Towards inference for skewed alpha stable Levy processes

|

|

|

- Prosper Banks

- 5 years ago

- Views:

Transcription

1 Towards inference for skewed alpha stable Levy processes Simon Godsill and Tatjana Lemke Signal Processing and Communications Lab. University of Cambridge www-sigproc.eng.cam.ac.uk/~sjg

2 Overview Motivation Continuous-time models Inference for models with jumps Inference for alpha-stable Levy processes Conclusions

models: Measurements (range,")

3 Motivation Traditional tracking applications run in discrete time discrete time state space models: Dynamic models of behaviour: Hidden state (position/velocity ) Sensor (observation) models: Measurements (range, bearing, )

4 State Space Model: Optimal Filtering (sequential inference):

5 It is often more natural to model in continuous time: Observations can arrive at arbitrary timings, and out of sequence Object manoeuvres are carried out in continuous time without reference to observation times Real objects undergo rapid and random changes of regime, or `jumps, occurring at unknown times on the continuous-time scale: Variable rate - C =60, C =2, T =100, N Particles= To appear

6 Can approximate this type of behaviour with jump Markov (or semi-markov) discrete time systems, allowing a finite set of discrete time switching models (HMMs, etc.) However, seems more natural to model directly in continuous time, without limiting regimes to a finite set (although can extend models to allow in addition regime switching between discrete states) Bayesian Monte Carlo computational tools are well suited to inference in these continuous time models

7 Continuous time models

} is comprised of (scaled) Brownian motion {B(t)} plus a pure Gaussian jump process{z(t)}: 2 1.5 1 0.5 0-0.5-1 -1.5-2 -2.")

8 100.3 Variable rate - C =60, C =2, T =100, N Particles=400 Example: stochastic trend model with Gaussian jumps Now assume that {W(t)} is comprised of (scaled) Brownian motion {B(t)} plus a pure Gaussian jump process{z(t)}: See Christensen, Murphy and Godsill, 2012

9

10 Observation of the jump process Now assume discrete-time observations of the continuous-time process, e.g. Filtering/ smoothing and parameter estimation can now be carried out using Kalman-filter conditional likelihoods:

and Bunch")

11 Fixed Interval Filtering and Smoothing Particle filter-smoother, See Godsill, Doucet, West (2004) and Bunch and Godsill (2012)

12 Tracking examples

13 Joint work with Tatjana Lemke, see Lemke and Godsill Proc. ICASSP 2011, ICASSP stable Levy processes Previously modelled jumps as a finite activity process Perhaps more realistic to model the jumps as an infinite collection of large/ small/tiny jumps occurring in each finite time interval -stable Levy processes provide a natural way to achieve this justified in many Communications, Signal Processing and Finance applications

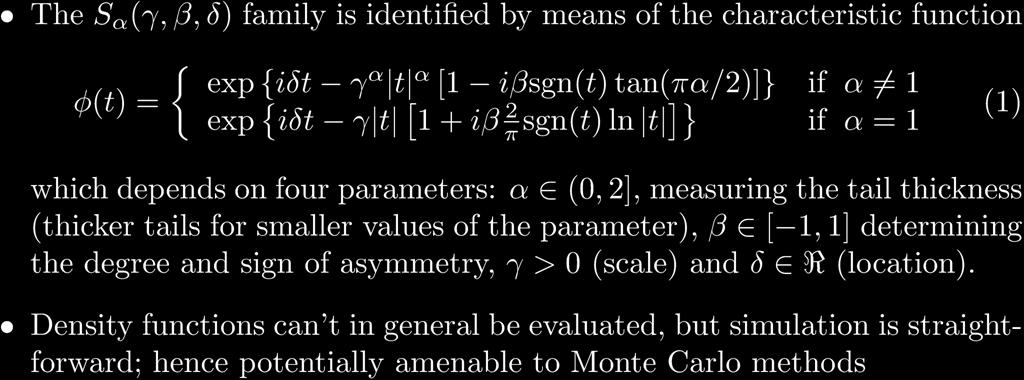

14 Stable distributions

15

16

17 Approaches to inference can be made by scale mixtures of normals for symmetric case, and Euler discretisation Godsill and Kuruoglu 1998, Godsill and Yang 2006, Tsionas See also Buckle (1995) Our current work focuses on a powerful series expansion for the general asymmetric case:

18 Arrival times of a unit rate Poisson process iid random variables satisfying some simple moment conditions, e.g. A Gaussian would do. [Here stated in its simplest form for a random variable with <1. A similar form applies for the stochastic integral.] [Samorodnitsky and Taqqu 1994]

19 now has a `physical interpretation as the scale of the ith jump. [Samorodnitsky and Taqqu 1994] [See also Barndorff-Nielsen and Shephard (2001,2001)]

can")

20 Now, taking W i to be iid N(¹ W,¾ W2 ), we have a Gaussian structure, conditional upon the terms i This can be readily handled using Bayesian Monte Carlo inference. As a significant bonus, (¹ W,¾ W2 ) can be analytically marginalised, leaving only to be sampled The trade-off is that we must also simulate an infinite series of i terms in practice we do this by truncating the series and approximating the residual.

21

22 Truncation of the Series In practice cannot compute the entire infinite series: Instead, truncate at a limit, i <c, and approximate the residual with a Gaussian matched to first two moments of the residual (analytically computed).

23

24

, one for each data")

25 Inference Schemes Consider e.g. A MCMC inference algorithm for the parameters and the latent variables. Parameters are, ¾ W, ¹ W, {m,v} The challenging part is the latent variables (m,v), one for each data point.

26 Latent Variables (m,v) Can sample directly from the prior p(m,v) and use rejection sampling (unbounded envelope, but can fix (condition on) the residual terms and make it bounded). Not good enough for large values of X (slow in the tails!); instead, look at p(m,v):

27 ca Observe that for large m, V is approximately m 2 This means that we can force prior samples of m into the tails of the distribution ( -stable and hence pareto) and perform rejection sampling with likelihood constrained to the line V=m 2 This is a rare-event tail approximation for large X values, but the approximation appears very good and speeds up sampling dramatically. Can tune accuracy vs. speed by selecting the switchover point between optimal (slow) and tail approximation (fast).

28 State-space models and continuous time Incorporation into discrete-time statespace models is fairly straightforward likelihood computation can then be done by a mean- and scale-shifted Kalman filter Continuous time is also a fairly straightforward extension also need to sample the {V i }

29

30

31

, Carter and Kohn (1994")

32 Conclusion A general framework for inference of -stable distribution parameters, linear state-space models and continuous-time Levy processes Straightforward computations using conditionally Gaussian models (Shephard (1993 Biometrika), Carter and Kohn (1994 Biometrika)), and particle filters Currently exploring Particle MCMC methods for parameter estimation

33 References S. J. Godsill, J. Vermaak, W. Ng and J.F. Li. Variable rate particle filters for tracking applications in Proceedings of the IEEE, Special Issue on Large Scale Dynamical Systems, S. J. Godsill and J. Vermaak. Variable rate particle filters for tracking applications. In Proc. IEEE Stat. Sig. Proc., Bordeaux, S. J. Godsill and J. Vermaak, Models and algorithms for tracking using trans-dimensional sequential Monte Carlo. In Proc. IEEE ICASSP 2004 Barndorff-Nielsen, Ole E. and Neil Shephard (2001) "Normal modified stable processes", Theory of Probability and Mathematical Statistics, 2001, Barndorff-Nielsen, Ole E. and Neil Shephard (2001) "Non-Gaussian Ornstein-Uhlenbeck-based models and some of their uses in financial economics", (with discussion) Journal of the Royal Statistical Society, Series B, 63, Buckle, D. J. (1995), Bayesian inference for stable distributions, JASA, 90: S. J. Godsill. Inference in symmetric alpha-stable noise using MCMC and the slice sampler. In Proc. IEEE International Conference on Acoustics, Speech and Signal Processing, volume VI, pages , ISBN S. J. Godsill. MCMC and EM-based methods for inference in heavy-tailed processes with alpha-stable innovations. In Proc. IEEE Signal processing workshop on higher-order statistics, June Caesarea, Israel.[ bib.ps ] S. J. Godsill and E. E. Kuruoglu. Bayesian inference for time series with heavy-tailed symmetric α-stable noise processes. In Proc. Applications of heavy tailed distributions in economics, engineering and statistics, June Washington DC, USA.[ bib.ps ] S.J. Godsill and L. Yang. Bayesian inference for continuous-time AR models driven by non-gaussian lévy processes. In Proc. IEEE International Conference on Acoustics, Speech and Signal Processing, Toulouse, France, May Tatjana Lemke, Simon J. Godsill: Enhanced Poisson sum representation for alpha-stable processes. ICASSP 2011: Tatjana Lemke, Simon J. Godsill: LINEAR GAUSSIAN COMPUTATIONS FOR NEAR-EXACT BAYESIAN MONTE CARLO INFERENCE IN SKEWED ALPHA-STABLE TIME SERIES MODELS, ICASSP 20112

PATTERN RECOGNITION AND MACHINE LEARNING CHAPTER 13: SEQUENTIAL DATA

PATTERN RECOGNITION AND MACHINE LEARNING CHAPTER 13: SEQUENTIAL DATA Contents in latter part Linear Dynamical Systems What is different from HMM? Kalman filter Its strength and limitation Particle Filter

PATTERN RECOGNITION AND MACHINE LEARNING CHAPTER 13: SEQUENTIAL DATA Contents in latter part Linear Dynamical Systems What is different from HMM? Kalman filter Its strength and limitation Particle Filter

Approximate Bayesian Computation and Particle Filters

Approximate Bayesian Computation and Particle Filters Dennis Prangle Reading University 5th February 2014 Introduction Talk is mostly a literature review A few comments on my own ongoing research See Jasra

Approximate Bayesian Computation and Particle Filters Dennis Prangle Reading University 5th February 2014 Introduction Talk is mostly a literature review A few comments on my own ongoing research See Jasra

STA 4273H: Statistical Machine Learning

STA 4273H: Statistical Machine Learning Russ Salakhutdinov Department of Statistics! rsalakhu@utstat.toronto.edu! http://www.utstat.utoronto.ca/~rsalakhu/ Sidney Smith Hall, Room 6002 Lecture 11 Project

STA 4273H: Statistical Machine Learning Russ Salakhutdinov Department of Statistics! rsalakhu@utstat.toronto.edu! http://www.utstat.utoronto.ca/~rsalakhu/ Sidney Smith Hall, Room 6002 Lecture 11 Project

Linear Dynamical Systems

Linear Dynamical Systems Sargur N. srihari@cedar.buffalo.edu Machine Learning Course: http://www.cedar.buffalo.edu/~srihari/cse574/index.html Two Models Described by Same Graph Latent variables Observations

Linear Dynamical Systems Sargur N. srihari@cedar.buffalo.edu Machine Learning Course: http://www.cedar.buffalo.edu/~srihari/cse574/index.html Two Models Described by Same Graph Latent variables Observations

Least Squares Estimators for Stochastic Differential Equations Driven by Small Lévy Noises

Least Squares Estimators for Stochastic Differential Equations Driven by Small Lévy Noises Hongwei Long* Department of Mathematical Sciences, Florida Atlantic University, Boca Raton Florida 33431-991,

Least Squares Estimators for Stochastic Differential Equations Driven by Small Lévy Noises Hongwei Long* Department of Mathematical Sciences, Florida Atlantic University, Boca Raton Florida 33431-991,

Density Propagation for Continuous Temporal Chains Generative and Discriminative Models

$ Technical Report, University of Toronto, CSRG-501, October 2004 Density Propagation for Continuous Temporal Chains Generative and Discriminative Models Cristian Sminchisescu and Allan Jepson Department

$ Technical Report, University of Toronto, CSRG-501, October 2004 Density Propagation for Continuous Temporal Chains Generative and Discriminative Models Cristian Sminchisescu and Allan Jepson Department

Likelihood-free MCMC

Bayesian inference for stable distributions with applications in finance Department of Mathematics University of Leicester September 2, 2011 MSc project final presentation Outline 1 2 3 4 Classical Monte

Bayesian inference for stable distributions with applications in finance Department of Mathematics University of Leicester September 2, 2011 MSc project final presentation Outline 1 2 3 4 Classical Monte

Sequential Monte Carlo Methods for Bayesian Computation

Sequential Monte Carlo Methods for Bayesian Computation A. Doucet Kyoto Sept. 2012 A. Doucet (MLSS Sept. 2012) Sept. 2012 1 / 136 Motivating Example 1: Generic Bayesian Model Let X be a vector parameter

Sequential Monte Carlo Methods for Bayesian Computation A. Doucet Kyoto Sept. 2012 A. Doucet (MLSS Sept. 2012) Sept. 2012 1 / 136 Motivating Example 1: Generic Bayesian Model Let X be a vector parameter

State-Space Methods for Inferring Spike Trains from Calcium Imaging

State-Space Methods for Inferring Spike Trains from Calcium Imaging Joshua Vogelstein Johns Hopkins April 23, 2009 Joshua Vogelstein (Johns Hopkins) State-Space Calcium Imaging April 23, 2009 1 / 78 Outline

State-Space Methods for Inferring Spike Trains from Calcium Imaging Joshua Vogelstein Johns Hopkins April 23, 2009 Joshua Vogelstein (Johns Hopkins) State-Space Calcium Imaging April 23, 2009 1 / 78 Outline

Bayesian Nonparametric Learning of Complex Dynamical Phenomena

Duke University Department of Statistical Science Bayesian Nonparametric Learning of Complex Dynamical Phenomena Emily Fox Joint work with Erik Sudderth (Brown University), Michael Jordan (UC Berkeley),

Duke University Department of Statistical Science Bayesian Nonparametric Learning of Complex Dynamical Phenomena Emily Fox Joint work with Erik Sudderth (Brown University), Michael Jordan (UC Berkeley),

An introduction to Sequential Monte Carlo

An introduction to Sequential Monte Carlo Thang Bui Jes Frellsen Department of Engineering University of Cambridge Research and Communication Club 6 February 2014 1 Sequential Monte Carlo (SMC) methods

An introduction to Sequential Monte Carlo Thang Bui Jes Frellsen Department of Engineering University of Cambridge Research and Communication Club 6 February 2014 1 Sequential Monte Carlo (SMC) methods

EVALUATING SYMMETRIC INFORMATION GAP BETWEEN DYNAMICAL SYSTEMS USING PARTICLE FILTER

EVALUATING SYMMETRIC INFORMATION GAP BETWEEN DYNAMICAL SYSTEMS USING PARTICLE FILTER Zhen Zhen 1, Jun Young Lee 2, and Abdus Saboor 3 1 Mingde College, Guizhou University, China zhenz2000@21cn.com 2 Department

EVALUATING SYMMETRIC INFORMATION GAP BETWEEN DYNAMICAL SYSTEMS USING PARTICLE FILTER Zhen Zhen 1, Jun Young Lee 2, and Abdus Saboor 3 1 Mingde College, Guizhou University, China zhenz2000@21cn.com 2 Department

Auxiliary Particle Methods

Auxiliary Particle Methods Perspectives & Applications Adam M. Johansen 1 adam.johansen@bristol.ac.uk Oxford University Man Institute 29th May 2008 1 Collaborators include: Arnaud Doucet, Nick Whiteley

Auxiliary Particle Methods Perspectives & Applications Adam M. Johansen 1 adam.johansen@bristol.ac.uk Oxford University Man Institute 29th May 2008 1 Collaborators include: Arnaud Doucet, Nick Whiteley

Kernel Sequential Monte Carlo

Kernel Sequential Monte Carlo Ingmar Schuster (Paris Dauphine) Heiko Strathmann (University College London) Brooks Paige (Oxford) Dino Sejdinovic (Oxford) * equal contribution April 25, 2016 1 / 37 Section

Kernel Sequential Monte Carlo Ingmar Schuster (Paris Dauphine) Heiko Strathmann (University College London) Brooks Paige (Oxford) Dino Sejdinovic (Oxford) * equal contribution April 25, 2016 1 / 37 Section

Unobserved. Components and. Time Series. Econometrics. Edited by. Siem Jan Koopman. and Neil Shephard OXFORD UNIVERSITY PRESS

Unobserved Components and Time Series Econometrics Edited by Siem Jan Koopman and Neil Shephard OXFORD UNIVERSITY PRESS CONTENTS LIST OF FIGURES LIST OF TABLES ix XV 1 Introduction 1 Siem Jan Koopman and

Unobserved Components and Time Series Econometrics Edited by Siem Jan Koopman and Neil Shephard OXFORD UNIVERSITY PRESS CONTENTS LIST OF FIGURES LIST OF TABLES ix XV 1 Introduction 1 Siem Jan Koopman and

Recent Advances in Bayesian Inference Techniques

Recent Advances in Bayesian Inference Techniques Christopher M. Bishop Microsoft Research, Cambridge, U.K. research.microsoft.com/~cmbishop SIAM Conference on Data Mining, April 2004 Abstract Bayesian

Recent Advances in Bayesian Inference Techniques Christopher M. Bishop Microsoft Research, Cambridge, U.K. research.microsoft.com/~cmbishop SIAM Conference on Data Mining, April 2004 Abstract Bayesian

Gaussian Process Approximations of Stochastic Differential Equations

Gaussian Process Approximations of Stochastic Differential Equations Cédric Archambeau Centre for Computational Statistics and Machine Learning University College London c.archambeau@cs.ucl.ac.uk CSML

Gaussian Process Approximations of Stochastic Differential Equations Cédric Archambeau Centre for Computational Statistics and Machine Learning University College London c.archambeau@cs.ucl.ac.uk CSML

RAO-BLACKWELLISED PARTICLE FILTERS: EXAMPLES OF APPLICATIONS

RAO-BLACKWELLISED PARTICLE FILTERS: EXAMPLES OF APPLICATIONS Frédéric Mustière e-mail: mustiere@site.uottawa.ca Miodrag Bolić e-mail: mbolic@site.uottawa.ca Martin Bouchard e-mail: bouchard@site.uottawa.ca

RAO-BLACKWELLISED PARTICLE FILTERS: EXAMPLES OF APPLICATIONS Frédéric Mustière e-mail: mustiere@site.uottawa.ca Miodrag Bolić e-mail: mbolic@site.uottawa.ca Martin Bouchard e-mail: bouchard@site.uottawa.ca

STA 4273H: Statistical Machine Learning

STA 4273H: Statistical Machine Learning Russ Salakhutdinov Department of Computer Science! Department of Statistical Sciences! rsalakhu@cs.toronto.edu! h0p://www.cs.utoronto.ca/~rsalakhu/ Lecture 7 Approximate

STA 4273H: Statistical Machine Learning Russ Salakhutdinov Department of Computer Science! Department of Statistical Sciences! rsalakhu@cs.toronto.edu! h0p://www.cs.utoronto.ca/~rsalakhu/ Lecture 7 Approximate

STA 414/2104: Machine Learning

STA 414/2104: Machine Learning Russ Salakhutdinov Department of Computer Science! Department of Statistics! rsalakhu@cs.toronto.edu! http://www.cs.toronto.edu/~rsalakhu/ Lecture 9 Sequential Data So far

STA 414/2104: Machine Learning Russ Salakhutdinov Department of Computer Science! Department of Statistics! rsalakhu@cs.toronto.edu! http://www.cs.toronto.edu/~rsalakhu/ Lecture 9 Sequential Data So far

A central limit theorem with application to inference in α-stable regression models

Central Limit Theorem for the α-stable Distribution A central limit theorem with application to inference in α-stable regression models Marina Riabiz Tohid Ardeshiri Simon J Godsill Department of Engineering

Central Limit Theorem for the α-stable Distribution A central limit theorem with application to inference in α-stable regression models Marina Riabiz Tohid Ardeshiri Simon J Godsill Department of Engineering

Bayesian Monte Carlo Filtering for Stochastic Volatility Models

Bayesian Monte Carlo Filtering for Stochastic Volatility Models Roberto Casarin CEREMADE University Paris IX (Dauphine) and Dept. of Economics University Ca Foscari, Venice Abstract Modelling of the financial

Bayesian Monte Carlo Filtering for Stochastic Volatility Models Roberto Casarin CEREMADE University Paris IX (Dauphine) and Dept. of Economics University Ca Foscari, Venice Abstract Modelling of the financial

Bayesian Methods for Machine Learning

Bayesian Methods for Machine Learning CS 584: Big Data Analytics Material adapted from Radford Neal s tutorial (http://ftp.cs.utoronto.ca/pub/radford/bayes-tut.pdf), Zoubin Ghahramni (http://hunch.net/~coms-4771/zoubin_ghahramani_bayesian_learning.pdf),

Bayesian Methods for Machine Learning CS 584: Big Data Analytics Material adapted from Radford Neal s tutorial (http://ftp.cs.utoronto.ca/pub/radford/bayes-tut.pdf), Zoubin Ghahramni (http://hunch.net/~coms-4771/zoubin_ghahramani_bayesian_learning.pdf),

Hierarchical Bayesian approaches for robust inference in ARX models

Hierarchical Bayesian approaches for robust inference in ARX models Johan Dahlin, Fredrik Lindsten, Thomas Bo Schön and Adrian George Wills Linköping University Post Print N.B.: When citing this work,

Hierarchical Bayesian approaches for robust inference in ARX models Johan Dahlin, Fredrik Lindsten, Thomas Bo Schön and Adrian George Wills Linköping University Post Print N.B.: When citing this work,

An efficient stochastic approximation EM algorithm using conditional particle filters

An efficient stochastic approximation EM algorithm using conditional particle filters Fredrik Lindsten Linköping University Post Print N.B.: When citing this work, cite the original article. Original Publication:

An efficient stochastic approximation EM algorithm using conditional particle filters Fredrik Lindsten Linköping University Post Print N.B.: When citing this work, cite the original article. Original Publication:

The Particle Filter. PD Dr. Rudolph Triebel Computer Vision Group. Machine Learning for Computer Vision

The Particle Filter Non-parametric implementation of Bayes filter Represents the belief (posterior) random state samples. by a set of This representation is approximate. Can represent distributions that

The Particle Filter Non-parametric implementation of Bayes filter Represents the belief (posterior) random state samples. by a set of This representation is approximate. Can represent distributions that

Bayesian harmonic models for musical signal analysis. Simon Godsill and Manuel Davy

Bayesian harmonic models for musical signal analysis Simon Godsill and Manuel Davy June 2, 2002 Cambridge University Engineering Department and IRCCyN UMR CNRS 6597 The work of both authors was partially

Bayesian harmonic models for musical signal analysis Simon Godsill and Manuel Davy June 2, 2002 Cambridge University Engineering Department and IRCCyN UMR CNRS 6597 The work of both authors was partially

ABC methods for phase-type distributions with applications in insurance risk problems

ABC methods for phase-type with applications problems Concepcion Ausin, Department of Statistics, Universidad Carlos III de Madrid Joint work with: Pedro Galeano, Universidad Carlos III de Madrid Simon

ABC methods for phase-type with applications problems Concepcion Ausin, Department of Statistics, Universidad Carlos III de Madrid Joint work with: Pedro Galeano, Universidad Carlos III de Madrid Simon

Time Series Analysis. James D. Hamilton PRINCETON UNIVERSITY PRESS PRINCETON, NEW JERSEY

Time Series Analysis James D. Hamilton PRINCETON UNIVERSITY PRESS PRINCETON, NEW JERSEY PREFACE xiii 1 Difference Equations 1.1. First-Order Difference Equations 1 1.2. pth-order Difference Equations 7

Time Series Analysis James D. Hamilton PRINCETON UNIVERSITY PRESS PRINCETON, NEW JERSEY PREFACE xiii 1 Difference Equations 1.1. First-Order Difference Equations 1 1.2. pth-order Difference Equations 7

Bayesian Networks BY: MOHAMAD ALSABBAGH

Bayesian Networks BY: MOHAMAD ALSABBAGH Outlines Introduction Bayes Rule Bayesian Networks (BN) Representation Size of a Bayesian Network Inference via BN BN Learning Dynamic BN Introduction Conditional

Bayesian Networks BY: MOHAMAD ALSABBAGH Outlines Introduction Bayes Rule Bayesian Networks (BN) Representation Size of a Bayesian Network Inference via BN BN Learning Dynamic BN Introduction Conditional

STA414/2104. Lecture 11: Gaussian Processes. Department of Statistics

STA414/2104 Lecture 11: Gaussian Processes Department of Statistics www.utstat.utoronto.ca Delivered by Mark Ebden with thanks to Russ Salakhutdinov Outline Gaussian Processes Exam review Course evaluations

STA414/2104 Lecture 11: Gaussian Processes Department of Statistics www.utstat.utoronto.ca Delivered by Mark Ebden with thanks to Russ Salakhutdinov Outline Gaussian Processes Exam review Course evaluations

Modelling Operational Risk Using Bayesian Inference

Pavel V. Shevchenko Modelling Operational Risk Using Bayesian Inference 4y Springer 1 Operational Risk and Basel II 1 1.1 Introduction to Operational Risk 1 1.2 Defining Operational Risk 4 1.3 Basel II

Pavel V. Shevchenko Modelling Operational Risk Using Bayesian Inference 4y Springer 1 Operational Risk and Basel II 1 1.1 Introduction to Operational Risk 1 1.2 Defining Operational Risk 4 1.3 Basel II

Learning Static Parameters in Stochastic Processes

Learning Static Parameters in Stochastic Processes Bharath Ramsundar December 14, 2012 1 Introduction Consider a Markovian stochastic process X T evolving (perhaps nonlinearly) over time variable T. We

Learning Static Parameters in Stochastic Processes Bharath Ramsundar December 14, 2012 1 Introduction Consider a Markovian stochastic process X T evolving (perhaps nonlinearly) over time variable T. We

Continuous State MRF s

EE64 Digital Image Processing II: Purdue University VISE - December 4, Continuous State MRF s Topics to be covered: Quadratic functions Non-Convex functions Continuous MAP estimation Convex functions EE64

EE64 Digital Image Processing II: Purdue University VISE - December 4, Continuous State MRF s Topics to be covered: Quadratic functions Non-Convex functions Continuous MAP estimation Convex functions EE64

Kalman filtering and friends: Inference in time series models. Herke van Hoof slides mostly by Michael Rubinstein

Kalman filtering and friends: Inference in time series models Herke van Hoof slides mostly by Michael Rubinstein Problem overview Goal Estimate most probable state at time k using measurement up to time

Kalman filtering and friends: Inference in time series models Herke van Hoof slides mostly by Michael Rubinstein Problem overview Goal Estimate most probable state at time k using measurement up to time

Introduction to Machine Learning

Introduction to Machine Learning Brown University CSCI 1950-F, Spring 2012 Prof. Erik Sudderth Lecture 25: Markov Chain Monte Carlo (MCMC) Course Review and Advanced Topics Many figures courtesy Kevin

Introduction to Machine Learning Brown University CSCI 1950-F, Spring 2012 Prof. Erik Sudderth Lecture 25: Markov Chain Monte Carlo (MCMC) Course Review and Advanced Topics Many figures courtesy Kevin

Fundamental Issues in Bayesian Functional Data Analysis. Dennis D. Cox Rice University

Fundamental Issues in Bayesian Functional Data Analysis Dennis D. Cox Rice University 1 Introduction Question: What are functional data? Answer: Data that are functions of a continuous variable.... say

Fundamental Issues in Bayesian Functional Data Analysis Dennis D. Cox Rice University 1 Introduction Question: What are functional data? Answer: Data that are functions of a continuous variable.... say

Hmms with variable dimension structures and extensions

Hmm days/enst/january 21, 2002 1 Hmms with variable dimension structures and extensions Christian P. Robert Université Paris Dauphine www.ceremade.dauphine.fr/ xian Hmm days/enst/january 21, 2002 2 1 Estimating

Hmm days/enst/january 21, 2002 1 Hmms with variable dimension structures and extensions Christian P. Robert Université Paris Dauphine www.ceremade.dauphine.fr/ xian Hmm days/enst/january 21, 2002 2 1 Estimating

Master 2 Informatique Probabilistic Learning and Data Analysis

Master 2 Informatique Probabilistic Learning and Data Analysis Faicel Chamroukhi Maître de Conférences USTV, LSIS UMR CNRS 7296 email: chamroukhi@univ-tln.fr web: chamroukhi.univ-tln.fr 2013/2014 Faicel

Master 2 Informatique Probabilistic Learning and Data Analysis Faicel Chamroukhi Maître de Conférences USTV, LSIS UMR CNRS 7296 email: chamroukhi@univ-tln.fr web: chamroukhi.univ-tln.fr 2013/2014 Faicel

Hidden Markov Models for precipitation

Hidden Markov Models for precipitation Pierre Ailliot Université de Brest Joint work with Peter Thomson Statistics Research Associates (NZ) Page 1 Context Part of the project Climate-related risks for

Hidden Markov Models for precipitation Pierre Ailliot Université de Brest Joint work with Peter Thomson Statistics Research Associates (NZ) Page 1 Context Part of the project Climate-related risks for

Exercises Tutorial at ICASSP 2016 Learning Nonlinear Dynamical Models Using Particle Filters

Exercises Tutorial at ICASSP 216 Learning Nonlinear Dynamical Models Using Particle Filters Andreas Svensson, Johan Dahlin and Thomas B. Schön March 18, 216 Good luck! 1 [Bootstrap particle filter for

Exercises Tutorial at ICASSP 216 Learning Nonlinear Dynamical Models Using Particle Filters Andreas Svensson, Johan Dahlin and Thomas B. Schön March 18, 216 Good luck! 1 [Bootstrap particle filter for

Machine Learning for OR & FE

Machine Learning for OR & FE Hidden Markov Models Martin Haugh Department of Industrial Engineering and Operations Research Columbia University Email: martin.b.haugh@gmail.com Additional References: David

Machine Learning for OR & FE Hidden Markov Models Martin Haugh Department of Industrial Engineering and Operations Research Columbia University Email: martin.b.haugh@gmail.com Additional References: David

Particle Learning and Smoothing

Particle Learning and Smoothing Carlos Carvalho, Michael Johannes, Hedibert Lopes and Nicholas Polson This version: September 2009 First draft: December 2007 Abstract In this paper we develop particle

Particle Learning and Smoothing Carlos Carvalho, Michael Johannes, Hedibert Lopes and Nicholas Polson This version: September 2009 First draft: December 2007 Abstract In this paper we develop particle

Assessment of Nonlinear Dynamic Models by Kolmogorov Smirnov Statistics

IEEE TRANSACTIONS ON SIGNAL PROCESSING, VOL 58, NO 10, OCTOBER 2010 5069 Assessment of Nonlinear Dynamic Models by Kolmogorov Smirnov Statistics Petar M Djuric, Fellow, IEEE, and Joaquín Míguez, Member,

IEEE TRANSACTIONS ON SIGNAL PROCESSING, VOL 58, NO 10, OCTOBER 2010 5069 Assessment of Nonlinear Dynamic Models by Kolmogorov Smirnov Statistics Petar M Djuric, Fellow, IEEE, and Joaquín Míguez, Member,

A Note on Auxiliary Particle Filters

A Note on Auxiliary Particle Filters Adam M. Johansen a,, Arnaud Doucet b a Department of Mathematics, University of Bristol, UK b Departments of Statistics & Computer Science, University of British Columbia,

A Note on Auxiliary Particle Filters Adam M. Johansen a,, Arnaud Doucet b a Department of Mathematics, University of Bristol, UK b Departments of Statistics & Computer Science, University of British Columbia,

STONY BROOK UNIVERSITY. CEAS Technical Report 829

1 STONY BROOK UNIVERSITY CEAS Technical Report 829 Variable and Multiple Target Tracking by Particle Filtering and Maximum Likelihood Monte Carlo Method Jaechan Lim January 4, 2006 2 Abstract In most applications

1 STONY BROOK UNIVERSITY CEAS Technical Report 829 Variable and Multiple Target Tracking by Particle Filtering and Maximum Likelihood Monte Carlo Method Jaechan Lim January 4, 2006 2 Abstract In most applications

Brief introduction to Markov Chain Monte Carlo

Brief introduction to Department of Probability and Mathematical Statistics seminar Stochastic modeling in economics and finance November 7, 2011 Brief introduction to Content 1 and motivation Classical

Brief introduction to Department of Probability and Mathematical Statistics seminar Stochastic modeling in economics and finance November 7, 2011 Brief introduction to Content 1 and motivation Classical

Non-Parametric Bayes

Non-Parametric Bayes Mark Schmidt UBC Machine Learning Reading Group January 2016 Current Hot Topics in Machine Learning Bayesian learning includes: Gaussian processes. Approximate inference. Bayesian

Non-Parametric Bayes Mark Schmidt UBC Machine Learning Reading Group January 2016 Current Hot Topics in Machine Learning Bayesian learning includes: Gaussian processes. Approximate inference. Bayesian

A short introduction to INLA and R-INLA

A short introduction to INLA and R-INLA Integrated Nested Laplace Approximation Thomas Opitz, BioSP, INRA Avignon Workshop: Theory and practice of INLA and SPDE November 7, 2018 2/21 Plan for this talk

A short introduction to INLA and R-INLA Integrated Nested Laplace Approximation Thomas Opitz, BioSP, INRA Avignon Workshop: Theory and practice of INLA and SPDE November 7, 2018 2/21 Plan for this talk

Measurements made for web data, media (IP Radio and TV, BBC Iplayer: Port 80 TCP) and VoIP (Skype: Port UDP) traffic.

and VoIP (Skype: Port UDP) traffic.") Real time statistical measurements of IPT(Inter-Packet time) of network traffic were done by designing and coding of efficient measurement tools based on the Libpcap package. Traditional Approach of measuring

Real time statistical measurements of IPT(Inter-Packet time) of network traffic were done by designing and coding of efficient measurement tools based on the Libpcap package. Traditional Approach of measuring

An Alternative to CARMA Models via Iterations of Ornstein Uhlenbeck Processes

An Alternative to CARMA Models via Iterations of Ornstein Uhlenbeck Processes Argimiro Arratia, Alejandra Cabaña, and Enrique M. Cabaña Abstract We present a new construction of continuous ARMA processes

An Alternative to CARMA Models via Iterations of Ornstein Uhlenbeck Processes Argimiro Arratia, Alejandra Cabaña, and Enrique M. Cabaña Abstract We present a new construction of continuous ARMA processes

Human Pose Tracking I: Basics. David Fleet University of Toronto

Human Pose Tracking I: Basics David Fleet University of Toronto CIFAR Summer School, 2009 Looking at People Challenges: Complex pose / motion People have many degrees of freedom, comprising an articulated

Human Pose Tracking I: Basics David Fleet University of Toronto CIFAR Summer School, 2009 Looking at People Challenges: Complex pose / motion People have many degrees of freedom, comprising an articulated

Lecture 2: From Linear Regression to Kalman Filter and Beyond

Lecture 2: From Linear Regression to Kalman Filter and Beyond January 18, 2017 Contents 1 Batch and Recursive Estimation 2 Towards Bayesian Filtering 3 Kalman Filter and Bayesian Filtering and Smoothing

Lecture 2: From Linear Regression to Kalman Filter and Beyond January 18, 2017 Contents 1 Batch and Recursive Estimation 2 Towards Bayesian Filtering 3 Kalman Filter and Bayesian Filtering and Smoothing

State Estimation using Moving Horizon Estimation and Particle Filtering

State Estimation using Moving Horizon Estimation and Particle Filtering James B. Rawlings Department of Chemical and Biological Engineering UW Math Probability Seminar Spring 2009 Rawlings MHE & PF 1 /

State Estimation using Moving Horizon Estimation and Particle Filtering James B. Rawlings Department of Chemical and Biological Engineering UW Math Probability Seminar Spring 2009 Rawlings MHE & PF 1 /

Robert Collins CSE586, PSU Intro to Sampling Methods

Robert Collins Intro to Sampling Methods CSE586 Computer Vision II Penn State Univ Robert Collins A Brief Overview of Sampling Monte Carlo Integration Sampling and Expected Values Inverse Transform Sampling

Robert Collins Intro to Sampling Methods CSE586 Computer Vision II Penn State Univ Robert Collins A Brief Overview of Sampling Monte Carlo Integration Sampling and Expected Values Inverse Transform Sampling

Computer Intensive Methods in Mathematical Statistics

Computer Intensive Methods in Mathematical Statistics Department of mathematics johawes@kth.se Lecture 5 Sequential Monte Carlo methods I 31 March 2017 Computer Intensive Methods (1) Plan of today s lecture

Computer Intensive Methods in Mathematical Statistics Department of mathematics johawes@kth.se Lecture 5 Sequential Monte Carlo methods I 31 March 2017 Computer Intensive Methods (1) Plan of today s lecture

F denotes cumulative density. denotes probability density function; (.)

") BAYESIAN ANALYSIS: FOREWORDS Notation. System means the real thing and a model is an assumed mathematical form for the system.. he probability model class M contains the set of the all admissible models

BAYESIAN ANALYSIS: FOREWORDS Notation. System means the real thing and a model is an assumed mathematical form for the system.. he probability model class M contains the set of the all admissible models

Markov chain Monte Carlo methods for visual tracking

Markov chain Monte Carlo methods for visual tracking Ray Luo rluo@cory.eecs.berkeley.edu Department of Electrical Engineering and Computer Sciences University of California, Berkeley Berkeley, CA 94720

Markov chain Monte Carlo methods for visual tracking Ray Luo rluo@cory.eecs.berkeley.edu Department of Electrical Engineering and Computer Sciences University of California, Berkeley Berkeley, CA 94720

Research Division Federal Reserve Bank of St. Louis Working Paper Series

Research Division Federal Reserve Bank of St Louis Working Paper Series Kalman Filtering with Truncated Normal State Variables for Bayesian Estimation of Macroeconomic Models Michael Dueker Working Paper

Research Division Federal Reserve Bank of St Louis Working Paper Series Kalman Filtering with Truncated Normal State Variables for Bayesian Estimation of Macroeconomic Models Michael Dueker Working Paper

Dynamical Models for Tracking with the Variable Rate Particle Filter

Dynamical Models for Tracking with the Variable Rate Particle Filter Pete Bunch and Simon Godsill Department of Engineering University of Cambridge Cambridge, UK Email: {pb44, sjg}@eng.cam.ac.uk Abstract

Dynamical Models for Tracking with the Variable Rate Particle Filter Pete Bunch and Simon Godsill Department of Engineering University of Cambridge Cambridge, UK Email: {pb44, sjg}@eng.cam.ac.uk Abstract

Lecture 2: From Linear Regression to Kalman Filter and Beyond

Lecture 2: From Linear Regression to Kalman Filter and Beyond Department of Biomedical Engineering and Computational Science Aalto University January 26, 2012 Contents 1 Batch and Recursive Estimation

Lecture 2: From Linear Regression to Kalman Filter and Beyond Department of Biomedical Engineering and Computational Science Aalto University January 26, 2012 Contents 1 Batch and Recursive Estimation

Sequential Monte Carlo Methods for Bayesian Model Selection in Positron Emission Tomography

Methods for Bayesian Model Selection in Positron Emission Tomography Yan Zhou John A.D. Aston and Adam M. Johansen 6th January 2014 Y. Zhou J. A. D. Aston and A. M. Johansen Outline Positron emission tomography

Methods for Bayesian Model Selection in Positron Emission Tomography Yan Zhou John A.D. Aston and Adam M. Johansen 6th January 2014 Y. Zhou J. A. D. Aston and A. M. Johansen Outline Positron emission tomography

Extreme Value Analysis and Spatial Extremes

Extreme Value Analysis and Department of Statistics Purdue University 11/07/2013 Outline Motivation 1 Motivation 2 Extreme Value Theorem and 3 Bayesian Hierarchical Models Copula Models Max-stable Models

Extreme Value Analysis and Department of Statistics Purdue University 11/07/2013 Outline Motivation 1 Motivation 2 Extreme Value Theorem and 3 Bayesian Hierarchical Models Copula Models Max-stable Models

Probabilistic Graphical Models

Probabilistic Graphical Models Brown University CSCI 2950-P, Spring 2013 Prof. Erik Sudderth Lecture 13: Learning in Gaussian Graphical Models, Non-Gaussian Inference, Monte Carlo Methods Some figures

Probabilistic Graphical Models Brown University CSCI 2950-P, Spring 2013 Prof. Erik Sudderth Lecture 13: Learning in Gaussian Graphical Models, Non-Gaussian Inference, Monte Carlo Methods Some figures

Regular Variation and Extreme Events for Stochastic Processes

1 Regular Variation and Extreme Events for Stochastic Processes FILIP LINDSKOG Royal Institute of Technology, Stockholm 2005 based on joint work with Henrik Hult www.math.kth.se/ lindskog 2 Extremes for

1 Regular Variation and Extreme Events for Stochastic Processes FILIP LINDSKOG Royal Institute of Technology, Stockholm 2005 based on joint work with Henrik Hult www.math.kth.se/ lindskog 2 Extremes for

Towards a Bayesian model for Cyber Security

Towards a Bayesian model for Cyber Security Mark Briers (mbriers@turing.ac.uk) Joint work with Henry Clausen and Prof. Niall Adams (Imperial College London) 27 September 2017 The Alan Turing Institute

Towards a Bayesian model for Cyber Security Mark Briers (mbriers@turing.ac.uk) Joint work with Henry Clausen and Prof. Niall Adams (Imperial College London) 27 September 2017 The Alan Turing Institute

Long-Range Dependence and Self-Similarity. c Vladas Pipiras and Murad S. Taqqu

Long-Range Dependence and Self-Similarity c Vladas Pipiras and Murad S. Taqqu January 24, 2016 Contents Contents 2 Preface 8 List of abbreviations 10 Notation 11 1 A brief overview of times series and

Long-Range Dependence and Self-Similarity c Vladas Pipiras and Murad S. Taqqu January 24, 2016 Contents Contents 2 Preface 8 List of abbreviations 10 Notation 11 1 A brief overview of times series and

Introduction to Machine Learning CMU-10701

Introduction to Machine Learning CMU-10701 Markov Chain Monte Carlo Methods Barnabás Póczos & Aarti Singh Contents Markov Chain Monte Carlo Methods Goal & Motivation Sampling Rejection Importance Markov

Introduction to Machine Learning CMU-10701 Markov Chain Monte Carlo Methods Barnabás Póczos & Aarti Singh Contents Markov Chain Monte Carlo Methods Goal & Motivation Sampling Rejection Importance Markov

Markov Chain Monte Carlo

Markov Chain Monte Carlo Michael Johannes Columbia University Nicholas Polson University of Chicago August 28, 2007 1 Introduction The Bayesian solution to any inference problem is a simple rule: compute

Markov Chain Monte Carlo Michael Johannes Columbia University Nicholas Polson University of Chicago August 28, 2007 1 Introduction The Bayesian solution to any inference problem is a simple rule: compute

Artificial Intelligence

Artificial Intelligence Roman Barták Department of Theoretical Computer Science and Mathematical Logic Summary of last lecture We know how to do probabilistic reasoning over time transition model P(X t

Artificial Intelligence Roman Barták Department of Theoretical Computer Science and Mathematical Logic Summary of last lecture We know how to do probabilistic reasoning over time transition model P(X t

A new iterated filtering algorithm

A new iterated filtering algorithm Edward Ionides University of Michigan, Ann Arbor ionides@umich.edu Statistics and Nonlinear Dynamics in Biology and Medicine Thursday July 31, 2014 Overview 1 Introduction

A new iterated filtering algorithm Edward Ionides University of Michigan, Ann Arbor ionides@umich.edu Statistics and Nonlinear Dynamics in Biology and Medicine Thursday July 31, 2014 Overview 1 Introduction

Infinite-State Markov-switching for Dynamic. Volatility Models : Web Appendix

Infinite-State Markov-switching for Dynamic Volatility Models : Web Appendix Arnaud Dufays 1 Centre de Recherche en Economie et Statistique March 19, 2014 1 Comparison of the two MS-GARCH approximations

Infinite-State Markov-switching for Dynamic Volatility Models : Web Appendix Arnaud Dufays 1 Centre de Recherche en Economie et Statistique March 19, 2014 1 Comparison of the two MS-GARCH approximations

Default Priors and Effcient Posterior Computation in Bayesian

Default Priors and Effcient Posterior Computation in Bayesian Factor Analysis January 16, 2010 Presented by Eric Wang, Duke University Background and Motivation A Brief Review of Parameter Expansion Literature

Default Priors and Effcient Posterior Computation in Bayesian Factor Analysis January 16, 2010 Presented by Eric Wang, Duke University Background and Motivation A Brief Review of Parameter Expansion Literature

1 What is a hidden Markov model?

1 What is a hidden Markov model? Consider a Markov chain {X k }, where k is a non-negative integer. Suppose {X k } embedded in signals corrupted by some noise. Indeed, {X k } is hidden due to noise and

1 What is a hidden Markov model? Consider a Markov chain {X k }, where k is a non-negative integer. Suppose {X k } embedded in signals corrupted by some noise. Indeed, {X k } is hidden due to noise and

Sequential Bayesian Updating

BS2 Statistical Inference, Lectures 14 and 15, Hilary Term 2009 May 28, 2009 We consider data arriving sequentially X 1,..., X n,... and wish to update inference on an unknown parameter θ online. In a

BS2 Statistical Inference, Lectures 14 and 15, Hilary Term 2009 May 28, 2009 We consider data arriving sequentially X 1,..., X n,... and wish to update inference on an unknown parameter θ online. In a

Hidden Markov Models. By Parisa Abedi. Slides courtesy: Eric Xing

Hidden Markov Models By Parisa Abedi Slides courtesy: Eric Xing i.i.d to sequential data So far we assumed independent, identically distributed data Sequential (non i.i.d.) data Time-series data E.g. Speech

Hidden Markov Models By Parisa Abedi Slides courtesy: Eric Xing i.i.d to sequential data So far we assumed independent, identically distributed data Sequential (non i.i.d.) data Time-series data E.g. Speech

Self Adaptive Particle Filter

Self Adaptive Particle Filter Alvaro Soto Pontificia Universidad Catolica de Chile Department of Computer Science Vicuna Mackenna 4860 (143), Santiago 22, Chile asoto@ing.puc.cl Abstract The particle filter

Self Adaptive Particle Filter Alvaro Soto Pontificia Universidad Catolica de Chile Department of Computer Science Vicuna Mackenna 4860 (143), Santiago 22, Chile asoto@ing.puc.cl Abstract The particle filter

Chapter 4 Dynamic Bayesian Networks Fall Jin Gu, Michael Zhang

Chapter 4 Dynamic Bayesian Networks 2016 Fall Jin Gu, Michael Zhang Reviews: BN Representation Basic steps for BN representations Define variables Define the preliminary relations between variables Check

Chapter 4 Dynamic Bayesian Networks 2016 Fall Jin Gu, Michael Zhang Reviews: BN Representation Basic steps for BN representations Define variables Define the preliminary relations between variables Check

CPSC 540: Machine Learning

CPSC 540: Machine Learning MCMC and Non-Parametric Bayes Mark Schmidt University of British Columbia Winter 2016 Admin I went through project proposals: Some of you got a message on Piazza. No news is

CPSC 540: Machine Learning MCMC and Non-Parametric Bayes Mark Schmidt University of British Columbia Winter 2016 Admin I went through project proposals: Some of you got a message on Piazza. No news is

Particle MCMC for Bayesian Microwave Control

Particle MCMC for Bayesian Microwave Control P. Minvielle 1, A. Todeschini 2, F. Caron 3, P. Del Moral 4, 1 CEA-CESTA, 33114 Le Barp, France 2 INRIA Bordeaux Sud-Ouest, 351, cours de la Liberation, 33405

Particle MCMC for Bayesian Microwave Control P. Minvielle 1, A. Todeschini 2, F. Caron 3, P. Del Moral 4, 1 CEA-CESTA, 33114 Le Barp, France 2 INRIA Bordeaux Sud-Ouest, 351, cours de la Liberation, 33405

Note Set 5: Hidden Markov Models

Note Set 5: Hidden Markov Models Probabilistic Learning: Theory and Algorithms, CS 274A, Winter 2016 1 Hidden Markov Models (HMMs) 1.1 Introduction Consider observed data vectors x t that are d-dimensional

Note Set 5: Hidden Markov Models Probabilistic Learning: Theory and Algorithms, CS 274A, Winter 2016 1 Hidden Markov Models (HMMs) 1.1 Introduction Consider observed data vectors x t that are d-dimensional

The Scaled Unscented Transformation

The Scaled Unscented Transformation Simon J. Julier, IDAK Industries, 91 Missouri Blvd., #179 Jefferson City, MO 6519 E-mail:sjulier@idak.com Abstract This paper describes a generalisation of the unscented

The Scaled Unscented Transformation Simon J. Julier, IDAK Industries, 91 Missouri Blvd., #179 Jefferson City, MO 6519 E-mail:sjulier@idak.com Abstract This paper describes a generalisation of the unscented

Monte Carlo Methods. Handbook of. University ofqueensland. Thomas Taimre. Zdravko I. Botev. Dirk P. Kroese. Universite de Montreal

Handbook of Monte Carlo Methods Dirk P. Kroese University ofqueensland Thomas Taimre University ofqueensland Zdravko I. Botev Universite de Montreal A JOHN WILEY & SONS, INC., PUBLICATION Preface Acknowledgments

Handbook of Monte Carlo Methods Dirk P. Kroese University ofqueensland Thomas Taimre University ofqueensland Zdravko I. Botev Universite de Montreal A JOHN WILEY & SONS, INC., PUBLICATION Preface Acknowledgments

Capturing Network Traffic Dynamics Small Scales. Rolf Riedi

Capturing Network Traffic Dynamics Small Scales Rolf Riedi Dept of Statistics Stochastic Systems and Modelling in Networking and Finance Part II Dependable Adaptive Systems and Mathematical Modeling Kaiserslautern,

Capturing Network Traffic Dynamics Small Scales Rolf Riedi Dept of Statistics Stochastic Systems and Modelling in Networking and Finance Part II Dependable Adaptive Systems and Mathematical Modeling Kaiserslautern,

STA 4273H: Statistical Machine Learning

STA 4273H: Statistical Machine Learning Russ Salakhutdinov Department of Statistics! rsalakhu@utstat.toronto.edu! http://www.utstat.utoronto.ca/~rsalakhu/ Sidney Smith Hall, Room 6002 Lecture 7 Approximate

STA 4273H: Statistical Machine Learning Russ Salakhutdinov Department of Statistics! rsalakhu@utstat.toronto.edu! http://www.utstat.utoronto.ca/~rsalakhu/ Sidney Smith Hall, Room 6002 Lecture 7 Approximate

9 Multi-Model State Estimation

Technion Israel Institute of Technology, Department of Electrical Engineering Estimation and Identification in Dynamical Systems (048825) Lecture Notes, Fall 2009, Prof. N. Shimkin 9 Multi-Model State

Technion Israel Institute of Technology, Department of Electrical Engineering Estimation and Identification in Dynamical Systems (048825) Lecture Notes, Fall 2009, Prof. N. Shimkin 9 Multi-Model State

Approximate Inference

Approximate Inference Simulation has a name: sampling Sampling is a hot topic in machine learning, and it s really simple Basic idea: Draw N samples from a sampling distribution S Compute an approximate

Approximate Inference Simulation has a name: sampling Sampling is a hot topic in machine learning, and it s really simple Basic idea: Draw N samples from a sampling distribution S Compute an approximate

A note on Reversible Jump Markov Chain Monte Carlo

A note on Reversible Jump Markov Chain Monte Carlo Hedibert Freitas Lopes Graduate School of Business The University of Chicago 5807 South Woodlawn Avenue Chicago, Illinois 60637 February, 1st 2006 1 Introduction

A note on Reversible Jump Markov Chain Monte Carlo Hedibert Freitas Lopes Graduate School of Business The University of Chicago 5807 South Woodlawn Avenue Chicago, Illinois 60637 February, 1st 2006 1 Introduction

Diagnostic Test for GARCH Models Based on Absolute Residual Autocorrelations

Diagnostic Test for GARCH Models Based on Absolute Residual Autocorrelations Farhat Iqbal Department of Statistics, University of Balochistan Quetta-Pakistan farhatiqb@gmail.com Abstract In this paper

Diagnostic Test for GARCH Models Based on Absolute Residual Autocorrelations Farhat Iqbal Department of Statistics, University of Balochistan Quetta-Pakistan farhatiqb@gmail.com Abstract In this paper

Markov Chain Monte Carlo methods

Markov Chain Monte Carlo methods Tomas McKelvey and Lennart Svensson Signal Processing Group Department of Signals and Systems Chalmers University of Technology, Sweden November 26, 2012 Today s learning

Markov Chain Monte Carlo methods Tomas McKelvey and Lennart Svensson Signal Processing Group Department of Signals and Systems Chalmers University of Technology, Sweden November 26, 2012 Today s learning

Applied Bayesian Nonparametrics 3. Infinite Hidden Markov Models

Applied Bayesian Nonparametrics 3. Infinite Hidden Markov Models Tutorial at CVPR 2012 Erik Sudderth Brown University Work by E. Fox, E. Sudderth, M. Jordan, & A. Willsky AOAS 2011: A Sticky HDP-HMM with

Applied Bayesian Nonparametrics 3. Infinite Hidden Markov Models Tutorial at CVPR 2012 Erik Sudderth Brown University Work by E. Fox, E. Sudderth, M. Jordan, & A. Willsky AOAS 2011: A Sticky HDP-HMM with

Part I State space models

Part I State space models 1 Introduction to state space time series analysis James Durbin Department of Statistics, London School of Economics and Political Science Abstract The paper presents a broad

Part I State space models 1 Introduction to state space time series analysis James Durbin Department of Statistics, London School of Economics and Political Science Abstract The paper presents a broad

The Poisson transform for unnormalised statistical models. Nicolas Chopin (ENSAE) joint work with Simon Barthelmé (CNRS, Gipsa-LAB)

joint work with Simon Barthelmé (CNRS, Gipsa-LAB)") The Poisson transform for unnormalised statistical models Nicolas Chopin (ENSAE) joint work with Simon Barthelmé (CNRS, Gipsa-LAB) Part I Unnormalised statistical models Unnormalised statistical models

The Poisson transform for unnormalised statistical models Nicolas Chopin (ENSAE) joint work with Simon Barthelmé (CNRS, Gipsa-LAB) Part I Unnormalised statistical models Unnormalised statistical models

Sensor Fusion: Particle Filter

Sensor Fusion: Particle Filter By: Gordana Stojceska stojcesk@in.tum.de Outline Motivation Applications Fundamentals Tracking People Advantages and disadvantages Summary June 05 JASS '05, St.Petersburg,

Sensor Fusion: Particle Filter By: Gordana Stojceska stojcesk@in.tum.de Outline Motivation Applications Fundamentals Tracking People Advantages and disadvantages Summary June 05 JASS '05, St.Petersburg,

Multiple Speaker Tracking with the Factorial von Mises- Fisher Filter

Multiple Speaker Tracking with the Factorial von Mises- Fisher Filter IEEE International Workshop on Machine Learning for Signal Processing Sept 21-24, 2014 Reims, France Johannes Traa, Paris Smaragdis

Multiple Speaker Tracking with the Factorial von Mises- Fisher Filter IEEE International Workshop on Machine Learning for Signal Processing Sept 21-24, 2014 Reims, France Johannes Traa, Paris Smaragdis

Kurume University Faculty of Economics Monograph Collection 18. Theoretical Advances and Applications in. Operations Research. Kyushu University Press

Kurume University Faculty of Economics Monograph Collection 18 Theoretical Advances and Applications in Operations Research Managing Editor Kangrong Tan General Advisor Joe Gani Kyushu University Press

Kurume University Faculty of Economics Monograph Collection 18 Theoretical Advances and Applications in Operations Research Managing Editor Kangrong Tan General Advisor Joe Gani Kyushu University Press

LINEAR PROGRAMMING-BASED ESTIMATORS IN NONNEGATIVE AUTOREGRESSION

LINEAR PROGRAMMING-BASED ESTIMATORS IN NONNEGATIVE AUTOREGRESSION DANIEL PREVE JUNE 10, 2013 Abstract. This note studies robust estimation of the autoregressive (AR) parameter in a nonlinear, nonnegative

LINEAR PROGRAMMING-BASED ESTIMATORS IN NONNEGATIVE AUTOREGRESSION DANIEL PREVE JUNE 10, 2013 Abstract. This note studies robust estimation of the autoregressive (AR) parameter in a nonlinear, nonnegative

Normalized kernel-weighted random measures

Normalized kernel-weighted random measures Jim Griffin University of Kent 1 August 27 Outline 1 Introduction 2 Ornstein-Uhlenbeck DP 3 Generalisations Bayesian Density Regression We observe data (x 1,

Normalized kernel-weighted random measures Jim Griffin University of Kent 1 August 27 Outline 1 Introduction 2 Ornstein-Uhlenbeck DP 3 Generalisations Bayesian Density Regression We observe data (x 1,

Nonparametric Bayesian Methods (Gaussian Processes)

") [70240413 Statistical Machine Learning, Spring, 2015] Nonparametric Bayesian Methods (Gaussian Processes) Jun Zhu dcszj@mail.tsinghua.edu.cn http://bigml.cs.tsinghua.edu.cn/~jun State Key Lab of Intelligent

[70240413 Statistical Machine Learning, Spring, 2015] Nonparametric Bayesian Methods (Gaussian Processes) Jun Zhu dcszj@mail.tsinghua.edu.cn http://bigml.cs.tsinghua.edu.cn/~jun State Key Lab of Intelligent

Probabilistic Graphical Models

Probabilistic Graphical Models Lecture 12 Dynamical Models CS/CNS/EE 155 Andreas Krause Homework 3 out tonight Start early!! Announcements Project milestones due today Please email to TAs 2 Parameter learning

Probabilistic Graphical Models Lecture 12 Dynamical Models CS/CNS/EE 155 Andreas Krause Homework 3 out tonight Start early!! Announcements Project milestones due today Please email to TAs 2 Parameter learning