FIN822 project 2 Project 2 contains part I and part II. (Due on November 10, 2008)

|

|

|

- Melinda Lewis

- 6 years ago

- Views:

Transcription

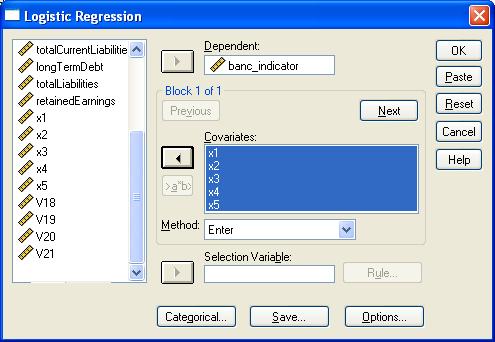

1 FIN822 project 2 Project 2 contains part I and part II. (Due on November 10, 2008) Part I Logit Model in Bankruptcy Prediction You do not believe in Altman and you decide to estimate the bankruptcy prediction model using the following logit model: y= Λ (a+b1* X1+b2* X2+b3* X3+b4* X4+b5* X5) + error term where variables are defined as: X1: re_ta=retainedearnings/totalassets X2: cacl_ta=(totalcurrentassetstotalcurrentliabilities)/totalassets X3: ebit_ta=earningsbeforeinterestandtaxes/totalassets (Do not use ROA) X4: totalliabilities/totalassets X5: totalrevenue/totalassets y= banc_indicator: a dummy variable that takes value of 1 if the firm goes bankrupt in year 2004 or 2005, and 0 otherwise. Download data that I have constructed from my web Say a few words on your sample (how many firms in total, how many went bankruptcy? etc). Report your estimated coefficients and the respective t-statistics (or p-values). Which variable(s) are significant at 0.05 levels? Do the results make sense? Based on your logit model output, what is the estimated bankruptcy probability for a firm with the following ratios: x1=0.2, x2=1, x3= - 20%, x4=0.7, x5=1? (Think of the in-class-work question on high school student graduation probability.) Tips: For illustration I will used an abbreviated version of the dataset which contains fewer observations. You should use the full sample.

2 Analyze>Regression>Binary Logistic 2

3 Coefficients are given in this table (you should expect different results): B are estimated coefficients, Sig. are the p-values. Ignore other statistics. Step 1 a x1 x2 x3 x4 x5 Variables in the Equation B S.E. Wald df Sig. Exp(B) Constant a. Variable(s) entered on step 1: x1, x2, x3, x4, x5. The numbers of non-bankrupt and bankrupt firms can be seen from this table: Classification Table(a,b) Predicted Percentage banc_indicator Correct Observed Step banc_indicator Overall Percentage 99.3 a Constant is included in the model. b The cut value is.500 3

in your ARIMA model. Write down the dynamic structure for the original time series. A tutorial is attached below.")

4 Part II. Conduct an analysis on a time series. Download data that I have constructed from Explain how you have chosen the number of lags (p=?, q=?) in your ARIMA model. Write down the dynamic structure for the original time series. A tutorial is attached below. You can estimate the time series using either of the two approaches illustrated in the example below. Time-Series Analysis Example Suppose you are given a time-series. The example data is available from my website at First, load in SPSS. If you see the following window, click cancel. Then open the excel file. Note that you should choose All Files (*.*) in the following window. Otherwise you may not see the excel file. 4

5 Click Ok if you see this. 5

6 Let s take a look at the time-series plot. Pull down the menu: Analyze> Times Series> Sequence Chart Then choose Y and X axis, and click OK Copy object and paste it below. The plot looks like this x

7 If you want to see a better-looking picture with horizontal axis shown, you have to export the graph as a PDF file or PowerPoint file and then select-paste it. What a pain It will look like this. Clearly there is a trend in this series. So I can either (1) run a regression on time (t) and get the residuals, or (2) compute the first difference. 7

8 First approach: regress the series on t Analyze>regression>linear Choose X as dependent variable, t as independent variable. Also click Save 8

Unstandardized Coefficients Standardized Coefficients t Sig. Model B Std. Error Beta B Std. Error 1 (Constant) 3.375.466 7.239.000 t.795.")

9 Select Unstandarized Residuals in the above window. This will save the residual from regression. Click Continue, OK Here is regression output: Coefficients(a) Unstandardized Coefficients Standardized Coefficients t Sig. Model B Std. Error Beta B Std. Error 1 (Constant) t a Dependent Variable: x You also see estimated residuals in the 3 rd column in the SPSS data window. (Below) 9

10 Now let s see a plot of the residual. It appears stationary Unstandardized Residual

11 Then let s draw the autocorrelation function (ACF) and partial-autocorrelation function (PACF) graphs for this residual. Analyze>Times Series>Autocorrelations Choose the unstandarized residuals as our interested variables. Click OK. Unstandardized Residual 1.0 Coefficient Upper Confidence L Lower Confidence L 0.5 ACF

12 Unstandardized Residual 1.0 Coefficient Upper Confidence L Lower Confidence L 0.5 Partial ACF From the above graphs, the ACF decays gradually while the PACF stands out only for lag 1. So a ARIMA(1,0,0)=ARMA(1,0)=AR(1) model may be appropriate. You also see some info like this 12

13 Series: Unstandardized Residual Lag Autocorrelations Autocorrel Box-Ljung Statistic ation Std. Error a Value df Sig. b a. The underlying process assumed is independence (white noise). b. Based on the asymptotic chi-square approximation. The p-value (Sig.) based on Box-Ljung statistic is significant for each lag. This means the time-series of unstandarized residuals are significantly different from a white noise process by examining all autocorrelations up to that lag. (We already know this because, from the two graphs above, the ACF and PACF at lag 1 are significant.) Then run the ARIMA model, Analyze>Times Series> ARIMA 13

14 Choose 1 for p and click OK. Choose Unstandarized residuals as the variable Then you will see this. It tells us that SPSS will add some residuals, fitted variable, and confidence intervals, to our dataset. Click OK. Here is the ARIMA coefficient estimate: Parameter Estimates Estimates Std Error t Approx Sig Non-Seasonal Lags AR Constant Melard's algorithm was used for estimation. (About the constant term: When d=0 a constant term equals to the mean of the time series. When d=1 a constant term reflects the non-zero average trend of the original time series.) 14

Analyze>Times Series> Autocorrelations.")

15 In the data window we also see that the residual from ARIMA modeling, under the name ERR_1 Did our model do a good job? Let s see the ACF and PACF of the new residual ERR_1 (This is the residual from ARIMA model, not the one from linear regression) Analyze>Times Series> Autocorrelations... Then update the name of our interested variable (as shown in the window below 15

16 Click OK. Error for RES_1 from ARIMA, MOD_2, CON 1.0 Coefficient Upper Confidence L Lower Confidence L 0.5 ACF Error for RES_1 from ARIMA, MOD_2, CON 1.0 Coefficient Upper Confidence L Lower Confidence L 0.5 Partial ACF No significant ACF or PACF, so the residual from our ARIMA modeling seems to be white noise. Our modeling job has finished. 16

17 What is the structure of the original time series? Let me call the residual from the linear regression (first step) z. So from ARIMA modeling: Parameter Estimates Estimates Std Error t Approx Sig Non-Seasonal Lags AR Constant Melard's algorithm was used for estimation. (About the constant term: When d=0 a constant term equals to the mean of the time series. When d=1 a constant term reflects the non-zero average trend of the original time series.) We have: ( z 0.011) = 0.451*( z 0.011) + ε (1) t t 1 t From step 1 linear regression, we know that x = * t+ z (2) t t Combing the two equations (1) and (2) together, we have ( x * t 0.011) = 0.451*( x *( t 1) 0.011) + ε t t 1 t That can be simplified as: x = * x * t+ ε (3) t t 1 t (3) is our description of the original time-series. 17

18 Second approach: Using the first difference Open the excel data file, compute first difference and call the variable u. Save the file. In SPSS, open the excel file just saved. Files of Type should choose All Files (*.*) Click OK 18

19 Plot the differenced series u. Analyze>Times Series>Sequence chart It appears stationary u Then plot the ACF and PACF graph for u ( u is the first difference of the original series ) 19

20 u 1.0 Coefficient Upper Confidence L Lower Confidence L 0.5 ACF u 1.0 Coefficient Upper Confidence L Lower Confidence L 0.5 Partial ACF The ACF and PACF both seems to decay over lags. So I choose an ARMA(1,1) model. (Some people might think it is an MA(1) but you will find out the residual from an MA(1) does not really follow a white noise. Sometimes the estimation does require try-and-error. ) 20

21 To estimate the parameters, we go Analyze > Times Series > ARIMA Select the differenced series u as dependent variable.then choose p=1 and q=1 in the window below. Alternatively, you can specify: p=1, d=1, and q=1 for the original series x. You will get same output. 21

22 Click Ok Click Ok Below is our model parameter estimates Parameter Estimates Estimates Std Error t Approx Sig Non-Seasonal AR Lags MA Constant Melard's algorithm was used for estimation. (About the constant term: When d=0 a constant term equals to the mean of the time series. When d=1 a constant term reflects the non-zero average trend of the original time series.) Did the model do a good job? We can check the ACF, PACF of the newly obtained residual and the Box- Ljung statistics. 22

23 Error for u from ARIMA, MOD_1, CON Error for u from ARIMA, MOD_1, CON 1.0 Coefficient Upper Confidence L Lower Confidence L 1.0 Coefficient Upper Confidence L Lower Confidence L ACF 0.0 Partial ACF Judging from the ACF and PACF the residual from ARIMA seems to be white noise, also the Box-Ljung statistics are not significant, so we can stop now. Autocorrelations Series: Error for u from ARIMA, MOD_1, CON Lag Autocorrel Box-Ljung Statistic ation Std. Error a Value df Sig. b a. The underlying process assumed is independence (white noise). b. Based on the asymptotic chi-square approximation. 23

24 What is the structure of the original time series? From ARIMA modeling, we have Parameter Estimates Estimates Std Error t Approx Sig Non-Seasonal AR Lags MA Constant Melard's algorithm was used for estimation. (About the constant term: When d=0 a constant term equals to the mean of the time series. When d=1 a constant term reflects the non-zero average trend of the original time series.) So, ( u 0.794) = 0.470( u 0.794) + ε 0.986* ε (4) t t 1 t t 1 By the way, SPSS tries to behave special and naughty, so unlike the general assumption as in other softwares which assume: X = φ X + φ X φ X + ε + θε + θ ε θ ε SPSS would assume a form: X = φ X + φ X φ X + ε θε θ ε... θ ε That is why you see a negative for the coefficient before In step 1, we took a first difference. That means: Combining the (4) and (5), we get: t 1 t 1 2 t 2 p t p t 1 t 1 2 t 2 q t q t 1 t 1 2 t 2 p t p t 1 t 1 2 t 2 q t q εt 1 xt = xt 1 + ut (5) x = x 0.47x + ε ε (6) t t 1 t 2 t t 1 (6) is our description of the original time-series. 24

25 Final comments Using two approaches we have derived the structure (3) and (6) respectively for the original time series. Are the structure (3) and (6) similar? (Did we get similar results using two different approaches?) Below I will show you that the two results indeed are very close. x = x * t+ ε (3) t t 1 t From (3) we can write xt 1 as x = x ( t 1) + ε (3') t 1 t 2 t 1 Subtract (3 ) from (3), we get x x = 0.451x 0.451x ε ε t t 1 t 1 t 2 t t 1 Which can be simplified to x = x 0.451x + ε ε t t 1 t 2 t t 1 This indeed is very close to equation (6) we derived using the second approach. 25

Scenario 5: Internet Usage Solution. θ j

Scenario : Internet Usage Solution Some more information would be interesting about the study in order to know if we can generalize possible findings. For example: Does each data point consist of the total

Scenario : Internet Usage Solution Some more information would be interesting about the study in order to know if we can generalize possible findings. For example: Does each data point consist of the total

FORECASTING SUGARCANE PRODUCTION IN INDIA WITH ARIMA MODEL

FORECASTING SUGARCANE PRODUCTION IN INDIA WITH ARIMA MODEL B. N. MANDAL Abstract: Yearly sugarcane production data for the period of - to - of India were analyzed by time-series methods. Autocorrelation

FORECASTING SUGARCANE PRODUCTION IN INDIA WITH ARIMA MODEL B. N. MANDAL Abstract: Yearly sugarcane production data for the period of - to - of India were analyzed by time-series methods. Autocorrelation

Minitab Project Report - Assignment 6

.. Sunspot data Minitab Project Report - Assignment Time Series Plot of y Time Series Plot of X y X 7 9 7 9 The data have a wavy pattern. However, they do not show any seasonality. There seem to be an

.. Sunspot data Minitab Project Report - Assignment Time Series Plot of y Time Series Plot of X y X 7 9 7 9 The data have a wavy pattern. However, they do not show any seasonality. There seem to be an

Advanced Quantitative Data Analysis

Chapter 24 Advanced Quantitative Data Analysis Daniel Muijs Doing Regression Analysis in SPSS When we want to do regression analysis in SPSS, we have to go through the following steps: 1 As usual, we choose

Chapter 24 Advanced Quantitative Data Analysis Daniel Muijs Doing Regression Analysis in SPSS When we want to do regression analysis in SPSS, we have to go through the following steps: 1 As usual, we choose

Basics: Definitions and Notation. Stationarity. A More Formal Definition

Basics: Definitions and Notation A Univariate is a sequence of measurements of the same variable collected over (usually regular intervals of) time. Usual assumption in many time series techniques is that

Basics: Definitions and Notation A Univariate is a sequence of measurements of the same variable collected over (usually regular intervals of) time. Usual assumption in many time series techniques is that

Lab: Box-Jenkins Methodology - US Wholesale Price Indicator

Lab: Box-Jenkins Methodology - US Wholesale Price Indicator In this lab we explore the Box-Jenkins methodology by applying it to a time-series data set comprising quarterly observations of the US Wholesale

Lab: Box-Jenkins Methodology - US Wholesale Price Indicator In this lab we explore the Box-Jenkins methodology by applying it to a time-series data set comprising quarterly observations of the US Wholesale

1 Correlation and Inference from Regression

1 Correlation and Inference from Regression Reading: Kennedy (1998) A Guide to Econometrics, Chapters 4 and 6 Maddala, G.S. (1992) Introduction to Econometrics p. 170-177 Moore and McCabe, chapter 12 is

1 Correlation and Inference from Regression Reading: Kennedy (1998) A Guide to Econometrics, Chapters 4 and 6 Maddala, G.S. (1992) Introduction to Econometrics p. 170-177 Moore and McCabe, chapter 12 is

The log transformation produces a time series whose variance can be treated as constant over time.

TAT 520 Homework 6 Fall 2017 Note: Problem 5 is mandatory for graduate students and extra credit for undergraduates. 1) The quarterly earnings per share for 1960-1980 are in the object in the TA package.

TAT 520 Homework 6 Fall 2017 Note: Problem 5 is mandatory for graduate students and extra credit for undergraduates. 1) The quarterly earnings per share for 1960-1980 are in the object in the TA package.

MODELING INFLATION RATES IN NIGERIA: BOX-JENKINS APPROACH. I. U. Moffat and A. E. David Department of Mathematics & Statistics, University of Uyo, Uyo

Vol.4, No.2, pp.2-27, April 216 MODELING INFLATION RATES IN NIGERIA: BOX-JENKINS APPROACH I. U. Moffat and A. E. David Department of Mathematics & Statistics, University of Uyo, Uyo ABSTRACT: This study

Vol.4, No.2, pp.2-27, April 216 MODELING INFLATION RATES IN NIGERIA: BOX-JENKINS APPROACH I. U. Moffat and A. E. David Department of Mathematics & Statistics, University of Uyo, Uyo ABSTRACT: This study

TIME SERIES ANALYSIS AND FORECASTING USING THE STATISTICAL MODEL ARIMA

CHAPTER 6 TIME SERIES ANALYSIS AND FORECASTING USING THE STATISTICAL MODEL ARIMA 6.1. Introduction A time series is a sequence of observations ordered in time. A basic assumption in the time series analysis

CHAPTER 6 TIME SERIES ANALYSIS AND FORECASTING USING THE STATISTICAL MODEL ARIMA 6.1. Introduction A time series is a sequence of observations ordered in time. A basic assumption in the time series analysis

Final Examination 7/6/2011

The Islamic University of Gaza Faculty of Commerce Department of Economics & Applied Statistics Time Series Analysis - Dr. Samir Safi Spring Semester 211 Final Examination 7/6/211 Name: ID: INSTRUCTIONS:

The Islamic University of Gaza Faculty of Commerce Department of Economics & Applied Statistics Time Series Analysis - Dr. Samir Safi Spring Semester 211 Final Examination 7/6/211 Name: ID: INSTRUCTIONS:

Using SPSS for One Way Analysis of Variance

Using SPSS for One Way Analysis of Variance This tutorial will show you how to use SPSS version 12 to perform a one-way, between- subjects analysis of variance and related post-hoc tests. This tutorial

Using SPSS for One Way Analysis of Variance This tutorial will show you how to use SPSS version 12 to perform a one-way, between- subjects analysis of variance and related post-hoc tests. This tutorial

TESTING FOR CO-INTEGRATION

Bo Sjö 2010-12-05 TESTING FOR CO-INTEGRATION To be used in combination with Sjö (2008) Testing for Unit Roots and Cointegration A Guide. Instructions: Use the Johansen method to test for Purchasing Power

Bo Sjö 2010-12-05 TESTING FOR CO-INTEGRATION To be used in combination with Sjö (2008) Testing for Unit Roots and Cointegration A Guide. Instructions: Use the Johansen method to test for Purchasing Power

at least 50 and preferably 100 observations should be available to build a proper model

III Box-Jenkins Methods 1. Pros and Cons of ARIMA Forecasting a) need for data at least 50 and preferably 100 observations should be available to build a proper model used most frequently for hourly or

III Box-Jenkins Methods 1. Pros and Cons of ARIMA Forecasting a) need for data at least 50 and preferably 100 observations should be available to build a proper model used most frequently for hourly or

Investigating Models with Two or Three Categories

Ronald H. Heck and Lynn N. Tabata 1 Investigating Models with Two or Three Categories For the past few weeks we have been working with discriminant analysis. Let s now see what the same sort of model might

Ronald H. Heck and Lynn N. Tabata 1 Investigating Models with Two or Three Categories For the past few weeks we have been working with discriminant analysis. Let s now see what the same sort of model might

Lecture 5: Estimation of time series

Lecture 5, page 1 Lecture 5: Estimation of time series Outline of lesson 5 (chapter 4) (Extended version of the book): a.) Model formulation Explorative analyses Model formulation b.) Model estimation

Lecture 5, page 1 Lecture 5: Estimation of time series Outline of lesson 5 (chapter 4) (Extended version of the book): a.) Model formulation Explorative analyses Model formulation b.) Model estimation

Firstly, the dataset is cleaned and the years and months are separated to provide better distinction (sample below).

.") Project: Forecasting Sales Step 1: Plan Your Analysis Answer the following questions to help you plan out your analysis: 1. Does the dataset meet the criteria of a time series dataset? Make sure to explore

Project: Forecasting Sales Step 1: Plan Your Analysis Answer the following questions to help you plan out your analysis: 1. Does the dataset meet the criteria of a time series dataset? Make sure to explore

Circle a single answer for each multiple choice question. Your choice should be made clearly.

TEST #1 STA 4853 March 4, 215 Name: Please read the following directions. DO NOT TURN THE PAGE UNTIL INSTRUCTED TO DO SO Directions This exam is closed book and closed notes. There are 31 questions. Circle

TEST #1 STA 4853 March 4, 215 Name: Please read the following directions. DO NOT TURN THE PAGE UNTIL INSTRUCTED TO DO SO Directions This exam is closed book and closed notes. There are 31 questions. Circle

Suan Sunandha Rajabhat University

Forecasting Exchange Rate between Thai Baht and the US Dollar Using Time Series Analysis Kunya Bowornchockchai Suan Sunandha Rajabhat University INTRODUCTION The objective of this research is to forecast

Forecasting Exchange Rate between Thai Baht and the US Dollar Using Time Series Analysis Kunya Bowornchockchai Suan Sunandha Rajabhat University INTRODUCTION The objective of this research is to forecast

Chapter 6: Model Specification for Time Series

Chapter 6: Model Specification for Time Series The ARIMA(p, d, q) class of models as a broad class can describe many real time series. Model specification for ARIMA(p, d, q) models involves 1. Choosing

Chapter 6: Model Specification for Time Series The ARIMA(p, d, q) class of models as a broad class can describe many real time series. Model specification for ARIMA(p, d, q) models involves 1. Choosing

Simple Linear Regression

Simple Linear Regression 1 Correlation indicates the magnitude and direction of the linear relationship between two variables. Linear Regression: variable Y (criterion) is predicted by variable X (predictor)

Simple Linear Regression 1 Correlation indicates the magnitude and direction of the linear relationship between two variables. Linear Regression: variable Y (criterion) is predicted by variable X (predictor)

Univariate ARIMA Models

Univariate ARIMA Models ARIMA Model Building Steps: Identification: Using graphs, statistics, ACFs and PACFs, transformations, etc. to achieve stationary and tentatively identify patterns and model components.

Univariate ARIMA Models ARIMA Model Building Steps: Identification: Using graphs, statistics, ACFs and PACFs, transformations, etc. to achieve stationary and tentatively identify patterns and model components.

Circle the single best answer for each multiple choice question. Your choice should be made clearly.

TEST #1 STA 4853 March 6, 2017 Name: Please read the following directions. DO NOT TURN THE PAGE UNTIL INSTRUCTED TO DO SO Directions This exam is closed book and closed notes. There are 32 multiple choice

TEST #1 STA 4853 March 6, 2017 Name: Please read the following directions. DO NOT TURN THE PAGE UNTIL INSTRUCTED TO DO SO Directions This exam is closed book and closed notes. There are 32 multiple choice

Decision 411: Class 9. HW#3 issues

Decision 411: Class 9 Presentation/discussion of HW#3 Introduction to ARIMA models Rules for fitting nonseasonal models Differencing and stationarity Reading the tea leaves : : ACF and PACF plots Unit

Decision 411: Class 9 Presentation/discussion of HW#3 Introduction to ARIMA models Rules for fitting nonseasonal models Differencing and stationarity Reading the tea leaves : : ACF and PACF plots Unit

University of Oxford. Statistical Methods Autocorrelation. Identification and Estimation

University of Oxford Statistical Methods Autocorrelation Identification and Estimation Dr. Órlaith Burke Michaelmas Term, 2011 Department of Statistics, 1 South Parks Road, Oxford OX1 3TG Contents 1 Model

University of Oxford Statistical Methods Autocorrelation Identification and Estimation Dr. Órlaith Burke Michaelmas Term, 2011 Department of Statistics, 1 South Parks Road, Oxford OX1 3TG Contents 1 Model

IT 403 Practice Problems (2-2) Answers

Answers") IT 403 Practice Problems (2-2) Answers #1. Which of the following is correct with respect to the correlation coefficient (r) and the slope of the leastsquares regression line (Choose one)? a. They will

IT 403 Practice Problems (2-2) Answers #1. Which of the following is correct with respect to the correlation coefficient (r) and the slope of the leastsquares regression line (Choose one)? a. They will

Computer simulation of radioactive decay

Computer simulation of radioactive decay y now you should have worked your way through the introduction to Maple, as well as the introduction to data analysis using Excel Now we will explore radioactive

Computer simulation of radioactive decay y now you should have worked your way through the introduction to Maple, as well as the introduction to data analysis using Excel Now we will explore radioactive

THE UNIVERSITY OF CHICAGO Graduate School of Business Business 41202, Spring Quarter 2003, Mr. Ruey S. Tsay

THE UNIVERSITY OF CHICAGO Graduate School of Business Business 41202, Spring Quarter 2003, Mr. Ruey S. Tsay Solutions to Homework Assignment #4 May 9, 2003 Each HW problem is 10 points throughout this

THE UNIVERSITY OF CHICAGO Graduate School of Business Business 41202, Spring Quarter 2003, Mr. Ruey S. Tsay Solutions to Homework Assignment #4 May 9, 2003 Each HW problem is 10 points throughout this

Forecasting using R. Rob J Hyndman. 3.2 Dynamic regression. Forecasting using R 1

Forecasting using R Rob J Hyndman 3.2 Dynamic regression Forecasting using R 1 Outline 1 Regression with ARIMA errors 2 Stochastic and deterministic trends 3 Periodic seasonality 4 Lab session 14 5 Dynamic

Forecasting using R Rob J Hyndman 3.2 Dynamic regression Forecasting using R 1 Outline 1 Regression with ARIMA errors 2 Stochastic and deterministic trends 3 Periodic seasonality 4 Lab session 14 5 Dynamic

Problem Set 2: Box-Jenkins methodology

Problem Set : Box-Jenkins methodology 1) For an AR1) process we have: γ0) = σ ε 1 φ σ ε γ0) = 1 φ Hence, For a MA1) process, p lim R = φ γ0) = 1 + θ )σ ε σ ε 1 = γ0) 1 + θ Therefore, p lim R = 1 1 1 +

Problem Set : Box-Jenkins methodology 1) For an AR1) process we have: γ0) = σ ε 1 φ σ ε γ0) = 1 φ Hence, For a MA1) process, p lim R = φ γ0) = 1 + θ )σ ε σ ε 1 = γ0) 1 + θ Therefore, p lim R = 1 1 1 +

NANYANG TECHNOLOGICAL UNIVERSITY SEMESTER II EXAMINATION MAS451/MTH451 Time Series Analysis TIME ALLOWED: 2 HOURS

NANYANG TECHNOLOGICAL UNIVERSITY SEMESTER II EXAMINATION 2012-2013 MAS451/MTH451 Time Series Analysis May 2013 TIME ALLOWED: 2 HOURS INSTRUCTIONS TO CANDIDATES 1. This examination paper contains FOUR (4)

NANYANG TECHNOLOGICAL UNIVERSITY SEMESTER II EXAMINATION 2012-2013 MAS451/MTH451 Time Series Analysis May 2013 TIME ALLOWED: 2 HOURS INSTRUCTIONS TO CANDIDATES 1. This examination paper contains FOUR (4)

Regression of Inflation on Percent M3 Change

ECON 497 Final Exam Page of ECON 497: Economic Research and Forecasting Name: Spring 2006 Bellas Final Exam Return this exam to me by midnight on Thursday, April 27. It may be e-mailed to me. It may be

ECON 497 Final Exam Page of ECON 497: Economic Research and Forecasting Name: Spring 2006 Bellas Final Exam Return this exam to me by midnight on Thursday, April 27. It may be e-mailed to me. It may be

Introduction. Pre-Lab Questions: Physics 1CL PERIODIC MOTION - PART II Fall 2009

Introduction This is the second of two labs on simple harmonic motion (SHM). In the first lab you studied elastic forces and elastic energy, and you measured the net force on a pendulum bob held at an

Introduction This is the second of two labs on simple harmonic motion (SHM). In the first lab you studied elastic forces and elastic energy, and you measured the net force on a pendulum bob held at an

176 Index. G Gradient, 4, 17, 22, 24, 42, 44, 45, 51, 52, 55, 56

References Aljandali, A. (2014). Exchange rate forecasting: Regional applications to ASEAN, CACM, MERCOSUR and SADC countries. Unpublished PhD thesis, London Metropolitan University, London. Aljandali,

References Aljandali, A. (2014). Exchange rate forecasting: Regional applications to ASEAN, CACM, MERCOSUR and SADC countries. Unpublished PhD thesis, London Metropolitan University, London. Aljandali,

2 Prediction and Analysis of Variance

2 Prediction and Analysis of Variance Reading: Chapters and 2 of Kennedy A Guide to Econometrics Achen, Christopher H. Interpreting and Using Regression (London: Sage, 982). Chapter 4 of Andy Field, Discovering

2 Prediction and Analysis of Variance Reading: Chapters and 2 of Kennedy A Guide to Econometrics Achen, Christopher H. Interpreting and Using Regression (London: Sage, 982). Chapter 4 of Andy Field, Discovering

Time Series I Time Domain Methods

Astrostatistics Summer School Penn State University University Park, PA 16802 May 21, 2007 Overview Filtering and the Likelihood Function Time series is the study of data consisting of a sequence of DEPENDENT

Astrostatistics Summer School Penn State University University Park, PA 16802 May 21, 2007 Overview Filtering and the Likelihood Function Time series is the study of data consisting of a sequence of DEPENDENT

The ARIMA Procedure: The ARIMA Procedure

Page 1 of 120 Overview: ARIMA Procedure Getting Started: ARIMA Procedure The Three Stages of ARIMA Modeling Identification Stage Estimation and Diagnostic Checking Stage Forecasting Stage Using ARIMA Procedure

Page 1 of 120 Overview: ARIMA Procedure Getting Started: ARIMA Procedure The Three Stages of ARIMA Modeling Identification Stage Estimation and Diagnostic Checking Stage Forecasting Stage Using ARIMA Procedure

SPSS LAB FILE 1

SPSS LAB FILE www.mcdtu.wordpress.com 1 www.mcdtu.wordpress.com 2 www.mcdtu.wordpress.com 3 OBJECTIVE 1: Transporation of Data Set to SPSS Editor INPUTS: Files: group1.xlsx, group1.txt PROCEDURE FOLLOWED:

SPSS LAB FILE www.mcdtu.wordpress.com 1 www.mcdtu.wordpress.com 2 www.mcdtu.wordpress.com 3 OBJECTIVE 1: Transporation of Data Set to SPSS Editor INPUTS: Files: group1.xlsx, group1.txt PROCEDURE FOLLOWED:

MAT3379 (Winter 2016)

") MAT3379 (Winter 2016) Assignment 4 - SOLUTIONS The following questions will be marked: 1a), 2, 4, 6, 7a Total number of points for Assignment 4: 20 Q1. (Theoretical Question, 2 points). Yule-Walker estimation

MAT3379 (Winter 2016) Assignment 4 - SOLUTIONS The following questions will be marked: 1a), 2, 4, 6, 7a Total number of points for Assignment 4: 20 Q1. (Theoretical Question, 2 points). Yule-Walker estimation

Chapter 19: Logistic regression

Chapter 19: Logistic regression Self-test answers SELF-TEST Rerun this analysis using a stepwise method (Forward: LR) entry method of analysis. The main analysis To open the main Logistic Regression dialog

Chapter 19: Logistic regression Self-test answers SELF-TEST Rerun this analysis using a stepwise method (Forward: LR) entry method of analysis. The main analysis To open the main Logistic Regression dialog

EDF 7405 Advanced Quantitative Methods in Educational Research MULTR.SAS

EDF 7405 Advanced Quantitative Methods in Educational Research MULTR.SAS The data used in this example describe teacher and student behavior in 8 classrooms. The variables are: Y percentage of interventions

EDF 7405 Advanced Quantitative Methods in Educational Research MULTR.SAS The data used in this example describe teacher and student behavior in 8 classrooms. The variables are: Y percentage of interventions

Introduction. Pre-Lab Questions: Physics 1CL PERIODIC MOTION - PART II Spring 2009

Introduction This is the second of two labs on simple harmonic motion (SHM). In the first lab you studied elastic forces and elastic energy, and you measured the net force on a pendulum bob held at an

Introduction This is the second of two labs on simple harmonic motion (SHM). In the first lab you studied elastic forces and elastic energy, and you measured the net force on a pendulum bob held at an

Inference with Simple Regression

1 Introduction Inference with Simple Regression Alan B. Gelder 06E:071, The University of Iowa 1 Moving to infinite means: In this course we have seen one-mean problems, twomean problems, and problems

1 Introduction Inference with Simple Regression Alan B. Gelder 06E:071, The University of Iowa 1 Moving to infinite means: In this course we have seen one-mean problems, twomean problems, and problems

STAT 436 / Lecture 16: Key

STAT 436 / 536 - Lecture 16: Key Modeling Non-Stationary Time Series Many time series models are non-stationary. Recall a time series is stationary if the mean and variance are constant in time and the

STAT 436 / 536 - Lecture 16: Key Modeling Non-Stationary Time Series Many time series models are non-stationary. Recall a time series is stationary if the mean and variance are constant in time and the

ECONOMETRIA II. CURSO 2009/2010 LAB # 3

ECONOMETRIA II. CURSO 2009/2010 LAB # 3 BOX-JENKINS METHODOLOGY The Box Jenkins approach combines the moving average and the autorregresive models. Although both models were already known, the contribution

ECONOMETRIA II. CURSO 2009/2010 LAB # 3 BOX-JENKINS METHODOLOGY The Box Jenkins approach combines the moving average and the autorregresive models. Although both models were already known, the contribution

Modeling and forecasting global mean temperature time series

Modeling and forecasting global mean temperature time series April 22, 2018 Abstract: An ARIMA time series model was developed to analyze the yearly records of the change in global annual mean surface

Modeling and forecasting global mean temperature time series April 22, 2018 Abstract: An ARIMA time series model was developed to analyze the yearly records of the change in global annual mean surface

Lecture Notes 12 Advanced Topics Econ 20150, Principles of Statistics Kevin R Foster, CCNY Spring 2012

Lecture Notes 2 Advanced Topics Econ 2050, Principles of Statistics Kevin R Foster, CCNY Spring 202 Endogenous Independent Variables are Invalid Need to have X causing Y not vice-versa or both! NEVER regress

Lecture Notes 2 Advanced Topics Econ 2050, Principles of Statistics Kevin R Foster, CCNY Spring 202 Endogenous Independent Variables are Invalid Need to have X causing Y not vice-versa or both! NEVER regress

Homework 2. For the homework, be sure to give full explanations where required and to turn in any relevant plots.

Homework 2 1 Data analysis problems For the homework, be sure to give full explanations where required and to turn in any relevant plots. 1. The file berkeley.dat contains average yearly temperatures for

Homework 2 1 Data analysis problems For the homework, be sure to give full explanations where required and to turn in any relevant plots. 1. The file berkeley.dat contains average yearly temperatures for

Prof. Dr. Roland Füss Lecture Series in Applied Econometrics Summer Term Introduction to Time Series Analysis

Introduction to Time Series Analysis 1 Contents: I. Basics of Time Series Analysis... 4 I.1 Stationarity... 5 I.2 Autocorrelation Function... 9 I.3 Partial Autocorrelation Function (PACF)... 14 I.4 Transformation

Introduction to Time Series Analysis 1 Contents: I. Basics of Time Series Analysis... 4 I.1 Stationarity... 5 I.2 Autocorrelation Function... 9 I.3 Partial Autocorrelation Function (PACF)... 14 I.4 Transformation

Ordinary Least Squares Regression Explained: Vartanian

Ordinary Least Squares Regression Eplained: Vartanian When to Use Ordinary Least Squares Regression Analysis A. Variable types. When you have an interval/ratio scale dependent variable.. When your independent

Ordinary Least Squares Regression Eplained: Vartanian When to Use Ordinary Least Squares Regression Analysis A. Variable types. When you have an interval/ratio scale dependent variable.. When your independent

1. How can you tell if there is serial correlation? 2. AR to model serial correlation. 3. Ignoring serial correlation. 4. GLS. 5. Projects.

1. How can you tell if there is serial correlation? 2. AR to model serial correlation. 3. Ignoring serial correlation. 4. GLS. 5. Projects. 1) Identifying serial correlation. Plot Y t versus Y t 1. See

1. How can you tell if there is serial correlation? 2. AR to model serial correlation. 3. Ignoring serial correlation. 4. GLS. 5. Projects. 1) Identifying serial correlation. Plot Y t versus Y t 1. See

Chapter 12: An introduction to Time Series Analysis. Chapter 12: An introduction to Time Series Analysis

Chapter 12: An introduction to Time Series Analysis Introduction In this chapter, we will discuss forecasting with single-series (univariate) Box-Jenkins models. The common name of the models is Auto-Regressive

Chapter 12: An introduction to Time Series Analysis Introduction In this chapter, we will discuss forecasting with single-series (univariate) Box-Jenkins models. The common name of the models is Auto-Regressive

Decision 411: Class 7

Decision 411: Class 7 Confidence limits for sums of coefficients Use of the time index as a regressor The difficulty of predicting the future Confidence intervals for sums of coefficients Sometimes the

Decision 411: Class 7 Confidence limits for sums of coefficients Use of the time index as a regressor The difficulty of predicting the future Confidence intervals for sums of coefficients Sometimes the

LAB 3 INSTRUCTIONS SIMPLE LINEAR REGRESSION

LAB 3 INSTRUCTIONS SIMPLE LINEAR REGRESSION In this lab you will first learn how to display the relationship between two quantitative variables with a scatterplot and also how to measure the strength of

LAB 3 INSTRUCTIONS SIMPLE LINEAR REGRESSION In this lab you will first learn how to display the relationship between two quantitative variables with a scatterplot and also how to measure the strength of

EDF 7405 Advanced Quantitative Methods in Educational Research. Data are available on IQ of the child and seven potential predictors.

EDF 7405 Advanced Quantitative Methods in Educational Research Data are available on IQ of the child and seven potential predictors. Four are medical variables available at the birth of the child: Birthweight

EDF 7405 Advanced Quantitative Methods in Educational Research Data are available on IQ of the child and seven potential predictors. Four are medical variables available at the birth of the child: Birthweight

Taguchi Method and Robust Design: Tutorial and Guideline

Taguchi Method and Robust Design: Tutorial and Guideline CONTENT 1. Introduction 2. Microsoft Excel: graphing 3. Microsoft Excel: Regression 4. Microsoft Excel: Variance analysis 5. Robust Design: An Example

Taguchi Method and Robust Design: Tutorial and Guideline CONTENT 1. Introduction 2. Microsoft Excel: graphing 3. Microsoft Excel: Regression 4. Microsoft Excel: Variance analysis 5. Robust Design: An Example

Ratio of Polynomials Fit One Variable

Chapter 375 Ratio of Polynomials Fit One Variable Introduction This program fits a model that is the ratio of two polynomials of up to fifth order. Examples of this type of model are: and Y = A0 + A1 X

Chapter 375 Ratio of Polynomials Fit One Variable Introduction This program fits a model that is the ratio of two polynomials of up to fifth order. Examples of this type of model are: and Y = A0 + A1 X

Problem Set 2 Solution Sketches Time Series Analysis Spring 2010

Problem Set 2 Solution Sketches Time Series Analysis Spring 2010 Forecasting 1. Let X and Y be two random variables such that E(X 2 ) < and E(Y 2 )

Problem Set 2 Solution Sketches Time Series Analysis Spring 2010 Forecasting 1. Let X and Y be two random variables such that E(X 2 ) < and E(Y 2 )

Analysis of Violent Crime in Los Angeles County

Analysis of Violent Crime in Los Angeles County Xiaohong Huang UID: 004693375 March 20, 2017 Abstract Violent crime can have a negative impact to the victims and the neighborhoods. It can affect people

Analysis of Violent Crime in Los Angeles County Xiaohong Huang UID: 004693375 March 20, 2017 Abstract Violent crime can have a negative impact to the victims and the neighborhoods. It can affect people

Topic 1. Definitions

S Topic. Definitions. Scalar A scalar is a number. 2. Vector A vector is a column of numbers. 3. Linear combination A scalar times a vector plus a scalar times a vector, plus a scalar times a vector...

S Topic. Definitions. Scalar A scalar is a number. 2. Vector A vector is a column of numbers. 3. Linear combination A scalar times a vector plus a scalar times a vector, plus a scalar times a vector...

Repeated-Measures ANOVA in SPSS Correct data formatting for a repeated-measures ANOVA in SPSS involves having a single line of data for each

Repeated-Measures ANOVA in SPSS Correct data formatting for a repeated-measures ANOVA in SPSS involves having a single line of data for each participant, with the repeated measures entered as separate

Repeated-Measures ANOVA in SPSS Correct data formatting for a repeated-measures ANOVA in SPSS involves having a single line of data for each participant, with the repeated measures entered as separate

Static and Kinetic Friction

Ryerson University - PCS 120 Introduction Static and Kinetic Friction In this lab we study the effect of friction on objects. We often refer to it as a frictional force yet it doesn t exactly behave as

Ryerson University - PCS 120 Introduction Static and Kinetic Friction In this lab we study the effect of friction on objects. We often refer to it as a frictional force yet it doesn t exactly behave as

Designing a Quilt with GIMP 2011

Planning your quilt and want to see what it will look like in the fabric you just got from your LQS? You don t need to purchase a super expensive program. Try this and the best part it s FREE!!! *** Please

Planning your quilt and want to see what it will look like in the fabric you just got from your LQS? You don t need to purchase a super expensive program. Try this and the best part it s FREE!!! *** Please

Motion II. Goals and Introduction

Motion II Goals and Introduction As you have probably already seen in lecture or homework, and if you ve performed the experiment Motion I, it is important to develop a strong understanding of how to model

Motion II Goals and Introduction As you have probably already seen in lecture or homework, and if you ve performed the experiment Motion I, it is important to develop a strong understanding of how to model

( ), which of the coefficients would end

, which of the coefficients would end") Discussion Sheet 29.7.9 Qualitative Variables We have devoted most of our attention in multiple regression to quantitative or numerical variables. MR models can become more useful and complex when we consider

Discussion Sheet 29.7.9 Qualitative Variables We have devoted most of our attention in multiple regression to quantitative or numerical variables. MR models can become more useful and complex when we consider

Box-Jenkins ARIMA Advanced Time Series

Box-Jenkins ARIMA Advanced Time Series www.realoptionsvaluation.com ROV Technical Papers Series: Volume 25 Theory In This Issue 1. Learn about Risk Simulator s ARIMA and Auto ARIMA modules. 2. Find out

Box-Jenkins ARIMA Advanced Time Series www.realoptionsvaluation.com ROV Technical Papers Series: Volume 25 Theory In This Issue 1. Learn about Risk Simulator s ARIMA and Auto ARIMA modules. 2. Find out

Ch 6. Model Specification. Time Series Analysis

We start to build ARIMA(p,d,q) models. The subjects include: 1 how to determine p, d, q for a given series (Chapter 6); 2 how to estimate the parameters (φ s and θ s) of a specific ARIMA(p,d,q) model (Chapter

We start to build ARIMA(p,d,q) models. The subjects include: 1 how to determine p, d, q for a given series (Chapter 6); 2 how to estimate the parameters (φ s and θ s) of a specific ARIMA(p,d,q) model (Chapter

The Identification of ARIMA Models

APPENDIX 4 The Identification of ARIMA Models As we have established in a previous lecture, there is a one-to-one correspondence between the parameters of an ARMA(p, q) model, including the variance of

APPENDIX 4 The Identification of ARIMA Models As we have established in a previous lecture, there is a one-to-one correspondence between the parameters of an ARMA(p, q) model, including the variance of

Gravity: How fast do objects fall? Teacher Advanced Version (Grade Level: 8 12)

") Gravity: How fast do objects fall? Teacher Advanced Version (Grade Level: 8 12) *** Experiment with Audacity and Excel to be sure you know how to do what s needed for the lab*** Kinematics is the study

Gravity: How fast do objects fall? Teacher Advanced Version (Grade Level: 8 12) *** Experiment with Audacity and Excel to be sure you know how to do what s needed for the lab*** Kinematics is the study

Univariate analysis. Simple and Multiple Regression. Univariate analysis. Simple Regression How best to summarise the data?

Univariate analysis Example - linear regression equation: y = ax + c Least squares criteria ( yobs ycalc ) = yobs ( ax + c) = minimum Simple and + = xa xc xy xa + nc = y Solve for a and c Univariate analysis

Univariate analysis Example - linear regression equation: y = ax + c Least squares criteria ( yobs ycalc ) = yobs ( ax + c) = minimum Simple and + = xa xc xy xa + nc = y Solve for a and c Univariate analysis

Univariate, Nonstationary Processes

Univariate, Nonstationary Processes Jamie Monogan University of Georgia March 20, 2018 Jamie Monogan (UGA) Univariate, Nonstationary Processes March 20, 2018 1 / 14 Objectives By the end of this meeting,

Univariate, Nonstationary Processes Jamie Monogan University of Georgia March 20, 2018 Jamie Monogan (UGA) Univariate, Nonstationary Processes March 20, 2018 1 / 14 Objectives By the end of this meeting,

Interactions and Centering in Regression: MRC09 Salaries for graduate faculty in psychology

Psychology 308c Dale Berger Interactions and Centering in Regression: MRC09 Salaries for graduate faculty in psychology This example illustrates modeling an interaction with centering and transformations.

Psychology 308c Dale Berger Interactions and Centering in Regression: MRC09 Salaries for graduate faculty in psychology This example illustrates modeling an interaction with centering and transformations.

Design of Time Series Model for Road Accident Fatal Death in Tamilnadu

Volume 109 No. 8 2016, 225-232 ISSN: 1311-8080 (printed version); ISSN: 1314-3395 (on-line version) url: http://www.ijpam.eu ijpam.eu Design of Time Series Model for Road Accident Fatal Death in Tamilnadu

Volume 109 No. 8 2016, 225-232 ISSN: 1311-8080 (printed version); ISSN: 1314-3395 (on-line version) url: http://www.ijpam.eu ijpam.eu Design of Time Series Model for Road Accident Fatal Death in Tamilnadu

Problems from Chapter 3 of Shumway and Stoffer s Book

UNIVERSITY OF UTAH GUIDED READING TIME SERIES Problems from Chapter 3 of Shumway and Stoffer s Book Author: Curtis MILLER Supervisor: Prof. Lajos HORVATH November 10, 2015 UNIVERSITY OF UTAH DEPARTMENT

UNIVERSITY OF UTAH GUIDED READING TIME SERIES Problems from Chapter 3 of Shumway and Stoffer s Book Author: Curtis MILLER Supervisor: Prof. Lajos HORVATH November 10, 2015 UNIVERSITY OF UTAH DEPARTMENT

Homework 4. 1 Data analysis problems

Homework 4 1 Data analysis problems This week we will be analyzing a number of data sets. We are going to build ARIMA models using the steps outlined in class. It is also a good idea to read section 3.8

Homework 4 1 Data analysis problems This week we will be analyzing a number of data sets. We are going to build ARIMA models using the steps outlined in class. It is also a good idea to read section 3.8

The data was collected from the website and then converted to a time-series indexed from 1 to 86.

Introduction For our group project, we analyzed the S&P 500s futures from 30 November, 2015 till 28 March, 2016. The S&P 500 futures give a reasonable estimate of the changes in the market in the short

Introduction For our group project, we analyzed the S&P 500s futures from 30 November, 2015 till 28 March, 2016. The S&P 500 futures give a reasonable estimate of the changes in the market in the short

Ch 8. MODEL DIAGNOSTICS. Time Series Analysis

Model diagnostics is concerned with testing the goodness of fit of a model and, if the fit is poor, suggesting appropriate modifications. We shall present two complementary approaches: analysis of residuals

Model diagnostics is concerned with testing the goodness of fit of a model and, if the fit is poor, suggesting appropriate modifications. We shall present two complementary approaches: analysis of residuals

Review of Multiple Regression

Ronald H. Heck 1 Let s begin with a little review of multiple regression this week. Linear models [e.g., correlation, t-tests, analysis of variance (ANOVA), multiple regression, path analysis, multivariate

Ronald H. Heck 1 Let s begin with a little review of multiple regression this week. Linear models [e.g., correlation, t-tests, analysis of variance (ANOVA), multiple regression, path analysis, multivariate

Designing Information Devices and Systems I Spring 2017 Babak Ayazifar, Vladimir Stojanovic Homework 2

EECS 16A Designing Information Devices and Systems I Spring 2017 Babak Ayazifar, Vladimir Stojanovic Homework 2 This homework is due February 6, 2017, at 23:59. Self-grades are due February 9, 2017, at

EECS 16A Designing Information Devices and Systems I Spring 2017 Babak Ayazifar, Vladimir Stojanovic Homework 2 This homework is due February 6, 2017, at 23:59. Self-grades are due February 9, 2017, at

The inductive effect in nitridosilicates and oxysilicates and its effects on 5d energy levels of Ce 3+

The inductive effect in nitridosilicates and oxysilicates and its effects on 5d energy levels of Ce 3+ Yuwei Kong, Zhen Song, Shuxin Wang, Zhiguo Xia and Quanlin Liu* The Beijing Municipal Key Laboratory

The inductive effect in nitridosilicates and oxysilicates and its effects on 5d energy levels of Ce 3+ Yuwei Kong, Zhen Song, Shuxin Wang, Zhiguo Xia and Quanlin Liu* The Beijing Municipal Key Laboratory

EASTERN MEDITERRANEAN UNIVERSITY ECON 604, FALL 2007 DEPARTMENT OF ECONOMICS MEHMET BALCILAR ARIMA MODELS: IDENTIFICATION

ARIMA MODELS: IDENTIFICATION A. Autocorrelations and Partial Autocorrelations 1. Summary of What We Know So Far: a) Series y t is to be modeled by Box-Jenkins methods. The first step was to convert y t

ARIMA MODELS: IDENTIFICATION A. Autocorrelations and Partial Autocorrelations 1. Summary of What We Know So Far: a) Series y t is to be modeled by Box-Jenkins methods. The first step was to convert y t

CHAPTER 8 MODEL DIAGNOSTICS. 8.1 Residual Analysis

CHAPTER 8 MODEL DIAGNOSTICS We have now discussed methods for specifying models and for efficiently estimating the parameters in those models. Model diagnostics, or model criticism, is concerned with testing

CHAPTER 8 MODEL DIAGNOSTICS We have now discussed methods for specifying models and for efficiently estimating the parameters in those models. Model diagnostics, or model criticism, is concerned with testing

Forecasting using R. Rob J Hyndman. 2.4 Non-seasonal ARIMA models. Forecasting using R 1

Forecasting using R Rob J Hyndman 2.4 Non-seasonal ARIMA models Forecasting using R 1 Outline 1 Autoregressive models 2 Moving average models 3 Non-seasonal ARIMA models 4 Partial autocorrelations 5 Estimation

Forecasting using R Rob J Hyndman 2.4 Non-seasonal ARIMA models Forecasting using R 1 Outline 1 Autoregressive models 2 Moving average models 3 Non-seasonal ARIMA models 4 Partial autocorrelations 5 Estimation

APPLIED ECONOMETRIC TIME SERIES 4TH EDITION

APPLIED ECONOMETRIC TIME SERIES 4TH EDITION Chapter 2: STATIONARY TIME-SERIES MODELS WALTER ENDERS, UNIVERSITY OF ALABAMA Copyright 2015 John Wiley & Sons, Inc. Section 1 STOCHASTIC DIFFERENCE EQUATION

APPLIED ECONOMETRIC TIME SERIES 4TH EDITION Chapter 2: STATIONARY TIME-SERIES MODELS WALTER ENDERS, UNIVERSITY OF ALABAMA Copyright 2015 John Wiley & Sons, Inc. Section 1 STOCHASTIC DIFFERENCE EQUATION

Analysis. Components of a Time Series

Module 8: Time Series Analysis 8.2 Components of a Time Series, Detection of Change Points and Trends, Time Series Models Components of a Time Series There can be several things happening simultaneously

Module 8: Time Series Analysis 8.2 Components of a Time Series, Detection of Change Points and Trends, Time Series Models Components of a Time Series There can be several things happening simultaneously

Stat 5100 Handout #12.e Notes: ARIMA Models (Unit 7) Key here: after stationary, identify dependence structure (and use for forecasting)

Key here: after stationary, identify dependence structure (and use for forecasting)") Stat 5100 Handout #12.e Notes: ARIMA Models (Unit 7) Key here: after stationary, identify dependence structure (and use for forecasting) (overshort example) White noise H 0 : Let Z t be the stationary

Stat 5100 Handout #12.e Notes: ARIMA Models (Unit 7) Key here: after stationary, identify dependence structure (and use for forecasting) (overshort example) White noise H 0 : Let Z t be the stationary

Read Section 1.1, Examples of time series, on pages 1-8. These example introduce the book; you are not tested on them.

TS Module 1 Time series overview (The attached PDF file has better formatting.)! Model building! Time series plots Read Section 1.1, Examples of time series, on pages 1-8. These example introduce the book;

TS Module 1 Time series overview (The attached PDF file has better formatting.)! Model building! Time series plots Read Section 1.1, Examples of time series, on pages 1-8. These example introduce the book;

Simulating Future Climate Change Using A Global Climate Model

Simulating Future Climate Change Using A Global Climate Model Introduction: (EzGCM: Web-based Version) The objective of this abridged EzGCM exercise is for you to become familiar with the steps involved

Simulating Future Climate Change Using A Global Climate Model Introduction: (EzGCM: Web-based Version) The objective of this abridged EzGCM exercise is for you to become familiar with the steps involved

A stochastic modeling for paddy production in Tamilnadu

2017; 2(5): 14-21 ISSN: 2456-1452 Maths 2017; 2(5): 14-21 2017 Stats & Maths www.mathsjournal.com Received: 04-07-2017 Accepted: 05-08-2017 M Saranyadevi Assistant Professor (GUEST), Department of Statistics,

2017; 2(5): 14-21 ISSN: 2456-1452 Maths 2017; 2(5): 14-21 2017 Stats & Maths www.mathsjournal.com Received: 04-07-2017 Accepted: 05-08-2017 M Saranyadevi Assistant Professor (GUEST), Department of Statistics,

Binary Dependent Variables

Binary Dependent Variables In some cases the outcome of interest rather than one of the right hand side variables - is discrete rather than continuous Binary Dependent Variables In some cases the outcome

Binary Dependent Variables In some cases the outcome of interest rather than one of the right hand side variables - is discrete rather than continuous Binary Dependent Variables In some cases the outcome

Classic Time Series Analysis

Classic Time Series Analysis Concepts and Definitions Let Y be a random number with PDF f Y t ~f,t Define t =E[Y t ] m(t) is known as the trend Define the autocovariance t, s =COV [Y t,y s ] =E[ Y t t

Classic Time Series Analysis Concepts and Definitions Let Y be a random number with PDF f Y t ~f,t Define t =E[Y t ] m(t) is known as the trend Define the autocovariance t, s =COV [Y t,y s ] =E[ Y t t

1 Introduction to Minitab

1 Introduction to Minitab Minitab is a statistical analysis software package. The software is freely available to all students and is downloadable through the Technology Tab at my.calpoly.edu. When you

1 Introduction to Minitab Minitab is a statistical analysis software package. The software is freely available to all students and is downloadable through the Technology Tab at my.calpoly.edu. When you

Marcel Dettling. Applied Time Series Analysis SS 2013 Week 05. ETH Zürich, March 18, Institute for Data Analysis and Process Design

Marcel Dettling Institute for Data Analysis and Process Design Zurich University of Applied Sciences marcel.dettling@zhaw.ch http://stat.ethz.ch/~dettling ETH Zürich, March 18, 2013 1 Basics of Modeling

Marcel Dettling Institute for Data Analysis and Process Design Zurich University of Applied Sciences marcel.dettling@zhaw.ch http://stat.ethz.ch/~dettling ETH Zürich, March 18, 2013 1 Basics of Modeling

477/577 In-class Exercise 5 : Fitting Wine Sales

477/577 In-class Exercise 5 : Fitting Wine Sales (due Fri 4/06/2017) Name: Use this file as a template for your report. Submit your code and comments together with (selected) output from R console. Your

477/577 In-class Exercise 5 : Fitting Wine Sales (due Fri 4/06/2017) Name: Use this file as a template for your report. Submit your code and comments together with (selected) output from R console. Your

STAT 153: Introduction to Time Series

STAT 153: Introduction to Time Series Instructor: Aditya Guntuboyina Lectures: 12:30 pm - 2 pm (Tuesdays and Thursdays) Office Hours: 10 am - 11 am (Tuesdays and Thursdays) 423 Evans Hall GSI: Brianna

STAT 153: Introduction to Time Series Instructor: Aditya Guntuboyina Lectures: 12:30 pm - 2 pm (Tuesdays and Thursdays) Office Hours: 10 am - 11 am (Tuesdays and Thursdays) 423 Evans Hall GSI: Brianna

A Data-Driven Model for Software Reliability Prediction

A Data-Driven Model for Software Reliability Prediction Author: Jung-Hua Lo IEEE International Conference on Granular Computing (2012) Young Taek Kim KAIST SE Lab. 9/4/2013 Contents Introduction Background

A Data-Driven Model for Software Reliability Prediction Author: Jung-Hua Lo IEEE International Conference on Granular Computing (2012) Young Taek Kim KAIST SE Lab. 9/4/2013 Contents Introduction Background

Econometrics for Policy Analysis A Train The Trainer Workshop Oct 22-28, 2016 Organized by African Heritage Institution

Econometrics for Policy Analysis A Train The Trainer Workshop Oct 22-28, 2016 Organized by African Heritage Institution Delivered by Dr. Nathaniel E. Urama Department of Economics, University of Nigeria,

Econometrics for Policy Analysis A Train The Trainer Workshop Oct 22-28, 2016 Organized by African Heritage Institution Delivered by Dr. Nathaniel E. Urama Department of Economics, University of Nigeria,

Modelling using ARMA processes

Modelling using ARMA processes Step 1. ARMA model identification; Step 2. ARMA parameter estimation Step 3. ARMA model selection ; Step 4. ARMA model checking; Step 5. forecasting from ARMA models. 33

Modelling using ARMA processes Step 1. ARMA model identification; Step 2. ARMA parameter estimation Step 3. ARMA model selection ; Step 4. ARMA model checking; Step 5. forecasting from ARMA models. 33

5:1LEC - BETWEEN-S FACTORIAL ANOVA

5:1LEC - BETWEEN-S FACTORIAL ANOVA The single-factor Between-S design described in previous classes is only appropriate when there is just one independent variable or factor in the study. Often, however,

5:1LEC - BETWEEN-S FACTORIAL ANOVA The single-factor Between-S design described in previous classes is only appropriate when there is just one independent variable or factor in the study. Often, however,

ARIMA Models. Jamie Monogan. January 25, University of Georgia. Jamie Monogan (UGA) ARIMA Models January 25, / 38

ARIMA Models January 25, / 38") ARIMA Models Jamie Monogan University of Georgia January 25, 2012 Jamie Monogan (UGA) ARIMA Models January 25, 2012 1 / 38 Objectives By the end of this meeting, participants should be able to: Describe

ARIMA Models Jamie Monogan University of Georgia January 25, 2012 Jamie Monogan (UGA) ARIMA Models January 25, 2012 1 / 38 Objectives By the end of this meeting, participants should be able to: Describe