More on Adaptive Learning and Applications in Monetary Policy. Noah Williams

|

|

|

- Lewis Bryant

- 5 years ago

- Views:

Transcription

1 More on Adaptive Learning and Applications in Monetary Policy Noah University of Wisconsin - Madison Econ 899

2 Beyond E-Stability: Perpetual Learning Orphanides and J. (2005). Lucas-type aggregate supply curve for inflation π t : π t+1 = φπ e t+1 + (1 φ)π t + αy t+1 + e t+1, Output gap y t+1 is set by monetary policy up to white noise control error y t+1 = x t + u t+1. Policy objective function L = (1 ω)var(y) + ωvar(π π ) gives rule x t = θ(π t π ). where under RE θ = θ P (ω, φ, α).

3 Perpetual Learning Under RE inflation satisfies π t = c 0 + c 1 π t 1 + v t. Under learning private agents estimate coefficients by constant gain (or discounted) least squares. Older data dated discounted at rate (1 ε). Discounting of data natural if agents are concerned to track structural shifts. There is empirical support for constant gain learning. With constant gain, LS estimates fluctuate randomly around ( c 0, c 1 ): there is perpetual learning and π e t+1 = c 0,t + c 1,t π t.

4 Perpetual Learning Results Perpetual learning increases inflation persistence. Naive application of RE policy leads to inefficient policy. Incorporating learning into policy response can lead to major improvement. Efficient policy is more hawkish, i.e. under learning policy should increase θ to reduce persistence. This helps guide expectations. Following a sequence of unanticipated inflation shocks, inflation doves (i.e. policy-makers with low θ) can do very poorly, as expectations become detached from RE. If agents know π and only estimate the AR(1) parameter the policy trade-off is more favorable.

5 Learning and inflation persistence Preceding analysis was an example of empirics based on calibration. Now we consider work that estimates learning dynamics (Milani 2005, 2007). The source of inflation persistence is subject to dispute. For good empirical fit, a backward-looking component is needed in the NK Phillips curve. The bulk of the literature assumes RE, but learning could be a reason for inflation persistence. Incorporate indexation to Calvo price setting: non-optimized prices indexed to past inflation. This yields π t γπ t 1 = δx t + βe t (π t+1 γπ t ) + u t, where x t is the output gap. Earlier work under RE finds γ 1.

6 Inflation under learning The preceding can be written as π t = γ 1 + βγ π t 1 + β 1 + βγ E t π t+1 + δ 1 + βγ x t + u t. For expectations assume a PLM π t = φ 0,t + φ 1,t π t 1 + ε t Agents use data {1, π i } t 1 0 to estimate φ 0, φ 1 using constant gain LS. The implied ALM is π t = βφ 0,t(1 + φ 1,t ) 1 + βγ + γ + βφ2 1,t 1 + βγ π t 1 + δ 1 + βγ x t + u t. Alternatively, could use with real marginal cost as the driving variable.

7 Empirical Model Data: GDP deflator, output gap is detrended GDP, real marginal cost is proxied by deviation of labor income share from 1960:01 to 2003:04. Initialization: agents initial parameter estimates obtained by using pre-sample data Methodology: PLM estimated from constant-gain learning using ε = Then estimate ALM using nonlinear LS, which separates learning effects from structural effects. Note: Simultaneous estimation of learning rule and the model would be much more ambitious.

8 Empirical Results PLM parameters: (i) φ 1,t initially low in 1950s and 60s, then higher (up to 0.958), then some decline to values above 0.8. (ii) φ 0,t initially low, then became much higher and then gradual decline after ALM structural estimates: Degree of indexation γ = (with output gap & ε = 0.015) and declining for higher ε. Model fit criterion (Schwartz BIC) suggest values ε (0.015, 0.03), with best fit at ε = Conclusion: Estimates for γ not significantly different from zero. Results are very different from those obtained under RE, which finds γ 1. Milani has also estimated full NK models under learning. He finds that also the degree of habit persistence is low in IS curve.

9 Learning by Policymakers So far have focused on learning by private agents and its implications for policy. However policymakers as well must learn about the economy. Beliefs of policymakers very influential, since they are large agents. Variation in beliefs or misspecification of model by policymakers can have a large impact on equilibrium dynamics. Sargent (1999) showed that misspecification and learning by policymakers can lead to temporary improvements in outcomes: Escaping Nash Inflation Model analyzed by Cho,, and Sargent (2002), Sargent and (2005), estimated by Sargent,, and Zha (2006)

10 The Conquest Model The economy is a simple rational expectations natural rate Phillips curve model: U n = u (π n ˆx n ) + σ 1 W 1n π n = x n + σ 2 W 2n ˆx n = x n Rational expectations: - Time consistency problem. - Nash inflation (u) > Ramsey inflation (0). Here: - Public has rational expectations. - Government doesn t know Phillips curve, learns adaptively.

11 The Government s Beliefs Government s Phillips curve model: Beliefs: γ = [γ 1, γ 1 ]. U n = γ 1 π n + γ 1 + η n, Can generalize to allow lags of inflation, unemployment in regression. Govt. treats regression error as orthogonal: ( [ ]) πn Ê η n = 0. 1 Use notation: Êg(γ, ξ n ) = 0.

12 The Government s Problem Based on estimates, each period government solves: ( ) min Ê U 2 x n + πn 2 n Results in feedback policy: x n = h(γ). A self-confirming equilibrium (SCE) is a vector γ such that the government s beliefs are confirmed by its observations: Eg(γ, ξ n ) = 0, where : - (U n, π n ) follow the true evolution given x n - x n solves government s problem given γ. Note: Unique SCE with Nash inflation level. If γ 1 = 0, x n = 0 : Ramsey outcome.

13 Adaptation of Beliefs Government updates beliefs γ n based on data. Sets inflation as h(γ n ). Govt. believes data are generated by: U n = α n 1Φ n + η n, (Eη 2 n = σ 2 ) α n = α n 1 + Λ n, (cov(λ n ) = V ) where Φ n = [π n, 1]. Update beliefs using CG RLS: γ n+1 = γ n + ɛrn 1 g(γ n, ξ n ) R n+1 = R n + ɛ(φ n Φ n R n ), Implicitly assumes V = ɛ 2 σ 2 E(ΦΦ ) 1 and σ = σ 1 (regression error=unemployment shocks) In this case, Kalman filter and RLS have same limits, different transient behavior. Sargent and (2005) study more general priors on V.

14 Learning in the Model Stability of SCE governed by same E-stability results as before. Find that SCE is E-stable, suggests beliefs should converge to it. However in simulations observe repeated episodes of decreases in inflation from Nash level down to Ramsey/commitment level of zero. The low inflation episodes are driven by reductions in government s estimated Phillips curve slope to near zero. Analyze the escape dynamics characterizing movements away from the SCE.

15 Conquest of American Inflation

16 Escape Dynamics Escape = beliefs fixed distance from SCE Convergence theorem probability of escape 0 as ε 0. For fixed ε, may be rare escapes. If an unlikely event occurs, it is very likely to occur in the most likely way. ( ), CWS determine: - most likely escape direction and full time path - probability of escape and bounds on escape times

17 Characterzing Escapes To find most likely escape path, find least cost perturbations v that push the beliefs out of a set G containing the SCE. Solve the least-squares control problem: s.t. 1 T S = inf { v,t} 2 0 γ = R 1 g(γ) + v γ(0) = γ, γ(t) / G. v(s) Q(γ(s)) 1 v(s)ds Minimizing path is most likely as w.p.1 all escape paths become close to minimizing path as ε 0. Times between escapes increase exponentially as ε 0, minimized value S determines rate of increase.

18 Distribution of Escapes

19 Direction of Escapes

20 Escape Paths

21 Interpretation of Results Starting at SCE, central bank downweights past observations. Occasionally will get a sequence of correlated shocks to inflation and unemployment. Implies unemployment varies less for a given inflation rate. Government reads this as a shift in Phillips curve toward more vertical. In response will cut inflation. Since have been near SCE, movements in intended inflation rate very influential for belief estimates. Leads to (locally) self-reinforcing dynamics: government believes Phillips curve even more vertical, cuts inflation more.

22 Implications of Results Once Phillips curve slope is zero, inflation set to zero. Economy remains near there for a while. Eventually shocks to inflation and unemployment make government pick up on true Phillips curve slope. Increases inflation, revises beliefs. But this process is slow. Government can temporarily learn to set optimal policy even if model is misspecified. Suggests lower inflation in US since 1970s may not be driven by changes in Fed s model, but just changes in estimates of that model. Does this story fit empirically?

23 Sargent,, Zha (2006) How to explain the Great Inflation of the 1970s, the decline in 1980s and relative stability in 1990s to the present? Has policy changed? Was it luck (shocks)? Is the improvement in outcomes sustainable? Can policy be modeled in a optimizing manner, rationalizing and explaining rise and fall in US inflation?

24 What We Do Develop structural model of learning with optimizing government. Able to explain rise & fall of inflation. Estimate and analyze predictions. Analyze intermediate and long run behavior of model. Interpretation of US experience: - Policy objective unchanged, but beliefs change over time. As in Sargent (1999), Primiceri (2003a) but different mechanism - Large shocks in 1970s accommodated, led to large inflation. - Not shocks vs. policy, but shocks policy s disinflation due to different govt. beliefs: Believed less or no Phillips curve tradeoff

25 A More General Model Economy: Expectational Phillips curve, govt. controls inflation u t u = θ 0 (π t E t 1 π t ) + θ 1 (π t 1 E t 2 π t 1 ) +τ 1 (u t 1 u ) + σ 1 w 1t, [w 1t N (0, 1)] π t = x t 1 + σ 2 w 2t, [w 2t N (0, 1)] Government problem: minê x t 1 β t ((π t π ) 2 + λ(u t u ) 2 ) t=1 subject to inflation equation and subjective model: u t = ˆα t t 1 Φ t + σw t, Φ t = [π t, π t 1, u t 1, π t 2, u t 2, 1] π t = f (ˆα t t 1 )Φ t

26 Government s Model Govt doesn t account for expectations misspecified model. Key identifying assumption: E [ Φ t (u t Φ tα) ] = 0 Govt always assumes it holds. Actually holds in a self-confirming equilibrium. Govt bases estimates ˆα t t 1 = E t 1 (α) on: u t = α tφ t + σw t, w t N (0, 1) α t = α t 1 + Λ t, Λ t N (0, V ) Updates ˆα t t 1 (and P t t 1 ) via Kalman filter

27 Estimation Estimate govt prior beliefs σ 2 and V along with structure. Fix β =.9936, λ = 1, π = 2, u = 1. Fix ˆα 1 0 on pre-sample regression from Estimate remaining: u, τ 1, θ 0, θ 1, ζ 1 = σ 2 1, ζ 2 = σ 2 2, and C P, C V s.t. C P C P = P 1 0, C V C V = V. Need to normalize σ 2 : would scale with beliefs P t t 1 and V. Set σ = σ 1 : Govt. prior var of u t shocks = true var. Use Bayesian methods (MLE similar). Gaussian likelihood L(I T φ), specify prior p(φ), maximize posterior: p(φ I T ) L (I T φ) p(φ)

28 Inference: Inflation Actual Lower band Higher band From March 1960 to December 2003 Actual vs one-step forecast with 90% error bands

29 Medium Run Dynamics So far have focused on fit one step ahead. Now look out to horizon of 4+ years. Take estimated initial conditions at each date, run 5000 Monte Carlo simulations going forward 50 periods. Focus on 1970s high inflation episodes and early 1980s disinflation. Assess model s implications for rise & fall.

30 Initial Condition: January, Actual Median forecast 10 Inflation rate (percent) Forecast months after 74:01

31 Initial Condition: April, Actual Median forecast 10 Inflation rate (percent) Forecast months after 80:04

32 Interpretation (Our) Previous research in this line has emphasized the time-consistency problem. [In contrast to Blinder (1998).] Not a major issue here: estimate small responses to inflation surprises. Nash inflation close to Ramsey (2.25 % vs. 2%). Government beliefs are still important, but so are shocks. Throughout early 1970s govt believed in Phillips curve tradeoff. One diagnostic: sum of coefficients on inflation. Implied very high perceived sacrifice ratio: very costly in unemployment terms to bring inflation down in response to a shock. Large shocks in 1970s were accommodated.

33 Government Beliefs 1 Sum of π coefs From March 1960 to December 2003 Sum of coefficients on π. If 0 no LR tradeoff.

34 Government s Perceived Sacrifice Ratio Perceived LR u u from switching to 2% inflation

35 Comparison to Literature Primiceri (2006): Different learning with same basic aim. - His fit is more comparable to a VAR. - Emphasizes high perceived sacrifice ratio, but also mismeasurement of natural rate. - Key difference theoretical: his main model is Keynesian, backward-looking. Cogley-Sargent (2006): Government has three different models, adapts weight it puts on them over time. Weight on Samuelson-Solow model low by mid-70s but very high losses if cut inflation, dominates.

36 South American Inflation: Sargent,, Zha (2009) In last 30 years several Latin American countries experienced repeated hyperinflations of % per month. What led to these, and how could they re-occur? Conventional view: Hyperinflation is a fiscal problem. But weak direct empirical results. Unorthodox view: Fiscal/monetary aspects not important. Our approach: Adaptive learning by private sector, time varying seignorage needs, time varying volatility. Minor departure from rational expectations allows us to fit data, provides insights on causes and consequences of hyperinflations. Rehabilitation of fiscal causes.

37 Adaptive and REE dynamics Mean adaptive dynamics and REE dynamics. π t β t G(β t ) π 1 π 2 β t H(β t )

38 Adaptive and REE dynamics Mean adaptive dynamics and REE dynamics. π t β t G(β t ) π 1 π 2 β t H(β t )

39 Adaptive dynamics and escapes Adaptive dynamics and the escape event. π t β t G(β t ) π 1 π 2 β t

40 Adaptive dynamics and escapes Adaptive dynamics and the escape event. π t β t G(β t ) π 1 π 2 β t

41 The Model Money demand: M t P t = 1 γ λ γ Government budget constraint: P e t+1 P t M t = θm t 1 + d t (s t )P t Deficit process, with regimes s t = [m t, v t ] (fiscal policy): d t (m t, v t ) = d(m t ) + η d t (v t ) Pr(m t+1 = i m t = j) = qij m, i, j = 1,..., m h Pr(v t+1 = i v t = j) = qij, v i, j = 1,..., v h {γ,d t (s t )} not identified, so normalize γ = 1 in estimation.

42 Beliefs Private sector forecasts inflation in setting money demand. Assume learns adaptively from past inflation observations. πt+1 b = β t β t = β t 1 + ε(π t 1 β t 1 ) ε is called the gain, giving weight on past observations. We assume it s constant: agents discount past data.

43 No-Breakdown Conditions Equilibrium inflation: π t = θ(1 λβ t 1) 1 λβ t d t (s t ) Makes sense only if numerator and denominator are both positive: Positive prices and positive real balances. For moments of inflation to exist, need denominator bounded away from zero. Thus we require, for some δ > 0: 1 λβ t 1 > 0, 1 λβ t d t (s t ) > δθ(1 λβ t 1 ), Leads to truncated normal distribution for η d.

44 Reforms Possible that a sequence of seignorage shocks pushes beliefs β t above high SS π2. Escape from domain of attraction of lower, stable equilibrium. Makes model unstable. May eventually threaten the no-breakdown conditions. Our solution: Reset inflation (to lower REE plus noise) after threatened breakdowns: π t = π t (s t ) π 1(s t ) + η π t (s t ) where η π is truncated normal. Stands in for cosmetic reforms (exchange rates, capital controls) which did not alter seignorage process. Beliefs may be slow to adjust reforms not immediately credible.

45 Estimation Our parameter estimates maximize the likelihood of a history of inflation, π t, t = 1,..., T. We use the model s joint density and the inflation data to estimate money creation rates and compare to data. The likelihood function is challenging numerically. Blocking and parallel computing come to our rescue.

46 Argentina Conditional SCEs Log Belief log β t βt 0.3 Deficits Data Model Probability 0.8 L deficit Escape log π t Actual Prediction

47 Argentina: Beliefs

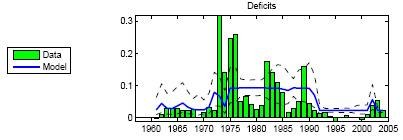

48 Argentina: Deficits

49 Argentina: Escapes and Regimes

50 Argentina: Inflation

51 Argentina Conditional SCEs Log Belief log β t βt 0.3 Deficits Data Model Probability 0.8 L deficit Escape log π t Actual Prediction

52 Brazil 0.5 Conditional SCEs 0.5 Log Belief log β t βt Data Model Deficits Probability 0.8 L & M deficit Escape log π t 0.6 Actual Prediction

53 The Rise and Fall of Hyperinflation Different hyperinflations were driven by different factors (escapes, shocks) and ended by different factors (monetary reform, fiscal deficit reform, smaller shocks). Table: Causes of the rise and fall of hyperinflation across countries Escape No Escape Monetary Reform Brazil (87-91) Peru (87-92) Fiscal Deficit Reform Argentina (87-91) Bolivia (82-86) Brazil (92-95) No Reform (Driven by Chile (71-78) Argentina (76-86) Deficit Shocks)

54 Conclusion Expectations play a large role in modern macroeconomics. People are smart, but boundedly rational. Cognitive consistency principle: economic agents should be about as smart as (good) economists, e.g. model agents as econometricians. Stability of RE under private agent learning is not automatic. Monetary policy must be designed to ensure both determinacy and stability under learning. Policymakers may need to use policy to guide expectations. Under learning there is the possibility of persistent deviations from RE. Appropriate policy design can minimize these risks. Learning dynamics can also help explain persistence of inflation and output dynamics, volatility of inflation, and rises and falls of inflation.

Learning and Monetary Policy. Lecture 4 Recent Applications of Learning to Monetary Policy

Learning and Monetary Policy Lecture 4 Recent Applications of Learning to Monetary Policy George W. Evans (University of Oregon) University of Paris X -Nanterre (September 2007) Lecture 4 Outline This

Learning and Monetary Policy Lecture 4 Recent Applications of Learning to Monetary Policy George W. Evans (University of Oregon) University of Paris X -Nanterre (September 2007) Lecture 4 Outline This

Adaptive Learning and Applications in Monetary Policy. Noah Williams

Adaptive Learning and Applications in Monetary Policy Noah University of Wisconsin - Madison Econ 899 Motivations J. C. Trichet: Understanding expectations formation as a process underscores the strategic

Adaptive Learning and Applications in Monetary Policy Noah University of Wisconsin - Madison Econ 899 Motivations J. C. Trichet: Understanding expectations formation as a process underscores the strategic

Recurent Hyperinflations and Learning

1 / 17 Recurent Hyperinflations and Learning Albert Marcet and Juan P. Nicolini (AER,2003) Manuel M. Mosquera T. UC3M November 24, 2015 2 / 17 Motivation of Literature Expectations play a key role in macroeconomics

1 / 17 Recurent Hyperinflations and Learning Albert Marcet and Juan P. Nicolini (AER,2003) Manuel M. Mosquera T. UC3M November 24, 2015 2 / 17 Motivation of Literature Expectations play a key role in macroeconomics

Evolution and Intelligent Design

Evolution and Intelligent Design Thomas J. Sargent April 2008 David Ricardo, 1816 The introduction of the precious metals for the purposes of money may with truth be considered as one of the most important

Evolution and Intelligent Design Thomas J. Sargent April 2008 David Ricardo, 1816 The introduction of the precious metals for the purposes of money may with truth be considered as one of the most important

Bayesian Econometrics of Learning Models (lecture notes for the Dynare learning workshop)

") Bayesian Econometrics of Learning Models (lecture notes for the Dynare learning workshop) Tao Zha Federal Reserve Bank of Atlanta October 25 Learning Models p. 1/93 Table of contents General framework.

Bayesian Econometrics of Learning Models (lecture notes for the Dynare learning workshop) Tao Zha Federal Reserve Bank of Atlanta October 25 Learning Models p. 1/93 Table of contents General framework.

FEDERAL RESERVE BANK of ATLANTA

FEDERAL RESERVE BANK of ATLANTA Shocks and Government Beliefs: The Rise and Fall of American Inflation Thomas Sargent, Noah Williams, and Tao Zha Working Paper 24-22 September 24 WORKING PAPER SERIES FEDERAL

FEDERAL RESERVE BANK of ATLANTA Shocks and Government Beliefs: The Rise and Fall of American Inflation Thomas Sargent, Noah Williams, and Tao Zha Working Paper 24-22 September 24 WORKING PAPER SERIES FEDERAL

NBER WORKING PAPER SERIES SHOCKS AND GOVERNMENT BELIEFS: THE RISE AND FALL OF AMERICAN INFLATION. Thomas Sargent Noah Williams Tao Zha

NBER WORKING PAPER SERIES SHOCKS AND GOVERNMENT BELIEFS: THE RISE AND FALL OF AMERICAN INFLATION Thomas Sargent Noah Williams Tao Zha Working Paper 1764 http://www.nber.org/papers/w1764 NATIONAL BUREAU

NBER WORKING PAPER SERIES SHOCKS AND GOVERNMENT BELIEFS: THE RISE AND FALL OF AMERICAN INFLATION Thomas Sargent Noah Williams Tao Zha Working Paper 1764 http://www.nber.org/papers/w1764 NATIONAL BUREAU

Expectations, Learning and Macroeconomic Policy

Expectations, Learning and Macroeconomic Policy George W. Evans (Univ. of Oregon and Univ. of St. Andrews) Lecture 4 Liquidity traps, learning and stagnation Evans, Guse & Honkapohja (EER, 2008), Evans

Expectations, Learning and Macroeconomic Policy George W. Evans (Univ. of Oregon and Univ. of St. Andrews) Lecture 4 Liquidity traps, learning and stagnation Evans, Guse & Honkapohja (EER, 2008), Evans

Learning and Monetary Policy

Learning and Monetary Policy Lecture 1 Introduction to Expectations and Adaptive Learning George W. Evans (University of Oregon) University of Paris X -Nanterre (September 2007) J. C. Trichet: Understanding

Learning and Monetary Policy Lecture 1 Introduction to Expectations and Adaptive Learning George W. Evans (University of Oregon) University of Paris X -Nanterre (September 2007) J. C. Trichet: Understanding

POLICY GAMES. u t = θ 0 θ 1 π t + ε t. (1) β t (u 2 t + ωπ 2 t ). (3)

β t (u 2 t + ωπ 2 t ). (3)") Eco5, Part II Spring C. Sims POLICY GAMES The policy authority believes 1. THE SAN JOSE MODEL u t = θ θ 1 π t + ε t. (1) In fact, though, u t = ū α (π t E t 1 π t ) + ξ t. () They minimize. POLICYMAKERS

Eco5, Part II Spring C. Sims POLICY GAMES The policy authority believes 1. THE SAN JOSE MODEL u t = θ θ 1 π t + ε t. (1) In fact, though, u t = ū α (π t E t 1 π t ) + ξ t. () They minimize. POLICYMAKERS

POLICY GAMES. u t = θ 0 θ 1 π t + ε t. (1) β t (u 2 t + ωπ 2 t ). (3) π t = g t 1 + ν t. (4) g t = θ 1θ 0 ω + θ 2 1. (5)

β t (u 2 t + ωπ 2 t ). (3) π t = g t 1 + ν t. (4) g t = θ 1θ 0 ω + θ 2 1. (5)") Eco504, Part II Spring 2004 C. Sims POLICY GAMES The policy authority believes In fact, though, 1. THE SAN JOSE MODEL u t = θ 0 θ 1 π t + ε t. (1) u t = ū α (π t E t 1 π t ) + ξ t. (2) They minimize 2.

Eco504, Part II Spring 2004 C. Sims POLICY GAMES The policy authority believes In fact, though, 1. THE SAN JOSE MODEL u t = θ 0 θ 1 π t + ε t. (1) u t = ū α (π t E t 1 π t ) + ξ t. (2) They minimize 2.

Eco504, Part II Spring 2008 C. Sims POLICY GAMES

Eco504, Part II Spring 2008 C. Sims POLICY GAMES The policy authority believes 1. THE SAN JOSE MODEL u t = θ 0 θ 1 π t + ε t. (1) In fact, though, u t = ū α (π t E t 1 π t ) + ξ t. (2) 2. POLICYMAKERS

Eco504, Part II Spring 2008 C. Sims POLICY GAMES The policy authority believes 1. THE SAN JOSE MODEL u t = θ 0 θ 1 π t + ε t. (1) In fact, though, u t = ū α (π t E t 1 π t ) + ξ t. (2) 2. POLICYMAKERS

THE CONQUEST OF SOUTH AMERICAN INFLATION

THE CONQUEST OF SOUTH AMERICAN INFLATION THOMAS SARGENT, NOAH WILLIAMS, AND TAO ZHA Abstract. We infer determinants of Latin American hyperinflations and stabilizations by using the method of maximum likelihood

THE CONQUEST OF SOUTH AMERICAN INFLATION THOMAS SARGENT, NOAH WILLIAMS, AND TAO ZHA Abstract. We infer determinants of Latin American hyperinflations and stabilizations by using the method of maximum likelihood

FEDERAL RESERVE BANK of ATLANTA

FEDERAL RESERVE BANK of ATLANTA The Conquest of South American Inflation Thomas Sargent, Noah Williams, and Tao Zha Working Paper 26-2 November 26 WORKING PAPER SERIES FEDERAL RESERVE BANK of ATLANTA WORKING

FEDERAL RESERVE BANK of ATLANTA The Conquest of South American Inflation Thomas Sargent, Noah Williams, and Tao Zha Working Paper 26-2 November 26 WORKING PAPER SERIES FEDERAL RESERVE BANK of ATLANTA WORKING

Indeterminacy and Sunspots in Macroeconomics

Indeterminacy and Sunspots in Macroeconomics Friday September 8 th : Lecture 10 Gerzensee, September 2017 Roger E. A. Farmer Warwick University and NIESR Topics for Lecture 10 Tying together the pieces

Indeterminacy and Sunspots in Macroeconomics Friday September 8 th : Lecture 10 Gerzensee, September 2017 Roger E. A. Farmer Warwick University and NIESR Topics for Lecture 10 Tying together the pieces

Identifying the Monetary Policy Shock Christiano et al. (1999)

") Identifying the Monetary Policy Shock Christiano et al. (1999) The question we are asking is: What are the consequences of a monetary policy shock a shock which is purely related to monetary conditions

Identifying the Monetary Policy Shock Christiano et al. (1999) The question we are asking is: What are the consequences of a monetary policy shock a shock which is purely related to monetary conditions

THE CONQUEST OF SOUTH AMERICAN INFLATION

THE CONQUEST OF SOUTH AMERICAN INFLATION THOMAS SARGENT, NOAH WILLIAMS, AND TAO ZHA Abstract. We infer determinants of Latin American hyperinflations and stabilizations by using the method of maximum likelihood

THE CONQUEST OF SOUTH AMERICAN INFLATION THOMAS SARGENT, NOAH WILLIAMS, AND TAO ZHA Abstract. We infer determinants of Latin American hyperinflations and stabilizations by using the method of maximum likelihood

Signaling Effects of Monetary Policy

Signaling Effects of Monetary Policy Leonardo Melosi London Business School 24 May 2012 Motivation Disperse information about aggregate fundamentals Morris and Shin (2003), Sims (2003), and Woodford (2002)

Signaling Effects of Monetary Policy Leonardo Melosi London Business School 24 May 2012 Motivation Disperse information about aggregate fundamentals Morris and Shin (2003), Sims (2003), and Woodford (2002)

Adaptive Learning in Macroeconomics: some methodological issues

Adaptive Learning in Macroeconomics: some methodological issues George W. Evans University of Oregon and University of St. Andrews INEXC Paris Conference June 27-29, 2012 J. C. Trichet: Understanding expectations

Adaptive Learning in Macroeconomics: some methodological issues George W. Evans University of Oregon and University of St. Andrews INEXC Paris Conference June 27-29, 2012 J. C. Trichet: Understanding expectations

Learning in Macroeconomic Models

Learning in Macroeconomic Models Wouter J. Den Haan London School of Economics c by Wouter J. Den Haan Overview A bit of history of economic thought How expectations are formed can matter in the long run

Learning in Macroeconomic Models Wouter J. Den Haan London School of Economics c by Wouter J. Den Haan Overview A bit of history of economic thought How expectations are formed can matter in the long run

The Return of the Gibson Paradox

The Return of the Gibson Paradox Timothy Cogley, Thomas J. Sargent, and Paolo Surico Conference to honor Warren Weber February 212 Introduction Previous work suggested a decline in inflation persistence

The Return of the Gibson Paradox Timothy Cogley, Thomas J. Sargent, and Paolo Surico Conference to honor Warren Weber February 212 Introduction Previous work suggested a decline in inflation persistence

A Discussion of Arouba, Cuba-Borda and Schorfheide: Macroeconomic Dynamics Near the ZLB: A Tale of Two Countries"

A Discussion of Arouba, Cuba-Borda and Schorfheide: Macroeconomic Dynamics Near the ZLB: A Tale of Two Countries" Morten O. Ravn, University College London, Centre for Macroeconomics and CEPR M.O. Ravn

A Discussion of Arouba, Cuba-Borda and Schorfheide: Macroeconomic Dynamics Near the ZLB: A Tale of Two Countries" Morten O. Ravn, University College London, Centre for Macroeconomics and CEPR M.O. Ravn

PANEL DISCUSSION: THE ROLE OF POTENTIAL OUTPUT IN POLICYMAKING

PANEL DISCUSSION: THE ROLE OF POTENTIAL OUTPUT IN POLICYMAKING James Bullard* Federal Reserve Bank of St. Louis 33rd Annual Economic Policy Conference St. Louis, MO October 17, 2008 Views expressed are

PANEL DISCUSSION: THE ROLE OF POTENTIAL OUTPUT IN POLICYMAKING James Bullard* Federal Reserve Bank of St. Louis 33rd Annual Economic Policy Conference St. Louis, MO October 17, 2008 Views expressed are

Macroeconomics II. Dynamic AD-AS model

Macroeconomics II Dynamic AD-AS model Vahagn Jerbashian Ch. 14 from Mankiw (2010) Spring 2018 Where we are heading to We will incorporate dynamics into the standard AD-AS model This will offer another

Macroeconomics II Dynamic AD-AS model Vahagn Jerbashian Ch. 14 from Mankiw (2010) Spring 2018 Where we are heading to We will incorporate dynamics into the standard AD-AS model This will offer another

Dynamic AD-AS model vs. AD-AS model Notes. Dynamic AD-AS model in a few words Notes. Notation to incorporate time-dimension Notes

Macroeconomics II Dynamic AD-AS model Vahagn Jerbashian Ch. 14 from Mankiw (2010) Spring 2018 Where we are heading to We will incorporate dynamics into the standard AD-AS model This will offer another

Macroeconomics II Dynamic AD-AS model Vahagn Jerbashian Ch. 14 from Mankiw (2010) Spring 2018 Where we are heading to We will incorporate dynamics into the standard AD-AS model This will offer another

Fiscal Multipliers in a Nonlinear World

Fiscal Multipliers in a Nonlinear World Jesper Lindé and Mathias Trabandt ECB-EABCN-Atlanta Nonlinearities Conference, December 15-16, 2014 Sveriges Riksbank and Federal Reserve Board December 16, 2014

Fiscal Multipliers in a Nonlinear World Jesper Lindé and Mathias Trabandt ECB-EABCN-Atlanta Nonlinearities Conference, December 15-16, 2014 Sveriges Riksbank and Federal Reserve Board December 16, 2014

Learning to Live in a Liquidity Trap

Jasmina Arifovic S. Schmitt-Grohé Martín Uribe Simon Fraser Columbia Columbia May 16, 218 1 The Starting Point In The Perils of Taylor Rules (JET,21), Benhabib, Schmitt- Grohé, and Uribe (BSU) show that

Jasmina Arifovic S. Schmitt-Grohé Martín Uribe Simon Fraser Columbia Columbia May 16, 218 1 The Starting Point In The Perils of Taylor Rules (JET,21), Benhabib, Schmitt- Grohé, and Uribe (BSU) show that

Forward Guidance without Common Knowledge

Forward Guidance without Common Knowledge George-Marios Angeletos 1 Chen Lian 2 1 MIT and NBER 2 MIT November 17, 2017 Outline 1 Introduction 2 Environment 3 GE Attenuation and Horizon Effects 4 Forward

Forward Guidance without Common Knowledge George-Marios Angeletos 1 Chen Lian 2 1 MIT and NBER 2 MIT November 17, 2017 Outline 1 Introduction 2 Environment 3 GE Attenuation and Horizon Effects 4 Forward

Monetary Policy and Unemployment: A New Keynesian Perspective

Monetary Policy and Unemployment: A New Keynesian Perspective Jordi Galí CREI, UPF and Barcelona GSE April 215 Jordi Galí (CREI, UPF and Barcelona GSE) Monetary Policy and Unemployment April 215 1 / 16

Monetary Policy and Unemployment: A New Keynesian Perspective Jordi Galí CREI, UPF and Barcelona GSE April 215 Jordi Galí (CREI, UPF and Barcelona GSE) Monetary Policy and Unemployment April 215 1 / 16

Taylor Rules and Technology Shocks

Taylor Rules and Technology Shocks Eric R. Sims University of Notre Dame and NBER January 17, 2012 Abstract In a standard New Keynesian model, a Taylor-type interest rate rule moves the equilibrium real

Taylor Rules and Technology Shocks Eric R. Sims University of Notre Dame and NBER January 17, 2012 Abstract In a standard New Keynesian model, a Taylor-type interest rate rule moves the equilibrium real

Searching for the Output Gap: Economic Variable or Statistical Illusion? Mark W. Longbrake* J. Huston McCulloch

Draft Draft Searching for the Output Gap: Economic Variable or Statistical Illusion? Mark W. Longbrake* The Ohio State University J. Huston McCulloch The Ohio State University August, 2007 Abstract This

Draft Draft Searching for the Output Gap: Economic Variable or Statistical Illusion? Mark W. Longbrake* The Ohio State University J. Huston McCulloch The Ohio State University August, 2007 Abstract This

ADVANCED MACROECONOMICS I

Name: Students ID: ADVANCED MACROECONOMICS I I. Short Questions (21/2 points each) Mark the following statements as True (T) or False (F) and give a brief explanation of your answer in each case. 1. 2.

Name: Students ID: ADVANCED MACROECONOMICS I I. Short Questions (21/2 points each) Mark the following statements as True (T) or False (F) and give a brief explanation of your answer in each case. 1. 2.

Lecture 4 The Centralized Economy: Extensions

Lecture 4 The Centralized Economy: Extensions Leopold von Thadden University of Mainz and ECB (on leave) Advanced Macroeconomics, Winter Term 2013 1 / 36 I Motivation This Lecture considers some applications

Lecture 4 The Centralized Economy: Extensions Leopold von Thadden University of Mainz and ECB (on leave) Advanced Macroeconomics, Winter Term 2013 1 / 36 I Motivation This Lecture considers some applications

Inflation Expectations and Monetary Policy Design: Evidence from the Laboratory

Inflation Expectations and Monetary Policy Design: Evidence from the Laboratory Damjan Pfajfar (CentER, University of Tilburg) and Blaž Žakelj (European University Institute) FRBNY Conference on Consumer

Inflation Expectations and Monetary Policy Design: Evidence from the Laboratory Damjan Pfajfar (CentER, University of Tilburg) and Blaž Žakelj (European University Institute) FRBNY Conference on Consumer

F11. Lecture 7. Inflation and Unemployment M&I 6. Adaptive vs Rational Expectations. M&B 19, p. 24

F11 Lecture 7 Inflation and Unemployment M&I 6 Adaptive vs Rational Expectations M&B 19, p. 24 Inflation and Unemployment Second of 3 motives gov t may have for ΔM/M, : 1. Inflationary Finance (Seigniorage)

F11 Lecture 7 Inflation and Unemployment M&I 6 Adaptive vs Rational Expectations M&B 19, p. 24 Inflation and Unemployment Second of 3 motives gov t may have for ΔM/M, : 1. Inflationary Finance (Seigniorage)

Douglas Laxton Economic Modeling Division January 30, 2014

Douglas Laxton Economic Modeling Division January 30, 2014 The GPM Team Produces quarterly projections before each WEO WEO numbers are produced by the country experts in the area departments Models used

Douglas Laxton Economic Modeling Division January 30, 2014 The GPM Team Produces quarterly projections before each WEO WEO numbers are produced by the country experts in the area departments Models used

Chapter 6. Maximum Likelihood Analysis of Dynamic Stochastic General Equilibrium (DSGE) Models

Models") Chapter 6. Maximum Likelihood Analysis of Dynamic Stochastic General Equilibrium (DSGE) Models Fall 22 Contents Introduction 2. An illustrative example........................... 2.2 Discussion...................................

Chapter 6. Maximum Likelihood Analysis of Dynamic Stochastic General Equilibrium (DSGE) Models Fall 22 Contents Introduction 2. An illustrative example........................... 2.2 Discussion...................................

New Keynesian Model Walsh Chapter 8

New Keynesian Model Walsh Chapter 8 1 General Assumptions Ignore variations in the capital stock There are differentiated goods with Calvo price stickiness Wages are not sticky Monetary policy is a choice

New Keynesian Model Walsh Chapter 8 1 General Assumptions Ignore variations in the capital stock There are differentiated goods with Calvo price stickiness Wages are not sticky Monetary policy is a choice

Aspects of Stickiness in Understanding Inflation

MPRA Munich Personal RePEc Archive Aspects of Stickiness in Understanding Inflation Minseong Kim 30 April 2016 Online at https://mpra.ub.uni-muenchen.de/71072/ MPRA Paper No. 71072, posted 5 May 2016 16:21

MPRA Munich Personal RePEc Archive Aspects of Stickiness in Understanding Inflation Minseong Kim 30 April 2016 Online at https://mpra.ub.uni-muenchen.de/71072/ MPRA Paper No. 71072, posted 5 May 2016 16:21

MA Macroeconomics 3. Introducing the IS-MP-PC Model

MA Macroeconomics 3. Introducing the IS-MP-PC Model Karl Whelan School of Economics, UCD Autumn 2014 Karl Whelan (UCD) Introducing the IS-MP-PC Model Autumn 2014 1 / 38 Beyond IS-LM We have reviewed the

MA Macroeconomics 3. Introducing the IS-MP-PC Model Karl Whelan School of Economics, UCD Autumn 2014 Karl Whelan (UCD) Introducing the IS-MP-PC Model Autumn 2014 1 / 38 Beyond IS-LM We have reviewed the

Lecture 7. The Dynamics of Market Equilibrium. ECON 5118 Macroeconomic Theory Winter Kam Yu Department of Economics Lakehead University

Lecture 7 The Dynamics of Market Equilibrium ECON 5118 Macroeconomic Theory Winter 2013 Phillips Department of Economics Lakehead University 7.1 Outline 1 2 3 4 5 Phillips Phillips 7.2 Market Equilibrium:

Lecture 7 The Dynamics of Market Equilibrium ECON 5118 Macroeconomic Theory Winter 2013 Phillips Department of Economics Lakehead University 7.1 Outline 1 2 3 4 5 Phillips Phillips 7.2 Market Equilibrium:

Eco504 Spring 2009 C. Sims MID-TERM EXAM

Eco504 Spring 2009 C. Sims MID-TERM EXAM This is a 90-minute exam. Answer all three questions, each of which is worth 30 points. You can get partial credit for partial answers. Do not spend disproportionate

Eco504 Spring 2009 C. Sims MID-TERM EXAM This is a 90-minute exam. Answer all three questions, each of which is worth 30 points. You can get partial credit for partial answers. Do not spend disproportionate

Learning to Optimize: Theory and Applications

Learning to Optimize: Theory and Applications George W. Evans University of Oregon and University of St Andrews Bruce McGough University of Oregon WAMS, December 12, 2015 Outline Introduction Shadow-price

Learning to Optimize: Theory and Applications George W. Evans University of Oregon and University of St Andrews Bruce McGough University of Oregon WAMS, December 12, 2015 Outline Introduction Shadow-price

Optimal Simple And Implementable Monetary and Fiscal Rules

Optimal Simple And Implementable Monetary and Fiscal Rules Stephanie Schmitt-Grohé Martín Uribe Duke University September 2007 1 Welfare-Based Policy Evaluation: Related Literature (ex: Rotemberg and Woodford,

Optimal Simple And Implementable Monetary and Fiscal Rules Stephanie Schmitt-Grohé Martín Uribe Duke University September 2007 1 Welfare-Based Policy Evaluation: Related Literature (ex: Rotemberg and Woodford,

Benefits from U.S. Monetary Policy Experimentation in the Days of Samuelson and Solow and Lucas

Benefits from U.S. Monetary Policy Experimentation in the Days of Samuelson and Solow and Lucas aaa Timothy Cogley, Riccardo Colacito and Thomas Sargent Monetary Policy Experimentation, FRB, Washington,

Benefits from U.S. Monetary Policy Experimentation in the Days of Samuelson and Solow and Lucas aaa Timothy Cogley, Riccardo Colacito and Thomas Sargent Monetary Policy Experimentation, FRB, Washington,

Source: US. Bureau of Economic Analysis Shaded areas indicate US recessions research.stlouisfed.org

Business Cycles 0 Real Gross Domestic Product 18,000 16,000 (Billions of Chained 2009 Dollars) 14,000 12,000 10,000 8,000 6,000 4,000 2,000 1940 1960 1980 2000 Source: US. Bureau of Economic Analysis Shaded

Business Cycles 0 Real Gross Domestic Product 18,000 16,000 (Billions of Chained 2009 Dollars) 14,000 12,000 10,000 8,000 6,000 4,000 2,000 1940 1960 1980 2000 Source: US. Bureau of Economic Analysis Shaded

Nowcasting Norwegian GDP

Nowcasting Norwegian GDP Knut Are Aastveit and Tørres Trovik May 13, 2007 Introduction Motivation The last decades of advances in information technology has made it possible to access a huge amount of

Nowcasting Norwegian GDP Knut Are Aastveit and Tørres Trovik May 13, 2007 Introduction Motivation The last decades of advances in information technology has made it possible to access a huge amount of

1.2. Structural VARs

1. Shocks Nr. 1 1.2. Structural VARs How to identify A 0? A review: Choleski (Cholesky?) decompositions. Short-run restrictions. Inequality restrictions. Long-run restrictions. Then, examples, applications,

1. Shocks Nr. 1 1.2. Structural VARs How to identify A 0? A review: Choleski (Cholesky?) decompositions. Short-run restrictions. Inequality restrictions. Long-run restrictions. Then, examples, applications,

The US Phillips Curve and inflation expectations: A State. Space Markov-Switching explanatory model.

The US Phillips Curve and inflation expectations: A State Space Markov-Switching explanatory model. Guillaume Guerrero Nicolas Million February 2004 We are grateful to P.Y Hénin, for helpful ideas and

The US Phillips Curve and inflation expectations: A State Space Markov-Switching explanatory model. Guillaume Guerrero Nicolas Million February 2004 We are grateful to P.Y Hénin, for helpful ideas and

Are Policy Counterfactuals Based on Structural VARs Reliable?

Are Policy Counterfactuals Based on Structural VARs Reliable? Luca Benati European Central Bank 2nd International Conference in Memory of Carlo Giannini 20 January 2010 The views expressed herein are personal,

Are Policy Counterfactuals Based on Structural VARs Reliable? Luca Benati European Central Bank 2nd International Conference in Memory of Carlo Giannini 20 January 2010 The views expressed herein are personal,

Identifying Aggregate Liquidity Shocks with Monetary Policy Shocks: An Application using UK Data

Identifying Aggregate Liquidity Shocks with Monetary Policy Shocks: An Application using UK Data Michael Ellington and Costas Milas Financial Services, Liquidity and Economic Activity Bank of England May

Identifying Aggregate Liquidity Shocks with Monetary Policy Shocks: An Application using UK Data Michael Ellington and Costas Milas Financial Services, Liquidity and Economic Activity Bank of England May

Forward Guidance without Common Knowledge

Forward Guidance without Common Knowledge George-Marios Angeletos Chen Lian November 9, 2017 MIT and NBER, MIT 1/30 Forward Guidance: Context or Pretext? How does the economy respond to news about the

Forward Guidance without Common Knowledge George-Marios Angeletos Chen Lian November 9, 2017 MIT and NBER, MIT 1/30 Forward Guidance: Context or Pretext? How does the economy respond to news about the

Adverse Effects of Monetary Policy Signalling

Adverse Effects of Monetary Policy Signalling Jan FILÁČEK and Jakub MATĚJŮ Monetary Department Czech National Bank CNB Research Open Day, 18 th May 21 Outline What do we mean by adverse effects of monetary

Adverse Effects of Monetary Policy Signalling Jan FILÁČEK and Jakub MATĚJŮ Monetary Department Czech National Bank CNB Research Open Day, 18 th May 21 Outline What do we mean by adverse effects of monetary

Perceived productivity and the natural rate of interest

Perceived productivity and the natural rate of interest Gianni Amisano and Oreste Tristani European Central Bank IRF 28 Frankfurt, 26 June Amisano-Tristani (European Central Bank) Productivity and the

Perceived productivity and the natural rate of interest Gianni Amisano and Oreste Tristani European Central Bank IRF 28 Frankfurt, 26 June Amisano-Tristani (European Central Bank) Productivity and the

Lecture 8: Aggregate demand and supply dynamics, closed economy case.

Lecture 8: Aggregate demand and supply dynamics, closed economy case. Ragnar Nymoen Department of Economics, University of Oslo October 20, 2008 1 Ch 17, 19 and 20 in IAM Since our primary concern is to

Lecture 8: Aggregate demand and supply dynamics, closed economy case. Ragnar Nymoen Department of Economics, University of Oslo October 20, 2008 1 Ch 17, 19 and 20 in IAM Since our primary concern is to

Toulouse School of Economics, Macroeconomics II Franck Portier. Homework 1 Solutions. Problem I An AD-AS Model

Toulouse School of Economics, 2009-200 Macroeconomics II Franck ortier Homework Solutions max Π = A FOC: d = ( A roblem I An AD-AS Model ) / ) 2 Equilibrium on the labor market: d = s = A and = = A Figure

Toulouse School of Economics, 2009-200 Macroeconomics II Franck ortier Homework Solutions max Π = A FOC: d = ( A roblem I An AD-AS Model ) / ) 2 Equilibrium on the labor market: d = s = A and = = A Figure

Learning and Global Dynamics

Learning and Global Dynamics James Bullard 10 February 2007 Learning and global dynamics The paper for this lecture is Liquidity Traps, Learning and Stagnation, by George Evans, Eran Guse, and Seppo Honkapohja.

Learning and Global Dynamics James Bullard 10 February 2007 Learning and global dynamics The paper for this lecture is Liquidity Traps, Learning and Stagnation, by George Evans, Eran Guse, and Seppo Honkapohja.

INFLATION AND UNEMPLOYMENT: THE PHILLIPS CURVE. Dongpeng Liu Department of Economics Nanjing University

INFLATION AND UNEMPLOYMENT: THE PHILLIPS CURVE Dongpeng Liu Department of Economics Nanjing University ROADMAP INCOME EXPENDITURE LIQUIDITY PREFERENCE IS CURVE LM CURVE SHORT-RUN IS-LM MODEL AGGREGATE

INFLATION AND UNEMPLOYMENT: THE PHILLIPS CURVE Dongpeng Liu Department of Economics Nanjing University ROADMAP INCOME EXPENDITURE LIQUIDITY PREFERENCE IS CURVE LM CURVE SHORT-RUN IS-LM MODEL AGGREGATE

General Examination in Macroeconomic Theory SPRING 2013

HARVARD UNIVERSITY DEPARTMENT OF ECONOMICS General Examination in Macroeconomic Theory SPRING 203 You have FOUR hours. Answer all questions Part A (Prof. Laibson): 48 minutes Part B (Prof. Aghion): 48

HARVARD UNIVERSITY DEPARTMENT OF ECONOMICS General Examination in Macroeconomic Theory SPRING 203 You have FOUR hours. Answer all questions Part A (Prof. Laibson): 48 minutes Part B (Prof. Aghion): 48

Modelling Czech and Slovak labour markets: A DSGE model with labour frictions

Modelling Czech and Slovak labour markets: A DSGE model with labour frictions Daniel Němec Faculty of Economics and Administrations Masaryk University Brno, Czech Republic nemecd@econ.muni.cz ESF MU (Brno)

Modelling Czech and Slovak labour markets: A DSGE model with labour frictions Daniel Němec Faculty of Economics and Administrations Masaryk University Brno, Czech Republic nemecd@econ.muni.cz ESF MU (Brno)

MA Macroeconomics 4. Analysing the IS-MP-PC Model

MA Macroeconomics 4. Analysing the IS-MP-PC Model Karl Whelan School of Economics, UCD Autumn 2014 Karl Whelan (UCD) Analysing the IS-MP-PC Model Autumn 2014 1 / 28 Part I Inflation Expectations Karl Whelan

MA Macroeconomics 4. Analysing the IS-MP-PC Model Karl Whelan School of Economics, UCD Autumn 2014 Karl Whelan (UCD) Analysing the IS-MP-PC Model Autumn 2014 1 / 28 Part I Inflation Expectations Karl Whelan

Expectations and Monetary Policy

Expectations and Monetary Policy Elena Gerko London Business School March 24, 2017 Abstract This paper uncovers a new channel of monetary policy in a New Keynesian DSGE model under the assumption of internal

Expectations and Monetary Policy Elena Gerko London Business School March 24, 2017 Abstract This paper uncovers a new channel of monetary policy in a New Keynesian DSGE model under the assumption of internal

The New Keynesian Model: Introduction

The New Keynesian Model: Introduction Vivaldo M. Mendes ISCTE Lisbon University Institute 13 November 2017 (Vivaldo M. Mendes) The New Keynesian Model: Introduction 13 November 2013 1 / 39 Summary 1 What

The New Keynesian Model: Introduction Vivaldo M. Mendes ISCTE Lisbon University Institute 13 November 2017 (Vivaldo M. Mendes) The New Keynesian Model: Introduction 13 November 2013 1 / 39 Summary 1 What

Learning and the Evolution of the Fed s Inflation Target

Learning and the Evolution of the Fed s Inflation Target Fabio Milani University of California, Irvine Abstract This paper tries to infer and compare the evolution of the Federal Reserve s(unobserved)

Learning and the Evolution of the Fed s Inflation Target Fabio Milani University of California, Irvine Abstract This paper tries to infer and compare the evolution of the Federal Reserve s(unobserved)

Strong Contagion with Weak Spillovers

Strong Contagion with Weak Spillovers Martin Ellison University of Warwick and CEPR Liam Graham University of Warwick Jouko Vilmunen Bank of Finland October 2004 Abstract In this paper, we develop a model

Strong Contagion with Weak Spillovers Martin Ellison University of Warwick and CEPR Liam Graham University of Warwick Jouko Vilmunen Bank of Finland October 2004 Abstract In this paper, we develop a model

1. Money in the utility function (start)

") Monetary Economics: Macro Aspects, 1/3 2012 Henrik Jensen Department of Economics University of Copenhagen 1. Money in the utility function (start) a. The basic money-in-the-utility function model b. Optimal

Monetary Economics: Macro Aspects, 1/3 2012 Henrik Jensen Department of Economics University of Copenhagen 1. Money in the utility function (start) a. The basic money-in-the-utility function model b. Optimal

The Lucas Imperfect Information Model

The Lucas Imperfect Information Model Based on the work of Lucas (972) and Phelps (970), the imperfect information model represents an important milestone in modern economics. The essential idea of the

The Lucas Imperfect Information Model Based on the work of Lucas (972) and Phelps (970), the imperfect information model represents an important milestone in modern economics. The essential idea of the

Generalized Stochastic Gradient Learning

Generalized Stochastic Gradient Learning George W. Evans University of Oregon Seppo Honkapohja Bank of Finland and University of Cambridge Noah Williams Princeton University and NBER May 18, 2008 Abstract

Generalized Stochastic Gradient Learning George W. Evans University of Oregon Seppo Honkapohja Bank of Finland and University of Cambridge Noah Williams Princeton University and NBER May 18, 2008 Abstract

A Dynamic Model of Aggregate Demand and Aggregate Supply

A Dynamic Model of Aggregate Demand and Aggregate Supply 1 Introduction Theoritical Backround 2 3 4 I Introduction Theoritical Backround The model emphasizes the dynamic nature of economic fluctuations.

A Dynamic Model of Aggregate Demand and Aggregate Supply 1 Introduction Theoritical Backround 2 3 4 I Introduction Theoritical Backround The model emphasizes the dynamic nature of economic fluctuations.

Discussion Global Dynamics at the Zero Lower Bound

Discussion Global Dynamics at the Zero Lower Bound Brent Bundick Federal Reserve Bank of Kansas City April 4 The opinions expressed in this discussion are those of the author and do not reflect the views

Discussion Global Dynamics at the Zero Lower Bound Brent Bundick Federal Reserve Bank of Kansas City April 4 The opinions expressed in this discussion are those of the author and do not reflect the views

Point, Interval, and Density Forecast Evaluation of Linear versus Nonlinear DSGE Models

Point, Interval, and Density Forecast Evaluation of Linear versus Nonlinear DSGE Models Francis X. Diebold Frank Schorfheide Minchul Shin University of Pennsylvania May 4, 2014 1 / 33 Motivation The use

Point, Interval, and Density Forecast Evaluation of Linear versus Nonlinear DSGE Models Francis X. Diebold Frank Schorfheide Minchul Shin University of Pennsylvania May 4, 2014 1 / 33 Motivation The use

Lessons of the long quiet ELB

Lessons of the long quiet ELB Comments on Monetary policy: Conventional and unconventional Nobel Symposium on Money and Banking John H. Cochrane Hoover Institution, Stanford University May 2018 1 / 20

Lessons of the long quiet ELB Comments on Monetary policy: Conventional and unconventional Nobel Symposium on Money and Banking John H. Cochrane Hoover Institution, Stanford University May 2018 1 / 20

Dynamics and Monetary Policy in a Fair Wage Model of the Business Cycle

Dynamics and Monetary Policy in a Fair Wage Model of the Business Cycle David de la Croix 1,3 Gregory de Walque 2 Rafael Wouters 2,1 1 dept. of economics, Univ. cath. Louvain 2 National Bank of Belgium

Dynamics and Monetary Policy in a Fair Wage Model of the Business Cycle David de la Croix 1,3 Gregory de Walque 2 Rafael Wouters 2,1 1 dept. of economics, Univ. cath. Louvain 2 National Bank of Belgium

Econ 5110 Solutions to the Practice Questions for the Midterm Exam

Econ 50 Solutions to the Practice Questions for the Midterm Exam Spring 202 Real Business Cycle Theory. Consider a simple neoclassical growth model (notation similar to class) where all agents are identical

Econ 50 Solutions to the Practice Questions for the Midterm Exam Spring 202 Real Business Cycle Theory. Consider a simple neoclassical growth model (notation similar to class) where all agents are identical

A Summary of Economic Methodology

A Summary of Economic Methodology I. The Methodology of Theoretical Economics All economic analysis begins with theory, based in part on intuitive insights that naturally spring from certain stylized facts,

A Summary of Economic Methodology I. The Methodology of Theoretical Economics All economic analysis begins with theory, based in part on intuitive insights that naturally spring from certain stylized facts,

The Return of the Wage Phillips Curve

The Return of the Wage Phillips Curve Jordi Galí CREI, UPF and Barcelona GSE March 2010 Jordi Galí (CREI, UPF and Barcelona GSE) The Return of the Wage Phillips Curve March 2010 1 / 15 Introduction Two

The Return of the Wage Phillips Curve Jordi Galí CREI, UPF and Barcelona GSE March 2010 Jordi Galí (CREI, UPF and Barcelona GSE) The Return of the Wage Phillips Curve March 2010 1 / 15 Introduction Two

Animal Spirits, Fundamental Factors and Business Cycle Fluctuations

Animal Spirits, Fundamental Factors and Business Cycle Fluctuations Stephane Dées Srečko Zimic Banque de France European Central Bank January 6, 218 Disclaimer Any views expressed represent those of the

Animal Spirits, Fundamental Factors and Business Cycle Fluctuations Stephane Dées Srečko Zimic Banque de France European Central Bank January 6, 218 Disclaimer Any views expressed represent those of the

Monetary Policy and Heterogeneous Expectations

Monetary Policy and Heterogeneous Expectations William A. Branch University of California, Irvine George W. Evans University of Oregon June 7, 9 Abstract This paper studies the implications for monetary

Monetary Policy and Heterogeneous Expectations William A. Branch University of California, Irvine George W. Evans University of Oregon June 7, 9 Abstract This paper studies the implications for monetary

Identification of the New Keynesian Phillips Curve: Problems and Consequences

MACROECONOMIC POLICY WORKSHOP: CENTRAL BANK OF CHILE The Relevance of the New Keynesian Phillips Curve Identification of the New Keynesian Phillips Curve: Problems and Consequences James. H. Stock Harvard

MACROECONOMIC POLICY WORKSHOP: CENTRAL BANK OF CHILE The Relevance of the New Keynesian Phillips Curve Identification of the New Keynesian Phillips Curve: Problems and Consequences James. H. Stock Harvard

THE CASE OF THE DISAPPEARING PHILLIPS CURVE

THE CASE OF THE DISAPPEARING PHILLIPS CURVE James Bullard President and CEO 2018 BOJ-IMES Conference Central Banking in a Changing World May 31, 2018 Tokyo, Japan Any opinions expressed here are my own

THE CASE OF THE DISAPPEARING PHILLIPS CURVE James Bullard President and CEO 2018 BOJ-IMES Conference Central Banking in a Changing World May 31, 2018 Tokyo, Japan Any opinions expressed here are my own

Behavioural & Experimental Macroeconomics: Some Recent Findings

Behavioural & Experimental Macroeconomics: Some Recent Findings Cars Hommes CeNDEF, University of Amsterdam MACFINROBODS Conference Goethe University, Frankfurt, Germany 3-4 April 27 Cars Hommes (CeNDEF,

Behavioural & Experimental Macroeconomics: Some Recent Findings Cars Hommes CeNDEF, University of Amsterdam MACFINROBODS Conference Goethe University, Frankfurt, Germany 3-4 April 27 Cars Hommes (CeNDEF,

Estimating Unobservable Inflation Expectations in the New Keynesian Phillips Curve

econometrics Article Estimating Unobservable Inflation Expectations in the New Keynesian Phillips Curve Francesca Rondina ID Department of Economics, University of Ottawa, 120 University Private, Ottawa,

econometrics Article Estimating Unobservable Inflation Expectations in the New Keynesian Phillips Curve Francesca Rondina ID Department of Economics, University of Ottawa, 120 University Private, Ottawa,

Model uncertainty and endogenous volatility

Review of Economic Dynamics 10 (2007) 207 237 www.elsevier.com/locate/red Model uncertainty and endogenous volatility William A. Branch a,, George W. Evans b a University of California, Irvine, USA b University

Review of Economic Dynamics 10 (2007) 207 237 www.elsevier.com/locate/red Model uncertainty and endogenous volatility William A. Branch a,, George W. Evans b a University of California, Irvine, USA b University

Ergodicity and Non-Ergodicity in Economics

Abstract An stochastic system is called ergodic if it tends in probability to a limiting form that is independent of the initial conditions. Breakdown of ergodicity gives rise to path dependence. We illustrate

Abstract An stochastic system is called ergodic if it tends in probability to a limiting form that is independent of the initial conditions. Breakdown of ergodicity gives rise to path dependence. We illustrate

A Bayesian DSGE Model with Infinite-Horizon Learning: Do Mechanical Sources of Persistence Become Superfluous?

A Bayesian DSGE Model with Infinite-Horizon Learning: Do Mechanical Sources of Persistence Become Superfluous? Fabio Milani University of California, Irvine This paper estimates a monetary DSGE model with

A Bayesian DSGE Model with Infinite-Horizon Learning: Do Mechanical Sources of Persistence Become Superfluous? Fabio Milani University of California, Irvine This paper estimates a monetary DSGE model with

Escape Dynamics in Learning Models

Escape Dynamics in Learning Models Noah Williams * Department of Economics, University of Wisconsin - Madison E-mail: nmwilliams@wisc.edu Revised January 28, 2009 Learning models have typically focused

Escape Dynamics in Learning Models Noah Williams * Department of Economics, University of Wisconsin - Madison E-mail: nmwilliams@wisc.edu Revised January 28, 2009 Learning models have typically focused

Can News be a Major Source of Aggregate Fluctuations?

Can News be a Major Source of Aggregate Fluctuations? A Bayesian DSGE Approach Ippei Fujiwara 1 Yasuo Hirose 1 Mototsugu 2 1 Bank of Japan 2 Vanderbilt University August 4, 2009 Contributions of this paper

Can News be a Major Source of Aggregate Fluctuations? A Bayesian DSGE Approach Ippei Fujiwara 1 Yasuo Hirose 1 Mototsugu 2 1 Bank of Japan 2 Vanderbilt University August 4, 2009 Contributions of this paper

On Determinacy and Learnability in a New Keynesian Model with Unemployment

On Determinacy and Learnability in a New Keynesian Model with Unemployment Mewael F. Tesfaselassie Eric Schaling This Version February 009 Abstract We analyze determinacy and stability under learning (E-stability)

On Determinacy and Learnability in a New Keynesian Model with Unemployment Mewael F. Tesfaselassie Eric Schaling This Version February 009 Abstract We analyze determinacy and stability under learning (E-stability)

Bayesian Econometrics - Computer section

Bayesian Econometrics - Computer section Leandro Magnusson Department of Economics Brown University Leandro Magnusson@brown.edu http://www.econ.brown.edu/students/leandro Magnusson/ April 26, 2006 Preliminary

Bayesian Econometrics - Computer section Leandro Magnusson Department of Economics Brown University Leandro Magnusson@brown.edu http://www.econ.brown.edu/students/leandro Magnusson/ April 26, 2006 Preliminary

Dynamic stochastic general equilibrium models. December 4, 2007

Dynamic stochastic general equilibrium models December 4, 2007 Dynamic stochastic general equilibrium models Random shocks to generate trajectories that look like the observed national accounts. Rational

Dynamic stochastic general equilibrium models December 4, 2007 Dynamic stochastic general equilibrium models Random shocks to generate trajectories that look like the observed national accounts. Rational

An Anatomy of the Business Cycle Data

An Anatomy of the Business Cycle Data G.M Angeletos, F. Collard and H. Dellas November 28, 2017 MIT and University of Bern 1 Motivation Main goal: Detect important regularities of business cycles data;

An Anatomy of the Business Cycle Data G.M Angeletos, F. Collard and H. Dellas November 28, 2017 MIT and University of Bern 1 Motivation Main goal: Detect important regularities of business cycles data;

A Modern Equilibrium Model. Jesús Fernández-Villaverde University of Pennsylvania

A Modern Equilibrium Model Jesús Fernández-Villaverde University of Pennsylvania 1 Household Problem Preferences: max E X β t t=0 c 1 σ t 1 σ ψ l1+γ t 1+γ Budget constraint: c t + k t+1 = w t l t + r t

A Modern Equilibrium Model Jesús Fernández-Villaverde University of Pennsylvania 1 Household Problem Preferences: max E X β t t=0 c 1 σ t 1 σ ψ l1+γ t 1+γ Budget constraint: c t + k t+1 = w t l t + r t

The Dornbusch overshooting model

4330 Lecture 8 Ragnar Nymoen 12 March 2012 References I Lecture 7: Portfolio model of the FEX market extended by money. Important concepts: monetary policy regimes degree of sterilization Monetary model

4330 Lecture 8 Ragnar Nymoen 12 March 2012 References I Lecture 7: Portfolio model of the FEX market extended by money. Important concepts: monetary policy regimes degree of sterilization Monetary model

Fundamental Disagreement

Fundamental Disagreement Philippe Andrade (Banque de France) Richard Crump (FRBNY) Stefano Eusepi (FRBNY) Emanuel Moench (Bundesbank) Price-setting and inflation Paris, Dec. 7 & 8, 5 The views expressed

Fundamental Disagreement Philippe Andrade (Banque de France) Richard Crump (FRBNY) Stefano Eusepi (FRBNY) Emanuel Moench (Bundesbank) Price-setting and inflation Paris, Dec. 7 & 8, 5 The views expressed

Indeterminacy and Learning: An Analysis of Monetary Policy in the Great Inflation

Indeterminacy and Learning: An Analysis of Monetary Policy in the Great Inflation Thomas A. Lubik Federal Reserve Bank of Richmond Christian Matthes Federal Reserve Bank of Richmond October 213 PRELIMINARY

Indeterminacy and Learning: An Analysis of Monetary Policy in the Great Inflation Thomas A. Lubik Federal Reserve Bank of Richmond Christian Matthes Federal Reserve Bank of Richmond October 213 PRELIMINARY

Estimating and Accounting for the Output Gap with Large Bayesian Vector Autoregressions

Estimating and Accounting for the Output Gap with Large Bayesian Vector Autoregressions James Morley 1 Benjamin Wong 2 1 University of Sydney 2 Reserve Bank of New Zealand The view do not necessarily represent

Estimating and Accounting for the Output Gap with Large Bayesian Vector Autoregressions James Morley 1 Benjamin Wong 2 1 University of Sydney 2 Reserve Bank of New Zealand The view do not necessarily represent

Monetary Policy and Unemployment: A New Keynesian Perspective

Monetary Policy and Unemployment: A New Keynesian Perspective Jordi Galí CREI, UPF and Barcelona GSE May 218 Jordi Galí (CREI, UPF and Barcelona GSE) Monetary Policy and Unemployment May 218 1 / 18 Introducing

Monetary Policy and Unemployment: A New Keynesian Perspective Jordi Galí CREI, UPF and Barcelona GSE May 218 Jordi Galí (CREI, UPF and Barcelona GSE) Monetary Policy and Unemployment May 218 1 / 18 Introducing

Topic 9. Monetary policy. Notes.

14.452. Topic 9. Monetary policy. Notes. Olivier Blanchard May 12, 2007 Nr. 1 Look at three issues: Time consistency. The inflation bias. The trade-off between inflation and activity. Implementation and

14.452. Topic 9. Monetary policy. Notes. Olivier Blanchard May 12, 2007 Nr. 1 Look at three issues: Time consistency. The inflation bias. The trade-off between inflation and activity. Implementation and

GCOE Discussion Paper Series

GCOE Discussion Paper Series Global COE Program Human Behavior and Socioeconomic Dynamics Discussion Paper No.34 Inflation Inertia and Optimal Delegation of Monetary Policy Keiichi Morimoto February 2009

GCOE Discussion Paper Series Global COE Program Human Behavior and Socioeconomic Dynamics Discussion Paper No.34 Inflation Inertia and Optimal Delegation of Monetary Policy Keiichi Morimoto February 2009

The New Keynesian Model

The New Keynesian Model Basic Issues Roberto Chang Rutgers January 2013 R. Chang (Rutgers) New Keynesian Model January 2013 1 / 22 Basic Ingredients of the New Keynesian Paradigm Representative agent paradigm

The New Keynesian Model Basic Issues Roberto Chang Rutgers January 2013 R. Chang (Rutgers) New Keynesian Model January 2013 1 / 22 Basic Ingredients of the New Keynesian Paradigm Representative agent paradigm