Ch3. TRENDS. Time Series Analysis

|

|

|

- Stella Miles

- 6 years ago

- Views:

Transcription

1

2 3.1 Deterministic Versus Stochastic Trends The simulated random walk in Exhibit 2.1 shows a upward trend. However, it is caused by a strong correlation between the series at nearby time points. The true process is Y t = Y t 1 + e t or Y t = t i=1 e t, which has zero mean and increasing variance over time. We call such a trend a stochastic trend. By comparison, the average monthly temperature series in Exhibit 1.7 shows a cyclical trend. We may model it by Y t = µ t + X t, where µ t is a deterministic function with period 12 (µ t = µ t 12 ), and X t is a zero mean unobserved variation (or noise). We say that this model has a deterministic trend.

3 3.2 Estimation of a Constant Mean Consider a model with a constant mean function Y t = µ + X t, E(X t ) = 0. The most common estimate of µ is the sample mean Y = 1 n Y t. Then E(Y ) = µ. So Y is a unbiased estimator n t=1 of µ. If {Y t } is stationary with acf ρ k, Ex 2.17 shows that [ VarY = γ n 1 ( k ) ] ρ k. (1) n n k=1 For many stationary processes, the acf decays quickly that ρ k <. Under this assumption, we have k=0 VarY γ 0 n [ k= ρ k ] for large n.

4 So for many stationary processes {Y t }, the variance of Y is inversely proportional to n. Increasing n will improve the estimation. Ex. We use (1) to investigate Y : 1 If {X t } is white noise, then ρ k = 0 for k > 0. So VarY = γ 0 n. 2 If ρ 1 0 but ρ k = 0 for k > 1, then VarY γ 0 n (1 + 2ρ 1 ) as n. 3 If {Y t } is a MA(1) model: Y t = e t + θe t 1, then ρ 1 = θ 1 + θ 2 and ρ k = 0 for k > 1. We have VarY = γ 0 n [ 1 + 2θ 1 + θ 2 ( )] n 1 n (1 + θ)2 1 + θ 2 γ 0 n. When 1 < θ < 0, say θ = 0.5, VarY 0.2γ 0 n. Comparing with the white noise, the negative correlation ρ 1 improves the estimation significantly. When 0 < θ < 1, say θ = +0.5, VarY 1.8γ 0. The positive n correlation ρ 1 reduces the accuracy of estimation.

5 Ex. For an order one autoregressive process Y t = φy t 1 + e t, 1 < φ < 1, we can show that ρ k = φ k for all k. Then [ VarY γ ] 0 φ k (1 + φ) γ 0 = n (1 φ) n. We plot in R the function k= (1 + φ) (1 φ) phi=seq(-.95,.95,0.05) factor=(1+phi)/(1-phi) plot(y=factor,x=phi,type= l ) abline(h=1,col= red ) for 1 < φ < 1: When φ 1, the variance of Y dramatically increases. In fact, φ = 1 is the nonstationary random walk process Y t = Y t 1 + e t. The variance of Y can be very different for a nonstationary process.

6 3.3 Regression Methods We use classical regression analysis to estimate the parameters in the nonconstant mean trend models Y t = µ t + X t, where µ t is deterministic and E(X t ) = 0. These include linear, quadratic, seasonal means, and cosine trends Linear and Quadratic Trends: The deterministic trend linear model is the most widely used model: µ t = β 0 + β 1 t we call β 0 the intercept, and β 1 the slope, resp. The classical least squares regression is to find ˆβ 0 and ˆβ 1 to minimize Q(β 0, β 1 ) = [Y t (β 0 + β 1 t)] 2. t=1 Use partial derivatives to solve that (formulas are not required): n t=1 ˆβ 1 = (Y t Y )(t t) n t=1 (t, ˆβ0 = Y ˆβ 1 t, where t = n + 1 t)2 2.

7 Exhibit. SCL in the Capital Asset Pricing Model (CAPM)

8 The function lm fits a linear model (a regression model) with its first argument being a formula, i.e., an expression including a tilde sign ( ), the left-hand side of which is the response variable and the right-hand side are the covariates or explanatory variables (separated by plus signs if there are two or more covariates). The intercept term can be removed by adding the term -1 on the right-hand side of the tilde sign. The covariates must be separated with a plus sign (+).

9 The function abline is a low-level graphics function. If a fitted simple regression model is passed to it, it adds the fitted straight line to an existing graph. Any straight line of the form y = β 0 + β 1 x can be superimposed on the graph by running the command abline(a=beta0,b=beta1)

10

11 3.3.2 Cyclical or Seasonal Trends Suppose that a seasonal trend, such as the average monthly temperature data in Exhibit 1.7, can be modeled as Y t = µ t + X t, E(X t ) = 0 for all t. One suitable model may be a seasonal mean model, where there are 12 constants (parameters), β 1, β 2,, β 12, giving the expected average temperature for each of the 12 months, such that β 1 t = 1, 13, 25, β 2 t = 2, 14, 26, µ t =. β 12 t = 12, 24, 36,

12 chap3.r: Exhibit 3.3 Regression Results for the Seasonal Means Model Exhibit 3.4 Results for Seasonal Means Model with an Intercept

13 R: The expression season(tempdub) outputs the monthly index of tempdub as a factor, and saves it into the object month.. A factor is a kind of data structure for handling qualitative (nominal) data that do not have a natural ordering like numbers do. However, for purposes of summary and graphics, the user may supply the levels argument to indicate an ordering among the factor values. See TS-ch3.R

14 Exhibit. We may analyze a data set Monthly milk production: pounds per cow. Jan 62 - Dec 75 (Source: Time Series Data Library (citing: Cryer (1986))) imported from Save it as milk.csv, and analyze by the R codes in TS-ch3.R. See TS-ch3.R The model milk.m2 is a combination of linear model with seasonal mean model. We may decompose a time series into a sum or product of trend, seasonal, and stochastic components by decompose command. See TS-ch3.R

15 3.3.3 Cosine Trends: In some cases, seasonal trends can be modeled economically with cosine curves (that incorporate the smooth change expected from one time period to the next while still preserving the seasonality.) The simplest such model is Y t = µ t + X t with µ t = β 0 + β cos(2πft + Φ) = β 0 + β 1 cos(2πft) + β 2 sin(2πft) where β 1 = β cos Φ and β 2 = β sin Φ. We call β(> 0) the amplitude, f the frequency, and Φ the phase of the curve. 1/f is called the period of the cosine wave.

Exhibit 3.6 Cosine Trend for the Temperature Series (chap3.")

and sin(2πt). See TS-ch3.")

16 Exhibit 3.5 Cosine Trend Model for Temperature Series (chap3.r) Exhibit 3.6 Cosine Trend for the Temperature Series (chap3.r) The harmonic function will return a matrix of the values of cos(2πt) and sin(2πt). See TS-ch3.R for some basic commands of matrix

17 3.4 Reliability and Efficiency of Regression Estimates Reliability and efficiency of estimates lie on the variances of the estimates. Let us analyze the raliability of estimates for some deterministic trends. Assumption: the series is represented as Y t = µ t + X t, where 1 µ t is a deterministic trend of the kind linear, seasonal means, or cosine curves, and 2 {X t } is a zero-mean stationary process with autocovariance and autocorrelation functions γ k and ρ k, respectively. Parameters in a linear model are estimated according to ordinary least squares regression.

18 3.4.1 The seasonal means For N complete years of monthly data, the estimate for the mean for the jth month is By (1), Var ˆβ j = γ 0 N [ N 1 k=1 ˆβ j = 1 N N 1 i=0 Y j+12i ( 1 k N ρ 12k) ], for j = 1, 2,, 12. Only the seasonal autocorrelations, ρ 12, ρ 24,, enter into the above equation. If {X t } is white noise, then Var ˆβ j = γ 0 N. (2)

19 3.4.2 The cosine trends µ t = β 0 + β 1 cos(2πft) + β 2 sin(2πft) For any frequency of the form f = m/n, where m is an integer satisfying 1 m < n/2, the estimates ˆβ 1 and ˆβ 2 are ˆβ 1 = 2 n n t=1 [ cos ( 2πmt n ) Y t ], ˆβ 2 = 2 n n t=1 [ sin ( 2πmt n ) Y t ], (3) Because these are linear functions of {Y t }, their variances can be computed by (1). 1 If {X t } is white noise, we get Var ˆβ 1 = Var ˆβ 2 = 2γ 0 /n. 2 If m/n = 1/12 and ρ k = 0 for k > 1, then Var ˆβ 1 = 2γ 0 n [ 1 + 4ρ 1 n n 1 cos t=1 ( ) πt cos 6 ( ) ] πt + 1 When n, we have (see (3.4.5) in the textbook) Var ˆβ 1 2γ ( ( 0 π )) 1 + 2ρ 1 cos 2γ 0 n 6 n ( ρ 1). Var ˆβ 2 has the same asymptotic behavior. 6

20 3.4.3 The seasonal mean trends v.s. the cosine trends Seasonal means and cosine trends are often competing models for a cyclical trend. Consider the two estimates for the trend in µ 1 (January). For the seasonal means, the variance is given by (2). With the cosine trend model, the estimate is ( ) 2π ˆµ 1 = ˆβ 0 + ˆβ 1 cos + ˆβ 2 sin 12 ( 2π 12 The terms ˆβ 0, ˆβ 1, ˆβ 2 are uncorrelated by (3). So Varˆµ 1 = Var ˆβ 0 + Var ˆβ 1 [cos ). ( )] 2π 2 [ ( )] + Var 12 ˆβ 2π 2 2 sin. 12 (4)

21 Consider two scenarios: 1. Assume that {X t } is white noise. The seasonal means model gives Varˆµ 1 = γ 0 /N. The cosine model has Var ˆβ 1 = Var ˆβ 2 = 2γ 0 /n and so Varˆµ 1 = γ 0 n { [ ( π )] 2 [ ( π )] } cos + 2 sin = 3 γ n. Since N = 12n, the ratio of the standard deviation in the cosine model to that in the seasonal means model is 3γ 0 /n 3N γ 0 /N = n = 0.5.

22 2. Assume that {X t } has ρ k = 0 for k > 1. The seasonal means model still has Varˆµ 1 = γ 0 /N. The cosine trend model for large n has Var ˆβ 0 γ 0 n (1+2ρ 1), Var ˆβ 1 Var ˆβ 2 2γ ( ( 0 π )) 1 + 2ρ 1 cos. n 6 So (4) implies that Varˆµ 1 = γ { [ ( 0 π )]} 1 + 2ρ ρ 1 cos n 6 = γ [ ( 0 π )]} {3 + 2ρ cos. n 6 If ρ 1 = 0.4, then we get 0.814γ 0 /n, and the ratio of the standard deviation in the cosine case to the standard deviation in the seasonal means case is [(0.814γ0 ] )/n 0.814N = = 0.26, a big reduction. γ 0 /N n

23 3.4.4 The linear time trends µ t = β 0 + β 1 t The least squares estimate of the slope is n t=1 ˆβ 1 = (t t)y t n. t=1 (t t)2 Since ˆβ 1 is a linear combination of Y s, we have [ ] Var ˆβ 1 = 12γ 0 24 n s 1 n(n ) n(n 2 (t t)(s t)ρ s t 1) s=2 t=1 For the case ρ k = 0 for k > 1, we get Var ˆβ 1 = 12γ ( 0 [1 n(n 2 + 2ρ )] 12γ 0(1 + 2ρ 1 ) 1) n n(n 2 1) In this situation, the variance increases as ρ 1 increases. The case ρ 1 = 0 is the white noise case, where for large n. Var ˆβ 1 = 12γ 0 n(n 2 1). (5)

24 3.4.5 Best linear unbiased estimates (BLUE, or GLS)

25 3.5 Interpreting Regression Output In many statistical softwares, some properties of the regression output depend heavily on the regression assumption that {X t } is white noise, and some depend on the further assumption that {X t } is approximately normally distributed. These assumptions are false for many time series! Therefore, we shall be very careful in interpreting the regression outputs for time series.

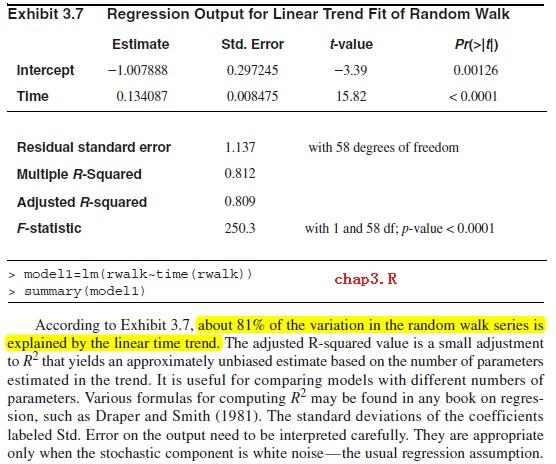

26 Consider the deterministic trend model Y t = µ t + X t. Let ˆµ t denote the estimated trend. We estimate X t by Y t ˆµ t, and the standard deviation γ0 of X t by the residual standard deviation s = 1 n (Y t ˆµ t ) n p 2 (6) where p is the number of parameters estimated in µ t and n p is the degree of freedom for s. The value of s (depent on the unit) gives an absolute measure of the goodness of fit of the estimated trend. A unitless measure of the goodness of fit is the R 2. (the coefficient of determination, or multiple R-squared). t=1 R 2 is the square of the sample correlation coefficient between the observed series and the estimated trend. R 2 is also the fraction of the variation in the series that is explained by the estimated trend.

27

28 3.6 Residual Analysis In the model Y t = µ t + X t, the unobserved stochastic component {X t } can be predicted by the residual ˆX t = Y t ˆµ t. We may investigate the standardized residual ˆX t /s. (most statistics software will produce standardized residuals using a more complicated standard error in the denominator that takes into account the specific regression model being fit.)

29 The expression rstudent(model3) returns the (externally) studentized residuals from the fitted model. [whereas rstandard(model3) gives the (internally) standardized residuals.] Exhibit 3.8 Residuals versus Time for Temperature Seasonal Means (chap3.r)

30 There are no apparent patterns relating to different months of the year. Exhibit 3.9 Residuals versus Time with Seasonal Plotting Symbols (chap3.r)

31 We look at the standardized residuals versus the corresponding trend estimate (fitted value). No dramatic patterns are found. Exhibit 3.10 Standardized Residuals versus Fitted Values for the Temperature Seasonal Means Model (chap3.r)

32 The normality of the standardized residuals may be checked by histogram and QQ plot. Gross nonnormality can be assessed by plotting a histogram of the residuals or standardized residuals.

33 Normality can be checked more carefully by plotting the so-called normal scores or quantile-quantile (QQ) plot. Such a plot displays the quantiles of the data versus the theoretical quantiles of a normal distribution. The straight-line pattern here supports the assumption of a normally distributed stochastic component in this model. qqnorm(rstudent(model3)) A reference straight line can be superimposed on the Q-Q normal score plot by qqline(rstudent(model3))

34

35 An excellent test of normality is known as the Shapiro-Wilk test. It essentially calculates the correlation between the residuals and the corresponding normal quantiles. shapiro.test(rstudent(model3)) The runs test tests the independence of a sequence of random variables by checking whether there are too many or too few runs above (or below) the median. runs(rstudent(model3))

36 The Sample Autocorrelation Function Another very important diagnostic tool for examining dependence is the sample autocorrelation function. Def. If {Y t } is a sequence of data, we define the sample autocorrelation function r k at lag k as r k = n t=k+1 (Y t Y )(Y t k Y ) n t=1 (Y t Y ) 2, for k = 1, 2, (7) A plot of r k versus lag k is often called a correlogram. When {Y t } is a stationary process, r k gives an estimate of ρ k.

acf(rstudent(model3)) Exhibit 3.")

37 win.graph(width=4.875, height=3, pointsize=8) acf(rstudent(model3)) Exhibit 3.13 Sample Autocorrelation of Residuals of Seasonal Means Model (chap3.r)

38 We now consider the standardized residuals from fitting a straight line to the rwalk dataset. Exhibit 3.14 Residuals from Straight Line Fit of the Random Walk (chap3.r)

39 Exhibit 3.15 Residuals versus Fitted Values from Straight Line Fit (chap3.r)

40 Exhibit 3.16 Sample Autocorrelation of Residuals from Straight Line Model (chap3.r)

41 Let us turn to the annual rainfall in Los Angeles (Exhibit 1.1). We found no evidence of dependence in that series, but we now look for evidence against normality. Exhibit 3.17 displays the normal quantile-quantile plot for that series. We see considerable curvature in the plot. Exhibit 3.17 Quantile-Quantile Plot of Los Angeles Annual Rainfall Series (chap3.r)

42 Exercises 3.6 & 3.12: The data file beersales contains monthly U.S. beer sales (in millions of barrels) for the period January 1975 through December (a) Display and interpret the time series plot for these data. (b) Now construct a time series plot that uses separate plotting symbols for the various months. Does your interpretation change from that in part (a)? (c) Use least squares to fit a seasonal-means trend to this time series. Interpret the regression output. Save the standardized residuals from the fit for further analysis. (d) Construct and interpret the time series plot of the standardized residuals from part (c). Be sure to use proper plotting symbols to check on seasonality in the standardized residuals. (e) Use least squares to fit a seasonal-means plus quadratic time trend to the beer sales time series. Interpret the regression output. Save the standardized residuals from the fit for further analysis. See TS-ch3.R

43 (f) Construct and interpret the time series plot of the standardized residuals from part (e). Again use proper plotting symbols to check for any remaining seasonality in the residuals. (g) Perform a runs test on the standardized residuals from part (e) and interpret the results. (h) Calculate and interpret the sample autocorrelations for the standardized residuals. (i) Investigate the normality of the standardized residuals (error terms). Consider histograms and normal probability plots. Interpret the plots. See TS-ch3.R

Chapter 3: Regression Methods for Trends

Chapter 3: Regression Methods for Trends Time series exhibiting trends over time have a mean function that is some simple function (not necessarily constant) of time. The example random walk graph from

Chapter 3: Regression Methods for Trends Time series exhibiting trends over time have a mean function that is some simple function (not necessarily constant) of time. The example random walk graph from

Econ 424 Time Series Concepts

Econ 424 Time Series Concepts Eric Zivot January 20 2015 Time Series Processes Stochastic (Random) Process { 1 2 +1 } = { } = sequence of random variables indexed by time Observed time series of length

Econ 424 Time Series Concepts Eric Zivot January 20 2015 Time Series Processes Stochastic (Random) Process { 1 2 +1 } = { } = sequence of random variables indexed by time Observed time series of length

Ch 5. Models for Nonstationary Time Series. Time Series Analysis

We have studied some deterministic and some stationary trend models. However, many time series data cannot be modeled in either way. Ex. The data set oil.price displays an increasing variation from the

We have studied some deterministic and some stationary trend models. However, many time series data cannot be modeled in either way. Ex. The data set oil.price displays an increasing variation from the

Reliability and Risk Analysis. Time Series, Types of Trend Functions and Estimates of Trends

Reliability and Risk Analysis Stochastic process The sequence of random variables {Y t, t = 0, ±1, ±2 } is called the stochastic process The mean function of a stochastic process {Y t} is the function

Reliability and Risk Analysis Stochastic process The sequence of random variables {Y t, t = 0, ±1, ±2 } is called the stochastic process The mean function of a stochastic process {Y t} is the function

Homework 2. For the homework, be sure to give full explanations where required and to turn in any relevant plots.

Homework 2 1 Data analysis problems For the homework, be sure to give full explanations where required and to turn in any relevant plots. 1. The file berkeley.dat contains average yearly temperatures for

Homework 2 1 Data analysis problems For the homework, be sure to give full explanations where required and to turn in any relevant plots. 1. The file berkeley.dat contains average yearly temperatures for

Regression of Time Series

Mahlerʼs Guide to Regression of Time Series CAS Exam S prepared by Howard C. Mahler, FCAS Copyright 2016 by Howard C. Mahler. Study Aid 2016F-S-9Supplement Howard Mahler hmahler@mac.com www.howardmahler.com/teaching

Mahlerʼs Guide to Regression of Time Series CAS Exam S prepared by Howard C. Mahler, FCAS Copyright 2016 by Howard C. Mahler. Study Aid 2016F-S-9Supplement Howard Mahler hmahler@mac.com www.howardmahler.com/teaching

Ch 9. FORECASTING. Time Series Analysis

In this chapter, we assume the model is known exactly, and consider the calculation of forecasts and their properties for both deterministic trend models and ARIMA models. 9.1 Minimum Mean Square Error

In this chapter, we assume the model is known exactly, and consider the calculation of forecasts and their properties for both deterministic trend models and ARIMA models. 9.1 Minimum Mean Square Error

3 Time Series Regression

3 Time Series Regression 3.1 Modelling Trend Using Regression Random Walk 2 0 2 4 6 8 Random Walk 0 2 4 6 8 0 10 20 30 40 50 60 (a) Time 0 10 20 30 40 50 60 (b) Time Random Walk 8 6 4 2 0 Random Walk 0

3 Time Series Regression 3.1 Modelling Trend Using Regression Random Walk 2 0 2 4 6 8 Random Walk 0 2 4 6 8 0 10 20 30 40 50 60 (a) Time 0 10 20 30 40 50 60 (b) Time Random Walk 8 6 4 2 0 Random Walk 0

Ch 8. MODEL DIAGNOSTICS. Time Series Analysis

Model diagnostics is concerned with testing the goodness of fit of a model and, if the fit is poor, suggesting appropriate modifications. We shall present two complementary approaches: analysis of residuals

Model diagnostics is concerned with testing the goodness of fit of a model and, if the fit is poor, suggesting appropriate modifications. We shall present two complementary approaches: analysis of residuals

Read Section 1.1, Examples of time series, on pages 1-8. These example introduce the book; you are not tested on them.

TS Module 1 Time series overview (The attached PDF file has better formatting.)! Model building! Time series plots Read Section 1.1, Examples of time series, on pages 1-8. These example introduce the book;

TS Module 1 Time series overview (The attached PDF file has better formatting.)! Model building! Time series plots Read Section 1.1, Examples of time series, on pages 1-8. These example introduce the book;

Ch 4. Models For Stationary Time Series. Time Series Analysis

This chapter discusses the basic concept of a broad class of stationary parametric time series models the autoregressive moving average (ARMA) models. Let {Y t } denote the observed time series, and {e

This chapter discusses the basic concept of a broad class of stationary parametric time series models the autoregressive moving average (ARMA) models. Let {Y t } denote the observed time series, and {e

Computational Data Analysis!

12.714 Computational Data Analysis! Alan Chave (alan@whoi.edu)! Thomas Herring (tah@mit.edu),! http://geoweb.mit.edu/~tah/12.714! Introduction to Spectral Analysis! Topics Today! Aspects of Time series

12.714 Computational Data Analysis! Alan Chave (alan@whoi.edu)! Thomas Herring (tah@mit.edu),! http://geoweb.mit.edu/~tah/12.714! Introduction to Spectral Analysis! Topics Today! Aspects of Time series

Chapter 12: An introduction to Time Series Analysis. Chapter 12: An introduction to Time Series Analysis

Chapter 12: An introduction to Time Series Analysis Introduction In this chapter, we will discuss forecasting with single-series (univariate) Box-Jenkins models. The common name of the models is Auto-Regressive

Chapter 12: An introduction to Time Series Analysis Introduction In this chapter, we will discuss forecasting with single-series (univariate) Box-Jenkins models. The common name of the models is Auto-Regressive

University of Oxford. Statistical Methods Autocorrelation. Identification and Estimation

University of Oxford Statistical Methods Autocorrelation Identification and Estimation Dr. Órlaith Burke Michaelmas Term, 2011 Department of Statistics, 1 South Parks Road, Oxford OX1 3TG Contents 1 Model

University of Oxford Statistical Methods Autocorrelation Identification and Estimation Dr. Órlaith Burke Michaelmas Term, 2011 Department of Statistics, 1 South Parks Road, Oxford OX1 3TG Contents 1 Model

Outline. Nature of the Problem. Nature of the Problem. Basic Econometrics in Transportation. Autocorrelation

1/30 Outline Basic Econometrics in Transportation Autocorrelation Amir Samimi What is the nature of autocorrelation? What are the theoretical and practical consequences of autocorrelation? Since the assumption

1/30 Outline Basic Econometrics in Transportation Autocorrelation Amir Samimi What is the nature of autocorrelation? What are the theoretical and practical consequences of autocorrelation? Since the assumption

Ch 6. Model Specification. Time Series Analysis

We start to build ARIMA(p,d,q) models. The subjects include: 1 how to determine p, d, q for a given series (Chapter 6); 2 how to estimate the parameters (φ s and θ s) of a specific ARIMA(p,d,q) model (Chapter

We start to build ARIMA(p,d,q) models. The subjects include: 1 how to determine p, d, q for a given series (Chapter 6); 2 how to estimate the parameters (φ s and θ s) of a specific ARIMA(p,d,q) model (Chapter

Scenario 5: Internet Usage Solution. θ j

Scenario : Internet Usage Solution Some more information would be interesting about the study in order to know if we can generalize possible findings. For example: Does each data point consist of the total

Scenario : Internet Usage Solution Some more information would be interesting about the study in order to know if we can generalize possible findings. For example: Does each data point consist of the total

Forecasting. Simon Shaw 2005/06 Semester II

Forecasting Simon Shaw s.c.shaw@maths.bath.ac.uk 2005/06 Semester II 1 Introduction A critical aspect of managing any business is planning for the future. events is called forecasting. Predicting future

Forecasting Simon Shaw s.c.shaw@maths.bath.ac.uk 2005/06 Semester II 1 Introduction A critical aspect of managing any business is planning for the future. events is called forecasting. Predicting future

Chapter 9: Forecasting

Chapter 9: Forecasting One of the critical goals of time series analysis is to forecast (predict) the values of the time series at times in the future. When forecasting, we ideally should evaluate the

Chapter 9: Forecasting One of the critical goals of time series analysis is to forecast (predict) the values of the time series at times in the future. When forecasting, we ideally should evaluate the

For a stochastic process {Y t : t = 0, ±1, ±2, ±3, }, the mean function is defined by (2.2.1) ± 2..., γ t,

± 2..., γ t,") CHAPTER 2 FUNDAMENTAL CONCEPTS This chapter describes the fundamental concepts in the theory of time series models. In particular, we introduce the concepts of stochastic processes, mean and covariance

CHAPTER 2 FUNDAMENTAL CONCEPTS This chapter describes the fundamental concepts in the theory of time series models. In particular, we introduce the concepts of stochastic processes, mean and covariance

Empirical Market Microstructure Analysis (EMMA)

") Empirical Market Microstructure Analysis (EMMA) Lecture 3: Statistical Building Blocks and Econometric Basics Prof. Dr. Michael Stein michael.stein@vwl.uni-freiburg.de Albert-Ludwigs-University of Freiburg

Empirical Market Microstructure Analysis (EMMA) Lecture 3: Statistical Building Blocks and Econometric Basics Prof. Dr. Michael Stein michael.stein@vwl.uni-freiburg.de Albert-Ludwigs-University of Freiburg

Statistics 910, #5 1. Regression Methods

Statistics 910, #5 1 Overview Regression Methods 1. Idea: effects of dependence 2. Examples of estimation (in R) 3. Review of regression 4. Comparisons and relative efficiencies Idea Decomposition Well-known

Statistics 910, #5 1 Overview Regression Methods 1. Idea: effects of dependence 2. Examples of estimation (in R) 3. Review of regression 4. Comparisons and relative efficiencies Idea Decomposition Well-known

STAT 520: Forecasting and Time Series. David B. Hitchcock University of South Carolina Department of Statistics

David B. University of South Carolina Department of Statistics What are Time Series Data? Time series data are collected sequentially over time. Some common examples include: 1. Meteorological data (temperatures,

David B. University of South Carolina Department of Statistics What are Time Series Data? Time series data are collected sequentially over time. Some common examples include: 1. Meteorological data (temperatures,

Part 1. Multiple Choice (50 questions, 1 point each) Part 2. Problems/Short Answer (10 questions, 5 points each)

Part 2. Problems/Short Answer (10 questions, 5 points each)") GROUND RULES: This exam contains two parts: Part 1. Multiple Choice (50 questions, 1 point each) Part 2. Problems/Short Answer (10 questions, 5 points each) The maximum number of points on this exam is

GROUND RULES: This exam contains two parts: Part 1. Multiple Choice (50 questions, 1 point each) Part 2. Problems/Short Answer (10 questions, 5 points each) The maximum number of points on this exam is

Part II. Time Series

Part II Time Series 12 Introduction This Part is mainly a summary of the book of Brockwell and Davis (2002). Additionally the textbook Shumway and Stoffer (2010) can be recommended. 1 Our purpose is to

Part II Time Series 12 Introduction This Part is mainly a summary of the book of Brockwell and Davis (2002). Additionally the textbook Shumway and Stoffer (2010) can be recommended. 1 Our purpose is to

Econometrics Summary Algebraic and Statistical Preliminaries

Econometrics Summary Algebraic and Statistical Preliminaries Elasticity: The point elasticity of Y with respect to L is given by α = ( Y/ L)/(Y/L). The arc elasticity is given by ( Y/ L)/(Y/L), when L

Econometrics Summary Algebraic and Statistical Preliminaries Elasticity: The point elasticity of Y with respect to L is given by α = ( Y/ L)/(Y/L). The arc elasticity is given by ( Y/ L)/(Y/L), when L

CHAPTER 8 MODEL DIAGNOSTICS. 8.1 Residual Analysis

CHAPTER 8 MODEL DIAGNOSTICS We have now discussed methods for specifying models and for efficiently estimating the parameters in those models. Model diagnostics, or model criticism, is concerned with testing

CHAPTER 8 MODEL DIAGNOSTICS We have now discussed methods for specifying models and for efficiently estimating the parameters in those models. Model diagnostics, or model criticism, is concerned with testing

Topic 4 Unit Roots. Gerald P. Dwyer. February Clemson University

Topic 4 Unit Roots Gerald P. Dwyer Clemson University February 2016 Outline 1 Unit Roots Introduction Trend and Difference Stationary Autocorrelations of Series That Have Deterministic or Stochastic Trends

Topic 4 Unit Roots Gerald P. Dwyer Clemson University February 2016 Outline 1 Unit Roots Introduction Trend and Difference Stationary Autocorrelations of Series That Have Deterministic or Stochastic Trends

Chapter 4: Models for Stationary Time Series

Chapter 4: Models for Stationary Time Series Now we will introduce some useful parametric models for time series that are stationary processes. We begin by defining the General Linear Process. Let {Y t

Chapter 4: Models for Stationary Time Series Now we will introduce some useful parametric models for time series that are stationary processes. We begin by defining the General Linear Process. Let {Y t

Some Time-Series Models

Some Time-Series Models Outline 1. Stochastic processes and their properties 2. Stationary processes 3. Some properties of the autocorrelation function 4. Some useful models Purely random processes, random

Some Time-Series Models Outline 1. Stochastic processes and their properties 2. Stationary processes 3. Some properties of the autocorrelation function 4. Some useful models Purely random processes, random

STAT Regression Methods

STAT 501 - Regression Methods Unit 9 Examples Example 1: Quake Data Let y t = the annual number of worldwide earthquakes with magnitude greater than 7 on the Richter scale for n = 99 years. Figure 1 gives

STAT 501 - Regression Methods Unit 9 Examples Example 1: Quake Data Let y t = the annual number of worldwide earthquakes with magnitude greater than 7 on the Richter scale for n = 99 years. Figure 1 gives

Applied Time Series Topics

Applied Time Series Topics Ivan Medovikov Brock University April 16, 2013 Ivan Medovikov, Brock University Applied Time Series Topics 1/34 Overview 1. Non-stationary data and consequences 2. Trends and

Applied Time Series Topics Ivan Medovikov Brock University April 16, 2013 Ivan Medovikov, Brock University Applied Time Series Topics 1/34 Overview 1. Non-stationary data and consequences 2. Trends and

Introductory Econometrics

Based on the textbook by Wooldridge: : A Modern Approach Robert M. Kunst robert.kunst@univie.ac.at University of Vienna and Institute for Advanced Studies Vienna December 17, 2012 Outline Heteroskedasticity

Based on the textbook by Wooldridge: : A Modern Approach Robert M. Kunst robert.kunst@univie.ac.at University of Vienna and Institute for Advanced Studies Vienna December 17, 2012 Outline Heteroskedasticity

Time Series Analysis -- An Introduction -- AMS 586

Time Series Analysis -- An Introduction -- AMS 586 1 Objectives of time series analysis Data description Data interpretation Modeling Control Prediction & Forecasting 2 Time-Series Data Numerical data

Time Series Analysis -- An Introduction -- AMS 586 1 Objectives of time series analysis Data description Data interpretation Modeling Control Prediction & Forecasting 2 Time-Series Data Numerical data

STAT 248: EDA & Stationarity Handout 3

STAT 248: EDA & Stationarity Handout 3 GSI: Gido van de Ven September 17th, 2010 1 Introduction Today s section we will deal with the following topics: the mean function, the auto- and crosscovariance

STAT 248: EDA & Stationarity Handout 3 GSI: Gido van de Ven September 17th, 2010 1 Introduction Today s section we will deal with the following topics: the mean function, the auto- and crosscovariance

TIME SERIES ANALYSIS. Forecasting and Control. Wiley. Fifth Edition GWILYM M. JENKINS GEORGE E. P. BOX GREGORY C. REINSEL GRETA M.

TIME SERIES ANALYSIS Forecasting and Control Fifth Edition GEORGE E. P. BOX GWILYM M. JENKINS GREGORY C. REINSEL GRETA M. LJUNG Wiley CONTENTS PREFACE TO THE FIFTH EDITION PREFACE TO THE FOURTH EDITION

TIME SERIES ANALYSIS Forecasting and Control Fifth Edition GEORGE E. P. BOX GWILYM M. JENKINS GREGORY C. REINSEL GRETA M. LJUNG Wiley CONTENTS PREFACE TO THE FIFTH EDITION PREFACE TO THE FOURTH EDITION

at least 50 and preferably 100 observations should be available to build a proper model

III Box-Jenkins Methods 1. Pros and Cons of ARIMA Forecasting a) need for data at least 50 and preferably 100 observations should be available to build a proper model used most frequently for hourly or

III Box-Jenkins Methods 1. Pros and Cons of ARIMA Forecasting a) need for data at least 50 and preferably 100 observations should be available to build a proper model used most frequently for hourly or

Time series and Forecasting

Chapter 2 Time series and Forecasting 2.1 Introduction Data are frequently recorded at regular time intervals, for instance, daily stock market indices, the monthly rate of inflation or annual profit figures.

Chapter 2 Time series and Forecasting 2.1 Introduction Data are frequently recorded at regular time intervals, for instance, daily stock market indices, the monthly rate of inflation or annual profit figures.

1. Fundamental concepts

. Fundamental concepts A time series is a sequence of data points, measured typically at successive times spaced at uniform intervals. Time series are used in such fields as statistics, signal processing

. Fundamental concepts A time series is a sequence of data points, measured typically at successive times spaced at uniform intervals. Time series are used in such fields as statistics, signal processing

Module 3. Descriptive Time Series Statistics and Introduction to Time Series Models

Module 3 Descriptive Time Series Statistics and Introduction to Time Series Models Class notes for Statistics 451: Applied Time Series Iowa State University Copyright 2015 W Q Meeker November 11, 2015

Module 3 Descriptive Time Series Statistics and Introduction to Time Series Models Class notes for Statistics 451: Applied Time Series Iowa State University Copyright 2015 W Q Meeker November 11, 2015

Lecture 4a: ARMA Model

Lecture 4a: ARMA Model 1 2 Big Picture Most often our goal is to find a statistical model to describe real time series (estimation), and then predict the future (forecasting) One particularly popular model

Lecture 4a: ARMA Model 1 2 Big Picture Most often our goal is to find a statistical model to describe real time series (estimation), and then predict the future (forecasting) One particularly popular model

A time series is called strictly stationary if the joint distribution of every collection (Y t

5 Time series A time series is a set of observations recorded over time. You can think for example at the GDP of a country over the years (or quarters) or the hourly measurements of temperature over a

5 Time series A time series is a set of observations recorded over time. You can think for example at the GDP of a country over the years (or quarters) or the hourly measurements of temperature over a

Regression Analysis: Exploring relationships between variables. Stat 251

Regression Analysis: Exploring relationships between variables Stat 251 Introduction Objective of regression analysis is to explore the relationship between two (or more) variables so that information

Regression Analysis: Exploring relationships between variables Stat 251 Introduction Objective of regression analysis is to explore the relationship between two (or more) variables so that information

Chapter 8: Model Diagnostics

Chapter 8: Model Diagnostics Model diagnostics involve checking how well the model fits. If the model fits poorly, we consider changing the specification of the model. A major tool of model diagnostics

Chapter 8: Model Diagnostics Model diagnostics involve checking how well the model fits. If the model fits poorly, we consider changing the specification of the model. A major tool of model diagnostics

STOCHASTIC MODELING OF MONTHLY RAINFALL AT KOTA REGION

STOCHASTIC MODELIG OF MOTHLY RAIFALL AT KOTA REGIO S. R. Bhakar, Raj Vir Singh, eeraj Chhajed and Anil Kumar Bansal Department of Soil and Water Engineering, CTAE, Udaipur, Rajasthan, India E-mail: srbhakar@rediffmail.com

STOCHASTIC MODELIG OF MOTHLY RAIFALL AT KOTA REGIO S. R. Bhakar, Raj Vir Singh, eeraj Chhajed and Anil Kumar Bansal Department of Soil and Water Engineering, CTAE, Udaipur, Rajasthan, India E-mail: srbhakar@rediffmail.com

Statistical View of Least Squares

Basic Ideas Some Examples Least Squares May 22, 2007 Basic Ideas Simple Linear Regression Basic Ideas Some Examples Least Squares Suppose we have two variables x and y Basic Ideas Simple Linear Regression

Basic Ideas Some Examples Least Squares May 22, 2007 Basic Ideas Simple Linear Regression Basic Ideas Some Examples Least Squares Suppose we have two variables x and y Basic Ideas Simple Linear Regression

TIME SERIES ANALYSIS AND FORECASTING USING THE STATISTICAL MODEL ARIMA

CHAPTER 6 TIME SERIES ANALYSIS AND FORECASTING USING THE STATISTICAL MODEL ARIMA 6.1. Introduction A time series is a sequence of observations ordered in time. A basic assumption in the time series analysis

CHAPTER 6 TIME SERIES ANALYSIS AND FORECASTING USING THE STATISTICAL MODEL ARIMA 6.1. Introduction A time series is a sequence of observations ordered in time. A basic assumption in the time series analysis

9) Time series econometrics

Time series econometrics") 30C00200 Econometrics 9) Time series econometrics Timo Kuosmanen Professor Management Science http://nomepre.net/index.php/timokuosmanen 1 Macroeconomic data: GDP Inflation rate Examples of time series

30C00200 Econometrics 9) Time series econometrics Timo Kuosmanen Professor Management Science http://nomepre.net/index.php/timokuosmanen 1 Macroeconomic data: GDP Inflation rate Examples of time series

Rob J Hyndman. Forecasting using. 3. Autocorrelation and seasonality OTexts.com/fpp/2/ OTexts.com/fpp/6/1. Forecasting using R 1

Rob J Hyndman Forecasting using 3. Autocorrelation and seasonality OTexts.com/fpp/2/ OTexts.com/fpp/6/1 Forecasting using R 1 Outline 1 Time series graphics 2 Seasonal or cyclic? 3 Autocorrelation Forecasting

Rob J Hyndman Forecasting using 3. Autocorrelation and seasonality OTexts.com/fpp/2/ OTexts.com/fpp/6/1 Forecasting using R 1 Outline 1 Time series graphics 2 Seasonal or cyclic? 3 Autocorrelation Forecasting

Financial Econometrics and Quantitative Risk Managenent Return Properties

Financial Econometrics and Quantitative Risk Managenent Return Properties Eric Zivot Updated: April 1, 2013 Lecture Outline Course introduction Return definitions Empirical properties of returns Reading

Financial Econometrics and Quantitative Risk Managenent Return Properties Eric Zivot Updated: April 1, 2013 Lecture Outline Course introduction Return definitions Empirical properties of returns Reading

White Noise Processes (Section 6.2)

") White Noise Processes (Section 6.) Recall that covariance stationary processes are time series, y t, such. E(y t ) = µ for all t. Var(y t ) = σ for all t, σ < 3. Cov(y t,y t-τ ) = γ(τ) for all t and τ

White Noise Processes (Section 6.) Recall that covariance stationary processes are time series, y t, such. E(y t ) = µ for all t. Var(y t ) = σ for all t, σ < 3. Cov(y t,y t-τ ) = γ(τ) for all t and τ

TESTING FOR CO-INTEGRATION

Bo Sjö 2010-12-05 TESTING FOR CO-INTEGRATION To be used in combination with Sjö (2008) Testing for Unit Roots and Cointegration A Guide. Instructions: Use the Johansen method to test for Purchasing Power

Bo Sjö 2010-12-05 TESTING FOR CO-INTEGRATION To be used in combination with Sjö (2008) Testing for Unit Roots and Cointegration A Guide. Instructions: Use the Johansen method to test for Purchasing Power

Financial Time Series Analysis: Part II

Department of Mathematics and Statistics, University of Vaasa, Finland Spring 2017 1 Unit root Deterministic trend Stochastic trend Testing for unit root ADF-test (Augmented Dickey-Fuller test) Testing

Department of Mathematics and Statistics, University of Vaasa, Finland Spring 2017 1 Unit root Deterministic trend Stochastic trend Testing for unit root ADF-test (Augmented Dickey-Fuller test) Testing

Stat 248 Lab 2: Stationarity, More EDA, Basic TS Models

Stat 248 Lab 2: Stationarity, More EDA, Basic TS Models Tessa L. Childers-Day February 8, 2013 1 Introduction Today s section will deal with topics such as: the mean function, the auto- and cross-covariance

Stat 248 Lab 2: Stationarity, More EDA, Basic TS Models Tessa L. Childers-Day February 8, 2013 1 Introduction Today s section will deal with topics such as: the mean function, the auto- and cross-covariance

Modules 1-2 are background; they are the same for regression analysis and time series.

Regression Analysis, Module 1: Regression models (The attached PDF file has better formatting.) Required reading: Chapter 1, pages 3 13 (until appendix 1.1). Updated: May 23, 2005 Modules 1-2 are background;

Regression Analysis, Module 1: Regression models (The attached PDF file has better formatting.) Required reading: Chapter 1, pages 3 13 (until appendix 1.1). Updated: May 23, 2005 Modules 1-2 are background;

Time Series Analysis. Smoothing Time Series. 2) assessment of/accounting for seasonality. 3) assessment of/exploiting "serial correlation"

assessment of/accounting for seasonality. 3) assessment of/exploiting serial correlation") Time Series Analysis 2) assessment of/accounting for seasonality This (not surprisingly) concerns the analysis of data collected over time... weekly values, monthly values, quarterly values, yearly values,

Time Series Analysis 2) assessment of/accounting for seasonality This (not surprisingly) concerns the analysis of data collected over time... weekly values, monthly values, quarterly values, yearly values,

Univariate ARIMA Models

Univariate ARIMA Models ARIMA Model Building Steps: Identification: Using graphs, statistics, ACFs and PACFs, transformations, etc. to achieve stationary and tentatively identify patterns and model components.

Univariate ARIMA Models ARIMA Model Building Steps: Identification: Using graphs, statistics, ACFs and PACFs, transformations, etc. to achieve stationary and tentatively identify patterns and model components.

Analysis. Components of a Time Series

Module 8: Time Series Analysis 8.2 Components of a Time Series, Detection of Change Points and Trends, Time Series Models Components of a Time Series There can be several things happening simultaneously

Module 8: Time Series Analysis 8.2 Components of a Time Series, Detection of Change Points and Trends, Time Series Models Components of a Time Series There can be several things happening simultaneously

8.2 Harmonic Regression and the Periodogram

Chapter 8 Spectral Methods 8.1 Introduction Spectral methods are based on thining of a time series as a superposition of sinusoidal fluctuations of various frequencies the analogue for a random process

Chapter 8 Spectral Methods 8.1 Introduction Spectral methods are based on thining of a time series as a superposition of sinusoidal fluctuations of various frequencies the analogue for a random process

Simple Linear Regression

Simple Linear Regression In simple linear regression we are concerned about the relationship between two variables, X and Y. There are two components to such a relationship. 1. The strength of the relationship.

Simple Linear Regression In simple linear regression we are concerned about the relationship between two variables, X and Y. There are two components to such a relationship. 1. The strength of the relationship.

Lecture 2: Univariate Time Series

Lecture 2: Univariate Time Series Analysis: Conditional and Unconditional Densities, Stationarity, ARMA Processes Prof. Massimo Guidolin 20192 Financial Econometrics Spring/Winter 2017 Overview Motivation:

Lecture 2: Univariate Time Series Analysis: Conditional and Unconditional Densities, Stationarity, ARMA Processes Prof. Massimo Guidolin 20192 Financial Econometrics Spring/Winter 2017 Overview Motivation:

ESSE Mid-Term Test 2017 Tuesday 17 October :30-09:45

ESSE 4020 3.0 - Mid-Term Test 207 Tuesday 7 October 207. 08:30-09:45 Symbols have their usual meanings. All questions are worth 0 marks, although some are more difficult than others. Answer as many questions

ESSE 4020 3.0 - Mid-Term Test 207 Tuesday 7 October 207. 08:30-09:45 Symbols have their usual meanings. All questions are worth 0 marks, although some are more difficult than others. Answer as many questions

Glossary. The ISI glossary of statistical terms provides definitions in a number of different languages:

Glossary The ISI glossary of statistical terms provides definitions in a number of different languages: http://isi.cbs.nl/glossary/index.htm Adjusted r 2 Adjusted R squared measures the proportion of the

Glossary The ISI glossary of statistical terms provides definitions in a number of different languages: http://isi.cbs.nl/glossary/index.htm Adjusted r 2 Adjusted R squared measures the proportion of the

Exercises - Time series analysis

Descriptive analysis of a time series (1) Estimate the trend of the series of gasoline consumption in Spain using a straight line in the period from 1945 to 1995 and generate forecasts for 24 months. Compare

Descriptive analysis of a time series (1) Estimate the trend of the series of gasoline consumption in Spain using a straight line in the period from 1945 to 1995 and generate forecasts for 24 months. Compare

1. How can you tell if there is serial correlation? 2. AR to model serial correlation. 3. Ignoring serial correlation. 4. GLS. 5. Projects.

1. How can you tell if there is serial correlation? 2. AR to model serial correlation. 3. Ignoring serial correlation. 4. GLS. 5. Projects. 1) Identifying serial correlation. Plot Y t versus Y t 1. See

1. How can you tell if there is serial correlation? 2. AR to model serial correlation. 3. Ignoring serial correlation. 4. GLS. 5. Projects. 1) Identifying serial correlation. Plot Y t versus Y t 1. See

Characteristics of Time Series

Characteristics of Time Series Al Nosedal University of Toronto January 12, 2016 Al Nosedal University of Toronto Characteristics of Time Series January 12, 2016 1 / 37 Signal and Noise In general, most

Characteristics of Time Series Al Nosedal University of Toronto January 12, 2016 Al Nosedal University of Toronto Characteristics of Time Series January 12, 2016 1 / 37 Signal and Noise In general, most

Midterm 2 - Solutions

Ecn 102 - Analysis of Economic Data University of California - Davis February 24, 2010 Instructor: John Parman Midterm 2 - Solutions You have until 10:20am to complete this exam. Please remember to put

Ecn 102 - Analysis of Economic Data University of California - Davis February 24, 2010 Instructor: John Parman Midterm 2 - Solutions You have until 10:20am to complete this exam. Please remember to put

FinQuiz Notes

Reading 9 A time series is any series of data that varies over time e.g. the quarterly sales for a company during the past five years or daily returns of a security. When assumptions of the regression

Reading 9 A time series is any series of data that varies over time e.g. the quarterly sales for a company during the past five years or daily returns of a security. When assumptions of the regression

7 Introduction to Time Series

Econ 495 - Econometric Review 1 7 Introduction to Time Series 7.1 Time Series vs. Cross-Sectional Data Time series data has a temporal ordering, unlike cross-section data, we will need to changes some

Econ 495 - Econometric Review 1 7 Introduction to Time Series 7.1 Time Series vs. Cross-Sectional Data Time series data has a temporal ordering, unlike cross-section data, we will need to changes some

1 Quantitative Techniques in Practice

1 Quantitative Techniques in Practice 1.1 Lecture 2: Stationarity, spurious regression, etc. 1.1.1 Overview In the rst part we shall look at some issues in time series economics. In the second part we

1 Quantitative Techniques in Practice 1.1 Lecture 2: Stationarity, spurious regression, etc. 1.1.1 Overview In the rst part we shall look at some issues in time series economics. In the second part we

7 Introduction to Time Series Time Series vs. Cross-Sectional Data Detrending Time Series... 15

Econ 495 - Econometric Review 1 Contents 7 Introduction to Time Series 3 7.1 Time Series vs. Cross-Sectional Data............ 3 7.2 Detrending Time Series................... 15 7.3 Types of Stochastic

Econ 495 - Econometric Review 1 Contents 7 Introduction to Time Series 3 7.1 Time Series vs. Cross-Sectional Data............ 3 7.2 Detrending Time Series................... 15 7.3 Types of Stochastic

A Second Course in Statistics: Regression Analysis

FIFTH E D I T I 0 N A Second Course in Statistics: Regression Analysis WILLIAM MENDENHALL University of Florida TERRY SINCICH University of South Florida PRENTICE HALL Upper Saddle River, New Jersey 07458

FIFTH E D I T I 0 N A Second Course in Statistics: Regression Analysis WILLIAM MENDENHALL University of Florida TERRY SINCICH University of South Florida PRENTICE HALL Upper Saddle River, New Jersey 07458

The regression model with one fixed regressor cont d

The regression model with one fixed regressor cont d 3150/4150 Lecture 4 Ragnar Nymoen 27 January 2012 The model with transformed variables Regression with transformed variables I References HGL Ch 2.8

The regression model with one fixed regressor cont d 3150/4150 Lecture 4 Ragnar Nymoen 27 January 2012 The model with transformed variables Regression with transformed variables I References HGL Ch 2.8

Circle a single answer for each multiple choice question. Your choice should be made clearly.

TEST #1 STA 4853 March 4, 215 Name: Please read the following directions. DO NOT TURN THE PAGE UNTIL INSTRUCTED TO DO SO Directions This exam is closed book and closed notes. There are 31 questions. Circle

TEST #1 STA 4853 March 4, 215 Name: Please read the following directions. DO NOT TURN THE PAGE UNTIL INSTRUCTED TO DO SO Directions This exam is closed book and closed notes. There are 31 questions. Circle

K. Model Diagnostics. residuals ˆɛ ij = Y ij ˆµ i N = Y ij Ȳ i semi-studentized residuals ω ij = ˆɛ ij. studentized deleted residuals ɛ ij =

K. Model Diagnostics We ve already seen how to check model assumptions prior to fitting a one-way ANOVA. Diagnostics carried out after model fitting by using residuals are more informative for assessing

K. Model Diagnostics We ve already seen how to check model assumptions prior to fitting a one-way ANOVA. Diagnostics carried out after model fitting by using residuals are more informative for assessing

Lecture 8a: Spurious Regression

Lecture 8a: Spurious Regression 1 Old Stuff The traditional statistical theory holds when we run regression using (weakly or covariance) stationary variables. For example, when we regress one stationary

Lecture 8a: Spurious Regression 1 Old Stuff The traditional statistical theory holds when we run regression using (weakly or covariance) stationary variables. For example, when we regress one stationary

Stochastic Processes: I. consider bowl of worms model for oscilloscope experiment:

Stochastic Processes: I consider bowl of worms model for oscilloscope experiment: SAPAscope 2.0 / 0 1 RESET SAPA2e 22, 23 II 1 stochastic process is: Stochastic Processes: II informally: bowl + drawing

Stochastic Processes: I consider bowl of worms model for oscilloscope experiment: SAPAscope 2.0 / 0 1 RESET SAPA2e 22, 23 II 1 stochastic process is: Stochastic Processes: II informally: bowl + drawing

If we want to analyze experimental or simulated data we might encounter the following tasks:

Chapter 1 Introduction If we want to analyze experimental or simulated data we might encounter the following tasks: Characterization of the source of the signal and diagnosis Studying dependencies Prediction

Chapter 1 Introduction If we want to analyze experimental or simulated data we might encounter the following tasks: Characterization of the source of the signal and diagnosis Studying dependencies Prediction

Decision 411: Class 3

Decision 411: Class 3 Discussion of HW#1 Introduction to seasonal models Seasonal decomposition Seasonal adjustment on a spreadsheet Forecasting with seasonal adjustment Forecasting inflation Poor man

Decision 411: Class 3 Discussion of HW#1 Introduction to seasonal models Seasonal decomposition Seasonal adjustment on a spreadsheet Forecasting with seasonal adjustment Forecasting inflation Poor man

5 Transfer function modelling

MSc Further Time Series Analysis 5 Transfer function modelling 5.1 The model Consider the construction of a model for a time series (Y t ) whose values are influenced by the earlier values of a series

MSc Further Time Series Analysis 5 Transfer function modelling 5.1 The model Consider the construction of a model for a time series (Y t ) whose values are influenced by the earlier values of a series

11.1 Gujarati(2003): Chapter 12

: Chapter 12") 11.1 Gujarati(2003): Chapter 12 Time Series Data 11.2 Time series process of economic variables e.g., GDP, M1, interest rate, echange rate, imports, eports, inflation rate, etc. Realization An observed

11.1 Gujarati(2003): Chapter 12 Time Series Data 11.2 Time series process of economic variables e.g., GDP, M1, interest rate, echange rate, imports, eports, inflation rate, etc. Realization An observed

Chapter 1. Introduction. The following abbreviations are used in these notes: TS Time Series. ma moving average filter rv random variable

Chapter 1 Introduction The following abbreviations are used in these notes: TS Time Series ma moving average filter rv random variable iid independently identically distributed cdf cumulative distribution

Chapter 1 Introduction The following abbreviations are used in these notes: TS Time Series ma moving average filter rv random variable iid independently identically distributed cdf cumulative distribution

Decision 411: Class 3

Decision 411: Class 3 Discussion of HW#1 Introduction to seasonal models Seasonal decomposition Seasonal adjustment on a spreadsheet Forecasting with seasonal adjustment Forecasting inflation Poor man

Decision 411: Class 3 Discussion of HW#1 Introduction to seasonal models Seasonal decomposition Seasonal adjustment on a spreadsheet Forecasting with seasonal adjustment Forecasting inflation Poor man

Forecasting using R. Rob J Hyndman. 3.2 Dynamic regression. Forecasting using R 1

Forecasting using R Rob J Hyndman 3.2 Dynamic regression Forecasting using R 1 Outline 1 Regression with ARIMA errors 2 Stochastic and deterministic trends 3 Periodic seasonality 4 Lab session 14 5 Dynamic

Forecasting using R Rob J Hyndman 3.2 Dynamic regression Forecasting using R 1 Outline 1 Regression with ARIMA errors 2 Stochastic and deterministic trends 3 Periodic seasonality 4 Lab session 14 5 Dynamic

MCMC analysis of classical time series algorithms.

MCMC analysis of classical time series algorithms. mbalawata@yahoo.com Lappeenranta University of Technology Lappeenranta, 19.03.2009 Outline Introduction 1 Introduction 2 3 Series generation Box-Jenkins

MCMC analysis of classical time series algorithms. mbalawata@yahoo.com Lappeenranta University of Technology Lappeenranta, 19.03.2009 Outline Introduction 1 Introduction 2 3 Series generation Box-Jenkins

Simple Linear Regression

Simple Linear Regression ST 430/514 Recall: A regression model describes how a dependent variable (or response) Y is affected, on average, by one or more independent variables (or factors, or covariates)

Simple Linear Regression ST 430/514 Recall: A regression model describes how a dependent variable (or response) Y is affected, on average, by one or more independent variables (or factors, or covariates)

Decision 411: Class 3

Decision 411: Class 3 Discussion of HW#1 Introduction to seasonal models Seasonal decomposition Seasonal adjustment on a spreadsheet Forecasting with seasonal adjustment Forecasting inflation Log transformation

Decision 411: Class 3 Discussion of HW#1 Introduction to seasonal models Seasonal decomposition Seasonal adjustment on a spreadsheet Forecasting with seasonal adjustment Forecasting inflation Log transformation

Covariance Stationary Time Series. Example: Independent White Noise (IWN(0,σ 2 )) Y t = ε t, ε t iid N(0,σ 2 )

) Y t = ε t, ε t iid N(0,σ 2 )") Covariance Stationary Time Series Stochastic Process: sequence of rv s ordered by time {Y t } {...,Y 1,Y 0,Y 1,...} Defn: {Y t } is covariance stationary if E[Y t ]μ for all t cov(y t,y t j )E[(Y t μ)(y

Covariance Stationary Time Series Stochastic Process: sequence of rv s ordered by time {Y t } {...,Y 1,Y 0,Y 1,...} Defn: {Y t } is covariance stationary if E[Y t ]μ for all t cov(y t,y t j )E[(Y t μ)(y

Volatility. Gerald P. Dwyer. February Clemson University

Volatility Gerald P. Dwyer Clemson University February 2016 Outline 1 Volatility Characteristics of Time Series Heteroskedasticity Simpler Estimation Strategies Exponentially Weighted Moving Average Use

Volatility Gerald P. Dwyer Clemson University February 2016 Outline 1 Volatility Characteristics of Time Series Heteroskedasticity Simpler Estimation Strategies Exponentially Weighted Moving Average Use

Chapter 2: simple regression model

Chapter 2: simple regression model Goal: understand how to estimate and more importantly interpret the simple regression Reading: chapter 2 of the textbook Advice: this chapter is foundation of econometrics.

Chapter 2: simple regression model Goal: understand how to estimate and more importantly interpret the simple regression Reading: chapter 2 of the textbook Advice: this chapter is foundation of econometrics.

Prof. Dr. Roland Füss Lecture Series in Applied Econometrics Summer Term Introduction to Time Series Analysis

Introduction to Time Series Analysis 1 Contents: I. Basics of Time Series Analysis... 4 I.1 Stationarity... 5 I.2 Autocorrelation Function... 9 I.3 Partial Autocorrelation Function (PACF)... 14 I.4 Transformation

Introduction to Time Series Analysis 1 Contents: I. Basics of Time Series Analysis... 4 I.1 Stationarity... 5 I.2 Autocorrelation Function... 9 I.3 Partial Autocorrelation Function (PACF)... 14 I.4 Transformation

IS THE NORTH ATLANTIC OSCILLATION A RANDOM WALK? A COMMENT WITH FURTHER RESULTS

INTERNATIONAL JOURNAL OF CLIMATOLOGY Int. J. Climatol. 24: 377 383 (24) Published online 11 February 24 in Wiley InterScience (www.interscience.wiley.com). DOI: 1.12/joc.13 IS THE NORTH ATLANTIC OSCILLATION

INTERNATIONAL JOURNAL OF CLIMATOLOGY Int. J. Climatol. 24: 377 383 (24) Published online 11 February 24 in Wiley InterScience (www.interscience.wiley.com). DOI: 1.12/joc.13 IS THE NORTH ATLANTIC OSCILLATION

CHAPTER 21: TIME SERIES ECONOMETRICS: SOME BASIC CONCEPTS

CHAPTER 21: TIME SERIES ECONOMETRICS: SOME BASIC CONCEPTS 21.1 A stochastic process is said to be weakly stationary if its mean and variance are constant over time and if the value of the covariance between

CHAPTER 21: TIME SERIES ECONOMETRICS: SOME BASIC CONCEPTS 21.1 A stochastic process is said to be weakly stationary if its mean and variance are constant over time and if the value of the covariance between

Forecasting Seasonal Time Series 1. Introduction. Philip Hans Franses Econometric Institute Erasmus University Rotterdam

Forecasting Seasonal Time Series 1. Introduction Philip Hans Franses Econometric Institute Erasmus University Rotterdam SMU and NUS, Singapore, April-May 2004 1 Outline of tutorial lectures 1 Introduction

Forecasting Seasonal Time Series 1. Introduction Philip Hans Franses Econometric Institute Erasmus University Rotterdam SMU and NUS, Singapore, April-May 2004 1 Outline of tutorial lectures 1 Introduction

Forecasting using R. Rob J Hyndman. 2.4 Non-seasonal ARIMA models. Forecasting using R 1

Forecasting using R Rob J Hyndman 2.4 Non-seasonal ARIMA models Forecasting using R 1 Outline 1 Autoregressive models 2 Moving average models 3 Non-seasonal ARIMA models 4 Partial autocorrelations 5 Estimation

Forecasting using R Rob J Hyndman 2.4 Non-seasonal ARIMA models Forecasting using R 1 Outline 1 Autoregressive models 2 Moving average models 3 Non-seasonal ARIMA models 4 Partial autocorrelations 5 Estimation

STAT 443 Final Exam Review. 1 Basic Definitions. 2 Statistical Tests. L A TEXer: W. Kong

STAT 443 Final Exam Review L A TEXer: W Kong 1 Basic Definitions Definition 11 The time series {X t } with E[X 2 t ] < is said to be weakly stationary if: 1 µ X (t) = E[X t ] is independent of t 2 γ X

STAT 443 Final Exam Review L A TEXer: W Kong 1 Basic Definitions Definition 11 The time series {X t } with E[X 2 t ] < is said to be weakly stationary if: 1 µ X (t) = E[X t ] is independent of t 2 γ X

Chapter 1. Introduction. The following abbreviations are used in these notes: TS Time Series. ma moving average filter. rv random variable

Chapter 1 Introduction The following abbreviations are used in these notes: TS Time Series ma moving average filter rv random variable iid independently identically distributed cdf cumulative distribution

Chapter 1 Introduction The following abbreviations are used in these notes: TS Time Series ma moving average filter rv random variable iid independently identically distributed cdf cumulative distribution

ECON/FIN 250: Forecasting in Finance and Economics: Section 6: Standard Univariate Models

ECON/FIN 250: Forecasting in Finance and Economics: Section 6: Standard Univariate Models Patrick Herb Brandeis University Spring 2016 Patrick Herb (Brandeis University) Standard Univariate Models ECON/FIN

ECON/FIN 250: Forecasting in Finance and Economics: Section 6: Standard Univariate Models Patrick Herb Brandeis University Spring 2016 Patrick Herb (Brandeis University) Standard Univariate Models ECON/FIN

Decision 411: Class 7

Decision 411: Class 7 Confidence limits for sums of coefficients Use of the time index as a regressor The difficulty of predicting the future Confidence intervals for sums of coefficients Sometimes the

Decision 411: Class 7 Confidence limits for sums of coefficients Use of the time index as a regressor The difficulty of predicting the future Confidence intervals for sums of coefficients Sometimes the

10) Time series econometrics

Time series econometrics") 30C00200 Econometrics 10) Time series econometrics Timo Kuosmanen Professor, Ph.D. 1 Topics today Static vs. dynamic time series model Suprious regression Stationary and nonstationary time series Unit

30C00200 Econometrics 10) Time series econometrics Timo Kuosmanen Professor, Ph.D. 1 Topics today Static vs. dynamic time series model Suprious regression Stationary and nonstationary time series Unit