VAR models with non-gaussian shocks

|

|

|

- Wesley Horn

- 5 years ago

- Views:

Transcription

1 VAR models with non-gaussian shocks Ching-Wai (Jeremy) Chiu Haroon Mumtaz Gabor Pinter September 27, 2016

")

2 Motivation and aims Density of the residuals from a recursive VAR(13) (1960m1-2015m6)

3 Motivation and aims Describe a BVAR model that features non-normal disturbances The non-normality is introduced in the model through a finite mixture of normals Consider if this specification can improve point and density forecasting performance Application to yield curve forecasting.

4 Related papers Closely related to Chiu et al. (2014). Kalliovirta et al. (2016) explore a similar model in a frequentist setting. Related to multivariate STAR model of Dueker et al. (2011). Non-normality explored in Curdia et al. (2013) for DSGE models. Villani et al. (2009) describe regression models with Gaussian mixtures. Econometric background in Koop (2003), Geweke (2005). Canova (1993), Sims (1992) explore the causes/implications of non-normality.

5 BVAR model with Non-normal disturbances The BVAR model is defined as follows y t = B 1 y t B p y t p + u t t = 1,..., T. (1) The covariance matrix of the residuals is defined as cov(u t ) = Σ = A 1 HA 1 (2) The orthogonalised residuals are given by e t = Au t

6 BVAR model with Non-normal disturbances The shock to the ith equation is assumed to follow: e it = α i,sit + σ i,sit ε it, ε it N(0, 1) (3) where S it = 1, 2,...M denotes the unobserved components or regimes. The formulation in equation 3, describes a mixture of M distributions where each component is N ( α i, σ 2 ) i. The state variable S determines the component that is active at a particular point in time. The law of motion for S it is chosen to be first order Markov process with transition probabilities P i (S i,t = J S i,t 1 = I ) = p i,ij (4) p i,ij can depend on a vector of unobserved variables P i (S i,t = J S i,t 1 = I ) = p i,ij (z t )

7 BVAR model with Non-normal disturbances The orthogonal shocks are described by a finite mixture of normals. If α i,sit are the same across components, the distribution is symmmetric but can have fat tails If α i,sit vary, the distribution can be skewed and have a kurtosis less than 3.

8 BVAR model with Non-normal disturbances The VAR model proposed above can also be interpreted as a Markov Switching VAR model (see Hamilton (1994)). ( Yt X t ( e1t e 2t ) ) = = ( ) ( b11 b 12 Yt 1 b 21 b 22 X t 1 ( ) ( ) 1 0 u1t A 21 1 ) ( u1t + u 2t where e 1t = α 1,S1t + σ 1,S1t ε 1t and e 2t = α 2,S2t + σ 2,S2t ε 2t u 2t ) (5) (6)

9 BVAR model with Non-normal disturbances Combining ( ) these equations we get: Yt = X t ( ) ( ) ( ) 1 ( b11 b 12 Yt α1,s1t + b 21 b 22 X t 1 A 21 1 α 2,S2t ( ) 1 ( ) ( ) 1 0 σ1,s1t 0 ε1t A σ 2,S2t ε ( ) 2t α Intercepts: 1,S1t α 2,S2t A 21 α ( 1,S1t σ 2 Covariance: 1,S 1t A 21 σ 2 ) 1,S 1t A 21 σ 2 1,S 1t σ 2 1,S t A σ2 2,S 2t ) + n different Markov chains govern the regime switches of the reduced form

10 Estimation We adopt a Bayesian approach to estimation. This has two advantages The marginal likelihood can be used to select the number of components A small extension of the MCMC algorithm provides the predictive density.

11 Estimation Given B,A the model can be written as e it = α i,sit + σ i,sit ε it Given S it, this is sequence of linear regressions and the draws from the conditional posterior of α and σ 2 are standard. Impose α i,sit =1 < α i,sit =2 <... < α i,sit =M Given α and σ 2, S it can be drawn using the Hamilton filter and the backward recursion described in Kim and Nelson (1999) and transition probabilities from the Dirichlet distribution. Given α and σ, the remaining parameters involve VARs, regressions with heteroscedasticity and standard methods apply after a GLS transformation

12 Model Selection We carry out model selection by comparing the marginal likelihood across models with a different number of components. The marginal likelihood is defined as: f (ỹ) = f (ỹ Ξ) p (Ξ) dξ (7) where ỹ = [y 1, y 2,.., y T ], Ξ denotes the unknown parameters of the model, f (ỹ Ξ) is the likelihood and p (Ξ) is the proper prior distribution. As is well known, the integration problem in equation 7 is non-trivial and several numerical methods have been proposed for this We use two methods Gelfand and Dey (1994) estimator and the bridge estimator Meng and Wong (1996) We also consider AIC, BIC and DIC.

13 Estimation on Artificial data The paper presents a Monte-Carlo experiment which shows some evidence that: 1. The MCMC algorithm displays a reasonable performance 2. ML estimators select the correct model almost 100% of the time 3. AIC and SIC perform well, but DIC tends to select the more complex model.

14 Empirical Application: Modelling and Forecasting the yield curve The Yield curve and the economy are closely related and thus it is interesting to forecast yields ( Diebold et al. (2006)) Note, however, that some recent papers have pointed out that the dynamics of the yield curve are subject to structural shifts. (For example, Mumtaz and Surico (2009) and Bianchi et al. (2009)) In addition, it is well known that yields at longer maturities have been trending downwards in recent years (i.e. Greenspan s conundrum ).

15 Empirical Application: Modelling and Forecasting the yield curve Following Diebold and Li (2006) we use the Nelson and Siegel (1987) specification. Letting y t (τ) denote zero coupon government bond yields at maturity τ, the Nelson and Siegel (1987) model is defined as: ( 1 e λ t ) ( τ 1 e λ t τ y t (τ) = β 1t + β 2t + β λ t τ 3t λ t τ where λ t controls the exponential decay rate. The level, slope and the curvature of the yield curve are captured by β 1t, β 2t and β 3t, respectively which can be estimated via OLS. ) e λ t τ (8)

16 Empirical Application: Modelling and Forecasting the yield curve The dynamics of the factors can be modelled as a VAR process which is used in Diebold and Li (2006) to produce out of sample forecasts. In this section, we compare this VAR specification with the following extended model: Z t = L B l Z t l + u t l=1 where Z t = {β 1t, β 2t, β 3t } and e t = Au t. The orthogonal shock to the ith equation of the VAR is a Markov mixture of normals: e it = α i,sit + σ i,sit ε it, ε it N(0, 1) (9)

17 Empirical Application: Modelling and Forecasting the yield curve ML suggests a model with 2 components

18 Empirical Application: Modelling and Forecasting the yield curve

19 Empirical Application: Modelling and Forecasting the yield curve

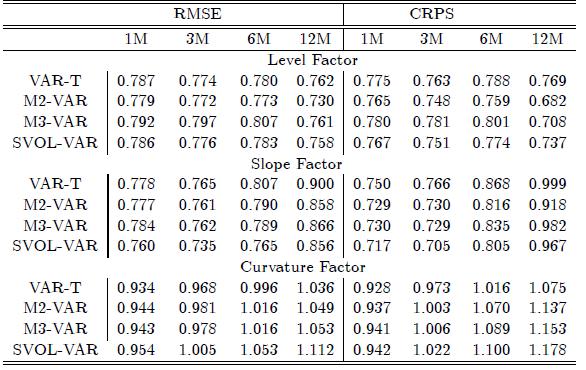

20 Forecasting performance Estimate up to December Then each model is estimated recursively adding one month of data at a time until January At each recursion, we produce a 12 month density forecast for the three factors from 1. Proposed model with 2 and 3 components (M2-VAR and M3-VAR) 2. A BVAR with T errors 3. A BVAR with SVOL We assess the point forecasts using root mean squared errors (RMSE) and the density forecasts using the continuous rank probability score (CRPS) as it is less sensitive to outlier outcomes (see Gneiting and Raftery (2007)). We consider the performance over the full sample and over the

21 Forecasting performance Over the full sample, the performance of these models is very similar and deliver a gain of about 10% over the BVAR. The proposed model with two components delivers point and density forecasts for the level of the yield curve that are more accurate than those obtained from the competing models. Over the post-1990 forecast sample, the improvement in forecasting performance over the BVAR is substantially larger. The M2-VAR delivers RMSEs in forecasting the level factor which are more than 20% lower than those obtained from the BVAR model. The performance of the SVOl-VAR is similar at short horizons. The proposed model does better at the one year horizon.

22 Summary We introduce Non-Gaussian disturbances in a BVAR model and provide the Gibbs algorithm. Provide evidence of non-normality in shocks using a US BVAR model. The proposed model may be useful in forecasting variables over more tranquil periods Forecasting Macroeconomic variables Looking at a wider range of countries Asymmetric number of components

23 Appendix

24 Bianchi, Francesco, Haroon Mumtaz and Paolo Surico, 2009, The great moderation of the term structure of UK interest rates, Journal of Monetary Economics 56(6), Canova, Fabio, 1993, Modelling and forecasting exchange rates with a Bayesian time-varying coeffi cient model, Journal of Economic Dynamics and Control 17(1-2), Chiu, Ching-Wai (Jeremy), Haroon Mumtaz and Gabor Pinter, 2014, Fat-tails in VAR Models, Working Papers 714, Queen Mary University of London, School of Economics and Finance. Curdia, Vasco, Marco Del Negro and Daniel L. Greenwald, 2013, Rare shocks, Great Recessions, Technical report. Diebold, Francis X. and Canlin Li, 2006, Forecasting the term structure of government bond yields, Journal of Econometrics 130(2), Diebold, Francis X., Glenn D. Rudebusch and S. BoragËĞan Aruoba, 2006, The macroeconomy and the yield curve: a dynamic latent factor approach, Journal of Econometrics 131(1âĂŞ2),

25 Dueker, Michael, Zacharias Psaradakis, Martin Sola and Fabio Spagnolo, 2011, Multivariate contemporaneous-threshold autoregressive models, Journal of Econometrics 160(2), Gelfand, A. E. and D. K. Dey, 1994, Bayesian Model Choice: Asymptotics and Exact Calculations, Journal of the Royal Statistical Society. Series B (Methodological) 56(3), pp Geweke, John, 2005, Contemporary Bayesian Econometrics and Statistics, Wiley. Gneiting, Tilmann and Adrian E. Raftery, 2007, Strictly Proper Scoring Rules, Prediction, and Estimation, Journal of the American Statistical Association 102, Hamilton, James D., 1994, Time Series Analysis, 1 edition, Princeton University Press. Kalliovirta, Leena, Mika Meitz and Pentti Saikkonen, 2016, Gaussian mixture vector autoregression, Journal of Econometrics 192(2), Innovations in Multiple Time Series Analysis.

26 Kim, Chang Jin and Charles R Nelson, 1999, State-Space Models with Regime Switching, MIT Press. Koop, Gary, 2003, Bayesian Econometrics, Wiley. Meng, Xiao Li and Wing Hung Wong, 1996, Simulating ratios of normalizing constants via a simple identity: A theoretical exploration, Statistica Sinica pp Mumtaz, Haroon and Paolo Surico, 2009, Time-varying yield curve dynamics and monetary policy, Journal of Applied Econometrics 24(6), Nelson, C R. and A F Siegel, 1987, Parsimonious modeling of yield curves, The Journal of Business 60(4), Sims, Christopher, 1992, A Nine Variable Probabilistic Macroeconomic Forecasting Model, Cowles Foundation Discussion Papers 1034, Cowles Foundation for Research in Economics, Yale University. Villani, M., R. Kohn and P. Giordani, 2009, Regression density estimation using smooth adaptive Gaussian mixtures, Journal of Econometrics 153(2), cited By 29.

Research Division Federal Reserve Bank of St. Louis Working Paper Series

Research Division Federal Reserve Bank of St Louis Working Paper Series Kalman Filtering with Truncated Normal State Variables for Bayesian Estimation of Macroeconomic Models Michael Dueker Working Paper

Research Division Federal Reserve Bank of St Louis Working Paper Series Kalman Filtering with Truncated Normal State Variables for Bayesian Estimation of Macroeconomic Models Michael Dueker Working Paper

Vector Autoregressive Model. Vector Autoregressions II. Estimation of Vector Autoregressions II. Estimation of Vector Autoregressions I.

Vector Autoregressive Model Vector Autoregressions II Empirical Macroeconomics - Lect 2 Dr. Ana Beatriz Galvao Queen Mary University of London January 2012 A VAR(p) model of the m 1 vector of time series

Vector Autoregressive Model Vector Autoregressions II Empirical Macroeconomics - Lect 2 Dr. Ana Beatriz Galvao Queen Mary University of London January 2012 A VAR(p) model of the m 1 vector of time series

A Gaussian mixture autoregressive model for univariate time series

A Gaussian mixture autoregressive model for univariate time series Leena Kalliovirta University of Helsinki Mika Meitz Koç University Pentti Saikkonen University of Helsinki August 14, 2012 Abstract This

A Gaussian mixture autoregressive model for univariate time series Leena Kalliovirta University of Helsinki Mika Meitz Koç University Pentti Saikkonen University of Helsinki August 14, 2012 Abstract This

Switching Regime Estimation

Switching Regime Estimation Series de Tiempo BIrkbeck March 2013 Martin Sola (FE) Markov Switching models 01/13 1 / 52 The economy (the time series) often behaves very different in periods such as booms

Switching Regime Estimation Series de Tiempo BIrkbeck March 2013 Martin Sola (FE) Markov Switching models 01/13 1 / 52 The economy (the time series) often behaves very different in periods such as booms

Are Policy Counterfactuals Based on Structural VARs Reliable?

Are Policy Counterfactuals Based on Structural VARs Reliable? Luca Benati European Central Bank 2nd International Conference in Memory of Carlo Giannini 20 January 2010 The views expressed herein are personal,

Are Policy Counterfactuals Based on Structural VARs Reliable? Luca Benati European Central Bank 2nd International Conference in Memory of Carlo Giannini 20 January 2010 The views expressed herein are personal,

Point, Interval, and Density Forecast Evaluation of Linear versus Nonlinear DSGE Models

Point, Interval, and Density Forecast Evaluation of Linear versus Nonlinear DSGE Models Francis X. Diebold Frank Schorfheide Minchul Shin University of Pennsylvania May 4, 2014 1 / 33 Motivation The use

Point, Interval, and Density Forecast Evaluation of Linear versus Nonlinear DSGE Models Francis X. Diebold Frank Schorfheide Minchul Shin University of Pennsylvania May 4, 2014 1 / 33 Motivation The use

Time-Varying Vector Autoregressive Models with Structural Dynamic Factors

Time-Varying Vector Autoregressive Models with Structural Dynamic Factors Paolo Gorgi, Siem Jan Koopman, Julia Schaumburg http://sjkoopman.net Vrije Universiteit Amsterdam School of Business and Economics

Time-Varying Vector Autoregressive Models with Structural Dynamic Factors Paolo Gorgi, Siem Jan Koopman, Julia Schaumburg http://sjkoopman.net Vrije Universiteit Amsterdam School of Business and Economics

Dynamic Factor Models and Factor Augmented Vector Autoregressions. Lawrence J. Christiano

Dynamic Factor Models and Factor Augmented Vector Autoregressions Lawrence J Christiano Dynamic Factor Models and Factor Augmented Vector Autoregressions Problem: the time series dimension of data is relatively

Dynamic Factor Models and Factor Augmented Vector Autoregressions Lawrence J Christiano Dynamic Factor Models and Factor Augmented Vector Autoregressions Problem: the time series dimension of data is relatively

A Gaussian mixture autoregressive model for univariate time series

ömmföäflsäafaäsflassflassflas ffffffffffffffffffffffffffffffffff Discussion Papers A Gaussian mixture autoregressive model for univariate time series Leena Kalliovirta University of Helsinki Mika Meitz

ömmföäflsäafaäsflassflassflas ffffffffffffffffffffffffffffffffff Discussion Papers A Gaussian mixture autoregressive model for univariate time series Leena Kalliovirta University of Helsinki Mika Meitz

Assessing Structural Convergence between Romanian Economy and Euro Area: A Bayesian Approach

Vol. 3, No.3, July 2013, pp. 372 383 ISSN: 2225-8329 2013 HRMARS www.hrmars.com Assessing Structural Convergence between Romanian Economy and Euro Area: A Bayesian Approach Alexie ALUPOAIEI 1 Ana-Maria

Vol. 3, No.3, July 2013, pp. 372 383 ISSN: 2225-8329 2013 HRMARS www.hrmars.com Assessing Structural Convergence between Romanian Economy and Euro Area: A Bayesian Approach Alexie ALUPOAIEI 1 Ana-Maria

doi /j. issn % % JOURNAL OF CHONGQING UNIVERSITY Social Science Edition Vol. 22 No.

doi1. 11835 /j. issn. 18-5831. 216. 1. 6 216 22 1 JOURNAL OF CHONGQING UNIVERSITYSocial Science EditionVol. 22 No. 1 216. J. 2161 5-57. Citation FormatJIN Chengxiao LU Yingchao. The decomposition of Chinese

doi1. 11835 /j. issn. 18-5831. 216. 1. 6 216 22 1 JOURNAL OF CHONGQING UNIVERSITYSocial Science EditionVol. 22 No. 1 216. J. 2161 5-57. Citation FormatJIN Chengxiao LU Yingchao. The decomposition of Chinese

Warwick Business School Forecasting System. Summary. Ana Galvao, Anthony Garratt and James Mitchell November, 2014

Warwick Business School Forecasting System Summary Ana Galvao, Anthony Garratt and James Mitchell November, 21 The main objective of the Warwick Business School Forecasting System is to provide competitive

Warwick Business School Forecasting System Summary Ana Galvao, Anthony Garratt and James Mitchell November, 21 The main objective of the Warwick Business School Forecasting System is to provide competitive

A quasi-bayesian nonparametric approach to time varying parameter VAR models Job Market Paper

A quasi-bayesian nonparametric approach to time varying parameter VAR models Job Market Paper Katerina Petrova December 9, 2015 Abstract The paper establishes a quasi-bayesian local likelihood (QBLL) estimation

A quasi-bayesian nonparametric approach to time varying parameter VAR models Job Market Paper Katerina Petrova December 9, 2015 Abstract The paper establishes a quasi-bayesian local likelihood (QBLL) estimation

Monetary Policy Regimes and Economic Performance: The Historical Record,

Monetary Policy Regimes and Economic Performance: The Historical Record, 1979-2008 Luca Benati Charles Goodhart European Central Bank London School of Economics Conference on: Key developments in monetary

Monetary Policy Regimes and Economic Performance: The Historical Record, 1979-2008 Luca Benati Charles Goodhart European Central Bank London School of Economics Conference on: Key developments in monetary

Evaluating FAVAR with Time-Varying Parameters and Stochastic Volatility

Evaluating FAVAR with Time-Varying Parameters and Stochastic Volatility Taiki Yamamura Queen Mary University of London September 217 Abstract This paper investigates the performance of FAVAR (Factor Augmented

Evaluating FAVAR with Time-Varying Parameters and Stochastic Volatility Taiki Yamamura Queen Mary University of London September 217 Abstract This paper investigates the performance of FAVAR (Factor Augmented

Dynamics of Real GDP Per Capita Growth

Dynamics of Real GDP Per Capita Growth Daniel Neuhoff Humboldt-Universität zu Berlin CRC 649 June 2015 Introduction Research question: Do the dynamics of the univariate time series of per capita GDP differ

Dynamics of Real GDP Per Capita Growth Daniel Neuhoff Humboldt-Universität zu Berlin CRC 649 June 2015 Introduction Research question: Do the dynamics of the univariate time series of per capita GDP differ

New Information Response Functions

New Information Response Functions Caroline JARDET (1) Banque de France Alain MONFORT (2) CNAM, CREST and Banque de France Fulvio PEGORARO (3) Banque de France and CREST First version : February, 2009.

New Information Response Functions Caroline JARDET (1) Banque de France Alain MONFORT (2) CNAM, CREST and Banque de France Fulvio PEGORARO (3) Banque de France and CREST First version : February, 2009.

Working Paper Series

Discussion of Cogley and Sargent s Drifts and Volatilities: Monetary Policy and Outcomes in the Post WWII U.S. Marco Del Negro Working Paper 23-26 October 23 Working Paper Series Federal Reserve Bank of

Discussion of Cogley and Sargent s Drifts and Volatilities: Monetary Policy and Outcomes in the Post WWII U.S. Marco Del Negro Working Paper 23-26 October 23 Working Paper Series Federal Reserve Bank of

Regime-Switching Cointegration

Regime-Switching Cointegration Markus Jochmann Newcastle University Rimini Centre for Economic Analysis Gary Koop University of Strathclyde Rimini Centre for Economic Analysis May 2011 Abstract We develop

Regime-Switching Cointegration Markus Jochmann Newcastle University Rimini Centre for Economic Analysis Gary Koop University of Strathclyde Rimini Centre for Economic Analysis May 2011 Abstract We develop

Forecasting the term structure interest rate of government bond yields

Forecasting the term structure interest rate of government bond yields Bachelor Thesis Econometrics & Operational Research Joost van Esch (419617) Erasmus School of Economics, Erasmus University Rotterdam

Forecasting the term structure interest rate of government bond yields Bachelor Thesis Econometrics & Operational Research Joost van Esch (419617) Erasmus School of Economics, Erasmus University Rotterdam

Online appendix to On the stability of the excess sensitivity of aggregate consumption growth in the US

Online appendix to On the stability of the excess sensitivity of aggregate consumption growth in the US Gerdie Everaert 1, Lorenzo Pozzi 2, and Ruben Schoonackers 3 1 Ghent University & SHERPPA 2 Erasmus

Online appendix to On the stability of the excess sensitivity of aggregate consumption growth in the US Gerdie Everaert 1, Lorenzo Pozzi 2, and Ruben Schoonackers 3 1 Ghent University & SHERPPA 2 Erasmus

Gaussian Mixture Approximations of Impulse Responses and the Non-Linear Effects of Monetary Shocks

Gaussian Mixture Approximations of Impulse Responses and the Non-Linear Effects of Monetary Shocks Regis Barnichon (CREI, Universitat Pompeu Fabra) Christian Matthes (Richmond Fed) Effects of monetary

Gaussian Mixture Approximations of Impulse Responses and the Non-Linear Effects of Monetary Shocks Regis Barnichon (CREI, Universitat Pompeu Fabra) Christian Matthes (Richmond Fed) Effects of monetary

Labor-Supply Shifts and Economic Fluctuations. Technical Appendix

Labor-Supply Shifts and Economic Fluctuations Technical Appendix Yongsung Chang Department of Economics University of Pennsylvania Frank Schorfheide Department of Economics University of Pennsylvania January

Labor-Supply Shifts and Economic Fluctuations Technical Appendix Yongsung Chang Department of Economics University of Pennsylvania Frank Schorfheide Department of Economics University of Pennsylvania January

Bayesian Semiparametric GARCH Models

Bayesian Semiparametric GARCH Models Xibin (Bill) Zhang and Maxwell L. King Department of Econometrics and Business Statistics Faculty of Business and Economics xibin.zhang@monash.edu Quantitative Methods

Bayesian Semiparametric GARCH Models Xibin (Bill) Zhang and Maxwell L. King Department of Econometrics and Business Statistics Faculty of Business and Economics xibin.zhang@monash.edu Quantitative Methods

Timevarying VARs. Wouter J. Den Haan London School of Economics. c Wouter J. Den Haan

Timevarying VARs Wouter J. Den Haan London School of Economics c Wouter J. Den Haan Time-Varying VARs Gibbs-Sampler general idea probit regression application (Inverted Wishart distribution Drawing from

Timevarying VARs Wouter J. Den Haan London School of Economics c Wouter J. Den Haan Time-Varying VARs Gibbs-Sampler general idea probit regression application (Inverted Wishart distribution Drawing from

Vector Auto-Regressive Models

Vector Auto-Regressive Models Laurent Ferrara 1 1 University of Paris Nanterre M2 Oct. 2018 Overview of the presentation 1. Vector Auto-Regressions Definition Estimation Testing 2. Impulse responses functions

Vector Auto-Regressive Models Laurent Ferrara 1 1 University of Paris Nanterre M2 Oct. 2018 Overview of the presentation 1. Vector Auto-Regressions Definition Estimation Testing 2. Impulse responses functions

VAR Models and Applications

VAR Models and Applications Laurent Ferrara 1 1 University of Paris West M2 EIPMC Oct. 2016 Overview of the presentation 1. Vector Auto-Regressions Definition Estimation Testing 2. Impulse responses functions

VAR Models and Applications Laurent Ferrara 1 1 University of Paris West M2 EIPMC Oct. 2016 Overview of the presentation 1. Vector Auto-Regressions Definition Estimation Testing 2. Impulse responses functions

Functional-Coefficient Dynamic Nelson-Siegel Model

Functional-Coefficient Dynamic Nelson-Siegel Model Yuan Yang March 12, 2014 Abstract I propose an Functional-coefficient Dynamic Nelson-Siegel (FDNS) model to forecast the yield curve. The model fits each

Functional-Coefficient Dynamic Nelson-Siegel Model Yuan Yang March 12, 2014 Abstract I propose an Functional-coefficient Dynamic Nelson-Siegel (FDNS) model to forecast the yield curve. The model fits each

Web Appendix for The Dynamics of Reciprocity, Accountability, and Credibility

Web Appendix for The Dynamics of Reciprocity, Accountability, and Credibility Patrick T. Brandt School of Economic, Political and Policy Sciences University of Texas at Dallas E-mail: pbrandt@utdallas.edu

Web Appendix for The Dynamics of Reciprocity, Accountability, and Credibility Patrick T. Brandt School of Economic, Political and Policy Sciences University of Texas at Dallas E-mail: pbrandt@utdallas.edu

The Effects of Monetary Policy on Stock Market Bubbles: Some Evidence

The Effects of Monetary Policy on Stock Market Bubbles: Some Evidence Jordi Gali Luca Gambetti ONLINE APPENDIX The appendix describes the estimation of the time-varying coefficients VAR model. The model

The Effects of Monetary Policy on Stock Market Bubbles: Some Evidence Jordi Gali Luca Gambetti ONLINE APPENDIX The appendix describes the estimation of the time-varying coefficients VAR model. The model

Multivariate Markov Switching With Weighted Regime Determination: Giving France More Weight than Finland

Multivariate Markov Switching With Weighted Regime Determination: Giving France More Weight than Finland November 2006 Michael Dueker Federal Reserve Bank of St. Louis P.O. Box 442, St. Louis, MO 63166

Multivariate Markov Switching With Weighted Regime Determination: Giving France More Weight than Finland November 2006 Michael Dueker Federal Reserve Bank of St. Louis P.O. Box 442, St. Louis, MO 63166

International Symposium on Mathematical Sciences & Computing Research (ismsc) 2015 (ismsc 15)

2015 (ismsc 15)") Model Performance Between Linear Vector Autoregressive and Markov Switching Vector Autoregressive Models on Modelling Structural Change in Time Series Data Phoong Seuk Wai Department of Economics Facultyof

Model Performance Between Linear Vector Autoregressive and Markov Switching Vector Autoregressive Models on Modelling Structural Change in Time Series Data Phoong Seuk Wai Department of Economics Facultyof

State-space Model. Eduardo Rossi University of Pavia. November Rossi State-space Model Fin. Econometrics / 53

State-space Model Eduardo Rossi University of Pavia November 2014 Rossi State-space Model Fin. Econometrics - 2014 1 / 53 Outline 1 Motivation 2 Introduction 3 The Kalman filter 4 Forecast errors 5 State

State-space Model Eduardo Rossi University of Pavia November 2014 Rossi State-space Model Fin. Econometrics - 2014 1 / 53 Outline 1 Motivation 2 Introduction 3 The Kalman filter 4 Forecast errors 5 State

Modeling conditional distributions with mixture models: Theory and Inference

Modeling conditional distributions with mixture models: Theory and Inference John Geweke University of Iowa, USA Journal of Applied Econometrics Invited Lecture Università di Venezia Italia June 2, 2005

Modeling conditional distributions with mixture models: Theory and Inference John Geweke University of Iowa, USA Journal of Applied Econometrics Invited Lecture Università di Venezia Italia June 2, 2005

Do Markov-Switching Models Capture Nonlinearities in the Data? Tests using Nonparametric Methods

Do Markov-Switching Models Capture Nonlinearities in the Data? Tests using Nonparametric Methods Robert V. Breunig Centre for Economic Policy Research, Research School of Social Sciences and School of

Do Markov-Switching Models Capture Nonlinearities in the Data? Tests using Nonparametric Methods Robert V. Breunig Centre for Economic Policy Research, Research School of Social Sciences and School of

Bayesian Semiparametric GARCH Models

Bayesian Semiparametric GARCH Models Xibin (Bill) Zhang and Maxwell L. King Department of Econometrics and Business Statistics Faculty of Business and Economics xibin.zhang@monash.edu Quantitative Methods

Bayesian Semiparametric GARCH Models Xibin (Bill) Zhang and Maxwell L. King Department of Econometrics and Business Statistics Faculty of Business and Economics xibin.zhang@monash.edu Quantitative Methods

Inference in VARs with Conditional Heteroskedasticity of Unknown Form

Inference in VARs with Conditional Heteroskedasticity of Unknown Form Ralf Brüggemann a Carsten Jentsch b Carsten Trenkler c University of Konstanz University of Mannheim University of Mannheim IAB Nuremberg

Inference in VARs with Conditional Heteroskedasticity of Unknown Form Ralf Brüggemann a Carsten Jentsch b Carsten Trenkler c University of Konstanz University of Mannheim University of Mannheim IAB Nuremberg

Identifying Aggregate Liquidity Shocks with Monetary Policy Shocks: An Application using UK Data

Identifying Aggregate Liquidity Shocks with Monetary Policy Shocks: An Application using UK Data Michael Ellington and Costas Milas Financial Services, Liquidity and Economic Activity Bank of England May

Identifying Aggregate Liquidity Shocks with Monetary Policy Shocks: An Application using UK Data Michael Ellington and Costas Milas Financial Services, Liquidity and Economic Activity Bank of England May

What is different this time? Investigating the declines of the U.S. real GDP during the Great Recession

What is different this time? Investigating the declines of the U.S. real GDP during the Great Recession Yu-Fan Huang Sui Luo International School of Economics and Management Capital University of Economics

What is different this time? Investigating the declines of the U.S. real GDP during the Great Recession Yu-Fan Huang Sui Luo International School of Economics and Management Capital University of Economics

A Comparison of Business Cycle Regime Nowcasting Performance between Real-time and Revised Data. By Arabinda Basistha (West Virginia University)

") A Comparison of Business Cycle Regime Nowcasting Performance between Real-time and Revised Data By Arabinda Basistha (West Virginia University) This version: 2.7.8 Markov-switching models used for nowcasting

A Comparison of Business Cycle Regime Nowcasting Performance between Real-time and Revised Data By Arabinda Basistha (West Virginia University) This version: 2.7.8 Markov-switching models used for nowcasting

BEAR 4.2. Introducing Stochastic Volatility, Time Varying Parameters and Time Varying Trends. A. Dieppe R. Legrand B. van Roye ECB.

BEAR 4.2 Introducing Stochastic Volatility, Time Varying Parameters and Time Varying Trends A. Dieppe R. Legrand B. van Roye ECB 25 June 2018 The views expressed in this presentation are the authors and

BEAR 4.2 Introducing Stochastic Volatility, Time Varying Parameters and Time Varying Trends A. Dieppe R. Legrand B. van Roye ECB 25 June 2018 The views expressed in this presentation are the authors and

Stargazing with Structural VARs: Shock Identification via Independent Component Analysis

Stargazing with Structural VARs: Shock Identification via Independent Component Analysis Dmitry Kulikov and Aleksei Netšunajev Eesti Pank Estonia pst. 13 19 Tallinn Estonia phone: +372 668777 e-mail: dmitry.kulikov@eestipank.ee

Stargazing with Structural VARs: Shock Identification via Independent Component Analysis Dmitry Kulikov and Aleksei Netšunajev Eesti Pank Estonia pst. 13 19 Tallinn Estonia phone: +372 668777 e-mail: dmitry.kulikov@eestipank.ee

Financial Econometrics

Financial Econometrics Nonlinear time series analysis Gerald P. Dwyer Trinity College, Dublin January 2016 Outline 1 Nonlinearity Does nonlinearity matter? Nonlinear models Tests for nonlinearity Forecasting

Financial Econometrics Nonlinear time series analysis Gerald P. Dwyer Trinity College, Dublin January 2016 Outline 1 Nonlinearity Does nonlinearity matter? Nonlinear models Tests for nonlinearity Forecasting

Signaling Effects of Monetary Policy

Signaling Effects of Monetary Policy Leonardo Melosi London Business School 24 May 2012 Motivation Disperse information about aggregate fundamentals Morris and Shin (2003), Sims (2003), and Woodford (2002)

Signaling Effects of Monetary Policy Leonardo Melosi London Business School 24 May 2012 Motivation Disperse information about aggregate fundamentals Morris and Shin (2003), Sims (2003), and Woodford (2002)

Business Cycle Comovements in Industrial Subsectors

Business Cycle Comovements in Industrial Subsectors Michael T. Owyang 1 Daniel Soques 2 1 Federal Reserve Bank of St. Louis 2 University of North Carolina Wilmington The views expressed here are those

Business Cycle Comovements in Industrial Subsectors Michael T. Owyang 1 Daniel Soques 2 1 Federal Reserve Bank of St. Louis 2 University of North Carolina Wilmington The views expressed here are those

Unobserved. Components and. Time Series. Econometrics. Edited by. Siem Jan Koopman. and Neil Shephard OXFORD UNIVERSITY PRESS

Unobserved Components and Time Series Econometrics Edited by Siem Jan Koopman and Neil Shephard OXFORD UNIVERSITY PRESS CONTENTS LIST OF FIGURES LIST OF TABLES ix XV 1 Introduction 1 Siem Jan Koopman and

Unobserved Components and Time Series Econometrics Edited by Siem Jan Koopman and Neil Shephard OXFORD UNIVERSITY PRESS CONTENTS LIST OF FIGURES LIST OF TABLES ix XV 1 Introduction 1 Siem Jan Koopman and

Research Division Federal Reserve Bank of St. Louis Working Paper Series

Research Division Federal Reserve Bank of St. Louis Working Paper Series A Time-Varying Threshold STAR Model of Unemployment and the Natural Rate Michael Dueker Michael T. Owyang and Martin Sola Working

Research Division Federal Reserve Bank of St. Louis Working Paper Series A Time-Varying Threshold STAR Model of Unemployment and the Natural Rate Michael Dueker Michael T. Owyang and Martin Sola Working

Bayesian modelling of real GDP rate in Romania

Bayesian modelling of real GDP rate in Romania Mihaela SIMIONESCU 1* 1 Romanian Academy, Institute for Economic Forecasting, Bucharest, Calea 13 Septembrie, no. 13, District 5, Bucharest 1 Abstract The

Bayesian modelling of real GDP rate in Romania Mihaela SIMIONESCU 1* 1 Romanian Academy, Institute for Economic Forecasting, Bucharest, Calea 13 Septembrie, no. 13, District 5, Bucharest 1 Abstract The

Why Has the U.S. Economy Stagnated Since the Great Recession?

Why Has the U.S. Economy Stagnated Since the Great Recession? Yunjong Eo, University of Sydney joint work with James Morley, University of Sydney Workshop on Nonlinear Models at the Norges Bank January

Why Has the U.S. Economy Stagnated Since the Great Recession? Yunjong Eo, University of Sydney joint work with James Morley, University of Sydney Workshop on Nonlinear Models at the Norges Bank January

Stock index returns density prediction using GARCH models: Frequentist or Bayesian estimation?

MPRA Munich Personal RePEc Archive Stock index returns density prediction using GARCH models: Frequentist or Bayesian estimation? Ardia, David; Lennart, Hoogerheide and Nienke, Corré aeris CAPITAL AG,

MPRA Munich Personal RePEc Archive Stock index returns density prediction using GARCH models: Frequentist or Bayesian estimation? Ardia, David; Lennart, Hoogerheide and Nienke, Corré aeris CAPITAL AG,

A Bayesian Approach to Testing for Markov Switching in Univariate and Dynamic Factor Models

A Bayesian Approach to Testing for Markov Switching in Univariate and Dynamic Factor Models by Chang-Jin Kim Korea University and Charles R. Nelson University of Washington August 25, 1998 Kim: Dept. of

A Bayesian Approach to Testing for Markov Switching in Univariate and Dynamic Factor Models by Chang-Jin Kim Korea University and Charles R. Nelson University of Washington August 25, 1998 Kim: Dept. of

Estimating VAR s Sampled at Mixed or Irregular Spaced Frequencies: A Bayesian Approach

Estimating VAR s Sampled at Mixed or Irregular Spaced Frequencies: A Bayesian Approach Ching Wai (Jeremy) Chiu, Bjørn Eraker, Andrew T. Foerster, Tae Bong Kim and Hernán D. Seoane December 211 RWP 11-11

Estimating VAR s Sampled at Mixed or Irregular Spaced Frequencies: A Bayesian Approach Ching Wai (Jeremy) Chiu, Bjørn Eraker, Andrew T. Foerster, Tae Bong Kim and Hernán D. Seoane December 211 RWP 11-11

University of Kent Department of Economics Discussion Papers

University of Kent Department of Economics Discussion Papers Testing for Granger (non-) Causality in a Time Varying Coefficient VAR Model Dimitris K. Christopoulos and Miguel León-Ledesma January 28 KDPE

University of Kent Department of Economics Discussion Papers Testing for Granger (non-) Causality in a Time Varying Coefficient VAR Model Dimitris K. Christopoulos and Miguel León-Ledesma January 28 KDPE

Are recoveries all the same?

Are recoveries all the same? Yu-Fan Huang, Sui Luo, and Richard Startz November 2015 Abstract Recessions and subsequent recoveries are frequently classified as L-shaped or U-shaped, with output losses

Are recoveries all the same? Yu-Fan Huang, Sui Luo, and Richard Startz November 2015 Abstract Recessions and subsequent recoveries are frequently classified as L-shaped or U-shaped, with output losses

Alina Barnett (1) Haroon Mumtaz (2) Konstantinos Theodoridis (3) Abstract

Haroon Mumtaz (2) Konstantinos Theodoridis (3) Abstract") Working Paper No.? Forecasting UK GDP growth, inflation and interest rates under structural change: a comparison of models with time-varying parameters Alina Barnett (1 Haroon Mumtaz (2 Konstantinos Theodoridis

Working Paper No.? Forecasting UK GDP growth, inflation and interest rates under structural change: a comparison of models with time-varying parameters Alina Barnett (1 Haroon Mumtaz (2 Konstantinos Theodoridis

Non-Markovian Regime Switching with Endogenous States and Time-Varying State Strengths

Non-Markovian Regime Switching with Endogenous States and Time-Varying State Strengths January 2004 Siddhartha Chib Olin School of Business Washington University chib@olin.wustl.edu Michael Dueker Federal

Non-Markovian Regime Switching with Endogenous States and Time-Varying State Strengths January 2004 Siddhartha Chib Olin School of Business Washington University chib@olin.wustl.edu Michael Dueker Federal

BUSINESS CYCLE ANALYSIS WITH MULTIVARIATE MARKOV SWITCHING MODELS

BUSINESS CYCLE ANALYSIS WITH MULTIVARIATE MARKOV SWITCHING MODELS Jacques Anas*, Monica Billio**, Laurent Ferrara* and Marco Lo Duca*** *Centre d Observation Economique, 27 Avenue de Friedland, 75382 Paris

BUSINESS CYCLE ANALYSIS WITH MULTIVARIATE MARKOV SWITCHING MODELS Jacques Anas*, Monica Billio**, Laurent Ferrara* and Marco Lo Duca*** *Centre d Observation Economique, 27 Avenue de Friedland, 75382 Paris

Structural Vector Autoregressions with Markov Switching. Markku Lanne University of Helsinki. Helmut Lütkepohl European University Institute, Florence

Structural Vector Autoregressions with Markov Switching Markku Lanne University of Helsinki Helmut Lütkepohl European University Institute, Florence Katarzyna Maciejowska European University Institute,

Structural Vector Autoregressions with Markov Switching Markku Lanne University of Helsinki Helmut Lütkepohl European University Institute, Florence Katarzyna Maciejowska European University Institute,

Predicting bond returns using the output gap in expansions and recessions

Erasmus university Rotterdam Erasmus school of economics Bachelor Thesis Quantitative finance Predicting bond returns using the output gap in expansions and recessions Author: Martijn Eertman Studentnumber:

Erasmus university Rotterdam Erasmus school of economics Bachelor Thesis Quantitative finance Predicting bond returns using the output gap in expansions and recessions Author: Martijn Eertman Studentnumber:

Estimating Unobservable Inflation Expectations in the New Keynesian Phillips Curve

econometrics Article Estimating Unobservable Inflation Expectations in the New Keynesian Phillips Curve Francesca Rondina ID Department of Economics, University of Ottawa, 120 University Private, Ottawa,

econometrics Article Estimating Unobservable Inflation Expectations in the New Keynesian Phillips Curve Francesca Rondina ID Department of Economics, University of Ottawa, 120 University Private, Ottawa,

A Time-Varying Threshold STAR Model of Unemployment

A Time-Varying Threshold STAR Model of Unemloyment michael dueker a michael owyang b martin sola c,d a Russell Investments b Federal Reserve Bank of St. Louis c Deartamento de Economia, Universidad Torcuato

A Time-Varying Threshold STAR Model of Unemloyment michael dueker a michael owyang b martin sola c,d a Russell Investments b Federal Reserve Bank of St. Louis c Deartamento de Economia, Universidad Torcuato

Regime-Switching Cointegration

Regime-Switching Cointegration Markus Jochmann Newcastle University Rimini Centre for Economic Analysis Gary Koop University of Strathclyde Rimini Centre for Economic Analysis July 2013 Abstract We develop

Regime-Switching Cointegration Markus Jochmann Newcastle University Rimini Centre for Economic Analysis Gary Koop University of Strathclyde Rimini Centre for Economic Analysis July 2013 Abstract We develop

Prediction of Term Structure with. Potentially Misspecified Macro-Finance Models. near the Zero Lower Bound

New ESRI Working Paper No.32 Prediction of Term Structure with Potentially Misspecified Macro-Finance Models near the Zero Lower Bound Tsz-Kin Chung, Hirokuni Iiboshi March 215 Economic and Social Research

New ESRI Working Paper No.32 Prediction of Term Structure with Potentially Misspecified Macro-Finance Models near the Zero Lower Bound Tsz-Kin Chung, Hirokuni Iiboshi March 215 Economic and Social Research

Interest Rate Uncertainty and Economic Fluctuations

Working Paper No. 14-32 Interest Rate Uncertainty and Economic Fluctuations Drew D. Creal University of Chicago Booth School of Business Jing Cynthia Wu University of Chicago Booth School of Business All

Working Paper No. 14-32 Interest Rate Uncertainty and Economic Fluctuations Drew D. Creal University of Chicago Booth School of Business Jing Cynthia Wu University of Chicago Booth School of Business All

TAKEHOME FINAL EXAM e iω e 2iω e iω e 2iω

ECO 513 Spring 2015 TAKEHOME FINAL EXAM (1) Suppose the univariate stochastic process y is ARMA(2,2) of the following form: y t = 1.6974y t 1.9604y t 2 + ε t 1.6628ε t 1 +.9216ε t 2, (1) where ε is i.i.d.

ECO 513 Spring 2015 TAKEHOME FINAL EXAM (1) Suppose the univariate stochastic process y is ARMA(2,2) of the following form: y t = 1.6974y t 1.9604y t 2 + ε t 1.6628ε t 1 +.9216ε t 2, (1) where ε is i.i.d.

U n iversity o f H ei delberg

U n iversity o f H ei delberg Department of Economics Discussion Paper Series No. 585 482482 Global Prediction of Recessions Jonas Dovern and Florian Huber March 2015 Global Prediction of Recessions Jonas

U n iversity o f H ei delberg Department of Economics Discussion Paper Series No. 585 482482 Global Prediction of Recessions Jonas Dovern and Florian Huber March 2015 Global Prediction of Recessions Jonas

Combining Macroeconomic Models for Prediction

Combining Macroeconomic Models for Prediction John Geweke University of Technology Sydney 15th Australasian Macro Workshop April 8, 2010 Outline 1 Optimal prediction pools 2 Models and data 3 Optimal pools

Combining Macroeconomic Models for Prediction John Geweke University of Technology Sydney 15th Australasian Macro Workshop April 8, 2010 Outline 1 Optimal prediction pools 2 Models and data 3 Optimal pools

Methods for Computing Marginal Data Densities from the Gibbs Output

Methods for Computing Marginal Data Densities from the Gibbs Output Cristina Fuentes-Albero Rutgers University Leonardo Melosi Federal Reserve Bank of Chicago January 2013 Abstract We introduce two estimators

Methods for Computing Marginal Data Densities from the Gibbs Output Cristina Fuentes-Albero Rutgers University Leonardo Melosi Federal Reserve Bank of Chicago January 2013 Abstract We introduce two estimators

Estimating Global Bank Network Connectedness

Estimating Global Bank Network Connectedness Mert Demirer (MIT) Francis X. Diebold (Penn) Laura Liu (Penn) Kamil Yılmaz (Koç) September 22, 2016 1 / 27 Financial and Macroeconomic Connectedness Market

Estimating Global Bank Network Connectedness Mert Demirer (MIT) Francis X. Diebold (Penn) Laura Liu (Penn) Kamil Yılmaz (Koç) September 22, 2016 1 / 27 Financial and Macroeconomic Connectedness Market

Markov Switching Regular Vine Copulas

Int. Statistical Inst.: Proc. 58th World Statistical Congress, 2011, Dublin (Session CPS057) p.5304 Markov Switching Regular Vine Copulas Stöber, Jakob and Czado, Claudia Lehrstuhl für Mathematische Statistik,

Int. Statistical Inst.: Proc. 58th World Statistical Congress, 2011, Dublin (Session CPS057) p.5304 Markov Switching Regular Vine Copulas Stöber, Jakob and Czado, Claudia Lehrstuhl für Mathematische Statistik,

The Bayesian Approach to Multi-equation Econometric Model Estimation

Journal of Statistical and Econometric Methods, vol.3, no.1, 2014, 85-96 ISSN: 2241-0384 (print), 2241-0376 (online) Scienpress Ltd, 2014 The Bayesian Approach to Multi-equation Econometric Model Estimation

Journal of Statistical and Econometric Methods, vol.3, no.1, 2014, 85-96 ISSN: 2241-0384 (print), 2241-0376 (online) Scienpress Ltd, 2014 The Bayesian Approach to Multi-equation Econometric Model Estimation

Modern Macroeconomics and Regional Economic Modeling

Modern Macroeconomics and Regional Economic Modeling by Dan S. Rickman Oklahoma State University prepared for presentation in the JRS 50 th Anniversary Symposium at the Federal Reserve Bank of New York

Modern Macroeconomics and Regional Economic Modeling by Dan S. Rickman Oklahoma State University prepared for presentation in the JRS 50 th Anniversary Symposium at the Federal Reserve Bank of New York

ECONOMICS 7200 MODERN TIME SERIES ANALYSIS Econometric Theory and Applications

ECONOMICS 7200 MODERN TIME SERIES ANALYSIS Econometric Theory and Applications Yongmiao Hong Department of Economics & Department of Statistical Sciences Cornell University Spring 2019 Time and uncertainty

ECONOMICS 7200 MODERN TIME SERIES ANALYSIS Econometric Theory and Applications Yongmiao Hong Department of Economics & Department of Statistical Sciences Cornell University Spring 2019 Time and uncertainty

Lecture 4: Bayesian VAR

s Lecture 4: Bayesian VAR Hedibert Freitas Lopes The University of Chicago Booth School of Business 5807 South Woodlawn Avenue, Chicago, IL 60637 http://faculty.chicagobooth.edu/hedibert.lopes hlopes@chicagobooth.edu

s Lecture 4: Bayesian VAR Hedibert Freitas Lopes The University of Chicago Booth School of Business 5807 South Woodlawn Avenue, Chicago, IL 60637 http://faculty.chicagobooth.edu/hedibert.lopes hlopes@chicagobooth.edu

Estimating VAR s Sampled at Mixed or Irregular Spaced Frequencies: A Bayesian Approach

Estimating VAR s Sampled at Mixed or Irregular Spaced Frequencies: A Bayesian Approach Ching Wai (Jeremy) Chiu, Bjørn Eraker, Andrew T. Foerster, Tae Bong Kim and Hernán D. Seoane December 211; Revised

Estimating VAR s Sampled at Mixed or Irregular Spaced Frequencies: A Bayesian Approach Ching Wai (Jeremy) Chiu, Bjørn Eraker, Andrew T. Foerster, Tae Bong Kim and Hernán D. Seoane December 211; Revised

DSGE Methods. Estimation of DSGE models: Maximum Likelihood & Bayesian. Willi Mutschler, M.Sc.

DSGE Methods Estimation of DSGE models: Maximum Likelihood & Bayesian Willi Mutschler, M.Sc. Institute of Econometrics and Economic Statistics University of Münster willi.mutschler@uni-muenster.de Summer

DSGE Methods Estimation of DSGE models: Maximum Likelihood & Bayesian Willi Mutschler, M.Sc. Institute of Econometrics and Economic Statistics University of Münster willi.mutschler@uni-muenster.de Summer

Constructing Turning Point Chronologies with Markov Switching Vector Autoregressive Models: the Euro Zone Business Cycle

Constructing Turning Point Chronologies with Markov Switching Vector Autoregressive Models: the Euro Zone Business Cycle Hans Martin Krolzig Department of Economics and Nuffield College, Oxford University.

Constructing Turning Point Chronologies with Markov Switching Vector Autoregressive Models: the Euro Zone Business Cycle Hans Martin Krolzig Department of Economics and Nuffield College, Oxford University.

Generalized Autoregressive Score Models

Generalized Autoregressive Score Models by: Drew Creal, Siem Jan Koopman, André Lucas To capture the dynamic behavior of univariate and multivariate time series processes, we can allow parameters to be

Generalized Autoregressive Score Models by: Drew Creal, Siem Jan Koopman, André Lucas To capture the dynamic behavior of univariate and multivariate time series processes, we can allow parameters to be

Non-nested model selection. in unstable environments

Non-nested model selection in unstable environments Raffaella Giacomini UCLA (with Barbara Rossi, Duke) Motivation The problem: select between two competing models, based on how well they fit thedata Both

Non-nested model selection in unstable environments Raffaella Giacomini UCLA (with Barbara Rossi, Duke) Motivation The problem: select between two competing models, based on how well they fit thedata Both

Factor models. March 13, 2017

Factor models March 13, 2017 Factor Models Macro economists have a peculiar data situation: Many data series, but usually short samples How can we utilize all this information without running into degrees

Factor models March 13, 2017 Factor Models Macro economists have a peculiar data situation: Many data series, but usually short samples How can we utilize all this information without running into degrees

Term Structure Surprises: The Predictive Content of Curvature, Level, and Slope

Term Structure Surprises: The Predictive Content of Curvature, Level, and Slope Emanuel Mönch Humboldt University Berlin COMMENTS WELCOME This draft: 5 July 26 Abstract This paper analyzes the predictive

Term Structure Surprises: The Predictive Content of Curvature, Level, and Slope Emanuel Mönch Humboldt University Berlin COMMENTS WELCOME This draft: 5 July 26 Abstract This paper analyzes the predictive

Gaussian kernel GARCH models

Gaussian kernel GARCH models Xibin (Bill) Zhang and Maxwell L. King Department of Econometrics and Business Statistics Faculty of Business and Economics 7 June 2013 Motivation A regression model is often

Gaussian kernel GARCH models Xibin (Bill) Zhang and Maxwell L. King Department of Econometrics and Business Statistics Faculty of Business and Economics 7 June 2013 Motivation A regression model is often

Oil Price Forecastability and Economic Uncertainty

Oil Price Forecastability and Economic Uncertainty Stelios Bekiros a,b Rangan Gupta a,cy Alessia Paccagnini dz a IPAG Business School, b European University Institute, c University of Pretoria, d University

Oil Price Forecastability and Economic Uncertainty Stelios Bekiros a,b Rangan Gupta a,cy Alessia Paccagnini dz a IPAG Business School, b European University Institute, c University of Pretoria, d University

Econometric Forecasting

Graham Elliott Econometric Forecasting Course Description We will review the theory of econometric forecasting with a view to understanding current research and methods. By econometric forecasting we mean

Graham Elliott Econometric Forecasting Course Description We will review the theory of econometric forecasting with a view to understanding current research and methods. By econometric forecasting we mean

The Kalman filter, Nonlinear filtering, and Markov Chain Monte Carlo

NBER Summer Institute Minicourse What s New in Econometrics: Time Series Lecture 5 July 5, 2008 The Kalman filter, Nonlinear filtering, and Markov Chain Monte Carlo Lecture 5, July 2, 2008 Outline. Models

NBER Summer Institute Minicourse What s New in Econometrics: Time Series Lecture 5 July 5, 2008 The Kalman filter, Nonlinear filtering, and Markov Chain Monte Carlo Lecture 5, July 2, 2008 Outline. Models

Statistical Inference and Methods

Department of Mathematics Imperial College London d.stephens@imperial.ac.uk http://stats.ma.ic.ac.uk/ das01/ 31st January 2006 Part VI Session 6: Filtering and Time to Event Data Session 6: Filtering and

Department of Mathematics Imperial College London d.stephens@imperial.ac.uk http://stats.ma.ic.ac.uk/ das01/ 31st January 2006 Part VI Session 6: Filtering and Time to Event Data Session 6: Filtering and

Katsuhiro Sugita Faculty of Law and Letters, University of the Ryukyus. Abstract

Bayesian analysis of a vector autoregressive model with multiple structural breaks Katsuhiro Sugita Faculty of Law and Letters, University of the Ryukyus Abstract This paper develops a Bayesian approach

Bayesian analysis of a vector autoregressive model with multiple structural breaks Katsuhiro Sugita Faculty of Law and Letters, University of the Ryukyus Abstract This paper develops a Bayesian approach

A note on Reversible Jump Markov Chain Monte Carlo

A note on Reversible Jump Markov Chain Monte Carlo Hedibert Freitas Lopes Graduate School of Business The University of Chicago 5807 South Woodlawn Avenue Chicago, Illinois 60637 February, 1st 2006 1 Introduction

A note on Reversible Jump Markov Chain Monte Carlo Hedibert Freitas Lopes Graduate School of Business The University of Chicago 5807 South Woodlawn Avenue Chicago, Illinois 60637 February, 1st 2006 1 Introduction

Chapter 6. Maximum Likelihood Analysis of Dynamic Stochastic General Equilibrium (DSGE) Models

Models") Chapter 6. Maximum Likelihood Analysis of Dynamic Stochastic General Equilibrium (DSGE) Models Fall 22 Contents Introduction 2. An illustrative example........................... 2.2 Discussion...................................

Chapter 6. Maximum Likelihood Analysis of Dynamic Stochastic General Equilibrium (DSGE) Models Fall 22 Contents Introduction 2. An illustrative example........................... 2.2 Discussion...................................

Session 5B: A worked example EGARCH model

Session 5B: A worked example EGARCH model John Geweke Bayesian Econometrics and its Applications August 7, worked example EGARCH model August 7, / 6 EGARCH Exponential generalized autoregressive conditional

Session 5B: A worked example EGARCH model John Geweke Bayesian Econometrics and its Applications August 7, worked example EGARCH model August 7, / 6 EGARCH Exponential generalized autoregressive conditional

News Shocks: Different Effects in Boom and Recession?

News Shocks: Different Effects in Boom and Recession? Maria Bolboaca, Sarah Fischer University of Bern Study Center Gerzensee June 7, 5 / Introduction News are defined in the literature as exogenous changes

News Shocks: Different Effects in Boom and Recession? Maria Bolboaca, Sarah Fischer University of Bern Study Center Gerzensee June 7, 5 / Introduction News are defined in the literature as exogenous changes

Markov-Switching Mixed Frequency VAR Models

Markov-Switching Mixed Frequency VAR Models Claudia Foroni Pierre Guérin Massimiliano Marcellino February 8, 2013 Preliminary version - Please do not circulate Abstract This paper introduces regime switching

Markov-Switching Mixed Frequency VAR Models Claudia Foroni Pierre Guérin Massimiliano Marcellino February 8, 2013 Preliminary version - Please do not circulate Abstract This paper introduces regime switching

Computational Macroeconomics. Prof. Dr. Maik Wolters Friedrich Schiller University Jena

Computational Macroeconomics Prof. Dr. Maik Wolters Friedrich Schiller University Jena Overview Objective: Learn doing empirical and applied theoretical work in monetary macroeconomics Implementing macroeconomic

Computational Macroeconomics Prof. Dr. Maik Wolters Friedrich Schiller University Jena Overview Objective: Learn doing empirical and applied theoretical work in monetary macroeconomics Implementing macroeconomic

STAT 518 Intro Student Presentation

STAT 518 Intro Student Presentation Wen Wei Loh April 11, 2013 Title of paper Radford M. Neal [1999] Bayesian Statistics, 6: 475-501, 1999 What the paper is about Regression and Classification Flexible

STAT 518 Intro Student Presentation Wen Wei Loh April 11, 2013 Title of paper Radford M. Neal [1999] Bayesian Statistics, 6: 475-501, 1999 What the paper is about Regression and Classification Flexible

Marginalized Predictive Likelihood Comparisons. of Linear Gaussian State-Space Models with. Applications to DSGE, DSGE-VAR, and VAR Models

Marginalized Predictive Likelihood Comparisons of Linear Gaussian State-Space Models with Applications to DSGE, DSGE-VAR, and VAR Models Anders Warne, Günter Coenen and Kai Christoffel* December 8, 2 Summary:

Marginalized Predictive Likelihood Comparisons of Linear Gaussian State-Space Models with Applications to DSGE, DSGE-VAR, and VAR Models Anders Warne, Günter Coenen and Kai Christoffel* December 8, 2 Summary:

Factor models. May 11, 2012

Factor models May 11, 2012 Factor Models Macro economists have a peculiar data situation: Many data series, but usually short samples How can we utilize all this information without running into degrees

Factor models May 11, 2012 Factor Models Macro economists have a peculiar data situation: Many data series, but usually short samples How can we utilize all this information without running into degrees

Comment on A Comparison of Two Business Cycle Dating Methods. James D. Hamilton

Comment on A Comparison of Two Business Cycle Dating Methods James D. Hamilton Harding and Pagan note that their stripped-down Markov-switching model (3)-(5) is an example of a standard state-space model,

Comment on A Comparison of Two Business Cycle Dating Methods James D. Hamilton Harding and Pagan note that their stripped-down Markov-switching model (3)-(5) is an example of a standard state-space model,

Robust Bayes Inference for Non-identified SVARs

1/29 Robust Bayes Inference for Non-identified SVARs Raffaella Giacomini (UCL) & Toru Kitagawa (UCL) 27, Dec, 2013 work in progress 2/29 Motivating Example Structural VAR (SVAR) is a useful tool to infer

1/29 Robust Bayes Inference for Non-identified SVARs Raffaella Giacomini (UCL) & Toru Kitagawa (UCL) 27, Dec, 2013 work in progress 2/29 Motivating Example Structural VAR (SVAR) is a useful tool to infer

Comparing Predictive Accuracy, Twenty Years Later: On The Use and Abuse of Diebold-Mariano Tests

Comparing Predictive Accuracy, Twenty Years Later: On The Use and Abuse of Diebold-Mariano Tests Francis X. Diebold April 28, 2014 1 / 24 Comparing Forecasts 2 / 24 Comparing Model-Free Forecasts Models

Comparing Predictive Accuracy, Twenty Years Later: On The Use and Abuse of Diebold-Mariano Tests Francis X. Diebold April 28, 2014 1 / 24 Comparing Forecasts 2 / 24 Comparing Model-Free Forecasts Models

BAYESIAN FORECASTS COMBINATION TO IMPROVE THE ROMANIAN INFLATION PREDICTIONS BASED ON ECONOMETRIC MODELS

Original scientific paper BAYESIAN FORECASTS COMBINATION TO IMPROVE THE ROMANIAN INFLATION PREDICTIONS BASED ON ECONOMETRIC MODELS Mihaela Simionescu Abstract There are many types of econometric models

Original scientific paper BAYESIAN FORECASTS COMBINATION TO IMPROVE THE ROMANIAN INFLATION PREDICTIONS BASED ON ECONOMETRIC MODELS Mihaela Simionescu Abstract There are many types of econometric models