Gravity Models, PPML Estimation and the Bias of the Robust Standard Errors

|

|

|

- Oscar Jones

- 5 years ago

- Views:

Transcription

1 Gravity Models, PPML Estimation and the Bias of the Robust Standard Errors Michael Pfaffermayr August 23, 2018 Abstract In gravity models with exporter and importer dummies the robust standard errors of the slope parameters tend to be severely downward biased when estimated by PPML. The coverage rate of confidence intervals of the estimated slope parameters may thus be much too small in cross-sections of the size typically used in empirical research. Keywords: Poisson Pseudo Maximum Likelihood Estimation; Heteroskedasticity-robust inference; Gravity Equation JEL: F10, F15, C13, C50 Department of Economic Theory, -Policy and -History, University of Innsbruck, Universitaetsstr. 15, A-6020 Innsbruck, Austria and Austrian Institute of Economic Research,

2 1 Introduction In cross-sections the Poisson pseudo maximum likelihood estimator (PPML, Santos Silva and Trenreyro, 2006) is routinely used to estimate gravity models with exporter and importer dummies. Fernandez-Val and Weidner (2017) show that the PPML estimator for two-dimensional panels with large n and large t asymptotics is among the few, which allow to estimate the slope parameters (but not the coefficients of the dummies) consistently and without asymptotic bias. This note demonstrates that under PPML the heteroskedasticity robust standard errors of the slope parameters tend to be severely downward biased in crosssections of the size typically used in empirical research. The reason is twofold. On the one hand, the distribution of trade flows is highly skewed and the PPMLprojection matrix used to estimate the residuals typically exhibits excessive leverage. On the other hand, due the inclusion of the exporter and importer dummies the convergence rate of the leverage to zero is of the order of the number of the countries, rather than its square. 2 Robust standard errors in a cross-section gravity model and their bias Formally, in a cross-section of C countries the DGP of the gravity model in levels generates bilateral trade flows, y ij, as y ij = e z ij α+β i+γ j η ij. (1) Bilateral trade flows depend on trade frictions collected in the the K 1 vector z ij with corresponding vector of slope parameter vector α. Exporter and importer specific effects are denoted by β i and γ j, respectively. The disturbances η ij are assumed to be independently distributed with E[η ij z ij ] = 1, but possibly heteroskedastic. For estimation, the gravity model can be reformulated with additive disturbances y ij = e z ij α+β i+γ j + ε ij, ε ij = e z ij α+β i+γ j (η ij 1), (2) Observations on the explanatory variables are collected in the C 2 K matrix Z and exporter and importer dummies (depending on the dummy design possibly also the constant) in the C 2 2C 1 design matrix D. W = [Z, D] contains all right hand side variables including exporter and importer dummies. For missing values one may define the selection matrix V that is derived from the identity matrix by setting all ones in the main diagonal to zero if the corresponding observation 1

3 is missing. Following Fernandez-Val and Weidner (2017) the PPML estimator for the slope parameters can be written as 1 ( Z) 1 α = Z V Q V D V Z V Q V Dỹ, (3) with M = diag(e z ij α+ β i + γ j j ), ỹ = M 1 2 y, Z = M 1 2 Z, D = M 1 2 D and Q V D = I V D ( D V D) 1 D V. Under a set of standard regularity conditions, the limit distribution of α can be derived as C ( α α 0 ) d N (0, V α ), where V α = B0 1 A 0 Ω ε A 0B0 1 1 with B 0 = p lim Z C V Q C D V Z 2 V is assumed to be invertible, A 0 Ω ε A 1 0 = p lim Z C V Q C D M V εε M 1 2 Q D V Z V. 2 and Ω ε = E[εε ]. Plugging in the estimated residuals ε, one can use 1 V C 2 α = C2 1B( α) 1 C 4 A( α) diag( ε ε )A( α) B( α) 1 for inference in finite samples. Following Chesher and Jewitt (1987) the bias of V α is given by ] E [ Vα V α = B0 1 A 0 M 0 diag(p W,ij (Ω η 2ω ij I C 2) p W,ij )M 0 A 0B0 1 + o(1). (4) p W,ij denotes the ij-th column of P W = M 1/2 0 V W ( W V W ) 1 W V M 1/2 0 and ω ij the ij, ij-th main diagonal element of Ω η. Under homoskedasticity of η the term diag(p W,ij (Ω η 2ω ij I C 2) p W,ij ) reverts to σ 2 diag(p W,ij,ij ), where p W,ij,ij denotes the leverage of observation ij (the diagonal element of P W referring to observation ij). In this case, V α is always downward biased of order O(C 1 ) rather than O(C 2 ), since the leverage is bounded in [0, 1] and rank(p W [ ) = ] K + 2C 1. v The proportionate bias (pb) can be defined as E ( V α V α)v for some vector v V αv ν and, as Chesher and Jewitt (1987) show, may be bounded by [ ] [( ) ] σ 2 sup pb( V α ) max η 1 v ij σ 2 η p W,ij,ij (1 p W,ij,ij ) p W,ij,ij = O(C 1 ) (5) ( ) ( ) ( ) inf pb( V α ) max v ij p W,ij,ij max ij (p W,ij,ij ) 2 = O(C 1 ) (6) 1 An Appendix provided as a supplement provides details on all derivations of the paper. PPML_standard_errors_Appendix.pdf 2 The star indicates that these matrices are evaluated at parameter values lying in between the estimated and true ones element by element. 2

4 If heteroskedastiy of η is not too severe ( σ2 η < 2), the proportionate bias of the σ 2 η ] ] V α is always negative, since in this case sup v [pb( V α ) max ij [ p 2 W,ij,ij. More importantly, the lower bound does not depend on the nature of heteroscedasticity, but only on the leverage. Using the cross-section data from WIOD (Timmer et al. 2015) covering 42 economies and estimating a standard gravity model specified as Model 3 in the next section for a random sample of 21 economies (441 country pairs) exhibits a maximum leverage of and the minimum leverage amounts to This translates in a lower bound of the proportionate bias of %. The maximum and minimum leverage changes only marginally to and 0.001, respectively, when using all 42 countries (1764 country pairs), as does the lower bound of the proportionate bias. Similar numbers are observed using trade data from OECD- STAN or GTAP. The estimated robust standard errors of the slope parameters are thus expected to be severely downward biased. 3 Monte Carlo simulations In each Monte Carlo run a simplified structural gravity model (Model 1) is generated as s ij = e 1,66z ij,1 0.90z ij,2 +β i +γ j η ij (7) C κ i = e 1,66z ij,1 0.90z ij,2 +β i +γ j (8) θ j = j=1 C e 1,66z ij,1 0.90z ij,2 +β i +γ j, (9) i=1 where the disturbances η ij are independent with E[η ij ] = 1 and enter in multiplicative form. Aggregate sales κ i,c and expenditure θ j,c (both measured as share of GDP in world GDP ) come from GTAP. β i and γ j, are derived as equilibrium solutions to the system of multilateral resistances (8) and (9) at true parameter values α 0. Data are sorted such that the sample always includes the C largest ones. z ij,1 is a border dummy taking the value 1 for i = j and zero else. z ij,2 refers to log weighted distance and is taken from CEPII s database (Model 1). To illustrate the impact of the leverage on the estimated robust standard errors, in Model 2 z i1 and z i2 are generated from a uniform distribution. Model 3 mimics a more realistic standard gravity model using dummies for contiguity, common language, colonial relationships and regional trade agreements as explanatory variables in addition to border and ln distance, all entering with coefficients as estimated by 3

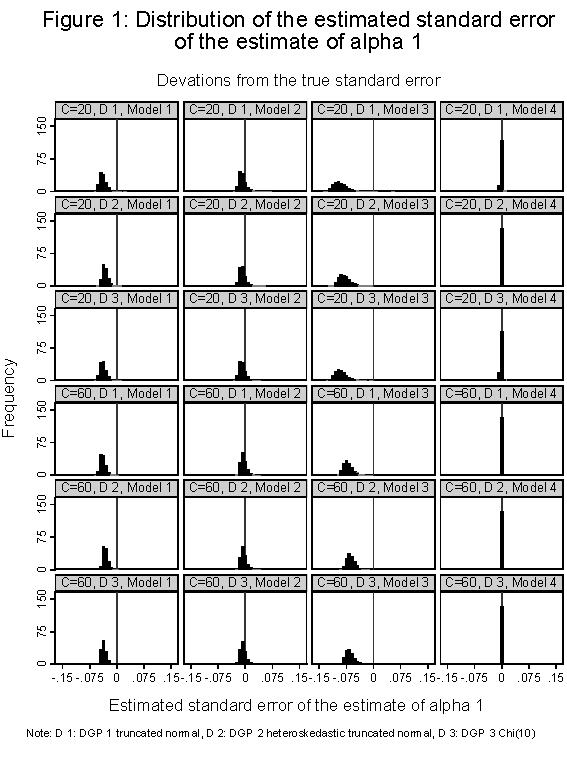

5 PPML ( 1.66, 0.90, 0.35, 0.49,.04, 0.41). Models 2 and 3 keep the exporter and importer effects as in Model 1. Lastly, Model 4 uses the explanatory variables of Model 2, but additionally generates the exporter and importer effects from a uniform distribution as well. In all four models the explanatory variables including the exporter and importer effects remain fixed in repeated samples. The Monte Carlo experiments consider C {20, 60} and generate independent disturbances from three different DGPs. DGP 1 generates the homoskedastic disturbances from a truncated normal that guarantees positive trade flows. DGP exp(0.1z 2 multiplies the truncated normal disturbances of DGP 1 by ij,2 ) C C i=1 j=1 exp(0.1z ij,2) to induce heteroskedasticity in addition to that stemming from the additive disturbances. The third DGP is based on a skewed distribution of the disturbances assuming that η is generated as χ 2 (10). In all three cases the disturbances are transformed to obtain E[η] = 1 and (an average) variance is 0.2. Under these assumptions the standard errors of the estimated parameters are similar to those found in the literature. Figure 1 delivers a clear message. The estimated standard errors of ˆα 1 under Models 1 and 3 are heavily downward biased and exhibit considerable variation. In Model 2 with uniformly distributed explanatory variables the bias is substantially reduced. However, comparing the results of Model 2 and Model 4 shows that it is mainly the skewness of the fixed exporter and importer effects that leads to the large variation of the estimated standard errors. Moreover, the bias disappears in Model 4 as one would expect. Table 1 exhibits the average of the simulated standard errors of α 1 along with its estimated counterpart, the simulated coverage rates of a 95%-confidence intervals and the simulated proportionate bias. 3 The simulated standard errors are calculated as the standard deviation of α 1 in Monte Carlo runs, while the estimated ones are based on the means of the estimated standard errors. In addition, the table reports the asymptotic lower and upper bound of the proportionate bias as derived in (5) and (6). 3 Results for α 2 are rather similar and available upon request. 4

6 5

7 Table 1: Monte Carlo simulation results: Leverage, simulated standard errors, estimated standard errors and 95% coverage rates of the slope parameters under dummy PPML for α 1 Model Leverage in % σ 2 η/σ 2 η sim. sd est. sd sim. bias in % cr lower b. upper b. C=20 Truncated normal Truncated normal, heteroskedastic χ(10) C=60 Truncated normal Truncated normal, heteroskedastic χ(10) Notes: Monte Carlo runs. cr refers to the coverage rate of a nominal 95%-confidence interval using the normal distribution. 6

8 In the sample of the 20 biggest countries, Model 1 implies a simulated proportionate bias of around minus 70% and a coverage rate of a 95%-confidence interval between 69.5% and 71.9% under the three considered DPGs. It turns out that the leverage is excessively high in bilateral trade data. Under DGP 1 and 3 the lower bound of the proportionate bias amounts to 99.86% at C = 20 and to 99.80% at C = 60, while its upper bound are 0.61% and 0.02%, respectively. Under DGP 2 the ratio of maximum and minimum variances of η ij amounts to σ 2 /σ 2 = 3.06 at C = 20 and 4.00 at C = 60. In Model 1 the upper bound is now at at C = 20 (33.40 at C = 60). The proportionate bias of the estimated standard error of α 1 decreases just marginally. Only very pronounced heteroskedasticty of η would reduce it substantially. Results for Model 2 generating the explanatory variables from a uniform distribution, indicate a considerable lower proportionate bias of the estimated standard error of α 1 and, at C = 20, a coverage ratio of the 95%-confidence interval between and Model 3 looks at the richer gravity model. With a simulated downward bias of as much as 77.86% it exhibits an even worse performance. In Model 4 all variables and the exporter and importer fixed effects come from the uniform distribution. The proportionate bias is negligible and lies between 6.48% and 4.79% at C = 20 and the coverage ratio is correct. Overall, these results suggest that the downward bias of the estimated standard error of α 1 is mainly determined by the large leverage induced by the trade friction indicators. Increasing the sample size to the 60 largest countries does not reduce the bias in Models 1 and 3, while for Models 2 and 4 the bias becomes smaller. The nature of the DGP seems not to make a big difference. Using a degrees of freedom correction reduces the bias and improves the coverage rate only marginally. Simulation results for this case are available upon request. 4 Conclusions PPML with dummies is now widely used for estimation of gravity models in levels. However, for calculating standard errors and confidence intervals of the estimated slope parameters it is of limited use. Typically, bilateral trade flows data are characterized by excessively high leverage with a slow convergence rate due to the increase of the number of parameters in sample size. As a result, the coverage rates of confidence intervals of the estimated slope parameters are far to small and parameter tests severely oversized. The present available statistical software such as stata and R does not account for this problem and there is an urgent need for improving the finite sample properties of PPML estimation in this respect. Approaches similar to those available for linear models and surveyed by MacKinnon (2013) could possibly bring improve- 7

9 ments. References Chesher A. and I. Jewitt (1987), The Bias of a Heteroskedasticity Consistent Covariance Matrix Estimator, Econometrica 55(5), Fernandez-Val, I. and M. Weidner (2016), Individual and Time Effects in Nonlinear Panel Models with large N, T, Journal of Econometrics 192(1), MacKinnon J.G. (2013), Thirty Years of Heteroskedasticity-Robust Inference. In: Chen X., Swanson N. (eds) Recent Advances and Future Directions in Causality, Prediction, and Specification Analysis. Springer, New York, NY. Santos Silva, J.M.C. and S. Tenreyro (2006), The Log of Gravity, Review of Economics and Statistics 88(4), Timmer, M. P., Dietzenbacher, E., Los, B., Stehrer, R. and de Vries, G. J. (2015), An Illustrated User Guide to the World Input Output Database: the Case of Global Automotive Production, Review of International Economics 23(3),

Constrained Poisson Pseudo Maximum Likelihood Estimation of Structural Gravity Models

Constrained Poisson Pseudo Maximum Likelihood Estimation of Structural Gravity Models Michael Pfaffermayr July 25, 2017 Abstract This paper reconsiders the estimation of structural gravity models, introducing

Constrained Poisson Pseudo Maximum Likelihood Estimation of Structural Gravity Models Michael Pfaffermayr July 25, 2017 Abstract This paper reconsiders the estimation of structural gravity models, introducing

Workshop for empirical trade analysis. December 2015 Bangkok, Thailand

Workshop for empirical trade analysis December 2015 Bangkok, Thailand Cosimo Beverelli (WTO) Rainer Lanz (WTO) Content a. What is the gravity equation? b. Naïve gravity estimation c. Theoretical foundations

Workshop for empirical trade analysis December 2015 Bangkok, Thailand Cosimo Beverelli (WTO) Rainer Lanz (WTO) Content a. What is the gravity equation? b. Naïve gravity estimation c. Theoretical foundations

A COMPARISON OF HETEROSCEDASTICITY ROBUST STANDARD ERRORS AND NONPARAMETRIC GENERALIZED LEAST SQUARES

A COMPARISON OF HETEROSCEDASTICITY ROBUST STANDARD ERRORS AND NONPARAMETRIC GENERALIZED LEAST SQUARES MICHAEL O HARA AND CHRISTOPHER F. PARMETER Abstract. This paper presents a Monte Carlo comparison of

A COMPARISON OF HETEROSCEDASTICITY ROBUST STANDARD ERRORS AND NONPARAMETRIC GENERALIZED LEAST SQUARES MICHAEL O HARA AND CHRISTOPHER F. PARMETER Abstract. This paper presents a Monte Carlo comparison of

The Poisson Quasi-Maximum Likelihood Estimator: A Solution to the Adding Up Problem in Gravity Models

Working Paper DTC-2011-3 The Poisson Quasi-Maximum Likelihood Estimator: A Solution to the Adding Up Problem in Gravity Models Jean-François Arvis, Senior Economist, the World Bank. Ben Shepherd, Principal,

Working Paper DTC-2011-3 The Poisson Quasi-Maximum Likelihood Estimator: A Solution to the Adding Up Problem in Gravity Models Jean-François Arvis, Senior Economist, the World Bank. Ben Shepherd, Principal,

Bootstrapping Heteroskedasticity Consistent Covariance Matrix Estimator

Bootstrapping Heteroskedasticity Consistent Covariance Matrix Estimator by Emmanuel Flachaire Eurequa, University Paris I Panthéon-Sorbonne December 2001 Abstract Recent results of Cribari-Neto and Zarkos

Bootstrapping Heteroskedasticity Consistent Covariance Matrix Estimator by Emmanuel Flachaire Eurequa, University Paris I Panthéon-Sorbonne December 2001 Abstract Recent results of Cribari-Neto and Zarkos

Further simulation evidence on the performance of the Poisson pseudo-maximum likelihood estimator

Further simulation evidence on the performance of the Poisson pseudo-maximum likelihood estimator J.M.C. Santos Silva Silvana Tenreyro January 27, 2009 Abstract We extend the simulation results given in

Further simulation evidence on the performance of the Poisson pseudo-maximum likelihood estimator J.M.C. Santos Silva Silvana Tenreyro January 27, 2009 Abstract We extend the simulation results given in

Trade costs in bilateral trade flows: Heterogeneity and zeroes in structural gravity models

Società Italiana degli Economisti 52.ma Riunione Scientifica Annuale Università degli Studi di Roma Tre, Roma, 14-15 ottobre 2011 Trade costs in bilateral trade flows: Heterogeneity and zeroes in structural

Società Italiana degli Economisti 52.ma Riunione Scientifica Annuale Università degli Studi di Roma Tre, Roma, 14-15 ottobre 2011 Trade costs in bilateral trade flows: Heterogeneity and zeroes in structural

1 Estimation of Persistent Dynamic Panel Data. Motivation

1 Estimation of Persistent Dynamic Panel Data. Motivation Consider the following Dynamic Panel Data (DPD) model y it = y it 1 ρ + x it β + µ i + v it (1.1) with i = {1, 2,..., N} denoting the individual

1 Estimation of Persistent Dynamic Panel Data. Motivation Consider the following Dynamic Panel Data (DPD) model y it = y it 1 ρ + x it β + µ i + v it (1.1) with i = {1, 2,..., N} denoting the individual

On the Problem of Endogenous Unobserved Effects in the Estimation of Gravity Models

Journal of Economic Integration 19(1), March 2004; 182-191 On the Problem of Endogenous Unobserved Effects in the Estimation of Gravity Models Peter Egger University of Innsbruck Abstract We propose to

Journal of Economic Integration 19(1), March 2004; 182-191 On the Problem of Endogenous Unobserved Effects in the Estimation of Gravity Models Peter Egger University of Innsbruck Abstract We propose to

Topic 7: Heteroskedasticity

Topic 7: Heteroskedasticity Advanced Econometrics (I Dong Chen School of Economics, Peking University Introduction If the disturbance variance is not constant across observations, the regression is heteroskedastic

Topic 7: Heteroskedasticity Advanced Econometrics (I Dong Chen School of Economics, Peking University Introduction If the disturbance variance is not constant across observations, the regression is heteroskedastic

Supplement to Quantile-Based Nonparametric Inference for First-Price Auctions

Supplement to Quantile-Based Nonparametric Inference for First-Price Auctions Vadim Marmer University of British Columbia Artyom Shneyerov CIRANO, CIREQ, and Concordia University August 30, 2010 Abstract

Supplement to Quantile-Based Nonparametric Inference for First-Price Auctions Vadim Marmer University of British Columbia Artyom Shneyerov CIRANO, CIREQ, and Concordia University August 30, 2010 Abstract

Reliability of inference (1 of 2 lectures)

") Reliability of inference (1 of 2 lectures) Ragnar Nymoen University of Oslo 5 March 2013 1 / 19 This lecture (#13 and 14): I The optimality of the OLS estimators and tests depend on the assumptions of

Reliability of inference (1 of 2 lectures) Ragnar Nymoen University of Oslo 5 March 2013 1 / 19 This lecture (#13 and 14): I The optimality of the OLS estimators and tests depend on the assumptions of

Heteroskedasticity-Robust Inference in Finite Samples

Heteroskedasticity-Robust Inference in Finite Samples Jerry Hausman and Christopher Palmer Massachusetts Institute of Technology December 011 Abstract Since the advent of heteroskedasticity-robust standard

Heteroskedasticity-Robust Inference in Finite Samples Jerry Hausman and Christopher Palmer Massachusetts Institute of Technology December 011 Abstract Since the advent of heteroskedasticity-robust standard

Nonlinear factor models for network and panel data

Nonlinear factor models for network and panel data Mingli Chen Iván Fernández-Val Martin Weidner The Institute for Fiscal Studies Department of Economics, UCL cemmap working paper CWP38/8 Nonlinear Factor

Nonlinear factor models for network and panel data Mingli Chen Iván Fernández-Val Martin Weidner The Institute for Fiscal Studies Department of Economics, UCL cemmap working paper CWP38/8 Nonlinear Factor

Elasticity of Trade Flow to Trade Barriers

Alessandro Olper Valentina Raimondi Elasticity of Trade Flow to Trade Barriers A Comparison among Emerging Estimation Techniques ARACNE Copyright MMVIII ARACNE editrice S.r.l. www.aracneeditrice.it info@aracneeditrice.it

Alessandro Olper Valentina Raimondi Elasticity of Trade Flow to Trade Barriers A Comparison among Emerging Estimation Techniques ARACNE Copyright MMVIII ARACNE editrice S.r.l. www.aracneeditrice.it info@aracneeditrice.it

LIML Estimation of Import Demand and Export Supply Elasticities. Vahagn Galstyan. TEP Working Paper No March 2016

LIML Estimation of Import Demand and Export Supply Elasticities Vahagn Galstyan TEP Working Paper No. 0316 March 2016 Trinity Economics Papers Department of Economics Trinity College Dublin LIML Estimation

LIML Estimation of Import Demand and Export Supply Elasticities Vahagn Galstyan TEP Working Paper No. 0316 March 2016 Trinity Economics Papers Department of Economics Trinity College Dublin LIML Estimation

SUR Estimation of Error Components Models With AR(1) Disturbances and Unobserved Endogenous Effects

Disturbances and Unobserved Endogenous Effects") SUR Estimation of Error Components Models With AR(1) Disturbances and Unobserved Endogenous Effects Peter Egger November 27, 2001 Abstract Thispaperfocussesontheestimationoferrorcomponentsmodels in the

SUR Estimation of Error Components Models With AR(1) Disturbances and Unobserved Endogenous Effects Peter Egger November 27, 2001 Abstract Thispaperfocussesontheestimationoferrorcomponentsmodels in the

Heteroskedasticity. Part VII. Heteroskedasticity

Part VII Heteroskedasticity As of Oct 15, 2015 1 Heteroskedasticity Consequences Heteroskedasticity-robust inference Testing for Heteroskedasticity Weighted Least Squares (WLS) Feasible generalized Least

Part VII Heteroskedasticity As of Oct 15, 2015 1 Heteroskedasticity Consequences Heteroskedasticity-robust inference Testing for Heteroskedasticity Weighted Least Squares (WLS) Feasible generalized Least

Trading partners and trading volumes: Implementing the Helpman-Melitz-Rubinstein model empirically

Trading partners and trading volumes: Implementing the Helpman-Melitz-Rubinstein model empirically J.M.C. SANTOS SILVA and SILVANA TENREYRO University of Essex and CEMAPRE. Wivenhoe Park, Colchester CO4

Trading partners and trading volumes: Implementing the Helpman-Melitz-Rubinstein model empirically J.M.C. SANTOS SILVA and SILVANA TENREYRO University of Essex and CEMAPRE. Wivenhoe Park, Colchester CO4

Estimating the Gravity Model When Zero Trade Flows Are Frequent. Will Martin and Cong S. Pham * February 2008

Estimating the Gravity Model When Zero Trade Flows Are Frequent Will Martin and Cong S. Pham * February 2008 Abstract In this paper we estimate the gravity model allowing for the pervasive issues of heteroscedasticity

Estimating the Gravity Model When Zero Trade Flows Are Frequent Will Martin and Cong S. Pham * February 2008 Abstract In this paper we estimate the gravity model allowing for the pervasive issues of heteroscedasticity

Quantifying the effects of NTMs. Xinyi Li Trade Policies Review Division, WTO Secretariat 12 th ARTNeT Capacity Building Workshop December 2016

Quantifying the effects of NTMs Xinyi Li Trade Policies Review Division, WTO Secretariat 12 th ARTNeT Capacity Building Workshop December 2016 1 Approaches to quantifying NTMs Chen and Novy (2012) described

Quantifying the effects of NTMs Xinyi Li Trade Policies Review Division, WTO Secretariat 12 th ARTNeT Capacity Building Workshop December 2016 1 Approaches to quantifying NTMs Chen and Novy (2012) described

The Exact Distribution of the t-ratio with Robust and Clustered Standard Errors

The Exact Distribution of the t-ratio with Robust and Clustered Standard Errors by Bruce E. Hansen Department of Economics University of Wisconsin October 2018 Bruce Hansen (University of Wisconsin) Exact

The Exact Distribution of the t-ratio with Robust and Clustered Standard Errors by Bruce E. Hansen Department of Economics University of Wisconsin October 2018 Bruce Hansen (University of Wisconsin) Exact

Lecture 4: Heteroskedasticity

Lecture 4: Heteroskedasticity Econometric Methods Warsaw School of Economics (4) Heteroskedasticity 1 / 24 Outline 1 What is heteroskedasticity? 2 Testing for heteroskedasticity White Goldfeld-Quandt Breusch-Pagan

Lecture 4: Heteroskedasticity Econometric Methods Warsaw School of Economics (4) Heteroskedasticity 1 / 24 Outline 1 What is heteroskedasticity? 2 Testing for heteroskedasticity White Goldfeld-Quandt Breusch-Pagan

The OLS Estimation of a basic gravity model. Dr. Selim Raihan Executive Director, SANEM Professor, Department of Economics, University of Dhaka

The OLS Estimation of a basic gravity model Dr. Selim Raihan Executive Director, SANEM Professor, Department of Economics, University of Dhaka Contents I. Regression Analysis II. Ordinary Least Square

The OLS Estimation of a basic gravity model Dr. Selim Raihan Executive Director, SANEM Professor, Department of Economics, University of Dhaka Contents I. Regression Analysis II. Ordinary Least Square

WISE International Masters

WISE International Masters ECONOMETRICS Instructor: Brett Graham INSTRUCTIONS TO STUDENTS 1 The time allowed for this examination paper is 2 hours. 2 This examination paper contains 32 questions. You are

WISE International Masters ECONOMETRICS Instructor: Brett Graham INSTRUCTIONS TO STUDENTS 1 The time allowed for this examination paper is 2 hours. 2 This examination paper contains 32 questions. You are

Lecture 7: Dynamic panel models 2

Lecture 7: Dynamic panel models 2 Ragnar Nymoen Department of Economics, UiO 25 February 2010 Main issues and references The Arellano and Bond method for GMM estimation of dynamic panel data models A stepwise

Lecture 7: Dynamic panel models 2 Ragnar Nymoen Department of Economics, UiO 25 February 2010 Main issues and references The Arellano and Bond method for GMM estimation of dynamic panel data models A stepwise

Topic 10: Panel Data Analysis

Topic 10: Panel Data Analysis Advanced Econometrics (I) Dong Chen School of Economics, Peking University 1 Introduction Panel data combine the features of cross section data time series. Usually a panel

Topic 10: Panel Data Analysis Advanced Econometrics (I) Dong Chen School of Economics, Peking University 1 Introduction Panel data combine the features of cross section data time series. Usually a panel

Heteroskedasticity. in the Error Component Model

Heteroskedasticity in the Error Component Model Baltagi Textbook Chapter 5 Mozhgan Raeisian Parvari (0.06.010) Content Introduction Cases of Heteroskedasticity Adaptive heteroskedastic estimators (EGLS,

Heteroskedasticity in the Error Component Model Baltagi Textbook Chapter 5 Mozhgan Raeisian Parvari (0.06.010) Content Introduction Cases of Heteroskedasticity Adaptive heteroskedastic estimators (EGLS,

A Practitioner s Guide to Cluster-Robust Inference

A Practitioner s Guide to Cluster-Robust Inference A. C. Cameron and D. L. Miller presented by Federico Curci March 4, 2015 Cameron Miller Cluster Clinic II March 4, 2015 1 / 20 In the previous episode

A Practitioner s Guide to Cluster-Robust Inference A. C. Cameron and D. L. Miller presented by Federico Curci March 4, 2015 Cameron Miller Cluster Clinic II March 4, 2015 1 / 20 In the previous episode

Bootstrapping heteroskedastic regression models: wild bootstrap vs. pairs bootstrap

Bootstrapping heteroskedastic regression models: wild bootstrap vs. pairs bootstrap Emmanuel Flachaire To cite this version: Emmanuel Flachaire. Bootstrapping heteroskedastic regression models: wild bootstrap

Bootstrapping heteroskedastic regression models: wild bootstrap vs. pairs bootstrap Emmanuel Flachaire To cite this version: Emmanuel Flachaire. Bootstrapping heteroskedastic regression models: wild bootstrap

Gravity Models: Theoretical Foundations and related estimation issues

Gravity Models: Theoretical Foundations and related estimation issues ARTNet Capacity Building Workshop for Trade Research Phnom Penh, Cambodia 2-6 June 2008 Outline 1. Theoretical foundations From Tinbergen

Gravity Models: Theoretical Foundations and related estimation issues ARTNet Capacity Building Workshop for Trade Research Phnom Penh, Cambodia 2-6 June 2008 Outline 1. Theoretical foundations From Tinbergen

IV Quantile Regression for Group-level Treatments, with an Application to the Distributional Effects of Trade

IV Quantile Regression for Group-level Treatments, with an Application to the Distributional Effects of Trade Denis Chetverikov Brad Larsen Christopher Palmer UCLA, Stanford and NBER, UC Berkeley September

IV Quantile Regression for Group-level Treatments, with an Application to the Distributional Effects of Trade Denis Chetverikov Brad Larsen Christopher Palmer UCLA, Stanford and NBER, UC Berkeley September

More efficient tests robust to heteroskedasticity of unknown form

More efficient tests robust to heteroskedasticity of unknown form Emmanuel Flachaire To cite this version: Emmanuel Flachaire. More efficient tests robust to heteroskedasticity of unknown form. Econometric

More efficient tests robust to heteroskedasticity of unknown form Emmanuel Flachaire To cite this version: Emmanuel Flachaire. More efficient tests robust to heteroskedasticity of unknown form. Econometric

Quantile regression and heteroskedasticity

Quantile regression and heteroskedasticity José A. F. Machado J.M.C. Santos Silva June 18, 2013 Abstract This note introduces a wrapper for qreg which reports standard errors and t statistics that are

Quantile regression and heteroskedasticity José A. F. Machado J.M.C. Santos Silva June 18, 2013 Abstract This note introduces a wrapper for qreg which reports standard errors and t statistics that are

Modelling Methods for Trade Policy II: Introduction to OLS Regression Analysis

Modelling Methods for Trade Policy II: Introduction to OLS Regression Analysis Roberta Piermartini Economic Research and Analysis Division WTO Bangkok, 19 April 2006 Outline A. What is an OLS regression?

Modelling Methods for Trade Policy II: Introduction to OLS Regression Analysis Roberta Piermartini Economic Research and Analysis Division WTO Bangkok, 19 April 2006 Outline A. What is an OLS regression?

the error term could vary over the observations, in ways that are related

Heteroskedasticity We now consider the implications of relaxing the assumption that the conditional variance Var(u i x i ) = σ 2 is common to all observations i = 1,..., n In many applications, we may

Heteroskedasticity We now consider the implications of relaxing the assumption that the conditional variance Var(u i x i ) = σ 2 is common to all observations i = 1,..., n In many applications, we may

Recent Advances in the Field of Trade Theory and Policy Analysis Using Micro-Level Data

Recent Advances in the Field of Trade Theory and Policy Analysis Using Micro-Level Data July 2012 Bangkok, Thailand Cosimo Beverelli (World Trade Organization) 1 Content a) Classical regression model b)

Recent Advances in the Field of Trade Theory and Policy Analysis Using Micro-Level Data July 2012 Bangkok, Thailand Cosimo Beverelli (World Trade Organization) 1 Content a) Classical regression model b)

Estimating Gravity Equation Models in the Presence of. Sample Selection and Heteroskedasticity

Estimating Gravity Equation Models in the Presence of Sample Selection and Heteroskedasticity Bo Xiong Sixia Chen Abstract: Gravity models are widely used to explain patterns of trade. However, two stylized

Estimating Gravity Equation Models in the Presence of Sample Selection and Heteroskedasticity Bo Xiong Sixia Chen Abstract: Gravity models are widely used to explain patterns of trade. However, two stylized

WISE MA/PhD Programs Econometrics Instructor: Brett Graham Spring Semester, Academic Year Exam Version: A

WISE MA/PhD Programs Econometrics Instructor: Brett Graham Spring Semester, 2015-16 Academic Year Exam Version: A INSTRUCTIONS TO STUDENTS 1 The time allowed for this examination paper is 2 hours. 2 This

WISE MA/PhD Programs Econometrics Instructor: Brett Graham Spring Semester, 2015-16 Academic Year Exam Version: A INSTRUCTIONS TO STUDENTS 1 The time allowed for this examination paper is 2 hours. 2 This

Andreas Steinhauer, University of Zurich Tobias Wuergler, University of Zurich. September 24, 2010

L C M E F -S IV R Andreas Steinhauer, University of Zurich Tobias Wuergler, University of Zurich September 24, 2010 Abstract This paper develops basic algebraic concepts for instrumental variables (IV)

L C M E F -S IV R Andreas Steinhauer, University of Zurich Tobias Wuergler, University of Zurich September 24, 2010 Abstract This paper develops basic algebraic concepts for instrumental variables (IV)

ARTNeT Interactive Gravity Modeling Tool

Evidence-Based Trade Policymaking Capacity Building Programme ARTNeT Interactive Gravity Modeling Tool Witada Anukoonwattaka (PhD) UNESCAP 26 July 2011 Outline Background on gravity model of trade and

Evidence-Based Trade Policymaking Capacity Building Programme ARTNeT Interactive Gravity Modeling Tool Witada Anukoonwattaka (PhD) UNESCAP 26 July 2011 Outline Background on gravity model of trade and

Determining Changes in Welfare Distributions at the Micro-level: Updating Poverty Maps By Chris Elbers, Jean O. Lanjouw, and Peter Lanjouw 1

Determining Changes in Welfare Distributions at the Micro-level: Updating Poverty Maps By Chris Elbers, Jean O. Lanjouw, and Peter Lanjouw 1 Income and wealth distributions have a prominent position in

Determining Changes in Welfare Distributions at the Micro-level: Updating Poverty Maps By Chris Elbers, Jean O. Lanjouw, and Peter Lanjouw 1 Income and wealth distributions have a prominent position in

The Exact Distribution of the t-ratio with Robust and Clustered Standard Errors

The Exact Distribution of the t-ratio with Robust and Clustered Standard Errors by Bruce E. Hansen Department of Economics University of Wisconsin June 2017 Bruce Hansen (University of Wisconsin) Exact

The Exact Distribution of the t-ratio with Robust and Clustered Standard Errors by Bruce E. Hansen Department of Economics University of Wisconsin June 2017 Bruce Hansen (University of Wisconsin) Exact

Elasticity of trade flow to trade barriers: A comparison among emerging estimation techniques

1 Elasticity of trade flow to trade barriers: A comparison among emerging estimation techniques Olper A. 1, Raimondi V. 1 1 University of Milano, Department of Agricultural Economics Abstract The objective

1 Elasticity of trade flow to trade barriers: A comparison among emerging estimation techniques Olper A. 1, Raimondi V. 1 1 University of Milano, Department of Agricultural Economics Abstract The objective

Modified Variance Ratio Test for Autocorrelation in the Presence of Heteroskedasticity

The Lahore Journal of Economics 23 : 1 (Summer 2018): pp. 1 19 Modified Variance Ratio Test for Autocorrelation in the Presence of Heteroskedasticity Sohail Chand * and Nuzhat Aftab ** Abstract Given that

The Lahore Journal of Economics 23 : 1 (Summer 2018): pp. 1 19 Modified Variance Ratio Test for Autocorrelation in the Presence of Heteroskedasticity Sohail Chand * and Nuzhat Aftab ** Abstract Given that

Migration Gravity Revisited

Migration Gravity Revisited Steen Sirries Preleminary draft. Please do not circulate. Abstract Recent contributions to the literature of international migration propose varieties of gravity estimations

Migration Gravity Revisited Steen Sirries Preleminary draft. Please do not circulate. Abstract Recent contributions to the literature of international migration propose varieties of gravity estimations

Repeated observations on the same cross-section of individual units. Important advantages relative to pure cross-section data

Panel data Repeated observations on the same cross-section of individual units. Important advantages relative to pure cross-section data - possible to control for some unobserved heterogeneity - possible

Panel data Repeated observations on the same cross-section of individual units. Important advantages relative to pure cross-section data - possible to control for some unobserved heterogeneity - possible

GLM estimation of trade gravity models with fixed effects

Empir Econ (2016) 50:137 175 DOI 10.1007/s00181-015-0935-x GLM estimation of trade gravity models with fixed effects Peter H. Egger Kevin E. Staub Received: 2 June 2014 / Accepted: 6 January 2015 / Published

Empir Econ (2016) 50:137 175 DOI 10.1007/s00181-015-0935-x GLM estimation of trade gravity models with fixed effects Peter H. Egger Kevin E. Staub Received: 2 June 2014 / Accepted: 6 January 2015 / Published

Testing Random Effects in Two-Way Spatial Panel Data Models

Testing Random Effects in Two-Way Spatial Panel Data Models Nicolas Debarsy May 27, 2010 Abstract This paper proposes an alternative testing procedure to the Hausman test statistic to help the applied

Testing Random Effects in Two-Way Spatial Panel Data Models Nicolas Debarsy May 27, 2010 Abstract This paper proposes an alternative testing procedure to the Hausman test statistic to help the applied

LESLIE GODFREY LIST OF PUBLICATIONS

LESLIE GODFREY LIST OF PUBLICATIONS This list is in two parts. First, there is a set of selected publications for the period 1971-1996. Second, there are details of more recent outputs. SELECTED PUBLICATIONS,

LESLIE GODFREY LIST OF PUBLICATIONS This list is in two parts. First, there is a set of selected publications for the period 1971-1996. Second, there are details of more recent outputs. SELECTED PUBLICATIONS,

Econometrics of Panel Data

Econometrics of Panel Data Jakub Mućk Meeting # 1 Jakub Mućk Econometrics of Panel Data Meeting # 1 1 / 31 Outline 1 Course outline 2 Panel data Advantages of Panel Data Limitations of Panel Data 3 Pooled

Econometrics of Panel Data Jakub Mućk Meeting # 1 Jakub Mućk Econometrics of Panel Data Meeting # 1 1 / 31 Outline 1 Course outline 2 Panel data Advantages of Panel Data Limitations of Panel Data 3 Pooled

New heteroskedasticity-robust standard errors for the linear regression model

Brazilian Journal of Probability and Statistics 2014, Vol. 28, No. 1, 83 95 DOI: 10.1214/12-BJPS196 Brazilian Statistical Association, 2014 New heteroskedasticity-robust standard errors for the linear

Brazilian Journal of Probability and Statistics 2014, Vol. 28, No. 1, 83 95 DOI: 10.1214/12-BJPS196 Brazilian Statistical Association, 2014 New heteroskedasticity-robust standard errors for the linear

Testing non-nested models for non-negative data with many zeros

Testing non-nested models for non-negative data with many zeros J.M.C. Santos Silva, Silvana Tenreyro, Frank Windmeijer 16 February 2014 Abstract In economic applications it is often the case that the

Testing non-nested models for non-negative data with many zeros J.M.C. Santos Silva, Silvana Tenreyro, Frank Windmeijer 16 February 2014 Abstract In economic applications it is often the case that the

Alternative HAC Covariance Matrix Estimators with Improved Finite Sample Properties

Alternative HAC Covariance Matrix Estimators with Improved Finite Sample Properties Luke Hartigan University of New South Wales September 5, 2016 Abstract HAC estimators are known to produce test statistics

Alternative HAC Covariance Matrix Estimators with Improved Finite Sample Properties Luke Hartigan University of New South Wales September 5, 2016 Abstract HAC estimators are known to produce test statistics

Finite Sample Performance of A Minimum Distance Estimator Under Weak Instruments

Finite Sample Performance of A Minimum Distance Estimator Under Weak Instruments Tak Wai Chau February 20, 2014 Abstract This paper investigates the nite sample performance of a minimum distance estimator

Finite Sample Performance of A Minimum Distance Estimator Under Weak Instruments Tak Wai Chau February 20, 2014 Abstract This paper investigates the nite sample performance of a minimum distance estimator

Spatial Autocorrelation and Interactions between Surface Temperature Trends and Socioeconomic Changes

Spatial Autocorrelation and Interactions between Surface Temperature Trends and Socioeconomic Changes Ross McKitrick Department of Economics University of Guelph December, 00 1 1 1 1 Spatial Autocorrelation

Spatial Autocorrelation and Interactions between Surface Temperature Trends and Socioeconomic Changes Ross McKitrick Department of Economics University of Guelph December, 00 1 1 1 1 Spatial Autocorrelation

Session 3-4: Estimating the gravity models

ARTNeT- KRI Capacity Building Workshop on Trade Policy Analysis: Evidence-based Policy Making and Gravity Modelling for Trade Analysis 18-20 August 2015, Kuala Lumpur Session 3-4: Estimating the gravity

ARTNeT- KRI Capacity Building Workshop on Trade Policy Analysis: Evidence-based Policy Making and Gravity Modelling for Trade Analysis 18-20 August 2015, Kuala Lumpur Session 3-4: Estimating the gravity

Gravity, log of gravity and the distance puzzle

Gravity, log of gravity and the distance puzzle Clément Bosquet, Hervé Boulhol To cite this version: Clément Bosquet, Hervé Boulhol. Gravity, log of gravity and the distance puzzle. 2009. HAL Id: halshs-00401386

Gravity, log of gravity and the distance puzzle Clément Bosquet, Hervé Boulhol To cite this version: Clément Bosquet, Hervé Boulhol. Gravity, log of gravity and the distance puzzle. 2009. HAL Id: halshs-00401386

Econometrics II. Nonstandard Standard Error Issues: A Guide for the. Practitioner

Econometrics II Nonstandard Standard Error Issues: A Guide for the Practitioner Måns Söderbom 10 May 2011 Department of Economics, University of Gothenburg. Email: mans.soderbom@economics.gu.se. Web: www.economics.gu.se/soderbom,

Econometrics II Nonstandard Standard Error Issues: A Guide for the Practitioner Måns Söderbom 10 May 2011 Department of Economics, University of Gothenburg. Email: mans.soderbom@economics.gu.se. Web: www.economics.gu.se/soderbom,

DEPARTMENT OF ECONOMICS

ISSN 0819-64 ISBN 0 7340 616 1 THE UNIVERSITY OF MELBOURNE DEPARTMENT OF ECONOMICS RESEARCH PAPER NUMBER 959 FEBRUARY 006 TESTING FOR RATE-DEPENDENCE AND ASYMMETRY IN INFLATION UNCERTAINTY: EVIDENCE FROM

ISSN 0819-64 ISBN 0 7340 616 1 THE UNIVERSITY OF MELBOURNE DEPARTMENT OF ECONOMICS RESEARCH PAPER NUMBER 959 FEBRUARY 006 TESTING FOR RATE-DEPENDENCE AND ASYMMETRY IN INFLATION UNCERTAINTY: EVIDENCE FROM

Some Monte Carlo Evidence for Adaptive Estimation of Unit-Time Varying Heteroscedastic Panel Data Models

Some Monte Carlo Evidence for Adaptive Estimation of Unit-Time Varying Heteroscedastic Panel Data Models G. R. Pasha Department of Statistics, Bahauddin Zakariya University Multan, Pakistan E-mail: drpasha@bzu.edu.pk

Some Monte Carlo Evidence for Adaptive Estimation of Unit-Time Varying Heteroscedastic Panel Data Models G. R. Pasha Department of Statistics, Bahauddin Zakariya University Multan, Pakistan E-mail: drpasha@bzu.edu.pk

Models for Heterogeneous Choices

APPENDIX B Models for Heterogeneous Choices Heteroskedastic Choice Models In the empirical chapters of the printed book we are interested in testing two different types of propositions about the beliefs

APPENDIX B Models for Heterogeneous Choices Heteroskedastic Choice Models In the empirical chapters of the printed book we are interested in testing two different types of propositions about the beliefs

NBER WORKING PAPER SERIES ROBUST STANDARD ERRORS IN SMALL SAMPLES: SOME PRACTICAL ADVICE. Guido W. Imbens Michal Kolesar

NBER WORKING PAPER SERIES ROBUST STANDARD ERRORS IN SMALL SAMPLES: SOME PRACTICAL ADVICE Guido W. Imbens Michal Kolesar Working Paper 18478 http://www.nber.org/papers/w18478 NATIONAL BUREAU OF ECONOMIC

NBER WORKING PAPER SERIES ROBUST STANDARD ERRORS IN SMALL SAMPLES: SOME PRACTICAL ADVICE Guido W. Imbens Michal Kolesar Working Paper 18478 http://www.nber.org/papers/w18478 NATIONAL BUREAU OF ECONOMIC

DEPARTMENT OF ECONOMICS AND FINANCE COLLEGE OF BUSINESS AND ECONOMICS UNIVERSITY OF CANTERBURY CHRISTCHURCH, NEW ZEALAND

DEPARTME OF ECONOMICS AND FINANCE COLLEGE OF BUSINESS AND ECONOMICS UNIVERSITY OF CAERBURY CHRISTCHURCH, NEW ZEALAND The PCSE Estimator is Good -- Just Not as Good as You Think W. Robert Reed and Rachel

DEPARTME OF ECONOMICS AND FINANCE COLLEGE OF BUSINESS AND ECONOMICS UNIVERSITY OF CAERBURY CHRISTCHURCH, NEW ZEALAND The PCSE Estimator is Good -- Just Not as Good as You Think W. Robert Reed and Rachel

DEPARTMENT OF ECONOMICS

ISSN 0819-2642 ISBN 0 7340 2601 3 THE UNIVERSITY OF MELBOURNE DEPARTMENT OF ECONOMICS RESEARCH PAPER NUMBER 945 AUGUST 2005 TESTING FOR ASYMMETRY IN INTEREST RATE VOLATILITY IN THE PRESENCE OF A NEGLECTED

ISSN 0819-2642 ISBN 0 7340 2601 3 THE UNIVERSITY OF MELBOURNE DEPARTMENT OF ECONOMICS RESEARCH PAPER NUMBER 945 AUGUST 2005 TESTING FOR ASYMMETRY IN INTEREST RATE VOLATILITY IN THE PRESENCE OF A NEGLECTED

Bayesian Interpretations of Heteroskedastic Consistent Covariance. Estimators Using the Informed Bayesian Bootstrap

Bayesian Interpretations of Heteroskedastic Consistent Covariance Estimators Using the Informed Bayesian Bootstrap Dale J. Poirier University of California, Irvine May 22, 2009 Abstract This paper provides

Bayesian Interpretations of Heteroskedastic Consistent Covariance Estimators Using the Informed Bayesian Bootstrap Dale J. Poirier University of California, Irvine May 22, 2009 Abstract This paper provides

Tests of the Present-Value Model of the Current Account: A Note

Tests of the Present-Value Model of the Current Account: A Note Hafedh Bouakez Takashi Kano March 5, 2007 Abstract Using a Monte Carlo approach, we evaluate the small-sample properties of four different

Tests of the Present-Value Model of the Current Account: A Note Hafedh Bouakez Takashi Kano March 5, 2007 Abstract Using a Monte Carlo approach, we evaluate the small-sample properties of four different

Econometrics I KS. Module 2: Multivariate Linear Regression. Alexander Ahammer. This version: April 16, 2018

Econometrics I KS Module 2: Multivariate Linear Regression Alexander Ahammer Department of Economics Johannes Kepler University of Linz This version: April 16, 2018 Alexander Ahammer (JKU) Module 2: Multivariate

Econometrics I KS Module 2: Multivariate Linear Regression Alexander Ahammer Department of Economics Johannes Kepler University of Linz This version: April 16, 2018 Alexander Ahammer (JKU) Module 2: Multivariate

The Case Against JIVE

The Case Against JIVE Related literature, Two comments and One reply PhD. student Freddy Rojas Cama Econometrics Theory II Rutgers University November 14th, 2011 Literature 1 Literature 2 Key de nitions

The Case Against JIVE Related literature, Two comments and One reply PhD. student Freddy Rojas Cama Econometrics Theory II Rutgers University November 14th, 2011 Literature 1 Literature 2 Key de nitions

EMERGING MARKETS - Lecture 2: Methodology refresher

EMERGING MARKETS - Lecture 2: Methodology refresher Maria Perrotta April 4, 2013 SITE http://www.hhs.se/site/pages/default.aspx My contact: maria.perrotta@hhs.se Aim of this class There are many different

EMERGING MARKETS - Lecture 2: Methodology refresher Maria Perrotta April 4, 2013 SITE http://www.hhs.se/site/pages/default.aspx My contact: maria.perrotta@hhs.se Aim of this class There are many different

Chapter 1 Statistical Inference

Chapter 1 Statistical Inference causal inference To infer causality, you need a randomized experiment (or a huge observational study and lots of outside information). inference to populations Generalizations

Chapter 1 Statistical Inference causal inference To infer causality, you need a randomized experiment (or a huge observational study and lots of outside information). inference to populations Generalizations

Casuality and Programme Evaluation

Casuality and Programme Evaluation Lecture V: Difference-in-Differences II Dr Martin Karlsson University of Duisburg-Essen Summer Semester 2017 M Karlsson (University of Duisburg-Essen) Casuality and Programme

Casuality and Programme Evaluation Lecture V: Difference-in-Differences II Dr Martin Karlsson University of Duisburg-Essen Summer Semester 2017 M Karlsson (University of Duisburg-Essen) Casuality and Programme

OSU Economics 444: Elementary Econometrics. Ch.10 Heteroskedasticity

OSU Economics 444: Elementary Econometrics Ch.0 Heteroskedasticity (Pure) heteroskedasticity is caused by the error term of a correctly speciþed equation: Var(² i )=σ 2 i, i =, 2,,n, i.e., the variance

OSU Economics 444: Elementary Econometrics Ch.0 Heteroskedasticity (Pure) heteroskedasticity is caused by the error term of a correctly speciþed equation: Var(² i )=σ 2 i, i =, 2,,n, i.e., the variance

The gravity models for trade research

The gravity models for trade research ARTNeT-CDRI Capacity Building Workshop Gravity Modelling 20-22 January 2015 Phnom Penh, Cambodia Dr. Witada Anukoonwattaka Trade and Investment Division, ESCAP anukoonwattaka@un.org

The gravity models for trade research ARTNeT-CDRI Capacity Building Workshop Gravity Modelling 20-22 January 2015 Phnom Penh, Cambodia Dr. Witada Anukoonwattaka Trade and Investment Division, ESCAP anukoonwattaka@un.org

The Simple Linear Regression Model

The Simple Linear Regression Model Lesson 3 Ryan Safner 1 1 Department of Economics Hood College ECON 480 - Econometrics Fall 2017 Ryan Safner (Hood College) ECON 480 - Lesson 3 Fall 2017 1 / 77 Bivariate

The Simple Linear Regression Model Lesson 3 Ryan Safner 1 1 Department of Economics Hood College ECON 480 - Econometrics Fall 2017 Ryan Safner (Hood College) ECON 480 - Lesson 3 Fall 2017 1 / 77 Bivariate

Econometrics of Panel Data

Econometrics of Panel Data Jakub Mućk Meeting # 6 Jakub Mućk Econometrics of Panel Data Meeting # 6 1 / 36 Outline 1 The First-Difference (FD) estimator 2 Dynamic panel data models 3 The Anderson and Hsiao

Econometrics of Panel Data Jakub Mućk Meeting # 6 Jakub Mućk Econometrics of Panel Data Meeting # 6 1 / 36 Outline 1 The First-Difference (FD) estimator 2 Dynamic panel data models 3 The Anderson and Hsiao

Motivation Non-linear Rational Expectations The Permanent Income Hypothesis The Log of Gravity Non-linear IV Estimation Summary.

Econometrics I Department of Economics Universidad Carlos III de Madrid Master in Industrial Economics and Markets Outline Motivation 1 Motivation 2 3 4 5 Motivation Hansen's contributions GMM was developed

Econometrics I Department of Economics Universidad Carlos III de Madrid Master in Industrial Economics and Markets Outline Motivation 1 Motivation 2 3 4 5 Motivation Hansen's contributions GMM was developed

Nonlinear Factor Models for Network and Panel Data

Nonlinear Factor Models for Network and Panel Data Mingli Chen Iván Fernández-Val Martin Weidner arxiv:1412.5647v2 [stat.me] 18 Jun 2018 June 19, 2018 Abstract Factor structures or interactive effects

Nonlinear Factor Models for Network and Panel Data Mingli Chen Iván Fernández-Val Martin Weidner arxiv:1412.5647v2 [stat.me] 18 Jun 2018 June 19, 2018 Abstract Factor structures or interactive effects

A Course in Applied Econometrics Lecture 7: Cluster Sampling. Jeff Wooldridge IRP Lectures, UW Madison, August 2008

A Course in Applied Econometrics Lecture 7: Cluster Sampling Jeff Wooldridge IRP Lectures, UW Madison, August 2008 1. The Linear Model with Cluster Effects 2. Estimation with a Small Number of roups and

A Course in Applied Econometrics Lecture 7: Cluster Sampling Jeff Wooldridge IRP Lectures, UW Madison, August 2008 1. The Linear Model with Cluster Effects 2. Estimation with a Small Number of roups and

LECTURE 10. Introduction to Econometrics. Multicollinearity & Heteroskedasticity

LECTURE 10 Introduction to Econometrics Multicollinearity & Heteroskedasticity November 22, 2016 1 / 23 ON PREVIOUS LECTURES We discussed the specification of a regression equation Specification consists

LECTURE 10 Introduction to Econometrics Multicollinearity & Heteroskedasticity November 22, 2016 1 / 23 ON PREVIOUS LECTURES We discussed the specification of a regression equation Specification consists

Robust covariance estimation for quantile regression

1 Robust covariance estimation for quantile regression J. M.C. Santos Silva School of Economics, University of Surrey UK STATA USERS GROUP, 21st MEETING, 10 Septeber 2015 2 Quantile regression (Koenker

1 Robust covariance estimation for quantile regression J. M.C. Santos Silva School of Economics, University of Surrey UK STATA USERS GROUP, 21st MEETING, 10 Septeber 2015 2 Quantile regression (Koenker

HETEROSKEDASTICITY, TEMPORAL AND SPATIAL CORRELATION MATTER

ACTA UNIVERSITATIS AGRICULTURAE ET SILVICULTURAE MENDELIANAE BRUNENSIS Volume LXI 239 Number 7, 2013 http://dx.doi.org/10.11118/actaun201361072151 HETEROSKEDASTICITY, TEMPORAL AND SPATIAL CORRELATION MATTER

ACTA UNIVERSITATIS AGRICULTURAE ET SILVICULTURAE MENDELIANAE BRUNENSIS Volume LXI 239 Number 7, 2013 http://dx.doi.org/10.11118/actaun201361072151 HETEROSKEDASTICITY, TEMPORAL AND SPATIAL CORRELATION MATTER

The Wild Bootstrap, Tamed at Last. Russell Davidson. Emmanuel Flachaire

The Wild Bootstrap, Tamed at Last GREQAM Centre de la Vieille Charité 2 rue de la Charité 13236 Marseille cedex 02, France by Russell Davidson email: RussellDavidson@mcgillca and Emmanuel Flachaire Université

The Wild Bootstrap, Tamed at Last GREQAM Centre de la Vieille Charité 2 rue de la Charité 13236 Marseille cedex 02, France by Russell Davidson email: RussellDavidson@mcgillca and Emmanuel Flachaire Université

Short T Panels - Review

Short T Panels - Review We have looked at methods for estimating parameters on time-varying explanatory variables consistently in panels with many cross-section observation units but a small number of

Short T Panels - Review We have looked at methods for estimating parameters on time-varying explanatory variables consistently in panels with many cross-section observation units but a small number of

TECHNICAL APPENDIX. 7. Agents Decisions in the Cobb-Douglas Case

TECHNICAL APPENDIX 7 Agents Decisions in the Cobb-Douglas Case A closed form solution for production and trade obtains if we assume that utility is a Cobb-Douglas function of the consumption bundle: u

TECHNICAL APPENDIX 7 Agents Decisions in the Cobb-Douglas Case A closed form solution for production and trade obtains if we assume that utility is a Cobb-Douglas function of the consumption bundle: u

The Bivariate Probit Model, Maximum Likelihood Estimation, Pseudo True Parameters and Partial Identification

ISSN 1440-771X Department of Econometrics and Business Statistics http://business.monash.edu/econometrics-and-business-statistics/research/publications The Bivariate Probit Model, Maximum Likelihood Estimation,

ISSN 1440-771X Department of Econometrics and Business Statistics http://business.monash.edu/econometrics-and-business-statistics/research/publications The Bivariate Probit Model, Maximum Likelihood Estimation,

Bias-Correction in Vector Autoregressive Models: A Simulation Study

Econometrics 2014, 2, 45-71; doi:10.3390/econometrics2010045 OPEN ACCESS econometrics ISSN 2225-1146 www.mdpi.com/journal/econometrics Article Bias-Correction in Vector Autoregressive Models: A Simulation

Econometrics 2014, 2, 45-71; doi:10.3390/econometrics2010045 OPEN ACCESS econometrics ISSN 2225-1146 www.mdpi.com/journal/econometrics Article Bias-Correction in Vector Autoregressive Models: A Simulation

mrw.dat is used in Section 14.2 to illustrate heteroskedasticity-robust tests of linear restrictions.

Chapter 4 Heteroskedasticity This chapter uses some of the applications from previous chapters to illustrate issues in model discovery. No new applications are introduced. houthak.dat is used in Section

Chapter 4 Heteroskedasticity This chapter uses some of the applications from previous chapters to illustrate issues in model discovery. No new applications are introduced. houthak.dat is used in Section

On the Power of Tests for Regime Switching

On the Power of Tests for Regime Switching joint work with Drew Carter and Ben Hansen Douglas G. Steigerwald UC Santa Barbara May 2015 D. Steigerwald (UCSB) Regime Switching May 2015 1 / 42 Motivating

On the Power of Tests for Regime Switching joint work with Drew Carter and Ben Hansen Douglas G. Steigerwald UC Santa Barbara May 2015 D. Steigerwald (UCSB) Regime Switching May 2015 1 / 42 Motivating

GMM estimation of spatial panels

MRA Munich ersonal ReEc Archive GMM estimation of spatial panels Francesco Moscone and Elisa Tosetti Brunel University 7. April 009 Online at http://mpra.ub.uni-muenchen.de/637/ MRA aper No. 637, posted

MRA Munich ersonal ReEc Archive GMM estimation of spatial panels Francesco Moscone and Elisa Tosetti Brunel University 7. April 009 Online at http://mpra.ub.uni-muenchen.de/637/ MRA aper No. 637, posted

GARCH Models Estimation and Inference

GARCH Models Estimation and Inference Eduardo Rossi University of Pavia December 013 Rossi GARCH Financial Econometrics - 013 1 / 1 Likelihood function The procedure most often used in estimating θ 0 in

GARCH Models Estimation and Inference Eduardo Rossi University of Pavia December 013 Rossi GARCH Financial Econometrics - 013 1 / 1 Likelihood function The procedure most often used in estimating θ 0 in

Least Absolute Value vs. Least Squares Estimation and Inference Procedures in Regression Models with Asymmetric Error Distributions

Journal of Modern Applied Statistical Methods Volume 8 Issue 1 Article 13 5-1-2009 Least Absolute Value vs. Least Squares Estimation and Inference Procedures in Regression Models with Asymmetric Error

Journal of Modern Applied Statistical Methods Volume 8 Issue 1 Article 13 5-1-2009 Least Absolute Value vs. Least Squares Estimation and Inference Procedures in Regression Models with Asymmetric Error

Heteroskedasticity-Consistent Covariance Matrix Estimators in Small Samples with High Leverage Points

Theoretical Economics Letters, 2016, 6, 658-677 Published Online August 2016 in SciRes. http://www.scirp.org/journal/tel http://dx.doi.org/10.4236/tel.2016.64071 Heteroskedasticity-Consistent Covariance

Theoretical Economics Letters, 2016, 6, 658-677 Published Online August 2016 in SciRes. http://www.scirp.org/journal/tel http://dx.doi.org/10.4236/tel.2016.64071 Heteroskedasticity-Consistent Covariance

The Bootstrap: Theory and Applications. Biing-Shen Kuo National Chengchi University

The Bootstrap: Theory and Applications Biing-Shen Kuo National Chengchi University Motivation: Poor Asymptotic Approximation Most of statistical inference relies on asymptotic theory. Motivation: Poor

The Bootstrap: Theory and Applications Biing-Shen Kuo National Chengchi University Motivation: Poor Asymptotic Approximation Most of statistical inference relies on asymptotic theory. Motivation: Poor

Obtaining Critical Values for Test of Markov Regime Switching

University of California, Santa Barbara From the SelectedWorks of Douglas G. Steigerwald November 1, 01 Obtaining Critical Values for Test of Markov Regime Switching Douglas G Steigerwald, University of

University of California, Santa Barbara From the SelectedWorks of Douglas G. Steigerwald November 1, 01 Obtaining Critical Values for Test of Markov Regime Switching Douglas G Steigerwald, University of

Robust Standard Errors in Small Samples: Some Practical Advice

Robust Standard Errors in Small Samples: Some Practical Advice Guido W. Imbens Michal Kolesár First Draft: October 2012 This Draft: December 2014 Abstract In this paper we discuss the properties of confidence

Robust Standard Errors in Small Samples: Some Practical Advice Guido W. Imbens Michal Kolesár First Draft: October 2012 This Draft: December 2014 Abstract In this paper we discuss the properties of confidence

Bayesian Heteroskedasticity-Robust Regression. Richard Startz * revised February Abstract

Bayesian Heteroskedasticity-Robust Regression Richard Startz * revised February 2015 Abstract I offer here a method for Bayesian heteroskedasticity-robust regression. The Bayesian version is derived by

Bayesian Heteroskedasticity-Robust Regression Richard Startz * revised February 2015 Abstract I offer here a method for Bayesian heteroskedasticity-robust regression. The Bayesian version is derived by

Ordinary Least Squares Regression

Ordinary Least Squares Regression Goals for this unit More on notation and terminology OLS scalar versus matrix derivation Some Preliminaries In this class we will be learning to analyze Cross Section

Ordinary Least Squares Regression Goals for this unit More on notation and terminology OLS scalar versus matrix derivation Some Preliminaries In this class we will be learning to analyze Cross Section

SMOOTHED BLOCK EMPIRICAL LIKELIHOOD FOR QUANTILES OF WEAKLY DEPENDENT PROCESSES

Statistica Sinica 19 (2009), 71-81 SMOOTHED BLOCK EMPIRICAL LIKELIHOOD FOR QUANTILES OF WEAKLY DEPENDENT PROCESSES Song Xi Chen 1,2 and Chiu Min Wong 3 1 Iowa State University, 2 Peking University and

Statistica Sinica 19 (2009), 71-81 SMOOTHED BLOCK EMPIRICAL LIKELIHOOD FOR QUANTILES OF WEAKLY DEPENDENT PROCESSES Song Xi Chen 1,2 and Chiu Min Wong 3 1 Iowa State University, 2 Peking University and

Vector Autoregressive Model. Vector Autoregressions II. Estimation of Vector Autoregressions II. Estimation of Vector Autoregressions I.

Vector Autoregressive Model Vector Autoregressions II Empirical Macroeconomics - Lect 2 Dr. Ana Beatriz Galvao Queen Mary University of London January 2012 A VAR(p) model of the m 1 vector of time series

Vector Autoregressive Model Vector Autoregressions II Empirical Macroeconomics - Lect 2 Dr. Ana Beatriz Galvao Queen Mary University of London January 2012 A VAR(p) model of the m 1 vector of time series