APPLIED ECONOMETRIC TIME SERIES 4TH EDITION

|

|

|

- Lionel Goodman

- 6 years ago

- Views:

Transcription

1 APPLIED ECONOMETRIC TIME SERIES 4TH EDITION Chapter 2: STATIONARY TIME-SERIES MODELS WALTER ENDERS, UNIVERSITY OF ALABAMA Copyright 2015 John Wiley & Sons, Inc.

2 Section 1 STOCHASTIC DIFFERENCE EQUATION MODELS

3 Example of a time-series model m = ρ(1.03) m + (1 ρ) m + ε t * t 0 t 1 t (2.2) 1. Although the money supply is a continuous variable, (2.2) is a discrete difference equation. Since the forcing process {ε t } is stochastic, the money supply is stochastic; we can call (2.2) a linear stochastic difference equation. 2. If we knew the distribution of {ε t }, we could calculate the distribution for each element in the {m t } sequence. Since (2.2) shows how the realizations of the {m t } sequence are linked across time, we would be able to calculate the various joint probabilities. Notice that the distribution of the money supply sequence is completely determined by the parameters of the difference equation (2.2) and the distribution of the {ε t } sequence. 3. Having observed the first t observations in the {m t } sequence, we can make forecasts of m t+1, m t+2,.

4 White Noise E(ε t ) = E(ε t 1 ) = = 0 E(ε t ) 2 = E(ε t 1 ) 2 = = σ 2 [or var(ε t ) = var(ε t 1 ) = = σ 2 ] E(ε t ε t-s ) = E(ε t-j ε t-j-s ) = 0 for all j and s [or cov(ε t, ε t-s ) = cov(ε t-j, ε t-j-s ) = 0] x q = βε t i t i i= 0 A sequence formed in this manner is called a moving average of order q and is denoted by MA(q)

5 2. ARMA MODELS In the ARMA(p, q) model y t = a 0 + a 1 y t a p y t-p + ε t + β 1 ε t β q ε t-q where ε t series are serially uncorrelated shocks The particular solution is: q p i yt= a 0 + βε i t i 1 ail i= 0 i= 1 Note that all roots must lie outside of the unit circle. If this is the case, we have the MA Representation y = c+ cε t i t i i= 0

6 tε Section 3 Stationarity Restrictions for an AR(1) Process STATIONARITY

7

8 Covariance Stationary Series Mean is time-invariant Variance is constant All covariances are constant all autocorrelations are constant Example of a series that are not covariance stationary y t = α + β time y t = y t-1 + ε t (Random Walk)

9 Formal Definition A stochastic process having a finite mean and variance is covariance stationary if for all t and t s, 1. E(y t ) = E(y t-s ) = µ 2. E[(y t µ) 2 ] = E[(y t-s µ) 2 ] or [var(y t ) = var(y t s ) = ] 3. E[(y t µ)(y t-s µ)] = E[(y t-j µ)(y t-j-s µ)] = γ s or cov(y t, y t-s ) = cov(y t-j, y t-j-s ) = γ s where µ, and γ s are all constants.

10 4. STATIONARITY RESTRICTIONS FOR AN ARMA(p, q) MODEL Stationarity Restrictions for the Autoregressive Coefficients

11 Stationarity of an AR(1) Process y t = a 0 + a 1 y t 1 + ε t with an initial condition t t 1 t 1 i t i i= 0 i= 0 y = a a+ ay + aε t i Only if t is large is this stationary: lim y t a 1 a 0 = + 1 i= 0 aε i 1 t i E[(y t µ)(y t-s µ)] = E{[ε t + a 1 ε t 1 + (a 1 ) 2 ε t 2 + ] [ε t-s + a 1 ε t-s 1 + (a 1 ) 2 ε t-s 2 + ]} = σ 2 (a 1 ) s [1 + (a 1 ) 2 + (a 1 ) 4 + ] = σ 2 (a 1 ) s /[1 (a 1 ) 2 ]

12 Let Restrictions for the AR Coefficients p y = a + ay + ε t 0 i t i t i= 1 p so that y = a / 1 a + cε t 0 i i t i i= 1 i= 0 We know that the sequence {c i } will eventually solve the difference equation c i a 1 c i 1 a 2 c i 2 a p c i p = 0 (2.21) If the characteristic roots of (2.21) are all inside the unit circle, the {c i } sequence will be convergent. The stability conditions can be stated succinctly: 1. The homogeneous solution must be zero. Either the sequence must have started infinitely far in the past or the process must always be in equilibrium (so that the arbitrary constant is zero). 2. The characteristic root a 1 must be less than unity in absolute value.

13 A Pure MA Process x = βε t i t i i= 0 1. Take the expected value of x t E(x t ) = E(ε t + β 1 ε t 1 + β 2 ε t 2 + ) = Eε t + β 1 Eε t 1 + β 2 Eε t 2 + = 0 E(x t s ) = E(ε t s + β 1 ε t s 1 + β 2 ε t s 2 + ) = 0 Hence, all elements in the {x t } sequence have the same finite mean (µ = 0). 2. Form var(x t ) as var(x t ) = E[(ε t + β 1 ε t 1 + β 2 ε t 2 + ) 2 ] = σ 2 [1 + (β 1 ) 2 + (β 2 ) 2 + ] As long as Σ(β i ) 2 is finite, it follows that var(x t ) is finite. var(x t s ) = E[(ε t s + β 1 ε t s 1 + β 2 ε t s 2 + ) 2 ] = σ 2 [1 + (β 1 ) 2 + (β 2 ) 2 + ] Thus, var(x t ) = var(x t s ) for all t and t s. Are all autocovariances finite and time independent? E[x t x t s ] = E[(ε t + β 1 ε t 1 + β 2 ε t 2 + )(ε t s + β 1 ε t s 1 + β 2 ε t s 2 + )] = σ 2 (β s + β 1 β s+1 + β 2 β s+2 + ) Restricting the sum β s + β 1 β s+1 + β 2 β s+2 + to be finite means that E(x t x t s ) is finite.

14 The Autocorrelation Function of an AR(2) Process The Autocorrelation Function of an MA(1) Process The Autocorrelation Function of an ARMA(1, 1) Process 5. THE AUTOCORRELATION FUNCTION

15 The Autocorrelation Function of an MA(1) Process Consider y t = ε t + βε t 1. Again, multiply y t by each y t s and take expectations γ 0 = var(y t ) = Ey t y t = E[(ε t + βε t 1 )(ε t + βε t 1 )] = (1 + β 2 )σ 2 γ 1 = cov(y t y t 1 ) = Ey t y t 1 = E[(ε t + βε t 1 )(ε t 1 + βε t 2 )] = βσ 2 and γ s = Ey t y t s = E[(ε t + βε t 1 )(ε t s + βε t s 1 )] = 0 for all s > 1

16

17 The ACF of an ARMA(1, 1) Process: Let y t = a 1 y t 1 + ε t + β 1 ε t 1. Ey t y t = a 1 Ey t 1 y t + Eε t y t + β 1 Eε t 1 y t γ 0 = a 1 γ 1 + σ 2 + β 1 (a 1 +β 1 )σ 2 Ey t y t 1 = a 1 Ey t 1 y t 1 + Eε t y t 1 + β 1 Eε t 1 y t 1 γ 1 = a 1 γ 0 + β 1 σ 2 Ey t y t 2 = a 1 Ey t 1 y t 2 + Eε t y t 2 + β 1 Eε t 1 y t 2 γ 2 = a 1 γ 1. Ey t y t s = a 1 Ey t 1 y t s + Eε t y t s + β 1 Eε t 1 y t s γ s = a 1 γ s 1

18 ACF of an AR(2) Process Ey t y t = a 1 Ey t 1 y t + a 2 Ey t 2 y t + Eε t y t Ey t y t 1 = a 1 Ey t 1 y t 1 + a 2 Ey t 2 y t 1 + Eε t y t 1 Ey t y t 2 = a 1 Ey t 1 y t 2 + a 2 Ey t 2 y t 2 + Eε t y t 2.. Ey t y t s = a 1 Ey t 1 y t s + a 2 Ey t 2 y t s + Eε t y t s So that γ 0 = a 1 γ 1 + a 2 γ 2 + σ 2 γ 1 = a 1 γ 0 + a 2 γ 1 ρ 1 = a 1 /(1 - a 2 ) γ s = a 1 γ s 1 + a 2 γ s 2 ρ i = a 1 ρ i-1 + a 2 ρ i-2

19 6. THE PARTIAL AUTOCORRELATION FUNCTION

20 PACF of an AR Process y t = a + a 1 y t-1 + ε t y t = a + a 1 y t-1 + a 2 y t-2 + ε t y t = a + a 1 y t-1 + a 2 y t-2 + a 3 y t-3 + ε t The successive estimates of the a i are the partial autocorrelations

21 PACF of a MA(1) y t = ε t + β 1 ε t-1 but ε t-1 = y t-1 - β 1 ε t-2 y t = ε t + β 1 [ y t-1 - β 1 ε t-2 ] = ε t + β 1 y t-1 (β 1 ) 2 ε t-2 y t = ε t + β 1 y t-1 (β 1 ) 2 [y t-2 - β 1 ε t-3 ] It looks like an MA( )

22 or Using Lag Operators y t = ε t + β 1 ε t 1 = (1 + β 1 L)ε t y t /(1 + β 1 L) = ε t Recall y t /(1 a 1 L) = y t + a 1 y t 1 + a 12 y t 2 + a 13 y t 3 + so that β 1 plays the role of a 1 y t /(1 + β 1 L)ε t = y t /[1 ( β 1 )L]ε t = y t β 1 y t 1 + β 12 y t 2 a 13 y t 3 + = ε t or y t =β 1 y t 1 β 12 y t 2 + β 13 y t 3 + = ε t

23 Summary: Autocorrelations and Partial Autocorrelations ACF AR(1) geometric decay MA(q) cuts off at lag q PACF AR(p) Cuts off at lag p MA(1) Geometric Decay

24 For stationary processes, the key points to note are the following: 1. The ACF of an ARMA(p,q) process will begin to decay after lag q. After lag q, the coefficients of the ACF (i.e., the r i ) will satisfy the difference equation (ρ i = a 1 ρ i 1 + a 2 ρ i a p ρ i-p ). 2. The PACF of an ARMA(p,q) process will begin to decay after lag p. After lag p, the coefficients of the PACF (i.e., the f ss ) will mimic the ACF coefficients from the model y t /(1 + β 1 L + β 2 L β q L q ).

All φ ss = 0 AR(1): a 1 > 0 s Direct exponential decay: ρ s = a φ 1 11 = ρ 1 ; φ ss = 0 for s 2 AR(1): a 1 < 0 s")

25 TABLE 2.1: Properties of the ACF and PACF Process ACF PACF White Noise All ρ s = 0 (s 0) All φ ss = 0 AR(1): a 1 > 0 s Direct exponential decay: ρ s = a φ 1 11 = ρ 1 ; φ ss = 0 for s 2 AR(1): a 1 < 0 s Oscillating decay: ρ s = a φ 1 11 = ρ 1 ; φ ss = 0 for s 2 AR(p) Decays toward zero. Coefficients may oscillate. Spikes through lag p. All φ ss = 0 for s > p. MA(1): β > 0 Positive spike at lag 1. ρ s = 0 for s 2 Oscillating decay: φ 11 > 0. MA(1): β < 0 Negative spike at lag 1. ρ s = 0 for s 2 Geometric decay: φ 11 < 0. ARMA(1, 1) a 1 > 0 ARMA(1, 1) a 1 < 0 ARMA(p, q) Geometric decay beginning after lag1. Sign ρ 1 = sign(a 1 +β) Oscillating decay beginning after lag 1. Sign ρ 1 = sign(a 1 +β) Decay (either direct or oscillatory) beginning after lag q. Oscillating decay after lag 1. φ 11 = ρ 1 Geometric decay beginning after lag 1. φ 11 = ρ 1 and sign(φ ss ) = sign(φ 11 ). Decay (either direct or oscillatory) beginning after lag p.

26 Testing the significance of ρ i Under the null ρ i = 0, the sample distribution of is: approximately normal (but bounded at -1.0 and +1.0) when T is large distributed as a students-t when T is small. The standard formula for computing the appropriate t value to test significance of a correlation coefficient is: t = ρ ˆi T 2 1 ˆ ρ 2 i SD(ρ) = [ ( 1 ρ 2 ) / (T 2) ] 1/2 with df = T 2 In reasonably large samples, the test for the null that ρ i = 0 is simplified to T 1/2. Alternatively, the standard deviation of the correlation coefficient is (1/T) 0.5.

27 Significance Levels A single autocorrelation st.dev(ρ) = [ ( 1 ρ 2 ) / (T 2) ] ½ For small ρ and large T, st.dev( ρ ) is approx. (1/T) 1/2 If the autocorrelation exceeds 2/T 1/2 we can reject the null that r = 0. A group of k autocorrelations: Q= TT ( + 2) ρi /( T k) i= 1 Is a Chi-square with degrees of freedom = k k

28 Model Selection Criteria Estimation of an AR(1) Model Estimation of an ARMA(1, 1) Model Estimation of an AR(2) Model 7. SAMPLE AUTOCORRELATIONS OF STATIONARY SERIES

29 Sample Autocorrelations r s = T t= s+ 1 ( y y)( y y) t T t= 1 t s ( y y) t 2 Form the sample autocorrelations ( s 2 2) k /( ) k = 1 Q= TT+ r T k Test groups of correlations If the sample value of Q exceeds the critical value of χ 2 with s derees of freedom, then at least one value of r k is statistically different from zero at the specified significance level. The Box Pierce and Ljung Box Q-statistics also serve as a check to see if the residuals from an estimated ARMA(p,q) model behave as a white-noise process. However, the degrees of freedom are reduced by the number of estimated parameters

30 Model Selection AIC = T ln(sum of squared residuals) + 2n SBC = T ln(sum of squared residuals) + n ln(t) where n = number of parameters estimated (p + q + possible constant term) T = number of usable observations. ALTERNATIVE AIC * = 2ln(L)/T + 2n/T SBC * = 2ln(L)/T + n ln(t)/t where n and T are as defined above, and L =maximized value of the log of the likelihood function. For a normal distribution, 2ln(L) = Tln(2π) +Tln(σ 2 ) + (1/σ 2 ) (sum of squared residuals)

31 Figure 2.3: ACF and PACF for two simulated processes 1.00 Panel a: ACF for the AR(1) Process 1.00 Panel b: PACF for the AR(1) Process Panel c: ACF for the ARMA(1,1) Process 1.00 Panel d: PACF for the ARM1(1,1) Process

32 Table 2.2: Estimates of an AR(1) Model Model 1 Model 2 y t = a 1 y t-1 + e t y t = a 1 y t-1 + e t + b 12 e t-12 Degrees of Freedom Sum of Squared Residuals Estimated a 1 (standard error) Estimated b (standard error) (0.0624) (0.0643) (0.1141) AIC / SBC AIC = ; SBC = AIC = ; SBC = Ljung-Box Q- Q(8) = 6.43 (0.490) Q(8) = 6.48 (0.485) statistics for the Q(16) = (0.391) Q(16) = (0.400) residuals Q(24) = (0.536) Q(24) = (0.547) (significance level in parentheses)

33 Figure 2.4: ACF of the Residuals from Model 1

34 Table 2.3: Estimates of an ARMA(1,1) Model Estimates Q-Statistics AIC / SBC Model 1 a 1 : (.053) Q(8) = (.000) Q(24) = (.001) AIC = SBC = Model 2 a 1 : (.076) b 1 : (.081) Model 3 a 1 : (.093) a 2 : (.092) Q(8) = 3.86 (.695) Q(24) = (.892) Q(8) = (.057) Q(24) = (.424) AIC = SBC = AIC = SBC = 487.9

35 ACF of Nonstationary Series Differences CORRS PARTIALS

36 Parsimony Stationarity and Invertibility Goodness of Fit Post-Estimation Evaluation 8. BOX JENKINS MODEL SELECTION

37 Box Jenkins Model Selection Parsimony Extra AR coefficients reduce degrees of freedom by 2 Similar processes can be approximated by very different models Common Factor Problem y t = ε t and y t = 0.5 y t-1 + ε t - 0.5ε t-1 Hence: All t-stats should exceed 2.0 Model should have a good fit as measured by AIC or BIC (SBC)

38 Box-Jenkins II Stationarity and Invertibility t-stats, ACF, Q-stats, all assume that the process is stationary Be suspicious of implied roots near the unit circle Invertibility implies the model has a finite AR representation. No unit root in MA part of the model Diagnostic Checking Plot residuals look for outliers, periods of poor fit Residuals should be serially uncorrrelated Examine ACF and PACF of residuals Overfit the model Divide sample into subperiods F = (ssr ssr 1 ssr 2 )/(p+q+1) / (ssr 1 + ssr 2 )/(T-2p-2q-2)

39 Residuals Plot 1500 Deviations from Trend GDP What can we learn by plotting the residuals? What if there is a systematic pattern in the residuals?

40 Requirements for Box-Jenkins Successful in practice, especially short term forecasts Good forecasts generally require at least 50 observations more with seasonality Most useful for short-term forecasts You need to detrend the data. Disadvantages Need to rely on individual judgment However, very different models can provide nearly identical forecasts

41 Higher-Order Models Forecast Evaluation The Granger Newbold Test The Diebold Mariano Test 9. PROPERTIES OF FORECASTS

42 Forecasting with ARMA Models The MA(1) Model y t = β 0 + β 1 ε t-1 + ε t Updating 1 period: y t+1 = β 0 + β 1 ε t + ε t+1 Hence, the optimal 1-step ahead forecast is: E t y t+1 = β 0 + β 1 ε t Note: E t y t+j is a short-hand way to write the conditional expectation of y t+j The 2-step ahead forecast is: E t y t+2 = E t [ β 0 + β 1 ε t+1 + ε t+2 ] = β 0 Similarly, the n-step ahead forecasts are all β 0

43 Forecast errors The 1-step ahead forecast error is: y t+1 - E t y t+1 = β 0 + β 1 ε t + ε t+1 - β 0 - β 1 ε t = ε t+1 Hence, the 1-step ahead forecast error is the "unforecastable" portion of y t+1 The 2-step ahead forecast error is: y t+2 - E t y t+2 = β 0 + β 1 ε t+1 + ε t+2 - β 0 = β 1 ε t+1 + ε t+2 Forecast error variance The variance of the 1-step ahead forecast error is: var(ε t+1 ) = σ 2 The variance of the 2-step ahead forecast error is: var(β 1 ε t+1 + ε t+2 ) = (1 + β 12 )σ 2 Confidence intervals The 95% confidence interval for the 1-step ahead forecast is: β 0 + β 1 ε t ± 1.96σ The 95% confidence interval for the 2-step ahead forecast is: β 0 ± 1.96(1 + β 12 ) 1/2 σ In the general case of an MA(q), the confidence intervals increase up to lag q.

44 The AR(1) Model: y t = a 0 + a 1 y t-1 + ε t. Updating 1 period, y t+1 = a 0 + a 1 y t + ε t+1, so that E t y t+1 = a 0 + a 1 y t [ * ] The 2-step ahead forecast is: E t y t+2 = a 0 + a 1 E t y t+1 and using [ * ] E t y t+2 = a 0 + a 0 a 1 + a 12 y t It should not take too much effort to convince yourself that: E t y t+3 = a 0 + a 0 a 1 + a 0 a a 13 y t and in general: E t y t+j = a 0 [ 1 + a 1 + a a 1 j-1 ] + a 1j y t If we take the limit of E t y t+j we find that E t y t+j = a 0 /(1 - a 1 ). This result is really quite general; for any stationary ARMA model, the conditional forecast of y t+j converges to the unconditional mean.

45 Forecast errors The 1-step ahead forecast error is: y t+1 E t y t+1 = a 0 + a 1 y t + ε t+1 - a 0 - a 1 y t = ε t+1 The 2-step ahead forecast error is: y t+2 - E t y t+2. Since y t+2 = a 0 + a 1 a 0 + a 12 y t + ε t+2 + a 1 ε t+1 and E t y t+2 = a 0 + a 1 a 0 + a 12 y t, it follows that: y t+2 - E t y t+2 = ε t+2 + a 1 ε t+1 Continuing is this fashion, the j-step ahead forecast error is : y t+j - E t y t+j = ε t+j + a 1 ε t+j-1 + a 12 ε t+j-2 + a 13 ε t+j a 1 j-1 ε t+1 Forecast error variance: The j-step ahead forecast error variance is: σ 2 [ 1 + a a a a 1 2(j-1) ] The variance of the forecast error is an increasing function of j. As such, you can have more confidence in short-term forecasts than in long-term forecasts. In the limit the forecast error variance converges to σ 2 /(1-a 12 ); hence, the forecast error variance converges to the unconditional variance of the {y t } sequence.

46 Confidence intervals The 95% confidence interval for the 1-step ahead forecast is: a 0 + a 1 y t ± 1.96σ Thus, the 95% confidence interval for the 2-step ahead forecast is: a 0 (1+a 1 ) + a 12 y t ± 1.96σ(1+a 12 ) 1/2.

47 Forecast Evaluation Out-of-sample Forecasts: 1. Hold back a portion of the observations from the estimation process and estimate the alternative models over the shortened span of data. 2. Use these estimates to forecast the observations of the holdback period. 3. Compare the properties of the forecast errors from the two models. Example: 1. If {y t } contains a total of 150 observations, use the first 100 observations to estimate an AR(1) and an MA(1) and use each to forecast the value of y 101. Construct the forecast error obtained from the AR(1) and from the MA(1). 2. Reestimate an AR(1) and an MA(1) model using the first 101 observations and construct two more forecast errors. 3. Continue this process so as to obtain two series of one-step ahead forecast errors, each containing 50 observations.

48 A regression based method to assess the forecasts is to use the 50 forecasts from the AR(1) to estimate an equation of the form y 100+t = a 0 + a 1 f 1t + v 1t If the forecasts are unbiased, an F-test should allow you to impose the restriction a 0 = 0 and a 1 = 1. Repeat the process with the forecasts from the MA(1). In particular, use the 50 forecasts from the MA(1) to estimate y 100+t = b 0 + b 1 f 2t + v 2t t = 1,, 50 If the significance levels from the two F-tests are similar, you might select the model with the smallest residual variance; that is, select the AR(1) if var(v 1t ) < var(v 2t ). Instead of using a regression-based approach, many researchers would select the model with the smallest mean square prediction error (MSPE). If there are H observations in the holdback periods, the MSPE for the AR(1) can be calculated as H 1 2 MSPE = e 1i H i = 1

49 The Diebold Mariano Test Let the loss from a forecast error in period i be denoted by g(e i ). In the typical case of mean-squared errors, the loss is e t 2 We can write the differential loss in period i from using model 1 versus model 2 as d i = g(e 1i ) g(e 2i ). The mean loss can be obtained as H 1 d= ge ge H i = 1 [ ( ) ( )] 1i 2i If the {d i } series is serially uncorrelated with a sample variance of γ 0, the estimate of var(d ) is simply γ 0 /(H 1). The expression d / γ /( H 1) 0 has a t-distribution with H 1 degrees of freedom

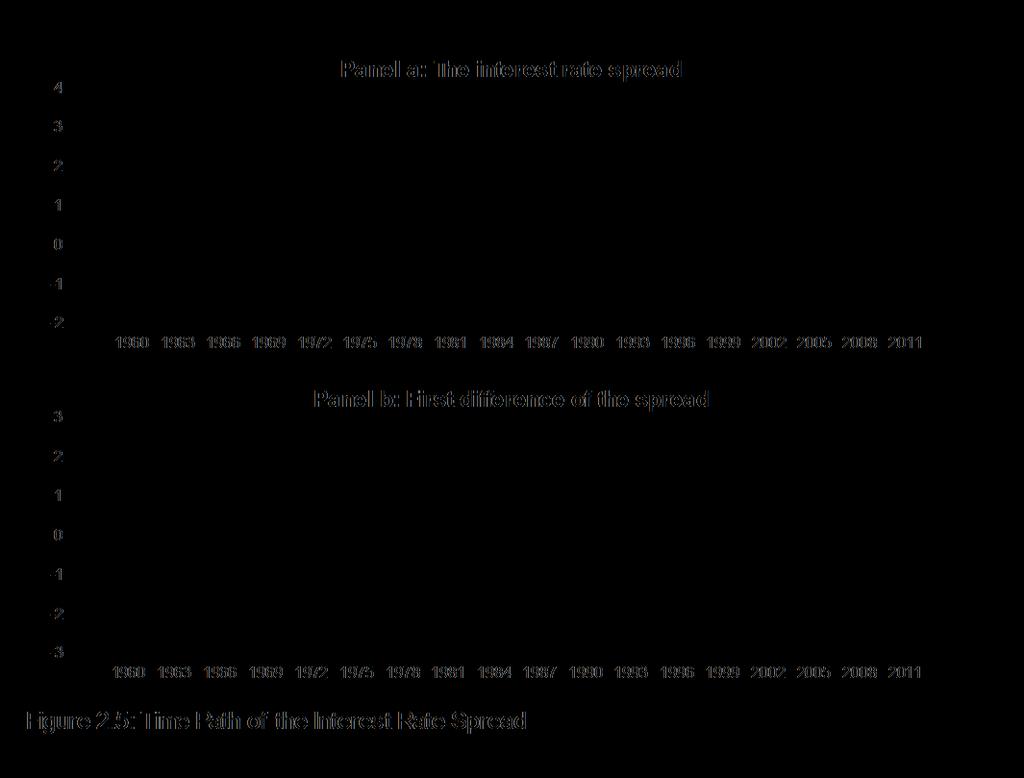

50 Out-of-Sample Forecasts 10. A MODEL OF THE INTEREST RATE SPREAD

51

52 Autocorrelations PA CF Figure 2.6: ACF and PACF of the Spread

53 Table 2.4: Estimates of the Interest Rate Spread AR(7) AR(6) AR(2) p = 1, 2, and 7 ARMA(1, 1) ARMA(2, 1) p = 2 ma = (1, 7) µ y (6.57) (7.55) (6.02) (6.80) (6.16) (5.56) (5.74) a (15.76) (15.54) (15.25) (14.83) (14.69) (2.78) (3.15) a (-4.33) (-4.11) (-3.18) (-2.80) (2.19) (3.52) a (3.68) (3.39) a (-2.70) (-2.30) a (2.02) (1.53) a (-2.86) (-2.11) a (1.93) (-0.77) β (5.23) (5.65) (9.62) β (-3.27) SSR AIC SBC Q(4) Q(8) Q(12)

54 Models of Seasonal Data Seasonal Differencing 11. SEASONALITY

55 Seasonality in the Box-Jenkins framework Seasonal AR coefficients y t = a 1 y t-1 +a 12 y t-12 + a 13 y t-13 y t = a 1 y t-1 +a 12 y t-12 + a 1 a 12 y t-13 (1 a 1 L)(1 a 12 L 12 )y t Seasonal MA Coefficients Seasonal differencing: y t = y t y t-1 versus 12 y t = y t y t-12 NOTE: You do not difference 12 times In RATS you can use: dif(sdiffs=1) y / sdy

56

57 Panel a: M1 Growth Autocorrelations PACF Figure 2.8: ACF and PACF

58 Three Models of Money growth Model 1: AR(1) with Seasonal MA m t = a 0 + a 1 m t 1 + ε t + β 4 ε t 4 Model 2: Multiplicative Autoregressive m t = a 0 + (1 + a 1 L)(1 + a 4 L 4 )m t 1 + ε t Model 3: Multiplicative Moving Average m t = a 0 + (1 + β 1 L)(1 + β 4 L 4 )ε t

59 Table 2.5 Three Models of Money Growth a (8.59) Model 1 Model 2 Model (7.66) a ( 7.28) β (6.84) β ( 15.11) ( 14.87) SSR AIC SBC Q(4) Q(8) Q(12) 1.39 (0.845) 6.34 (0.609) (0.279) 3.97 (0.410) (0.002) (0.001) (0.000) (0.000) (0.000)

60 M1 in Billions Forecasts Figure 2.9: Forecasts of M1

61 Testing for Structural Change Endogenous Breaks Parameter Instability An Example of a Break 12. PARAMETER INSTABILITY AND STRUCTURAL CHANGE

62 Parameter Instability and the CUSUMs Brown, Durbin and Evans (1975) calculate whether the cumulated sum of the forecast errors is statistically different from zero. Define: CUSUM N = ei(1) / σ e N i= n N = n,, T 1 n = date of the first forecast error you constructed, σ e is the estimated standard deviation of the forecast errors. Example: With 150 total observations (T = 150), if you start the procedure using the first 10 observations (n = 10), 140 forecast errors (T n) can be created. Note thatσ e is created using all T n forecast errors. To create CUSUM 10, use the first ten observations to create e 10 (1)/σ e. Now let N = 11 and create CUSUM 11 as [e 10 (1)+e 11 (1)]/σ e. Similarly, CUSUM T-1 = [e 10 (1)+ +e T-1 (1)]/σ e. If you use the 5% significance level, the plot value of each value of CUSUM N should be within a band of approximately ± [ (T n) (N n) (T n) -0.5 ].

63 Figure 2.10: Recursive Estimation of the Model 12 Panel 1: The Series 7 Panel 2: Intercept Intercept + 2 sds. - 2 stds. 2.0 Panel 3: AR(1) Coefficient 50 Panel 4: The CUSUM TEST AR(1) + 2 sds. - 2 stds. CUSUMS Upper 5% Lower 5%

64 Section 13 COMBINING FORECASTS

65 13 Combining Forecasts Consider the composite forecast f ct constructed as weighted average of the individual forecasts f ct = w 1 f 1t + w 2 f 2t + + w n f nt (2.71) and w i = 1 If the forecasts are unbiased (so that E t 1 f it = y t ), it follows that the composite forecast is also unbiased: E t 1 f ct = w 1 E t-1 f 1t + w 2 E t 1 f 2t + + w n E t 1 f nt = w 1 y t + w 2 y t + + w n y t = y t

66 A Simple Example To keep the notation simple, let n = 2. Subtract y t from each side of (2.71) to obtain f ct y t = w 1 (f 1t y t ) + (1 w 1 )(f 2t y t ) Now let e 1t and e 2t denote the series containing the one-step-ahead forecast errors from models 1 and 2 (i.e., e it = y t f it ) and let e ct be the composite forecast error. As such, we can write e ct = w 1 e 1t + (1 w 1 )e 2t The variance of the composite forecast error is var(e ct ) = w 12 var(e 1t ) + (1 w 1 ) 2 var(e 2t ) + 2w 1 (1 w 1 )cov(e 1t e 2t ) (2.72) Suppose that the forecast error variances are the same size and that cov(e 1t e 2t ) =0. If you take a simple average by setting w 1 = 0.5, (2.72) indicates that the variance of the composite forecast is 25% of the variances of either forecast: var(e ct ) = 0.25var(e 1t ) = 0.25var(e 2t ).

67 Optimal Weights var(e ct ) = (w 1 ) 2 var(e 1t ) + (1 w 1 ) 2 var(e 2t ) + 2w 1 (1 w 1 )cov(e 1t e 2t ) Select the weight w 1 so as to minimize var(e ct ): δ var( ect ) δ w 1 = 2w var( e) 2(1 w) var( e ) + 2(1 2 w)cov( ee ) 1 1t 1 2t 1 1t 2t Bates and Granger (1969), recommend constructing the weights excluding the covariance terms. w var( e ) var( e ) 1 * 2t 1t 1 = = 1 1 var( e1 t) + var( e2t) var( e1 t) + var( e2t) In the n-variable case: w var( e ) 1 * 1t n = var( e1 t ) + var( e2t ) var( ent )

68 Alternative methods Consider the regression equation y t = α 0 + α 1 f 1t + α 2 f 2t + + α n f nt + v t (2.75) It is also possible to force α 0 = 0 and α 1 + α α n = 1. Under these conditions, the α i s would have the direct interpretation of optimal weights. Here, an estimated weight may be negative. Some researchers would reestimate the regression without the forecast associated with the most negative coefficient. Granger and Ramanathan recommend the inclusion of an intercept to account for any bias and to leave the α i s unconstrained. As surveyed in Clemen (1989), not all researchers agree with the Granger Ramanathan recommendation and a substantial amount of work has been conducted so as to obtain optimal weights.

69 The SBC Let SBC i be the SBC from model i and let SBC * be the SBC from the best fitting model. Form α i = exp[(sbc * SBC i )/2] and then construct the weights n * i = i / i t= 1 w α α Since exp(0) = 1, the model with the best fit has the weight 1/Σα i. Since α i is decreasing in the value of SBC i, models with a poor fit with have smaller weights than models with large values of the SBC.

70 Example of the Spread I estimated seven different ARMA models of the interest rate spread. The data ends in April 2012 and if I use each of the seven models to make a one-stepahead forecast for January 2013: AR(7) AR(6) AR(2) AR( 1,2,7 ) ARMA(1,1) ARMA(2,1) ARMA(2, 1,7 ) f i2013: Simple averaging of the individual forecasts results in a combined forecast of Construct 50 1-step-ahead out-of-sample forecasts for each model so as to obtain AR(7) AR(6) AR(2) AR( 1,2,7 ) ARMA(1,1 ARMA(2,1) ARMA(2, 1,7 ) ) var(e it ) w i

71 Next, use the spread (s t ) to estimate a regression in the form of (5). If you omit the intercept and constrain the weights to unity, you should obtain: s t = 0.55f 1t 0.25f 2t 2.37f 3t f 4t f 5t 0.28f 6t f 7t (6) Although some researchers would include the negative weights in (6), most would eliminate those that are negative. If you successively reestimate the model by eliminating the forecast with the most negative coefficient, you should obtain: s t = 0.326f 4t f 5t f 7t The composite forecast using the regression method is: 0.326(0.687) (0.729) (0.799) = If you use the values of the SBC as weights, you should obtain: AR(7) AR(6) AR(2) AR( 1,2,7 ) ARMA(1,1) ARMA(2,1) ARMA(2, 1,7 ) w i The composite forecast using SBC weights is In actuality, the spread in 2013:1 turned out to be 0.74 (the actual data contains only two decimal places). Of the four methods, simple averaging and weighting by the forecast error variances did quite well. In this instance, the regression method and constructing the weights using the SBC provided the worst composite forecasts.

72 APPENDIX 2.1: ML ESTIMATION OF A REGRESSION 1 2 2πσ ε exp 2 σ 2 t 2 T 2 1 ε t exp 2 2 t = 1 2πσ 2 σ T T 1 ln L = ln(2 π) lnσ ε Let ε t = y t bx t T T T t σ t = 1 T 2 2 ln L= ln (2 π) ln σ ( ) 2 yt βxt 2 2 2σ t= 1 1 T ln L T 1 = + ( ) yt β xt σ 2σ 2σ t= 1 2 ln L 1 = y 2 x x β σ T 2 ( t t β t) t= 1

73 ML ESTIMATION OF AN MA(1) Now let y t = βε t 1 + ε t. The problem is to construct the {ε t } sequence from the observed values of {y t }. If we knew the true value of β and knew that ε 0 = 0, we could construct ε 1,, ε T recursively. Given that ε 0 = 0, it follows that: ε 1 = y 1 ε 2 = y 2 βε 1 = y 2 βy 1 ε 3 = y 3 βε 2 = y 3 β (y 2 βy 1 ) ε 4 = y 4 βε 3 = y 4 β [y 3 β (y 2 βy 1 ) ] In general, ε t = y t βε t 1 so that if L is the lag operator t 1 i t= yt/(1 + L) = ( ) yt i i= 0 T t 1 2 T T 2 1 i ln L= ln(2 π) lnσ 2 ( β) yt i 2 2 2σ t= 1 i= 0 ε β β

Empirical Market Microstructure Analysis (EMMA)

") Empirical Market Microstructure Analysis (EMMA) Lecture 3: Statistical Building Blocks and Econometric Basics Prof. Dr. Michael Stein michael.stein@vwl.uni-freiburg.de Albert-Ludwigs-University of Freiburg

Empirical Market Microstructure Analysis (EMMA) Lecture 3: Statistical Building Blocks and Econometric Basics Prof. Dr. Michael Stein michael.stein@vwl.uni-freiburg.de Albert-Ludwigs-University of Freiburg

Univariate ARIMA Models

Univariate ARIMA Models ARIMA Model Building Steps: Identification: Using graphs, statistics, ACFs and PACFs, transformations, etc. to achieve stationary and tentatively identify patterns and model components.

Univariate ARIMA Models ARIMA Model Building Steps: Identification: Using graphs, statistics, ACFs and PACFs, transformations, etc. to achieve stationary and tentatively identify patterns and model components.

Prof. Dr. Roland Füss Lecture Series in Applied Econometrics Summer Term Introduction to Time Series Analysis

Introduction to Time Series Analysis 1 Contents: I. Basics of Time Series Analysis... 4 I.1 Stationarity... 5 I.2 Autocorrelation Function... 9 I.3 Partial Autocorrelation Function (PACF)... 14 I.4 Transformation

Introduction to Time Series Analysis 1 Contents: I. Basics of Time Series Analysis... 4 I.1 Stationarity... 5 I.2 Autocorrelation Function... 9 I.3 Partial Autocorrelation Function (PACF)... 14 I.4 Transformation

at least 50 and preferably 100 observations should be available to build a proper model

III Box-Jenkins Methods 1. Pros and Cons of ARIMA Forecasting a) need for data at least 50 and preferably 100 observations should be available to build a proper model used most frequently for hourly or

III Box-Jenkins Methods 1. Pros and Cons of ARIMA Forecasting a) need for data at least 50 and preferably 100 observations should be available to build a proper model used most frequently for hourly or

NANYANG TECHNOLOGICAL UNIVERSITY SEMESTER II EXAMINATION MAS451/MTH451 Time Series Analysis TIME ALLOWED: 2 HOURS

NANYANG TECHNOLOGICAL UNIVERSITY SEMESTER II EXAMINATION 2012-2013 MAS451/MTH451 Time Series Analysis May 2013 TIME ALLOWED: 2 HOURS INSTRUCTIONS TO CANDIDATES 1. This examination paper contains FOUR (4)

NANYANG TECHNOLOGICAL UNIVERSITY SEMESTER II EXAMINATION 2012-2013 MAS451/MTH451 Time Series Analysis May 2013 TIME ALLOWED: 2 HOURS INSTRUCTIONS TO CANDIDATES 1. This examination paper contains FOUR (4)

Autoregressive Moving Average (ARMA) Models and their Practical Applications

Models and their Practical Applications") Autoregressive Moving Average (ARMA) Models and their Practical Applications Massimo Guidolin February 2018 1 Essential Concepts in Time Series Analysis 1.1 Time Series and Their Properties Time series:

Autoregressive Moving Average (ARMA) Models and their Practical Applications Massimo Guidolin February 2018 1 Essential Concepts in Time Series Analysis 1.1 Time Series and Their Properties Time series:

Covariance Stationary Time Series. Example: Independent White Noise (IWN(0,σ 2 )) Y t = ε t, ε t iid N(0,σ 2 )

) Y t = ε t, ε t iid N(0,σ 2 )") Covariance Stationary Time Series Stochastic Process: sequence of rv s ordered by time {Y t } {...,Y 1,Y 0,Y 1,...} Defn: {Y t } is covariance stationary if E[Y t ]μ for all t cov(y t,y t j )E[(Y t μ)(y

Covariance Stationary Time Series Stochastic Process: sequence of rv s ordered by time {Y t } {...,Y 1,Y 0,Y 1,...} Defn: {Y t } is covariance stationary if E[Y t ]μ for all t cov(y t,y t j )E[(Y t μ)(y

STAT Financial Time Series

STAT 6104 - Financial Time Series Chapter 4 - Estimation in the time Domain Chun Yip Yau (CUHK) STAT 6104:Financial Time Series 1 / 46 Agenda 1 Introduction 2 Moment Estimates 3 Autoregressive Models (AR

STAT 6104 - Financial Time Series Chapter 4 - Estimation in the time Domain Chun Yip Yau (CUHK) STAT 6104:Financial Time Series 1 / 46 Agenda 1 Introduction 2 Moment Estimates 3 Autoregressive Models (AR

EASTERN MEDITERRANEAN UNIVERSITY ECON 604, FALL 2007 DEPARTMENT OF ECONOMICS MEHMET BALCILAR ARIMA MODELS: IDENTIFICATION

ARIMA MODELS: IDENTIFICATION A. Autocorrelations and Partial Autocorrelations 1. Summary of What We Know So Far: a) Series y t is to be modeled by Box-Jenkins methods. The first step was to convert y t

ARIMA MODELS: IDENTIFICATION A. Autocorrelations and Partial Autocorrelations 1. Summary of What We Know So Far: a) Series y t is to be modeled by Box-Jenkins methods. The first step was to convert y t

Dynamic Time Series Regression: A Panacea for Spurious Correlations

International Journal of Scientific and Research Publications, Volume 6, Issue 10, October 2016 337 Dynamic Time Series Regression: A Panacea for Spurious Correlations Emmanuel Alphonsus Akpan *, Imoh

International Journal of Scientific and Research Publications, Volume 6, Issue 10, October 2016 337 Dynamic Time Series Regression: A Panacea for Spurious Correlations Emmanuel Alphonsus Akpan *, Imoh

FE570 Financial Markets and Trading. Stevens Institute of Technology

FE570 Financial Markets and Trading Lecture 5. Linear Time Series Analysis and Its Applications (Ref. Joel Hasbrouck - Empirical Market Microstructure ) Steve Yang Stevens Institute of Technology 9/25/2012

FE570 Financial Markets and Trading Lecture 5. Linear Time Series Analysis and Its Applications (Ref. Joel Hasbrouck - Empirical Market Microstructure ) Steve Yang Stevens Institute of Technology 9/25/2012

Applied time-series analysis

Robert M. Kunst robert.kunst@univie.ac.at University of Vienna and Institute for Advanced Studies Vienna October 18, 2011 Outline Introduction and overview Econometric Time-Series Analysis In principle,

Robert M. Kunst robert.kunst@univie.ac.at University of Vienna and Institute for Advanced Studies Vienna October 18, 2011 Outline Introduction and overview Econometric Time-Series Analysis In principle,

Lesson 13: Box-Jenkins Modeling Strategy for building ARMA models

Lesson 13: Box-Jenkins Modeling Strategy for building ARMA models Facoltà di Economia Università dell Aquila umberto.triacca@gmail.com Introduction In this lesson we present a method to construct an ARMA(p,

Lesson 13: Box-Jenkins Modeling Strategy for building ARMA models Facoltà di Economia Università dell Aquila umberto.triacca@gmail.com Introduction In this lesson we present a method to construct an ARMA(p,

TIME SERIES ANALYSIS AND FORECASTING USING THE STATISTICAL MODEL ARIMA

CHAPTER 6 TIME SERIES ANALYSIS AND FORECASTING USING THE STATISTICAL MODEL ARIMA 6.1. Introduction A time series is a sequence of observations ordered in time. A basic assumption in the time series analysis

CHAPTER 6 TIME SERIES ANALYSIS AND FORECASTING USING THE STATISTICAL MODEL ARIMA 6.1. Introduction A time series is a sequence of observations ordered in time. A basic assumption in the time series analysis

Midterm Suggested Solutions

CUHK Dept. of Economics Spring 2011 ECON 4120 Sung Y. Park Midterm Suggested Solutions Q1 (a) In time series, autocorrelation measures the correlation between y t and its lag y t τ. It is defined as. ρ(τ)

CUHK Dept. of Economics Spring 2011 ECON 4120 Sung Y. Park Midterm Suggested Solutions Q1 (a) In time series, autocorrelation measures the correlation between y t and its lag y t τ. It is defined as. ρ(τ)

Univariate Time Series Analysis; ARIMA Models

Econometrics 2 Fall 24 Univariate Time Series Analysis; ARIMA Models Heino Bohn Nielsen of4 Outline of the Lecture () Introduction to univariate time series analysis. (2) Stationarity. (3) Characterizing

Econometrics 2 Fall 24 Univariate Time Series Analysis; ARIMA Models Heino Bohn Nielsen of4 Outline of the Lecture () Introduction to univariate time series analysis. (2) Stationarity. (3) Characterizing

Ch 6. Model Specification. Time Series Analysis

We start to build ARIMA(p,d,q) models. The subjects include: 1 how to determine p, d, q for a given series (Chapter 6); 2 how to estimate the parameters (φ s and θ s) of a specific ARIMA(p,d,q) model (Chapter

We start to build ARIMA(p,d,q) models. The subjects include: 1 how to determine p, d, q for a given series (Chapter 6); 2 how to estimate the parameters (φ s and θ s) of a specific ARIMA(p,d,q) model (Chapter

Lecture 1: Stationary Time Series Analysis

Syllabus Stationarity ARMA AR MA Model Selection Estimation Lecture 1: Stationary Time Series Analysis 222061-1617: Time Series Econometrics Spring 2018 Jacek Suda Syllabus Stationarity ARMA AR MA Model

Syllabus Stationarity ARMA AR MA Model Selection Estimation Lecture 1: Stationary Time Series Analysis 222061-1617: Time Series Econometrics Spring 2018 Jacek Suda Syllabus Stationarity ARMA AR MA Model

Problem Set 2: Box-Jenkins methodology

Problem Set : Box-Jenkins methodology 1) For an AR1) process we have: γ0) = σ ε 1 φ σ ε γ0) = 1 φ Hence, For a MA1) process, p lim R = φ γ0) = 1 + θ )σ ε σ ε 1 = γ0) 1 + θ Therefore, p lim R = 1 1 1 +

Problem Set : Box-Jenkins methodology 1) For an AR1) process we have: γ0) = σ ε 1 φ σ ε γ0) = 1 φ Hence, For a MA1) process, p lim R = φ γ0) = 1 + θ )σ ε σ ε 1 = γ0) 1 + θ Therefore, p lim R = 1 1 1 +

Circle a single answer for each multiple choice question. Your choice should be made clearly.

TEST #1 STA 4853 March 4, 215 Name: Please read the following directions. DO NOT TURN THE PAGE UNTIL INSTRUCTED TO DO SO Directions This exam is closed book and closed notes. There are 31 questions. Circle

TEST #1 STA 4853 March 4, 215 Name: Please read the following directions. DO NOT TURN THE PAGE UNTIL INSTRUCTED TO DO SO Directions This exam is closed book and closed notes. There are 31 questions. Circle

Topic 4 Unit Roots. Gerald P. Dwyer. February Clemson University

Topic 4 Unit Roots Gerald P. Dwyer Clemson University February 2016 Outline 1 Unit Roots Introduction Trend and Difference Stationary Autocorrelations of Series That Have Deterministic or Stochastic Trends

Topic 4 Unit Roots Gerald P. Dwyer Clemson University February 2016 Outline 1 Unit Roots Introduction Trend and Difference Stationary Autocorrelations of Series That Have Deterministic or Stochastic Trends

Time Series Analysis

Time Series Analysis Christopher Ting http://mysmu.edu.sg/faculty/christophert/ christopherting@smu.edu.sg Quantitative Finance Singapore Management University March 3, 2017 Christopher Ting Week 9 March

Time Series Analysis Christopher Ting http://mysmu.edu.sg/faculty/christophert/ christopherting@smu.edu.sg Quantitative Finance Singapore Management University March 3, 2017 Christopher Ting Week 9 March

Chapter 4: Models for Stationary Time Series

Chapter 4: Models for Stationary Time Series Now we will introduce some useful parametric models for time series that are stationary processes. We begin by defining the General Linear Process. Let {Y t

Chapter 4: Models for Stationary Time Series Now we will introduce some useful parametric models for time series that are stationary processes. We begin by defining the General Linear Process. Let {Y t

Circle the single best answer for each multiple choice question. Your choice should be made clearly.

TEST #1 STA 4853 March 6, 2017 Name: Please read the following directions. DO NOT TURN THE PAGE UNTIL INSTRUCTED TO DO SO Directions This exam is closed book and closed notes. There are 32 multiple choice

TEST #1 STA 4853 March 6, 2017 Name: Please read the following directions. DO NOT TURN THE PAGE UNTIL INSTRUCTED TO DO SO Directions This exam is closed book and closed notes. There are 32 multiple choice

Class 1: Stationary Time Series Analysis

Class 1: Stationary Time Series Analysis Macroeconometrics - Fall 2009 Jacek Suda, BdF and PSE February 28, 2011 Outline Outline: 1 Covariance-Stationary Processes 2 Wold Decomposition Theorem 3 ARMA Models

Class 1: Stationary Time Series Analysis Macroeconometrics - Fall 2009 Jacek Suda, BdF and PSE February 28, 2011 Outline Outline: 1 Covariance-Stationary Processes 2 Wold Decomposition Theorem 3 ARMA Models

TIME SERIES ANALYSIS. Forecasting and Control. Wiley. Fifth Edition GWILYM M. JENKINS GEORGE E. P. BOX GREGORY C. REINSEL GRETA M.

TIME SERIES ANALYSIS Forecasting and Control Fifth Edition GEORGE E. P. BOX GWILYM M. JENKINS GREGORY C. REINSEL GRETA M. LJUNG Wiley CONTENTS PREFACE TO THE FIFTH EDITION PREFACE TO THE FOURTH EDITION

TIME SERIES ANALYSIS Forecasting and Control Fifth Edition GEORGE E. P. BOX GWILYM M. JENKINS GREGORY C. REINSEL GRETA M. LJUNG Wiley CONTENTS PREFACE TO THE FIFTH EDITION PREFACE TO THE FOURTH EDITION

Econometrics II Heij et al. Chapter 7.1

Chapter 7.1 p. 1/2 Econometrics II Heij et al. Chapter 7.1 Linear Time Series Models for Stationary data Marius Ooms Tinbergen Institute Amsterdam Chapter 7.1 p. 2/2 Program Introduction Modelling philosophy

Chapter 7.1 p. 1/2 Econometrics II Heij et al. Chapter 7.1 Linear Time Series Models for Stationary data Marius Ooms Tinbergen Institute Amsterdam Chapter 7.1 p. 2/2 Program Introduction Modelling philosophy

Note: The primary reference for these notes is Enders (2004). An alternative and more technical treatment can be found in Hamilton (1994).

. An alternative and more technical treatment can be found in Hamilton (1994).") Chapter 4 Analysis of a Single Time Series Note: The primary reference for these notes is Enders (4). An alternative and more technical treatment can be found in Hamilton (994). Most data used in financial

Chapter 4 Analysis of a Single Time Series Note: The primary reference for these notes is Enders (4). An alternative and more technical treatment can be found in Hamilton (994). Most data used in financial

Stat 5100 Handout #12.e Notes: ARIMA Models (Unit 7) Key here: after stationary, identify dependence structure (and use for forecasting)

Key here: after stationary, identify dependence structure (and use for forecasting)") Stat 5100 Handout #12.e Notes: ARIMA Models (Unit 7) Key here: after stationary, identify dependence structure (and use for forecasting) (overshort example) White noise H 0 : Let Z t be the stationary

Stat 5100 Handout #12.e Notes: ARIMA Models (Unit 7) Key here: after stationary, identify dependence structure (and use for forecasting) (overshort example) White noise H 0 : Let Z t be the stationary

MODELING INFLATION RATES IN NIGERIA: BOX-JENKINS APPROACH. I. U. Moffat and A. E. David Department of Mathematics & Statistics, University of Uyo, Uyo

Vol.4, No.2, pp.2-27, April 216 MODELING INFLATION RATES IN NIGERIA: BOX-JENKINS APPROACH I. U. Moffat and A. E. David Department of Mathematics & Statistics, University of Uyo, Uyo ABSTRACT: This study

Vol.4, No.2, pp.2-27, April 216 MODELING INFLATION RATES IN NIGERIA: BOX-JENKINS APPROACH I. U. Moffat and A. E. David Department of Mathematics & Statistics, University of Uyo, Uyo ABSTRACT: This study

Econ 623 Econometrics II Topic 2: Stationary Time Series

1 Introduction Econ 623 Econometrics II Topic 2: Stationary Time Series In the regression model we can model the error term as an autoregression AR(1) process. That is, we can use the past value of the

1 Introduction Econ 623 Econometrics II Topic 2: Stationary Time Series In the regression model we can model the error term as an autoregression AR(1) process. That is, we can use the past value of the

1 Time Series Concepts and Challenges

Forecasting Time Series Data Notes from Rebecca Sela Stern Business School Spring, 2004 1 Time Series Concepts and Challenges The linear regression model (and most other models) assume that observations

Forecasting Time Series Data Notes from Rebecca Sela Stern Business School Spring, 2004 1 Time Series Concepts and Challenges The linear regression model (and most other models) assume that observations

Module 3. Descriptive Time Series Statistics and Introduction to Time Series Models

Module 3 Descriptive Time Series Statistics and Introduction to Time Series Models Class notes for Statistics 451: Applied Time Series Iowa State University Copyright 2015 W Q Meeker November 11, 2015

Module 3 Descriptive Time Series Statistics and Introduction to Time Series Models Class notes for Statistics 451: Applied Time Series Iowa State University Copyright 2015 W Q Meeker November 11, 2015

Ross Bettinger, Analytical Consultant, Seattle, WA

ABSTRACT DYNAMIC REGRESSION IN ARIMA MODELING Ross Bettinger, Analytical Consultant, Seattle, WA Box-Jenkins time series models that contain exogenous predictor variables are called dynamic regression

ABSTRACT DYNAMIC REGRESSION IN ARIMA MODELING Ross Bettinger, Analytical Consultant, Seattle, WA Box-Jenkins time series models that contain exogenous predictor variables are called dynamic regression

Lecture 2: Univariate Time Series

Lecture 2: Univariate Time Series Analysis: Conditional and Unconditional Densities, Stationarity, ARMA Processes Prof. Massimo Guidolin 20192 Financial Econometrics Spring/Winter 2017 Overview Motivation:

Lecture 2: Univariate Time Series Analysis: Conditional and Unconditional Densities, Stationarity, ARMA Processes Prof. Massimo Guidolin 20192 Financial Econometrics Spring/Winter 2017 Overview Motivation:

A time series is called strictly stationary if the joint distribution of every collection (Y t

5 Time series A time series is a set of observations recorded over time. You can think for example at the GDP of a country over the years (or quarters) or the hourly measurements of temperature over a

5 Time series A time series is a set of observations recorded over time. You can think for example at the GDP of a country over the years (or quarters) or the hourly measurements of temperature over a

{ } Stochastic processes. Models for time series. Specification of a process. Specification of a process. , X t3. ,...X tn }

Stochastic processes Time series are an example of a stochastic or random process Models for time series A stochastic process is 'a statistical phenomenon that evolves in time according to probabilistic

Stochastic processes Time series are an example of a stochastic or random process Models for time series A stochastic process is 'a statistical phenomenon that evolves in time according to probabilistic

Ch 8. MODEL DIAGNOSTICS. Time Series Analysis

Model diagnostics is concerned with testing the goodness of fit of a model and, if the fit is poor, suggesting appropriate modifications. We shall present two complementary approaches: analysis of residuals

Model diagnostics is concerned with testing the goodness of fit of a model and, if the fit is poor, suggesting appropriate modifications. We shall present two complementary approaches: analysis of residuals

Univariate linear models

Univariate linear models The specification process of an univariate ARIMA model is based on the theoretical properties of the different processes and it is also important the observation and interpretation

Univariate linear models The specification process of an univariate ARIMA model is based on the theoretical properties of the different processes and it is also important the observation and interpretation

10. Time series regression and forecasting

10. Time series regression and forecasting Key feature of this section: Analysis of data on a single entity observed at multiple points in time (time series data) Typical research questions: What is the

10. Time series regression and forecasting Key feature of this section: Analysis of data on a single entity observed at multiple points in time (time series data) Typical research questions: What is the

Solutions to Odd-Numbered End-of-Chapter Exercises: Chapter 14

Introduction to Econometrics (3 rd Updated Edition) by James H. Stock and Mark W. Watson Solutions to Odd-Numbered End-of-Chapter Exercises: Chapter 14 (This version July 0, 014) 015 Pearson Education,

Introduction to Econometrics (3 rd Updated Edition) by James H. Stock and Mark W. Watson Solutions to Odd-Numbered End-of-Chapter Exercises: Chapter 14 (This version July 0, 014) 015 Pearson Education,

2. An Introduction to Moving Average Models and ARMA Models

. An Introduction to Moving Average Models and ARMA Models.1 White Noise. The MA(1) model.3 The MA(q) model..4 Estimation and forecasting of MA models..5 ARMA(p,q) models. The Moving Average (MA) models

. An Introduction to Moving Average Models and ARMA Models.1 White Noise. The MA(1) model.3 The MA(q) model..4 Estimation and forecasting of MA models..5 ARMA(p,q) models. The Moving Average (MA) models

CHAPTER 8 FORECASTING PRACTICE I

CHAPTER 8 FORECASTING PRACTICE I Sometimes we find time series with mixed AR and MA properties (ACF and PACF) We then can use mixed models: ARMA(p,q) These slides are based on: González-Rivera: Forecasting

CHAPTER 8 FORECASTING PRACTICE I Sometimes we find time series with mixed AR and MA properties (ACF and PACF) We then can use mixed models: ARMA(p,q) These slides are based on: González-Rivera: Forecasting

SOME BASICS OF TIME-SERIES ANALYSIS

SOME BASICS OF TIME-SERIES ANALYSIS John E. Floyd University of Toronto December 8, 26 An excellent place to learn about time series analysis is from Walter Enders textbook. For a basic understanding of

SOME BASICS OF TIME-SERIES ANALYSIS John E. Floyd University of Toronto December 8, 26 An excellent place to learn about time series analysis is from Walter Enders textbook. For a basic understanding of

Econ 424 Time Series Concepts

Econ 424 Time Series Concepts Eric Zivot January 20 2015 Time Series Processes Stochastic (Random) Process { 1 2 +1 } = { } = sequence of random variables indexed by time Observed time series of length

Econ 424 Time Series Concepts Eric Zivot January 20 2015 Time Series Processes Stochastic (Random) Process { 1 2 +1 } = { } = sequence of random variables indexed by time Observed time series of length

Estimation and application of best ARIMA model for forecasting the uranium price.

Estimation and application of best ARIMA model for forecasting the uranium price. Medeu Amangeldi May 13, 2018 Capstone Project Superviser: Dongming Wei Second reader: Zhenisbek Assylbekov Abstract This

Estimation and application of best ARIMA model for forecasting the uranium price. Medeu Amangeldi May 13, 2018 Capstone Project Superviser: Dongming Wei Second reader: Zhenisbek Assylbekov Abstract This

Lecture 1: Stationary Time Series Analysis

Syllabus Stationarity ARMA AR MA Model Selection Estimation Forecasting Lecture 1: Stationary Time Series Analysis 222061-1617: Time Series Econometrics Spring 2018 Jacek Suda Syllabus Stationarity ARMA

Syllabus Stationarity ARMA AR MA Model Selection Estimation Forecasting Lecture 1: Stationary Time Series Analysis 222061-1617: Time Series Econometrics Spring 2018 Jacek Suda Syllabus Stationarity ARMA

Ch. 15 Forecasting. 1.1 Forecasts Based on Conditional Expectations

Ch 15 Forecasting Having considered in Chapter 14 some of the properties of ARMA models, we now show how they may be used to forecast future values of an observed time series For the present we proceed

Ch 15 Forecasting Having considered in Chapter 14 some of the properties of ARMA models, we now show how they may be used to forecast future values of an observed time series For the present we proceed

Lab: Box-Jenkins Methodology - US Wholesale Price Indicator

Lab: Box-Jenkins Methodology - US Wholesale Price Indicator In this lab we explore the Box-Jenkins methodology by applying it to a time-series data set comprising quarterly observations of the US Wholesale

Lab: Box-Jenkins Methodology - US Wholesale Price Indicator In this lab we explore the Box-Jenkins methodology by applying it to a time-series data set comprising quarterly observations of the US Wholesale

ARIMA Models. Jamie Monogan. January 16, University of Georgia. Jamie Monogan (UGA) ARIMA Models January 16, / 27

ARIMA Models January 16, / 27") ARIMA Models Jamie Monogan University of Georgia January 16, 2018 Jamie Monogan (UGA) ARIMA Models January 16, 2018 1 / 27 Objectives By the end of this meeting, participants should be able to: Argue why

ARIMA Models Jamie Monogan University of Georgia January 16, 2018 Jamie Monogan (UGA) ARIMA Models January 16, 2018 1 / 27 Objectives By the end of this meeting, participants should be able to: Argue why

Chapter 12: An introduction to Time Series Analysis. Chapter 12: An introduction to Time Series Analysis

Chapter 12: An introduction to Time Series Analysis Introduction In this chapter, we will discuss forecasting with single-series (univariate) Box-Jenkins models. The common name of the models is Auto-Regressive

Chapter 12: An introduction to Time Series Analysis Introduction In this chapter, we will discuss forecasting with single-series (univariate) Box-Jenkins models. The common name of the models is Auto-Regressive

Discrete time processes

Discrete time processes Predictions are difficult. Especially about the future Mark Twain. Florian Herzog 2013 Modeling observed data When we model observed (realized) data, we encounter usually the following

Discrete time processes Predictions are difficult. Especially about the future Mark Twain. Florian Herzog 2013 Modeling observed data When we model observed (realized) data, we encounter usually the following

Some Time-Series Models

Some Time-Series Models Outline 1. Stochastic processes and their properties 2. Stationary processes 3. Some properties of the autocorrelation function 4. Some useful models Purely random processes, random

Some Time-Series Models Outline 1. Stochastic processes and their properties 2. Stationary processes 3. Some properties of the autocorrelation function 4. Some useful models Purely random processes, random

Stochastic Modelling Solutions to Exercises on Time Series

Stochastic Modelling Solutions to Exercises on Time Series Dr. Iqbal Owadally March 3, 2003 Solutions to Elementary Problems Q1. (i) (1 0.5B)X t = Z t. The characteristic equation 1 0.5z = 0 does not have

Stochastic Modelling Solutions to Exercises on Time Series Dr. Iqbal Owadally March 3, 2003 Solutions to Elementary Problems Q1. (i) (1 0.5B)X t = Z t. The characteristic equation 1 0.5z = 0 does not have

Econometric Forecasting

Robert M. Kunst robert.kunst@univie.ac.at University of Vienna and Institute for Advanced Studies Vienna October 1, 2014 Outline Introduction Model-free extrapolation Univariate time-series models Trend

Robert M. Kunst robert.kunst@univie.ac.at University of Vienna and Institute for Advanced Studies Vienna October 1, 2014 Outline Introduction Model-free extrapolation Univariate time-series models Trend

10) Time series econometrics

Time series econometrics") 30C00200 Econometrics 10) Time series econometrics Timo Kuosmanen Professor, Ph.D. 1 Topics today Static vs. dynamic time series model Suprious regression Stationary and nonstationary time series Unit

30C00200 Econometrics 10) Time series econometrics Timo Kuosmanen Professor, Ph.D. 1 Topics today Static vs. dynamic time series model Suprious regression Stationary and nonstationary time series Unit

ARIMA Modelling and Forecasting

ARIMA Modelling and Forecasting Economic time series often appear nonstationary, because of trends, seasonal patterns, cycles, etc. However, the differences may appear stationary. Δx t x t x t 1 (first

ARIMA Modelling and Forecasting Economic time series often appear nonstationary, because of trends, seasonal patterns, cycles, etc. However, the differences may appear stationary. Δx t x t x t 1 (first

Lecture 3: Autoregressive Moving Average (ARMA) Models and their Practical Applications

Models and their Practical Applications") Lecture 3: Autoregressive Moving Average (ARMA) Models and their Practical Applications Prof. Massimo Guidolin 20192 Financial Econometrics Winter/Spring 2018 Overview Moving average processes Autoregressive

Lecture 3: Autoregressive Moving Average (ARMA) Models and their Practical Applications Prof. Massimo Guidolin 20192 Financial Econometrics Winter/Spring 2018 Overview Moving average processes Autoregressive

Chapter 9: Forecasting

Chapter 9: Forecasting One of the critical goals of time series analysis is to forecast (predict) the values of the time series at times in the future. When forecasting, we ideally should evaluate the

Chapter 9: Forecasting One of the critical goals of time series analysis is to forecast (predict) the values of the time series at times in the future. When forecasting, we ideally should evaluate the

Advanced Econometrics

Advanced Econometrics Marco Sunder Nov 04 2010 Marco Sunder Advanced Econometrics 1/ 25 Contents 1 2 3 Marco Sunder Advanced Econometrics 2/ 25 Music Marco Sunder Advanced Econometrics 3/ 25 Music Marco

Advanced Econometrics Marco Sunder Nov 04 2010 Marco Sunder Advanced Econometrics 1/ 25 Contents 1 2 3 Marco Sunder Advanced Econometrics 2/ 25 Music Marco Sunder Advanced Econometrics 3/ 25 Music Marco

Stationary Stochastic Time Series Models

Stationary Stochastic Time Series Models When modeling time series it is useful to regard an observed time series, (x 1,x,..., x n ), as the realisation of a stochastic process. In general a stochastic

Stationary Stochastic Time Series Models When modeling time series it is useful to regard an observed time series, (x 1,x,..., x n ), as the realisation of a stochastic process. In general a stochastic

FORECASTING SUGARCANE PRODUCTION IN INDIA WITH ARIMA MODEL

FORECASTING SUGARCANE PRODUCTION IN INDIA WITH ARIMA MODEL B. N. MANDAL Abstract: Yearly sugarcane production data for the period of - to - of India were analyzed by time-series methods. Autocorrelation

FORECASTING SUGARCANE PRODUCTION IN INDIA WITH ARIMA MODEL B. N. MANDAL Abstract: Yearly sugarcane production data for the period of - to - of India were analyzed by time-series methods. Autocorrelation

Introduction to Time Series Analysis. Lecture 11.

Introduction to Time Series Analysis. Lecture 11. Peter Bartlett 1. Review: Time series modelling and forecasting 2. Parameter estimation 3. Maximum likelihood estimator 4. Yule-Walker estimation 5. Yule-Walker

Introduction to Time Series Analysis. Lecture 11. Peter Bartlett 1. Review: Time series modelling and forecasting 2. Parameter estimation 3. Maximum likelihood estimator 4. Yule-Walker estimation 5. Yule-Walker

Lecture on ARMA model

Lecture on ARMA model Robert M. de Jong Ohio State University Columbus, OH 43210 USA Chien-Ho Wang National Taipei University Taipei City, 104 Taiwan ROC October 19, 2006 (Very Preliminary edition, Comment

Lecture on ARMA model Robert M. de Jong Ohio State University Columbus, OH 43210 USA Chien-Ho Wang National Taipei University Taipei City, 104 Taiwan ROC October 19, 2006 (Very Preliminary edition, Comment

Econometrics I. Professor William Greene Stern School of Business Department of Economics 25-1/25. Part 25: Time Series

Econometrics I Professor William Greene Stern School of Business Department of Economics 25-1/25 Econometrics I Part 25 Time Series 25-2/25 Modeling an Economic Time Series Observed y 0, y 1,, y t, What

Econometrics I Professor William Greene Stern School of Business Department of Economics 25-1/25 Econometrics I Part 25 Time Series 25-2/25 Modeling an Economic Time Series Observed y 0, y 1,, y t, What

Review Session: Econometrics - CLEFIN (20192)

") Review Session: Econometrics - CLEFIN (20192) Part II: Univariate time series analysis Daniele Bianchi March 20, 2013 Fundamentals Stationarity A time series is a sequence of random variables x t, t =

Review Session: Econometrics - CLEFIN (20192) Part II: Univariate time series analysis Daniele Bianchi March 20, 2013 Fundamentals Stationarity A time series is a sequence of random variables x t, t =

CHAPTER 8 MODEL DIAGNOSTICS. 8.1 Residual Analysis

CHAPTER 8 MODEL DIAGNOSTICS We have now discussed methods for specifying models and for efficiently estimating the parameters in those models. Model diagnostics, or model criticism, is concerned with testing

CHAPTER 8 MODEL DIAGNOSTICS We have now discussed methods for specifying models and for efficiently estimating the parameters in those models. Model diagnostics, or model criticism, is concerned with testing

Time Series I Time Domain Methods

Astrostatistics Summer School Penn State University University Park, PA 16802 May 21, 2007 Overview Filtering and the Likelihood Function Time series is the study of data consisting of a sequence of DEPENDENT

Astrostatistics Summer School Penn State University University Park, PA 16802 May 21, 2007 Overview Filtering and the Likelihood Function Time series is the study of data consisting of a sequence of DEPENDENT

Econometrics I: Univariate Time Series Econometrics (1)

") Econometrics I: Dipartimento di Economia Politica e Metodi Quantitativi University of Pavia Overview of the Lecture 1 st EViews Session VI: Some Theoretical Premises 2 Overview of the Lecture 1 st EViews

Econometrics I: Dipartimento di Economia Politica e Metodi Quantitativi University of Pavia Overview of the Lecture 1 st EViews Session VI: Some Theoretical Premises 2 Overview of the Lecture 1 st EViews

G. S. Maddala Kajal Lahiri. WILEY A John Wiley and Sons, Ltd., Publication

G. S. Maddala Kajal Lahiri WILEY A John Wiley and Sons, Ltd., Publication TEMT Foreword Preface to the Fourth Edition xvii xix Part I Introduction and the Linear Regression Model 1 CHAPTER 1 What is Econometrics?

G. S. Maddala Kajal Lahiri WILEY A John Wiley and Sons, Ltd., Publication TEMT Foreword Preface to the Fourth Edition xvii xix Part I Introduction and the Linear Regression Model 1 CHAPTER 1 What is Econometrics?

AR, MA and ARMA models

AR, MA and AR by Hedibert Lopes P Based on Tsay s Analysis of Financial Time Series (3rd edition) P 1 Stationarity 2 3 4 5 6 7 P 8 9 10 11 Outline P Linear Time Series Analysis and Its Applications For

AR, MA and AR by Hedibert Lopes P Based on Tsay s Analysis of Financial Time Series (3rd edition) P 1 Stationarity 2 3 4 5 6 7 P 8 9 10 11 Outline P Linear Time Series Analysis and Its Applications For

Time Series Models and Inference. James L. Powell Department of Economics University of California, Berkeley

Time Series Models and Inference James L. Powell Department of Economics University of California, Berkeley Overview In contrast to the classical linear regression model, in which the components of the

Time Series Models and Inference James L. Powell Department of Economics University of California, Berkeley Overview In contrast to the classical linear regression model, in which the components of the

Time Series Econometrics Lecture Notes. Burak Saltoğlu

Time Series Econometrics Lecture Notes Burak Saltoğlu May 2017 2 Contents 1 Introduction 7 1.1 Linear Time Series................................ 7 1.1.1 Why do we study time series in econometrics..............

Time Series Econometrics Lecture Notes Burak Saltoğlu May 2017 2 Contents 1 Introduction 7 1.1 Linear Time Series................................ 7 1.1.1 Why do we study time series in econometrics..............

Week 5 Quantitative Analysis of Financial Markets Characterizing Cycles

Week 5 Quantitative Analysis of Financial Markets Characterizing Cycles Christopher Ting http://www.mysmu.edu/faculty/christophert/ Christopher Ting : christopherting@smu.edu.sg : 6828 0364 : LKCSB 5036

Week 5 Quantitative Analysis of Financial Markets Characterizing Cycles Christopher Ting http://www.mysmu.edu/faculty/christophert/ Christopher Ting : christopherting@smu.edu.sg : 6828 0364 : LKCSB 5036

Ch 9. FORECASTING. Time Series Analysis

In this chapter, we assume the model is known exactly, and consider the calculation of forecasts and their properties for both deterministic trend models and ARIMA models. 9.1 Minimum Mean Square Error

In this chapter, we assume the model is known exactly, and consider the calculation of forecasts and their properties for both deterministic trend models and ARIMA models. 9.1 Minimum Mean Square Error

Econometrics of Panel Data

Econometrics of Panel Data Jakub Mućk Meeting # 9 Jakub Mućk Econometrics of Panel Data Meeting # 9 1 / 22 Outline 1 Time series analysis Stationarity Unit Root Tests for Nonstationarity 2 Panel Unit Root

Econometrics of Panel Data Jakub Mućk Meeting # 9 Jakub Mućk Econometrics of Panel Data Meeting # 9 1 / 22 Outline 1 Time series analysis Stationarity Unit Root Tests for Nonstationarity 2 Panel Unit Root

Time Series Econometrics 4 Vijayamohanan Pillai N

Time Series Econometrics 4 Vijayamohanan Pillai N Vijayamohan: CDS MPhil: Time Series 5 1 Autoregressive Moving Average Process: ARMA(p, q) Vijayamohan: CDS MPhil: Time Series 5 2 1 Autoregressive Moving

Time Series Econometrics 4 Vijayamohanan Pillai N Vijayamohan: CDS MPhil: Time Series 5 1 Autoregressive Moving Average Process: ARMA(p, q) Vijayamohan: CDS MPhil: Time Series 5 2 1 Autoregressive Moving

A SARIMAX coupled modelling applied to individual load curves intraday forecasting

A SARIMAX coupled modelling applied to individual load curves intraday forecasting Frédéric Proïa Workshop EDF Institut Henri Poincaré - Paris 05 avril 2012 INRIA Bordeaux Sud-Ouest Institut de Mathématiques

A SARIMAX coupled modelling applied to individual load curves intraday forecasting Frédéric Proïa Workshop EDF Institut Henri Poincaré - Paris 05 avril 2012 INRIA Bordeaux Sud-Ouest Institut de Mathématiques

University of Oxford. Statistical Methods Autocorrelation. Identification and Estimation

University of Oxford Statistical Methods Autocorrelation Identification and Estimation Dr. Órlaith Burke Michaelmas Term, 2011 Department of Statistics, 1 South Parks Road, Oxford OX1 3TG Contents 1 Model

University of Oxford Statistical Methods Autocorrelation Identification and Estimation Dr. Órlaith Burke Michaelmas Term, 2011 Department of Statistics, 1 South Parks Road, Oxford OX1 3TG Contents 1 Model

distributed approximately according to white noise. Likewise, for general ARMA(p,q), the residuals can be expressed as

, the residuals can be expressed as") library(forecast) log_ap

library(forecast) log_ap

Decision 411: Class 9. HW#3 issues

Decision 411: Class 9 Presentation/discussion of HW#3 Introduction to ARIMA models Rules for fitting nonseasonal models Differencing and stationarity Reading the tea leaves : : ACF and PACF plots Unit

Decision 411: Class 9 Presentation/discussion of HW#3 Introduction to ARIMA models Rules for fitting nonseasonal models Differencing and stationarity Reading the tea leaves : : ACF and PACF plots Unit

Time Series 2. Robert Almgren. Sept. 21, 2009

Time Series 2 Robert Almgren Sept. 21, 2009 This week we will talk about linear time series models: AR, MA, ARMA, ARIMA, etc. First we will talk about theory and after we will talk about fitting the models

Time Series 2 Robert Almgren Sept. 21, 2009 This week we will talk about linear time series models: AR, MA, ARMA, ARIMA, etc. First we will talk about theory and after we will talk about fitting the models

Time Series Analysis -- An Introduction -- AMS 586

Time Series Analysis -- An Introduction -- AMS 586 1 Objectives of time series analysis Data description Data interpretation Modeling Control Prediction & Forecasting 2 Time-Series Data Numerical data

Time Series Analysis -- An Introduction -- AMS 586 1 Objectives of time series analysis Data description Data interpretation Modeling Control Prediction & Forecasting 2 Time-Series Data Numerical data

Advanced Econometrics

Based on the textbook by Verbeek: A Guide to Modern Econometrics Robert M. Kunst robert.kunst@univie.ac.at University of Vienna and Institute for Advanced Studies Vienna May 2, 2013 Outline Univariate

Based on the textbook by Verbeek: A Guide to Modern Econometrics Robert M. Kunst robert.kunst@univie.ac.at University of Vienna and Institute for Advanced Studies Vienna May 2, 2013 Outline Univariate

Chapter 3 - Temporal processes

STK4150 - Intro 1 Chapter 3 - Temporal processes Odd Kolbjørnsen and Geir Storvik January 23 2017 STK4150 - Intro 2 Temporal processes Data collected over time Past, present, future, change Temporal aspect

STK4150 - Intro 1 Chapter 3 - Temporal processes Odd Kolbjørnsen and Geir Storvik January 23 2017 STK4150 - Intro 2 Temporal processes Data collected over time Past, present, future, change Temporal aspect

Stochastic Processes: I. consider bowl of worms model for oscilloscope experiment:

Stochastic Processes: I consider bowl of worms model for oscilloscope experiment: SAPAscope 2.0 / 0 1 RESET SAPA2e 22, 23 II 1 stochastic process is: Stochastic Processes: II informally: bowl + drawing

Stochastic Processes: I consider bowl of worms model for oscilloscope experiment: SAPAscope 2.0 / 0 1 RESET SAPA2e 22, 23 II 1 stochastic process is: Stochastic Processes: II informally: bowl + drawing

Chapter 8: Model Diagnostics

Chapter 8: Model Diagnostics Model diagnostics involve checking how well the model fits. If the model fits poorly, we consider changing the specification of the model. A major tool of model diagnostics

Chapter 8: Model Diagnostics Model diagnostics involve checking how well the model fits. If the model fits poorly, we consider changing the specification of the model. A major tool of model diagnostics

Basic concepts and terminology: AR, MA and ARMA processes

ECON 5101 ADVANCED ECONOMETRICS TIME SERIES Lecture note no. 1 (EB) Erik Biørn, Department of Economics Version of February 1, 2011 Basic concepts and terminology: AR, MA and ARMA processes This lecture

ECON 5101 ADVANCED ECONOMETRICS TIME SERIES Lecture note no. 1 (EB) Erik Biørn, Department of Economics Version of February 1, 2011 Basic concepts and terminology: AR, MA and ARMA processes This lecture

5 Autoregressive-Moving-Average Modeling

5 Autoregressive-Moving-Average Modeling 5. Purpose. Autoregressive-moving-average (ARMA models are mathematical models of the persistence, or autocorrelation, in a time series. ARMA models are widely

5 Autoregressive-Moving-Average Modeling 5. Purpose. Autoregressive-moving-average (ARMA models are mathematical models of the persistence, or autocorrelation, in a time series. ARMA models are widely

Minitab Project Report - Assignment 6

.. Sunspot data Minitab Project Report - Assignment Time Series Plot of y Time Series Plot of X y X 7 9 7 9 The data have a wavy pattern. However, they do not show any seasonality. There seem to be an

.. Sunspot data Minitab Project Report - Assignment Time Series Plot of y Time Series Plot of X y X 7 9 7 9 The data have a wavy pattern. However, they do not show any seasonality. There seem to be an

7. Forecasting with ARIMA models

7. Forecasting with ARIMA models 309 Outline: Introduction The prediction equation of an ARIMA model Interpreting the predictions Variance of the predictions Forecast updating Measuring predictability

7. Forecasting with ARIMA models 309 Outline: Introduction The prediction equation of an ARIMA model Interpreting the predictions Variance of the predictions Forecast updating Measuring predictability

3. ARMA Modeling. Now: Important class of stationary processes

3. ARMA Modeling Now: Important class of stationary processes Definition 3.1: (ARMA(p, q) process) Let {ɛ t } t Z WN(0, σ 2 ) be a white noise process. The process {X t } t Z is called AutoRegressive-Moving-Average

3. ARMA Modeling Now: Important class of stationary processes Definition 3.1: (ARMA(p, q) process) Let {ɛ t } t Z WN(0, σ 2 ) be a white noise process. The process {X t } t Z is called AutoRegressive-Moving-Average

Lecture 4a: ARMA Model

Lecture 4a: ARMA Model 1 2 Big Picture Most often our goal is to find a statistical model to describe real time series (estimation), and then predict the future (forecasting) One particularly popular model

Lecture 4a: ARMA Model 1 2 Big Picture Most often our goal is to find a statistical model to describe real time series (estimation), and then predict the future (forecasting) One particularly popular model

6 NONSEASONAL BOX-JENKINS MODELS

6 NONSEASONAL BOX-JENKINS MODELS In this section, we will discuss a class of models for describing time series commonly referred to as Box-Jenkins models. There are two types of Box-Jenkins models, seasonal

6 NONSEASONAL BOX-JENKINS MODELS In this section, we will discuss a class of models for describing time series commonly referred to as Box-Jenkins models. There are two types of Box-Jenkins models, seasonal

3 Theory of stationary random processes

3 Theory of stationary random processes 3.1 Linear filters and the General linear process A filter is a transformation of one random sequence {U t } into another, {Y t }. A linear filter is a transformation

3 Theory of stationary random processes 3.1 Linear filters and the General linear process A filter is a transformation of one random sequence {U t } into another, {Y t }. A linear filter is a transformation

Econometrics Summary Algebraic and Statistical Preliminaries

Econometrics Summary Algebraic and Statistical Preliminaries Elasticity: The point elasticity of Y with respect to L is given by α = ( Y/ L)/(Y/L). The arc elasticity is given by ( Y/ L)/(Y/L), when L

Econometrics Summary Algebraic and Statistical Preliminaries Elasticity: The point elasticity of Y with respect to L is given by α = ( Y/ L)/(Y/L). The arc elasticity is given by ( Y/ L)/(Y/L), when L

Forecasting using R. Rob J Hyndman. 2.4 Non-seasonal ARIMA models. Forecasting using R 1

Forecasting using R Rob J Hyndman 2.4 Non-seasonal ARIMA models Forecasting using R 1 Outline 1 Autoregressive models 2 Moving average models 3 Non-seasonal ARIMA models 4 Partial autocorrelations 5 Estimation

Forecasting using R Rob J Hyndman 2.4 Non-seasonal ARIMA models Forecasting using R 1 Outline 1 Autoregressive models 2 Moving average models 3 Non-seasonal ARIMA models 4 Partial autocorrelations 5 Estimation

ARIMA Models. Jamie Monogan. January 25, University of Georgia. Jamie Monogan (UGA) ARIMA Models January 25, / 38

ARIMA Models January 25, / 38") ARIMA Models Jamie Monogan University of Georgia January 25, 2012 Jamie Monogan (UGA) ARIMA Models January 25, 2012 1 / 38 Objectives By the end of this meeting, participants should be able to: Describe

ARIMA Models Jamie Monogan University of Georgia January 25, 2012 Jamie Monogan (UGA) ARIMA Models January 25, 2012 1 / 38 Objectives By the end of this meeting, participants should be able to: Describe

Ch. 14 Stationary ARMA Process

Ch. 14 Stationary ARMA Process A general linear stochastic model is described that suppose a time series to be generated by a linear aggregation of random shock. For practical representation it is desirable

Ch. 14 Stationary ARMA Process A general linear stochastic model is described that suppose a time series to be generated by a linear aggregation of random shock. For practical representation it is desirable

LECTURE 11. Introduction to Econometrics. Autocorrelation

LECTURE 11 Introduction to Econometrics Autocorrelation November 29, 2016 1 / 24 ON PREVIOUS LECTURES We discussed the specification of a regression equation Specification consists of choosing: 1. correct

LECTURE 11 Introduction to Econometrics Autocorrelation November 29, 2016 1 / 24 ON PREVIOUS LECTURES We discussed the specification of a regression equation Specification consists of choosing: 1. correct