ECON 616: Lecture 1: Time Series Basics

|

|

|

- Chad Moore

- 5 years ago

- Views:

Transcription

1 ECON 616: Lecture 1: Time Series Basics ED HERBST August 30, 2017

2 References Overview: Chapters 1-3 from Hamilton (1994). Technical Details: Chapters 2-3 from Brockwell and Davis (1987). Intuition: Chapters 1-4 from Cochrane.

3 Time Series A time series is a family of random variables indexed by time {Y t, t T } dened on a probability space (Ω, F, P). (Everybody uses "time series" to mean both the random variables and their realizations) For this class, T = {0, ±1, ±2,...}. Some examples: 1. y t = β 0 + β 1 t + ɛ t, ɛ t iidn(0, σ 2 ). 2. y t = ρy t 1 + ɛ t, ɛ t iidn(0, σ 2 ). 3. y t = ɛ 1 cos(ωt) + ɛ 2 sin(ωt), ω [0, 2π).

4 Time Series Examples

5 Why time series analysis? Seems like any area of econometrics, but: 1. We (often) only have one realization for a given time series probability model (and it's short)! (A single path of xx quarterly observations for real GDP since ) 2. Focus (mostly) on parametric models to describe time series. 3. More emphasis on prediction than some subelds.

6 Denitions The autocovariance function of a time series is the set of functions {γ t (τ), t T } γ t (τ) = E [(Y t EY t )(Y t+τ EY t+τ ) ] A time series is covariance stationary if 1. E [X 2 t ] for all t T. 2. E [X t ] = µ for all t T. 3. γ t (τ) = γ(τ) for all t, τ T. Note that γ(τ) γ(0) and γ(τ) = γ( τ).

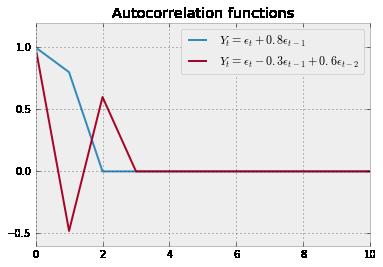

7 Some Examples 1. y t = βt + ɛ t, ɛ iidn(0, σ 2 ). E[y t ] = βt, depends on time, not covariance stationary! 2. y t = ɛ t + 0.5ɛ t 1, ɛ iidn(0, σ 2 ) E[y t ] = 0, γ(0) = 1.25, γ(±1) = 0.5, γ(τ) = 0 = covariance stationary.

8 Building Blocks of Stationary Processes A stationary process {Z t } is called white noise if it satises 1. E[Z t ] = γ(0) = σ γ(τ) = 0 for τ 0. These processes are kind of boring on their own, but using them we can construct arbitrary stationary processes! Special Case: Z t iidn(0, σ 2 )

9 White Noise

10 Asymptotics for Covariance Stationary MA pr. Covariance Stationarity isn't necessary or sucient to ensure the convergence of sample averages to population averages. We'll talk about a special case now. Consider the moving average process of order q where ɛ t is iid WN(0, σ 2 ). y t = ɛ t + θ 1 ɛ t θ q ɛ t q We'll show a weak law of large numbers and central limit theorem applies to this process using the Beveridge-Nelson decomposition following Phillips and Solo (1992). Using the lag operator LX t = X t 1 we can write y t = θ(l)ɛ t, θ(z) = 1 + θ 1 z θ q z q.

11 Deriving Asymptotics Write θ( ) in Taylor expansion-ish sort of way θ(l) = = = q θ j L j, j=0 ( q θ j j=0 ) ( q q θ j + θ j j=1 ( q + θ j j=2 j=1 ) q θ j L j=3 ) q θ j L j=2 ( q q ) ( q ) θ j + θ j (L 1) + θ j (L 2 L) +... j=0 j=1 j=2 = θ(1) + ˆθ 1 (L 1) + ˆθ 2 L(L 1) +... = θ(1) + ˆθ(L)(L 1)

12 WLLN / CLT We can write y t as y t = θ(1)ɛ t + ˆθ(L)ɛ t 1 ˆθ(L)ɛ t An average of y t cancels most of the second and third term... 1 T We have T y t = 1 T T θ(1) ɛ t + 1 (ˆθ(L)ɛ0 T ˆθ(L)ɛ ) T t=1 t=1 1 T (ˆθ(L)ɛ0 ˆθ(L)ɛ T ) 0. Then we can apply a WLLN / CLT for iid sequences with Slutsky's Theorem to deduce that 1 T T y t 0 and t=1 1 T T t=1 y t N(0, σ 2 θ(1) 2 )

13 ARMA Processes The processes {Y t } is said to be an ARMA(p,q) prcess if {Y t } is stationary and if for it can be represented by the linear dierence equation: Y t = φ 1 Y t φ p Y t p + Z t + θ 1 Z t θ q Z t q with {Z t } WN(0, σ 2 ). Using the lag operator LX t = X t 1 we can write: φ(l)y t = θ(l)z t where φ(z) = 1 φ 1 z... φ p z p and θ(z) = 1 + θ 1 z θ q z q. Special cases: 1. AR(1) : Y t = φ 1 Y t 1 + Z t. 2. MA(1) : Y t = Z t + θ 1 Z t. 3. AR(p), MA(q),...

14 Why are ARMA processes important? 1. Dened in terms of linear dierence equations (something we know a lot about!) 2. Parametric family = some hope for estimating these things 3. It turns out that for any stationary process with autocovariance function γ Y ( ) with lim τ γ ( τ) = 0, we can, for any integer k > 0, nd an ARMA process with γ(τ) = γ Y (τ) for τ = 0, 1,..., k. They are pretty exible!

15 MA(q) Process Revisited Y t = Z t + θ 1 Z t θ q Z t 1 Is it covariance stationary? Well, E[Y t ] = E[Z t ] + θ 1 E[Z t 1 ] θ q E[Z t 1 ] = 0 and E[Y t Y t h ] = E[(Z t +θ 1 Z t θ q Z t 1 )(Z t h +θ 1 Z t h θ q Z t If q h, this equals σ 2 (θ h θ θ q θ q h ) and 0 otherwise. This doesn't depend on t, so this process is covariance stationary regardless of values of θ.

16 Autocorrelation Function

17 AR(1) Model Y t = φ 1 Y t 1 + Z t From the perspective of a linear dierence equation, Y t can be solved for as a function {Z t } via backwards subsitution: J 1 Y t = φ 1 ɛ t 1 + φ 2 Y t 2 + ɛ t (1) j=0 = ɛ t + φ 1 ɛ t 1 + φ 2 1ɛ t (2) = φ j ɛ 1 t j (3) j=0 How do we know whether this is covariance stationary?

18 Analysis of AR(1), continued We want to know if Y t converges to some random variable as we consider the innite past of innovations. The relevant concept (assuming that E[Y 2 t ] < ) is mean square convergence. We say that Y t converges in mean square to a random variable Y if E [ (Y t Y ) 2] 0 as n. It turns out that there is a connection to deterministic sums j=0 a j. We can prove mean square convergence by showing that the sequence generated by partial summations satises a Cauchy criteria, very similar to the way you would for a deterministic sequence.

19 Analysis of AR(1), continued What this boils down to: We need square summability: j=0 (φj 1 )2 <. We'll often work with the stronger condition absolute summability : j=0 φj 1 <. For the AR(1) model, this means we need φ 1 < 1, for covariance stationarity.

20 Relationship Between AR and MA Processes You may have noticed that we worked with the innite moving average representation of the AR(1) model to show convergence. We got there by doing some lag operator arithmatic: (1 φ 1 L)Y t = ɛ t We inverted the polynomial φ(z) = (1 φ 1 z) by (1 φ 1 z) 1 = 1 + φ 1 z + φ 2 1z Note that this is only valid when z < 1 = we can't always perform inversion! To think about covariance stationarity in the context of ARMA processes, we always try to use the MA( ) representation of a given series.

21 A General Theorem If {X t } is a covariance stationary process with autocovariance function γ X ( ) and if j=0 θ j <, than the innite sum Y t = θ(l)x t = θ j X t j j=0 converges in mean square. The process {Y t } is covariance stationary with autocovariance function γ(h) = θ j θ k γ x (h j + k) j=0 k=0 If the autocovariances of {X t } are absolutely summable, then so are the autocovrainces of {Y t }.

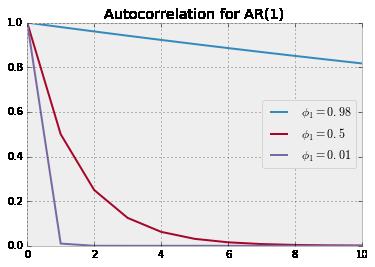

22 Back to AR(1) Y t = φ 1 Y t 1 + ɛ t, ɛ t WN(0, σ 2 ), φ 1 < 1 The variance can be found using the MA( ) representation Y t = φ j ɛ 1 t j = j=0 This means that [( ) ( )] E[Yt 2 ] = E φ j ɛ 1 t j φ j ɛ 1 t j = j=0 j=0 E [ ] φ 2j ɛ 2 t j = φ 2j σ 2 (4) j=0 σ2 γ(0) = V[Y t ] = 1 φ 2 1 j=0

23 Autocovariance of AR(1) To nd the autocovariance: Y t Y t 1 = φ 1 Y 2 t 1 + ɛ t Y t 1 = γ(1) = φ 1 γ(0) Y t Y t 2 = φ 1 Y t 1 Y t 2 + ɛ t Y t 2 Y t Y t 3 = φ 1 Y t 1 Y t 3 + ɛ t Y t 3 Let's look at autocorrelation ρ(τ) = γ(τ) γ(0) = γ(2) = φ 1 γ(1) = γ(3) = φ 1 γ(2)

24 Autocorrelation for AR(1)

25 Simulated Paths

26 Analysis of AR(2) Model Which means Y t = φ 1 Y t 1 + φ 2 Y t 2 + ɛ t φ(l)y t = ɛ t, φ(z) = 1 φ 1 z φ 2 z 2 Under what conditions can we invert φ( )? Factoring the polynomial 1 φ 1 z φ 2 z 2 = (1 λ 1 z)(1 λ 2 z) Using the above theorem, if both λ 1 and λ 2 are less than one in length (they can be complex!) we can apply the earlier logic succesively to obtain conditions for covariance stationarity. Note: λ 1 λ 2 = φ 2 and λ 1 + λ 2 = φ 1

27 Companion Form [ Yt Y t 1 ] = [ φ1 φ ] [ Yt 1 Y t 2 ] + [ ɛt 0 ] (5) Y t = FY t 1 + ɛ t F has eigenvalues λ which solve λ 2 φ 1 λ φ 2 = 0

28 Finding the Autocovariance Function Multiplying and using the symmetry of the autocovariance function: Y t : γ(0) = φ 1 γ(1) + φ 2 γ(2) + σ 2 (6) Y t 1 : γ(1) = φ 1 γ(0) + φ 1 γ(1) (7) Y t 2 : γ(2) = φ 1 γ(1) + φ 1 γ(0) (8). (9) Y t h : γ(h) = φ 1 γ(h 1) + φ 1 γ(h 2) (10) We can solve for γ(0), γ(1), γ(2) using the rst three equations: (1 φ 2 )σ 2 γ(0) = (1 + φ 2 )[(1 φ 2 ) 2 φ 2] 1 We can solve for the rest using the recursions. Note pth order AR(1) have autocovariances / autocorrelations that follow the same pth order dierence equations.

29 Why are we so obsessed iwth autocovariance/correlation functions? For covariance stationary processes, we are really only concerned with the rst two moments. If, in addition, the white noise is actually IID normal, those two moments characterize everything! So if two processes have the same autocovariance (and mean... ), they're the same. We saw that with the AR(1) and MA( ) example. How do we distinguish between the dierent processes yielding an identical series?

30 Invertibility Recall φ(l)y t = θ(l)ɛ t We already discussed conditions under which we can invert φ(l) for the AR(1) model to represent Y t as an MA( ). What about other direction? An MA process is invertible if θ(l) 1 exists. so $MA(1) : θ 1 <1, MA(q):... $

31 MA(1) with θ 1 > 1 Consider Y t = ɛ t + 0.5ɛ t 1, ɛ t WN(0, σ 2 ) γ(0) = 1.25σ 2, γ(1) = 0.5σ 2. vs. Y t = ɛ t + 2 ɛ t 1, ɛ t WN(0, σ 2 ) γ(0) = 5 σ 2, γ(1) = 2 σ 2 For σ = 2 σ, these are the same! Prefer invertible process: 1. Mimics AR case. 2. Intuitive to think of errors as decaying. 3. Noninvertibility pops up in macro: news shocks!

32 Why ARMA, again? ARMA models seem cool, but they are inherently linear Many important phenomenom are nonlinear (hello great recession!) It turns out that any covariance stationary process has a linear ARMA representation! This is called the Wold Theorem; it's a big deal.

33 Wold Decomposition Theorem Any zero mean covariance stationary process {Y t } can be represented as Y t = ψ j ɛ t j + κ t j=0 where ψ 0 = 1 and j=0 ψ2 j <. The term ɛ t is white noise are represents the error made in forecasting Y t on the basis of a linear function of lagged Y (denoted by Ê[ ]): ɛ t = y t Ê[Y t y t 1, y t 2, ] The value of κ t is uncorrelated with ɛ t j for any value of j, and can be predicted arbitrary well from a linear function of past values of Y : κ t = Ê[κ t y t 1, y t 2, ]

34 Strict Stationarity A time series is strictly stationary if for all t 1,..., t k, k, h T if Y t1,..., Y tk Y t1 +h,..., Y tk +h What is the relationship between strict and covariance stationarity? {Y t } strictly stationary (with nite second moment) = covariance stationarity. The corollary need not be true! Important Exception if {Y t } is gaussian series covariance stationarity = strict stationarity.

35 Ergodicity In earlier econometrics classes, you (might have) examined large sample properties of estimators using LLN and CLT for sums of independent RVs. Times series are obviously not independent, so we need some other tools. Under what conditions do time averages converge to population averages. One helpful concept: A stationary process is said to be ergodic if, for any two bounded and measurable functions f : R k R and g : R l R, lim E [f (y t,..., y t+k )g(y t+n,..., g t+n+l ] n E [f (y t,..., y t+k )] E [g(y t+n,..., y t+n+l ] = 0 Ergodicity is a tedious concept. At an intuitive level, a process if ergodic if the dependence between an event today and event at some horizon in the future vanishes as the horizon increases.

36 The Ergodic Theorem If {y t } is strictly stationary and ergodic with E[y 1 ] <, then 1 T T y t E[y 1 ] t=1 CLT for strictly stationary and ergodic processes_ If {y t } is strictly stationary and ergodic with E[y 1 ] <, E[y 2 1 ] <, and σ 2 = var(t 1/2 y t ) σ 2 <, then 1 T σt T t=1 y t N(0, 1)

37 Facts About Ergodic Theorem 1. iid sequences are stationary and ergodic 2. If {Y t } is strictly stationary and ergodic, and f : R R is a measurable function: Z t = f ({Y t }) Then Z t is strictly stationary and ergodic. (Note this is for strictly stationary processes!)

38 Example Example: an MA( ) with iid Gaussian white noise. Y t = θ j ɛ t j, j=0 θ j <. j=0 This means that {Y t }, {Y 2 t }, and {Y t Y t h } are ergodic! 1 T Y t E[Y 0 ], t=0 1 T t=0 Y 2 t E[Y 2 0 ], 1 T Y t Y t h E[Y 0 Y h ], t=0

39 Martingale Dierence Sequences {Z t } is a Martingale Dierence Sequence (with respect to the information sets {F t }) if E[Z t F t 1 ] = 0 for all t LLN and CLT for MDS Let {Y t, F t } be a martingale dierence sequence such that E[ Y t 2r ] < < for some r > 1, and all t. Then ȲT = T 1 T t=1 Y t p 0. Moreover, if var( T ȲT ) = σ 2 T σ2 > 0, then T Ȳ T / σ T = N (0, 1).

40 References Brockwell, P. J. and Davis, R. A. (1987). Time series: Theory and methods. Springer Series in Statistics. Hamilton, J. (1994). Time Series Analysis. Princeton University Press, Princeton, New Jersey.

Introduction to Stochastic processes

Università di Pavia Introduction to Stochastic processes Eduardo Rossi Stochastic Process Stochastic Process: A stochastic process is an ordered sequence of random variables defined on a probability space

Università di Pavia Introduction to Stochastic processes Eduardo Rossi Stochastic Process Stochastic Process: A stochastic process is an ordered sequence of random variables defined on a probability space

1 Linear Difference Equations

ARMA Handout Jialin Yu 1 Linear Difference Equations First order systems Let {ε t } t=1 denote an input sequence and {y t} t=1 sequence generated by denote an output y t = φy t 1 + ε t t = 1, 2,... with

ARMA Handout Jialin Yu 1 Linear Difference Equations First order systems Let {ε t } t=1 denote an input sequence and {y t} t=1 sequence generated by denote an output y t = φy t 1 + ε t t = 1, 2,... with

5: MULTIVARATE STATIONARY PROCESSES

5: MULTIVARATE STATIONARY PROCESSES 1 1 Some Preliminary Definitions and Concepts Random Vector: A vector X = (X 1,..., X n ) whose components are scalarvalued random variables on the same probability

5: MULTIVARATE STATIONARY PROCESSES 1 1 Some Preliminary Definitions and Concepts Random Vector: A vector X = (X 1,..., X n ) whose components are scalarvalued random variables on the same probability

Class 1: Stationary Time Series Analysis

Class 1: Stationary Time Series Analysis Macroeconometrics - Fall 2009 Jacek Suda, BdF and PSE February 28, 2011 Outline Outline: 1 Covariance-Stationary Processes 2 Wold Decomposition Theorem 3 ARMA Models

Class 1: Stationary Time Series Analysis Macroeconometrics - Fall 2009 Jacek Suda, BdF and PSE February 28, 2011 Outline Outline: 1 Covariance-Stationary Processes 2 Wold Decomposition Theorem 3 ARMA Models

3. ARMA Modeling. Now: Important class of stationary processes

3. ARMA Modeling Now: Important class of stationary processes Definition 3.1: (ARMA(p, q) process) Let {ɛ t } t Z WN(0, σ 2 ) be a white noise process. The process {X t } t Z is called AutoRegressive-Moving-Average

3. ARMA Modeling Now: Important class of stationary processes Definition 3.1: (ARMA(p, q) process) Let {ɛ t } t Z WN(0, σ 2 ) be a white noise process. The process {X t } t Z is called AutoRegressive-Moving-Average

Ch. 14 Stationary ARMA Process

Ch. 14 Stationary ARMA Process A general linear stochastic model is described that suppose a time series to be generated by a linear aggregation of random shock. For practical representation it is desirable

Ch. 14 Stationary ARMA Process A general linear stochastic model is described that suppose a time series to be generated by a linear aggregation of random shock. For practical representation it is desirable

TIME SERIES AND FORECASTING. Luca Gambetti UAB, Barcelona GSE Master in Macroeconomic Policy and Financial Markets

TIME SERIES AND FORECASTING Luca Gambetti UAB, Barcelona GSE 2014-2015 Master in Macroeconomic Policy and Financial Markets 1 Contacts Prof.: Luca Gambetti Office: B3-1130 Edifici B Office hours: email:

TIME SERIES AND FORECASTING Luca Gambetti UAB, Barcelona GSE 2014-2015 Master in Macroeconomic Policy and Financial Markets 1 Contacts Prof.: Luca Gambetti Office: B3-1130 Edifici B Office hours: email:

7. MULTIVARATE STATIONARY PROCESSES

7. MULTIVARATE STATIONARY PROCESSES 1 1 Some Preliminary Definitions and Concepts Random Vector: A vector X = (X 1,..., X n ) whose components are scalar-valued random variables on the same probability

7. MULTIVARATE STATIONARY PROCESSES 1 1 Some Preliminary Definitions and Concepts Random Vector: A vector X = (X 1,..., X n ) whose components are scalar-valued random variables on the same probability

Week 5 Quantitative Analysis of Financial Markets Characterizing Cycles

Week 5 Quantitative Analysis of Financial Markets Characterizing Cycles Christopher Ting http://www.mysmu.edu/faculty/christophert/ Christopher Ting : christopherting@smu.edu.sg : 6828 0364 : LKCSB 5036

Week 5 Quantitative Analysis of Financial Markets Characterizing Cycles Christopher Ting http://www.mysmu.edu/faculty/christophert/ Christopher Ting : christopherting@smu.edu.sg : 6828 0364 : LKCSB 5036

Forecasting with ARMA

Forecasting with ARMA Eduardo Rossi University of Pavia October 2013 Rossi Forecasting Financial Econometrics - 2013 1 / 32 Mean Squared Error Linear Projection Forecast of Y t+1 based on a set of variables

Forecasting with ARMA Eduardo Rossi University of Pavia October 2013 Rossi Forecasting Financial Econometrics - 2013 1 / 32 Mean Squared Error Linear Projection Forecast of Y t+1 based on a set of variables

ECON/FIN 250: Forecasting in Finance and Economics: Section 6: Standard Univariate Models

ECON/FIN 250: Forecasting in Finance and Economics: Section 6: Standard Univariate Models Patrick Herb Brandeis University Spring 2016 Patrick Herb (Brandeis University) Standard Univariate Models ECON/FIN

ECON/FIN 250: Forecasting in Finance and Economics: Section 6: Standard Univariate Models Patrick Herb Brandeis University Spring 2016 Patrick Herb (Brandeis University) Standard Univariate Models ECON/FIN

Introduction to ARMA and GARCH processes

Introduction to ARMA and GARCH processes Fulvio Corsi SNS Pisa 3 March 2010 Fulvio Corsi Introduction to ARMA () and GARCH processes SNS Pisa 3 March 2010 1 / 24 Stationarity Strict stationarity: (X 1,

Introduction to ARMA and GARCH processes Fulvio Corsi SNS Pisa 3 March 2010 Fulvio Corsi Introduction to ARMA () and GARCH processes SNS Pisa 3 March 2010 1 / 24 Stationarity Strict stationarity: (X 1,

Time Series Models and Inference. James L. Powell Department of Economics University of California, Berkeley

Time Series Models and Inference James L. Powell Department of Economics University of California, Berkeley Overview In contrast to the classical linear regression model, in which the components of the

Time Series Models and Inference James L. Powell Department of Economics University of California, Berkeley Overview In contrast to the classical linear regression model, in which the components of the

Covariance Stationary Time Series. Example: Independent White Noise (IWN(0,σ 2 )) Y t = ε t, ε t iid N(0,σ 2 )

) Y t = ε t, ε t iid N(0,σ 2 )") Covariance Stationary Time Series Stochastic Process: sequence of rv s ordered by time {Y t } {...,Y 1,Y 0,Y 1,...} Defn: {Y t } is covariance stationary if E[Y t ]μ for all t cov(y t,y t j )E[(Y t μ)(y

Covariance Stationary Time Series Stochastic Process: sequence of rv s ordered by time {Y t } {...,Y 1,Y 0,Y 1,...} Defn: {Y t } is covariance stationary if E[Y t ]μ for all t cov(y t,y t j )E[(Y t μ)(y

Permanent Income Hypothesis (PIH) Instructor: Dmytro Hryshko

Instructor: Dmytro Hryshko") Permanent Income Hypothesis (PIH) Instructor: Dmytro Hryshko 1 / 36 The PIH Utility function is quadratic, u(c t ) = 1 2 (c t c) 2 ; borrowing/saving is allowed using only the risk-free bond; β(1 + r)

Permanent Income Hypothesis (PIH) Instructor: Dmytro Hryshko 1 / 36 The PIH Utility function is quadratic, u(c t ) = 1 2 (c t c) 2 ; borrowing/saving is allowed using only the risk-free bond; β(1 + r)

ECON 616: Lecture Two: Deterministic Trends, Nonstationary Processes

ECON 616: Lecture Two: Deterministic Trends, Nonstationary Processes ED HERBST September 11, 2017 Background Hamilton, chapters 15-16 Trends vs Cycles A commond decomposition of macroeconomic time series

ECON 616: Lecture Two: Deterministic Trends, Nonstationary Processes ED HERBST September 11, 2017 Background Hamilton, chapters 15-16 Trends vs Cycles A commond decomposition of macroeconomic time series

1 Class Organization. 2 Introduction

Time Series Analysis, Lecture 1, 2018 1 1 Class Organization Course Description Prerequisite Homework and Grading Readings and Lecture Notes Course Website: http://www.nanlifinance.org/teaching.html wechat

Time Series Analysis, Lecture 1, 2018 1 1 Class Organization Course Description Prerequisite Homework and Grading Readings and Lecture Notes Course Website: http://www.nanlifinance.org/teaching.html wechat

Ch. 15 Forecasting. 1.1 Forecasts Based on Conditional Expectations

Ch 15 Forecasting Having considered in Chapter 14 some of the properties of ARMA models, we now show how they may be used to forecast future values of an observed time series For the present we proceed

Ch 15 Forecasting Having considered in Chapter 14 some of the properties of ARMA models, we now show how they may be used to forecast future values of an observed time series For the present we proceed

Midterm Suggested Solutions

CUHK Dept. of Economics Spring 2011 ECON 4120 Sung Y. Park Midterm Suggested Solutions Q1 (a) In time series, autocorrelation measures the correlation between y t and its lag y t τ. It is defined as. ρ(τ)

CUHK Dept. of Economics Spring 2011 ECON 4120 Sung Y. Park Midterm Suggested Solutions Q1 (a) In time series, autocorrelation measures the correlation between y t and its lag y t τ. It is defined as. ρ(τ)

ECON/FIN 250: Forecasting in Finance and Economics: Section 7: Unit Roots & Dickey-Fuller Tests

ECON/FIN 250: Forecasting in Finance and Economics: Section 7: Unit Roots & Dickey-Fuller Tests Patrick Herb Brandeis University Spring 2016 Patrick Herb (Brandeis University) Unit Root Tests ECON/FIN

ECON/FIN 250: Forecasting in Finance and Economics: Section 7: Unit Roots & Dickey-Fuller Tests Patrick Herb Brandeis University Spring 2016 Patrick Herb (Brandeis University) Unit Root Tests ECON/FIN

11. Further Issues in Using OLS with TS Data

11. Further Issues in Using OLS with TS Data With TS, including lags of the dependent variable often allow us to fit much better the variation in y Exact distribution theory is rarely available in TS applications,

11. Further Issues in Using OLS with TS Data With TS, including lags of the dependent variable often allow us to fit much better the variation in y Exact distribution theory is rarely available in TS applications,

Trend-Cycle Decompositions

Trend-Cycle Decompositions Eric Zivot April 22, 2005 1 Introduction A convenient way of representing an economic time series y t is through the so-called trend-cycle decomposition y t = TD t + Z t (1)

Trend-Cycle Decompositions Eric Zivot April 22, 2005 1 Introduction A convenient way of representing an economic time series y t is through the so-called trend-cycle decomposition y t = TD t + Z t (1)

Review Session: Econometrics - CLEFIN (20192)

") Review Session: Econometrics - CLEFIN (20192) Part II: Univariate time series analysis Daniele Bianchi March 20, 2013 Fundamentals Stationarity A time series is a sequence of random variables x t, t =

Review Session: Econometrics - CLEFIN (20192) Part II: Univariate time series analysis Daniele Bianchi March 20, 2013 Fundamentals Stationarity A time series is a sequence of random variables x t, t =

Econ 623 Econometrics II Topic 2: Stationary Time Series

1 Introduction Econ 623 Econometrics II Topic 2: Stationary Time Series In the regression model we can model the error term as an autoregression AR(1) process. That is, we can use the past value of the

1 Introduction Econ 623 Econometrics II Topic 2: Stationary Time Series In the regression model we can model the error term as an autoregression AR(1) process. That is, we can use the past value of the

Basic concepts and terminology: AR, MA and ARMA processes

ECON 5101 ADVANCED ECONOMETRICS TIME SERIES Lecture note no. 1 (EB) Erik Biørn, Department of Economics Version of February 1, 2011 Basic concepts and terminology: AR, MA and ARMA processes This lecture

ECON 5101 ADVANCED ECONOMETRICS TIME SERIES Lecture note no. 1 (EB) Erik Biørn, Department of Economics Version of February 1, 2011 Basic concepts and terminology: AR, MA and ARMA processes This lecture

Single Equation Linear GMM with Serially Correlated Moment Conditions

Single Equation Linear GMM with Serially Correlated Moment Conditions Eric Zivot October 28, 2009 Univariate Time Series Let {y t } be an ergodic-stationary time series with E[y t ]=μ and var(y t )

Single Equation Linear GMM with Serially Correlated Moment Conditions Eric Zivot October 28, 2009 Univariate Time Series Let {y t } be an ergodic-stationary time series with E[y t ]=μ and var(y t )

Discrete time processes

Discrete time processes Predictions are difficult. Especially about the future Mark Twain. Florian Herzog 2013 Modeling observed data When we model observed (realized) data, we encounter usually the following

Discrete time processes Predictions are difficult. Especially about the future Mark Twain. Florian Herzog 2013 Modeling observed data When we model observed (realized) data, we encounter usually the following

3 Theory of stationary random processes

3 Theory of stationary random processes 3.1 Linear filters and the General linear process A filter is a transformation of one random sequence {U t } into another, {Y t }. A linear filter is a transformation

3 Theory of stationary random processes 3.1 Linear filters and the General linear process A filter is a transformation of one random sequence {U t } into another, {Y t }. A linear filter is a transformation

Time Series Analysis. James D. Hamilton PRINCETON UNIVERSITY PRESS PRINCETON, NEW JERSEY

Time Series Analysis James D. Hamilton PRINCETON UNIVERSITY PRESS PRINCETON, NEW JERSEY & Contents PREFACE xiii 1 1.1. 1.2. Difference Equations First-Order Difference Equations 1 /?th-order Difference

Time Series Analysis James D. Hamilton PRINCETON UNIVERSITY PRESS PRINCETON, NEW JERSEY & Contents PREFACE xiii 1 1.1. 1.2. Difference Equations First-Order Difference Equations 1 /?th-order Difference

Lesson 9: Autoregressive-Moving Average (ARMA) models

models") Lesson 9: Autoregressive-Moving Average (ARMA) models Dipartimento di Ingegneria e Scienze dell Informazione e Matematica Università dell Aquila, umberto.triacca@ec.univaq.it Introduction We have seen

Lesson 9: Autoregressive-Moving Average (ARMA) models Dipartimento di Ingegneria e Scienze dell Informazione e Matematica Università dell Aquila, umberto.triacca@ec.univaq.it Introduction We have seen

ECONOMETRICS Part II PhD LBS

ECONOMETRICS Part II PhD LBS Luca Gambetti UAB, Barcelona GSE February-March 2014 1 Contacts Prof.: Luca Gambetti email: luca.gambetti@uab.es webpage: http://pareto.uab.es/lgambetti/ Description This is

ECONOMETRICS Part II PhD LBS Luca Gambetti UAB, Barcelona GSE February-March 2014 1 Contacts Prof.: Luca Gambetti email: luca.gambetti@uab.es webpage: http://pareto.uab.es/lgambetti/ Description This is

LECTURE 10 LINEAR PROCESSES II: SPECTRAL DENSITY, LAG OPERATOR, ARMA. In this lecture, we continue to discuss covariance stationary processes.

MAY, 0 LECTURE 0 LINEAR PROCESSES II: SPECTRAL DENSITY, LAG OPERATOR, ARMA In this lecture, we continue to discuss covariance stationary processes. Spectral density Gourieroux and Monfort 990), Ch. 5;

MAY, 0 LECTURE 0 LINEAR PROCESSES II: SPECTRAL DENSITY, LAG OPERATOR, ARMA In this lecture, we continue to discuss covariance stationary processes. Spectral density Gourieroux and Monfort 990), Ch. 5;

Problem Set 1 Solution Sketches Time Series Analysis Spring 2010

Problem Set 1 Solution Sketches Time Series Analysis Spring 2010 1. Construct a martingale difference process that is not weakly stationary. Simplest e.g.: Let Y t be a sequence of independent, non-identically

Problem Set 1 Solution Sketches Time Series Analysis Spring 2010 1. Construct a martingale difference process that is not weakly stationary. Simplest e.g.: Let Y t be a sequence of independent, non-identically

Lecture 1: Fundamental concepts in Time Series Analysis (part 2)

") Lecture 1: Fundamental concepts in Time Series Analysis (part 2) Florian Pelgrin University of Lausanne, École des HEC Department of mathematics (IMEA-Nice) Sept. 2011 - Jan. 2012 Florian Pelgrin (HEC)

Lecture 1: Fundamental concepts in Time Series Analysis (part 2) Florian Pelgrin University of Lausanne, École des HEC Department of mathematics (IMEA-Nice) Sept. 2011 - Jan. 2012 Florian Pelgrin (HEC)

Lecture 3 Stationary Processes and the Ergodic LLN (Reference Section 2.2, Hayashi)

") Lecture 3 Stationary Processes and the Ergodic LLN (Reference Section 2.2, Hayashi) Our immediate goal is to formulate an LLN and a CLT which can be applied to establish sufficient conditions for the consistency

Lecture 3 Stationary Processes and the Ergodic LLN (Reference Section 2.2, Hayashi) Our immediate goal is to formulate an LLN and a CLT which can be applied to establish sufficient conditions for the consistency

Class: Trend-Cycle Decomposition

Class: Trend-Cycle Decomposition Macroeconometrics - Spring 2011 Jacek Suda, BdF and PSE June 1, 2011 Outline Outline: 1 Unobserved Component Approach 2 Beveridge-Nelson Decomposition 3 Spectral Analysis

Class: Trend-Cycle Decomposition Macroeconometrics - Spring 2011 Jacek Suda, BdF and PSE June 1, 2011 Outline Outline: 1 Unobserved Component Approach 2 Beveridge-Nelson Decomposition 3 Spectral Analysis

Autoregressive Moving Average (ARMA) Models and their Practical Applications

Models and their Practical Applications") Autoregressive Moving Average (ARMA) Models and their Practical Applications Massimo Guidolin February 2018 1 Essential Concepts in Time Series Analysis 1.1 Time Series and Their Properties Time series:

Autoregressive Moving Average (ARMA) Models and their Practical Applications Massimo Guidolin February 2018 1 Essential Concepts in Time Series Analysis 1.1 Time Series and Their Properties Time series:

A time series is called strictly stationary if the joint distribution of every collection (Y t

5 Time series A time series is a set of observations recorded over time. You can think for example at the GDP of a country over the years (or quarters) or the hourly measurements of temperature over a

5 Time series A time series is a set of observations recorded over time. You can think for example at the GDP of a country over the years (or quarters) or the hourly measurements of temperature over a

2. An Introduction to Moving Average Models and ARMA Models

. An Introduction to Moving Average Models and ARMA Models.1 White Noise. The MA(1) model.3 The MA(q) model..4 Estimation and forecasting of MA models..5 ARMA(p,q) models. The Moving Average (MA) models

. An Introduction to Moving Average Models and ARMA Models.1 White Noise. The MA(1) model.3 The MA(q) model..4 Estimation and forecasting of MA models..5 ARMA(p,q) models. The Moving Average (MA) models

Università di Pavia. Forecasting. Eduardo Rossi

Università di Pavia Forecasting Eduardo Rossi Mean Squared Error Forecast of Y t+1 based on a set of variables observed at date t, X t : Yt+1 t. The loss function MSE(Y t+1 t ) = E[Y t+1 Y t+1 t ]2 The

Università di Pavia Forecasting Eduardo Rossi Mean Squared Error Forecast of Y t+1 based on a set of variables observed at date t, X t : Yt+1 t. The loss function MSE(Y t+1 t ) = E[Y t+1 Y t+1 t ]2 The

Prof. Dr. Roland Füss Lecture Series in Applied Econometrics Summer Term Introduction to Time Series Analysis

Introduction to Time Series Analysis 1 Contents: I. Basics of Time Series Analysis... 4 I.1 Stationarity... 5 I.2 Autocorrelation Function... 9 I.3 Partial Autocorrelation Function (PACF)... 14 I.4 Transformation

Introduction to Time Series Analysis 1 Contents: I. Basics of Time Series Analysis... 4 I.1 Stationarity... 5 I.2 Autocorrelation Function... 9 I.3 Partial Autocorrelation Function (PACF)... 14 I.4 Transformation

EC402: Serial Correlation. Danny Quah Economics Department, LSE Lent 2015

EC402: Serial Correlation Danny Quah Economics Department, LSE Lent 2015 OUTLINE 1. Stationarity 1.1 Covariance stationarity 1.2 Explicit Models. Special cases: ARMA processes 2. Some complex numbers.

EC402: Serial Correlation Danny Quah Economics Department, LSE Lent 2015 OUTLINE 1. Stationarity 1.1 Covariance stationarity 1.2 Explicit Models. Special cases: ARMA processes 2. Some complex numbers.

Time Series Analysis. James D. Hamilton PRINCETON UNIVERSITY PRESS PRINCETON, NEW JERSEY

Time Series Analysis James D. Hamilton PRINCETON UNIVERSITY PRESS PRINCETON, NEW JERSEY PREFACE xiii 1 Difference Equations 1.1. First-Order Difference Equations 1 1.2. pth-order Difference Equations 7

Time Series Analysis James D. Hamilton PRINCETON UNIVERSITY PRESS PRINCETON, NEW JERSEY PREFACE xiii 1 Difference Equations 1.1. First-Order Difference Equations 1 1.2. pth-order Difference Equations 7

Chapter 2. Some basic tools. 2.1 Time series: Theory Stochastic processes

Chapter 2 Some basic tools 2.1 Time series: Theory 2.1.1 Stochastic processes A stochastic process is a sequence of random variables..., x 0, x 1, x 2,.... In this class, the subscript always means time.

Chapter 2 Some basic tools 2.1 Time series: Theory 2.1.1 Stochastic processes A stochastic process is a sequence of random variables..., x 0, x 1, x 2,.... In this class, the subscript always means time.

Ch. 19 Models of Nonstationary Time Series

Ch. 19 Models of Nonstationary Time Series In time series analysis we do not confine ourselves to the analysis of stationary time series. In fact, most of the time series we encounter are non stationary.

Ch. 19 Models of Nonstationary Time Series In time series analysis we do not confine ourselves to the analysis of stationary time series. In fact, most of the time series we encounter are non stationary.

Single Equation Linear GMM with Serially Correlated Moment Conditions

Single Equation Linear GMM with Serially Correlated Moment Conditions Eric Zivot November 2, 2011 Univariate Time Series Let {y t } be an ergodic-stationary time series with E[y t ]=μ and var(y t )

Single Equation Linear GMM with Serially Correlated Moment Conditions Eric Zivot November 2, 2011 Univariate Time Series Let {y t } be an ergodic-stationary time series with E[y t ]=μ and var(y t )

Time Series Analysis -- An Introduction -- AMS 586

Time Series Analysis -- An Introduction -- AMS 586 1 Objectives of time series analysis Data description Data interpretation Modeling Control Prediction & Forecasting 2 Time-Series Data Numerical data

Time Series Analysis -- An Introduction -- AMS 586 1 Objectives of time series analysis Data description Data interpretation Modeling Control Prediction & Forecasting 2 Time-Series Data Numerical data

Notes on Time Series Modeling

Notes on Time Series Modeling Garey Ramey University of California, San Diego January 17 1 Stationary processes De nition A stochastic process is any set of random variables y t indexed by t T : fy t g

Notes on Time Series Modeling Garey Ramey University of California, San Diego January 17 1 Stationary processes De nition A stochastic process is any set of random variables y t indexed by t T : fy t g

Lecture 2: ARMA(p,q) models (part 2)

models (part 2)") Lecture 2: ARMA(p,q) models (part 2) Florian Pelgrin University of Lausanne, École des HEC Department of mathematics (IMEA-Nice) Sept. 2011 - Jan. 2012 Florian Pelgrin (HEC) Univariate time series Sept.

Lecture 2: ARMA(p,q) models (part 2) Florian Pelgrin University of Lausanne, École des HEC Department of mathematics (IMEA-Nice) Sept. 2011 - Jan. 2012 Florian Pelgrin (HEC) Univariate time series Sept.

Time Series 3. Robert Almgren. Sept. 28, 2009

Time Series 3 Robert Almgren Sept. 28, 2009 Last time we discussed two main categories of linear models, and their combination. Here w t denotes a white noise: a stationary process with E w t ) = 0, E

Time Series 3 Robert Almgren Sept. 28, 2009 Last time we discussed two main categories of linear models, and their combination. Here w t denotes a white noise: a stationary process with E w t ) = 0, E

Lecture 3: Autoregressive Moving Average (ARMA) Models and their Practical Applications

Models and their Practical Applications") Lecture 3: Autoregressive Moving Average (ARMA) Models and their Practical Applications Prof. Massimo Guidolin 20192 Financial Econometrics Winter/Spring 2018 Overview Moving average processes Autoregressive

Lecture 3: Autoregressive Moving Average (ARMA) Models and their Practical Applications Prof. Massimo Guidolin 20192 Financial Econometrics Winter/Spring 2018 Overview Moving average processes Autoregressive

LECTURES 2-3 : Stochastic Processes, Autocorrelation function. Stationarity.

LECTURES 2-3 : Stochastic Processes, Autocorrelation function. Stationarity. Important points of Lecture 1: A time series {X t } is a series of observations taken sequentially over time: x t is an observation

LECTURES 2-3 : Stochastic Processes, Autocorrelation function. Stationarity. Important points of Lecture 1: A time series {X t } is a series of observations taken sequentially over time: x t is an observation

Empirical Market Microstructure Analysis (EMMA)

") Empirical Market Microstructure Analysis (EMMA) Lecture 3: Statistical Building Blocks and Econometric Basics Prof. Dr. Michael Stein michael.stein@vwl.uni-freiburg.de Albert-Ludwigs-University of Freiburg

Empirical Market Microstructure Analysis (EMMA) Lecture 3: Statistical Building Blocks and Econometric Basics Prof. Dr. Michael Stein michael.stein@vwl.uni-freiburg.de Albert-Ludwigs-University of Freiburg

Chapter 4: Models for Stationary Time Series

Chapter 4: Models for Stationary Time Series Now we will introduce some useful parametric models for time series that are stationary processes. We begin by defining the General Linear Process. Let {Y t

Chapter 4: Models for Stationary Time Series Now we will introduce some useful parametric models for time series that are stationary processes. We begin by defining the General Linear Process. Let {Y t

Problem Set 2 Solution Sketches Time Series Analysis Spring 2010

Problem Set 2 Solution Sketches Time Series Analysis Spring 2010 Forecasting 1. Let X and Y be two random variables such that E(X 2 ) < and E(Y 2 )

Problem Set 2 Solution Sketches Time Series Analysis Spring 2010 Forecasting 1. Let X and Y be two random variables such that E(X 2 ) < and E(Y 2 )

MA Advanced Econometrics: Applying Least Squares to Time Series

MA Advanced Econometrics: Applying Least Squares to Time Series Karl Whelan School of Economics, UCD February 15, 2011 Karl Whelan (UCD) Time Series February 15, 2011 1 / 24 Part I Time Series: Standard

MA Advanced Econometrics: Applying Least Squares to Time Series Karl Whelan School of Economics, UCD February 15, 2011 Karl Whelan (UCD) Time Series February 15, 2011 1 / 24 Part I Time Series: Standard

Time Series (Part II)

") Time Series (Part II) Luca Gambetti UAB IDEA Winter 2011 1 Contacts Prof.: Luca Gambetti Office: B3-1130 Edifici B Office hours: email: luca.gambetti@uab.es webpage: http://pareto.uab.es/lgambetti/ 2 Goal

Time Series (Part II) Luca Gambetti UAB IDEA Winter 2011 1 Contacts Prof.: Luca Gambetti Office: B3-1130 Edifici B Office hours: email: luca.gambetti@uab.es webpage: http://pareto.uab.es/lgambetti/ 2 Goal

Some Time-Series Models

Some Time-Series Models Outline 1. Stochastic processes and their properties 2. Stationary processes 3. Some properties of the autocorrelation function 4. Some useful models Purely random processes, random

Some Time-Series Models Outline 1. Stochastic processes and their properties 2. Stationary processes 3. Some properties of the autocorrelation function 4. Some useful models Purely random processes, random

Lecture 1: Stationary Time Series Analysis

Syllabus Stationarity ARMA AR MA Model Selection Estimation Lecture 1: Stationary Time Series Analysis 222061-1617: Time Series Econometrics Spring 2018 Jacek Suda Syllabus Stationarity ARMA AR MA Model

Syllabus Stationarity ARMA AR MA Model Selection Estimation Lecture 1: Stationary Time Series Analysis 222061-1617: Time Series Econometrics Spring 2018 Jacek Suda Syllabus Stationarity ARMA AR MA Model

Econ 424 Time Series Concepts

Econ 424 Time Series Concepts Eric Zivot January 20 2015 Time Series Processes Stochastic (Random) Process { 1 2 +1 } = { } = sequence of random variables indexed by time Observed time series of length

Econ 424 Time Series Concepts Eric Zivot January 20 2015 Time Series Processes Stochastic (Random) Process { 1 2 +1 } = { } = sequence of random variables indexed by time Observed time series of length

Applied time-series analysis

Robert M. Kunst robert.kunst@univie.ac.at University of Vienna and Institute for Advanced Studies Vienna October 18, 2011 Outline Introduction and overview Econometric Time-Series Analysis In principle,

Robert M. Kunst robert.kunst@univie.ac.at University of Vienna and Institute for Advanced Studies Vienna October 18, 2011 Outline Introduction and overview Econometric Time-Series Analysis In principle,

Autoregressive and Moving-Average Models

Chapter 3 Autoregressive and Moving-Average Models 3.1 Introduction Let y be a random variable. We consider the elements of an observed time series {y 0,y 1,y2,...,y t } as being realizations of this randoms

Chapter 3 Autoregressive and Moving-Average Models 3.1 Introduction Let y be a random variable. We consider the elements of an observed time series {y 0,y 1,y2,...,y t } as being realizations of this randoms

Time Series Analysis Fall 2008

MIT OpenCourseWare http://ocw.mit.edu 14.384 Time Series Analysis Fall 008 For information about citing these materials or our Terms of Use, visit: http://ocw.mit.edu/terms. Introduction 1 14.384 Time

MIT OpenCourseWare http://ocw.mit.edu 14.384 Time Series Analysis Fall 008 For information about citing these materials or our Terms of Use, visit: http://ocw.mit.edu/terms. Introduction 1 14.384 Time

Statistics of stochastic processes

Introduction Statistics of stochastic processes Generally statistics is performed on observations y 1,..., y n assumed to be realizations of independent random variables Y 1,..., Y n. 14 settembre 2014

Introduction Statistics of stochastic processes Generally statistics is performed on observations y 1,..., y n assumed to be realizations of independent random variables Y 1,..., Y n. 14 settembre 2014

Time Series 2. Robert Almgren. Sept. 21, 2009

Time Series 2 Robert Almgren Sept. 21, 2009 This week we will talk about linear time series models: AR, MA, ARMA, ARIMA, etc. First we will talk about theory and after we will talk about fitting the models

Time Series 2 Robert Almgren Sept. 21, 2009 This week we will talk about linear time series models: AR, MA, ARMA, ARIMA, etc. First we will talk about theory and after we will talk about fitting the models

Nonlinear time series

Based on the book by Fan/Yao: Nonlinear Time Series Robert M. Kunst robert.kunst@univie.ac.at University of Vienna and Institute for Advanced Studies Vienna October 27, 2009 Outline Characteristics of

Based on the book by Fan/Yao: Nonlinear Time Series Robert M. Kunst robert.kunst@univie.ac.at University of Vienna and Institute for Advanced Studies Vienna October 27, 2009 Outline Characteristics of

ARIMA Models. Richard G. Pierse

ARIMA Models Richard G. Pierse 1 Introduction Time Series Analysis looks at the properties of time series from a purely statistical point of view. No attempt is made to relate variables using a priori

ARIMA Models Richard G. Pierse 1 Introduction Time Series Analysis looks at the properties of time series from a purely statistical point of view. No attempt is made to relate variables using a priori

1 Introduction to Generalized Least Squares

ECONOMICS 7344, Spring 2017 Bent E. Sørensen April 12, 2017 1 Introduction to Generalized Least Squares Consider the model Y = Xβ + ɛ, where the N K matrix of regressors X is fixed, independent of the

ECONOMICS 7344, Spring 2017 Bent E. Sørensen April 12, 2017 1 Introduction to Generalized Least Squares Consider the model Y = Xβ + ɛ, where the N K matrix of regressors X is fixed, independent of the

Stat 248 Lab 2: Stationarity, More EDA, Basic TS Models

Stat 248 Lab 2: Stationarity, More EDA, Basic TS Models Tessa L. Childers-Day February 8, 2013 1 Introduction Today s section will deal with topics such as: the mean function, the auto- and cross-covariance

Stat 248 Lab 2: Stationarity, More EDA, Basic TS Models Tessa L. Childers-Day February 8, 2013 1 Introduction Today s section will deal with topics such as: the mean function, the auto- and cross-covariance

Lecture 2: Univariate Time Series

Lecture 2: Univariate Time Series Analysis: Conditional and Unconditional Densities, Stationarity, ARMA Processes Prof. Massimo Guidolin 20192 Financial Econometrics Spring/Winter 2017 Overview Motivation:

Lecture 2: Univariate Time Series Analysis: Conditional and Unconditional Densities, Stationarity, ARMA Processes Prof. Massimo Guidolin 20192 Financial Econometrics Spring/Winter 2017 Overview Motivation:

5 Transfer function modelling

MSc Further Time Series Analysis 5 Transfer function modelling 5.1 The model Consider the construction of a model for a time series (Y t ) whose values are influenced by the earlier values of a series

MSc Further Time Series Analysis 5 Transfer function modelling 5.1 The model Consider the construction of a model for a time series (Y t ) whose values are influenced by the earlier values of a series

STAT 248: EDA & Stationarity Handout 3

STAT 248: EDA & Stationarity Handout 3 GSI: Gido van de Ven September 17th, 2010 1 Introduction Today s section we will deal with the following topics: the mean function, the auto- and crosscovariance

STAT 248: EDA & Stationarity Handout 3 GSI: Gido van de Ven September 17th, 2010 1 Introduction Today s section we will deal with the following topics: the mean function, the auto- and crosscovariance

Multivariate Time Series: VAR(p) Processes and Models

Processes and Models") Multivariate Time Series: VAR(p) Processes and Models A VAR(p) model, for p > 0 is X t = φ 0 + Φ 1 X t 1 + + Φ p X t p + A t, where X t, φ 0, and X t i are k-vectors, Φ 1,..., Φ p are k k matrices, with

Multivariate Time Series: VAR(p) Processes and Models A VAR(p) model, for p > 0 is X t = φ 0 + Φ 1 X t 1 + + Φ p X t p + A t, where X t, φ 0, and X t i are k-vectors, Φ 1,..., Φ p are k k matrices, with

Univariate Time Series Analysis; ARIMA Models

Econometrics 2 Fall 24 Univariate Time Series Analysis; ARIMA Models Heino Bohn Nielsen of4 Outline of the Lecture () Introduction to univariate time series analysis. (2) Stationarity. (3) Characterizing

Econometrics 2 Fall 24 Univariate Time Series Analysis; ARIMA Models Heino Bohn Nielsen of4 Outline of the Lecture () Introduction to univariate time series analysis. (2) Stationarity. (3) Characterizing

Univariate Nonstationary Time Series 1

Univariate Nonstationary Time Series 1 Sebastian Fossati University of Alberta 1 These slides are based on Eric Zivot s time series notes available at: http://faculty.washington.edu/ezivot Introduction

Univariate Nonstationary Time Series 1 Sebastian Fossati University of Alberta 1 These slides are based on Eric Zivot s time series notes available at: http://faculty.washington.edu/ezivot Introduction

AR, MA and ARMA models

AR, MA and AR by Hedibert Lopes P Based on Tsay s Analysis of Financial Time Series (3rd edition) P 1 Stationarity 2 3 4 5 6 7 P 8 9 10 11 Outline P Linear Time Series Analysis and Its Applications For

AR, MA and AR by Hedibert Lopes P Based on Tsay s Analysis of Financial Time Series (3rd edition) P 1 Stationarity 2 3 4 5 6 7 P 8 9 10 11 Outline P Linear Time Series Analysis and Its Applications For

Chapter 1. Basics. 1.1 Definition. A time series (or stochastic process) is a function Xpt, ωq such that for

is a function Xpt, ωq such that for") Chapter 1 Basics 1.1 Definition A time series (or stochastic process) is a function Xpt, ωq such that for each fixed t, Xpt, ωq is a random variable [denoted by X t pωq]. For a fixed ω, Xpt, ωq is simply

Chapter 1 Basics 1.1 Definition A time series (or stochastic process) is a function Xpt, ωq such that for each fixed t, Xpt, ωq is a random variable [denoted by X t pωq]. For a fixed ω, Xpt, ωq is simply

Econometría 2: Análisis de series de Tiempo

Econometría 2: Análisis de series de Tiempo Karoll GOMEZ kgomezp@unal.edu.co http://karollgomez.wordpress.com Segundo semestre 2016 II. Basic definitions A time series is a set of observations X t, each

Econometría 2: Análisis de series de Tiempo Karoll GOMEZ kgomezp@unal.edu.co http://karollgomez.wordpress.com Segundo semestre 2016 II. Basic definitions A time series is a set of observations X t, each

Forecasting and Estimation

February 3, 2009 Forecasting I Very frequently the goal of estimating time series is to provide forecasts of future values. This typically means you treat the data di erently than if you were simply tting

February 3, 2009 Forecasting I Very frequently the goal of estimating time series is to provide forecasts of future values. This typically means you treat the data di erently than if you were simply tting

Part III Example Sheet 1 - Solutions YC/Lent 2015 Comments and corrections should be ed to

TIME SERIES Part III Example Sheet 1 - Solutions YC/Lent 2015 Comments and corrections should be emailed to Y.Chen@statslab.cam.ac.uk. 1. Let {X t } be a weakly stationary process with mean zero and let

TIME SERIES Part III Example Sheet 1 - Solutions YC/Lent 2015 Comments and corrections should be emailed to Y.Chen@statslab.cam.ac.uk. 1. Let {X t } be a weakly stationary process with mean zero and let

Lecture 1: Stationary Time Series Analysis

Syllabus Stationarity ARMA AR MA Model Selection Estimation Forecasting Lecture 1: Stationary Time Series Analysis 222061-1617: Time Series Econometrics Spring 2018 Jacek Suda Syllabus Stationarity ARMA

Syllabus Stationarity ARMA AR MA Model Selection Estimation Forecasting Lecture 1: Stationary Time Series Analysis 222061-1617: Time Series Econometrics Spring 2018 Jacek Suda Syllabus Stationarity ARMA

Covariances of ARMA Processes

Statistics 910, #10 1 Overview Covariances of ARMA Processes 1. Review ARMA models: causality and invertibility 2. AR covariance functions 3. MA and ARMA covariance functions 4. Partial autocorrelation

Statistics 910, #10 1 Overview Covariances of ARMA Processes 1. Review ARMA models: causality and invertibility 2. AR covariance functions 3. MA and ARMA covariance functions 4. Partial autocorrelation

Empirical Macroeconomics

Empirical Macroeconomics Francesco Franco Nova SBE April 5, 2016 Francesco Franco Empirical Macroeconomics 1/39 Growth and Fluctuations Supply and Demand Figure : US dynamics Francesco Franco Empirical

Empirical Macroeconomics Francesco Franco Nova SBE April 5, 2016 Francesco Franco Empirical Macroeconomics 1/39 Growth and Fluctuations Supply and Demand Figure : US dynamics Francesco Franco Empirical

Chapter 3 - Temporal processes

STK4150 - Intro 1 Chapter 3 - Temporal processes Odd Kolbjørnsen and Geir Storvik January 23 2017 STK4150 - Intro 2 Temporal processes Data collected over time Past, present, future, change Temporal aspect

STK4150 - Intro 1 Chapter 3 - Temporal processes Odd Kolbjørnsen and Geir Storvik January 23 2017 STK4150 - Intro 2 Temporal processes Data collected over time Past, present, future, change Temporal aspect

Econometrics II Heij et al. Chapter 7.1

Chapter 7.1 p. 1/2 Econometrics II Heij et al. Chapter 7.1 Linear Time Series Models for Stationary data Marius Ooms Tinbergen Institute Amsterdam Chapter 7.1 p. 2/2 Program Introduction Modelling philosophy

Chapter 7.1 p. 1/2 Econometrics II Heij et al. Chapter 7.1 Linear Time Series Models for Stationary data Marius Ooms Tinbergen Institute Amsterdam Chapter 7.1 p. 2/2 Program Introduction Modelling philosophy

Empirical Macroeconomics

Empirical Macroeconomics Francesco Franco Nova SBE April 18, 2018 Francesco Franco Empirical Macroeconomics 1/23 Invertible Moving Average A difference equation interpretation Consider an invertible MA1)

Empirical Macroeconomics Francesco Franco Nova SBE April 18, 2018 Francesco Franco Empirical Macroeconomics 1/23 Invertible Moving Average A difference equation interpretation Consider an invertible MA1)

Statistical signal processing

Statistical signal processing Short overview of the fundamentals Outline Random variables Random processes Stationarity Ergodicity Spectral analysis Random variable and processes Intuition: A random variable

Statistical signal processing Short overview of the fundamentals Outline Random variables Random processes Stationarity Ergodicity Spectral analysis Random variable and processes Intuition: A random variable

Difference equations. Definitions: A difference equation takes the general form. x t f x t 1,,x t m.

Difference equations Definitions: A difference equation takes the general form x t fx t 1,x t 2, defining the current value of a variable x as a function of previously generated values. A finite order

Difference equations Definitions: A difference equation takes the general form x t fx t 1,x t 2, defining the current value of a variable x as a function of previously generated values. A finite order

γ 0 = Var(X i ) = Var(φ 1 X i 1 +W i ) = φ 2 1γ 0 +σ 2, which implies that we must have φ 1 < 1, and γ 0 = σ2 . 1 φ 2 1 We may also calculate for j 1

= Var(φ 1 X i 1 +W i ) = φ 2 1γ 0 +σ 2, which implies that we must have φ 1 < 1, and γ 0 = σ2 . 1 φ 2 1 We may also calculate for j 1") 4.2 Autoregressive (AR) Moving average models are causal linear processes by definition. There is another class of models, based on a recursive formulation similar to the exponentially weighted moving

4.2 Autoregressive (AR) Moving average models are causal linear processes by definition. There is another class of models, based on a recursive formulation similar to the exponentially weighted moving

4. MA(2) +drift: y t = µ + ɛ t + θ 1 ɛ t 1 + θ 2 ɛ t 2. Mean: where θ(l) = 1 + θ 1 L + θ 2 L 2. Therefore,

+drift: y t = µ + ɛ t + θ 1 ɛ t 1 + θ 2 ɛ t 2. Mean: where θ(l) = 1 + θ 1 L + θ 2 L 2. Therefore,") 61 4. MA(2) +drift: y t = µ + ɛ t + θ 1 ɛ t 1 + θ 2 ɛ t 2 Mean: y t = µ + θ(l)ɛ t, where θ(l) = 1 + θ 1 L + θ 2 L 2. Therefore, E(y t ) = µ + θ(l)e(ɛ t ) = µ 62 Example: MA(q) Model: y t = ɛ t + θ 1 ɛ

61 4. MA(2) +drift: y t = µ + ɛ t + θ 1 ɛ t 1 + θ 2 ɛ t 2 Mean: y t = µ + θ(l)ɛ t, where θ(l) = 1 + θ 1 L + θ 2 L 2. Therefore, E(y t ) = µ + θ(l)e(ɛ t ) = µ 62 Example: MA(q) Model: y t = ɛ t + θ 1 ɛ

Stationary Stochastic Time Series Models

Stationary Stochastic Time Series Models When modeling time series it is useful to regard an observed time series, (x 1,x,..., x n ), as the realisation of a stochastic process. In general a stochastic

Stationary Stochastic Time Series Models When modeling time series it is useful to regard an observed time series, (x 1,x,..., x n ), as the realisation of a stochastic process. In general a stochastic

9. Multivariate Linear Time Series (II). MA6622, Ernesto Mordecki, CityU, HK, 2006.

. MA6622, Ernesto Mordecki, CityU, HK, 2006.") 9. Multivariate Linear Time Series (II). MA6622, Ernesto Mordecki, CityU, HK, 2006. References for this Lecture: Introduction to Time Series and Forecasting. P.J. Brockwell and R. A. Davis, Springer Texts

9. Multivariate Linear Time Series (II). MA6622, Ernesto Mordecki, CityU, HK, 2006. References for this Lecture: Introduction to Time Series and Forecasting. P.J. Brockwell and R. A. Davis, Springer Texts

STA 6857 Autocorrelation and Cross-Correlation & Stationary Time Series ( 1.4, 1.5)

") STA 6857 Autocorrelation and Cross-Correlation & Stationary Time Series ( 1.4, 1.5) Outline 1 Announcements 2 Autocorrelation and Cross-Correlation 3 Stationary Time Series 4 Homework 1c Arthur Berg STA

STA 6857 Autocorrelation and Cross-Correlation & Stationary Time Series ( 1.4, 1.5) Outline 1 Announcements 2 Autocorrelation and Cross-Correlation 3 Stationary Time Series 4 Homework 1c Arthur Berg STA

6.3 Forecasting ARMA processes

6.3. FORECASTING ARMA PROCESSES 123 6.3 Forecasting ARMA processes The purpose of forecasting is to predict future values of a TS based on the data collected to the present. In this section we will discuss

6.3. FORECASTING ARMA PROCESSES 123 6.3 Forecasting ARMA processes The purpose of forecasting is to predict future values of a TS based on the data collected to the present. In this section we will discuss

Estimating Moving Average Processes with an improved version of Durbin s Method

Estimating Moving Average Processes with an improved version of Durbin s Method Maximilian Ludwig this version: June 7, 4, initial version: April, 3 arxiv:347956v [statme] 6 Jun 4 Abstract This paper provides

Estimating Moving Average Processes with an improved version of Durbin s Method Maximilian Ludwig this version: June 7, 4, initial version: April, 3 arxiv:347956v [statme] 6 Jun 4 Abstract This paper provides

Stochastic Processes: I. consider bowl of worms model for oscilloscope experiment:

Stochastic Processes: I consider bowl of worms model for oscilloscope experiment: SAPAscope 2.0 / 0 1 RESET SAPA2e 22, 23 II 1 stochastic process is: Stochastic Processes: II informally: bowl + drawing

Stochastic Processes: I consider bowl of worms model for oscilloscope experiment: SAPAscope 2.0 / 0 1 RESET SAPA2e 22, 23 II 1 stochastic process is: Stochastic Processes: II informally: bowl + drawing

Lecture on ARMA model

Lecture on ARMA model Robert M. de Jong Ohio State University Columbus, OH 43210 USA Chien-Ho Wang National Taipei University Taipei City, 104 Taiwan ROC October 19, 2006 (Very Preliminary edition, Comment

Lecture on ARMA model Robert M. de Jong Ohio State University Columbus, OH 43210 USA Chien-Ho Wang National Taipei University Taipei City, 104 Taiwan ROC October 19, 2006 (Very Preliminary edition, Comment

Multivariate Time Series

Multivariate Time Series Notation: I do not use boldface (or anything else) to distinguish vectors from scalars. Tsay (and many other writers) do. I denote a multivariate stochastic process in the form

Multivariate Time Series Notation: I do not use boldface (or anything else) to distinguish vectors from scalars. Tsay (and many other writers) do. I denote a multivariate stochastic process in the form

Strictly Stationary Solutions of Autoregressive Moving Average Equations

Strictly Stationary Solutions of Autoregressive Moving Average Equations Peter J. Brockwell Alexander Lindner Abstract Necessary and sufficient conditions for the existence of a strictly stationary solution

Strictly Stationary Solutions of Autoregressive Moving Average Equations Peter J. Brockwell Alexander Lindner Abstract Necessary and sufficient conditions for the existence of a strictly stationary solution

STAT 443 Final Exam Review. 1 Basic Definitions. 2 Statistical Tests. L A TEXer: W. Kong

STAT 443 Final Exam Review L A TEXer: W Kong 1 Basic Definitions Definition 11 The time series {X t } with E[X 2 t ] < is said to be weakly stationary if: 1 µ X (t) = E[X t ] is independent of t 2 γ X

STAT 443 Final Exam Review L A TEXer: W Kong 1 Basic Definitions Definition 11 The time series {X t } with E[X 2 t ] < is said to be weakly stationary if: 1 µ X (t) = E[X t ] is independent of t 2 γ X