Asymmetry of the exchange rate pass-through: An exercise on the Polish data

|

|

|

- Ethel McBride

- 5 years ago

- Views:

Transcription

1 National Bank of Poland Asymmetry of the exchange rate pass-through: An exercise on the Polish data Jan Przystupa Ewa Wróbel 0th Annual NBP - SNB Seminar June 4, 03 Zurich

2

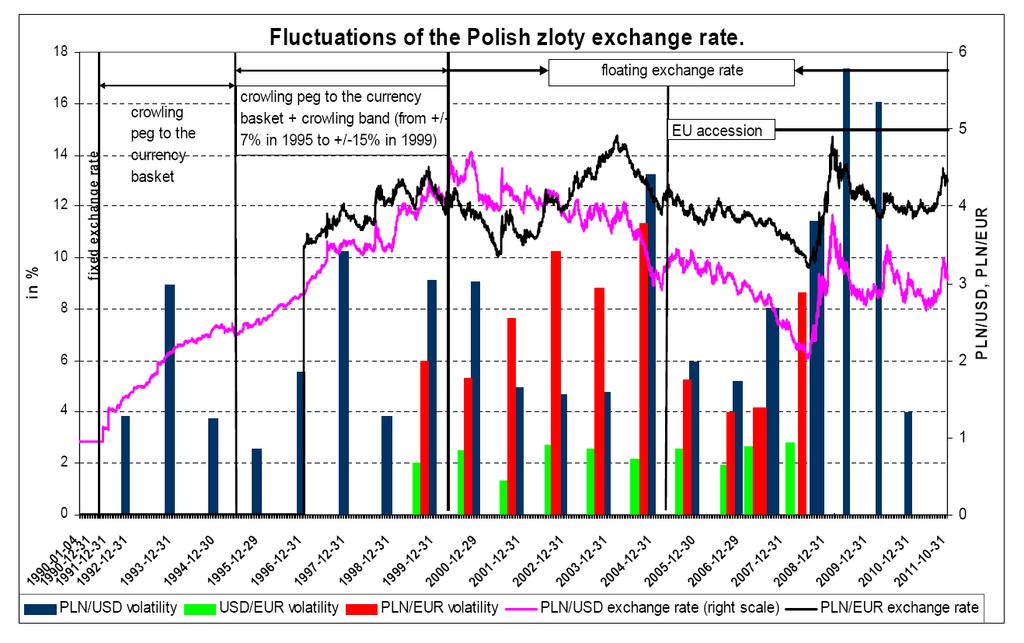

3 PLN/USD fluctuations Band +/-5% Floating exchange rate (April 998) EU accession (May 004)

4 The exchange rate Exchange rate vs. inflation crow ling peg to a currency basket crowling peg to a currency basket + crawling band floating exchange rate fixed exchange rate Inflation (left scale) NER (right scale)

5 MOTIVATION Understanding how prices respond to exchange rate is of key importance for any open economy. An extra stimulus: FAQ: What is an impact of currerent depreciation (appreciation) on consumer prices? Does it depend on the scale of the ex changes or on the phase of the business cycle? What is the pricing policy of the foreign exporting firms towards the Polish market? To answer these questions we propose a complex investigation of the exchange rate channel of the monetary transmission mechanism for an open economy with the floating exchange rate regime.

6 First: we assessed the level of the exchange rate pass-through. Based on McCarthy (999) where the impact of a sequence of supply, demand and exchange rate shocks on the import, producer and consumer prices is examined. Since it is a popular method we used it for the sake of comparability with other studies and to have an idea about the level of the pass-through effect in Poland. Flowchart of the pass-through effect. Money (M3) Interest rate oil price (Brent, in USD) (supply shock) output gap (demand shock) NEER (30% USD; 70% EUR) CPI PPI Import prices (in domestic currency)

7 McCarthy s model (999) πm - index of the import transaction prices expressed in the domestic currency; εm - unexpected change of the import price ( π m ) + αε s + αε d + α ε e m m = Et 3 ε π + πw - price index of the sold production of industry (PPI); εw - unexpected change of the production price ( π w ) + β ε s + β ε d + β ε e + β ε m w π + w = Et 3 4 ε πc - consumption price index (CPI); εc - unexpected change of the CPI Coefficients explain a part of the shock assigned to the corresponding variable ( π c ) + γ ε s + γ ε d + γ ε e + γ ε m + γ ε w c π + c = Et ε

8 Exchange rate pass-through. Estimation based on the McCarthy s SVAR PT ( z t ) h = z e t, t+ h t, t+ h Pass-through effect: changes of the variable z (import, production, consumption prices) from t to t+h being the response on the exchange rate changes between t and t+h Pass-through effect after Import transaction prices (PM) for Price index of the sold production of industry (PPI) Consumption price index CPI) quarters 4 quarters 8 quarters Est.0 Est. Est.0 Est. Est.0 Est

9 Exchange rate pass-through. Estimation based on the McCarthy s SVAR Time decomposition of the pass-through effect. Time decomposition of the pass-through effect for (total P-T=00) Quarter after shock Q 0 Q Q Q 3 Q 4 -Q 8 Import transaction prices (PM) Price index of the sold production of industry (PPI) Consumption price index CPI)

10 Assessing the level of the exchange rate pass-through to the import prices and pricing to market (PTM) with cointegration technics. Cointergating vector, exchange rate - NEER p = α + α e + α p + α p + α y + ε IMP F H H t 0 t t 3 t 4 t t VECM (cointegration Johansen), - t stat in [ ] unrestricted α [5.9] α.44 [.] α (If significant then PTM exists) [5.9] α (If significant then PT is full) Chi - square=0.56, p restricted: α = α [7.50] α 0.8 [7.50] α.3 [7.65] 3 restricted: α = restricted: α = α =, 3 α = (Law of one price) Chi - square=9.64, p α =0 (Unit homogeneity) Chi - square=., p. 0.0 restricted: α = α = (Unit coeff. at EX & FP) Chi - square=0., p

11 EX pass-through to the import prices Cointegrating vector, bilateral exchange rate EUR/PLN p = + e + p + p + y + α α α α α ε IMP F H H t 0 t t 3 t 4 t t VECM (cointegration Johansen),t- stat in [ ] Fully modified least squares t - stat in [ ] unrestricted α [.47] [4.73] α 0.4 [0.35] 0.74 [.09] α 0.83 [.7] 0.8 [4. 4] 3 restricted: α = α Chi - square=0.03, p Chi - square=0.08, p. 0.9 α [5.8] [7.5] α 0.78 [5.8] 0.67 [7.5] α 0.7 [7.] 0.84 [5.9] 3 restricted: α = α = Chi - square=7.4, p Chi - square=.46, p restricted: α = α =, α 3 =0 Chi - square=7.49, p Chi - square=60, p restricted: α = α = Chi - square=6.87, p Chi - square=40.0, p

12 IMP F H IMP t β0 β t β, i t i β3, i t i β4, i t i β5, i t i t i= 0 i= 0 i= 0 i= p = + EC + e + p + p + p + v Table A. Dynamic import price equation Variable Coefficient t-stat β β β ,0 β PTM ,0 Return to equilibrium EX pass-through (short term) Dynamic import price equations Table A. Dynamic import price eq uation: appreciation of the EUR /PLN, usa ble obs.: 4. Variable Coefficient t - stat, p - value in ( ) A β (0.874) 0 A β (0.008) A β, (0.3) A β 4,0.9.8 (0.09) A t = t { if e 0 0 otherwise Table A 3. Dynamic import price equ ation: depreciation of the EUR /PLN, usable obs.: 0 Variable Coefficient t - stat β D 0 D β D β, D β 4, D t = t { if e 0 0 otherwise

13 Dynamic import price equations IMP F H IMP t β0 β t β, i t i β3, i t i β4, i t i β5, i t i t i= 0 i= 0 i= 0 i= p = + EC + e + p + p + p + v Table A4. Dynamic import price equation: positive EC, usable obs.:. Variable Coefficient t-stat β EC 0 EC β EC β +, EC β + 4, Table A5. Dynamic import price equation: negative EC, usable obs.: 3. Variable Coefficient t-stat β EC 0 EC β EC β, EC β 4, EC+ import prices are lower than the equilibrium level determined by exporters prices and domestic prices EC- import prices are higher than the equilibrium level determined by exporters prices and domestic prices

14 Exchange rate pass-through models based on the Phillips curve π = α Eπ + ( α α ) π + α ( e ) + α y + ε qi qi qi qi qi r qi tk,, k t t+, k, k t, k t 3, k t t where: π stands for inflation (CPI); qi is a variable (i= 4) stands for: i= output gap (y); i= nominal effective exchange rate ( e); i=3 volatility of the nominal effective exchange rate (s); i=4 inflation (π): actual inflation inflation target (π*); k=,; Threshold estimated with SETAR (Self-Exciting Threshold AutoRegresive) model k= for qi > τ (τ = threshold); k= for qi τ k=3,4; Investigate nonreversibility of the linear functions through segmenting the variables. k=3 for qi > qi- k=4 for qi qi- r et is a nominal effective exchange rate (in log) plus foreign inflation (HICP in the euro zone; in log)

15 The economic interpretation of the threshold model and model based on nonreversibility of the linear functions % 3 0 Threshold models Nonreversible linear models t t0 recession expansion Nonreversible linear models t>t0 EU accession Threshold models - Russian crisis Threshold models Q 997Q3 998Q 998Q3 999Q 999Q3 000Q 000Q3 00Q 00Q3 00Q 00Q3 slump 003Q 003Q3 004Q 004Q3 005Q 005Q3 006Q 006Q3 prosperity 007Q 007Q3 008Q 008Q3 output gap threshold business cycle

16 The economic interpretation of the threshold model and model based on nonreversibility of the linear functions Inflation - target inflation (π - π * ) Early recession = t r a cost t r = a t cos θ θ Late expansion Early expansion Output gap (y) Late recession Two-leaf clover curve

17 Asymmetry of the exchange rate passthrough to CPI related to: The asymmetry of the exchange rate pass-through to the consumer prices Threshold models (τ = threshold) Nonreversible linear models variable > τ variable τ t > t 0 t t 0 Output gap (y) nominal effective exchange rate ( e) τ = 0.4% τ =.08% Volatility of the nominal effective exchange rate (s) Inflation (π) Pass-through (general) τ = 4.3% τ = level of official inflation target

18 The asymmetry of the exchange rate pass-through to the consumer prices 3 Recession Expansion 0,4 EU accession 0,35 0,3 0 - Russian crisis Average pass-through 0,5 0, 0,5 pass-through effect Max. pass-through 0, Q 997Q3 Average pass-through 998Q 998Q3 999Q Min. pass-through 999Q3 000Q 000Q3 00Q 00Q3 00Q 00Q3 Average pass-through 003Q 003Q3 004Q 004Q3 005Q 005Q3 006Q 006Q3 007Q 007Q3 008Q 008Q3 output gap pass-through effect (right scale) proxy of the business cycle This is coherent with the behavior of enterprises in the business cycle, conditioning their investment decisions on expected profits with a maximum in the early expansion and a minimum in the early recession. The enterprises propensity to change prices follows profit expectations. 0,05 0

19 Exchange rate pass-through and inflation. I q`08 II q'08 III q'08 IV q'08 I q`09 II q'09 III q'09 IV q'09 I q`0 II q'0 III q'0 IV q'0 I q` II q' III q' IV q' I q` II q' III q' IV q' I q`3 Linear PT -0,65-0,684-0,59-0,56 0,84 0,44 0,8-0,05-0,0-0,070 0,056 0,0-0,83-0,35-0,047 0,77,4 0,50-0,06-0,49-0,60 Asym.PT -0,573-0,707-0,783-0,57,707,646,99-0,404-0,64-0,339 0,05 0,065-0,90-0,46-0,067 0,509 0,885 0,356-0,08-0,77-0,7 Figures shown in the table indicate by how many percentage points inflation in a given quarter would be higher (-) or lower (+) than the counterfactual inflation that assumes no exchange rate changes. A year on year impact is calculated as an average impact in the consecutive four quarters.

20 THANK YOU

Applied Econometrics and International Development Vol.9-1 (2009)

") FUNCTIONAL FORMS AND PPP: THE CASE OF CANADA, THE EU, JAPAN, AND THE U.K. HSING, Yu Abstract This paper applies an extended Box-Cox model to test the functional form of the purchasing power parity hypothesis

FUNCTIONAL FORMS AND PPP: THE CASE OF CANADA, THE EU, JAPAN, AND THE U.K. HSING, Yu Abstract This paper applies an extended Box-Cox model to test the functional form of the purchasing power parity hypothesis

Introduction to Macroeconomics

Introduction to Macroeconomics Martin Ellison Nuffi eld College Michaelmas Term 2018 Martin Ellison (Nuffi eld) Introduction Michaelmas Term 2018 1 / 39 Macroeconomics is Dynamic Decisions are taken over

Introduction to Macroeconomics Martin Ellison Nuffi eld College Michaelmas Term 2018 Martin Ellison (Nuffi eld) Introduction Michaelmas Term 2018 1 / 39 Macroeconomics is Dynamic Decisions are taken over

An Empirical Analysis of RMB Exchange Rate changes impact on PPI of China

2nd International Conference on Economics, Management Engineering and Education Technology (ICEMEET 206) An Empirical Analysis of RMB Exchange Rate changes impact on PPI of China Chao Li, a and Yonghua

2nd International Conference on Economics, Management Engineering and Education Technology (ICEMEET 206) An Empirical Analysis of RMB Exchange Rate changes impact on PPI of China Chao Li, a and Yonghua

Asymmetries in central bank intervention

Matthieu Stigler Ila Patnaik Ajay Shah September 16, 2009 1 The question 2 3 4 Outline The question 1 The question 2 3 4 Understanding more-flexible but not floating rates Highly inflexible exchange rates:

Matthieu Stigler Ila Patnaik Ajay Shah September 16, 2009 1 The question 2 3 4 Outline The question 1 The question 2 3 4 Understanding more-flexible but not floating rates Highly inflexible exchange rates:

The transmission mechanism How the monetary-policy instrument affects the economy and the target variables

Eco 200, part 3, Fall 2004 200L2.tex Lars Svensson 11/18/04 The transmission mechanism How the monetary-policy instrument affects the economy and the target variables Variables t =..., 1, 0, 1,... denotes

Eco 200, part 3, Fall 2004 200L2.tex Lars Svensson 11/18/04 The transmission mechanism How the monetary-policy instrument affects the economy and the target variables Variables t =..., 1, 0, 1,... denotes

NATIONAL BANK OF POLAND WORKING PAPER No. 125

NATIONAL BANK OF POLAND WORKING PAPER No. 125 On asymmetric effects in a monetary policy rule. The case of Poland Anna Sznajderska Warsaw 2012 Anna Sznajderska National Bank of Poland; e-mail: Anna.Sznajderska@nbp.pl

NATIONAL BANK OF POLAND WORKING PAPER No. 125 On asymmetric effects in a monetary policy rule. The case of Poland Anna Sznajderska Warsaw 2012 Anna Sznajderska National Bank of Poland; e-mail: Anna.Sznajderska@nbp.pl

Information Bulletin 5/2010

Information Bulletin /2010 Warsaw, 2010 Compiled from NBP materials by the Department of Statistics as at July 13, 2010. Design: Oliwka s.c. Cover photo: Corbis/Free Layout and print: NBP Printshop Published

Information Bulletin /2010 Warsaw, 2010 Compiled from NBP materials by the Department of Statistics as at July 13, 2010. Design: Oliwka s.c. Cover photo: Corbis/Free Layout and print: NBP Printshop Published

The TransPacific agreement A good thing for VietNam?

The TransPacific agreement A good thing for VietNam? Jean Louis Brillet, France For presentation at the LINK 2014 Conference New York, 22nd 24th October, 2014 Advertisement!!! The model uses EViews The

The TransPacific agreement A good thing for VietNam? Jean Louis Brillet, France For presentation at the LINK 2014 Conference New York, 22nd 24th October, 2014 Advertisement!!! The model uses EViews The

Oil price and macroeconomy in Russia. Abstract

Oil price and macroeconomy in Russia Katsuya Ito Fukuoka University Abstract In this note, using the VEC model we attempt to empirically investigate the effects of oil price and monetary shocks on the

Oil price and macroeconomy in Russia Katsuya Ito Fukuoka University Abstract In this note, using the VEC model we attempt to empirically investigate the effects of oil price and monetary shocks on the

Eco 200, part 3, Fall 2004 Lars Svensson 12/6/04. Liquidity traps, the zero lower bound for interest rates, and deflation

Eco 00, part 3, Fall 004 00L5.tex Lars Svensson /6/04 Liquidity traps, the zero lower bound for interest rates, and deflation The zero lower bound for interest rates (ZLB) A forward-looking aggregate-demand

Eco 00, part 3, Fall 004 00L5.tex Lars Svensson /6/04 Liquidity traps, the zero lower bound for interest rates, and deflation The zero lower bound for interest rates (ZLB) A forward-looking aggregate-demand

Information Bulletin 11/2011

Information Bulletin 11/2011 Warsaw, 2012 Compiled from NBP materials by the Department of Statistics as at January 13, 2012. Design: Oliwka s.c. Cover photo: Corbis/Free Layout and print: NBP Printshop

Information Bulletin 11/2011 Warsaw, 2012 Compiled from NBP materials by the Department of Statistics as at January 13, 2012. Design: Oliwka s.c. Cover photo: Corbis/Free Layout and print: NBP Printshop

Queen s University Department of Economics Instructor: Kevin Andrew

Queen s University Department of Economics Instructor: Kevin Andrew Econ 320: Assignment 4 Section A (100%): Long Answer Due: April 2nd 2014 3pm All questions of Equal Value 1. Consider the following version

Queen s University Department of Economics Instructor: Kevin Andrew Econ 320: Assignment 4 Section A (100%): Long Answer Due: April 2nd 2014 3pm All questions of Equal Value 1. Consider the following version

Information Bulletin 9/2011

Information Bulletin 9/2011 Warsaw, 2011 Compiled from NBP materials by the Department of Statistics as at November 1, 2011. Design: Oliwka s.c. Cover photo: Corbis/Free Layout and print: NBP Printshop

Information Bulletin 9/2011 Warsaw, 2011 Compiled from NBP materials by the Department of Statistics as at November 1, 2011. Design: Oliwka s.c. Cover photo: Corbis/Free Layout and print: NBP Printshop

Information Bulletin 12/2003

Information Bulletin 12/2003 Warsaw, April 2003 Compiled from NBP materials by the Department of Statistics as at March 15, 2004. Design: Oliwka s.c. Cover photo: Corbis/Free Layout and print: NBP Printshop

Information Bulletin 12/2003 Warsaw, April 2003 Compiled from NBP materials by the Department of Statistics as at March 15, 2004. Design: Oliwka s.c. Cover photo: Corbis/Free Layout and print: NBP Printshop

Information Bulletin 4/2007

Information Bulletin 4/2007 Warsaw, September 2007 Compiled from NBP materials by the Department of Statistics as at May 18, 2007. Design: Oliwka s.c. Cover photo: Corbis/Free Layout and print: NBP Printshop

Information Bulletin 4/2007 Warsaw, September 2007 Compiled from NBP materials by the Department of Statistics as at May 18, 2007. Design: Oliwka s.c. Cover photo: Corbis/Free Layout and print: NBP Printshop

Information Bulletin 4/2008

Information Bulletin 4/2008 Warsaw, August 2008 Compiled from NBP materials by the Department of Statistics as at June 17, 2008. Design: Oliwka s.c. Cover photo: Corbis/Free Layout and print: NBP Printshop

Information Bulletin 4/2008 Warsaw, August 2008 Compiled from NBP materials by the Department of Statistics as at June 17, 2008. Design: Oliwka s.c. Cover photo: Corbis/Free Layout and print: NBP Printshop

Information Bulletin 5/2007

Information Bulletin /2007 Warsaw, September 2007 Compiled from NBP materials by the Department of Statistics as at July 13, 2007. Design: Oliwka s.c. Cover photo: Corbis/Free Layout and print: NBP Printshop

Information Bulletin /2007 Warsaw, September 2007 Compiled from NBP materials by the Department of Statistics as at July 13, 2007. Design: Oliwka s.c. Cover photo: Corbis/Free Layout and print: NBP Printshop

Information Bulletin 12/2008

Information Bulletin 12/2008 Warsaw, May 2009 Compiled from NBP materials by the Department of Statistics as at February 12, 2009. Design: Oliwka s.c. Cover photo: Corbis/Free Layout and print: NBP Printshop

Information Bulletin 12/2008 Warsaw, May 2009 Compiled from NBP materials by the Department of Statistics as at February 12, 2009. Design: Oliwka s.c. Cover photo: Corbis/Free Layout and print: NBP Printshop

Monetary Policy and Exchange Rate Volatility in a Small Open Economy. Jordi Galí and Tommaso Monacelli. March 2005

Monetary Policy and Exchange Rate Volatility in a Small Open Economy by Jordi Galí and Tommaso Monacelli March 2005 Motivation The new Keynesian model for the closed economy - equilibrium dynamics: simple

Monetary Policy and Exchange Rate Volatility in a Small Open Economy by Jordi Galí and Tommaso Monacelli March 2005 Motivation The new Keynesian model for the closed economy - equilibrium dynamics: simple

Lars Svensson 10/2/05. Liquidity traps, the zero lower bound for interest rates, and deflation

Eco 00, part, Fall 005 00L5_F05.tex Lars Svensson 0//05 Liquidity traps, the zero lower bound for interest rates, and deflation Japan: recession, low growth since early 90s, deflation in GDP deflator and

Eco 00, part, Fall 005 00L5_F05.tex Lars Svensson 0//05 Liquidity traps, the zero lower bound for interest rates, and deflation Japan: recession, low growth since early 90s, deflation in GDP deflator and

Stagnation Traps. Gianluca Benigno and Luca Fornaro

Stagnation Traps Gianluca Benigno and Luca Fornaro May 2015 Research question and motivation Can insu cient aggregate demand lead to economic stagnation? This question goes back, at least, to the Great

Stagnation Traps Gianluca Benigno and Luca Fornaro May 2015 Research question and motivation Can insu cient aggregate demand lead to economic stagnation? This question goes back, at least, to the Great

Macroeconomics II. Dynamic AD-AS model

Macroeconomics II Dynamic AD-AS model Vahagn Jerbashian Ch. 14 from Mankiw (2010) Spring 2018 Where we are heading to We will incorporate dynamics into the standard AD-AS model This will offer another

Macroeconomics II Dynamic AD-AS model Vahagn Jerbashian Ch. 14 from Mankiw (2010) Spring 2018 Where we are heading to We will incorporate dynamics into the standard AD-AS model This will offer another

Dynamic AD-AS model vs. AD-AS model Notes. Dynamic AD-AS model in a few words Notes. Notation to incorporate time-dimension Notes

Macroeconomics II Dynamic AD-AS model Vahagn Jerbashian Ch. 14 from Mankiw (2010) Spring 2018 Where we are heading to We will incorporate dynamics into the standard AD-AS model This will offer another

Macroeconomics II Dynamic AD-AS model Vahagn Jerbashian Ch. 14 from Mankiw (2010) Spring 2018 Where we are heading to We will incorporate dynamics into the standard AD-AS model This will offer another

Information Bulletin 11/2010

Information Bulletin 11/2010 Warsaw, 2011 Compiled from NBP materials by the Department of Statistics as at January 13, 2011. Design: Oliwka s.c. Cover photo: Corbis/Free Layout and print: NBP Printshop

Information Bulletin 11/2010 Warsaw, 2011 Compiled from NBP materials by the Department of Statistics as at January 13, 2011. Design: Oliwka s.c. Cover photo: Corbis/Free Layout and print: NBP Printshop

Information Bulletin 8/2009

Information Bulletin 8/2009 Warsaw, 2010 Compiled from NBP materials by the Department of Statistics as at October 13, 2009. Design: Oliwka s.c. Cover photo: Corbis/Free Layout and print: NBP Printshop

Information Bulletin 8/2009 Warsaw, 2010 Compiled from NBP materials by the Department of Statistics as at October 13, 2009. Design: Oliwka s.c. Cover photo: Corbis/Free Layout and print: NBP Printshop

Final Exam. You may not use calculators, notes, or aids of any kind.

Professor Christiano Economics 311, Winter 2005 Final Exam IMPORTANT: read the following notes You may not use calculators, notes, or aids of any kind. A total of 100 points is possible, with the distribution

Professor Christiano Economics 311, Winter 2005 Final Exam IMPORTANT: read the following notes You may not use calculators, notes, or aids of any kind. A total of 100 points is possible, with the distribution

The Dornbusch overshooting model

4330 Lecture 8 Ragnar Nymoen 12 March 2012 References I Lecture 7: Portfolio model of the FEX market extended by money. Important concepts: monetary policy regimes degree of sterilization Monetary model

4330 Lecture 8 Ragnar Nymoen 12 March 2012 References I Lecture 7: Portfolio model of the FEX market extended by money. Important concepts: monetary policy regimes degree of sterilization Monetary model

Has the crisis changed the monetary transmission mechanism in Albania? An application of kernel density estimation technique.

Has the crisis changed the monetary transmission mechanism in Albania? An application of kernel density estimation technique. 6th Research Conference Central Banking under Prolonged Global Uncertainty:

Has the crisis changed the monetary transmission mechanism in Albania? An application of kernel density estimation technique. 6th Research Conference Central Banking under Prolonged Global Uncertainty:

Lecture 1 Introduction and Historical Notes

Lecture and Historical Notes s 5415 Index Number Theory Winter 2019 Outline Test 2 3 4 5 6 Test 7 Required Readings Test Diewert, W.E. (1993) Early History of Price Index Research, in Diewert and Nakamura

Lecture and Historical Notes s 5415 Index Number Theory Winter 2019 Outline Test 2 3 4 5 6 Test 7 Required Readings Test Diewert, W.E. (1993) Early History of Price Index Research, in Diewert and Nakamura

Gold Rush Fever in Business Cycles

Gold Rush Fever in Business Cycles Paul Beaudry, Fabrice Collard & Franck Portier University of British Columbia & Université de Toulouse UAB Seminar Barcelona November, 29, 26 The Klondike Gold Rush of

Gold Rush Fever in Business Cycles Paul Beaudry, Fabrice Collard & Franck Portier University of British Columbia & Université de Toulouse UAB Seminar Barcelona November, 29, 26 The Klondike Gold Rush of

Information Bulletin 2/2011

Information Bulletin 2/2011 Warsaw, 2011 Compiled from NBP materials by the Department of Statistics as at April 13, 2011. Design: Oliwka s.c. Cover photo: Corbis/Free Layout and print: NBP Printshop Published

Information Bulletin 2/2011 Warsaw, 2011 Compiled from NBP materials by the Department of Statistics as at April 13, 2011. Design: Oliwka s.c. Cover photo: Corbis/Free Layout and print: NBP Printshop Published

Gold Rush Fever in Business Cycles

Gold Rush Fever in Business Cycles Paul Beaudry, Fabrice Collard & Franck Portier University of British Columbia & Université de Toulouse Banque Nationale Nationale Bank Belgischen de Belgique van Belgïe

Gold Rush Fever in Business Cycles Paul Beaudry, Fabrice Collard & Franck Portier University of British Columbia & Université de Toulouse Banque Nationale Nationale Bank Belgischen de Belgique van Belgïe

The Neo Fisher Effect and Exiting a Liquidity Trap

The Neo Fisher Effect and Exiting a Liquidity Trap Stephanie Schmitt-Grohé and Martín Uribe Columbia University European Central Bank Conference on Monetary Policy Frankfurt am Main, October 29-3, 218

The Neo Fisher Effect and Exiting a Liquidity Trap Stephanie Schmitt-Grohé and Martín Uribe Columbia University European Central Bank Conference on Monetary Policy Frankfurt am Main, October 29-3, 218

Information Bulletin 10/2008

Information Bulletin 10/2008 Warsaw, February 2009 Compiled from NBP materials by the Department of Statistics as at December 12, 2008. Design: Oliwka s.c. Cover photo: Corbis/Free Layout and print: NBP

Information Bulletin 10/2008 Warsaw, February 2009 Compiled from NBP materials by the Department of Statistics as at December 12, 2008. Design: Oliwka s.c. Cover photo: Corbis/Free Layout and print: NBP

Part A: Answer question A1 (required), plus either question A2 or A3.

, plus either question A2 or A3.") Ph.D. Core Exam -- Macroeconomics 5 January 2015 -- 8:00 am to 3:00 pm Part A: Answer question A1 (required), plus either question A2 or A3. A1 (required): Ending Quantitative Easing Now that the U.S.

Ph.D. Core Exam -- Macroeconomics 5 January 2015 -- 8:00 am to 3:00 pm Part A: Answer question A1 (required), plus either question A2 or A3. A1 (required): Ending Quantitative Easing Now that the U.S.

Toulouse School of Economics, Macroeconomics II Franck Portier. Homework 1. Problem I An AD-AS Model

Toulouse School of Economics, 2009-2010 Macroeconomics II Franck Portier Homework 1 Problem I An AD-AS Model Let us consider an economy with three agents (a firm, a household and a government) and four

Toulouse School of Economics, 2009-2010 Macroeconomics II Franck Portier Homework 1 Problem I An AD-AS Model Let us consider an economy with three agents (a firm, a household and a government) and four

Financial Factors in Economic Fluctuations. Lawrence Christiano Roberto Motto Massimo Rostagno

Financial Factors in Economic Fluctuations Lawrence Christiano Roberto Motto Massimo Rostagno Background Much progress made on constructing and estimating models that fit quarterly data well (Smets-Wouters,

Financial Factors in Economic Fluctuations Lawrence Christiano Roberto Motto Massimo Rostagno Background Much progress made on constructing and estimating models that fit quarterly data well (Smets-Wouters,

Information Bulletin 1/2008

Information Bulletin 1/2008 Warsaw, May 2008 Compiled from NBP materials by the Department of Statistics as at March 13, 2008. Design: Oliwka s.c. Cover photo: Corbis/Free Layout and print: NBP Printshop

Information Bulletin 1/2008 Warsaw, May 2008 Compiled from NBP materials by the Department of Statistics as at March 13, 2008. Design: Oliwka s.c. Cover photo: Corbis/Free Layout and print: NBP Printshop

Source: US. Bureau of Economic Analysis Shaded areas indicate US recessions research.stlouisfed.org

Business Cycles 0 Real Gross Domestic Product 18,000 16,000 (Billions of Chained 2009 Dollars) 14,000 12,000 10,000 8,000 6,000 4,000 2,000 1940 1960 1980 2000 Source: US. Bureau of Economic Analysis Shaded

Business Cycles 0 Real Gross Domestic Product 18,000 16,000 (Billions of Chained 2009 Dollars) 14,000 12,000 10,000 8,000 6,000 4,000 2,000 1940 1960 1980 2000 Source: US. Bureau of Economic Analysis Shaded

Identifying the Monetary Policy Shock Christiano et al. (1999)

") Identifying the Monetary Policy Shock Christiano et al. (1999) The question we are asking is: What are the consequences of a monetary policy shock a shock which is purely related to monetary conditions

Identifying the Monetary Policy Shock Christiano et al. (1999) The question we are asking is: What are the consequences of a monetary policy shock a shock which is purely related to monetary conditions

Extended IS-LM model - construction and analysis of behavior

Extended IS-LM model - construction and analysis of behavior David Martinčík Department of Economics and Finance, Faculty of Economics, University of West Bohemia, martinci@kef.zcu.cz Blanka Šedivá Department

Extended IS-LM model - construction and analysis of behavior David Martinčík Department of Economics and Finance, Faculty of Economics, University of West Bohemia, martinci@kef.zcu.cz Blanka Šedivá Department

A Modern Equilibrium Model. Jesús Fernández-Villaverde University of Pennsylvania

A Modern Equilibrium Model Jesús Fernández-Villaverde University of Pennsylvania 1 Household Problem Preferences: max E X β t t=0 c 1 σ t 1 σ ψ l1+γ t 1+γ Budget constraint: c t + k t+1 = w t l t + r t

A Modern Equilibrium Model Jesús Fernández-Villaverde University of Pennsylvania 1 Household Problem Preferences: max E X β t t=0 c 1 σ t 1 σ ψ l1+γ t 1+γ Budget constraint: c t + k t+1 = w t l t + r t

4- Current Method of Explaining Business Cycles: DSGE Models. Basic Economic Models

4- Current Method of Explaining Business Cycles: DSGE Models Basic Economic Models In Economics, we use theoretical models to explain the economic processes in the real world. These models de ne a relation

4- Current Method of Explaining Business Cycles: DSGE Models Basic Economic Models In Economics, we use theoretical models to explain the economic processes in the real world. These models de ne a relation

Information Bulletin 6/2008

Information Bulletin 6/2008 Warsaw, October 2008 Compiled from NBP materials by the Department of Statistics as at August 12, 2008. Design: Oliwka s.c. Cover photo: Corbis/Free Layout and print: NBP Printshop

Information Bulletin 6/2008 Warsaw, October 2008 Compiled from NBP materials by the Department of Statistics as at August 12, 2008. Design: Oliwka s.c. Cover photo: Corbis/Free Layout and print: NBP Printshop

A Dynamic Model of Aggregate Demand and Aggregate Supply

A Dynamic Model of Aggregate Demand and Aggregate Supply 1 Introduction Theoritical Backround 2 3 4 I Introduction Theoritical Backround The model emphasizes the dynamic nature of economic fluctuations.

A Dynamic Model of Aggregate Demand and Aggregate Supply 1 Introduction Theoritical Backround 2 3 4 I Introduction Theoritical Backround The model emphasizes the dynamic nature of economic fluctuations.

Topic 4 Forecasting Exchange Rate

Topic 4 Forecasting Exchange Rate Why Firms Forecast Exchange Rates MNCs need exchange rate forecasts for their: hedging decisions, short-term financing decisions, short-term investment decisions, capital

Topic 4 Forecasting Exchange Rate Why Firms Forecast Exchange Rates MNCs need exchange rate forecasts for their: hedging decisions, short-term financing decisions, short-term investment decisions, capital

Online Appendix for Investment Hangover and the Great Recession

ONLINE APPENDIX INVESTMENT HANGOVER A1 Online Appendix for Investment Hangover and the Great Recession By MATTHEW ROGNLIE, ANDREI SHLEIFER, AND ALP SIMSEK APPENDIX A: CALIBRATION This appendix describes

ONLINE APPENDIX INVESTMENT HANGOVER A1 Online Appendix for Investment Hangover and the Great Recession By MATTHEW ROGNLIE, ANDREI SHLEIFER, AND ALP SIMSEK APPENDIX A: CALIBRATION This appendix describes

THE LONG-RUN DETERMINANTS OF MONEY DEMAND IN SLOVAKIA MARTIN LUKÁČIK - ADRIANA LUKÁČIKOVÁ - KAROL SZOMOLÁNYI

92 Multiple Criteria Decision Making XIII THE LONG-RUN DETERMINANTS OF MONEY DEMAND IN SLOVAKIA MARTIN LUKÁČIK - ADRIANA LUKÁČIKOVÁ - KAROL SZOMOLÁNYI Abstract: The paper verifies the long-run determinants

92 Multiple Criteria Decision Making XIII THE LONG-RUN DETERMINANTS OF MONEY DEMAND IN SLOVAKIA MARTIN LUKÁČIK - ADRIANA LUKÁČIKOVÁ - KAROL SZOMOLÁNYI Abstract: The paper verifies the long-run determinants

Lecture 3, November 30: The Basic New Keynesian Model (Galí, Chapter 3)

") MakØk3, Fall 2 (blok 2) Business cycles and monetary stabilization policies Henrik Jensen Department of Economics University of Copenhagen Lecture 3, November 3: The Basic New Keynesian Model (Galí, Chapter

MakØk3, Fall 2 (blok 2) Business cycles and monetary stabilization policies Henrik Jensen Department of Economics University of Copenhagen Lecture 3, November 3: The Basic New Keynesian Model (Galí, Chapter

Relationships between phases of business cycles in two large open economies

Journal of Regional Development Studies2010 131 Relationships between phases of business cycles in two large open economies Ken-ichi ISHIYAMA 1. Introduction We have observed large increases in trade and

Journal of Regional Development Studies2010 131 Relationships between phases of business cycles in two large open economies Ken-ichi ISHIYAMA 1. Introduction We have observed large increases in trade and

Optimal Simple And Implementable Monetary and Fiscal Rules

Optimal Simple And Implementable Monetary and Fiscal Rules Stephanie Schmitt-Grohé Martín Uribe Duke University September 2007 1 Welfare-Based Policy Evaluation: Related Literature (ex: Rotemberg and Woodford,

Optimal Simple And Implementable Monetary and Fiscal Rules Stephanie Schmitt-Grohé Martín Uribe Duke University September 2007 1 Welfare-Based Policy Evaluation: Related Literature (ex: Rotemberg and Woodford,

Monetary Economics. Lecture 15: unemployment in the new Keynesian model, part one. Chris Edmond. 2nd Semester 2014

Monetary Economics Lecture 15: unemployment in the new Keynesian model, part one Chris Edmond 2nd Semester 214 1 This class Unemployment fluctuations in the new Keynesian model, part one Main reading:

Monetary Economics Lecture 15: unemployment in the new Keynesian model, part one Chris Edmond 2nd Semester 214 1 This class Unemployment fluctuations in the new Keynesian model, part one Main reading:

EXAMINATION QUESTIONS 63. P f. P d. = e n

EXAMINATION QUESTIONS 63 If e r is constant its growth rate is zero, so that this may be rearranged as e n = e n P f P f P d P d This is positive if the foreign inflation rate exceeds the domestic, indicating

EXAMINATION QUESTIONS 63 If e r is constant its growth rate is zero, so that this may be rearranged as e n = e n P f P f P d P d This is positive if the foreign inflation rate exceeds the domestic, indicating

Adverse Effects of Monetary Policy Signalling

Adverse Effects of Monetary Policy Signalling Jan FILÁČEK and Jakub MATĚJŮ Monetary Department Czech National Bank CNB Research Open Day, 18 th May 21 Outline What do we mean by adverse effects of monetary

Adverse Effects of Monetary Policy Signalling Jan FILÁČEK and Jakub MATĚJŮ Monetary Department Czech National Bank CNB Research Open Day, 18 th May 21 Outline What do we mean by adverse effects of monetary

The welfare cost of energy insecurity

The welfare cost of energy insecurity Baltasar Manzano (Universidade de Vigo) Luis Rey (bc3) IEW 2013 1 INTRODUCTION The 1973-1974 oil crisis revealed the vulnerability of developed economies to oil price

The welfare cost of energy insecurity Baltasar Manzano (Universidade de Vigo) Luis Rey (bc3) IEW 2013 1 INTRODUCTION The 1973-1974 oil crisis revealed the vulnerability of developed economies to oil price

The Basic New Keynesian Model. Jordi Galí. November 2010

The Basic New Keynesian Model by Jordi Galí November 2 Motivation and Outline Evidence on Money, Output, and Prices: Short Run E ects of Monetary Policy Shocks (i) persistent e ects on real variables (ii)

The Basic New Keynesian Model by Jordi Galí November 2 Motivation and Outline Evidence on Money, Output, and Prices: Short Run E ects of Monetary Policy Shocks (i) persistent e ects on real variables (ii)

Information Bulletin 7/2007

Information Bulletin 7/2007 Warsaw, December 2007 Compiled from NBP materials by the Department of Statistics as at September 12, 2007. Design: Oliwka s.c. Cover photo: Corbis/Free Layout and print: NBP

Information Bulletin 7/2007 Warsaw, December 2007 Compiled from NBP materials by the Department of Statistics as at September 12, 2007. Design: Oliwka s.c. Cover photo: Corbis/Free Layout and print: NBP

Business Cycles and Exchange Rate Regimes

Business Cycles and Exchange Rate Regimes Christian Zimmermann Département des sciences économiques, Université du Québec à Montréal (UQAM) Center for Research on Economic Fluctuations and Employment (CREFE)

Business Cycles and Exchange Rate Regimes Christian Zimmermann Département des sciences économiques, Université du Québec à Montréal (UQAM) Center for Research on Economic Fluctuations and Employment (CREFE)

Information Bulletin 9/2007

Information Bulletin 9/2007 Warsaw, January 2008 Compiled from NBP materials by the Department of Statistics as at November 13, 2007. Design: Oliwka s.c. Cover photo: Corbis/Free Layout and print: NBP

Information Bulletin 9/2007 Warsaw, January 2008 Compiled from NBP materials by the Department of Statistics as at November 13, 2007. Design: Oliwka s.c. Cover photo: Corbis/Free Layout and print: NBP

Dynamic stochastic general equilibrium models. December 4, 2007

Dynamic stochastic general equilibrium models December 4, 2007 Dynamic stochastic general equilibrium models Random shocks to generate trajectories that look like the observed national accounts. Rational

Dynamic stochastic general equilibrium models December 4, 2007 Dynamic stochastic general equilibrium models Random shocks to generate trajectories that look like the observed national accounts. Rational

The Basic New Keynesian Model. Jordi Galí. June 2008

The Basic New Keynesian Model by Jordi Galí June 28 Motivation and Outline Evidence on Money, Output, and Prices: Short Run E ects of Monetary Policy Shocks (i) persistent e ects on real variables (ii)

The Basic New Keynesian Model by Jordi Galí June 28 Motivation and Outline Evidence on Money, Output, and Prices: Short Run E ects of Monetary Policy Shocks (i) persistent e ects on real variables (ii)

The Dynamics of the U.S. Trade Balance and the Real Exchange Rate: The J Curve and Trade Costs? by George Alessandria (Rochester) Horag Choi (Monash)

Horag Choi (Monash)") Discussion of The Dynamics of the U.S. Trade Balance and the Real Exchange Rate: The J Curve and Trade Costs? by George Alessandria (Rochester) Horag Choi (Monash) Brent Neiman University of Chicago and

Discussion of The Dynamics of the U.S. Trade Balance and the Real Exchange Rate: The J Curve and Trade Costs? by George Alessandria (Rochester) Horag Choi (Monash) Brent Neiman University of Chicago and

The Central Bank of Iceland forecasting record

Forecasting errors are inevitable. Some stem from errors in the models used for forecasting, others are due to inaccurate information on the economic variables on which the models are based measurement

Forecasting errors are inevitable. Some stem from errors in the models used for forecasting, others are due to inaccurate information on the economic variables on which the models are based measurement

LEIBNIZ INSTITUTE OF AGRICULTURAL DEVELOPMENT

LEIBNIZ INSTITUTE OF AGRICULTURAL DEVELOPMENT IN TRANSITION ECONOMIES IAMO Forum 2017 Halle (Saale) Estimates for the residual demand elasticity of Russian wheat exports Kerstin Uhl, Oleksandr Perekhozhuk,

LEIBNIZ INSTITUTE OF AGRICULTURAL DEVELOPMENT IN TRANSITION ECONOMIES IAMO Forum 2017 Halle (Saale) Estimates for the residual demand elasticity of Russian wheat exports Kerstin Uhl, Oleksandr Perekhozhuk,

Monetary Economics: Problem Set #4 Solutions

Monetary Economics Problem Set #4 Monetary Economics: Problem Set #4 Solutions This problem set is marked out of 100 points. The weight given to each part is indicated below. Please contact me asap if

Monetary Economics Problem Set #4 Monetary Economics: Problem Set #4 Solutions This problem set is marked out of 100 points. The weight given to each part is indicated below. Please contact me asap if

Inflation Report April June 2012

August, 212 Outline 1. External Conditions 2. Economic Activity in Mexico 3. Monetary Policy and Inflation Determinants. Forecasts and Balance of Risks External Conditions Global economic growth slowed

August, 212 Outline 1. External Conditions 2. Economic Activity in Mexico 3. Monetary Policy and Inflation Determinants. Forecasts and Balance of Risks External Conditions Global economic growth slowed

Latent variables and shocks contribution in DSGE models with occasionally binding constraints

Latent variables and shocks contribution in DSGE models with occasionally binding constraints May 29, 2016 1 Marco Ratto, Massimo Giovannini (European Commission, Joint Research Centre) We implement an

Latent variables and shocks contribution in DSGE models with occasionally binding constraints May 29, 2016 1 Marco Ratto, Massimo Giovannini (European Commission, Joint Research Centre) We implement an

Dynamics and Monetary Policy in a Fair Wage Model of the Business Cycle

Dynamics and Monetary Policy in a Fair Wage Model of the Business Cycle David de la Croix 1,3 Gregory de Walque 2 Rafael Wouters 2,1 1 dept. of economics, Univ. cath. Louvain 2 National Bank of Belgium

Dynamics and Monetary Policy in a Fair Wage Model of the Business Cycle David de la Croix 1,3 Gregory de Walque 2 Rafael Wouters 2,1 1 dept. of economics, Univ. cath. Louvain 2 National Bank of Belgium

Melitz, M. J. & G. I. P. Ottaviano. Peter Eppinger. July 22, 2011

Melitz, M. J. & G. I. P. Ottaviano University of Munich July 22, 2011 & 1 / 20 & & 2 / 20 My Bachelor Thesis: Ottaviano et al. (2009) apply the model to study gains from the euro & 3 / 20 Melitz and Ottaviano

Melitz, M. J. & G. I. P. Ottaviano University of Munich July 22, 2011 & 1 / 20 & & 2 / 20 My Bachelor Thesis: Ottaviano et al. (2009) apply the model to study gains from the euro & 3 / 20 Melitz and Ottaviano

ADVANCED MACROECONOMICS I

Name: Students ID: ADVANCED MACROECONOMICS I I. Short Questions (21/2 points each) Mark the following statements as True (T) or False (F) and give a brief explanation of your answer in each case. 1. 2.

Name: Students ID: ADVANCED MACROECONOMICS I I. Short Questions (21/2 points each) Mark the following statements as True (T) or False (F) and give a brief explanation of your answer in each case. 1. 2.

Nonlinear Exchange Rate Pass-Through : Does Business Cycle Matter? Abstract

Journal of Economic Integration Vol.33 No.2, June, 2018, 1234~1261 http://dx.doi.org/10.11130/.2018.33.2.1235 Nonlinear Exchange Rate Pass-Through : Does Business Cycle Matter? Nidhaleddine Ben Cheikh

Journal of Economic Integration Vol.33 No.2, June, 2018, 1234~1261 http://dx.doi.org/10.11130/.2018.33.2.1235 Nonlinear Exchange Rate Pass-Through : Does Business Cycle Matter? Nidhaleddine Ben Cheikh

Melitz, M. J. & G. I. P. Ottaviano. Peter Eppinger. July 22, 2011

Melitz, M. J. & G. I. P. Ottaviano University of Munich July 22, 2011 & 1 / 20 & & 2 / 20 My Bachelor Thesis: Ottaviano et al. (2009) apply the model to study gains from the euro & 3 / 20 Melitz and Ottaviano

Melitz, M. J. & G. I. P. Ottaviano University of Munich July 22, 2011 & 1 / 20 & & 2 / 20 My Bachelor Thesis: Ottaviano et al. (2009) apply the model to study gains from the euro & 3 / 20 Melitz and Ottaviano

Aggregate Demand, Idle Time, and Unemployment

Aggregate Demand, Idle Time, and Unemployment Pascal Michaillat (LSE) & Emmanuel Saez (Berkeley) September 2014 1 / 44 Motivation 11% Unemployment rate 9% 7% 5% 3% 1974 1984 1994 2004 2014 2 / 44 Motivation

Aggregate Demand, Idle Time, and Unemployment Pascal Michaillat (LSE) & Emmanuel Saez (Berkeley) September 2014 1 / 44 Motivation 11% Unemployment rate 9% 7% 5% 3% 1974 1984 1994 2004 2014 2 / 44 Motivation

The New Keynesian Model: Introduction

The New Keynesian Model: Introduction Vivaldo M. Mendes ISCTE Lisbon University Institute 13 November 2017 (Vivaldo M. Mendes) The New Keynesian Model: Introduction 13 November 2013 1 / 39 Summary 1 What

The New Keynesian Model: Introduction Vivaldo M. Mendes ISCTE Lisbon University Institute 13 November 2017 (Vivaldo M. Mendes) The New Keynesian Model: Introduction 13 November 2013 1 / 39 Summary 1 What

Does Pleasing Export-Oriented Foreign Investors Help Your. Balance of Payments? A General Equilibrium Analysis. (Available on Request Appendix)

") Does Pleasing Export-Oriented Foreign Investors Help Your Balance of Payments? A General Equilibrium Analysis (Available on Request Appendix) Derivation of the Excess Demand Equations, the IS Equation,

Does Pleasing Export-Oriented Foreign Investors Help Your Balance of Payments? A General Equilibrium Analysis (Available on Request Appendix) Derivation of the Excess Demand Equations, the IS Equation,

Aggregate Demand, Idle Time, and Unemployment

Aggregate Demand, Idle Time, and Unemployment Pascal Michaillat (LSE) & Emmanuel Saez (Berkeley) July 2014 1 / 46 Motivation 11% Unemployment rate 9% 7% 5% 3% 1974 1984 1994 2004 2014 2 / 46 Motivation

Aggregate Demand, Idle Time, and Unemployment Pascal Michaillat (LSE) & Emmanuel Saez (Berkeley) July 2014 1 / 46 Motivation 11% Unemployment rate 9% 7% 5% 3% 1974 1984 1994 2004 2014 2 / 46 Motivation

Problem Set 4. Graduate Macro II, Spring 2011 The University of Notre Dame Professor Sims

Problem Set 4 Graduate Macro II, Spring 2011 The University of Notre Dame Professor Sims Instructions: You may consult with other members of the class, but please make sure to turn in your own work. Where

Problem Set 4 Graduate Macro II, Spring 2011 The University of Notre Dame Professor Sims Instructions: You may consult with other members of the class, but please make sure to turn in your own work. Where

Monetary Policy and Unemployment: A New Keynesian Perspective

Monetary Policy and Unemployment: A New Keynesian Perspective Jordi Galí CREI, UPF and Barcelona GSE April 215 Jordi Galí (CREI, UPF and Barcelona GSE) Monetary Policy and Unemployment April 215 1 / 16

Monetary Policy and Unemployment: A New Keynesian Perspective Jordi Galí CREI, UPF and Barcelona GSE April 215 Jordi Galí (CREI, UPF and Barcelona GSE) Monetary Policy and Unemployment April 215 1 / 16

Identifying Aggregate Liquidity Shocks with Monetary Policy Shocks: An Application using UK Data

Identifying Aggregate Liquidity Shocks with Monetary Policy Shocks: An Application using UK Data Michael Ellington and Costas Milas Financial Services, Liquidity and Economic Activity Bank of England May

Identifying Aggregate Liquidity Shocks with Monetary Policy Shocks: An Application using UK Data Michael Ellington and Costas Milas Financial Services, Liquidity and Economic Activity Bank of England May

Monetary Policy in a Macro Model

Monetary Policy in a Macro Model ECON 40364: Monetary Theory & Policy Eric Sims University of Notre Dame Fall 2017 1 / 67 Readings Mishkin Ch. 20 Mishkin Ch. 21 Mishkin Ch. 22 Mishkin Ch. 23, pg. 553-569

Monetary Policy in a Macro Model ECON 40364: Monetary Theory & Policy Eric Sims University of Notre Dame Fall 2017 1 / 67 Readings Mishkin Ch. 20 Mishkin Ch. 21 Mishkin Ch. 22 Mishkin Ch. 23, pg. 553-569

Forecasting the Canadian Dollar Exchange Rate Wissam Saleh & Pablo Navarro

Forecasting the Canadian Dollar Exchange Rate Wissam Saleh & Pablo Navarro Research Question: What variables effect the Canadian/US exchange rate? Do energy prices have an effect on the Canadian/US exchange

Forecasting the Canadian Dollar Exchange Rate Wissam Saleh & Pablo Navarro Research Question: What variables effect the Canadian/US exchange rate? Do energy prices have an effect on the Canadian/US exchange

Macroeconomics Theory II

Macroeconomics Theory II Francesco Franco Nova SBE March 9, 216 Francesco Franco Macroeconomics Theory II 1/29 The Open Economy Two main paradigms Small Open Economy: the economy trades with the ROW but

Macroeconomics Theory II Francesco Franco Nova SBE March 9, 216 Francesco Franco Macroeconomics Theory II 1/29 The Open Economy Two main paradigms Small Open Economy: the economy trades with the ROW but

Modeling the Global Wheat Market Using a GVAR Model. Elselien Breman and Cornelis Gardebroek

Modeling the Global Wheat Market Using a GVAR Model Elselien Breman and Cornelis Gardebroek Selected Paper prepared for presentation at the International Agricultural Trade Research Consortium s (IATRC

Modeling the Global Wheat Market Using a GVAR Model Elselien Breman and Cornelis Gardebroek Selected Paper prepared for presentation at the International Agricultural Trade Research Consortium s (IATRC

International Macro Finance

International Macro Finance Economies as Dynamic Systems Francesco Franco Nova SBE February 21, 2013 Francesco Franco International Macro Finance 1/39 Flashback Mundell-Fleming MF on the whiteboard Francesco

International Macro Finance Economies as Dynamic Systems Francesco Franco Nova SBE February 21, 2013 Francesco Franco International Macro Finance 1/39 Flashback Mundell-Fleming MF on the whiteboard Francesco

IS-LM Analysis. Math 202. Brian D. Fitzpatrick. Duke University. February 14, 2018 MATH

IS-LM Analysis Math 202 Brian D. Fitzpatrick Duke University February 14, 2018 MATH Overview Background History Variables The GDP Equation Definition of GDP Assumptions The GDP Equation with Assumptions

IS-LM Analysis Math 202 Brian D. Fitzpatrick Duke University February 14, 2018 MATH Overview Background History Variables The GDP Equation Definition of GDP Assumptions The GDP Equation with Assumptions

MA Macroeconomics 3. Introducing the IS-MP-PC Model

MA Macroeconomics 3. Introducing the IS-MP-PC Model Karl Whelan School of Economics, UCD Autumn 2014 Karl Whelan (UCD) Introducing the IS-MP-PC Model Autumn 2014 1 / 38 Beyond IS-LM We have reviewed the

MA Macroeconomics 3. Introducing the IS-MP-PC Model Karl Whelan School of Economics, UCD Autumn 2014 Karl Whelan (UCD) Introducing the IS-MP-PC Model Autumn 2014 1 / 38 Beyond IS-LM We have reviewed the

Demand Shocks, Monetary Policy, and the Optimal Use of Dispersed Information

Demand Shocks, Monetary Policy, and the Optimal Use of Dispersed Information Guido Lorenzoni (MIT) WEL-MIT-Central Banks, December 2006 Motivation Central bank observes an increase in spending Is it driven

Demand Shocks, Monetary Policy, and the Optimal Use of Dispersed Information Guido Lorenzoni (MIT) WEL-MIT-Central Banks, December 2006 Motivation Central bank observes an increase in spending Is it driven

Product Introductions, Currency Unions, and the Real Exchange Rate

Product Introductions, Currency Unions, and the Real Exchange Rate Alberto Cavallo Brent Neiman Roberto Rigobon MIT University of Chicago MIT May, 2013 Motivation Classic theories of the real exchange

Product Introductions, Currency Unions, and the Real Exchange Rate Alberto Cavallo Brent Neiman Roberto Rigobon MIT University of Chicago MIT May, 2013 Motivation Classic theories of the real exchange

Monetary Economics: Solutions Problem Set 1

Monetary Economics: Solutions Problem Set 1 December 14, 2006 Exercise 1 A Households Households maximise their intertemporal utility function by optimally choosing consumption, savings, and the mix of

Monetary Economics: Solutions Problem Set 1 December 14, 2006 Exercise 1 A Households Households maximise their intertemporal utility function by optimally choosing consumption, savings, and the mix of

Can News be a Major Source of Aggregate Fluctuations?

Can News be a Major Source of Aggregate Fluctuations? A Bayesian DSGE Approach Ippei Fujiwara 1 Yasuo Hirose 1 Mototsugu 2 1 Bank of Japan 2 Vanderbilt University August 4, 2009 Contributions of this paper

Can News be a Major Source of Aggregate Fluctuations? A Bayesian DSGE Approach Ippei Fujiwara 1 Yasuo Hirose 1 Mototsugu 2 1 Bank of Japan 2 Vanderbilt University August 4, 2009 Contributions of this paper

S TICKY I NFORMATION Fabio Verona Bank of Finland, Monetary Policy and Research Department, Research Unit

B USINESS C YCLE DYNAMICS UNDER S TICKY I NFORMATION Fabio Verona Bank of Finland, Monetary Policy and Research Department, Research Unit fabio.verona@bof.fi O BJECTIVE : analyze how and to what extent

B USINESS C YCLE DYNAMICS UNDER S TICKY I NFORMATION Fabio Verona Bank of Finland, Monetary Policy and Research Department, Research Unit fabio.verona@bof.fi O BJECTIVE : analyze how and to what extent

Learning about Monetary Policy using (S)VARs? Some Pitfalls and Possible Solutions

VARs? Some Pitfalls and Possible Solutions") Learning about Monetary Policy using (S)VARs? Some Pitfalls and Possible Solutions Michal Andrle and Jan Brůha Interim: B4/13, April 214 Michal Andrle: The views expressed herein are those of the authors

Learning about Monetary Policy using (S)VARs? Some Pitfalls and Possible Solutions Michal Andrle and Jan Brůha Interim: B4/13, April 214 Michal Andrle: The views expressed herein are those of the authors

Euro-indicators Working Group

Euro-indicators Working Group Luxembourg, 9 th & 10 th June 2011 Item 9.4 of the Agenda New developments in EuroMIND estimates Rosa Ruggeri Cannata Doc 309/11 What is EuroMIND? EuroMIND is a Monthly INDicator

Euro-indicators Working Group Luxembourg, 9 th & 10 th June 2011 Item 9.4 of the Agenda New developments in EuroMIND estimates Rosa Ruggeri Cannata Doc 309/11 What is EuroMIND? EuroMIND is a Monthly INDicator

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 10

UNIVERSIT OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 10 THE ZERO LOWER BOUND IN THE IS-MP-IA FRAMEWORK FEBRUAR 21, 2018 I. INTRODUCTION II. THE IS-MP-IA

UNIVERSIT OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 10 THE ZERO LOWER BOUND IN THE IS-MP-IA FRAMEWORK FEBRUAR 21, 2018 I. INTRODUCTION II. THE IS-MP-IA

The 2001 recession displayed unique characteristics in comparison to other

Smoothing the Shocks of a Dynamic Stochastic General Equilibrium Model ANDREW BAUER NICHOLAS HALTOM AND JUAN F RUBIO-RAMÍREZ Bauer and Haltom are senior economic analysts and Rubio-Ramírez is an economist

Smoothing the Shocks of a Dynamic Stochastic General Equilibrium Model ANDREW BAUER NICHOLAS HALTOM AND JUAN F RUBIO-RAMÍREZ Bauer and Haltom are senior economic analysts and Rubio-Ramírez is an economist

Seoul National University Mini-Course: Monetary & Fiscal Policy Interactions II

Seoul National University Mini-Course: Monetary & Fiscal Policy Interactions II Eric M. Leeper Indiana University July/August 2013 Linear Analysis Generalize policy behavior with a conventional parametric

Seoul National University Mini-Course: Monetary & Fiscal Policy Interactions II Eric M. Leeper Indiana University July/August 2013 Linear Analysis Generalize policy behavior with a conventional parametric

APPENDIX TO RESERVE REQUIREMENTS AND OPTIMAL CHINESE STABILIZATION POLICY

APPENDIX TO RESERVE REQUIREMENTS AND OPTIMAL CHINESE STABILIZATION POLICY CHUN CHANG ZHENG LIU MARK M. SPIEGEL JINGYI ZHANG Abstract. This appendix shows some additional details of the model and equilibrium

APPENDIX TO RESERVE REQUIREMENTS AND OPTIMAL CHINESE STABILIZATION POLICY CHUN CHANG ZHENG LIU MARK M. SPIEGEL JINGYI ZHANG Abstract. This appendix shows some additional details of the model and equilibrium

Economics 232c Spring 2003 International Macroeconomics. Problem Set 3. May 15, 2003

Economics 232c Spring 2003 International Macroeconomics Problem Set 3 May 15, 2003 Due: Thu, June 5, 2003 Instructor: Marc-Andreas Muendler E-mail: muendler@ucsd.edu 1 Trending Fundamentals in a Target

Economics 232c Spring 2003 International Macroeconomics Problem Set 3 May 15, 2003 Due: Thu, June 5, 2003 Instructor: Marc-Andreas Muendler E-mail: muendler@ucsd.edu 1 Trending Fundamentals in a Target

The Lucas Imperfect Information Model

The Lucas Imperfect Information Model Based on the work of Lucas (972) and Phelps (970), the imperfect information model represents an important milestone in modern economics. The essential idea of the

The Lucas Imperfect Information Model Based on the work of Lucas (972) and Phelps (970), the imperfect information model represents an important milestone in modern economics. The essential idea of the

Exchange Rate Nonlinearities in India s Exports to the US

Exchange Rate Nonlinearities in India s Exports to the US Dr. Somesh K. Mathur, Abhishek S. Shekhawat Abstract The investigation and estimation of e ect of movements in exchange rate on the trade have

Exchange Rate Nonlinearities in India s Exports to the US Dr. Somesh K. Mathur, Abhishek S. Shekhawat Abstract The investigation and estimation of e ect of movements in exchange rate on the trade have