Heteroskedasticity in Time Series

|

|

|

- Gervase George

- 6 years ago

- Views:

Transcription

1 Heteroskedasticity in Time Series Figure: Time Series of Daily NYSE Returns. 206 / 285

2 Key Fact 1: Stock Returns are Approximately Serially Uncorrelated Figure: Correlogram of Daily Stock Market Returns. 207 / 285

3 Key Fact 2: Returns are Unconditionally Non-Gaussian Figure: Histogram and Statistics for Daily NYSE Returns. 208 / 285

4 Unconditional Volatility Measures Variance: σ 2 = E(r t µ) 2 (or standard deviation: σ) Mean Absolute Deviation: MAD = E r t µ Interquartile Range: IQR = 75% 25% Outlier probability: P r t µ > 5σ (for example) Tail index: γ s.t. P(r t > r) = k r γ Kurtosis: K = E(r µ) 4 /σ 4 p% Value at Risk (VaR p )): x s.t. P(r t < x) = p 209 / 285

5 Key Fact 3: Returns are Conditionally Heteroskedastic I Figure: Time Series of Daily Squared NYSE Returns 210 / 285

6 Key Fact 3: Returns are Conditionally Heteroskedastic II Figure: Correlogram of Daily Squared NYSE Returns. 211 / 285

7 Conditional Return Distributions f (r t ) vs. f (r t Ω t 1 ) Key 1: E(r t Ω t 1 ) Are returns conditional mean independent? Arguably yes. Returns are (arguably) approximately serially uncorrelated, and (arguably) approximately free of additional non-linear conditional mean dependence. 216 / 285

8 Conditional Return Distributions, Continued Key 2: var(r t Ω t 1 ) = E((r t µ) 2 Ω t 1 ) Are returns conditional variance independent? No way! Squared returns serially correlated, often with very slow decay. 217 / 285

9 Linear Models (e.g., AR(1)) r t = φr t 1 + ε t ε t iid(0, σ 2 ), φ < 1 Uncond. mean: E(r t ) = 0 (constant) Uncond. variance: E(r 2 t ) = σ 2 /(1 φ 2 ) (constant) Cond. mean: E(r t Ω t 1 ) = φr t 1 (varies) Cond. variance: E([r t E(r t Ω t 1 )] 2 Ω t 1 ) = σ 2 (constant) Conditional mean adapts, but conditional variance does not 218 / 285

10 ARCH(1) Process r t Ω t 1 N(0, h t ) h t = ω + αr 2 t 1 E(r t ) = 0 E(r 2 ω t ) = (1 α) E(r t Ω t 1 ) = 0 E([r t E(r t Ω t 1 )] 2 Ω t 1 ) = ω + αr 2 t / 285

11 GARCH(1,1) Process ( Generalized ARCH ) r t Ω t 1 N(0, h t ) h t = ω + αr 2 t 1 + βh t 1 E(r t 2 ) = E(r t ) = 0 ω (1 α β) E(r t Ω t 1 ) = 0 E([r t E(r t Ω t 1 )] 2 Ω t 1 ) = ω + αr 2 t 1 + βh t 1 Well-defined and covariance stationary if 0 < α < 1, 0 < β < 1, α + β < / 285

12 GARCH(1,1) and Exponential Smoothing Exponential smoothing recursion: ˆσ 2 t = λˆσ 2 t 1 + (1 λ)r 2 t = ˆσ 2 t = (1 λ) j λ j r 2 t j But in GARCH(1,1) we have: h t = ω + αr 2 t 1 + βh t 1 h t = ω 1 β + α β j 1 r 2 t j 221 / 285

13 Unified Theoretical Framework Volatility dynamics (of course, by construction) Volatility clustering produces unconditional leptokurtosis Temporal aggregation reduces the leptokurtosis 222 / 285

14 Tractable Empirical Framework L(θ; r 1,..., r T ) = f (r T Ω T 1 ; θ)f ((r T 1 Ω T 2 ; θ)..., where θ = (ω, α, β) If the conditional densities are Gaussian, f (r t Ω t 1 ; θ) = 1 ( h t (θ) 1/2 exp 1 r 2 ) t, 2π 2 h t (θ) t so ln L = const 1 ln h t (θ) 1 rt h t (θ) t 223 / 285

15 Variations on the GARCH Theme Explanatory variables in the variance equation: GARCH-X Fat-tailed conditional densities: t-garch Asymmetric response and the leverage effect: T-GARCH Regression with GARCH disturbances Time-varying risk premia: GARCH-M 224 / 285

16 Explanatory variables in the Variance Equation: GARCH-X h t = ω + αr 2 t 1 + βh t 1 + γz t where z is a positive explanatory variable 225 / 285

17 Fat-Tailed Conditional Densities: t-garch If r is conditionally Gaussian, then r t = h t N(0, 1) But often with high-frequency data, r t ht leptokurtic So take: r t = h t t d std(t d ) and treat d as another parameter to be estimated 226 / 285

18 Asymmetric Response and the Leverage Effect: T-GARCH Standard GARCH: h t = ω + αr 2 t 1 + βh t 1 T-GARCH: h t = ω + αr 2 t 1 + γr 2 t 1 D t 1 + βh t 1 D t = { 1 if rt < 0 0 otherwise positive return (good news): α effect on volatility negative return (bad news): α + γ effect on volatility γ 0: Asymetric news response γ > 0: Leverage effect 227 / 285

19 Regression with GARCH Disturbances y t = x tβ + ε t ε t Ω t 1 N(0, h t ) 228 / 285

20 Time-Varying Risk Premia: GARCH-M Standard GARCH regression model: y t = x tβ + ε t ε t Ω t 1 N(0, h t ) GARCH-M model is a special case: y t = x tβ + γh t + ε t ε t Ω t 1 N(0, h t ) 229 / 285

230 /")

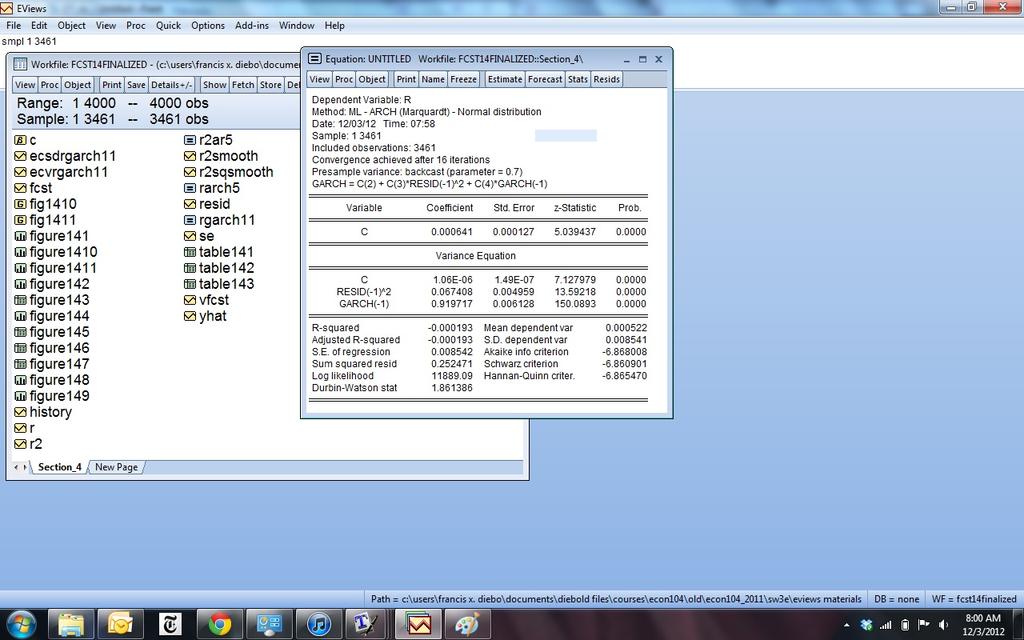

21 Back to Empirical Work Standard GARCH(1,1) 230 / 285

22 GARCH(1,1) 231 / 285

23 GARCH(1,1) 232 / 285

24 GARCH(1,1) Figure: Estimated Conditional Standard Deviation, Daily NYSE Returns. 233 / 285

25 GARCH(1,1) Figure: Conditional Standard Deviation, History and Forecast, Daily NYSE Returns. 234 / 285

")

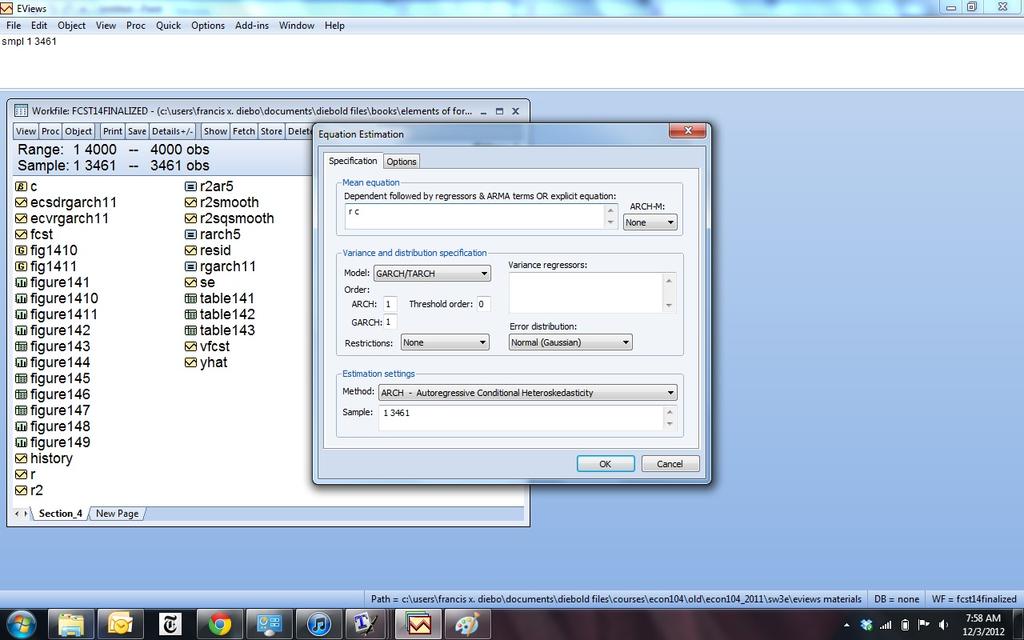

26 Fancy GARCH(1,1) 237 / 285

27 Fancy GARCH(1,1) Dependent Variable: R Method: ML - ARCH (Marquardt) - Student's t distribution Date: 04/10/12 Time: 13:48 Sample (adjusted): Included observations: 3460 after adjustments Convergence achieved after 19 iterations Presample variance: backcast (parameter = 0.7) GARCH = C(4) + C(5)*RESID(-1)^2 + C(6)*RESID(-1)^2*(RESID(-1)<0) + C(7)*GARCH(-1) Variable Coefficient Std. Error z-statistic C 1.28E R(-1) Variance Equation C 1.03E E RESID(-1)^ RESID(-1)^2*(RESID(- 1)<0) GARCH(-1) T-DIST. DOF / 285

28 Nonstationarity and Random Walks Random walk: y t = y t 1 + ε t ε t iid(0, σ 2 ) Just a simple special case of AR(1) φ = / 285

29 Recall Properties of AR(1) with φ < 1 Shocks ε t have persistent but not permanent effects y t = φ j ε t j (note φ j 0) j=0 Series y t varies but not too extremely var(y t ) = σ2 1 φ 2 (note var(y t ) < ) Autocorrelations ρ(τ) nonzero but decay to zero ρ(τ) = φ τ (note φ τ 0) 251 / 285

30 Properties of the Random Walk (AR(1) With φ = 1) Shocks have permanent effects t 1 y t = y 0 + j=0 ε t j Series is infinitely variable E(y t ) = y 0 var(y t ) = tσ 2 lim var(y t) = t Autocorrelations ρ(τ) do not decay ρ(τ) 1 (formally not defined) 252 / 285

31 Random Walk with Drift y t = δ + y t 1 + ε t ε t iid(0, σ 2 ) y t = tδ + y 0 + t i=1 ε i E(y t ) = y 0 + tδ var(y t ) = tσ 2 lim var(y t) = t 250 / 285

32 Forecasting a Linear Trend + Stationary AR(1) x t = a + bt + y t y t = φy t 1 + ε t ε t WN(0, σ 2 ) Optimal forecast: x T +h,t = a + b(t + h) + φ h y T Forecast reverts to trend 7 / 40

33 Forecasting a Random Walk with Drift x t = b + x t 1 + ε t ε t WN(0, σ 2 ) Optimal forecast: x T +h,t = bh + x T Forecast does not revert to trend 6 / 40

34 Stochastic Trend vs. Deterministic Trend 9 / 40

35 A Key Insight Regarding the Random Walk Level series y t is non-stationary (of course) Differenced series y t is stationary (indeed white noise)! y t = ε t A series is called I (d) if it is non-stationary in levels but is appropriately made stationary by differencing d times. Random walk is the key I (1) process. Other I (1) processes are similar. Why? 253 / 285

36 The Beveridge-Nelson Decomposition y t I (1) = y t = x t + z t x t = random walk z t = covariance stationary Hence the random walk is the key ingredient for all I (1) processes. The Beveridge-Nelson decomposition implies that shocks to any I (1) process have some permanent effect, as with a random walk. But the effects are not completely permanent, unless the process is a pure random walk. 254 / 285

37 I (1) Processes and Unit Roots Random walk is an I (1) AR(1) process: y t = y t 1 + ε t (1 L) }{{} y t = ε t deg 1 One (unit) root, L = 1 y t is standard covariance-stationary WN More general I (1) AR(p) process: Φ(L) }{{} y t = ε t deg p [Φ (L) (1 L) }{{}}{{} ]y t = ε t (deg p-1)(deg 1) p 1 stationary roots, one unit root y t is standard covariance stationary AR(p 1) 255 / 285

38 Some Language... Random walk with drift vs. stat. AR(1) around linear trend unit root vs. stationary root Difference stationary vs. trend stationary Stochastic trend vs. deterministic trend I (1) vs. I (0) 8 / 40

Volatility. Gerald P. Dwyer. February Clemson University

Volatility Gerald P. Dwyer Clemson University February 2016 Outline 1 Volatility Characteristics of Time Series Heteroskedasticity Simpler Estimation Strategies Exponentially Weighted Moving Average Use

Volatility Gerald P. Dwyer Clemson University February 2016 Outline 1 Volatility Characteristics of Time Series Heteroskedasticity Simpler Estimation Strategies Exponentially Weighted Moving Average Use

Introduction to ARMA and GARCH processes

Introduction to ARMA and GARCH processes Fulvio Corsi SNS Pisa 3 March 2010 Fulvio Corsi Introduction to ARMA () and GARCH processes SNS Pisa 3 March 2010 1 / 24 Stationarity Strict stationarity: (X 1,

Introduction to ARMA and GARCH processes Fulvio Corsi SNS Pisa 3 March 2010 Fulvio Corsi Introduction to ARMA () and GARCH processes SNS Pisa 3 March 2010 1 / 24 Stationarity Strict stationarity: (X 1,

Final Exam Financial Data Analysis at the University of Freiburg (Winter Semester 2008/2009) Friday, November 14, 2008,

Friday, November 14, 2008,") Professor Dr. Roman Liesenfeld Final Exam Financial Data Analysis at the University of Freiburg (Winter Semester 2008/2009) Friday, November 14, 2008, 10.00 11.30am 1 Part 1 (38 Points) Consider the following

Professor Dr. Roman Liesenfeld Final Exam Financial Data Analysis at the University of Freiburg (Winter Semester 2008/2009) Friday, November 14, 2008, 10.00 11.30am 1 Part 1 (38 Points) Consider the following

GARCH Models. Eduardo Rossi University of Pavia. December Rossi GARCH Financial Econometrics / 50

GARCH Models Eduardo Rossi University of Pavia December 013 Rossi GARCH Financial Econometrics - 013 1 / 50 Outline 1 Stylized Facts ARCH model: definition 3 GARCH model 4 EGARCH 5 Asymmetric Models 6

GARCH Models Eduardo Rossi University of Pavia December 013 Rossi GARCH Financial Econometrics - 013 1 / 50 Outline 1 Stylized Facts ARCH model: definition 3 GARCH model 4 EGARCH 5 Asymmetric Models 6

Romanian Economic and Business Review Vol. 3, No. 3 THE EVOLUTION OF SNP PETROM STOCK LIST - STUDY THROUGH AUTOREGRESSIVE MODELS

THE EVOLUTION OF SNP PETROM STOCK LIST - STUDY THROUGH AUTOREGRESSIVE MODELS Marian Zaharia, Ioana Zaheu, and Elena Roxana Stan Abstract Stock exchange market is one of the most dynamic and unpredictable

THE EVOLUTION OF SNP PETROM STOCK LIST - STUDY THROUGH AUTOREGRESSIVE MODELS Marian Zaharia, Ioana Zaheu, and Elena Roxana Stan Abstract Stock exchange market is one of the most dynamic and unpredictable

Prof. Dr. Roland Füss Lecture Series in Applied Econometrics Summer Term Introduction to Time Series Analysis

Introduction to Time Series Analysis 1 Contents: I. Basics of Time Series Analysis... 4 I.1 Stationarity... 5 I.2 Autocorrelation Function... 9 I.3 Partial Autocorrelation Function (PACF)... 14 I.4 Transformation

Introduction to Time Series Analysis 1 Contents: I. Basics of Time Series Analysis... 4 I.1 Stationarity... 5 I.2 Autocorrelation Function... 9 I.3 Partial Autocorrelation Function (PACF)... 14 I.4 Transformation

THE UNIVERSITY OF CHICAGO Graduate School of Business Business 41202, Spring Quarter 2003, Mr. Ruey S. Tsay

THE UNIVERSITY OF CHICAGO Graduate School of Business Business 41202, Spring Quarter 2003, Mr. Ruey S. Tsay Solutions to Homework Assignment #4 May 9, 2003 Each HW problem is 10 points throughout this

THE UNIVERSITY OF CHICAGO Graduate School of Business Business 41202, Spring Quarter 2003, Mr. Ruey S. Tsay Solutions to Homework Assignment #4 May 9, 2003 Each HW problem is 10 points throughout this

13. Estimation and Extensions in the ARCH model. MA6622, Ernesto Mordecki, CityU, HK, References for this Lecture:

13. Estimation and Extensions in the ARCH model MA6622, Ernesto Mordecki, CityU, HK, 2006. References for this Lecture: Robert F. Engle. GARCH 101: The Use of ARCH/GARCH Models in Applied Econometrics,

13. Estimation and Extensions in the ARCH model MA6622, Ernesto Mordecki, CityU, HK, 2006. References for this Lecture: Robert F. Engle. GARCH 101: The Use of ARCH/GARCH Models in Applied Econometrics,

Symmetric btw positive & negative prior returns. where c is referred to as risk premium, which is expected to be positive.

Advantages of GARCH model Simplicity Generates volatility clustering Heavy tails (high kurtosis) Weaknesses of GARCH model Symmetric btw positive & negative prior returns Restrictive Provides no explanation

Advantages of GARCH model Simplicity Generates volatility clustering Heavy tails (high kurtosis) Weaknesses of GARCH model Symmetric btw positive & negative prior returns Restrictive Provides no explanation

1 Linear Difference Equations

ARMA Handout Jialin Yu 1 Linear Difference Equations First order systems Let {ε t } t=1 denote an input sequence and {y t} t=1 sequence generated by denote an output y t = φy t 1 + ε t t = 1, 2,... with

ARMA Handout Jialin Yu 1 Linear Difference Equations First order systems Let {ε t } t=1 denote an input sequence and {y t} t=1 sequence generated by denote an output y t = φy t 1 + ε t t = 1, 2,... with

Week 5 Quantitative Analysis of Financial Markets Characterizing Cycles

Week 5 Quantitative Analysis of Financial Markets Characterizing Cycles Christopher Ting http://www.mysmu.edu/faculty/christophert/ Christopher Ting : christopherting@smu.edu.sg : 6828 0364 : LKCSB 5036

Week 5 Quantitative Analysis of Financial Markets Characterizing Cycles Christopher Ting http://www.mysmu.edu/faculty/christophert/ Christopher Ting : christopherting@smu.edu.sg : 6828 0364 : LKCSB 5036

Nonstationary Time Series:

Nonstationary Time Series: Unit Roots Egon Zakrajšek Division of Monetary Affairs Federal Reserve Board Summer School in Financial Mathematics Faculty of Mathematics & Physics University of Ljubljana September

Nonstationary Time Series: Unit Roots Egon Zakrajšek Division of Monetary Affairs Federal Reserve Board Summer School in Financial Mathematics Faculty of Mathematics & Physics University of Ljubljana September

Lecture 2: Univariate Time Series

Lecture 2: Univariate Time Series Analysis: Conditional and Unconditional Densities, Stationarity, ARMA Processes Prof. Massimo Guidolin 20192 Financial Econometrics Spring/Winter 2017 Overview Motivation:

Lecture 2: Univariate Time Series Analysis: Conditional and Unconditional Densities, Stationarity, ARMA Processes Prof. Massimo Guidolin 20192 Financial Econometrics Spring/Winter 2017 Overview Motivation:

Introduction to Stochastic processes

Università di Pavia Introduction to Stochastic processes Eduardo Rossi Stochastic Process Stochastic Process: A stochastic process is an ordered sequence of random variables defined on a probability space

Università di Pavia Introduction to Stochastic processes Eduardo Rossi Stochastic Process Stochastic Process: A stochastic process is an ordered sequence of random variables defined on a probability space

1 Class Organization. 2 Introduction

Time Series Analysis, Lecture 1, 2018 1 1 Class Organization Course Description Prerequisite Homework and Grading Readings and Lecture Notes Course Website: http://www.nanlifinance.org/teaching.html wechat

Time Series Analysis, Lecture 1, 2018 1 1 Class Organization Course Description Prerequisite Homework and Grading Readings and Lecture Notes Course Website: http://www.nanlifinance.org/teaching.html wechat

Stochastic Processes

Stochastic Processes Stochastic Process Non Formal Definition: Non formal: A stochastic process (random process) is the opposite of a deterministic process such as one defined by a differential equation.

Stochastic Processes Stochastic Process Non Formal Definition: Non formal: A stochastic process (random process) is the opposite of a deterministic process such as one defined by a differential equation.

Class 1: Stationary Time Series Analysis

Class 1: Stationary Time Series Analysis Macroeconometrics - Fall 2009 Jacek Suda, BdF and PSE February 28, 2011 Outline Outline: 1 Covariance-Stationary Processes 2 Wold Decomposition Theorem 3 ARMA Models

Class 1: Stationary Time Series Analysis Macroeconometrics - Fall 2009 Jacek Suda, BdF and PSE February 28, 2011 Outline Outline: 1 Covariance-Stationary Processes 2 Wold Decomposition Theorem 3 ARMA Models

in the time series. The relation between y and x is contemporaneous.

9 Regression with Time Series 9.1 Some Basic Concepts Static Models (1) y t = β 0 + β 1 x t + u t t = 1, 2,..., T, where T is the number of observation in the time series. The relation between y and x

9 Regression with Time Series 9.1 Some Basic Concepts Static Models (1) y t = β 0 + β 1 x t + u t t = 1, 2,..., T, where T is the number of observation in the time series. The relation between y and x

Univariate linear models

Univariate linear models The specification process of an univariate ARIMA model is based on the theoretical properties of the different processes and it is also important the observation and interpretation

Univariate linear models The specification process of an univariate ARIMA model is based on the theoretical properties of the different processes and it is also important the observation and interpretation

ECON/FIN 250: Forecasting in Finance and Economics: Section 7: Unit Roots & Dickey-Fuller Tests

ECON/FIN 250: Forecasting in Finance and Economics: Section 7: Unit Roots & Dickey-Fuller Tests Patrick Herb Brandeis University Spring 2016 Patrick Herb (Brandeis University) Unit Root Tests ECON/FIN

ECON/FIN 250: Forecasting in Finance and Economics: Section 7: Unit Roots & Dickey-Fuller Tests Patrick Herb Brandeis University Spring 2016 Patrick Herb (Brandeis University) Unit Root Tests ECON/FIN

1. Fundamental concepts

. Fundamental concepts A time series is a sequence of data points, measured typically at successive times spaced at uniform intervals. Time series are used in such fields as statistics, signal processing

. Fundamental concepts A time series is a sequence of data points, measured typically at successive times spaced at uniform intervals. Time series are used in such fields as statistics, signal processing

Econ 423 Lecture Notes: Additional Topics in Time Series 1

Econ 423 Lecture Notes: Additional Topics in Time Series 1 John C. Chao April 25, 2017 1 These notes are based in large part on Chapter 16 of Stock and Watson (2011). They are for instructional purposes

Econ 423 Lecture Notes: Additional Topics in Time Series 1 John C. Chao April 25, 2017 1 These notes are based in large part on Chapter 16 of Stock and Watson (2011). They are for instructional purposes

Multivariate Time Series: VAR(p) Processes and Models

Processes and Models") Multivariate Time Series: VAR(p) Processes and Models A VAR(p) model, for p > 0 is X t = φ 0 + Φ 1 X t 1 + + Φ p X t p + A t, where X t, φ 0, and X t i are k-vectors, Φ 1,..., Φ p are k k matrices, with

Multivariate Time Series: VAR(p) Processes and Models A VAR(p) model, for p > 0 is X t = φ 0 + Φ 1 X t 1 + + Φ p X t p + A t, where X t, φ 0, and X t i are k-vectors, Φ 1,..., Φ p are k k matrices, with

Financial Time Series Analysis: Part II

Department of Mathematics and Statistics, University of Vaasa, Finland Spring 2017 1 Unit root Deterministic trend Stochastic trend Testing for unit root ADF-test (Augmented Dickey-Fuller test) Testing

Department of Mathematics and Statistics, University of Vaasa, Finland Spring 2017 1 Unit root Deterministic trend Stochastic trend Testing for unit root ADF-test (Augmented Dickey-Fuller test) Testing

Lecture 6a: Unit Root and ARIMA Models

Lecture 6a: Unit Root and ARIMA Models 1 2 Big Picture A time series is non-stationary if it contains a unit root unit root nonstationary The reverse is not true. For example, y t = cos(t) + u t has no

Lecture 6a: Unit Root and ARIMA Models 1 2 Big Picture A time series is non-stationary if it contains a unit root unit root nonstationary The reverse is not true. For example, y t = cos(t) + u t has no

Lecture 6: Univariate Volatility Modelling: ARCH and GARCH Models

Lecture 6: Univariate Volatility Modelling: ARCH and GARCH Models Prof. Massimo Guidolin 019 Financial Econometrics Winter/Spring 018 Overview ARCH models and their limitations Generalized ARCH models

Lecture 6: Univariate Volatility Modelling: ARCH and GARCH Models Prof. Massimo Guidolin 019 Financial Econometrics Winter/Spring 018 Overview ARCH models and their limitations Generalized ARCH models

Econ 424 Time Series Concepts

Econ 424 Time Series Concepts Eric Zivot January 20 2015 Time Series Processes Stochastic (Random) Process { 1 2 +1 } = { } = sequence of random variables indexed by time Observed time series of length

Econ 424 Time Series Concepts Eric Zivot January 20 2015 Time Series Processes Stochastic (Random) Process { 1 2 +1 } = { } = sequence of random variables indexed by time Observed time series of length

Permanent Income Hypothesis (PIH) Instructor: Dmytro Hryshko

Instructor: Dmytro Hryshko") Permanent Income Hypothesis (PIH) Instructor: Dmytro Hryshko 1 / 36 The PIH Utility function is quadratic, u(c t ) = 1 2 (c t c) 2 ; borrowing/saving is allowed using only the risk-free bond; β(1 + r)

Permanent Income Hypothesis (PIH) Instructor: Dmytro Hryshko 1 / 36 The PIH Utility function is quadratic, u(c t ) = 1 2 (c t c) 2 ; borrowing/saving is allowed using only the risk-free bond; β(1 + r)

ECON3327: Financial Econometrics, Spring 2016

ECON3327: Financial Econometrics, Spring 2016 Wooldridge, Introductory Econometrics (5th ed, 2012) Chapter 11: OLS with time series data Stationary and weakly dependent time series The notion of a stationary

ECON3327: Financial Econometrics, Spring 2016 Wooldridge, Introductory Econometrics (5th ed, 2012) Chapter 11: OLS with time series data Stationary and weakly dependent time series The notion of a stationary

Problem Set 2: Box-Jenkins methodology

Problem Set : Box-Jenkins methodology 1) For an AR1) process we have: γ0) = σ ε 1 φ σ ε γ0) = 1 φ Hence, For a MA1) process, p lim R = φ γ0) = 1 + θ )σ ε σ ε 1 = γ0) 1 + θ Therefore, p lim R = 1 1 1 +

Problem Set : Box-Jenkins methodology 1) For an AR1) process we have: γ0) = σ ε 1 φ σ ε γ0) = 1 φ Hence, For a MA1) process, p lim R = φ γ0) = 1 + θ )σ ε σ ε 1 = γ0) 1 + θ Therefore, p lim R = 1 1 1 +

GARCH Models Estimation and Inference. Eduardo Rossi University of Pavia

GARCH Models Estimation and Inference Eduardo Rossi University of Pavia Likelihood function The procedure most often used in estimating θ 0 in ARCH models involves the maximization of a likelihood function

GARCH Models Estimation and Inference Eduardo Rossi University of Pavia Likelihood function The procedure most often used in estimating θ 0 in ARCH models involves the maximization of a likelihood function

6. The econometrics of Financial Markets: Empirical Analysis of Financial Time Series. MA6622, Ernesto Mordecki, CityU, HK, 2006.

6. The econometrics of Financial Markets: Empirical Analysis of Financial Time Series MA6622, Ernesto Mordecki, CityU, HK, 2006. References for Lecture 5: Quantitative Risk Management. A. McNeil, R. Frey,

6. The econometrics of Financial Markets: Empirical Analysis of Financial Time Series MA6622, Ernesto Mordecki, CityU, HK, 2006. References for Lecture 5: Quantitative Risk Management. A. McNeil, R. Frey,

Multivariate GARCH models.

Multivariate GARCH models. Financial market volatility moves together over time across assets and markets. Recognizing this commonality through a multivariate modeling framework leads to obvious gains

Multivariate GARCH models. Financial market volatility moves together over time across assets and markets. Recognizing this commonality through a multivariate modeling framework leads to obvious gains

Trend-Cycle Decompositions

Trend-Cycle Decompositions Eric Zivot April 22, 2005 1 Introduction A convenient way of representing an economic time series y t is through the so-called trend-cycle decomposition y t = TD t + Z t (1)

Trend-Cycle Decompositions Eric Zivot April 22, 2005 1 Introduction A convenient way of representing an economic time series y t is through the so-called trend-cycle decomposition y t = TD t + Z t (1)

TIME SERIES ANALYSIS. Forecasting and Control. Wiley. Fifth Edition GWILYM M. JENKINS GEORGE E. P. BOX GREGORY C. REINSEL GRETA M.

TIME SERIES ANALYSIS Forecasting and Control Fifth Edition GEORGE E. P. BOX GWILYM M. JENKINS GREGORY C. REINSEL GRETA M. LJUNG Wiley CONTENTS PREFACE TO THE FIFTH EDITION PREFACE TO THE FOURTH EDITION

TIME SERIES ANALYSIS Forecasting and Control Fifth Edition GEORGE E. P. BOX GWILYM M. JENKINS GREGORY C. REINSEL GRETA M. LJUNG Wiley CONTENTS PREFACE TO THE FIFTH EDITION PREFACE TO THE FOURTH EDITION

Topic 4 Unit Roots. Gerald P. Dwyer. February Clemson University

Topic 4 Unit Roots Gerald P. Dwyer Clemson University February 2016 Outline 1 Unit Roots Introduction Trend and Difference Stationary Autocorrelations of Series That Have Deterministic or Stochastic Trends

Topic 4 Unit Roots Gerald P. Dwyer Clemson University February 2016 Outline 1 Unit Roots Introduction Trend and Difference Stationary Autocorrelations of Series That Have Deterministic or Stochastic Trends

Sample Exam Questions for Econometrics

Sample Exam Questions for Econometrics 1 a) What is meant by marginalisation and conditioning in the process of model reduction within the dynamic modelling tradition? (30%) b) Having derived a model for

Sample Exam Questions for Econometrics 1 a) What is meant by marginalisation and conditioning in the process of model reduction within the dynamic modelling tradition? (30%) b) Having derived a model for

Chapter 2: Unit Roots

Chapter 2: Unit Roots 1 Contents: Lehrstuhl für Department Empirische of Wirtschaftsforschung Empirical Research and undeconometrics II. Unit Roots... 3 II.1 Integration Level... 3 II.2 Nonstationarity

Chapter 2: Unit Roots 1 Contents: Lehrstuhl für Department Empirische of Wirtschaftsforschung Empirical Research and undeconometrics II. Unit Roots... 3 II.1 Integration Level... 3 II.2 Nonstationarity

Time Series Econometrics 4 Vijayamohanan Pillai N

Time Series Econometrics 4 Vijayamohanan Pillai N Vijayamohan: CDS MPhil: Time Series 5 1 Autoregressive Moving Average Process: ARMA(p, q) Vijayamohan: CDS MPhil: Time Series 5 2 1 Autoregressive Moving

Time Series Econometrics 4 Vijayamohanan Pillai N Vijayamohan: CDS MPhil: Time Series 5 1 Autoregressive Moving Average Process: ARMA(p, q) Vijayamohan: CDS MPhil: Time Series 5 2 1 Autoregressive Moving

Econ 427, Spring Problem Set 3 suggested answers (with minor corrections) Ch 6. Problems and Complements:

Ch 6. Problems and Complements:") Econ 427, Spring 2010 Problem Set 3 suggested answers (with minor corrections) Ch 6. Problems and Complements: 1. (page 132) In each case, the idea is to write these out in general form (without the lag

Econ 427, Spring 2010 Problem Set 3 suggested answers (with minor corrections) Ch 6. Problems and Complements: 1. (page 132) In each case, the idea is to write these out in general form (without the lag

Example 2.1: Consider the following daily close-toclose SP500 values [January 3, 2000 to March 27, 2009] SP500 Daily Returns and Index Values

![Example 2.1: Consider the following daily close-toclose SP500 values [January 3, 2000 to March 27, 2009] SP500 Daily Returns and Index Values](/thumbs/89/100587521.jpg "Example 2.1: Consider the following daily close-toclose SP500 values [January 3, 2000 to March 27, 2009] SP500 Daily Returns and Index Values") 2. Volatility Models 2.1 Background Example 2.1: Consider the following daily close-toclose SP500 values [January 3, 2000 to March 27, 2009] SP500 Daily Returns and Index Values -10-5 0 5 10 Return (%)

2. Volatility Models 2.1 Background Example 2.1: Consider the following daily close-toclose SP500 values [January 3, 2000 to March 27, 2009] SP500 Daily Returns and Index Values -10-5 0 5 10 Return (%)

Empirical Market Microstructure Analysis (EMMA)

") Empirical Market Microstructure Analysis (EMMA) Lecture 3: Statistical Building Blocks and Econometric Basics Prof. Dr. Michael Stein michael.stein@vwl.uni-freiburg.de Albert-Ludwigs-University of Freiburg

Empirical Market Microstructure Analysis (EMMA) Lecture 3: Statistical Building Blocks and Econometric Basics Prof. Dr. Michael Stein michael.stein@vwl.uni-freiburg.de Albert-Ludwigs-University of Freiburg

ECON 616: Lecture 1: Time Series Basics

ECON 616: Lecture 1: Time Series Basics ED HERBST August 30, 2017 References Overview: Chapters 1-3 from Hamilton (1994). Technical Details: Chapters 2-3 from Brockwell and Davis (1987). Intuition: Chapters

ECON 616: Lecture 1: Time Series Basics ED HERBST August 30, 2017 References Overview: Chapters 1-3 from Hamilton (1994). Technical Details: Chapters 2-3 from Brockwell and Davis (1987). Intuition: Chapters

Econometric Forecasting

Robert M. Kunst robert.kunst@univie.ac.at University of Vienna and Institute for Advanced Studies Vienna October 1, 2014 Outline Introduction Model-free extrapolation Univariate time-series models Trend

Robert M. Kunst robert.kunst@univie.ac.at University of Vienna and Institute for Advanced Studies Vienna October 1, 2014 Outline Introduction Model-free extrapolation Univariate time-series models Trend

Time Series 4. Robert Almgren. Oct. 5, 2009

Time Series 4 Robert Almgren Oct. 5, 2009 1 Nonstationarity How should you model a process that has drift? ARMA models are intrinsically stationary, that is, they are mean-reverting: when the value of

Time Series 4 Robert Almgren Oct. 5, 2009 1 Nonstationarity How should you model a process that has drift? ARMA models are intrinsically stationary, that is, they are mean-reverting: when the value of

Non-Stationary Time Series and Unit Root Testing

Econometrics II Non-Stationary Time Series and Unit Root Testing Morten Nyboe Tabor Course Outline: Non-Stationary Time Series and Unit Root Testing 1 Stationarity and Deviation from Stationarity Trend-Stationarity

Econometrics II Non-Stationary Time Series and Unit Root Testing Morten Nyboe Tabor Course Outline: Non-Stationary Time Series and Unit Root Testing 1 Stationarity and Deviation from Stationarity Trend-Stationarity

Forecasting. Francis X. Diebold University of Pennsylvania. August 11, / 323

Forecasting Francis X. Diebold University of Pennsylvania August 11, 2015 1 / 323 Copyright c 2013 onward, by Francis X. Diebold. These materials are freely available for your use, but be warned: they

Forecasting Francis X. Diebold University of Pennsylvania August 11, 2015 1 / 323 Copyright c 2013 onward, by Francis X. Diebold. These materials are freely available for your use, but be warned: they

Financial Econometrics

Financial Econometrics Topic 5: Modelling Volatility Lecturer: Nico Katzke nicokatzke@sun.ac.za Department of Economics Texts used The notes and code in R were created using many references. Intuitively,

Financial Econometrics Topic 5: Modelling Volatility Lecturer: Nico Katzke nicokatzke@sun.ac.za Department of Economics Texts used The notes and code in R were created using many references. Intuitively,

GARCH processes probabilistic properties (Part 1)

") GARCH processes probabilistic properties (Part 1) Alexander Lindner Centre of Mathematical Sciences Technical University of Munich D 85747 Garching Germany lindner@ma.tum.de http://www-m1.ma.tum.de/m4/pers/lindner/

GARCH processes probabilistic properties (Part 1) Alexander Lindner Centre of Mathematical Sciences Technical University of Munich D 85747 Garching Germany lindner@ma.tum.de http://www-m1.ma.tum.de/m4/pers/lindner/

Univariate Nonstationary Time Series 1

Univariate Nonstationary Time Series 1 Sebastian Fossati University of Alberta 1 These slides are based on Eric Zivot s time series notes available at: http://faculty.washington.edu/ezivot Introduction

Univariate Nonstationary Time Series 1 Sebastian Fossati University of Alberta 1 These slides are based on Eric Zivot s time series notes available at: http://faculty.washington.edu/ezivot Introduction

Non-Stationary Time Series and Unit Root Testing

Econometrics II Non-Stationary Time Series and Unit Root Testing Morten Nyboe Tabor Course Outline: Non-Stationary Time Series and Unit Root Testing 1 Stationarity and Deviation from Stationarity Trend-Stationarity

Econometrics II Non-Stationary Time Series and Unit Root Testing Morten Nyboe Tabor Course Outline: Non-Stationary Time Series and Unit Root Testing 1 Stationarity and Deviation from Stationarity Trend-Stationarity

Econometrics II Heij et al. Chapter 7.1

Chapter 7.1 p. 1/2 Econometrics II Heij et al. Chapter 7.1 Linear Time Series Models for Stationary data Marius Ooms Tinbergen Institute Amsterdam Chapter 7.1 p. 2/2 Program Introduction Modelling philosophy

Chapter 7.1 p. 1/2 Econometrics II Heij et al. Chapter 7.1 Linear Time Series Models for Stationary data Marius Ooms Tinbergen Institute Amsterdam Chapter 7.1 p. 2/2 Program Introduction Modelling philosophy

ECONOMETRIC REVIEWS, 5(1), (1986) MODELING THE PERSISTENCE OF CONDITIONAL VARIANCES: A COMMENT

, (1986) MODELING THE PERSISTENCE OF CONDITIONAL VARIANCES: A COMMENT") ECONOMETRIC REVIEWS, 5(1), 51-56 (1986) MODELING THE PERSISTENCE OF CONDITIONAL VARIANCES: A COMMENT Professors Engle and Bollerslev have delivered an excellent blend of "forest" and "trees"; their important

ECONOMETRIC REVIEWS, 5(1), 51-56 (1986) MODELING THE PERSISTENCE OF CONDITIONAL VARIANCES: A COMMENT Professors Engle and Bollerslev have delivered an excellent blend of "forest" and "trees"; their important

FORECASTING IN FINANCIAL MARKET USING MARKOV R MARKOV REGIME SWITCHING AND PRINCIPAL COMPONENT ANALYSIS.

FORECASTING IN FINANCIAL MARKET USING MARKOV REGIME SWITCHING AND PRINCIPAL COMPONENT ANALYSIS. September 13, 2012 1 2 3 4 5 Heteroskedasticity Model Multicollinearily 6 In Thai Outline การพยากรณ ในตลาดทางการเง

FORECASTING IN FINANCIAL MARKET USING MARKOV REGIME SWITCHING AND PRINCIPAL COMPONENT ANALYSIS. September 13, 2012 1 2 3 4 5 Heteroskedasticity Model Multicollinearily 6 In Thai Outline การพยากรณ ในตลาดทางการเง

Covariance Stationary Time Series. Example: Independent White Noise (IWN(0,σ 2 )) Y t = ε t, ε t iid N(0,σ 2 )

) Y t = ε t, ε t iid N(0,σ 2 )") Covariance Stationary Time Series Stochastic Process: sequence of rv s ordered by time {Y t } {...,Y 1,Y 0,Y 1,...} Defn: {Y t } is covariance stationary if E[Y t ]μ for all t cov(y t,y t j )E[(Y t μ)(y

Covariance Stationary Time Series Stochastic Process: sequence of rv s ordered by time {Y t } {...,Y 1,Y 0,Y 1,...} Defn: {Y t } is covariance stationary if E[Y t ]μ for all t cov(y t,y t j )E[(Y t μ)(y

Chapter 4: Models for Stationary Time Series

Chapter 4: Models for Stationary Time Series Now we will introduce some useful parametric models for time series that are stationary processes. We begin by defining the General Linear Process. Let {Y t

Chapter 4: Models for Stationary Time Series Now we will introduce some useful parametric models for time series that are stationary processes. We begin by defining the General Linear Process. Let {Y t

Cointegration, Stationarity and Error Correction Models.

Cointegration, Stationarity and Error Correction Models. STATIONARITY Wold s decomposition theorem states that a stationary time series process with no deterministic components has an infinite moving average

Cointegration, Stationarity and Error Correction Models. STATIONARITY Wold s decomposition theorem states that a stationary time series process with no deterministic components has an infinite moving average

Nonlinear time series

Based on the book by Fan/Yao: Nonlinear Time Series Robert M. Kunst robert.kunst@univie.ac.at University of Vienna and Institute for Advanced Studies Vienna October 27, 2009 Outline Characteristics of

Based on the book by Fan/Yao: Nonlinear Time Series Robert M. Kunst robert.kunst@univie.ac.at University of Vienna and Institute for Advanced Studies Vienna October 27, 2009 Outline Characteristics of

6.435, System Identification

System Identification 6.435 SET 3 Nonparametric Identification Munther A. Dahleh 1 Nonparametric Methods for System ID Time domain methods Impulse response Step response Correlation analysis / time Frequency

System Identification 6.435 SET 3 Nonparametric Identification Munther A. Dahleh 1 Nonparametric Methods for System ID Time domain methods Impulse response Step response Correlation analysis / time Frequency

9) Time series econometrics

Time series econometrics") 30C00200 Econometrics 9) Time series econometrics Timo Kuosmanen Professor Management Science http://nomepre.net/index.php/timokuosmanen 1 Macroeconomic data: GDP Inflation rate Examples of time series

30C00200 Econometrics 9) Time series econometrics Timo Kuosmanen Professor Management Science http://nomepre.net/index.php/timokuosmanen 1 Macroeconomic data: GDP Inflation rate Examples of time series

Lecture 5: Unit Roots, Cointegration and Error Correction Models The Spurious Regression Problem

Lecture 5: Unit Roots, Cointegration and Error Correction Models The Spurious Regression Problem Prof. Massimo Guidolin 20192 Financial Econometrics Winter/Spring 2018 Overview Stochastic vs. deterministic

Lecture 5: Unit Roots, Cointegration and Error Correction Models The Spurious Regression Problem Prof. Massimo Guidolin 20192 Financial Econometrics Winter/Spring 2018 Overview Stochastic vs. deterministic

Autoregressive and Moving-Average Models

Chapter 3 Autoregressive and Moving-Average Models 3.1 Introduction Let y be a random variable. We consider the elements of an observed time series {y 0,y 1,y2,...,y t } as being realizations of this randoms

Chapter 3 Autoregressive and Moving-Average Models 3.1 Introduction Let y be a random variable. We consider the elements of an observed time series {y 0,y 1,y2,...,y t } as being realizations of this randoms

Lecture 2: ARMA(p,q) models (part 2)

models (part 2)") Lecture 2: ARMA(p,q) models (part 2) Florian Pelgrin University of Lausanne, École des HEC Department of mathematics (IMEA-Nice) Sept. 2011 - Jan. 2012 Florian Pelgrin (HEC) Univariate time series Sept.

Lecture 2: ARMA(p,q) models (part 2) Florian Pelgrin University of Lausanne, École des HEC Department of mathematics (IMEA-Nice) Sept. 2011 - Jan. 2012 Florian Pelgrin (HEC) Univariate time series Sept.

Shape of the return probability density function and extreme value statistics

Shape of the return probability density function and extreme value statistics 13/09/03 Int. Workshop on Risk and Regulation, Budapest Overview I aim to elucidate a relation between one field of research

Shape of the return probability density function and extreme value statistics 13/09/03 Int. Workshop on Risk and Regulation, Budapest Overview I aim to elucidate a relation between one field of research

TIME SERIES AND FORECASTING. Luca Gambetti UAB, Barcelona GSE Master in Macroeconomic Policy and Financial Markets

TIME SERIES AND FORECASTING Luca Gambetti UAB, Barcelona GSE 2014-2015 Master in Macroeconomic Policy and Financial Markets 1 Contacts Prof.: Luca Gambetti Office: B3-1130 Edifici B Office hours: email:

TIME SERIES AND FORECASTING Luca Gambetti UAB, Barcelona GSE 2014-2015 Master in Macroeconomic Policy and Financial Markets 1 Contacts Prof.: Luca Gambetti Office: B3-1130 Edifici B Office hours: email:

Class: Trend-Cycle Decomposition

Class: Trend-Cycle Decomposition Macroeconometrics - Spring 2011 Jacek Suda, BdF and PSE June 1, 2011 Outline Outline: 1 Unobserved Component Approach 2 Beveridge-Nelson Decomposition 3 Spectral Analysis

Class: Trend-Cycle Decomposition Macroeconometrics - Spring 2011 Jacek Suda, BdF and PSE June 1, 2011 Outline Outline: 1 Unobserved Component Approach 2 Beveridge-Nelson Decomposition 3 Spectral Analysis

Time Series Models for Measuring Market Risk

Time Series Models for Measuring Market Risk José Miguel Hernández Lobato Universidad Autónoma de Madrid, Computer Science Department June 28, 2007 1/ 32 Outline 1 Introduction 2 Competitive and collaborative

Time Series Models for Measuring Market Risk José Miguel Hernández Lobato Universidad Autónoma de Madrid, Computer Science Department June 28, 2007 1/ 32 Outline 1 Introduction 2 Competitive and collaborative

2. Volatility Models. 2.1 Background. Below are autocorrelations of the log-index.

2. Volatility Models 2.1 Background Example 2.1: Consider the following daily close-toclose SP500 values [January 3, 2000 to March 27, 2009] Below are autocorrelations of the log-index. Obviously the persistence

2. Volatility Models 2.1 Background Example 2.1: Consider the following daily close-toclose SP500 values [January 3, 2000 to March 27, 2009] Below are autocorrelations of the log-index. Obviously the persistence

Time Series Models of Heteroskedasticity

Chapter 21 Time Series Models of Heteroskedasticity There are no worked examples in the text, so we will work with the Federal Funds rate as shown on page 658 and below in Figure 21.1. It will turn out

Chapter 21 Time Series Models of Heteroskedasticity There are no worked examples in the text, so we will work with the Federal Funds rate as shown on page 658 and below in Figure 21.1. It will turn out

MFE Financial Econometrics 2018 Final Exam Model Solutions

MFE Financial Econometrics 2018 Final Exam Model Solutions Tuesday 12 th March, 2019 1. If (X, ε) N (0, I 2 ) what is the distribution of Y = µ + β X + ε? Y N ( µ, β 2 + 1 ) 2. What is the Cramer-Rao lower

MFE Financial Econometrics 2018 Final Exam Model Solutions Tuesday 12 th March, 2019 1. If (X, ε) N (0, I 2 ) what is the distribution of Y = µ + β X + ε? Y N ( µ, β 2 + 1 ) 2. What is the Cramer-Rao lower

GARCH Models Estimation and Inference

GARCH Models Estimation and Inference Eduardo Rossi University of Pavia December 013 Rossi GARCH Financial Econometrics - 013 1 / 1 Likelihood function The procedure most often used in estimating θ 0 in

GARCH Models Estimation and Inference Eduardo Rossi University of Pavia December 013 Rossi GARCH Financial Econometrics - 013 1 / 1 Likelihood function The procedure most often used in estimating θ 0 in

The Slow Convergence of OLS Estimators of α, β and Portfolio. β and Portfolio Weights under Long Memory Stochastic Volatility

The Slow Convergence of OLS Estimators of α, β and Portfolio Weights under Long Memory Stochastic Volatility New York University Stern School of Business June 21, 2018 Introduction Bivariate long memory

The Slow Convergence of OLS Estimators of α, β and Portfolio Weights under Long Memory Stochastic Volatility New York University Stern School of Business June 21, 2018 Introduction Bivariate long memory

Covers Chapter 10-12, some of 16, some of 18 in Wooldridge. Regression Analysis with Time Series Data

Covers Chapter 10-12, some of 16, some of 18 in Wooldridge Regression Analysis with Time Series Data Obviously time series data different from cross section in terms of source of variation in x and y temporal

Covers Chapter 10-12, some of 16, some of 18 in Wooldridge Regression Analysis with Time Series Data Obviously time series data different from cross section in terms of source of variation in x and y temporal

Time Series Methods. Sanjaya Desilva

Time Series Methods Sanjaya Desilva 1 Dynamic Models In estimating time series models, sometimes we need to explicitly model the temporal relationships between variables, i.e. does X affect Y in the same

Time Series Methods Sanjaya Desilva 1 Dynamic Models In estimating time series models, sometimes we need to explicitly model the temporal relationships between variables, i.e. does X affect Y in the same

Chapter 9: Forecasting

Chapter 9: Forecasting One of the critical goals of time series analysis is to forecast (predict) the values of the time series at times in the future. When forecasting, we ideally should evaluate the

Chapter 9: Forecasting One of the critical goals of time series analysis is to forecast (predict) the values of the time series at times in the future. When forecasting, we ideally should evaluate the

7. Integrated Processes

7. Integrated Processes Up to now: Analysis of stationary processes (stationary ARMA(p, q) processes) Problem: Many economic time series exhibit non-stationary patterns over time 226 Example: We consider

7. Integrated Processes Up to now: Analysis of stationary processes (stationary ARMA(p, q) processes) Problem: Many economic time series exhibit non-stationary patterns over time 226 Example: We consider

Define y t+h t as the forecast of y t+h based on I t known parameters. The forecast error is. Forecasting

Forecasting Let {y t } be a covariance stationary are ergodic process, eg an ARMA(p, q) process with Wold representation y t = X μ + ψ j ε t j, ε t ~WN(0,σ 2 ) j=0 = μ + ε t + ψ 1 ε t 1 + ψ 2 ε t 2 + Let

Forecasting Let {y t } be a covariance stationary are ergodic process, eg an ARMA(p, q) process with Wold representation y t = X μ + ψ j ε t j, ε t ~WN(0,σ 2 ) j=0 = μ + ε t + ψ 1 ε t 1 + ψ 2 ε t 2 + Let

The Evolution of Snp Petrom Stock List - Study Through Autoregressive Models

The Evolution of Snp Petrom Stock List Study Through Autoregressive Models Marian Zaharia Ioana Zaheu Elena Roxana Stan Faculty of Internal and International Economy of Tourism RomanianAmerican University,

The Evolution of Snp Petrom Stock List Study Through Autoregressive Models Marian Zaharia Ioana Zaheu Elena Roxana Stan Faculty of Internal and International Economy of Tourism RomanianAmerican University,

at least 50 and preferably 100 observations should be available to build a proper model

III Box-Jenkins Methods 1. Pros and Cons of ARIMA Forecasting a) need for data at least 50 and preferably 100 observations should be available to build a proper model used most frequently for hourly or

III Box-Jenkins Methods 1. Pros and Cons of ARIMA Forecasting a) need for data at least 50 and preferably 100 observations should be available to build a proper model used most frequently for hourly or

The Size and Power of Four Tests for Detecting Autoregressive Conditional Heteroskedasticity in the Presence of Serial Correlation

The Size and Power of Four s for Detecting Conditional Heteroskedasticity in the Presence of Serial Correlation A. Stan Hurn Department of Economics Unversity of Melbourne Australia and A. David McDonald

The Size and Power of Four s for Detecting Conditional Heteroskedasticity in the Presence of Serial Correlation A. Stan Hurn Department of Economics Unversity of Melbourne Australia and A. David McDonald

Univariate Volatility Modeling

Univariate Volatility Modeling Kevin Sheppard http://www.kevinsheppard.com Oxford MFE This version: January 10, 2013 January 14, 2013 Financial Econometrics (Finally) This term Volatility measurement and

Univariate Volatility Modeling Kevin Sheppard http://www.kevinsheppard.com Oxford MFE This version: January 10, 2013 January 14, 2013 Financial Econometrics (Finally) This term Volatility measurement and

Introduction to Economic Time Series

Econometrics II Introduction to Economic Time Series Morten Nyboe Tabor Learning Goals 1 Give an account for the important differences between (independent) cross-sectional data and time series data. 2

Econometrics II Introduction to Economic Time Series Morten Nyboe Tabor Learning Goals 1 Give an account for the important differences between (independent) cross-sectional data and time series data. 2

4. MA(2) +drift: y t = µ + ɛ t + θ 1 ɛ t 1 + θ 2 ɛ t 2. Mean: where θ(l) = 1 + θ 1 L + θ 2 L 2. Therefore,

+drift: y t = µ + ɛ t + θ 1 ɛ t 1 + θ 2 ɛ t 2. Mean: where θ(l) = 1 + θ 1 L + θ 2 L 2. Therefore,") 61 4. MA(2) +drift: y t = µ + ɛ t + θ 1 ɛ t 1 + θ 2 ɛ t 2 Mean: y t = µ + θ(l)ɛ t, where θ(l) = 1 + θ 1 L + θ 2 L 2. Therefore, E(y t ) = µ + θ(l)e(ɛ t ) = µ 62 Example: MA(q) Model: y t = ɛ t + θ 1 ɛ

61 4. MA(2) +drift: y t = µ + ɛ t + θ 1 ɛ t 1 + θ 2 ɛ t 2 Mean: y t = µ + θ(l)ɛ t, where θ(l) = 1 + θ 1 L + θ 2 L 2. Therefore, E(y t ) = µ + θ(l)e(ɛ t ) = µ 62 Example: MA(q) Model: y t = ɛ t + θ 1 ɛ

7. Integrated Processes

7. Integrated Processes Up to now: Analysis of stationary processes (stationary ARMA(p, q) processes) Problem: Many economic time series exhibit non-stationary patterns over time 226 Example: We consider

7. Integrated Processes Up to now: Analysis of stationary processes (stationary ARMA(p, q) processes) Problem: Many economic time series exhibit non-stationary patterns over time 226 Example: We consider

This note introduces some key concepts in time series econometrics. First, we

INTRODUCTION TO TIME SERIES Econometrics 2 Heino Bohn Nielsen September, 2005 This note introduces some key concepts in time series econometrics. First, we present by means of examples some characteristic

INTRODUCTION TO TIME SERIES Econometrics 2 Heino Bohn Nielsen September, 2005 This note introduces some key concepts in time series econometrics. First, we present by means of examples some characteristic

Lecture 19 - Decomposing a Time Series into its Trend and Cyclical Components

Lecture 19 - Decomposing a Time Series into its Trend and Cyclical Components It is often assumed that many macroeconomic time series are subject to two sorts of forces: those that influence the long-run

Lecture 19 - Decomposing a Time Series into its Trend and Cyclical Components It is often assumed that many macroeconomic time series are subject to two sorts of forces: those that influence the long-run

Financial Econometrics and Quantitative Risk Managenent Return Properties

Financial Econometrics and Quantitative Risk Managenent Return Properties Eric Zivot Updated: April 1, 2013 Lecture Outline Course introduction Return definitions Empirical properties of returns Reading

Financial Econometrics and Quantitative Risk Managenent Return Properties Eric Zivot Updated: April 1, 2013 Lecture Outline Course introduction Return definitions Empirical properties of returns Reading

GARCH Models Estimation and Inference

Università di Pavia GARCH Models Estimation and Inference Eduardo Rossi Likelihood function The procedure most often used in estimating θ 0 in ARCH models involves the maximization of a likelihood function

Università di Pavia GARCH Models Estimation and Inference Eduardo Rossi Likelihood function The procedure most often used in estimating θ 0 in ARCH models involves the maximization of a likelihood function

State-space Model. Eduardo Rossi University of Pavia. November Rossi State-space Model Fin. Econometrics / 53

State-space Model Eduardo Rossi University of Pavia November 2014 Rossi State-space Model Fin. Econometrics - 2014 1 / 53 Outline 1 Motivation 2 Introduction 3 The Kalman filter 4 Forecast errors 5 State

State-space Model Eduardo Rossi University of Pavia November 2014 Rossi State-space Model Fin. Econometrics - 2014 1 / 53 Outline 1 Motivation 2 Introduction 3 The Kalman filter 4 Forecast errors 5 State

1. How can you tell if there is serial correlation? 2. AR to model serial correlation. 3. Ignoring serial correlation. 4. GLS. 5. Projects.

1. How can you tell if there is serial correlation? 2. AR to model serial correlation. 3. Ignoring serial correlation. 4. GLS. 5. Projects. 1) Identifying serial correlation. Plot Y t versus Y t 1. See

1. How can you tell if there is serial correlation? 2. AR to model serial correlation. 3. Ignoring serial correlation. 4. GLS. 5. Projects. 1) Identifying serial correlation. Plot Y t versus Y t 1. See

13. Time Series Analysis: Asymptotics Weakly Dependent and Random Walk Process. Strict Exogeneity

Outline: Further Issues in Using OLS with Time Series Data 13. Time Series Analysis: Asymptotics Weakly Dependent and Random Walk Process I. Stationary and Weakly Dependent Time Series III. Highly Persistent

Outline: Further Issues in Using OLS with Time Series Data 13. Time Series Analysis: Asymptotics Weakly Dependent and Random Walk Process I. Stationary and Weakly Dependent Time Series III. Highly Persistent

MGR-815. Notes for the MGR-815 course. 12 June School of Superior Technology. Professor Zbigniew Dziong

Modeling, Estimation and Control, for Telecommunication Networks Notes for the MGR-815 course 12 June 2010 School of Superior Technology Professor Zbigniew Dziong 1 Table of Contents Preface 5 1. Example

Modeling, Estimation and Control, for Telecommunication Networks Notes for the MGR-815 course 12 June 2010 School of Superior Technology Professor Zbigniew Dziong 1 Table of Contents Preface 5 1. Example

1 Time Series Concepts and Challenges

Forecasting Time Series Data Notes from Rebecca Sela Stern Business School Spring, 2004 1 Time Series Concepts and Challenges The linear regression model (and most other models) assume that observations

Forecasting Time Series Data Notes from Rebecca Sela Stern Business School Spring, 2004 1 Time Series Concepts and Challenges The linear regression model (and most other models) assume that observations

Financial Econometrics

Financial Econometrics Nonlinear time series analysis Gerald P. Dwyer Trinity College, Dublin January 2016 Outline 1 Nonlinearity Does nonlinearity matter? Nonlinear models Tests for nonlinearity Forecasting

Financial Econometrics Nonlinear time series analysis Gerald P. Dwyer Trinity College, Dublin January 2016 Outline 1 Nonlinearity Does nonlinearity matter? Nonlinear models Tests for nonlinearity Forecasting

Time Series Analysis -- An Introduction -- AMS 586

Time Series Analysis -- An Introduction -- AMS 586 1 Objectives of time series analysis Data description Data interpretation Modeling Control Prediction & Forecasting 2 Time-Series Data Numerical data

Time Series Analysis -- An Introduction -- AMS 586 1 Objectives of time series analysis Data description Data interpretation Modeling Control Prediction & Forecasting 2 Time-Series Data Numerical data

Financial Econometrics Using Stata

Financial Econometrics Using Stata SIMONA BOFFELLI University of Bergamo (Italy) and Centre for Econometric Analysis, Cass Business School, City University London (UK) GIOVANNI URGA Centre for Econometric

Financial Econometrics Using Stata SIMONA BOFFELLI University of Bergamo (Italy) and Centre for Econometric Analysis, Cass Business School, City University London (UK) GIOVANNI URGA Centre for Econometric

July 31, 2009 / Ben Kedem Symposium

ing The s ing The Department of Statistics North Carolina State University July 31, 2009 / Ben Kedem Symposium Outline ing The s 1 2 s 3 4 5 Ben Kedem ing The s Ben has made many contributions to time

ing The s ing The Department of Statistics North Carolina State University July 31, 2009 / Ben Kedem Symposium Outline ing The s 1 2 s 3 4 5 Ben Kedem ing The s Ben has made many contributions to time

Stationary Time Series, Conditional Heteroscedasticity, Random Walk, Test for a Unit Root, Endogenity, Causality and IV Estimation

1 / 67 Stationary Time Series, Conditional Heteroscedasticity, Random Walk, Test for a Unit Root, Endogenity, Causality and IV Estimation Chapter 1 Financial Econometrics Michael Hauser WS18/19 2 / 67

1 / 67 Stationary Time Series, Conditional Heteroscedasticity, Random Walk, Test for a Unit Root, Endogenity, Causality and IV Estimation Chapter 1 Financial Econometrics Michael Hauser WS18/19 2 / 67

7. Forecasting with ARIMA models

7. Forecasting with ARIMA models 309 Outline: Introduction The prediction equation of an ARIMA model Interpreting the predictions Variance of the predictions Forecast updating Measuring predictability

7. Forecasting with ARIMA models 309 Outline: Introduction The prediction equation of an ARIMA model Interpreting the predictions Variance of the predictions Forecast updating Measuring predictability

Non-Stationary Time Series and Unit Root Testing

Econometrics II Non-Stationary Time Series and Unit Root Testing Morten Nyboe Tabor Course Outline: Non-Stationary Time Series and Unit Root Testing 1 Stationarity and Deviation from Stationarity Trend-Stationarity

Econometrics II Non-Stationary Time Series and Unit Root Testing Morten Nyboe Tabor Course Outline: Non-Stationary Time Series and Unit Root Testing 1 Stationarity and Deviation from Stationarity Trend-Stationarity