150: Introductory Econometrics. 18 May 2016; 09:00h-12.00h. This is an open book examination where all printed and written resources, in addition to a calculator, are allowed. If you are

Exam ECON3150/4150: Introductory Econometrics. 18 May 2016; 09:00h-12.00h. This is an open book examination where all printed and written resources, in addition to a calculator, are allowed. If you are

7/28/15. Review Homework. Overview. Lecture 6: Logistic Regression Analysis

Lecture 6: Logistic Regression Analysis Christopher S. Hollenbeak, PhD Jane R. Schubart, PhD The Outcomes Research Toolbox Review Homework 2 Overview Logistic regression model conceptually Logistic regression

Lecture 6: Logistic Regression Analysis Christopher S. Hollenbeak, PhD Jane R. Schubart, PhD The Outcomes Research Toolbox Review Homework 2 Overview Logistic regression model conceptually Logistic regression

Immigration attitudes (opposes immigration or supports it) it may seriously misestimate the magnitude of the effects of IVs

it may seriously misestimate the magnitude of the effects of IVs") Logistic Regression, Part I: Problems with the Linear Probability Model (LPM) Richard Williams, University of Notre Dame, https://www3.nd.edu/~rwilliam/ Last revised February 22, 2015 This handout steals

Logistic Regression, Part I: Problems with the Linear Probability Model (LPM) Richard Williams, University of Notre Dame, https://www3.nd.edu/~rwilliam/ Last revised February 22, 2015 This handout steals

EPSY 905: Fundamentals of Multivariate Modeling Online Lecture #7

Introduction to Generalized Univariate Models: Models for Binary Outcomes EPSY 905: Fundamentals of Multivariate Modeling Online Lecture #7 EPSY 905: Intro to Generalized In This Lecture A short review

Introduction to Generalized Univariate Models: Models for Binary Outcomes EPSY 905: Fundamentals of Multivariate Modeling Online Lecture #7 EPSY 905: Intro to Generalized In This Lecture A short review

Applied Statistics and Econometrics

Applied Statistics and Econometrics Lecture 5 Saul Lach September 2017 Saul Lach () Applied Statistics and Econometrics September 2017 1 / 44 Outline of Lecture 5 Now that we know the sampling distribution

Applied Statistics and Econometrics Lecture 5 Saul Lach September 2017 Saul Lach () Applied Statistics and Econometrics September 2017 1 / 44 Outline of Lecture 5 Now that we know the sampling distribution

ECON 594: Lecture #6

ECON 594: Lecture #6 Thomas Lemieux Vancouver School of Economics, UBC May 2018 1 Limited dependent variables: introduction Up to now, we have been implicitly assuming that the dependent variable, y, was

ECON 594: Lecture #6 Thomas Lemieux Vancouver School of Economics, UBC May 2018 1 Limited dependent variables: introduction Up to now, we have been implicitly assuming that the dependent variable, y, was

Lecture 3.1 Basic Logistic LDA

y Lecture.1 Basic Logistic LDA 0.2.4.6.8 1 Outline Quick Refresher on Ordinary Logistic Regression and Stata Women s employment example Cross-Over Trial LDA Example -100-50 0 50 100 -- Longitudinal Data

y Lecture.1 Basic Logistic LDA 0.2.4.6.8 1 Outline Quick Refresher on Ordinary Logistic Regression and Stata Women s employment example Cross-Over Trial LDA Example -100-50 0 50 100 -- Longitudinal Data

Assessing Studies Based on Multiple Regression

Assessing Studies Based on Multiple Regression Outline 1. Internal and External Validity 2. Threats to Internal Validity a. Omitted variable bias b. Functional form misspecification c. Errors-in-variables

Assessing Studies Based on Multiple Regression Outline 1. Internal and External Validity 2. Threats to Internal Validity a. Omitted variable bias b. Functional form misspecification c. Errors-in-variables

ECON Introductory Econometrics. Lecture 7: OLS with Multiple Regressors Hypotheses tests

ECON4150 - Introductory Econometrics Lecture 7: OLS with Multiple Regressors Hypotheses tests Monique de Haan (moniqued@econ.uio.no) Stock and Watson Chapter 7 Lecture outline 2 Hypothesis test for single

ECON4150 - Introductory Econometrics Lecture 7: OLS with Multiple Regressors Hypotheses tests Monique de Haan (moniqued@econ.uio.no) Stock and Watson Chapter 7 Lecture outline 2 Hypothesis test for single

Introduction to Regression Analysis. Dr. Devlina Chatterjee 11 th August, 2017

Introduction to Regression Analysis Dr. Devlina Chatterjee 11 th August, 2017 What is regression analysis? Regression analysis is a statistical technique for studying linear relationships. One dependent

Introduction to Regression Analysis Dr. Devlina Chatterjee 11 th August, 2017 What is regression analysis? Regression analysis is a statistical technique for studying linear relationships. One dependent

Introduction to Maximum Likelihood Estimation

Introduction to Maximum Likelihood Estimation Eric Zivot July 26, 2012 The Likelihood Function Let 1 be an iid sample with pdf ( ; ) where is a ( 1) vector of parameters that characterize ( ; ) Example:

Introduction to Maximum Likelihood Estimation Eric Zivot July 26, 2012 The Likelihood Function Let 1 be an iid sample with pdf ( ; ) where is a ( 1) vector of parameters that characterize ( ; ) Example:

Quiz 1. Name: Instructions: Closed book, notes, and no electronic devices.

Quiz 1. Name: Instructions: Closed book, notes, and no electronic devices. 1. What is the difference between a deterministic model and a probabilistic model? (Two or three sentences only). 2. What is the

Quiz 1. Name: Instructions: Closed book, notes, and no electronic devices. 1. What is the difference between a deterministic model and a probabilistic model? (Two or three sentences only). 2. What is the

Econometrics Homework 1

Econometrics Homework Due Date: March, 24. by This problem set includes questions for Lecture -4 covered before midterm exam. Question Let z be a random column vector of size 3 : z = @ (a) Write out z

Econometrics Homework Due Date: March, 24. by This problem set includes questions for Lecture -4 covered before midterm exam. Question Let z be a random column vector of size 3 : z = @ (a) Write out z

5. Let W follow a normal distribution with mean of μ and the variance of 1. Then, the pdf of W is

Practice Final Exam Last Name:, First Name:. Please write LEGIBLY. Answer all questions on this exam in the space provided (you may use the back of any page if you need more space). Show all work but do

Practice Final Exam Last Name:, First Name:. Please write LEGIBLY. Answer all questions on this exam in the space provided (you may use the back of any page if you need more space). Show all work but do

ECON Introductory Econometrics. Lecture 17: Experiments

ECON4150 - Introductory Econometrics Lecture 17: Experiments Monique de Haan (moniqued@econ.uio.no) Stock and Watson Chapter 13 Lecture outline 2 Why study experiments? The potential outcome framework.

ECON4150 - Introductory Econometrics Lecture 17: Experiments Monique de Haan (moniqued@econ.uio.no) Stock and Watson Chapter 13 Lecture outline 2 Why study experiments? The potential outcome framework.

Generalized Linear Models for Non-Normal Data

Generalized Linear Models for Non-Normal Data Today s Class: 3 parts of a generalized model Models for binary outcomes Complications for generalized multivariate or multilevel models SPLH 861: Lecture

Generalized Linear Models for Non-Normal Data Today s Class: 3 parts of a generalized model Models for binary outcomes Complications for generalized multivariate or multilevel models SPLH 861: Lecture

CRE METHODS FOR UNBALANCED PANELS Correlated Random Effects Panel Data Models IZA Summer School in Labor Economics May 13-19, 2013 Jeffrey M.

CRE METHODS FOR UNBALANCED PANELS Correlated Random Effects Panel Data Models IZA Summer School in Labor Economics May 13-19, 2013 Jeffrey M. Wooldridge Michigan State University 1. Introduction 2. Linear

CRE METHODS FOR UNBALANCED PANELS Correlated Random Effects Panel Data Models IZA Summer School in Labor Economics May 13-19, 2013 Jeffrey M. Wooldridge Michigan State University 1. Introduction 2. Linear

Binary Logistic Regression

The coefficients of the multiple regression model are estimated using sample data with k independent variables Estimated (or predicted) value of Y Estimated intercept Estimated slope coefficients Ŷ = b

The coefficients of the multiple regression model are estimated using sample data with k independent variables Estimated (or predicted) value of Y Estimated intercept Estimated slope coefficients Ŷ = b

Using the same data as before, here is part of the output we get in Stata when we do a logistic regression of Grade on Gpa, Tuce and Psi.

Logistic Regression, Part III: Hypothesis Testing, Comparisons to OLS Richard Williams, University of Notre Dame, https://www3.nd.edu/~rwilliam/ Last revised January 14, 2018 This handout steals heavily

Logistic Regression, Part III: Hypothesis Testing, Comparisons to OLS Richard Williams, University of Notre Dame, https://www3.nd.edu/~rwilliam/ Last revised January 14, 2018 This handout steals heavily

i (x i x) 2 1 N i x i(y i y) Var(x) = P (x 1 x) Var(x)

2 1 N i x i(y i y) Var(x) = P (x 1 x) Var(x)") ECO 6375 Prof Millimet Problem Set #2: Answer Key Stata problem 2 Q 3 Q (a) The sample average of the individual-specific marginal effects is 0039 for educw and -0054 for white Thus, on average, an extra

ECO 6375 Prof Millimet Problem Set #2: Answer Key Stata problem 2 Q 3 Q (a) The sample average of the individual-specific marginal effects is 0039 for educw and -0054 for white Thus, on average, an extra

Introduction to Econometrics

Introduction to Econometrics STAT-S-301 Panel Data (2016/2017) Lecturer: Yves Dominicy Teaching Assistant: Elise Petit 1 Regression with Panel Data A panel dataset contains observations on multiple entities

Introduction to Econometrics STAT-S-301 Panel Data (2016/2017) Lecturer: Yves Dominicy Teaching Assistant: Elise Petit 1 Regression with Panel Data A panel dataset contains observations on multiple entities

Consider Table 1 (Note connection to start-stop process).

.") Discrete-Time Data and Models Discretized duration data are still duration data! Consider Table 1 (Note connection to start-stop process). Table 1: Example of Discrete-Time Event History Data Case Event

Discrete-Time Data and Models Discretized duration data are still duration data! Consider Table 1 (Note connection to start-stop process). Table 1: Example of Discrete-Time Event History Data Case Event

Ch 7: Dummy (binary, indicator) variables

variables") Ch 7: Dummy (binary, indicator) variables :Examples Dummy variable are used to indicate the presence or absence of a characteristic. For example, define female i 1 if obs i is female 0 otherwise or male

Ch 7: Dummy (binary, indicator) variables :Examples Dummy variable are used to indicate the presence or absence of a characteristic. For example, define female i 1 if obs i is female 0 otherwise or male

Applied Statistics and Econometrics

Applied Statistics and Econometrics Lecture 7 Saul Lach September 2017 Saul Lach () Applied Statistics and Econometrics September 2017 1 / 68 Outline of Lecture 7 1 Empirical example: Italian labor force

Applied Statistics and Econometrics Lecture 7 Saul Lach September 2017 Saul Lach () Applied Statistics and Econometrics September 2017 1 / 68 Outline of Lecture 7 1 Empirical example: Italian labor force

Truncation and Censoring

Truncation and Censoring Laura Magazzini laura.magazzini@univr.it Laura Magazzini (@univr.it) Truncation and Censoring 1 / 35 Truncation and censoring Truncation: sample data are drawn from a subset of

Truncation and Censoring Laura Magazzini laura.magazzini@univr.it Laura Magazzini (@univr.it) Truncation and Censoring 1 / 35 Truncation and censoring Truncation: sample data are drawn from a subset of

Lecture notes to Chapter 11, Regression with binary dependent variables - probit and logit regression

Lecture notes to Chapter 11, Regression with binary dependent variables - probit and logit regression Tore Schweder October 28, 2011 Outline Examples of binary respons variables Probit and logit - examples

Lecture notes to Chapter 11, Regression with binary dependent variables - probit and logit regression Tore Schweder October 28, 2011 Outline Examples of binary respons variables Probit and logit - examples

Discrete Dependent Variable Models

Discrete Dependent Variable Models James J. Heckman University of Chicago This draft, April 10, 2006 Here s the general approach of this lecture: Economic model Decision rule (e.g. utility maximization)

Discrete Dependent Variable Models James J. Heckman University of Chicago This draft, April 10, 2006 Here s the general approach of this lecture: Economic model Decision rule (e.g. utility maximization)

Essential of Simple regression

Essential of Simple regression We use simple regression when we are interested in the relationship between two variables (e.g., x is class size, and y is student s GPA). For simplicity we assume the relationship

Essential of Simple regression We use simple regression when we are interested in the relationship between two variables (e.g., x is class size, and y is student s GPA). For simplicity we assume the relationship

ECON3150/4150 Spring 2015

ECON3150/4150 Spring 2015 Lecture 3&4 - The linear regression model Siv-Elisabeth Skjelbred University of Oslo January 29, 2015 1 / 67 Chapter 4 in S&W Section 17.1 in S&W (extended OLS assumptions) 2

ECON3150/4150 Spring 2015 Lecture 3&4 - The linear regression model Siv-Elisabeth Skjelbred University of Oslo January 29, 2015 1 / 67 Chapter 4 in S&W Section 17.1 in S&W (extended OLS assumptions) 2

Final Exam. Question 1 (20 points) 2 (25 points) 3 (30 points) 4 (25 points) 5 (10 points) 6 (40 points) Total (150 points) Bonus question (10)

2 (25 points) 3 (30 points) 4 (25 points) 5 (10 points) 6 (40 points) Total (150 points) Bonus question (10)") Name Economics 170 Spring 2004 Honor pledge: I have neither given nor received aid on this exam including the preparation of my one page formula list and the preparation of the Stata assignment for the

Name Economics 170 Spring 2004 Honor pledge: I have neither given nor received aid on this exam including the preparation of my one page formula list and the preparation of the Stata assignment for the

h=1 exp (X : J h=1 Even the direction of the e ect is not determined by jk. A simpler interpretation of j is given by the odds-ratio

Multivariate Response Models The response variable is unordered and takes more than two values. The term unordered refers to the fact that response 3 is not more favored than response 2. One choice from

Multivariate Response Models The response variable is unordered and takes more than two values. The term unordered refers to the fact that response 3 is not more favored than response 2. One choice from

WISE MA/PhD Programs Econometrics Instructor: Brett Graham Spring Semester, Academic Year Exam Version: A

WISE MA/PhD Programs Econometrics Instructor: Brett Graham Spring Semester, 2015-16 Academic Year Exam Version: A INSTRUCTIONS TO STUDENTS 1 The time allowed for this examination paper is 2 hours. 2 This

WISE MA/PhD Programs Econometrics Instructor: Brett Graham Spring Semester, 2015-16 Academic Year Exam Version: A INSTRUCTIONS TO STUDENTS 1 The time allowed for this examination paper is 2 hours. 2 This

WISE International Masters

WISE International Masters ECONOMETRICS Instructor: Brett Graham INSTRUCTIONS TO STUDENTS 1 The time allowed for this examination paper is 2 hours. 2 This examination paper contains 32 questions. You are

WISE International Masters ECONOMETRICS Instructor: Brett Graham INSTRUCTIONS TO STUDENTS 1 The time allowed for this examination paper is 2 hours. 2 This examination paper contains 32 questions. You are

6. Assessing studies based on multiple regression

6. Assessing studies based on multiple regression Questions of this section: What makes a study using multiple regression (un)reliable? When does multiple regression provide a useful estimate of the causal

6. Assessing studies based on multiple regression Questions of this section: What makes a study using multiple regression (un)reliable? When does multiple regression provide a useful estimate of the causal

Multivariate Regression: Part I

Topic 1 Multivariate Regression: Part I ARE/ECN 240 A Graduate Econometrics Professor: Òscar Jordà Outline of this topic Statement of the objective: we want to explain the behavior of one variable as a

Topic 1 Multivariate Regression: Part I ARE/ECN 240 A Graduate Econometrics Professor: Òscar Jordà Outline of this topic Statement of the objective: we want to explain the behavior of one variable as a

Econometrics I KS. Module 2: Multivariate Linear Regression. Alexander Ahammer. This version: April 16, 2018

Econometrics I KS Module 2: Multivariate Linear Regression Alexander Ahammer Department of Economics Johannes Kepler University of Linz This version: April 16, 2018 Alexander Ahammer (JKU) Module 2: Multivariate

Econometrics I KS Module 2: Multivariate Linear Regression Alexander Ahammer Department of Economics Johannes Kepler University of Linz This version: April 16, 2018 Alexander Ahammer (JKU) Module 2: Multivariate

Non-linear panel data modeling

Non-linear panel data modeling Laura Magazzini University of Verona laura.magazzini@univr.it http://dse.univr.it/magazzini May 2010 Laura Magazzini (@univr.it) Non-linear panel data modeling May 2010 1

Non-linear panel data modeling Laura Magazzini University of Verona laura.magazzini@univr.it http://dse.univr.it/magazzini May 2010 Laura Magazzini (@univr.it) Non-linear panel data modeling May 2010 1

Exam ECON5106/9106 Fall 2018

Exam ECO506/906 Fall 208. Suppose you observe (y i,x i ) for i,2,, and you assume f (y i x i ;α,β) γ i exp( γ i y i ) where γ i exp(α + βx i ). ote that in this case, the conditional mean of E(y i X x

Exam ECO506/906 Fall 208. Suppose you observe (y i,x i ) for i,2,, and you assume f (y i x i ;α,β) γ i exp( γ i y i ) where γ i exp(α + βx i ). ote that in this case, the conditional mean of E(y i X x

Lecture 4: Multivariate Regression, Part 2

Lecture 4: Multivariate Regression, Part 2 Gauss-Markov Assumptions 1) Linear in Parameters: Y X X X i 0 1 1 2 2 k k 2) Random Sampling: we have a random sample from the population that follows the above

Lecture 4: Multivariate Regression, Part 2 Gauss-Markov Assumptions 1) Linear in Parameters: Y X X X i 0 1 1 2 2 k k 2) Random Sampling: we have a random sample from the population that follows the above

POLI 8501 Introduction to Maximum Likelihood Estimation

POLI 8501 Introduction to Maximum Likelihood Estimation Maximum Likelihood Intuition Consider a model that looks like this: Y i N(µ, σ 2 ) So: E(Y ) = µ V ar(y ) = σ 2 Suppose you have some data on Y,

POLI 8501 Introduction to Maximum Likelihood Estimation Maximum Likelihood Intuition Consider a model that looks like this: Y i N(µ, σ 2 ) So: E(Y ) = µ V ar(y ) = σ 2 Suppose you have some data on Y,

Hypothesis Tests and Confidence Intervals. in Multiple Regression

ECON4135, LN6 Hypothesis Tests and Confidence Intervals Outline 1. Why multipple regression? in Multiple Regression (SW Chapter 7) 2. Simpson s paradox (omitted variables bias) 3. Hypothesis tests and

ECON4135, LN6 Hypothesis Tests and Confidence Intervals Outline 1. Why multipple regression? in Multiple Regression (SW Chapter 7) 2. Simpson s paradox (omitted variables bias) 3. Hypothesis tests and

Econ 371 Problem Set #6 Answer Sheet In this first question, you are asked to consider the following equation:

Econ 37 Problem Set #6 Answer Sheet 0. In this first question, you are asked to consider the following equation: Y it = β 0 + β X it + β 3 S t + u it. () You are asked how you might time-demean the data

Econ 37 Problem Set #6 Answer Sheet 0. In this first question, you are asked to consider the following equation: Y it = β 0 + β X it + β 3 S t + u it. () You are asked how you might time-demean the data

Recent Advances in the Field of Trade Theory and Policy Analysis Using Micro-Level Data

Recent Advances in the Field of Trade Theory and Policy Analysis Using Micro-Level Data July 2012 Bangkok, Thailand Cosimo Beverelli (World Trade Organization) 1 Content a) Classical regression model b)

Recent Advances in the Field of Trade Theory and Policy Analysis Using Micro-Level Data July 2012 Bangkok, Thailand Cosimo Beverelli (World Trade Organization) 1 Content a) Classical regression model b)

Linear Regression with Multiple Regressors

Linear Regression with Multiple Regressors (SW Chapter 6) Outline 1. Omitted variable bias 2. Causality and regression analysis 3. Multiple regression and OLS 4. Measures of fit 5. Sampling distribution

Linear Regression with Multiple Regressors (SW Chapter 6) Outline 1. Omitted variable bias 2. Causality and regression analysis 3. Multiple regression and OLS 4. Measures of fit 5. Sampling distribution

ESTIMATING AVERAGE TREATMENT EFFECTS: REGRESSION DISCONTINUITY DESIGNS Jeff Wooldridge Michigan State University BGSE/IZA Course in Microeconometrics

ESTIMATING AVERAGE TREATMENT EFFECTS: REGRESSION DISCONTINUITY DESIGNS Jeff Wooldridge Michigan State University BGSE/IZA Course in Microeconometrics July 2009 1. Introduction 2. The Sharp RD Design 3.

ESTIMATING AVERAGE TREATMENT EFFECTS: REGRESSION DISCONTINUITY DESIGNS Jeff Wooldridge Michigan State University BGSE/IZA Course in Microeconometrics July 2009 1. Introduction 2. The Sharp RD Design 3.

Introduction to Econometrics

Introduction to Econometrics STAT-S-301 Introduction to Time Series Regression and Forecasting (2016/2017) Lecturer: Yves Dominicy Teaching Assistant: Elise Petit 1 Introduction to Time Series Regression

Introduction to Econometrics STAT-S-301 Introduction to Time Series Regression and Forecasting (2016/2017) Lecturer: Yves Dominicy Teaching Assistant: Elise Petit 1 Introduction to Time Series Regression

4. Nonlinear regression functions

4. Nonlinear regression functions Up to now: Population regression function was assumed to be linear The slope(s) of the population regression function is (are) constant The effect on Y of a unit-change

4. Nonlinear regression functions Up to now: Population regression function was assumed to be linear The slope(s) of the population regression function is (are) constant The effect on Y of a unit-change

Chapter 6: Linear Regression With Multiple Regressors

Chapter 6: Linear Regression With Multiple Regressors 1-1 Outline 1. Omitted variable bias 2. Causality and regression analysis 3. Multiple regression and OLS 4. Measures of fit 5. Sampling distribution

Chapter 6: Linear Regression With Multiple Regressors 1-1 Outline 1. Omitted variable bias 2. Causality and regression analysis 3. Multiple regression and OLS 4. Measures of fit 5. Sampling distribution

Empirical Application of Simple Regression (Chapter 2)

") Empirical Application of Simple Regression (Chapter 2) 1. The data file is House Data, which can be downloaded from my webpage. 2. Use stata menu File Import Excel Spreadsheet to read the data. Don t forget

Empirical Application of Simple Regression (Chapter 2) 1. The data file is House Data, which can be downloaded from my webpage. 2. Use stata menu File Import Excel Spreadsheet to read the data. Don t forget

Lecture#12. Instrumental variables regression Causal parameters III

Lecture#12 Instrumental variables regression Causal parameters III 1 Demand experiment, market data analysis & simultaneous causality 2 Simultaneous causality Your task is to estimate the demand function

Lecture#12 Instrumental variables regression Causal parameters III 1 Demand experiment, market data analysis & simultaneous causality 2 Simultaneous causality Your task is to estimate the demand function

Lecture 4: Multivariate Regression, Part 2

Lecture 4: Multivariate Regression, Part 2 Gauss-Markov Assumptions 1) Linear in Parameters: Y X X X i 0 1 1 2 2 k k 2) Random Sampling: we have a random sample from the population that follows the above

Lecture 4: Multivariate Regression, Part 2 Gauss-Markov Assumptions 1) Linear in Parameters: Y X X X i 0 1 1 2 2 k k 2) Random Sampling: we have a random sample from the population that follows the above

STOCKHOLM UNIVERSITY Department of Economics Course name: Empirical Methods Course code: EC40 Examiner: Lena Nekby Number of credits: 7,5 credits Date of exam: Saturday, May 9, 008 Examination time: 3

STOCKHOLM UNIVERSITY Department of Economics Course name: Empirical Methods Course code: EC40 Examiner: Lena Nekby Number of credits: 7,5 credits Date of exam: Saturday, May 9, 008 Examination time: 3

ECO220Y Simple Regression: Testing the Slope

ECO220Y Simple Regression: Testing the Slope Readings: Chapter 18 (Sections 18.3-18.5) Winter 2012 Lecture 19 (Winter 2012) Simple Regression Lecture 19 1 / 32 Simple Regression Model y i = β 0 + β 1 x

ECO220Y Simple Regression: Testing the Slope Readings: Chapter 18 (Sections 18.3-18.5) Winter 2012 Lecture 19 (Winter 2012) Simple Regression Lecture 19 1 / 32 Simple Regression Model y i = β 0 + β 1 x

Econ 583 Homework 7 Suggested Solutions: Wald, LM and LR based on GMM and MLE

Econ 583 Homework 7 Suggested Solutions: Wald, LM and LR based on GMM and MLE Eric Zivot Winter 013 1 Wald, LR and LM statistics based on generalized method of moments estimation Let 1 be an iid sample

Econ 583 Homework 7 Suggested Solutions: Wald, LM and LR based on GMM and MLE Eric Zivot Winter 013 1 Wald, LR and LM statistics based on generalized method of moments estimation Let 1 be an iid sample

1 Motivation for Instrumental Variable (IV) Regression

Regression") ECON 370: IV & 2SLS 1 Instrumental Variables Estimation and Two Stage Least Squares Econometric Methods, ECON 370 Let s get back to the thiking in terms of cross sectional (or pooled cross sectional) data

ECON 370: IV & 2SLS 1 Instrumental Variables Estimation and Two Stage Least Squares Econometric Methods, ECON 370 Let s get back to the thiking in terms of cross sectional (or pooled cross sectional) data

The F distribution. If: 1. u 1,,u n are normally distributed; and 2. X i is distributed independently of u i (so in particular u i is homoskedastic)

") The F distribution If: 1. u 1,,u n are normally distributed; and. X i is distributed independently of u i (so in particular u i is homoskedastic) then the homoskedasticity-only F-statistic has the F q,n-k

The F distribution If: 1. u 1,,u n are normally distributed; and. X i is distributed independently of u i (so in particular u i is homoskedastic) then the homoskedasticity-only F-statistic has the F q,n-k

Applied Health Economics (for B.Sc.)

") Applied Health Economics (for B.Sc.) Helmut Farbmacher Department of Economics University of Mannheim Autumn Semester 2017 Outlook 1 Linear models (OLS, Omitted variables, 2SLS) 2 Limited and qualitative

Applied Health Economics (for B.Sc.) Helmut Farbmacher Department of Economics University of Mannheim Autumn Semester 2017 Outlook 1 Linear models (OLS, Omitted variables, 2SLS) 2 Limited and qualitative

Ninth ARTNeT Capacity Building Workshop for Trade Research "Trade Flows and Trade Policy Analysis"

Ninth ARTNeT Capacity Building Workshop for Trade Research "Trade Flows and Trade Policy Analysis" June 2013 Bangkok, Thailand Cosimo Beverelli and Rainer Lanz (World Trade Organization) 1 Selected econometric

Ninth ARTNeT Capacity Building Workshop for Trade Research "Trade Flows and Trade Policy Analysis" June 2013 Bangkok, Thailand Cosimo Beverelli and Rainer Lanz (World Trade Organization) 1 Selected econometric

ECON3150/4150 Spring 2016

ECON3150/4150 Spring 2016 Lecture 6 Multiple regression model Siv-Elisabeth Skjelbred University of Oslo February 5th Last updated: February 3, 2016 1 / 49 Outline Multiple linear regression model and

ECON3150/4150 Spring 2016 Lecture 6 Multiple regression model Siv-Elisabeth Skjelbred University of Oslo February 5th Last updated: February 3, 2016 1 / 49 Outline Multiple linear regression model and

Control Function and Related Methods: Nonlinear Models

Control Function and Related Methods: Nonlinear Models Jeff Wooldridge Michigan State University Programme Evaluation for Policy Analysis Institute for Fiscal Studies June 2012 1. General Approach 2. Nonlinear

Control Function and Related Methods: Nonlinear Models Jeff Wooldridge Michigan State University Programme Evaluation for Policy Analysis Institute for Fiscal Studies June 2012 1. General Approach 2. Nonlinear

Limited Dependent Variable Models II

Limited Dependent Variable Models II Fall 2008 Environmental Econometrics (GR03) LDV Fall 2008 1 / 15 Models with Multiple Choices The binary response model was dealing with a decision problem with two

Limited Dependent Variable Models II Fall 2008 Environmental Econometrics (GR03) LDV Fall 2008 1 / 15 Models with Multiple Choices The binary response model was dealing with a decision problem with two

Introduction to Econometrics. Regression with Panel Data

Introduction to Econometrics The statistical analysis of economic (and related) data STATS301 Regression with Panel Data Titulaire: Christopher Bruffaerts Assistant: Lorenzo Ricci 1 Regression with Panel

Introduction to Econometrics The statistical analysis of economic (and related) data STATS301 Regression with Panel Data Titulaire: Christopher Bruffaerts Assistant: Lorenzo Ricci 1 Regression with Panel

L6: Regression II. JJ Chen. July 2, 2015

L6: Regression II JJ Chen July 2, 2015 Today s Plan Review basic inference based on Sample average Difference in sample average Extrapolate the knowledge to sample regression coefficients Standard error,

L6: Regression II JJ Chen July 2, 2015 Today s Plan Review basic inference based on Sample average Difference in sample average Extrapolate the knowledge to sample regression coefficients Standard error,

Recent Developments in Multilevel Modeling

Recent Developments in Multilevel Modeling Roberto G. Gutierrez Director of Statistics StataCorp LP 2007 North American Stata Users Group Meeting, Boston R. Gutierrez (StataCorp) Multilevel Modeling August

Recent Developments in Multilevel Modeling Roberto G. Gutierrez Director of Statistics StataCorp LP 2007 North American Stata Users Group Meeting, Boston R. Gutierrez (StataCorp) Multilevel Modeling August

Lab 11 - Heteroskedasticity

Lab 11 - Heteroskedasticity Spring 2017 Contents 1 Introduction 2 2 Heteroskedasticity 2 3 Addressing heteroskedasticity in Stata 3 4 Testing for heteroskedasticity 4 5 A simple example 5 1 1 Introduction

Lab 11 - Heteroskedasticity Spring 2017 Contents 1 Introduction 2 2 Heteroskedasticity 2 3 Addressing heteroskedasticity in Stata 3 4 Testing for heteroskedasticity 4 5 A simple example 5 1 1 Introduction

Binary Choice Models Probit & Logit. = 0 with Pr = 0 = 1. decision-making purchase of durable consumer products unemployment

BINARY CHOICE MODELS Y ( Y ) ( Y ) 1 with Pr = 1 = P = 0 with Pr = 0 = 1 P Examples: decision-making purchase of durable consumer products unemployment Estimation with OLS? Yi = Xiβ + εi Problems: nonsense

BINARY CHOICE MODELS Y ( Y ) ( Y ) 1 with Pr = 1 = P = 0 with Pr = 0 = 1 P Examples: decision-making purchase of durable consumer products unemployment Estimation with OLS? Yi = Xiβ + εi Problems: nonsense

Practice exam questions

Practice exam questions Nathaniel Higgins nhiggins@jhu.edu, nhiggins@ers.usda.gov 1. The following question is based on the model y = β 0 + β 1 x 1 + β 2 x 2 + β 3 x 3 + u. Discuss the following two hypotheses.

Practice exam questions Nathaniel Higgins nhiggins@jhu.edu, nhiggins@ers.usda.gov 1. The following question is based on the model y = β 0 + β 1 x 1 + β 2 x 2 + β 3 x 3 + u. Discuss the following two hypotheses.

Problem Set 1 ANSWERS

Economics 20 Prof. Patricia M. Anderson Problem Set 1 ANSWERS Part I. Multiple Choice Problems 1. If X and Z are two random variables, then E[X-Z] is d. E[X] E[Z] This is just a simple application of one

Economics 20 Prof. Patricia M. Anderson Problem Set 1 ANSWERS Part I. Multiple Choice Problems 1. If X and Z are two random variables, then E[X-Z] is d. E[X] E[Z] This is just a simple application of one