Projective Expected Utility

|

|

|

- Doreen Rogers

- 6 years ago

- Views:

Transcription

1 Projective Expected Utility Pierfrancesco La Mura Department of Microeconomics and Information Systems Leipzig Graduate School of Management (HHL) April 24, Introduction John von Neumann ( ) is widely regarded as a founding father of many fields, including game theory, decision theory, quantum mechanics and computer science. Two of his contributions are of special importance in our context. In 1932, von Neumann proposed the first rigorous foundation for quantum mechanics, based on a calculus of projections in Hilbert spaces. In 1944, together with Oskar Morgenstern, he gave the first axiomatic foundation for the expected utility hypothesis (Bernoulli 1738). In both cases, the frameworks he pioneered are still at the core of the respective fields. In particular, the expected utility hypothesis is still the de facto foundation of fields such as finance and game theory. The von Neumann - Morgenstern axiomatization of expected utility was immediately greeted as simple and intuitively compelling. Yet, in the course of time, a number of empirical violations and paradoxes (Allais 1953, Ellsberg 1961, Rabin and Thaler 2001) came to cast doubt on the validity of the hypothesis as a foundation for the theory of rational decisions in conditions of risk and subjective uncertainty. In economics and in the social sciences, the shortcomings of the expected utility hypothesis are generally well known, but often tacitly accepted in view of the great tractability and usefulness of the corresponding mathematical framework. In fact, the hypothesis postulates that preferences can be represented by way of a utility functional which is linear in probabilities, and linearity makes expected utility representations particularly tractable in models and applications. The experimental paradoxes, which in the context of physics motivated the introduction of quantum mechanics, bear interesting relations with some of the decision-theoretic paradoxes which came to challenge the status of expected utility in the social sciences. In physics, quantum mechanics was introduced as a tractable and empirically accurate mathematical framework in the presence of such violations. In economics and the social sciences, the importance of accounting for violations of the expected utility hypothesis has long been recognized, but so far none of its numerous alternatives has emerged as dominant, 1

2 sometimes due to a lack of mathematical tractability, or to the ad-hoc nature of some axiomatic proposals. Motivated by these considerations, we would like to introduce a decision-theoretic framework which accommodates the dominant paradoxes while retaining significant simplicity and tractability. As we shall see, this is obtained by weakening the expected utility hypothesis to its projective counterpart, in analogy with the quantum-mechanical generalization of classical probability theory. The structure of the paper is as follows. The next section briefly reviews the von Neumann-Morgenstern framework. Sections 3 and 4, respectively, present Allais and Ellsberg s paradoxes. Section 5 introduces a mathematical framework for projective expected utility, and our main result. Section 6 contains a brief discussion. Sections 7 and 8 show how Allais and Ellsberg s paradoxes, respectively, can be accommodated within the new framework. Section 9 discusses applications and extensions, then concludes. 2 von Neumann - Morgenstern expected utility Let S be a finite set of outcomes, and be the set of probability functions defined on S, taken to represent risky prospects (lotteries). Next, let be a complete and transitive binary relation defined on, representing a decisionmaker s preference ordering over lotteries. As usual, indifference of p, q is defined as [p q and q p] and denoted as p q, while strict preference of p over q is defined as [p q and not q p], and denoted by p q. The preference ordering is assumed to satisfy the following two conditions. Axiom 1 For all p, q, r with p q r, there exist α, β (0, 1) such that αp + (1 α)r q βp + (1 β)r. Axiom 2 For all p, q, r, p q if, and only if, αp+(1 α)r αq +(1 α)r for all α [0, 1]. A functional u : R is said to represent if, for all p, q, p q if and only if u(p) u(q). Theorem 3 Axioms 1 and 2 are jointly equivalent to the existence of a functional u : R which represents such that, for all p, u(p) = s S u(s)p(s). 2

3 3 The double-slit paradox of decision theory The following paradox is due to Allais (1953). First, please choose between: A: A chance of winning 4000 dollars with probability 0.2 (expected value 800 dollars) B: A chance of winning 3000 dollars with probability 0.25 (expected value 750 dollars). Next, please choose between: C: A chance of winning 4000 dollars with probability 0.8 (expected value 3200 dollars) B: A chance of winning 3000 dollars with certainty. If you chose A over B, and D over C, then you are in the modal class of respondents. The paradox lies in the observation that A and C are special cases of a two-stage lottery E which in the first stage either returns zero dollars with probably (1 α) or, with probability α, it leads to a second stage where one gets 4000 dollars with probability 0.8 and zero otherwise. In particular, if α is set to 1 then E reduces to C, and if α is set to 0.25 it reduces to A. Similarly, B and D are special cases of a two-stage lottery F which again with probability (1 α) returns zero, and with probability α continues to a second stage where one wins 3000 dollars with probability 1. Again, if α = 1 then F reduces to D, and if α = 0.25 it reduces to B. Then it is easy to see that the [A B, D C] pattern violates the Independence axiom, as E can be regarded as a lottery αp + (1 α)r, and F as a lottery αq + (1 α)r, where p and q represent lottery C and D respectively and r represents the lottery in which one gets zero dollars with certainty. Why should it matter what is the value of α? Yet, experimentally one finds that it does. Allais paradox bears a certain resemblance with the well-known double-slit paradox in physics. Imagine cutting two parallel slits in a sheet of cardboard, shining light through them, and observing the resulting pattern as particles going through the two slits scatter on a wall behind the cardboard barrier. Experimentally, one finds that when both slits are open, the overall scattering pattern is not the sum of the two scattering patterns produced when one slit is open and the other closed. The effect does not go away even if particles of light are shone one by one, and this is paradoxical: why should it matter to an individual particle which happens to go through the left slit, when determining where to scatter later on, with what probability it could have gone through the right slit instead? In a sense, each particle in the double-slit experiment behaves like a decision-maker who violates the Independence axiom in Allais experiment. 3

4 4 Ellsberg s paradox Another disturbing violation of the expected utility hypothesis was pointed out by Ellsberg (1961). Suppose that a box contains 300 balls of three possible colors: red (R), green (G), and blue (B). You know that the box contains exactly 100 red balls, but are given no information on the proportion of green and blue. You win if you guess which color will be drawn. Do you prefer to bet on red (R) or on green (G)? Many respondents choose R, on grounds that the probability of drawing a red ball is known (1/3), while the only information on the probability of drawing a green ball is that it is between 0 and 2/3. Now suppose that you win if you guess which color will not be drawn. Do you prefer to bet that red will not be drawn (R) or that green will not be drawn (G)? Again many respondents prefer to bet on R, as the probability is known (2/3) while the probability of G is only known to be between 1 and 1/3. The pattern [R G, R G] is incompatible with von Neumann - Morgenstern expected utility, which only deals with known probabilities, and is also incompatible with the Savage (1954) formulation of expected utility with subjective probability as it violates its Sure Thing axiom. Hence, the paradox suggests that subjective uncertainty and risk should be handled as distinct notions. 5 Projective expected utility Let S + be the positive orthant of the unit sphere in R n, where n is the cardinality of the set of relevant outcomes S := {s 1, s 2,..., s n }. Then von Neumann - Morgenstern lotteries, regarded as elements of the unit simplex, are in oneto-one correspondence with elements of S +, which can therefore be interpreted as risky prospects, where the relevant probabilities are fully known. Observe that, while the projections of elements of the unit simplex (and hence, L 1 unit vectors) on the basis vectors can be naturally associated with probabilities, if we choose to model von Neumann - Morgenstern lotteries as elements of the unit sphere (and hence, as unit vectors in L 2 ) probabilities are naturally associated with squared projections. The advantage of such move is that L 2 is the only L p space which is also a Hilbert space, and Hilbert spaces have a very tractable projective structure that our representation shall exploit. We call such prospects, whereas the relevant probabilities are fully known, pure lotteries, and reserve the name mixed lotteries for convex combinations (mixtures) in R n, which we interpret as situations of subjective uncertainty about the actual pure lottery faced. Let M be the convex closure of S + in R n. Observe that pure lotteries cannot be obtained as non-trivial mixtures, and that is why we refer to them as pure. Next, let.. denote the usual inner product in R n, and let p si (x) be the probability of state s i in lottery x, as perceived by the decision-maker. Axiom 4 (Born s Rule) There exists an orthonormal basis (z 1,..., z n ) such that, 4

5 for all x S + and all s i S, p si (x) = x z i 2. Axiom 4 requires that there exist an interpretation of elements of S + in terms of the relevant dimensions of risk as perceived by the decision-maker. In the von Neumann - Morgenstern treatment, Axiom 4 is tacitly assumed to hold with respect to the natural basis in R n. By contrast, the preferred basis postulated in Axiom 4 is allowed to vary across different decision-makers, capturing the idea that the relevant dimensions of risk may be perceived differently by different subjects, perhaps due to portfolio effects, while the natural basis may be taken to represent the relevant dimensions of risk as perceived by the modeler or an external observer. In our context, orthogonality captures the idea that two events or outcomes are mutually exclusive (for one event to have probability one, the other must have probability zero). The preferred basis captures which, among all the possible ways to partition the relevant uncertainty into a set of mutually exclusive events or outcomes, leads to a set of payoff-relevant orthogonal lotteries from which preferences on all other lotteries can be assigned in a linear fashion. In particular, the basis elements must span the whole range of preferences. For instance, in case a decision-maker is indifferent between two outcomes, but strictly prefers to receive both of them with the same frequency, preferences on the two outcomes do not span all the relevant range; therefore, this preference pattern cannot be captured in the natural basis, and hence in von Neumann - Morgenstern expected utility. Axiom 4 postulates that each lottery is evaluated by the decision maker solely by the uncertainty it induces on appropriately chosen payoff-relevant dimensions. Once an orthonormal basis is given, each mixed lottery x uniquely corresponds to a function p(x) : S [0, 1], such that p si (x) = x z i 2.for all s i S. If x is a pure lottery, then s S p s(x) = 1 and p(x) can therefore be regarded as a probability function. For a general mixed lottery x M, 1/ x 2 can be regarded as a measure of subjective uncertainty, and q si (x) := 1 x 2 x z i 2 as subjective probability. We interpret p(x) as the degree of belief assigned to each outcome by lottery x. Let B be the set of all p(x), for x M, and let be a complete and transitive preference ordering defined on B B. We postulate the following two axioms, which mirror those in the von Neumann - Morgenstern treatment. Axiom 5 (Archimedean) For all x, y, z M with p(x) p(y) p(z), there exist α, β (0, 1) such that αp(x) + (1 α)p(z) p(y) βp(x) + (1 β)p(z). Axiom 6 (Independence) For all x, y, z M, p(x) p(y) if, and only if, αp(x) + (1 α)p(z) ap(y) + (1 α)p(z) for all α [0, 1]. 5

6 Observe that the two axioms impose conditions solely on beliefs, and not on the underlying lotteries. In particular, note that a convex combination αp(x) + (1 α)p(y), where x and y are pure lotteries, also corresponds to a pure lottery, since the convex combination of two probability functions remains a probability function. Hence, the type of mixing in Axioms 5 and 6 can be regarded as objective, while subjective mixing is captured by convex combinations of the underlying lotteries, such as αx + (1 α)y, which is generally not a pure lottery even when both x and y are. Theorem 7 Axioms 4-6 are jointly equivalent to the existence of a symmetric matrix U such that u(x) := x Ux for all x M represents. Proof. Assume that Axiom 4 holds with respect to a given orthonormal basis (z 1,, z n ). By the von Neumann - Morgenstern result (which applies to any convex mixture set, such as B) Axioms 5 and 6 are jointly equivalent to the existence of a functional u which represents the ordering and is linear in p, i.e. u(x) = n u(s i )p si (x) = i=1 n u(s i ) x z i 2, where the second equality is by definition of p as squared inner product with respect to the preferred basis. The above can be equivalently written, in matrix form, as u(x) = x P DP x = x Ux, where D is the diagonal matrix with the payoffs on the main diagonal, P is the projection matrix associated to (z 1,, z n ), and U := P DP is symmetric. Conversely, by the Spectral Decomposition theorem, for any symmetric matrix U there exist a diagonal matrix D and a projection matrix P such that i=1 x Ux = x P DP x for all x M. But this is just expected utility with respect to the orthonormal basis defined by P. Hence, the three axioms are jointly equivalent to the existence of a symmetric matrix U such that u(x) := x Ux represents the preference ordering. 6 Properties of the representation The representation introduced in the previous section generalizes von Neumann- Morgenstern expected utility in three directions. First, subjective uncertainty (from mixed states) and risk (from pure states) are treated as distinct notions. Second, within this class of preferences both Allais and Ellsberg s paradoxes are accommodated. Finally, the construction easily extends to the complex unit ball, provided that x y 2 is replaced by x y 2 in the definition of p, in which case Theorem 7 holds with respect to a Hermitian (rather than symmetric) 6

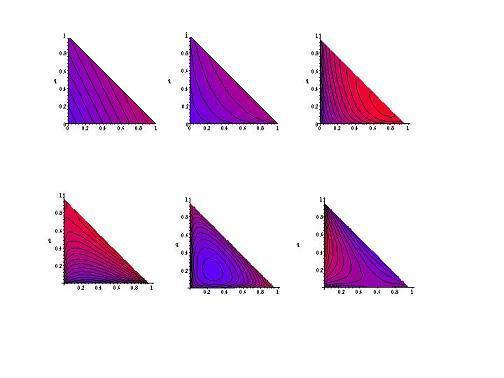

7 payoff matrix U, and the result also provides axiomatic foundations for decisions involving quantum uncertainty. Let e i, e j be the degenerate lotteries assigning probability 1 to outcomes s i and s j, respectively, and let e i,j be the lottery assigning probability 1/2 to each of the two states. Observe that, for any two distinct s i and s j, U ij = u(e i,j ) ( 1 2 u(e i) u(e j)). It follows that the off-diagonal entry U ij in the payoff matrix can be interpreted as the discount, or premium, attached to an equiprobable combination of the two outcomes with respect to its expected utility base-line, and hence as a measure of risk aversion along the specific dimension of risk involving outcomes s i and s j. Observe that the functional in Theorem 7 is quadratic in x, but linear in p. If U is diagonal, then its eigenvalues coincide with the diagonal elements. In von Neumann - Morgenstern expected utility, those eigenvalues contain all the relevant information about the decision-maker s risk attitudes. In our framework, risk attitudes are jointly captured by both the diagonal and non-diagonal elements of U, which are completely characterized by a diagonal matrix D with the eigenvalues of U on the main diagonal and a projection matrix P. Furthermore, in our setting attitudes towards uncertainty are captured by the concavity or convexity (in x) of the quadratic form x Ux, and therefore, ultimately, by the definiteness condition of U and the sign of its eigenvalues. Convexity corresponds to the case of all positive eigenvalues, and captures the idea that risk is ceteris paribus preferred to uncertainty, while concavity corresponds to the case of all negative eigenvalues and captures the opposite idea. 7 Example: objective uncertainty Figure 1 below presents several examples of indifference maps on pure lotteries which can be obtained within our class of preferences for different choices of U. The first pattern (parallel straight lines) characterizes von Neumann - Morgenstern expected utility. Within our class of representations, it corresponds to the special case of a diagonal payoff matrix U. All other patterns are impossible within von Neumann - Morgenstern expected utility. Our representation is sufficiently general to accommodate Allais paradox from section 3. In the context of the example in section 3, let {s 1, s 2, s 3 } be the states in which 4000, 3000, and 0 dollars are won, respectively. To accommodate Allais paradox, assume a slight aversion to the risk of obtaining no gain (s 3 ): U = s 1 s 2 s s s s 3 7

8 8

9 Let the four lotteries A, B, C, D be defined, respectively, as the following unit vectors in S + : a = 0 ; b = 0.25 ; c = 0 ; d = Then lottery A is preferred to B, while D is preferred to C, as u(a) = a Ua = 1.8, u(b) = b Ub = 1.634, u(c) = c Uc = 9.6, u(d) = d Ud = Example: subjective uncertainty In the Ellsberg puzzle, suppose that either all the non-red balls are green (R = 100, G = 200, B = 0), or they are all blue (R = 100, G = 0, B = 200), with equal subjective probability. Further, suppose that there are just two payoff-relevant outcomes, Win and Lose. Then the following specification of the payoff matrix accommodates the paradox: W in Lose U = W in 1 0. Lose 0 0 In fact, ( let ) ( ) 1/3 r = 2/3, r = be the lotteries representing R and R, 2/3 1/3 ( ) ( ) 1 0 respectively, and let w =, l = be the lotteries corresponding to 0 1 a sure win and a sure loss, respectively. Further, let g := αr + (1 α) l and g := βw + (1 β)r be the lotteries representing G and G, respectively, with α and β chosen to be the unique solutions to g1 2 = 1/3, g 2 1 = 2/3, respectively (as the subjective probability of winning in G is 1/3, and in G is 2/3). Then α = 1/6, β = 1/(3 3), and u(r) = r Ur = 1/3, u(r) = r Ur = 2/3, u(g) = g Ug = 1/9 u(g) = g Ug = 0.4, so the paradox is accommodated. Conversely, if the payoff matrix is given by U = W in Lose W in 0 0 Lose 0 1, 9

10 the opposite pattern emerges, as subjective uncertainty is now ceteris paribus preferred to risk. 9 Multi-agent decisions and equilibrium Within the class of preferences characterized by Theorem 7, is it still true that every finite game has a Nash equilibrium? If the payoff matrix U is diagonal and non-negative we are in the classical case, so we know that any finite game has an equilibrium, which moreover only involves (objective) risk (in our terms, this type of equilibrium should be referred to as pure, as it involves no subjective uncertainty). For the general case, consider that u(p) is still continuous and linear in p B, while B is a convex and compact set. Therefore, all the necessary steps in Nash proof (showing that the best response correspondence is non-empty, convex-valued and upper-hemicontinuous in order to apply Kakutani s fixed-point theorem) also follow in our case. Hence, any finite game has an equilibrium even within this larger class of preferences, even though the equilibrium may not be pure (in our sense): in general, an equilibrium will rest on a combination of objective randomization and subjective uncertainty about the players decisions. 10

11 10 Conclusions We presented a projective generalization of expected utility, and showed that it can accommodate the dominant decision-theoretic paradoxes. Whereas other generalizations of expected utility are typically non-linear in probabilities, our representation is linear in degrees of belief (and hence subjective probabilities), and therefore quite tractable in applications. In particular, every finite game still has an equilibrium even within this larger class of preferences. Our generalization of expected utility is closest to the one in Gyntelberg and Hansen (2004), which is obtained in a Savage context by postulating a nonclassical (that is, non-boolean) structure for the relevant events. By contrast, while our representation is obtained in a von Neumann - Morgenstern context (that is, beliefs are taken as already given), it does not impose specific requirements on the nature of the relevant uncertainty. In particular, in our context the dominant paradoxes can be resolved even if the relevant uncertainty is of completely classical nature. Furthermore, in case the event space is non-classical, our result also provides foundations for decisions involving quantum uncertainty. 11 References Maurice Allais (1953), Le Comportement de l Homme Rationnel devant le Risque: Critique des postulats et axiomes de l École Americaine. Econometrica 21, Daniel Bernoulli (1738), Specimen theoriae novae de mensura sortis. In Commentarii Academiae Scientiarum Imperialis Petropolitanae 5, Translated as Exposition of a new theory of the measurement of risk. Econometrica 22 (1954), Daniel Ellsberg (1961), Risk, Ambiguity and the Savage Axioms. Quarterly Journal of Economics 75, Jacob Gyntelberg and Frank Hansen (2004), Expected utility theory with small worlds, University of Copenhagen, Department of Economics Discussion Paper 04-20, John von Neumann (1932), Mathematische Grundlagen der Quantenmechanic. Berlin, Springer. Translated as Mathematical foundations of quantum mechanics, 1955, Princeton University Press, Princeton NJ. John von Neumann and Oskar Morgenstern (1944), Theory of Games and Economic Behavior. Princeton University Press, Princeton NJ. Matthew Rabin and Richard H. Thaler (2001), Anomalies: Risk Aversion. Journal of Economic Perspectives 15, Leonard J. Savage (1954), The Foundations of Statistics. Wiley, New York, NY. 11

Game Theory without Decision-Theoretic Paradoxes

Game Theory without Decision-Theoretic Paradoxes Pierfrancesco La Mura Department of Economics and Information Systems HHL - Leipzig Graduate School of Management Jahnallee 59, 04109 Leipzig (Germany)

Game Theory without Decision-Theoretic Paradoxes Pierfrancesco La Mura Department of Economics and Information Systems HHL - Leipzig Graduate School of Management Jahnallee 59, 04109 Leipzig (Germany)

Expected Utility Framework

Expected Utility Framework Preferences We want to examine the behavior of an individual, called a player, who must choose from among a set of outcomes. Let X be the (finite) set of outcomes with common

Expected Utility Framework Preferences We want to examine the behavior of an individual, called a player, who must choose from among a set of outcomes. Let X be the (finite) set of outcomes with common

Quantum Decision Theory

Quantum Decision Theory V.I. Yukalov and D. Sornette Department of Management, Technology and Economics\ ETH Zürich Plan 1. Classical Decision Theory 1.1. Notations and definitions 1.2. Typical paradoxes

Quantum Decision Theory V.I. Yukalov and D. Sornette Department of Management, Technology and Economics\ ETH Zürich Plan 1. Classical Decision Theory 1.1. Notations and definitions 1.2. Typical paradoxes

Expected utility without full transitivity

Expected utility without full transitivity Walter Bossert Department of Economics and CIREQ University of Montreal P.O. Box 6128, Station Downtown Montreal QC H3C 3J7 Canada FAX: (+1 514) 343 7221 e-mail:

Expected utility without full transitivity Walter Bossert Department of Economics and CIREQ University of Montreal P.O. Box 6128, Station Downtown Montreal QC H3C 3J7 Canada FAX: (+1 514) 343 7221 e-mail:

Recursive Ambiguity and Machina s Examples

Recursive Ambiguity and Machina s Examples David Dillenberger Uzi Segal May 0, 0 Abstract Machina (009, 0) lists a number of situations where standard models of ambiguity aversion are unable to capture

Recursive Ambiguity and Machina s Examples David Dillenberger Uzi Segal May 0, 0 Abstract Machina (009, 0) lists a number of situations where standard models of ambiguity aversion are unable to capture

Recursive Ambiguity and Machina s Examples

Recursive Ambiguity and Machina s Examples David Dillenberger Uzi Segal January 9, 204 Abstract Machina (2009, 202) lists a number of situations where Choquet expected utility, as well as other known models

Recursive Ambiguity and Machina s Examples David Dillenberger Uzi Segal January 9, 204 Abstract Machina (2009, 202) lists a number of situations where Choquet expected utility, as well as other known models

Choice Under Uncertainty

Choice Under Uncertainty Z a finite set of outcomes. P the set of probabilities on Z. p P is (p 1,...,p n ) with each p i 0 and n i=1 p i = 1 Binary relation on P. Objective probability case. Decision

Choice Under Uncertainty Z a finite set of outcomes. P the set of probabilities on Z. p P is (p 1,...,p n ) with each p i 0 and n i=1 p i = 1 Binary relation on P. Objective probability case. Decision

Towards a Theory of Decision Making without Paradoxes

Towards a Theory of Decision Making without Paradoxes Roman V. Belavkin (R.Belavkin@mdx.ac.uk) School of Computing Science, Middlesex University London NW4 4BT, United Kingdom Abstract Human subjects often

Towards a Theory of Decision Making without Paradoxes Roman V. Belavkin (R.Belavkin@mdx.ac.uk) School of Computing Science, Middlesex University London NW4 4BT, United Kingdom Abstract Human subjects often

RECURSIVE AMBIGUITY AND MACHINA S EXAMPLES 1. INTRODUCTION

INTERNATIONAL ECONOMIC REVIEW Vol. 56, No., February 05 RECURSIVE AMBIGUITY AND MACHINA S EXAMPLES BY DAVID DILLENBERGER AND UZI SEGAL University of Pennsylvania, U.S.A.; Boston College, U.S.A., and Warwick

INTERNATIONAL ECONOMIC REVIEW Vol. 56, No., February 05 RECURSIVE AMBIGUITY AND MACHINA S EXAMPLES BY DAVID DILLENBERGER AND UZI SEGAL University of Pennsylvania, U.S.A.; Boston College, U.S.A., and Warwick

Choice under Uncertainty

In the Name of God Sharif University of Technology Graduate School of Management and Economics Microeconomics 2 44706 (1394-95 2 nd term) Group 2 Dr. S. Farshad Fatemi Chapter 6: Choice under Uncertainty

In the Name of God Sharif University of Technology Graduate School of Management and Economics Microeconomics 2 44706 (1394-95 2 nd term) Group 2 Dr. S. Farshad Fatemi Chapter 6: Choice under Uncertainty

CERGE-EI. Back to the St. Petersburg Paradox? Pavlo Blavatskyy. WORKING PAPER SERIES (ISSN ) Electronic Version

Electronic Version") Back to the St. Petersburg Paradox? Pavlo Blavatskyy CERGE-EI Charles University Center for Economic Research and Graduate Education Academy of Sciences of the Czech Republic Economics Institute WORKING

Back to the St. Petersburg Paradox? Pavlo Blavatskyy CERGE-EI Charles University Center for Economic Research and Graduate Education Academy of Sciences of the Czech Republic Economics Institute WORKING

Von Neumann Morgenstern Expected Utility. I. Introduction, Definitions, and Applications. Decision Theory Spring 2014

Von Neumann Morgenstern Expected Utility I. Introduction, Definitions, and Applications Decision Theory Spring 2014 Origins Blaise Pascal, 1623 1662 Early inventor of the mechanical calculator Invented

Von Neumann Morgenstern Expected Utility I. Introduction, Definitions, and Applications Decision Theory Spring 2014 Origins Blaise Pascal, 1623 1662 Early inventor of the mechanical calculator Invented

Event-Separability in the Ellsberg urn

Econ Theory (2011) 48:425 436 DOI 10.1007/s00199-011-0652-4 SYMPOSIUM Event-Separability in the Ellsberg urn Mark J. Machina Received: 5 April 2011 / Accepted: 9 June 2011 / Published online: 16 July 2011

Econ Theory (2011) 48:425 436 DOI 10.1007/s00199-011-0652-4 SYMPOSIUM Event-Separability in the Ellsberg urn Mark J. Machina Received: 5 April 2011 / Accepted: 9 June 2011 / Published online: 16 July 2011

Homework #6 (10/18/2017)

") Homework #6 (0/8/207). Let G be the set of compound gambles over a finite set of deterministic payoffs {a, a 2,...a n } R +. A decision maker s preference relation over compound gambles can be represented

Homework #6 (0/8/207). Let G be the set of compound gambles over a finite set of deterministic payoffs {a, a 2,...a n } R +. A decision maker s preference relation over compound gambles can be represented

Preference, Choice and Utility

Preference, Choice and Utility Eric Pacuit January 2, 205 Relations Suppose that X is a non-empty set. The set X X is the cross-product of X with itself. That is, it is the set of all pairs of elements

Preference, Choice and Utility Eric Pacuit January 2, 205 Relations Suppose that X is a non-empty set. The set X X is the cross-product of X with itself. That is, it is the set of all pairs of elements

DECISIONS UNDER UNCERTAINTY

August 18, 2003 Aanund Hylland: # DECISIONS UNDER UNCERTAINTY Standard theory and alternatives 1. Introduction Individual decision making under uncertainty can be characterized as follows: The decision

August 18, 2003 Aanund Hylland: # DECISIONS UNDER UNCERTAINTY Standard theory and alternatives 1. Introduction Individual decision making under uncertainty can be characterized as follows: The decision

Expected utility without full transitivity

Expected utility without full transitivity Walter Bossert Department of Economics and CIREQ University of Montreal P.O. Box 6128, Station Downtown Montreal QC H3C 3J7 Canada FAX: (+1 514) 343 7221 e-mail:

Expected utility without full transitivity Walter Bossert Department of Economics and CIREQ University of Montreal P.O. Box 6128, Station Downtown Montreal QC H3C 3J7 Canada FAX: (+1 514) 343 7221 e-mail:

Decision-making with belief functions

Decision-making with belief functions Thierry Denœux Université de Technologie de Compiègne, France HEUDIASYC (UMR CNRS 7253) https://www.hds.utc.fr/ tdenoeux Fourth School on Belief Functions and their

Decision-making with belief functions Thierry Denœux Université de Technologie de Compiègne, France HEUDIASYC (UMR CNRS 7253) https://www.hds.utc.fr/ tdenoeux Fourth School on Belief Functions and their

Confronting Theory with Experimental Data and vice versa. Lecture I Choice under risk. The Norwegian School of Economics Nov 7-11, 2011

Confronting Theory with Experimental Data and vice versa Lecture I Choice under risk The Norwegian School of Economics Nov 7-11, 2011 Preferences Let X be some set of alternatives (consumption set). Formally,

Confronting Theory with Experimental Data and vice versa Lecture I Choice under risk The Norwegian School of Economics Nov 7-11, 2011 Preferences Let X be some set of alternatives (consumption set). Formally,

14.12 Game Theory Lecture Notes Theory of Choice

14.12 Game Theory Lecture Notes Theory of Choice Muhamet Yildiz (Lecture 2) 1 The basic theory of choice We consider a set X of alternatives. Alternatives are mutually exclusive in the sense that one cannot

14.12 Game Theory Lecture Notes Theory of Choice Muhamet Yildiz (Lecture 2) 1 The basic theory of choice We consider a set X of alternatives. Alternatives are mutually exclusive in the sense that one cannot

Correlated Equilibria of Classical Strategic Games with Quantum Signals

Correlated Equilibria of Classical Strategic Games with Quantum Signals Pierfrancesco La Mura Leipzig Graduate School of Management plamura@hhl.de comments welcome September 4, 2003 Abstract Correlated

Correlated Equilibria of Classical Strategic Games with Quantum Signals Pierfrancesco La Mura Leipzig Graduate School of Management plamura@hhl.de comments welcome September 4, 2003 Abstract Correlated

Recitation 7: Uncertainty. Xincheng Qiu

Econ 701A Fall 2018 University of Pennsylvania Recitation 7: Uncertainty Xincheng Qiu (qiux@sas.upenn.edu 1 Expected Utility Remark 1. Primitives: in the basic consumer theory, a preference relation is

Econ 701A Fall 2018 University of Pennsylvania Recitation 7: Uncertainty Xincheng Qiu (qiux@sas.upenn.edu 1 Expected Utility Remark 1. Primitives: in the basic consumer theory, a preference relation is

Intertemporal Risk Aversion, Stationarity, and Discounting

Traeger, CES ifo 10 p. 1 Intertemporal Risk Aversion, Stationarity, and Discounting Christian Traeger Department of Agricultural & Resource Economics, UC Berkeley Introduce a more general preference representation

Traeger, CES ifo 10 p. 1 Intertemporal Risk Aversion, Stationarity, and Discounting Christian Traeger Department of Agricultural & Resource Economics, UC Berkeley Introduce a more general preference representation

Rationality and Uncertainty

Rationality and Uncertainty Based on papers by Itzhak Gilboa, Massimo Marinacci, Andy Postlewaite, and David Schmeidler Warwick Aug 23, 2013 Risk and Uncertainty Dual use of probability: empirical frequencies

Rationality and Uncertainty Based on papers by Itzhak Gilboa, Massimo Marinacci, Andy Postlewaite, and David Schmeidler Warwick Aug 23, 2013 Risk and Uncertainty Dual use of probability: empirical frequencies

Uncertainty & Decision

Uncertainty & Decision von Neumann Morgenstern s Theorem Stéphane Airiau & Umberto Grandi ILLC - University of Amsterdam Stéphane Airiau & Umberto Grandi (ILLC) - Uncertainty & Decision von Neumann Morgenstern

Uncertainty & Decision von Neumann Morgenstern s Theorem Stéphane Airiau & Umberto Grandi ILLC - University of Amsterdam Stéphane Airiau & Umberto Grandi (ILLC) - Uncertainty & Decision von Neumann Morgenstern

Anti-comonotone random variables and Anti-monotone risk aversion

Anti-comonotone random variables and Anti-monotone risk aversion Moez Abouda Elyéss Farhoud Abstract This paper focuses on the study of decision making under risk. We, first, recall some model-free definitions

Anti-comonotone random variables and Anti-monotone risk aversion Moez Abouda Elyéss Farhoud Abstract This paper focuses on the study of decision making under risk. We, first, recall some model-free definitions

Choice under uncertainty

Choice under uncertainty Expected utility theory The agent chooses among a set of risky alternatives (lotteries) Description of risky alternatives (lotteries) a lottery L = a random variable on a set of

Choice under uncertainty Expected utility theory The agent chooses among a set of risky alternatives (lotteries) Description of risky alternatives (lotteries) a lottery L = a random variable on a set of

Week of May 5, lecture 1: Expected utility theory

Microeconomics 3 Andreas Ortmann, Ph.D. Summer 2003 (420 2) 240 05 117 andreas.ortmann@cerge-ei.cz http://home.cerge-ei.cz/ortmann Week of May 5, lecture 1: Expected utility theory Key readings: MWG 6.A.,

Microeconomics 3 Andreas Ortmann, Ph.D. Summer 2003 (420 2) 240 05 117 andreas.ortmann@cerge-ei.cz http://home.cerge-ei.cz/ortmann Week of May 5, lecture 1: Expected utility theory Key readings: MWG 6.A.,

Ambiguity Aversion: An Axiomatic Approach Using Second Order Probabilities

Ambiguity Aversion: An Axiomatic Approach Using Second Order Probabilities William S. Neilson Department of Economics University of Tennessee Knoxville, TN 37996-0550 wneilson@utk.edu April 1993 Abstract

Ambiguity Aversion: An Axiomatic Approach Using Second Order Probabilities William S. Neilson Department of Economics University of Tennessee Knoxville, TN 37996-0550 wneilson@utk.edu April 1993 Abstract

Review of Probability, Expected Utility

Review of Probability, Expected Utility Economics 302 - Microeconomic Theory II: Strategic Behavior Instructor: Songzi Du compiled by Shih En Lu Simon Fraser University May 8, 2018 ECON 302 (SFU) Lecture

Review of Probability, Expected Utility Economics 302 - Microeconomic Theory II: Strategic Behavior Instructor: Songzi Du compiled by Shih En Lu Simon Fraser University May 8, 2018 ECON 302 (SFU) Lecture

Rational Expectations and Ambiguity: A Comment on Abel (2002)

") Rational Expectations and Ambiguity: A Comment on Abel (2002) Alexander Ludwig and Alexander Zimper 66-20 mea Mannheimer Forschungsinstitut Ökonomie und Demographischer Wandel Gebäude L 13, 17_D-68131

Rational Expectations and Ambiguity: A Comment on Abel (2002) Alexander Ludwig and Alexander Zimper 66-20 mea Mannheimer Forschungsinstitut Ökonomie und Demographischer Wandel Gebäude L 13, 17_D-68131

Consumer theory Topics in consumer theory. Microeconomics. Joana Pais. Fall Joana Pais

Microeconomics Fall 2016 Indirect utility and expenditure Properties of consumer demand The indirect utility function The relationship among prices, incomes, and the maximised value of utility can be summarised

Microeconomics Fall 2016 Indirect utility and expenditure Properties of consumer demand The indirect utility function The relationship among prices, incomes, and the maximised value of utility can be summarised

Conditional and Dynamic Preferences

Conditional and Dynamic Preferences How can we Understand Risk in a Dynamic Setting? Samuel Drapeau Joint work with Hans Föllmer Humboldt University Berlin Jena - March 17th 2009 Samuel Drapeau Joint work

Conditional and Dynamic Preferences How can we Understand Risk in a Dynamic Setting? Samuel Drapeau Joint work with Hans Föllmer Humboldt University Berlin Jena - March 17th 2009 Samuel Drapeau Joint work

Economic uncertainty principle? Alexander Harin

Economic uncertainty principle? Alexander Harin This preliminary paper presents a qualitative description of the economic principle of (hidden, latent) uncertainty. Mathematical expressions of principle,

Economic uncertainty principle? Alexander Harin This preliminary paper presents a qualitative description of the economic principle of (hidden, latent) uncertainty. Mathematical expressions of principle,

Measurable Ambiguity. with Wolfgang Pesendorfer. August 2009

Measurable Ambiguity with Wolfgang Pesendorfer August 2009 A Few Definitions A Lottery is a (cumulative) probability distribution over monetary prizes. It is a probabilistic description of the DMs uncertain

Measurable Ambiguity with Wolfgang Pesendorfer August 2009 A Few Definitions A Lottery is a (cumulative) probability distribution over monetary prizes. It is a probabilistic description of the DMs uncertain

Prospect Theory: An Analysis of Decision Under Risk

Prospect Theory: An Analysis of Decision Under Risk Daniel Kahneman and Amos Tversky(1979) Econometrica, 47(2) Presented by Hirofumi Kurokawa(Osaka Univ.) 1 Introduction This paper shows that there are

Prospect Theory: An Analysis of Decision Under Risk Daniel Kahneman and Amos Tversky(1979) Econometrica, 47(2) Presented by Hirofumi Kurokawa(Osaka Univ.) 1 Introduction This paper shows that there are

An Axiomatic Model of Reference Dependence under Uncertainty. Yosuke Hashidate

An Axiomatic Model of Reference Dependence under Uncertainty Yosuke Hashidate Abstract This paper presents a behavioral characteization of a reference-dependent choice under uncertainty in the Anscombe-Aumann

An Axiomatic Model of Reference Dependence under Uncertainty Yosuke Hashidate Abstract This paper presents a behavioral characteization of a reference-dependent choice under uncertainty in the Anscombe-Aumann

Game Theory. Lecture Notes By Y. Narahari. Department of Computer Science and Automation Indian Institute of Science Bangalore, India August 2012

Game Theory Lecture Notes By Y. Narahari Department of Computer Science and Automation Indian Institute of Science Bangalore, India August 2012 Chapter 7: Von Neumann - Morgenstern Utilities Note: This

Game Theory Lecture Notes By Y. Narahari Department of Computer Science and Automation Indian Institute of Science Bangalore, India August 2012 Chapter 7: Von Neumann - Morgenstern Utilities Note: This

Are Probabilities Used in Markets? 1

Journal of Economic Theory 91, 8690 (2000) doi:10.1006jeth.1999.2590, available online at http:www.idealibrary.com on NOTES, COMMENTS, AND LETTERS TO THE EDITOR Are Probabilities Used in Markets? 1 Larry

Journal of Economic Theory 91, 8690 (2000) doi:10.1006jeth.1999.2590, available online at http:www.idealibrary.com on NOTES, COMMENTS, AND LETTERS TO THE EDITOR Are Probabilities Used in Markets? 1 Larry

6.891 Games, Decision, and Computation February 5, Lecture 2

6.891 Games, Decision, and Computation February 5, 2015 Lecture 2 Lecturer: Constantinos Daskalakis Scribe: Constantinos Daskalakis We formally define games and the solution concepts overviewed in Lecture

6.891 Games, Decision, and Computation February 5, 2015 Lecture 2 Lecturer: Constantinos Daskalakis Scribe: Constantinos Daskalakis We formally define games and the solution concepts overviewed in Lecture

Suzumura-consistent relations: an overview

Suzumura-consistent relations: an overview Walter Bossert Department of Economics and CIREQ University of Montreal P.O. Box 6128, Station Downtown Montreal QC H3C 3J7 Canada walter.bossert@videotron.ca

Suzumura-consistent relations: an overview Walter Bossert Department of Economics and CIREQ University of Montreal P.O. Box 6128, Station Downtown Montreal QC H3C 3J7 Canada walter.bossert@videotron.ca

Anscombe & Aumann Expected Utility Betting and Insurance

Anscombe & Aumann Expected Utility Betting and Insurance Econ 2100 Fall 2017 Lecture 11, October 3 Outline 1 Subjective Expected Utility 2 Qualitative Probabilities 3 Allais and Ellsebrg Paradoxes 4 Utility

Anscombe & Aumann Expected Utility Betting and Insurance Econ 2100 Fall 2017 Lecture 11, October 3 Outline 1 Subjective Expected Utility 2 Qualitative Probabilities 3 Allais and Ellsebrg Paradoxes 4 Utility

Stochastic Utility Theorem

Institute for Empirical Research in Economics University of Zurich Working Paper Series ISSN 44-0459 Working Paper No. Stochastic Utility Theorem Pavlo R. Blavatskyy Januar 007 Stochastic Utility Theorem

Institute for Empirical Research in Economics University of Zurich Working Paper Series ISSN 44-0459 Working Paper No. Stochastic Utility Theorem Pavlo R. Blavatskyy Januar 007 Stochastic Utility Theorem

Allais, Ellsberg, and Preferences for Hedging

Allais, Ellsberg, and Preferences for Hedging Mark Dean and Pietro Ortoleva Abstract Two of the most well-known regularities observed in preferences under risk and uncertainty are ambiguity aversion and

Allais, Ellsberg, and Preferences for Hedging Mark Dean and Pietro Ortoleva Abstract Two of the most well-known regularities observed in preferences under risk and uncertainty are ambiguity aversion and

Expected Utility Calibration for Continuous Distributions

Epected Utility Calibration for Continuous Distributions David R. Just Assistant Professor Applied Economics and Management Cornell University 54 Warren Hall Ithaca, NY 4853 Tel: (607) 55-086 Fa: (607)

Epected Utility Calibration for Continuous Distributions David R. Just Assistant Professor Applied Economics and Management Cornell University 54 Warren Hall Ithaca, NY 4853 Tel: (607) 55-086 Fa: (607)

Problem Set 4 - Solution Hints

ETH Zurich D-MTEC Chair of Risk & Insurance Economics (Prof. Mimra) Exercise Class Spring 206 Anastasia Sycheva Contact: asycheva@ethz.ch Office Hour: on appointment Zürichbergstrasse 8 / ZUE, Room F2

ETH Zurich D-MTEC Chair of Risk & Insurance Economics (Prof. Mimra) Exercise Class Spring 206 Anastasia Sycheva Contact: asycheva@ethz.ch Office Hour: on appointment Zürichbergstrasse 8 / ZUE, Room F2

Bayesian consistent prior selection

Bayesian consistent prior selection Christopher P. Chambers and Takashi Hayashi August 2005 Abstract A subjective expected utility agent is given information about the state of the world in the form of

Bayesian consistent prior selection Christopher P. Chambers and Takashi Hayashi August 2005 Abstract A subjective expected utility agent is given information about the state of the world in the form of

Certainty Equivalent Representation of Binary Gambles That Are Decomposed into Risky and Sure Parts

Review of Economics & Finance Submitted on 28/Nov./2011 Article ID: 1923-7529-2012-02-65-11 Yutaka Matsushita Certainty Equivalent Representation of Binary Gambles That Are Decomposed into Risky and Sure

Review of Economics & Finance Submitted on 28/Nov./2011 Article ID: 1923-7529-2012-02-65-11 Yutaka Matsushita Certainty Equivalent Representation of Binary Gambles That Are Decomposed into Risky and Sure

Ph.D. Preliminary Examination MICROECONOMIC THEORY Applied Economics Graduate Program June 2016

Ph.D. Preliminary Examination MICROECONOMIC THEORY Applied Economics Graduate Program June 2016 The time limit for this exam is four hours. The exam has four sections. Each section includes two questions.

Ph.D. Preliminary Examination MICROECONOMIC THEORY Applied Economics Graduate Program June 2016 The time limit for this exam is four hours. The exam has four sections. Each section includes two questions.

Weak* Axiom of Independence and the Non-Expected Utility Theory

Review of Economic Analysis 4 (01) 67-75 1973-3909/01067 Weak* Axiom of Independence and the Non-Expected Utility Theory TAPAN BISWAS University of Hull 1 Introduction The axiomatic foundation of the expected

Review of Economic Analysis 4 (01) 67-75 1973-3909/01067 Weak* Axiom of Independence and the Non-Expected Utility Theory TAPAN BISWAS University of Hull 1 Introduction The axiomatic foundation of the expected

1 Uncertainty and Insurance

Uncertainty and Insurance Reading: Some fundamental basics are in Varians intermediate micro textbook (Chapter 2). A good (advanced, but still rather accessible) treatment is in Kreps A Course in Microeconomic

Uncertainty and Insurance Reading: Some fundamental basics are in Varians intermediate micro textbook (Chapter 2). A good (advanced, but still rather accessible) treatment is in Kreps A Course in Microeconomic

Decision Making Under Uncertainty. First Masterclass

Decision Making Under Uncertainty First Masterclass 1 Outline A short history Decision problems Uncertainty The Ellsberg paradox Probability as a measure of uncertainty Ignorance 2 Probability Blaise Pascal

Decision Making Under Uncertainty First Masterclass 1 Outline A short history Decision problems Uncertainty The Ellsberg paradox Probability as a measure of uncertainty Ignorance 2 Probability Blaise Pascal

1 Uncertainty. These notes correspond to chapter 2 of Jehle and Reny.

These notes correspond to chapter of Jehle and Reny. Uncertainty Until now we have considered our consumer s making decisions in a world with perfect certainty. However, we can extend the consumer theory

These notes correspond to chapter of Jehle and Reny. Uncertainty Until now we have considered our consumer s making decisions in a world with perfect certainty. However, we can extend the consumer theory

4.1. Chapter 4. timing risk information utility

4. Chapter 4 timing risk information utility 4.2. Money pumps Rationality in economics is identified with consistency. In particular, a preference relation must be total and transitive Transitivity implies

4. Chapter 4 timing risk information utility 4.2. Money pumps Rationality in economics is identified with consistency. In particular, a preference relation must be total and transitive Transitivity implies

Mathematical Social Sciences

Mathematical Social Sciences 74 (2015) 68 72 Contents lists available at ScienceDirect Mathematical Social Sciences journal homepage: www.elsevier.com/locate/econbase Continuity, completeness, betweenness

Mathematical Social Sciences 74 (2015) 68 72 Contents lists available at ScienceDirect Mathematical Social Sciences journal homepage: www.elsevier.com/locate/econbase Continuity, completeness, betweenness

Chapter 1 - Preference and choice

http://selod.ensae.net/m1 Paris School of Economics (selod@ens.fr) September 27, 2007 Notations Consider an individual (agent) facing a choice set X. Definition (Choice set, "Consumption set") X is a set

http://selod.ensae.net/m1 Paris School of Economics (selod@ens.fr) September 27, 2007 Notations Consider an individual (agent) facing a choice set X. Definition (Choice set, "Consumption set") X is a set

ECO 317 Economics of Uncertainty Fall Term 2009 Notes for lectures 3. Risk Aversion

Reminders ECO 317 Economics of Uncertainty Fall Term 009 Notes for lectures 3. Risk Aversion On the space of lotteries L that offer a finite number of consequences (C 1, C,... C n ) with probabilities

Reminders ECO 317 Economics of Uncertainty Fall Term 009 Notes for lectures 3. Risk Aversion On the space of lotteries L that offer a finite number of consequences (C 1, C,... C n ) with probabilities

Range-Dependent Utility

Range-Dependent Utility Micha l Lewandowski joint work with Krzysztof Kontek March 23, 207 Outline. Inspired by Parducci (964) we propose range-dependent utility (RDU) as a general framework for decisions

Range-Dependent Utility Micha l Lewandowski joint work with Krzysztof Kontek March 23, 207 Outline. Inspired by Parducci (964) we propose range-dependent utility (RDU) as a general framework for decisions

Common ratio using delay

Theory Dec. (2010) 68:149 158 DOI 10.1007/s18-008-9130-2 Common ratio using delay Manel Baucells Franz H. Heukamp Published online: 4 January 2009 Springer Science+Business Media, LLC. 2009 Abstract We

Theory Dec. (2010) 68:149 158 DOI 10.1007/s18-008-9130-2 Common ratio using delay Manel Baucells Franz H. Heukamp Published online: 4 January 2009 Springer Science+Business Media, LLC. 2009 Abstract We

Probabilistic Subjective Expected Utility. Pavlo R. Blavatskyy

Probabilistic Subjective Expected Utility Pavlo R. Blavatskyy Institute of Public Finance University of Innsbruck Universitaetsstrasse 15 A-6020 Innsbruck Austria Phone: +43 (0) 512 507 71 56 Fax: +43

Probabilistic Subjective Expected Utility Pavlo R. Blavatskyy Institute of Public Finance University of Innsbruck Universitaetsstrasse 15 A-6020 Innsbruck Austria Phone: +43 (0) 512 507 71 56 Fax: +43

Decision Making under Uncertainty and Subjective. Probabilities

Decision Making under Uncertainty and Subjective Probabilities Edi Karni Johns Hopkins University September 7, 2005 Abstract This paper presents two axiomatic models of decision making under uncertainty

Decision Making under Uncertainty and Subjective Probabilities Edi Karni Johns Hopkins University September 7, 2005 Abstract This paper presents two axiomatic models of decision making under uncertainty

Uncertainty. Michael Peters December 27, 2013

Uncertainty Michael Peters December 27, 20 Lotteries In many problems in economics, people are forced to make decisions without knowing exactly what the consequences will be. For example, when you buy

Uncertainty Michael Peters December 27, 20 Lotteries In many problems in economics, people are forced to make decisions without knowing exactly what the consequences will be. For example, when you buy

Almost essential: Consumption and Uncertainty Probability Distributions MICROECONOMICS

Prerequisites Almost essential: Consumption and Uncertainty Probability Distributions RISK MICROECONOMICS Principles and Analysis Frank Cowell July 2017 1 Risk and uncertainty In dealing with uncertainty

Prerequisites Almost essential: Consumption and Uncertainty Probability Distributions RISK MICROECONOMICS Principles and Analysis Frank Cowell July 2017 1 Risk and uncertainty In dealing with uncertainty

Ambiguity Framed. Mark Schneider, Jonathan Leland, and Nathaniel T. Wilcox

Ambiguity Framed Mark Schneider, Jonathan Leland, and Nathaniel T. Wilcox In his exposition of subjective expected utility theory, Savage (1954) proposed that the Allais paradox could be reduced if it

Ambiguity Framed Mark Schneider, Jonathan Leland, and Nathaniel T. Wilcox In his exposition of subjective expected utility theory, Savage (1954) proposed that the Allais paradox could be reduced if it

3 Intertemporal Risk Aversion

3 Intertemporal Risk Aversion 3. Axiomatic Characterization This section characterizes the invariant quantity found in proposition 2 axiomatically. The axiomatic characterization below is for a decision

3 Intertemporal Risk Aversion 3. Axiomatic Characterization This section characterizes the invariant quantity found in proposition 2 axiomatically. The axiomatic characterization below is for a decision

Dominance and Admissibility without Priors

Dominance and Admissibility without Priors Jörg Stoye Cornell University September 14, 2011 Abstract This note axiomatizes the incomplete preference ordering that reflects statewise dominance with respect

Dominance and Admissibility without Priors Jörg Stoye Cornell University September 14, 2011 Abstract This note axiomatizes the incomplete preference ordering that reflects statewise dominance with respect

Cautious and Globally Ambiguity Averse

Ozgur Evren New Economic School August, 2016 Introduction Subject: Segal s (1987) theory of recursive preferences. Ambiguity aversion: Tendency to prefer risk to ambiguity. (Ellsberg paradox) risk objective,

Ozgur Evren New Economic School August, 2016 Introduction Subject: Segal s (1987) theory of recursive preferences. Ambiguity aversion: Tendency to prefer risk to ambiguity. (Ellsberg paradox) risk objective,

ON LOSS AVERSION IN BIMATRIX GAMES

Theory and Decision (2010) 68:367 391 The Author(s) 2008 DOI 10.1007/s11238-008-9102-6 BRAM DRIESEN, ANDRÉS PEREA, and HANS PETERS ON LOSS AVERSION IN BIMATRIX GAMES ABSTRACT. In this article three different

Theory and Decision (2010) 68:367 391 The Author(s) 2008 DOI 10.1007/s11238-008-9102-6 BRAM DRIESEN, ANDRÉS PEREA, and HANS PETERS ON LOSS AVERSION IN BIMATRIX GAMES ABSTRACT. In this article three different

Preference for Commitment

Preference for Commitment Mark Dean Behavioral Economics G6943 Fall 2016 Introduction In order to discuss preference for commitment we need to be able to discuss preferences over menus Interpretation:

Preference for Commitment Mark Dean Behavioral Economics G6943 Fall 2016 Introduction In order to discuss preference for commitment we need to be able to discuss preferences over menus Interpretation:

Preferences and Utility

Preferences and Utility How can we formally describe an individual s preference for different amounts of a good? How can we represent his preference for a particular list of goods (a bundle) over another?

Preferences and Utility How can we formally describe an individual s preference for different amounts of a good? How can we represent his preference for a particular list of goods (a bundle) over another?

A theory of robust experiments for choice under uncertainty

A theory of robust experiments for choice under uncertainty S. Grant a,, J. Kline b, I. Meneghel a, J. Quiggin b, R. Tourky a a Australian National University b The University of Queensland Abstract Thought

A theory of robust experiments for choice under uncertainty S. Grant a,, J. Kline b, I. Meneghel a, J. Quiggin b, R. Tourky a a Australian National University b The University of Queensland Abstract Thought

Lecture Note Set 4 4 UTILITY THEORY. IE675 Game Theory. Wayne F. Bialas 1 Thursday, March 6, Introduction

IE675 Game Theory Lecture Note Set 4 Wayne F. Bialas 1 Thursday, March 6, 2003 4 UTILITY THEORY 4.1 Introduction 4.2 The basic theory This section is really independent of the field of game theory, and

IE675 Game Theory Lecture Note Set 4 Wayne F. Bialas 1 Thursday, March 6, 2003 4 UTILITY THEORY 4.1 Introduction 4.2 The basic theory This section is really independent of the field of game theory, and

* Professor of Finance at INSEAD, Boulevard de Constance, Fontainebleau Cedex, France.

DIFFERENTIABLE UTILITY by L. T. NIELSEN* 97/28/FIN * Professor of Finance at INSEAD, Boulevard de Constance, Fontainebleau 77305 Cedex, France. A working paper in the INSEAD Working Paper Series is intended

DIFFERENTIABLE UTILITY by L. T. NIELSEN* 97/28/FIN * Professor of Finance at INSEAD, Boulevard de Constance, Fontainebleau 77305 Cedex, France. A working paper in the INSEAD Working Paper Series is intended

Chapter 2. Decision Making under Risk. 2.1 Consequences and Lotteries

Chapter 2 Decision Making under Risk In the previous lecture I considered abstract choice problems. In this section, I will focus on a special class of choice problems and impose more structure on the

Chapter 2 Decision Making under Risk In the previous lecture I considered abstract choice problems. In this section, I will focus on a special class of choice problems and impose more structure on the

Axiomatic bargaining. theory

Axiomatic bargaining theory Objective: To formulate and analyse reasonable criteria for dividing the gains or losses from a cooperative endeavour among several agents. We begin with a non-empty set of

Axiomatic bargaining theory Objective: To formulate and analyse reasonable criteria for dividing the gains or losses from a cooperative endeavour among several agents. We begin with a non-empty set of

A Note on the Existence of Ratifiable Acts

A Note on the Existence of Ratifiable Acts Joseph Y. Halpern Cornell University Computer Science Department Ithaca, NY 14853 halpern@cs.cornell.edu http://www.cs.cornell.edu/home/halpern August 15, 2018

A Note on the Existence of Ratifiable Acts Joseph Y. Halpern Cornell University Computer Science Department Ithaca, NY 14853 halpern@cs.cornell.edu http://www.cs.cornell.edu/home/halpern August 15, 2018

Uncertainty and Disagreement in Equilibrium Models

Uncertainty and Disagreement in Equilibrium Models Nabil I. Al-Najjar & Northwestern University Eran Shmaya Tel Aviv University RUD, Warwick, June 2014 Forthcoming: Journal of Political Economy Motivation

Uncertainty and Disagreement in Equilibrium Models Nabil I. Al-Najjar & Northwestern University Eran Shmaya Tel Aviv University RUD, Warwick, June 2014 Forthcoming: Journal of Political Economy Motivation

Action-Independent Subjective Expected Utility without States of the World

heoretical Economics Letters, 013, 3, 17-1 http://dxdoiorg/10436/tel01335a004 Published Online September 013 (http://wwwscirporg/journal/tel) Action-Independent Subjective Expected Utility without States

heoretical Economics Letters, 013, 3, 17-1 http://dxdoiorg/10436/tel01335a004 Published Online September 013 (http://wwwscirporg/journal/tel) Action-Independent Subjective Expected Utility without States

arxiv: v1 [cs.ai] 16 Aug 2018

![arxiv: v1 [cs.ai] 16 Aug 2018](/thumbs/89/97937400.jpg "arxiv: v1 [cs.ai] 16 Aug 2018") Decision-Making with Belief Functions: a Review Thierry Denœux arxiv:1808.05322v1 [cs.ai] 16 Aug 2018 Université de Technologie de Compiègne, CNRS UMR 7253 Heudiasyc, Compiègne, France email: thierry.denoeux@utc.fr

Decision-Making with Belief Functions: a Review Thierry Denœux arxiv:1808.05322v1 [cs.ai] 16 Aug 2018 Université de Technologie de Compiègne, CNRS UMR 7253 Heudiasyc, Compiègne, France email: thierry.denoeux@utc.fr

Relative Benefit Equilibrating Bargaining Solution and the Ordinal Interpretation of Gauthier s Arbitration Scheme

Relative Benefit Equilibrating Bargaining Solution and the Ordinal Interpretation of Gauthier s Arbitration Scheme Mantas Radzvilas July 2017 Abstract In 1986 David Gauthier proposed an arbitration scheme

Relative Benefit Equilibrating Bargaining Solution and the Ordinal Interpretation of Gauthier s Arbitration Scheme Mantas Radzvilas July 2017 Abstract In 1986 David Gauthier proposed an arbitration scheme

Third down with a yard to go : the Dixit-Skeath conundrum on equilibria in competitive games.

June 28, 1999 Third down with a yard to go : the Dixit-Skeath conundrum on equilibria in competitive games. Abstract In strictly competitive games, equilibrium mixed strategies are invariant to changes

June 28, 1999 Third down with a yard to go : the Dixit-Skeath conundrum on equilibria in competitive games. Abstract In strictly competitive games, equilibrium mixed strategies are invariant to changes

Msc Micro I exam. Lecturer: Todd Kaplan.

Msc Micro I 204-205 exam. Lecturer: Todd Kaplan. Please answer exactly 5 questions. Answer one question from each of sections: A, B, C, and D and answer one additional question from any of the sections

Msc Micro I 204-205 exam. Lecturer: Todd Kaplan. Please answer exactly 5 questions. Answer one question from each of sections: A, B, C, and D and answer one additional question from any of the sections

A Theory of Subjective Compound Lotteries

A Theory of Subjective Compound Lotteries Haluk Ergin Washington University in St Louis and Faruk Gul Princeton University September 2008 Abstract We develop a Savage-type model of choice under uncertainty

A Theory of Subjective Compound Lotteries Haluk Ergin Washington University in St Louis and Faruk Gul Princeton University September 2008 Abstract We develop a Savage-type model of choice under uncertainty

MATH 446/546 Homework 2: Due October 8th, 2014

MATH 446/546 Homework 2: Due October 8th, 2014 Answer the following questions. Some of which come from Winston s text book. 1. We are going to invest $1,000 for a period of 6 months. Two potential investments

MATH 446/546 Homework 2: Due October 8th, 2014 Answer the following questions. Some of which come from Winston s text book. 1. We are going to invest $1,000 for a period of 6 months. Two potential investments

A Bayesian Approach to Uncertainty Aversion

Review of Economic Studies (2005) 72, 449 466 0034-6527/05/00190449$02.00 c 2005 The Review of Economic Studies Limited A Bayesian Approach to Uncertainty Aversion YORAM HALEVY University of British Columbia

Review of Economic Studies (2005) 72, 449 466 0034-6527/05/00190449$02.00 c 2005 The Review of Economic Studies Limited A Bayesian Approach to Uncertainty Aversion YORAM HALEVY University of British Columbia

The Expected Utility Model

1 The Expected Utility Model Before addressing any decision problem under uncertainty, it is necessary to build a preference functional that evaluates the level of satisfaction of the decision maker who

1 The Expected Utility Model Before addressing any decision problem under uncertainty, it is necessary to build a preference functional that evaluates the level of satisfaction of the decision maker who

Economics 201B Economic Theory (Spring 2017) Bargaining. Topics: the axiomatic approach (OR 15) and the strategic approach (OR 7).

Bargaining. Topics: the axiomatic approach (OR 15) and the strategic approach (OR 7).") Economics 201B Economic Theory (Spring 2017) Bargaining Topics: the axiomatic approach (OR 15) and the strategic approach (OR 7). The axiomatic approach (OR 15) Nash s (1950) work is the starting point

Economics 201B Economic Theory (Spring 2017) Bargaining Topics: the axiomatic approach (OR 15) and the strategic approach (OR 7). The axiomatic approach (OR 15) Nash s (1950) work is the starting point

Comment on The Veil of Public Ignorance

Comment on The Veil of Public Ignorance Geoffroy de Clippel February 2010 Nehring (2004) proposes an interesting methodology to extend the utilitarian criterion defined under complete information to an

Comment on The Veil of Public Ignorance Geoffroy de Clippel February 2010 Nehring (2004) proposes an interesting methodology to extend the utilitarian criterion defined under complete information to an

Great Expectations. Part I: On the Customizability of Generalized Expected Utility*

Great Expectations. Part I: On the Customizability of Generalized Expected Utility* Francis C. Chu and Joseph Y. Halpern Department of Computer Science Cornell University Ithaca, NY 14853, U.S.A. Email:

Great Expectations. Part I: On the Customizability of Generalized Expected Utility* Francis C. Chu and Joseph Y. Halpern Department of Computer Science Cornell University Ithaca, NY 14853, U.S.A. Email:

The Interdisciplinary Center, Herzliya School of Economics Advanced Microeconomics Fall Bargaining The Axiomatic Approach

The Interdisciplinary Center, Herzliya School of Economics Advanced Microeconomics Fall 2011 Bargaining The Axiomatic Approach Bargaining problem Nash s (1950) work is the starting point for formal bargaining

The Interdisciplinary Center, Herzliya School of Economics Advanced Microeconomics Fall 2011 Bargaining The Axiomatic Approach Bargaining problem Nash s (1950) work is the starting point for formal bargaining

Information, Utility & Bounded Rationality

Information, Utility & Bounded Rationality Pedro A. Ortega and Daniel A. Braun Department of Engineering, University of Cambridge Trumpington Street, Cambridge, CB2 PZ, UK {dab54,pao32}@cam.ac.uk Abstract.

Information, Utility & Bounded Rationality Pedro A. Ortega and Daniel A. Braun Department of Engineering, University of Cambridge Trumpington Street, Cambridge, CB2 PZ, UK {dab54,pao32}@cam.ac.uk Abstract.

Utility and rational decision-making

Chapter 5 Utility and rational decision-making The ability of making appropriate decisions in any given situation is clearly a necessary prerequisite for the survival of any animal and, indeed, even simple

Chapter 5 Utility and rational decision-making The ability of making appropriate decisions in any given situation is clearly a necessary prerequisite for the survival of any animal and, indeed, even simple

Second-Order Expected Utility

Second-Order Expected Utility Simon Grant Ben Polak Tomasz Strzalecki Preliminary version: November 2009 Abstract We present two axiomatizations of the Second-Order Expected Utility model in the context

Second-Order Expected Utility Simon Grant Ben Polak Tomasz Strzalecki Preliminary version: November 2009 Abstract We present two axiomatizations of the Second-Order Expected Utility model in the context

Course Handouts ECON 4161/8001 MICROECONOMIC ANALYSIS. Jan Werner. University of Minnesota

Course Handouts ECON 4161/8001 MICROECONOMIC ANALYSIS Jan Werner University of Minnesota FALL SEMESTER 2017 1 PART I: Producer Theory 1. Production Set Production set is a subset Y of commodity space IR

Course Handouts ECON 4161/8001 MICROECONOMIC ANALYSIS Jan Werner University of Minnesota FALL SEMESTER 2017 1 PART I: Producer Theory 1. Production Set Production set is a subset Y of commodity space IR

Economic Theory and Experimental Economics: Confronting Theory with Experimental Data and vice versa. Risk Preferences

Economic Theory and Experimental Economics: Confronting Theory with Experimental Data and vice versa Risk Preferences Hong Kong University of Science and Technology December 2013 Preferences Let X be some

Economic Theory and Experimental Economics: Confronting Theory with Experimental Data and vice versa Risk Preferences Hong Kong University of Science and Technology December 2013 Preferences Let X be some

Allais Paradox. The set of prizes is X = {$0, $1, 000, 000, $5, 000, 000}.

1 Allais Paradox The set of prizes is X = {$0, $1, 000, 000, $5, 000, 000}. Which probability do you prefer: p 1 = (0.00, 1.00, 0.00) or p 2 = (0.01, 0.89, 0.10)? Which probability do you prefer: p 3 =

1 Allais Paradox The set of prizes is X = {$0, $1, 000, 000, $5, 000, 000}. Which probability do you prefer: p 1 = (0.00, 1.00, 0.00) or p 2 = (0.01, 0.89, 0.10)? Which probability do you prefer: p 3 =

Glimcher Decision Making

Glimcher Decision Making Signal Detection Theory With Gaussian Assumption Without Gaussian Assumption Equivalent to Maximum Likelihood w/o Cost Function Newsome Dot Task QuickTime and a Video decompressor

Glimcher Decision Making Signal Detection Theory With Gaussian Assumption Without Gaussian Assumption Equivalent to Maximum Likelihood w/o Cost Function Newsome Dot Task QuickTime and a Video decompressor

Transitive Regret over Statistically Independent Lotteries

Transitive Regret over Statistically Independent Lotteries April 2, 2012 Abstract Preferences may arise from regret, i.e., from comparisons with alternatives forgone by the decision maker. We show that

Transitive Regret over Statistically Independent Lotteries April 2, 2012 Abstract Preferences may arise from regret, i.e., from comparisons with alternatives forgone by the decision maker. We show that

Parametric weighting functions

Journal of Economic Theory 144 (2009) 1102 1118 www.elsevier.com/locate/jet Parametric weighting functions Enrico Diecidue a, Ulrich Schmidt b,c, Horst Zank d, a Decision Sciences Area, INSEAD, Fontainebleau,

Journal of Economic Theory 144 (2009) 1102 1118 www.elsevier.com/locate/jet Parametric weighting functions Enrico Diecidue a, Ulrich Schmidt b,c, Horst Zank d, a Decision Sciences Area, INSEAD, Fontainebleau,

September 2007, France

LIKELIHOOD CONSISTENCY M h dabd ll i (& P t P W kk ) Mohammed Abdellaoui (& Peter P. Wakker) September 2007, France A new method is presented for measuring beliefs/likelihoods under uncertainty. It will

LIKELIHOOD CONSISTENCY M h dabd ll i (& P t P W kk ) Mohammed Abdellaoui (& Peter P. Wakker) September 2007, France A new method is presented for measuring beliefs/likelihoods under uncertainty. It will