Question 1 [17 points]: (ch 11)

|

|

|

- Rolf Cook

- 5 years ago

- Views:

Transcription

1 Question 1 [17 points]: (ch 11) A study analyzed the probability that Major League Baseball (MLB) players "survive" for another season, or, in other words, play one more season. They studied a model of the following form: The dependent variable is a binary variable that takes on a value of one if the player played one more season (a minimum of 50 at bats or 25 innings pitched), and zero otherwise. Seasons is the number of total seasons played, measured in years, Perf is the performance of the player this year, and Avgperf is the average performance of the player over their career. The researchers had a sample of 4,728 hitters and 3,803 pitchers for the years All explanatory variables are standardized (sample mean of 0, variance of 1). Probit estimation yielded the results as shown in the table: Regression (1) Hitters (2) Pitchers Regression model probit probit constant (0.030) (0.031) number of seasons played (0.004) (0.005) performance (0.025) (0.026) average performance (0.033) (0.036) (a) (6p) Interpret the two probit equations and calculate survival probabilities for hitters and pitchers at the sample mean. Provide an explanation for why these are so high. (b) (6p) Calculate the change in the survival probability for a player who has a very bad year by performing two standard deviations below the average (assume also that this player has been in the majors for many years so that his average performance is negligibly affected). How does this change the survival probability when compared to the answer in (a)? (c) (5p) Since the results for hitters and pitchers seem similar, the researcher could consider combining the two samples. With a combined sample, how could you test the hypothesis that the coefficients for the explanatory variables are the same for hitters and pitchers? Explain in some detail.. Answer: (a) Note that all variables are standardized, so that the mean is zero. This results in a survival probability of for hitters and for pitchers. These results are so 2

2 high because there is a high probability, in general, for a player to return the following season. (b) Since the variables are standardized, this implies a change of two for the performance variable. The result for hitters is a lowering of the survival probability to 0.65, and for pitchers to (c) After combining the sample for hitters and pitchers, you would allow for a different intercept and slopes by introducing a binary variable for pitchers if hitters are the default. This binary variable would be introduced by itself and in combination with each of the above variables, thereby allowing all coefficients to differ. You could then conduct an F-test for the joint hypothesis that all coefficients involving the binary variables are zero. If the hypothesis cannot be rejected, then there is no difference between the coefficients for hitters and pitchers. 3

3 Question 2 [21 points]: (ch 10) Consider the following panel data regression with a single explanatory variable Yit = β0 + β1xit +. In each of the examples below, you will be including entity and time fixed effects. (a) (3 p) Consider the effect of beer taxes on the fatality rate using annual data from , and nine U.S. regions (New England, Pacific, Mid-Atlantic, South, etc.). How many total coefficients do you need to estimate? (b) (4 p) Certain regions (e.g. New England) that tend to have higher beer taxes also tend to have consistently higher quality hospitals. Does this pose a threat to your analysis? (c) (3 p) Consider the effect of the minimum wage on teenage employment using annual data from for five Canadian Regions (Atlantic Provinces, Quebec, Ontario, Prairies, British Columbia). How many total coefficients do you need to estimate? (d) (4 p) Nationwide recessions impact both teenage employment and the minimum wage across the country. Does this pose a threat to your analysis? (e) (3 p) Consider the effect of savings rates on per capita income using data for three decades ( , , ; one observation per decade) and 104 countries. How many total coefficients do you need to estimate? (f) (4 p) A number of countries industrialized at different times between , a process which can impact both the savings rate and per capita income. Does this pose a threat to your analysis? Answer: (a) 16 coefficients (6 time fixed effects, 8 entity fixed effects, intercept, slope). (b) No, entity fixed effects will account for entity constant omitted variables. (c) 43 coefficients (37 time fixed effects, 5 entity fixed effects, intercept, slope). (d) No, time fixed effects will account for this. (e) 107 coefficients (3 time fixed effects, 103 entity fixed effects, intercept, slope). (f) Yes, industrialization is a time and entity varying omitted variable. 4

4 Question 3 [15 points]: (IV regression) (Ch 12) Consider a supply model for edible chicken, which the the U.S. Department of Agriculture calls broilers Data for this question is adapted from the data provided by Epple and McCallum (2006) 1. The data are annual, The Supply equation is: ( ) ( ) ( ) ( ) where is aggregate production of young chickens, is the real price index of fresh chicken, is real price index of broiler feed, and which is included to capture any technical progress in the production. Some potential external instrumental variables are ( ), where is the real per capita income; ( ), where is the real price of beef; is the percent population growth from year t-1 to year t; ( ) is the lagged log of real price of chickens; ( ) is the log of exports of chicken. Estimated supply equation for chicken can be written from the following output: Regression 1:. reg lnqprod lnp lnpf TIME lnqprod_1 Source SS df MS Number of obs = F( 4, 35) = Model Prob > F = Residual R-squared = Adj R-squared = Total Root MSE = lnqprod Coef. Std. Err. t P> t [95% Conf. Interval] lnp lnpf TIME lnqprod_ _cons Regression 2:. ivreg lnqprod (lnp=lnpb lny POPGRO lnexpts) lnpf TIME lnqprod_1 Instrumental variables (2SLS) regression Source SS df MS Number of obs = F( 4, 35) = Model Prob > F = Residual R-squared = Adj R-squared = Total Root MSE = Simultaneous Equation Econometrics: The Missing Example, Economic Inquiry, 44(2),

5 lnqprod Coef. Std. Err. t P> t [95% Conf. Interval] lnp lnpf TIME lnqprod_ _cons Instrumented: lnp Instruments: lnpf TIME lnqprod_1 lnpb lny POPGRO lnexpts Regression 3:. reg lnp lnpb lny POPGRO lnexpts lnpf TIME lnqprod_1 Source SS df MS Number of obs = F( 7, 32) = Model Prob > F = Residual R-squared = Adj R-squared = Total Root MSE = lnp Coef. Std. Err. t P> t [95% Conf. Interval] lnpb lny POPGRO lnexpts lnpf TIME lnqprod_ _cons c Regression 4:. reg lnqprod lnp lnpf TIME lnqprod_1 Source SS df MS Number of obs = F( 4, 35) = Model Prob > F = Residual R-squared = Adj R-squared = Total Root MSE = lnqprod Coef. Std. Err. t P> t [95% Conf. Interval] lnp lnpf TIME lnqprod_ _cons

6 . predict e, residuals (1 missing values generated) Regression 5:. reg e lnpb lny POPGRO lnexpts lnpf TIME lnqprod_1 Source SS df MS Number of obs = F( 7, 32) = 2.19 Model Prob > F = Residual R-squared = Adj R-squared = Total Root MSE = e Coef. Std. Err. t P> t [95% Conf. Interval] lnpb lny POPGRO lnexpts lnpf TIME lnqprod_ _cons test lnpb lny POPGRO lnexpts ( 1) lnpb = 0 ( 2) lny = 0 ( 3) POPGRO = 0 ( 4) lnexpts = 0 F( 4, 32) = 3.83 Prob > F = (a) (4p) Compare the results in regression 1 and 2. Explain the reasons for instrumental variables in regression 2? Answer: (b) (5p) What are the requirements for valid instruments? Explain with mathematical conditions. Answer: 7

7 Relevance: ( ) Exogeneity: ( ) (c) (6p) Do these instruments satisfy the requirements? You must use the necessary regression results for your answer. Please specify the regression number you use while answering each part of this questions. (1) Relevancy: Using regression 3, square of t test is greater than 10 only for lnexprt, that is the only relevant IV. (2) Exogeneity: ( ) Hence, reject Therefore IV are not exogeneous. 8

8 Question 4 [15 points]: (Ch 15) There is some economic research that suggests that oil prices play a central role in causing recessions in developed countries. In particular, this research suggests that it is specifically increases in oil prices that matter. As a result, economists often look only at the percentage point difference between oil prices at date t and the maximum value over the previous year. However, you notice that energy prices can fluctuate quite dramatically in both directions and believe that geographic areas also benefit substantially from oil price decreases. As a result, you decide to consider the effect of real oil prices (Poil/CPI) on GDP growth (Yt) You estimate the following distributed lag model using annual data (numbers in parenthesis are HAC standard errors): t = (Poil/CPI)t (Poil/CPI)t-1 (0.27) (0.010) (0.011) t = , R2 = 0.15, SER = 1.88 (a) (5p) What is the impact effect of a 25 percentage point increase in real oil prices? (b) (5p) What is the predicted cumulative change in GDP Growth over two years of this effect? (c) (5p) The HAC F-statistic is Can you reject the null hypothesis that oil price changes have no effect on real GDP growth? What is the critical value you considered? Is there any reason why you should be cautious using an F-test in this case, given the sample period? Answer: a. GDP growth would decrease by almost a quarter of a percentage point. b. The predicted decline in growth would be almost one percentage point (-0.925). c. The critical value of F2, = 3.00 at the 5% significance level. Hence you can reject the null hypothesis that oil prices have no effect on real GDP growth. However, since the sample period involves only 50 or so observations, it is not clear that the test statistic is actually F-distributes (small sample). 9

9 Question 5 [20 points]: (Ch 14) Given the following STATA output, you can find a VAR(2) (VectorAutoregression) model of change in inflation ( ) and unemployment rate ( ). var unem cinf Vector autoregression Sample: No. of obs = 62 Log likelihood = AIC = FPE = HQIC = Det(Sigma_ml) = SBIC = Equation Parms RMSE R-sq chi2 P>chi unem cinf Coef. Std. Err. z P> z [95% Conf. Interval] unem unem L L cinf L L _cons cinf unem L L cinf L L _cons Table 1 Year Unem Inflation (a) (4p) Given the actual realizations of unemployment and inflation in table 1, forecast unemployment for 2013, show your work 10

10 (b) (4p) Given the actual realizations of unemployment and inflation in table 1, forecast inflation for 2013, show your work (c) (4p) Following is the joint test result for the second lags of unemployment rate and the inflation rate, according to the following test, would a VAR(1) model be better forecasting model than a VAR(2) model, explain why?. test L2.cinf L2.unem ( 1) [unem]l2.cinf = 0 ( 2) [cinf]l2.cinf = 0 ( 3) [unem]l2.unem = 0 ( 4) [cinf]l2.unem = 0 chi2( 4) = Prob > chi2 = (d) (4p) Why might a researcher use change in inflation as opposed to inflation in this model? Explain. (e) (4p) Should one use change in unemployment instead of unemployment? Explain. 11

11 Question 6 [12 points]: (Derivation question) Consider the panel data model: where are i.i.d. and independent of Xs with mean zero and variance, (a) (3 p) Define and, the entity demeaned values of X and Y. (b) (3 p) Rewrite the model in terms of these demeaned variables. (c) (3 p) Derive algebraically the fixed-effects estimator of. The fixed effects estimator minimizes the sum of squared residuals of the model you wrote in part b. (d) (3 p) Show that, if is a random variable that is independent of X and u, the estimator is unbiased for. Explain your answer. Answer: (a) (b) (c) 12

12 Subtracting the last equation from the first we would get; ( ) or we can also write it as; (d) The fixed-effects estimator of is the OLS estimator of the above regression. ( ) ( ) Hence, Using We can write ( ) Since is independent of X s and U s, using Law of Iterated Expectations we can show that [ ] 13

13 Bonus Question [2 points]: The two conditions for instrument validity are corr(zi, Xi) 0 and corr(zi, ui) = 0. The reason for the inconsistency of OLS is that corr(xi, ui) 0. If X and Z are correlated, and X and u are also correlated, how is it possible that Z and u are not correlated? Explain. Answer: The major idea is that corr(xi, ui) has two parts: one for which the correlation is zero and a second for which it is non-zero. The trick is to isolate the uncorrelated part of X. For the instrument to be valid, corr(zi, ui) = 0 and corr(zi, Xi) 0 must hold. TSLS then generates predicted values of X in the first stage by using a linear combination of the instruments. As long as corr(zi, Xi) 0 and corr(zi, ui) = 0, then the part of X which is uncorrelated with the error term is extracted through the prediction. In the second stage, this captured exogenous variation in X is then used to estimate the effect of X on Y, which is exogenous. 14

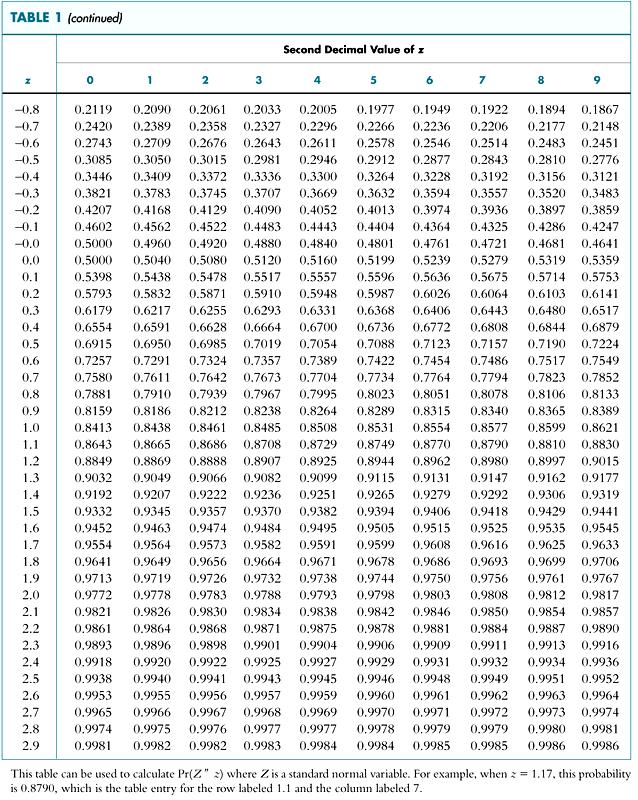

14 Selected Tables from Stock and Watson, Introduction to Econometrics 15

15 16

16 17

17 18

Lecture#17. Time series III

Lecture#17 Time series III 1 Dynamic causal effects Think of macroeconomic data. Difficult to think of an RCT. Substitute: different treatments to the same (observation unit) at different points in time.

Lecture#17 Time series III 1 Dynamic causal effects Think of macroeconomic data. Difficult to think of an RCT. Substitute: different treatments to the same (observation unit) at different points in time.

Handout 12. Endogeneity & Simultaneous Equation Models

Handout 12. Endogeneity & Simultaneous Equation Models In which you learn about another potential source of endogeneity caused by the simultaneous determination of economic variables, and learn how to

Handout 12. Endogeneity & Simultaneous Equation Models In which you learn about another potential source of endogeneity caused by the simultaneous determination of economic variables, and learn how to

Please discuss each of the 3 problems on a separate sheet of paper, not just on a separate page!

Econometrics - Exam May 11, 2011 1 Exam Please discuss each of the 3 problems on a separate sheet of paper, not just on a separate page! Problem 1: (15 points) A researcher has data for the year 2000 from

Econometrics - Exam May 11, 2011 1 Exam Please discuss each of the 3 problems on a separate sheet of paper, not just on a separate page! Problem 1: (15 points) A researcher has data for the year 2000 from

Lab 07 Introduction to Econometrics

Lab 07 Introduction to Econometrics Learning outcomes for this lab: Introduce the different typologies of data and the econometric models that can be used Understand the rationale behind econometrics Understand

Lab 07 Introduction to Econometrics Learning outcomes for this lab: Introduce the different typologies of data and the econometric models that can be used Understand the rationale behind econometrics Understand

(a) Briefly discuss the advantage of using panel data in this situation rather than pure crosssections

Briefly discuss the advantage of using panel data in this situation rather than pure crosssections") Answer Key Fixed Effect and First Difference Models 1. See discussion in class.. David Neumark and William Wascher published a study in 199 of the effect of minimum wages on teenage employment using a

Answer Key Fixed Effect and First Difference Models 1. See discussion in class.. David Neumark and William Wascher published a study in 199 of the effect of minimum wages on teenage employment using a

Introduction to Econometrics

Introduction to Econometrics STAT-S-301 Introduction to Time Series Regression and Forecasting (2016/2017) Lecturer: Yves Dominicy Teaching Assistant: Elise Petit 1 Introduction to Time Series Regression

Introduction to Econometrics STAT-S-301 Introduction to Time Series Regression and Forecasting (2016/2017) Lecturer: Yves Dominicy Teaching Assistant: Elise Petit 1 Introduction to Time Series Regression

Answer all questions from part I. Answer two question from part II.a, and one question from part II.b.

B203: Quantitative Methods Answer all questions from part I. Answer two question from part II.a, and one question from part II.b. Part I: Compulsory Questions. Answer all questions. Each question carries

B203: Quantitative Methods Answer all questions from part I. Answer two question from part II.a, and one question from part II.b. Part I: Compulsory Questions. Answer all questions. Each question carries

Econometrics. 8) Instrumental variables

Instrumental variables") 30C00200 Econometrics 8) Instrumental variables Timo Kuosmanen Professor, Ph.D. http://nomepre.net/index.php/timokuosmanen Today s topics Thery of IV regression Overidentification Two-stage least squates

30C00200 Econometrics 8) Instrumental variables Timo Kuosmanen Professor, Ph.D. http://nomepre.net/index.php/timokuosmanen Today s topics Thery of IV regression Overidentification Two-stage least squates

Testing methodology. It often the case that we try to determine the form of the model on the basis of data

Testing methodology It often the case that we try to determine the form of the model on the basis of data The simplest case: we try to determine the set of explanatory variables in the model Testing for

Testing methodology It often the case that we try to determine the form of the model on the basis of data The simplest case: we try to determine the set of explanatory variables in the model Testing for

Introduction to Econometrics

Introduction to Econometrics T H I R D E D I T I O N Global Edition James H. Stock Harvard University Mark W. Watson Princeton University Boston Columbus Indianapolis New York San Francisco Upper Saddle

Introduction to Econometrics T H I R D E D I T I O N Global Edition James H. Stock Harvard University Mark W. Watson Princeton University Boston Columbus Indianapolis New York San Francisco Upper Saddle

ECONOMETRICS HONOR S EXAM REVIEW SESSION

ECONOMETRICS HONOR S EXAM REVIEW SESSION Eunice Han ehan@fas.harvard.edu March 26 th, 2013 Harvard University Information 2 Exam: April 3 rd 3-6pm @ Emerson 105 Bring a calculator and extra pens. Notes

ECONOMETRICS HONOR S EXAM REVIEW SESSION Eunice Han ehan@fas.harvard.edu March 26 th, 2013 Harvard University Information 2 Exam: April 3 rd 3-6pm @ Emerson 105 Bring a calculator and extra pens. Notes

Practice exam questions

Practice exam questions Nathaniel Higgins nhiggins@jhu.edu, nhiggins@ers.usda.gov 1. The following question is based on the model y = β 0 + β 1 x 1 + β 2 x 2 + β 3 x 3 + u. Discuss the following two hypotheses.

Practice exam questions Nathaniel Higgins nhiggins@jhu.edu, nhiggins@ers.usda.gov 1. The following question is based on the model y = β 0 + β 1 x 1 + β 2 x 2 + β 3 x 3 + u. Discuss the following two hypotheses.

Measurement Error. Often a data set will contain imperfect measures of the data we would ideally like.

Measurement Error Often a data set will contain imperfect measures of the data we would ideally like. Aggregate Data: (GDP, Consumption, Investment are only best guesses of theoretical counterparts and

Measurement Error Often a data set will contain imperfect measures of the data we would ideally like. Aggregate Data: (GDP, Consumption, Investment are only best guesses of theoretical counterparts and

ECON Introductory Econometrics. Lecture 7: OLS with Multiple Regressors Hypotheses tests

ECON4150 - Introductory Econometrics Lecture 7: OLS with Multiple Regressors Hypotheses tests Monique de Haan (moniqued@econ.uio.no) Stock and Watson Chapter 7 Lecture outline 2 Hypothesis test for single

ECON4150 - Introductory Econometrics Lecture 7: OLS with Multiple Regressors Hypotheses tests Monique de Haan (moniqued@econ.uio.no) Stock and Watson Chapter 7 Lecture outline 2 Hypothesis test for single

Nonlinear Regression Functions

Nonlinear Regression Functions (SW Chapter 8) Outline 1. Nonlinear regression functions general comments 2. Nonlinear functions of one variable 3. Nonlinear functions of two variables: interactions 4.

Nonlinear Regression Functions (SW Chapter 8) Outline 1. Nonlinear regression functions general comments 2. Nonlinear functions of one variable 3. Nonlinear functions of two variables: interactions 4.

Final Exam. Question 1 (20 points) 2 (25 points) 3 (30 points) 4 (25 points) 5 (10 points) 6 (40 points) Total (150 points) Bonus question (10)

2 (25 points) 3 (30 points) 4 (25 points) 5 (10 points) 6 (40 points) Total (150 points) Bonus question (10)") Name Economics 170 Spring 2004 Honor pledge: I have neither given nor received aid on this exam including the preparation of my one page formula list and the preparation of the Stata assignment for the

Name Economics 170 Spring 2004 Honor pledge: I have neither given nor received aid on this exam including the preparation of my one page formula list and the preparation of the Stata assignment for the

Problem Set #5-Key Sonoma State University Dr. Cuellar Economics 317- Introduction to Econometrics

Problem Set #5-Key Sonoma State University Dr. Cuellar Economics 317- Introduction to Econometrics C1.1 Use the data set Wage1.dta to answer the following questions. Estimate regression equation wage =

Problem Set #5-Key Sonoma State University Dr. Cuellar Economics 317- Introduction to Econometrics C1.1 Use the data set Wage1.dta to answer the following questions. Estimate regression equation wage =

9) Time series econometrics

Time series econometrics") 30C00200 Econometrics 9) Time series econometrics Timo Kuosmanen Professor Management Science http://nomepre.net/index.php/timokuosmanen 1 Macroeconomic data: GDP Inflation rate Examples of time series

30C00200 Econometrics 9) Time series econometrics Timo Kuosmanen Professor Management Science http://nomepre.net/index.php/timokuosmanen 1 Macroeconomic data: GDP Inflation rate Examples of time series

Econometrics. 9) Heteroscedasticity and autocorrelation

Heteroscedasticity and autocorrelation") 30C00200 Econometrics 9) Heteroscedasticity and autocorrelation Timo Kuosmanen Professor, Ph.D. http://nomepre.net/index.php/timokuosmanen Today s topics Heteroscedasticity Possible causes Testing for

30C00200 Econometrics 9) Heteroscedasticity and autocorrelation Timo Kuosmanen Professor, Ph.D. http://nomepre.net/index.php/timokuosmanen Today s topics Heteroscedasticity Possible causes Testing for

Econometrics Midterm Examination Answers

Econometrics Midterm Examination Answers March 4, 204. Question (35 points) Answer the following short questions. (i) De ne what is an unbiased estimator. Show that X is an unbiased estimator for E(X i

Econometrics Midterm Examination Answers March 4, 204. Question (35 points) Answer the following short questions. (i) De ne what is an unbiased estimator. Show that X is an unbiased estimator for E(X i

10) Time series econometrics

Time series econometrics") 30C00200 Econometrics 10) Time series econometrics Timo Kuosmanen Professor, Ph.D. 1 Topics today Static vs. dynamic time series model Suprious regression Stationary and nonstationary time series Unit

30C00200 Econometrics 10) Time series econometrics Timo Kuosmanen Professor, Ph.D. 1 Topics today Static vs. dynamic time series model Suprious regression Stationary and nonstationary time series Unit

Warwick Economics Summer School Topics in Microeconometrics Instrumental Variables Estimation

Warwick Economics Summer School Topics in Microeconometrics Instrumental Variables Estimation Michele Aquaro University of Warwick This version: July 21, 2016 1 / 31 Reading material Textbook: Introductory

Warwick Economics Summer School Topics in Microeconometrics Instrumental Variables Estimation Michele Aquaro University of Warwick This version: July 21, 2016 1 / 31 Reading material Textbook: Introductory

Instrumental Variables, Simultaneous and Systems of Equations

Chapter 6 Instrumental Variables, Simultaneous and Systems of Equations 61 Instrumental variables In the linear regression model y i = x iβ + ε i (61) we have been assuming that bf x i and ε i are uncorrelated

Chapter 6 Instrumental Variables, Simultaneous and Systems of Equations 61 Instrumental variables In the linear regression model y i = x iβ + ε i (61) we have been assuming that bf x i and ε i are uncorrelated

INTRODUCTION TO BASIC LINEAR REGRESSION MODEL

INTRODUCTION TO BASIC LINEAR REGRESSION MODEL 13 September 2011 Yogyakarta, Indonesia Cosimo Beverelli (World Trade Organization) 1 LINEAR REGRESSION MODEL In general, regression models estimate the effect

INTRODUCTION TO BASIC LINEAR REGRESSION MODEL 13 September 2011 Yogyakarta, Indonesia Cosimo Beverelli (World Trade Organization) 1 LINEAR REGRESSION MODEL In general, regression models estimate the effect

Empirical Application of Simple Regression (Chapter 2)

") Empirical Application of Simple Regression (Chapter 2) 1. The data file is House Data, which can be downloaded from my webpage. 2. Use stata menu File Import Excel Spreadsheet to read the data. Don t forget

Empirical Application of Simple Regression (Chapter 2) 1. The data file is House Data, which can be downloaded from my webpage. 2. Use stata menu File Import Excel Spreadsheet to read the data. Don t forget

Lecture 14. More on using dummy variables (deal with seasonality)

") Lecture 14. More on using dummy variables (deal with seasonality) More things to worry about: measurement error in variables (can lead to bias in OLS (endogeneity) ) Have seen that dummy variables are

Lecture 14. More on using dummy variables (deal with seasonality) More things to worry about: measurement error in variables (can lead to bias in OLS (endogeneity) ) Have seen that dummy variables are

Problem Set 10: Panel Data

Problem Set 10: Panel Data 1. Read in the data set, e11panel1.dta from the course website. This contains data on a sample or 1252 men and women who were asked about their hourly wage in two years, 2005

Problem Set 10: Panel Data 1. Read in the data set, e11panel1.dta from the course website. This contains data on a sample or 1252 men and women who were asked about their hourly wage in two years, 2005

Econometrics Honor s Exam Review Session. Spring 2012 Eunice Han

Econometrics Honor s Exam Review Session Spring 2012 Eunice Han Topics 1. OLS The Assumptions Omitted Variable Bias Conditional Mean Independence Hypothesis Testing and Confidence Intervals Homoskedasticity

Econometrics Honor s Exam Review Session Spring 2012 Eunice Han Topics 1. OLS The Assumptions Omitted Variable Bias Conditional Mean Independence Hypothesis Testing and Confidence Intervals Homoskedasticity

University of California at Berkeley Fall Introductory Applied Econometrics Final examination. Scores add up to 125 points

EEP 118 / IAS 118 Elisabeth Sadoulet and Kelly Jones University of California at Berkeley Fall 2008 Introductory Applied Econometrics Final examination Scores add up to 125 points Your name: SID: 1 1.

EEP 118 / IAS 118 Elisabeth Sadoulet and Kelly Jones University of California at Berkeley Fall 2008 Introductory Applied Econometrics Final examination Scores add up to 125 points Your name: SID: 1 1.

Introduction to Econometrics

Introduction to Econometrics STAT-S-301 Panel Data (2016/2017) Lecturer: Yves Dominicy Teaching Assistant: Elise Petit 1 Regression with Panel Data A panel dataset contains observations on multiple entities

Introduction to Econometrics STAT-S-301 Panel Data (2016/2017) Lecturer: Yves Dominicy Teaching Assistant: Elise Petit 1 Regression with Panel Data A panel dataset contains observations on multiple entities

ECON Introductory Econometrics. Lecture 5: OLS with One Regressor: Hypothesis Tests

ECON4150 - Introductory Econometrics Lecture 5: OLS with One Regressor: Hypothesis Tests Monique de Haan (moniqued@econ.uio.no) Stock and Watson Chapter 5 Lecture outline 2 Testing Hypotheses about one

ECON4150 - Introductory Econometrics Lecture 5: OLS with One Regressor: Hypothesis Tests Monique de Haan (moniqued@econ.uio.no) Stock and Watson Chapter 5 Lecture outline 2 Testing Hypotheses about one

University of Maryland Spring Economics 422 Final Examination

Department of Economics John C. Chao University of Maryland Spring 2009 Economics 422 Final Examination This exam contains 4 regular questions and 1 bonus question. The total number of points for the regular

Department of Economics John C. Chao University of Maryland Spring 2009 Economics 422 Final Examination This exam contains 4 regular questions and 1 bonus question. The total number of points for the regular

Vector Autogregression and Impulse Response Functions

Chapter 8 Vector Autogregression and Impulse Response Functions 8.1 Vector Autogregressions Consider two sequences {y t } and {z t }, where the time path of {y t } is affected by current and past realizations

Chapter 8 Vector Autogregression and Impulse Response Functions 8.1 Vector Autogregressions Consider two sequences {y t } and {z t }, where the time path of {y t } is affected by current and past realizations

Econometrics Homework 1

Econometrics Homework Due Date: March, 24. by This problem set includes questions for Lecture -4 covered before midterm exam. Question Let z be a random column vector of size 3 : z = @ (a) Write out z

Econometrics Homework Due Date: March, 24. by This problem set includes questions for Lecture -4 covered before midterm exam. Question Let z be a random column vector of size 3 : z = @ (a) Write out z

4 Instrumental Variables Single endogenous variable One continuous instrument. 2

Econ 495 - Econometric Review 1 Contents 4 Instrumental Variables 2 4.1 Single endogenous variable One continuous instrument. 2 4.2 Single endogenous variable more than one continuous instrument..........................

Econ 495 - Econometric Review 1 Contents 4 Instrumental Variables 2 4.1 Single endogenous variable One continuous instrument. 2 4.2 Single endogenous variable more than one continuous instrument..........................

Problem Set #3-Key. wage Coef. Std. Err. t P> t [95% Conf. Interval]

![Problem Set #3-Key. wage Coef. Std. Err. t P> t [95% Conf. Interval]](/thumbs/84/90891969.jpg "Problem Set #3-Key. wage Coef. Std. Err. t P> t [95% Conf. Interval]") Problem Set #3-Key Sonoma State University Economics 317- Introduction to Econometrics Dr. Cuellar 1. Use the data set Wage1.dta to answer the following questions. a. For the regression model Wage i =

Problem Set #3-Key Sonoma State University Economics 317- Introduction to Econometrics Dr. Cuellar 1. Use the data set Wage1.dta to answer the following questions. a. For the regression model Wage i =

Autoregressive models with distributed lags (ADL)

") Autoregressive models with distributed lags (ADL) It often happens than including the lagged dependent variable in the model results in model which is better fitted and needs less parameters. It can be

Autoregressive models with distributed lags (ADL) It often happens than including the lagged dependent variable in the model results in model which is better fitted and needs less parameters. It can be

Essential of Simple regression

Essential of Simple regression We use simple regression when we are interested in the relationship between two variables (e.g., x is class size, and y is student s GPA). For simplicity we assume the relationship

Essential of Simple regression We use simple regression when we are interested in the relationship between two variables (e.g., x is class size, and y is student s GPA). For simplicity we assume the relationship

Introduction to Econometrics. Regression with Panel Data

Introduction to Econometrics The statistical analysis of economic (and related) data STATS301 Regression with Panel Data Titulaire: Christopher Bruffaerts Assistant: Lorenzo Ricci 1 Regression with Panel

Introduction to Econometrics The statistical analysis of economic (and related) data STATS301 Regression with Panel Data Titulaire: Christopher Bruffaerts Assistant: Lorenzo Ricci 1 Regression with Panel

Autocorrelation. Think of autocorrelation as signifying a systematic relationship between the residuals measured at different points in time

Autocorrelation Given the model Y t = b 0 + b 1 X t + u t Think of autocorrelation as signifying a systematic relationship between the residuals measured at different points in time This could be caused

Autocorrelation Given the model Y t = b 0 + b 1 X t + u t Think of autocorrelation as signifying a systematic relationship between the residuals measured at different points in time This could be caused

Handout 11: Measurement Error

Handout 11: Measurement Error In which you learn to recognise the consequences for OLS estimation whenever some of the variables you use are not measured as accurately as you might expect. A (potential)

Handout 11: Measurement Error In which you learn to recognise the consequences for OLS estimation whenever some of the variables you use are not measured as accurately as you might expect. A (potential)

Exercices for Applied Econometrics A

QEM F. Gardes-C. Starzec-M.A. Diaye Exercices for Applied Econometrics A I. Exercice: The panel of households expenditures in Poland, for years 1997 to 2000, gives the following statistics for the whole

QEM F. Gardes-C. Starzec-M.A. Diaye Exercices for Applied Econometrics A I. Exercice: The panel of households expenditures in Poland, for years 1997 to 2000, gives the following statistics for the whole

. regress lchnimp lchempi lgas lrtwex befile6 affile6 afdec6 t

BOSTON COLLEGE Department of Economics EC 228 Econometrics, Prof. Baum, Ms. Yu, Fall 2003 Problem Set 7 Solutions Problem sets should be your own work. You may work together with classmates, but if you

BOSTON COLLEGE Department of Economics EC 228 Econometrics, Prof. Baum, Ms. Yu, Fall 2003 Problem Set 7 Solutions Problem sets should be your own work. You may work together with classmates, but if you

Fixed and Random Effects Models: Vartanian, SW 683

: Vartanian, SW 683 Fixed and random effects models See: http://teaching.sociology.ul.ie/dcw/confront/node45.html When you have repeated observations per individual this is a problem and an advantage:

: Vartanian, SW 683 Fixed and random effects models See: http://teaching.sociology.ul.ie/dcw/confront/node45.html When you have repeated observations per individual this is a problem and an advantage:

Introductory Econometrics. Lecture 13: Hypothesis testing in the multiple regression model, Part 1

Introductory Econometrics Lecture 13: Hypothesis testing in the multiple regression model, Part 1 Jun Ma School of Economics Renmin University of China October 19, 2016 The model I We consider the classical

Introductory Econometrics Lecture 13: Hypothesis testing in the multiple regression model, Part 1 Jun Ma School of Economics Renmin University of China October 19, 2016 The model I We consider the classical

Unemployment Rate Example

Unemployment Rate Example Find unemployment rates for men and women in your age bracket Go to FRED Categories/Population/Current Population Survey/Unemployment Rate Release Tables/Selected unemployment

Unemployment Rate Example Find unemployment rates for men and women in your age bracket Go to FRED Categories/Population/Current Population Survey/Unemployment Rate Release Tables/Selected unemployment

WISE MA/PhD Programs Econometrics Instructor: Brett Graham Spring Semester, Academic Year Exam Version: A

WISE MA/PhD Programs Econometrics Instructor: Brett Graham Spring Semester, 2015-16 Academic Year Exam Version: A INSTRUCTIONS TO STUDENTS 1 The time allowed for this examination paper is 2 hours. 2 This

WISE MA/PhD Programs Econometrics Instructor: Brett Graham Spring Semester, 2015-16 Academic Year Exam Version: A INSTRUCTIONS TO STUDENTS 1 The time allowed for this examination paper is 2 hours. 2 This

4 Instrumental Variables Single endogenous variable One continuous instrument. 2

Econ 495 - Econometric Review 1 Contents 4 Instrumental Variables 2 4.1 Single endogenous variable One continuous instrument. 2 4.2 Single endogenous variable more than one continuous instrument..........................

Econ 495 - Econometric Review 1 Contents 4 Instrumental Variables 2 4.1 Single endogenous variable One continuous instrument. 2 4.2 Single endogenous variable more than one continuous instrument..........................

-redprob- A Stata program for the Heckman estimator of the random effects dynamic probit model

-redprob- A Stata program for the Heckman estimator of the random effects dynamic probit model Mark B. Stewart University of Warwick January 2006 1 The model The latent equation for the random effects

-redprob- A Stata program for the Heckman estimator of the random effects dynamic probit model Mark B. Stewart University of Warwick January 2006 1 The model The latent equation for the random effects

ECON Introductory Econometrics. Lecture 13: Internal and external validity

ECON4150 - Introductory Econometrics Lecture 13: Internal and external validity Monique de Haan (moniqued@econ.uio.no) Stock and Watson Chapter 9 Lecture outline 2 Definitions of internal and external

ECON4150 - Introductory Econometrics Lecture 13: Internal and external validity Monique de Haan (moniqued@econ.uio.no) Stock and Watson Chapter 9 Lecture outline 2 Definitions of internal and external

Exam ECON3150/4150: Introductory Econometrics. 18 May 2016; 09:00h-12.00h.

Exam ECON3150/4150: Introductory Econometrics. 18 May 2016; 09:00h-12.00h. This is an open book examination where all printed and written resources, in addition to a calculator, are allowed. If you are

Exam ECON3150/4150: Introductory Econometrics. 18 May 2016; 09:00h-12.00h. This is an open book examination where all printed and written resources, in addition to a calculator, are allowed. If you are

Econ 423 Lecture Notes

Econ 423 Lecture Notes (These notes are slightly modified versions of lecture notes provided by Stock and Watson, 2007. They are for instructional purposes only and are not to be distributed outside of

Econ 423 Lecture Notes (These notes are slightly modified versions of lecture notes provided by Stock and Watson, 2007. They are for instructional purposes only and are not to be distributed outside of

7 Introduction to Time Series Time Series vs. Cross-Sectional Data Detrending Time Series... 15

Econ 495 - Econometric Review 1 Contents 7 Introduction to Time Series 3 7.1 Time Series vs. Cross-Sectional Data............ 3 7.2 Detrending Time Series................... 15 7.3 Types of Stochastic

Econ 495 - Econometric Review 1 Contents 7 Introduction to Time Series 3 7.1 Time Series vs. Cross-Sectional Data............ 3 7.2 Detrending Time Series................... 15 7.3 Types of Stochastic

ECON Introductory Econometrics. Lecture 16: Instrumental variables

ECON4150 - Introductory Econometrics Lecture 16: Instrumental variables Monique de Haan (moniqued@econ.uio.no) Stock and Watson Chapter 12 Lecture outline 2 OLS assumptions and when they are violated Instrumental

ECON4150 - Introductory Econometrics Lecture 16: Instrumental variables Monique de Haan (moniqued@econ.uio.no) Stock and Watson Chapter 12 Lecture outline 2 OLS assumptions and when they are violated Instrumental

Nonrecursive Models Highlights Richard Williams, University of Notre Dame, https://www3.nd.edu/~rwilliam/ Last revised April 6, 2015

Nonrecursive Models Highlights Richard Williams, University of Notre Dame, https://www3.nd.edu/~rwilliam/ Last revised April 6, 2015 This lecture borrows heavily from Duncan s Introduction to Structural

Nonrecursive Models Highlights Richard Williams, University of Notre Dame, https://www3.nd.edu/~rwilliam/ Last revised April 6, 2015 This lecture borrows heavily from Duncan s Introduction to Structural

ECON Introductory Econometrics. Lecture 11: Binary dependent variables

ECON4150 - Introductory Econometrics Lecture 11: Binary dependent variables Monique de Haan (moniqued@econ.uio.no) Stock and Watson Chapter 11 Lecture Outline 2 The linear probability model Nonlinear probability

ECON4150 - Introductory Econometrics Lecture 11: Binary dependent variables Monique de Haan (moniqued@econ.uio.no) Stock and Watson Chapter 11 Lecture Outline 2 The linear probability model Nonlinear probability

2.1. Consider the following production function, known in the literature as the transcendental production function (TPF).

.") CHAPTER Functional Forms of Regression Models.1. Consider the following production function, known in the literature as the transcendental production function (TPF). Q i B 1 L B i K i B 3 e B L B K 4 i

CHAPTER Functional Forms of Regression Models.1. Consider the following production function, known in the literature as the transcendental production function (TPF). Q i B 1 L B i K i B 3 e B L B K 4 i

Ecmt 675: Econometrics I

Ecmt 675: Econometrics I Assignment 7 Problem 1 a. reg hours lwage educ age kidslt6 kidsge6 nwifeinc, r Linear regression Number of obs = 428 F( 6, 421) = 3.93 Prob > F = 0.0008 R-squared = 0.0670 Root

Ecmt 675: Econometrics I Assignment 7 Problem 1 a. reg hours lwage educ age kidslt6 kidsge6 nwifeinc, r Linear regression Number of obs = 428 F( 6, 421) = 3.93 Prob > F = 0.0008 R-squared = 0.0670 Root

Econometrics I KS. Module 2: Multivariate Linear Regression. Alexander Ahammer. This version: April 16, 2018

Econometrics I KS Module 2: Multivariate Linear Regression Alexander Ahammer Department of Economics Johannes Kepler University of Linz This version: April 16, 2018 Alexander Ahammer (JKU) Module 2: Multivariate

Econometrics I KS Module 2: Multivariate Linear Regression Alexander Ahammer Department of Economics Johannes Kepler University of Linz This version: April 16, 2018 Alexander Ahammer (JKU) Module 2: Multivariate

Cointegration and Error-Correction

Chapter 9 Cointegration and Error-Correction In this chapter we will estimate structural VAR models that include nonstationary variables. This exploits the possibility that there could be a linear combination

Chapter 9 Cointegration and Error-Correction In this chapter we will estimate structural VAR models that include nonstationary variables. This exploits the possibility that there could be a linear combination

Graduate Econometrics Lecture 4: Heteroskedasticity

Graduate Econometrics Lecture 4: Heteroskedasticity Department of Economics University of Gothenburg November 30, 2014 1/43 and Autocorrelation Consequences for OLS Estimator Begin from the linear model

Graduate Econometrics Lecture 4: Heteroskedasticity Department of Economics University of Gothenburg November 30, 2014 1/43 and Autocorrelation Consequences for OLS Estimator Begin from the linear model

Applied Statistics and Econometrics

Applied Statistics and Econometrics Lecture 6 Saul Lach September 2017 Saul Lach () Applied Statistics and Econometrics September 2017 1 / 53 Outline of Lecture 6 1 Omitted variable bias (SW 6.1) 2 Multiple

Applied Statistics and Econometrics Lecture 6 Saul Lach September 2017 Saul Lach () Applied Statistics and Econometrics September 2017 1 / 53 Outline of Lecture 6 1 Omitted variable bias (SW 6.1) 2 Multiple

Quantitative Methods Final Exam (2017/1)

") Quantitative Methods Final Exam (2017/1) 1. Please write down your name and student ID number. 2. Calculator is allowed during the exam, but DO NOT use a smartphone. 3. List your answers (together with

Quantitative Methods Final Exam (2017/1) 1. Please write down your name and student ID number. 2. Calculator is allowed during the exam, but DO NOT use a smartphone. 3. List your answers (together with

7 Introduction to Time Series

Econ 495 - Econometric Review 1 7 Introduction to Time Series 7.1 Time Series vs. Cross-Sectional Data Time series data has a temporal ordering, unlike cross-section data, we will need to changes some

Econ 495 - Econometric Review 1 7 Introduction to Time Series 7.1 Time Series vs. Cross-Sectional Data Time series data has a temporal ordering, unlike cross-section data, we will need to changes some

Empirical Application of Panel Data Regression

Empirical Application of Panel Data Regression 1. We use Fatality data, and we are interested in whether rising beer tax rate can help lower traffic death. So the dependent variable is traffic death, while

Empirical Application of Panel Data Regression 1. We use Fatality data, and we are interested in whether rising beer tax rate can help lower traffic death. So the dependent variable is traffic death, while

Econometrics -- Final Exam (Sample)

") Econometrics -- Final Exam (Sample) 1) The sample regression line estimated by OLS A) has an intercept that is equal to zero. B) is the same as the population regression line. C) cannot have negative and

Econometrics -- Final Exam (Sample) 1) The sample regression line estimated by OLS A) has an intercept that is equal to zero. B) is the same as the population regression line. C) cannot have negative and

Dynamic Panel Data Models

Models Amjad Naveed, Nora Prean, Alexander Rabas 15th June 2011 Motivation Many economic issues are dynamic by nature. These dynamic relationships are characterized by the presence of a lagged dependent

Models Amjad Naveed, Nora Prean, Alexander Rabas 15th June 2011 Motivation Many economic issues are dynamic by nature. These dynamic relationships are characterized by the presence of a lagged dependent

ECON3150/4150 Spring 2015

ECON3150/4150 Spring 2015 Lecture 3&4 - The linear regression model Siv-Elisabeth Skjelbred University of Oslo January 29, 2015 1 / 67 Chapter 4 in S&W Section 17.1 in S&W (extended OLS assumptions) 2

ECON3150/4150 Spring 2015 Lecture 3&4 - The linear regression model Siv-Elisabeth Skjelbred University of Oslo January 29, 2015 1 / 67 Chapter 4 in S&W Section 17.1 in S&W (extended OLS assumptions) 2

ECON Introductory Econometrics. Lecture 17: Experiments

ECON4150 - Introductory Econometrics Lecture 17: Experiments Monique de Haan (moniqued@econ.uio.no) Stock and Watson Chapter 13 Lecture outline 2 Why study experiments? The potential outcome framework.

ECON4150 - Introductory Econometrics Lecture 17: Experiments Monique de Haan (moniqued@econ.uio.no) Stock and Watson Chapter 13 Lecture outline 2 Why study experiments? The potential outcome framework.

ECON2228 Notes 7. Christopher F Baum. Boston College Economics. cfb (BC Econ) ECON2228 Notes / 41

ECON2228 Notes / 41") ECON2228 Notes 7 Christopher F Baum Boston College Economics 2014 2015 cfb (BC Econ) ECON2228 Notes 6 2014 2015 1 / 41 Chapter 8: Heteroskedasticity In laying out the standard regression model, we made

ECON2228 Notes 7 Christopher F Baum Boston College Economics 2014 2015 cfb (BC Econ) ECON2228 Notes 6 2014 2015 1 / 41 Chapter 8: Heteroskedasticity In laying out the standard regression model, we made

ECO220Y Simple Regression: Testing the Slope

ECO220Y Simple Regression: Testing the Slope Readings: Chapter 18 (Sections 18.3-18.5) Winter 2012 Lecture 19 (Winter 2012) Simple Regression Lecture 19 1 / 32 Simple Regression Model y i = β 0 + β 1 x

ECO220Y Simple Regression: Testing the Slope Readings: Chapter 18 (Sections 18.3-18.5) Winter 2012 Lecture 19 (Winter 2012) Simple Regression Lecture 19 1 / 32 Simple Regression Model y i = β 0 + β 1 x

ECON3150/4150 Spring 2016

ECON3150/4150 Spring 2016 Lecture 6 Multiple regression model Siv-Elisabeth Skjelbred University of Oslo February 5th Last updated: February 3, 2016 1 / 49 Outline Multiple linear regression model and

ECON3150/4150 Spring 2016 Lecture 6 Multiple regression model Siv-Elisabeth Skjelbred University of Oslo February 5th Last updated: February 3, 2016 1 / 49 Outline Multiple linear regression model and

Introduction to Regression Analysis. Dr. Devlina Chatterjee 11 th August, 2017

Introduction to Regression Analysis Dr. Devlina Chatterjee 11 th August, 2017 What is regression analysis? Regression analysis is a statistical technique for studying linear relationships. One dependent

Introduction to Regression Analysis Dr. Devlina Chatterjee 11 th August, 2017 What is regression analysis? Regression analysis is a statistical technique for studying linear relationships. One dependent

F Tests and F statistics

F Tests and F statistics Testing Linear estrictions F Stats and F Tests F Distributions F stats (w/ ) F Stats and tstat s eported F Stat's in OLS Output Example I: Bodyfat Babies and Bathwater F Stats,

F Tests and F statistics Testing Linear estrictions F Stats and F Tests F Distributions F stats (w/ ) F Stats and tstat s eported F Stat's in OLS Output Example I: Bodyfat Babies and Bathwater F Stats,

Lecture 8: Instrumental Variables Estimation

Lecture Notes on Advanced Econometrics Lecture 8: Instrumental Variables Estimation Endogenous Variables Consider a population model: y α y + β + β x + β x +... + β x + u i i i i k ik i Takashi Yamano

Lecture Notes on Advanced Econometrics Lecture 8: Instrumental Variables Estimation Endogenous Variables Consider a population model: y α y + β + β x + β x +... + β x + u i i i i k ik i Takashi Yamano

Answers: Problem Set 9. Dynamic Models

Answers: Problem Set 9. Dynamic Models 1. Given annual data for the period 1970-1999, you undertake an OLS regression of log Y on a time trend, defined as taking the value 1 in 1970, 2 in 1972 etc. The

Answers: Problem Set 9. Dynamic Models 1. Given annual data for the period 1970-1999, you undertake an OLS regression of log Y on a time trend, defined as taking the value 1 in 1970, 2 in 1972 etc. The

Longitudinal Data Analysis Using Stata Paul D. Allison, Ph.D. Upcoming Seminar: May 18-19, 2017, Chicago, Illinois

Longitudinal Data Analysis Using Stata Paul D. Allison, Ph.D. Upcoming Seminar: May 18-19, 217, Chicago, Illinois Outline 1. Opportunities and challenges of panel data. a. Data requirements b. Control

Longitudinal Data Analysis Using Stata Paul D. Allison, Ph.D. Upcoming Seminar: May 18-19, 217, Chicago, Illinois Outline 1. Opportunities and challenges of panel data. a. Data requirements b. Control

Linear Regression with Multiple Regressors

Linear Regression with Multiple Regressors (SW Chapter 6) Outline 1. Omitted variable bias 2. Causality and regression analysis 3. Multiple regression and OLS 4. Measures of fit 5. Sampling distribution

Linear Regression with Multiple Regressors (SW Chapter 6) Outline 1. Omitted variable bias 2. Causality and regression analysis 3. Multiple regression and OLS 4. Measures of fit 5. Sampling distribution

Econometrics Homework 4 Solutions

Econometrics Homework 4 Solutions Computer Question (Optional, no need to hand in) (a) c i may capture some state-specific factor that contributes to higher or low rate of accident or fatality. For example,

Econometrics Homework 4 Solutions Computer Question (Optional, no need to hand in) (a) c i may capture some state-specific factor that contributes to higher or low rate of accident or fatality. For example,

Recent Advances in the Field of Trade Theory and Policy Analysis Using Micro-Level Data

Recent Advances in the Field of Trade Theory and Policy Analysis Using Micro-Level Data July 2012 Bangkok, Thailand Cosimo Beverelli (World Trade Organization) 1 Content a) Classical regression model b)

Recent Advances in the Field of Trade Theory and Policy Analysis Using Micro-Level Data July 2012 Bangkok, Thailand Cosimo Beverelli (World Trade Organization) 1 Content a) Classical regression model b)

Problem Set 5 ANSWERS

Economics 20 Problem Set 5 ANSWERS Prof. Patricia M. Anderson 1, 2 and 3 Suppose that Vermont has passed a law requiring employers to provide 6 months of paid maternity leave. You are concerned that women

Economics 20 Problem Set 5 ANSWERS Prof. Patricia M. Anderson 1, 2 and 3 Suppose that Vermont has passed a law requiring employers to provide 6 months of paid maternity leave. You are concerned that women

Practice 2SLS with Artificial Data Part 1

Practice 2SLS with Artificial Data Part 1 Yona Rubinstein July 2016 Yona Rubinstein (LSE) Practice 2SLS with Artificial Data Part 1 07/16 1 / 16 Practice with Artificial Data In this note we use artificial

Practice 2SLS with Artificial Data Part 1 Yona Rubinstein July 2016 Yona Rubinstein (LSE) Practice 2SLS with Artificial Data Part 1 07/16 1 / 16 Practice with Artificial Data In this note we use artificial

Lecture 4: Multivariate Regression, Part 2

Lecture 4: Multivariate Regression, Part 2 Gauss-Markov Assumptions 1) Linear in Parameters: Y X X X i 0 1 1 2 2 k k 2) Random Sampling: we have a random sample from the population that follows the above

Lecture 4: Multivariate Regression, Part 2 Gauss-Markov Assumptions 1) Linear in Parameters: Y X X X i 0 1 1 2 2 k k 2) Random Sampling: we have a random sample from the population that follows the above

2. (3.5) (iii) Simply drop one of the independent variables, say leisure: GP A = β 0 + β 1 study + β 2 sleep + β 3 work + u.

(iii) Simply drop one of the independent variables, say leisure: GP A = β 0 + β 1 study + β 2 sleep + β 3 work + u.") BOSTON COLLEGE Department of Economics EC 228 Econometrics, Prof. Baum, Ms. Yu, Fall 2003 Problem Set 3 Solutions Problem sets should be your own work. You may work together with classmates, but if you

BOSTON COLLEGE Department of Economics EC 228 Econometrics, Prof. Baum, Ms. Yu, Fall 2003 Problem Set 3 Solutions Problem sets should be your own work. You may work together with classmates, but if you

Estimating Markov-switching regression models in Stata

Estimating Markov-switching regression models in Stata Ashish Rajbhandari Senior Econometrician StataCorp LP Stata Conference 2015 Ashish Rajbhandari (StataCorp LP) Markov-switching regression Stata Conference

Estimating Markov-switching regression models in Stata Ashish Rajbhandari Senior Econometrician StataCorp LP Stata Conference 2015 Ashish Rajbhandari (StataCorp LP) Markov-switching regression Stata Conference

ECON Introductory Econometrics. Lecture 6: OLS with Multiple Regressors

ECON4150 - Introductory Econometrics Lecture 6: OLS with Multiple Regressors Monique de Haan (moniqued@econ.uio.no) Stock and Watson Chapter 6 Lecture outline 2 Violation of first Least Squares assumption

ECON4150 - Introductory Econometrics Lecture 6: OLS with Multiple Regressors Monique de Haan (moniqued@econ.uio.no) Stock and Watson Chapter 6 Lecture outline 2 Violation of first Least Squares assumption

Heteroskedasticity. Occurs when the Gauss Markov assumption that the residual variance is constant across all observations in the data set

Heteroskedasticity Occurs when the Gauss Markov assumption that the residual variance is constant across all observations in the data set Heteroskedasticity Occurs when the Gauss Markov assumption that

Heteroskedasticity Occurs when the Gauss Markov assumption that the residual variance is constant across all observations in the data set Heteroskedasticity Occurs when the Gauss Markov assumption that

Specification Error: Omitted and Extraneous Variables

Specification Error: Omitted and Extraneous Variables Richard Williams, University of Notre Dame, https://www3.nd.edu/~rwilliam/ Last revised February 5, 05 Omitted variable bias. Suppose that the correct

Specification Error: Omitted and Extraneous Variables Richard Williams, University of Notre Dame, https://www3.nd.edu/~rwilliam/ Last revised February 5, 05 Omitted variable bias. Suppose that the correct

Basic econometrics. Tutorial 3. Dipl.Kfm. Johannes Metzler

Basic econometrics Tutorial 3 Dipl.Kfm. Introduction Some of you were asking about material to revise/prepare econometrics fundamentals. First of all, be aware that I will not be too technical, only as

Basic econometrics Tutorial 3 Dipl.Kfm. Introduction Some of you were asking about material to revise/prepare econometrics fundamentals. First of all, be aware that I will not be too technical, only as

WISE International Masters

WISE International Masters ECONOMETRICS Instructor: Brett Graham INSTRUCTIONS TO STUDENTS 1 The time allowed for this examination paper is 2 hours. 2 This examination paper contains 32 questions. You are

WISE International Masters ECONOMETRICS Instructor: Brett Graham INSTRUCTIONS TO STUDENTS 1 The time allowed for this examination paper is 2 hours. 2 This examination paper contains 32 questions. You are

Interpreting coefficients for transformed variables

Interpreting coefficients for transformed variables! Recall that when both independent and dependent variables are untransformed, an estimated coefficient represents the change in the dependent variable

Interpreting coefficients for transformed variables! Recall that when both independent and dependent variables are untransformed, an estimated coefficient represents the change in the dependent variable

Heteroskedasticity. (In practice this means the spread of observations around any given value of X will not now be constant)

") Heteroskedasticity Occurs when the Gauss Markov assumption that the residual variance is constant across all observations in the data set so that E(u 2 i /X i ) σ 2 i (In practice this means the spread

Heteroskedasticity Occurs when the Gauss Markov assumption that the residual variance is constant across all observations in the data set so that E(u 2 i /X i ) σ 2 i (In practice this means the spread

Binary Dependent Variables

Binary Dependent Variables In some cases the outcome of interest rather than one of the right hand side variables - is discrete rather than continuous Binary Dependent Variables In some cases the outcome

Binary Dependent Variables In some cases the outcome of interest rather than one of the right hand side variables - is discrete rather than continuous Binary Dependent Variables In some cases the outcome

At this point, if you ve done everything correctly, you should have data that looks something like:

This homework is due on July 19 th. Economics 375: Introduction to Econometrics Homework #4 1. One tool to aid in understanding econometrics is the Monte Carlo experiment. A Monte Carlo experiment allows

This homework is due on July 19 th. Economics 375: Introduction to Econometrics Homework #4 1. One tool to aid in understanding econometrics is the Monte Carlo experiment. A Monte Carlo experiment allows

Lecture 8: Functional Form

Lecture 8: Functional Form What we know now OLS - fitting a straight line y = b 0 + b 1 X through the data using the principle of choosing the straight line that minimises the sum of squared residuals

Lecture 8: Functional Form What we know now OLS - fitting a straight line y = b 0 + b 1 X through the data using the principle of choosing the straight line that minimises the sum of squared residuals

1 The basics of panel data

Introductory Applied Econometrics EEP/IAS 118 Spring 2015 Related materials: Steven Buck Notes to accompany fixed effects material 4-16-14 ˆ Wooldridge 5e, Ch. 1.3: The Structure of Economic Data ˆ Wooldridge

Introductory Applied Econometrics EEP/IAS 118 Spring 2015 Related materials: Steven Buck Notes to accompany fixed effects material 4-16-14 ˆ Wooldridge 5e, Ch. 1.3: The Structure of Economic Data ˆ Wooldridge

Write your identification number on each paper and cover sheet (the number stated in the upper right hand corner on your exam cover).

.") STOCKHOLM UNIVERSITY Department of Economics Course name: Empirical Methods in Economics 2 Course code: EC2402 Examiner: Peter Skogman Thoursie Number of credits: 7,5 credits (hp) Date of exam: Saturday,

STOCKHOLM UNIVERSITY Department of Economics Course name: Empirical Methods in Economics 2 Course code: EC2402 Examiner: Peter Skogman Thoursie Number of credits: 7,5 credits (hp) Date of exam: Saturday,

An explanation of Two Stage Least Squares

Introduction Introduction to Econometrics An explanation of Two Stage Least Squares When we get an endogenous variable we know that OLS estimator will be inconsistent. In addition OLS regressors will also

Introduction Introduction to Econometrics An explanation of Two Stage Least Squares When we get an endogenous variable we know that OLS estimator will be inconsistent. In addition OLS regressors will also

Problem Set 1 ANSWERS

Economics 20 Prof. Patricia M. Anderson Problem Set 1 ANSWERS Part I. Multiple Choice Problems 1. If X and Z are two random variables, then E[X-Z] is d. E[X] E[Z] This is just a simple application of one

Economics 20 Prof. Patricia M. Anderson Problem Set 1 ANSWERS Part I. Multiple Choice Problems 1. If X and Z are two random variables, then E[X-Z] is d. E[X] E[Z] This is just a simple application of one

Economics 326 Methods of Empirical Research in Economics. Lecture 14: Hypothesis testing in the multiple regression model, Part 2

Economics 326 Methods of Empirical Research in Economics Lecture 14: Hypothesis testing in the multiple regression model, Part 2 Vadim Marmer University of British Columbia May 5, 2010 Multiple restrictions

Economics 326 Methods of Empirical Research in Economics Lecture 14: Hypothesis testing in the multiple regression model, Part 2 Vadim Marmer University of British Columbia May 5, 2010 Multiple restrictions