Whither News Shocks?

|

|

|

- Clyde Young

- 5 years ago

- Views:

Transcription

1 Discussion of Whither News Shocks? Barsky, Basu and Lee Christiano

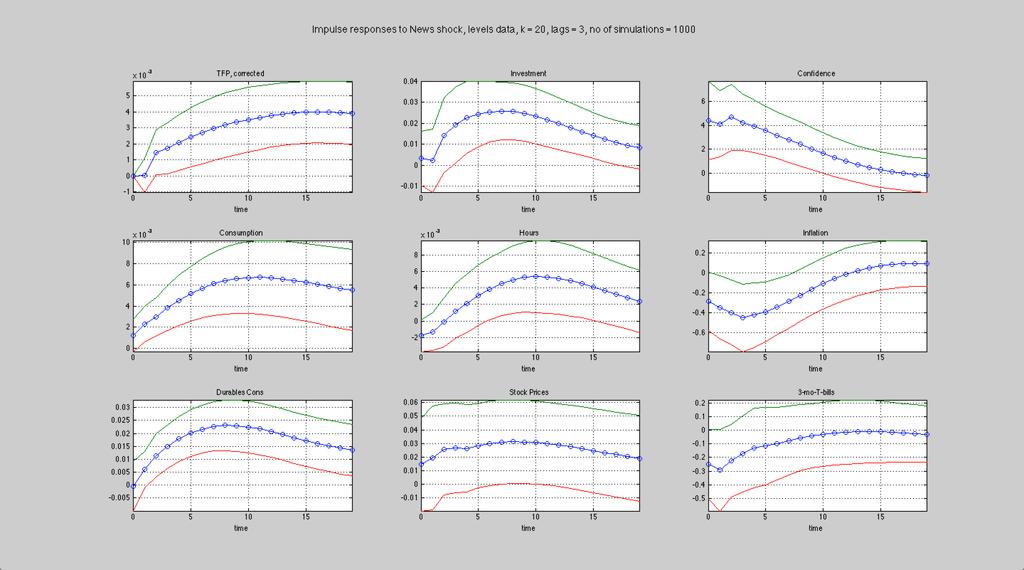

2 Outline Identification assumptions for news shocks Empirical Findings Using NK model used to think about BBL identification. Why should we care about news shocks?

3 BBL Identification for News Shocks Identification problem: Y t A L Y t 1 u t, u t C fundamental shocks t, E t t I N 2 unknowns C C Eu t u t N N 1 2 known things V

4 BBL News Identification Problem must get this vector u t C t CN N,t i N C i i,t Revision in forecast of TFP growth k periods in the future: E t TFP t k E t 1 TFP t k A k u t Here, A ~ companion matrix of VAR

5 Two Identifying Assumptions For large enough k, the revision in expectations is proportional to news shock: E t TFP t k E t 1 TFP t k A k u t a N,t News shock does not have an immediate impact on technology: C N 0 x x

6 Identification cov u t, A k u t cov u t,a N,t cov cov C N N,t,a N,t C N a. C N N,t i N C i i,t,a N,t std A k u t std a N,t a cov u t, A k u t std A k u t C N

7 Results Results reported in the paper are preliminary. Confidence intervals ignore sampling uncertainty in estimator of C N. Confidence intervals overstate precision.

8 All the confidence intervals are length zero, because C N was imposed to have no sampling uncertainty.

9 Not a lot of news: TFP starts moving 2 quarters after news

10 Nice!

11 Hard to say what initial response is, positive or negative.

12 Significant expansion

13 Pretty noisy estimate.perhaps because discount rate rises a lot, in addition to future dividends.

14 Significant!

15 Puzzle: Why Does News Drive Down Inflation? BBL interpret their impulse responses using an RBC model. Allocations and real interest rate, r π e, driven by real part of model. Split of real rate into nominal rate and inflation determined by monetary policy. Real rate, r π e, rises, and monetary policy cuts r a lot. Monetary policy drives r down a lot because the coefficient on output growth in the Taylor rule is very large (0.65). Notion that cut in r drives inflation down seems inconsistent with a lot of evidence. Very likely, a fully fleshed out version of the model implies the Friedman rule is optimal.

16 Would be helpful if model impulse responses were placed in the same diagram. This has been standard practice for a long time (see, e.g., Sims, 1989, Models and Their Uses, American Journal of Agricultural Economics; Rotemberg and Woodford, Macro Annual, 1997) Inflation goes down for only two quarters, versus eight quarters in the VAR.

17 Would be helpful if model impulse responses were placed in the same diagram. This has been standard practice for a long time (see, e.g., Sims, 1989, Models and Their Uses, American Journal of Agricultural Economics; Rotemberg and Woodford, Macro Annual, 1997) Inflation goes down for only two quarters, versus eight quarters in the VAR.

18 Next, Use New Keynesian Model to: get a sense of whether the identification strategy works. think about the inflation puzzle. think about the question, why care about news shocks?

19 Model with three shocks: Simple NK Model t s t E t t 1 x t E t x t 1 r t E t t 1 r t r t 0.8 r t t u t r t E t a t 1 s t 1 1 x t a t 1,t g t 1, g t 0.2 g t 1 news 2,t VAR with two variables: Y t a t log employment t

20 The BBL Identification Strategy Correctly recovers the news shock from the VAR disturbance if there are two shocks (i.e., same number of shocks as variables) To get things exactly right, require infinite lags in VAR Short number of lags works pretty well. When there are three shocks, then news shock not recoverable from VAR disturbance. Suggests that approach goes awry if there are more shocks than variables. I interpret this as good news for the VAR approach in the paper, which uses a lot of variables.

21 Inflation Puzzle Inflation in the model t s t E t s t 1 2 E t s t 2... If news about future technology improvement caused future marginal cost to fall, could drive down current inflation. Requires that technology improvement drive marginal cost down. MC w MP L

22 NK Model and the Inflation Puzzle Period t response to 1 percent news shock, 2,t 0.01 natural rate actual rate log employment inflation a t 1 1,t 1 g t, g t 0.2g t 1 2,t a t 1 1,t 1 g t, g t 0.2g t 1 2,t Smaller wealth effect associated with second time series representation: future technology shock drives marginal cost down.

23 Broader Lesson for Monetary Policy Taylor rule: natural rate (normally left out of Taylor rule) r t Natural rate: rt r t E t a t 1 a t t x x t Traditionally, natural rate left out of Taylor rule. Why? Hard to measure. People used to think that the natural rate was roughly constant anyway: RBC model technology shock always had autocorrelation 0.95 NK DSGE model shocks always have high autocorrelation.

24 Implication of News Shock for Monetary Policy Old argument about why natural rate shouldn t be put in the Taylor rule falls apart. News shocks move the future without having a big impact on the present. Have big impact on natural rate. Finding proxies for the natural rate not necessarily hard. Need indicators that the future looks good. High credit growth, high stock market growth.

25 Conclusion A pleasure reading and thinking about BBL work. BBL impulse responses not as precise as they suggest. Some patterns, which drive them towards RBC model not significant. Their identification strategy seems to make sense in a NK model. We should care about news shocks: They have potentially important implications for monetary policy.

Y t = log (employment t )

") Advanced Macroeconomics, Christiano Econ 416 Homework #7 Due: November 21 1. Consider the linearized equilibrium conditions of the New Keynesian model, on the slide, The Equilibrium Conditions in the handout,

Advanced Macroeconomics, Christiano Econ 416 Homework #7 Due: November 21 1. Consider the linearized equilibrium conditions of the New Keynesian model, on the slide, The Equilibrium Conditions in the handout,

Graduate Macro Theory II: Notes on Quantitative Analysis in DSGE Models

Graduate Macro Theory II: Notes on Quantitative Analysis in DSGE Models Eric Sims University of Notre Dame Spring 2011 This note describes very briefly how to conduct quantitative analysis on a linearized

Graduate Macro Theory II: Notes on Quantitative Analysis in DSGE Models Eric Sims University of Notre Dame Spring 2011 This note describes very briefly how to conduct quantitative analysis on a linearized

Taylor Rules and Technology Shocks

Taylor Rules and Technology Shocks Eric R. Sims University of Notre Dame and NBER January 17, 2012 Abstract In a standard New Keynesian model, a Taylor-type interest rate rule moves the equilibrium real

Taylor Rules and Technology Shocks Eric R. Sims University of Notre Dame and NBER January 17, 2012 Abstract In a standard New Keynesian model, a Taylor-type interest rate rule moves the equilibrium real

Simple New Keynesian Model without Capital

Simple New Keynesian Model without Capital Lawrence J. Christiano January 5, 2018 Objective Review the foundations of the basic New Keynesian model without capital. Clarify the role of money supply/demand.

Simple New Keynesian Model without Capital Lawrence J. Christiano January 5, 2018 Objective Review the foundations of the basic New Keynesian model without capital. Clarify the role of money supply/demand.

LECTURE 3 The Effects of Monetary Changes: Statistical Identification. September 5, 2018

Economics 210c/236a Fall 2018 Christina Romer David Romer LECTURE 3 The Effects of Monetary Changes: Statistical Identification September 5, 2018 I. SOME BACKGROUND ON VARS A Two-Variable VAR Suppose the

Economics 210c/236a Fall 2018 Christina Romer David Romer LECTURE 3 The Effects of Monetary Changes: Statistical Identification September 5, 2018 I. SOME BACKGROUND ON VARS A Two-Variable VAR Suppose the

1 Teaching notes on structural VARs.

Bent E. Sørensen February 22, 2007 1 Teaching notes on structural VARs. 1.1 Vector MA models: 1.1.1 Probability theory The simplest (to analyze, estimation is a different matter) time series models are

Bent E. Sørensen February 22, 2007 1 Teaching notes on structural VARs. 1.1 Vector MA models: 1.1.1 Probability theory The simplest (to analyze, estimation is a different matter) time series models are

Assessing Structural VAR s

... Assessing Structural VAR s by Lawrence J. Christiano, Martin Eichenbaum and Robert Vigfusson Zurich, September 2005 1 Background Structural Vector Autoregressions Address the Following Type of Question:

... Assessing Structural VAR s by Lawrence J. Christiano, Martin Eichenbaum and Robert Vigfusson Zurich, September 2005 1 Background Structural Vector Autoregressions Address the Following Type of Question:

Assessing Structural VAR s

... Assessing Structural VAR s by Lawrence J. Christiano, Martin Eichenbaum and Robert Vigfusson Columbia, October 2005 1 Background Structural Vector Autoregressions Can be Used to Address the Following

... Assessing Structural VAR s by Lawrence J. Christiano, Martin Eichenbaum and Robert Vigfusson Columbia, October 2005 1 Background Structural Vector Autoregressions Can be Used to Address the Following

A. Recursively orthogonalized. VARs

Orthogonalized VARs A. Recursively orthogonalized VAR B. Variance decomposition C. Historical decomposition D. Structural interpretation E. Generalized IRFs 1 A. Recursively orthogonalized Nonorthogonal

Orthogonalized VARs A. Recursively orthogonalized VAR B. Variance decomposition C. Historical decomposition D. Structural interpretation E. Generalized IRFs 1 A. Recursively orthogonalized Nonorthogonal

Lars Svensson 2/16/06. Y t = Y. (1) Assume exogenous constant government consumption (determined by government), G t = G<Y. (2)

Assume exogenous constant government consumption (determined by government), G t = G<Y. (2)") Eco 504, part 1, Spring 2006 504_L3_S06.tex Lars Svensson 2/16/06 Specify equilibrium under perfect foresight in model in L2 Assume M 0 and B 0 given. Determine {C t,g t,y t,m t,b t,t t,r t,i t,p t } that

Eco 504, part 1, Spring 2006 504_L3_S06.tex Lars Svensson 2/16/06 Specify equilibrium under perfect foresight in model in L2 Assume M 0 and B 0 given. Determine {C t,g t,y t,m t,b t,t t,r t,i t,p t } that

VARs and factors. Lecture to Bristol MSc Time Series, Spring 2014 Tony Yates

VARs and factors Lecture to Bristol MSc Time Series, Spring 2014 Tony Yates What we will cover Why factor models are useful in VARs Static and dynamic factor models VAR in the factors Factor augmented

VARs and factors Lecture to Bristol MSc Time Series, Spring 2014 Tony Yates What we will cover Why factor models are useful in VARs Static and dynamic factor models VAR in the factors Factor augmented

Estimating and Identifying Vector Autoregressions Under Diagonality and Block Exogeneity Restrictions

Estimating and Identifying Vector Autoregressions Under Diagonality and Block Exogeneity Restrictions William D. Lastrapes Department of Economics Terry College of Business University of Georgia Athens,

Estimating and Identifying Vector Autoregressions Under Diagonality and Block Exogeneity Restrictions William D. Lastrapes Department of Economics Terry College of Business University of Georgia Athens,

1 Teaching notes on structural VARs.

Bent E. Sørensen November 8, 2016 1 Teaching notes on structural VARs. 1.1 Vector MA models: 1.1.1 Probability theory The simplest to analyze, estimation is a different matter time series models are the

Bent E. Sørensen November 8, 2016 1 Teaching notes on structural VARs. 1.1 Vector MA models: 1.1.1 Probability theory The simplest to analyze, estimation is a different matter time series models are the

MA Advanced Macroeconomics: Solving Models with Rational Expectations

MA Advanced Macroeconomics: Solving Models with Rational Expectations Karl Whelan School of Economics, UCD February 6, 2009 Karl Whelan (UCD) Models with Rational Expectations February 6, 2009 1 / 32 Moving

MA Advanced Macroeconomics: Solving Models with Rational Expectations Karl Whelan School of Economics, UCD February 6, 2009 Karl Whelan (UCD) Models with Rational Expectations February 6, 2009 1 / 32 Moving

Indeterminacy and Sunspots in Macroeconomics

Indeterminacy and Sunspots in Macroeconomics Friday September 8 th : Lecture 10 Gerzensee, September 2017 Roger E. A. Farmer Warwick University and NIESR Topics for Lecture 10 Tying together the pieces

Indeterminacy and Sunspots in Macroeconomics Friday September 8 th : Lecture 10 Gerzensee, September 2017 Roger E. A. Farmer Warwick University and NIESR Topics for Lecture 10 Tying together the pieces

Assessing Structural VAR s

... Assessing Structural VAR s by Lawrence J. Christiano, Martin Eichenbaum and Robert Vigfusson Yale, October 2005 1 Background Structural Vector Autoregressions Can be Used to Address the Following Type

... Assessing Structural VAR s by Lawrence J. Christiano, Martin Eichenbaum and Robert Vigfusson Yale, October 2005 1 Background Structural Vector Autoregressions Can be Used to Address the Following Type

Gaussian Mixture Approximations of Impulse Responses and the Non-Linear Effects of Monetary Shocks

Gaussian Mixture Approximations of Impulse Responses and the Non-Linear Effects of Monetary Shocks Regis Barnichon (CREI, Universitat Pompeu Fabra) Christian Matthes (Richmond Fed) Effects of monetary

Gaussian Mixture Approximations of Impulse Responses and the Non-Linear Effects of Monetary Shocks Regis Barnichon (CREI, Universitat Pompeu Fabra) Christian Matthes (Richmond Fed) Effects of monetary

Assessing Structural VAR s

... Assessing Structural VAR s by Lawrence J. Christiano, Martin Eichenbaum and Robert Vigfusson Minneapolis, August 2005 1 Background In Principle, Impulse Response Functions from SVARs are useful as

... Assessing Structural VAR s by Lawrence J. Christiano, Martin Eichenbaum and Robert Vigfusson Minneapolis, August 2005 1 Background In Principle, Impulse Response Functions from SVARs are useful as

Changing expectations of future fed moves could be a shock!

START HERE 10/14. The alternative shock measures are poorly correlated. (Figure 1) Doesn t this indicate that at least two of them are seriously wrong? A: see p. 24. CEE note the responses are the same.

START HERE 10/14. The alternative shock measures are poorly correlated. (Figure 1) Doesn t this indicate that at least two of them are seriously wrong? A: see p. 24. CEE note the responses are the same.

Simple New Keynesian Model without Capital

Simple New Keynesian Model without Capital Lawrence J. Christiano March, 28 Objective Review the foundations of the basic New Keynesian model without capital. Clarify the role of money supply/demand. Derive

Simple New Keynesian Model without Capital Lawrence J. Christiano March, 28 Objective Review the foundations of the basic New Keynesian model without capital. Clarify the role of money supply/demand. Derive

Are Policy Counterfactuals Based on Structural VARs Reliable?

Are Policy Counterfactuals Based on Structural VARs Reliable? Luca Benati European Central Bank 2nd International Conference in Memory of Carlo Giannini 20 January 2010 The views expressed herein are personal,

Are Policy Counterfactuals Based on Structural VARs Reliable? Luca Benati European Central Bank 2nd International Conference in Memory of Carlo Giannini 20 January 2010 The views expressed herein are personal,

Factor models. March 13, 2017

Factor models March 13, 2017 Factor Models Macro economists have a peculiar data situation: Many data series, but usually short samples How can we utilize all this information without running into degrees

Factor models March 13, 2017 Factor Models Macro economists have a peculiar data situation: Many data series, but usually short samples How can we utilize all this information without running into degrees

Discussion of Riccardo DiCecio \Comovement: It's not a Puzzle" Matteo Iacoviello Boston College

Discussion of Riccardo DiCecio \Comovement: It's not a Puzzle" Matteo Iacoviello Boston College THE QUESTION Question: can we construct a coherent DSGE macro model that explains the comovement puzzle?

Discussion of Riccardo DiCecio \Comovement: It's not a Puzzle" Matteo Iacoviello Boston College THE QUESTION Question: can we construct a coherent DSGE macro model that explains the comovement puzzle?

Monetary Policy Design in the Basic New Keynesian Model. Jordi Galí. October 2015

Monetary Policy Design in the Basic New Keynesian Model by Jordi Galí October 2015 The E cient Allocation where C t R 1 0 C t(i) 1 1 1 di Optimality conditions: max U (C t ; N t ; Z t ) subject to: C t

Monetary Policy Design in the Basic New Keynesian Model by Jordi Galí October 2015 The E cient Allocation where C t R 1 0 C t(i) 1 1 1 di Optimality conditions: max U (C t ; N t ; Z t ) subject to: C t

Can News be a Major Source of Aggregate Fluctuations?

Can News be a Major Source of Aggregate Fluctuations? A Bayesian DSGE Approach Ippei Fujiwara 1 Yasuo Hirose 1 Mototsugu 2 1 Bank of Japan 2 Vanderbilt University August 4, 2009 Contributions of this paper

Can News be a Major Source of Aggregate Fluctuations? A Bayesian DSGE Approach Ippei Fujiwara 1 Yasuo Hirose 1 Mototsugu 2 1 Bank of Japan 2 Vanderbilt University August 4, 2009 Contributions of this paper

Macroeconomics Field Exam. August 2007

Macroeconomics Field Exam August 2007 Answer all questions in the exam. Suggested times correspond to the questions weights in the exam grade. Make your answers as precise as possible, using graphs, equations,

Macroeconomics Field Exam August 2007 Answer all questions in the exam. Suggested times correspond to the questions weights in the exam grade. Make your answers as precise as possible, using graphs, equations,

Macroeconomics II. Dynamic AD-AS model

Macroeconomics II Dynamic AD-AS model Vahagn Jerbashian Ch. 14 from Mankiw (2010) Spring 2018 Where we are heading to We will incorporate dynamics into the standard AD-AS model This will offer another

Macroeconomics II Dynamic AD-AS model Vahagn Jerbashian Ch. 14 from Mankiw (2010) Spring 2018 Where we are heading to We will incorporate dynamics into the standard AD-AS model This will offer another

Dynamic AD-AS model vs. AD-AS model Notes. Dynamic AD-AS model in a few words Notes. Notation to incorporate time-dimension Notes

Macroeconomics II Dynamic AD-AS model Vahagn Jerbashian Ch. 14 from Mankiw (2010) Spring 2018 Where we are heading to We will incorporate dynamics into the standard AD-AS model This will offer another

Macroeconomics II Dynamic AD-AS model Vahagn Jerbashian Ch. 14 from Mankiw (2010) Spring 2018 Where we are heading to We will incorporate dynamics into the standard AD-AS model This will offer another

Identifying the Monetary Policy Shock Christiano et al. (1999)

") Identifying the Monetary Policy Shock Christiano et al. (1999) The question we are asking is: What are the consequences of a monetary policy shock a shock which is purely related to monetary conditions

Identifying the Monetary Policy Shock Christiano et al. (1999) The question we are asking is: What are the consequences of a monetary policy shock a shock which is purely related to monetary conditions

MA Advanced Macroeconomics: 7. The Real Business Cycle Model

MA Advanced Macroeconomics: 7. The Real Business Cycle Model Karl Whelan School of Economics, UCD Spring 2016 Karl Whelan (UCD) Real Business Cycles Spring 2016 1 / 38 Working Through A DSGE Model We have

MA Advanced Macroeconomics: 7. The Real Business Cycle Model Karl Whelan School of Economics, UCD Spring 2016 Karl Whelan (UCD) Real Business Cycles Spring 2016 1 / 38 Working Through A DSGE Model We have

Macroeconomics Theory II

Macroeconomics Theory II Francesco Franco FEUNL February 2016 Francesco Franco Macroeconomics Theory II 1/23 Housekeeping. Class organization. Website with notes and papers as no "Mas-Collel" in macro

Macroeconomics Theory II Francesco Franco FEUNL February 2016 Francesco Franco Macroeconomics Theory II 1/23 Housekeeping. Class organization. Website with notes and papers as no "Mas-Collel" in macro

Forward Guidance without Common Knowledge

Forward Guidance without Common Knowledge George-Marios Angeletos 1 Chen Lian 2 1 MIT and NBER 2 MIT November 17, 2017 Outline 1 Introduction 2 Environment 3 GE Attenuation and Horizon Effects 4 Forward

Forward Guidance without Common Knowledge George-Marios Angeletos 1 Chen Lian 2 1 MIT and NBER 2 MIT November 17, 2017 Outline 1 Introduction 2 Environment 3 GE Attenuation and Horizon Effects 4 Forward

Flexible Inflation Forecast Targeting: Evidence for Canada (and Australia)

") Flexible Inflation Forecast Targeting: Evidence for Canada (and Australia) Glenn Otto School of Economics UNSW g.otto@unsw.edu.a & Graham Voss Department of Economics University of Victoria gvoss@uvic.ca

Flexible Inflation Forecast Targeting: Evidence for Canada (and Australia) Glenn Otto School of Economics UNSW g.otto@unsw.edu.a & Graham Voss Department of Economics University of Victoria gvoss@uvic.ca

News Shocks: Different Effects in Boom and Recession?

News Shocks: Different Effects in Boom and Recession? Maria Bolboaca, Sarah Fischer University of Bern Study Center Gerzensee June 7, 5 / Introduction News are defined in the literature as exogenous changes

News Shocks: Different Effects in Boom and Recession? Maria Bolboaca, Sarah Fischer University of Bern Study Center Gerzensee June 7, 5 / Introduction News are defined in the literature as exogenous changes

Gold Rush Fever in Business Cycles

Gold Rush Fever in Business Cycles Paul Beaudry, Fabrice Collard & Franck Portier University of British Columbia & Université de Toulouse UAB Seminar Barcelona November, 29, 26 The Klondike Gold Rush of

Gold Rush Fever in Business Cycles Paul Beaudry, Fabrice Collard & Franck Portier University of British Columbia & Université de Toulouse UAB Seminar Barcelona November, 29, 26 The Klondike Gold Rush of

Vector Autoregressions as a Guide to Constructing Dynamic General Equilibrium Models

Vector Autoregressions as a Guide to Constructing Dynamic General Equilibrium Models by Lawrence J. Christiano, Martin Eichenbaum and Robert Vigfusson 1 Background We Use VAR Impulse Response Functions

Vector Autoregressions as a Guide to Constructing Dynamic General Equilibrium Models by Lawrence J. Christiano, Martin Eichenbaum and Robert Vigfusson 1 Background We Use VAR Impulse Response Functions

Structural VARs II. February 17, 2016

Structural VARs II February 17, 216 Structural VARs Today: Long-run restrictions Two critiques of SVARs Blanchard and Quah (1989), Rudebusch (1998), Gali (1999) and Chari, Kehoe McGrattan (28). Recap:

Structural VARs II February 17, 216 Structural VARs Today: Long-run restrictions Two critiques of SVARs Blanchard and Quah (1989), Rudebusch (1998), Gali (1999) and Chari, Kehoe McGrattan (28). Recap:

1.2. Structural VARs

1. Shocks Nr. 1 1.2. Structural VARs How to identify A 0? A review: Choleski (Cholesky?) decompositions. Short-run restrictions. Inequality restrictions. Long-run restrictions. Then, examples, applications,

1. Shocks Nr. 1 1.2. Structural VARs How to identify A 0? A review: Choleski (Cholesky?) decompositions. Short-run restrictions. Inequality restrictions. Long-run restrictions. Then, examples, applications,

Simple New Keynesian Model without Capital. Lawrence J. Christiano

Simple New Keynesian Model without Capital Lawrence J. Christiano Outline Formulate the nonlinear equilibrium conditions of the model. Need actual nonlinear conditions to study Ramsey optimal policy, even

Simple New Keynesian Model without Capital Lawrence J. Christiano Outline Formulate the nonlinear equilibrium conditions of the model. Need actual nonlinear conditions to study Ramsey optimal policy, even

Matching DSGE models,vars, and state space models. Fabio Canova EUI and CEPR September 2012

Matching DSGE models,vars, and state space models Fabio Canova EUI and CEPR September 2012 Outline Alternative representations of the solution of a DSGE model. Fundamentalness and finite VAR representation

Matching DSGE models,vars, and state space models Fabio Canova EUI and CEPR September 2012 Outline Alternative representations of the solution of a DSGE model. Fundamentalness and finite VAR representation

Assessing Structural VAR s

... Assessing Structural VAR s by Lawrence J. Christiano, Martin Eichenbaum and Robert Vigfusson University of Maryland, September 2005 1 Background In Principle, Impulse Response Functions from SVARs

... Assessing Structural VAR s by Lawrence J. Christiano, Martin Eichenbaum and Robert Vigfusson University of Maryland, September 2005 1 Background In Principle, Impulse Response Functions from SVARs

Nonperforming Loans and Rules of Monetary Policy

Nonperforming Loans and Rules of Monetary Policy preliminary and incomplete draft: any comment will be welcome Emiliano Brancaccio Università degli Studi del Sannio Andrea Califano andrea.califano@iusspavia.it

Nonperforming Loans and Rules of Monetary Policy preliminary and incomplete draft: any comment will be welcome Emiliano Brancaccio Università degli Studi del Sannio Andrea Califano andrea.califano@iusspavia.it

Advanced Macroeconomics II. Real Business Cycle Models. Jordi Galí. Universitat Pompeu Fabra Spring 2018

Advanced Macroeconomics II Real Business Cycle Models Jordi Galí Universitat Pompeu Fabra Spring 2018 Assumptions Optimization by consumers and rms Perfect competition General equilibrium Absence of a

Advanced Macroeconomics II Real Business Cycle Models Jordi Galí Universitat Pompeu Fabra Spring 2018 Assumptions Optimization by consumers and rms Perfect competition General equilibrium Absence of a

Animal Spirits, Fundamental Factors and Business Cycle Fluctuations

Animal Spirits, Fundamental Factors and Business Cycle Fluctuations Stephane Dées Srečko Zimic Banque de France European Central Bank January 6, 218 Disclaimer Any views expressed represent those of the

Animal Spirits, Fundamental Factors and Business Cycle Fluctuations Stephane Dées Srečko Zimic Banque de France European Central Bank January 6, 218 Disclaimer Any views expressed represent those of the

Simple New Keynesian Model without Capital

Simple New Keynesian Model without Capital Lawrence J. Christiano Gerzensee, August 27 Objective Review the foundations of the basic New Keynesian model without capital. Clarify the role of money supply/demand.

Simple New Keynesian Model without Capital Lawrence J. Christiano Gerzensee, August 27 Objective Review the foundations of the basic New Keynesian model without capital. Clarify the role of money supply/demand.

MA Macroeconomics 3. Introducing the IS-MP-PC Model

MA Macroeconomics 3. Introducing the IS-MP-PC Model Karl Whelan School of Economics, UCD Autumn 2014 Karl Whelan (UCD) Introducing the IS-MP-PC Model Autumn 2014 1 / 38 Beyond IS-LM We have reviewed the

MA Macroeconomics 3. Introducing the IS-MP-PC Model Karl Whelan School of Economics, UCD Autumn 2014 Karl Whelan (UCD) Introducing the IS-MP-PC Model Autumn 2014 1 / 38 Beyond IS-LM We have reviewed the

DSGE-Models. Calibration and Introduction to Dynare. Institute of Econometrics and Economic Statistics

DSGE-Models Calibration and Introduction to Dynare Dr. Andrea Beccarini Willi Mutschler, M.Sc. Institute of Econometrics and Economic Statistics willi.mutschler@uni-muenster.de Summer 2012 Willi Mutschler

DSGE-Models Calibration and Introduction to Dynare Dr. Andrea Beccarini Willi Mutschler, M.Sc. Institute of Econometrics and Economic Statistics willi.mutschler@uni-muenster.de Summer 2012 Willi Mutschler

Inference when identifying assumptions are doubted. A. Theory B. Applications

Inference when identifying assumptions are doubted A. Theory B. Applications 1 A. Theory Structural model of interest: A y t B 1 y t1 B m y tm u t nn n1 u t i.i.d. N0, D D diagonal 2 Bayesian approach:

Inference when identifying assumptions are doubted A. Theory B. Applications 1 A. Theory Structural model of interest: A y t B 1 y t1 B m y tm u t nn n1 u t i.i.d. N0, D D diagonal 2 Bayesian approach:

Dynamic Factor Models and Factor Augmented Vector Autoregressions. Lawrence J. Christiano

Dynamic Factor Models and Factor Augmented Vector Autoregressions Lawrence J Christiano Dynamic Factor Models and Factor Augmented Vector Autoregressions Problem: the time series dimension of data is relatively

Dynamic Factor Models and Factor Augmented Vector Autoregressions Lawrence J Christiano Dynamic Factor Models and Factor Augmented Vector Autoregressions Problem: the time series dimension of data is relatively

Lessons of the long quiet ELB

Lessons of the long quiet ELB Comments on Monetary policy: Conventional and unconventional Nobel Symposium on Money and Banking John H. Cochrane Hoover Institution, Stanford University May 2018 1 / 20

Lessons of the long quiet ELB Comments on Monetary policy: Conventional and unconventional Nobel Symposium on Money and Banking John H. Cochrane Hoover Institution, Stanford University May 2018 1 / 20

Topic 3. RBCs

14.452. Topic 3. RBCs Olivier Blanchard April 8, 2007 Nr. 1 1. Motivation, and organization Looked at Ramsey model, with productivity shocks. Replicated fairly well co-movements in output, consumption,

14.452. Topic 3. RBCs Olivier Blanchard April 8, 2007 Nr. 1 1. Motivation, and organization Looked at Ramsey model, with productivity shocks. Replicated fairly well co-movements in output, consumption,

Resolving the Missing Deflation Puzzle. June 7, 2018

Resolving the Missing Deflation Puzzle Jesper Lindé Sveriges Riksbank Mathias Trabandt Freie Universität Berlin June 7, 218 Motivation Key observations during the Great Recession: Extraordinary contraction

Resolving the Missing Deflation Puzzle Jesper Lindé Sveriges Riksbank Mathias Trabandt Freie Universität Berlin June 7, 218 Motivation Key observations during the Great Recession: Extraordinary contraction

Factor models. May 11, 2012

Factor models May 11, 2012 Factor Models Macro economists have a peculiar data situation: Many data series, but usually short samples How can we utilize all this information without running into degrees

Factor models May 11, 2012 Factor Models Macro economists have a peculiar data situation: Many data series, but usually short samples How can we utilize all this information without running into degrees

Paper s contribution (1)

") Discussion of The Timing of Monetary Policy Shocks by Giovanni Olivei and Silvana Tenreyro Marc Giannoni Columbia University and NBER NBER s Universities Research Conference Cambridge, December 9, 2005

Discussion of The Timing of Monetary Policy Shocks by Giovanni Olivei and Silvana Tenreyro Marc Giannoni Columbia University and NBER NBER s Universities Research Conference Cambridge, December 9, 2005

Formulating, Estimating, and Solving Dynamic Equilibrium Models: an Introduction. Jesús Fernández-Villaverde University of Pennsylvania

Formulating, Estimating, and Solving Dynamic Equilibrium Models: an Introduction Jesús Fernández-Villaverde University of Pennsylvania 1 Models Tradition in macroeconomics of using models: 1. Policy Analysis.

Formulating, Estimating, and Solving Dynamic Equilibrium Models: an Introduction Jesús Fernández-Villaverde University of Pennsylvania 1 Models Tradition in macroeconomics of using models: 1. Policy Analysis.

Inference Based on SVARs Identified with Sign and Zero Restrictions: Theory and Applications

Inference Based on SVARs Identified with Sign and Zero Restrictions: Theory and Applications Jonas Arias 1 Juan F. Rubio-Ramírez 2,3 Daniel F. Waggoner 3 1 Federal Reserve Board 2 Duke University 3 Federal

Inference Based on SVARs Identified with Sign and Zero Restrictions: Theory and Applications Jonas Arias 1 Juan F. Rubio-Ramírez 2,3 Daniel F. Waggoner 3 1 Federal Reserve Board 2 Duke University 3 Federal

Financial Econometrics

Financial Econometrics Long-run Relationships in Finance Gerald P. Dwyer Trinity College, Dublin January 2016 Outline 1 Long-Run Relationships Review of Nonstationarity in Mean Cointegration Vector Error

Financial Econometrics Long-run Relationships in Finance Gerald P. Dwyer Trinity College, Dublin January 2016 Outline 1 Long-Run Relationships Review of Nonstationarity in Mean Cointegration Vector Error

Session 4: Money. Jean Imbs. November 2010

Session 4: Jean November 2010 I So far, focused on real economy. Real quantities consumed, produced, invested. No money, no nominal in uences. I Now, introduce nominal dimension in the economy. First and

Session 4: Jean November 2010 I So far, focused on real economy. Real quantities consumed, produced, invested. No money, no nominal in uences. I Now, introduce nominal dimension in the economy. First and

Bayesian Inference for DSGE Models. Lawrence J. Christiano

Bayesian Inference for DSGE Models Lawrence J. Christiano Outline State space-observer form. convenient for model estimation and many other things. Bayesian inference Bayes rule. Monte Carlo integation.

Bayesian Inference for DSGE Models Lawrence J. Christiano Outline State space-observer form. convenient for model estimation and many other things. Bayesian inference Bayes rule. Monte Carlo integation.

Adaptive Learning and Applications in Monetary Policy. Noah Williams

Adaptive Learning and Applications in Monetary Policy Noah University of Wisconsin - Madison Econ 899 Motivations J. C. Trichet: Understanding expectations formation as a process underscores the strategic

Adaptive Learning and Applications in Monetary Policy Noah University of Wisconsin - Madison Econ 899 Motivations J. C. Trichet: Understanding expectations formation as a process underscores the strategic

Introduction to Macroeconomics

Introduction to Macroeconomics Martin Ellison Nuffi eld College Michaelmas Term 2018 Martin Ellison (Nuffi eld) Introduction Michaelmas Term 2018 1 / 39 Macroeconomics is Dynamic Decisions are taken over

Introduction to Macroeconomics Martin Ellison Nuffi eld College Michaelmas Term 2018 Martin Ellison (Nuffi eld) Introduction Michaelmas Term 2018 1 / 39 Macroeconomics is Dynamic Decisions are taken over

Inference in VARs with Conditional Heteroskedasticity of Unknown Form

Inference in VARs with Conditional Heteroskedasticity of Unknown Form Ralf Brüggemann a Carsten Jentsch b Carsten Trenkler c University of Konstanz University of Mannheim University of Mannheim IAB Nuremberg

Inference in VARs with Conditional Heteroskedasticity of Unknown Form Ralf Brüggemann a Carsten Jentsch b Carsten Trenkler c University of Konstanz University of Mannheim University of Mannheim IAB Nuremberg

The Making Of A Great Contraction. With A Liquidity Trap And A Jobless Recovery. Columbia University

The Making Of A Great Contraction With A Liquidity Trap And A Jobless Recovery Stephanie Schmitt-Grohé Martín Uribe Columbia University November 5, 2013 A jobless recovery is a situation in which: Output

The Making Of A Great Contraction With A Liquidity Trap And A Jobless Recovery Stephanie Schmitt-Grohé Martín Uribe Columbia University November 5, 2013 A jobless recovery is a situation in which: Output

Signaling Effects of Monetary Policy

Signaling Effects of Monetary Policy Leonardo Melosi London Business School 24 May 2012 Motivation Disperse information about aggregate fundamentals Morris and Shin (2003), Sims (2003), and Woodford (2002)

Signaling Effects of Monetary Policy Leonardo Melosi London Business School 24 May 2012 Motivation Disperse information about aggregate fundamentals Morris and Shin (2003), Sims (2003), and Woodford (2002)

Macroeconomic Analysis: VAR, DSGE and Factor Models

Macroeconomic Analysis: VAR, DSGE and Factor Models Marco Lippi, Einaudi Institute for Economics and Finance Scuola di Dottorato in Economia 24 Febbraio 2016 Outline Motivation The simplest model Singularity

Macroeconomic Analysis: VAR, DSGE and Factor Models Marco Lippi, Einaudi Institute for Economics and Finance Scuola di Dottorato in Economia 24 Febbraio 2016 Outline Motivation The simplest model Singularity

Looking for the stars

Looking for the stars Mengheng Li 12 Irma Hindrayanto 1 1 Economic Research and Policy Division, De Nederlandsche Bank 2 Department of Econometrics, Vrije Universiteit Amsterdam April 5, 2018 1 / 35 Outline

Looking for the stars Mengheng Li 12 Irma Hindrayanto 1 1 Economic Research and Policy Division, De Nederlandsche Bank 2 Department of Econometrics, Vrije Universiteit Amsterdam April 5, 2018 1 / 35 Outline

THE CASE OF THE DISAPPEARING PHILLIPS CURVE

THE CASE OF THE DISAPPEARING PHILLIPS CURVE James Bullard President and CEO 2018 BOJ-IMES Conference Central Banking in a Changing World May 31, 2018 Tokyo, Japan Any opinions expressed here are my own

THE CASE OF THE DISAPPEARING PHILLIPS CURVE James Bullard President and CEO 2018 BOJ-IMES Conference Central Banking in a Changing World May 31, 2018 Tokyo, Japan Any opinions expressed here are my own

Inference when identifying assumptions are doubted. A. Theory. Structural model of interest: B 1 y t1. u t. B m y tm. u t i.i.d.

Inference when identifying assumptions are doubted A. Theory B. Applications Structural model of interest: A y t B y t B m y tm nn n i.i.d. N, D D diagonal A. Theory Bayesian approach: Summarize whatever

Inference when identifying assumptions are doubted A. Theory B. Applications Structural model of interest: A y t B y t B m y tm nn n i.i.d. N, D D diagonal A. Theory Bayesian approach: Summarize whatever

The Labor Market in the New Keynesian Model: Incorporating a Simple DMP Version of the Labor Market and Rediscovering the Shimer Puzzle

The Labor Market in the New Keynesian Model: Incorporating a Simple DMP Version of the Labor Market and Rediscovering the Shimer Puzzle Lawrence J. Christiano April 1, 2013 Outline We present baseline

The Labor Market in the New Keynesian Model: Incorporating a Simple DMP Version of the Labor Market and Rediscovering the Shimer Puzzle Lawrence J. Christiano April 1, 2013 Outline We present baseline

Equilibrium Conditions (symmetric across all differentiated goods)

") MONOPOLISTIC COMPETITION IN A DSGE MODEL: PART II SEPTEMBER 30, 200 Canonical Dixit-Stiglitz Model MONOPOLISTICALLY-COMPETITIVE EQUILIBRIUM Equilibrium Conditions (symmetric across all differentiated goods)

MONOPOLISTIC COMPETITION IN A DSGE MODEL: PART II SEPTEMBER 30, 200 Canonical Dixit-Stiglitz Model MONOPOLISTICALLY-COMPETITIVE EQUILIBRIUM Equilibrium Conditions (symmetric across all differentiated goods)

4- Current Method of Explaining Business Cycles: DSGE Models. Basic Economic Models

4- Current Method of Explaining Business Cycles: DSGE Models Basic Economic Models In Economics, we use theoretical models to explain the economic processes in the real world. These models de ne a relation

4- Current Method of Explaining Business Cycles: DSGE Models Basic Economic Models In Economics, we use theoretical models to explain the economic processes in the real world. These models de ne a relation

Foundations for the New Keynesian Model. Lawrence J. Christiano

Foundations for the New Keynesian Model Lawrence J. Christiano Objective Describe a very simple model economy with no monetary frictions. Describe its properties. markets work well Modify the model to

Foundations for the New Keynesian Model Lawrence J. Christiano Objective Describe a very simple model economy with no monetary frictions. Describe its properties. markets work well Modify the model to

Technology Shocks and Aggregate Fluctuations: How Well Does the RBC Model Fit Postwar U.S. Data?

Technology Shocks and Aggregate Fluctuations: How Well Does the RBC Model Fit Postwar U.S. Data? by Jordi Gali and Pau Rabanal Comments by Ellen R. McGrattan, Minneapolis Fed Overview of Gali-Rabanal Part

Technology Shocks and Aggregate Fluctuations: How Well Does the RBC Model Fit Postwar U.S. Data? by Jordi Gali and Pau Rabanal Comments by Ellen R. McGrattan, Minneapolis Fed Overview of Gali-Rabanal Part

THE CASE OF THE DISAPPEARING PHILLIPS CURVE

THE CASE OF THE DISAPPEARING PHILLIPS CURVE James Bullard President and CEO 2018 ECB Forum on Central Banking Macroeconomics of Price- and Wage-Setting June 19, 2018 Sintra, Portugal Any opinions expressed

THE CASE OF THE DISAPPEARING PHILLIPS CURVE James Bullard President and CEO 2018 ECB Forum on Central Banking Macroeconomics of Price- and Wage-Setting June 19, 2018 Sintra, Portugal Any opinions expressed

Solving a Dynamic (Stochastic) General Equilibrium Model under the Discrete Time Framework

General Equilibrium Model under the Discrete Time Framework") Solving a Dynamic (Stochastic) General Equilibrium Model under the Discrete Time Framework Dongpeng Liu Nanjing University Sept 2016 D. Liu (NJU) Solving D(S)GE 09/16 1 / 63 Introduction Targets of the

Solving a Dynamic (Stochastic) General Equilibrium Model under the Discrete Time Framework Dongpeng Liu Nanjing University Sept 2016 D. Liu (NJU) Solving D(S)GE 09/16 1 / 63 Introduction Targets of the

Discussion of "Noisy News in Business Cycle" by Forni, Gambetti, Lippi, and Sala

Judgement Discussion of Cycle" by Università degli Studi Milano - Bicocca IV International Conference in memory of Carlo Giannini Judgement Great contribution in the literature of NEWS and NOISE shocks:

Judgement Discussion of Cycle" by Università degli Studi Milano - Bicocca IV International Conference in memory of Carlo Giannini Judgement Great contribution in the literature of NEWS and NOISE shocks:

Lecture 8: Aggregate demand and supply dynamics, closed economy case.

Lecture 8: Aggregate demand and supply dynamics, closed economy case. Ragnar Nymoen Department of Economics, University of Oslo October 20, 2008 1 Ch 17, 19 and 20 in IAM Since our primary concern is to

Lecture 8: Aggregate demand and supply dynamics, closed economy case. Ragnar Nymoen Department of Economics, University of Oslo October 20, 2008 1 Ch 17, 19 and 20 in IAM Since our primary concern is to

MA Advanced Macroeconomics: 6. Solving Models with Rational Expectations

MA Advanced Macroeconomics: 6. Solving Models with Rational Expectations Karl Whelan School of Economics, UCD Spring 2016 Karl Whelan (UCD) Models with Rational Expectations Spring 2016 1 / 36 Moving Beyond

MA Advanced Macroeconomics: 6. Solving Models with Rational Expectations Karl Whelan School of Economics, UCD Spring 2016 Karl Whelan (UCD) Models with Rational Expectations Spring 2016 1 / 36 Moving Beyond

Do Long Run Restrictions Identify Supply and Demand Disturbances?

Do Long Run Restrictions Identify Supply and Demand Disturbances? U. Michael Bergman Department of Economics, University of Copenhagen, Studiestræde 6, DK 1455 Copenhagen K, Denmark October 25, 2005 Abstract

Do Long Run Restrictions Identify Supply and Demand Disturbances? U. Michael Bergman Department of Economics, University of Copenhagen, Studiestræde 6, DK 1455 Copenhagen K, Denmark October 25, 2005 Abstract

Perceived productivity and the natural rate of interest

Perceived productivity and the natural rate of interest Gianni Amisano and Oreste Tristani European Central Bank IRF 28 Frankfurt, 26 June Amisano-Tristani (European Central Bank) Productivity and the

Perceived productivity and the natural rate of interest Gianni Amisano and Oreste Tristani European Central Bank IRF 28 Frankfurt, 26 June Amisano-Tristani (European Central Bank) Productivity and the

The Zero Lower Bound

The Zero Lower Bound Eric Sims University of Notre Dame Spring 7 Introduction In the standard New Keynesian model, monetary policy is often described by an interest rate rule (e.g. a Taylor rule) that

The Zero Lower Bound Eric Sims University of Notre Dame Spring 7 Introduction In the standard New Keynesian model, monetary policy is often described by an interest rate rule (e.g. a Taylor rule) that

MSc Time Series Econometrics

MSc Time Series Econometrics Module 2: multivariate time series topics Lecture 1: VARs, introduction, motivation, estimation, preliminaries Tony Yates Spring 2014, Bristol Topics we will cover Vector autoregressions:

MSc Time Series Econometrics Module 2: multivariate time series topics Lecture 1: VARs, introduction, motivation, estimation, preliminaries Tony Yates Spring 2014, Bristol Topics we will cover Vector autoregressions:

Class 4: VAR. Macroeconometrics - Fall October 11, Jacek Suda, Banque de France

VAR IRF Short-run Restrictions Long-run Restrictions Granger Summary Jacek Suda, Banque de France October 11, 2013 VAR IRF Short-run Restrictions Long-run Restrictions Granger Summary Outline Outline:

VAR IRF Short-run Restrictions Long-run Restrictions Granger Summary Jacek Suda, Banque de France October 11, 2013 VAR IRF Short-run Restrictions Long-run Restrictions Granger Summary Outline Outline:

Source: US. Bureau of Economic Analysis Shaded areas indicate US recessions research.stlouisfed.org

Business Cycles 0 Real Gross Domestic Product 18,000 16,000 (Billions of Chained 2009 Dollars) 14,000 12,000 10,000 8,000 6,000 4,000 2,000 1940 1960 1980 2000 Source: US. Bureau of Economic Analysis Shaded

Business Cycles 0 Real Gross Domestic Product 18,000 16,000 (Billions of Chained 2009 Dollars) 14,000 12,000 10,000 8,000 6,000 4,000 2,000 1940 1960 1980 2000 Source: US. Bureau of Economic Analysis Shaded

Financial Factors in Economic Fluctuations. Lawrence Christiano Roberto Motto Massimo Rostagno

Financial Factors in Economic Fluctuations Lawrence Christiano Roberto Motto Massimo Rostagno Background Much progress made on constructing and estimating models that fit quarterly data well (Smets-Wouters,

Financial Factors in Economic Fluctuations Lawrence Christiano Roberto Motto Massimo Rostagno Background Much progress made on constructing and estimating models that fit quarterly data well (Smets-Wouters,

Supplementary Notes on Chapter 6 of D. Romer s Advanced Macroeconomics Textbook (4th Edition)

") Supplementary Notes on Chapter 6 of D. Romer s Advanced Macroeconomics Textbook (4th Edition) Changsheng Xu & Ming Yi School of Economics, Huazhong University of Science and Technology This version: June

Supplementary Notes on Chapter 6 of D. Romer s Advanced Macroeconomics Textbook (4th Edition) Changsheng Xu & Ming Yi School of Economics, Huazhong University of Science and Technology This version: June

Bayesian Estimation of DSGE Models: Lessons from Second-order Approximations

Bayesian Estimation of DSGE Models: Lessons from Second-order Approximations Sungbae An Singapore Management University Bank Indonesia/BIS Workshop: STRUCTURAL DYNAMIC MACROECONOMIC MODELS IN ASIA-PACIFIC

Bayesian Estimation of DSGE Models: Lessons from Second-order Approximations Sungbae An Singapore Management University Bank Indonesia/BIS Workshop: STRUCTURAL DYNAMIC MACROECONOMIC MODELS IN ASIA-PACIFIC

Lecture on State Dependent Government Spending Multipliers

Lecture on State Dependent Government Spending Multipliers Valerie A. Ramey University of California, San Diego and NBER February 25, 2014 Does the Multiplier Depend on the State of Economy? Evidence suggests

Lecture on State Dependent Government Spending Multipliers Valerie A. Ramey University of California, San Diego and NBER February 25, 2014 Does the Multiplier Depend on the State of Economy? Evidence suggests

Warwick Business School Forecasting System. Summary. Ana Galvao, Anthony Garratt and James Mitchell November, 2014

Warwick Business School Forecasting System Summary Ana Galvao, Anthony Garratt and James Mitchell November, 21 The main objective of the Warwick Business School Forecasting System is to provide competitive

Warwick Business School Forecasting System Summary Ana Galvao, Anthony Garratt and James Mitchell November, 21 The main objective of the Warwick Business School Forecasting System is to provide competitive

Gold Rush Fever in Business Cycles

Gold Rush Fever in Business Cycles Paul Beaudry, Fabrice Collard & Franck Portier University of British Columbia & Université de Toulouse Banque Nationale Nationale Bank Belgischen de Belgique van Belgïe

Gold Rush Fever in Business Cycles Paul Beaudry, Fabrice Collard & Franck Portier University of British Columbia & Université de Toulouse Banque Nationale Nationale Bank Belgischen de Belgique van Belgïe

Econometrics in a nutshell: Variation and Identification Linear Regression Model in STATA. Research Methods. Carlos Noton.

1/17 Research Methods Carlos Noton Term 2-2012 Outline 2/17 1 Econometrics in a nutshell: Variation and Identification 2 Main Assumptions 3/17 Dependent variable or outcome Y is the result of two forces:

1/17 Research Methods Carlos Noton Term 2-2012 Outline 2/17 1 Econometrics in a nutshell: Variation and Identification 2 Main Assumptions 3/17 Dependent variable or outcome Y is the result of two forces:

Monetary Policy Regimes and Economic Performance: The Historical Record,

Monetary Policy Regimes and Economic Performance: The Historical Record, 1979-2008 Luca Benati Charles Goodhart European Central Bank London School of Economics Conference on: Key developments in monetary

Monetary Policy Regimes and Economic Performance: The Historical Record, 1979-2008 Luca Benati Charles Goodhart European Central Bank London School of Economics Conference on: Key developments in monetary

General Examination in Macroeconomic Theory SPRING 2013

HARVARD UNIVERSITY DEPARTMENT OF ECONOMICS General Examination in Macroeconomic Theory SPRING 203 You have FOUR hours. Answer all questions Part A (Prof. Laibson): 48 minutes Part B (Prof. Aghion): 48

HARVARD UNIVERSITY DEPARTMENT OF ECONOMICS General Examination in Macroeconomic Theory SPRING 203 You have FOUR hours. Answer all questions Part A (Prof. Laibson): 48 minutes Part B (Prof. Aghion): 48

Neoclassical Business Cycle Model

Neoclassical Business Cycle Model Prof. Eric Sims University of Notre Dame Fall 2015 1 / 36 Production Economy Last time: studied equilibrium in an endowment economy Now: study equilibrium in an economy

Neoclassical Business Cycle Model Prof. Eric Sims University of Notre Dame Fall 2015 1 / 36 Production Economy Last time: studied equilibrium in an endowment economy Now: study equilibrium in an economy

Are Structural VARs Useful Guides for Developing Business Cycle Theories? by Larry Christiano

Discussion of: Chari-Kehoe-McGrattan: Are Structural VARs Useful Guides for Developing Business Cycle Theories? by Larry Christiano 1 Chari-Kehoe-McGrattan: Are Structural VARs Useful Guides for Developing

Discussion of: Chari-Kehoe-McGrattan: Are Structural VARs Useful Guides for Developing Business Cycle Theories? by Larry Christiano 1 Chari-Kehoe-McGrattan: Are Structural VARs Useful Guides for Developing

The Price Puzzle: Mixing the Temporary and Permanent Monetary Policy Shocks.

The Price Puzzle: Mixing the Temporary and Permanent Monetary Policy Shocks. Ida Wolden Bache Norges Bank Kai Leitemo Norwegian School of Management BI September 2, 2008 Abstract We argue that the correct

The Price Puzzle: Mixing the Temporary and Permanent Monetary Policy Shocks. Ida Wolden Bache Norges Bank Kai Leitemo Norwegian School of Management BI September 2, 2008 Abstract We argue that the correct

S TICKY I NFORMATION Fabio Verona Bank of Finland, Monetary Policy and Research Department, Research Unit

B USINESS C YCLE DYNAMICS UNDER S TICKY I NFORMATION Fabio Verona Bank of Finland, Monetary Policy and Research Department, Research Unit fabio.verona@bof.fi O BJECTIVE : analyze how and to what extent

B USINESS C YCLE DYNAMICS UNDER S TICKY I NFORMATION Fabio Verona Bank of Finland, Monetary Policy and Research Department, Research Unit fabio.verona@bof.fi O BJECTIVE : analyze how and to what extent

Monetary Policy and Unemployment: A New Keynesian Perspective

Monetary Policy and Unemployment: A New Keynesian Perspective Jordi Galí CREI, UPF and Barcelona GSE April 215 Jordi Galí (CREI, UPF and Barcelona GSE) Monetary Policy and Unemployment April 215 1 / 16

Monetary Policy and Unemployment: A New Keynesian Perspective Jordi Galí CREI, UPF and Barcelona GSE April 215 Jordi Galí (CREI, UPF and Barcelona GSE) Monetary Policy and Unemployment April 215 1 / 16

What You Match Does Matter: The Effects of Data on DSGE Estimation

Discussion of What You Match Does Matter: The Effects of Data on DSGE Estimation by Pablo Guerron-Quintana Marc Giannoni Columbia University, NBER and CEPR Workshop on Methods and Applications for DSGE

Discussion of What You Match Does Matter: The Effects of Data on DSGE Estimation by Pablo Guerron-Quintana Marc Giannoni Columbia University, NBER and CEPR Workshop on Methods and Applications for DSGE

Structural VAR Models and Applications

Structural VAR Models and Applications Laurent Ferrara 1 1 University of Paris Nanterre M2 Oct. 2018 SVAR: Objectives Whereas the VAR model is able to capture efficiently the interactions between the different

Structural VAR Models and Applications Laurent Ferrara 1 1 University of Paris Nanterre M2 Oct. 2018 SVAR: Objectives Whereas the VAR model is able to capture efficiently the interactions between the different