Toulouse School of Economics, M2 Macroeconomics 1 Professor Franck Portier. Exam Solution

|

|

|

- Egbert Thompson

- 6 years ago

- Views:

Transcription

1 Toulouse School of Economics, M2 Macroeconomics 1 Professor Franck Portier Exam Solution This is a 3 hours exam. Class slides and any handwritten material are allowed. You must write legibly. I True,False,Uncertain?(1/2 of the points) For each of those statements, say whether it is true, false, or uncertain and explain why. You should target around 10 to 15 lines per question. Copying the slides will not bring any points. 1 It is optimal that unemployment rate is zero. FALSE. That would be true in a competitive and frictionless labor market: unemployment would correspond to unexploited gains from trade. Things are quite di erent if there are frictions to trade. If we take the example of matching models, the number of hirings is typically H = m(u, V )where U is the number of unemployed and V the number of vacancies. In such a vase, U can be seen as an input to produce hirings. If the economy needs at each date a flow of hirings (for example because jobs are destroyed), then it is suboptimal to have U = 0, as it would lead to zero hirings. 2 In the Ramsey model, the transversality condition states that the level of capital should tend to zero. FALSE. Let s assume that the economy terminates in period T.Insuchaneconomy,itisoptimal for the planner to leave zero capital stock at the end of period T. Why? Assume that the optimal path leaves a positive amount of capital at the end of period T. Allocate this capital stock to consumption of period T. The intertemporal utility will be higher. Hence a contradiction with the assumption that the path was optimal. When one considers an infinite horizon problem, the condition is: lim e T µ T K T =0. T!1 where µ is the shadow value of capital. The condition is not that the level of capital should tend to zero, but its discounted value, which is a weaker condition. 3 Labour-augmenting technical progress is a necessary condition for long run growth of income per capita. FALSE. We represent technological progress as an expansion of the production set: more output can be produced with the same inputs. Take a Neo-classical economy, whose key ingredients are (i) a production function Y (t) =F (K(t),L(t)), (ii) an equation for capital accumulation K(t) = Y (t) C(t) wherey = output, L =labour,k = capital, and C = consumption and where 8t L(t) is equal to the workforce which is an exogenous variable. Technical progress can be modelled in three ways: (1) labour-augmenting technical progress: Y (t) = F (K(t),A(t)L(t)), (2) capital-augmenting technical progress: Y (t) = F (A(t)K(t),L(t)) and (3) output-augmenting technical progress: Y (t) = A(t)F (K(t),L(t)). In the three cases, there will be increasing income per capita. But only in the labor-augmenting case does the model satisfies the five following stylized facts of balanced growth, which are (SF1) Y/L and K/L go up over time, (SF2) K/Y is constant, (SF3) wages go up, (SF4) the profit rate is constant, (SF5) The share of labour and capital in GDP are constant. 4 Intellectual property rights have ambiguous e ects on growth and welfare. TRUE. One the one hand, in R&D models, innovators typically do not entirely appropriate the social surplus from their innovation. They get profits but part of the surplus goes to the consumers. 1

2 This tends to make innovation too low compared with the optimum. Better enforcement of intellectual property rights foster R&D, therefore growth, and is a good thing for welfare. But on the other hand, ideas are non rival goods. The monopoly distortion in price-setting that is created by intellectual property rights tends to push prices above marginal cost. In equilibrium this means that real wages are too low relative to the social optimum, which is bad for welfare. 5 The speed of convergence is high in the AK model. FALSE. Consider a Solow model (assume that Y and K are per capita): Y = AK, K = sy K. A grows at a constant rate g A,bothY and K grow at the common constant rate g in the long run. Let ŷ = Y Y LR be the relative deviation from the BGP (same definition for ˆk). Y LR By definition, the speed of convergence is given by v = It can be shown that v =(g + )(1 ). In an AK model, =1,sothatspeedofconvergenceisactuallynull. Thisisbecausethereisno decreasing returns in K: startingwithalowk does not imply that marginal productivity of capital is very high and therefore growth temporarily higher. 6 Time is continuous and the interest rate is r. Consider a blue asset (value V b )thatpaysb per unit of time and a yellow asset (value V y )thatpaysy per unit of time. A green asset is an asset that is blue and that can turn yellow according to a Poisson distribution with intensity. Using a discrete time approximation and taking the limit when the length of the period tends to zero, one can prove that rv g (t) =b + (V b (t) V y (t)) + V. (t) 1 dŷ. ŷ dt FALSE. Consider a distrete time version of the problem. By arbitrage: V g (t)(1 + r.dt) =b.dt +(1 dt)v g (t + dt)+ dtv y (t + dt) First order Taylor expansion: so that the arbitrage equation writes V x (t + dt) =V x (t)+. V x (t)dt V g (t)+rv g (t)dt = b.dt +(1 dt)(v g (t)+. V g (t)dt)+ dt(v y (t)+. V y (t)dt) Neglecting the terms in (dt) 2 gives rv g (t) =b + (V y (t) V g (t)) +. V g (t) 7 Unemployment benefits increase unemployment because they shift upwards the Beveridge curve. FALSE. The basic building block of the Beveridge curve is the matching function, which relates hirings per unit of time to the two key inputs in the search process, unemployment and vacancies: H t = m(u t,v t ). Here H t =thegrosshiringrateperunitoftime,u t =thenumberofunemployed workers,v t = the number of vacant jobs. The matching function is similar to a production function, and we assume it has the same properties including constant returns to scale. Assume that a fraction s of all jobs is destroyed per unit of time. Let L =thetotallaborforce,l t = employment at t. Then we can define the hiring, unemployment, and vacancy rates in relation to the total workforce: u t = Ut L = L L t L, v t = Vt L and h t = Ht. Because of constant returns to scale, we can L write h t = m(u t,v t ). The evolution of the unemployment rate is du = h dt t + s(1 u t )= m(u t,v t )+s(1 u t ). The Beveridge curve is the locus du/dt =0locusinthe(u, v). It does not depend on unemployment benefits. It is a resource constraint, that does not assume any optimal labor demand nor supply. 2

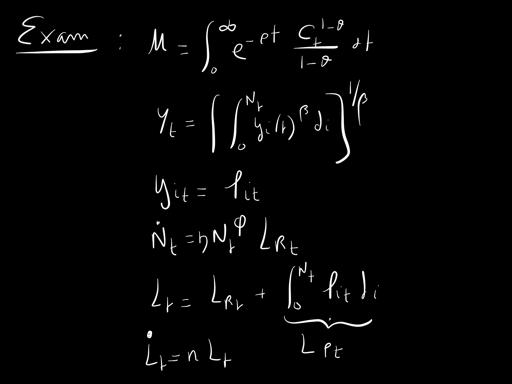

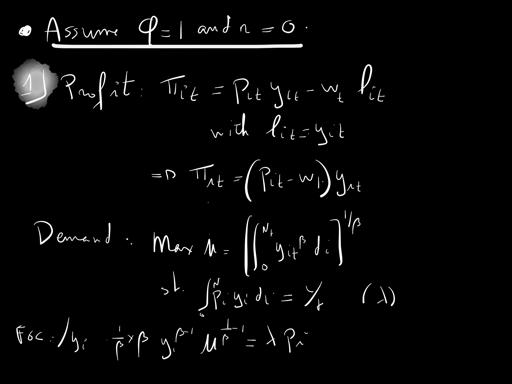

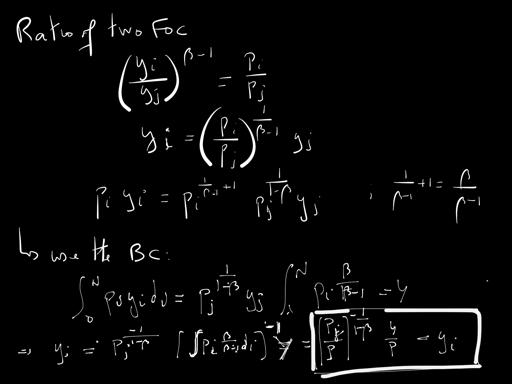

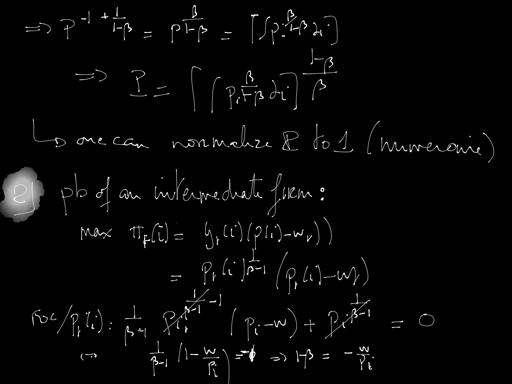

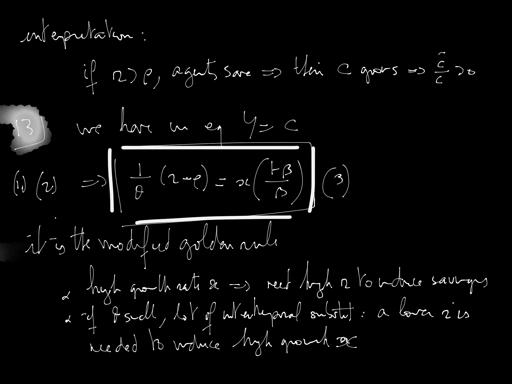

3 8 With Nash-bargaining, the surplus of a match is e ciently shared. TRUE. Any sharing rule that does not leave some of the surplus undistributed is e cient. This is the case of the Nash-Bargaining. What can be ine cient is vacancy creation (and job search or job destruction when they are endogenous) 9 Hours worked per person cannot grow along a balanced growth path. TRUE. Along a BGP, all variables grow at a constant (positive) rate or do not grow. Hours worked per person are bounded above by the total amount of time available per period. They cannot grow at a constant positive rate without violating the time constraint. Therefore, they cannot grow. 10 In the real business cycle model, stabilizing output following a productivity shock is Pareto improving. In the canonical RBC model, allocations are Pareto optimal. Therefore, fluctuations are the socially optimal responses to shocks. No policy can improve welfare. This does not mean that fluctuations are not costly: agents would prefer to live in an economy without shocks to productivity (assuming that they have zero mean). II Endogenous Growth (1/2 of the points) Time is continuous. We use the notation X t = X(t). Consider an economy in which population at time t is L t and grows at the constant rate n, suchthat L. t = nl t. All agents have preferences given by Z 1 0 e t C1 t 1 1 where C is consumption defined over the final good of the economy. This good is produced as dt, applez N Y t = y t (i) di 0 1, where y(i) isintermediategoodi and 0 < is <1. The production function of each intermediate good y t (i) =`t(i), where `(i) islaborallocatedtogoodi. Thewageisdenotedw t. New goods are produced by allocating workers to the R&D process, with the production function. N t = N t L Rt, where apple 1andL Rt is labor allocated to R&D. Labor market clearing requires Z N `t(i)di +L Rt = L t. 0 {z } L Pt L Pt is the amount of labor required for production. Risk-neutral firms hire workers for R&D. A firm who discovers a new good becomes the monopoly supplier, with a perfectly and indefinitely enforced patent. There is free entry on the R&D market. For the time being, let s consider the case = 1 and n = 0. 1 Write the instantaneous profit of the final good firm. Show that the demand for intermediate good i is y t (i) =p t (i) 1 1 Yt. 3

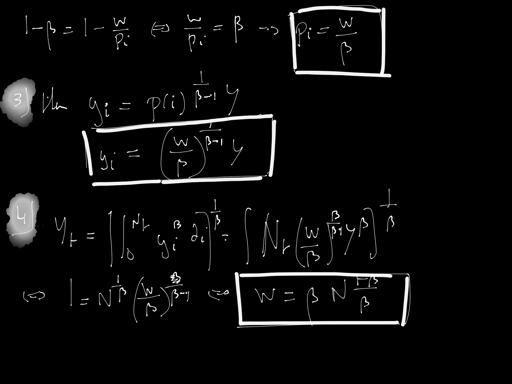

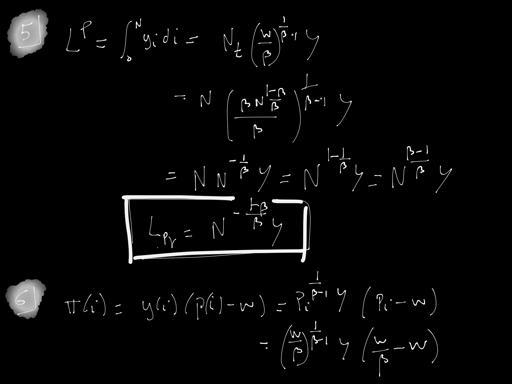

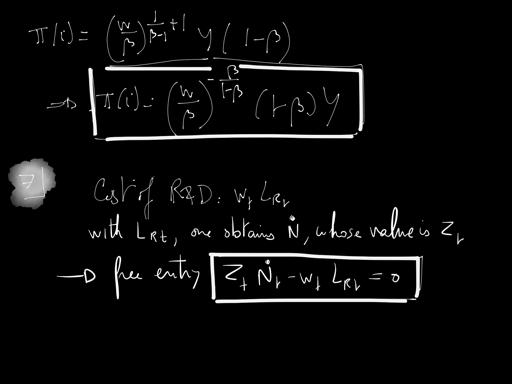

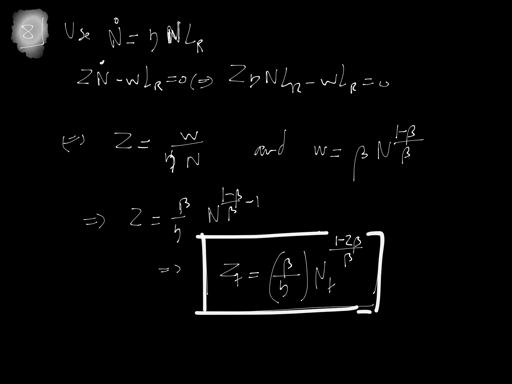

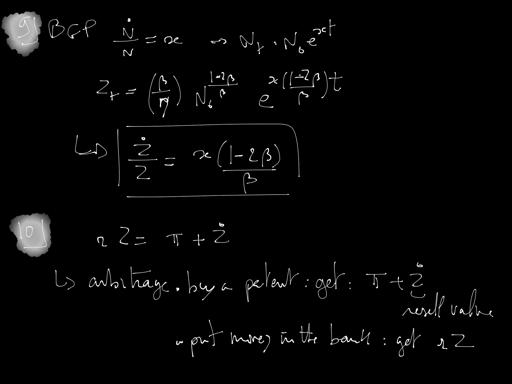

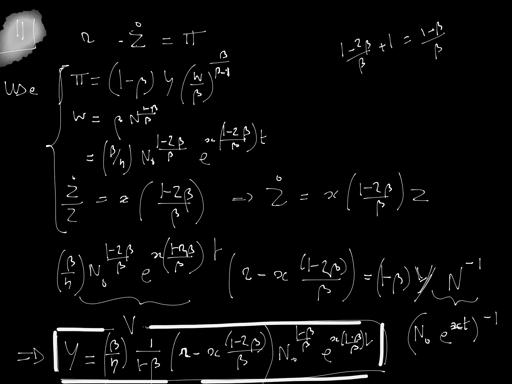

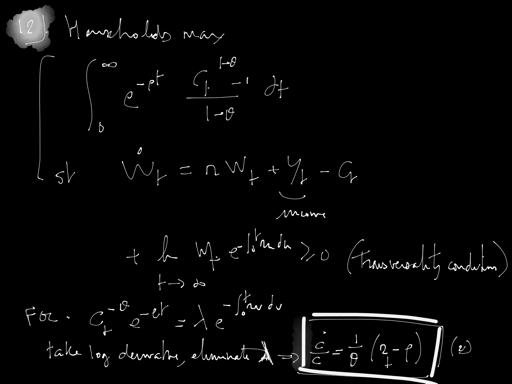

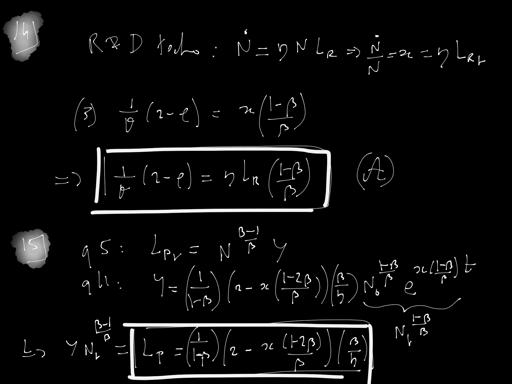

4 2 Show that profit maximization of each intermediate firm results in them setting price as a constant percentage markup over their marginal cost. 3 Show then that demand for good i can be written as function of Y and w. 4 Using the previous result and the production function of final good, determine the equilibrium wage as a function of N t. 5 Using the demand for good i, expressl Pt as a function of Y and N. 6 Show that the profit of an intermediate firm can be written as a function of Y and w. 7 We now turn to the R&D sector. Let Z t denote the present discounted value of the profits of an intermediate good producer at time t. Next consider a firm undertaking R&D to create a new intermediary. Explain why does the free entry condition on the R&D market writes Z t Ṅ t w t L Rt =0. 8 Derive an expression for Z as a function of N. (Hint: use the law of motion of N) 9 Let us restrict to balanced growth path (BGP) and guess that N grows at a constant rate x (needed to be verified at some point). Using that guess and the expression for Z, derivethegrowth rate of Z along a BGP. 10 Why does the the following equation holds? What does it mean? (r is the interest rate, t is the instantaneous profit of any intermediate firm at a symmetric equilibrium where all intermediate firms are taking the same decisions; this is the equilibrium that we consider here) rz t = t + Ż t. 11 Using all the previous equations, derive an expression for Y as a function of r, x, N 0 and t. Express the growth rate of Y (and hence C) asafunctionof and x. Denotethisequation(1). 12 Without doing the algebra, explain how do we get the following relation from the household intertemporal maximization problem: Ċ t = 1 (r ). (2) C t How do you interpret this relation? 13 Use (1) and (2) to obtain a relation (3) between x and r. Comment. 14 We now need to determine x in equilibrium. Use the R&D technology and (3) to derive a equation between L R and r. Calltherelation(A). 15 Using the expression of L P of question 5 and the one of Y in question 11, get an expression of L P as a function of r and x. Using L R = L L P,obtainasecondrelation(B) betweenl R and x. 16 Compute the equilibrium level of L R.Checkthatx is indeed constant and derive its equilibrium level. Compute also the equilibrium level of r. 17 Compute the growth rate of the economy (which is the growth rate of Y or C). How does it depend on? Why? 18 How does the growth rate depend on L? Why? Discuss the empirical relevance of that result. 4

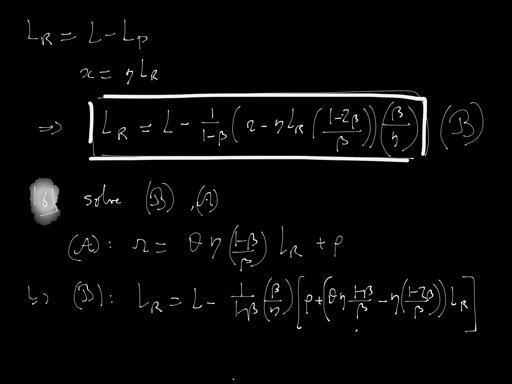

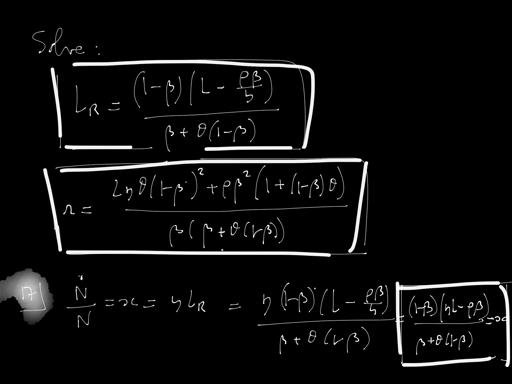

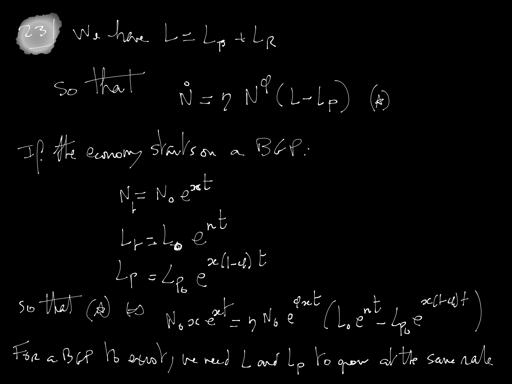

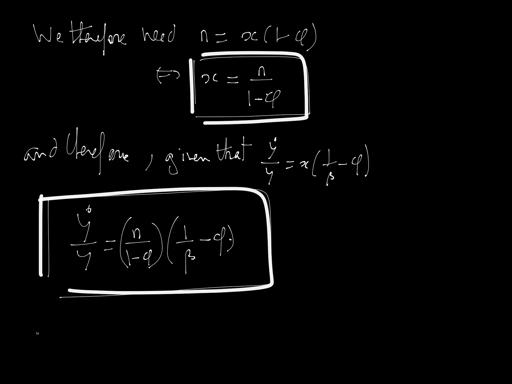

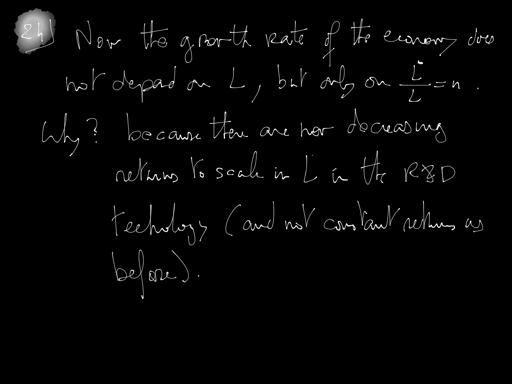

5 19 We now want to characterize the balanced growth path equilibrium when <1 and n > 0. Explain how to derive the new free entry condition Z t N t L Rt w t L Rt =0. 20 Derive an expression for Z t as a function of N t. 21 Using rz t = t + Ż t and the expression of the profit, derive the growth rate of Y as a function of x. 22 Derive the growth rate of L Pt as a function of x. 23 Derive the growth rate of Y assuming that the economy began on a balanced growth path at date Does the growth rate of the economy depend on L? Why? Discuss. 5

6

7

8

9

10

11

12

13

14

15

16

17

18

14.452: Introduction to Economic Growth Problem Set 4

14.452: Introduction to Economic Growth Problem Set 4 Daron Acemoglu Due date: December 5, 12pm noon Please only hand in Question 3, which will be graded. The rest will be reviewed in the recitation but

14.452: Introduction to Economic Growth Problem Set 4 Daron Acemoglu Due date: December 5, 12pm noon Please only hand in Question 3, which will be graded. The rest will be reviewed in the recitation but

A simple macro dynamic model with endogenous saving rate: the representative agent model

A simple macro dynamic model with endogenous saving rate: the representative agent model Virginia Sánchez-Marcos Macroeconomics, MIE-UNICAN Macroeconomics (MIE-UNICAN) A simple macro dynamic model with

A simple macro dynamic model with endogenous saving rate: the representative agent model Virginia Sánchez-Marcos Macroeconomics, MIE-UNICAN Macroeconomics (MIE-UNICAN) A simple macro dynamic model with

The Ramsey Model. (Lecture Note, Advanced Macroeconomics, Thomas Steger, SS 2013)

") The Ramsey Model (Lecture Note, Advanced Macroeconomics, Thomas Steger, SS 213) 1 Introduction The Ramsey model (or neoclassical growth model) is one of the prototype models in dynamic macroeconomics.

The Ramsey Model (Lecture Note, Advanced Macroeconomics, Thomas Steger, SS 213) 1 Introduction The Ramsey model (or neoclassical growth model) is one of the prototype models in dynamic macroeconomics.

Macroeconomics Theory II

Macroeconomics Theory II Francesco Franco FEUNL February 2016 Francesco Franco (FEUNL) Macroeconomics Theory II February 2016 1 / 18 Road Map Research question: we want to understand businesses cycles.

Macroeconomics Theory II Francesco Franco FEUNL February 2016 Francesco Franco (FEUNL) Macroeconomics Theory II February 2016 1 / 18 Road Map Research question: we want to understand businesses cycles.

Advanced Macroeconomics

Advanced Macroeconomics The Ramsey Model Marcin Kolasa Warsaw School of Economics Marcin Kolasa (WSE) Ad. Macro - Ramsey model 1 / 30 Introduction Authors: Frank Ramsey (1928), David Cass (1965) and Tjalling

Advanced Macroeconomics The Ramsey Model Marcin Kolasa Warsaw School of Economics Marcin Kolasa (WSE) Ad. Macro - Ramsey model 1 / 30 Introduction Authors: Frank Ramsey (1928), David Cass (1965) and Tjalling

(a) Write down the Hamilton-Jacobi-Bellman (HJB) Equation in the dynamic programming

Write down the Hamilton-Jacobi-Bellman (HJB) Equation in the dynamic programming") 1. Government Purchases and Endogenous Growth Consider the following endogenous growth model with government purchases (G) in continuous time. Government purchases enhance production, and the production

1. Government Purchases and Endogenous Growth Consider the following endogenous growth model with government purchases (G) in continuous time. Government purchases enhance production, and the production

Master 2 Macro I. Lecture 2 : Balance Growth Paths

2012-2013 Master 2 Macro I Lecture 2 : Balance Growth Paths Franck Portier (based on Gilles Saint-Paul lecture notes) franck.portier@tse-fr.eu Toulouse School of Economics Version 1.1 24/09/2012 Changes

2012-2013 Master 2 Macro I Lecture 2 : Balance Growth Paths Franck Portier (based on Gilles Saint-Paul lecture notes) franck.portier@tse-fr.eu Toulouse School of Economics Version 1.1 24/09/2012 Changes

Expanding Variety Models

Expanding Variety Models Yin-Chi Wang The Chinese University of Hong Kong November, 2012 References: Acemoglu (2009) ch13 Introduction R&D and technology adoption are purposeful activities The simplest

Expanding Variety Models Yin-Chi Wang The Chinese University of Hong Kong November, 2012 References: Acemoglu (2009) ch13 Introduction R&D and technology adoption are purposeful activities The simplest

Economic Growth: Lecture 9, Neoclassical Endogenous Growth

14.452 Economic Growth: Lecture 9, Neoclassical Endogenous Growth Daron Acemoglu MIT November 28, 2017. Daron Acemoglu (MIT) Economic Growth Lecture 9 November 28, 2017. 1 / 41 First-Generation Models

14.452 Economic Growth: Lecture 9, Neoclassical Endogenous Growth Daron Acemoglu MIT November 28, 2017. Daron Acemoglu (MIT) Economic Growth Lecture 9 November 28, 2017. 1 / 41 First-Generation Models

Advanced Economic Growth: Lecture 3, Review of Endogenous Growth: Schumpeterian Models

Advanced Economic Growth: Lecture 3, Review of Endogenous Growth: Schumpeterian Models Daron Acemoglu MIT September 12, 2007 Daron Acemoglu (MIT) Advanced Growth Lecture 3 September 12, 2007 1 / 40 Introduction

Advanced Economic Growth: Lecture 3, Review of Endogenous Growth: Schumpeterian Models Daron Acemoglu MIT September 12, 2007 Daron Acemoglu (MIT) Advanced Growth Lecture 3 September 12, 2007 1 / 40 Introduction

Master 2 Macro I. Lecture notes #9 : the Mortensen-Pissarides matching model

2012-2013 Master 2 Macro I Lecture notes #9 : the Mortensen-Pissarides matching model Franck Portier (based on Gilles Saint-Paul lecture notes) franck.portier@tse-fr.eu Toulouse School of Economics Version

2012-2013 Master 2 Macro I Lecture notes #9 : the Mortensen-Pissarides matching model Franck Portier (based on Gilles Saint-Paul lecture notes) franck.portier@tse-fr.eu Toulouse School of Economics Version

Schumpeterian Growth Models

Schumpeterian Growth Models Yin-Chi Wang The Chinese University of Hong Kong November, 2012 References: Acemoglu (2009) ch14 Introduction Most process innovations either increase the quality of an existing

Schumpeterian Growth Models Yin-Chi Wang The Chinese University of Hong Kong November, 2012 References: Acemoglu (2009) ch14 Introduction Most process innovations either increase the quality of an existing

Modelling Czech and Slovak labour markets: A DSGE model with labour frictions

Modelling Czech and Slovak labour markets: A DSGE model with labour frictions Daniel Němec Faculty of Economics and Administrations Masaryk University Brno, Czech Republic nemecd@econ.muni.cz ESF MU (Brno)

Modelling Czech and Slovak labour markets: A DSGE model with labour frictions Daniel Němec Faculty of Economics and Administrations Masaryk University Brno, Czech Republic nemecd@econ.muni.cz ESF MU (Brno)

Macroeconomics Theory II

Macroeconomics Theory II Francesco Franco FEUNL February 2011 Francesco Franco Macroeconomics Theory II 1/34 The log-linear plain vanilla RBC and ν(σ n )= ĉ t = Y C ẑt +(1 α) Y C ˆn t + K βc ˆk t 1 + K

Macroeconomics Theory II Francesco Franco FEUNL February 2011 Francesco Franco Macroeconomics Theory II 1/34 The log-linear plain vanilla RBC and ν(σ n )= ĉ t = Y C ẑt +(1 α) Y C ˆn t + K βc ˆk t 1 + K

Advanced Macroeconomics

Advanced Macroeconomics Endogenous Growth Marcin Kolasa Warsaw School of Economics Marcin Kolasa (WSE) Ad. Macro - Endogenous growth 1 / 18 Introduction The Solow and Ramsey models are exogenous growth

Advanced Macroeconomics Endogenous Growth Marcin Kolasa Warsaw School of Economics Marcin Kolasa (WSE) Ad. Macro - Endogenous growth 1 / 18 Introduction The Solow and Ramsey models are exogenous growth

Neoclassical Models of Endogenous Growth

Neoclassical Models of Endogenous Growth October 2007 () Endogenous Growth October 2007 1 / 20 Motivation What are the determinants of long run growth? Growth in the "e ectiveness of labour" should depend

Neoclassical Models of Endogenous Growth October 2007 () Endogenous Growth October 2007 1 / 20 Motivation What are the determinants of long run growth? Growth in the "e ectiveness of labour" should depend

Economic Growth: Lectures 10 and 11, Endogenous Technological Change

14.452 Economic Growth: Lectures 10 and 11, Endogenous Technological Change Daron Acemoglu MIT December 1 and 6, 2011. Daron Acemoglu (MIT) Economic Growth Lectures 10 end 11 December 1 and 6, 2011. 1

14.452 Economic Growth: Lectures 10 and 11, Endogenous Technological Change Daron Acemoglu MIT December 1 and 6, 2011. Daron Acemoglu (MIT) Economic Growth Lectures 10 end 11 December 1 and 6, 2011. 1

Job Search Models. Jesús Fernández-Villaverde. University of Pennsylvania. February 12, 2016

Job Search Models Jesús Fernández-Villaverde University of Pennsylvania February 12, 2016 Jesús Fernández-Villaverde (PENN) Job Search February 12, 2016 1 / 57 Motivation Introduction Trade in the labor

Job Search Models Jesús Fernández-Villaverde University of Pennsylvania February 12, 2016 Jesús Fernández-Villaverde (PENN) Job Search February 12, 2016 1 / 57 Motivation Introduction Trade in the labor

Public Economics The Macroeconomic Perspective Chapter 2: The Ramsey Model. Burkhard Heer University of Augsburg, Germany

Public Economics The Macroeconomic Perspective Chapter 2: The Ramsey Model Burkhard Heer University of Augsburg, Germany October 3, 2018 Contents I 1 Central Planner 2 3 B. Heer c Public Economics: Chapter

Public Economics The Macroeconomic Perspective Chapter 2: The Ramsey Model Burkhard Heer University of Augsburg, Germany October 3, 2018 Contents I 1 Central Planner 2 3 B. Heer c Public Economics: Chapter

Equilibrium in a Production Economy

Equilibrium in a Production Economy Prof. Eric Sims University of Notre Dame Fall 2012 Sims (ND) Equilibrium in a Production Economy Fall 2012 1 / 23 Production Economy Last time: studied equilibrium in

Equilibrium in a Production Economy Prof. Eric Sims University of Notre Dame Fall 2012 Sims (ND) Equilibrium in a Production Economy Fall 2012 1 / 23 Production Economy Last time: studied equilibrium in

Simple New Keynesian Model without Capital

Simple New Keynesian Model without Capital Lawrence J. Christiano Gerzensee, August 27 Objective Review the foundations of the basic New Keynesian model without capital. Clarify the role of money supply/demand.

Simple New Keynesian Model without Capital Lawrence J. Christiano Gerzensee, August 27 Objective Review the foundations of the basic New Keynesian model without capital. Clarify the role of money supply/demand.

Advanced Economic Growth: Lecture 2, Review of Endogenous Growth: Expanding Variety Models

Advanced Economic Growth: Lecture 2, Review of Endogenous Growth: Expanding Variety Models Daron Acemoglu MIT September 10, 2007 Daron Acemoglu (MIT) Advanced Growth Lecture 2 September 10, 2007 1 / 56

Advanced Economic Growth: Lecture 2, Review of Endogenous Growth: Expanding Variety Models Daron Acemoglu MIT September 10, 2007 Daron Acemoglu (MIT) Advanced Growth Lecture 2 September 10, 2007 1 / 56

Economic Growth: Lectures 9 and 10, Endogenous Technological Change

14.452 Economic Growth: Lectures 9 and 10, Endogenous Technological Change Daron Acemoglu MIT Nov. 29 and Dec. 4 Daron Acemoglu (MIT) Economic Growth Lectures 9 and 10 Nov. 29 and Dec. 4 1 / 73 Endogenous

14.452 Economic Growth: Lectures 9 and 10, Endogenous Technological Change Daron Acemoglu MIT Nov. 29 and Dec. 4 Daron Acemoglu (MIT) Economic Growth Lectures 9 and 10 Nov. 29 and Dec. 4 1 / 73 Endogenous

The Basic New Keynesian Model, the Labor Market and Sticky Wages

The Basic New Keynesian Model, the Labor Market and Sticky Wages Lawrence J. Christiano August 25, 203 Baseline NK model with no capital and with a competitive labor market. private sector equilibrium

The Basic New Keynesian Model, the Labor Market and Sticky Wages Lawrence J. Christiano August 25, 203 Baseline NK model with no capital and with a competitive labor market. private sector equilibrium

Ramsey Cass Koopmans Model (1): Setup of the Model and Competitive Equilibrium Path

: Setup of the Model and Competitive Equilibrium Path") Ramsey Cass Koopmans Model (1): Setup of the Model and Competitive Equilibrium Path Ryoji Ohdoi Dept. of Industrial Engineering and Economics, Tokyo Tech This lecture note is mainly based on Ch. 8 of Acemoglu

Ramsey Cass Koopmans Model (1): Setup of the Model and Competitive Equilibrium Path Ryoji Ohdoi Dept. of Industrial Engineering and Economics, Tokyo Tech This lecture note is mainly based on Ch. 8 of Acemoglu

Neoclassical Business Cycle Model

Neoclassical Business Cycle Model Prof. Eric Sims University of Notre Dame Fall 2015 1 / 36 Production Economy Last time: studied equilibrium in an endowment economy Now: study equilibrium in an economy

Neoclassical Business Cycle Model Prof. Eric Sims University of Notre Dame Fall 2015 1 / 36 Production Economy Last time: studied equilibrium in an endowment economy Now: study equilibrium in an economy

Simple New Keynesian Model without Capital

Simple New Keynesian Model without Capital Lawrence J. Christiano January 5, 2018 Objective Review the foundations of the basic New Keynesian model without capital. Clarify the role of money supply/demand.

Simple New Keynesian Model without Capital Lawrence J. Christiano January 5, 2018 Objective Review the foundations of the basic New Keynesian model without capital. Clarify the role of money supply/demand.

Chapter 12 Ramsey Cass Koopmans model

Chapter 12 Ramsey Cass Koopmans model O. Afonso, P. B. Vasconcelos Computational Economics: a concise introduction O. Afonso, P. B. Vasconcelos Computational Economics 1 / 33 Overview 1 Introduction 2

Chapter 12 Ramsey Cass Koopmans model O. Afonso, P. B. Vasconcelos Computational Economics: a concise introduction O. Afonso, P. B. Vasconcelos Computational Economics 1 / 33 Overview 1 Introduction 2

Lecture 2 The Centralized Economy: Basic features

Lecture 2 The Centralized Economy: Basic features Leopold von Thadden University of Mainz and ECB (on leave) Advanced Macroeconomics, Winter Term 2013 1 / 41 I Motivation This Lecture introduces the basic

Lecture 2 The Centralized Economy: Basic features Leopold von Thadden University of Mainz and ECB (on leave) Advanced Macroeconomics, Winter Term 2013 1 / 41 I Motivation This Lecture introduces the basic

problem. max Both k (0) and h (0) are given at time 0. (a) Write down the Hamilton-Jacobi-Bellman (HJB) Equation in the dynamic programming

and h (0) are given at time 0. (a) Write down the Hamilton-Jacobi-Bellman (HJB) Equation in the dynamic programming") 1. Endogenous Growth with Human Capital Consider the following endogenous growth model with both physical capital (k (t)) and human capital (h (t)) in continuous time. The representative household solves

1. Endogenous Growth with Human Capital Consider the following endogenous growth model with both physical capital (k (t)) and human capital (h (t)) in continuous time. The representative household solves

4- Current Method of Explaining Business Cycles: DSGE Models. Basic Economic Models

4- Current Method of Explaining Business Cycles: DSGE Models Basic Economic Models In Economics, we use theoretical models to explain the economic processes in the real world. These models de ne a relation

4- Current Method of Explaining Business Cycles: DSGE Models Basic Economic Models In Economics, we use theoretical models to explain the economic processes in the real world. These models de ne a relation

Lecture 15. Dynamic Stochastic General Equilibrium Model. Randall Romero Aguilar, PhD I Semestre 2017 Last updated: July 3, 2017

Lecture 15 Dynamic Stochastic General Equilibrium Model Randall Romero Aguilar, PhD I Semestre 2017 Last updated: July 3, 2017 Universidad de Costa Rica EC3201 - Teoría Macroeconómica 2 Table of contents

Lecture 15 Dynamic Stochastic General Equilibrium Model Randall Romero Aguilar, PhD I Semestre 2017 Last updated: July 3, 2017 Universidad de Costa Rica EC3201 - Teoría Macroeconómica 2 Table of contents

The Ramsey Model. Alessandra Pelloni. October TEI Lecture. Alessandra Pelloni (TEI Lecture) Economic Growth October / 61

Economic Growth October / 61") The Ramsey Model Alessandra Pelloni TEI Lecture October 2015 Alessandra Pelloni (TEI Lecture) Economic Growth October 2015 1 / 61 Introduction Introduction Introduction Ramsey-Cass-Koopmans model: di ers

The Ramsey Model Alessandra Pelloni TEI Lecture October 2015 Alessandra Pelloni (TEI Lecture) Economic Growth October 2015 1 / 61 Introduction Introduction Introduction Ramsey-Cass-Koopmans model: di ers

Advanced Macroeconomics II. Real Business Cycle Models. Jordi Galí. Universitat Pompeu Fabra Spring 2018

Advanced Macroeconomics II Real Business Cycle Models Jordi Galí Universitat Pompeu Fabra Spring 2018 Assumptions Optimization by consumers and rms Perfect competition General equilibrium Absence of a

Advanced Macroeconomics II Real Business Cycle Models Jordi Galí Universitat Pompeu Fabra Spring 2018 Assumptions Optimization by consumers and rms Perfect competition General equilibrium Absence of a

14.461: Technological Change, Lecture 1

14.461: Technological Change, Lecture 1 Daron Acemoglu MIT September 8, 2016. Daron Acemoglu (MIT) Technological Change, Lecture 1 September 8, 2016. 1 / 60 Endogenous Technological Change Expanding Variety

14.461: Technological Change, Lecture 1 Daron Acemoglu MIT September 8, 2016. Daron Acemoglu (MIT) Technological Change, Lecture 1 September 8, 2016. 1 / 60 Endogenous Technological Change Expanding Variety

Stagnation Traps. Gianluca Benigno and Luca Fornaro

Stagnation Traps Gianluca Benigno and Luca Fornaro May 2015 Research question and motivation Can insu cient aggregate demand lead to economic stagnation? This question goes back, at least, to the Great

Stagnation Traps Gianluca Benigno and Luca Fornaro May 2015 Research question and motivation Can insu cient aggregate demand lead to economic stagnation? This question goes back, at least, to the Great

Econ 204A: Section 3

Econ 204A: Section 3 Ryan Sherrard University of California, Santa Barbara 18 October 2016 Sherrard (UCSB) Section 3 18 October 2016 1 / 19 Notes on Problem Set 2 Total Derivative Review sf (k ) = (δ +

Econ 204A: Section 3 Ryan Sherrard University of California, Santa Barbara 18 October 2016 Sherrard (UCSB) Section 3 18 October 2016 1 / 19 Notes on Problem Set 2 Total Derivative Review sf (k ) = (δ +

The Labor Market in the New Keynesian Model: Incorporating a Simple DMP Version of the Labor Market and Rediscovering the Shimer Puzzle

The Labor Market in the New Keynesian Model: Incorporating a Simple DMP Version of the Labor Market and Rediscovering the Shimer Puzzle Lawrence J. Christiano April 1, 2013 Outline We present baseline

The Labor Market in the New Keynesian Model: Incorporating a Simple DMP Version of the Labor Market and Rediscovering the Shimer Puzzle Lawrence J. Christiano April 1, 2013 Outline We present baseline

An adaptation of Pissarides (1990) by using random job destruction rate

by using random job destruction rate") MPRA Munich Personal RePEc Archive An adaptation of Pissarides (990) by using random job destruction rate Huiming Wang December 2009 Online at http://mpra.ub.uni-muenchen.de/203/ MPRA Paper No. 203, posted

MPRA Munich Personal RePEc Archive An adaptation of Pissarides (990) by using random job destruction rate Huiming Wang December 2009 Online at http://mpra.ub.uni-muenchen.de/203/ MPRA Paper No. 203, posted

Economic Growth: Lecture 13, Directed Technological Change

14.452 Economic Growth: Lecture 13, Directed Technological Change Daron Acemoglu MIT December 13, 2011. Daron Acemoglu (MIT) Economic Growth Lecture 13 December 13, 2011. 1 / 71 Directed Technological

14.452 Economic Growth: Lecture 13, Directed Technological Change Daron Acemoglu MIT December 13, 2011. Daron Acemoglu (MIT) Economic Growth Lecture 13 December 13, 2011. 1 / 71 Directed Technological

The Harris-Todaro model

Yves Zenou Research Institute of Industrial Economics July 3, 2006 The Harris-Todaro model In two seminal papers, Todaro (1969) and Harris and Todaro (1970) have developed a canonical model of rural-urban

Yves Zenou Research Institute of Industrial Economics July 3, 2006 The Harris-Todaro model In two seminal papers, Todaro (1969) and Harris and Todaro (1970) have developed a canonical model of rural-urban

Advanced Macroeconomics

Advanced Macroeconomics The Ramsey Model Micha l Brzoza-Brzezina/Marcin Kolasa Warsaw School of Economics Micha l Brzoza-Brzezina/Marcin Kolasa (WSE) Ad. Macro - Ramsey model 1 / 47 Introduction Authors:

Advanced Macroeconomics The Ramsey Model Micha l Brzoza-Brzezina/Marcin Kolasa Warsaw School of Economics Micha l Brzoza-Brzezina/Marcin Kolasa (WSE) Ad. Macro - Ramsey model 1 / 47 Introduction Authors:

Simple New Keynesian Model without Capital

Simple New Keynesian Model without Capital Lawrence J. Christiano March, 28 Objective Review the foundations of the basic New Keynesian model without capital. Clarify the role of money supply/demand. Derive

Simple New Keynesian Model without Capital Lawrence J. Christiano March, 28 Objective Review the foundations of the basic New Keynesian model without capital. Clarify the role of money supply/demand. Derive

Real Business Cycle Model (RBC)

") Real Business Cycle Model (RBC) Seyed Ali Madanizadeh November 2013 RBC Model Lucas 1980: One of the functions of theoretical economics is to provide fully articulated, artificial economic systems that

Real Business Cycle Model (RBC) Seyed Ali Madanizadeh November 2013 RBC Model Lucas 1980: One of the functions of theoretical economics is to provide fully articulated, artificial economic systems that

Labor Union and the Wealth-Income Ratio

Labor Union and the Wealth-Income Ratio Angus C. Chu Zonglai Kou Xueyue Liu November 2017 Abstract We explore how labor union affects the wealth-income ratio in an innovation-driven growth model and find

Labor Union and the Wealth-Income Ratio Angus C. Chu Zonglai Kou Xueyue Liu November 2017 Abstract We explore how labor union affects the wealth-income ratio in an innovation-driven growth model and find

1. Unemployment. March 20, Nr. 1

1. Unemployment March 20, 2007 Nr. 1 Job destruction, and employment protection. I So far, only creation decision. Clearly both creation and destruction margins. So endogenize job destruction. Can then

1. Unemployment March 20, 2007 Nr. 1 Job destruction, and employment protection. I So far, only creation decision. Clearly both creation and destruction margins. So endogenize job destruction. Can then

The TransPacific agreement A good thing for VietNam?

The TransPacific agreement A good thing for VietNam? Jean Louis Brillet, France For presentation at the LINK 2014 Conference New York, 22nd 24th October, 2014 Advertisement!!! The model uses EViews The

The TransPacific agreement A good thing for VietNam? Jean Louis Brillet, France For presentation at the LINK 2014 Conference New York, 22nd 24th October, 2014 Advertisement!!! The model uses EViews The

Economics 2450A: Public Economics Section 8: Optimal Minimum Wage and Introduction to Capital Taxation

Economics 2450A: Public Economics Section 8: Optimal Minimum Wage and Introduction to Capital Taxation Matteo Paradisi November 1, 2016 In this Section we develop a theoretical analysis of optimal minimum

Economics 2450A: Public Economics Section 8: Optimal Minimum Wage and Introduction to Capital Taxation Matteo Paradisi November 1, 2016 In this Section we develop a theoretical analysis of optimal minimum

Growth Theory: Review

Growth Theory: Review Lecture 1.1, Exogenous Growth Topics in Growth, Part 2 June 11, 2007 Lecture 1.1, Exogenous Growth 1/76 Topics in Growth, Part 2 Growth Accounting: Objective and Technical Framework

Growth Theory: Review Lecture 1.1, Exogenous Growth Topics in Growth, Part 2 June 11, 2007 Lecture 1.1, Exogenous Growth 1/76 Topics in Growth, Part 2 Growth Accounting: Objective and Technical Framework

Equilibrium Conditions for the Simple New Keynesian Model

Equilibrium Conditions for the Simple New Keynesian Model Lawrence J. Christiano August 4, 04 Baseline NK model with no capital and with a competitive labor market. private sector equilibrium conditions

Equilibrium Conditions for the Simple New Keynesian Model Lawrence J. Christiano August 4, 04 Baseline NK model with no capital and with a competitive labor market. private sector equilibrium conditions

Assumption 5. The technology is represented by a production function, F : R 3 + R +, F (K t, N t, A t )

") 6. Economic growth Let us recall the main facts on growth examined in the first chapter and add some additional ones. (1) Real output (per-worker) roughly grows at a constant rate (i.e. labor productivity

6. Economic growth Let us recall the main facts on growth examined in the first chapter and add some additional ones. (1) Real output (per-worker) roughly grows at a constant rate (i.e. labor productivity

ECON 582: The Neoclassical Growth Model (Chapter 8, Acemoglu)

") ECON 582: The Neoclassical Growth Model (Chapter 8, Acemoglu) Instructor: Dmytro Hryshko 1 / 21 Consider the neoclassical economy without population growth and technological progress. The optimal growth

ECON 582: The Neoclassical Growth Model (Chapter 8, Acemoglu) Instructor: Dmytro Hryshko 1 / 21 Consider the neoclassical economy without population growth and technological progress. The optimal growth

Dynamic (Stochastic) General Equilibrium and Growth

General Equilibrium and Growth") Dynamic (Stochastic) General Equilibrium and Growth Martin Ellison Nuffi eld College Michaelmas Term 2018 Martin Ellison (Nuffi eld) D(S)GE and Growth Michaelmas Term 2018 1 / 43 Macroeconomics is Dynamic

Dynamic (Stochastic) General Equilibrium and Growth Martin Ellison Nuffi eld College Michaelmas Term 2018 Martin Ellison (Nuffi eld) D(S)GE and Growth Michaelmas Term 2018 1 / 43 Macroeconomics is Dynamic

Online Appendix I: Wealth Inequality in the Standard Neoclassical Growth Model

Online Appendix I: Wealth Inequality in the Standard Neoclassical Growth Model Dan Cao Georgetown University Wenlan Luo Georgetown University July 2016 The textbook Ramsey-Cass-Koopman neoclassical growth

Online Appendix I: Wealth Inequality in the Standard Neoclassical Growth Model Dan Cao Georgetown University Wenlan Luo Georgetown University July 2016 The textbook Ramsey-Cass-Koopman neoclassical growth

Optimal Insurance of Search Risk

Optimal Insurance of Search Risk Mikhail Golosov Yale University and NBER Pricila Maziero University of Pennsylvania Guido Menzio University of Pennsylvania and NBER November 2011 Introduction Search and

Optimal Insurance of Search Risk Mikhail Golosov Yale University and NBER Pricila Maziero University of Pennsylvania Guido Menzio University of Pennsylvania and NBER November 2011 Introduction Search and

The Labor Market in the New Keynesian Model: Foundations of the Sticky Wage Approach and a Critical Commentary

The Labor Market in the New Keynesian Model: Foundations of the Sticky Wage Approach and a Critical Commentary Lawrence J. Christiano March 30, 2013 Baseline developed earlier: NK model with no capital

The Labor Market in the New Keynesian Model: Foundations of the Sticky Wage Approach and a Critical Commentary Lawrence J. Christiano March 30, 2013 Baseline developed earlier: NK model with no capital

The Solow Growth Model

The Solow Growth Model Lectures 5, 6 & 7 Topics in Macroeconomics Topic 2 October 20, 21 & 27, 2008 Lectures 5, 6 & 7 1/37 Topics in Macroeconomics From Growth Accounting to the Solow Model Goal 1: Stylized

The Solow Growth Model Lectures 5, 6 & 7 Topics in Macroeconomics Topic 2 October 20, 21 & 27, 2008 Lectures 5, 6 & 7 1/37 Topics in Macroeconomics From Growth Accounting to the Solow Model Goal 1: Stylized

Economics 210B Due: September 16, Problem Set 10. s.t. k t+1 = R(k t c t ) for all t 0, and k 0 given, lim. and

for all t 0, and k 0 given, lim. and") Economics 210B Due: September 16, 2010 Problem 1: Constant returns to saving Consider the following problem. c0,k1,c1,k2,... β t Problem Set 10 1 α c1 α t s.t. k t+1 = R(k t c t ) for all t 0, and k 0

Economics 210B Due: September 16, 2010 Problem 1: Constant returns to saving Consider the following problem. c0,k1,c1,k2,... β t Problem Set 10 1 α c1 α t s.t. k t+1 = R(k t c t ) for all t 0, and k 0

Part A: Answer question A1 (required), plus either question A2 or A3.

, plus either question A2 or A3.") Ph.D. Core Exam -- Macroeconomics 5 January 2015 -- 8:00 am to 3:00 pm Part A: Answer question A1 (required), plus either question A2 or A3. A1 (required): Ending Quantitative Easing Now that the U.S.

Ph.D. Core Exam -- Macroeconomics 5 January 2015 -- 8:00 am to 3:00 pm Part A: Answer question A1 (required), plus either question A2 or A3. A1 (required): Ending Quantitative Easing Now that the U.S.

Chapter 7. Endogenous Growth II: R&D and Technological Change

Chapter 7 Endogenous Growth II: R&D and Technological Change 225 Economic Growth: Lecture Notes 7.1 Expanding Product Variety: The Romer Model There are three sectors: one for the final good sector, one

Chapter 7 Endogenous Growth II: R&D and Technological Change 225 Economic Growth: Lecture Notes 7.1 Expanding Product Variety: The Romer Model There are three sectors: one for the final good sector, one

Problem 1 (30 points)

") Problem (30 points) Prof. Robert King Consider an economy in which there is one period and there are many, identical households. Each household derives utility from consumption (c), leisure (l) and a public

Problem (30 points) Prof. Robert King Consider an economy in which there is one period and there are many, identical households. Each household derives utility from consumption (c), leisure (l) and a public

Economic Growth: Lecture 8, Overlapping Generations

14.452 Economic Growth: Lecture 8, Overlapping Generations Daron Acemoglu MIT November 20, 2018 Daron Acemoglu (MIT) Economic Growth Lecture 8 November 20, 2018 1 / 46 Growth with Overlapping Generations

14.452 Economic Growth: Lecture 8, Overlapping Generations Daron Acemoglu MIT November 20, 2018 Daron Acemoglu (MIT) Economic Growth Lecture 8 November 20, 2018 1 / 46 Growth with Overlapping Generations

The Real Business Cycle Model

The Real Business Cycle Model Macroeconomics II 2 The real business cycle model. Introduction This model explains the comovements in the fluctuations of aggregate economic variables around their trend.

The Real Business Cycle Model Macroeconomics II 2 The real business cycle model. Introduction This model explains the comovements in the fluctuations of aggregate economic variables around their trend.

Macroeconomics Qualifying Examination

Macroeconomics Qualifying Examination August 2015 Department of Economics UNC Chapel Hill Instructions: This examination consists of 4 questions. Answer all questions. If you believe a question is ambiguously

Macroeconomics Qualifying Examination August 2015 Department of Economics UNC Chapel Hill Instructions: This examination consists of 4 questions. Answer all questions. If you believe a question is ambiguously

Growth Theory: Review

Growth Theory: Review Lecture 1, Endogenous Growth Economic Policy in Development 2, Part 2 March 2009 Lecture 1, Exogenous Growth 1/104 Economic Policy in Development 2, Part 2 Outline Growth Accounting

Growth Theory: Review Lecture 1, Endogenous Growth Economic Policy in Development 2, Part 2 March 2009 Lecture 1, Exogenous Growth 1/104 Economic Policy in Development 2, Part 2 Outline Growth Accounting

Solution to Homework 2 - Exogeneous Growth Models

Solution to Homework 2 - Exogeneous Growth Models ECO-3211 Macroeconomia Aplicada (Applied Macroeconomics Question 1: Solow Model with a Fixed Factor 1 The law of motion for capital in the Solow economy

Solution to Homework 2 - Exogeneous Growth Models ECO-3211 Macroeconomia Aplicada (Applied Macroeconomics Question 1: Solow Model with a Fixed Factor 1 The law of motion for capital in the Solow economy

1 Bewley Economies with Aggregate Uncertainty

1 Bewley Economies with Aggregate Uncertainty Sofarwehaveassumedawayaggregatefluctuations (i.e., business cycles) in our description of the incomplete-markets economies with uninsurable idiosyncratic risk

1 Bewley Economies with Aggregate Uncertainty Sofarwehaveassumedawayaggregatefluctuations (i.e., business cycles) in our description of the incomplete-markets economies with uninsurable idiosyncratic risk

RBC Model with Indivisible Labor. Advanced Macroeconomic Theory

RBC Model with Indivisible Labor Advanced Macroeconomic Theory 1 Last Class What are business cycles? Using HP- lter to decompose data into trend and cyclical components Business cycle facts Standard RBC

RBC Model with Indivisible Labor Advanced Macroeconomic Theory 1 Last Class What are business cycles? Using HP- lter to decompose data into trend and cyclical components Business cycle facts Standard RBC

Foundations of Modern Macroeconomics B. J. Heijdra & F. van der Ploeg Chapter 9: Search in the Labour Market

Foundations of Modern Macroeconomics: Chapter 9 1 Foundations of Modern Macroeconomics B. J. Heijdra & F. van der Ploeg Chapter 9: Search in the Labour Market Foundations of Modern Macroeconomics: Chapter

Foundations of Modern Macroeconomics: Chapter 9 1 Foundations of Modern Macroeconomics B. J. Heijdra & F. van der Ploeg Chapter 9: Search in the Labour Market Foundations of Modern Macroeconomics: Chapter

Economic Growth: Lectures 5-7, Neoclassical Growth

14.452 Economic Growth: Lectures 5-7, Neoclassical Growth Daron Acemoglu MIT November 7, 9 and 14, 2017. Daron Acemoglu (MIT) Economic Growth Lectures 5-7 November 7, 9 and 14, 2017. 1 / 83 Introduction

14.452 Economic Growth: Lectures 5-7, Neoclassical Growth Daron Acemoglu MIT November 7, 9 and 14, 2017. Daron Acemoglu (MIT) Economic Growth Lectures 5-7 November 7, 9 and 14, 2017. 1 / 83 Introduction

h Edition Money in Search Equilibrium

In the Name of God Sharif University of Technology Graduate School of Management and Economics Money in Search Equilibrium Diamond (1984) Navid Raeesi Spring 2014 Page 1 Introduction: Markets with Search

In the Name of God Sharif University of Technology Graduate School of Management and Economics Money in Search Equilibrium Diamond (1984) Navid Raeesi Spring 2014 Page 1 Introduction: Markets with Search

TOBB-ETU - Econ 532 Practice Problems II (Solutions)

") TOBB-ETU - Econ 532 Practice Problems II (Solutions) Q: Ramsey Model: Exponential Utility Assume that in nite-horizon households maximize a utility function of the exponential form 1R max U = e (n )t (1=)e

TOBB-ETU - Econ 532 Practice Problems II (Solutions) Q: Ramsey Model: Exponential Utility Assume that in nite-horizon households maximize a utility function of the exponential form 1R max U = e (n )t (1=)e

Dynamic stochastic general equilibrium models. December 4, 2007

Dynamic stochastic general equilibrium models December 4, 2007 Dynamic stochastic general equilibrium models Random shocks to generate trajectories that look like the observed national accounts. Rational

Dynamic stochastic general equilibrium models December 4, 2007 Dynamic stochastic general equilibrium models Random shocks to generate trajectories that look like the observed national accounts. Rational

Permanent Income Hypothesis Intro to the Ramsey Model

Consumption and Savings Permanent Income Hypothesis Intro to the Ramsey Model Lecture 10 Topics in Macroeconomics November 6, 2007 Lecture 10 1/18 Topics in Macroeconomics Consumption and Savings Outline

Consumption and Savings Permanent Income Hypothesis Intro to the Ramsey Model Lecture 10 Topics in Macroeconomics November 6, 2007 Lecture 10 1/18 Topics in Macroeconomics Consumption and Savings Outline

Economic Growth: Lecture 12, Directed Technological Change

14.452 Economic Growth: Lecture 12, Directed Technological Change Daron Acemoglu MIT December 6, 2018 Daron Acemoglu (MIT) Economic Growth Lecture12 December 6, 2018 1 / 62 Directed Technological Change

14.452 Economic Growth: Lecture 12, Directed Technological Change Daron Acemoglu MIT December 6, 2018 Daron Acemoglu (MIT) Economic Growth Lecture12 December 6, 2018 1 / 62 Directed Technological Change

ECON 5118 Macroeconomic Theory

ECON 5118 Macroeconomic Theory Winter 013 Test 1 February 1, 013 Answer ALL Questions Time Allowed: 1 hour 0 min Attention: Please write your answers on the answer book provided Use the right-side pages

ECON 5118 Macroeconomic Theory Winter 013 Test 1 February 1, 013 Answer ALL Questions Time Allowed: 1 hour 0 min Attention: Please write your answers on the answer book provided Use the right-side pages

Endogenous IPR and Economic Growth

Endogenous IPR and Economic Growth Andreas Schäfer University of Leipzig Maik T. Schneider ETH Zurich Preliminary version 8. May 2008 Abstract Why are intellectual property rights in some countries higher

Endogenous IPR and Economic Growth Andreas Schäfer University of Leipzig Maik T. Schneider ETH Zurich Preliminary version 8. May 2008 Abstract Why are intellectual property rights in some countries higher

Economic Growth: Lectures 10 and 11, Endogenous Technological Change

14.452 Economic Growth: Lectures 10 and 11, Endogenous Technological Change Daron Acemoglu MIT Nov. 30 and Dec. 5, 2017. Daron Acemoglu (MIT) Economic Growth Lectures 10 and 11 Nov. 30 and Dec. 5, 2017.

14.452 Economic Growth: Lectures 10 and 11, Endogenous Technological Change Daron Acemoglu MIT Nov. 30 and Dec. 5, 2017. Daron Acemoglu (MIT) Economic Growth Lectures 10 and 11 Nov. 30 and Dec. 5, 2017.

Mortenson Pissarides Model

Mortenson Pissarides Model Prof. Lutz Hendricks Econ720 November 22, 2017 1 / 47 Mortenson / Pissarides Model Search models are popular in many contexts: labor markets, monetary theory, etc. They are distinguished

Mortenson Pissarides Model Prof. Lutz Hendricks Econ720 November 22, 2017 1 / 47 Mortenson / Pissarides Model Search models are popular in many contexts: labor markets, monetary theory, etc. They are distinguished

14.461: Technological Change, Lectures 1 and 2 Review of Models of Endogenous Technological Change

14.461: Technological Change, Lectures 1 and 2 Review of Models of Endogenous Technological Change Daron Acemoglu MIT September 7 and 12, 2011. Daron Acemoglu (MIT) Review of Endogenous Technology September

14.461: Technological Change, Lectures 1 and 2 Review of Models of Endogenous Technological Change Daron Acemoglu MIT September 7 and 12, 2011. Daron Acemoglu (MIT) Review of Endogenous Technology September

Small Open Economy RBC Model Uribe, Chapter 4

Small Open Economy RBC Model Uribe, Chapter 4 1 Basic Model 1.1 Uzawa Utility E 0 t=0 θ t U (c t, h t ) θ 0 = 1 θ t+1 = β (c t, h t ) θ t ; β c < 0; β h > 0. Time-varying discount factor With a constant

Small Open Economy RBC Model Uribe, Chapter 4 1 Basic Model 1.1 Uzawa Utility E 0 t=0 θ t U (c t, h t ) θ 0 = 1 θ t+1 = β (c t, h t ) θ t ; β c < 0; β h > 0. Time-varying discount factor With a constant

Macroeconomics Qualifying Examination

Macroeconomics Qualifying Examination January 2016 Department of Economics UNC Chapel Hill Instructions: This examination consists of 3 questions. Answer all questions. If you believe a question is ambiguously

Macroeconomics Qualifying Examination January 2016 Department of Economics UNC Chapel Hill Instructions: This examination consists of 3 questions. Answer all questions. If you believe a question is ambiguously

Macroeconomics Qualifying Examination

Macroeconomics Qualifying Examination August 2016 Department of Economics UNC Chapel Hill Instructions: This examination consists of 4 questions. Answer all questions. If you believe a question is ambiguously

Macroeconomics Qualifying Examination August 2016 Department of Economics UNC Chapel Hill Instructions: This examination consists of 4 questions. Answer all questions. If you believe a question is ambiguously

UNIVERSITY OF WISCONSIN DEPARTMENT OF ECONOMICS MACROECONOMICS THEORY Preliminary Exam August 1, :00 am - 2:00 pm

UNIVERSITY OF WISCONSIN DEPARTMENT OF ECONOMICS MACROECONOMICS THEORY Preliminary Exam August 1, 2017 9:00 am - 2:00 pm INSTRUCTIONS Please place a completed label (from the label sheet provided) on the

UNIVERSITY OF WISCONSIN DEPARTMENT OF ECONOMICS MACROECONOMICS THEORY Preliminary Exam August 1, 2017 9:00 am - 2:00 pm INSTRUCTIONS Please place a completed label (from the label sheet provided) on the

1 The Basic RBC Model

IHS 2016, Macroeconomics III Michael Reiter Ch. 1: Notes on RBC Model 1 1 The Basic RBC Model 1.1 Description of Model Variables y z k L c I w r output level of technology (exogenous) capital at end of

IHS 2016, Macroeconomics III Michael Reiter Ch. 1: Notes on RBC Model 1 1 The Basic RBC Model 1.1 Description of Model Variables y z k L c I w r output level of technology (exogenous) capital at end of

Lecture 6, January 7 and 15: Sticky Wages and Prices (Galí, Chapter 6)

") MakØk3, Fall 2012/2013 (Blok 2) Business cycles and monetary stabilization policies Henrik Jensen Department of Economics University of Copenhagen Lecture 6, January 7 and 15: Sticky Wages and Prices (Galí,

MakØk3, Fall 2012/2013 (Blok 2) Business cycles and monetary stabilization policies Henrik Jensen Department of Economics University of Copenhagen Lecture 6, January 7 and 15: Sticky Wages and Prices (Galí,

Foundations for the New Keynesian Model. Lawrence J. Christiano

Foundations for the New Keynesian Model Lawrence J. Christiano Objective Describe a very simple model economy with no monetary frictions. Describe its properties. markets work well Modify the model to

Foundations for the New Keynesian Model Lawrence J. Christiano Objective Describe a very simple model economy with no monetary frictions. Describe its properties. markets work well Modify the model to

Lecture 2 The Centralized Economy

Lecture 2 The Centralized Economy Economics 5118 Macroeconomic Theory Kam Yu Winter 2013 Outline 1 Introduction 2 The Basic DGE Closed Economy 3 Golden Rule Solution 4 Optimal Solution The Euler Equation

Lecture 2 The Centralized Economy Economics 5118 Macroeconomic Theory Kam Yu Winter 2013 Outline 1 Introduction 2 The Basic DGE Closed Economy 3 Golden Rule Solution 4 Optimal Solution The Euler Equation

Capital Structure and Investment Dynamics with Fire Sales

Capital Structure and Investment Dynamics with Fire Sales Douglas Gale Piero Gottardi NYU April 23, 2013 Douglas Gale, Piero Gottardi (NYU) Capital Structure April 23, 2013 1 / 55 Introduction Corporate

Capital Structure and Investment Dynamics with Fire Sales Douglas Gale Piero Gottardi NYU April 23, 2013 Douglas Gale, Piero Gottardi (NYU) Capital Structure April 23, 2013 1 / 55 Introduction Corporate

Solow Growth Model. Michael Bar. February 28, Introduction Some facts about modern growth Questions... 4

Solow Growth Model Michael Bar February 28, 208 Contents Introduction 2. Some facts about modern growth........................ 3.2 Questions..................................... 4 2 The Solow Model 5

Solow Growth Model Michael Bar February 28, 208 Contents Introduction 2. Some facts about modern growth........................ 3.2 Questions..................................... 4 2 The Solow Model 5

Introduction to Continuous-Time Dynamic Optimization: Optimal Control Theory

Econ 85/Chatterjee Introduction to Continuous-ime Dynamic Optimization: Optimal Control heory 1 States and Controls he concept of a state in mathematical modeling typically refers to a specification of

Econ 85/Chatterjee Introduction to Continuous-ime Dynamic Optimization: Optimal Control heory 1 States and Controls he concept of a state in mathematical modeling typically refers to a specification of

This process was named creative destruction by Joseph Schumpeter.

This process was named creative destruction by Joseph Schumpeter. Aghion and Howitt (1992) formalized Schumpeter s ideas in a growth model of the type we have been studying. A simple version of their model

This process was named creative destruction by Joseph Schumpeter. Aghion and Howitt (1992) formalized Schumpeter s ideas in a growth model of the type we have been studying. A simple version of their model

Endogenous Growth Theory

Endogenous Growth Theory Lecture Notes for the winter term 2010/2011 Ingrid Ott Tim Deeken October 21st, 2010 CHAIR IN ECONOMIC POLICY KIT University of the State of Baden-Wuerttemberg and National Laboratory

Endogenous Growth Theory Lecture Notes for the winter term 2010/2011 Ingrid Ott Tim Deeken October 21st, 2010 CHAIR IN ECONOMIC POLICY KIT University of the State of Baden-Wuerttemberg and National Laboratory

Economic Growth: Lectures 12 and 13, Directed Technological Change and Applications

14.452 Economic Growth: Lectures 12 and 13, Directed Technological Change and Applications Daron Acemoglu MIT December 8 and 13, 2016. Daron Acemoglu (MIT) Economic Growth Lectures 12 and 13 December 8

14.452 Economic Growth: Lectures 12 and 13, Directed Technological Change and Applications Daron Acemoglu MIT December 8 and 13, 2016. Daron Acemoglu (MIT) Economic Growth Lectures 12 and 13 December 8

Lecture 4 The Centralized Economy: Extensions

Lecture 4 The Centralized Economy: Extensions Leopold von Thadden University of Mainz and ECB (on leave) Advanced Macroeconomics, Winter Term 2013 1 / 36 I Motivation This Lecture considers some applications

Lecture 4 The Centralized Economy: Extensions Leopold von Thadden University of Mainz and ECB (on leave) Advanced Macroeconomics, Winter Term 2013 1 / 36 I Motivation This Lecture considers some applications

Macroeconomics Theory II

Macroeconomics Theory II Francesco Franco Novasbe February 2016 Francesco Franco (Novasbe) Macroeconomics Theory II February 2016 1 / 8 The Social Planner Solution Notice no intertemporal issues (Y t =

Macroeconomics Theory II Francesco Franco Novasbe February 2016 Francesco Franco (Novasbe) Macroeconomics Theory II February 2016 1 / 8 The Social Planner Solution Notice no intertemporal issues (Y t =

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics Ph. D. Comprehensive Examination: Macroeconomics Fall, 202 Answer Key to Section 2 Questions Section. (Suggested Time: 45 Minutes) For 3 of

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics Ph. D. Comprehensive Examination: Macroeconomics Fall, 202 Answer Key to Section 2 Questions Section. (Suggested Time: 45 Minutes) For 3 of

Lecture notes on modern growth theory

Lecture notes on modern growth theory Part 2 Mario Tirelli Very preliminary material Not to be circulated without the permission of the author October 25, 2017 Contents 1. Introduction 1 2. Optimal economic

Lecture notes on modern growth theory Part 2 Mario Tirelli Very preliminary material Not to be circulated without the permission of the author October 25, 2017 Contents 1. Introduction 1 2. Optimal economic

Diamond-Mortensen-Pissarides Model

Diamond-Mortensen-Pissarides Model Dongpeng Liu Nanjing University March 2016 D. Liu (NJU) DMP 03/16 1 / 35 Introduction Motivation In the previous lecture, McCall s model was introduced McCall s model

Diamond-Mortensen-Pissarides Model Dongpeng Liu Nanjing University March 2016 D. Liu (NJU) DMP 03/16 1 / 35 Introduction Motivation In the previous lecture, McCall s model was introduced McCall s model

Lecture 5 Search and matching theory

Lecture 5 Search and matching theory Leszek Wincenciak, Ph.D. Warsaw University December 16th, 2009 2/48 Lecture outline: Introduction Search and matching theory Search and matching theory The dynamics

Lecture 5 Search and matching theory Leszek Wincenciak, Ph.D. Warsaw University December 16th, 2009 2/48 Lecture outline: Introduction Search and matching theory Search and matching theory The dynamics