Optimization Problems with Probabilistic Constraints

|

|

|

- Maude Spencer

- 5 years ago

- Views:

Transcription

1 Optimization Problems with Probabilistic Constraints R. Henrion Weierstrass Institute Berlin 10 th International Conference on Stochastic Programming University of Arizona, Tucson

: Stochastic Programming.")

2 Recommended Reading A. Prekopa: Stochastic Programming Kluwer, Dordrecht, A. Prekopa: Probabilistic Programming Chapter 5 in A. Ruszczynski and A. Shapiro (eds.): Stochastic Programming. Handbooks in Operations Research and Management Science, Vol. 10, Elsevier, 2003.Amsterdam

3 Overview 1. Example 2. Models 3. Structure 4. Numerics 5. Stability

4 Probabilistic Constraints conventional optimization problem: min f x h j x 0 j 1,...,m In many real life problems from finance, engineering etc., the constraints involve random parameters due to demographic, meteorological, economical etc. uncertainties: h j x, 0 Often, a decision x has to be taken before is observed ('here and now'). No matter, how x is chosen, there is no guarantee that for all possible realizations of. h j x, 0 If the distribution of is known, we may calculate for each x the probability of constraint satisfaction: P h j x, 0 j 1,...,m reasonable: x feasible if this probability is larger than some safety level p. optimization problem with probabilistic constraints:: min f x P h j x 0 j 1,...,m p p 0,1 Applications: finance, power generation, water managment, telecommunication, chemical engineering etc.

5 1. Example

6 The cash matching problem 1 The pension fund of a company has to make payments for the next 15 years. Payments shall be covered by investing an initial capital K in bonds of 3 different types. Decision variables: x 1, x 2, x 3 - number of bonds of each type to be bought. Objective: Maximize final amount of cash (after 15 years) Constraints: cover payments in all years. 1 A. Ruszczynski ( and Dentcheva, Lai, Ruszczynski (2003)

7 Data and liquidity constraints year payments ,000 12,000 14,000 15,000 16,000 18,000 20,000 21,000 22,000 24,000 25,000 30,000 31,000 31,000 31,000 yields per bond of type cost per bond: ij cash available at the end of year j: 3 K i x i ik x i i 1 k 1 i 1 k 1 cash after buying bonds Rearrangement: a ij : k 1 3 i 1 K = 250,000 (initial capital) j j 3 cumulative yields of bonds ik i b j : k 1 liquidity constraints: a ij x i b j j k 0 cumulative payments j k K 0 j 1,...,15 j i

8 Linear optimization problem liquidity in year j: 3 i 1 a ij x i b j 0 final cash: 3 i 1 a i,15 x i b 15 optimization problem: 3 max i 1 3 a i,15 x i i 1 a ij x i b j j 1,...,15

9 Solution of the deterministic cash matching problem x opt 31.1,55.5,147.3 f x opt 127,332 payments cash

number of scenarios violating positive cash (empirical probability of constraint violation) 50")

10 payments (expected value + 2 scenarios) Random Payments cash (expected value + 2 scenarios) payments (expected value scenarios) cash (expected value scenarios) number of scenarios violating positive cash (empirical probability of constraint violation) 50 %

11 Model with individual probabilistic constraints Now, payments are random variables Assumption: independent, normal distribution, E j j, Var j 500 j j expected payments = deterministic payments variance increasing with time j cumulative payments: j : k k 1 j E j b j, Var j k 1 optimization problem with random parameter: 3 max i 1 3 a i,15 x i i 1 Difficulty: decide on x before normal distribution Var j a ij x i j j 1,...,15 is observed ('here-and-now' decision)

12 3 max i 1 3 a i,15 x i i 1 (continued) expected-value problem ( = our deterministic problem): a ij x i E j b j j 1,...,15 probabilistic constraint: 3 P i 1 a ij x i j p 0,1 probability measure probability level optimization problem with individual probabilistic constraints: 3 max i 1 a i,15 x i P i 1 3 a ij x i j p j 1,...,15

13 (continued) P 3 i 1 a ij x i j P 3 i 1 a ij x i E j Var j j E j Var j P 3 i 1 a ij x i j 3 p i 1 standard normal a ij x i E j q p Var j Linear optimization problem: p-quantile of standard normal 3 max i 1 3 a i,15 x i i 1 a ij x i b j q p Var j j 1,...,15 safety term

14 Solution of the cash matching problem with individual probabilistic constraints (p=0.95) x opt 62.8,72.6,101.1 x opt 31.1,55.5,147.3 f x opt 103,925 recall expected value (or deterministic) solution: f x opt 127,332 cash (indiv. prob. cons.) 100 scenarios cash (expected value solution) 100 scenarios

15 (continued) number of scenarios violating positive cash (empirical probability of constraint violation) expected value solution final cash as a function of the probability level p exp. value prob. constr. final cash worst case indiv. prob. constr. p over a wide range robustness can be increased at moderate costs

16 Model with joint probabilistic constraints individual probabilistic constraints: at each fixed time probability of constraint violation low but: over the whole time interval violation may be likely cash at each t at most 1 out of 5 scenarios violates positive cash 0 time but: all 5 scenarios violate positive cash Therefore, replace the collection P 3 i 1 a ij x i j p j 1,...,15 of individual probabilistic constraints by one single P joint probabilistic constraint: 3 i 1 a ij x i j j 1,...,15 p

17 Solution of the cash matching problem with joint probabilistic constraints (p=0.95) x opt 31.1,55.5,147.3 f x opt 127,332 expected value solution 85 violating scenarios x opt 62.8,72.6,101.1 indiv. prob. constr. 12 violating scenarios f x opt 103,925 x opt 65.8,83.7,86.2 joint prob. constr. 2 violating scenarios f x opt 98,160

18 2. Models

19 Types of Probabilistic Constraints Probabilistic constraints may be given in individual: P h j x, 0 p j 1,...,m or joint form: P h j x, 0 j 1,...,m p decision vector random vector 3 cash matching problem: h j x, i 1 a ij x i j Structural properties and solution methods depend on: Form of the probabilistic constraint (individual or joint) Distribution of the random vector (continuous, discrete, independence) Properties of the constraint function h (linear, convex, separable)

20 Random right-hand side Assume that the constraint function has separable structure: h j x, g j x j individual prob. constr.: p-quantile P h j x, 0 p P g j x j p g j x q p j 1,...,m Probabilistic constraints of same type as deterministic constraints (no additional difficulties by randomness). Cash matching problem: g j linear prob. constr. linear too joint prob. constr.: P h j x, 0 j 1,...,m p P g j x j j 1,...,m p F g x p (no quantile!) multivariate distribution function g is analytically given, in general. Main task: calculate F

21 Independent components joint prob. constr. with random rhs.: F g x p 1,..., s independent F 1 g 1 x F s g s x p 1-dimensional distribution functions (easy to calculate) Independence of components rarely satisfied. Cash matching problem: payments j were assumed to be independent But: cumulative payments j are correlated nevertheless. covariance matrix: Var j j

22 Polyhedral Probabilistic Constraints Let h j x, b j x a j x, b j : n, a j : n s joint prob. constr.: P b j x a j x, j 1,...,m p, 1 Decision and random vector no longer separated. x fixed: probability of a polyhedron Multivariate normal distribution: N,, a j x a j j : a j, 1 : F b x p, N A, A A T normal probability of a polyhedron = normal distribution function value But: If m>s (more inequalities than random components, e.g., networks) singular normal distribution

23 Random Coefficients Let h j x, b j x x, j b j : n, j n Special case of polyhedral prob. constr.: a j x x, T : 1 T,..., m T joint probabilistic constraint: P x b x p random matrix Example: cash matching problem with random yields.

24 3. Structure

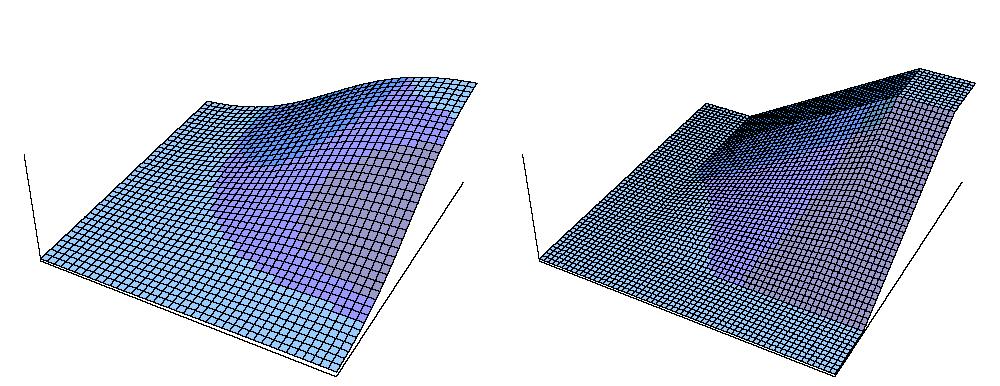

25 Structural properties We are interested in properties (continuity, differentiability, convexity) of the constraint function x : P h j x, 0 j 1,...,m and of the feasible set M : x n x p Lemma: h j uppersemicontinuous uppersemicontinuous M closed Example: standardnormal, h 1 x, : x 1, h 2 x, : x 2 discontinuous although all data are smooth h j, distribution of x 1,x 2 x 2 For 0<p<1, the feasible set (blue) 0 is not convex. x 1

26 Properties by composition recall joint prob. constr. with random rhs.: F g x p When is F g continuous, Lipschitzian, differentiable? By composition, all these properties are inherited from F, g. This is obvious, in general, for g. How about F? Lemma: F is continuous if it has a density. F is Lipschitzian if it has bounded marginal densities 1 F is differentiable if the functions t F x x i t are continuous for all x,i. conditional distribution function 1 Römisch/Schultz (1993)

27 Convexity joint prob. constr. with random rhs.: F g x p 2 When is F g concave? convex optimization algorithms components g j concave, A 1 concave and nondecreasing e.g., linear, see cash matching problem automatically satisfied for distribution functions When is F concave? Never! (distribution functions are bounded from below and above but not constant) Is there a nondecreasing function : such that F concave? If so, then 2 F g x p F g concave if components g j concave. increasing and concave Possible candidates: log, n

28 Logconcavity of distribution functions normal uniform F normal uniform exponential Cauchy log F exponential Cauchy normal uniform exponential F 1 Cauchy

29 bivariate normal uniform on unit square Log (bivariate normal) Log (uniform on unit square)

30 Prekopa's Theorem (reduced version) multivariate distribution functions extremely difficult to calculate (no analytic formula) almost impossible to check log-concavity directly Prekopa's Theorem: If the distribution function F has a density f, and if log f is concave, then log F is concave too. Example: multivariate normal distribution f K exp 1 2 x T 1 x log f log K 1 2 x T 1 x concave log F concave Other examples: uniform distribution on convex compact sets, Dirichlet, Gamma, etc.

31 Van de Panne/Popp - Theorem (extended version) Theorem: Let N, have a multivariate normal distribution. Consider a single probabilistic constraint with random coefficients: P x, 0 x p The induced feasible set M x n x p is convex, if p 0, ,1, 1-dim. standard normal distribution function smallest eigenvalue of Theorem generalizes to several individual prob. constr. (intersection of convex sets is convex) but not to joint prob. constr. (see example above).

32 Example: x M x 2 P x, 0 p N 1,0, I 2 x p = 0.8 p = 0.5 convex p = 0.2 convex nonconvex

33 Related Properties constraint set M x P Ax p Theorem: 1 Let have any distribution and let A have positively linear independent rows. Then, M is connected. Example: ~ uniform distribution on (1,-2,0),(-2,1,0),(-2,-2, ), p=0.5 0 A 1 1 M not convex but connected M rows pos. lin. indep. A 1 1 cash matching problem does not satisfy the assumption! 1: H. (2001) 2: H./Römisch (2004) M not connected rows not pos. lin. indep. Theorem: 2 Let ~ nondeg. multiv. normal, independent components. Then, log F is strongly concave on bounded sets. Let ~ uniform on s-dim. interval [a,b]. Then, log F is strongly concave on int[a,b]. Not true for arbitrary polytopes!

34 4. Numerics

35 Random r.h.s, normal distribution joint linear prob. constr. with random rhs.: P Ax p F Ax p Assumptions has a nondegenerate multivariate normal distribution example: cash matching problem with joint probabilistic constraints F A differentiable and concave (recall that F is log-concave) Algorithms from differentiable convex optimization (e.g., supporting hyperplanes) numerical requirements: calculation of F and of F. calculation of gradients may be reduced to the calculation of values 1 (in one dimension less) main challenge: calculation of F 1 Prekopa: Stochastic Programming

36 Calculating the normal distribution function (s = dimension of random vector) 'exact' calculation for s = 1,2 1,2 numerical integration (up to s~15) 3,4 efficient simulation techniques 5,6 bounds (linear programming 7 ; graph-theoretical constructions 8 combined use of bounding and simulation techniques (up to s~50) 1: Donnely (1973) 2: Drezner, Wesolowsky (1990) 3: Schervish (1984) 4: Genz (1992) 5: Deak (1986) 6: Szantai (1985) 7: Prekopa (1990) 8: Bukszar, Prekopa (2001),

37 Bounds Let have a 4-dim. standard normal distribution (independent components) For x:=(2,1,2,1), we want to estimate F x P 1 2, 2 1, 3 2, 4 1 : 1 dim.standardnormaldistr. funct., , exact value: F x trivial upper bound: F x min 1, A i : i x i first order complementary events A ij : i x i j x j second order complementary events S 1 : i P A i, S 2 : i j In the example: S , S P A ij can be calculated exactly (1- and 2-dim. normal distributions) Bonferroni bounds: 1 S 1 F x 1 S 1 S F x improved lower bound: 1 S 1 2 s S 2 F x F x

38 Hunters lower bound Define a graph with nodes = A i, edges = A ij and weights of edges = P(A ij ): A 1 P(A 14 ) = A 4 Find a spanning tree T with maximum P(A 12 ) = A 2 P(A 24 ) = P(A 13 ) = P(A 23 ) = A 3 P(A 34 ) = weight #T. new lower bound: 1 S 1 + #T Here: #T = F 2,1,2, Comparison of bounds: true value: trivial upper bound: Bonferroni lower bound: Bonferroni upper bound: improved lower bound: Hunters lower bound: 0.670

39 Cutting Plane Method min c,x F Ax p c F Ax p F A x p line search: precise values expansive, imprecise values require safe cuts

40 p Line Search (Szantai) acceptance region safety region upper bound true value lower bound repeat bisection until in acceptance region if in safety region increase precision 0 true 1

41 Discrete Distributions min c,x F Ax p 3 finite discrete distribution p level set of F : y s N F y p j 1 z j s p-level efficient points 3 min j J min c,x Ax z j convex hull F y p F y p p-level efficient points conceptual solution method: determine all p-level efficient points (too many!) solve all resulting linear programs select the best solution (out of finitely many) relaxed problem: N min c,x Ax co j 1 min c,x Ax j z j, j j 1 stepwise generation of p-level efficient points 1 1 Dentcheva, Prekopa, Ruszczynski (2000) N z j s N 0, j 1 j 1

42 5. Stability

43 Approximation Original optimization problem with linear joint probabilistic constraint: min f x F Ax p Assumption: f convex, F log-concave (e.g., multivariate normal). Problem: distribution of in general not known Approximation by some (e.g., empirical approximation) F F v : inf f x F Ax p (optimal value) S : x F Ax p, f x v (solution set) How do v and S behave near? sample (N=10)

44 Qualitative Stability min f x F Ax p P Theorem: 1 For the original problem (P) suppose that: S is nonempty and bounded There is some x with F A x p (Slater point). Then, S is upper semicontinuous at converge to a true solution). (approximating solutions will Furthermore, there are L, 0, such that v v L F F : F F 1 H./Römisch (2004)

45 Lipschitz-Continuity of the Value-at-Risk VaR p inf t P t p p 0,1 usually not continuous! Corollary: Let p 0,1 and have a log-concave distribution. Then, there exist L, 0 such that VaR p VaR p F F : F F

46 Quantitative Stability (Hölder type) min c,x x,hx F Ax p H 0 convex quadratic objective Theorem: 1 In addition to the assumptions in the previous Theorem, suppose that F is strongly convex on some open convex set U A S Then, there are L, 0, such that d H S,S L F F : F F 1 H./Römisch (2004)

Optimization Problems with Linear Chance Constraints Structure, Numerics and Applications. R. Henrion

Optimization Problems with Linear Chance Constraints Structure, Numerics and Applications R. Henrion Weierstraß-Institut Berlin Introduction with Examples Structure (convexity, differentiability, existence

Optimization Problems with Linear Chance Constraints Structure, Numerics and Applications R. Henrion Weierstraß-Institut Berlin Introduction with Examples Structure (convexity, differentiability, existence

Lipschitz and differentiability properties of quasi-concave and singular normal distribution functions

Ann Oper Res (2010) 177: 115 125 DOI 10.1007/s10479-009-0598-0 Lipschitz and differentiability properties of quasi-concave and singular normal distribution functions René Henrion Werner Römisch Published

Ann Oper Res (2010) 177: 115 125 DOI 10.1007/s10479-009-0598-0 Lipschitz and differentiability properties of quasi-concave and singular normal distribution functions René Henrion Werner Römisch Published

Convexity of chance constraints with dependent random variables: the use of copulae

Convexity of chance constraints with dependent random variables: the use of copulae René Henrion 1 and Cyrille Strugarek 2 1 Weierstrass Institute for Applied Analysis and Stochastics, 10117 Berlin, Germany.

Convexity of chance constraints with dependent random variables: the use of copulae René Henrion 1 and Cyrille Strugarek 2 1 Weierstrass Institute for Applied Analysis and Stochastics, 10117 Berlin, Germany.

2 Chance constrained programming

2 Chance constrained programming In this Chapter we give a brief introduction to chance constrained programming. The goals are to motivate the subject and to give the reader an idea of the related difficulties.

2 Chance constrained programming In this Chapter we give a brief introduction to chance constrained programming. The goals are to motivate the subject and to give the reader an idea of the related difficulties.

Semidefinite and Second Order Cone Programming Seminar Fall 2012 Project: Robust Optimization and its Application of Robust Portfolio Optimization

Semidefinite and Second Order Cone Programming Seminar Fall 2012 Project: Robust Optimization and its Application of Robust Portfolio Optimization Instructor: Farid Alizadeh Author: Ai Kagawa 12/12/2012

Semidefinite and Second Order Cone Programming Seminar Fall 2012 Project: Robust Optimization and its Application of Robust Portfolio Optimization Instructor: Farid Alizadeh Author: Ai Kagawa 12/12/2012

Reformulation of chance constrained problems using penalty functions

Reformulation of chance constrained problems using penalty functions Martin Branda Charles University in Prague Faculty of Mathematics and Physics EURO XXIV July 11-14, 2010, Lisbon Martin Branda (MFF

Reformulation of chance constrained problems using penalty functions Martin Branda Charles University in Prague Faculty of Mathematics and Physics EURO XXIV July 11-14, 2010, Lisbon Martin Branda (MFF

A gradient formula for linear chance constraints under Gaussian distribution

A gradient formula for linear chance constraints under Gaussian distribution René Henrion Weierstrass Institute Berlin, 10117 Berlin, Germany Andris Möller Weierstrass Institute Berlin, 10117 Berlin, Germany

A gradient formula for linear chance constraints under Gaussian distribution René Henrion Weierstrass Institute Berlin, 10117 Berlin, Germany Andris Möller Weierstrass Institute Berlin, 10117 Berlin, Germany

Threshold Boolean Form for Joint Probabilistic Constraints with Random Technology Matrix

Threshold Boolean Form for Joint Probabilistic Constraints with Random Technology Matrix Alexander Kogan, Miguel A. Leeune Abstract We develop a new modeling and exact solution method for stochastic programming

Threshold Boolean Form for Joint Probabilistic Constraints with Random Technology Matrix Alexander Kogan, Miguel A. Leeune Abstract We develop a new modeling and exact solution method for stochastic programming

Portfolio optimization with stochastic dominance constraints

Charles University in Prague Faculty of Mathematics and Physics Portfolio optimization with stochastic dominance constraints December 16, 2014 Contents Motivation 1 Motivation 2 3 4 5 Contents Motivation

Charles University in Prague Faculty of Mathematics and Physics Portfolio optimization with stochastic dominance constraints December 16, 2014 Contents Motivation 1 Motivation 2 3 4 5 Contents Motivation

ORIGINS OF STOCHASTIC PROGRAMMING

ORIGINS OF STOCHASTIC PROGRAMMING Early 1950 s: in applications of Linear Programming unknown values of coefficients: demands, technological coefficients, yields, etc. QUOTATION Dantzig, Interfaces 20,1990

ORIGINS OF STOCHASTIC PROGRAMMING Early 1950 s: in applications of Linear Programming unknown values of coefficients: demands, technological coefficients, yields, etc. QUOTATION Dantzig, Interfaces 20,1990

Chance Constrained Problems

W eierstraß -Institut für Angew andte Analysis und Stochastik Chance Constrained Problems René Henrion Weierstraß-Institut Berlin August 15, 2009 Suggested Reading Contents Models (Examples, Linear Chance

W eierstraß -Institut für Angew andte Analysis und Stochastik Chance Constrained Problems René Henrion Weierstraß-Institut Berlin August 15, 2009 Suggested Reading Contents Models (Examples, Linear Chance

Solution of Probabilistic Constrained Stochastic Programming Problems with Poisson, Binomial and Geometric Random Variables

R u t c o r Research R e p o r t Solution of Probabilistic Constrained Stochastic Programming Problems with Poisson, Binomial and Geometric Random Variables Tongyin Liu a András Prékopa b RRR 29-2005,

R u t c o r Research R e p o r t Solution of Probabilistic Constrained Stochastic Programming Problems with Poisson, Binomial and Geometric Random Variables Tongyin Liu a András Prékopa b RRR 29-2005,

Włodzimierz Ogryczak. Warsaw University of Technology, ICCE ON ROBUST SOLUTIONS TO MULTI-OBJECTIVE LINEAR PROGRAMS. Introduction. Abstract.

Włodzimierz Ogryczak Warsaw University of Technology, ICCE ON ROBUST SOLUTIONS TO MULTI-OBJECTIVE LINEAR PROGRAMS Abstract In multiple criteria linear programming (MOLP) any efficient solution can be found

Włodzimierz Ogryczak Warsaw University of Technology, ICCE ON ROBUST SOLUTIONS TO MULTI-OBJECTIVE LINEAR PROGRAMS Abstract In multiple criteria linear programming (MOLP) any efficient solution can be found

Distributionally Robust Discrete Optimization with Entropic Value-at-Risk

Distributionally Robust Discrete Optimization with Entropic Value-at-Risk Daniel Zhuoyu Long Department of SEEM, The Chinese University of Hong Kong, zylong@se.cuhk.edu.hk Jin Qi NUS Business School, National

Distributionally Robust Discrete Optimization with Entropic Value-at-Risk Daniel Zhuoyu Long Department of SEEM, The Chinese University of Hong Kong, zylong@se.cuhk.edu.hk Jin Qi NUS Business School, National

R u t c o r Research R e p o r t. Application of the Solution of the Univariate Discrete Moment Problem for the Multivariate Case. Gergely Mádi-Nagy a

R u t c o r Research R e p o r t Application of the Solution of the Univariate Discrete Moment Problem for the Multivariate Case Gergely Mádi-Nagy a RRR 9-28, April 28 RUTCOR Rutgers Center for Operations

R u t c o r Research R e p o r t Application of the Solution of the Univariate Discrete Moment Problem for the Multivariate Case Gergely Mádi-Nagy a RRR 9-28, April 28 RUTCOR Rutgers Center for Operations

Sharp bounds on the VaR for sums of dependent risks

Paul Embrechts Sharp bounds on the VaR for sums of dependent risks joint work with Giovanni Puccetti (university of Firenze, Italy) and Ludger Rüschendorf (university of Freiburg, Germany) Mathematical

Paul Embrechts Sharp bounds on the VaR for sums of dependent risks joint work with Giovanni Puccetti (university of Firenze, Italy) and Ludger Rüschendorf (university of Freiburg, Germany) Mathematical

Inverse Stochastic Dominance Constraints Duality and Methods

Duality and Methods Darinka Dentcheva 1 Andrzej Ruszczyński 2 1 Stevens Institute of Technology Hoboken, New Jersey, USA 2 Rutgers University Piscataway, New Jersey, USA Research supported by NSF awards

Duality and Methods Darinka Dentcheva 1 Andrzej Ruszczyński 2 1 Stevens Institute of Technology Hoboken, New Jersey, USA 2 Rutgers University Piscataway, New Jersey, USA Research supported by NSF awards

Convex relaxations of chance constrained optimization problems

Convex relaxations of chance constrained optimization problems Shabbir Ahmed School of Industrial & Systems Engineering, Georgia Institute of Technology, 765 Ferst Drive, Atlanta, GA 30332. May 12, 2011

Convex relaxations of chance constrained optimization problems Shabbir Ahmed School of Industrial & Systems Engineering, Georgia Institute of Technology, 765 Ferst Drive, Atlanta, GA 30332. May 12, 2011

Valid Inequalities and Restrictions for Stochastic Programming Problems with First Order Stochastic Dominance Constraints

Valid Inequalities and Restrictions for Stochastic Programming Problems with First Order Stochastic Dominance Constraints Nilay Noyan Andrzej Ruszczyński March 21, 2006 Abstract Stochastic dominance relations

Valid Inequalities and Restrictions for Stochastic Programming Problems with First Order Stochastic Dominance Constraints Nilay Noyan Andrzej Ruszczyński March 21, 2006 Abstract Stochastic dominance relations

Solving Chance-Constrained Stochastic Programs via Sampling and Integer Programming

IFORMS 2008 c 2008 IFORMS isbn 978-1-877640-23-0 doi 10.1287/educ.1080.0048 Solving Chance-Constrained Stochastic Programs via Sampling and Integer Programming Shabbir Ahmed and Alexander Shapiro H. Milton

IFORMS 2008 c 2008 IFORMS isbn 978-1-877640-23-0 doi 10.1287/educ.1080.0048 Solving Chance-Constrained Stochastic Programs via Sampling and Integer Programming Shabbir Ahmed and Alexander Shapiro H. Milton

Robust Optimization for Risk Control in Enterprise-wide Optimization

Robust Optimization for Risk Control in Enterprise-wide Optimization Juan Pablo Vielma Department of Industrial Engineering University of Pittsburgh EWO Seminar, 011 Pittsburgh, PA Uncertainty in Optimization

Robust Optimization for Risk Control in Enterprise-wide Optimization Juan Pablo Vielma Department of Industrial Engineering University of Pittsburgh EWO Seminar, 011 Pittsburgh, PA Uncertainty in Optimization

Separation Techniques for Constrained Nonlinear 0 1 Programming

Separation Techniques for Constrained Nonlinear 0 1 Programming Christoph Buchheim Computer Science Department, University of Cologne and DEIS, University of Bologna MIP 2008, Columbia University, New

Separation Techniques for Constrained Nonlinear 0 1 Programming Christoph Buchheim Computer Science Department, University of Cologne and DEIS, University of Bologna MIP 2008, Columbia University, New

MAT-INF4110/MAT-INF9110 Mathematical optimization

MAT-INF4110/MAT-INF9110 Mathematical optimization Geir Dahl August 20, 2013 Convexity Part IV Chapter 4 Representation of convex sets different representations of convex sets, boundary polyhedra and polytopes:

MAT-INF4110/MAT-INF9110 Mathematical optimization Geir Dahl August 20, 2013 Convexity Part IV Chapter 4 Representation of convex sets different representations of convex sets, boundary polyhedra and polytopes:

Lectures 6, 7 and part of 8

Lectures 6, 7 and part of 8 Uriel Feige April 26, May 3, May 10, 2015 1 Linear programming duality 1.1 The diet problem revisited Recall the diet problem from Lecture 1. There are n foods, m nutrients,

Lectures 6, 7 and part of 8 Uriel Feige April 26, May 3, May 10, 2015 1 Linear programming duality 1.1 The diet problem revisited Recall the diet problem from Lecture 1. There are n foods, m nutrients,

Solving the MWT. Recall the ILP for the MWT. We can obtain a solution to the MWT problem by solving the following ILP:

Solving the MWT Recall the ILP for the MWT. We can obtain a solution to the MWT problem by solving the following ILP: max subject to e i E ω i x i e i C E x i {0, 1} x i C E 1 for all critical mixed cycles

Solving the MWT Recall the ILP for the MWT. We can obtain a solution to the MWT problem by solving the following ILP: max subject to e i E ω i x i e i C E x i {0, 1} x i C E 1 for all critical mixed cycles

A model for dynamic chance constraints in hydro power reservoir management

A model for dynamic chance constraints in hydro power reservoir management L. Andrieu, R. Henrion, W. Römisch January 18, 2009 2000 Mathematics Subject Classification. 90C15, 90B05. Keywords: dynamic chance

A model for dynamic chance constraints in hydro power reservoir management L. Andrieu, R. Henrion, W. Römisch January 18, 2009 2000 Mathematics Subject Classification. 90C15, 90B05. Keywords: dynamic chance

Assignment 1: From the Definition of Convexity to Helley Theorem

Assignment 1: From the Definition of Convexity to Helley Theorem Exercise 1 Mark in the following list the sets which are convex: 1. {x R 2 : x 1 + i 2 x 2 1, i = 1,..., 10} 2. {x R 2 : x 2 1 + 2ix 1x

Assignment 1: From the Definition of Convexity to Helley Theorem Exercise 1 Mark in the following list the sets which are convex: 1. {x R 2 : x 1 + i 2 x 2 1, i = 1,..., 10} 2. {x R 2 : x 2 1 + 2ix 1x

Motivation General concept of CVaR Optimization Comparison. VaR and CVaR. Přemysl Bejda.

VaR and CVaR Přemysl Bejda premyslbejda@gmail.com 2014 Contents 1 Motivation 2 General concept of CVaR 3 Optimization 4 Comparison Contents 1 Motivation 2 General concept of CVaR 3 Optimization 4 Comparison

VaR and CVaR Přemysl Bejda premyslbejda@gmail.com 2014 Contents 1 Motivation 2 General concept of CVaR 3 Optimization 4 Comparison Contents 1 Motivation 2 General concept of CVaR 3 Optimization 4 Comparison

Section Notes 8. Integer Programming II. Applied Math 121. Week of April 5, expand your knowledge of big M s and logical constraints.

Section Notes 8 Integer Programming II Applied Math 121 Week of April 5, 2010 Goals for the week understand IP relaxations be able to determine the relative strength of formulations understand the branch

Section Notes 8 Integer Programming II Applied Math 121 Week of April 5, 2010 Goals for the week understand IP relaxations be able to determine the relative strength of formulations understand the branch

On Kusuoka Representation of Law Invariant Risk Measures

MATHEMATICS OF OPERATIONS RESEARCH Vol. 38, No. 1, February 213, pp. 142 152 ISSN 364-765X (print) ISSN 1526-5471 (online) http://dx.doi.org/1.1287/moor.112.563 213 INFORMS On Kusuoka Representation of

MATHEMATICS OF OPERATIONS RESEARCH Vol. 38, No. 1, February 213, pp. 142 152 ISSN 364-765X (print) ISSN 1526-5471 (online) http://dx.doi.org/1.1287/moor.112.563 213 INFORMS On Kusuoka Representation of

Appendix PRELIMINARIES 1. THEOREMS OF ALTERNATIVES FOR SYSTEMS OF LINEAR CONSTRAINTS

Appendix PRELIMINARIES 1. THEOREMS OF ALTERNATIVES FOR SYSTEMS OF LINEAR CONSTRAINTS Here we consider systems of linear constraints, consisting of equations or inequalities or both. A feasible solution

Appendix PRELIMINARIES 1. THEOREMS OF ALTERNATIVES FOR SYSTEMS OF LINEAR CONSTRAINTS Here we consider systems of linear constraints, consisting of equations or inequalities or both. A feasible solution

Computational Integer Programming. Lecture 2: Modeling and Formulation. Dr. Ted Ralphs

Computational Integer Programming Lecture 2: Modeling and Formulation Dr. Ted Ralphs Computational MILP Lecture 2 1 Reading for This Lecture N&W Sections I.1.1-I.1.6 Wolsey Chapter 1 CCZ Chapter 2 Computational

Computational Integer Programming Lecture 2: Modeling and Formulation Dr. Ted Ralphs Computational MILP Lecture 2 1 Reading for This Lecture N&W Sections I.1.1-I.1.6 Wolsey Chapter 1 CCZ Chapter 2 Computational

Werner Romisch. Humboldt University Berlin. Abstract. Perturbations of convex chance constrained stochastic programs are considered the underlying

Stability of solutions to chance constrained stochastic programs Rene Henrion Weierstrass Institute for Applied Analysis and Stochastics D-7 Berlin, Germany and Werner Romisch Humboldt University Berlin

Stability of solutions to chance constrained stochastic programs Rene Henrion Weierstrass Institute for Applied Analysis and Stochastics D-7 Berlin, Germany and Werner Romisch Humboldt University Berlin

Sequential Convex Approximations to Joint Chance Constrained Programs: A Monte Carlo Approach

Sequential Convex Approximations to Joint Chance Constrained Programs: A Monte Carlo Approach L. Jeff Hong Department of Industrial Engineering and Logistics Management The Hong Kong University of Science

Sequential Convex Approximations to Joint Chance Constrained Programs: A Monte Carlo Approach L. Jeff Hong Department of Industrial Engineering and Logistics Management The Hong Kong University of Science

Stochastic Programming: From statistical data to optimal decisions

Stochastic Programming: From statistical data to optimal decisions W. Römisch Humboldt-University Berlin Department of Mathematics (K. Emich, H. Heitsch, A. Möller) Page 1 of 24 6th International Conference

Stochastic Programming: From statistical data to optimal decisions W. Römisch Humboldt-University Berlin Department of Mathematics (K. Emich, H. Heitsch, A. Möller) Page 1 of 24 6th International Conference

Structured Problems and Algorithms

Integer and quadratic optimization problems Dept. of Engg. and Comp. Sci., Univ. of Cal., Davis Aug. 13, 2010 Table of contents Outline 1 2 3 Benefits of Structured Problems Optimization problems may become

Integer and quadratic optimization problems Dept. of Engg. and Comp. Sci., Univ. of Cal., Davis Aug. 13, 2010 Table of contents Outline 1 2 3 Benefits of Structured Problems Optimization problems may become

3.10 Lagrangian relaxation

3.10 Lagrangian relaxation Consider a generic ILP problem min {c t x : Ax b, Dx d, x Z n } with integer coefficients. Suppose Dx d are the complicating constraints. Often the linear relaxation and the

3.10 Lagrangian relaxation Consider a generic ILP problem min {c t x : Ax b, Dx d, x Z n } with integer coefficients. Suppose Dx d are the complicating constraints. Often the linear relaxation and the

CVaR and Examples of Deviation Risk Measures

CVaR and Examples of Deviation Risk Measures Jakub Černý Department of Probability and Mathematical Statistics Stochastic Modelling in Economics and Finance November 10, 2014 1 / 25 Contents CVaR - Dual

CVaR and Examples of Deviation Risk Measures Jakub Černý Department of Probability and Mathematical Statistics Stochastic Modelling in Economics and Finance November 10, 2014 1 / 25 Contents CVaR - Dual

Complexity of two and multi-stage stochastic programming problems

Complexity of two and multi-stage stochastic programming problems A. Shapiro School of Industrial and Systems Engineering, Georgia Institute of Technology, Atlanta, Georgia 30332-0205, USA The concept

Complexity of two and multi-stage stochastic programming problems A. Shapiro School of Industrial and Systems Engineering, Georgia Institute of Technology, Atlanta, Georgia 30332-0205, USA The concept

Robustness in Stochastic Programs with Risk Constraints

Robustness in Stochastic Programs with Risk Constraints Dept. of Probability and Mathematical Statistics, Faculty of Mathematics and Physics Charles University, Prague, Czech Republic www.karlin.mff.cuni.cz/~kopa

Robustness in Stochastic Programs with Risk Constraints Dept. of Probability and Mathematical Statistics, Faculty of Mathematics and Physics Charles University, Prague, Czech Republic www.karlin.mff.cuni.cz/~kopa

LP Duality: outline. Duality theory for Linear Programming. alternatives. optimization I Idea: polyhedra

LP Duality: outline I Motivation and definition of a dual LP I Weak duality I Separating hyperplane theorem and theorems of the alternatives I Strong duality and complementary slackness I Using duality

LP Duality: outline I Motivation and definition of a dual LP I Weak duality I Separating hyperplane theorem and theorems of the alternatives I Strong duality and complementary slackness I Using duality

Integer Programming ISE 418. Lecture 8. Dr. Ted Ralphs

Integer Programming ISE 418 Lecture 8 Dr. Ted Ralphs ISE 418 Lecture 8 1 Reading for This Lecture Wolsey Chapter 2 Nemhauser and Wolsey Sections II.3.1, II.3.6, II.4.1, II.4.2, II.5.4 Duality for Mixed-Integer

Integer Programming ISE 418 Lecture 8 Dr. Ted Ralphs ISE 418 Lecture 8 1 Reading for This Lecture Wolsey Chapter 2 Nemhauser and Wolsey Sections II.3.1, II.3.6, II.4.1, II.4.2, II.5.4 Duality for Mixed-Integer

A CONVEXITY THEOREM IN PROGRAMMING UNDER PROBABILISTIC CONSTRAINTS

R u t c o r Research R e p o r t A CONVEXITY THEOREM IN PROGRAMMING UNDER PROBABILISTIC CONSTRAINTS András Prékopa a Mine Subasi b RRR 32-2007, December 2007 RUTCOR Rutgers Center for Operations Research

R u t c o r Research R e p o r t A CONVEXITY THEOREM IN PROGRAMMING UNDER PROBABILISTIC CONSTRAINTS András Prékopa a Mine Subasi b RRR 32-2007, December 2007 RUTCOR Rutgers Center for Operations Research

arxiv: v1 [cs.dm] 27 Jan 2014

![arxiv: v1 [cs.dm] 27 Jan 2014](/thumbs/82/84894440.jpg "arxiv: v1 [cs.dm] 27 Jan 2014") Randomized Minmax Regret for Combinatorial Optimization Under Uncertainty Andrew Mastin, Patrick Jaillet, Sang Chin arxiv:1401.7043v1 [cs.dm] 27 Jan 2014 January 29, 2014 Abstract The minmax regret problem

Randomized Minmax Regret for Combinatorial Optimization Under Uncertainty Andrew Mastin, Patrick Jaillet, Sang Chin arxiv:1401.7043v1 [cs.dm] 27 Jan 2014 January 29, 2014 Abstract The minmax regret problem

I.3. LMI DUALITY. Didier HENRION EECI Graduate School on Control Supélec - Spring 2010

I.3. LMI DUALITY Didier HENRION henrion@laas.fr EECI Graduate School on Control Supélec - Spring 2010 Primal and dual For primal problem p = inf x g 0 (x) s.t. g i (x) 0 define Lagrangian L(x, z) = g 0

I.3. LMI DUALITY Didier HENRION henrion@laas.fr EECI Graduate School on Control Supélec - Spring 2010 Primal and dual For primal problem p = inf x g 0 (x) s.t. g i (x) 0 define Lagrangian L(x, z) = g 0

Author's personal copy

Comput Manag Sci (2015) 12:435 459 DOI 10.1007/s10287-015-0228-z ORIGINAL PAPER Probabilistic constraints via SQP solver: application to a renewable energy management problem I. Bremer R. Henrion A. Möller

Comput Manag Sci (2015) 12:435 459 DOI 10.1007/s10287-015-0228-z ORIGINAL PAPER Probabilistic constraints via SQP solver: application to a renewable energy management problem I. Bremer R. Henrion A. Möller

Concepts and Applications of Stochastically Weighted Stochastic Dominance

Concepts and Applications of Stochastically Weighted Stochastic Dominance Jian Hu Department of Industrial Engineering and Management Sciences Northwestern University jianhu@northwestern.edu Tito Homem-de-Mello

Concepts and Applications of Stochastically Weighted Stochastic Dominance Jian Hu Department of Industrial Engineering and Management Sciences Northwestern University jianhu@northwestern.edu Tito Homem-de-Mello

Uncertainty modeling for robust verifiable design. Arnold Neumaier University of Vienna Vienna, Austria

Uncertainty modeling for robust verifiable design Arnold Neumaier University of Vienna Vienna, Austria Safety Safety studies in structural engineering are supposed to guard against failure in all reasonable

Uncertainty modeling for robust verifiable design Arnold Neumaier University of Vienna Vienna, Austria Safety Safety studies in structural engineering are supposed to guard against failure in all reasonable

Cut Generation for Optimization Problems with Multivariate Risk Constraints

Cut Generation for Optimization Problems with Multivariate Risk Constraints Simge Küçükyavuz Department of Integrated Systems Engineering, The Ohio State University, kucukyavuz.2@osu.edu Nilay Noyan 1

Cut Generation for Optimization Problems with Multivariate Risk Constraints Simge Küçükyavuz Department of Integrated Systems Engineering, The Ohio State University, kucukyavuz.2@osu.edu Nilay Noyan 1

Chance constrained optimization - applications, properties and numerical issues

Chance constrained optimization - applications, properties and numerical issues Dr. Abebe Geletu Ilmenau University of Technology Department of Simulation and Optimal Processes (SOP) May 31, 2012 This

Chance constrained optimization - applications, properties and numerical issues Dr. Abebe Geletu Ilmenau University of Technology Department of Simulation and Optimal Processes (SOP) May 31, 2012 This

EMPIRICAL ESTIMATES IN STOCHASTIC OPTIMIZATION VIA DISTRIBUTION TAILS

K Y BERNETIKA VOLUM E 46 ( 2010), NUMBER 3, P AGES 459 471 EMPIRICAL ESTIMATES IN STOCHASTIC OPTIMIZATION VIA DISTRIBUTION TAILS Vlasta Kaňková Classical optimization problems depending on a probability

K Y BERNETIKA VOLUM E 46 ( 2010), NUMBER 3, P AGES 459 471 EMPIRICAL ESTIMATES IN STOCHASTIC OPTIMIZATION VIA DISTRIBUTION TAILS Vlasta Kaňková Classical optimization problems depending on a probability

A randomized method for handling a difficult function in a convex optimization problem, motivated by probabilistic programming

A randomized method for handling a difficult function in a convex optimization problem, motivated by probabilistic programming Csaba I. Fábián Tamás Szántai Abstract We propose a randomized gradient method

A randomized method for handling a difficult function in a convex optimization problem, motivated by probabilistic programming Csaba I. Fábián Tamás Szántai Abstract We propose a randomized gradient method

On deterministic reformulations of distributionally robust joint chance constrained optimization problems

On deterministic reformulations of distributionally robust joint chance constrained optimization problems Weijun Xie and Shabbir Ahmed School of Industrial & Systems Engineering Georgia Institute of Technology,

On deterministic reformulations of distributionally robust joint chance constrained optimization problems Weijun Xie and Shabbir Ahmed School of Industrial & Systems Engineering Georgia Institute of Technology,

The Bayes classifier

The Bayes classifier Consider where is a random vector in is a random variable (depending on ) Let be a classifier with probability of error/risk given by The Bayes classifier (denoted ) is the optimal

The Bayes classifier Consider where is a random vector in is a random variable (depending on ) Let be a classifier with probability of error/risk given by The Bayes classifier (denoted ) is the optimal

Stochastic Programming with Multivariate Second Order Stochastic Dominance Constraints with Applications in Portfolio Optimization

Stochastic Programming with Multivariate Second Order Stochastic Dominance Constraints with Applications in Portfolio Optimization Rudabeh Meskarian 1 Department of Engineering Systems and Design, Singapore

Stochastic Programming with Multivariate Second Order Stochastic Dominance Constraints with Applications in Portfolio Optimization Rudabeh Meskarian 1 Department of Engineering Systems and Design, Singapore

Miloš Kopa. Decision problems with stochastic dominance constraints

Decision problems with stochastic dominance constraints Motivation Portfolio selection model Mean risk models max λ Λ m(λ r) νr(λ r) or min λ Λ r(λ r) s.t. m(λ r) µ r is a random vector of assets returns

Decision problems with stochastic dominance constraints Motivation Portfolio selection model Mean risk models max λ Λ m(λ r) νr(λ r) or min λ Λ r(λ r) s.t. m(λ r) µ r is a random vector of assets returns

A SECOND ORDER STOCHASTIC DOMINANCE PORTFOLIO EFFICIENCY MEASURE

K Y B E R N E I K A V O L U M E 4 4 ( 2 0 0 8 ), N U M B E R 2, P A G E S 2 4 3 2 5 8 A SECOND ORDER SOCHASIC DOMINANCE PORFOLIO EFFICIENCY MEASURE Miloš Kopa and Petr Chovanec In this paper, we introduce

K Y B E R N E I K A V O L U M E 4 4 ( 2 0 0 8 ), N U M B E R 2, P A G E S 2 4 3 2 5 8 A SECOND ORDER SOCHASIC DOMINANCE PORFOLIO EFFICIENCY MEASURE Miloš Kopa and Petr Chovanec In this paper, we introduce

Branch-and-cut Approaches for Chance-constrained Formulations of Reliable Network Design Problems

Branch-and-cut Approaches for Chance-constrained Formulations of Reliable Network Design Problems Yongjia Song James R. Luedtke August 9, 2012 Abstract We study solution approaches for the design of reliably

Branch-and-cut Approaches for Chance-constrained Formulations of Reliable Network Design Problems Yongjia Song James R. Luedtke August 9, 2012 Abstract We study solution approaches for the design of reliably

Basic Sampling Methods

Basic Sampling Methods Sargur Srihari srihari@cedar.buffalo.edu 1 1. Motivation Topics Intractability in ML How sampling can help 2. Ancestral Sampling Using BNs 3. Transforming a Uniform Distribution

Basic Sampling Methods Sargur Srihari srihari@cedar.buffalo.edu 1 1. Motivation Topics Intractability in ML How sampling can help 2. Ancestral Sampling Using BNs 3. Transforming a Uniform Distribution

Chapter 2: Preliminaries and elements of convex analysis

Chapter 2: Preliminaries and elements of convex analysis Edoardo Amaldi DEIB Politecnico di Milano edoardo.amaldi@polimi.it Website: http://home.deib.polimi.it/amaldi/opt-14-15.shtml Academic year 2014-15

Chapter 2: Preliminaries and elements of convex analysis Edoardo Amaldi DEIB Politecnico di Milano edoardo.amaldi@polimi.it Website: http://home.deib.polimi.it/amaldi/opt-14-15.shtml Academic year 2014-15

Stability of Stochastic Programming Problems

Stability of Stochastic Programming Problems W. Römisch Humboldt-University Berlin Institute of Mathematics 10099 Berlin, Germany http://www.math.hu-berlin.de/~romisch Page 1 of 35 Spring School Stochastic

Stability of Stochastic Programming Problems W. Römisch Humboldt-University Berlin Institute of Mathematics 10099 Berlin, Germany http://www.math.hu-berlin.de/~romisch Page 1 of 35 Spring School Stochastic

Convex optimization problems. Optimization problem in standard form

Convex optimization problems optimization problem in standard form convex optimization problems linear optimization quadratic optimization geometric programming quasiconvex optimization generalized inequality

Convex optimization problems optimization problem in standard form convex optimization problems linear optimization quadratic optimization geometric programming quasiconvex optimization generalized inequality

4. Convex optimization problems

Convex Optimization Boyd & Vandenberghe 4. Convex optimization problems optimization problem in standard form convex optimization problems quasiconvex optimization linear optimization quadratic optimization

Convex Optimization Boyd & Vandenberghe 4. Convex optimization problems optimization problem in standard form convex optimization problems quasiconvex optimization linear optimization quadratic optimization

GENERALIZED CONVEXITY AND OPTIMALITY CONDITIONS IN SCALAR AND VECTOR OPTIMIZATION

Chapter 4 GENERALIZED CONVEXITY AND OPTIMALITY CONDITIONS IN SCALAR AND VECTOR OPTIMIZATION Alberto Cambini Department of Statistics and Applied Mathematics University of Pisa, Via Cosmo Ridolfi 10 56124

Chapter 4 GENERALIZED CONVEXITY AND OPTIMALITY CONDITIONS IN SCALAR AND VECTOR OPTIMIZATION Alberto Cambini Department of Statistics and Applied Mathematics University of Pisa, Via Cosmo Ridolfi 10 56124

Review. DS GA 1002 Statistical and Mathematical Models. Carlos Fernandez-Granda

Review DS GA 1002 Statistical and Mathematical Models http://www.cims.nyu.edu/~cfgranda/pages/dsga1002_fall16 Carlos Fernandez-Granda Probability and statistics Probability: Framework for dealing with

Review DS GA 1002 Statistical and Mathematical Models http://www.cims.nyu.edu/~cfgranda/pages/dsga1002_fall16 Carlos Fernandez-Granda Probability and statistics Probability: Framework for dealing with

Robust linear optimization under general norms

Operations Research Letters 3 (004) 50 56 Operations Research Letters www.elsevier.com/locate/dsw Robust linear optimization under general norms Dimitris Bertsimas a; ;, Dessislava Pachamanova b, Melvyn

Operations Research Letters 3 (004) 50 56 Operations Research Letters www.elsevier.com/locate/dsw Robust linear optimization under general norms Dimitris Bertsimas a; ;, Dessislava Pachamanova b, Melvyn

Risk Aggregation with Dependence Uncertainty

Introduction Extreme Scenarios Asymptotic Behavior Challenges Risk Aggregation with Dependence Uncertainty Department of Statistics and Actuarial Science University of Waterloo, Canada Seminar at ETH Zurich

Introduction Extreme Scenarios Asymptotic Behavior Challenges Risk Aggregation with Dependence Uncertainty Department of Statistics and Actuarial Science University of Waterloo, Canada Seminar at ETH Zurich

Solving Dual Problems

Lecture 20 Solving Dual Problems We consider a constrained problem where, in addition to the constraint set X, there are also inequality and linear equality constraints. Specifically the minimization problem

Lecture 20 Solving Dual Problems We consider a constrained problem where, in addition to the constraint set X, there are also inequality and linear equality constraints. Specifically the minimization problem

Stochastic Optimization One-stage problem

Stochastic Optimization One-stage problem V. Leclère September 28 2017 September 28 2017 1 / Déroulement du cours 1 Problèmes d optimisation stochastique à une étape 2 Problèmes d optimisation stochastique

Stochastic Optimization One-stage problem V. Leclère September 28 2017 September 28 2017 1 / Déroulement du cours 1 Problèmes d optimisation stochastique à une étape 2 Problèmes d optimisation stochastique

14 : Theory of Variational Inference: Inner and Outer Approximation

10-708: Probabilistic Graphical Models 10-708, Spring 2014 14 : Theory of Variational Inference: Inner and Outer Approximation Lecturer: Eric P. Xing Scribes: Yu-Hsin Kuo, Amos Ng 1 Introduction Last lecture

10-708: Probabilistic Graphical Models 10-708, Spring 2014 14 : Theory of Variational Inference: Inner and Outer Approximation Lecturer: Eric P. Xing Scribes: Yu-Hsin Kuo, Amos Ng 1 Introduction Last lecture

MIP reformulations of some chance-constrained mathematical programs

MIP reformulations of some chance-constrained mathematical programs Ricardo Fukasawa Department of Combinatorics & Optimization University of Waterloo December 4th, 2012 FIELDS Industrial Optimization

MIP reformulations of some chance-constrained mathematical programs Ricardo Fukasawa Department of Combinatorics & Optimization University of Waterloo December 4th, 2012 FIELDS Industrial Optimization

Maximization of a Strongly Unimodal Multivariate Discrete Distribution

R u t c o r Research R e p o r t Maximization of a Strongly Unimodal Multivariate Discrete Distribution Mine Subasi a Ersoy Subasi b András Prékopa c RRR 12-2009, July 2009 RUTCOR Rutgers Center for Operations

R u t c o r Research R e p o r t Maximization of a Strongly Unimodal Multivariate Discrete Distribution Mine Subasi a Ersoy Subasi b András Prékopa c RRR 12-2009, July 2009 RUTCOR Rutgers Center for Operations

1 Review Session. 1.1 Lecture 2

1 Review Session Note: The following lists give an overview of the material that was covered in the lectures and sections. Your TF will go through these lists. If anything is unclear or you have questions

1 Review Session Note: The following lists give an overview of the material that was covered in the lectures and sections. Your TF will go through these lists. If anything is unclear or you have questions

4. Convex optimization problems

Convex Optimization Boyd & Vandenberghe 4. Convex optimization problems optimization problem in standard form convex optimization problems quasiconvex optimization linear optimization quadratic optimization

Convex Optimization Boyd & Vandenberghe 4. Convex optimization problems optimization problem in standard form convex optimization problems quasiconvex optimization linear optimization quadratic optimization

Optimization methods

Lecture notes 3 February 8, 016 1 Introduction Optimization methods In these notes we provide an overview of a selection of optimization methods. We focus on methods which rely on first-order information,

Lecture notes 3 February 8, 016 1 Introduction Optimization methods In these notes we provide an overview of a selection of optimization methods. We focus on methods which rely on first-order information,

STAT 7032 Probability. Wlodek Bryc

STAT 7032 Probability Wlodek Bryc Revised for Spring 2019 Printed: January 14, 2019 File: Grad-Prob-2019.TEX Department of Mathematical Sciences, University of Cincinnati, Cincinnati, OH 45221 E-mail address:

STAT 7032 Probability Wlodek Bryc Revised for Spring 2019 Printed: January 14, 2019 File: Grad-Prob-2019.TEX Department of Mathematical Sciences, University of Cincinnati, Cincinnati, OH 45221 E-mail address:

Coherent Risk Measures. Acceptance Sets. L = {X G : X(ω) < 0, ω Ω}.

< 0, ω Ω}.") So far in this course we have used several different mathematical expressions to quantify risk, without a deeper discussion of their properties. Coherent Risk Measures Lecture 11, Optimisation in Finance

So far in this course we have used several different mathematical expressions to quantify risk, without a deeper discussion of their properties. Coherent Risk Measures Lecture 11, Optimisation in Finance

Extreme Abridgment of Boyd and Vandenberghe s Convex Optimization

Extreme Abridgment of Boyd and Vandenberghe s Convex Optimization Compiled by David Rosenberg Abstract Boyd and Vandenberghe s Convex Optimization book is very well-written and a pleasure to read. The

Extreme Abridgment of Boyd and Vandenberghe s Convex Optimization Compiled by David Rosenberg Abstract Boyd and Vandenberghe s Convex Optimization book is very well-written and a pleasure to read. The

min f(x). (2.1) Objectives consisting of a smooth convex term plus a nonconvex regularization term;

. (2.1) Objectives consisting of a smooth convex term plus a nonconvex regularization term;") Chapter 2 Gradient Methods The gradient method forms the foundation of all of the schemes studied in this book. We will provide several complementary perspectives on this algorithm that highlight the many

Chapter 2 Gradient Methods The gradient method forms the foundation of all of the schemes studied in this book. We will provide several complementary perspectives on this algorithm that highlight the many

SOME HISTORY OF STOCHASTIC PROGRAMMING

SOME HISTORY OF STOCHASTIC PROGRAMMING Early 1950 s: in applications of Linear Programming unknown values of coefficients: demands, technological coefficients, yields, etc. QUOTATION Dantzig, Interfaces

SOME HISTORY OF STOCHASTIC PROGRAMMING Early 1950 s: in applications of Linear Programming unknown values of coefficients: demands, technological coefficients, yields, etc. QUOTATION Dantzig, Interfaces

Chapter 1: Linear Programming

Chapter 1: Linear Programming Math 368 c Copyright 2013 R Clark Robinson May 22, 2013 Chapter 1: Linear Programming 1 Max and Min For f : D R n R, f (D) = {f (x) : x D } is set of attainable values of

Chapter 1: Linear Programming Math 368 c Copyright 2013 R Clark Robinson May 22, 2013 Chapter 1: Linear Programming 1 Max and Min For f : D R n R, f (D) = {f (x) : x D } is set of attainable values of

Minimizing Cubic and Homogeneous Polynomials over Integers in the Plane

Minimizing Cubic and Homogeneous Polynomials over Integers in the Plane Alberto Del Pia Department of Industrial and Systems Engineering & Wisconsin Institutes for Discovery, University of Wisconsin-Madison

Minimizing Cubic and Homogeneous Polynomials over Integers in the Plane Alberto Del Pia Department of Industrial and Systems Engineering & Wisconsin Institutes for Discovery, University of Wisconsin-Madison

Modeling Uncertainty in Linear Programs: Stochastic and Robust Linear Programming

Modeling Uncertainty in Linear Programs: Stochastic and Robust Programming DGA PhD Student - PhD Thesis EDF-INRIA 10 November 2011 and motivations In real life, Linear Programs are uncertain for several

Modeling Uncertainty in Linear Programs: Stochastic and Robust Programming DGA PhD Student - PhD Thesis EDF-INRIA 10 November 2011 and motivations In real life, Linear Programs are uncertain for several

A Brief Review on Convex Optimization

A Brief Review on Convex Optimization 1 Convex set S R n is convex if x,y S, λ,µ 0, λ+µ = 1 λx+µy S geometrically: x,y S line segment through x,y S examples (one convex, two nonconvex sets): A Brief Review

A Brief Review on Convex Optimization 1 Convex set S R n is convex if x,y S, λ,µ 0, λ+µ = 1 λx+µy S geometrically: x,y S line segment through x,y S examples (one convex, two nonconvex sets): A Brief Review

Dynamic Macroeconomic Theory Notes. David L. Kelly. Department of Economics University of Miami Box Coral Gables, FL

Dynamic Macroeconomic Theory Notes David L. Kelly Department of Economics University of Miami Box 248126 Coral Gables, FL 33134 dkelly@miami.edu Current Version: Fall 2013/Spring 2013 I Introduction A

Dynamic Macroeconomic Theory Notes David L. Kelly Department of Economics University of Miami Box 248126 Coral Gables, FL 33134 dkelly@miami.edu Current Version: Fall 2013/Spring 2013 I Introduction A

FINANCIAL OPTIMIZATION

FINANCIAL OPTIMIZATION Lecture 1: General Principles and Analytic Optimization Philip H. Dybvig Washington University Saint Louis, Missouri Copyright c Philip H. Dybvig 2008 Choose x R N to minimize f(x)

FINANCIAL OPTIMIZATION Lecture 1: General Principles and Analytic Optimization Philip H. Dybvig Washington University Saint Louis, Missouri Copyright c Philip H. Dybvig 2008 Choose x R N to minimize f(x)

Convex Analysis and Economic Theory AY Elementary properties of convex functions

Division of the Humanities and Social Sciences Ec 181 KC Border Convex Analysis and Economic Theory AY 2018 2019 Topic 6: Convex functions I 6.1 Elementary properties of convex functions We may occasionally

Division of the Humanities and Social Sciences Ec 181 KC Border Convex Analysis and Economic Theory AY 2018 2019 Topic 6: Convex functions I 6.1 Elementary properties of convex functions We may occasionally

RISK AND RELIABILITY IN OPTIMIZATION UNDER UNCERTAINTY

RISK AND RELIABILITY IN OPTIMIZATION UNDER UNCERTAINTY Terry Rockafellar University of Washington, Seattle AMSI Optimise Melbourne, Australia 18 Jun 2018 Decisions in the Face of Uncertain Outcomes = especially

RISK AND RELIABILITY IN OPTIMIZATION UNDER UNCERTAINTY Terry Rockafellar University of Washington, Seattle AMSI Optimise Melbourne, Australia 18 Jun 2018 Decisions in the Face of Uncertain Outcomes = especially

Stochastic geometric optimization with joint probabilistic constraints

Stochastic geometric optimization with joint probabilistic constraints Jia Liu a,b, Abdel Lisser 1a, Zhiping Chen b a Laboratoire de Recherche en Informatique (LRI), Université Paris Sud - XI, Bât. 650,

Stochastic geometric optimization with joint probabilistic constraints Jia Liu a,b, Abdel Lisser 1a, Zhiping Chen b a Laboratoire de Recherche en Informatique (LRI), Université Paris Sud - XI, Bât. 650,

Linear Programming. Chapter Introduction

Chapter 3 Linear Programming Linear programs (LP) play an important role in the theory and practice of optimization problems. Many COPs can directly be formulated as LPs. Furthermore, LPs are invaluable

Chapter 3 Linear Programming Linear programs (LP) play an important role in the theory and practice of optimization problems. Many COPs can directly be formulated as LPs. Furthermore, LPs are invaluable

Deterministic Dynamic Programming

Deterministic Dynamic Programming 1 Value Function Consider the following optimal control problem in Mayer s form: V (t 0, x 0 ) = inf u U J(t 1, x(t 1 )) (1) subject to ẋ(t) = f(t, x(t), u(t)), x(t 0

Deterministic Dynamic Programming 1 Value Function Consider the following optimal control problem in Mayer s form: V (t 0, x 0 ) = inf u U J(t 1, x(t 1 )) (1) subject to ẋ(t) = f(t, x(t), u(t)), x(t 0

Analysis of Sparse Cutting-plane for Sparse IPs with Applications to Stochastic IPs

Analysis of Sparse Cutting-plane for Sparse IPs with Applications to Stochastic IPs Santanu S. Dey 1, Marco Molinaro 2, and Qianyi Wang 1 1 School of Industrial and Systems Engineering, Georgia Institute

Analysis of Sparse Cutting-plane for Sparse IPs with Applications to Stochastic IPs Santanu S. Dey 1, Marco Molinaro 2, and Qianyi Wang 1 1 School of Industrial and Systems Engineering, Georgia Institute

Quantifying Stochastic Model Errors via Robust Optimization

Quantifying Stochastic Model Errors via Robust Optimization IPAM Workshop on Uncertainty Quantification for Multiscale Stochastic Systems and Applications Jan 19, 2016 Henry Lam Industrial & Operations

Quantifying Stochastic Model Errors via Robust Optimization IPAM Workshop on Uncertainty Quantification for Multiscale Stochastic Systems and Applications Jan 19, 2016 Henry Lam Industrial & Operations

Solution Methods for Stochastic Programs

Solution Methods for Stochastic Programs Huseyin Topaloglu School of Operations Research and Information Engineering Cornell University ht88@cornell.edu August 14, 2010 1 Outline Cutting plane methods

Solution Methods for Stochastic Programs Huseyin Topaloglu School of Operations Research and Information Engineering Cornell University ht88@cornell.edu August 14, 2010 1 Outline Cutting plane methods

Handout 6: Some Applications of Conic Linear Programming

ENGG 550: Foundations of Optimization 08 9 First Term Handout 6: Some Applications of Conic Linear Programming Instructor: Anthony Man Cho So November, 08 Introduction Conic linear programming CLP, and

ENGG 550: Foundations of Optimization 08 9 First Term Handout 6: Some Applications of Conic Linear Programming Instructor: Anthony Man Cho So November, 08 Introduction Conic linear programming CLP, and

On the Power of Robust Solutions in Two-Stage Stochastic and Adaptive Optimization Problems

MATHEMATICS OF OPERATIONS RESEARCH Vol. 35, No., May 010, pp. 84 305 issn 0364-765X eissn 156-5471 10 350 084 informs doi 10.187/moor.1090.0440 010 INFORMS On the Power of Robust Solutions in Two-Stage

MATHEMATICS OF OPERATIONS RESEARCH Vol. 35, No., May 010, pp. 84 305 issn 0364-765X eissn 156-5471 10 350 084 informs doi 10.187/moor.1090.0440 010 INFORMS On the Power of Robust Solutions in Two-Stage

The Comparison of Stochastic and Deterministic DEA Models

The International Scientific Conference INPROFORUM 2015, November 5-6, 2015, České Budějovice, 140-145, ISBN 978-80-7394-536-7. The Comparison of Stochastic and Deterministic DEA Models Michal Houda, Jana

The International Scientific Conference INPROFORUM 2015, November 5-6, 2015, České Budějovice, 140-145, ISBN 978-80-7394-536-7. The Comparison of Stochastic and Deterministic DEA Models Michal Houda, Jana

Lecture 1. Stochastic Optimization: Introduction. January 8, 2018

Lecture 1 Stochastic Optimization: Introduction January 8, 2018 Optimization Concerned with mininmization/maximization of mathematical functions Often subject to constraints Euler (1707-1783): Nothing

Lecture 1 Stochastic Optimization: Introduction January 8, 2018 Optimization Concerned with mininmization/maximization of mathematical functions Often subject to constraints Euler (1707-1783): Nothing

PROGRAMMING UNDER PROBABILISTIC CONSTRAINTS WITH A RANDOM TECHNOLOGY MATRIX

Math. Operationsforsch. u. Statist. 5 974, Heft 2. pp. 09 6. PROGRAMMING UNDER PROBABILISTIC CONSTRAINTS WITH A RANDOM TECHNOLOGY MATRIX András Prékopa Technological University of Budapest and Computer

Math. Operationsforsch. u. Statist. 5 974, Heft 2. pp. 09 6. PROGRAMMING UNDER PROBABILISTIC CONSTRAINTS WITH A RANDOM TECHNOLOGY MATRIX András Prékopa Technological University of Budapest and Computer

Ambiguity in portfolio optimization

May/June 2006 Introduction: Risk and Ambiguity Frank Knight Risk, Uncertainty and Profit (1920) Risk: the decision-maker can assign mathematical probabilities to random phenomena Uncertainty: randomness

May/June 2006 Introduction: Risk and Ambiguity Frank Knight Risk, Uncertainty and Profit (1920) Risk: the decision-maker can assign mathematical probabilities to random phenomena Uncertainty: randomness