FISCAL MULTIPLIERS IN JAPAN

|

|

|

- Flora Fisher

- 5 years ago

- Views:

Transcription

1 FISCAL MULTIPLIERS IN JAPAN Alan Auerbach and Yuriy Gorodnichenko UC Berkeley July 25, 2013

2 How Large are Fiscal Multipliers? Previous papers (AG 2012, 2013): Multipliers of government purchases are larger in recession than in expansion; result holds for different indicators for distinguishing recession from expansion. Definition of shocks matters; purging VAR innovations of components predictable using realtime forecasts tends to increase multiplier estimates, particularly for periods of recession.

3 How Large are Fiscal Multipliers? This paper: Adapt methodology from AG 2013 (for a panel of OECD countries) to study Japan. Initial results, for longest sample period ( ) consistent with earlier findings. But evidence of multiplier instability over time, and issues to confront involving data and defining the business cycle.

4 Methodology Follow AG 2013, using direct projection approach to study effects of (log) government purchases (G) on (log) output (Y): +h = h + ( 1 ),h ( ) ( 1 ),h ( ) 1 + ( 1 ),h + 1 ( 1 ),h +,h (1) where: ( ) = exp ( ) 1+exp ( ), > 0 (2)

5 Methodology Follow AG 2013, using direct projection approach to study effects of (log) government purchases (G) on (log) output (Y): +h = h + ( 1 ),h ( ) ( 1 ),h ( ) 1 + ( 1 ),h + 1 ( 1 ),h +,h (1) where: ( ) = exp ( ) 1+exp ( ), > 0 (2) X t-1 is a vector of control variables, including 4 lags of Y and G

6 Methodology Follow AG 2013, using direct projection approach to study effects of (log) government purchases (G) on (log) output (Y): +h = h + ( 1 ),h ( ) ( 1 ),h ( ) 1 + ( 1 ),h + 1 ( 1 ),h +,h (1) where: ( ) = exp ( ) 1+exp ( ), > 0 (2) G FE t is contemporaneous shock to G, conditional on X t-1 and real-time forecasts

7 Methodology Follow AG 2013, using direct projection approach to study effects of (log) government purchases (G) on (log) output (Y): +h = h + ( 1 ),h ( ) ( 1 ),h ( ) 1 + ( 1 ),h + 1 ( 1 ),h +,h (1) where: ( ) = exp ( ) 1+exp ( ), > 0 (2) h is the number of periods ahead the forecast is being made

8 Methodology Follow AG 2013, using direct projection approach to study effects of (log) government purchases (G) on (log) output (Y): +h = h + ( 1 ),h ( ) ( 1 ),h ( ) 1 + ( 1 ),h + 1 ( 1 ),h +,h (1) where: ( ) = exp ( ) 1+exp ( ), > 0 (2) z is a standardized indicator of the state of the business cycle; higher values correspond to stronger economies

9 Methodology Follow AG 2013, using direct projection approach to study effects of (log) government purchases (G) on (log) output (Y): +h = h + ( 1 ),h ( ) ( 1 ),h ( ) 1 + ( 1 ),h + 1 ( 1 ),h +,h (1) where: ( ) = exp ( ) 1+exp ( ), > 0 (2) ( ) ranges between 0 (for strong expansions) and 1 (for deep recessions); set at 1.5 as before.

10 Methodology Follow AG 2013, using direct projection approach to study effects of (log) government purchases (G) on (log) output (Y): +h = h + ( 1 ),h ( ) ( 1 ),h ( ) 1 + ( 1 ),h + 1 ( 1 ),h +,h (1) where: ( ) = exp ( ) 1+exp ( ), > 0 (2) Coefficients depend on the state of the business cycle, with F(z t-1 ) determining weights

11 Methodology Follow AG 2013, using direct projection approach to study effects of (log) government purchases (G) on (log) output (Y): +h = h + ( 1 ),h ( ) ( 1 ),h ( ) 1 + ( 1 ),h + 1 ( 1 ),h +,h (1) where: ( ) = exp ( ) 1+exp ( ), > 0 (2) Impulse response functions come directly from estimates of Φ i,h for different values of h.

12 Data Issues To get long time series for quarterly data on Y and G, need to splice overlapping series from different versions of SNA. Only shorter series for taxes; omit since results for shorter sample similar with and without taxes. Real-time forecasts available only from OECD and IMF, either semiannually from 1985 or quarterly from Present results in paper, but large standard errors.

13 Business Cycle Indicators In previous work, used lagged average (over 7 quarters or 6 semiannual periods) growth rate of real GDP, relative to HP-filtered trend. AG 2013 also considered other measures; little impact on results because alternative indicator series had similar time series patterns For Japan, however, the choice may be more important, so present results for alternative definitions

14 Figure 1. State of Business Cycle

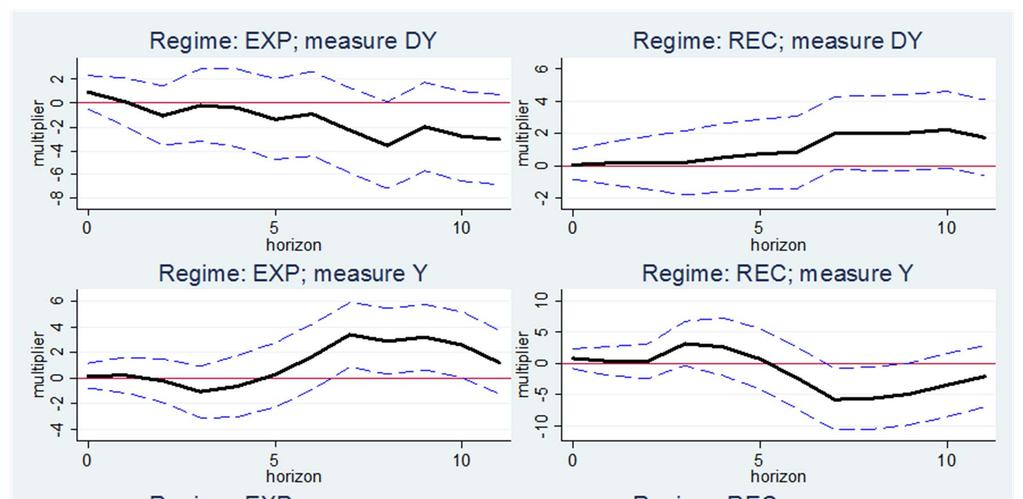

15 Basic Results For full sample period ( ) without controlling for real-time forecasts, results differ by z but in line with our earlier findings Multipliers stronger in recessions

16 Figure 3. Multipliers,

17 Basic Results For full sample period ( ) without controlling for real-time forecasts, results differ by z but in line with our earlier findings Multipliers stronger in recessions In fact, larger than in our previous work (avg(y)/avg(g)) ranges from (measured by scaling coefficients by sample average ratio of output to government purchases, 4.1)

18 Basic Results For full sample period ( ) without controlling for real-time forecasts, results differ by z but in line with our earlier findings Multipliers stronger in recessions In fact, larger than in our previous work (avg(y)/avg(g)) ranges from (measured by scaling coefficients by sample average ratio of output to government purchases, 4.1) But results for later sample weaker, for linear model but also individual regimes

19 Figure 2A. Linear Results, multiplier horizon

20 Figure 2B. Linear Results, multiplier horizon

21 Figure 4. Multipliers,

22 Rolling Sample Results More generally, evidence of time variation in multipliers. Consider 10-year rolling sample periods; focus on linear model due to fewer observations.

23 Figure 5. Multiplier Time Variation

24 Conclusions Some evidence consistent with earlier work, but results don t appear stable over time Multiplier variation may be due to other factors not considered (e.g., ZLB, zombie lending, etc.), but hard to tell with available data Ability to get a clear sense hindered by Data limits (national accounts, real-time forecasts) Difficulty of distinguishing trend and cycle

Lecture on State Dependent Government Spending Multipliers

Lecture on State Dependent Government Spending Multipliers Valerie A. Ramey University of California, San Diego and NBER February 25, 2014 Does the Multiplier Depend on the State of Economy? Evidence suggests

Lecture on State Dependent Government Spending Multipliers Valerie A. Ramey University of California, San Diego and NBER February 25, 2014 Does the Multiplier Depend on the State of Economy? Evidence suggests

Is it the How or the When that Matters in Fiscal Adjustments?

Is it the How or the When that Matters in Fiscal Adjustments? Alberto Alesina, Gualtiero Azzalini, Carlo Favero, Francesco Giavazzi, Armando Miano IGIER, Bocconi University November 2016 1 / 41 Question

Is it the How or the When that Matters in Fiscal Adjustments? Alberto Alesina, Gualtiero Azzalini, Carlo Favero, Francesco Giavazzi, Armando Miano IGIER, Bocconi University November 2016 1 / 41 Question

Tackling unemployment in recessions: The effects of short-time work policy

Tackling unemployment in recessions: The effects of short-time work policy Britta Gehrke 1,2 Brigitte Hochmuth 1 1 Friedrich-Alexander University Erlangen-Nuremberg (FAU) 2 Institute for Employment Research

Tackling unemployment in recessions: The effects of short-time work policy Britta Gehrke 1,2 Brigitte Hochmuth 1 1 Friedrich-Alexander University Erlangen-Nuremberg (FAU) 2 Institute for Employment Research

Predicting economic turning points by professional forecasters -Are they useful?

Predicting economic turning points by professional forecasters -Are they useful? 21 Feb 2013 Nobuo Iizuka KANAGAWA University nobuo iizuka 0915@kanagawa u.ac.jp Motivation Evaluating Economic forecasting

Predicting economic turning points by professional forecasters -Are they useful? 21 Feb 2013 Nobuo Iizuka KANAGAWA University nobuo iizuka 0915@kanagawa u.ac.jp Motivation Evaluating Economic forecasting

Understanding the Size of the Government Spending Multiplier: It s in the Sign

Understanding the Size of the Government Spending Multiplier: It s in the Sign Regis Barnichon Federal Reserve Bank of San Francisco, CREI, Universitat Pompeu Fabra, CEPR Christian Matthes Federal Reserve

Understanding the Size of the Government Spending Multiplier: It s in the Sign Regis Barnichon Federal Reserve Bank of San Francisco, CREI, Universitat Pompeu Fabra, CEPR Christian Matthes Federal Reserve

News Shocks: Different Effects in Boom and Recession?

News Shocks: Different Effects in Boom and Recession? Maria Bolboaca, Sarah Fischer University of Bern Study Center Gerzensee June 7, 5 / Introduction News are defined in the literature as exogenous changes

News Shocks: Different Effects in Boom and Recession? Maria Bolboaca, Sarah Fischer University of Bern Study Center Gerzensee June 7, 5 / Introduction News are defined in the literature as exogenous changes

CENTRE FOR APPLIED MACROECONOMIC ANALYSIS

CENTRE FOR APPLIED MACROECONOMIC ANALYSIS The Australian National University CAMA Working Paper Series May, 2005 SINGLE SOURCE OF ERROR STATE SPACE APPROACH TO THE BEVERIDGE NELSON DECOMPOSITION Heather

CENTRE FOR APPLIED MACROECONOMIC ANALYSIS The Australian National University CAMA Working Paper Series May, 2005 SINGLE SOURCE OF ERROR STATE SPACE APPROACH TO THE BEVERIDGE NELSON DECOMPOSITION Heather

The Econometrics of Fiscal Policy

The Econometrics of Fiscal Policy Carlo Favero, F.Giavazzi, M.Karamisheva Carlo Favero, F.Giavazzi, M.Karamisheva () The Econometrics of Fiscal Policy 1 / 33 Papers This presentation is based on the following

The Econometrics of Fiscal Policy Carlo Favero, F.Giavazzi, M.Karamisheva Carlo Favero, F.Giavazzi, M.Karamisheva () The Econometrics of Fiscal Policy 1 / 33 Papers This presentation is based on the following

Explaining the Effects of Government Spending Shocks on Consumption and the Real Exchange Rate. M. Ravn S. Schmitt-Grohé M. Uribe.

Explaining the Effects of Government Spending Shocks on Consumption and the Real Exchange Rate M. Ravn S. Schmitt-Grohé M. Uribe November 2, 27 Effects of Government Spending Shocks: SVAR Evidence A rise

Explaining the Effects of Government Spending Shocks on Consumption and the Real Exchange Rate M. Ravn S. Schmitt-Grohé M. Uribe November 2, 27 Effects of Government Spending Shocks: SVAR Evidence A rise

MFx Macroeconomic Forecasting

MFx Macroeconomic Forecasting Structural Vector Autoregressive Models Part II IMFx This training material is the property of the International Monetary Fund (IMF) and is intended for use in IMF Institute

MFx Macroeconomic Forecasting Structural Vector Autoregressive Models Part II IMFx This training material is the property of the International Monetary Fund (IMF) and is intended for use in IMF Institute

Latent variables and shocks contribution in DSGE models with occasionally binding constraints

Latent variables and shocks contribution in DSGE models with occasionally binding constraints May 29, 2016 1 Marco Ratto, Massimo Giovannini (European Commission, Joint Research Centre) We implement an

Latent variables and shocks contribution in DSGE models with occasionally binding constraints May 29, 2016 1 Marco Ratto, Massimo Giovannini (European Commission, Joint Research Centre) We implement an

Identifying the Monetary Policy Shock Christiano et al. (1999)

") Identifying the Monetary Policy Shock Christiano et al. (1999) The question we are asking is: What are the consequences of a monetary policy shock a shock which is purely related to monetary conditions

Identifying the Monetary Policy Shock Christiano et al. (1999) The question we are asking is: What are the consequences of a monetary policy shock a shock which is purely related to monetary conditions

Threshold effects in Okun s Law: a panel data analysis. Abstract

Threshold effects in Okun s Law: a panel data analysis Julien Fouquau ESC Rouen and LEO Abstract Our approach involves the use of switching regime models, to take account of the structural asymmetry and

Threshold effects in Okun s Law: a panel data analysis Julien Fouquau ESC Rouen and LEO Abstract Our approach involves the use of switching regime models, to take account of the structural asymmetry and

Modelling Czech and Slovak labour markets: A DSGE model with labour frictions

Modelling Czech and Slovak labour markets: A DSGE model with labour frictions Daniel Němec Faculty of Economics and Administrations Masaryk University Brno, Czech Republic nemecd@econ.muni.cz ESF MU (Brno)

Modelling Czech and Slovak labour markets: A DSGE model with labour frictions Daniel Němec Faculty of Economics and Administrations Masaryk University Brno, Czech Republic nemecd@econ.muni.cz ESF MU (Brno)

Animal Spirits, Fundamental Factors and Business Cycle Fluctuations

Animal Spirits, Fundamental Factors and Business Cycle Fluctuations Stephane Dées Srečko Zimic Banque de France European Central Bank January 6, 218 Disclaimer Any views expressed represent those of the

Animal Spirits, Fundamental Factors and Business Cycle Fluctuations Stephane Dées Srečko Zimic Banque de France European Central Bank January 6, 218 Disclaimer Any views expressed represent those of the

1.2. Structural VARs

1. Shocks Nr. 1 1.2. Structural VARs How to identify A 0? A review: Choleski (Cholesky?) decompositions. Short-run restrictions. Inequality restrictions. Long-run restrictions. Then, examples, applications,

1. Shocks Nr. 1 1.2. Structural VARs How to identify A 0? A review: Choleski (Cholesky?) decompositions. Short-run restrictions. Inequality restrictions. Long-run restrictions. Then, examples, applications,

Douglas Laxton Economic Modeling Division January 30, 2014

Douglas Laxton Economic Modeling Division January 30, 2014 The GPM Team Produces quarterly projections before each WEO WEO numbers are produced by the country experts in the area departments Models used

Douglas Laxton Economic Modeling Division January 30, 2014 The GPM Team Produces quarterly projections before each WEO WEO numbers are produced by the country experts in the area departments Models used

ESRI Research Note Nowcasting and the Need for Timely Estimates of Movements in Irish Output

ESRI Research Note Nowcasting and the Need for Timely Estimates of Movements in Irish Output David Byrne, Kieran McQuinn and Ciara Morley Research Notes are short papers on focused research issues. Nowcasting

ESRI Research Note Nowcasting and the Need for Timely Estimates of Movements in Irish Output David Byrne, Kieran McQuinn and Ciara Morley Research Notes are short papers on focused research issues. Nowcasting

A Comparison of Business Cycle Regime Nowcasting Performance between Real-time and Revised Data. By Arabinda Basistha (West Virginia University)

") A Comparison of Business Cycle Regime Nowcasting Performance between Real-time and Revised Data By Arabinda Basistha (West Virginia University) This version: 2.7.8 Markov-switching models used for nowcasting

A Comparison of Business Cycle Regime Nowcasting Performance between Real-time and Revised Data By Arabinda Basistha (West Virginia University) This version: 2.7.8 Markov-switching models used for nowcasting

IDENTIFYING BUSINESS CYCLE TURNING POINTS IN CROATIA

IDENTIFYING IN CROATIA Ivo Krznar HNB 6 May 2011 IVO KRZNAR (HNB) 6 MAY 2011 1 / 20 WHAT: MAIN GOALS Identify turning points of croatian economic activity for the period 1998-(end) 2010 Provide clear and

IDENTIFYING IN CROATIA Ivo Krznar HNB 6 May 2011 IVO KRZNAR (HNB) 6 MAY 2011 1 / 20 WHAT: MAIN GOALS Identify turning points of croatian economic activity for the period 1998-(end) 2010 Provide clear and

Euro-indicators Working Group

Euro-indicators Working Group Luxembourg, 9 th & 10 th June 2011 Item 9.3 of the Agenda Towards an early warning system for the Euro area By Gian Luigi Mazzi Doc 308/11 Introduction Clear picture of economic

Euro-indicators Working Group Luxembourg, 9 th & 10 th June 2011 Item 9.3 of the Agenda Towards an early warning system for the Euro area By Gian Luigi Mazzi Doc 308/11 Introduction Clear picture of economic

Identifying Aggregate Liquidity Shocks with Monetary Policy Shocks: An Application using UK Data

Identifying Aggregate Liquidity Shocks with Monetary Policy Shocks: An Application using UK Data Michael Ellington and Costas Milas Financial Services, Liquidity and Economic Activity Bank of England May

Identifying Aggregate Liquidity Shocks with Monetary Policy Shocks: An Application using UK Data Michael Ellington and Costas Milas Financial Services, Liquidity and Economic Activity Bank of England May

Volume 35, Issue 4. Joao Tovar Jalles Center for Globalization and Governance, Portugal

Volume 35, Issue 4 How Quickly is News Incorporated in Fiscal Forecasts? Joao Tovar Jalles Center for Globalization and Governance, Portugal Abstract This paper tests for the existence of information rigidities

Volume 35, Issue 4 How Quickly is News Incorporated in Fiscal Forecasts? Joao Tovar Jalles Center for Globalization and Governance, Portugal Abstract This paper tests for the existence of information rigidities

GDP forecast errors Satish Ranchhod

GDP forecast errors Satish Ranchhod Editor s note This paper looks more closely at our forecasts of growth in Gross Domestic Product (GDP). It considers two different measures of GDP, production and expenditure,

GDP forecast errors Satish Ranchhod Editor s note This paper looks more closely at our forecasts of growth in Gross Domestic Product (GDP). It considers two different measures of GDP, production and expenditure,

U n iversity o f H ei delberg

U n iversity o f H ei delberg Department of Economics Discussion Paper Series No. 585 482482 Global Prediction of Recessions Jonas Dovern and Florian Huber March 2015 Global Prediction of Recessions Jonas

U n iversity o f H ei delberg Department of Economics Discussion Paper Series No. 585 482482 Global Prediction of Recessions Jonas Dovern and Florian Huber March 2015 Global Prediction of Recessions Jonas

CAN SOLAR ACTIVITY INFLUENCE THE OCCURRENCE OF RECESSIONS? Mikhail Gorbanev January 2015

CAN SOLAR ACTIVITY INFLUENCE THE OCCURRENCE OF RECESSIONS? Mikhail Gorbanev January 2015 Outline What are the sunspots, solar cycles, and solar maximums? Literature: Jevons and Chizhevsky Methodology:

CAN SOLAR ACTIVITY INFLUENCE THE OCCURRENCE OF RECESSIONS? Mikhail Gorbanev January 2015 Outline What are the sunspots, solar cycles, and solar maximums? Literature: Jevons and Chizhevsky Methodology:

e Yield Spread Puzzle and the Information Content of SPF forecasts

Economics Letters, Volume 118, Issue 1, January 2013, Pages 219 221 e Yield Spread Puzzle and the Information Content of SPF forecasts Kajal Lahiri, George Monokroussos, Yongchen Zhao Department of Economics,

Economics Letters, Volume 118, Issue 1, January 2013, Pages 219 221 e Yield Spread Puzzle and the Information Content of SPF forecasts Kajal Lahiri, George Monokroussos, Yongchen Zhao Department of Economics,

1 The Basic RBC Model

IHS 2016, Macroeconomics III Michael Reiter Ch. 1: Notes on RBC Model 1 1 The Basic RBC Model 1.1 Description of Model Variables y z k L c I w r output level of technology (exogenous) capital at end of

IHS 2016, Macroeconomics III Michael Reiter Ch. 1: Notes on RBC Model 1 1 The Basic RBC Model 1.1 Description of Model Variables y z k L c I w r output level of technology (exogenous) capital at end of

1 Teaching notes on structural VARs.

Bent E. Sørensen November 8, 2016 1 Teaching notes on structural VARs. 1.1 Vector MA models: 1.1.1 Probability theory The simplest to analyze, estimation is a different matter time series models are the

Bent E. Sørensen November 8, 2016 1 Teaching notes on structural VARs. 1.1 Vector MA models: 1.1.1 Probability theory The simplest to analyze, estimation is a different matter time series models are the

WORKING PAPER NO DO GDP FORECASTS RESPOND EFFICIENTLY TO CHANGES IN INTEREST RATES?

WORKING PAPER NO. 16-17 DO GDP FORECASTS RESPOND EFFICIENTLY TO CHANGES IN INTEREST RATES? Dean Croushore Professor of Economics and Rigsby Fellow, University of Richmond and Visiting Scholar, Federal

WORKING PAPER NO. 16-17 DO GDP FORECASTS RESPOND EFFICIENTLY TO CHANGES IN INTEREST RATES? Dean Croushore Professor of Economics and Rigsby Fellow, University of Richmond and Visiting Scholar, Federal

Confidence and the Transmission of Macroeconomic Uncertainty in U.S. Recessions

Confidence and the Transmission of Macroeconomic Uncertainty in U.S. Recessions Fang Zhang January 1, 216 Abstract This paper studies the role of confidence in the transmission of uncertainty shocks during

Confidence and the Transmission of Macroeconomic Uncertainty in U.S. Recessions Fang Zhang January 1, 216 Abstract This paper studies the role of confidence in the transmission of uncertainty shocks during

Inference Based on SVARs Identified with Sign and Zero Restrictions: Theory and Applications

Inference Based on SVARs Identified with Sign and Zero Restrictions: Theory and Applications Jonas Arias 1 Juan F. Rubio-Ramírez 2,3 Daniel F. Waggoner 3 1 Federal Reserve Board 2 Duke University 3 Federal

Inference Based on SVARs Identified with Sign and Zero Restrictions: Theory and Applications Jonas Arias 1 Juan F. Rubio-Ramírez 2,3 Daniel F. Waggoner 3 1 Federal Reserve Board 2 Duke University 3 Federal

The International Transmission of Shocks A Factor Structural Analysis Using Forecast Data

The International Transmission of Shocks A Factor Structural Analysis Using Forecast Data Kajal Lahiri Department of Economics University at Albany, SUNY (Joint work with Herbert Zhao) For presentation

The International Transmission of Shocks A Factor Structural Analysis Using Forecast Data Kajal Lahiri Department of Economics University at Albany, SUNY (Joint work with Herbert Zhao) For presentation

What can survey forecasts tell us about information rigidities?

What can survey forecasts tell us about information rigidities? Olivier Coibion College of William & Mary and NBER Yuriy Gorodnichenko UC Berkeley and NBER This Draft: June 1 th, 211 Abstract: A lot. We

What can survey forecasts tell us about information rigidities? Olivier Coibion College of William & Mary and NBER Yuriy Gorodnichenko UC Berkeley and NBER This Draft: June 1 th, 211 Abstract: A lot. We

5 Medium-Term Forecasts

CHAPTER 5 Medium-Term Forecasts You ve got to be very careful if you don t know where you re going, because you might not get there. Attributed to Yogi Berra, American baseball player and amateur philosopher

CHAPTER 5 Medium-Term Forecasts You ve got to be very careful if you don t know where you re going, because you might not get there. Attributed to Yogi Berra, American baseball player and amateur philosopher

A. Recursively orthogonalized. VARs

Orthogonalized VARs A. Recursively orthogonalized VAR B. Variance decomposition C. Historical decomposition D. Structural interpretation E. Generalized IRFs 1 A. Recursively orthogonalized Nonorthogonal

Orthogonalized VARs A. Recursively orthogonalized VAR B. Variance decomposition C. Historical decomposition D. Structural interpretation E. Generalized IRFs 1 A. Recursively orthogonalized Nonorthogonal

The Inflation Response to Government Spending Shocks: A Fiscal Price Puzzle?

The Inflation Response to Government Spending Shocks: A Fiscal Price Puzzle? Peter Lihn Jørgensen Søren Hove Ravn February 28 Abstract Based on a Structural Vector Autoregression SVAR model, this paper

The Inflation Response to Government Spending Shocks: A Fiscal Price Puzzle? Peter Lihn Jørgensen Søren Hove Ravn February 28 Abstract Based on a Structural Vector Autoregression SVAR model, this paper

The Information Content of Capacity Utilisation Rates for Output Gap Estimates

The Information Content of Capacity Utilisation Rates for Output Gap Estimates Michael Graff and Jan-Egbert Sturm 15 November 2010 Overview Introduction and motivation Data Output gap data: OECD Economic

The Information Content of Capacity Utilisation Rates for Output Gap Estimates Michael Graff and Jan-Egbert Sturm 15 November 2010 Overview Introduction and motivation Data Output gap data: OECD Economic

TIGER: Tracking Indexes for the Global Economic Recovery By Eswar Prasad and Karim Foda

TIGER: Tracking Indexes for the Global Economic Recovery By Eswar Prasad and Karim Foda Technical Appendix Methodology In our analysis, we employ a statistical procedure called Principal Compon Analysis

TIGER: Tracking Indexes for the Global Economic Recovery By Eswar Prasad and Karim Foda Technical Appendix Methodology In our analysis, we employ a statistical procedure called Principal Compon Analysis

Multivariate Markov Switching With Weighted Regime Determination: Giving France More Weight than Finland

Multivariate Markov Switching With Weighted Regime Determination: Giving France More Weight than Finland November 2006 Michael Dueker Federal Reserve Bank of St. Louis P.O. Box 442, St. Louis, MO 63166

Multivariate Markov Switching With Weighted Regime Determination: Giving France More Weight than Finland November 2006 Michael Dueker Federal Reserve Bank of St. Louis P.O. Box 442, St. Louis, MO 63166

Research Brief December 2018

Research Brief https://doi.org/10.21799/frbp.rb.2018.dec Battle of the Forecasts: Mean vs. Median as the Survey of Professional Forecasters Consensus Fatima Mboup Ardy L. Wurtzel Battle of the Forecasts:

Research Brief https://doi.org/10.21799/frbp.rb.2018.dec Battle of the Forecasts: Mean vs. Median as the Survey of Professional Forecasters Consensus Fatima Mboup Ardy L. Wurtzel Battle of the Forecasts:

Variable Targeting and Reduction in High-Dimensional Vector Autoregressions

Variable Targeting and Reduction in High-Dimensional Vector Autoregressions Tucker McElroy (U.S. Census Bureau) Frontiers in Forecasting February 21-23, 2018 1 / 22 Disclaimer This presentation is released

Variable Targeting and Reduction in High-Dimensional Vector Autoregressions Tucker McElroy (U.S. Census Bureau) Frontiers in Forecasting February 21-23, 2018 1 / 22 Disclaimer This presentation is released

Optimal Simple And Implementable Monetary and Fiscal Rules

Optimal Simple And Implementable Monetary and Fiscal Rules Stephanie Schmitt-Grohé Martín Uribe Duke University September 2007 1 Welfare-Based Policy Evaluation: Related Literature (ex: Rotemberg and Woodford,

Optimal Simple And Implementable Monetary and Fiscal Rules Stephanie Schmitt-Grohé Martín Uribe Duke University September 2007 1 Welfare-Based Policy Evaluation: Related Literature (ex: Rotemberg and Woodford,

HEALTHCARE. 5 Components of Accurate Rolling Forecasts in Healthcare

HEALTHCARE 5 Components of Accurate Rolling Forecasts in Healthcare Introduction Rolling Forecasts Improve Accuracy and Optimize Decisions Accurate budgeting, planning, and forecasting are essential for

HEALTHCARE 5 Components of Accurate Rolling Forecasts in Healthcare Introduction Rolling Forecasts Improve Accuracy and Optimize Decisions Accurate budgeting, planning, and forecasting are essential for

Testing the MC Model. 9.1 Introduction. 9.2 The Size and Solution of the MC model

9 Testing the MC Model 9.1 Introduction This chapter is concerned with testing the overall MC model. It is the counterpart of Chapter 8 for the US model. There are, however, many fewer tests in this chapter

9 Testing the MC Model 9.1 Introduction This chapter is concerned with testing the overall MC model. It is the counterpart of Chapter 8 for the US model. There are, however, many fewer tests in this chapter

FaMIDAS: A Mixed Frequency Factor Model with MIDAS structure

FaMIDAS: A Mixed Frequency Factor Model with MIDAS structure Frale C., Monteforte L. Computational and Financial Econometrics Limassol, October 2009 Introduction After the recent financial and economic

FaMIDAS: A Mixed Frequency Factor Model with MIDAS structure Frale C., Monteforte L. Computational and Financial Econometrics Limassol, October 2009 Introduction After the recent financial and economic

Graduate Macro Theory II: Notes on Quantitative Analysis in DSGE Models

Graduate Macro Theory II: Notes on Quantitative Analysis in DSGE Models Eric Sims University of Notre Dame Spring 2011 This note describes very briefly how to conduct quantitative analysis on a linearized

Graduate Macro Theory II: Notes on Quantitative Analysis in DSGE Models Eric Sims University of Notre Dame Spring 2011 This note describes very briefly how to conduct quantitative analysis on a linearized

REGIONAL SPILLOVER EFFECTS OF THE TOHOKU EARTHQUAKE (MARCH 2016)

") REGIONAL SPILLOVER EFFECTS OF THE TOHOKU EARTHQUAKE (MARCH 2016) Robert Dekle, Eunpyo Hong, and Wei Xie Department of Economics University of Southern California Work to understand how the 2011 earthquake

REGIONAL SPILLOVER EFFECTS OF THE TOHOKU EARTHQUAKE (MARCH 2016) Robert Dekle, Eunpyo Hong, and Wei Xie Department of Economics University of Southern California Work to understand how the 2011 earthquake

Discussion Paper Series

Discussion Paper Series China's Increasing Global Influence: Changes in International Growth Spillovers By Erdenebat Bataa, Denise R.Osborn, Marianne Sensier Centre for Growth and Business Cycle Research,

Discussion Paper Series China's Increasing Global Influence: Changes in International Growth Spillovers By Erdenebat Bataa, Denise R.Osborn, Marianne Sensier Centre for Growth and Business Cycle Research,

Why Has the U.S. Economy Stagnated Since the Great Recession?

Why Has the U.S. Economy Stagnated Since the Great Recession? Yunjong Eo, University of Sydney joint work with James Morley, University of Sydney Workshop on Nonlinear Models at the Norges Bank January

Why Has the U.S. Economy Stagnated Since the Great Recession? Yunjong Eo, University of Sydney joint work with James Morley, University of Sydney Workshop on Nonlinear Models at the Norges Bank January

Forecasting Global Recessions in a GVAR Model of Actual and Expected Output in the G7

Forecasting Global Recessions in a GVAR Model of Actual and Expected Output in the G Tony Garratt, Kevin Lee and Kalvinder Shields Ron Smith Conference London, June Lee (Ron Smith Conference) G Recessions

Forecasting Global Recessions in a GVAR Model of Actual and Expected Output in the G Tony Garratt, Kevin Lee and Kalvinder Shields Ron Smith Conference London, June Lee (Ron Smith Conference) G Recessions

PANEL DISCUSSION: THE ROLE OF POTENTIAL OUTPUT IN POLICYMAKING

PANEL DISCUSSION: THE ROLE OF POTENTIAL OUTPUT IN POLICYMAKING James Bullard* Federal Reserve Bank of St. Louis 33rd Annual Economic Policy Conference St. Louis, MO October 17, 2008 Views expressed are

PANEL DISCUSSION: THE ROLE OF POTENTIAL OUTPUT IN POLICYMAKING James Bullard* Federal Reserve Bank of St. Louis 33rd Annual Economic Policy Conference St. Louis, MO October 17, 2008 Views expressed are

Economic Forecasts. Too smooth by far? Prakash Loungani & Jair Rodriguez

Economic Forecasts Too smooth by far? Prakash Loungani & Jair Rodriguez Two questions about the global economic outlook are a matter of active conjecture at the moment: First, will the US economy go into

Economic Forecasts Too smooth by far? Prakash Loungani & Jair Rodriguez Two questions about the global economic outlook are a matter of active conjecture at the moment: First, will the US economy go into

1 Teaching notes on structural VARs.

Bent E. Sørensen February 22, 2007 1 Teaching notes on structural VARs. 1.1 Vector MA models: 1.1.1 Probability theory The simplest (to analyze, estimation is a different matter) time series models are

Bent E. Sørensen February 22, 2007 1 Teaching notes on structural VARs. 1.1 Vector MA models: 1.1.1 Probability theory The simplest (to analyze, estimation is a different matter) time series models are

South African Reserve Bank Working Paper

WP/13/02 South African Reserve Bank Working Paper The Impact of International Spillovers on the South African Economy Franz Ruch May 2013 Working Papers describe research in progress and are intended to

WP/13/02 South African Reserve Bank Working Paper The Impact of International Spillovers on the South African Economy Franz Ruch May 2013 Working Papers describe research in progress and are intended to

A Horse-Race Contest of Selected Economic Indicators & Their Potential Prediction Abilities on GDP

A Horse-Race Contest of Selected Economic Indicators & Their Potential Prediction Abilities on GDP Tahmoures Afshar, Woodbury University, USA ABSTRACT This paper empirically investigates, in the context

A Horse-Race Contest of Selected Economic Indicators & Their Potential Prediction Abilities on GDP Tahmoures Afshar, Woodbury University, USA ABSTRACT This paper empirically investigates, in the context

No Staff Memo. Evaluating real-time forecasts from Norges Bank s system for averaging models. Anne Sofie Jore, Norges Bank Monetary Policy

No. 12 2012 Staff Memo Evaluating real-time forecasts from Norges Bank s system for averaging models Anne Sofie Jore, Norges Bank Monetary Policy Staff Memos present reports and documentation written by

No. 12 2012 Staff Memo Evaluating real-time forecasts from Norges Bank s system for averaging models Anne Sofie Jore, Norges Bank Monetary Policy Staff Memos present reports and documentation written by

Information Rigidity in Growth Forecasts: Some Cross-Country Evidence

WP/11/125 Information Rigidity in Growth Forecasts: Some Cross-Country Evidence Prakash Loungani, Herman Stekler and Natalia Tamirisa 2011 International Monetary Fund WP/11/125 IMF Working Paper Research

WP/11/125 Information Rigidity in Growth Forecasts: Some Cross-Country Evidence Prakash Loungani, Herman Stekler and Natalia Tamirisa 2011 International Monetary Fund WP/11/125 IMF Working Paper Research

Are US Output Expectations Unbiased? A Cointegrated VAR Analysis in Real Time

Are US Output Expectations Unbiased? A Cointegrated VAR Analysis in Real Time by Dimitrios Papaikonomou a and Jacinta Pires b, a Ministry of Finance, Greece b Christ Church, University of Oxford, UK Abstract

Are US Output Expectations Unbiased? A Cointegrated VAR Analysis in Real Time by Dimitrios Papaikonomou a and Jacinta Pires b, a Ministry of Finance, Greece b Christ Church, University of Oxford, UK Abstract

Adverse Effects of Monetary Policy Signalling

Adverse Effects of Monetary Policy Signalling Jan FILÁČEK and Jakub MATĚJŮ Monetary Department Czech National Bank CNB Research Open Day, 18 th May 21 Outline What do we mean by adverse effects of monetary

Adverse Effects of Monetary Policy Signalling Jan FILÁČEK and Jakub MATĚJŮ Monetary Department Czech National Bank CNB Research Open Day, 18 th May 21 Outline What do we mean by adverse effects of monetary

Identifying SVARs with Sign Restrictions and Heteroskedasticity

Identifying SVARs with Sign Restrictions and Heteroskedasticity Srečko Zimic VERY PRELIMINARY AND INCOMPLETE NOT FOR DISTRIBUTION February 13, 217 Abstract This paper introduces a new method to identify

Identifying SVARs with Sign Restrictions and Heteroskedasticity Srečko Zimic VERY PRELIMINARY AND INCOMPLETE NOT FOR DISTRIBUTION February 13, 217 Abstract This paper introduces a new method to identify

Panel Discussion on Uses of Models at Central Banks

Slide 1 of 25 on Uses of Models at Central Banks ECB Workshop on DSGE Models and Forecasting September 23, 2016 Slide 1 of 24 How are models used at the Board of Governors? For forecasting For alternative

Slide 1 of 25 on Uses of Models at Central Banks ECB Workshop on DSGE Models and Forecasting September 23, 2016 Slide 1 of 24 How are models used at the Board of Governors? For forecasting For alternative

Economics 618B: Time Series Analysis Department of Economics State University of New York at Binghamton

Problem Set #1 1. Generate n =500random numbers from both the uniform 1 (U [0, 1], uniformbetween zero and one) and exponential λ exp ( λx) (set λ =2and let x U [0, 1]) b a distributions. Plot the histograms

Problem Set #1 1. Generate n =500random numbers from both the uniform 1 (U [0, 1], uniformbetween zero and one) and exponential λ exp ( λx) (set λ =2and let x U [0, 1]) b a distributions. Plot the histograms

News, Noise, and Fluctuations: An Empirical Exploration

News, Noise, and Fluctuations: An Empirical Exploration Olivier J. Blanchard, Jean-Paul L Huillier, Guido Lorenzoni January 2009 Abstract We explore empirically a model of aggregate fluctuations with two

News, Noise, and Fluctuations: An Empirical Exploration Olivier J. Blanchard, Jean-Paul L Huillier, Guido Lorenzoni January 2009 Abstract We explore empirically a model of aggregate fluctuations with two

Information Rigidities in Economic Growth Forecasts: Evidence from a Large International Panel

WP/13/56 Information Rigidities in Economic Growth Forecasts: Evidence from a Large International Panel Jonas Dovern, Ulrich Fritsche, Prakash Loungani, and Natalia Tamirisa 213 International Monetary

WP/13/56 Information Rigidities in Economic Growth Forecasts: Evidence from a Large International Panel Jonas Dovern, Ulrich Fritsche, Prakash Loungani, and Natalia Tamirisa 213 International Monetary

Etsuro Shioji (Hitotsubashi)

") JES 2017, February 10 Discussion on Miyamoto, Nguyen and Sergeyev Government Spending Multipliers under the Zero Lower Bound: Evidence from Japan Etsuro Shioji (Hitotsubashi) Major comment: This is a great

JES 2017, February 10 Discussion on Miyamoto, Nguyen and Sergeyev Government Spending Multipliers under the Zero Lower Bound: Evidence from Japan Etsuro Shioji (Hitotsubashi) Major comment: This is a great

EUROPEAN ECONOMY EUROPEAN COMMISSION DIRECTORATE-GENERAL FOR ECONOMIC AND FINANCIAL AFFAIRS

EUROPEAN ECONOMY EUROPEAN COMMISSION DIRECTORATE-GENERAL FOR ECONOMIC AND FINANCIAL AFFAIRS ECONOMIC PAPERS ISSN 1725-3187 http://europa.eu.int/comm/economy_finance N 249 June 2006 The Stacked Leading

EUROPEAN ECONOMY EUROPEAN COMMISSION DIRECTORATE-GENERAL FOR ECONOMIC AND FINANCIAL AFFAIRS ECONOMIC PAPERS ISSN 1725-3187 http://europa.eu.int/comm/economy_finance N 249 June 2006 The Stacked Leading

Switching Regime Estimation

Switching Regime Estimation Series de Tiempo BIrkbeck March 2013 Martin Sola (FE) Markov Switching models 01/13 1 / 52 The economy (the time series) often behaves very different in periods such as booms

Switching Regime Estimation Series de Tiempo BIrkbeck March 2013 Martin Sola (FE) Markov Switching models 01/13 1 / 52 The economy (the time series) often behaves very different in periods such as booms

Are Forecast Updates Progressive?

MPRA Munich Personal RePEc Archive Are Forecast Updates Progressive? Chia-Lin Chang and Philip Hans Franses and Michael McAleer National Chung Hsing University, Erasmus University Rotterdam, Erasmus University

MPRA Munich Personal RePEc Archive Are Forecast Updates Progressive? Chia-Lin Chang and Philip Hans Franses and Michael McAleer National Chung Hsing University, Erasmus University Rotterdam, Erasmus University

Variance Decomposition Analysis for Nonlinear DSGE Models: An Application with ZLB

Variance Decomposition Analysis for Nonlinear DSGE Models: An Application with ZLB Phuong V. Ngo Maksim Isakin Francois Gourio January 5, 2018 Abstract In this paper, we first proposes two new methods

Variance Decomposition Analysis for Nonlinear DSGE Models: An Application with ZLB Phuong V. Ngo Maksim Isakin Francois Gourio January 5, 2018 Abstract In this paper, we first proposes two new methods

A Critical Note on the Forecast Error Variance Decomposition

A Critical Note on the Forecast Error Variance Decomposition Atilim Seymen This Version: March, 28 Preliminary: Do not cite without author s permisson. Abstract The paper questions the reasonability of

A Critical Note on the Forecast Error Variance Decomposition Atilim Seymen This Version: March, 28 Preliminary: Do not cite without author s permisson. Abstract The paper questions the reasonability of

The Size and Evolution of the Government Spending Multiplier in France - Technical Appendix -

The Size and Evolution of the Government Spending Multiplier in France - Technical Appendix - Guillaume CLÉAUD INSEE-CREST Matthieu LEMOINE Banque de France Pierre-Alain PIONNIER INSEE-CREST November 2015

The Size and Evolution of the Government Spending Multiplier in France - Technical Appendix - Guillaume CLÉAUD INSEE-CREST Matthieu LEMOINE Banque de France Pierre-Alain PIONNIER INSEE-CREST November 2015

A Nonparametric Approach to Identifying a Subset of Forecasters that Outperforms the Simple Average

A Nonparametric Approach to Identifying a Subset of Forecasters that Outperforms the Simple Average Constantin Bürgi The George Washington University cburgi@gwu.edu Tara M. Sinclair The George Washington

A Nonparametric Approach to Identifying a Subset of Forecasters that Outperforms the Simple Average Constantin Bürgi The George Washington University cburgi@gwu.edu Tara M. Sinclair The George Washington

VARMA versus VAR for Macroeconomic Forecasting

VARMA versus VAR for Macroeconomic Forecasting 1 VARMA versus VAR for Macroeconomic Forecasting George Athanasopoulos Department of Econometrics and Business Statistics Monash University Farshid Vahid

VARMA versus VAR for Macroeconomic Forecasting 1 VARMA versus VAR for Macroeconomic Forecasting George Athanasopoulos Department of Econometrics and Business Statistics Monash University Farshid Vahid

Nowcasting gross domestic product in Japan using professional forecasters information

Kanagawa University Economic Society Discussion Paper No. 2017-4 Nowcasting gross domestic product in Japan using professional forecasters information Nobuo Iizuka March 9, 2018 Nowcasting gross domestic

Kanagawa University Economic Society Discussion Paper No. 2017-4 Nowcasting gross domestic product in Japan using professional forecasters information Nobuo Iizuka March 9, 2018 Nowcasting gross domestic

Constructing Turning Point Chronologies with Markov Switching Vector Autoregressive Models: the Euro Zone Business Cycle

Constructing Turning Point Chronologies with Markov Switching Vector Autoregressive Models: the Euro Zone Business Cycle Hans Martin Krolzig Department of Economics and Nuffield College, Oxford University.

Constructing Turning Point Chronologies with Markov Switching Vector Autoregressive Models: the Euro Zone Business Cycle Hans Martin Krolzig Department of Economics and Nuffield College, Oxford University.

WORKING PAPER NO FISCAL SURPRISES AT THE FOMC

WORKING PAPER NO. 17-13 FISCAL SURPRISES AT THE FOMC Dean Croushore Professor of Economics and Rigsby Fellow, University of Richmond and Visiting Scholar, Federal Reserve Bank of Philadelphia Simon van

WORKING PAPER NO. 17-13 FISCAL SURPRISES AT THE FOMC Dean Croushore Professor of Economics and Rigsby Fellow, University of Richmond and Visiting Scholar, Federal Reserve Bank of Philadelphia Simon van

Nowcasting Norwegian GDP

Nowcasting Norwegian GDP Knut Are Aastveit and Tørres Trovik May 13, 2007 Introduction Motivation The last decades of advances in information technology has made it possible to access a huge amount of

Nowcasting Norwegian GDP Knut Are Aastveit and Tørres Trovik May 13, 2007 Introduction Motivation The last decades of advances in information technology has made it possible to access a huge amount of

Assessing recent external forecasts

Assessing recent external forecasts Felipe Labbé and Hamish Pepper This article compares the performance between external forecasts and Reserve Bank of New Zealand published projections for real GDP growth,

Assessing recent external forecasts Felipe Labbé and Hamish Pepper This article compares the performance between external forecasts and Reserve Bank of New Zealand published projections for real GDP growth,

Quarterly Journal of Economics and Modelling Shahid Beheshti University SVAR * SVAR * **

1392 Quarterly Journal of Economics and Modelling Shahid Beheshti University : SVAR * ** 93/9/2 93/2/15 SVAR h-dargahi@sbuacir esedaghatparast@ibiacir ( 1 * ** 1392 13 2 SVAR H30, C32, E62, E52, E32 JEL

1392 Quarterly Journal of Economics and Modelling Shahid Beheshti University : SVAR * ** 93/9/2 93/2/15 SVAR h-dargahi@sbuacir esedaghatparast@ibiacir ( 1 * ** 1392 13 2 SVAR H30, C32, E62, E52, E32 JEL

Nonlinear Relation of Inflation and Nominal Interest Rates A Local Nonparametric Investigation

Nonlinear Relation of Inflation and Nominal Interest Rates A Local Nonparametric Investigation Marcelle Chauvet and Heather L. R. Tierney * Abstract This paper investigates the relationship between nominal

Nonlinear Relation of Inflation and Nominal Interest Rates A Local Nonparametric Investigation Marcelle Chauvet and Heather L. R. Tierney * Abstract This paper investigates the relationship between nominal

U n iversity o f H ei delberg. A Multivariate Analysis of Forecast Disagreement: Confronting Models of Disagreement with SPF Data

U n iversity o f H ei delberg Department of Economics Discussion Paper Series No. 571 482482 A Multivariate Analysis of Forecast Disagreement: Confronting Models of Disagreement with SPF Data Jonas Dovern

U n iversity o f H ei delberg Department of Economics Discussion Paper Series No. 571 482482 A Multivariate Analysis of Forecast Disagreement: Confronting Models of Disagreement with SPF Data Jonas Dovern

Time-varying Fiscal Multipliers Identified with Sign and Zero Restrictions: A Bayesian Approach to TVP-VAR-SV model

Time-varying Fiscal Multipliers Identified with Sign and Zero Restrictions: A Bayesian Approach to TVP-VAR-SV model Hirokuni Iiboshi and Yasuharu Iwata May 5 (Work in Progress) Abstract This study might

Time-varying Fiscal Multipliers Identified with Sign and Zero Restrictions: A Bayesian Approach to TVP-VAR-SV model Hirokuni Iiboshi and Yasuharu Iwata May 5 (Work in Progress) Abstract This study might

Great Recession and Monetary Policy Transmission

Great Recession and Monetary Policy Transmission German Lopez Buenache University of Alicante November 19, 2014 Abstract This paper studies the existence of changes in the transmission mechanism of monetary

Great Recession and Monetary Policy Transmission German Lopez Buenache University of Alicante November 19, 2014 Abstract This paper studies the existence of changes in the transmission mechanism of monetary

The Central Bank of Iceland forecasting record

Forecasting errors are inevitable. Some stem from errors in the models used for forecasting, others are due to inaccurate information on the economic variables on which the models are based measurement

Forecasting errors are inevitable. Some stem from errors in the models used for forecasting, others are due to inaccurate information on the economic variables on which the models are based measurement

Time-Varying Vector Autoregressive Models with Structural Dynamic Factors

Time-Varying Vector Autoregressive Models with Structural Dynamic Factors Paolo Gorgi, Siem Jan Koopman, Julia Schaumburg http://sjkoopman.net Vrije Universiteit Amsterdam School of Business and Economics

Time-Varying Vector Autoregressive Models with Structural Dynamic Factors Paolo Gorgi, Siem Jan Koopman, Julia Schaumburg http://sjkoopman.net Vrije Universiteit Amsterdam School of Business and Economics

Accuracy of models with heterogeneous agents

Accuracy of models with heterogeneous agents Wouter J. Den Haan London School of Economics c by Wouter J. Den Haan Introduction Models with heterogeneous agents have many different dimensions Krusell-Smith

Accuracy of models with heterogeneous agents Wouter J. Den Haan London School of Economics c by Wouter J. Den Haan Introduction Models with heterogeneous agents have many different dimensions Krusell-Smith

Y t = log (employment t )

") Advanced Macroeconomics, Christiano Econ 416 Homework #7 Due: November 21 1. Consider the linearized equilibrium conditions of the New Keynesian model, on the slide, The Equilibrium Conditions in the handout,

Advanced Macroeconomics, Christiano Econ 416 Homework #7 Due: November 21 1. Consider the linearized equilibrium conditions of the New Keynesian model, on the slide, The Equilibrium Conditions in the handout,

Pricing To Habits and the Law of One Price

Pricing To Habits and the Law of One Price Morten Ravn 1 Stephanie Schmitt-Grohé 2 Martin Uribe 2 1 European University Institute 2 Duke University Izmir, May 18, 27 Stylized facts we wish to address Pricing-to-Market:

Pricing To Habits and the Law of One Price Morten Ravn 1 Stephanie Schmitt-Grohé 2 Martin Uribe 2 1 European University Institute 2 Duke University Izmir, May 18, 27 Stylized facts we wish to address Pricing-to-Market:

Matching DSGE models,vars, and state space models. Fabio Canova EUI and CEPR September 2012

Matching DSGE models,vars, and state space models Fabio Canova EUI and CEPR September 2012 Outline Alternative representations of the solution of a DSGE model. Fundamentalness and finite VAR representation

Matching DSGE models,vars, and state space models Fabio Canova EUI and CEPR September 2012 Outline Alternative representations of the solution of a DSGE model. Fundamentalness and finite VAR representation

New Shocks: Different Effects in Boom and Recession?

THE TENTH YOUNG ECONOMISTS SEMINAR TO THE TWENTY-FIRST DUBROVNIK ECONOMIC CONFERENCE Organized by the Croatian National Bank Maria Bolboaca and Sarah Fischer New Shocks: Different Effects in Boom and Recession?

THE TENTH YOUNG ECONOMISTS SEMINAR TO THE TWENTY-FIRST DUBROVNIK ECONOMIC CONFERENCE Organized by the Croatian National Bank Maria Bolboaca and Sarah Fischer New Shocks: Different Effects in Boom and Recession?

Warwick Business School Forecasting System. Summary. Ana Galvao, Anthony Garratt and James Mitchell November, 2014

Warwick Business School Forecasting System Summary Ana Galvao, Anthony Garratt and James Mitchell November, 21 The main objective of the Warwick Business School Forecasting System is to provide competitive

Warwick Business School Forecasting System Summary Ana Galvao, Anthony Garratt and James Mitchell November, 21 The main objective of the Warwick Business School Forecasting System is to provide competitive

TIGER: Tracking Indexes for the Global Economic Recovery By Eswar Prasad, Karim Foda, and Ethan Wu

TIGER: Tracking Indexes for the Global Economic Recovery By Eswar Prasad, Karim Foda, and Ethan Wu Technical Appendix Methodology In our analysis, we employ a statistical procedure called Principal Component

TIGER: Tracking Indexes for the Global Economic Recovery By Eswar Prasad, Karim Foda, and Ethan Wu Technical Appendix Methodology In our analysis, we employ a statistical procedure called Principal Component

problem. max Both k (0) and h (0) are given at time 0. (a) Write down the Hamilton-Jacobi-Bellman (HJB) Equation in the dynamic programming

and h (0) are given at time 0. (a) Write down the Hamilton-Jacobi-Bellman (HJB) Equation in the dynamic programming") 1. Endogenous Growth with Human Capital Consider the following endogenous growth model with both physical capital (k (t)) and human capital (h (t)) in continuous time. The representative household solves

1. Endogenous Growth with Human Capital Consider the following endogenous growth model with both physical capital (k (t)) and human capital (h (t)) in continuous time. The representative household solves

Intervention Analysis and Transfer Function Models

Chapter 7 Intervention Analysis and Transfer Function Models The idea in intervention analysis and transfer function models is to generalize the univariate methods studies previously to allow the time

Chapter 7 Intervention Analysis and Transfer Function Models The idea in intervention analysis and transfer function models is to generalize the univariate methods studies previously to allow the time

CHAPTER III RESEARCH METHODOLOGY. trade balance performance of selected ASEAN-5 countries and exchange rate

CHAPTER III RESEARCH METHODOLOGY 3.1 Research s Object The research object is taking the macroeconomic perspective and focused on selected ASEAN-5 countries. This research is conducted to describe how

CHAPTER III RESEARCH METHODOLOGY 3.1 Research s Object The research object is taking the macroeconomic perspective and focused on selected ASEAN-5 countries. This research is conducted to describe how

Is the Purchasing Managers Index a Reliable Indicator of GDP Growth?

Is the Purchasing Managers Index a Reliable Indicator of GDP Growth? Some Evidence from Indian Data i c r a b u l l e t i n Suchismita Bose Abstract Purchasing Managers Index (PMI) surveys have been developed

Is the Purchasing Managers Index a Reliable Indicator of GDP Growth? Some Evidence from Indian Data i c r a b u l l e t i n Suchismita Bose Abstract Purchasing Managers Index (PMI) surveys have been developed

Periklis. Gogas. Tel: +27. Working May 2017

University of Pretoria Department of Economics Working Paper Series Macroeconomicc Uncertainty, Growth and Inflation in the Eurozone: A Causal Approach Vasilios Plakandaras Democritus University of Thrace

University of Pretoria Department of Economics Working Paper Series Macroeconomicc Uncertainty, Growth and Inflation in the Eurozone: A Causal Approach Vasilios Plakandaras Democritus University of Thrace

DISCUSSION PAPERS IN ECONOMICS

STRATHCLYDE DISCUSSION PAPERS IN ECONOMICS UK HOUSE PRICES: CONVERGENCE CLUBS AND SPILLOVERS BY ALBERTO MONTAGNOLI AND JUN NAGAYASU NO 13-22 DEPARTMENT OF ECONOMICS UNIVERSITY OF STRATHCLYDE GLASGOW UK

STRATHCLYDE DISCUSSION PAPERS IN ECONOMICS UK HOUSE PRICES: CONVERGENCE CLUBS AND SPILLOVERS BY ALBERTO MONTAGNOLI AND JUN NAGAYASU NO 13-22 DEPARTMENT OF ECONOMICS UNIVERSITY OF STRATHCLYDE GLASGOW UK

Estimating Causal Effects in Macroeconomics: General Methods and Pitfalls. By Valerie A. Ramey

Estimating Causal Effects in Macroeconomics: General Methods and Pitfalls By Valerie A. Ramey 1 Question we want to answer: How can we estimate empirically the key parameters that help us answer the following

Estimating Causal Effects in Macroeconomics: General Methods and Pitfalls By Valerie A. Ramey 1 Question we want to answer: How can we estimate empirically the key parameters that help us answer the following