Kumamoto International Symposium

|

|

|

- Adrian Conley

- 6 years ago

- Views:

Transcription

1

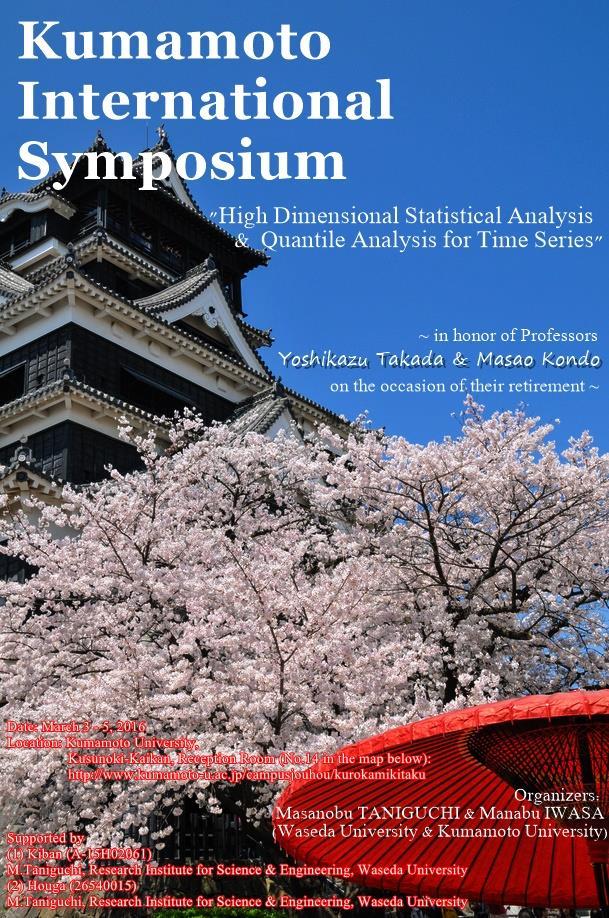

2 Kumamoto International Symposium "High Dimensional Statistical Analysis & Quantile Analysis for Time Series" ~ in honor of Professors Yoshikazu Takada & Masao Kondo on the occasion of their retirement ~ Organizers: Masanobu TANIGUCHI & Manabu IWASA (Waseda University & Kumamoto University) Date: March 3-5, 2016 Location: Kumamoto University, Kusunoki-Kaikan, Reception Room (No.14 in the map below): Supported by (1) Kiban (A-15H02061) M.Taniguchi, Research Institute for Science & Engineering, Waseda University (2) Houga ( ) M.Taniguchi, Research Institute for Science & Engineering, Waseda University

3 Program (* Speaker) March 3 Session (I): 13:25-15:30: chaired by G.D. Lin 13:25-13:30: Masanobu Taniguchi (Waseda Univ.) Opening 13:30-14:00: Fumiya Akashi (Waseda Univ.) Self-weighted empirical likelihood approach for infinite variance processes 14:00-14:30: Xiaoling Dou* (Waseda Univ.), Satoshi Kuriki, Gwo Dong Lin, Donald Richards EM algorithm for estimation of B-spline copula 14:30-15:00: Junichi Hirukawa* (Niigata Univ.), Minehiro Takahashi and Ryota Tanaka On the extension of Lo's modified R/S statistics against to locally stationary short-range dependence 15:00-15:30: Hiroko Kato Solvang (Institute of Marine Research Sundstgt.) and Masanobu Taniguchi Estimation for spectral density of categorical time series data Break: 15:30-15:45 Session (II): 15:45-17:45: chaired by J. Hirukawa 15:45-16:15: Ching Kang Ing (Institute of Statistical Science, Academia Sinica) On high-dimensional cross-validation 16:15-16:45: Richard Davis (Columbia Univ.)

4 Big n, Big p: Eigenvalues for Covariance Matrices of Heavy-Tailed Multivariate Time Series 16:45-17:15: William T.M. Dunsmuir (The Univ. of New South Wales) Topics in Binomial Time Series Regression Analysis 17:15-17:45: Liudas Giraitis* (Queen Mary Univ. of London), G. Kapetanios and Y. Dendramis Estimation of time varying stochastic covariance matrices for large datasets March 4 Session (III): 9:00-11:00: chaired by Solvang Kato 9:00-9:30: Toshinari Kamakura (Chuo Univ.) Properties of LM tests for survival distributions 9:30-10:00: Yan Liu (Waseda Univ.) Robust parameter estimation for irregularly observed stationary process 10:00-10:30: Hiroshi Shiraishi (Keio Univ.) Statistical Estimation for Optimal Dividend Barrier with Insurance Portfolio 10:30-11:00: Shu Hui Yu (National Univ. of Kaohsiung) A VaR estimator under correlated defaults Session (IV): 11:00-12:30: chaired by H. Shiraishi 11:00-11:30: Marc Hallin (Université libre de Bruxelles) R-estimation in semiparametric dynamic location-scale models 11:30-12:00: Gwo Dong Lin* (Institute of Statistical Science, Academia Sinica), Chin-Diew Lai and K. Govindaraju Correlation Structure of the Marshall--Olkin Bivariate Exponential Distribution

5 12:00-12:30: Murad Taqqu (Boston Univ.) A unified approach to self-normalized block sampling Lunch 12:30-13:30: Session (V): 13:30-14:30: chaired by Y. Liu 13:30-14:00: Yoshihiro Yajima (Univ. of Tokyo) On a discrete Fourier transform of irregularly spaced spatial data and its applications 14:00-14:30: Nobuhiro Taneichi (Kagoshima Univ.) Improvement of deviance for binary models Break: 14:30-14:45 Session (VI): 14:45-15:45: chaired by X. Dou 14:45-15:15: Makoto Aoshima (Univ. of Tsukuba) High-dimensional classification in non-sparse settings 15:15-15:45: Satoru Koda, Ryuei Nishii* (Kyushu Univ.), K. Mochida, Y. Onda, T. Sakurai and T. Yoshida (Riken Institute) Sparse modeling of gene networks based on time series of gene expressions Break: 15:45-16:00 Session (VII): 16:00-17:00: chaired by F. Akashi 16:00-16:30: Rinya Takahashi (Kobe Univ.) On von Mises' condition for the domain of attraction of the generalized Pareto distribution 16:30-17:00: Takemi Yanagimoto (Institute of Statistical Mathematics) Three Innovative Techniques for Reducing the Variance of an Estimator: What is

6 the Fourth? 18:30 - Celebration Dinner March 5 Session (VIII): 9:30-10:30: chaired by Shu Hui Yu 9:30-10:00: Hiroto Hyakutake* (National Defense Academy) and Kohei Sawatsuhashi Profile analysis for random effect model with missing data 10:00-10:30: Shinto Eguchi (Institute of Statistical Mathematics) A reconsideration of mathematical statistics Break 10:30-10:45: Session (IV): 10:45-11:45: chaired by H. Hyakutake 10:45-11:15: Shuya Kanagawa* (Tokyo City Univ.) and Saneyuki Ishida Identification of jump times of large jumps for the Nikkei 225 stock index from daily share prices via a stochastic volatility model 11:15-11:45: Yoshihiko Maesono* and Taku Moriyama (Kyushu Univ.) Direct kernel type estimator of a conditional density and its application to regression

7 Abstracts Akashi, F. Self-weighted empirical likelihood approach for infinite variance processes Abstract: This talk applies the empirical likelihood method to the testing problem for a linear hypothesis of infinite variance ARMA models. A self-weighted least absolute deviation-based empirical likelihood ratio (SWLAD-EL) test statistic is constructed, and remarkably, the proposed test statistic is shown to converge to a standard chi-square distribution although we deal with the infinite variance models. We also compare the finite sample performance of the proposed test with that of classical LAD-based test by simulation experiments. It is also reported that the proposed test is applicable to the real data analysis such as variable selection or testing serial correlations. Dou, X. EM algorithm for estimation of B-spline copula Abstract: Baker's distribution is a method proposed to construct multivariate distributions using order statistics with given marginal distributions. This can be considered as the Bernstein copulas. We investigate the properties of Baker's distribution and the Bernstein polynomials, and propose the B-spline copula including the Bernstein copula as a special case. For the estimation of parameters, the EM algorithm designed for the Bernstein copula is applicable with minor changes. A data set is analyzed as an illustrative numerical example. (Joint work with S. Kuriki, G.D. Lin and D. Richards) Hirukawa, J. On the extension of Lo's modified R/S statistics against to locally stationary short-range dependence Abstract: Lo (1991) developed test for long-run memory that is robust to short-range dependence. It was extension of the range over standard deviation

8 or R/S statistic, for which the relevant asymptotic sampling theory was derived via functional central limit theory. In this case, we consider extension of Lo's modified R/S statistics which is aimed to be robust against locally stationary short-range dependence. (Joint work with M. Takahashi and R. Tanaka) Kato, S.H. Estimation for spectral density of categorical time series data Abstract: Stoffer et al. [1993] developed the Spectrum Envelop approach to explore periodical characteristics for categorical time series. It was applied to the study of DNA sequences to find inconsistencies in established gene segments. The Spectrum Envelope is maximized by the optimal scaling for each category to help emphasize any periodic feature in the categorical process. This is recognized as an analogue of mean-variance portfolio. We will discuss about the relationship between them by applying the mean-diversification portfolio approach by Meucci [2009]. (Joint work with M. Taniguchi) Ing, C-K. On high-dimensional cross-validation Abstract: Cross-validation (CV) is one of the most popular methods for model selection. By splitting n data points into a training sample of size n c and a validation sample of size n v in which n v /n 1 and n c, Shao (1993) showed that subset selection based on CV is consistent in a regression model of p candidate variables with p n. However, in the case of p n, the number of candidate variables, is much greater than n, not only does CV's consistency remain undeveloped, but subset selection is also practically infeasible. In this paper, we fill this gap by using CV as a backward elimination tool for eliminating variables that are included by high-dimensional variable screening methods possessing sure screening property. By choosing an n v such that n v /n converges to 1 at a rate faster than the one suggested by Shao (1993), we establish the desired consistency result. We also illustrate the finite-sample performance of the proposed procedure using Monte Carlo simulation.

9 Davis, R. Big n, Big p: Eigenvalues for Cov Matrices of Heavy-Tailed Multivariate Time Series Abstract: In this paper we give an asymptotic theory for the eigenvalues of the sample covariance matrix of a multivariate time series when the number of components p goes to infinity with the sample size. The time series constitutes a linear process across time and between components. The input noise of the linear process has regularly varying tails with index between 0 and 4; in particular, the time series has infinite fourth moment. We derive the limiting behavior for the largest eigenvalues of the sample covariance matrix and show point process convergence of the normalized eigenvalues as n and p go to infinity. The limiting process has an explicit form involving points of a Poisson process and eigenvalues of a non-negative definite matrix. Based on this convergence we derive limit theory for a host of other continuous functionals of the eigenvalues, including the joint convergence of the largest eigenvalues, the joint convergence of the largest eigenvalue and the trace of the sample covariance matrix, and the ratio of the largest eigenvalue to their sum. In addition, we apply the limit theory in the setting of a paper by Lam and Yao (2012, AoS) who suggested a tool for determining a number of relevant eigenvalues in the context of high-dimensional financial time series analysis. (Joint work with Thomas Mikosch, Johann Heiny and Xiaolei Xie) Dunsmuir, W. Topics in Binomial Time Series Regression Analysis Abstract: This review talk presents several connected results about the modelling of binomial valued time series regression. Conditional on a state equation, W t, consisting of a linear regression term, x T t β and a correlated time series U t the observed time series, Y t consists of independent observations on a binomial distribution B(m t, π t ) in which the number of trials m t for the tth observation can vary in time and logit π t = W t. Two specifications for the correlated series U t will be considered. Observation driven U t are generated using past values of the observed responses according

10 to a generalized linear autoregressive moving average recursion. Parameter driven U t use an unobserved (latent) Gaussian autoregressive moving average process to induce serial dependence in the observed series. The talk will review score type tests for detecting both types of serial dependence. For the observation driven models these can be derived based on the simple logistic regression fit but there are questions of non-standard hypothesis testing that can arise for certain specifications of the serial dependence leading to parameters that are not estimable under the null hypothesis of no serial dependence. In these cases we propose the use of the supremum type test. For the parameter driven model, the score test is given in two stages: first, test for existence of a latent process leading to a non-standard score test; and, second, test for serial dependence in the process. The first test relies only on the logistic regression fit. The second test relies on using marginal likelihood based on the generalized linear mixed model fitting procedure. Here some interesting issues about variance estimates on the boundary and non-standard testing procedures also arise particularly in the binary case (where m t =1 for all t) The talk will also explain how the models with serial dependence can be fit to data. Applications of the method to several binary and binomial series will be given to illustrate the methods. Giraitis, L. Estimation of time varying stochastic covariance matrices for large datasets Abstract: In this paper we extend the strand of the literature of estimation of covariance matrix for large dimensional datasets to dependent heterogenious variables. We combine kernel estimation with fixed coefficient estimation methods for large dimensional covariance matrices. Theoretical results allow both stochastic and deterministic structural change and hold under weaker conditions than usually assumed. Monte Carlo analysis illustrates the utility of estimation methods. The paper include brief but illustrative empirical application in the context of forecasting macroeconomic data. (Joint work with G. Kapetanios, Y. Dendramis)

11 Kamakura, T. Properties of LM tests for survival distributions Abstract: Weibull distributions are wildly used in engineering and medical fields. Many researchers are interested in devising methods of testing and estimating parameters for applications to reliability and survival data. In this article we will investigate small sample behaviors of testing and estimating Weibull models based on the likelihood including censored data. The Lagrange multiplier (LM) test is simple and may have good performance according to our experience recently. We will derive several LM tests for Weibull parameters; shape parameter, scale parameter and mean parameter with handling censored data. For comparing performance with other statistics we will conduct simulations studies on nominal and actual significance levels for the LM test, the likelihood ratio test and the Wald test. In case of shape parameter with one the derived LM test is very simple without any likelihood calculations, which include iterations. We find that the LM test tend to assures α-size test in that the true significance levels are smaller than the predefined size of α for any sample size and the true α approaches the nominal α from undersides in accordance with sample size n larger. Liu, Y. Robust parameter estimation for irregularly observed stationary process Abstract: We define a new class of disparities for robust parameter estimation of irregularly observed stationary process. The proposed disparities of spectral densities are derived from the point of view of prediction problem. The proposed disparities are not contained in the class of either location disparities or scale disparities. We investigate asymptotic properties of the minimum contrast estimators based on the new disparities for irregularly observed stationary processes with both finite and infinite variance innovations. The method provides a new way to estimate parameters robust against irregularly observed stationary process with infinite variance innovations. The relative efficiencies under regularly observed cases and the ratio of mean squared error under irregularly observed cases for comparison of different disparities are shown in our simulation studies.

12 Shiraishi, H. Statistical Estimation for Optimal Dividend Barrier with Insurance Portfolio Abstract: We consider a problem where an insurance portfolio is used to provide dividend income for the insurance company s shareholders. This is an important problem in application of risk theory. Whenever the surplus attains the level barrier, the premium income is paid to the shareholders as dividends until the next claim occurs. In this presentation, we consider the classical compound Poisson model as the aggregate claims process, under which the dividends are paid to the shareholders according to a barrier strategy. Optimal dividend barrier is defined as the level of the barrier that maximizes the expectation of the discounted dividends until ruin, which was initially proposed by De Finetti (1957) in the discrete time model and thereafter discussed by Bu hlmann (1970) in the classical risk model with the foundation laid. Although this problem was actively studied around 2000, it is less discussed with the estimation of the unknown barrier. In this presentation, we propose the estimation problem of the optimal dividend barrier, which is critical in application. Yu, S-H. A VaR estimator under correlated defaults Abstract: Correlation between assets is an important issue after the financial crisis and it is also crucial for studying portfolio s performance. Therefore, we consider a portfolio with two assets, and assume that the returns of these assets are distributed as bivariate normal. In order to predict the returns of the assets and to know how they will be influenced by correlation, we establish the correlation between the worst performances of these assets, which is evaluated by order statistics. In addition, we estimate Value-at Risk (VaR) of the portfolio and try to find the optimal portfolio. Several simulations and case studies are executed. We show that choosing optimal portfolio assets by previous results can reduce the losses on the portfolio effectively.

13 Hallin, M. R-estimation in semiparametric dynamic location-scale models Abstract: We propose rank-based estimation (R-estimators) as a substitute for Gaussian quasi-likelihood and standard semiparametric estimation in time series models where conditional location and/or scale depend on a Euclidean parameter of interest, while the unspecified innovation density is an infinite-dimensional nuisance. Applications include linear and nonlinear models, featuring either homo- or heteroskedastic conditional distributions (e.g. conditional duration models, AR-ARCH, discretely observed diffusions with jumps, etc.). We show how to construct R-estimators achieving semiparametric efficiency at some predetermined reference density while preserving root-$n$ consistency and asymptotic normality irrespective of the actual density. Contrary to the standard semiparametric estimators (in the style of Bickel, Klaassen, Ritov, and Wellner), our R-estimators neither require tangent space calculations nor innovation density estimation. Numerical examples illustrate their good performances on simulated data. A real-data analysis of the log-return and log-transformed realized volatility of the USD/CHF exchange rate concludes the talk. (Joint work with D. La Vecchia) Lin, G.D. Correlation Structure of the Marshall--Olkin Bivariate Exponential Distribution Abstract: We first review the basic properties of Marshall--Olkin bivariate exponential distribution (BVE) and then investigate its correlation structure. We provide the correct reasonings for deriving some properties of the Marshall--Olkin BVE and show that the correlation of the BVE is always smaller than that of its copula regardless of the parameters. The latter implies that the BVE does not have Lancaster's phenomenon (any nonlinear transformation of variables decreases the correlation in absolute value). The dependence structure of the BVE is also investigated. (Joint work with C.D. Lai and K. Govindaraju) Taqqu, M.

14 A unified approach to self-normalized block sampling Abstract: The inference procedure for the mean of a stationary time series is usually quite different under various model assumptions because the partial sum process behaves differently depending on whether the time series is short or long-range dependent, or whether it has a light or heavy-tailed marginal distribution. We develop an asymptotic theory for the self-normalized block sampling, and prove that the corresponding block sampling method can provide a unified inference approach for the aforementioned different situations in the sense that it does not require the a priori estimation of auxiliary parameters. (Joint work with Shuyang Bai and Ting Zhang) Yajima, Y. On a discrete Fourier transform of irregularly spaced spatial data and its applications Abstract: Let X = {X t ; t = (t 1,, t d ) R d } be a stationary Gaussian random field with mean zero and autocovariance function Cov(X t, X s ) γ(t s), t, s R d, where R = (, )and d = 1, 2,. We assume that γ(h) is expressed by γ(h) = exp i(h ω)f(ω)dω, where f(ω) is the spectral density function. R d The sampling points, t p (p = 1, n) are i.i.d. random variables located in [ λ n /2, λ n /2 ] d and define the discrete Fourier transform and the raw periodogram by J n (ω) = (2π) d/2 λ n d/2 n 1 n X tp p=1 exp ( it p ω) (Discrete Fourier Transform for Irregularly Spaced Data), I n (ω) = J n (ω) 2 (Raw Periodogram). We derive their asymptotic properties as n and λ n. Next we apply them to testing hypothesis for f(ω). Taneichi, N. Improvement of deviance for binary models Abstract: A logistic regression model, complementary log-log model and probit

15 model are frequently used for a generalised linear model of binary data. We consider deviance as a goodness-of-fit statistic. In this presentation, using the continuous term of asymptotic expansion for the deviance under the null hypothesis that each model is correct, we obtain the Bartlett adjusted deviance statistic for each model that improves the speed of convergence to chi-square limiting distribution of deviance. Performance of each adjusted deviance statistic is also investigated numerically. (Joint work with Y. Sekiya and J. Toyama) Aoshima, M. High-dimensional classification in non-sparse settings Abstract: We consider high-dimensional quadratic classifiers in non-sparse settings. The target of classification rules is not Bayes error rates in the context. The classifier based on the Mahalanobis distance does not always give a preferable performance even if the populations are normal distributions having known covariance matrices. The quadratic classifiers proposed in this paper draw information about heterogeneity effectively through both the differences of expanding mean vectors and covariance matrices. We show that they hold a consistency property in which misclassification rates tend to zero as the dimension goes to infinity under non-sparse settings. We verify that they are asymptotically distributed as a normal distribution under certain conditions. We also propose a quadratic classifier after feature selection by using both the differences of mean vectors and covariance matrices. Finally, we discuss performances of the classifiers in actual data analyses. The proposed classifiers achieve highly accurate classification with very low computational costs. Nishii, R. Sparse modeling of gene networks based on time series of gene expressions Abstract: Our aim here is to implement gene expression data in vitro to growth model. A role of each gene has been elucidated little by little. It is also known that gene expression patterns and those network structure are changing

16 according to growth of plants. Furthermore, the network changes dynamically by the part of the plants. A study proposed here is to identify key genes about the plant growth by sparse modeling for time-series of gene expressions. (Joint work with S. Koda, K. Mochida, Y. Onda, T. Sakurai and T. Yoshida) Takahashi, R. On von Mises' condition for the domain of attraction of the generalized Pareto distribution Abstract: Let F be a continuous distribution function (df) and suppose that F satisfies the von Mises condition. Then, for large enough threshold, the conditional excess df of the df F over threshold is approximated by the generalized Pareto distribution (GPD). For some commonly used distributions, we illustrate how their excess dfs are approximated by the GPDs. Yanagimoto, T. Three Innovative Techniques for Reducing the Variance of an Estimator: What is the Fourth? Abstract: We begin with the innovating contributions by Professor Takada, Kumamoto University. Then this expository talk moves to a review of historical developments of the variance reduction of an estimator. It is our understanding that three notable innovative techniques can be listed as follow: a) Sample mean x, b) Estimator based on the sufficient statistic t, and c) Posterior mean E{μ π(μ x)}. We learn that the contributions on mathematical statistics provided us with the framework of the estimation problem, and enhanced the progress of researches on this subject. The aim of this review is to examine the possible existence of the fourth one. Hyakutake, H. Profile analysis for random effect model with missing data

17 Abstract: For random effects models, the profile analysis in two sample problem is considered with monotone missing. The model considered in this paper has an intraclass correlation structure. Exact testing procedures for parallelism hypothesis are given. Under parallelism, we give approximation to the distribution for constructing a confidence interval of the level difference. The accuracy of approximation is examined by simulation. (Joint work with K. Sawatsuhashi) Key Words: Intraclass correlation, Monotone missing, Parallelism, Profile analysis, Random effects. Eguchi, S. A reconsideration of mathematical statistics Abstract: In mathematical statistics there is a pair of the most important ideas in which one is an exponential family and the other is a log-likelihood function. The ideas of sufficiency, efficient estimation, the most powerful test and so forth developed on the exponential model and the methods of maximum likelihood, likelihood ratio test by the use of the log likelihood function are both necessary tools to understand mathematical statistics. We discuss a possible generalization by replacing from exp and log functions to a strictly increasing convex function and the inverse function. Then we observe that there are many properties similar to standard framework in mathematical statistics; while there are many aspects different from the standard one. Finally we summarize several issues to be solved in the extension of framework of statistics. Kanagawa, S. Identification of jump times of large jumps for the Nikkei 225 stock index from daily share prices via a stochastic volatility model Abstract: We investigate daily share prices of the Nikkei 225 stock index to identify jump times of the stock index using a jump-diffusion model which consists of the Black-Scholes model with a stochastic volatility and a compound Poisson process. Since the data of daily share prices of the Nikkei 225 stock index are observed at discrete times, it is difficult to find real jump-times from the

18 data. In this talk we consider how to separate jump-times from the observed times. The volatility of the stock index is estimated by the historical volatility from the observation of some daily share prices. We also refer to the number of daily share prices for the historical volatility and show that the number is essential for the accuracy of the identification of jump times. (Joint work with S. Ishida) Maesono, Y. Direct kernel type estimator of a conditional density and its application to regression Abstract: In this talk, we propose a new direct kernel type estimator of a conditional density function. Cwik and Mielniczuk (1989) have proposed a direct kernel type estimator of a density ratio. Extending their idea, we propose the kernel type estimator of the conditional density function. A new direct estimator of a regression function is also proposed, which is a competitor of the Nadaraya-Watson estimator. We will discuss mean squared errors of the ordinary and proposed estimators. (Joint work with T. Moriyama)

Waseda International Symposium on Stable Process, Semimartingale, Finance & Pension Mathematics

! Waseda International Symposium on Stable Process, Semimartingale, Finance & Pension Mathematics Organizers: Masanobu Taniguchi (Waseda Univ.), Dou Xiaoling (ISM) and Kenta Hamada (Waseda Univ.) Waseda

! Waseda International Symposium on Stable Process, Semimartingale, Finance & Pension Mathematics Organizers: Masanobu Taniguchi (Waseda Univ.), Dou Xiaoling (ISM) and Kenta Hamada (Waseda Univ.) Waseda

Hakone Seminar Recent Developments in Statistics

Hakone Seminar Recent Developments in Statistics November 12-14, 2015 Hotel Green Plaza Hakone: http://www.hgp.co.jp/language/english/sp/ Organizer: Masanobu TANIGUCHI (Research Institute for Science &

Hakone Seminar Recent Developments in Statistics November 12-14, 2015 Hotel Green Plaza Hakone: http://www.hgp.co.jp/language/english/sp/ Organizer: Masanobu TANIGUCHI (Research Institute for Science &

Kyoto (Fushimi-Uji) International Seminar

International Seminar") Kyoto (Fushimi-Uji) International Seminar "Recent Developments for Statistical Science" Date: October 26-28, 2017. Venue: Kyoto Terrsa (http://www.kyoto-terrsa.or.jp/floor_map/en.php) Organizer: Masanobu

Kyoto (Fushimi-Uji) International Seminar "Recent Developments for Statistical Science" Date: October 26-28, 2017. Venue: Kyoto Terrsa (http://www.kyoto-terrsa.or.jp/floor_map/en.php) Organizer: Masanobu

INTERNATIONAL SYMPOSIUM

WASEDA INTERNATIONAL SYMPOSIUM - High Dimensional Statistical Analysis for Time Spatial Processes & Quantile Analysis for Time Series - Organized by Masanobu Taniguchi (Research Institute for Science &

WASEDA INTERNATIONAL SYMPOSIUM - High Dimensional Statistical Analysis for Time Spatial Processes & Quantile Analysis for Time Series - Organized by Masanobu Taniguchi (Research Institute for Science &

Supported by. (1) Kiban (A-15H02061) (2) Houga ( ) M. Taniguchi, Research Institute for Science & Engineering, Waseda University

Kiban (A-15H02061) (2) Houga ( ) M. Taniguchi, Research Institute for Science & Engineering, Waseda University") Supported by (1) Kiban (A-15H02061) M. Taniguchi, Research Institute for Science & Engineering, Waseda University (2) Houga (26540015) M. Taniguchi, Research Institute for Science & Engineering, Waseda

Supported by (1) Kiban (A-15H02061) M. Taniguchi, Research Institute for Science & Engineering, Waseda University (2) Houga (26540015) M. Taniguchi, Research Institute for Science & Engineering, Waseda

Stat 5101 Lecture Notes

Stat 5101 Lecture Notes Charles J. Geyer Copyright 1998, 1999, 2000, 2001 by Charles J. Geyer May 7, 2001 ii Stat 5101 (Geyer) Course Notes Contents 1 Random Variables and Change of Variables 1 1.1 Random

Stat 5101 Lecture Notes Charles J. Geyer Copyright 1998, 1999, 2000, 2001 by Charles J. Geyer May 7, 2001 ii Stat 5101 (Geyer) Course Notes Contents 1 Random Variables and Change of Variables 1 1.1 Random

Waseda International Symposium

Waseda International Symposium "High Dimensional Statistical Analysis for Time Spatial Processes & Quantile Analysis for Time Series" Date: February 27 - March 1, 2017. Venue: Waseda University, Nishi-Waseda

Waseda International Symposium "High Dimensional Statistical Analysis for Time Spatial Processes & Quantile Analysis for Time Series" Date: February 27 - March 1, 2017. Venue: Waseda University, Nishi-Waseda

TIME SERIES ANALYSIS. Forecasting and Control. Wiley. Fifth Edition GWILYM M. JENKINS GEORGE E. P. BOX GREGORY C. REINSEL GRETA M.

TIME SERIES ANALYSIS Forecasting and Control Fifth Edition GEORGE E. P. BOX GWILYM M. JENKINS GREGORY C. REINSEL GRETA M. LJUNG Wiley CONTENTS PREFACE TO THE FIFTH EDITION PREFACE TO THE FOURTH EDITION

TIME SERIES ANALYSIS Forecasting and Control Fifth Edition GEORGE E. P. BOX GWILYM M. JENKINS GREGORY C. REINSEL GRETA M. LJUNG Wiley CONTENTS PREFACE TO THE FIFTH EDITION PREFACE TO THE FOURTH EDITION

A Guide to Modern Econometric:

A Guide to Modern Econometric: 4th edition Marno Verbeek Rotterdam School of Management, Erasmus University, Rotterdam B 379887 )WILEY A John Wiley & Sons, Ltd., Publication Contents Preface xiii 1 Introduction

A Guide to Modern Econometric: 4th edition Marno Verbeek Rotterdam School of Management, Erasmus University, Rotterdam B 379887 )WILEY A John Wiley & Sons, Ltd., Publication Contents Preface xiii 1 Introduction

Introduction to Econometrics

Introduction to Econometrics T H I R D E D I T I O N Global Edition James H. Stock Harvard University Mark W. Watson Princeton University Boston Columbus Indianapolis New York San Francisco Upper Saddle

Introduction to Econometrics T H I R D E D I T I O N Global Edition James H. Stock Harvard University Mark W. Watson Princeton University Boston Columbus Indianapolis New York San Francisco Upper Saddle

Waseda Cherry Blossom Workshop

Waseda Cherry Blossom Workshop Time Series Factor Models & Causality Venue: Waseda University, Nishi-Waseda Campus Building 63-1 Meeting Room (Access map: http://www.sci.waseda.ac.jp/eng/access) Date:

Waseda Cherry Blossom Workshop Time Series Factor Models & Causality Venue: Waseda University, Nishi-Waseda Campus Building 63-1 Meeting Room (Access map: http://www.sci.waseda.ac.jp/eng/access) Date:

Econometric Analysis of Cross Section and Panel Data

Econometric Analysis of Cross Section and Panel Data Jeffrey M. Wooldridge / The MIT Press Cambridge, Massachusetts London, England Contents Preface Acknowledgments xvii xxiii I INTRODUCTION AND BACKGROUND

Econometric Analysis of Cross Section and Panel Data Jeffrey M. Wooldridge / The MIT Press Cambridge, Massachusetts London, England Contents Preface Acknowledgments xvii xxiii I INTRODUCTION AND BACKGROUND

Extremogram and ex-periodogram for heavy-tailed time series

Extremogram and ex-periodogram for heavy-tailed time series 1 Thomas Mikosch University of Copenhagen Joint work with Richard A. Davis (Columbia) and Yuwei Zhao (Ulm) 1 Zagreb, June 6, 2014 1 2 Extremal

Extremogram and ex-periodogram for heavy-tailed time series 1 Thomas Mikosch University of Copenhagen Joint work with Richard A. Davis (Columbia) and Yuwei Zhao (Ulm) 1 Zagreb, June 6, 2014 1 2 Extremal

Multilevel Statistical Models: 3 rd edition, 2003 Contents

Multilevel Statistical Models: 3 rd edition, 2003 Contents Preface Acknowledgements Notation Two and three level models. A general classification notation and diagram Glossary Chapter 1 An introduction

Multilevel Statistical Models: 3 rd edition, 2003 Contents Preface Acknowledgements Notation Two and three level models. A general classification notation and diagram Glossary Chapter 1 An introduction

Time Series: Theory and Methods

Peter J. Brockwell Richard A. Davis Time Series: Theory and Methods Second Edition With 124 Illustrations Springer Contents Preface to the Second Edition Preface to the First Edition vn ix CHAPTER 1 Stationary

Peter J. Brockwell Richard A. Davis Time Series: Theory and Methods Second Edition With 124 Illustrations Springer Contents Preface to the Second Edition Preface to the First Edition vn ix CHAPTER 1 Stationary

Extremogram and Ex-Periodogram for heavy-tailed time series

Extremogram and Ex-Periodogram for heavy-tailed time series 1 Thomas Mikosch University of Copenhagen Joint work with Richard A. Davis (Columbia) and Yuwei Zhao (Ulm) 1 Jussieu, April 9, 2014 1 2 Extremal

Extremogram and Ex-Periodogram for heavy-tailed time series 1 Thomas Mikosch University of Copenhagen Joint work with Richard A. Davis (Columbia) and Yuwei Zhao (Ulm) 1 Jussieu, April 9, 2014 1 2 Extremal

G. S. Maddala Kajal Lahiri. WILEY A John Wiley and Sons, Ltd., Publication

G. S. Maddala Kajal Lahiri WILEY A John Wiley and Sons, Ltd., Publication TEMT Foreword Preface to the Fourth Edition xvii xix Part I Introduction and the Linear Regression Model 1 CHAPTER 1 What is Econometrics?

G. S. Maddala Kajal Lahiri WILEY A John Wiley and Sons, Ltd., Publication TEMT Foreword Preface to the Fourth Edition xvii xix Part I Introduction and the Linear Regression Model 1 CHAPTER 1 What is Econometrics?

Volatility. Gerald P. Dwyer. February Clemson University

Volatility Gerald P. Dwyer Clemson University February 2016 Outline 1 Volatility Characteristics of Time Series Heteroskedasticity Simpler Estimation Strategies Exponentially Weighted Moving Average Use

Volatility Gerald P. Dwyer Clemson University February 2016 Outline 1 Volatility Characteristics of Time Series Heteroskedasticity Simpler Estimation Strategies Exponentially Weighted Moving Average Use

Discussion of Bootstrap prediction intervals for linear, nonlinear, and nonparametric autoregressions, by Li Pan and Dimitris Politis

Discussion of Bootstrap prediction intervals for linear, nonlinear, and nonparametric autoregressions, by Li Pan and Dimitris Politis Sílvia Gonçalves and Benoit Perron Département de sciences économiques,

Discussion of Bootstrap prediction intervals for linear, nonlinear, and nonparametric autoregressions, by Li Pan and Dimitris Politis Sílvia Gonçalves and Benoit Perron Département de sciences économiques,

Time Series Analysis. James D. Hamilton PRINCETON UNIVERSITY PRESS PRINCETON, NEW JERSEY

Time Series Analysis James D. Hamilton PRINCETON UNIVERSITY PRESS PRINCETON, NEW JERSEY & Contents PREFACE xiii 1 1.1. 1.2. Difference Equations First-Order Difference Equations 1 /?th-order Difference

Time Series Analysis James D. Hamilton PRINCETON UNIVERSITY PRESS PRINCETON, NEW JERSEY & Contents PREFACE xiii 1 1.1. 1.2. Difference Equations First-Order Difference Equations 1 /?th-order Difference

When is a copula constant? A test for changing relationships

When is a copula constant? A test for changing relationships Fabio Busetti and Andrew Harvey Bank of Italy and University of Cambridge November 2007 usetti and Harvey (Bank of Italy and University of Cambridge)

When is a copula constant? A test for changing relationships Fabio Busetti and Andrew Harvey Bank of Italy and University of Cambridge November 2007 usetti and Harvey (Bank of Italy and University of Cambridge)

Nonparametric Bayesian Methods (Gaussian Processes)

") [70240413 Statistical Machine Learning, Spring, 2015] Nonparametric Bayesian Methods (Gaussian Processes) Jun Zhu dcszj@mail.tsinghua.edu.cn http://bigml.cs.tsinghua.edu.cn/~jun State Key Lab of Intelligent

[70240413 Statistical Machine Learning, Spring, 2015] Nonparametric Bayesian Methods (Gaussian Processes) Jun Zhu dcszj@mail.tsinghua.edu.cn http://bigml.cs.tsinghua.edu.cn/~jun State Key Lab of Intelligent

ECONOMICS 7200 MODERN TIME SERIES ANALYSIS Econometric Theory and Applications

ECONOMICS 7200 MODERN TIME SERIES ANALYSIS Econometric Theory and Applications Yongmiao Hong Department of Economics & Department of Statistical Sciences Cornell University Spring 2019 Time and uncertainty

ECONOMICS 7200 MODERN TIME SERIES ANALYSIS Econometric Theory and Applications Yongmiao Hong Department of Economics & Department of Statistical Sciences Cornell University Spring 2019 Time and uncertainty

Introduction to the Mathematical and Statistical Foundations of Econometrics Herman J. Bierens Pennsylvania State University

Introduction to the Mathematical and Statistical Foundations of Econometrics 1 Herman J. Bierens Pennsylvania State University November 13, 2003 Revised: March 15, 2004 2 Contents Preface Chapter 1: Probability

Introduction to the Mathematical and Statistical Foundations of Econometrics 1 Herman J. Bierens Pennsylvania State University November 13, 2003 Revised: March 15, 2004 2 Contents Preface Chapter 1: Probability

Thomas J. Fisher. Research Statement. Preliminary Results

Thomas J. Fisher Research Statement Preliminary Results Many applications of modern statistics involve a large number of measurements and can be considered in a linear algebra framework. In many of these

Thomas J. Fisher Research Statement Preliminary Results Many applications of modern statistics involve a large number of measurements and can be considered in a linear algebra framework. In many of these

Research Article Optimal Portfolio Estimation for Dependent Financial Returns with Generalized Empirical Likelihood

Advances in Decision Sciences Volume 2012, Article ID 973173, 8 pages doi:10.1155/2012/973173 Research Article Optimal Portfolio Estimation for Dependent Financial Returns with Generalized Empirical Likelihood

Advances in Decision Sciences Volume 2012, Article ID 973173, 8 pages doi:10.1155/2012/973173 Research Article Optimal Portfolio Estimation for Dependent Financial Returns with Generalized Empirical Likelihood

Keio International Symposium

Keio International Symposium "Statistical Analysis for High-Dimensional, Circular or Time Series Data" Date: March 2 and 3, 2017. (March 4: Free Discussion) Venue: Keio University, Hiyoshi Campus, Raiosha,

Keio International Symposium "Statistical Analysis for High-Dimensional, Circular or Time Series Data" Date: March 2 and 3, 2017. (March 4: Free Discussion) Venue: Keio University, Hiyoshi Campus, Raiosha,

Subject CS1 Actuarial Statistics 1 Core Principles

Institute of Actuaries of India Subject CS1 Actuarial Statistics 1 Core Principles For 2019 Examinations Aim The aim of the Actuarial Statistics 1 subject is to provide a grounding in mathematical and

Institute of Actuaries of India Subject CS1 Actuarial Statistics 1 Core Principles For 2019 Examinations Aim The aim of the Actuarial Statistics 1 subject is to provide a grounding in mathematical and

Kouchi International Seminar Recent Developments of Quantile Method, Causality and High Dim Statistics

Kouchi International Seminar Recent Developments of Quantile Method, Causality and High Dim Statistics Date: March 3-5, 2018 Venue: Tosa Royal Hotel Organizer: Masanobu TANIGUCHI Supported by (1) Kiban

Kouchi International Seminar Recent Developments of Quantile Method, Causality and High Dim Statistics Date: March 3-5, 2018 Venue: Tosa Royal Hotel Organizer: Masanobu TANIGUCHI Supported by (1) Kiban

Inference in VARs with Conditional Heteroskedasticity of Unknown Form

Inference in VARs with Conditional Heteroskedasticity of Unknown Form Ralf Brüggemann a Carsten Jentsch b Carsten Trenkler c University of Konstanz University of Mannheim University of Mannheim IAB Nuremberg

Inference in VARs with Conditional Heteroskedasticity of Unknown Form Ralf Brüggemann a Carsten Jentsch b Carsten Trenkler c University of Konstanz University of Mannheim University of Mannheim IAB Nuremberg

The Slow Convergence of OLS Estimators of α, β and Portfolio. β and Portfolio Weights under Long Memory Stochastic Volatility

The Slow Convergence of OLS Estimators of α, β and Portfolio Weights under Long Memory Stochastic Volatility New York University Stern School of Business June 21, 2018 Introduction Bivariate long memory

The Slow Convergence of OLS Estimators of α, β and Portfolio Weights under Long Memory Stochastic Volatility New York University Stern School of Business June 21, 2018 Introduction Bivariate long memory

Contents. Part I: Fundamentals of Bayesian Inference 1

Contents Preface xiii Part I: Fundamentals of Bayesian Inference 1 1 Probability and inference 3 1.1 The three steps of Bayesian data analysis 3 1.2 General notation for statistical inference 4 1.3 Bayesian

Contents Preface xiii Part I: Fundamentals of Bayesian Inference 1 1 Probability and inference 3 1.1 The three steps of Bayesian data analysis 3 1.2 General notation for statistical inference 4 1.3 Bayesian

Generalized Linear Models

York SPIDA John Fox Notes Generalized Linear Models Copyright 2010 by John Fox Generalized Linear Models 1 1. Topics I The structure of generalized linear models I Poisson and other generalized linear

York SPIDA John Fox Notes Generalized Linear Models Copyright 2010 by John Fox Generalized Linear Models 1 1. Topics I The structure of generalized linear models I Poisson and other generalized linear

Diagnostic Test for GARCH Models Based on Absolute Residual Autocorrelations

Diagnostic Test for GARCH Models Based on Absolute Residual Autocorrelations Farhat Iqbal Department of Statistics, University of Balochistan Quetta-Pakistan farhatiqb@gmail.com Abstract In this paper

Diagnostic Test for GARCH Models Based on Absolute Residual Autocorrelations Farhat Iqbal Department of Statistics, University of Balochistan Quetta-Pakistan farhatiqb@gmail.com Abstract In this paper

covariance function, 174 probability structure of; Yule-Walker equations, 174 Moving average process, fluctuations, 5-6, 175 probability structure of

Index* The Statistical Analysis of Time Series by T. W. Anderson Copyright 1971 John Wiley & Sons, Inc. Aliasing, 387-388 Autoregressive {continued) Amplitude, 4, 94 case of first-order, 174 Associated

Index* The Statistical Analysis of Time Series by T. W. Anderson Copyright 1971 John Wiley & Sons, Inc. Aliasing, 387-388 Autoregressive {continued) Amplitude, 4, 94 case of first-order, 174 Associated

Econ 423 Lecture Notes: Additional Topics in Time Series 1

Econ 423 Lecture Notes: Additional Topics in Time Series 1 John C. Chao April 25, 2017 1 These notes are based in large part on Chapter 16 of Stock and Watson (2011). They are for instructional purposes

Econ 423 Lecture Notes: Additional Topics in Time Series 1 John C. Chao April 25, 2017 1 These notes are based in large part on Chapter 16 of Stock and Watson (2011). They are for instructional purposes

6. The econometrics of Financial Markets: Empirical Analysis of Financial Time Series. MA6622, Ernesto Mordecki, CityU, HK, 2006.

6. The econometrics of Financial Markets: Empirical Analysis of Financial Time Series MA6622, Ernesto Mordecki, CityU, HK, 2006. References for Lecture 5: Quantitative Risk Management. A. McNeil, R. Frey,

6. The econometrics of Financial Markets: Empirical Analysis of Financial Time Series MA6622, Ernesto Mordecki, CityU, HK, 2006. References for Lecture 5: Quantitative Risk Management. A. McNeil, R. Frey,

Pattern Recognition and Machine Learning

Christopher M. Bishop Pattern Recognition and Machine Learning ÖSpri inger Contents Preface Mathematical notation Contents vii xi xiii 1 Introduction 1 1.1 Example: Polynomial Curve Fitting 4 1.2 Probability

Christopher M. Bishop Pattern Recognition and Machine Learning ÖSpri inger Contents Preface Mathematical notation Contents vii xi xiii 1 Introduction 1 1.1 Example: Polynomial Curve Fitting 4 1.2 Probability

INSTITUTE AND FACULTY OF ACTUARIES. Curriculum 2019 SPECIMEN SOLUTIONS

INSTITUTE AND FACULTY OF ACTUARIES Curriculum 09 SPECIMEN SOLUTIONS Subject CSA Risk Modelling and Survival Analysis Institute and Faculty of Actuaries Sample path A continuous time, discrete state process

INSTITUTE AND FACULTY OF ACTUARIES Curriculum 09 SPECIMEN SOLUTIONS Subject CSA Risk Modelling and Survival Analysis Institute and Faculty of Actuaries Sample path A continuous time, discrete state process

Issues using Logistic Regression for Highly Imbalanced data

Issues using Logistic Regression for Highly Imbalanced data Yazhe Li, Niall Adams, Tony Bellotti Imperial College London yli16@imperialacuk Credit Scoring and Credit Control conference, Aug 2017 Yazhe

Issues using Logistic Regression for Highly Imbalanced data Yazhe Li, Niall Adams, Tony Bellotti Imperial College London yli16@imperialacuk Credit Scoring and Credit Control conference, Aug 2017 Yazhe

STA414/2104 Statistical Methods for Machine Learning II

STA414/2104 Statistical Methods for Machine Learning II Murat A. Erdogdu & David Duvenaud Department of Computer Science Department of Statistical Sciences Lecture 3 Slide credits: Russ Salakhutdinov Announcements

STA414/2104 Statistical Methods for Machine Learning II Murat A. Erdogdu & David Duvenaud Department of Computer Science Department of Statistical Sciences Lecture 3 Slide credits: Russ Salakhutdinov Announcements

Time Series Analysis. James D. Hamilton PRINCETON UNIVERSITY PRESS PRINCETON, NEW JERSEY

Time Series Analysis James D. Hamilton PRINCETON UNIVERSITY PRESS PRINCETON, NEW JERSEY PREFACE xiii 1 Difference Equations 1.1. First-Order Difference Equations 1 1.2. pth-order Difference Equations 7

Time Series Analysis James D. Hamilton PRINCETON UNIVERSITY PRESS PRINCETON, NEW JERSEY PREFACE xiii 1 Difference Equations 1.1. First-Order Difference Equations 1 1.2. pth-order Difference Equations 7

Econ 424 Time Series Concepts

Econ 424 Time Series Concepts Eric Zivot January 20 2015 Time Series Processes Stochastic (Random) Process { 1 2 +1 } = { } = sequence of random variables indexed by time Observed time series of length

Econ 424 Time Series Concepts Eric Zivot January 20 2015 Time Series Processes Stochastic (Random) Process { 1 2 +1 } = { } = sequence of random variables indexed by time Observed time series of length

388 Index Differencing test ,232 Distributed lags , 147 arithmetic lag.

INDEX Aggregation... 104 Almon lag... 135-140,149 AR(1) process... 114-130,240,246,324-325,366,370,374 ARCH... 376-379 ARlMA... 365 Asymptotically unbiased... 13,50 Autocorrelation... 113-130, 142-150,324-325,365-369

INDEX Aggregation... 104 Almon lag... 135-140,149 AR(1) process... 114-130,240,246,324-325,366,370,374 ARCH... 376-379 ARlMA... 365 Asymptotically unbiased... 13,50 Autocorrelation... 113-130, 142-150,324-325,365-369

Research Statement. Zhongwen Liang

Research Statement Zhongwen Liang My research is concentrated on theoretical and empirical econometrics, with the focus of developing statistical methods and tools to do the quantitative analysis of empirical

Research Statement Zhongwen Liang My research is concentrated on theoretical and empirical econometrics, with the focus of developing statistical methods and tools to do the quantitative analysis of empirical

The exam is closed book, closed notes except your one-page (two sides) or two-page (one side) crib sheet.

or two-page (one side) crib sheet.") CS 189 Spring 013 Introduction to Machine Learning Final You have 3 hours for the exam. The exam is closed book, closed notes except your one-page (two sides) or two-page (one side) crib sheet. Please

CS 189 Spring 013 Introduction to Machine Learning Final You have 3 hours for the exam. The exam is closed book, closed notes except your one-page (two sides) or two-page (one side) crib sheet. Please

Extreme Value Analysis and Spatial Extremes

Extreme Value Analysis and Department of Statistics Purdue University 11/07/2013 Outline Motivation 1 Motivation 2 Extreme Value Theorem and 3 Bayesian Hierarchical Models Copula Models Max-stable Models

Extreme Value Analysis and Department of Statistics Purdue University 11/07/2013 Outline Motivation 1 Motivation 2 Extreme Value Theorem and 3 Bayesian Hierarchical Models Copula Models Max-stable Models

A Non-Parametric Approach of Heteroskedasticity Robust Estimation of Vector-Autoregressive (VAR) Models

Models") Journal of Finance and Investment Analysis, vol.1, no.1, 2012, 55-67 ISSN: 2241-0988 (print version), 2241-0996 (online) International Scientific Press, 2012 A Non-Parametric Approach of Heteroskedasticity

Journal of Finance and Investment Analysis, vol.1, no.1, 2012, 55-67 ISSN: 2241-0988 (print version), 2241-0996 (online) International Scientific Press, 2012 A Non-Parametric Approach of Heteroskedasticity

Empirical properties of large covariance matrices in finance

Empirical properties of large covariance matrices in finance Ex: RiskMetrics Group, Geneva Since 2010: Swissquote, Gland December 2009 Covariance and large random matrices Many problems in finance require

Empirical properties of large covariance matrices in finance Ex: RiskMetrics Group, Geneva Since 2010: Swissquote, Gland December 2009 Covariance and large random matrices Many problems in finance require

Gaussian processes. Basic Properties VAG002-

Gaussian processes The class of Gaussian processes is one of the most widely used families of stochastic processes for modeling dependent data observed over time, or space, or time and space. The popularity

Gaussian processes The class of Gaussian processes is one of the most widely used families of stochastic processes for modeling dependent data observed over time, or space, or time and space. The popularity

Introduction to Algorithmic Trading Strategies Lecture 10

Introduction to Algorithmic Trading Strategies Lecture 10 Risk Management Haksun Li haksun.li@numericalmethod.com www.numericalmethod.com Outline Value at Risk (VaR) Extreme Value Theory (EVT) References

Introduction to Algorithmic Trading Strategies Lecture 10 Risk Management Haksun Li haksun.li@numericalmethod.com www.numericalmethod.com Outline Value at Risk (VaR) Extreme Value Theory (EVT) References

Statistical Inference and Methods

Department of Mathematics Imperial College London d.stephens@imperial.ac.uk http://stats.ma.ic.ac.uk/ das01/ 31st January 2006 Part VI Session 6: Filtering and Time to Event Data Session 6: Filtering and

Department of Mathematics Imperial College London d.stephens@imperial.ac.uk http://stats.ma.ic.ac.uk/ das01/ 31st January 2006 Part VI Session 6: Filtering and Time to Event Data Session 6: Filtering and

Linear Models for Regression CS534

Linear Models for Regression CS534 Example Regression Problems Predict housing price based on House size, lot size, Location, # of rooms Predict stock price based on Price history of the past month Predict

Linear Models for Regression CS534 Example Regression Problems Predict housing price based on House size, lot size, Location, # of rooms Predict stock price based on Price history of the past month Predict

PATTERN RECOGNITION AND MACHINE LEARNING CHAPTER 2: PROBABILITY DISTRIBUTIONS

PATTERN RECOGNITION AND MACHINE LEARNING CHAPTER 2: PROBABILITY DISTRIBUTIONS Parametric Distributions Basic building blocks: Need to determine given Representation: or? Recall Curve Fitting Binary Variables

PATTERN RECOGNITION AND MACHINE LEARNING CHAPTER 2: PROBABILITY DISTRIBUTIONS Parametric Distributions Basic building blocks: Need to determine given Representation: or? Recall Curve Fitting Binary Variables

Research Projects. Hanxiang Peng. March 4, Department of Mathematical Sciences Indiana University-Purdue University at Indianapolis

Hanxiang Department of Mathematical Sciences Indiana University-Purdue University at Indianapolis March 4, 2009 Outline Project I: Free Knot Spline Cox Model Project I: Free Knot Spline Cox Model Consider

Hanxiang Department of Mathematical Sciences Indiana University-Purdue University at Indianapolis March 4, 2009 Outline Project I: Free Knot Spline Cox Model Project I: Free Knot Spline Cox Model Consider

Probability for Statistics and Machine Learning

~Springer Anirban DasGupta Probability for Statistics and Machine Learning Fundamentals and Advanced Topics Contents Suggested Courses with Diffe~ent Themes........................... xix 1 Review of Univariate

~Springer Anirban DasGupta Probability for Statistics and Machine Learning Fundamentals and Advanced Topics Contents Suggested Courses with Diffe~ent Themes........................... xix 1 Review of Univariate

Stochastic Processes

Stochastic Processes Stochastic Process Non Formal Definition: Non formal: A stochastic process (random process) is the opposite of a deterministic process such as one defined by a differential equation.

Stochastic Processes Stochastic Process Non Formal Definition: Non formal: A stochastic process (random process) is the opposite of a deterministic process such as one defined by a differential equation.

Generalized Autoregressive Score Models

Generalized Autoregressive Score Models by: Drew Creal, Siem Jan Koopman, André Lucas To capture the dynamic behavior of univariate and multivariate time series processes, we can allow parameters to be

Generalized Autoregressive Score Models by: Drew Creal, Siem Jan Koopman, André Lucas To capture the dynamic behavior of univariate and multivariate time series processes, we can allow parameters to be

Testing Statistical Hypotheses

E.L. Lehmann Joseph P. Romano Testing Statistical Hypotheses Third Edition 4y Springer Preface vii I Small-Sample Theory 1 1 The General Decision Problem 3 1.1 Statistical Inference and Statistical Decisions

E.L. Lehmann Joseph P. Romano Testing Statistical Hypotheses Third Edition 4y Springer Preface vii I Small-Sample Theory 1 1 The General Decision Problem 3 1.1 Statistical Inference and Statistical Decisions

Linear Models for Regression CS534

Linear Models for Regression CS534 Example Regression Problems Predict housing price based on House size, lot size, Location, # of rooms Predict stock price based on Price history of the past month Predict

Linear Models for Regression CS534 Example Regression Problems Predict housing price based on House size, lot size, Location, # of rooms Predict stock price based on Price history of the past month Predict

HANDBOOK OF APPLICABLE MATHEMATICS

HANDBOOK OF APPLICABLE MATHEMATICS Chief Editor: Walter Ledermann Volume VI: Statistics PART A Edited by Emlyn Lloyd University of Lancaster A Wiley-Interscience Publication JOHN WILEY & SONS Chichester

HANDBOOK OF APPLICABLE MATHEMATICS Chief Editor: Walter Ledermann Volume VI: Statistics PART A Edited by Emlyn Lloyd University of Lancaster A Wiley-Interscience Publication JOHN WILEY & SONS Chichester

Assessing the dependence of high-dimensional time series via sample autocovariances and correlations

Assessing the dependence of high-dimensional time series via sample autocovariances and correlations Johannes Heiny University of Aarhus Joint work with Thomas Mikosch (Copenhagen), Richard Davis (Columbia),

Assessing the dependence of high-dimensional time series via sample autocovariances and correlations Johannes Heiny University of Aarhus Joint work with Thomas Mikosch (Copenhagen), Richard Davis (Columbia),

If we want to analyze experimental or simulated data we might encounter the following tasks:

Chapter 1 Introduction If we want to analyze experimental or simulated data we might encounter the following tasks: Characterization of the source of the signal and diagnosis Studying dependencies Prediction

Chapter 1 Introduction If we want to analyze experimental or simulated data we might encounter the following tasks: Characterization of the source of the signal and diagnosis Studying dependencies Prediction

New Introduction to Multiple Time Series Analysis

Helmut Lütkepohl New Introduction to Multiple Time Series Analysis With 49 Figures and 36 Tables Springer Contents 1 Introduction 1 1.1 Objectives of Analyzing Multiple Time Series 1 1.2 Some Basics 2

Helmut Lütkepohl New Introduction to Multiple Time Series Analysis With 49 Figures and 36 Tables Springer Contents 1 Introduction 1 1.1 Objectives of Analyzing Multiple Time Series 1 1.2 Some Basics 2

Introduction to Regression Analysis. Dr. Devlina Chatterjee 11 th August, 2017

Introduction to Regression Analysis Dr. Devlina Chatterjee 11 th August, 2017 What is regression analysis? Regression analysis is a statistical technique for studying linear relationships. One dependent

Introduction to Regression Analysis Dr. Devlina Chatterjee 11 th August, 2017 What is regression analysis? Regression analysis is a statistical technique for studying linear relationships. One dependent

Fundamentals of Applied Probability and Random Processes

Fundamentals of Applied Probability and Random Processes,nd 2 na Edition Oliver C. Ibe University of Massachusetts, LoweLL, Massachusetts ip^ W >!^ AMSTERDAM BOSTON HEIDELBERG LONDON NEW YORK OXFORD PARIS

Fundamentals of Applied Probability and Random Processes,nd 2 na Edition Oliver C. Ibe University of Massachusetts, LoweLL, Massachusetts ip^ W >!^ AMSTERDAM BOSTON HEIDELBERG LONDON NEW YORK OXFORD PARIS

Model Selection and Geometry

Model Selection and Geometry Pascal Massart Université Paris-Sud, Orsay Leipzig, February Purpose of the talk! Concentration of measure plays a fundamental role in the theory of model selection! Model

Model Selection and Geometry Pascal Massart Université Paris-Sud, Orsay Leipzig, February Purpose of the talk! Concentration of measure plays a fundamental role in the theory of model selection! Model

Multivariate GARCH models.

Multivariate GARCH models. Financial market volatility moves together over time across assets and markets. Recognizing this commonality through a multivariate modeling framework leads to obvious gains

Multivariate GARCH models. Financial market volatility moves together over time across assets and markets. Recognizing this commonality through a multivariate modeling framework leads to obvious gains

Additive Isotonic Regression

Additive Isotonic Regression Enno Mammen and Kyusang Yu 11. July 2006 INTRODUCTION: We have i.i.d. random vectors (Y 1, X 1 ),..., (Y n, X n ) with X i = (X1 i,..., X d i ) and we consider the additive

Additive Isotonic Regression Enno Mammen and Kyusang Yu 11. July 2006 INTRODUCTION: We have i.i.d. random vectors (Y 1, X 1 ),..., (Y n, X n ) with X i = (X1 i,..., X d i ) and we consider the additive

New Developments in Econometrics and Time Series

New Developments in Econometrics and Time Series September 10-11, 2012 Einaudi Institute for Economics and Finance (EIEF), Rome Organization: Holger Dette (Ruhr-Universität Bochum), Marc Hallin (ECARES,

New Developments in Econometrics and Time Series September 10-11, 2012 Einaudi Institute for Economics and Finance (EIEF), Rome Organization: Holger Dette (Ruhr-Universität Bochum), Marc Hallin (ECARES,

1. Fundamental concepts

. Fundamental concepts A time series is a sequence of data points, measured typically at successive times spaced at uniform intervals. Time series are used in such fields as statistics, signal processing

. Fundamental concepts A time series is a sequence of data points, measured typically at successive times spaced at uniform intervals. Time series are used in such fields as statistics, signal processing

Introduction to Eco n o m et rics

2008 AGI-Information Management Consultants May be used for personal purporses only or by libraries associated to dandelon.com network. Introduction to Eco n o m et rics Third Edition G.S. Maddala Formerly

2008 AGI-Information Management Consultants May be used for personal purporses only or by libraries associated to dandelon.com network. Introduction to Eco n o m et rics Third Edition G.S. Maddala Formerly

Financial Econometrics

Financial Econometrics Nonlinear time series analysis Gerald P. Dwyer Trinity College, Dublin January 2016 Outline 1 Nonlinearity Does nonlinearity matter? Nonlinear models Tests for nonlinearity Forecasting

Financial Econometrics Nonlinear time series analysis Gerald P. Dwyer Trinity College, Dublin January 2016 Outline 1 Nonlinearity Does nonlinearity matter? Nonlinear models Tests for nonlinearity Forecasting

What s New in Econometrics? Lecture 14 Quantile Methods

What s New in Econometrics? Lecture 14 Quantile Methods Jeff Wooldridge NBER Summer Institute, 2007 1. Reminders About Means, Medians, and Quantiles 2. Some Useful Asymptotic Results 3. Quantile Regression

What s New in Econometrics? Lecture 14 Quantile Methods Jeff Wooldridge NBER Summer Institute, 2007 1. Reminders About Means, Medians, and Quantiles 2. Some Useful Asymptotic Results 3. Quantile Regression

Final Overview. Introduction to ML. Marek Petrik 4/25/2017

Final Overview Introduction to ML Marek Petrik 4/25/2017 This Course: Introduction to Machine Learning Build a foundation for practice and research in ML Basic machine learning concepts: max likelihood,

Final Overview Introduction to ML Marek Petrik 4/25/2017 This Course: Introduction to Machine Learning Build a foundation for practice and research in ML Basic machine learning concepts: max likelihood,

A short introduction to INLA and R-INLA

A short introduction to INLA and R-INLA Integrated Nested Laplace Approximation Thomas Opitz, BioSP, INRA Avignon Workshop: Theory and practice of INLA and SPDE November 7, 2018 2/21 Plan for this talk

A short introduction to INLA and R-INLA Integrated Nested Laplace Approximation Thomas Opitz, BioSP, INRA Avignon Workshop: Theory and practice of INLA and SPDE November 7, 2018 2/21 Plan for this talk

Introduction An approximated EM algorithm Simulation studies Discussion

1 / 33 An Approximated Expectation-Maximization Algorithm for Analysis of Data with Missing Values Gong Tang Department of Biostatistics, GSPH University of Pittsburgh NISS Workshop on Nonignorable Nonresponse

1 / 33 An Approximated Expectation-Maximization Algorithm for Analysis of Data with Missing Values Gong Tang Department of Biostatistics, GSPH University of Pittsburgh NISS Workshop on Nonignorable Nonresponse

Adjusted Empirical Likelihood for Long-memory Time Series Models

Adjusted Empirical Likelihood for Long-memory Time Series Models arxiv:1604.06170v1 [stat.me] 21 Apr 2016 Ramadha D. Piyadi Gamage, Wei Ning and Arjun K. Gupta Department of Mathematics and Statistics

Adjusted Empirical Likelihood for Long-memory Time Series Models arxiv:1604.06170v1 [stat.me] 21 Apr 2016 Ramadha D. Piyadi Gamage, Wei Ning and Arjun K. Gupta Department of Mathematics and Statistics

Lecture 2: Univariate Time Series

Lecture 2: Univariate Time Series Analysis: Conditional and Unconditional Densities, Stationarity, ARMA Processes Prof. Massimo Guidolin 20192 Financial Econometrics Spring/Winter 2017 Overview Motivation:

Lecture 2: Univariate Time Series Analysis: Conditional and Unconditional Densities, Stationarity, ARMA Processes Prof. Massimo Guidolin 20192 Financial Econometrics Spring/Winter 2017 Overview Motivation:

International Conference on Applied Probability and Computational Methods in Applied Sciences

International Conference on Applied Probability and Computational Methods in Applied Sciences Organizing Committee Zhiliang Ying, Columbia University and Shanghai Center for Mathematical Sciences Jingchen

International Conference on Applied Probability and Computational Methods in Applied Sciences Organizing Committee Zhiliang Ying, Columbia University and Shanghai Center for Mathematical Sciences Jingchen

Commemoration Day In Honour of Professor Maurice Priestley th December Programme

Commemoration Day In Honour of Professor Maurice Priestley 1933-2013 18th December 2013 Programme Venue: Frank Adams Rooms, Alan Turing Building (opposite Citroën dealer), Upper Brook Street, University

Commemoration Day In Honour of Professor Maurice Priestley 1933-2013 18th December 2013 Programme Venue: Frank Adams Rooms, Alan Turing Building (opposite Citroën dealer), Upper Brook Street, University

Financial Econometrics and Quantitative Risk Managenent Return Properties

Financial Econometrics and Quantitative Risk Managenent Return Properties Eric Zivot Updated: April 1, 2013 Lecture Outline Course introduction Return definitions Empirical properties of returns Reading

Financial Econometrics and Quantitative Risk Managenent Return Properties Eric Zivot Updated: April 1, 2013 Lecture Outline Course introduction Return definitions Empirical properties of returns Reading

Overview of Extreme Value Theory. Dr. Sawsan Hilal space

Overview of Extreme Value Theory Dr. Sawsan Hilal space Maths Department - University of Bahrain space November 2010 Outline Part-1: Univariate Extremes Motivation Threshold Exceedances Part-2: Bivariate

Overview of Extreme Value Theory Dr. Sawsan Hilal space Maths Department - University of Bahrain space November 2010 Outline Part-1: Univariate Extremes Motivation Threshold Exceedances Part-2: Bivariate

GARCH Models. Eduardo Rossi University of Pavia. December Rossi GARCH Financial Econometrics / 50

GARCH Models Eduardo Rossi University of Pavia December 013 Rossi GARCH Financial Econometrics - 013 1 / 50 Outline 1 Stylized Facts ARCH model: definition 3 GARCH model 4 EGARCH 5 Asymmetric Models 6

GARCH Models Eduardo Rossi University of Pavia December 013 Rossi GARCH Financial Econometrics - 013 1 / 50 Outline 1 Stylized Facts ARCH model: definition 3 GARCH model 4 EGARCH 5 Asymmetric Models 6

Introduction to Statistical Analysis

Introduction to Statistical Analysis Changyu Shen Richard A. and Susan F. Smith Center for Outcomes Research in Cardiology Beth Israel Deaconess Medical Center Harvard Medical School Objectives Descriptive

Introduction to Statistical Analysis Changyu Shen Richard A. and Susan F. Smith Center for Outcomes Research in Cardiology Beth Israel Deaconess Medical Center Harvard Medical School Objectives Descriptive

Long-Range Dependence and Self-Similarity. c Vladas Pipiras and Murad S. Taqqu

Long-Range Dependence and Self-Similarity c Vladas Pipiras and Murad S. Taqqu January 24, 2016 Contents Contents 2 Preface 8 List of abbreviations 10 Notation 11 1 A brief overview of times series and

Long-Range Dependence and Self-Similarity c Vladas Pipiras and Murad S. Taqqu January 24, 2016 Contents Contents 2 Preface 8 List of abbreviations 10 Notation 11 1 A brief overview of times series and

STA 4273H: Statistical Machine Learning

STA 4273H: Statistical Machine Learning Russ Salakhutdinov Department of Statistics! rsalakhu@utstat.toronto.edu! http://www.utstat.utoronto.ca/~rsalakhu/ Sidney Smith Hall, Room 6002 Lecture 11 Project

STA 4273H: Statistical Machine Learning Russ Salakhutdinov Department of Statistics! rsalakhu@utstat.toronto.edu! http://www.utstat.utoronto.ca/~rsalakhu/ Sidney Smith Hall, Room 6002 Lecture 11 Project

Elements of Multivariate Time Series Analysis

Gregory C. Reinsel Elements of Multivariate Time Series Analysis Second Edition With 14 Figures Springer Contents Preface to the Second Edition Preface to the First Edition vii ix 1. Vector Time Series

Gregory C. Reinsel Elements of Multivariate Time Series Analysis Second Edition With 14 Figures Springer Contents Preface to the Second Edition Preface to the First Edition vii ix 1. Vector Time Series

A nonparametric test for seasonal unit roots

Robert M. Kunst robert.kunst@univie.ac.at University of Vienna and Institute for Advanced Studies Vienna To be presented in Innsbruck November 7, 2007 Abstract We consider a nonparametric test for the

Robert M. Kunst robert.kunst@univie.ac.at University of Vienna and Institute for Advanced Studies Vienna To be presented in Innsbruck November 7, 2007 Abstract We consider a nonparametric test for the

Bayesian Methods for Machine Learning

Bayesian Methods for Machine Learning CS 584: Big Data Analytics Material adapted from Radford Neal s tutorial (http://ftp.cs.utoronto.ca/pub/radford/bayes-tut.pdf), Zoubin Ghahramni (http://hunch.net/~coms-4771/zoubin_ghahramani_bayesian_learning.pdf),

Bayesian Methods for Machine Learning CS 584: Big Data Analytics Material adapted from Radford Neal s tutorial (http://ftp.cs.utoronto.ca/pub/radford/bayes-tut.pdf), Zoubin Ghahramni (http://hunch.net/~coms-4771/zoubin_ghahramani_bayesian_learning.pdf),

Solutions of the Financial Risk Management Examination

Solutions of the Financial Risk Management Examination Thierry Roncalli January 9 th 03 Remark The first five questions are corrected in TR-GDR and in the document of exercise solutions, which is available

Solutions of the Financial Risk Management Examination Thierry Roncalli January 9 th 03 Remark The first five questions are corrected in TR-GDR and in the document of exercise solutions, which is available

PRINCIPLES OF STATISTICAL INFERENCE

Advanced Series on Statistical Science & Applied Probability PRINCIPLES OF STATISTICAL INFERENCE from a Neo-Fisherian Perspective Luigi Pace Department of Statistics University ofudine, Italy Alessandra

Advanced Series on Statistical Science & Applied Probability PRINCIPLES OF STATISTICAL INFERENCE from a Neo-Fisherian Perspective Luigi Pace Department of Statistics University ofudine, Italy Alessandra

Sequential Procedure for Testing Hypothesis about Mean of Latent Gaussian Process

Applied Mathematical Sciences, Vol. 4, 2010, no. 62, 3083-3093 Sequential Procedure for Testing Hypothesis about Mean of Latent Gaussian Process Julia Bondarenko Helmut-Schmidt University Hamburg University

Applied Mathematical Sciences, Vol. 4, 2010, no. 62, 3083-3093 Sequential Procedure for Testing Hypothesis about Mean of Latent Gaussian Process Julia Bondarenko Helmut-Schmidt University Hamburg University

STAT 4385 Topic 01: Introduction & Review

STAT 4385 Topic 01: Introduction & Review Xiaogang Su, Ph.D. Department of Mathematical Science University of Texas at El Paso xsu@utep.edu Spring, 2016 Outline Welcome What is Regression Analysis? Basics

STAT 4385 Topic 01: Introduction & Review Xiaogang Su, Ph.D. Department of Mathematical Science University of Texas at El Paso xsu@utep.edu Spring, 2016 Outline Welcome What is Regression Analysis? Basics

Choice of Spectral Density Estimator in Ng-Perron Test: Comparative Analysis

MPRA Munich Personal RePEc Archive Choice of Spectral Density Estimator in Ng-Perron Test: Comparative Analysis Muhammad Irfan Malik and Atiq-ur- Rehman International Institute of Islamic Economics, International

MPRA Munich Personal RePEc Archive Choice of Spectral Density Estimator in Ng-Perron Test: Comparative Analysis Muhammad Irfan Malik and Atiq-ur- Rehman International Institute of Islamic Economics, International

Modelling geoadditive survival data

Modelling geoadditive survival data Thomas Kneib & Ludwig Fahrmeir Department of Statistics, Ludwig-Maximilians-University Munich 1. Leukemia survival data 2. Structured hazard regression 3. Mixed model

Modelling geoadditive survival data Thomas Kneib & Ludwig Fahrmeir Department of Statistics, Ludwig-Maximilians-University Munich 1. Leukemia survival data 2. Structured hazard regression 3. Mixed model

Empirical likelihood and self-weighting approach for hypothesis testing of infinite variance processes and its applications

Empirical likelihood and self-weighting approach for hypothesis testing of infinite variance processes and its applications Fumiya Akashi Research Associate Department of Applied Mathematics Waseda University

Empirical likelihood and self-weighting approach for hypothesis testing of infinite variance processes and its applications Fumiya Akashi Research Associate Department of Applied Mathematics Waseda University

Multivariate Time Series: VAR(p) Processes and Models

Processes and Models") Multivariate Time Series: VAR(p) Processes and Models A VAR(p) model, for p > 0 is X t = φ 0 + Φ 1 X t 1 + + Φ p X t p + A t, where X t, φ 0, and X t i are k-vectors, Φ 1,..., Φ p are k k matrices, with

Multivariate Time Series: VAR(p) Processes and Models A VAR(p) model, for p > 0 is X t = φ 0 + Φ 1 X t 1 + + Φ p X t p + A t, where X t, φ 0, and X t i are k-vectors, Φ 1,..., Φ p are k k matrices, with

Prerequisite: STATS 7 or STATS 8 or AP90 or (STATS 120A and STATS 120B and STATS 120C). AP90 with a minimum score of 3

. AP90 with a minimum score of 3") University of California, Irvine 2017-2018 1 Statistics (STATS) Courses STATS 5. Seminar in Data Science. 1 Unit. An introduction to the field of Data Science; intended for entering freshman and transfers.

University of California, Irvine 2017-2018 1 Statistics (STATS) Courses STATS 5. Seminar in Data Science. 1 Unit. An introduction to the field of Data Science; intended for entering freshman and transfers.

A Course in Applied Econometrics Lecture 18: Missing Data. Jeff Wooldridge IRP Lectures, UW Madison, August Linear model with IVs: y i x i u i,

A Course in Applied Econometrics Lecture 18: Missing Data Jeff Wooldridge IRP Lectures, UW Madison, August 2008 1. When Can Missing Data be Ignored? 2. Inverse Probability Weighting 3. Imputation 4. Heckman-Type

A Course in Applied Econometrics Lecture 18: Missing Data Jeff Wooldridge IRP Lectures, UW Madison, August 2008 1. When Can Missing Data be Ignored? 2. Inverse Probability Weighting 3. Imputation 4. Heckman-Type