Asian Economic and Financial Review. SEASONAL ARIMA MODELLING OF NIGERIAN MONTHLY CRUDE OIL PRICES Ette Harrison Etuk

|

|

|

- Homer Higgins

- 5 years ago

- Views:

Transcription

1 Asian Economic and Financial Review journal homepage: SEASONAL ARIMA MODELLING OF NIGERIAN MONTHLY CRUDE OIL PRICES Ette Harrison Etuk Department of Mathematics/Computer Science Rivers State University of Science and Technology NIGERIA ABSTRACT The time plot of the series NCOP reveals a peak in 2008 and a depression in early The overall trend is horizontal and no seasonality is obvious. Twelve-month differencing yields SDNCOP exhibiting still a peak in 2008 and a trough in 2009, the overall trend being slightly positive and seasonality not easily discernible. Nonseasonal differencing of SDNCOP yields DSDNCOP with an overall horizontal trend and no obvious seasonality. However its correlogram reveals an autocorrelation structure of a seasonal model of order 12. Moreover it suggests the product of two moving average components both of order one, one non-seasonal and the other 12- month seasonal. The partial autocorrelation function suggests the involvement of a seasonal (i.e. 12-month) autoregressive component of order one. A (0, 1, 1)x(1, 1, 1) 12 autoregressive integrated moving average model was therefore proposed and fitted. It has been shown to be adequate. Keywords: Seasonal Time Series, ARIMA models, Crude Oil Prices, Nigeria. INTRODUCTION Many economic time series are seasonal. Its volatility notwithstanding, Nigerian monthly crude oil price series tends to exhibit some seasonality. Box and Jenkins (1976), Madsen (2008) and Boubaker (2011) are a few of authors that have written extensively on seasonal ARIMA models which are specially articulated for seasonal time series. This paper is focussed on the modelling of the prices by a multiplicative seasonal ARIMA model. Crude oil being the mainstay of the Nigerian economy, the modelling of its prices has engaged the attention of many researchers, a few of whom are Bolton (2012), King et al. (2012) and Salisu and Fasanya (2012). Seasonal ARIMA Models ARIMA modelling, proposed by Box and Jenkins (1976) is well known. However for the purpose of this paper, seasonal ARIMA modelling is briefly highlighted. 333

2 A time series {X t } is said to follow an autoregressive moving average model of order (p, q) (denoted by ARMA(p, q)) if it satisfies the following difference equation X t - 1X t-1-2x t px t-p = t + 1 t t q t-q (1) Or A(L)X t = B(L) t (2) Here A(L) = 1-1L - 2L pl p and B(L) = 1 + 1L + 2L ql q where L is the backward shift operator defined by L k X t = X t-k. Moreover the s and the s are constants such that the model is stationary and invertible, i.e. A(L) and B(L) have zeros all outside the unit circle respectively, and { t } is a sequence of uncorrelated random variables each with mean zero and constant variance called a white noise process. Most real life time series are non-stationary. Box and Jenkins (1976) proposed that differencing to an appropriate degree could render such a series stationary. Let d X t denote the d th difference of X t. Then = 1- L. If X t is replaced by d X t in (1), then the series {X t } is said to follow an autoregressive integrated moving average of order (p, d, q) designated ARIMA(p, d, q). Suppose the time series is seasonal of period s. Let D be the degree of seasonal differencing applied to the series d X t. The resultant series may be denoted by A time series {X t } is said to follow a multiplicative (p, d, q)x(p, D, Q) s seasonal ARIMA model if it satisfies the following equation d s D X t. A(L) (L s ) d s D X t = B(L) (L s ) t (3) where (L) = 1 +!L P L P and (L) = 1 + 1L QL Q and the s and s are constants such that the zeros of (L) and (L) are all outside of the unit circle for seasonal stationarity and invertibility, respectively. Box and Jenkins (1976), Priestley (1981), Madsen (2008), Surhatono. (2011) and Etuk (2012) are a few of the authors that have written extensively on seasonal ARIMA modelling. MATERIALS AND METHODS Data The data for this work are monthly Nigerian (Bonny Light) crude oil prices in US$/barrel from 2006 to 2011 obtainable from the website of the Central Bank of Nigeria, This 72-point time series shall be referred to as NCOP. Model Estimation A knowledge of the theoretical properties of ARIMA models helps a lot in their identification and estimation. An existent seasonality can be revealed by the time-plot. Where it is not so obvious 334

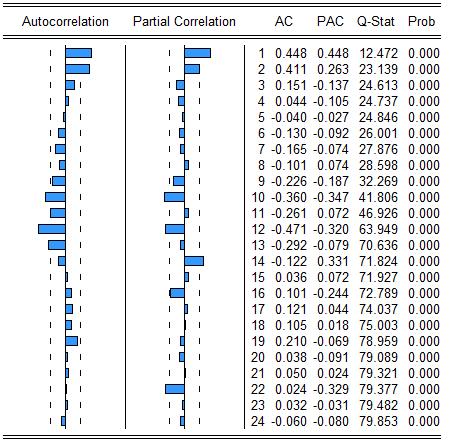

3 from the time plot, the autocorrelation plot or the correlogram shows it up. A significant spike at the seasonal lag on the correlogram suggests seasonality. A negative spike at the seasonal lag suggests the involvement of a seasonal moving average component. A positive spike at the seasonal lag suggests the involvement of a seasonal autoregressive component. In addition, if the autocorrelation function cuts off, the cut-off lag is an estimate of the non-seasonal moving average order, q. If, however, the partial autocorrelation plot cuts off, the cut-off lag is an estimate of the non-seasonal autoregressive order p. It has been advised that D + d < 3 to avoid undue model complexity. Once the model orders have been estimated, the model parameters may be estimated. Optimization criteria like the least error sum of squares criterion, the maximum likelihood criterion, the maximum entropy criterion, etc. may be used. Involvement of the white noise process in the definition of an ARMA process necessitates the application of non-linear optimization techniques for their estimation. Such a process involves iterations after an initial estimate has been made, each iteration being an improvement on the previous one until the process converges to an optimal solution. However, efforts have been made with some measure of success to use linear optimization techniques to estimate ARMA models (See for example, Oyetunji (1985), (Etuk, 1987; Etuk, 1998). In this work, the software Eviews, which is based on the least squares approach, shall be used. Diagnostic Checking A fitted model must be checked for goodness-of-fit to the data. Eviews has facilities for such purposes. In particular, some residual analysis shall be performed. Under the hypothesis of an adequate model, the residuals should be uncorrelated with zero mean and should follow a Gaussian distribution. RESULTS The time plot of the original series NCOP in Figure 1 reveals a peak in 2008 and a trough in A twelve-month differencing yields the series SDNCOP with a deep trough in 2009 (See Figure 2). A non-seasonal differencing of SDNCOP yields the series DSDNCOP which exhibits an overall horizontal trend with no obvious seasonality (See Figure 3). Its correlogram in Figure 4 shows significant spikes at lags 1, 11, 12 and 13, with autocorrelations at lags 11 and 13 fairly comparable. That can be interpreted as the autocorrelation structure of the product of two moving average components, each of order one: one seasonal (i.e. 12-month) and the other nonseasonal. Moreover the partial autocorrelation function, PAC, has a significant spike at lag 12, indicating the involvement of a seasonal autoregressive component of order one. The following (0, 1, 1)x(1, 1, 1) 12 multiplicative seasonal model is hereby proposed. That means the model is 335

4 DSDNCOP t = 12DSDNCOP t t + 12 t t-13 (4) An estimate of (4) is given in Table 1 as DSDNCOP t DSDNCOP t-12 = t t t-13 + t (5) ( ) ( ) ( ) ( ) In the model (5), only the MA(1) coefficient is not statistically significant, being less than twice its standard error. As much as 55% of the variation in DSDNCOP is explained by the model. The fitted model has been shown to agree closely with observations (See Figure 5). The residuals follow a fairly normal distribution with zero mean(except for two outliers between 20 and 30)(See Figure 6) and they are uncorrelated (See Figure 7). Therefore the model is adequate. CONCLUSION The Nigerian monthly crude oil price series has been shown to follow a (0, 1, 1)x(1, 1, 1) 12 seasonal ARIMA model. This has been shown to be adequate by various techniques. REFERENCES Bolton, P., Oil prices. Available from Boubaker, H.B.H., The forecasting performance of seasonal and nonlinear models. Asian Economic and Financial Review 1(1): Box, G.E.P. and G.M. Jenkins, Time series analysis, forecasing and control, holdenday, san francisco. Etuk, E.H., On the selection of autoregressive moving average models. An unpublished Ph. D. Thesis, Department of Statistics, University of Ibadan, Nigeria. Etuk, E.H., An autoregressive integrated moving average (arima) simulation mode. A Case Study. Discovery and Innovation, 10(1): Etuk, E.H., Predicting inflation rates of nigeria using a seasonal box-jenkins model. Journal of Statistical and Econometric Methods 1(3): King, K., A. Deng and D. Metz, An econometric analysis of oil price movements:. The Role of Political Events and Economic News, Financial Trading and Market Fundamentals. Bates White Economic Consulting. Available from Madsen, H., Time series analysis,. London: Chapman & Hall/CRC,. Oyetunji, O.B., Inverse autocorrelations and moving average time serie modelling.. Journal of Official Statistics, 1: Priestley, M.B., Spectral analysis and time series. London: Academic Press,. 336

5 Salisu, A.A. and I.O. Fasanya, Comparative performance of validity models for oil price. International Journal of Energy Economics and Policy 2(3): Surhatono., Time series forecasting by using seasonal autoregressive integrated moving average: Subset, multiplicative or additive model. Journal of Mathematics and Statistics 7(1):

6 Figure-4. Correlogram of Dsdncop 338

7 Table-1. Model Estimation 339

8 Figure-6. Histogram of the Residuals Figure-7. Correlogram of the Residuals 340

Multiplicative Sarima Modelling Of Nigerian Monthly Crude Oil Domestic Production

Journal of Applied Mathematics & Bioinformatics, vol.3, no.3, 2013, 103-112 ISSN: 1792-6602 (print), 1792-6939 (online) Scienpress Ltd, 2013 Multiplicative Sarima Modelling Of Nigerian Monthly Crude Oil

Journal of Applied Mathematics & Bioinformatics, vol.3, no.3, 2013, 103-112 ISSN: 1792-6602 (print), 1792-6939 (online) Scienpress Ltd, 2013 Multiplicative Sarima Modelling Of Nigerian Monthly Crude Oil

A SEASONAL TIME SERIES MODEL FOR NIGERIAN MONTHLY AIR TRAFFIC DATA

www.arpapress.com/volumes/vol14issue3/ijrras_14_3_14.pdf A SEASONAL TIME SERIES MODEL FOR NIGERIAN MONTHLY AIR TRAFFIC DATA Ette Harrison Etuk Department of Mathematics/Computer Science, Rivers State University

www.arpapress.com/volumes/vol14issue3/ijrras_14_3_14.pdf A SEASONAL TIME SERIES MODEL FOR NIGERIAN MONTHLY AIR TRAFFIC DATA Ette Harrison Etuk Department of Mathematics/Computer Science, Rivers State University

The Fitting of a SARIMA model to Monthly Naira-Euro Exchange Rates

The Fitting of a SARIMA model to Monthly Naira-Euro Exchange Rates Abstract Ette Harrison Etuk (Corresponding author) Department of Mathematics/Computer Science, Rivers State University of Science and

The Fitting of a SARIMA model to Monthly Naira-Euro Exchange Rates Abstract Ette Harrison Etuk (Corresponding author) Department of Mathematics/Computer Science, Rivers State University of Science and

Modelling Monthly Rainfall Data of Port Harcourt, Nigeria by Seasonal Box-Jenkins Methods

International Journal of Sciences Research Article (ISSN 2305-3925) Volume 2, Issue July 2013 http://www.ijsciences.com Modelling Monthly Rainfall Data of Port Harcourt, Nigeria by Seasonal Box-Jenkins

International Journal of Sciences Research Article (ISSN 2305-3925) Volume 2, Issue July 2013 http://www.ijsciences.com Modelling Monthly Rainfall Data of Port Harcourt, Nigeria by Seasonal Box-Jenkins

Time Series Analysis of Monthly Rainfall data for the Gadaref rainfall station, Sudan, by Sarima Methods

International Journal of Scientific Research in Knowledge, 2(7), pp. 320-327, 2014 Available online at http://www.ijsrpub.com/ijsrk ISSN: 2322-4541; 2014 IJSRPUB http://dx.doi.org/10.12983/ijsrk-2014-p0320-0327

International Journal of Scientific Research in Knowledge, 2(7), pp. 320-327, 2014 Available online at http://www.ijsrpub.com/ijsrk ISSN: 2322-4541; 2014 IJSRPUB http://dx.doi.org/10.12983/ijsrk-2014-p0320-0327

A Model for Daily Exchange Rates of the Naira and the XOF by Seasonal ARIMA Methods

Euro-Asian Journal of Economics and Finance ISSN: 2310-0184 (print) ISSN: 2310-4929 (online) Volume: 2, Issue: 3 (July 2014), Pages: 203-215 Academy of Business & Scientific Research http://www.absronline.org/journals

Euro-Asian Journal of Economics and Finance ISSN: 2310-0184 (print) ISSN: 2310-4929 (online) Volume: 2, Issue: 3 (July 2014), Pages: 203-215 Academy of Business & Scientific Research http://www.absronline.org/journals

A Simulating Model For Daily Uganda Shilling-Nigerian Naira Exchange Rates

Available online at www.scinzer.com Austrian Journal of Mathematics and Statistics, Vol 1, Issue 1, (2017): 23-28 ISSN 0000-0000 A Simulating Model For Daily Uganda Shilling-Nigerian Naira Exchange Rates

Available online at www.scinzer.com Austrian Journal of Mathematics and Statistics, Vol 1, Issue 1, (2017): 23-28 ISSN 0000-0000 A Simulating Model For Daily Uganda Shilling-Nigerian Naira Exchange Rates

Available online Journal of Scientific and Engineering Research, 2016, 3(2): Research Article

: Research Article") Available online www.jsaer.com, 2016, 3(2):11-15 Research Article ISSN: 2394-2630 CODEN(USA): JSERBR A Box-Jenkins Method Based Subset Simulating Model for Daily Ugx-Ngn Exchange Rates Ette Harrison Etuk

Available online www.jsaer.com, 2016, 3(2):11-15 Research Article ISSN: 2394-2630 CODEN(USA): JSERBR A Box-Jenkins Method Based Subset Simulating Model for Daily Ugx-Ngn Exchange Rates Ette Harrison Etuk

MODELING INFLATION RATES IN NIGERIA: BOX-JENKINS APPROACH. I. U. Moffat and A. E. David Department of Mathematics & Statistics, University of Uyo, Uyo

Vol.4, No.2, pp.2-27, April 216 MODELING INFLATION RATES IN NIGERIA: BOX-JENKINS APPROACH I. U. Moffat and A. E. David Department of Mathematics & Statistics, University of Uyo, Uyo ABSTRACT: This study

Vol.4, No.2, pp.2-27, April 216 MODELING INFLATION RATES IN NIGERIA: BOX-JENKINS APPROACH I. U. Moffat and A. E. David Department of Mathematics & Statistics, University of Uyo, Uyo ABSTRACT: This study

Chapter 12: An introduction to Time Series Analysis. Chapter 12: An introduction to Time Series Analysis

Chapter 12: An introduction to Time Series Analysis Introduction In this chapter, we will discuss forecasting with single-series (univariate) Box-Jenkins models. The common name of the models is Auto-Regressive

Chapter 12: An introduction to Time Series Analysis Introduction In this chapter, we will discuss forecasting with single-series (univariate) Box-Jenkins models. The common name of the models is Auto-Regressive

Forecasting. Simon Shaw 2005/06 Semester II

Forecasting Simon Shaw s.c.shaw@maths.bath.ac.uk 2005/06 Semester II 1 Introduction A critical aspect of managing any business is planning for the future. events is called forecasting. Predicting future

Forecasting Simon Shaw s.c.shaw@maths.bath.ac.uk 2005/06 Semester II 1 Introduction A critical aspect of managing any business is planning for the future. events is called forecasting. Predicting future

Forecasting Bangladesh's Inflation through Econometric Models

American Journal of Economics and Business Administration Original Research Paper Forecasting Bangladesh's Inflation through Econometric Models 1,2 Nazmul Islam 1 Department of Humanities, Bangladesh University

American Journal of Economics and Business Administration Original Research Paper Forecasting Bangladesh's Inflation through Econometric Models 1,2 Nazmul Islam 1 Department of Humanities, Bangladesh University

Empirical Approach to Modelling and Forecasting Inflation in Ghana

Current Research Journal of Economic Theory 4(3): 83-87, 2012 ISSN: 2042-485X Maxwell Scientific Organization, 2012 Submitted: April 13, 2012 Accepted: May 06, 2012 Published: June 30, 2012 Empirical Approach

Current Research Journal of Economic Theory 4(3): 83-87, 2012 ISSN: 2042-485X Maxwell Scientific Organization, 2012 Submitted: April 13, 2012 Accepted: May 06, 2012 Published: June 30, 2012 Empirical Approach

ARIMA modeling to forecast area and production of rice in West Bengal

Journal of Crop and Weed, 9(2):26-31(2013) ARIMA modeling to forecast area and production of rice in West Bengal R. BISWAS AND B. BHATTACHARYYA Department of Agricultural Statistics Bidhan Chandra Krishi

Journal of Crop and Weed, 9(2):26-31(2013) ARIMA modeling to forecast area and production of rice in West Bengal R. BISWAS AND B. BHATTACHARYYA Department of Agricultural Statistics Bidhan Chandra Krishi

Lesson 13: Box-Jenkins Modeling Strategy for building ARMA models

Lesson 13: Box-Jenkins Modeling Strategy for building ARMA models Facoltà di Economia Università dell Aquila umberto.triacca@gmail.com Introduction In this lesson we present a method to construct an ARMA(p,

Lesson 13: Box-Jenkins Modeling Strategy for building ARMA models Facoltà di Economia Università dell Aquila umberto.triacca@gmail.com Introduction In this lesson we present a method to construct an ARMA(p,

5 Autoregressive-Moving-Average Modeling

5 Autoregressive-Moving-Average Modeling 5. Purpose. Autoregressive-moving-average (ARMA models are mathematical models of the persistence, or autocorrelation, in a time series. ARMA models are widely

5 Autoregressive-Moving-Average Modeling 5. Purpose. Autoregressive-moving-average (ARMA models are mathematical models of the persistence, or autocorrelation, in a time series. ARMA models are widely

Empirical Market Microstructure Analysis (EMMA)

") Empirical Market Microstructure Analysis (EMMA) Lecture 3: Statistical Building Blocks and Econometric Basics Prof. Dr. Michael Stein michael.stein@vwl.uni-freiburg.de Albert-Ludwigs-University of Freiburg

Empirical Market Microstructure Analysis (EMMA) Lecture 3: Statistical Building Blocks and Econometric Basics Prof. Dr. Michael Stein michael.stein@vwl.uni-freiburg.de Albert-Ludwigs-University of Freiburg

Time Series Analysis -- An Introduction -- AMS 586

Time Series Analysis -- An Introduction -- AMS 586 1 Objectives of time series analysis Data description Data interpretation Modeling Control Prediction & Forecasting 2 Time-Series Data Numerical data

Time Series Analysis -- An Introduction -- AMS 586 1 Objectives of time series analysis Data description Data interpretation Modeling Control Prediction & Forecasting 2 Time-Series Data Numerical data

SOME BASICS OF TIME-SERIES ANALYSIS

SOME BASICS OF TIME-SERIES ANALYSIS John E. Floyd University of Toronto December 8, 26 An excellent place to learn about time series analysis is from Walter Enders textbook. For a basic understanding of

SOME BASICS OF TIME-SERIES ANALYSIS John E. Floyd University of Toronto December 8, 26 An excellent place to learn about time series analysis is from Walter Enders textbook. For a basic understanding of

ARIMA Models. Richard G. Pierse

ARIMA Models Richard G. Pierse 1 Introduction Time Series Analysis looks at the properties of time series from a purely statistical point of view. No attempt is made to relate variables using a priori

ARIMA Models Richard G. Pierse 1 Introduction Time Series Analysis looks at the properties of time series from a purely statistical point of view. No attempt is made to relate variables using a priori

FORECASTING SUGARCANE PRODUCTION IN INDIA WITH ARIMA MODEL

FORECASTING SUGARCANE PRODUCTION IN INDIA WITH ARIMA MODEL B. N. MANDAL Abstract: Yearly sugarcane production data for the period of - to - of India were analyzed by time-series methods. Autocorrelation

FORECASTING SUGARCANE PRODUCTION IN INDIA WITH ARIMA MODEL B. N. MANDAL Abstract: Yearly sugarcane production data for the period of - to - of India were analyzed by time-series methods. Autocorrelation

Lecture 2: Univariate Time Series

Lecture 2: Univariate Time Series Analysis: Conditional and Unconditional Densities, Stationarity, ARMA Processes Prof. Massimo Guidolin 20192 Financial Econometrics Spring/Winter 2017 Overview Motivation:

Lecture 2: Univariate Time Series Analysis: Conditional and Unconditional Densities, Stationarity, ARMA Processes Prof. Massimo Guidolin 20192 Financial Econometrics Spring/Winter 2017 Overview Motivation:

Some Time-Series Models

Some Time-Series Models Outline 1. Stochastic processes and their properties 2. Stationary processes 3. Some properties of the autocorrelation function 4. Some useful models Purely random processes, random

Some Time-Series Models Outline 1. Stochastic processes and their properties 2. Stationary processes 3. Some properties of the autocorrelation function 4. Some useful models Purely random processes, random

Oil price volatility in the Philippines using generalized autoregressive conditional heteroscedasticity

Oil price volatility in the Philippines using generalized autoregressive conditional heteroscedasticity Carl Ceasar F. Talungon University of Southern Mindanao, Cotabato Province, Philippines Email: carlceasar04@gmail.com

Oil price volatility in the Philippines using generalized autoregressive conditional heteroscedasticity Carl Ceasar F. Talungon University of Southern Mindanao, Cotabato Province, Philippines Email: carlceasar04@gmail.com

Author: Yesuf M. Awel 1c. Affiliation: 1 PhD, Economist-Consultant; P.O Box , Addis Ababa, Ethiopia. c.

ISSN: 2415-0304 (Print) ISSN: 2522-2465 (Online) Indexing/Abstracting Forecasting GDP Growth: Application of Autoregressive Integrated Moving Average Model Author: Yesuf M. Awel 1c Affiliation: 1 PhD,

ISSN: 2415-0304 (Print) ISSN: 2522-2465 (Online) Indexing/Abstracting Forecasting GDP Growth: Application of Autoregressive Integrated Moving Average Model Author: Yesuf M. Awel 1c Affiliation: 1 PhD,

at least 50 and preferably 100 observations should be available to build a proper model

III Box-Jenkins Methods 1. Pros and Cons of ARIMA Forecasting a) need for data at least 50 and preferably 100 observations should be available to build a proper model used most frequently for hourly or

III Box-Jenkins Methods 1. Pros and Cons of ARIMA Forecasting a) need for data at least 50 and preferably 100 observations should be available to build a proper model used most frequently for hourly or

Available online Journal of Scientific and Engineering Research, 2017, 4(10): Research Article

: Research Article") Available online www.jsaer.com, 2017, 4(10):233-237 Research Article ISSN: 2394-2630 CODEN(USA): JSERBR Interrupted Time Series Modelling of Daily Amounts of British Pound Per Euro due to Brexit Ette Harrison

Available online www.jsaer.com, 2017, 4(10):233-237 Research Article ISSN: 2394-2630 CODEN(USA): JSERBR Interrupted Time Series Modelling of Daily Amounts of British Pound Per Euro due to Brexit Ette Harrison

FE570 Financial Markets and Trading. Stevens Institute of Technology

FE570 Financial Markets and Trading Lecture 5. Linear Time Series Analysis and Its Applications (Ref. Joel Hasbrouck - Empirical Market Microstructure ) Steve Yang Stevens Institute of Technology 9/25/2012

FE570 Financial Markets and Trading Lecture 5. Linear Time Series Analysis and Its Applications (Ref. Joel Hasbrouck - Empirical Market Microstructure ) Steve Yang Stevens Institute of Technology 9/25/2012

Time Series Analysis of Currency in Circulation in Nigeria

ISSN -3 (Paper) ISSN 5-091 (Online) Time Series Analysis of Currency in Circulation in Nigeria Omekara C.O Okereke O.E. Ire K.I. Irokwe O. Department of Statistics, Michael Okpara University of Agriculture

ISSN -3 (Paper) ISSN 5-091 (Online) Time Series Analysis of Currency in Circulation in Nigeria Omekara C.O Okereke O.E. Ire K.I. Irokwe O. Department of Statistics, Michael Okpara University of Agriculture

Stochastic Analysis of Benue River Flow Using Moving Average (Ma) Model.

Model.") American Journal of Engineering Research (AJER) 24 American Journal of Engineering Research (AJER) e-issn : 232-847 p-issn : 232-936 Volume-3, Issue-3, pp-274-279 www.ajer.org Research Paper Open Access

American Journal of Engineering Research (AJER) 24 American Journal of Engineering Research (AJER) e-issn : 232-847 p-issn : 232-936 Volume-3, Issue-3, pp-274-279 www.ajer.org Research Paper Open Access

Forecasting the Prices of Indian Natural Rubber using ARIMA Model

Available online at www.ijpab.com Rani and Krishnan Int. J. Pure App. Biosci. 6 (2): 217-221 (2018) ISSN: 2320 7051 DOI: http://dx.doi.org/10.18782/2320-7051.5464 ISSN: 2320 7051 Int. J. Pure App. Biosci.

Available online at www.ijpab.com Rani and Krishnan Int. J. Pure App. Biosci. 6 (2): 217-221 (2018) ISSN: 2320 7051 DOI: http://dx.doi.org/10.18782/2320-7051.5464 ISSN: 2320 7051 Int. J. Pure App. Biosci.

Minitab Project Report - Assignment 6

.. Sunspot data Minitab Project Report - Assignment Time Series Plot of y Time Series Plot of X y X 7 9 7 9 The data have a wavy pattern. However, they do not show any seasonality. There seem to be an

.. Sunspot data Minitab Project Report - Assignment Time Series Plot of y Time Series Plot of X y X 7 9 7 9 The data have a wavy pattern. However, they do not show any seasonality. There seem to be an

Forecasting Egyptian GDP Using ARIMA Models

Reports on Economics and Finance, Vol. 5, 2019, no. 1, 35-47 HIKARI Ltd, www.m-hikari.com https://doi.org/10.12988/ref.2019.81023 Forecasting Egyptian GDP Using ARIMA Models Mohamed Reda Abonazel * and

Reports on Economics and Finance, Vol. 5, 2019, no. 1, 35-47 HIKARI Ltd, www.m-hikari.com https://doi.org/10.12988/ref.2019.81023 Forecasting Egyptian GDP Using ARIMA Models Mohamed Reda Abonazel * and

Time Series Analysis Model for Rainfall Data in Jordan: Case Study for Using Time Series Analysis

American Journal of Environmental Sciences 5 (5): 599-604, 2009 ISSN 1553-345X 2009 Science Publications Time Series Analysis Model for Rainfall Data in Jordan: Case Study for Using Time Series Analysis

American Journal of Environmental Sciences 5 (5): 599-604, 2009 ISSN 1553-345X 2009 Science Publications Time Series Analysis Model for Rainfall Data in Jordan: Case Study for Using Time Series Analysis

TIME SERIES ANALYSIS AND FORECASTING USING THE STATISTICAL MODEL ARIMA

CHAPTER 6 TIME SERIES ANALYSIS AND FORECASTING USING THE STATISTICAL MODEL ARIMA 6.1. Introduction A time series is a sequence of observations ordered in time. A basic assumption in the time series analysis

CHAPTER 6 TIME SERIES ANALYSIS AND FORECASTING USING THE STATISTICAL MODEL ARIMA 6.1. Introduction A time series is a sequence of observations ordered in time. A basic assumption in the time series analysis

Suan Sunandha Rajabhat University

Forecasting Exchange Rate between Thai Baht and the US Dollar Using Time Series Analysis Kunya Bowornchockchai Suan Sunandha Rajabhat University INTRODUCTION The objective of this research is to forecast

Forecasting Exchange Rate between Thai Baht and the US Dollar Using Time Series Analysis Kunya Bowornchockchai Suan Sunandha Rajabhat University INTRODUCTION The objective of this research is to forecast

ARIMA Models. Jamie Monogan. January 16, University of Georgia. Jamie Monogan (UGA) ARIMA Models January 16, / 27

ARIMA Models January 16, / 27") ARIMA Models Jamie Monogan University of Georgia January 16, 2018 Jamie Monogan (UGA) ARIMA Models January 16, 2018 1 / 27 Objectives By the end of this meeting, participants should be able to: Argue why

ARIMA Models Jamie Monogan University of Georgia January 16, 2018 Jamie Monogan (UGA) ARIMA Models January 16, 2018 1 / 27 Objectives By the end of this meeting, participants should be able to: Argue why

Dynamic Time Series Regression: A Panacea for Spurious Correlations

International Journal of Scientific and Research Publications, Volume 6, Issue 10, October 2016 337 Dynamic Time Series Regression: A Panacea for Spurious Correlations Emmanuel Alphonsus Akpan *, Imoh

International Journal of Scientific and Research Publications, Volume 6, Issue 10, October 2016 337 Dynamic Time Series Regression: A Panacea for Spurious Correlations Emmanuel Alphonsus Akpan *, Imoh

Stat 565. (S)Arima & Forecasting. Charlotte Wickham. stat565.cwick.co.nz. Feb

Arima & Forecasting. Charlotte Wickham. stat565.cwick.co.nz. Feb") Stat 565 (S)Arima & Forecasting Feb 2 2016 Charlotte Wickham stat565.cwick.co.nz Today A note from HW #3 Pick up with ARIMA processes Introduction to forecasting HW #3 The sample autocorrelation coefficients

Stat 565 (S)Arima & Forecasting Feb 2 2016 Charlotte Wickham stat565.cwick.co.nz Today A note from HW #3 Pick up with ARIMA processes Introduction to forecasting HW #3 The sample autocorrelation coefficients

Estimation and application of best ARIMA model for forecasting the uranium price.

Estimation and application of best ARIMA model for forecasting the uranium price. Medeu Amangeldi May 13, 2018 Capstone Project Superviser: Dongming Wei Second reader: Zhenisbek Assylbekov Abstract This

Estimation and application of best ARIMA model for forecasting the uranium price. Medeu Amangeldi May 13, 2018 Capstone Project Superviser: Dongming Wei Second reader: Zhenisbek Assylbekov Abstract This

Econometrics for Policy Analysis A Train The Trainer Workshop Oct 22-28, 2016 Organized by African Heritage Institution

Econometrics for Policy Analysis A Train The Trainer Workshop Oct 22-28, 2016 Organized by African Heritage Institution Delivered by Dr. Nathaniel E. Urama Department of Economics, University of Nigeria,

Econometrics for Policy Analysis A Train The Trainer Workshop Oct 22-28, 2016 Organized by African Heritage Institution Delivered by Dr. Nathaniel E. Urama Department of Economics, University of Nigeria,

Romanian Economic and Business Review Vol. 3, No. 3 THE EVOLUTION OF SNP PETROM STOCK LIST - STUDY THROUGH AUTOREGRESSIVE MODELS

THE EVOLUTION OF SNP PETROM STOCK LIST - STUDY THROUGH AUTOREGRESSIVE MODELS Marian Zaharia, Ioana Zaheu, and Elena Roxana Stan Abstract Stock exchange market is one of the most dynamic and unpredictable

THE EVOLUTION OF SNP PETROM STOCK LIST - STUDY THROUGH AUTOREGRESSIVE MODELS Marian Zaharia, Ioana Zaheu, and Elena Roxana Stan Abstract Stock exchange market is one of the most dynamic and unpredictable

CHAPTER 8 MODEL DIAGNOSTICS. 8.1 Residual Analysis

CHAPTER 8 MODEL DIAGNOSTICS We have now discussed methods for specifying models and for efficiently estimating the parameters in those models. Model diagnostics, or model criticism, is concerned with testing

CHAPTER 8 MODEL DIAGNOSTICS We have now discussed methods for specifying models and for efficiently estimating the parameters in those models. Model diagnostics, or model criticism, is concerned with testing

A stochastic modeling for paddy production in Tamilnadu

2017; 2(5): 14-21 ISSN: 2456-1452 Maths 2017; 2(5): 14-21 2017 Stats & Maths www.mathsjournal.com Received: 04-07-2017 Accepted: 05-08-2017 M Saranyadevi Assistant Professor (GUEST), Department of Statistics,

2017; 2(5): 14-21 ISSN: 2456-1452 Maths 2017; 2(5): 14-21 2017 Stats & Maths www.mathsjournal.com Received: 04-07-2017 Accepted: 05-08-2017 M Saranyadevi Assistant Professor (GUEST), Department of Statistics,

Study on Modeling and Forecasting of the GDP of Manufacturing Industries in Bangladesh

CHIANG MAI UNIVERSITY JOURNAL OF SOCIAL SCIENCE AND HUMANITIES M. N. A. Bhuiyan 1*, Kazi Saleh Ahmed 2 and Roushan Jahan 1 Study on Modeling and Forecasting of the GDP of Manufacturing Industries in Bangladesh

CHIANG MAI UNIVERSITY JOURNAL OF SOCIAL SCIENCE AND HUMANITIES M. N. A. Bhuiyan 1*, Kazi Saleh Ahmed 2 and Roushan Jahan 1 Study on Modeling and Forecasting of the GDP of Manufacturing Industries in Bangladesh

{ } Stochastic processes. Models for time series. Specification of a process. Specification of a process. , X t3. ,...X tn }

Stochastic processes Time series are an example of a stochastic or random process Models for time series A stochastic process is 'a statistical phenomenon that evolves in time according to probabilistic

Stochastic processes Time series are an example of a stochastic or random process Models for time series A stochastic process is 'a statistical phenomenon that evolves in time according to probabilistic

MCMC analysis of classical time series algorithms.

MCMC analysis of classical time series algorithms. mbalawata@yahoo.com Lappeenranta University of Technology Lappeenranta, 19.03.2009 Outline Introduction 1 Introduction 2 3 Series generation Box-Jenkins

MCMC analysis of classical time series algorithms. mbalawata@yahoo.com Lappeenranta University of Technology Lappeenranta, 19.03.2009 Outline Introduction 1 Introduction 2 3 Series generation Box-Jenkins

Asitha Kodippili. Deepthika Senaratne. Department of Mathematics and Computer Science,Fayetteville State University, USA.

Forecasting Tourist Arrivals to Sri Lanka Using Seasonal ARIMA Asitha Kodippili Department of Mathematics and Computer Science,Fayetteville State University, USA. akodippili@uncfsu.edu Deepthika Senaratne

Forecasting Tourist Arrivals to Sri Lanka Using Seasonal ARIMA Asitha Kodippili Department of Mathematics and Computer Science,Fayetteville State University, USA. akodippili@uncfsu.edu Deepthika Senaratne

The ARIMA Procedure: The ARIMA Procedure

Page 1 of 120 Overview: ARIMA Procedure Getting Started: ARIMA Procedure The Three Stages of ARIMA Modeling Identification Stage Estimation and Diagnostic Checking Stage Forecasting Stage Using ARIMA Procedure

Page 1 of 120 Overview: ARIMA Procedure Getting Started: ARIMA Procedure The Three Stages of ARIMA Modeling Identification Stage Estimation and Diagnostic Checking Stage Forecasting Stage Using ARIMA Procedure

International Journal of Advancement in Physical Sciences, Volume 4, Number 2, 2012

International Journal of Advancement in Physical Sciences, Volume, Number, RELIABILIY IN HE ESIMAES AND COMPLIANCE O INVERIBILIY CONDIION OF SAIONARY AND NONSAIONARY IME SERIES MODELS Usoro, A. E. and

International Journal of Advancement in Physical Sciences, Volume, Number, RELIABILIY IN HE ESIMAES AND COMPLIANCE O INVERIBILIY CONDIION OF SAIONARY AND NONSAIONARY IME SERIES MODELS Usoro, A. E. and

Time Series: Theory and Methods

Peter J. Brockwell Richard A. Davis Time Series: Theory and Methods Second Edition With 124 Illustrations Springer Contents Preface to the Second Edition Preface to the First Edition vn ix CHAPTER 1 Stationary

Peter J. Brockwell Richard A. Davis Time Series: Theory and Methods Second Edition With 124 Illustrations Springer Contents Preface to the Second Edition Preface to the First Edition vn ix CHAPTER 1 Stationary

Econometric Forecasting

Robert M. Kunst robert.kunst@univie.ac.at University of Vienna and Institute for Advanced Studies Vienna October 1, 2014 Outline Introduction Model-free extrapolation Univariate time-series models Trend

Robert M. Kunst robert.kunst@univie.ac.at University of Vienna and Institute for Advanced Studies Vienna October 1, 2014 Outline Introduction Model-free extrapolation Univariate time-series models Trend

Univariate ARIMA Models

Univariate ARIMA Models ARIMA Model Building Steps: Identification: Using graphs, statistics, ACFs and PACFs, transformations, etc. to achieve stationary and tentatively identify patterns and model components.

Univariate ARIMA Models ARIMA Model Building Steps: Identification: Using graphs, statistics, ACFs and PACFs, transformations, etc. to achieve stationary and tentatively identify patterns and model components.

Basics: Definitions and Notation. Stationarity. A More Formal Definition

Basics: Definitions and Notation A Univariate is a sequence of measurements of the same variable collected over (usually regular intervals of) time. Usual assumption in many time series techniques is that

Basics: Definitions and Notation A Univariate is a sequence of measurements of the same variable collected over (usually regular intervals of) time. Usual assumption in many time series techniques is that

Forecasting using R. Rob J Hyndman. 2.4 Non-seasonal ARIMA models. Forecasting using R 1

Forecasting using R Rob J Hyndman 2.4 Non-seasonal ARIMA models Forecasting using R 1 Outline 1 Autoregressive models 2 Moving average models 3 Non-seasonal ARIMA models 4 Partial autocorrelations 5 Estimation

Forecasting using R Rob J Hyndman 2.4 Non-seasonal ARIMA models Forecasting using R 1 Outline 1 Autoregressive models 2 Moving average models 3 Non-seasonal ARIMA models 4 Partial autocorrelations 5 Estimation

Ch 8. MODEL DIAGNOSTICS. Time Series Analysis

Model diagnostics is concerned with testing the goodness of fit of a model and, if the fit is poor, suggesting appropriate modifications. We shall present two complementary approaches: analysis of residuals

Model diagnostics is concerned with testing the goodness of fit of a model and, if the fit is poor, suggesting appropriate modifications. We shall present two complementary approaches: analysis of residuals

Forecasting Gold Price. A Comparative Study

Course of Financial Econometrics FIRM Forecasting Gold Price A Comparative Study Alessio Azzutti, University of Florence Abstract: This paper seeks to evaluate the appropriateness of a variety of existing

Course of Financial Econometrics FIRM Forecasting Gold Price A Comparative Study Alessio Azzutti, University of Florence Abstract: This paper seeks to evaluate the appropriateness of a variety of existing

TRANSFER FUNCTION MODEL FOR GLOSS PREDICTION OF COATED ALUMINUM USING THE ARIMA PROCEDURE

TRANSFER FUNCTION MODEL FOR GLOSS PREDICTION OF COATED ALUMINUM USING THE ARIMA PROCEDURE Mozammel H. Khan Kuwait Institute for Scientific Research Introduction The objective of this work was to investigate

TRANSFER FUNCTION MODEL FOR GLOSS PREDICTION OF COATED ALUMINUM USING THE ARIMA PROCEDURE Mozammel H. Khan Kuwait Institute for Scientific Research Introduction The objective of this work was to investigate

Lecture 19 Box-Jenkins Seasonal Models

Lecture 19 Box-Jenkins Seasonal Models If the time series is nonstationary with respect to its variance, then we can stabilize the variance of the time series by using a pre-differencing transformation.

Lecture 19 Box-Jenkins Seasonal Models If the time series is nonstationary with respect to its variance, then we can stabilize the variance of the time series by using a pre-differencing transformation.

Analysis. Components of a Time Series

Module 8: Time Series Analysis 8.2 Components of a Time Series, Detection of Change Points and Trends, Time Series Models Components of a Time Series There can be several things happening simultaneously

Module 8: Time Series Analysis 8.2 Components of a Time Series, Detection of Change Points and Trends, Time Series Models Components of a Time Series There can be several things happening simultaneously

Arma-Arch Modeling Of The Returns Of First Bank Of Nigeria

Arma-Arch Modeling Of The Returns Of First Bank Of Nigeria Emmanuel Alphonsus Akpan Imoh Udo Moffat Department of Mathematics and Statistics University of Uyo, Nigeria Ntiedo Bassey Ekpo Department of

Arma-Arch Modeling Of The Returns Of First Bank Of Nigeria Emmanuel Alphonsus Akpan Imoh Udo Moffat Department of Mathematics and Statistics University of Uyo, Nigeria Ntiedo Bassey Ekpo Department of

Forecasting Area, Production and Yield of Cotton in India using ARIMA Model

Forecasting Area, Production and Yield of Cotton in India using ARIMA Model M. K. Debnath 1, Kartic Bera 2 *, P. Mishra 1 1 Department of Agricultural Statistics, Bidhan Chanda Krishi Vishwavidyalaya,

Forecasting Area, Production and Yield of Cotton in India using ARIMA Model M. K. Debnath 1, Kartic Bera 2 *, P. Mishra 1 1 Department of Agricultural Statistics, Bidhan Chanda Krishi Vishwavidyalaya,

Using Analysis of Time Series to Forecast numbers of The Patients with Malignant Tumors in Anbar Provinc

Using Analysis of Time Series to Forecast numbers of The Patients with Malignant Tumors in Anbar Provinc /. ) ( ) / (Box & Jenkins).(.(2010-2006) ARIMA(2,1,0). Abstract: The aim of this research is to

Using Analysis of Time Series to Forecast numbers of The Patients with Malignant Tumors in Anbar Provinc /. ) ( ) / (Box & Jenkins).(.(2010-2006) ARIMA(2,1,0). Abstract: The aim of this research is to

TIME SERIES ANALYSIS. Forecasting and Control. Wiley. Fifth Edition GWILYM M. JENKINS GEORGE E. P. BOX GREGORY C. REINSEL GRETA M.

TIME SERIES ANALYSIS Forecasting and Control Fifth Edition GEORGE E. P. BOX GWILYM M. JENKINS GREGORY C. REINSEL GRETA M. LJUNG Wiley CONTENTS PREFACE TO THE FIFTH EDITION PREFACE TO THE FOURTH EDITION

TIME SERIES ANALYSIS Forecasting and Control Fifth Edition GEORGE E. P. BOX GWILYM M. JENKINS GREGORY C. REINSEL GRETA M. LJUNG Wiley CONTENTS PREFACE TO THE FIFTH EDITION PREFACE TO THE FOURTH EDITION

Chapter 8: Model Diagnostics

Chapter 8: Model Diagnostics Model diagnostics involve checking how well the model fits. If the model fits poorly, we consider changing the specification of the model. A major tool of model diagnostics

Chapter 8: Model Diagnostics Model diagnostics involve checking how well the model fits. If the model fits poorly, we consider changing the specification of the model. A major tool of model diagnostics

Sugarcane Productivity in Bihar- A Forecast through ARIMA Model

Available online at www.ijpab.com Kumar et al Int. J. Pure App. Biosci. 5 (6): 1042-1051 (2017) ISSN: 2320 7051 DOI: http://dx.doi.org/10.18782/2320-7051.5838 ISSN: 2320 7051 Int. J. Pure App. Biosci.

Available online at www.ijpab.com Kumar et al Int. J. Pure App. Biosci. 5 (6): 1042-1051 (2017) ISSN: 2320 7051 DOI: http://dx.doi.org/10.18782/2320-7051.5838 ISSN: 2320 7051 Int. J. Pure App. Biosci.

TIME SERIES DATA PREDICTION OF NATURAL GAS CONSUMPTION USING ARIMA MODEL

International Journal of Information Technology & Management Information System (IJITMIS) Volume 7, Issue 3, Sep-Dec-2016, pp. 01 07, Article ID: IJITMIS_07_03_001 Available online at http://www.iaeme.com/ijitmis/issues.asp?jtype=ijitmis&vtype=7&itype=3

International Journal of Information Technology & Management Information System (IJITMIS) Volume 7, Issue 3, Sep-Dec-2016, pp. 01 07, Article ID: IJITMIS_07_03_001 Available online at http://www.iaeme.com/ijitmis/issues.asp?jtype=ijitmis&vtype=7&itype=3

IS THE NORTH ATLANTIC OSCILLATION A RANDOM WALK? A COMMENT WITH FURTHER RESULTS

INTERNATIONAL JOURNAL OF CLIMATOLOGY Int. J. Climatol. 24: 377 383 (24) Published online 11 February 24 in Wiley InterScience (www.interscience.wiley.com). DOI: 1.12/joc.13 IS THE NORTH ATLANTIC OSCILLATION

INTERNATIONAL JOURNAL OF CLIMATOLOGY Int. J. Climatol. 24: 377 383 (24) Published online 11 February 24 in Wiley InterScience (www.interscience.wiley.com). DOI: 1.12/joc.13 IS THE NORTH ATLANTIC OSCILLATION

Financial Econometrics

Financial Econometrics Nonlinear time series analysis Gerald P. Dwyer Trinity College, Dublin January 2016 Outline 1 Nonlinearity Does nonlinearity matter? Nonlinear models Tests for nonlinearity Forecasting

Financial Econometrics Nonlinear time series analysis Gerald P. Dwyer Trinity College, Dublin January 2016 Outline 1 Nonlinearity Does nonlinearity matter? Nonlinear models Tests for nonlinearity Forecasting

Time Series and Forecasting

Time Series and Forecasting Introduction to Forecasting n What is forecasting? n Primary Function is to Predict the Future using (time series related or other) data we have in hand n Why are we interested?

Time Series and Forecasting Introduction to Forecasting n What is forecasting? n Primary Function is to Predict the Future using (time series related or other) data we have in hand n Why are we interested?

Time Series 4. Robert Almgren. Oct. 5, 2009

Time Series 4 Robert Almgren Oct. 5, 2009 1 Nonstationarity How should you model a process that has drift? ARMA models are intrinsically stationary, that is, they are mean-reverting: when the value of

Time Series 4 Robert Almgren Oct. 5, 2009 1 Nonstationarity How should you model a process that has drift? ARMA models are intrinsically stationary, that is, they are mean-reverting: when the value of

ECONOMETRIA II. CURSO 2009/2010 LAB # 3

ECONOMETRIA II. CURSO 2009/2010 LAB # 3 BOX-JENKINS METHODOLOGY The Box Jenkins approach combines the moving average and the autorregresive models. Although both models were already known, the contribution

ECONOMETRIA II. CURSO 2009/2010 LAB # 3 BOX-JENKINS METHODOLOGY The Box Jenkins approach combines the moving average and the autorregresive models. Although both models were already known, the contribution

1. Fundamental concepts

. Fundamental concepts A time series is a sequence of data points, measured typically at successive times spaced at uniform intervals. Time series are used in such fields as statistics, signal processing

. Fundamental concepts A time series is a sequence of data points, measured typically at successive times spaced at uniform intervals. Time series are used in such fields as statistics, signal processing

Automatic seasonal auto regressive moving average models and unit root test detection

ISSN 1750-9653, England, UK International Journal of Management Science and Engineering Management Vol. 3 (2008) No. 4, pp. 266-274 Automatic seasonal auto regressive moving average models and unit root

ISSN 1750-9653, England, UK International Journal of Management Science and Engineering Management Vol. 3 (2008) No. 4, pp. 266-274 Automatic seasonal auto regressive moving average models and unit root

Forecasting of the Austrian Inflation Rate

Forecasting of the Austrian Inflation Rate Case Study for the Course of Econometric Forecasting Winter Semester 2007 by Nadir Shahzad Virkun Tomas Sedliacik Goal setting and Data selection The goal of

Forecasting of the Austrian Inflation Rate Case Study for the Course of Econometric Forecasting Winter Semester 2007 by Nadir Shahzad Virkun Tomas Sedliacik Goal setting and Data selection The goal of

FORECASTING OF COTTON PRODUCTION IN INDIA USING ARIMA MODEL

FORECASTING OF COTTON PRODUCTION IN INDIA USING ARIMA MODEL S.Poyyamozhi 1, Dr. A. Kachi Mohideen 2. 1 Assistant Professor and Head, Department of Statistics, Government Arts College (Autonomous), Kumbakonam

FORECASTING OF COTTON PRODUCTION IN INDIA USING ARIMA MODEL S.Poyyamozhi 1, Dr. A. Kachi Mohideen 2. 1 Assistant Professor and Head, Department of Statistics, Government Arts College (Autonomous), Kumbakonam

Forecasting Foreign Direct Investment Inflows into India Using ARIMA Model

Forecasting Foreign Direct Investment Inflows into India Using ARIMA Model Dr.K.Nithya Kala & Aruna.P.Remesh, 1 Assistant Professor, PSGR Krishnammal College for Women, Coimbatore, Tamilnadu, India 2 PhD

Forecasting Foreign Direct Investment Inflows into India Using ARIMA Model Dr.K.Nithya Kala & Aruna.P.Remesh, 1 Assistant Professor, PSGR Krishnammal College for Women, Coimbatore, Tamilnadu, India 2 PhD

Automatic Forecasting

Automatic Forecasting Summary The Automatic Forecasting procedure is designed to forecast future values of time series data. A time series consists of a set of sequential numeric data taken at equally

Automatic Forecasting Summary The Automatic Forecasting procedure is designed to forecast future values of time series data. A time series consists of a set of sequential numeric data taken at equally

Classification of Forecasting Methods Based On Application

Classification of Forecasting Methods Based On Application C.Narayana 1, G.Y.Mythili 2, J. Prabhakara Naik 3, K.Vasu 4, G. Mokesh Rayalu 5 1 Assistant professor, Department of Mathematics, Sriharsha Institute

Classification of Forecasting Methods Based On Application C.Narayana 1, G.Y.Mythili 2, J. Prabhakara Naik 3, K.Vasu 4, G. Mokesh Rayalu 5 1 Assistant professor, Department of Mathematics, Sriharsha Institute

Elements of Multivariate Time Series Analysis

Gregory C. Reinsel Elements of Multivariate Time Series Analysis Second Edition With 14 Figures Springer Contents Preface to the Second Edition Preface to the First Edition vii ix 1. Vector Time Series

Gregory C. Reinsel Elements of Multivariate Time Series Analysis Second Edition With 14 Figures Springer Contents Preface to the Second Edition Preface to the First Edition vii ix 1. Vector Time Series

Statistical Methods for Forecasting

Statistical Methods for Forecasting BOVAS ABRAHAM University of Waterloo JOHANNES LEDOLTER University of Iowa John Wiley & Sons New York Chichester Brisbane Toronto Singapore Contents 1 INTRODUCTION AND

Statistical Methods for Forecasting BOVAS ABRAHAM University of Waterloo JOHANNES LEDOLTER University of Iowa John Wiley & Sons New York Chichester Brisbane Toronto Singapore Contents 1 INTRODUCTION AND

of seasonal data demonstrating the usefulness of the devised tests. We conclude in "Conclusion" section with a discussion.

DOI 10.1186/s40064-016-3167-4 RESEARCH Open Access Portmanteau test statistics for seasonal serial correlation in time series models Esam Mahdi * *Correspondence: emahdi@iugaza.edu.ps Department of Mathematics,

DOI 10.1186/s40064-016-3167-4 RESEARCH Open Access Portmanteau test statistics for seasonal serial correlation in time series models Esam Mahdi * *Correspondence: emahdi@iugaza.edu.ps Department of Mathematics,

BJEST. Function: Usage:

BJEST BJEST (CONSTANT, CUMPLOT, EXACTML, NAR=number of AR parameters, NBACK=number of back-forecasted residuals,ndiff=degree of differencing, NLAG=number of autocorrelations,nma=number of MA parameters,

BJEST BJEST (CONSTANT, CUMPLOT, EXACTML, NAR=number of AR parameters, NBACK=number of back-forecasted residuals,ndiff=degree of differencing, NLAG=number of autocorrelations,nma=number of MA parameters,

Seasonal Autoregressive Integrated Moving Average Model for Precipitation Time Series

Journal of Mathematics and Statistics 8 (4): 500-505, 2012 ISSN 1549-3644 2012 doi:10.3844/jmssp.2012.500.505 Published Online 8 (4) 2012 (http://www.thescipub.com/jmss.toc) Seasonal Autoregressive Integrated

Journal of Mathematics and Statistics 8 (4): 500-505, 2012 ISSN 1549-3644 2012 doi:10.3844/jmssp.2012.500.505 Published Online 8 (4) 2012 (http://www.thescipub.com/jmss.toc) Seasonal Autoregressive Integrated

Modeling and forecasting global mean temperature time series

Modeling and forecasting global mean temperature time series April 22, 2018 Abstract: An ARIMA time series model was developed to analyze the yearly records of the change in global annual mean surface

Modeling and forecasting global mean temperature time series April 22, 2018 Abstract: An ARIMA time series model was developed to analyze the yearly records of the change in global annual mean surface

Lab: Box-Jenkins Methodology - US Wholesale Price Indicator

Lab: Box-Jenkins Methodology - US Wholesale Price Indicator In this lab we explore the Box-Jenkins methodology by applying it to a time-series data set comprising quarterly observations of the US Wholesale

Lab: Box-Jenkins Methodology - US Wholesale Price Indicator In this lab we explore the Box-Jenkins methodology by applying it to a time-series data set comprising quarterly observations of the US Wholesale

Time Series I Time Domain Methods

Astrostatistics Summer School Penn State University University Park, PA 16802 May 21, 2007 Overview Filtering and the Likelihood Function Time series is the study of data consisting of a sequence of DEPENDENT

Astrostatistics Summer School Penn State University University Park, PA 16802 May 21, 2007 Overview Filtering and the Likelihood Function Time series is the study of data consisting of a sequence of DEPENDENT

Time Series and Forecasting

Time Series and Forecasting Introduction to Forecasting n What is forecasting? n Primary Function is to Predict the Future using (time series related or other) data we have in hand n Why are we interested?

Time Series and Forecasting Introduction to Forecasting n What is forecasting? n Primary Function is to Predict the Future using (time series related or other) data we have in hand n Why are we interested?

Univariate linear models

Univariate linear models The specification process of an univariate ARIMA model is based on the theoretical properties of the different processes and it is also important the observation and interpretation

Univariate linear models The specification process of an univariate ARIMA model is based on the theoretical properties of the different processes and it is also important the observation and interpretation

EASTERN MEDITERRANEAN UNIVERSITY ECON 604, FALL 2007 DEPARTMENT OF ECONOMICS MEHMET BALCILAR ARIMA MODELS: IDENTIFICATION

ARIMA MODELS: IDENTIFICATION A. Autocorrelations and Partial Autocorrelations 1. Summary of What We Know So Far: a) Series y t is to be modeled by Box-Jenkins methods. The first step was to convert y t

ARIMA MODELS: IDENTIFICATION A. Autocorrelations and Partial Autocorrelations 1. Summary of What We Know So Far: a) Series y t is to be modeled by Box-Jenkins methods. The first step was to convert y t

ANALYZING THE IMPACT OF HISTORICAL DATA LENGTH IN NON SEASONAL ARIMA MODELS FORECASTING

ANALYZING THE IMPACT OF HISTORICAL DATA LENGTH IN NON SEASONAL ARIMA MODELS FORECASTING Amon Mwenda, Dmitry Kuznetsov, Silas Mirau School of Computational and Communication Science and Engineering Nelson

ANALYZING THE IMPACT OF HISTORICAL DATA LENGTH IN NON SEASONAL ARIMA MODELS FORECASTING Amon Mwenda, Dmitry Kuznetsov, Silas Mirau School of Computational and Communication Science and Engineering Nelson

SAS/ETS 14.1 User s Guide. The ARIMA Procedure

SAS/ETS 14.1 User s Guide The ARIMA Procedure This document is an individual chapter from SAS/ETS 14.1 User s Guide. The correct bibliographic citation for this manual is as follows: SAS Institute Inc.

SAS/ETS 14.1 User s Guide The ARIMA Procedure This document is an individual chapter from SAS/ETS 14.1 User s Guide. The correct bibliographic citation for this manual is as follows: SAS Institute Inc.

Applied time-series analysis

Robert M. Kunst robert.kunst@univie.ac.at University of Vienna and Institute for Advanced Studies Vienna October 18, 2011 Outline Introduction and overview Econometric Time-Series Analysis In principle,

Robert M. Kunst robert.kunst@univie.ac.at University of Vienna and Institute for Advanced Studies Vienna October 18, 2011 Outline Introduction and overview Econometric Time-Series Analysis In principle,

Stochastic Modelling Solutions to Exercises on Time Series

Stochastic Modelling Solutions to Exercises on Time Series Dr. Iqbal Owadally March 3, 2003 Solutions to Elementary Problems Q1. (i) (1 0.5B)X t = Z t. The characteristic equation 1 0.5z = 0 does not have

Stochastic Modelling Solutions to Exercises on Time Series Dr. Iqbal Owadally March 3, 2003 Solutions to Elementary Problems Q1. (i) (1 0.5B)X t = Z t. The characteristic equation 1 0.5z = 0 does not have

Austrian Inflation Rate

Austrian Inflation Rate Course of Econometric Forecasting Nadir Shahzad Virkun Tomas Sedliacik Goal and Data Selection Our goal is to find a relatively accurate procedure in order to forecast the Austrian

Austrian Inflation Rate Course of Econometric Forecasting Nadir Shahzad Virkun Tomas Sedliacik Goal and Data Selection Our goal is to find a relatively accurate procedure in order to forecast the Austrian

Autoregressive Integrated Moving Average Model to Predict Graduate Unemployment in Indonesia

DOI 10.1515/ptse-2017-0005 PTSE 12 (1): 43-50 Autoregressive Integrated Moving Average Model to Predict Graduate Unemployment in Indonesia Umi MAHMUDAH u_mudah@yahoo.com (State Islamic University of Pekalongan,

DOI 10.1515/ptse-2017-0005 PTSE 12 (1): 43-50 Autoregressive Integrated Moving Average Model to Predict Graduate Unemployment in Indonesia Umi MAHMUDAH u_mudah@yahoo.com (State Islamic University of Pekalongan,

The autocorrelation and autocovariance functions - helpful tools in the modelling problem

The autocorrelation and autocovariance functions - helpful tools in the modelling problem J. Nowicka-Zagrajek A. Wy lomańska Institute of Mathematics and Computer Science Wroc law University of Technology,

The autocorrelation and autocovariance functions - helpful tools in the modelling problem J. Nowicka-Zagrajek A. Wy lomańska Institute of Mathematics and Computer Science Wroc law University of Technology,

Econometría 2: Análisis de series de Tiempo

Econometría 2: Análisis de series de Tiempo Karoll GOMEZ kgomezp@unal.edu.co http://karollgomez.wordpress.com Segundo semestre 2016 IX. Vector Time Series Models VARMA Models A. 1. Motivation: The vector

Econometría 2: Análisis de series de Tiempo Karoll GOMEZ kgomezp@unal.edu.co http://karollgomez.wordpress.com Segundo semestre 2016 IX. Vector Time Series Models VARMA Models A. 1. Motivation: The vector

MULTI-YEAR AVERAGES FROM A ROLLING SAMPLE SURVEY

MULTI-YEAR AVERAGES FROM A ROLLING SAMPLE SURVEY Nanak Chand Charles H. Alexander U.S. Bureau of the Census Nanak Chand U.S. Bureau of the Census Washington D.C. 20233 1. Introduction Rolling sample surveys

MULTI-YEAR AVERAGES FROM A ROLLING SAMPLE SURVEY Nanak Chand Charles H. Alexander U.S. Bureau of the Census Nanak Chand U.S. Bureau of the Census Washington D.C. 20233 1. Introduction Rolling sample surveys

Chapter 5: Models for Nonstationary Time Series

Chapter 5: Models for Nonstationary Time Series Recall that any time series that is a stationary process has a constant mean function. So a process that has a mean function that varies over time must be

Chapter 5: Models for Nonstationary Time Series Recall that any time series that is a stationary process has a constant mean function. So a process that has a mean function that varies over time must be