Introduction to Econometrics

|

|

|

- Lydia Holmes

- 5 years ago

- Views:

Transcription

1 Introduction to Econometrics STAT-S-301 Introduction to Time Series Regression and Forecasting (2016/2017) Lecturer: Yves Dominicy Teaching Assistant: Elise Petit 1

2 Introduction to Time Series Regression and Forecasting Time series data are data collected on the same observational unit at multiple time periods: Aggregate consumption and GDP for a country (for example, 20 years of quarterly observations = 80 observations). Yen/$, pound/$ and Euro/$ exchange rates (daily data for 1 year = 365 observations). Cigarette consumption per capital in California, by year. 2

3 Example #1 of time series data: US rate of inflation 3

4 Example #2: US rate of unemployment 4

5 Why use time series data? To develop forecasting models: o What will the rate of inflation be next year? To estimate dynamic causal effects: o If the Fed increases the Federal Funds rate now, what will be the effect on the rates of inflation and unemployment in 3 months? in 12 months? o What is the effect over time on cigarette consumption of a hike in the cigarette tax. Modeling risks, which is used in financial markets, e.g. modeling changing variances and volatility clustering. Applications outside of economics include environmental and climate modeling, engineering, compuer science. 5

6 Time series data raises new technical issues Time lags. Correlation over time (serial correlation or autocorrelation, which we encountered in panel data). Forecasting models that have no causal interpretation (specialized tools for forecasting): o autoregressive (AR) models o autoregressive distributed lag (ADL) models. Conditions under which dynamic effects can be estimated, and how to estimate them. Calculation of standard errors when the errors are serially correlated. 6

7 Using Regression Models for Forecasting Forecasting and estimation of causal effects are quite different objectives. For forecasting, o 2 R matters (a lot!) o Omitted variable bias isn t a problem! o We will not worry about interpreting coefficients in forecasting models. o External validity is paramount: the model estimated using historical data must hold into the (near) future. 7

8 Notation for time series data Y t = value of Y in period t. Data set: Y 1,,Y T = T observations on the time series random variable Y. We consider only consecutive, evenly-spaced observations (for example, monthly, 1960 to 1999, no missing months) (else yet more complications...). 8

9 We will transform time series variables using lags, first differences, logarithms, & growth rates 9

10 Example: Quarterly rate of inflation at an annual rate CPI in the first quarter of 1999 (1999:I) = CPI in the second quarter of 1999 (1999:II) = Percentage change in CPI, 1999:I to 1999:II = = = 0.703%. Percentage change in CPI, 1999:I to 1999:II, at an annual rate = 4 x = 2.81% (percent per year). Like interest rates, inflation rates are (as a matter of convention) reported at an annual rate. Using the logarithmic approximation to percent changes yields 4 x100 x[log(166.03) log(164.87)] = 2.80%. 10

")

11 Example: US CPI inflation its first lag and its change CPI = Consumer price index (Bureau of Labor Statistics) 11

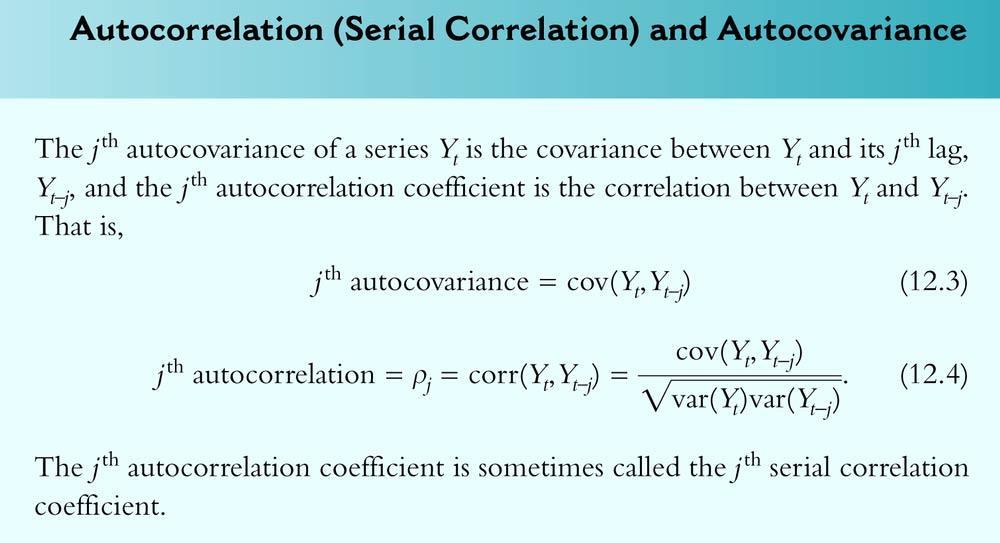

12 Autocorrelation The correlation of a series with its own lagged values is called autocorrelation or serial correlation. The first autocorrelation of Y t is corr(y t,y t 1 ). The first autocovariance of Y t is cov(y t,y t 1 ). Thus cov( Yt, Yt 1) corr(y t,y t 1 ) = = 1. var( Y ) var( Y ) t t 1 These are population correlations they describe the population joint distribution of (Y t,y t 1 ). 12

13 13

the quarter-to-quarter change in the quarterly rate of")

14 Example: Autocorrelations of: (1) the quarterly rate of U.S. inflation, (2) the quarter-to-quarter change in the quarterly rate of inflation. 14

15 The inflation rate is highly serially correlated ( 1 =.85). Last quarter s inflation rate contains much information about this quarter s inflation rate. The plot is dominated by multiyear swings. But there are still surprise movements! 15

16 16

17 17

18 Stationarity: a key idea for external validity of time series regression Stationarity says that the past is like the present and the future, at least in a probabilistic sense. We will focus on the case that Y t stationary. 18

19 Autoregressions A natural starting point for a forecasting model is to use past values of Y (that is, Y t 1, Y t 2, ) to forecast Y t. An autoregression is a regression model in which Y t is regressed against its own lagged values. The number of lags used as regressors is called the order of the autoregression. o In a first order autoregression, Y t is regressed against Y t 1. o In a p th order autoregression, Y t is regressed against Y t 1,Y t 2,,Y t p. The First Order Autoregressive (AR(1)) Model. 19

20 The population AR(1) model is Y t = Y t 1 + u t. 0 and 1 do not have causal interpretations. if 1 = 0, Y t 1 is not useful for forecasting Y t. The AR(1) model can be estimated by OLS regression of Y t against Y t 1. Testing 1 = 0 v. 1 0 provides a test of the hypothesis that Y t 1 is not useful for forecasting Y t. 20

21 Example: AR(1) model of the change in inflation Estimated using data from 1962:I 1999:IV. First, let STATA know you are using time series data generate time=q(1959q1)+_n-1; format time %tq; sort time; tsset time; _n is the observation no. So this command creates a new variable time that has a special quarterly date format. Specify the quarterly date format. Sort by time. Let STATA know that the variable time is the variable you want to indicate the time scale. 21

22 Example: AR(1) model of inflation STATA, ctd.. gen lcpi = log(cpi); variable cpi is already in memory.. gen inf = 400*(lcpi[_n]-lcpi[_n-1]); quarterly rate of inflation at an annual rate.. corrgram inf, noplot lags(8); computes first 8 sample autocorrelations LAG AC PAC Q Prob>Q gen inf = 400*(lcpi[_n]-lcpi[_n-1]) This syntax creates a new variable, inf, the nth observation of which is 400 times the difference between the nth observation on lcpi and the n- 1 th observation on lcpi, that is, the first difference of lcpi. 22

23 Example: AR(1) model of inflation STATA, ctd Syntax: L.dinf is the first lag of dinf. reg dinf L.dinf if tin(1962q1,1999q4), r; Regression with robust standard errors Number of obs = 152 F( 1, 150) = 3.96 Prob > F = R-squared = Root MSE = Robust dinf Coef. Std. Err. t P> t [95% Conf. Interval] dinf L _cons if tin(1962q1,1999q4) STATA time series syntax for using only observations between 1962q1 and 1999q4 (inclusive). This requires defining the time scale first, as we did above. 23

24 Forecasts and forecast errors A note on terminology: A predicted value refers to the value of Y predicted (using a regression) for an observation in the sample used to estimate the regression this is the usual definition. A forecast refers to the value of Y forecasted for an observation not in the sample used to estimate the regression. Predicted values are in sample. Forecasts are forecasts of the future which cannot have been used to estimate the regression. 24

25 Forecasts: notation Y t t 1 = forecast of Y t based on Y t 1,Y t 2,, using the population (true unknown) coefficients. Yˆtt 1= forecast of Y t based on Y t 1,Y t 2,, using the estimated coefficients, which were estimated using data through period t 1. For an AR(1), Y t t 1 = Y t 1 Y = ˆ 0 + ˆ 1Y t 1, where ˆ 0 and ˆ 1 were estimated ˆtt 1 using data through period t 1. 25

26 Forecast errors The one-period ahead forecast error is, forecast error = Y t Yˆtt 1. The distinction between a forecast error and a residual is the same as between a forecast and a predicted value: a residual is in-sample, a forecast error is out-of-sample the value of Y t isn t used in the estimation of the regression coefficients. 26

27 The root mean squared forecast error (RMSFE) RMSFE = E Y ˆ 2 [( t Yt t 1) ] The RMSFE is a measure of the spread of the forecast error distribution. The RMSFE is like the standard deviation of u t, except that it explicitly focuses on the forecast error using estimated coefficients, not using the population regression line. The RMSFE is a measure of the magnitude of a typical forecasting mistake. 27

28 Example: forecasting inflation using and AR(1) AR(1) estimated using data from 1962:I 1999:IV: Inf_est= Inf t 1 Inf 1999:III = 2.8 (units are percent, at an annual rate) Inf 1999:IV = 3.2 Inf 1999:IV = 0.4 So the forecast of Inf 2000:I is, Inf_est = x0.4 = so Inf_est = Inf 1999:IV + Inf_est = =

29 The p th order autoregressive model (AR(p)) Y t = Y t Y t p Y t p + u t The AR(p) model uses p lags of Y as regressors. The AR(1) model is a special case. The coefficients do not have a causal interpretation. To test the hypothesis that Y t 2,,Y t p do not further help forecast Y t, beyond Y t 1, use an F-test. Use t- or F-tests to determine the lag order p. Or, better, determine p using an information criterion. 29

30 Example: AR(4) model of inflation Inf_est = Inf t 1.32 Inf t Inf t 3 (.12) (.10) (.09) (.09).04 Inf t 4, (.10) 2 R = 0.21 F-statistic testing lags 2, 3, 4 is 6.43 (p-value <.001). 2 R increased from.04 to.21 by adding lags 2, 3, 4. Lags 2, 3, 4 (jointly) help to predict the change in inflation, above and beyond the first lag. 30

31 Example: AR(4) model of inflation STATA. reg dinf L(1/4).dinf if tin(1962q1,1999q4), r; Regression with robust standard errors Number of obs = 152 F( 4, 147) = 6.79 Prob > F = R-squared = Root MSE = Robust dinf Coef. Std. Err. t P> t [95% Conf. Interval] dinf L L L L _cons NOTES L(1/4).dinf is A convenient way to say use lags 1 4 of dinf as regressors. L1,,L4 refer to the first, second, 4 th lags of dinf. 31

32 . dis "Adjusted Rsquared = " _result(8); result(8) is the rbar-squared Adjusted Rsquared = of the most recently run regression.. test L2.dinf L3.dinf L4.dinf; L2.dinf is the second lag of dinf, etc. ( 1) L2.dinf = 0.0 ( 2) L3.dinf = 0.0 ( 3) L4.dinf = 0.0 F( 3, 147) = 6.43 Prob > F = Note: some of the time series features of STATA differ between STATA v. 7 and STATA v. 8 32

33 Digression: we used Inf, not Inf, in the AR s. Why? The AR(1) model of Inf t 1 is an AR(2) model of Inf t : or or so Inf t = Inf t 1 + u t Inf t Inf t 1 = (Inf t 1 Inf t 2 ) + u t Inf t = Inf t Inf t 1 1 Inf t 2 + u t Inf t = 0 + (1+ 1 )Inf t 1 1 Inf t 2 + u t 33

34 So why use Inf t, not Inf t? AR(1) model of Inf: AR(2) model of Inf: Inf t = Inf t 1 + u t Inf t = Inf t + 2 Inf t 1 + v t When Y t is strongly serially correlated, the OLS estimator of the AR coefficient is biased towards zero. In the extreme case that the AR coefficient = 1, Y t isn t stationary: the u t s accumulate and Y t blows up. If Y t isn t stationary, our regression theory are working with here breaks down. Here, Inf t is strongly serially correlated so to keep ourselves in a framework we understand, the regressions are specified using Inf. 34

35 Time Series Regression with Additional Predictors and the Autoregressive Distributed Lag (ADL) Model So far we have considered forecasting models that use only past values of Y. It makes sense to add other variables (X) that might be useful predictors of Y, above and beyond the predictive value of lagged values of Y: Y t = Y t p Y t p + 1 X t r X t r + u t. This is an autoregressive distributed lag (ADL) model. 35

36 Example: lagged unemployment and inflation According to the Phillips curve says that if unemployment is above its equilibrium, or natural, rate, then the rate of inflation will increase. That is, Inf t should be related to lagged values of the unemployment rate, with a negative coefficient. The rate of unemployment at which inflation neither increases nor decreases is often called the nonaccelerating rate of inflation unemployment rate: the NAIRU. Is this relation found in US economic data? Can this relation be exploited for forecasting inflation? 36

37 The empirical Phillips Curve The NAIRU is the value of u for which Inf = 0 37

38 Example: ADL(4,4) model of inflation Inf_est = Inf t 1.34 Inf t Inf t 3.03 Inf t 4 (.47) (.09) (.10) (.08) (.09) 2.68Unem t Unem t Unem t Unemp t 4 (.47) (.89) (.89) (.44) 2 R = 0.35 a big improvement over the AR(4), for which 2 R =.21 38

39 Example: dinf and unem STATA. reg dinf L(1/4).dinf L(1/4).unem if tin(1962q1,1999q4), r; Regression with robust standard errors Number of obs = 152 F( 8, 143) = 7.99 Prob > F = R-squared = Root MSE = Robust dinf Coef. Std. Err. t P> t [95% Conf. Interval] dinf L L L L unem L L L L _cons

40 Example: ADL(4,4) model of inflation STATA, ctd.. dis "Adjusted Rsquared = " _result(8); Adjusted Rsquared = test L2.dinf L3.dinf L4.dinf; ( 1) L2.dinf = 0.0 ( 2) L3.dinf = 0.0 ( 3) L4.dinf = 0.0 F( 3, 143) = 4.93 The extra lags of dinf are signif. Prob > F = test L1.unem L2.unem L3.unem L4.unem; ( 1) L.unem = 0.0 ( 2) L2.unem = 0.0 ( 3) L3.unem = 0.0 ( 4) L4.unem = 0.0 F( 4, 143) = 8.51 The lags of unem are significant Prob > F = The null hypothesis that the coefficients on the lags of the unemployment rate are all zero is rejected at the 1% significance level using the F- statistic. 40

predictive content.")

41 The test of the joint hypothesis that none of the X s is a useful predictor, above and beyond lagged values of Y, is called a Granger causality test causality is an unfortunate term here: Granger Causality simply refers to (marginal) predictive content. 41

42 Summary: Time Series Forecasting Models For forecasting purposes, it isn t important to have coefficients with a causal interpretation! Simple and reliable forecasts can be produced using AR(p) models these are common benchmark forecasts against which more complicated forecasting models can be assessed. Additional predictors (X s) can be added; the result is an autoregressive distributed lag (ADL) model. Stationary means that the models can be used outside the range of data for which they were estimated. We now have the tools we need to estimate dynamic causal effects... 42

Introduction to Time Series Regression and Forecasting

Introduction to Time Series Regression and Forecasting (SW Chapter 14) Outline 1. Time Series Data: What s Different? 2. Using Regression Models for Forecasting 3. Lags, Differences, Autocorrelation, &

Introduction to Time Series Regression and Forecasting (SW Chapter 14) Outline 1. Time Series Data: What s Different? 2. Using Regression Models for Forecasting 3. Lags, Differences, Autocorrelation, &

Econ 423 Lecture Notes

Econ 423 Lecture Notes (These notes are slightly modified versions of lecture notes provided by Stock and Watson, 2007. They are for instructional purposes only and are not to be distributed outside of

Econ 423 Lecture Notes (These notes are slightly modified versions of lecture notes provided by Stock and Watson, 2007. They are for instructional purposes only and are not to be distributed outside of

Chapter 14: Time Series: Regression & Forecasting

Chapter 14: Time Series: Regression & Forecasting 14-1 1-1 Outline 1. Time Series Data: What s Different? 2. Using Regression Models for Forecasting 3. Lags, Differences, Autocorrelation, & Stationarity

Chapter 14: Time Series: Regression & Forecasting 14-1 1-1 Outline 1. Time Series Data: What s Different? 2. Using Regression Models for Forecasting 3. Lags, Differences, Autocorrelation, & Stationarity

Introduction to Time Series Regression and Forecasting

Introduction to Time Series Regression and Forecasting (SW Chapter 14) Outline 1. Time Series Data: What s Different? 2. Using Regression Models for Forecasting 3. Lags, Differences, Autocorrelation, &

Introduction to Time Series Regression and Forecasting (SW Chapter 14) Outline 1. Time Series Data: What s Different? 2. Using Regression Models for Forecasting 3. Lags, Differences, Autocorrelation, &

10. Time series regression and forecasting

10. Time series regression and forecasting Key feature of this section: Analysis of data on a single entity observed at multiple points in time (time series data) Typical research questions: What is the

10. Time series regression and forecasting Key feature of this section: Analysis of data on a single entity observed at multiple points in time (time series data) Typical research questions: What is the

Econometrics and Structural

Introduction to Time Series Econometrics and Structural Breaks Ziyodullo Parpiev, PhD Outline 1. Stochastic processes 2. Stationary processes 3. Purely random processes 4. Nonstationary processes 5. Integrated

Introduction to Time Series Econometrics and Structural Breaks Ziyodullo Parpiev, PhD Outline 1. Stochastic processes 2. Stationary processes 3. Purely random processes 4. Nonstationary processes 5. Integrated

7 Introduction to Time Series

Econ 495 - Econometric Review 1 7 Introduction to Time Series 7.1 Time Series vs. Cross-Sectional Data Time series data has a temporal ordering, unlike cross-section data, we will need to changes some

Econ 495 - Econometric Review 1 7 Introduction to Time Series 7.1 Time Series vs. Cross-Sectional Data Time series data has a temporal ordering, unlike cross-section data, we will need to changes some

7 Introduction to Time Series Time Series vs. Cross-Sectional Data Detrending Time Series... 15

Econ 495 - Econometric Review 1 Contents 7 Introduction to Time Series 3 7.1 Time Series vs. Cross-Sectional Data............ 3 7.2 Detrending Time Series................... 15 7.3 Types of Stochastic

Econ 495 - Econometric Review 1 Contents 7 Introduction to Time Series 3 7.1 Time Series vs. Cross-Sectional Data............ 3 7.2 Detrending Time Series................... 15 7.3 Types of Stochastic

Econ 423 Lecture Notes: Additional Topics in Time Series 1

Econ 423 Lecture Notes: Additional Topics in Time Series 1 John C. Chao April 25, 2017 1 These notes are based in large part on Chapter 16 of Stock and Watson (2011). They are for instructional purposes

Econ 423 Lecture Notes: Additional Topics in Time Series 1 John C. Chao April 25, 2017 1 These notes are based in large part on Chapter 16 of Stock and Watson (2011). They are for instructional purposes

9) Time series econometrics

Time series econometrics") 30C00200 Econometrics 9) Time series econometrics Timo Kuosmanen Professor Management Science http://nomepre.net/index.php/timokuosmanen 1 Macroeconomic data: GDP Inflation rate Examples of time series

30C00200 Econometrics 9) Time series econometrics Timo Kuosmanen Professor Management Science http://nomepre.net/index.php/timokuosmanen 1 Macroeconomic data: GDP Inflation rate Examples of time series

10) Time series econometrics

Time series econometrics") 30C00200 Econometrics 10) Time series econometrics Timo Kuosmanen Professor, Ph.D. 1 Topics today Static vs. dynamic time series model Suprious regression Stationary and nonstationary time series Unit

30C00200 Econometrics 10) Time series econometrics Timo Kuosmanen Professor, Ph.D. 1 Topics today Static vs. dynamic time series model Suprious regression Stationary and nonstationary time series Unit

Econ 423 Lecture Notes

Econ 423 Lecture Notes (hese notes are modified versions of lecture notes provided by Stock and Watson, 2007. hey are for instructional purposes only and are not to be distributed outside of the classroom.)

Econ 423 Lecture Notes (hese notes are modified versions of lecture notes provided by Stock and Watson, 2007. hey are for instructional purposes only and are not to be distributed outside of the classroom.)

Autoregressive models with distributed lags (ADL)

") Autoregressive models with distributed lags (ADL) It often happens than including the lagged dependent variable in the model results in model which is better fitted and needs less parameters. It can be

Autoregressive models with distributed lags (ADL) It often happens than including the lagged dependent variable in the model results in model which is better fitted and needs less parameters. It can be

Autocorrelation. Think of autocorrelation as signifying a systematic relationship between the residuals measured at different points in time

Autocorrelation Given the model Y t = b 0 + b 1 X t + u t Think of autocorrelation as signifying a systematic relationship between the residuals measured at different points in time This could be caused

Autocorrelation Given the model Y t = b 0 + b 1 X t + u t Think of autocorrelation as signifying a systematic relationship between the residuals measured at different points in time This could be caused

Autoregressive distributed lag models

Introduction In economics, most cases we want to model relationships between variables, and often simultaneously. That means we need to move from univariate time series to multivariate. We do it in two

Introduction In economics, most cases we want to model relationships between variables, and often simultaneously. That means we need to move from univariate time series to multivariate. We do it in two

Question 1 [17 points]: (ch 11)

![Question 1 [17 points]: (ch 11)](/thumbs/95/123686850.jpg "Question 1 [17 points]: (ch 11)") Question 1 [17 points]: (ch 11) A study analyzed the probability that Major League Baseball (MLB) players "survive" for another season, or, in other words, play one more season. They studied a model of

Question 1 [17 points]: (ch 11) A study analyzed the probability that Major League Baseball (MLB) players "survive" for another season, or, in other words, play one more season. They studied a model of

Introduction to Econometrics

Introduction to Econometrics STAT-S-301 Panel Data (2016/2017) Lecturer: Yves Dominicy Teaching Assistant: Elise Petit 1 Regression with Panel Data A panel dataset contains observations on multiple entities

Introduction to Econometrics STAT-S-301 Panel Data (2016/2017) Lecturer: Yves Dominicy Teaching Assistant: Elise Petit 1 Regression with Panel Data A panel dataset contains observations on multiple entities

Handout 12. Endogeneity & Simultaneous Equation Models

Handout 12. Endogeneity & Simultaneous Equation Models In which you learn about another potential source of endogeneity caused by the simultaneous determination of economic variables, and learn how to

Handout 12. Endogeneity & Simultaneous Equation Models In which you learn about another potential source of endogeneity caused by the simultaneous determination of economic variables, and learn how to

Chapter 7. Hypothesis Tests and Confidence Intervals in Multiple Regression

Chapter 7 Hypothesis Tests and Confidence Intervals in Multiple Regression Outline 1. Hypothesis tests and confidence intervals for a single coefficie. Joint hypothesis tests on multiple coefficients 3.

Chapter 7 Hypothesis Tests and Confidence Intervals in Multiple Regression Outline 1. Hypothesis tests and confidence intervals for a single coefficie. Joint hypothesis tests on multiple coefficients 3.

Introduction to Econometrics

Introduction to Econometrics T H I R D E D I T I O N Global Edition James H. Stock Harvard University Mark W. Watson Princeton University Boston Columbus Indianapolis New York San Francisco Upper Saddle

Introduction to Econometrics T H I R D E D I T I O N Global Edition James H. Stock Harvard University Mark W. Watson Princeton University Boston Columbus Indianapolis New York San Francisco Upper Saddle

(a) Briefly discuss the advantage of using panel data in this situation rather than pure crosssections

Briefly discuss the advantage of using panel data in this situation rather than pure crosssections") Answer Key Fixed Effect and First Difference Models 1. See discussion in class.. David Neumark and William Wascher published a study in 199 of the effect of minimum wages on teenage employment using a

Answer Key Fixed Effect and First Difference Models 1. See discussion in class.. David Neumark and William Wascher published a study in 199 of the effect of minimum wages on teenage employment using a

Lecture 4: Multivariate Regression, Part 2

Lecture 4: Multivariate Regression, Part 2 Gauss-Markov Assumptions 1) Linear in Parameters: Y X X X i 0 1 1 2 2 k k 2) Random Sampling: we have a random sample from the population that follows the above

Lecture 4: Multivariate Regression, Part 2 Gauss-Markov Assumptions 1) Linear in Parameters: Y X X X i 0 1 1 2 2 k k 2) Random Sampling: we have a random sample from the population that follows the above

Empirical Application of Simple Regression (Chapter 2)

") Empirical Application of Simple Regression (Chapter 2) 1. The data file is House Data, which can be downloaded from my webpage. 2. Use stata menu File Import Excel Spreadsheet to read the data. Don t forget

Empirical Application of Simple Regression (Chapter 2) 1. The data file is House Data, which can be downloaded from my webpage. 2. Use stata menu File Import Excel Spreadsheet to read the data. Don t forget

Econometrics. 9) Heteroscedasticity and autocorrelation

Heteroscedasticity and autocorrelation") 30C00200 Econometrics 9) Heteroscedasticity and autocorrelation Timo Kuosmanen Professor, Ph.D. http://nomepre.net/index.php/timokuosmanen Today s topics Heteroscedasticity Possible causes Testing for

30C00200 Econometrics 9) Heteroscedasticity and autocorrelation Timo Kuosmanen Professor, Ph.D. http://nomepre.net/index.php/timokuosmanen Today s topics Heteroscedasticity Possible causes Testing for

Measures of Fit from AR(p)

") Measures of Fit from AR(p) Residual Sum of Squared Errors Residual Mean Squared Error Root MSE (Standard Error of Regression) R-squared R-bar-squared = = T t e t SSR 1 2 ˆ = = T t e t p T s 1 2 2 ˆ 1 1

Measures of Fit from AR(p) Residual Sum of Squared Errors Residual Mean Squared Error Root MSE (Standard Error of Regression) R-squared R-bar-squared = = T t e t SSR 1 2 ˆ = = T t e t p T s 1 2 2 ˆ 1 1

Answer all questions from part I. Answer two question from part II.a, and one question from part II.b.

B203: Quantitative Methods Answer all questions from part I. Answer two question from part II.a, and one question from part II.b. Part I: Compulsory Questions. Answer all questions. Each question carries

B203: Quantitative Methods Answer all questions from part I. Answer two question from part II.a, and one question from part II.b. Part I: Compulsory Questions. Answer all questions. Each question carries

Lecture 4: Multivariate Regression, Part 2

Lecture 4: Multivariate Regression, Part 2 Gauss-Markov Assumptions 1) Linear in Parameters: Y X X X i 0 1 1 2 2 k k 2) Random Sampling: we have a random sample from the population that follows the above

Lecture 4: Multivariate Regression, Part 2 Gauss-Markov Assumptions 1) Linear in Parameters: Y X X X i 0 1 1 2 2 k k 2) Random Sampling: we have a random sample from the population that follows the above

Unemployment Rate Example

Unemployment Rate Example Find unemployment rates for men and women in your age bracket Go to FRED Categories/Population/Current Population Survey/Unemployment Rate Release Tables/Selected unemployment

Unemployment Rate Example Find unemployment rates for men and women in your age bracket Go to FRED Categories/Population/Current Population Survey/Unemployment Rate Release Tables/Selected unemployment

Introduction to Econometrics. Multiple Regression (2016/2017)

") Introduction to Econometrics STAT-S-301 Multiple Regression (016/017) Lecturer: Yves Dominicy Teaching Assistant: Elise Petit 1 OLS estimate of the TS/STR relation: OLS estimate of the Test Score/STR relation:

Introduction to Econometrics STAT-S-301 Multiple Regression (016/017) Lecturer: Yves Dominicy Teaching Assistant: Elise Petit 1 OLS estimate of the TS/STR relation: OLS estimate of the Test Score/STR relation:

Statistical Inference with Regression Analysis

Introductory Applied Econometrics EEP/IAS 118 Spring 2015 Steven Buck Lecture #13 Statistical Inference with Regression Analysis Next we turn to calculating confidence intervals and hypothesis testing

Introductory Applied Econometrics EEP/IAS 118 Spring 2015 Steven Buck Lecture #13 Statistical Inference with Regression Analysis Next we turn to calculating confidence intervals and hypothesis testing

ECON3150/4150 Spring 2016

ECON3150/4150 Spring 2016 Lecture 4 - The linear regression model Siv-Elisabeth Skjelbred University of Oslo Last updated: January 26, 2016 1 / 49 Overview These lecture slides covers: The linear regression

ECON3150/4150 Spring 2016 Lecture 4 - The linear regression model Siv-Elisabeth Skjelbred University of Oslo Last updated: January 26, 2016 1 / 49 Overview These lecture slides covers: The linear regression

1: a b c d e 2: a b c d e 3: a b c d e 4: a b c d e 5: a b c d e. 6: a b c d e 7: a b c d e 8: a b c d e 9: a b c d e 10: a b c d e

Economics 102: Analysis of Economic Data Cameron Spring 2016 Department of Economics, U.C.-Davis Final Exam (A) Tuesday June 7 Compulsory. Closed book. Total of 58 points and worth 45% of course grade.

Economics 102: Analysis of Economic Data Cameron Spring 2016 Department of Economics, U.C.-Davis Final Exam (A) Tuesday June 7 Compulsory. Closed book. Total of 58 points and worth 45% of course grade.

Lab 07 Introduction to Econometrics

Lab 07 Introduction to Econometrics Learning outcomes for this lab: Introduce the different typologies of data and the econometric models that can be used Understand the rationale behind econometrics Understand

Lab 07 Introduction to Econometrics Learning outcomes for this lab: Introduce the different typologies of data and the econometric models that can be used Understand the rationale behind econometrics Understand

Augmenting our AR(4) Model of Inflation. The Autoregressive Distributed Lag (ADL) Model

Model of Inflation. The Autoregressive Distributed Lag (ADL) Model") Augmenting our AR(4) Model of Inflation Adding lagged unemployment to our model of inflationary change, we get: Inf t =1.28 (0.31) Inf t 1 (0.39) Inf t 2 +(0.09) Inf t 3 (0.53) (0.09) (0.09) (0.08) (0.08)

Augmenting our AR(4) Model of Inflation Adding lagged unemployment to our model of inflationary change, we get: Inf t =1.28 (0.31) Inf t 1 (0.39) Inf t 2 +(0.09) Inf t 3 (0.53) (0.09) (0.09) (0.08) (0.08)

Lecture#17. Time series III

Lecture#17 Time series III 1 Dynamic causal effects Think of macroeconomic data. Difficult to think of an RCT. Substitute: different treatments to the same (observation unit) at different points in time.

Lecture#17 Time series III 1 Dynamic causal effects Think of macroeconomic data. Difficult to think of an RCT. Substitute: different treatments to the same (observation unit) at different points in time.

Time Series Econometrics For the 21st Century

Time Series Econometrics For the 21st Century by Bruce E. Hansen Department of Economics University of Wisconsin January 2017 Bruce Hansen (University of Wisconsin) Time Series Econometrics January 2017

Time Series Econometrics For the 21st Century by Bruce E. Hansen Department of Economics University of Wisconsin January 2017 Bruce Hansen (University of Wisconsin) Time Series Econometrics January 2017

4. MA(2) +drift: y t = µ + ɛ t + θ 1 ɛ t 1 + θ 2 ɛ t 2. Mean: where θ(l) = 1 + θ 1 L + θ 2 L 2. Therefore,

+drift: y t = µ + ɛ t + θ 1 ɛ t 1 + θ 2 ɛ t 2. Mean: where θ(l) = 1 + θ 1 L + θ 2 L 2. Therefore,") 61 4. MA(2) +drift: y t = µ + ɛ t + θ 1 ɛ t 1 + θ 2 ɛ t 2 Mean: y t = µ + θ(l)ɛ t, where θ(l) = 1 + θ 1 L + θ 2 L 2. Therefore, E(y t ) = µ + θ(l)e(ɛ t ) = µ 62 Example: MA(q) Model: y t = ɛ t + θ 1 ɛ

61 4. MA(2) +drift: y t = µ + ɛ t + θ 1 ɛ t 1 + θ 2 ɛ t 2 Mean: y t = µ + θ(l)ɛ t, where θ(l) = 1 + θ 1 L + θ 2 L 2. Therefore, E(y t ) = µ + θ(l)e(ɛ t ) = µ 62 Example: MA(q) Model: y t = ɛ t + θ 1 ɛ

Nonlinear Regression Functions

Nonlinear Regression Functions (SW Chapter 8) Outline 1. Nonlinear regression functions general comments 2. Nonlinear functions of one variable 3. Nonlinear functions of two variables: interactions 4.

Nonlinear Regression Functions (SW Chapter 8) Outline 1. Nonlinear regression functions general comments 2. Nonlinear functions of one variable 3. Nonlinear functions of two variables: interactions 4.

ECON3327: Financial Econometrics, Spring 2016

ECON3327: Financial Econometrics, Spring 2016 Wooldridge, Introductory Econometrics (5th ed, 2012) Chapter 11: OLS with time series data Stationary and weakly dependent time series The notion of a stationary

ECON3327: Financial Econometrics, Spring 2016 Wooldridge, Introductory Econometrics (5th ed, 2012) Chapter 11: OLS with time series data Stationary and weakly dependent time series The notion of a stationary

ECON Introductory Econometrics. Lecture 13: Internal and external validity

ECON4150 - Introductory Econometrics Lecture 13: Internal and external validity Monique de Haan (moniqued@econ.uio.no) Stock and Watson Chapter 9 Lecture outline 2 Definitions of internal and external

ECON4150 - Introductory Econometrics Lecture 13: Internal and external validity Monique de Haan (moniqued@econ.uio.no) Stock and Watson Chapter 9 Lecture outline 2 Definitions of internal and external

Testing methodology. It often the case that we try to determine the form of the model on the basis of data

Testing methodology It often the case that we try to determine the form of the model on the basis of data The simplest case: we try to determine the set of explanatory variables in the model Testing for

Testing methodology It often the case that we try to determine the form of the model on the basis of data The simplest case: we try to determine the set of explanatory variables in the model Testing for

Warwick Business School Forecasting System. Summary. Ana Galvao, Anthony Garratt and James Mitchell November, 2014

Warwick Business School Forecasting System Summary Ana Galvao, Anthony Garratt and James Mitchell November, 21 The main objective of the Warwick Business School Forecasting System is to provide competitive

Warwick Business School Forecasting System Summary Ana Galvao, Anthony Garratt and James Mitchell November, 21 The main objective of the Warwick Business School Forecasting System is to provide competitive

7. Integrated Processes

7. Integrated Processes Up to now: Analysis of stationary processes (stationary ARMA(p, q) processes) Problem: Many economic time series exhibit non-stationary patterns over time 226 Example: We consider

7. Integrated Processes Up to now: Analysis of stationary processes (stationary ARMA(p, q) processes) Problem: Many economic time series exhibit non-stationary patterns over time 226 Example: We consider

LECTURE 9: GENTLE INTRODUCTION TO

LECTURE 9: GENTLE INTRODUCTION TO REGRESSION WITH TIME SERIES From random variables to random processes (cont d) 2 in cross-sectional regression, we were making inferences about the whole population based

LECTURE 9: GENTLE INTRODUCTION TO REGRESSION WITH TIME SERIES From random variables to random processes (cont d) 2 in cross-sectional regression, we were making inferences about the whole population based

Multivariate Time Series

Multivariate Time Series Fall 2008 Environmental Econometrics (GR03) TSII Fall 2008 1 / 16 More on AR(1) In AR(1) model (Y t = µ + ρy t 1 + u t ) with ρ = 1, the series is said to have a unit root or a

Multivariate Time Series Fall 2008 Environmental Econometrics (GR03) TSII Fall 2008 1 / 16 More on AR(1) In AR(1) model (Y t = µ + ρy t 1 + u t ) with ρ = 1, the series is said to have a unit root or a

ECONOMETRICS HONOR S EXAM REVIEW SESSION

ECONOMETRICS HONOR S EXAM REVIEW SESSION Eunice Han ehan@fas.harvard.edu March 26 th, 2013 Harvard University Information 2 Exam: April 3 rd 3-6pm @ Emerson 105 Bring a calculator and extra pens. Notes

ECONOMETRICS HONOR S EXAM REVIEW SESSION Eunice Han ehan@fas.harvard.edu March 26 th, 2013 Harvard University Information 2 Exam: April 3 rd 3-6pm @ Emerson 105 Bring a calculator and extra pens. Notes

Introduction to Regression Analysis. Dr. Devlina Chatterjee 11 th August, 2017

Introduction to Regression Analysis Dr. Devlina Chatterjee 11 th August, 2017 What is regression analysis? Regression analysis is a statistical technique for studying linear relationships. One dependent

Introduction to Regression Analysis Dr. Devlina Chatterjee 11 th August, 2017 What is regression analysis? Regression analysis is a statistical technique for studying linear relationships. One dependent

7. Integrated Processes

7. Integrated Processes Up to now: Analysis of stationary processes (stationary ARMA(p, q) processes) Problem: Many economic time series exhibit non-stationary patterns over time 226 Example: We consider

7. Integrated Processes Up to now: Analysis of stationary processes (stationary ARMA(p, q) processes) Problem: Many economic time series exhibit non-stationary patterns over time 226 Example: We consider

Answers: Problem Set 9. Dynamic Models

Answers: Problem Set 9. Dynamic Models 1. Given annual data for the period 1970-1999, you undertake an OLS regression of log Y on a time trend, defined as taking the value 1 in 1970, 2 in 1972 etc. The

Answers: Problem Set 9. Dynamic Models 1. Given annual data for the period 1970-1999, you undertake an OLS regression of log Y on a time trend, defined as taking the value 1 in 1970, 2 in 1972 etc. The

Exam ECON3150/4150: Introductory Econometrics. 18 May 2016; 09:00h-12.00h.

Exam ECON3150/4150: Introductory Econometrics. 18 May 2016; 09:00h-12.00h. This is an open book examination where all printed and written resources, in addition to a calculator, are allowed. If you are

Exam ECON3150/4150: Introductory Econometrics. 18 May 2016; 09:00h-12.00h. This is an open book examination where all printed and written resources, in addition to a calculator, are allowed. If you are

11.1 Gujarati(2003): Chapter 12

: Chapter 12") 11.1 Gujarati(2003): Chapter 12 Time Series Data 11.2 Time series process of economic variables e.g., GDP, M1, interest rate, echange rate, imports, eports, inflation rate, etc. Realization An observed

11.1 Gujarati(2003): Chapter 12 Time Series Data 11.2 Time series process of economic variables e.g., GDP, M1, interest rate, echange rate, imports, eports, inflation rate, etc. Realization An observed

Longitudinal Data Analysis Using Stata Paul D. Allison, Ph.D. Upcoming Seminar: May 18-19, 2017, Chicago, Illinois

Longitudinal Data Analysis Using Stata Paul D. Allison, Ph.D. Upcoming Seminar: May 18-19, 217, Chicago, Illinois Outline 1. Opportunities and challenges of panel data. a. Data requirements b. Control

Longitudinal Data Analysis Using Stata Paul D. Allison, Ph.D. Upcoming Seminar: May 18-19, 217, Chicago, Illinois Outline 1. Opportunities and challenges of panel data. a. Data requirements b. Control

Empirical Application of Panel Data Regression

Empirical Application of Panel Data Regression 1. We use Fatality data, and we are interested in whether rising beer tax rate can help lower traffic death. So the dependent variable is traffic death, while

Empirical Application of Panel Data Regression 1. We use Fatality data, and we are interested in whether rising beer tax rate can help lower traffic death. So the dependent variable is traffic death, while

2.1. Consider the following production function, known in the literature as the transcendental production function (TPF).

.") CHAPTER Functional Forms of Regression Models.1. Consider the following production function, known in the literature as the transcendental production function (TPF). Q i B 1 L B i K i B 3 e B L B K 4 i

CHAPTER Functional Forms of Regression Models.1. Consider the following production function, known in the literature as the transcendental production function (TPF). Q i B 1 L B i K i B 3 e B L B K 4 i

Introduction to Modern Time Series Analysis

Introduction to Modern Time Series Analysis Gebhard Kirchgässner, Jürgen Wolters and Uwe Hassler Second Edition Springer 3 Teaching Material The following figures and tables are from the above book. They

Introduction to Modern Time Series Analysis Gebhard Kirchgässner, Jürgen Wolters and Uwe Hassler Second Edition Springer 3 Teaching Material The following figures and tables are from the above book. They

Covers Chapter 10-12, some of 16, some of 18 in Wooldridge. Regression Analysis with Time Series Data

Covers Chapter 10-12, some of 16, some of 18 in Wooldridge Regression Analysis with Time Series Data Obviously time series data different from cross section in terms of source of variation in x and y temporal

Covers Chapter 10-12, some of 16, some of 18 in Wooldridge Regression Analysis with Time Series Data Obviously time series data different from cross section in terms of source of variation in x and y temporal

Econometrics of financial markets, -solutions to seminar 1. Problem 1

Econometrics of financial markets, -solutions to seminar 1. Problem 1 a) Estimate with OLS. For any regression y i α + βx i + u i for OLS to be unbiased we need cov (u i,x j )0 i, j. For the autoregressive

Econometrics of financial markets, -solutions to seminar 1. Problem 1 a) Estimate with OLS. For any regression y i α + βx i + u i for OLS to be unbiased we need cov (u i,x j )0 i, j. For the autoregressive

The multiple regression model; Indicator variables as regressors

The multiple regression model; Indicator variables as regressors Ragnar Nymoen University of Oslo 28 February 2013 1 / 21 This lecture (#12): Based on the econometric model specification from Lecture 9

The multiple regression model; Indicator variables as regressors Ragnar Nymoen University of Oslo 28 February 2013 1 / 21 This lecture (#12): Based on the econometric model specification from Lecture 9

Lecture#12. Instrumental variables regression Causal parameters III

Lecture#12 Instrumental variables regression Causal parameters III 1 Demand experiment, market data analysis & simultaneous causality 2 Simultaneous causality Your task is to estimate the demand function

Lecture#12 Instrumental variables regression Causal parameters III 1 Demand experiment, market data analysis & simultaneous causality 2 Simultaneous causality Your task is to estimate the demand function

Lecture 8a: Spurious Regression

Lecture 8a: Spurious Regression 1 2 Old Stuff The traditional statistical theory holds when we run regression using stationary variables. For example, when we regress one stationary series onto another

Lecture 8a: Spurious Regression 1 2 Old Stuff The traditional statistical theory holds when we run regression using stationary variables. For example, when we regress one stationary series onto another

Lecture 8a: Spurious Regression

Lecture 8a: Spurious Regression 1 Old Stuff The traditional statistical theory holds when we run regression using (weakly or covariance) stationary variables. For example, when we regress one stationary

Lecture 8a: Spurious Regression 1 Old Stuff The traditional statistical theory holds when we run regression using (weakly or covariance) stationary variables. For example, when we regress one stationary

Problem set 1 - Solutions

EMPIRICAL FINANCE AND FINANCIAL ECONOMETRICS - MODULE (8448) Problem set 1 - Solutions Exercise 1 -Solutions 1. The correct answer is (a). In fact, the process generating daily prices is usually assumed

EMPIRICAL FINANCE AND FINANCIAL ECONOMETRICS - MODULE (8448) Problem set 1 - Solutions Exercise 1 -Solutions 1. The correct answer is (a). In fact, the process generating daily prices is usually assumed

LECTURE 3 The Effects of Monetary Changes: Statistical Identification. September 5, 2018

Economics 210c/236a Fall 2018 Christina Romer David Romer LECTURE 3 The Effects of Monetary Changes: Statistical Identification September 5, 2018 I. SOME BACKGROUND ON VARS A Two-Variable VAR Suppose the

Economics 210c/236a Fall 2018 Christina Romer David Romer LECTURE 3 The Effects of Monetary Changes: Statistical Identification September 5, 2018 I. SOME BACKGROUND ON VARS A Two-Variable VAR Suppose the

Introduction to Econometrics. Review of Probability & Statistics

1 Introduction to Econometrics Review of Probability & Statistics Peerapat Wongchaiwat, Ph.D. wongchaiwat@hotmail.com Introduction 2 What is Econometrics? Econometrics consists of the application of mathematical

1 Introduction to Econometrics Review of Probability & Statistics Peerapat Wongchaiwat, Ph.D. wongchaiwat@hotmail.com Introduction 2 What is Econometrics? Econometrics consists of the application of mathematical

THE LONG-RUN DETERMINANTS OF MONEY DEMAND IN SLOVAKIA MARTIN LUKÁČIK - ADRIANA LUKÁČIKOVÁ - KAROL SZOMOLÁNYI

92 Multiple Criteria Decision Making XIII THE LONG-RUN DETERMINANTS OF MONEY DEMAND IN SLOVAKIA MARTIN LUKÁČIK - ADRIANA LUKÁČIKOVÁ - KAROL SZOMOLÁNYI Abstract: The paper verifies the long-run determinants

92 Multiple Criteria Decision Making XIII THE LONG-RUN DETERMINANTS OF MONEY DEMAND IN SLOVAKIA MARTIN LUKÁČIK - ADRIANA LUKÁČIKOVÁ - KAROL SZOMOLÁNYI Abstract: The paper verifies the long-run determinants

Applied Econometrics. Professor Bernard Fingleton

Applied Econometrics Professor Bernard Fingleton 1 Causation & Prediction 2 Causation One of the main difficulties in the social sciences is estimating whether a variable has a true causal effect Data

Applied Econometrics Professor Bernard Fingleton 1 Causation & Prediction 2 Causation One of the main difficulties in the social sciences is estimating whether a variable has a true causal effect Data

Economics 308: Econometrics Professor Moody

Economics 308: Econometrics Professor Moody References on reserve: Text Moody, Basic Econometrics with Stata (BES) Pindyck and Rubinfeld, Econometric Models and Economic Forecasts (PR) Wooldridge, Jeffrey

Economics 308: Econometrics Professor Moody References on reserve: Text Moody, Basic Econometrics with Stata (BES) Pindyck and Rubinfeld, Econometric Models and Economic Forecasts (PR) Wooldridge, Jeffrey

Hypothesis Tests and Confidence Intervals in Multiple Regression

Hypothesis Tests and Confidence Intervals in Multiple Regression (SW Chapter 7) Outline 1. Hypothesis tests and confidence intervals for one coefficient. Joint hypothesis tests on multiple coefficients

Hypothesis Tests and Confidence Intervals in Multiple Regression (SW Chapter 7) Outline 1. Hypothesis tests and confidence intervals for one coefficient. Joint hypothesis tests on multiple coefficients

1: a b c d e 2: a b c d e 3: a b c d e 4: a b c d e 5: a b c d e. 6: a b c d e 7: a b c d e 8: a b c d e 9: a b c d e 10: a b c d e

Economics 102: Analysis of Economic Data Cameron Spring 2015 Department of Economics, U.C.-Davis Final Exam (A) Saturday June 6 Compulsory. Closed book. Total of 56 points and worth 45% of course grade.

Economics 102: Analysis of Economic Data Cameron Spring 2015 Department of Economics, U.C.-Davis Final Exam (A) Saturday June 6 Compulsory. Closed book. Total of 56 points and worth 45% of course grade.

1 Regression with Time Series Variables

1 Regression with Time Series Variables With time series regression, Y might not only depend on X, but also lags of Y and lags of X Autoregressive Distributed lag (or ADL(p; q)) model has these features:

1 Regression with Time Series Variables With time series regression, Y might not only depend on X, but also lags of Y and lags of X Autoregressive Distributed lag (or ADL(p; q)) model has these features:

ECON2228 Notes 10. Christopher F Baum. Boston College Economics. cfb (BC Econ) ECON2228 Notes / 54

ECON2228 Notes / 54") ECON2228 Notes 10 Christopher F Baum Boston College Economics 2014 2015 cfb (BC Econ) ECON2228 Notes 10 2014 2015 1 / 54 erial correlation and heteroskedasticity in time series regressions Chapter 12:

ECON2228 Notes 10 Christopher F Baum Boston College Economics 2014 2015 cfb (BC Econ) ECON2228 Notes 10 2014 2015 1 / 54 erial correlation and heteroskedasticity in time series regressions Chapter 12:

Introductory Econometrics. Lecture 13: Hypothesis testing in the multiple regression model, Part 1

Introductory Econometrics Lecture 13: Hypothesis testing in the multiple regression model, Part 1 Jun Ma School of Economics Renmin University of China October 19, 2016 The model I We consider the classical

Introductory Econometrics Lecture 13: Hypothesis testing in the multiple regression model, Part 1 Jun Ma School of Economics Renmin University of China October 19, 2016 The model I We consider the classical

Outline. Nature of the Problem. Nature of the Problem. Basic Econometrics in Transportation. Autocorrelation

1/30 Outline Basic Econometrics in Transportation Autocorrelation Amir Samimi What is the nature of autocorrelation? What are the theoretical and practical consequences of autocorrelation? Since the assumption

1/30 Outline Basic Econometrics in Transportation Autocorrelation Amir Samimi What is the nature of autocorrelation? What are the theoretical and practical consequences of autocorrelation? Since the assumption

Lecture 5. In the last lecture, we covered. This lecture introduces you to

Lecture 5 In the last lecture, we covered. homework 2. The linear regression model (4.) 3. Estimating the coefficients (4.2) This lecture introduces you to. Measures of Fit (4.3) 2. The Least Square Assumptions

Lecture 5 In the last lecture, we covered. homework 2. The linear regression model (4.) 3. Estimating the coefficients (4.2) This lecture introduces you to. Measures of Fit (4.3) 2. The Least Square Assumptions

A Guide to Modern Econometric:

A Guide to Modern Econometric: 4th edition Marno Verbeek Rotterdam School of Management, Erasmus University, Rotterdam B 379887 )WILEY A John Wiley & Sons, Ltd., Publication Contents Preface xiii 1 Introduction

A Guide to Modern Econometric: 4th edition Marno Verbeek Rotterdam School of Management, Erasmus University, Rotterdam B 379887 )WILEY A John Wiley & Sons, Ltd., Publication Contents Preface xiii 1 Introduction

Econometrics Honor s Exam Review Session. Spring 2012 Eunice Han

Econometrics Honor s Exam Review Session Spring 2012 Eunice Han Topics 1. OLS The Assumptions Omitted Variable Bias Conditional Mean Independence Hypothesis Testing and Confidence Intervals Homoskedasticity

Econometrics Honor s Exam Review Session Spring 2012 Eunice Han Topics 1. OLS The Assumptions Omitted Variable Bias Conditional Mean Independence Hypothesis Testing and Confidence Intervals Homoskedasticity

Econ 424 Time Series Concepts

Econ 424 Time Series Concepts Eric Zivot January 20 2015 Time Series Processes Stochastic (Random) Process { 1 2 +1 } = { } = sequence of random variables indexed by time Observed time series of length

Econ 424 Time Series Concepts Eric Zivot January 20 2015 Time Series Processes Stochastic (Random) Process { 1 2 +1 } = { } = sequence of random variables indexed by time Observed time series of length

Introductory Workshop on Time Series Analysis. Sara McLaughlin Mitchell Department of Political Science University of Iowa

Introductory Workshop on Time Series Analysis Sara McLaughlin Mitchell Department of Political Science University of Iowa Overview Properties of time series data Approaches to time series analysis Stationarity

Introductory Workshop on Time Series Analysis Sara McLaughlin Mitchell Department of Political Science University of Iowa Overview Properties of time series data Approaches to time series analysis Stationarity

Lecture 14. More on using dummy variables (deal with seasonality)

") Lecture 14. More on using dummy variables (deal with seasonality) More things to worry about: measurement error in variables (can lead to bias in OLS (endogeneity) ) Have seen that dummy variables are

Lecture 14. More on using dummy variables (deal with seasonality) More things to worry about: measurement error in variables (can lead to bias in OLS (endogeneity) ) Have seen that dummy variables are

STATISTICS 110/201 PRACTICE FINAL EXAM

STATISTICS 110/201 PRACTICE FINAL EXAM Questions 1 to 5: There is a downloadable Stata package that produces sequential sums of squares for regression. In other words, the SS is built up as each variable

STATISTICS 110/201 PRACTICE FINAL EXAM Questions 1 to 5: There is a downloadable Stata package that produces sequential sums of squares for regression. In other words, the SS is built up as each variable

ECON3150/4150 Spring 2016

ECON3150/4150 Spring 2016 Lecture 6 Multiple regression model Siv-Elisabeth Skjelbred University of Oslo February 5th Last updated: February 3, 2016 1 / 49 Outline Multiple linear regression model and

ECON3150/4150 Spring 2016 Lecture 6 Multiple regression model Siv-Elisabeth Skjelbred University of Oslo February 5th Last updated: February 3, 2016 1 / 49 Outline Multiple linear regression model and

ECON Introductory Econometrics. Lecture 7: OLS with Multiple Regressors Hypotheses tests

ECON4150 - Introductory Econometrics Lecture 7: OLS with Multiple Regressors Hypotheses tests Monique de Haan (moniqued@econ.uio.no) Stock and Watson Chapter 7 Lecture outline 2 Hypothesis test for single

ECON4150 - Introductory Econometrics Lecture 7: OLS with Multiple Regressors Hypotheses tests Monique de Haan (moniqued@econ.uio.no) Stock and Watson Chapter 7 Lecture outline 2 Hypothesis test for single

Econometrics Homework 1

Econometrics Homework Due Date: March, 24. by This problem set includes questions for Lecture -4 covered before midterm exam. Question Let z be a random column vector of size 3 : z = @ (a) Write out z

Econometrics Homework Due Date: March, 24. by This problem set includes questions for Lecture -4 covered before midterm exam. Question Let z be a random column vector of size 3 : z = @ (a) Write out z

Auto correlation 2. Note: In general we can have AR(p) errors which implies p lagged terms in the error structure, i.e.,

errors which implies p lagged terms in the error structure, i.e.,") 1 Motivation Auto correlation 2 Autocorrelation occurs when what happens today has an impact on what happens tomorrow, and perhaps further into the future This is a phenomena mainly found in time-series

1 Motivation Auto correlation 2 Autocorrelation occurs when what happens today has an impact on what happens tomorrow, and perhaps further into the future This is a phenomena mainly found in time-series

LATVIAN GDP: TIME SERIES FORECASTING USING VECTOR AUTO REGRESSION

LATVIAN GDP: TIME SERIES FORECASTING USING VECTOR AUTO REGRESSION BEZRUCKO Aleksandrs, (LV) Abstract: The target goal of this work is to develop a methodology of forecasting Latvian GDP using ARMA (AutoRegressive-Moving-Average)

LATVIAN GDP: TIME SERIES FORECASTING USING VECTOR AUTO REGRESSION BEZRUCKO Aleksandrs, (LV) Abstract: The target goal of this work is to develop a methodology of forecasting Latvian GDP using ARMA (AutoRegressive-Moving-Average)

Please discuss each of the 3 problems on a separate sheet of paper, not just on a separate page!

Econometrics - Exam May 11, 2011 1 Exam Please discuss each of the 3 problems on a separate sheet of paper, not just on a separate page! Problem 1: (15 points) A researcher has data for the year 2000 from

Econometrics - Exam May 11, 2011 1 Exam Please discuss each of the 3 problems on a separate sheet of paper, not just on a separate page! Problem 1: (15 points) A researcher has data for the year 2000 from

Problem Set 5 ANSWERS

Economics 20 Problem Set 5 ANSWERS Prof. Patricia M. Anderson 1, 2 and 3 Suppose that Vermont has passed a law requiring employers to provide 6 months of paid maternity leave. You are concerned that women

Economics 20 Problem Set 5 ANSWERS Prof. Patricia M. Anderson 1, 2 and 3 Suppose that Vermont has passed a law requiring employers to provide 6 months of paid maternity leave. You are concerned that women

ECON2228 Notes 10. Christopher F Baum. Boston College Economics. cfb (BC Econ) ECON2228 Notes / 48

ECON2228 Notes / 48") ECON2228 Notes 10 Christopher F Baum Boston College Economics 2014 2015 cfb (BC Econ) ECON2228 Notes 10 2014 2015 1 / 48 Serial correlation and heteroskedasticity in time series regressions Chapter 12:

ECON2228 Notes 10 Christopher F Baum Boston College Economics 2014 2015 cfb (BC Econ) ECON2228 Notes 10 2014 2015 1 / 48 Serial correlation and heteroskedasticity in time series regressions Chapter 12:

UPPSALA UNIVERSITY - DEPARTMENT OF STATISTICS MIDAS. Forecasting quarterly GDP using higherfrequency

UPPSALA UNIVERSITY - DEPARTMENT OF STATISTICS MIDAS Forecasting quarterly GDP using higherfrequency data Authors: Hanna Lindgren and Victor Nilsson Supervisor: Lars Forsberg January 12, 2015 We forecast

UPPSALA UNIVERSITY - DEPARTMENT OF STATISTICS MIDAS Forecasting quarterly GDP using higherfrequency data Authors: Hanna Lindgren and Victor Nilsson Supervisor: Lars Forsberg January 12, 2015 We forecast

Postestimation commands predict estat Remarks and examples Stored results Methods and formulas

Title stata.com mswitch postestimation Postestimation tools for mswitch Postestimation commands predict estat Remarks and examples Stored results Methods and formulas References Also see Postestimation

Title stata.com mswitch postestimation Postestimation tools for mswitch Postestimation commands predict estat Remarks and examples Stored results Methods and formulas References Also see Postestimation

Chapter 11. Regression with a Binary Dependent Variable

Chapter 11 Regression with a Binary Dependent Variable 2 Regression with a Binary Dependent Variable (SW Chapter 11) So far the dependent variable (Y) has been continuous: district-wide average test score

Chapter 11 Regression with a Binary Dependent Variable 2 Regression with a Binary Dependent Variable (SW Chapter 11) So far the dependent variable (Y) has been continuous: district-wide average test score

ECON3150/4150 Spring 2015

ECON3150/4150 Spring 2015 Lecture 3&4 - The linear regression model Siv-Elisabeth Skjelbred University of Oslo January 29, 2015 1 / 67 Chapter 4 in S&W Section 17.1 in S&W (extended OLS assumptions) 2

ECON3150/4150 Spring 2015 Lecture 3&4 - The linear regression model Siv-Elisabeth Skjelbred University of Oslo January 29, 2015 1 / 67 Chapter 4 in S&W Section 17.1 in S&W (extended OLS assumptions) 2

Introduction to Econometrics. Regression with Panel Data

Introduction to Econometrics The statistical analysis of economic (and related) data STATS301 Regression with Panel Data Titulaire: Christopher Bruffaerts Assistant: Lorenzo Ricci 1 Regression with Panel

Introduction to Econometrics The statistical analysis of economic (and related) data STATS301 Regression with Panel Data Titulaire: Christopher Bruffaerts Assistant: Lorenzo Ricci 1 Regression with Panel

Applied Statistics and Econometrics

Applied Statistics and Econometrics Lecture 6 Saul Lach September 2017 Saul Lach () Applied Statistics and Econometrics September 2017 1 / 53 Outline of Lecture 6 1 Omitted variable bias (SW 6.1) 2 Multiple

Applied Statistics and Econometrics Lecture 6 Saul Lach September 2017 Saul Lach () Applied Statistics and Econometrics September 2017 1 / 53 Outline of Lecture 6 1 Omitted variable bias (SW 6.1) 2 Multiple

Austrian Inflation Rate

Austrian Inflation Rate Course of Econometric Forecasting Nadir Shahzad Virkun Tomas Sedliacik Goal and Data Selection Our goal is to find a relatively accurate procedure in order to forecast the Austrian

Austrian Inflation Rate Course of Econometric Forecasting Nadir Shahzad Virkun Tomas Sedliacik Goal and Data Selection Our goal is to find a relatively accurate procedure in order to forecast the Austrian

FinQuiz Notes

Reading 9 A time series is any series of data that varies over time e.g. the quarterly sales for a company during the past five years or daily returns of a security. When assumptions of the regression

Reading 9 A time series is any series of data that varies over time e.g. the quarterly sales for a company during the past five years or daily returns of a security. When assumptions of the regression

Oil price and macroeconomy in Russia. Abstract

Oil price and macroeconomy in Russia Katsuya Ito Fukuoka University Abstract In this note, using the VEC model we attempt to empirically investigate the effects of oil price and monetary shocks on the

Oil price and macroeconomy in Russia Katsuya Ito Fukuoka University Abstract In this note, using the VEC model we attempt to empirically investigate the effects of oil price and monetary shocks on the

8. Nonstandard standard error issues 8.1. The bias of robust standard errors

8.1. The bias of robust standard errors Bias Robust standard errors are now easily obtained using e.g. Stata option robust Robust standard errors are preferable to normal standard errors when residuals

8.1. The bias of robust standard errors Bias Robust standard errors are now easily obtained using e.g. Stata option robust Robust standard errors are preferable to normal standard errors when residuals

Regression with a Single Regressor: Hypothesis Tests and Confidence Intervals

Regression with a Single Regressor: Hypothesis Tests and Confidence Intervals (SW Chapter 5) Outline. The standard error of ˆ. Hypothesis tests concerning β 3. Confidence intervals for β 4. Regression

Regression with a Single Regressor: Hypothesis Tests and Confidence Intervals (SW Chapter 5) Outline. The standard error of ˆ. Hypothesis tests concerning β 3. Confidence intervals for β 4. Regression

Stationary and nonstationary variables

Stationary and nonstationary variables Stationary variable: 1. Finite and constant in time expected value: E (y t ) = µ < 2. Finite and constant in time variance: Var (y t ) = σ 2 < 3. Covariance dependent

Stationary and nonstationary variables Stationary variable: 1. Finite and constant in time expected value: E (y t ) = µ < 2. Finite and constant in time variance: Var (y t ) = σ 2 < 3. Covariance dependent