Trending Models in the Data

|

|

|

- Kevin Smith

- 5 years ago

- Views:

Transcription

1 April 13, 2009

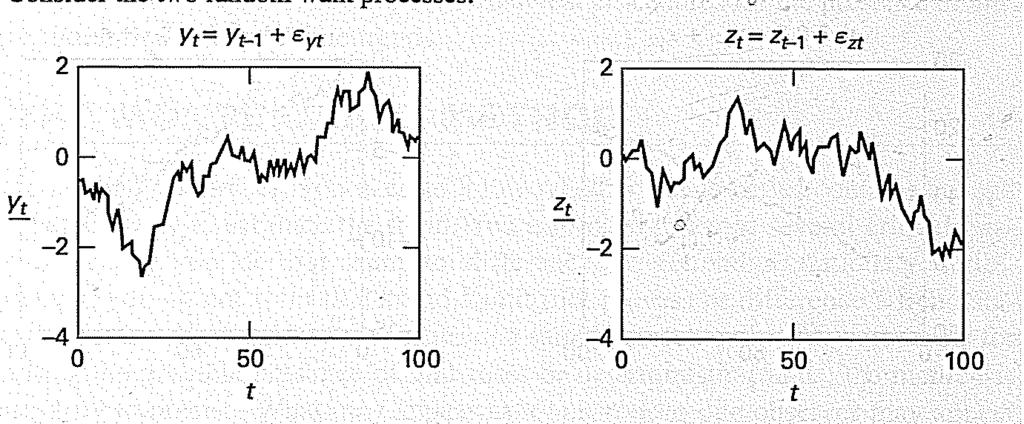

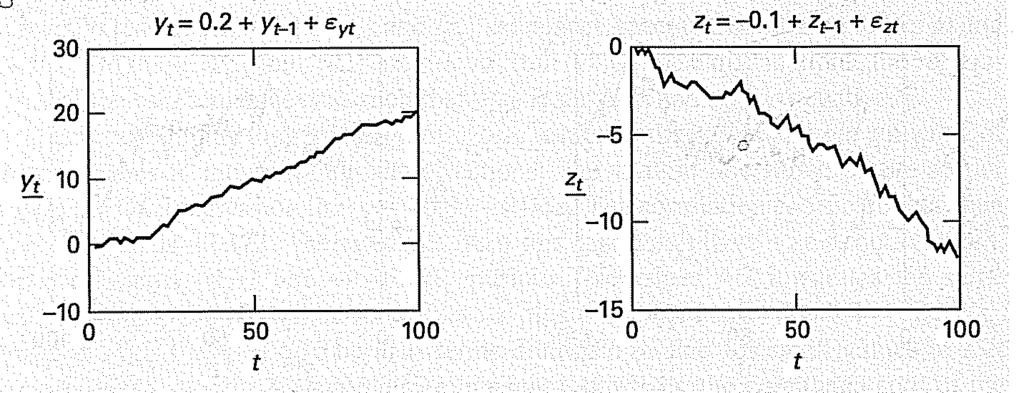

2 Spurious regression I Before we proceed to test for unit root and trend-stationary models, we will examine the phenomena of spurious regression. The material in this lecture can be found in Enders Chapter 4. This demonstrates the importance of knowing whether the series in your dataset are stationary or not. Consider the following two independent AR(1) processes: y t = ρy t 1 + ε yt, ρ 1 z t = θz t 1 + ε zt, θ 1 Now consider the following regression: y t = a 0 + a 1 z t + u t

3 Spurious regression II Since y t and z t are independent, we d like (expect?) to not reject H 0 : a 1 = 0. Granger and Newbold (1974) estimated this regression for ρ = 1 and θ = 1 and found the following: 1 They could not reject a 1 = 0 75% of the time, not the desired 95%. 2 The R 2 values were very high. 3 The residuals had a large amount of serial correlation. To start explaining this, consider the properties of the error process of the regression: u t = y t a 0 a 1 z t

4 Spurious regression III Note that we can re-write: y t = t 1 ρy t 1 + ε yt = ρ i ε y (t i) + ρ t y 0 i=0 z t = t 1 θz t 1 + ε zt = θ i ε z(t i) + θ t z 0 i=0 For simplicity assume that y 0 = z 0 = 0. Then u t = t 1 i=0 ρ i t 1 ε y (t i) a 0 a 1 θ i ε z(t i) i=0

5 Spurious regression IV Then and E (u t ) = a 0 V (u t ) = σ 2 y t 1 ρ 2i + σ 2 t 1 z i=0 i=0 We now see that if jρj < 1 and jθj < 1 fu t g is a heteroscedastic process, at least initially, but eventually it is a nicely behaved stationary process and we can use all our standard tools. If, however, either ρ or θ or both are equal to 1, then V (u t )! θ 2i

6 Spurious regression V Also, if both ρ and θ are equal to 1, u t+1 = y t+1 a 0 a 1 z t+1 = y t + ε yt+1 a 0 a 1 z t a 1 ε zt+1 = u t + ε yt+1 a 1 ε zt+1 Thus u t is I (1). This in terms implies that the process y t can wander in nitely far from it s supposed conditional mean, a 0 + a 1 z t. Also, this is clearly why we see so much serial correlation in the residuals.

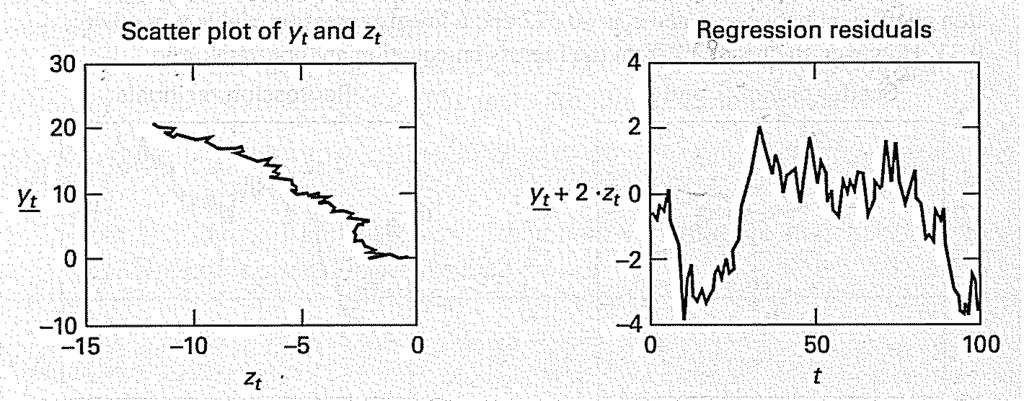

7 Spurious regression VI Finally there is another possibility, if ρ = θ = 1 and ε yt and ε zt are not independent. Then we can write: u t+1 = u t + ε yt+1 a 1 ε zt+1 = u t 1 + ε yt + ε yt+1 a 1 ε zt a 1 ε zt+1 t+1 i=1 = ε yi t+1 a 1 ε zi i=1 If, for example, ε yt and ε zt are perfectly correlated and a 1 = 1, then u t+1 = 0, which is certainly stationary. Thus, y t and z t are both I (1), but y t z t is stationary. This is called cointegration. To sum up: We consider the regression: y t = a 0 + a 1 z t + u t

8 Spurious regression VII If both y t and z t are stationary, so is u t and all our usual regression theory holds. If y t and z t are integrated of di erent orders, u t is nessesarily non-stationary, the regression is meaningless and none of our usual theory holds. If both y t and z t are integrated of order 1, there are two possibilities: They are unrelated series, but you do no nessesarily reject a 1 = 0 and R 2 is high. In this case u t is again non-stationary. The series are cointegrated and thus u t is stationary. How to treat these models is a whole separate topic. Bottomline: It is VERY important to know whether your variables are integrated or not when you apply regression analysis. Spurious regression, visuals:

9 Spurious regression VIII

10 Spurious regression IX

11 Distinguishing Di erent Models I Consider the following data from four di erent models:

12 Distinguishing Di erent Models II It is clear that we cannot tell these apart by visual inspection. Will the ACF tell us that we are dealing with a unit root process? Consider the simple example: and y t = y t 1 + ε t, y t = y 0 + E (y t ) = y 0 t ε j j=1

13 Distinguishing Di erent Models III The autocovariance is: γ s = E [(y t y 0 ) (y t s y 0 )] " # t t s = E ε j ε i = (t s) σ 2 j=1 i=1 The variance is: V (y t ) = tσ 2 and therefore the ACF is r (t s) (t s) ρ s = p = (t s) t t

14 Distinguishing Di erent Models IV Note that as s increases the ACF falls, making it hard to tell the di erence between the unit root process and an AR process, even when the errors are white noise. For a trend model: and y t = α + δt + u t E (y t ) = α + δt V (y t ) = V (u t )

15 Distinguishing Di erent Models V So and γ s = E [(y t (α + δt)) (y t s (α + δ (t s)))] = E (u t u t s ) ρ s = E (u tu t s ) V (u t ) V (u s ) So the ACF re ects the ACF of the error process. Clearly recognizable if the error process is white noise... The rst investigation to distinguish between these two types of series was made using the ACF of the residuals series tted to either stochastic or deterministic trends.

16 Distinguishing Di erent Models VI Consider the following estimation on real GDP data: rgdp t = t t t 3 The graph of the data and the tted values looks like:

17 Distinguishing Di erent Models VII If we just eyeball, this seems like a very good model. An alternative estimation is: ln (rgdp t ) = ln (rgdp t 1 ) ln (rgdp t 2 ) The ACF and PACF from the residuals look like:

18 Distinguishing Di erent Models VIII

19 Distinguishing Di erent Models IX Clearly there is a lot of persistence left after de-trending, even though the t looked very good, where as the estimated unit root model seems to have residuals that behave like white noise. This point was rst made by Nelson and Plosser in They tted thirteen important macroeconomic series that had been treated as trend-stationary up until that point.

20 Unit Root Testing in a Simple Model I Consider the very simple model y t = α + ρy t 1 + ε t We know we cannot use standard hypothesis testing to test ρ = 1. (Although ρ = 0 would work). Especially with OLS we know that our estimates of ρ are downwards biased, making the model look more like a stationary AR (1) process. The asymptotic distribution of ˆρ can be found, but it has no nice closed form. It turns out that we can use the computer to nd the distribution under the null of ρ = 1. How?

21 Unit Root Testing in a Simple Model II You generate data according to y t = α + y t 1 + ε t Then you estimate y t = α + ρy t 1 + ε t using OLS and record the value of ˆρ and s 2, or, more importantly t = ˆρ 1 q s 2 (y t 1 ȳ) 2 You repeat this process many times and keep the results.

22 Unit Root Testing in a Simple Model III Dickey and Fuller found that 90% of the time t was less than % of the time t was less than % of the time t was less than 3.51 How do you use this information to carry out tests? What type of mistake would we have been making if we used standard normal critical values? How would you create a two-sided test? Caution: These methods only work if a CLT actually applies! It is also nessesary to investigate how the assumptions under which you generated the data a ects the reults. In this case: Do the numbers depend on the exact distribution of ε t? Do the numbers depend on the value of α used to generate the data?

23 Dickey-Fuller Tests I A little about Dickey and Fuller and Iowa State. Dickey and Fuller considered three di erent models: y t = γy t 1 + ε t (1) y t = a 0 + γy t 1 + ε t (2) y t = a 0 + γy t 1 + a 2 t + ε t (3) Note that (1) is equivalent to the model we considered last section. The hypothesis of interest now is H 0 : γ = 0. The alternative we are considering is H A : γ < 0. Typically we ignore the possibility that y t = y t 1 + ε t, even though, stricly speaking, this is also a unit root.

24 Dickey-Fuller Tests II To test γ = 0, we simply calculate the standard t statistic. Unfortunately the critical values are di erent for the three di erent models above. The t-test statitistic for the three models above are ususally labelled: τ, τ µ and τ τ. Dickey and Fuller also provide critical values for F test of joint hypotheses in these three models. We will apply these in an example later.

25 Augmented Dickey-Fuller Tests I Clearly AR (1) models are not always su cient to describe our data. Consider an AR (p) process: y t = a 0 + a 1 y t 1 + a 2 y t a p y t p + ε t We can rewrite this model in the following way: y t = a 0 + a 1 y t a p 1 y t p+1 + a p y t p+1 a p y t p+1 + ε t = a 0 + a 1 y t (a p 1 + a p ) y t p+1 a p y t p+1 + ε t = a 0 + a 1 y t a p 2 y t p+2 + (a p 1 + a p ) y t p+2 (a p 1 + a p ) y t p+2 a p y t p+1 + ε t

26 Augmented Dickey-Fuller Tests II y t = a 0 + a 1 y t (a p 2 + a p 1 + a p ) y t p+2 (a p 1 + a p ) y t p+2 a p y t p+1 + ε t = a 0 + (a a p 1 + a p ) y t 1 From this expression we get: (a a p 1 + a p ) y t 1... a p y t p+1 + ε t y t = a 0 + (a a p 1 + a p 1) y t 1 (a a p 1 + a p ) y t 1... a p y t p+1 + ε t = a 0 + γy t 1 + p i=2 β i y t i+1 + ε t

27 Augmented Dickey-Fuller Tests III where γ = β i = p i=1 p a j j=i a i! 1 and Again, we have a unit root if γ = 0. If this model is correctly speci ed we can use the critical values which applied to the simpler models.

28 Augmented Dickey-Fuller Tests IV This still leaves many important issues to deal with in the data: The model may contain unknown MA components. We need to have the right number of autoregressive lags. The data might be I (2) or higher. There might be structural breaks in the data. These can confuse and make it seem like otherwise stationary data has a unit root. We may not know whether to include the constant and trend in the model. Unknown MA components are reaonable simple to deal with. We can write an invertible ARMA process as an AR ( ) process, such that: y t = a 0 + γy t 1 + i=2 β i y t i+1 + ε t This we cannot estimate with nite samples...

29 Augmented Dickey-Fuller Tests V Dickey and Fuller have shown that an unknown ARIMA (p, 1, q) process can be well approximated by an ARIMA (n, 1, 0), where n T 3 1. Clearly we can estimate an ARIMA T 1 3, 1, 0 with a dataset of T observations.

30 Augmented Dickey-Fuller Tests I Lag-length Selection An important practical issue for the implementation ofthe ADF test is the speci cation of the lag length p. If p is too small then the remaining serial correlation in the errors will bias the test. If p is too large then the power of the test will su er. (Why?) Monte Carlo experiments suggest it is better to err on the side of including too many lags. A standard method for lag selection is: Set an upper bound p max for p. Estimate the ADF test regression with p = p max.

31 Augmented Dickey-Fuller Tests II Lag-length Selection If the absolute value of the t statistic for testing the signi cance of the last lagged di erence is greater than 1.6 then set p = p max and perform the unit root test. Otherwise, reduce the lag length by one and repeat the process. A common rule of thumb for determining p max, suggested by Schwert (1989), is p max = " 12 1 # T where [x] denotes the integer part of x. Note that this choice is completely ad hoc! Remember to check that the residuals look like white noise after selecting a lag length (regardless of selection method...)

32 Augmented Dickey-Fuller Tests III Lag-length Selection A di erent way to determine lag length is to use information criteria. The standard AIC and SBC are often used. Example of lag length selection. 200 observations were generated by: y t = y t y t 3 + ε t Here the series does contain a unit root and the correct lag length is 3. The data looks like:

33 Augmented Dickey-Fuller Tests IV Lag-length Selection

34 Augmented Dickey-Fuller Tests V Lag-length Selection Seeing this data we clearly cannot tell whether or not to include a trend, so we estimate: y t = a 0 + a 2 t + γy t 1 + p i=2 β i y t i+1 + ε t The estimation results are:

35 Augmented Dickey-Fuller Tests VI Lag-length Selection For this model the critical value for the DF test is t test < 3.43) SBC and AIC do not agree on the lag length choice (Reject if It turns out, however, that this does not a ect the conclusion of the unit root test... The φ 2 statistic tests the hypothesis that a 0 = a 2 = γ = 0 and the φ 3 statistic tests the hypothesis that a 2 = γ = 0. The critical values are 4.88 and As a result we do reject the presence of a trend, but not the presence of a constant. If we had tested this model with t and F tests, β 4 = 0, β 3 = β 4 = 0 and so forth, we would have concluded that we should have included 2 lags.

36 Augmented Dickey-Fuller Tests VII Lag-length Selection Also note that had we used four lags, we would not have been able to reject a 0 = a 2 = γ = 0. This is because of the reduced power of the test. Finally note that he current state of the art for lag selection was introduced by Ng and Perron in This critereon is the MAIC (k).

Topic 4 Unit Roots. Gerald P. Dwyer. February Clemson University

Topic 4 Unit Roots Gerald P. Dwyer Clemson University February 2016 Outline 1 Unit Roots Introduction Trend and Difference Stationary Autocorrelations of Series That Have Deterministic or Stochastic Trends

Topic 4 Unit Roots Gerald P. Dwyer Clemson University February 2016 Outline 1 Unit Roots Introduction Trend and Difference Stationary Autocorrelations of Series That Have Deterministic or Stochastic Trends

1 Regression with Time Series Variables

1 Regression with Time Series Variables With time series regression, Y might not only depend on X, but also lags of Y and lags of X Autoregressive Distributed lag (or ADL(p; q)) model has these features:

1 Regression with Time Series Variables With time series regression, Y might not only depend on X, but also lags of Y and lags of X Autoregressive Distributed lag (or ADL(p; q)) model has these features:

Multivariate Time Series

Multivariate Time Series Fall 2008 Environmental Econometrics (GR03) TSII Fall 2008 1 / 16 More on AR(1) In AR(1) model (Y t = µ + ρy t 1 + u t ) with ρ = 1, the series is said to have a unit root or a

Multivariate Time Series Fall 2008 Environmental Econometrics (GR03) TSII Fall 2008 1 / 16 More on AR(1) In AR(1) model (Y t = µ + ρy t 1 + u t ) with ρ = 1, the series is said to have a unit root or a

Problem set 1 - Solutions

EMPIRICAL FINANCE AND FINANCIAL ECONOMETRICS - MODULE (8448) Problem set 1 - Solutions Exercise 1 -Solutions 1. The correct answer is (a). In fact, the process generating daily prices is usually assumed

EMPIRICAL FINANCE AND FINANCIAL ECONOMETRICS - MODULE (8448) Problem set 1 - Solutions Exercise 1 -Solutions 1. The correct answer is (a). In fact, the process generating daily prices is usually assumed

Unit Root and Cointegration

Unit Root and Cointegration Carlos Hurtado Department of Economics University of Illinois at Urbana-Champaign hrtdmrt@illinois.edu Oct 7th, 016 C. Hurtado (UIUC - Economics) Applied Econometrics On the

Unit Root and Cointegration Carlos Hurtado Department of Economics University of Illinois at Urbana-Champaign hrtdmrt@illinois.edu Oct 7th, 016 C. Hurtado (UIUC - Economics) Applied Econometrics On the

Econometrics. Week 11. Fall Institute of Economic Studies Faculty of Social Sciences Charles University in Prague

Econometrics Week 11 Institute of Economic Studies Faculty of Social Sciences Charles University in Prague Fall 2012 1 / 30 Recommended Reading For the today Advanced Time Series Topics Selected topics

Econometrics Week 11 Institute of Economic Studies Faculty of Social Sciences Charles University in Prague Fall 2012 1 / 30 Recommended Reading For the today Advanced Time Series Topics Selected topics

Stationary and nonstationary variables

Stationary and nonstationary variables Stationary variable: 1. Finite and constant in time expected value: E (y t ) = µ < 2. Finite and constant in time variance: Var (y t ) = σ 2 < 3. Covariance dependent

Stationary and nonstationary variables Stationary variable: 1. Finite and constant in time expected value: E (y t ) = µ < 2. Finite and constant in time variance: Var (y t ) = σ 2 < 3. Covariance dependent

Lecture 5: Unit Roots, Cointegration and Error Correction Models The Spurious Regression Problem

Lecture 5: Unit Roots, Cointegration and Error Correction Models The Spurious Regression Problem Prof. Massimo Guidolin 20192 Financial Econometrics Winter/Spring 2018 Overview Stochastic vs. deterministic

Lecture 5: Unit Roots, Cointegration and Error Correction Models The Spurious Regression Problem Prof. Massimo Guidolin 20192 Financial Econometrics Winter/Spring 2018 Overview Stochastic vs. deterministic

Non-Stationary Time Series and Unit Root Testing

Econometrics II Non-Stationary Time Series and Unit Root Testing Morten Nyboe Tabor Course Outline: Non-Stationary Time Series and Unit Root Testing 1 Stationarity and Deviation from Stationarity Trend-Stationarity

Econometrics II Non-Stationary Time Series and Unit Root Testing Morten Nyboe Tabor Course Outline: Non-Stationary Time Series and Unit Root Testing 1 Stationarity and Deviation from Stationarity Trend-Stationarity

E 4101/5101 Lecture 9: Non-stationarity

E 4101/5101 Lecture 9: Non-stationarity Ragnar Nymoen 30 March 2011 Introduction I Main references: Hamilton Ch 15,16 and 17. Davidson and MacKinnon Ch 14.3 and 14.4 Also read Ch 2.4 and Ch 2.5 in Davidson

E 4101/5101 Lecture 9: Non-stationarity Ragnar Nymoen 30 March 2011 Introduction I Main references: Hamilton Ch 15,16 and 17. Davidson and MacKinnon Ch 14.3 and 14.4 Also read Ch 2.4 and Ch 2.5 in Davidson

Empirical Market Microstructure Analysis (EMMA)

") Empirical Market Microstructure Analysis (EMMA) Lecture 3: Statistical Building Blocks and Econometric Basics Prof. Dr. Michael Stein michael.stein@vwl.uni-freiburg.de Albert-Ludwigs-University of Freiburg

Empirical Market Microstructure Analysis (EMMA) Lecture 3: Statistical Building Blocks and Econometric Basics Prof. Dr. Michael Stein michael.stein@vwl.uni-freiburg.de Albert-Ludwigs-University of Freiburg

Prof. Dr. Roland Füss Lecture Series in Applied Econometrics Summer Term Introduction to Time Series Analysis

Introduction to Time Series Analysis 1 Contents: I. Basics of Time Series Analysis... 4 I.1 Stationarity... 5 I.2 Autocorrelation Function... 9 I.3 Partial Autocorrelation Function (PACF)... 14 I.4 Transformation

Introduction to Time Series Analysis 1 Contents: I. Basics of Time Series Analysis... 4 I.1 Stationarity... 5 I.2 Autocorrelation Function... 9 I.3 Partial Autocorrelation Function (PACF)... 14 I.4 Transformation

Cointegration, Stationarity and Error Correction Models.

Cointegration, Stationarity and Error Correction Models. STATIONARITY Wold s decomposition theorem states that a stationary time series process with no deterministic components has an infinite moving average

Cointegration, Stationarity and Error Correction Models. STATIONARITY Wold s decomposition theorem states that a stationary time series process with no deterministic components has an infinite moving average

Time Series Analysis. James D. Hamilton PRINCETON UNIVERSITY PRESS PRINCETON, NEW JERSEY

Time Series Analysis James D. Hamilton PRINCETON UNIVERSITY PRESS PRINCETON, NEW JERSEY & Contents PREFACE xiii 1 1.1. 1.2. Difference Equations First-Order Difference Equations 1 /?th-order Difference

Time Series Analysis James D. Hamilton PRINCETON UNIVERSITY PRESS PRINCETON, NEW JERSEY & Contents PREFACE xiii 1 1.1. 1.2. Difference Equations First-Order Difference Equations 1 /?th-order Difference

E 4160 Autumn term Lecture 9: Deterministic trends vs integrated series; Spurious regression; Dickey-Fuller distribution and test

E 4160 Autumn term 2016. Lecture 9: Deterministic trends vs integrated series; Spurious regression; Dickey-Fuller distribution and test Ragnar Nymoen Department of Economics, University of Oslo 24 October

E 4160 Autumn term 2016. Lecture 9: Deterministic trends vs integrated series; Spurious regression; Dickey-Fuller distribution and test Ragnar Nymoen Department of Economics, University of Oslo 24 October

Advanced Econometrics

Advanced Econometrics Marco Sunder Nov 04 2010 Marco Sunder Advanced Econometrics 1/ 25 Contents 1 2 3 Marco Sunder Advanced Econometrics 2/ 25 Music Marco Sunder Advanced Econometrics 3/ 25 Music Marco

Advanced Econometrics Marco Sunder Nov 04 2010 Marco Sunder Advanced Econometrics 1/ 25 Contents 1 2 3 Marco Sunder Advanced Econometrics 2/ 25 Music Marco Sunder Advanced Econometrics 3/ 25 Music Marco

Non-Stationary Time Series and Unit Root Testing

Econometrics II Non-Stationary Time Series and Unit Root Testing Morten Nyboe Tabor Course Outline: Non-Stationary Time Series and Unit Root Testing 1 Stationarity and Deviation from Stationarity Trend-Stationarity

Econometrics II Non-Stationary Time Series and Unit Root Testing Morten Nyboe Tabor Course Outline: Non-Stationary Time Series and Unit Root Testing 1 Stationarity and Deviation from Stationarity Trend-Stationarity

MA Advanced Econometrics: Applying Least Squares to Time Series

MA Advanced Econometrics: Applying Least Squares to Time Series Karl Whelan School of Economics, UCD February 15, 2011 Karl Whelan (UCD) Time Series February 15, 2011 1 / 24 Part I Time Series: Standard

MA Advanced Econometrics: Applying Least Squares to Time Series Karl Whelan School of Economics, UCD February 15, 2011 Karl Whelan (UCD) Time Series February 15, 2011 1 / 24 Part I Time Series: Standard

Non-Stationary Time Series and Unit Root Testing

Econometrics II Non-Stationary Time Series and Unit Root Testing Morten Nyboe Tabor Course Outline: Non-Stationary Time Series and Unit Root Testing 1 Stationarity and Deviation from Stationarity Trend-Stationarity

Econometrics II Non-Stationary Time Series and Unit Root Testing Morten Nyboe Tabor Course Outline: Non-Stationary Time Series and Unit Root Testing 1 Stationarity and Deviation from Stationarity Trend-Stationarity

Econometrics of Panel Data

Econometrics of Panel Data Jakub Mućk Meeting # 9 Jakub Mućk Econometrics of Panel Data Meeting # 9 1 / 22 Outline 1 Time series analysis Stationarity Unit Root Tests for Nonstationarity 2 Panel Unit Root

Econometrics of Panel Data Jakub Mućk Meeting # 9 Jakub Mućk Econometrics of Panel Data Meeting # 9 1 / 22 Outline 1 Time series analysis Stationarity Unit Root Tests for Nonstationarity 2 Panel Unit Root

BCT Lecture 3. Lukas Vacha.

BCT Lecture 3 Lukas Vacha vachal@utia.cas.cz Stationarity and Unit Root Testing Why do we need to test for Non-Stationarity? The stationarity or otherwise of a series can strongly influence its behaviour

BCT Lecture 3 Lukas Vacha vachal@utia.cas.cz Stationarity and Unit Root Testing Why do we need to test for Non-Stationarity? The stationarity or otherwise of a series can strongly influence its behaviour

11/18/2008. So run regression in first differences to examine association. 18 November November November 2008

Time Series Econometrics 7 Vijayamohanan Pillai N Unit Root Tests Vijayamohan: CDS M Phil: Time Series 7 1 Vijayamohan: CDS M Phil: Time Series 7 2 R 2 > DW Spurious/Nonsense Regression. Integrated but

Time Series Econometrics 7 Vijayamohanan Pillai N Unit Root Tests Vijayamohan: CDS M Phil: Time Series 7 1 Vijayamohan: CDS M Phil: Time Series 7 2 R 2 > DW Spurious/Nonsense Regression. Integrated but

Econ 423 Lecture Notes: Additional Topics in Time Series 1

Econ 423 Lecture Notes: Additional Topics in Time Series 1 John C. Chao April 25, 2017 1 These notes are based in large part on Chapter 16 of Stock and Watson (2011). They are for instructional purposes

Econ 423 Lecture Notes: Additional Topics in Time Series 1 John C. Chao April 25, 2017 1 These notes are based in large part on Chapter 16 of Stock and Watson (2011). They are for instructional purposes

Response surface models for the Elliott, Rothenberg, Stock DF-GLS unit-root test

Response surface models for the Elliott, Rothenberg, Stock DF-GLS unit-root test Christopher F Baum Jesús Otero Stata Conference, Baltimore, July 2017 Baum, Otero (BC, U. del Rosario) DF-GLS response surfaces

Response surface models for the Elliott, Rothenberg, Stock DF-GLS unit-root test Christopher F Baum Jesús Otero Stata Conference, Baltimore, July 2017 Baum, Otero (BC, U. del Rosario) DF-GLS response surfaces

Chapter 2: Unit Roots

Chapter 2: Unit Roots 1 Contents: Lehrstuhl für Department Empirische of Wirtschaftsforschung Empirical Research and undeconometrics II. Unit Roots... 3 II.1 Integration Level... 3 II.2 Nonstationarity

Chapter 2: Unit Roots 1 Contents: Lehrstuhl für Department Empirische of Wirtschaftsforschung Empirical Research and undeconometrics II. Unit Roots... 3 II.1 Integration Level... 3 II.2 Nonstationarity

Economics 618B: Time Series Analysis Department of Economics State University of New York at Binghamton

Problem Set #1 1. Generate n =500random numbers from both the uniform 1 (U [0, 1], uniformbetween zero and one) and exponential λ exp ( λx) (set λ =2and let x U [0, 1]) b a distributions. Plot the histograms

Problem Set #1 1. Generate n =500random numbers from both the uniform 1 (U [0, 1], uniformbetween zero and one) and exponential λ exp ( λx) (set λ =2and let x U [0, 1]) b a distributions. Plot the histograms

ECON 616: Lecture Two: Deterministic Trends, Nonstationary Processes

ECON 616: Lecture Two: Deterministic Trends, Nonstationary Processes ED HERBST September 11, 2017 Background Hamilton, chapters 15-16 Trends vs Cycles A commond decomposition of macroeconomic time series

ECON 616: Lecture Two: Deterministic Trends, Nonstationary Processes ED HERBST September 11, 2017 Background Hamilton, chapters 15-16 Trends vs Cycles A commond decomposition of macroeconomic time series

Time Series Analysis. James D. Hamilton PRINCETON UNIVERSITY PRESS PRINCETON, NEW JERSEY

Time Series Analysis James D. Hamilton PRINCETON UNIVERSITY PRESS PRINCETON, NEW JERSEY PREFACE xiii 1 Difference Equations 1.1. First-Order Difference Equations 1 1.2. pth-order Difference Equations 7

Time Series Analysis James D. Hamilton PRINCETON UNIVERSITY PRESS PRINCETON, NEW JERSEY PREFACE xiii 1 Difference Equations 1.1. First-Order Difference Equations 1 1.2. pth-order Difference Equations 7

GLS-based unit root tests with multiple structural breaks both under the null and the alternative hypotheses

GLS-based unit root tests with multiple structural breaks both under the null and the alternative hypotheses Josep Lluís Carrion-i-Silvestre University of Barcelona Dukpa Kim Boston University Pierre Perron

GLS-based unit root tests with multiple structural breaks both under the null and the alternative hypotheses Josep Lluís Carrion-i-Silvestre University of Barcelona Dukpa Kim Boston University Pierre Perron

10) Time series econometrics

Time series econometrics") 30C00200 Econometrics 10) Time series econometrics Timo Kuosmanen Professor, Ph.D. 1 Topics today Static vs. dynamic time series model Suprious regression Stationary and nonstationary time series Unit

30C00200 Econometrics 10) Time series econometrics Timo Kuosmanen Professor, Ph.D. 1 Topics today Static vs. dynamic time series model Suprious regression Stationary and nonstationary time series Unit

Univariate, Nonstationary Processes

Univariate, Nonstationary Processes Jamie Monogan University of Georgia March 20, 2018 Jamie Monogan (UGA) Univariate, Nonstationary Processes March 20, 2018 1 / 14 Objectives By the end of this meeting,

Univariate, Nonstationary Processes Jamie Monogan University of Georgia March 20, 2018 Jamie Monogan (UGA) Univariate, Nonstationary Processes March 20, 2018 1 / 14 Objectives By the end of this meeting,

9) Time series econometrics

Time series econometrics") 30C00200 Econometrics 9) Time series econometrics Timo Kuosmanen Professor Management Science http://nomepre.net/index.php/timokuosmanen 1 Macroeconomic data: GDP Inflation rate Examples of time series

30C00200 Econometrics 9) Time series econometrics Timo Kuosmanen Professor Management Science http://nomepre.net/index.php/timokuosmanen 1 Macroeconomic data: GDP Inflation rate Examples of time series

Response surface models for the Elliott, Rothenberg, Stock DF-GLS unit-root test

Response surface models for the Elliott, Rothenberg, Stock DF-GLS unit-root test Christopher F Baum Jesús Otero UK Stata Users Group Meetings, London, September 2017 Baum, Otero (BC, U. del Rosario) DF-GLS

Response surface models for the Elliott, Rothenberg, Stock DF-GLS unit-root test Christopher F Baum Jesús Otero UK Stata Users Group Meetings, London, September 2017 Baum, Otero (BC, U. del Rosario) DF-GLS

Nonstationary Time Series:

Nonstationary Time Series: Unit Roots Egon Zakrajšek Division of Monetary Affairs Federal Reserve Board Summer School in Financial Mathematics Faculty of Mathematics & Physics University of Ljubljana September

Nonstationary Time Series: Unit Roots Egon Zakrajšek Division of Monetary Affairs Federal Reserve Board Summer School in Financial Mathematics Faculty of Mathematics & Physics University of Ljubljana September

1 Augmented Dickey Fuller, ADF, Test

Applied Econometrics 1 Augmented Dickey Fuller, ADF, Test Consider a simple general AR(p) process given by Y t = ¹ + Á 1 Y t 1 + Á 2 Y t 2 + ::::Á p Y t p + ² t (1) If this is the process generating the

Applied Econometrics 1 Augmented Dickey Fuller, ADF, Test Consider a simple general AR(p) process given by Y t = ¹ + Á 1 Y t 1 + Á 2 Y t 2 + ::::Á p Y t p + ² t (1) If this is the process generating the

Testing for Unit Roots with Cointegrated Data

Discussion Paper No. 2015-57 August 19, 2015 http://www.economics-ejournal.org/economics/discussionpapers/2015-57 Testing for Unit Roots with Cointegrated Data W. Robert Reed Abstract This paper demonstrates

Discussion Paper No. 2015-57 August 19, 2015 http://www.economics-ejournal.org/economics/discussionpapers/2015-57 Testing for Unit Roots with Cointegrated Data W. Robert Reed Abstract This paper demonstrates

On the robustness of cointegration tests when series are fractionally integrated

On the robustness of cointegration tests when series are fractionally integrated JESUS GONZALO 1 &TAE-HWYLEE 2, 1 Universidad Carlos III de Madrid, Spain and 2 University of California, Riverside, USA

On the robustness of cointegration tests when series are fractionally integrated JESUS GONZALO 1 &TAE-HWYLEE 2, 1 Universidad Carlos III de Madrid, Spain and 2 University of California, Riverside, USA

Multivariate Time Series: Part 4

Multivariate Time Series: Part 4 Cointegration Gerald P. Dwyer Clemson University March 2016 Outline 1 Multivariate Time Series: Part 4 Cointegration Engle-Granger Test for Cointegration Johansen Test

Multivariate Time Series: Part 4 Cointegration Gerald P. Dwyer Clemson University March 2016 Outline 1 Multivariate Time Series: Part 4 Cointegration Engle-Granger Test for Cointegration Johansen Test

Time Series Econometrics 4 Vijayamohanan Pillai N

Time Series Econometrics 4 Vijayamohanan Pillai N Vijayamohan: CDS MPhil: Time Series 5 1 Autoregressive Moving Average Process: ARMA(p, q) Vijayamohan: CDS MPhil: Time Series 5 2 1 Autoregressive Moving

Time Series Econometrics 4 Vijayamohanan Pillai N Vijayamohan: CDS MPhil: Time Series 5 1 Autoregressive Moving Average Process: ARMA(p, q) Vijayamohan: CDS MPhil: Time Series 5 2 1 Autoregressive Moving

FE570 Financial Markets and Trading. Stevens Institute of Technology

FE570 Financial Markets and Trading Lecture 5. Linear Time Series Analysis and Its Applications (Ref. Joel Hasbrouck - Empirical Market Microstructure ) Steve Yang Stevens Institute of Technology 9/25/2012

FE570 Financial Markets and Trading Lecture 5. Linear Time Series Analysis and Its Applications (Ref. Joel Hasbrouck - Empirical Market Microstructure ) Steve Yang Stevens Institute of Technology 9/25/2012

Economic modelling and forecasting. 2-6 February 2015

Economic modelling and forecasting 2-6 February 2015 Bank of England 2015 Ole Rummel Adviser, CCBS at the Bank of England ole.rummel@bankofengland.co.uk Philosophy of my presentations Everything should

Economic modelling and forecasting 2-6 February 2015 Bank of England 2015 Ole Rummel Adviser, CCBS at the Bank of England ole.rummel@bankofengland.co.uk Philosophy of my presentations Everything should

Cointegration and Error Correction Exercise Class, Econometrics II

u n i v e r s i t y o f c o p e n h a g e n Faculty of Social Sciences Cointegration and Error Correction Exercise Class, Econometrics II Department of Economics March 19, 2017 Slide 1/39 Todays plan!

u n i v e r s i t y o f c o p e n h a g e n Faculty of Social Sciences Cointegration and Error Correction Exercise Class, Econometrics II Department of Economics March 19, 2017 Slide 1/39 Todays plan!

A TIME SERIES PARADOX: UNIT ROOT TESTS PERFORM POORLY WHEN DATA ARE COINTEGRATED

A TIME SERIES PARADOX: UNIT ROOT TESTS PERFORM POORLY WHEN DATA ARE COINTEGRATED by W. Robert Reed Department of Economics and Finance University of Canterbury, New Zealand Email: bob.reed@canterbury.ac.nz

A TIME SERIES PARADOX: UNIT ROOT TESTS PERFORM POORLY WHEN DATA ARE COINTEGRATED by W. Robert Reed Department of Economics and Finance University of Canterbury, New Zealand Email: bob.reed@canterbury.ac.nz

Cointegration Tests Using Instrumental Variables Estimation and the Demand for Money in England

Cointegration Tests Using Instrumental Variables Estimation and the Demand for Money in England Kyung So Im Junsoo Lee Walter Enders June 12, 2005 Abstract In this paper, we propose new cointegration tests

Cointegration Tests Using Instrumental Variables Estimation and the Demand for Money in England Kyung So Im Junsoo Lee Walter Enders June 12, 2005 Abstract In this paper, we propose new cointegration tests

Moreover, the second term is derived from: 1 T ) 2 1

2 1") 170 Moreover, the second term is derived from: 1 T T ɛt 2 σ 2 ɛ. Therefore, 1 σ 2 ɛt T y t 1 ɛ t = 1 2 ( yt σ T ) 2 1 2σ 2 ɛ 1 T T ɛt 2 1 2 (χ2 (1) 1). (b) Next, consider y 2 t 1. T E y 2 t 1 T T = E(y

170 Moreover, the second term is derived from: 1 T T ɛt 2 σ 2 ɛ. Therefore, 1 σ 2 ɛt T y t 1 ɛ t = 1 2 ( yt σ T ) 2 1 2σ 2 ɛ 1 T T ɛt 2 1 2 (χ2 (1) 1). (b) Next, consider y 2 t 1. T E y 2 t 1 T T = E(y

Time Series Models and Inference. James L. Powell Department of Economics University of California, Berkeley

Time Series Models and Inference James L. Powell Department of Economics University of California, Berkeley Overview In contrast to the classical linear regression model, in which the components of the

Time Series Models and Inference James L. Powell Department of Economics University of California, Berkeley Overview In contrast to the classical linear regression model, in which the components of the

Lecture: Testing Stationarity: Structural Change Problem

Lecture: Testing Stationarity: Structural Change Problem Applied Econometrics Jozef Barunik IES, FSV, UK Summer Semester 2009/2010 Lecture: Testing Stationarity: Structural Change Summer ProblemSemester

Lecture: Testing Stationarity: Structural Change Problem Applied Econometrics Jozef Barunik IES, FSV, UK Summer Semester 2009/2010 Lecture: Testing Stationarity: Structural Change Summer ProblemSemester

Financial Time Series Analysis: Part II

Department of Mathematics and Statistics, University of Vaasa, Finland Spring 2017 1 Unit root Deterministic trend Stochastic trend Testing for unit root ADF-test (Augmented Dickey-Fuller test) Testing

Department of Mathematics and Statistics, University of Vaasa, Finland Spring 2017 1 Unit root Deterministic trend Stochastic trend Testing for unit root ADF-test (Augmented Dickey-Fuller test) Testing

Econometrics Lecture 9 Time Series Methods

Econometrics Lecture 9 Time Series Methods Tak Wai Chau Shanghai University of Finance and Economics Spring 2014 1 / 82 Time Series Data I Time series data are data observed for the same unit repeatedly

Econometrics Lecture 9 Time Series Methods Tak Wai Chau Shanghai University of Finance and Economics Spring 2014 1 / 82 Time Series Data I Time series data are data observed for the same unit repeatedly

Economics 620, Lecture 13: Time Series I

Economics 620, Lecture 13: Time Series I Nicholas M. Kiefer Cornell University Professor N. M. Kiefer (Cornell University) Lecture 13: Time Series I 1 / 19 AUTOCORRELATION Consider y = X + u where y is

Economics 620, Lecture 13: Time Series I Nicholas M. Kiefer Cornell University Professor N. M. Kiefer (Cornell University) Lecture 13: Time Series I 1 / 19 AUTOCORRELATION Consider y = X + u where y is

Finite-sample quantiles of the Jarque-Bera test

Finite-sample quantiles of the Jarque-Bera test Steve Lawford Department of Economics and Finance, Brunel University First draft: February 2004. Abstract The nite-sample null distribution of the Jarque-Bera

Finite-sample quantiles of the Jarque-Bera test Steve Lawford Department of Economics and Finance, Brunel University First draft: February 2004. Abstract The nite-sample null distribution of the Jarque-Bera

Föreläsning /31

1/31 Föreläsning 10 090420 Chapter 13 Econometric Modeling: Model Speci cation and Diagnostic testing 2/31 Types of speci cation errors Consider the following models: Y i = β 1 + β 2 X i + β 3 X 2 i +

1/31 Föreläsning 10 090420 Chapter 13 Econometric Modeling: Model Speci cation and Diagnostic testing 2/31 Types of speci cation errors Consider the following models: Y i = β 1 + β 2 X i + β 3 X 2 i +

Econometric Methods for Panel Data

Based on the books by Baltagi: Econometric Analysis of Panel Data and by Hsiao: Analysis of Panel Data Robert M. Kunst robert.kunst@univie.ac.at University of Vienna and Institute for Advanced Studies

Based on the books by Baltagi: Econometric Analysis of Panel Data and by Hsiao: Analysis of Panel Data Robert M. Kunst robert.kunst@univie.ac.at University of Vienna and Institute for Advanced Studies

LECTURE 13: TIME SERIES I

1 LECTURE 13: TIME SERIES I AUTOCORRELATION: Consider y = X + u where y is T 1, X is T K, is K 1 and u is T 1. We are using T and not N for sample size to emphasize that this is a time series. The natural

1 LECTURE 13: TIME SERIES I AUTOCORRELATION: Consider y = X + u where y is T 1, X is T K, is K 1 and u is T 1. We are using T and not N for sample size to emphasize that this is a time series. The natural

Consider the trend-cycle decomposition of a time series y t

1 Unit Root Tests Consider the trend-cycle decomposition of a time series y t y t = TD t + TS t + C t = TD t + Z t The basic issue in unit root testing is to determine if TS t = 0. Two classes of tests,

1 Unit Root Tests Consider the trend-cycle decomposition of a time series y t y t = TD t + TS t + C t = TD t + Z t The basic issue in unit root testing is to determine if TS t = 0. Two classes of tests,

Questions and Answers on Unit Roots, Cointegration, VARs and VECMs

Questions and Answers on Unit Roots, Cointegration, VARs and VECMs L. Magee Winter, 2012 1. Let ɛ t, t = 1,..., T be a series of independent draws from a N[0,1] distribution. Let w t, t = 1,..., T, be

Questions and Answers on Unit Roots, Cointegration, VARs and VECMs L. Magee Winter, 2012 1. Let ɛ t, t = 1,..., T be a series of independent draws from a N[0,1] distribution. Let w t, t = 1,..., T, be

Cointegration and the joint con rmation hypothesis

Cointegration and the joint con rmation hypothesis VASCO J. GABRIEL Department of Economics, Birkbeck College, UK University of Minho, Portugal October 2001 Abstract Recent papers by Charemza and Syczewska

Cointegration and the joint con rmation hypothesis VASCO J. GABRIEL Department of Economics, Birkbeck College, UK University of Minho, Portugal October 2001 Abstract Recent papers by Charemza and Syczewska

Stationarity and cointegration tests: Comparison of Engle - Granger and Johansen methodologies

MPRA Munich Personal RePEc Archive Stationarity and cointegration tests: Comparison of Engle - Granger and Johansen methodologies Faik Bilgili Erciyes University, Faculty of Economics and Administrative

MPRA Munich Personal RePEc Archive Stationarity and cointegration tests: Comparison of Engle - Granger and Johansen methodologies Faik Bilgili Erciyes University, Faculty of Economics and Administrative

DEPARTMENT OF ECONOMICS AND FINANCE COLLEGE OF BUSINESS AND ECONOMICS UNIVERSITY OF CANTERBURY CHRISTCHURCH, NEW ZEALAND

DEPARTMENT OF ECONOMICS AND FINANCE COLLEGE OF BUSINESS AND ECONOMICS UNIVERSITY OF CANTERBURY CHRISTCHURCH, NEW ZEALAND Testing For Unit Roots With Cointegrated Data NOTE: This paper is a revision of

DEPARTMENT OF ECONOMICS AND FINANCE COLLEGE OF BUSINESS AND ECONOMICS UNIVERSITY OF CANTERBURY CHRISTCHURCH, NEW ZEALAND Testing For Unit Roots With Cointegrated Data NOTE: This paper is a revision of

An Improved Panel Unit Root Test Using GLS-Detrending

An Improved Panel Unit Root Test Using GLS-Detrending Claude Lopez 1 University of Cincinnati August 2004 This paper o ers a panel extension of the unit root test proposed by Elliott, Rothenberg and Stock

An Improved Panel Unit Root Test Using GLS-Detrending Claude Lopez 1 University of Cincinnati August 2004 This paper o ers a panel extension of the unit root test proposed by Elliott, Rothenberg and Stock

Regression with random walks and Cointegration. Spurious Regression

Regression with random walks and Cointegration Spurious Regression Generally speaking (an exception will follow) it s a really really bad idea to regress one random walk process on another. That is, if

Regression with random walks and Cointegration Spurious Regression Generally speaking (an exception will follow) it s a really really bad idea to regress one random walk process on another. That is, if

7 Introduction to Time Series

Econ 495 - Econometric Review 1 7 Introduction to Time Series 7.1 Time Series vs. Cross-Sectional Data Time series data has a temporal ordering, unlike cross-section data, we will need to changes some

Econ 495 - Econometric Review 1 7 Introduction to Time Series 7.1 Time Series vs. Cross-Sectional Data Time series data has a temporal ordering, unlike cross-section data, we will need to changes some

Trends and Unit Roots in Greek Real Money Supply, Real GDP and Nominal Interest Rate

European Research Studies Volume V, Issue (3-4), 00, pp. 5-43 Trends and Unit Roots in Greek Real Money Supply, Real GDP and Nominal Interest Rate Karpetis Christos & Varelas Erotokritos * Abstract This

European Research Studies Volume V, Issue (3-4), 00, pp. 5-43 Trends and Unit Roots in Greek Real Money Supply, Real GDP and Nominal Interest Rate Karpetis Christos & Varelas Erotokritos * Abstract This

Forecasting and Estimation

February 3, 2009 Forecasting I Very frequently the goal of estimating time series is to provide forecasts of future values. This typically means you treat the data di erently than if you were simply tting

February 3, 2009 Forecasting I Very frequently the goal of estimating time series is to provide forecasts of future values. This typically means you treat the data di erently than if you were simply tting

It is easily seen that in general a linear combination of y t and x t is I(1). However, in particular cases, it can be I(0), i.e. stationary.

. However, in particular cases, it can be I(0), i.e. stationary.") 6. COINTEGRATION 1 1 Cointegration 1.1 Definitions I(1) variables. z t = (y t x t ) is I(1) (integrated of order 1) if it is not stationary but its first difference z t is stationary. It is easily seen

6. COINTEGRATION 1 1 Cointegration 1.1 Definitions I(1) variables. z t = (y t x t ) is I(1) (integrated of order 1) if it is not stationary but its first difference z t is stationary. It is easily seen

7 Introduction to Time Series Time Series vs. Cross-Sectional Data Detrending Time Series... 15

Econ 495 - Econometric Review 1 Contents 7 Introduction to Time Series 3 7.1 Time Series vs. Cross-Sectional Data............ 3 7.2 Detrending Time Series................... 15 7.3 Types of Stochastic

Econ 495 - Econometric Review 1 Contents 7 Introduction to Time Series 3 7.1 Time Series vs. Cross-Sectional Data............ 3 7.2 Detrending Time Series................... 15 7.3 Types of Stochastic

1 Quantitative Techniques in Practice

1 Quantitative Techniques in Practice 1.1 Lecture 2: Stationarity, spurious regression, etc. 1.1.1 Overview In the rst part we shall look at some issues in time series economics. In the second part we

1 Quantitative Techniques in Practice 1.1 Lecture 2: Stationarity, spurious regression, etc. 1.1.1 Overview In the rst part we shall look at some issues in time series economics. In the second part we

Finite-sample critical values of the AugmentedDickey-Fuller statistic: The role of lag order

Finite-sample critical values of the AugmentedDickey-Fuller statistic: The role of lag order Abstract The lag order dependence of nite-sample Augmented Dickey-Fuller (ADF) critical values is examined.

Finite-sample critical values of the AugmentedDickey-Fuller statistic: The role of lag order Abstract The lag order dependence of nite-sample Augmented Dickey-Fuller (ADF) critical values is examined.

Econometrics I: Univariate Time Series Econometrics (1)

") Econometrics I: Dipartimento di Economia Politica e Metodi Quantitativi University of Pavia Overview of the Lecture 1 st EViews Session VI: Some Theoretical Premises 2 Overview of the Lecture 1 st EViews

Econometrics I: Dipartimento di Economia Politica e Metodi Quantitativi University of Pavia Overview of the Lecture 1 st EViews Session VI: Some Theoretical Premises 2 Overview of the Lecture 1 st EViews

The Number of Bootstrap Replicates in Bootstrap Dickey-Fuller Unit Root Tests

Working Paper 2013:8 Department of Statistics The Number of Bootstrap Replicates in Bootstrap Dickey-Fuller Unit Root Tests Jianxin Wei Working Paper 2013:8 June 2013 Department of Statistics Uppsala

Working Paper 2013:8 Department of Statistics The Number of Bootstrap Replicates in Bootstrap Dickey-Fuller Unit Root Tests Jianxin Wei Working Paper 2013:8 June 2013 Department of Statistics Uppsala

Groupe de Recherche en Économie et Développement International. Cahier de recherche / Working Paper 08-17

Groupe de Recherche en Économie et Développement International Cahier de recherche / Working Paper 08-17 Modified Fast Double Sieve Bootstraps for ADF Tests Patrick Richard Modified Fast Double Sieve Bootstraps

Groupe de Recherche en Économie et Développement International Cahier de recherche / Working Paper 08-17 Modified Fast Double Sieve Bootstraps for ADF Tests Patrick Richard Modified Fast Double Sieve Bootstraps

Time Series Methods. Sanjaya Desilva

Time Series Methods Sanjaya Desilva 1 Dynamic Models In estimating time series models, sometimes we need to explicitly model the temporal relationships between variables, i.e. does X affect Y in the same

Time Series Methods Sanjaya Desilva 1 Dynamic Models In estimating time series models, sometimes we need to explicitly model the temporal relationships between variables, i.e. does X affect Y in the same

ECON 4160, Spring term Lecture 12

ECON 4160, Spring term 2013. Lecture 12 Non-stationarity and co-integration 2/2 Ragnar Nymoen Department of Economics 13 Nov 2013 1 / 53 Introduction I So far we have considered: Stationary VAR, with deterministic

ECON 4160, Spring term 2013. Lecture 12 Non-stationarity and co-integration 2/2 Ragnar Nymoen Department of Economics 13 Nov 2013 1 / 53 Introduction I So far we have considered: Stationary VAR, with deterministic

CHAPTER 21: TIME SERIES ECONOMETRICS: SOME BASIC CONCEPTS

CHAPTER 21: TIME SERIES ECONOMETRICS: SOME BASIC CONCEPTS 21.1 A stochastic process is said to be weakly stationary if its mean and variance are constant over time and if the value of the covariance between

CHAPTER 21: TIME SERIES ECONOMETRICS: SOME BASIC CONCEPTS 21.1 A stochastic process is said to be weakly stationary if its mean and variance are constant over time and if the value of the covariance between

The Seasonal KPSS Test When Neglecting Seasonal Dummies: A Monte Carlo analysis. Ghassen El Montasser, Talel Boufateh, Fakhri Issaoui

EERI Economics and Econometrics Research Institute The Seasonal KPSS Test When Neglecting Seasonal Dummies: A Monte Carlo analysis Ghassen El Montasser, Talel Boufateh, Fakhri Issaoui EERI Research Paper

EERI Economics and Econometrics Research Institute The Seasonal KPSS Test When Neglecting Seasonal Dummies: A Monte Carlo analysis Ghassen El Montasser, Talel Boufateh, Fakhri Issaoui EERI Research Paper

Circle the single best answer for each multiple choice question. Your choice should be made clearly.

TEST #1 STA 4853 March 6, 2017 Name: Please read the following directions. DO NOT TURN THE PAGE UNTIL INSTRUCTED TO DO SO Directions This exam is closed book and closed notes. There are 32 multiple choice

TEST #1 STA 4853 March 6, 2017 Name: Please read the following directions. DO NOT TURN THE PAGE UNTIL INSTRUCTED TO DO SO Directions This exam is closed book and closed notes. There are 32 multiple choice

Autoregressive Moving Average (ARMA) Models and their Practical Applications

Models and their Practical Applications") Autoregressive Moving Average (ARMA) Models and their Practical Applications Massimo Guidolin February 2018 1 Essential Concepts in Time Series Analysis 1.1 Time Series and Their Properties Time series:

Autoregressive Moving Average (ARMA) Models and their Practical Applications Massimo Guidolin February 2018 1 Essential Concepts in Time Series Analysis 1.1 Time Series and Their Properties Time series:

MEI Exam Review. June 7, 2002

MEI Exam Review June 7, 2002 1 Final Exam Revision Notes 1.1 Random Rules and Formulas Linear transformations of random variables. f y (Y ) = f x (X) dx. dg Inverse Proof. (AB)(AB) 1 = I. (B 1 A 1 )(AB)(AB)

MEI Exam Review June 7, 2002 1 Final Exam Revision Notes 1.1 Random Rules and Formulas Linear transformations of random variables. f y (Y ) = f x (X) dx. dg Inverse Proof. (AB)(AB) 1 = I. (B 1 A 1 )(AB)(AB)

Nonstationary Panels

Nonstationary Panels Based on chapters 12.4, 12.5, and 12.6 of Baltagi, B. (2005): Econometric Analysis of Panel Data, 3rd edition. Chichester, John Wiley & Sons. June 3, 2009 Agenda 1 Spurious Regressions

Nonstationary Panels Based on chapters 12.4, 12.5, and 12.6 of Baltagi, B. (2005): Econometric Analysis of Panel Data, 3rd edition. Chichester, John Wiley & Sons. June 3, 2009 Agenda 1 Spurious Regressions

EASTERN MEDITERRANEAN UNIVERSITY ECON 604, FALL 2007 DEPARTMENT OF ECONOMICS MEHMET BALCILAR ARIMA MODELS: IDENTIFICATION

ARIMA MODELS: IDENTIFICATION A. Autocorrelations and Partial Autocorrelations 1. Summary of What We Know So Far: a) Series y t is to be modeled by Box-Jenkins methods. The first step was to convert y t

ARIMA MODELS: IDENTIFICATION A. Autocorrelations and Partial Autocorrelations 1. Summary of What We Know So Far: a) Series y t is to be modeled by Box-Jenkins methods. The first step was to convert y t

Inflation Revisited: New Evidence from Modified Unit Root Tests

1 Inflation Revisited: New Evidence from Modified Unit Root Tests Walter Enders and Yu Liu * University of Alabama in Tuscaloosa and University of Texas at El Paso Abstract: We propose a simple modification

1 Inflation Revisited: New Evidence from Modified Unit Root Tests Walter Enders and Yu Liu * University of Alabama in Tuscaloosa and University of Texas at El Paso Abstract: We propose a simple modification

10. Time series regression and forecasting

10. Time series regression and forecasting Key feature of this section: Analysis of data on a single entity observed at multiple points in time (time series data) Typical research questions: What is the

10. Time series regression and forecasting Key feature of this section: Analysis of data on a single entity observed at multiple points in time (time series data) Typical research questions: What is the

Introductory Workshop on Time Series Analysis. Sara McLaughlin Mitchell Department of Political Science University of Iowa

Introductory Workshop on Time Series Analysis Sara McLaughlin Mitchell Department of Political Science University of Iowa Overview Properties of time series data Approaches to time series analysis Stationarity

Introductory Workshop on Time Series Analysis Sara McLaughlin Mitchell Department of Political Science University of Iowa Overview Properties of time series data Approaches to time series analysis Stationarity

On Perron s Unit Root Tests in the Presence. of an Innovation Variance Break

Applied Mathematical Sciences, Vol. 3, 2009, no. 27, 1341-1360 On Perron s Unit Root ests in the Presence of an Innovation Variance Break Amit Sen Department of Economics, 3800 Victory Parkway Xavier University,

Applied Mathematical Sciences, Vol. 3, 2009, no. 27, 1341-1360 On Perron s Unit Root ests in the Presence of an Innovation Variance Break Amit Sen Department of Economics, 3800 Victory Parkway Xavier University,

G. S. Maddala Kajal Lahiri. WILEY A John Wiley and Sons, Ltd., Publication

G. S. Maddala Kajal Lahiri WILEY A John Wiley and Sons, Ltd., Publication TEMT Foreword Preface to the Fourth Edition xvii xix Part I Introduction and the Linear Regression Model 1 CHAPTER 1 What is Econometrics?

G. S. Maddala Kajal Lahiri WILEY A John Wiley and Sons, Ltd., Publication TEMT Foreword Preface to the Fourth Edition xvii xix Part I Introduction and the Linear Regression Model 1 CHAPTER 1 What is Econometrics?

Joint hypothesis speci cation for unit root tests with. a structural break

Joint hypothesis speci cation for unit root tests with a structural break Josep Lluís Carrion-i-Silvestre Grup de Recerca AQR Departament d Econometria, Estadística i Economia Espanyola Universitat de

Joint hypothesis speci cation for unit root tests with a structural break Josep Lluís Carrion-i-Silvestre Grup de Recerca AQR Departament d Econometria, Estadística i Economia Espanyola Universitat de

Lecture 7: Dynamic panel models 2

Lecture 7: Dynamic panel models 2 Ragnar Nymoen Department of Economics, UiO 25 February 2010 Main issues and references The Arellano and Bond method for GMM estimation of dynamic panel data models A stepwise

Lecture 7: Dynamic panel models 2 Ragnar Nymoen Department of Economics, UiO 25 February 2010 Main issues and references The Arellano and Bond method for GMM estimation of dynamic panel data models A stepwise

Empirical Macroeconomics

Empirical Macroeconomics Francesco Franco Nova SBE April 5, 2016 Francesco Franco Empirical Macroeconomics 1/39 Growth and Fluctuations Supply and Demand Figure : US dynamics Francesco Franco Empirical

Empirical Macroeconomics Francesco Franco Nova SBE April 5, 2016 Francesco Franco Empirical Macroeconomics 1/39 Growth and Fluctuations Supply and Demand Figure : US dynamics Francesco Franco Empirical

ECONOMICS SERIES SWP 2009/11 A New Unit Root Tes t with Two Structural Breaks in Level and S lope at Unknown Time

Faculty of Business and Law School of Accounting, Economics and Finance ECONOMICS SERIES SWP 2009/11 A New Unit Root Test with Two Structural Breaks in Level and Slope at Unknown Time Paresh Kumar Narayan

Faculty of Business and Law School of Accounting, Economics and Finance ECONOMICS SERIES SWP 2009/11 A New Unit Root Test with Two Structural Breaks in Level and Slope at Unknown Time Paresh Kumar Narayan

EC408 Topics in Applied Econometrics. B Fingleton, Dept of Economics, Strathclyde University

EC408 Topics in Applied Econometrics B Fingleton, Dept of Economics, Strathclyde University Applied Econometrics What is spurious regression? How do we check for stochastic trends? Cointegration and Error

EC408 Topics in Applied Econometrics B Fingleton, Dept of Economics, Strathclyde University Applied Econometrics What is spurious regression? How do we check for stochastic trends? Cointegration and Error

Convergence of prices and rates of in ation

Convergence of prices and rates of in ation Fabio Busetti, Silvia Fabiani y, Andrew Harvey z May 18, 2006 Abstract We consider how unit root and stationarity tests can be used to study the convergence

Convergence of prices and rates of in ation Fabio Busetti, Silvia Fabiani y, Andrew Harvey z May 18, 2006 Abstract We consider how unit root and stationarity tests can be used to study the convergence

This note discusses some central issues in the analysis of non-stationary time

NON-STATIONARY TIME SERIES AND UNIT ROOT TESTING Econometrics 2 LectureNote5 Heino Bohn Nielsen January 14, 2007 This note discusses some central issues in the analysis of non-stationary time series. We

NON-STATIONARY TIME SERIES AND UNIT ROOT TESTING Econometrics 2 LectureNote5 Heino Bohn Nielsen January 14, 2007 This note discusses some central issues in the analysis of non-stationary time series. We

ECON 4160, Lecture 11 and 12

ECON 4160, 2016. Lecture 11 and 12 Co-integration Ragnar Nymoen Department of Economics 9 November 2017 1 / 43 Introduction I So far we have considered: Stationary VAR ( no unit roots ) Standard inference

ECON 4160, 2016. Lecture 11 and 12 Co-integration Ragnar Nymoen Department of Economics 9 November 2017 1 / 43 Introduction I So far we have considered: Stationary VAR ( no unit roots ) Standard inference

When is a copula constant? A test for changing relationships

When is a copula constant? A test for changing relationships Fabio Busetti and Andrew Harvey Bank of Italy and University of Cambridge November 2007 usetti and Harvey (Bank of Italy and University of Cambridge)

When is a copula constant? A test for changing relationships Fabio Busetti and Andrew Harvey Bank of Italy and University of Cambridge November 2007 usetti and Harvey (Bank of Italy and University of Cambridge)

Problem Set 2: Box-Jenkins methodology

Problem Set : Box-Jenkins methodology 1) For an AR1) process we have: γ0) = σ ε 1 φ σ ε γ0) = 1 φ Hence, For a MA1) process, p lim R = φ γ0) = 1 + θ )σ ε σ ε 1 = γ0) 1 + θ Therefore, p lim R = 1 1 1 +

Problem Set : Box-Jenkins methodology 1) For an AR1) process we have: γ0) = σ ε 1 φ σ ε γ0) = 1 φ Hence, For a MA1) process, p lim R = φ γ0) = 1 + θ )σ ε σ ε 1 = γ0) 1 + θ Therefore, p lim R = 1 1 1 +

Univariate Unit Root Process (May 14, 2018)

") Ch. Univariate Unit Root Process (May 4, 8) Introduction Much conventional asymptotic theory for least-squares estimation (e.g. the standard proofs of consistency and asymptotic normality of OLS estimators)

Ch. Univariate Unit Root Process (May 4, 8) Introduction Much conventional asymptotic theory for least-squares estimation (e.g. the standard proofs of consistency and asymptotic normality of OLS estimators)

Non-Stationary Time Series, Cointegration, and Spurious Regression

Econometrics II Non-Stationary Time Series, Cointegration, and Spurious Regression Econometrics II Course Outline: Non-Stationary Time Series, Cointegration and Spurious Regression 1 Regression with Non-Stationarity

Econometrics II Non-Stationary Time Series, Cointegration, and Spurious Regression Econometrics II Course Outline: Non-Stationary Time Series, Cointegration and Spurious Regression 1 Regression with Non-Stationarity

Unit-Root Tests and the Burden of Proof

Unit-Root Tests and the Burden of Proof Robert A. Amano and Simon van Norden 1 International Department Bank of Canada Ottawa, Ontario K1A 0G9 First Draft: March 1992 This Revision: September 1992 Abstract

Unit-Root Tests and the Burden of Proof Robert A. Amano and Simon van Norden 1 International Department Bank of Canada Ottawa, Ontario K1A 0G9 First Draft: March 1992 This Revision: September 1992 Abstract

Ch 6. Model Specification. Time Series Analysis

We start to build ARIMA(p,d,q) models. The subjects include: 1 how to determine p, d, q for a given series (Chapter 6); 2 how to estimate the parameters (φ s and θ s) of a specific ARIMA(p,d,q) model (Chapter

We start to build ARIMA(p,d,q) models. The subjects include: 1 how to determine p, d, q for a given series (Chapter 6); 2 how to estimate the parameters (φ s and θ s) of a specific ARIMA(p,d,q) model (Chapter

Testing for non-stationarity

20 November, 2009 Overview The tests for investigating the non-stationary of a time series falls into four types: 1 Check the null that there is a unit root against stationarity. Within these, there are

20 November, 2009 Overview The tests for investigating the non-stationary of a time series falls into four types: 1 Check the null that there is a unit root against stationarity. Within these, there are