IV Estimation and its Limitations: Weak Instruments and Weakly Endogeneous Regressors

|

|

|

- Gertrude Brenda Lee

- 5 years ago

- Views:

Transcription

1 IV Estimation and its Limitations: Weak Instruments and Weakly Endogeneous Regressors Laura Mayoral, IAE, Barcelona GSE and University of Gothenburg U. of Gothenburg, May 2015

2 Roadmap Testing for deviations from the standard framework Detection of weak instruments Inference robust to weak instruments Software: ivreg2 (STATA) Examples

3 Testing for deviations from the standard framework Testing for the failure of the exclusion restriction: not possible to test, unless the model is overidentified (i.e., there are more instruments that endogenous variables), but strong assumptions are needed (basically you need to assume what you want to test!) Testing for the failure of the relevance condition/weak instruments: different tests are available, most of them based on the F statistic of the null hypothesis that Π = 0 in the first stage.

4 Testing the exclusion restriction: J tests of overidentifying restrictions In an exactly identified model we cannot test the hypothesis that the instrument is valid, i.e. that the exclusion restriction is a valid one the assumption that the instrument is valid will essentially have to be taken on faith. See Murray (2005, 2006) for tips that will help you to motivate this faith If the model is overidentified, it s possible to test for the validity of the overidentifying restrictions. Strong assumption: you need to assume that a set of instruments (enough to identify the parameters) are valid and you can test whether the remaining ones are also one.

5 If you reject the null that the remaining instruments are exogenous: there is something wrong in your model you need to reconsider the validity of the instruments But not rejecting the null doesn t mean that your instruments are valid!! Sargan test: you don t need to specify which instruments are the valid ones and which are the dubious ones. But still, you need as least K instruments that are valid! (K=number of endogenous variables). Otherwise the test is not consistent.

6 Detection of weak instruments Two types of test Tests of underidentification: test whether instruments are irrelevant (Π=0) Tests of weak identification: test whether instrument are weak. Always interpret tests of underidentification with caution: if you reject underidentification, it can still be the case that your model is only weakly identified since instruments are weak.

7 Detection of weak instruments, II Goal: determine when instruments are irrelevant (test of under identification) or weak (tests of weak identification). For the 1 endogenous variable case, consider the reduced-form regression X = ZΠ + W δ + v where W are exogenous regressors.

8 Using F to test for weak instruments The concentration parameter µ 2 = Π Z ZΠ/σv 2 is closely related to the F statistic associated to testing H 0 : Π = 0. More specifically (under conditional homocedasticity) F 1 + µ 2 /K, where K is the number of instruments. weak instruments a low value of µ 2 a low value of F. But: this relation relies heavily on the assumption of conditional homokedasticity of the error term.

9 Staiger and Stock s rule of thumb Staiger and Stock (1997) showed that the weak instrument problem can arise even if the hypothesis of Π = 0 is rejected at standard t-tests at conventional significance levels. Staiger and Stock s Rule of thumb (1 endogenous variable): Reject that your instruments are weak if F 10, where F is the F-statistic testing Π=0 in the regression of y on Z and W (where W are the exogenous regressors included in the equation of interest).

10 Stock and Yogo (2005) s bias and size methods Stock and Yogo (SY, 2005) formalise Staiger and Stock s procedure. They show that their rule of thumb is not always enough! (see below) SY s tests can be used with multiple endogenous regressors and multiple instruments.

11 How weak is weak? We need a cutoff value for µ 2 such that for values smaller than µ 2, instruments are deemed to be weak. Since (under conditional homokedasticity) the F statistic of the first stage regression and µ 2 are related, the cutoff value is usually compared with it. There are different ways in which we can define this cutoff value, depending what we want to control (bias of β, size of t- test), etc. The value of the cutoff depends on the method employed. This means that the same instrument can be weak for one estimation method but not for other! 2SLS is one of the least robust

12 How weak is weak, II Stock and Yogo propose two methods to select the cutoffs: The bias method: find a cutoff value for µ 2 such that µ 2 the relative bias of the 2SLS with respect to OLS doesn t exceed certain quantity. The size method: find a cutoff value for µ 2 such that the maximal size of a Wald test of all the elements of β doesn t exceed a certain amount.

13 Stock and Yogo (2005) s bias method Let µ 2 10%bias be the value of µ2 such that if µ 2 µ 2 10%bias, the maximum bias of the 2SLS estimator will be no more than 10% of the bias of OLS. Decision rule is (5% significance level ) Reject that your instruments are weak if F > J 10 (k), where J 10 (k) is chosen such that P (F > J 10 (k); µ 2 = µ 2 10%bias ) = 0.05

14 Stock and Yogo (2005) s bias method, II Test statistic: 1 endogenous regressor: computed using F from the first stage regression. more than 1 endogenous regressor: Cragg- Donald (1993) statistic (multivariate version of the F statistic). Stock and Yogo (2005) provide critical values that depend on the number of endogenous regressors, the number of instruments, the maximum bias. The estimation procedure (2SLS, LIML,...) ivreg2 (STATA): gives you the critical values.

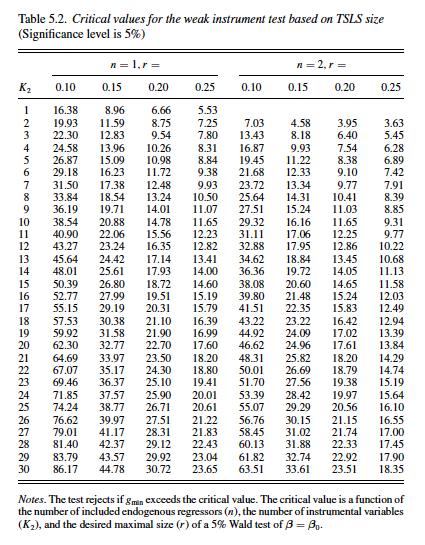

15 Stock and Yogo (2005) s size method Similar logic but instead of controlling bias, control the size of a Wald test of β=β 0 Use F statistic first stage if 1 endogenous regressor or Cragg- Donald if more than 1 Decision rule: Reject weak instruments if statistic is larger than the critical value Have a look at the critical values (and compare to Staiger and Stock s rule of thumb!)

16

17

18 Detecting weak instruments, final comments As mentioned before, the logic of using the first-stage using the F statistics relies heavily on the assumption of conditional homokedasticity. Solution: ongoing research Kleibergen-Paap rk Wald statistic: ivreg2 reports this test as a test for weak instruments when robust options are called for. However, this test is not formally justified in the context of weak instruments. It is justified in the case of under identification and if errors are i.i.d., it becomes the Cragg-Donald test (but not under weak instruments!).

19 Olea Montiel and Pflueger (2013) and (2014): tests valid under heteroskedasticity, autocorrelation, and clus- tering robust weak instrument tests, for 2SLS and LIML. But only applicable if there is only 1 endogenous regressor. Stata: weakivtest (you need to install the package first). See also Andrews 2014

20 Angrist and Pischke (2009) introduced first-stage F statistics for tests of under- and weak identification when there is more than one endogenous regressor. In contrast to the Cragg-Donald and Kleibergen-Paap statistics, which test the identification of the equation as a whole, the AP first-stage F statistics are tests of whether one of the endogenous regressors is under- or weakly identified.

21 Inference methods robust to weak instruments Problem: is it still possible to test hypothesis about β if instruments are weak? YES! But, why do you want to do that? If you know your instruments are weak, you should look for better instruments! But there are cases where the literature on weak IV detection is still limited (non i.i.d. errors for instance) so maybe you don t know.

22 Two approaches to improving inference: Fully robust methods: Inference that is valid for any value of the concentration parameter (including zero!), at least if the sample size is large, under weak instrument asymptotics. For tests: asymptotically correct size (and good power!) For confidence intervals: asymptotically correct coverage rates Partially robust methods: Methods are less sensitive to weak instruments than 2SLS (e.g. bias is small for a large range of values of µ 2 )

23 Fully Robust Testing Results are much more developed for the case of 1 endogenous regressor If more than 1 endogenous regressor: still an open econometric problem. The model (1 endogenous regressor). y = Xβ + ɛ where X is (N 1) and endogenous, Z is a matrix of instruments, maybe weak. We want to test H 0 : β = β 0.

24 Two approaches Approach 1: use a statistic whose distribution does not depend on µ 2 Two statistics here: The Anderson-Rubin (1949) test and LM statistic (Moreira 2002 and Kleiberger 2002). Approach 2: Use statistics whose distribution depends on µ 2, but compute the critical values as a function of another statistic that is sufficient for µ 2 under the null hypothesis. Conditional likelihood ratio test (Moreira 2003). Both approaches have advantages and disadvantages. We discuss both.

25 Tests robust to Weak instruments: Approach 1 The Anderson-Rubin test Set up: y = Xβ + ɛ, X endogenous, Z is a matrix (N k) of instruments. We want to test H 0 : β = β 0. AR s test: F test in the regression of (y Xβ 0 ) on Z. AR(β 0 ) = (y Xβ 0) P z /(y Xβ 0 )/k (y Xβ 0 ) M z (y Xβ 0 ) /(N k) where P z = Z (Z Z) 1Z and M z = I P z under H 0, y Xβ 0 = ɛ, so (if ɛ is iid) AR(β 0 ) = ɛ P z ɛ/k ɛ M z ɛ/(n k) d χ 2 k /k

26 Advantages and disadvantages of AR Advantages Easy to use (entirely regression based) Uses standard F critical values (asymptotic distribution doesn t depend on µ 2 Works for m > 1 (more than 1 endogenous regressor). Disadvantages Difficult to interpret: rejection arises for two reasons: H 0 is false or Z is endogenous! Power loss relative to other tests (we shall see) Is not efficient if instruments are strong under strong instruments, not as powerful as TSLS Wald test.

27 Approach 1, cont. Kleibergen s (2002) LM test Kleibergen developed an LM test that has a null distribution that is also χ 2 1 (doesn t depend on µ2 ) Advantages Fairly easy to implement Is efficient if instruments are strong Disadvantages Has very strange power properties (power function isn t monotonic) Its power is dominated by the conditional likelihood ratio test

28 Tests robust to Weak instruments. Approach 2: Conditional maximum likelihood tests Recall your probability and statistics courses: Let S be a statistic with a distribution that depends on θ Let T be a sufficient statistic for θ Then the distribution of S T does not depend on θ

29 Conditional maximum likelihood tests Moreira (2003): LR will be a statistic testing β = β 0 above) (LR is S in notation Q T will be sufficient for µ 2 under the null (Q T is T ) Thus the distribution of LR Q T the null does not depend on µ 2 under Thus valid inference can be conducted using the quantiles of LR Q T ; that is, using critical values that are a function of Q T Implementation: condivreg (STATA)

30 Advantages More powerful than AR or LM Disadvantages More complicated to explain and write down Only developed (so far) for a single included endogenous regressor As written, the software requires homoskedastic errors; extensions to heteroskedasticity and serial correlation have been developed but are not in common statistical software

31 Constructing confidence intervals It is possible to construct confidence intervals for β by inverting the robust tests described above. How? Test all the hypotheses of the form H 0 : β = β 0 values of β 0 for different Examine the set of values for which H 0 could not be rejected. Inverting the AR test: see Dufour and Taamouti (2005).

32 Inverting the Conditional test: see Mikusheva (2005) only available for 1 endogenous regressor. the CI based on conditional test is more efficient than that based on AR. Extensions: More than 1 endogenous regressor. This literature is still very incomplete Kleiberger (2007) provides an extension of the AR test when the interest in testing a joint hypotheses on β.

33 Partially Robust Estimators Estimation under weak instruments is much harder than testing or confidence intervals Estimation must be divorced from confidence intervals (ie., use robust methods!). k-class estimators 2SLS: k = 1 ˆβ = [X (I k M Z X) 1[X (I k M Z )y] LIML: k = k liml (smallest root of some matrix A) 2SLS: k = kliml H, (where H is a function of exogenous regressors)

34 Under strong instruments, LIML, 2SLS and Fuller will be similar Under weak instruments, 2SLS has greater bias and larger MSE LIML has the advantage of minimizing the AR statistic thus, will be always contained in the AR (and CLR) confidence set. These properties make LIML be a reasonable good choice as an alternative to 2SLS

35 Wrapping up 1. Always test formally for weak instruments (but be aware from the limitations of the existing theory) 2. Divorce estimation and testing (i.e., it s not enough to test the significance of β using the standard errors of the estimators.) 3. Conduct hypothesis testing using the conditional likelihood ratio (CLR) test or its robust variants. 4. Build confidence intervals based on CLR.

IV Estimation and its Limitations: Weak Instruments and Weakly Endogeneous Regressors

IV Estimation and its Limitations: Weak Instruments and Weakly Endogeneous Regressors Laura Mayoral IAE, Barcelona GSE and University of Gothenburg Gothenburg, May 2015 Roadmap of the course Introduction.

IV Estimation and its Limitations: Weak Instruments and Weakly Endogeneous Regressors Laura Mayoral IAE, Barcelona GSE and University of Gothenburg Gothenburg, May 2015 Roadmap of the course Introduction.

IV Estimation and its Limitations: Weak Instruments and Weakly Endogeneous Regressors

IV Estimation and its Limitations: Weak Instruments and Weakly Endogeneous Regressors Laura Mayoral IAE, Barcelona GSE and University of Gothenburg Gothenburg, May 2015 Roadmap Deviations from the standard

IV Estimation and its Limitations: Weak Instruments and Weakly Endogeneous Regressors Laura Mayoral IAE, Barcelona GSE and University of Gothenburg Gothenburg, May 2015 Roadmap Deviations from the standard

Lecture 11 Weak IV. Econ 715

Lecture 11 Weak IV Instrument exogeneity and instrument relevance are two crucial requirements in empirical analysis using GMM. It now appears that in many applications of GMM and IV regressions, instruments

Lecture 11 Weak IV Instrument exogeneity and instrument relevance are two crucial requirements in empirical analysis using GMM. It now appears that in many applications of GMM and IV regressions, instruments

Instrumental Variables Estimation in Stata

Christopher F Baum 1 Faculty Micro Resource Center Boston College March 2007 1 Thanks to Austin Nichols for the use of his material on weak instruments and Mark Schaffer for helpful comments. The standard

Christopher F Baum 1 Faculty Micro Resource Center Boston College March 2007 1 Thanks to Austin Nichols for the use of his material on weak instruments and Mark Schaffer for helpful comments. The standard

A Robust Test for Weak Instruments in Stata

A Robust Test for Weak Instruments in Stata José Luis Montiel Olea, Carolin Pflueger, and Su Wang 1 First draft: July 2013 This draft: November 2013 Abstract We introduce and describe a Stata routine ivrobust

A Robust Test for Weak Instruments in Stata José Luis Montiel Olea, Carolin Pflueger, and Su Wang 1 First draft: July 2013 This draft: November 2013 Abstract We introduce and describe a Stata routine ivrobust

What s New in Econometrics. Lecture 13

What s New in Econometrics Lecture 13 Weak Instruments and Many Instruments Guido Imbens NBER Summer Institute, 2007 Outline 1. Introduction 2. Motivation 3. Weak Instruments 4. Many Weak) Instruments

What s New in Econometrics Lecture 13 Weak Instruments and Many Instruments Guido Imbens NBER Summer Institute, 2007 Outline 1. Introduction 2. Motivation 3. Weak Instruments 4. Many Weak) Instruments

IV and IV-GMM. Christopher F Baum. EC 823: Applied Econometrics. Boston College, Spring 2014

IV and IV-GMM Christopher F Baum EC 823: Applied Econometrics Boston College, Spring 2014 Christopher F Baum (BC / DIW) IV and IV-GMM Boston College, Spring 2014 1 / 1 Instrumental variables estimators

IV and IV-GMM Christopher F Baum EC 823: Applied Econometrics Boston College, Spring 2014 Christopher F Baum (BC / DIW) IV and IV-GMM Boston College, Spring 2014 1 / 1 Instrumental variables estimators

Weak Instruments in IV Regression: Theory and Practice

Weak Instruments in IV Regression: Theory and Practice Isaiah Andrews, James Stock, and Liyang Sun November 20, 2018 Abstract When instruments are weakly correlated with endogenous regressors, conventional

Weak Instruments in IV Regression: Theory and Practice Isaiah Andrews, James Stock, and Liyang Sun November 20, 2018 Abstract When instruments are weakly correlated with endogenous regressors, conventional

Instrumental Variables Regression, GMM, and Weak Instruments in Time Series

009 Granger Lecture Granger Center for Time Series The University of Nottingham Instrumental Variables Regression, GMM, and Weak Instruments in Time Series James H. Stock Department of Economics Harvard

009 Granger Lecture Granger Center for Time Series The University of Nottingham Instrumental Variables Regression, GMM, and Weak Instruments in Time Series James H. Stock Department of Economics Harvard

Imbens/Wooldridge, Lecture Notes 13, Summer 07 1

Imbens/Wooldridge, Lecture Notes 13, Summer 07 1 What s New in Econometrics NBER, Summer 2007 Lecture 13, Wednesday, Aug 1st, 2.00-3.00pm Weak Instruments and Many Instruments 1. Introduction In recent

Imbens/Wooldridge, Lecture Notes 13, Summer 07 1 What s New in Econometrics NBER, Summer 2007 Lecture 13, Wednesday, Aug 1st, 2.00-3.00pm Weak Instruments and Many Instruments 1. Introduction In recent

Robust Two Step Confidence Sets, and the Trouble with the First Stage F Statistic

Robust Two Step Confidence Sets, and the Trouble with the First Stage F Statistic Isaiah Andrews Discussion by Bruce Hansen September 27, 2014 Discussion (Bruce Hansen) Robust Confidence Sets Sept 27,

Robust Two Step Confidence Sets, and the Trouble with the First Stage F Statistic Isaiah Andrews Discussion by Bruce Hansen September 27, 2014 Discussion (Bruce Hansen) Robust Confidence Sets Sept 27,

1 Procedures robust to weak instruments

Comment on Weak instrument robust tests in GMM and the new Keynesian Phillips curve By Anna Mikusheva We are witnessing a growing awareness among applied researchers about the possibility of having weak

Comment on Weak instrument robust tests in GMM and the new Keynesian Phillips curve By Anna Mikusheva We are witnessing a growing awareness among applied researchers about the possibility of having weak

Likelihood Ratio Based Test for the Exogeneity and the Relevance of Instrumental Variables

Likelihood Ratio Based est for the Exogeneity and the Relevance of Instrumental Variables Dukpa Kim y Yoonseok Lee z September [under revision] Abstract his paper develops a test for the exogeneity and

Likelihood Ratio Based est for the Exogeneity and the Relevance of Instrumental Variables Dukpa Kim y Yoonseok Lee z September [under revision] Abstract his paper develops a test for the exogeneity and

Econometrics. Week 8. Fall Institute of Economic Studies Faculty of Social Sciences Charles University in Prague

Econometrics Week 8 Institute of Economic Studies Faculty of Social Sciences Charles University in Prague Fall 2012 1 / 25 Recommended Reading For the today Instrumental Variables Estimation and Two Stage

Econometrics Week 8 Institute of Economic Studies Faculty of Social Sciences Charles University in Prague Fall 2012 1 / 25 Recommended Reading For the today Instrumental Variables Estimation and Two Stage

Reply to Manovskii s Discussion on The Limited Macroeconomic Effects of Unemployment Benefit Extensions

Reply to Manovskii s Discussion on The Limited Macroeconomic Effects of Unemployment Benefit Extensions Gabriel Chodorow-Reich Harvard University and NBER Loukas Karabarbounis University of Minnesota and

Reply to Manovskii s Discussion on The Limited Macroeconomic Effects of Unemployment Benefit Extensions Gabriel Chodorow-Reich Harvard University and NBER Loukas Karabarbounis University of Minnesota and

Weak Identification & Many Instruments in IV Regression and GMM, Part I

AEA Continuing Education Course Time Series Econometrics Lectures 5 and 6 James H. Stock January 6, 2010 Weak Identification & Many Instruments in IV Regression and GMM, Part I Revised December 21, 2009

AEA Continuing Education Course Time Series Econometrics Lectures 5 and 6 James H. Stock January 6, 2010 Weak Identification & Many Instruments in IV Regression and GMM, Part I Revised December 21, 2009

Inference with Weak Instruments

Inference with Weak Instruments Donald W. K. Andrews 1 Cowles Foundation for Research in Economics Yale University James H. Stock Department of Economics Harvard University March 2005 Revised: September

Inference with Weak Instruments Donald W. K. Andrews 1 Cowles Foundation for Research in Economics Yale University James H. Stock Department of Economics Harvard University March 2005 Revised: September

A CONDITIONAL LIKELIHOOD RATIO TEST FOR STRUCTURAL MODELS. By Marcelo J. Moreira 1

Econometrica, Vol. 71, No. 4 (July, 2003), 1027 1048 A CONDITIONAL LIKELIHOOD RATIO TEST FOR STRUCTURAL MODELS By Marcelo J. Moreira 1 This paper develops a general method for constructing exactly similar

Econometrica, Vol. 71, No. 4 (July, 2003), 1027 1048 A CONDITIONAL LIKELIHOOD RATIO TEST FOR STRUCTURAL MODELS By Marcelo J. Moreira 1 This paper develops a general method for constructing exactly similar

Implementing Conditional Tests with Correct Size in the Simultaneous Equations Model

The Stata Journal (2001) 1, Number 1, pp. 1 15 Implementing Conditional Tests with Correct Size in the Simultaneous Equations Model Marcelo J. Moreira Department of Economics Harvard University Brian P.

The Stata Journal (2001) 1, Number 1, pp. 1 15 Implementing Conditional Tests with Correct Size in the Simultaneous Equations Model Marcelo J. Moreira Department of Economics Harvard University Brian P.

Weak Instruments, Weak Identification, and Many Instruments, Part II

NBER Summer Institute What s New in Econometrics ime Series Lecture 4 July 14, 2008 Weak Instruments, Weak Identification, and Many Instruments, Part II Revised July 22, 2008 4-1 Outline Lecture 3 1) What

NBER Summer Institute What s New in Econometrics ime Series Lecture 4 July 14, 2008 Weak Instruments, Weak Identification, and Many Instruments, Part II Revised July 22, 2008 4-1 Outline Lecture 3 1) What

ROBUST CONFIDENCE SETS IN THE PRESENCE OF WEAK INSTRUMENTS By Anna Mikusheva 1, MIT, Department of Economics. Abstract

ROBUST CONFIDENCE SETS IN THE PRESENCE OF WEAK INSTRUMENTS By Anna Mikusheva 1, MIT, Department of Economics Abstract This paper considers instrumental variable regression with a single endogenous variable

ROBUST CONFIDENCE SETS IN THE PRESENCE OF WEAK INSTRUMENTS By Anna Mikusheva 1, MIT, Department of Economics Abstract This paper considers instrumental variable regression with a single endogenous variable

Regression. Saraswata Chaudhuri, Thomas Richardson, James Robins and Eric Zivot. Working Paper no. 73. Center for Statistics and the Social Sciences

Split-Sample Score Tests in Linear Instrumental Variables Regression Saraswata Chaudhuri, Thomas Richardson, James Robins and Eric Zivot Working Paper no. 73 Center for Statistics and the Social Sciences

Split-Sample Score Tests in Linear Instrumental Variables Regression Saraswata Chaudhuri, Thomas Richardson, James Robins and Eric Zivot Working Paper no. 73 Center for Statistics and the Social Sciences

Split-Sample Score Tests in Linear Instrumental Variables Regression

Split-Sample Score Tests in Linear Instrumental Variables Regression Saraswata Chaudhuri, Thomas Richardson, James Robins and Eric Zivot Working Paper no. 73 Center for Statistics and the Social Sciences

Split-Sample Score Tests in Linear Instrumental Variables Regression Saraswata Chaudhuri, Thomas Richardson, James Robins and Eric Zivot Working Paper no. 73 Center for Statistics and the Social Sciences

Asymptotic Distributions of Instrumental Variables Statistics with Many Instruments

CHAPTER 6 Asymptotic Distributions of Instrumental Variables Statistics with Many Instruments James H. Stock and Motohiro Yogo ABSTRACT This paper extends Staiger and Stock s (1997) weak instrument asymptotic

CHAPTER 6 Asymptotic Distributions of Instrumental Variables Statistics with Many Instruments James H. Stock and Motohiro Yogo ABSTRACT This paper extends Staiger and Stock s (1997) weak instrument asymptotic

Weak Instruments and the First-Stage Robust F-statistic in an IV regression with heteroskedastic errors

Weak Instruments and the First-Stage Robust F-statistic in an IV regression with heteroskedastic errors Uijin Kim u.kim@bristol.ac.uk Department of Economics, University of Bristol January 2016. Preliminary,

Weak Instruments and the First-Stage Robust F-statistic in an IV regression with heteroskedastic errors Uijin Kim u.kim@bristol.ac.uk Department of Economics, University of Bristol January 2016. Preliminary,

ROBUST CONFIDENCE SETS IN THE PRESENCE OF WEAK INSTRUMENTS By Anna Mikusheva 1, MIT, Department of Economics. Abstract

ROBUST CONFIDENCE SETS IN THE PRESENCE OF WEAK INSTRUMENTS By Anna Mikusheva 1, MIT, Department of Economics Abstract This paper considers instrumental variable regression with a single endogenous variable

ROBUST CONFIDENCE SETS IN THE PRESENCE OF WEAK INSTRUMENTS By Anna Mikusheva 1, MIT, Department of Economics Abstract This paper considers instrumental variable regression with a single endogenous variable

ECON Introductory Econometrics. Lecture 16: Instrumental variables

ECON4150 - Introductory Econometrics Lecture 16: Instrumental variables Monique de Haan (moniqued@econ.uio.no) Stock and Watson Chapter 12 Lecture outline 2 OLS assumptions and when they are violated Instrumental

ECON4150 - Introductory Econometrics Lecture 16: Instrumental variables Monique de Haan (moniqued@econ.uio.no) Stock and Watson Chapter 12 Lecture outline 2 OLS assumptions and when they are violated Instrumental

A more powerful subvector Anderson Rubin test in linear instrumental variables regression

A more powerful subvector Anderson Rubin test in linear instrumental variables regression Patrik Guggenberger Department of Economics Pennsylvania State University Frank Kleibergen Department of Quantitative

A more powerful subvector Anderson Rubin test in linear instrumental variables regression Patrik Guggenberger Department of Economics Pennsylvania State University Frank Kleibergen Department of Quantitative

Quantitative Methods Final Exam (2017/1)

") Quantitative Methods Final Exam (2017/1) 1. Please write down your name and student ID number. 2. Calculator is allowed during the exam, but DO NOT use a smartphone. 3. List your answers (together with

Quantitative Methods Final Exam (2017/1) 1. Please write down your name and student ID number. 2. Calculator is allowed during the exam, but DO NOT use a smartphone. 3. List your answers (together with

Just How Sensitive are Instrumental Variable Estimates?

Foundations and Trends R in Accounting Just How Sensitive are Instrumental Variable Estimates? Suggested Citation: Peter C. Reiss (2016), Just How Sensitive are Instrumental Variable Estimates?, Foundations

Foundations and Trends R in Accounting Just How Sensitive are Instrumental Variable Estimates? Suggested Citation: Peter C. Reiss (2016), Just How Sensitive are Instrumental Variable Estimates?, Foundations

1 Motivation for Instrumental Variable (IV) Regression

Regression") ECON 370: IV & 2SLS 1 Instrumental Variables Estimation and Two Stage Least Squares Econometric Methods, ECON 370 Let s get back to the thiking in terms of cross sectional (or pooled cross sectional) data

ECON 370: IV & 2SLS 1 Instrumental Variables Estimation and Two Stage Least Squares Econometric Methods, ECON 370 Let s get back to the thiking in terms of cross sectional (or pooled cross sectional) data

Location Properties of Point Estimators in Linear Instrumental Variables and Related Models

Location Properties of Point Estimators in Linear Instrumental Variables and Related Models Keisuke Hirano Department of Economics University of Arizona hirano@u.arizona.edu Jack R. Porter Department of

Location Properties of Point Estimators in Linear Instrumental Variables and Related Models Keisuke Hirano Department of Economics University of Arizona hirano@u.arizona.edu Jack R. Porter Department of

Applied Econometrics (MSc.) Lecture 3 Instrumental Variables

Lecture 3 Instrumental Variables") Applied Econometrics (MSc.) Lecture 3 Instrumental Variables Estimation - Theory Department of Economics University of Gothenburg December 4, 2014 1/28 Why IV estimation? So far, in OLS, we assumed independence.

Applied Econometrics (MSc.) Lecture 3 Instrumental Variables Estimation - Theory Department of Economics University of Gothenburg December 4, 2014 1/28 Why IV estimation? So far, in OLS, we assumed independence.

The Exact Distribution of the t-ratio with Robust and Clustered Standard Errors

The Exact Distribution of the t-ratio with Robust and Clustered Standard Errors by Bruce E. Hansen Department of Economics University of Wisconsin October 2018 Bruce Hansen (University of Wisconsin) Exact

The Exact Distribution of the t-ratio with Robust and Clustered Standard Errors by Bruce E. Hansen Department of Economics University of Wisconsin October 2018 Bruce Hansen (University of Wisconsin) Exact

Testing for Weak Instruments in Linear IV Regression

Testing for Weak Instruments in Linear IV Regression August 001 James H. Stock Kennedy School of Government, Harvard University and the National Bureau of Economic Research and Motohiro Yogo* Department

Testing for Weak Instruments in Linear IV Regression August 001 James H. Stock Kennedy School of Government, Harvard University and the National Bureau of Economic Research and Motohiro Yogo* Department

Implementing weak-instrument robust tests for a general class of instrumental-variables models

The Stata Journal (2009) 9, Number 3, pp. 398 421 Implementing weak-instrument robust tests for a general class of instrumental-variables models Keith Finlay Tulane University New Orleans, LA kfinlay@tulane.edu

The Stata Journal (2009) 9, Number 3, pp. 398 421 Implementing weak-instrument robust tests for a general class of instrumental-variables models Keith Finlay Tulane University New Orleans, LA kfinlay@tulane.edu

OPTIMAL TWO-SIDED INVARIANT SIMILAR TESTS FOR INSTRUMENTAL VARIABLES REGRESSION DONALD W. K. ANDREWS, MARCELO J. MOREIRA AND JAMES H.

OPTIMAL TWO-SIDED INVARIANT SIMILAR TESTS FOR INSTRUMENTAL VARIABLES REGRESSION BY DONALD W. K. ANDREWS, MARCELO J. MOREIRA AND JAMES H. STOCK COWLES FOUNDATION PAPER NO. 1168 COWLES FOUNDATION FOR RESEARCH

OPTIMAL TWO-SIDED INVARIANT SIMILAR TESTS FOR INSTRUMENTAL VARIABLES REGRESSION BY DONALD W. K. ANDREWS, MARCELO J. MOREIRA AND JAMES H. STOCK COWLES FOUNDATION PAPER NO. 1168 COWLES FOUNDATION FOR RESEARCH

Econometrics II. Lecture 4: Instrumental Variables Part I

Econometrics II Lecture 4: Instrumental Variables Part I Måns Söderbom 12 April 2011 mans.soderbom@economics.gu.se. www.economics.gu.se/soderbom. www.soderbom.net 1. Introduction Recall from lecture 3

Econometrics II Lecture 4: Instrumental Variables Part I Måns Söderbom 12 April 2011 mans.soderbom@economics.gu.se. www.economics.gu.se/soderbom. www.soderbom.net 1. Introduction Recall from lecture 3

Conditional Linear Combination Tests for Weakly Identified Models

Conditional Linear Combination Tests for Weakly Identified Models Isaiah Andrews JOB MARKET PAPER Abstract This paper constructs powerful tests applicable in a wide range of weakly identified contexts,

Conditional Linear Combination Tests for Weakly Identified Models Isaiah Andrews JOB MARKET PAPER Abstract This paper constructs powerful tests applicable in a wide range of weakly identified contexts,

Consistency without Inference: Instrumental Variables in Practical Application *

Consistency without Inference: Instrumental Variables in Practical Application * Alwyn Young London School of Economics This draft: September 07 Abstract I use the bootstrap to study a comprehensive sample

Consistency without Inference: Instrumental Variables in Practical Application * Alwyn Young London School of Economics This draft: September 07 Abstract I use the bootstrap to study a comprehensive sample

Warwick Economics Summer School Topics in Microeconometrics Instrumental Variables Estimation

Warwick Economics Summer School Topics in Microeconometrics Instrumental Variables Estimation Michele Aquaro University of Warwick This version: July 21, 2016 1 / 31 Reading material Textbook: Introductory

Warwick Economics Summer School Topics in Microeconometrics Instrumental Variables Estimation Michele Aquaro University of Warwick This version: July 21, 2016 1 / 31 Reading material Textbook: Introductory

Wooldridge, Introductory Econometrics, 4th ed. Chapter 15: Instrumental variables and two stage least squares

Wooldridge, Introductory Econometrics, 4th ed. Chapter 15: Instrumental variables and two stage least squares Many economic models involve endogeneity: that is, a theoretical relationship does not fit

Wooldridge, Introductory Econometrics, 4th ed. Chapter 15: Instrumental variables and two stage least squares Many economic models involve endogeneity: that is, a theoretical relationship does not fit

GMM, Weak Instruments, and Weak Identification

GMM, Weak Instruments, and Weak Identification James H. Stock Kennedy School of Government, Harvard University and the National Bureau of Economic Research Jonathan Wright Federal Reserve Board, Washington,

GMM, Weak Instruments, and Weak Identification James H. Stock Kennedy School of Government, Harvard University and the National Bureau of Economic Research Jonathan Wright Federal Reserve Board, Washington,

LECTURE 10: MORE ON RANDOM PROCESSES

LECTURE 10: MORE ON RANDOM PROCESSES AND SERIAL CORRELATION 2 Classification of random processes (cont d) stationary vs. non-stationary processes stationary = distribution does not change over time more

LECTURE 10: MORE ON RANDOM PROCESSES AND SERIAL CORRELATION 2 Classification of random processes (cont d) stationary vs. non-stationary processes stationary = distribution does not change over time more

Graduate Econometrics Lecture 4: Heteroskedasticity

Graduate Econometrics Lecture 4: Heteroskedasticity Department of Economics University of Gothenburg November 30, 2014 1/43 and Autocorrelation Consequences for OLS Estimator Begin from the linear model

Graduate Econometrics Lecture 4: Heteroskedasticity Department of Economics University of Gothenburg November 30, 2014 1/43 and Autocorrelation Consequences for OLS Estimator Begin from the linear model

Recent Advances in the Field of Trade Theory and Policy Analysis Using Micro-Level Data

Recent Advances in the Field of Trade Theory and Policy Analysis Using Micro-Level Data July 2012 Bangkok, Thailand Cosimo Beverelli (World Trade Organization) 1 Content a) Endogeneity b) Instrumental

Recent Advances in the Field of Trade Theory and Policy Analysis Using Micro-Level Data July 2012 Bangkok, Thailand Cosimo Beverelli (World Trade Organization) 1 Content a) Endogeneity b) Instrumental

Testing the New Keynesian Phillips Curve without assuming. identification

Testing the New Keynesian Phillips Curve without assuming identification Sophocles Mavroeidis Brown University sophocles mavroeidis@brown.edu First version: 15 April 2006 This version March 12, 2007 Abstract

Testing the New Keynesian Phillips Curve without assuming identification Sophocles Mavroeidis Brown University sophocles mavroeidis@brown.edu First version: 15 April 2006 This version March 12, 2007 Abstract

Likelihood Ratio based Joint Test for the Exogeneity and. the Relevance of Instrumental Variables

Likelihood Ratio based Joint Test for the Exogeneity and the Relevance of Instrumental Variables Dukpa Kim Yoonseok Lee March 12, 2009 Abstract This paper develops a joint test for the exogeneity and the

Likelihood Ratio based Joint Test for the Exogeneity and the Relevance of Instrumental Variables Dukpa Kim Yoonseok Lee March 12, 2009 Abstract This paper develops a joint test for the exogeneity and the

Instrumental Variables and the Problem of Endogeneity

Instrumental Variables and the Problem of Endogeneity September 15, 2015 1 / 38 Exogeneity: Important Assumption of OLS In a standard OLS framework, y = xβ + ɛ (1) and for unbiasedness we need E[x ɛ] =

Instrumental Variables and the Problem of Endogeneity September 15, 2015 1 / 38 Exogeneity: Important Assumption of OLS In a standard OLS framework, y = xβ + ɛ (1) and for unbiasedness we need E[x ɛ] =

Approximate Distributions of the Likelihood Ratio Statistic in a Structural Equation with Many Instruments

CIRJE-F-466 Approximate Distributions of the Likelihood Ratio Statistic in a Structural Equation with Many Instruments Yukitoshi Matsushita CIRJE, Faculty of Economics, University of Tokyo February 2007

CIRJE-F-466 Approximate Distributions of the Likelihood Ratio Statistic in a Structural Equation with Many Instruments Yukitoshi Matsushita CIRJE, Faculty of Economics, University of Tokyo February 2007

8. Instrumental variables regression

8. Instrumental variables regression Recall: In Section 5 we analyzed five sources of estimation bias arising because the regressor is correlated with the error term Violation of the first OLS assumption

8. Instrumental variables regression Recall: In Section 5 we analyzed five sources of estimation bias arising because the regressor is correlated with the error term Violation of the first OLS assumption

Instrumental Variables

Instrumental Variables Kosuke Imai Harvard University STAT186/GOV2002 CAUSAL INFERENCE Fall 2018 Kosuke Imai (Harvard) Noncompliance in Experiments Stat186/Gov2002 Fall 2018 1 / 18 Instrumental Variables

Instrumental Variables Kosuke Imai Harvard University STAT186/GOV2002 CAUSAL INFERENCE Fall 2018 Kosuke Imai (Harvard) Noncompliance in Experiments Stat186/Gov2002 Fall 2018 1 / 18 Instrumental Variables

Improved Inference in Weakly Identified Instrumental Variables Regression

Improved Inference in Weakly Identified Instrumental Variables Regression Richard Startz, Eric Zivot and Charles R. Nelson Department of Economics, University of Washington December 9, 2002 This version:

Improved Inference in Weakly Identified Instrumental Variables Regression Richard Startz, Eric Zivot and Charles R. Nelson Department of Economics, University of Washington December 9, 2002 This version:

LECTURE 5 HYPOTHESIS TESTING

October 25, 2016 LECTURE 5 HYPOTHESIS TESTING Basic concepts In this lecture we continue to discuss the normal classical linear regression defined by Assumptions A1-A5. Let θ Θ R d be a parameter of interest.

October 25, 2016 LECTURE 5 HYPOTHESIS TESTING Basic concepts In this lecture we continue to discuss the normal classical linear regression defined by Assumptions A1-A5. Let θ Θ R d be a parameter of interest.

Comments on Weak instrument robust tests in GMM and the new Keynesian Phillips curve by F. Kleibergen and S. Mavroeidis

Comments on Weak instrument robust tests in GMM and the new Keynesian Phillips curve by F. Kleibergen and S. Mavroeidis Jean-Marie Dufour First version: August 2008 Revised: September 2008 This version:

Comments on Weak instrument robust tests in GMM and the new Keynesian Phillips curve by F. Kleibergen and S. Mavroeidis Jean-Marie Dufour First version: August 2008 Revised: September 2008 This version:

Review of Econometrics

Review of Econometrics Zheng Tian June 5th, 2017 1 The Essence of the OLS Estimation Multiple regression model involves the models as follows Y i = β 0 + β 1 X 1i + β 2 X 2i + + β k X ki + u i, i = 1,...,

Review of Econometrics Zheng Tian June 5th, 2017 1 The Essence of the OLS Estimation Multiple regression model involves the models as follows Y i = β 0 + β 1 X 1i + β 2 X 2i + + β k X ki + u i, i = 1,...,

Alternative Graphical Representations of the Confidence Intervals for the Structural Coefficient from Exactly Identified Two-Stage Least Squares.

Alternative Graphical Representations of the Confidence Intervals for the Structural Coefficient from Exactly Identified wo-stage Least Squares. Joe Hirschberg &Jenny Lye Economics, University of Melbourne,

Alternative Graphical Representations of the Confidence Intervals for the Structural Coefficient from Exactly Identified wo-stage Least Squares. Joe Hirschberg &Jenny Lye Economics, University of Melbourne,

Spatial Regression. 9. Specification Tests (1) Luc Anselin. Copyright 2017 by Luc Anselin, All Rights Reserved

Luc Anselin. Copyright 2017 by Luc Anselin, All Rights Reserved") Spatial Regression 9. Specification Tests (1) Luc Anselin http://spatial.uchicago.edu 1 basic concepts types of tests Moran s I classic ML-based tests LM tests 2 Basic Concepts 3 The Logic of Specification

Spatial Regression 9. Specification Tests (1) Luc Anselin http://spatial.uchicago.edu 1 basic concepts types of tests Moran s I classic ML-based tests LM tests 2 Basic Concepts 3 The Logic of Specification

Economics 308: Econometrics Professor Moody

Economics 308: Econometrics Professor Moody References on reserve: Text Moody, Basic Econometrics with Stata (BES) Pindyck and Rubinfeld, Econometric Models and Economic Forecasts (PR) Wooldridge, Jeffrey

Economics 308: Econometrics Professor Moody References on reserve: Text Moody, Basic Econometrics with Stata (BES) Pindyck and Rubinfeld, Econometric Models and Economic Forecasts (PR) Wooldridge, Jeffrey

Bootstrap Tests for Overidentification in Linear Regression Models

Bootstrap Tests for Overidentification in Linear Regression Models Department of Economics and CIREQ McGill University Montréal, Québec, Canada H3A 2T7 Russell Davidson russelldavidson@mcgillca and James

Bootstrap Tests for Overidentification in Linear Regression Models Department of Economics and CIREQ McGill University Montréal, Québec, Canada H3A 2T7 Russell Davidson russelldavidson@mcgillca and James

Chapter 6. Panel Data. Joan Llull. Quantitative Statistical Methods II Barcelona GSE

Chapter 6. Panel Data Joan Llull Quantitative Statistical Methods II Barcelona GSE Introduction Chapter 6. Panel Data 2 Panel data The term panel data refers to data sets with repeated observations over

Chapter 6. Panel Data Joan Llull Quantitative Statistical Methods II Barcelona GSE Introduction Chapter 6. Panel Data 2 Panel data The term panel data refers to data sets with repeated observations over

A more powerful subvector Anderson and Rubin test in linear instrumental variables regression. Patrik Guggenberger Pennsylvania State University

A more powerful subvector Anderson and Rubin test in linear instrumental variables regression Patrik Guggenberger Pennsylvania State University Joint work with Frank Kleibergen (University of Amsterdam)

A more powerful subvector Anderson and Rubin test in linear instrumental variables regression Patrik Guggenberger Pennsylvania State University Joint work with Frank Kleibergen (University of Amsterdam)

Regression with a Single Regressor: Hypothesis Tests and Confidence Intervals

Regression with a Single Regressor: Hypothesis Tests and Confidence Intervals (SW Chapter 5) Outline. The standard error of ˆ. Hypothesis tests concerning β 3. Confidence intervals for β 4. Regression

Regression with a Single Regressor: Hypothesis Tests and Confidence Intervals (SW Chapter 5) Outline. The standard error of ˆ. Hypothesis tests concerning β 3. Confidence intervals for β 4. Regression

Online-Only Appendix to Blunt Instruments: Avoiding Common Pitfalls in Identifying the Causes of Economic Growth

Not for Publication Online-Only Appendix to Blunt Instruments: Avoiding Common Pitfalls in Identifying the Causes of Economic Growth A Testing for underidentification and weak instruments We provide here

Not for Publication Online-Only Appendix to Blunt Instruments: Avoiding Common Pitfalls in Identifying the Causes of Economic Growth A Testing for underidentification and weak instruments We provide here

A more powerful subvector Anderson Rubin test in linear instrumental variable regression

A more powerful subvector Anderson Rubin test in linear instrumental variable regression Patrik Guggenberger Department of Economics Pennsylvania State University Frank Kleibergen Department of Quantitative

A more powerful subvector Anderson Rubin test in linear instrumental variable regression Patrik Guggenberger Department of Economics Pennsylvania State University Frank Kleibergen Department of Quantitative

A more powerful subvector Anderson Rubin test in linear instrumental variable regression

A more powerful subvector Anderson Rubin test in linear instrumental variable regression Patrik Guggenberger Department of Economics Pennsylvania State University Frank Kleibergen Department of Quantitative

A more powerful subvector Anderson Rubin test in linear instrumental variable regression Patrik Guggenberger Department of Economics Pennsylvania State University Frank Kleibergen Department of Quantitative

Birkbeck Working Papers in Economics & Finance

ISSN 1745-8587 Birkbeck Working Papers in Economics & Finance Department of Economics, Mathematics and Statistics BWPEF 1809 A Note on Specification Testing in Some Structural Regression Models Walter

ISSN 1745-8587 Birkbeck Working Papers in Economics & Finance Department of Economics, Mathematics and Statistics BWPEF 1809 A Note on Specification Testing in Some Structural Regression Models Walter

Identification of the New Keynesian Phillips Curve: Problems and Consequences

MACROECONOMIC POLICY WORKSHOP: CENTRAL BANK OF CHILE The Relevance of the New Keynesian Phillips Curve Identification of the New Keynesian Phillips Curve: Problems and Consequences James. H. Stock Harvard

MACROECONOMIC POLICY WORKSHOP: CENTRAL BANK OF CHILE The Relevance of the New Keynesian Phillips Curve Identification of the New Keynesian Phillips Curve: Problems and Consequences James. H. Stock Harvard

Lecture 8: Instrumental Variables Estimation

Lecture Notes on Advanced Econometrics Lecture 8: Instrumental Variables Estimation Endogenous Variables Consider a population model: y α y + β + β x + β x +... + β x + u i i i i k ik i Takashi Yamano

Lecture Notes on Advanced Econometrics Lecture 8: Instrumental Variables Estimation Endogenous Variables Consider a population model: y α y + β + β x + β x +... + β x + u i i i i k ik i Takashi Yamano

Chapter 7. Hypothesis Tests and Confidence Intervals in Multiple Regression

Chapter 7 Hypothesis Tests and Confidence Intervals in Multiple Regression Outline 1. Hypothesis tests and confidence intervals for a single coefficie. Joint hypothesis tests on multiple coefficients 3.

Chapter 7 Hypothesis Tests and Confidence Intervals in Multiple Regression Outline 1. Hypothesis tests and confidence intervals for a single coefficie. Joint hypothesis tests on multiple coefficients 3.

Econometrics Summary Algebraic and Statistical Preliminaries

Econometrics Summary Algebraic and Statistical Preliminaries Elasticity: The point elasticity of Y with respect to L is given by α = ( Y/ L)/(Y/L). The arc elasticity is given by ( Y/ L)/(Y/L), when L

Econometrics Summary Algebraic and Statistical Preliminaries Elasticity: The point elasticity of Y with respect to L is given by α = ( Y/ L)/(Y/L). The arc elasticity is given by ( Y/ L)/(Y/L), when L

Unbiased Instrumental Variables Estimation Under Known First-Stage Sign

Unbiased Instrumental Variables Estimation Under Known First-Stage Sign Isaiah Andrews Harvard Society of Fellows Timothy B. Armstrong Yale University April 9, 2016 Abstract We derive mean-unbiased estimators

Unbiased Instrumental Variables Estimation Under Known First-Stage Sign Isaiah Andrews Harvard Society of Fellows Timothy B. Armstrong Yale University April 9, 2016 Abstract We derive mean-unbiased estimators

Exogeneity tests and weak identification

Cireq, Cirano, Départ. Sc. Economiques Université de Montréal Jean-Marie Dufour Cireq, Cirano, William Dow Professor of Economics Department of Economics Mcgill University June 20, 2008 Main Contributions

Cireq, Cirano, Départ. Sc. Economiques Université de Montréal Jean-Marie Dufour Cireq, Cirano, William Dow Professor of Economics Department of Economics Mcgill University June 20, 2008 Main Contributions

Increasing the Power of Specification Tests. November 18, 2018

Increasing the Power of Specification Tests T W J A. H U A MIT November 18, 2018 A. This paper shows how to increase the power of Hausman s (1978) specification test as well as the difference test in a

Increasing the Power of Specification Tests T W J A. H U A MIT November 18, 2018 A. This paper shows how to increase the power of Hausman s (1978) specification test as well as the difference test in a

Simultaneous Equation Models Learning Objectives Introduction Introduction (2) Introduction (3) Solving the Model structural equations

Introduction (3) Solving the Model structural equations") Simultaneous Equation Models. Introduction: basic definitions 2. Consequences of ignoring simultaneity 3. The identification problem 4. Estimation of simultaneous equation models 5. Example: IS LM model

Simultaneous Equation Models. Introduction: basic definitions 2. Consequences of ignoring simultaneity 3. The identification problem 4. Estimation of simultaneous equation models 5. Example: IS LM model

A Practitioner s Guide to Cluster-Robust Inference

A Practitioner s Guide to Cluster-Robust Inference A. C. Cameron and D. L. Miller presented by Federico Curci March 4, 2015 Cameron Miller Cluster Clinic II March 4, 2015 1 / 20 In the previous episode

A Practitioner s Guide to Cluster-Robust Inference A. C. Cameron and D. L. Miller presented by Federico Curci March 4, 2015 Cameron Miller Cluster Clinic II March 4, 2015 1 / 20 In the previous episode

Instrumental Variables Estimation and Weak-Identification-Robust. Inference Based on a Conditional Quantile Restriction

Instrumental Variables Estimation and Weak-Identification-Robust Inference Based on a Conditional Quantile Restriction Vadim Marmer Department of Economics University of British Columbia vadim.marmer@gmail.com

Instrumental Variables Estimation and Weak-Identification-Robust Inference Based on a Conditional Quantile Restriction Vadim Marmer Department of Economics University of British Columbia vadim.marmer@gmail.com

Performance of conditional Wald tests in IV regression with weak instruments

Journal of Econometrics 139 (2007) 116 132 www.elsevier.com/locate/jeconom Performance of conditional Wald tests in IV regression with weak instruments Donald W.K. Andrews a, Marcelo J. Moreira b, James

Journal of Econometrics 139 (2007) 116 132 www.elsevier.com/locate/jeconom Performance of conditional Wald tests in IV regression with weak instruments Donald W.K. Andrews a, Marcelo J. Moreira b, James

Instrumental Variables and GMM: Estimation and Testing. Steven Stillman, New Zealand Department of Labour

Instrumental Variables and GMM: Estimation and Testing Christopher F Baum, Boston College Mark E. Schaffer, Heriot Watt University Steven Stillman, New Zealand Department of Labour March 2003 Stata Journal,

Instrumental Variables and GMM: Estimation and Testing Christopher F Baum, Boston College Mark E. Schaffer, Heriot Watt University Steven Stillman, New Zealand Department of Labour March 2003 Stata Journal,

Instrument endogeneity, weak identification, and inference in IV regressions

Instrument endogeneity, weak identification, and inference in IV regressions Firmin Doko Tchatoka The University of Adelaide August 18, 14 School of Economics, The University of Adelaide, 1 Pulteney Street,

Instrument endogeneity, weak identification, and inference in IV regressions Firmin Doko Tchatoka The University of Adelaide August 18, 14 School of Economics, The University of Adelaide, 1 Pulteney Street,

Econometrics. Week 4. Fall Institute of Economic Studies Faculty of Social Sciences Charles University in Prague

Econometrics Week 4 Institute of Economic Studies Faculty of Social Sciences Charles University in Prague Fall 2012 1 / 23 Recommended Reading For the today Serial correlation and heteroskedasticity in

Econometrics Week 4 Institute of Economic Studies Faculty of Social Sciences Charles University in Prague Fall 2012 1 / 23 Recommended Reading For the today Serial correlation and heteroskedasticity in

Applied Statistics and Econometrics

Applied Statistics and Econometrics Lecture 6 Saul Lach September 2017 Saul Lach () Applied Statistics and Econometrics September 2017 1 / 53 Outline of Lecture 6 1 Omitted variable bias (SW 6.1) 2 Multiple

Applied Statistics and Econometrics Lecture 6 Saul Lach September 2017 Saul Lach () Applied Statistics and Econometrics September 2017 1 / 53 Outline of Lecture 6 1 Omitted variable bias (SW 6.1) 2 Multiple

Econometrics Honor s Exam Review Session. Spring 2012 Eunice Han

Econometrics Honor s Exam Review Session Spring 2012 Eunice Han Topics 1. OLS The Assumptions Omitted Variable Bias Conditional Mean Independence Hypothesis Testing and Confidence Intervals Homoskedasticity

Econometrics Honor s Exam Review Session Spring 2012 Eunice Han Topics 1. OLS The Assumptions Omitted Variable Bias Conditional Mean Independence Hypothesis Testing and Confidence Intervals Homoskedasticity

Spatial Regression. 10. Specification Tests (2) Luc Anselin. Copyright 2017 by Luc Anselin, All Rights Reserved

Luc Anselin. Copyright 2017 by Luc Anselin, All Rights Reserved") Spatial Regression 10. Specification Tests (2) Luc Anselin http://spatial.uchicago.edu 1 robust LM tests higher order tests 2SLS residuals specification search 2 Robust LM Tests 3 Recap and Notation LM-Error

Spatial Regression 10. Specification Tests (2) Luc Anselin http://spatial.uchicago.edu 1 robust LM tests higher order tests 2SLS residuals specification search 2 Robust LM Tests 3 Recap and Notation LM-Error

Recall that a measure of fit is the sum of squared residuals: where. The F-test statistic may be written as:

1 Joint hypotheses The null and alternative hypotheses can usually be interpreted as a restricted model ( ) and an model ( ). In our example: Note that if the model fits significantly better than the restricted

1 Joint hypotheses The null and alternative hypotheses can usually be interpreted as a restricted model ( ) and an model ( ). In our example: Note that if the model fits significantly better than the restricted

Applied Statistics and Econometrics. Giuseppe Ragusa Lecture 15: Instrumental Variables

Applied Statistics and Econometrics Giuseppe Ragusa Lecture 15: Instrumental Variables Outline Introduction Endogeneity and Exogeneity Valid Instruments TSLS Testing Validity 2 Instrumental Variables Regression

Applied Statistics and Econometrics Giuseppe Ragusa Lecture 15: Instrumental Variables Outline Introduction Endogeneity and Exogeneity Valid Instruments TSLS Testing Validity 2 Instrumental Variables Regression

Central Bank of Chile October 29-31, 2013 Bruce Hansen (University of Wisconsin) Structural Breaks October 29-31, / 91. Bruce E.

Structural Breaks October 29-31, / 91. Bruce E.") Forecasting Lecture 3 Structural Breaks Central Bank of Chile October 29-31, 2013 Bruce Hansen (University of Wisconsin) Structural Breaks October 29-31, 2013 1 / 91 Bruce E. Hansen Organization Detection

Forecasting Lecture 3 Structural Breaks Central Bank of Chile October 29-31, 2013 Bruce Hansen (University of Wisconsin) Structural Breaks October 29-31, 2013 1 / 91 Bruce E. Hansen Organization Detection

New Keynesian Phillips Curves, structural econometrics and weak identification

New Keynesian Phillips Curves, structural econometrics and weak identification Jean-Marie Dufour First version: December 2006 This version: December 7, 2006, 8:29pm This work was supported by the Canada

New Keynesian Phillips Curves, structural econometrics and weak identification Jean-Marie Dufour First version: December 2006 This version: December 7, 2006, 8:29pm This work was supported by the Canada

Specification Test for Instrumental Variables Regression with Many Instruments

Specification Test for Instrumental Variables Regression with Many Instruments Yoonseok Lee and Ryo Okui April 009 Preliminary; comments are welcome Abstract This paper considers specification testing

Specification Test for Instrumental Variables Regression with Many Instruments Yoonseok Lee and Ryo Okui April 009 Preliminary; comments are welcome Abstract This paper considers specification testing

ECON Introductory Econometrics. Lecture 5: OLS with One Regressor: Hypothesis Tests

ECON4150 - Introductory Econometrics Lecture 5: OLS with One Regressor: Hypothesis Tests Monique de Haan (moniqued@econ.uio.no) Stock and Watson Chapter 5 Lecture outline 2 Testing Hypotheses about one

ECON4150 - Introductory Econometrics Lecture 5: OLS with One Regressor: Hypothesis Tests Monique de Haan (moniqued@econ.uio.no) Stock and Watson Chapter 5 Lecture outline 2 Testing Hypotheses about one

A Course in Applied Econometrics Lecture 14: Control Functions and Related Methods. Jeff Wooldridge IRP Lectures, UW Madison, August 2008

A Course in Applied Econometrics Lecture 14: Control Functions and Related Methods Jeff Wooldridge IRP Lectures, UW Madison, August 2008 1. Linear-in-Parameters Models: IV versus Control Functions 2. Correlated

A Course in Applied Econometrics Lecture 14: Control Functions and Related Methods Jeff Wooldridge IRP Lectures, UW Madison, August 2008 1. Linear-in-Parameters Models: IV versus Control Functions 2. Correlated

G. S. Maddala Kajal Lahiri. WILEY A John Wiley and Sons, Ltd., Publication

G. S. Maddala Kajal Lahiri WILEY A John Wiley and Sons, Ltd., Publication TEMT Foreword Preface to the Fourth Edition xvii xix Part I Introduction and the Linear Regression Model 1 CHAPTER 1 What is Econometrics?

G. S. Maddala Kajal Lahiri WILEY A John Wiley and Sons, Ltd., Publication TEMT Foreword Preface to the Fourth Edition xvii xix Part I Introduction and the Linear Regression Model 1 CHAPTER 1 What is Econometrics?

Reliability of inference (1 of 2 lectures)

") Reliability of inference (1 of 2 lectures) Ragnar Nymoen University of Oslo 5 March 2013 1 / 19 This lecture (#13 and 14): I The optimality of the OLS estimators and tests depend on the assumptions of

Reliability of inference (1 of 2 lectures) Ragnar Nymoen University of Oslo 5 March 2013 1 / 19 This lecture (#13 and 14): I The optimality of the OLS estimators and tests depend on the assumptions of

Econometrics of Panel Data

Econometrics of Panel Data Jakub Mućk Meeting # 6 Jakub Mućk Econometrics of Panel Data Meeting # 6 1 / 36 Outline 1 The First-Difference (FD) estimator 2 Dynamic panel data models 3 The Anderson and Hsiao

Econometrics of Panel Data Jakub Mućk Meeting # 6 Jakub Mućk Econometrics of Panel Data Meeting # 6 1 / 36 Outline 1 The First-Difference (FD) estimator 2 Dynamic panel data models 3 The Anderson and Hsiao

Selective Instrumental Variable Regression

Selective Instrumental Variable Regression Alberto Abadie, Jiaying Gu and Shu Shen March 1, 2015 Incomplete Draft, Do Not Circulate Abstract In this paper, we propose consistent data-driven selective instrumental

Selective Instrumental Variable Regression Alberto Abadie, Jiaying Gu and Shu Shen March 1, 2015 Incomplete Draft, Do Not Circulate Abstract In this paper, we propose consistent data-driven selective instrumental

Endogeneity. Tom Smith

Endogeneity Tom Smith 1 What is Endogeneity? Classic Problem in Econometrics: More police officers might reduce crime but cities with higher crime rates might demand more police officers. More diffuse

Endogeneity Tom Smith 1 What is Endogeneity? Classic Problem in Econometrics: More police officers might reduce crime but cities with higher crime rates might demand more police officers. More diffuse

A Course in Applied Econometrics Lecture 18: Missing Data. Jeff Wooldridge IRP Lectures, UW Madison, August Linear model with IVs: y i x i u i,

A Course in Applied Econometrics Lecture 18: Missing Data Jeff Wooldridge IRP Lectures, UW Madison, August 2008 1. When Can Missing Data be Ignored? 2. Inverse Probability Weighting 3. Imputation 4. Heckman-Type

A Course in Applied Econometrics Lecture 18: Missing Data Jeff Wooldridge IRP Lectures, UW Madison, August 2008 1. When Can Missing Data be Ignored? 2. Inverse Probability Weighting 3. Imputation 4. Heckman-Type

Lecture: Simultaneous Equation Model (Wooldridge s Book Chapter 16)

") Lecture: Simultaneous Equation Model (Wooldridge s Book Chapter 16) 1 2 Model Consider a system of two regressions y 1 = β 1 y 2 + u 1 (1) y 2 = β 2 y 1 + u 2 (2) This is a simultaneous equation model

Lecture: Simultaneous Equation Model (Wooldridge s Book Chapter 16) 1 2 Model Consider a system of two regressions y 1 = β 1 y 2 + u 1 (1) y 2 = β 2 y 1 + u 2 (2) This is a simultaneous equation model

WISE International Masters

WISE International Masters ECONOMETRICS Instructor: Brett Graham INSTRUCTIONS TO STUDENTS 1 The time allowed for this examination paper is 2 hours. 2 This examination paper contains 32 questions. You are

WISE International Masters ECONOMETRICS Instructor: Brett Graham INSTRUCTIONS TO STUDENTS 1 The time allowed for this examination paper is 2 hours. 2 This examination paper contains 32 questions. You are

Applied Health Economics (for B.Sc.)

") Applied Health Economics (for B.Sc.) Helmut Farbmacher Department of Economics University of Mannheim Autumn Semester 2017 Outlook 1 Linear models (OLS, Omitted variables, 2SLS) 2 Limited and qualitative

Applied Health Economics (for B.Sc.) Helmut Farbmacher Department of Economics University of Mannheim Autumn Semester 2017 Outlook 1 Linear models (OLS, Omitted variables, 2SLS) 2 Limited and qualitative