Small Open Economy. Lawrence Christiano. Department of Economics, Northwestern University

|

|

|

- Bertram Paul

- 5 years ago

- Views:

Transcription

1 Small Open Economy Lawrence Christiano Department of Economics, Northwestern University

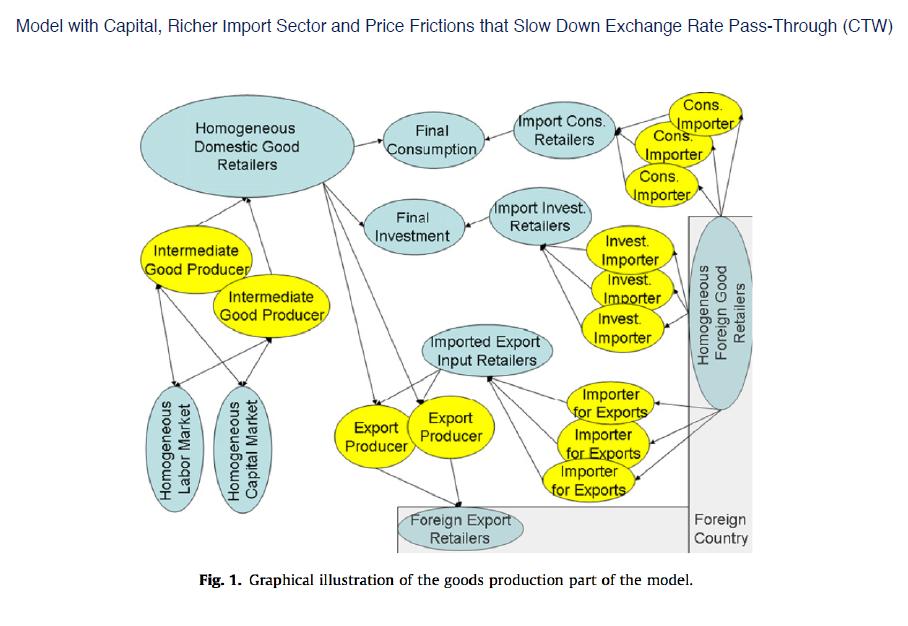

2 Outline Simple Closed Economy Model Extend Model to Open Economy Equilibrium conditions Indicate complications to bring the model to the data. Similar in spirit to Ramses I model Adolfson-Laséen-Lindé-Villan at Swedish Riksbank Brief Discussion of Introducing Financial Frictions Christiano-Trabandt-Walentin (CTW) Model, Ramses II model. Based on Christiano-Motto-Rostagno ( Risk Shocks ) Mihai Copaciu of Romanian Central Bank. Application: will US lift off act like a locomotive to rest of world economy, or will it be a problem (especially for EME s)?

3 Simple Closed Economy Model Results from closed economy model Household preferences: ( E 0 β t { t=0 u (C t ) exp (τ t ) N1+ϕ t 1 + ϕ ), u (C t ) log C t Aggregate resources and household intertemporal optimization: Y t = pt R t A t N t, u c,t = βe t u c,t+1 π t+1 Law of motion of price distortion: ( pt 1 θ (π t ) = (1 ε 1 θ) 1 θ ) ε ε 1 + θπε t pt 1 1 (1)

4 Simple Closed Economy Model Equilibrium conditions associated with price setting: Y t C t + E t π ε 1 t+1 βθf t+1 = F t (2) [ 1 θπ ε 1 t F t 1 θ ] 1 1 ε = K t (3) ε (1 ν) ε 1 = W t Pt by household optimization {}}{ exp (τ t ) N ϕ t 1 Y t u c,t A t C t +E t βθπt+1k ε t+1 = K t (4) note: in simple closed economy model, Y t = C t, but this is not so in open economy. For a derivation in the simple closed economy, see, e.g., Labor_market_handout.pdf

5

6 Extensions to Small Open Economy Outline: the equilibrium conditions of the open economy model system jumps from 6 equations in basic model to 16 equations in 16 variables!

7 Extensions to Small Open Economy: 16 variables rate of depreciation, exports, real foreign assets, terms of trade, real exchange rate {}}{ s t, x t, a f t, p x t, q t price of domestic consumption (now, c is a composite of domestically produced goods & imports) {}}{ p c t price of imports {}}{ p m t consumption price inflation {}}{ π c t reduced form object to (i) achieve technical objective, (ii) adjust UIP implication {}}{ Φ t closed economy variables {}}{ R t, π t, N t, c t, K t, F t, p t

8 Extensions to Small Open Economy- Outline After describing 16 equilibrium conditions: compute the steady state the uncovered interest parity puzzle, and the role of Φ t in addressing the puzzle. summary of the endogenous and exogenous variables of the model, as well as the equations. several computational experiments to illustrate the properties of the model.

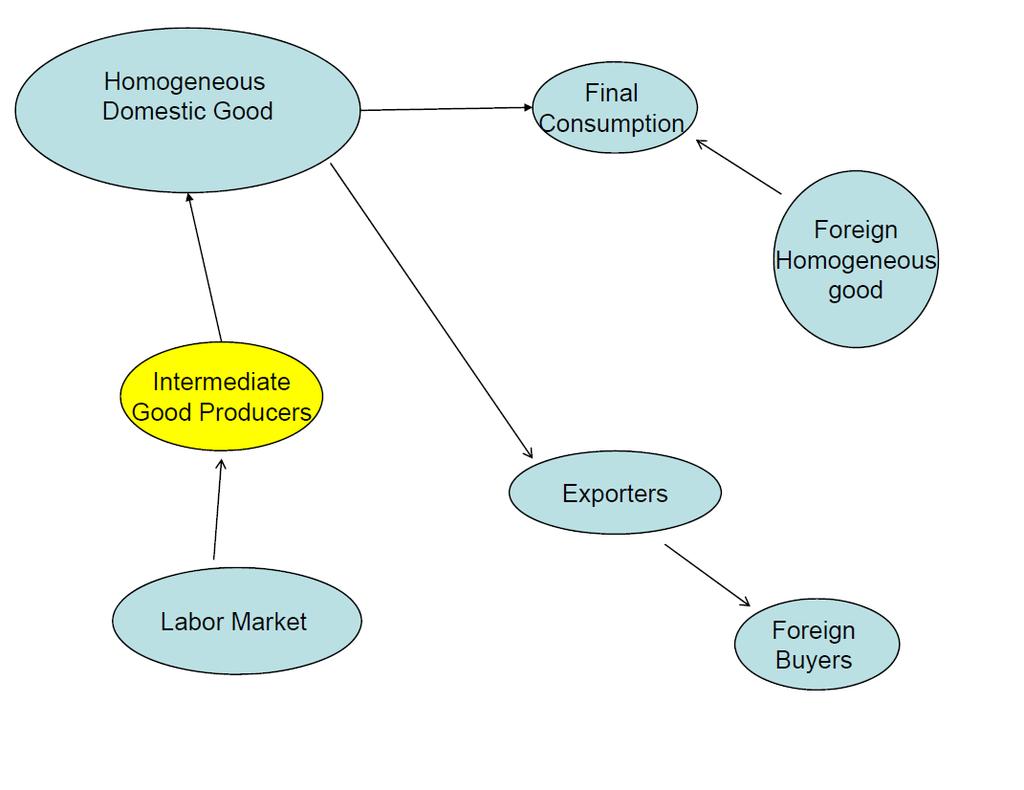

9 Modifications to Simple Model to Create Open Economy Unchanged: household preferences production of (domestic) homogeneous good, Y t (= A t pt N t) three Calvo price friction equations Changes: household budget constraint includes opportunity to acquire foreign assets/liabilities. intertemporal Euler equation changed as a reduced form accommodation of evidence on uncovered interest parity. Y t = C t no longer true. introduce exports, imports, balance of payments. exchange rate, S t = domestic currency price of one unit of foreign currency domestic money S t = foreign money

10 Monetary Policy: two approaches Taylor rule ( ) Rt log R = ρ R log +r y log ( Rt 1 R ( yt+1 y ) + (1 ρ R ) E t [r π log ) ] + ε R,t ( π c ) t+1 π c (5) where (could also add exchange rate, real exchange rate and other things): π c ~target consumer price inflation ε R,t ~iid, mean zero monetary policy shock y t ~Y t /A t R t ~ risk free nominal rate of interest ε R,t ~mean zero monetary policy shock.

11 Monetary Policy: two approaches Second approach (Norges Bank, Riksbank) Solve a type of Ramsey problem in which preferences correspond to preferences of monetary policy committee: ( E t β j { 100 [π c t π c t 1 πc t 2 πc t 3 (πc ) 4]) 2 j=0 ( )) 2 yt + λ y (100 log y +λ R (400 [R t R t 1 ]) 2 + λ s (S t S) 2 } straightforward to implement in Dynare. We will stress first approach.

12 Household Budget Constraint Uses of funds less than or equal to sources of funds S t A f t+1 + P t C t + B t+1 B t R t 1 + S t [Φ t 1 R f t 1 Domestic bonds Foreign assets ] A f t + W t N t + transfers and profits t B t ~beginning of period t stock of loans R t ~rate of return on bonds A f t ~beginning-of-period t net stock of foreign assets (liabilities, if negative) held by domestic residents. Φ t Rt f ~rate of return on A f t Φ t ~premium on foreign asset returns

13 Household Intertemporal First Order Conditions: Foreign Assets Optimality of foreign asset choice (verify this by solving Lagrangian representation of household problem) utility cost of 1 unit of foreign currency=s t units of domestic currency, S t /P c t {}}{ u c,t S t P c t units of C t conversion into utility units {}}{ = βe t u c,t+1 quantity of domestic cons. goods purchased from the payoff of 1 unit of foreign currency {}}{ foreign currency payoff next period from one unit of foreign currency today {}}{ S t+1 Rt f Φ t Pt+1 c

14 Household Intertemporal First Order Conditions: Foreign Assets First order condition: Scaling: S t P c t C t = βe t S t+1 R f t Φ t P c t+1 C t+1 1 c t = βe t s t+1 R f t Φ t π c t+1 c t+1 exp ( a t+1 ), s t S t S t 1, c t = C t A t. (6) Technology: a t log (A t ), a t = a t a t 1.

15 Household Intertemporal First Order Conditions: Domestic Assets First order condition: Scaling: 1 R t Pt c = βe t C t Pt+1 c C t+1 1 R t = βe t c t π c t+1 c t+1 exp ( a t+1 ). (7)

16 Final Domestic Consumption Goods Produced by representative, competitive firm using: where C t = [ (1 ω c ) 1 η c ( C d t ) η c 1 η c + ω 1 ηc c ] ηc (Ct m ) η c 1 η c 1 η c Ct d ~ domestic homogeneous output good, price P t Ct m ~ imported good, price Pt m ( St Pt f ) C t ~ final consumption good, Pt c η c ~ elasticity of substitution, domestic and foreign goods.

17 Final Domestic Consumption Goods Profit maximization by representative firm: max P c t C t P m t C m t P t C d t, subject to production function. First order conditions associated with maximization: C m t : P c t ( ) 1 = ω Ct ηc c Ct {}} m { dc t dct m = P m t, C d t : P c t ( ) 1 ηc = (1 ω c ) C t Ct {}}{ d dc t dct d = P t so that the demand functions are: C m t = ω c ( P c t P m t ) ηc Ct, C d t = (1 ω c ) ( ) P c ηc t Ct. P t

18 Price Function Substituting demand functions back into the production function: or C t = [(1 ω c ) 1 η c (C t ( P c t +ω p c t = 1 η c c ( ω c ( P c t P m t P t ) ηc (1 ωc )) η c 1 η c ) ηc Ct ) η c 1 η c ] η c η c 1, [ ] (1 ω c ) + ω c (pt m ) 1 η 1 1 η, c c (8) where p c t Pc t P t, p m t Pm t P t.

19 Real Exchange Rate and Consumption Price Inflation Real Exchange Rate: p m t = Pc t P c t = p c t P m t P t S t P f t P c t, real exchange rate {}}{ q t (9) Consumption good inflation and homogeneous good inflation: π c t Pc t P c t 1 = P tp c t P t 1 p c t 1 = π t [ (1 ω c ) + ω c (p m t ) 1 η c (1 ω c ) + ω c ( p m t 1 ) 1 ηc ] 1 1 η c (10)

20 Exports Foreign demand for domestic goods: ( P x X t = t P f t ) ηf Y f t = (p x t ) η f Y f t, terms of trade {}}{ p x t = Px t P f t Yt f ~ foreign output Pt f ~ foreign currency price of foreign good Pt x ~ foreign currency price of export good Scaling by A t x t = (p x t ) η f y f t (11)

21 Rate of Depreciation, Inflation... Competition: Price of export equals marginal cost: Scaling: Also, S t P x t = P t. 1 = S tpt x = Pc t S t Pt f Pt x P t P t Pt c Pt f = q t pt x pt c (12) q t π = f t s t q t 1 π c, s t S t, π f t t S t 1 Pf t P f t 1 (13)

22 Homogeneous Goods Market Clearing Clearing in domestic homogeneous goods market: output of domestic homogeneous good, Y t = uses of domestic homogeneous goods = goods used in production of final consumption, C t {}}{ exports government {}}{{}}{ Ct d + X t + G t = (1 ω c ) (p c t ) η c C t + X t + G t.

23 Aggregate Employment and Uses of Homogeneous Goods Substituting out in previous expression for Y t : A t p t N t = (1 ω c ) (p c t ) η c C t + X t + G t, or, p t N t = (1 ω c ) (p c t ) η c c t + x t + g t, (14) c t C t A t, x t X t A t, g t G t A t.

24 Balance of Payments equality of international flows relating to trade in goods and in financial assets: acquisition of new net foreign assets, in domestic currency units {}}{ S t A f t+1 + expenses on imports t = receipts from exports t + receipts from existing stock of net foreign assets {}}{ S t R f t 1Φ t 1 A f t

25 Balance of Payments, the Pieces Exports and imports: expenses on imports t = S t P f t ω c ( p c t receipts from exports t = S t P x t X t. p m t ) ηc C t Balance of payments: ) ηc Ct ( p S t A f t+1 + S t Pt f c ω t c pt m = S t Pt x X t + S t Rt 1Φ f t 1 A f t.

26 Balance of Payments, Scaling Scaling by P t A t : S t A f t+1 P t A t + S tp f t P t ω c ( p c t p m t ) ηc ct or, = S tp x t P t x t + S tr f t 1 Φ t 1A f t P t A t, a f t + p m t ω c ( p c t p m t ) ηc ct = pt c q t pt x x t + s trt 1 f Φ t 1at 1 f, (15) π t exp ( a t ) where a f t is scaled, homogeneous goods value of net foreign assets : a f t = S ta f t+1 P t A t.

27 Risk Term ) Φ t = Φ (at f, Rt f, R t, φ t = (16) ( ) ( exp ( φ a at f ā + φ s R t Rt f (R )) ) R f + φ t φ a > 0, small and not important for dynamics φ s > 0, important φ t ~mean zero, iid. Discussion of φ a. φ a > 0 implies (i) if at f > ā, then return on foreign assets low and f ; (ii) if at f < ā, then return on foreign assets high and at f implication: φ a > 0 is a force that drives at f ā in steady state, independent of initial conditions. logic is same as reason why steady state stock of capital in neoclassical growth model is unique, independent of initial conditions. in practice, put in a tiny value of φ a, so that its only effect is to pin down at f in steady state and it does not affect dynamics (see Schmitt-Grohe and Uribe).

28 Risk Term Discussion of φ t : Captures, informally, the possibility that there is a shock to the required return on domestic assets. Discussion of φ s : When φ t > 0, capital outflow shock, people stop liking domestic assets When φ t < 0, safe haven shock, people love domestic assets (e.g., Swiss Franc in recent years). φ s reduced form fix for the model. With φ s = 0, model implies Uncovered Interest Parity (UIP), which does not hold in the data. to better explain this, it is convenient to first solve for the model s steady state.

29 Steady State household intertemporal effi ciency conditions: sr 1 = f β π c exp ( a) (6) R 1 = β π c exp ( a) (7) assumption about foreign households: π f t Pf t P f t 1 (exogenous) R f 1 = β π f exp ( a)

30 Steady State Taylor rule implies: π c = π c, (5). Additional steady state equations: π P t P t 1 = π c (inflation target) (10) p = s = πc π f, R = R f = R/s 1 θπ ε 1 θ ( 1 θ(π) ε 1 1 θ π exp ( a) β ) ε, (no distortion if π c = 1) (1) ε 1 (13) (7) ((6),(7))

31 Steady State, Potentially Iterative Part Rest of the algorithm solves a single non-linear equation in a single unknown, ϕ. Set ϕ = p c q p m = ϕ (9) and p x = 1 ϕ (12) p c = [ ] (1 ω c ) + ω c (p m ) 1 η 1 1 η c c (8) q = ϕ p c

32 Steady State, Potentially Iterative Part... Let g = η g y, ā = η a y. Then, ( ) p 0 = p m c ηc ( ω c c p c p m qp x sr x f ) π exp ( a) 1 η a p N (15) ) 0 = (1 ω c ) (p c ) η c c + x (1 η g Np (14) p F = N c (1 π ε 1 βθ) (2) [ ] 1 1 θπ ε 1 1 ε K = F (3) 1 θ ε 0 = ε 1 (1 ν) N1+ϕ p + (βθπ ε 1) K (4), These five equations involve the five unknowns: c, N, F, K, x. Solve these. Adjust ϕ until (11) is satisfied. In practice, we simply set ϕ = 1 and used (11) to solve for y f.

33 Uncovered Interest Parity Algebra subtract equations (6) and (7): [ R t s t+1 R f ] t Φ t E t c t+1 π c t+1 exp ( a = 0. t+1) totally different object in square brackets and evaluate in steady state: where R t s d t+1 Rt f Φ t c t+1 π c t+1 exp ( a t+1) dr t = cπ c exp ( a) 1 ] [sr f cπ c dφ t + sdrt f + R f ds exp ( a) t+1 R sr f [cπ c exp ( a)] 2 d [ c t+1 π c t+1 exp ( a t+1) ] = 1 { [ ]} ˆR t ˆΦ t + ˆR t f + ŝ t+1 βc ˆx t (x t x) /x = dx t /x.

34 Uncovered Interest Parity, Linearized Representation Then, is, to a first approximation, or, [ R t s t+1 R f ] t Φ t E t c t+1 π c t+1 exp ( a = 0, t+1) [ 1 { [ ]} ] E t ˆR t ˆΦ t + ˆR t f + ŝ t+1 = 0 βc ˆR t = E t ŝ t+1 + ˆR f t + ˆΦ t. Conclude, using dx t x log (x t /x), log Φ = 0 : log R t log R = E t [log s t+1 log (s)] + log R f t log R f + log Φ t or, using log R f = log R log s, definition of s t+1, r t log R t, rt f log Rt f E t log S t+1 log S t = r t r f t + log Φ t

35 Uncovered Interest Parity Under UIP, ˆΦ t = 0 : r t > r f t must be an anticipated depreciation (instantaneous appreciation) of the currency for people to be happy holding the existing stock of net foreign assets Consider regression relation: log S t+1 log S t = β 0 + β 1 (r t r f t ) + u t. Under UIP (and, rational expectations), ˆβ 0 = 0, ˆβ 1 = 1. When ˆΦ t = 0: ˆβ 1 = cov ( log S t+1 log S t, r t rt f ) var ( ) r t rt f = 1 φ s,

36 UIP Puzzle In data, ˆβ 1.75, so UIP rejected (that s the UIP puzzle) Note: because φ s = 1.75 ˆβ 1 = ˆβ 1 = cov ( log S t+1 log S t, r t rt f ) var ( ) r t rt f = 1 φ s, Another way to see UIP puzzle is from VAR impulse responses by Eichenbaum and Evans (QJE, 1992) Data: r t after monetary policy shock log S t+j falls slowly for j = 1, 2, 3,.... UIP theory: r t after monetary policy shock log S t+1 log S t.

37 Intuition Behind UIP Puzzle UIP puzzle: r t and expected appreciation of the currency represents a double-boost to the return on domestic assets. On the face of it, it appears that there is an irresistible profit opportunity. Why doesn t the double-boost to domestic returns launch an avalanche of pressure to buy the domestic currency? In standard models, this pressure produces a greater instantaneous appreciation in the exchange rate, until the familiar UIP overshooting result emerges - the pressure to buy the currency leads to such a large appreciation, that expectations of depreciation emerge. In this way, UIP leads to the counterfactual prediction that a higher r t will be followed (after an instantaneous appreciation) by a period of time during which the currency depreciates.

38 Intuition Behind Resolution of Puzzle Model s resolution of the UIP puzzle: when r t the return required for people to hold domestic bonds rises. This is why the double-boost to domestic returns does not create an appetite to buy large amounts of domestic assets. Possibly this is a reduced form way to capture the notion that increases in r t make the domestic economy more risky. (However, the precise mechanism by which the domestic required return rises - earnings on foreign assets go up - may be diffi cult to interpret. An alternative specification was explored, with risk-premia affecting domestic bonds, but this resulted in indeterminacy problems.)

39 Dynamics 16 equations: price setting, (1),(2),(3),(4); monetary policy rule, (5); household intertemporal Euler equations (6),(7); relative price equations (8),(9),(10),(12),(13); aggregate resource condition, (14); balance of payments, (15); risk term, (16); demand for exports (11). 16 endogenous variables: p c t, p m t, q t, R t, π t, π c t, p x t, N t, p t, a f t, Φ t, s t, x t, c t, K t, F t. exogenous variables: R f t, y f t, φ t, g t, ε R,t, a t, τ t, π f t. for the purpose of numerical calculations, these were modeled as independent scalar AR(1) processes.

40 Extensions to Small Open Economy... the model was solved in the manner described above: - compute the steady state using the formulas described above - log-linearize the 16 equations about steady state - solve the log-linearized system - these calculations were made easy by implementing them in Dynare.

41 Parameter Values Numerical examples: Parameter values: π f = π c = φ a = 0.03 β = /4 θ = 3/4 ϕ = 1 ε = 6 1 ν = ε 1 ε η c = 5 ω c = 0.4 η g = 0.3 η a = 0 η f = 1.5 ρ R = 0.9 r π = 1.5 r y = 0.15

42 Modifying UIP iid shock, 0.01, to ε R,t. φ s = 0 after instantaneous appreciation, positive ε R,t shock followed by depreciation. for higher φ s, shock followed by appreciation. long run appreciation is increasing function of persistence of ρ R.

43 Impact of Modifications to UIP We now consider a monetary policy shock, ε R,t = According to (5), implies a four percentage point (at an annual rate) policy-induced jump in R t. The dynamic effects are displayed in the following figure, for φ s = 0, φ s = 1.75 Note: (i) appreciation smaller, though more drawn out, when φ s is big; (ii) smaller appreciation results in smaller drop in net exports, so less of a drop in demand, so less fall in output and inflation; (iii) smaller drop in net exports results in smaller drop in real foreign assets.

44 Capital Outflow Shock Consider now a domestic economy risk premium shock, a jump in the innovation to φ t equal to With the reduced interest in domestic assets, (i) the currency depreciates, (ii) net exports rise, (iii) hours and output rise, (iv) the upward pressure on costs associated with higher output leads to a rise in prices.

45

46

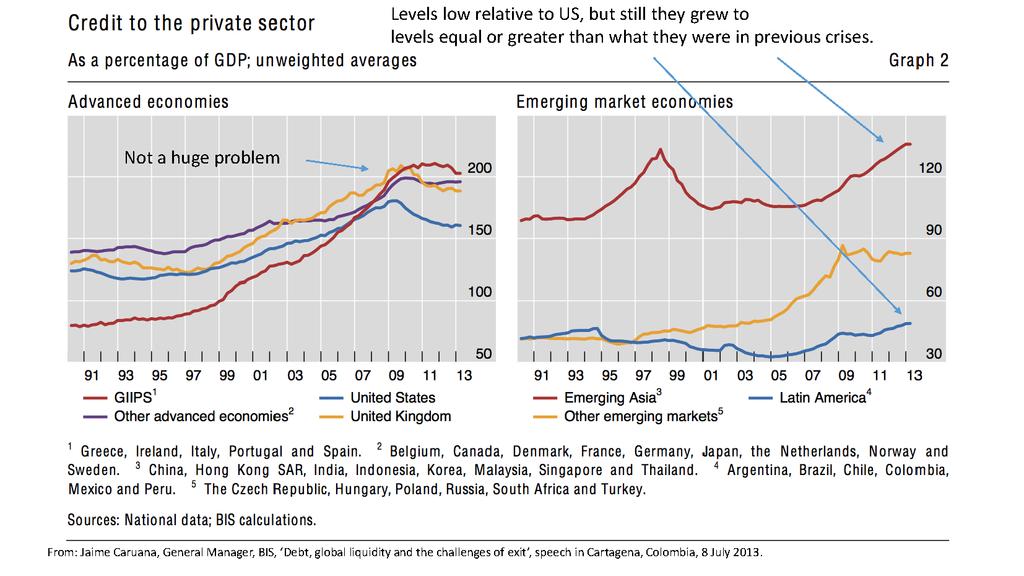

47 Question Confronting Many Emerging Market Economies.. At some point, the Fed will implement its exit strategy and raise US interest rates ( basis points?). In the past, when Fed raised rates sharply (e.g., 1982 Volcker disinflation, 1994 run-up in interest rates), hit the rest of world like a brick: Chilean crisis of 1982, Mexican default of August Mexican crisis of Will the US exit strategy inflict financial crises around the world, especially in emerging market economies? Summer 2013 taper episode makes people worry about this possibility. I ll call the above possibility the BIS scenario.

48 BIS Scenario Low US interest rates since 2008 have encouraged excessive accumulation of debt in the world. This has particularly affected emerging market economies in Asia andlatin America.

49

50 Currency Mismatch Problem May Be Understated.. (Hyun Shin, The Second Phase of Global Liquidity..., November, 2013) Many emerging market borrowers issue dollar-denominated debt through foreign subsidiaries (say in the UK). By the usual definition (based on the residence of the issuer), the bonds are a liability of the UK entity. But, it s the consolidated balance sheet that matters to the emerging market firm. So, the debt issued via a foreign subsidiary could make the emerging market firm vulnerable to currency mismatch problems.

51 Hyun Shin argues: Amount of dollar denominated debt from emerging market firms may be greatly understated. This is suggested by evidence that foreign currency debt by nationality can be much larger than foreign debt by the usual residency definition.

52

53

54

55 Shin conjectures that distinction between external debt according to nationality and residence helps to resolve the taper puzzle: convulsions in emerging markets during taper episode in summer 2013 seem inconsistent with apparently small net external debt position (measured in residence terms) of firms in emerging markets. Less surprising if external debt position is in fact much bigger.

56 BIS Scenario US raises interest rates. Emerging market exchange rates depreciate. Financial health of emerging market firms compromised. They cut back on investment activity....recessions start. Runs on emerging market banks known to be have made loans to now-questionable emerging market non-financial firms. And so on...

57 Locomotive Scenario Previous episodes of US interest rate hikes may be playing too big a role in the pessimistic outlook. The circumstances in which the US raises interest rates may make a difference. In present circumstances, Fed has (credibly, I think) committed to only raise rates until well after the US economy has returned to health. Under these circumstances, interest rate hikes occur when the US is firmly in the position of a locomotive, pulling the rest of the world economy forward in its wake.

58 Which Will it Be: BIS or Locomotive Scenario? Need a model to think about this question. Build in the BIS-type factors that raise concerns about the world economy. Accurately capture the degree of foreign currency indebtedness of financial and nonfinancial firms (i.e., avoid the biases that Hyun Shin is concerned about). Build in the nature of the constraints that cause firms to pull back when their net worth contracts with exchange rate depreciation. Build in the locomotive scenario: Carefully model forward guidance Fed commitment to keep interest rates low even after the US economy has begun to strengthen.

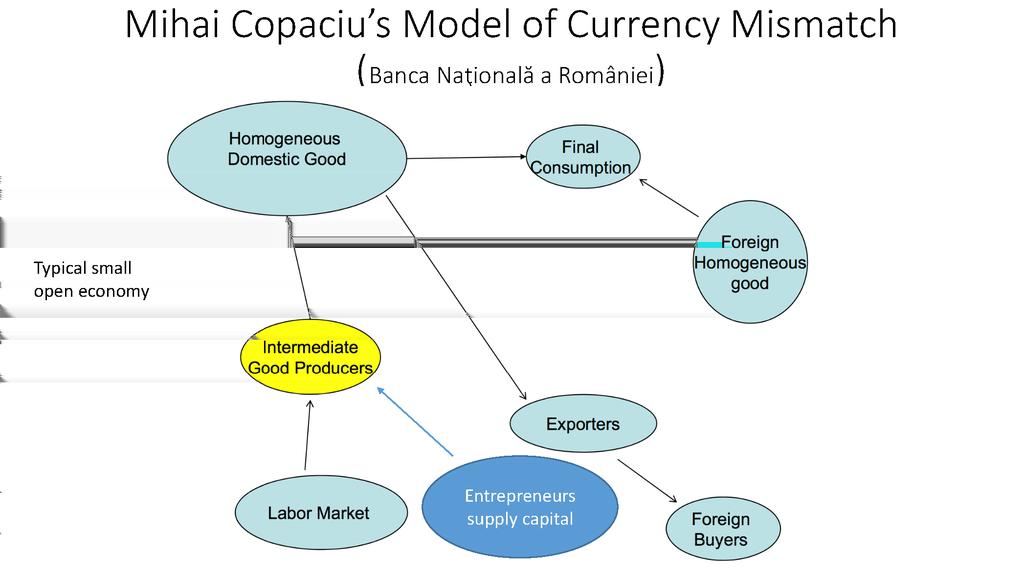

59 A Model Mihai Copaciu (Romanian Central Bank) Constructs small open economy models in which investment is sustained by purchases of entrepreneurs, who earn their revenues in domestic currency units. Entrepreneurs need financing, and the amount of financing they can get is partially a function of their accumulated net worth. Some of the financing is obtained from abroad. When the currency depreciates, entrepreneurs that borrowed abroad make capital losses and their net worth suffers. They are forced to cut back on expenditures, so that investment crashes, bringing down the economy. Same model also contains the usual features that imply an expansion in the US acts as a locomotive on the rest of the world.

60

61

62 DSGE Models Can Play a Useful Role in Discussions about Fed Exit Strategy New Keynesian Open Economy Models can Capture Two Competing Views. Potential for US take-off to: be a locomotive. cause a loss of net worth by foreign firms/financial institutions and force a cut-back in foreign investment ( BIS scenario ).

Simple New Keynesian Model without Capital

Simple New Keynesian Model without Capital Lawrence J. Christiano January 5, 2018 Objective Review the foundations of the basic New Keynesian model without capital. Clarify the role of money supply/demand.

Simple New Keynesian Model without Capital Lawrence J. Christiano January 5, 2018 Objective Review the foundations of the basic New Keynesian model without capital. Clarify the role of money supply/demand.

Simple New Keynesian Model without Capital

Simple New Keynesian Model without Capital Lawrence J. Christiano March, 28 Objective Review the foundations of the basic New Keynesian model without capital. Clarify the role of money supply/demand. Derive

Simple New Keynesian Model without Capital Lawrence J. Christiano March, 28 Objective Review the foundations of the basic New Keynesian model without capital. Clarify the role of money supply/demand. Derive

Foundations for the New Keynesian Model. Lawrence J. Christiano

Foundations for the New Keynesian Model Lawrence J. Christiano Objective Describe a very simple model economy with no monetary frictions. Describe its properties. markets work well Modify the model to

Foundations for the New Keynesian Model Lawrence J. Christiano Objective Describe a very simple model economy with no monetary frictions. Describe its properties. markets work well Modify the model to

Financial Factors in Economic Fluctuations. Lawrence Christiano Roberto Motto Massimo Rostagno

Financial Factors in Economic Fluctuations Lawrence Christiano Roberto Motto Massimo Rostagno Background Much progress made on constructing and estimating models that fit quarterly data well (Smets-Wouters,

Financial Factors in Economic Fluctuations Lawrence Christiano Roberto Motto Massimo Rostagno Background Much progress made on constructing and estimating models that fit quarterly data well (Smets-Wouters,

Lecture 4 The Centralized Economy: Extensions

Lecture 4 The Centralized Economy: Extensions Leopold von Thadden University of Mainz and ECB (on leave) Advanced Macroeconomics, Winter Term 2013 1 / 36 I Motivation This Lecture considers some applications

Lecture 4 The Centralized Economy: Extensions Leopold von Thadden University of Mainz and ECB (on leave) Advanced Macroeconomics, Winter Term 2013 1 / 36 I Motivation This Lecture considers some applications

The New Keynesian Model: Introduction

The New Keynesian Model: Introduction Vivaldo M. Mendes ISCTE Lisbon University Institute 13 November 2017 (Vivaldo M. Mendes) The New Keynesian Model: Introduction 13 November 2013 1 / 39 Summary 1 What

The New Keynesian Model: Introduction Vivaldo M. Mendes ISCTE Lisbon University Institute 13 November 2017 (Vivaldo M. Mendes) The New Keynesian Model: Introduction 13 November 2013 1 / 39 Summary 1 What

problem. max Both k (0) and h (0) are given at time 0. (a) Write down the Hamilton-Jacobi-Bellman (HJB) Equation in the dynamic programming

and h (0) are given at time 0. (a) Write down the Hamilton-Jacobi-Bellman (HJB) Equation in the dynamic programming") 1. Endogenous Growth with Human Capital Consider the following endogenous growth model with both physical capital (k (t)) and human capital (h (t)) in continuous time. The representative household solves

1. Endogenous Growth with Human Capital Consider the following endogenous growth model with both physical capital (k (t)) and human capital (h (t)) in continuous time. The representative household solves

Simple New Keynesian Model without Capital. Lawrence J. Christiano

Simple New Keynesian Model without Capital Lawrence J. Christiano Outline Formulate the nonlinear equilibrium conditions of the model. Need actual nonlinear conditions to study Ramsey optimal policy, even

Simple New Keynesian Model without Capital Lawrence J. Christiano Outline Formulate the nonlinear equilibrium conditions of the model. Need actual nonlinear conditions to study Ramsey optimal policy, even

Macroeconomics II. Dynamic AD-AS model

Macroeconomics II Dynamic AD-AS model Vahagn Jerbashian Ch. 14 from Mankiw (2010) Spring 2018 Where we are heading to We will incorporate dynamics into the standard AD-AS model This will offer another

Macroeconomics II Dynamic AD-AS model Vahagn Jerbashian Ch. 14 from Mankiw (2010) Spring 2018 Where we are heading to We will incorporate dynamics into the standard AD-AS model This will offer another

Dynamic AD-AS model vs. AD-AS model Notes. Dynamic AD-AS model in a few words Notes. Notation to incorporate time-dimension Notes

Macroeconomics II Dynamic AD-AS model Vahagn Jerbashian Ch. 14 from Mankiw (2010) Spring 2018 Where we are heading to We will incorporate dynamics into the standard AD-AS model This will offer another

Macroeconomics II Dynamic AD-AS model Vahagn Jerbashian Ch. 14 from Mankiw (2010) Spring 2018 Where we are heading to We will incorporate dynamics into the standard AD-AS model This will offer another

Foundations for the New Keynesian Model. Lawrence J. Christiano

Foundations for the New Keynesian Model Lawrence J. Christiano Objective Describe a very simple model economy with no monetary frictions. Describe its properties. markets work well Modify the model dlto

Foundations for the New Keynesian Model Lawrence J. Christiano Objective Describe a very simple model economy with no monetary frictions. Describe its properties. markets work well Modify the model dlto

Optimal Simple And Implementable Monetary and Fiscal Rules

Optimal Simple And Implementable Monetary and Fiscal Rules Stephanie Schmitt-Grohé Martín Uribe Duke University September 2007 1 Welfare-Based Policy Evaluation: Related Literature (ex: Rotemberg and Woodford,

Optimal Simple And Implementable Monetary and Fiscal Rules Stephanie Schmitt-Grohé Martín Uribe Duke University September 2007 1 Welfare-Based Policy Evaluation: Related Literature (ex: Rotemberg and Woodford,

Resolving the Missing Deflation Puzzle. June 7, 2018

Resolving the Missing Deflation Puzzle Jesper Lindé Sveriges Riksbank Mathias Trabandt Freie Universität Berlin June 7, 218 Motivation Key observations during the Great Recession: Extraordinary contraction

Resolving the Missing Deflation Puzzle Jesper Lindé Sveriges Riksbank Mathias Trabandt Freie Universität Berlin June 7, 218 Motivation Key observations during the Great Recession: Extraordinary contraction

Fiscal Multipliers in a Nonlinear World

Fiscal Multipliers in a Nonlinear World Jesper Lindé and Mathias Trabandt ECB-EABCN-Atlanta Nonlinearities Conference, December 15-16, 2014 Sveriges Riksbank and Federal Reserve Board December 16, 2014

Fiscal Multipliers in a Nonlinear World Jesper Lindé and Mathias Trabandt ECB-EABCN-Atlanta Nonlinearities Conference, December 15-16, 2014 Sveriges Riksbank and Federal Reserve Board December 16, 2014

Monetary Economics: Solutions Problem Set 1

Monetary Economics: Solutions Problem Set 1 December 14, 2006 Exercise 1 A Households Households maximise their intertemporal utility function by optimally choosing consumption, savings, and the mix of

Monetary Economics: Solutions Problem Set 1 December 14, 2006 Exercise 1 A Households Households maximise their intertemporal utility function by optimally choosing consumption, savings, and the mix of

Economics 232c Spring 2003 International Macroeconomics. Problem Set 3. May 15, 2003

Economics 232c Spring 2003 International Macroeconomics Problem Set 3 May 15, 2003 Due: Thu, June 5, 2003 Instructor: Marc-Andreas Muendler E-mail: muendler@ucsd.edu 1 Trending Fundamentals in a Target

Economics 232c Spring 2003 International Macroeconomics Problem Set 3 May 15, 2003 Due: Thu, June 5, 2003 Instructor: Marc-Andreas Muendler E-mail: muendler@ucsd.edu 1 Trending Fundamentals in a Target

Fiscal Multipliers in a Nonlinear World

Fiscal Multipliers in a Nonlinear World Jesper Lindé Sveriges Riksbank Mathias Trabandt Freie Universität Berlin November 28, 2016 Lindé and Trabandt Multipliers () in Nonlinear Models November 28, 2016

Fiscal Multipliers in a Nonlinear World Jesper Lindé Sveriges Riksbank Mathias Trabandt Freie Universität Berlin November 28, 2016 Lindé and Trabandt Multipliers () in Nonlinear Models November 28, 2016

Monetary Policy in a Macro Model

Monetary Policy in a Macro Model ECON 40364: Monetary Theory & Policy Eric Sims University of Notre Dame Fall 2017 1 / 67 Readings Mishkin Ch. 20 Mishkin Ch. 21 Mishkin Ch. 22 Mishkin Ch. 23, pg. 553-569

Monetary Policy in a Macro Model ECON 40364: Monetary Theory & Policy Eric Sims University of Notre Dame Fall 2017 1 / 67 Readings Mishkin Ch. 20 Mishkin Ch. 21 Mishkin Ch. 22 Mishkin Ch. 23, pg. 553-569

Advanced Macroeconomics

Advanced Macroeconomics The Ramsey Model Marcin Kolasa Warsaw School of Economics Marcin Kolasa (WSE) Ad. Macro - Ramsey model 1 / 30 Introduction Authors: Frank Ramsey (1928), David Cass (1965) and Tjalling

Advanced Macroeconomics The Ramsey Model Marcin Kolasa Warsaw School of Economics Marcin Kolasa (WSE) Ad. Macro - Ramsey model 1 / 30 Introduction Authors: Frank Ramsey (1928), David Cass (1965) and Tjalling

Dynamic stochastic general equilibrium models. December 4, 2007

Dynamic stochastic general equilibrium models December 4, 2007 Dynamic stochastic general equilibrium models Random shocks to generate trajectories that look like the observed national accounts. Rational

Dynamic stochastic general equilibrium models December 4, 2007 Dynamic stochastic general equilibrium models Random shocks to generate trajectories that look like the observed national accounts. Rational

A Modern Equilibrium Model. Jesús Fernández-Villaverde University of Pennsylvania

A Modern Equilibrium Model Jesús Fernández-Villaverde University of Pennsylvania 1 Household Problem Preferences: max E X β t t=0 c 1 σ t 1 σ ψ l1+γ t 1+γ Budget constraint: c t + k t+1 = w t l t + r t

A Modern Equilibrium Model Jesús Fernández-Villaverde University of Pennsylvania 1 Household Problem Preferences: max E X β t t=0 c 1 σ t 1 σ ψ l1+γ t 1+γ Budget constraint: c t + k t+1 = w t l t + r t

Final Exam. You may not use calculators, notes, or aids of any kind.

Professor Christiano Economics 311, Winter 2005 Final Exam IMPORTANT: read the following notes You may not use calculators, notes, or aids of any kind. A total of 100 points is possible, with the distribution

Professor Christiano Economics 311, Winter 2005 Final Exam IMPORTANT: read the following notes You may not use calculators, notes, or aids of any kind. A total of 100 points is possible, with the distribution

Can News be a Major Source of Aggregate Fluctuations?

Can News be a Major Source of Aggregate Fluctuations? A Bayesian DSGE Approach Ippei Fujiwara 1 Yasuo Hirose 1 Mototsugu 2 1 Bank of Japan 2 Vanderbilt University August 4, 2009 Contributions of this paper

Can News be a Major Source of Aggregate Fluctuations? A Bayesian DSGE Approach Ippei Fujiwara 1 Yasuo Hirose 1 Mototsugu 2 1 Bank of Japan 2 Vanderbilt University August 4, 2009 Contributions of this paper

Learning and Global Dynamics

Learning and Global Dynamics James Bullard 10 February 2007 Learning and global dynamics The paper for this lecture is Liquidity Traps, Learning and Stagnation, by George Evans, Eran Guse, and Seppo Honkapohja.

Learning and Global Dynamics James Bullard 10 February 2007 Learning and global dynamics The paper for this lecture is Liquidity Traps, Learning and Stagnation, by George Evans, Eran Guse, and Seppo Honkapohja.

Signaling Effects of Monetary Policy

Signaling Effects of Monetary Policy Leonardo Melosi London Business School 24 May 2012 Motivation Disperse information about aggregate fundamentals Morris and Shin (2003), Sims (2003), and Woodford (2002)

Signaling Effects of Monetary Policy Leonardo Melosi London Business School 24 May 2012 Motivation Disperse information about aggregate fundamentals Morris and Shin (2003), Sims (2003), and Woodford (2002)

Session 4: Money. Jean Imbs. November 2010

Session 4: Jean November 2010 I So far, focused on real economy. Real quantities consumed, produced, invested. No money, no nominal in uences. I Now, introduce nominal dimension in the economy. First and

Session 4: Jean November 2010 I So far, focused on real economy. Real quantities consumed, produced, invested. No money, no nominal in uences. I Now, introduce nominal dimension in the economy. First and

Deviant Behavior in Monetary Economics

Deviant Behavior in Monetary Economics Lawrence Christiano and Yuta Takahashi July 26, 2018 Multiple Equilibria Standard NK Model Standard, New Keynesian (NK) Monetary Model: Taylor rule satisfying Taylor

Deviant Behavior in Monetary Economics Lawrence Christiano and Yuta Takahashi July 26, 2018 Multiple Equilibria Standard NK Model Standard, New Keynesian (NK) Monetary Model: Taylor rule satisfying Taylor

DSGE-Models. Calibration and Introduction to Dynare. Institute of Econometrics and Economic Statistics

DSGE-Models Calibration and Introduction to Dynare Dr. Andrea Beccarini Willi Mutschler, M.Sc. Institute of Econometrics and Economic Statistics willi.mutschler@uni-muenster.de Summer 2012 Willi Mutschler

DSGE-Models Calibration and Introduction to Dynare Dr. Andrea Beccarini Willi Mutschler, M.Sc. Institute of Econometrics and Economic Statistics willi.mutschler@uni-muenster.de Summer 2012 Willi Mutschler

Simple New Keynesian Model without Capital

Simple New Keynesian Model without Capital Lawrence J. Christiano Gerzensee, August 27 Objective Review the foundations of the basic New Keynesian model without capital. Clarify the role of money supply/demand.

Simple New Keynesian Model without Capital Lawrence J. Christiano Gerzensee, August 27 Objective Review the foundations of the basic New Keynesian model without capital. Clarify the role of money supply/demand.

The Labor Market in the New Keynesian Model: Foundations of the Sticky Wage Approach and a Critical Commentary

The Labor Market in the New Keynesian Model: Foundations of the Sticky Wage Approach and a Critical Commentary Lawrence J. Christiano March 30, 2013 Baseline developed earlier: NK model with no capital

The Labor Market in the New Keynesian Model: Foundations of the Sticky Wage Approach and a Critical Commentary Lawrence J. Christiano March 30, 2013 Baseline developed earlier: NK model with no capital

Equilibrium Conditions for the Simple New Keynesian Model

Equilibrium Conditions for the Simple New Keynesian Model Lawrence J. Christiano August 4, 04 Baseline NK model with no capital and with a competitive labor market. private sector equilibrium conditions

Equilibrium Conditions for the Simple New Keynesian Model Lawrence J. Christiano August 4, 04 Baseline NK model with no capital and with a competitive labor market. private sector equilibrium conditions

Getting to page 31 in Galí (2008)

") Getting to page 31 in Galí 2008) H J Department of Economics University of Copenhagen December 4 2012 Abstract This note shows in detail how to compute the solutions for output inflation and the nominal

Getting to page 31 in Galí 2008) H J Department of Economics University of Copenhagen December 4 2012 Abstract This note shows in detail how to compute the solutions for output inflation and the nominal

The Basic New Keynesian Model, the Labor Market and Sticky Wages

The Basic New Keynesian Model, the Labor Market and Sticky Wages Lawrence J. Christiano August 25, 203 Baseline NK model with no capital and with a competitive labor market. private sector equilibrium

The Basic New Keynesian Model, the Labor Market and Sticky Wages Lawrence J. Christiano August 25, 203 Baseline NK model with no capital and with a competitive labor market. private sector equilibrium

Dynare Class on Heathcote-Perri JME 2002

Dynare Class on Heathcote-Perri JME 2002 Tim Uy University of Cambridge March 10, 2015 Introduction Solving DSGE models used to be very time consuming due to log-linearization required Dynare is a collection

Dynare Class on Heathcote-Perri JME 2002 Tim Uy University of Cambridge March 10, 2015 Introduction Solving DSGE models used to be very time consuming due to log-linearization required Dynare is a collection

Part A: Answer question A1 (required), plus either question A2 or A3.

, plus either question A2 or A3.") Ph.D. Core Exam -- Macroeconomics 5 January 2015 -- 8:00 am to 3:00 pm Part A: Answer question A1 (required), plus either question A2 or A3. A1 (required): Ending Quantitative Easing Now that the U.S.

Ph.D. Core Exam -- Macroeconomics 5 January 2015 -- 8:00 am to 3:00 pm Part A: Answer question A1 (required), plus either question A2 or A3. A1 (required): Ending Quantitative Easing Now that the U.S.

The Labor Market in the New Keynesian Model: Incorporating a Simple DMP Version of the Labor Market and Rediscovering the Shimer Puzzle

The Labor Market in the New Keynesian Model: Incorporating a Simple DMP Version of the Labor Market and Rediscovering the Shimer Puzzle Lawrence J. Christiano April 1, 2013 Outline We present baseline

The Labor Market in the New Keynesian Model: Incorporating a Simple DMP Version of the Labor Market and Rediscovering the Shimer Puzzle Lawrence J. Christiano April 1, 2013 Outline We present baseline

(a) Write down the Hamilton-Jacobi-Bellman (HJB) Equation in the dynamic programming

Write down the Hamilton-Jacobi-Bellman (HJB) Equation in the dynamic programming") 1. Government Purchases and Endogenous Growth Consider the following endogenous growth model with government purchases (G) in continuous time. Government purchases enhance production, and the production

1. Government Purchases and Endogenous Growth Consider the following endogenous growth model with government purchases (G) in continuous time. Government purchases enhance production, and the production

Real Business Cycle Model (RBC)

") Real Business Cycle Model (RBC) Seyed Ali Madanizadeh November 2013 RBC Model Lucas 1980: One of the functions of theoretical economics is to provide fully articulated, artificial economic systems that

Real Business Cycle Model (RBC) Seyed Ali Madanizadeh November 2013 RBC Model Lucas 1980: One of the functions of theoretical economics is to provide fully articulated, artificial economic systems that

1. Constant-elasticity-of-substitution (CES) or Dixit-Stiglitz aggregators. Consider the following function J: J(x) = a(j)x(j) ρ dj

or Dixit-Stiglitz aggregators. Consider the following function J: J(x) = a(j)x(j) ρ dj") Macro II (UC3M, MA/PhD Econ) Professor: Matthias Kredler Problem Set 1 Due: 29 April 216 You are encouraged to work in groups; however, every student has to hand in his/her own version of the solution.

Macro II (UC3M, MA/PhD Econ) Professor: Matthias Kredler Problem Set 1 Due: 29 April 216 You are encouraged to work in groups; however, every student has to hand in his/her own version of the solution.

Source: US. Bureau of Economic Analysis Shaded areas indicate US recessions research.stlouisfed.org

Business Cycles 0 Real Gross Domestic Product 18,000 16,000 (Billions of Chained 2009 Dollars) 14,000 12,000 10,000 8,000 6,000 4,000 2,000 1940 1960 1980 2000 Source: US. Bureau of Economic Analysis Shaded

Business Cycles 0 Real Gross Domestic Product 18,000 16,000 (Billions of Chained 2009 Dollars) 14,000 12,000 10,000 8,000 6,000 4,000 2,000 1940 1960 1980 2000 Source: US. Bureau of Economic Analysis Shaded

The Real Business Cycle Model

The Real Business Cycle Model Macroeconomics II 2 The real business cycle model. Introduction This model explains the comovements in the fluctuations of aggregate economic variables around their trend.

The Real Business Cycle Model Macroeconomics II 2 The real business cycle model. Introduction This model explains the comovements in the fluctuations of aggregate economic variables around their trend.

Taylor Rules and Technology Shocks

Taylor Rules and Technology Shocks Eric R. Sims University of Notre Dame and NBER January 17, 2012 Abstract In a standard New Keynesian model, a Taylor-type interest rate rule moves the equilibrium real

Taylor Rules and Technology Shocks Eric R. Sims University of Notre Dame and NBER January 17, 2012 Abstract In a standard New Keynesian model, a Taylor-type interest rate rule moves the equilibrium real

Eco 200, part 3, Fall 2004 Lars Svensson 12/6/04. Liquidity traps, the zero lower bound for interest rates, and deflation

Eco 00, part 3, Fall 004 00L5.tex Lars Svensson /6/04 Liquidity traps, the zero lower bound for interest rates, and deflation The zero lower bound for interest rates (ZLB) A forward-looking aggregate-demand

Eco 00, part 3, Fall 004 00L5.tex Lars Svensson /6/04 Liquidity traps, the zero lower bound for interest rates, and deflation The zero lower bound for interest rates (ZLB) A forward-looking aggregate-demand

Money in the utility model

Money in the utility model Monetary Economics Michaª Brzoza-Brzezina Warsaw School of Economics 1 / 59 Plan of the Presentation 1 Motivation 2 Model 3 Steady state 4 Short run dynamics 5 Simulations 6

Money in the utility model Monetary Economics Michaª Brzoza-Brzezina Warsaw School of Economics 1 / 59 Plan of the Presentation 1 Motivation 2 Model 3 Steady state 4 Short run dynamics 5 Simulations 6

Monetary Policy and the Uncovered Interest Rate Parity Puzzle. David K. Backus, Chris Telmer and Stanley E. Zin

Monetary Policy and the Uncovered Interest Rate Parity Puzzle David K. Backus, Chris Telmer and Stanley E. Zin UIP Puzzle Standard regression: s t+1 s t = α + β(i t i t) + residuals Estimates of β are

Monetary Policy and the Uncovered Interest Rate Parity Puzzle David K. Backus, Chris Telmer and Stanley E. Zin UIP Puzzle Standard regression: s t+1 s t = α + β(i t i t) + residuals Estimates of β are

Assignment #5. 1 Keynesian Cross. Econ 302: Intermediate Macroeconomics. December 2, 2009

Assignment #5 Econ 0: Intermediate Macroeconomics December, 009 Keynesian Cross Consider a closed economy. Consumption function: C = C + M C(Y T ) () In addition, suppose that planned investment expenditure

Assignment #5 Econ 0: Intermediate Macroeconomics December, 009 Keynesian Cross Consider a closed economy. Consumption function: C = C + M C(Y T ) () In addition, suppose that planned investment expenditure

SLOVAK REPUBLIC. Time Series Data on International Reserves/Foreign Currency Liquidity

SLOVAK REPUBLIC Time Series Data on International Reserves/Foreign Currency Liquidity 1 2 3 (Information to be disclosed by the monetary authorities and other central government, excluding social security)

SLOVAK REPUBLIC Time Series Data on International Reserves/Foreign Currency Liquidity 1 2 3 (Information to be disclosed by the monetary authorities and other central government, excluding social security)

Lars Svensson 10/2/05. Liquidity traps, the zero lower bound for interest rates, and deflation

Eco 00, part, Fall 005 00L5_F05.tex Lars Svensson 0//05 Liquidity traps, the zero lower bound for interest rates, and deflation Japan: recession, low growth since early 90s, deflation in GDP deflator and

Eco 00, part, Fall 005 00L5_F05.tex Lars Svensson 0//05 Liquidity traps, the zero lower bound for interest rates, and deflation Japan: recession, low growth since early 90s, deflation in GDP deflator and

The New Keynesian Model

The New Keynesian Model Basic Issues Roberto Chang Rutgers January 2013 R. Chang (Rutgers) New Keynesian Model January 2013 1 / 22 Basic Ingredients of the New Keynesian Paradigm Representative agent paradigm

The New Keynesian Model Basic Issues Roberto Chang Rutgers January 2013 R. Chang (Rutgers) New Keynesian Model January 2013 1 / 22 Basic Ingredients of the New Keynesian Paradigm Representative agent paradigm

Advanced Macroeconomics II. Monetary Models with Nominal Rigidities. Jordi Galí Universitat Pompeu Fabra April 2018

Advanced Macroeconomics II Monetary Models with Nominal Rigidities Jordi Galí Universitat Pompeu Fabra April 208 Motivation Empirical Evidence Macro evidence on the e ects of monetary policy shocks (i)

Advanced Macroeconomics II Monetary Models with Nominal Rigidities Jordi Galí Universitat Pompeu Fabra April 208 Motivation Empirical Evidence Macro evidence on the e ects of monetary policy shocks (i)

Small Open Economy RBC Model Uribe, Chapter 4

Small Open Economy RBC Model Uribe, Chapter 4 1 Basic Model 1.1 Uzawa Utility E 0 t=0 θ t U (c t, h t ) θ 0 = 1 θ t+1 = β (c t, h t ) θ t ; β c < 0; β h > 0. Time-varying discount factor With a constant

Small Open Economy RBC Model Uribe, Chapter 4 1 Basic Model 1.1 Uzawa Utility E 0 t=0 θ t U (c t, h t ) θ 0 = 1 θ t+1 = β (c t, h t ) θ t ; β c < 0; β h > 0. Time-varying discount factor With a constant

Problem 1 (30 points)

") Problem (30 points) Prof. Robert King Consider an economy in which there is one period and there are many, identical households. Each household derives utility from consumption (c), leisure (l) and a public

Problem (30 points) Prof. Robert King Consider an economy in which there is one period and there are many, identical households. Each household derives utility from consumption (c), leisure (l) and a public

Lecture 3, November 30: The Basic New Keynesian Model (Galí, Chapter 3)

") MakØk3, Fall 2 (blok 2) Business cycles and monetary stabilization policies Henrik Jensen Department of Economics University of Copenhagen Lecture 3, November 3: The Basic New Keynesian Model (Galí, Chapter

MakØk3, Fall 2 (blok 2) Business cycles and monetary stabilization policies Henrik Jensen Department of Economics University of Copenhagen Lecture 3, November 3: The Basic New Keynesian Model (Galí, Chapter

V. The Speed of adjustment of Endogenous Variables and Overshooting

V. The Speed of adjustment of Endogenous Variables and Overshooting The second section of Chapter 11 of Dornbusch (1980) draws on Dornbusch (1976) Expectations and Exchange Rate Dynamics, Journal of Political

V. The Speed of adjustment of Endogenous Variables and Overshooting The second section of Chapter 11 of Dornbusch (1980) draws on Dornbusch (1976) Expectations and Exchange Rate Dynamics, Journal of Political

Dynamic Optimization: An Introduction

Dynamic Optimization An Introduction M. C. Sunny Wong University of San Francisco University of Houston, June 20, 2014 Outline 1 Background What is Optimization? EITM: The Importance of Optimization 2

Dynamic Optimization An Introduction M. C. Sunny Wong University of San Francisco University of Houston, June 20, 2014 Outline 1 Background What is Optimization? EITM: The Importance of Optimization 2

ECON 5118 Macroeconomic Theory

ECON 5118 Macroeconomic Theory Winter 013 Test 1 February 1, 013 Answer ALL Questions Time Allowed: 1 hour 0 min Attention: Please write your answers on the answer book provided Use the right-side pages

ECON 5118 Macroeconomic Theory Winter 013 Test 1 February 1, 013 Answer ALL Questions Time Allowed: 1 hour 0 min Attention: Please write your answers on the answer book provided Use the right-side pages

Macroeconomics Qualifying Examination

Macroeconomics Qualifying Examination January 2016 Department of Economics UNC Chapel Hill Instructions: This examination consists of 3 questions. Answer all questions. If you believe a question is ambiguously

Macroeconomics Qualifying Examination January 2016 Department of Economics UNC Chapel Hill Instructions: This examination consists of 3 questions. Answer all questions. If you believe a question is ambiguously

New Keynesian Model Walsh Chapter 8

New Keynesian Model Walsh Chapter 8 1 General Assumptions Ignore variations in the capital stock There are differentiated goods with Calvo price stickiness Wages are not sticky Monetary policy is a choice

New Keynesian Model Walsh Chapter 8 1 General Assumptions Ignore variations in the capital stock There are differentiated goods with Calvo price stickiness Wages are not sticky Monetary policy is a choice

slides chapter 3 an open economy with capital

slides chapter 3 an open economy with capital Princeton University Press, 2017 Motivation In this chaper we introduce production and physical capital accumulation. Doing so will allow us to address two

slides chapter 3 an open economy with capital Princeton University Press, 2017 Motivation In this chaper we introduce production and physical capital accumulation. Doing so will allow us to address two

Optimal Inflation Stabilization in a Medium-Scale Macroeconomic Model

Optimal Inflation Stabilization in a Medium-Scale Macroeconomic Model Stephanie Schmitt-Grohé Martín Uribe Duke University 1 Objective of the Paper: Within a mediumscale estimated model of the macroeconomy

Optimal Inflation Stabilization in a Medium-Scale Macroeconomic Model Stephanie Schmitt-Grohé Martín Uribe Duke University 1 Objective of the Paper: Within a mediumscale estimated model of the macroeconomy

The Basic New Keynesian Model. Jordi Galí. June 2008

The Basic New Keynesian Model by Jordi Galí June 28 Motivation and Outline Evidence on Money, Output, and Prices: Short Run E ects of Monetary Policy Shocks (i) persistent e ects on real variables (ii)

The Basic New Keynesian Model by Jordi Galí June 28 Motivation and Outline Evidence on Money, Output, and Prices: Short Run E ects of Monetary Policy Shocks (i) persistent e ects on real variables (ii)

Modelling Czech and Slovak labour markets: A DSGE model with labour frictions

Modelling Czech and Slovak labour markets: A DSGE model with labour frictions Daniel Němec Faculty of Economics and Administrations Masaryk University Brno, Czech Republic nemecd@econ.muni.cz ESF MU (Brno)

Modelling Czech and Slovak labour markets: A DSGE model with labour frictions Daniel Němec Faculty of Economics and Administrations Masaryk University Brno, Czech Republic nemecd@econ.muni.cz ESF MU (Brno)

Government The government faces an exogenous sequence {g t } t=0

Part 6 1. Borrowing Constraints II 1.1. Borrowing Constraints and the Ricardian Equivalence Equivalence between current taxes and current deficits? Basic paper on the Ricardian Equivalence: Barro, JPE,

Part 6 1. Borrowing Constraints II 1.1. Borrowing Constraints and the Ricardian Equivalence Equivalence between current taxes and current deficits? Basic paper on the Ricardian Equivalence: Barro, JPE,

Economic Growth: Lecture 9, Neoclassical Endogenous Growth

14.452 Economic Growth: Lecture 9, Neoclassical Endogenous Growth Daron Acemoglu MIT November 28, 2017. Daron Acemoglu (MIT) Economic Growth Lecture 9 November 28, 2017. 1 / 41 First-Generation Models

14.452 Economic Growth: Lecture 9, Neoclassical Endogenous Growth Daron Acemoglu MIT November 28, 2017. Daron Acemoglu (MIT) Economic Growth Lecture 9 November 28, 2017. 1 / 41 First-Generation Models

Stochastic simulations with DYNARE. A practical guide.

Stochastic simulations with DYNARE. A practical guide. Fabrice Collard (GREMAQ, University of Toulouse) Adapted for Dynare 4.1 by Michel Juillard and Sébastien Villemot (CEPREMAP) First draft: February

Stochastic simulations with DYNARE. A practical guide. Fabrice Collard (GREMAQ, University of Toulouse) Adapted for Dynare 4.1 by Michel Juillard and Sébastien Villemot (CEPREMAP) First draft: February

Introduction to Macroeconomics

Introduction to Macroeconomics Martin Ellison Nuffi eld College Michaelmas Term 2018 Martin Ellison (Nuffi eld) Introduction Michaelmas Term 2018 1 / 39 Macroeconomics is Dynamic Decisions are taken over

Introduction to Macroeconomics Martin Ellison Nuffi eld College Michaelmas Term 2018 Martin Ellison (Nuffi eld) Introduction Michaelmas Term 2018 1 / 39 Macroeconomics is Dynamic Decisions are taken over

Stagnation Traps. Gianluca Benigno and Luca Fornaro

Stagnation Traps Gianluca Benigno and Luca Fornaro May 2015 Research question and motivation Can insu cient aggregate demand lead to economic stagnation? This question goes back, at least, to the Great

Stagnation Traps Gianluca Benigno and Luca Fornaro May 2015 Research question and motivation Can insu cient aggregate demand lead to economic stagnation? This question goes back, at least, to the Great

Expectations, Learning and Macroeconomic Policy

Expectations, Learning and Macroeconomic Policy George W. Evans (Univ. of Oregon and Univ. of St. Andrews) Lecture 4 Liquidity traps, learning and stagnation Evans, Guse & Honkapohja (EER, 2008), Evans

Expectations, Learning and Macroeconomic Policy George W. Evans (Univ. of Oregon and Univ. of St. Andrews) Lecture 4 Liquidity traps, learning and stagnation Evans, Guse & Honkapohja (EER, 2008), Evans

Comprehensive Exam. Macro Spring 2014 Retake. August 22, 2014

Comprehensive Exam Macro Spring 2014 Retake August 22, 2014 You have a total of 180 minutes to complete the exam. If a question seems ambiguous, state why, sharpen it up and answer the sharpened-up question.

Comprehensive Exam Macro Spring 2014 Retake August 22, 2014 You have a total of 180 minutes to complete the exam. If a question seems ambiguous, state why, sharpen it up and answer the sharpened-up question.

Dynamic (Stochastic) General Equilibrium and Growth

General Equilibrium and Growth") Dynamic (Stochastic) General Equilibrium and Growth Martin Ellison Nuffi eld College Michaelmas Term 2018 Martin Ellison (Nuffi eld) D(S)GE and Growth Michaelmas Term 2018 1 / 43 Macroeconomics is Dynamic

Dynamic (Stochastic) General Equilibrium and Growth Martin Ellison Nuffi eld College Michaelmas Term 2018 Martin Ellison (Nuffi eld) D(S)GE and Growth Michaelmas Term 2018 1 / 43 Macroeconomics is Dynamic

Small Open Economy. Macroeconomic Theory, Lecture 9. Adam Gulan. February Bank of Finland

Small Open Economy Macroeconomic Theory, Lecture 9 Adam Gulan Bank of Finland February 2018 Course material Readings for lecture 9: Schmitt-Grohé and Uribe ( Open Economy Macroeconomics online manuscript),

Small Open Economy Macroeconomic Theory, Lecture 9 Adam Gulan Bank of Finland February 2018 Course material Readings for lecture 9: Schmitt-Grohé and Uribe ( Open Economy Macroeconomics online manuscript),

The Dornbusch overshooting model

4330 Lecture 8 Ragnar Nymoen 12 March 2012 References I Lecture 7: Portfolio model of the FEX market extended by money. Important concepts: monetary policy regimes degree of sterilization Monetary model

4330 Lecture 8 Ragnar Nymoen 12 March 2012 References I Lecture 7: Portfolio model of the FEX market extended by money. Important concepts: monetary policy regimes degree of sterilization Monetary model

Dynamics and Monetary Policy in a Fair Wage Model of the Business Cycle

Dynamics and Monetary Policy in a Fair Wage Model of the Business Cycle David de la Croix 1,3 Gregory de Walque 2 Rafael Wouters 2,1 1 dept. of economics, Univ. cath. Louvain 2 National Bank of Belgium

Dynamics and Monetary Policy in a Fair Wage Model of the Business Cycle David de la Croix 1,3 Gregory de Walque 2 Rafael Wouters 2,1 1 dept. of economics, Univ. cath. Louvain 2 National Bank of Belgium

MA Advanced Macroeconomics: 7. The Real Business Cycle Model

MA Advanced Macroeconomics: 7. The Real Business Cycle Model Karl Whelan School of Economics, UCD Spring 2016 Karl Whelan (UCD) Real Business Cycles Spring 2016 1 / 38 Working Through A DSGE Model We have

MA Advanced Macroeconomics: 7. The Real Business Cycle Model Karl Whelan School of Economics, UCD Spring 2016 Karl Whelan (UCD) Real Business Cycles Spring 2016 1 / 38 Working Through A DSGE Model We have

Chapter 11 The Stochastic Growth Model and Aggregate Fluctuations

George Alogoskoufis, Dynamic Macroeconomics, 2016 Chapter 11 The Stochastic Growth Model and Aggregate Fluctuations In previous chapters we studied the long run evolution of output and consumption, real

George Alogoskoufis, Dynamic Macroeconomics, 2016 Chapter 11 The Stochastic Growth Model and Aggregate Fluctuations In previous chapters we studied the long run evolution of output and consumption, real

Dynamics of Firms and Trade in General Equilibrium. Robert Dekle, Hyeok Jeong and Nobuhiro Kiyotaki USC, Seoul National University and Princeton

Dynamics of Firms and Trade in General Equilibrium Robert Dekle, Hyeok Jeong and Nobuhiro Kiyotaki USC, Seoul National University and Princeton Figure a. Aggregate exchange rate disconnect (levels) 28.5

Dynamics of Firms and Trade in General Equilibrium Robert Dekle, Hyeok Jeong and Nobuhiro Kiyotaki USC, Seoul National University and Princeton Figure a. Aggregate exchange rate disconnect (levels) 28.5

Demand Shocks, Monetary Policy, and the Optimal Use of Dispersed Information

Demand Shocks, Monetary Policy, and the Optimal Use of Dispersed Information Guido Lorenzoni (MIT) WEL-MIT-Central Banks, December 2006 Motivation Central bank observes an increase in spending Is it driven

Demand Shocks, Monetary Policy, and the Optimal Use of Dispersed Information Guido Lorenzoni (MIT) WEL-MIT-Central Banks, December 2006 Motivation Central bank observes an increase in spending Is it driven

Macroeconomics Theory II

Macroeconomics Theory II Francesco Franco Novasbe February 2016 Francesco Franco (Novasbe) Macroeconomics Theory II February 2016 1 / 8 The Social Planner Solution Notice no intertemporal issues (Y t =

Macroeconomics Theory II Francesco Franco Novasbe February 2016 Francesco Franco (Novasbe) Macroeconomics Theory II February 2016 1 / 8 The Social Planner Solution Notice no intertemporal issues (Y t =

Foundations of Modern Macroeconomics Second Edition

Foundations of Modern Macroeconomics Second Edition Chapter 5: The government budget deficit Ben J. Heijdra Department of Economics & Econometrics University of Groningen 1 September 2009 Foundations of

Foundations of Modern Macroeconomics Second Edition Chapter 5: The government budget deficit Ben J. Heijdra Department of Economics & Econometrics University of Groningen 1 September 2009 Foundations of

Economics Discussion Paper Series EDP Measuring monetary policy deviations from the Taylor rule

Economics Discussion Paper Series EDP-1803 Measuring monetary policy deviations from the Taylor rule João Madeira Nuno Palma February 2018 Economics School of Social Sciences The University of Manchester

Economics Discussion Paper Series EDP-1803 Measuring monetary policy deviations from the Taylor rule João Madeira Nuno Palma February 2018 Economics School of Social Sciences The University of Manchester

Global Value Chain Participation and Current Account Imbalances

Global Value Chain Participation and Current Account Imbalances Johannes Brumm University of Zurich Georgios Georgiadis European Central Bank Johannes Gräb European Central Bank Fabian Trottner Princeton

Global Value Chain Participation and Current Account Imbalances Johannes Brumm University of Zurich Georgios Georgiadis European Central Bank Johannes Gräb European Central Bank Fabian Trottner Princeton

A suggested solution to the problem set at the re-exam in Advanced Macroeconomics. February 15, 2016

Christian Groth A suggested solution to the problem set at the re-exam in Advanced Macroeconomics February 15, 216 (3-hours closed book exam) 1 As formulated in the course description, a score of 12 is

Christian Groth A suggested solution to the problem set at the re-exam in Advanced Macroeconomics February 15, 216 (3-hours closed book exam) 1 As formulated in the course description, a score of 12 is

Graduate Macro Theory II: Notes on Quantitative Analysis in DSGE Models

Graduate Macro Theory II: Notes on Quantitative Analysis in DSGE Models Eric Sims University of Notre Dame Spring 2011 This note describes very briefly how to conduct quantitative analysis on a linearized

Graduate Macro Theory II: Notes on Quantitative Analysis in DSGE Models Eric Sims University of Notre Dame Spring 2011 This note describes very briefly how to conduct quantitative analysis on a linearized

Online Appendix for Investment Hangover and the Great Recession

ONLINE APPENDIX INVESTMENT HANGOVER A1 Online Appendix for Investment Hangover and the Great Recession By MATTHEW ROGNLIE, ANDREI SHLEIFER, AND ALP SIMSEK APPENDIX A: CALIBRATION This appendix describes

ONLINE APPENDIX INVESTMENT HANGOVER A1 Online Appendix for Investment Hangover and the Great Recession By MATTHEW ROGNLIE, ANDREI SHLEIFER, AND ALP SIMSEK APPENDIX A: CALIBRATION This appendix describes

1. Money in the utility function (start)

") Monetary Economics: Macro Aspects, 1/3 2012 Henrik Jensen Department of Economics University of Copenhagen 1. Money in the utility function (start) a. The basic money-in-the-utility function model b. Optimal

Monetary Economics: Macro Aspects, 1/3 2012 Henrik Jensen Department of Economics University of Copenhagen 1. Money in the utility function (start) a. The basic money-in-the-utility function model b. Optimal

UNIVERSITY OF WISCONSIN DEPARTMENT OF ECONOMICS MACROECONOMICS THEORY Preliminary Exam August 1, :00 am - 2:00 pm

UNIVERSITY OF WISCONSIN DEPARTMENT OF ECONOMICS MACROECONOMICS THEORY Preliminary Exam August 1, 2017 9:00 am - 2:00 pm INSTRUCTIONS Please place a completed label (from the label sheet provided) on the

UNIVERSITY OF WISCONSIN DEPARTMENT OF ECONOMICS MACROECONOMICS THEORY Preliminary Exam August 1, 2017 9:00 am - 2:00 pm INSTRUCTIONS Please place a completed label (from the label sheet provided) on the

Lecture 2 The Centralized Economy

Lecture 2 The Centralized Economy Economics 5118 Macroeconomic Theory Kam Yu Winter 2013 Outline 1 Introduction 2 The Basic DGE Closed Economy 3 Golden Rule Solution 4 Optimal Solution The Euler Equation

Lecture 2 The Centralized Economy Economics 5118 Macroeconomic Theory Kam Yu Winter 2013 Outline 1 Introduction 2 The Basic DGE Closed Economy 3 Golden Rule Solution 4 Optimal Solution The Euler Equation

A t = B A F (φ A t K t, N A t X t ) S t = B S F (φ S t K t, N S t X t ) M t + δk + K = B M F (φ M t K t, N M t X t )

S t = B S F (φ S t K t, N S t X t ) M t + δk + K = B M F (φ M t K t, N M t X t )") Notes on Kongsamut et al. (2001) The goal of this model is to be consistent with the Kaldor facts (constancy of growth rates, capital shares, capital-output ratios) and the Kuznets facts (employment in

Notes on Kongsamut et al. (2001) The goal of this model is to be consistent with the Kaldor facts (constancy of growth rates, capital shares, capital-output ratios) and the Kuznets facts (employment in

Sticky Leverage. João Gomes, Urban Jermann & Lukas Schmid Wharton School and UCLA/Duke. September 28, 2013

Sticky Leverage João Gomes, Urban Jermann & Lukas Schmid Wharton School and UCLA/Duke September 28, 213 Introduction Models of monetary non-neutrality have traditionally emphasized the importance of sticky

Sticky Leverage João Gomes, Urban Jermann & Lukas Schmid Wharton School and UCLA/Duke September 28, 213 Introduction Models of monetary non-neutrality have traditionally emphasized the importance of sticky

General Examination in Macroeconomic Theory SPRING 2013

HARVARD UNIVERSITY DEPARTMENT OF ECONOMICS General Examination in Macroeconomic Theory SPRING 203 You have FOUR hours. Answer all questions Part A (Prof. Laibson): 48 minutes Part B (Prof. Aghion): 48

HARVARD UNIVERSITY DEPARTMENT OF ECONOMICS General Examination in Macroeconomic Theory SPRING 203 You have FOUR hours. Answer all questions Part A (Prof. Laibson): 48 minutes Part B (Prof. Aghion): 48

Bayesian Estimation of DSGE Models: Lessons from Second-order Approximations

Bayesian Estimation of DSGE Models: Lessons from Second-order Approximations Sungbae An Singapore Management University Bank Indonesia/BIS Workshop: STRUCTURAL DYNAMIC MACROECONOMIC MODELS IN ASIA-PACIFIC

Bayesian Estimation of DSGE Models: Lessons from Second-order Approximations Sungbae An Singapore Management University Bank Indonesia/BIS Workshop: STRUCTURAL DYNAMIC MACROECONOMIC MODELS IN ASIA-PACIFIC

Permanent Income Hypothesis Intro to the Ramsey Model

Consumption and Savings Permanent Income Hypothesis Intro to the Ramsey Model Lecture 10 Topics in Macroeconomics November 6, 2007 Lecture 10 1/18 Topics in Macroeconomics Consumption and Savings Outline

Consumption and Savings Permanent Income Hypothesis Intro to the Ramsey Model Lecture 10 Topics in Macroeconomics November 6, 2007 Lecture 10 1/18 Topics in Macroeconomics Consumption and Savings Outline

Advanced Macroeconomics

Advanced Macroeconomics The Ramsey Model Micha l Brzoza-Brzezina/Marcin Kolasa Warsaw School of Economics Micha l Brzoza-Brzezina/Marcin Kolasa (WSE) Ad. Macro - Ramsey model 1 / 47 Introduction Authors:

Advanced Macroeconomics The Ramsey Model Micha l Brzoza-Brzezina/Marcin Kolasa Warsaw School of Economics Micha l Brzoza-Brzezina/Marcin Kolasa (WSE) Ad. Macro - Ramsey model 1 / 47 Introduction Authors:

Assessing Structural VAR s

... Assessing Structural VAR s by Lawrence J. Christiano, Martin Eichenbaum and Robert Vigfusson Zurich, September 2005 1 Background Structural Vector Autoregressions Address the Following Type of Question:

... Assessing Structural VAR s by Lawrence J. Christiano, Martin Eichenbaum and Robert Vigfusson Zurich, September 2005 1 Background Structural Vector Autoregressions Address the Following Type of Question:

1. Using the model and notations covered in class, the expected returns are:

Econ 510a second half Yale University Fall 2006 Prof. Tony Smith HOMEWORK #5 This homework assignment is due at 5PM on Friday, December 8 in Marnix Amand s mailbox. Solution 1. a In the Mehra-Prescott

Econ 510a second half Yale University Fall 2006 Prof. Tony Smith HOMEWORK #5 This homework assignment is due at 5PM on Friday, December 8 in Marnix Amand s mailbox. Solution 1. a In the Mehra-Prescott

Topic 2. Consumption/Saving and Productivity shocks

14.452. Topic 2. Consumption/Saving and Productivity shocks Olivier Blanchard April 2006 Nr. 1 1. What starting point? Want to start with a model with at least two ingredients: Shocks, so uncertainty.

14.452. Topic 2. Consumption/Saving and Productivity shocks Olivier Blanchard April 2006 Nr. 1 1. What starting point? Want to start with a model with at least two ingredients: Shocks, so uncertainty.

14.05 Lecture Notes Crises and Multiple Equilibria

14.05 Lecture Notes Crises and Multiple Equilibria George-Marios Angeletos Spring 2013 1 George-Marios Angeletos 1 Obstfeld (1996): self-fulfilling currency crises What triggers speculative currency crises?

14.05 Lecture Notes Crises and Multiple Equilibria George-Marios Angeletos Spring 2013 1 George-Marios Angeletos 1 Obstfeld (1996): self-fulfilling currency crises What triggers speculative currency crises?

Business Failure and Labour Market Fluctuations

Business Failure and Labour Market Fluctuations Seong-Hoon Kim* Seongman Moon** *Centre for Dynamic Macroeconomic Analysis, St Andrews, UK **Korea Institute for International Economic Policy, Seoul, Korea

Business Failure and Labour Market Fluctuations Seong-Hoon Kim* Seongman Moon** *Centre for Dynamic Macroeconomic Analysis, St Andrews, UK **Korea Institute for International Economic Policy, Seoul, Korea

Based on the specification in Mansoorian and Mohsin(2006), the model in this

, the model in this") Chapter 2 The Model Based on the specification in Mansoorian and Mohsin(2006), the model in this paper is composed of a small open economy with a single good. The foreign currency 立 政 治 price of the good

Chapter 2 The Model Based on the specification in Mansoorian and Mohsin(2006), the model in this paper is composed of a small open economy with a single good. The foreign currency 立 政 治 price of the good

Macroeconomics Qualifying Examination

Macroeconomics Qualifying Examination August 2015 Department of Economics UNC Chapel Hill Instructions: This examination consists of 4 questions. Answer all questions. If you believe a question is ambiguously

Macroeconomics Qualifying Examination August 2015 Department of Economics UNC Chapel Hill Instructions: This examination consists of 4 questions. Answer all questions. If you believe a question is ambiguously