Arima Fit to Nigerian Unemployment Data

|

|

|

- Scot Ramsey

- 6 years ago

- Views:

Transcription

1 2012, TexRoad Publicaion ISSN Journal of Basic and Applied Scienific Research Arima Fi o Nigerian Unemploymen Daa Ee Harrison ETUK 1, Barholomew UCHENDU 2, Uyodhu VICTOR-EDEMA 3 1 Deparmen of Mahemaics/Compuer Science, Rivers Sae Universiy of Science and Technology, Nigeria 2 Deparmen of Mahemaics/Saisics, Federal Polyechnic, Nekede, Imo Sae, Nigeria 3 Deparmen of Mahemaics/Saisics, Rivers Sae Universiy of Educaion, Nigeria ABSTRACT Nigerian unemploymen daa is modelled by Box-Jenkins approach and he use of auomaic model selecion crieria Akaike Informaion crierion (AIC) and Schwarz Informaion Crierion (SIC). I is inferred ha he mos adequae model is auoregressive inegraed moving average of orders 1, 2 and 1(ARIMA(1,2,). Forecass are obained on he basis of he model. KEY WORDS: Unemploymen daa, ARIMA modelling, AIC, SIC, Nigeria. INTRODUCTION A ime series is defined as a se of daa colleced sequenially in ime. I has he propery ha neighbouring values are correlaed. This endency is called auocorrelaion. A ime series is said o be saionary if i has a consan mean and variance. Moreover he auocorrelaion is a funcion of he lag separaing he correlaed values called he auocorrelaion funcion (ACF). A saionary ime series { } is said o follow an auoregressive moving average model of orders p and q (designaed ARMA(p,q) ) if i saisfies he following difference equaion or p p q q ( (B) = (B) (2) where { } is a sequence of random variables wih zero mean and consan variance, called a whie noise process, and he i s and j s consans; (B) = B + 2 B p B p and (B) = B + 2 B q B q and B is he backward shif operaor defined by B k = -k. If p=0, model ( becomes a moving average model of order q (designaed MA(q)). If, however, q=0 i becomes an auoregressive process of order p (designaed AR(p)). An AR(p) model of order p may be defined as a model whereby a curren value of he ime series depends on he immediae pas p values: -1, -2,..., -p. On he oher hand an MA(q) model of order q is such ha he curren value is a linear combinaion of immediae pas values of he whie noise process: 1, 2,..., q. Apar from saionariy, inveribiliy is anoher imporan requiremen for a ime series. I refers o he propery whereby he covariance srucure of he eries is unique [7]. Moreover i allows for meaningful associaion of curren evens wih he pas hisory of he series [2]. An AR(p) model may be more specifically wrien as + p1-1 + p pp -p = Then he sequence of he las coefficiens{ ii } is called he parial auocorrelaion funcion(pacf) of { }. The ACF of an MA(q) model cus off afer lag q whereas ha of an AR(p) model is a combinaion of sinusoidals dying off slowly. On he oher hand he PACF of an MA(q) model dies off slowly whereas ha of an AR(p) model cus off afer lag p. AR and MA models are known o have some dualiy properies. These include: 1. A finie order AR model is equivalen o an infinie order MA model. 2. A finie order MA model is equivalen o an infinie order AR model. 3. The ACF of an AR model exhibis he same behaviour as he PACF of an MA model. 4. The PACF of an AR model exhibis he same behaviour as he ACF of an MA model. 5. An AR model is always inverible bu is saionary if (B) = 0 has zeros ouside he uni circle. 6. An MA model is always saionary bu is inverible if (B) = 0 has zeros ouside he uni circle. Parameric parsimony consideraion in model building enails preference for he mixed ARMA fi o eiher he pure AR or he pure MA fi. Saionariy and inveribiliy condiions for model ( or (2) are ha he equaions (B) = 0 and (B) = 0 should have roos ouside he uni circle respecively. *Corresponding Auhor: Ee Harrison ETUK, Deparmen of Mahemaics/Compuer Science, Rivers Sae Universiy of Science and Technology, Nigeria. eeuk@yahoo.com 5964

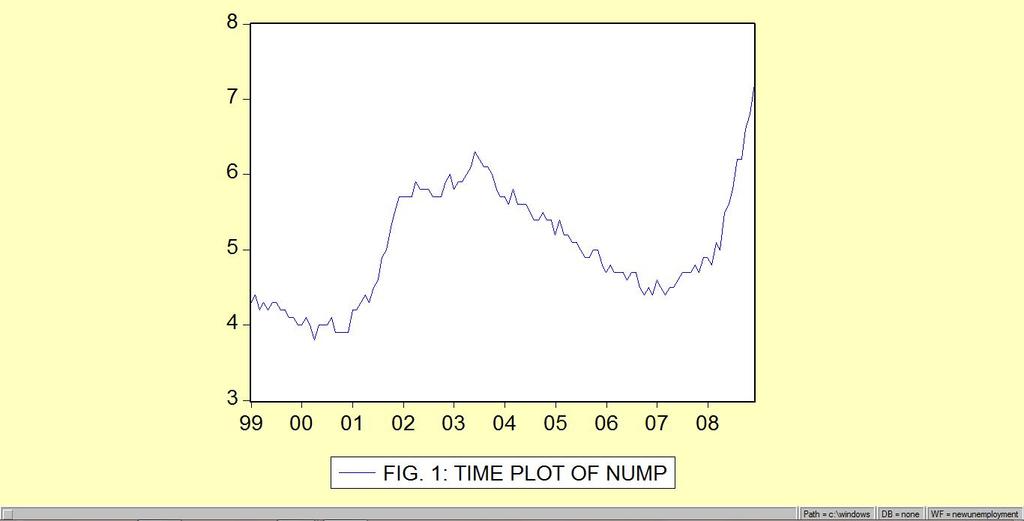

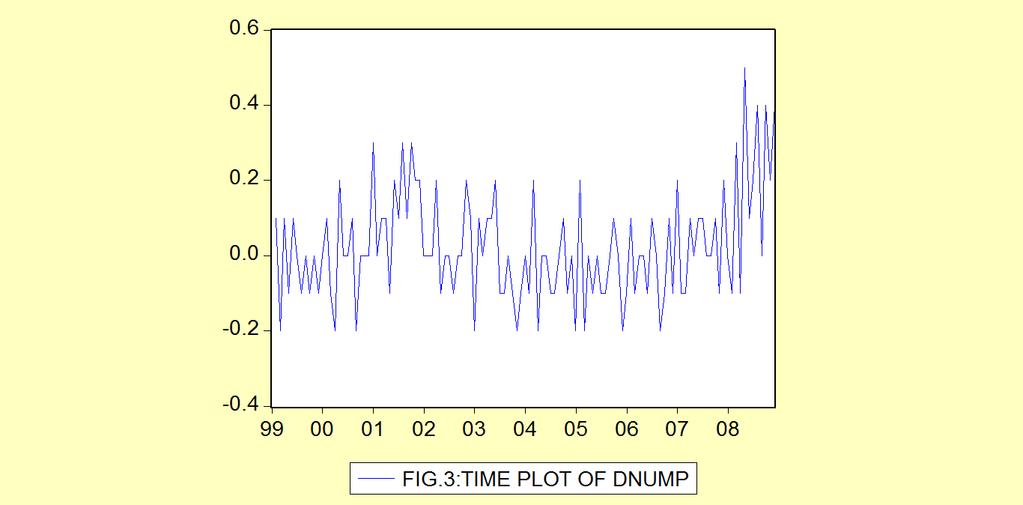

2 ETUK e al., 2012 Ofen, in pracice, a ime series is non-saionary. Box and Jenkins [2] proposed ha differencing of an appropriae daa could render a non-saionary series { } saionary. Le degree of differencing necessary for saionariy be d. Such a series { } may be modelled as (1 + α B ) d = (B) (3) where = 1 B and in which case (B) = (1 + α B ) = 0 shall have uni roos d imes. Then differencing o degree d renders he series saionary. The model (3) is said o be an auoregressive inegraed moving average model of orders p, d and q and designaed ARIMA(p, d, q). The purpose of his paper is o fi an ARIMA model o monhly unemploymen rae daa of Nigeria. MATERIALS AND METHODS The daa for his work are monhly unemploymen rae daa from 1999 o 2008 obainable from quarerly absracs of he Cenral Bank of Nigeria. Unemploymen rae in his conex is he percenage of he workforce ha are wihou jobs. Deerminaion of he differencing order d: Preliminary analysis of ime series involves he ime-plo and he correlogram. A saionary ime series exhibis no rend and he degree of variabiliy is invarian wih ime. In addiion he covariance is a funcion of he ime lag. The ime plo of a saionary ime series shows no change in he mean level as well as he variance over ime. The auocorrelaion funcion should decay fas o zero. Tes for saionariy: The ACF of a non-saionary ime series sars high and declines slowly. Moreover o es for saionariy we shall be using he Augmened Dickey-Fuller (ADF) es. This involves esing for b=1 agains b < 1 in = a + b The sofware Eviews 3.1 ha we shall use has faciliy for he ADF es also. Deerminaion of he orders p and q: As already menioned above, an AR(p) model has a PACF ha runcaes a lag p and an MA(q)) has an ACF ha runcaes a lag q. In pracice ±2 n are he nonsignificance limis for boh funcions. We shall explore he range of models ARMA(a,b), 0 a p, 0 b q for an opimum one. To do his we shall use he auomaic model deerminaion crieria AIC and SIC ( e.g. [1], [3], [4] and[ 8]) defined by: AIC p d q n ~ 2 ( ) ln p d q 2( p d q) SIC( p d q) nln ~ 2 ( p d q)ln( n) / n p d q where σ is he maximum likelihood esimae of he residual variance when he model has k parameers.the opimum model corresponds o he minimum of he crieria wihin he explored range. Model Esimaion: The involvemen of he whie noise erms in an ARIMA model enails a nonlinear ieraive process in he esimaion of he parameers, i s and j s. An opimizaion crierion like leas error of sum of squares, maximum likelihood or maximum enropy is used. An iniial esimae is usually used. Each ieraion is expeced o be an improvemen of he las one unil he esimae converges o an opimal one. However,for pure AR and pure MA models linear opimizaion echniques exis (See for example [2],[6]). There are aemps o adop linear mehods o esimae ARMA models (See for example, [3], [4], [5]). Diagnosic Checking: The model ha is fied o he daa should be esed for goodness-of-fi. The auomaic order deerminaion crieria AIC and SIC are hemselves diagnosic checking ools. Furher checking can be done by he analysis of he residuals of he model. If he model is correc, he residuals would be uncorrelaed and would follow a normal disribuion wih mean zero and consan variance. RESULTS AND DISCUSSION The ime plo of he original series NUMP in Fig.1and he correlogram of Figure 2 clearly depic nonsaionariy. Differencing he series once yields a sill non-saionary process, DNUMP; he ADF es of Table 1 confirms he non-saionary naure. This necessiaed second order differencing. The ADF es of Table 2 aess o he saionary naure of he second differences SNUMP. We noe ha in his able he dependen variable is he hird difference TNUMP of he original series. From fig. 4, he ACF cus off a lag 5 and he PACF a lag 4. Exploring he range of models {ARMA(p,q): 0 p 4, 0 q 5}for he opimal on he basis of AIC and SIC yields an ARMA(1, as summarized in Table

3 FIG. 2. CORRELOGRAM OF NUMP 5966

4 ETUK e al., 2012 TABLE 1: Augmened Dickey Fuller Tes on DNUMP ADF Tes Saisic % Criical Value* % Criical Value % Criical Value *MacKinnon criical values for rejecion of hypohesis of a uni roo. Augmened Dickey-Fuller Tes Equaion Dependen Variable: SDNUMP Mehod: Leas Squares Dae: 12/24/11 Time: 17:16 Sample(adjused): 1999: :12 Included observaions: 114 afer adjusing endpoins Variable Coefficien Sd. Error -Saisic Prob. D((-) D((-,2) D((-2),2) D((-3),2) D((-4),2) C R-squared Mean dependen var Adjused R-squared S.D. dependen var S.E. of regression Akaike info crierion Sum squared resid Schwarz crierion Log likelihood F-saisic Durbin-Wason sa Prob(F-saisic) TABLE 2: Augmened Dickey Fuller Tes on SDNUMP ADF Tes Saisic % Criical Value* % Criical Value % Criical Value *MacKinnon criical values for rejecion of hypohesis of a uni roo. Augmened Dickey-Fuller Tes Equaion Dependen Variable: TNUMP Mehod: Leas Squares Dae: 12/24/11 Time: 17:10 Sample(adjused): 1999: :12 Included observaions: 113 afer adjusing endpoins Variable Coefficien Sd. Error -Saisic Prob. D((-,2) D((-,3) D((-2),3) D((-3),3) D((-4),3) C R-squared Mean dependen var Adjused R-squared S.D. dependen var S.E. of regression Akaike info crierion Sum squared resid Schwarz crierion Log likelihood F-saisic Durbin-Wason sa Prob(F-saisic) FIG. 4: CORRELOGRAM OF SNUMP 5967

5 Table 3. Comparison of models wihin he range of exploraion using AIC and SIC p q AIC SIC TABLE 4: Model Esimaion Dependen Variable: SDNUMP Mehod: Leas Squares Dae: 12/24/11 Time: 18:32 Sample(adjused): 1999: :12 Included observaions: 117 afer adjusing endpoins Convergence achieved afer 6 ieraions Backcas: 1999:03 Variable Coefficien Sd. Error -Saisic Prob. AR( MA( R-squared Mean dependen var Adjused R-squared S.D. dependen var S.E. of regression Akaike info crierion Sum squared resid Schwarz crierion Log likelihood F-saisic Durbin-Wason sa Prob(F-saisic) Invered AR Roos -.39 Invered MA Roos.72 The chosen model as summarized in Table 4 is ARIMA(1, 2, and is given by SDNUMP = SDNUMP ( ) ( ) Clearly non-linear echniques used by Eviews 3.1 involved an ieraive process ha converged afer six ieraions. We observe ha he coefficiens are boh highly significan, each being more han wice is sandard error. The roos of (B) = 0 and (B) = 0 are and 1.39, boh ouside he uni circle indicaing saionariy and inveribiliy respecively. Besides he residual plo of Fig. 5 confirms ha he residuals follow he normal 5968

1 1 Tha is, ( 1 2) 1 2 1 3 1 1 A ime +k, he model may be wrien as k ( 1 2) k 1 k 2 1 k 3 1 k 1 Taking condiional expecaions a ime, we have ˆ ( ( 1")

6 ETUK e al., 2012 disribuion wih zero (acually 0.0 mean. The kurosis is 2.8 which compares favourably wih he normal disribuion sandard of Forecasing: An ARIMA(1, 2, model may be wrien as 2 This ranslaes ino FIG. 5. HISTOGRAM OF THE MODEL RESIDUALS 1 2 1( ) 1 1 Tha is, ( 1 2) A ime +k, he model may be wrien as k ( 1 2) k 1 k 2 1 k 3 1 k 1 Taking condiional expecaions a ime, we have ˆ ( ( 1 2) ˆ ˆ (2) ( 1 2) ( 1 1 ˆ (3) ( 1 2) ˆ (2) ˆ ( 1 ˆ ( k) ( 2) ˆ ( k ) ˆ ( k 2) ˆ ( k 3), ˆ k where ( k) is he k-sep ahead forecas. Tha is he forecas of +k. TABLE 6. Forecass Ocober 2008 November 2008 December 2008 January 2009 February 2009 March 2009 Residuals SNUMP DNUMP NUMP

7 Conclusion We have successfully fied an ARIMA(1, 2, model o Nigerian monhly unemploymen daa. This means ha he second differences SNUMP follow an ARMA(1, model. Is adequacy has been esablished and on is basis we have made forecass. REFERENCES 1. Akaike, H. (1970). Saisical Predicor Idenificaion. Annals of he Insiue of Saisical Mahemaics, Volume 22: pp Box, G. E. P. And Jenkins, G. M. (1976). Time Series Analysis, Forecasing and Conrol, Holden-Day, San Francisco. 3. Euk, E. H. (1987). On he Selecion of Auoregressive Moving Average Models. An unpublished Ph. D. Thesis, Deparmen of Saisics, Universiy of Ibadan, Nigeria. 4. Euk, E. H. (1988). On Auoregressive Model Idenificaion. Journal of Official Saisics, Volume 4, No. 2; pp Euk, E. H. (1996). An Auoregressive Inegraed Moving Average(ARIMA) Simulaion Model: A Case Sudy. Discovery and Innovaion, Volume 10, Nos 1 & 2:pp Oyeunji, O. B. (1985). Inverse Auocorrelaions and Moving Average Time Series Modelling. Journal of Official Saisics, Volume 1: pp Priesley, M. B. (198. Specral Analysis and Time Sreies. Academic Press, London. 8. Schwarz, G. (1978). Esimaing he dimension of a model. Annals of Saisics, Volume 6: pp

Box-Jenkins Modelling of Nigerian Stock Prices Data

Greener Journal of Science Engineering and Technological Research ISSN: 76-7835 Vol. (), pp. 03-038, Sepember 0. Research Aricle Box-Jenkins Modelling of Nigerian Sock Prices Daa Ee Harrison Euk*, Barholomew

Greener Journal of Science Engineering and Technological Research ISSN: 76-7835 Vol. (), pp. 03-038, Sepember 0. Research Aricle Box-Jenkins Modelling of Nigerian Sock Prices Daa Ee Harrison Euk*, Barholomew

Licenciatura de ADE y Licenciatura conjunta Derecho y ADE. Hoja de ejercicios 2 PARTE A

Licenciaura de ADE y Licenciaura conjuna Derecho y ADE Hoja de ejercicios PARTE A 1. Consider he following models Δy = 0.8 + ε (1 + 0.8L) Δ 1 y = ε where ε and ε are independen whie noise processes. In

Licenciaura de ADE y Licenciaura conjuna Derecho y ADE Hoja de ejercicios PARTE A 1. Consider he following models Δy = 0.8 + ε (1 + 0.8L) Δ 1 y = ε where ε and ε are independen whie noise processes. In

Stationary Time Series

3-Jul-3 Time Series Analysis Assoc. Prof. Dr. Sevap Kesel July 03 Saionary Time Series Sricly saionary process: If he oin dis. of is he same as he oin dis. of ( X,... X n) ( X h,... X nh) Weakly Saionary

3-Jul-3 Time Series Analysis Assoc. Prof. Dr. Sevap Kesel July 03 Saionary Time Series Sricly saionary process: If he oin dis. of is he same as he oin dis. of ( X,... X n) ( X h,... X nh) Weakly Saionary

Methodology. -ratios are biased and that the appropriate critical values have to be increased by an amount. that depends on the sample size.

Mehodology. Uni Roo Tess A ime series is inegraed when i has a mean revering propery and a finie variance. I is only emporarily ou of equilibrium and is called saionary in I(0). However a ime series ha

Mehodology. Uni Roo Tess A ime series is inegraed when i has a mean revering propery and a finie variance. I is only emporarily ou of equilibrium and is called saionary in I(0). However a ime series ha

Vectorautoregressive Model and Cointegration Analysis. Time Series Analysis Dr. Sevtap Kestel 1

Vecorauoregressive Model and Coinegraion Analysis Par V Time Series Analysis Dr. Sevap Kesel 1 Vecorauoregression Vecor auoregression (VAR) is an economeric model used o capure he evoluion and he inerdependencies

Vecorauoregressive Model and Coinegraion Analysis Par V Time Series Analysis Dr. Sevap Kesel 1 Vecorauoregression Vecor auoregression (VAR) is an economeric model used o capure he evoluion and he inerdependencies

- The whole joint distribution is independent of the date at which it is measured and depends only on the lag.

Saionary Processes Sricly saionary - The whole join disribuion is indeenden of he dae a which i is measured and deends only on he lag. - E y ) is a finie consan. ( - V y ) is a finie consan. ( ( y, y s

Saionary Processes Sricly saionary - The whole join disribuion is indeenden of he dae a which i is measured and deends only on he lag. - E y ) is a finie consan. ( - V y ) is a finie consan. ( ( y, y s

Section 4 NABE ASTEF 232

Secion 4 NABE ASTEF 3 APPLIED ECONOMETRICS: TIME-SERIES ANALYSIS 33 Inroducion and Review The Naure of Economic Modeling Judgemen calls unavoidable Economerics an ar Componens of Applied Economerics Specificaion

Secion 4 NABE ASTEF 3 APPLIED ECONOMETRICS: TIME-SERIES ANALYSIS 33 Inroducion and Review The Naure of Economic Modeling Judgemen calls unavoidable Economerics an ar Componens of Applied Economerics Specificaion

Nonstationarity-Integrated Models. Time Series Analysis Dr. Sevtap Kestel 1

Nonsaionariy-Inegraed Models Time Series Analysis Dr. Sevap Kesel 1 Diagnosic Checking Residual Analysis: Whie noise. P-P or Q-Q plos of he residuals follow a normal disribuion, he series is called a Gaussian

Nonsaionariy-Inegraed Models Time Series Analysis Dr. Sevap Kesel 1 Diagnosic Checking Residual Analysis: Whie noise. P-P or Q-Q plos of he residuals follow a normal disribuion, he series is called a Gaussian

Cointegration and Implications for Forecasting

Coinegraion and Implicaions for Forecasing Two examples (A) Y Y 1 1 1 2 (B) Y 0.3 0.9 1 1 2 Example B: Coinegraion Y and coinegraed wih coinegraing vecor [1, 0.9] because Y 0.9 0.3 is a saionary process

Coinegraion and Implicaions for Forecasing Two examples (A) Y Y 1 1 1 2 (B) Y 0.3 0.9 1 1 2 Example B: Coinegraion Y and coinegraed wih coinegraing vecor [1, 0.9] because Y 0.9 0.3 is a saionary process

Modeling and Forecasting Volatility Autoregressive Conditional Heteroskedasticity Models. Economic Forecasting Anthony Tay Slide 1

Modeling and Forecasing Volailiy Auoregressive Condiional Heeroskedasiciy Models Anhony Tay Slide 1 smpl @all line(m) sii dl_sii S TII D L _ S TII 4,000. 3,000.1.0,000 -.1 1,000 -. 0 86 88 90 9 94 96 98

Modeling and Forecasing Volailiy Auoregressive Condiional Heeroskedasiciy Models Anhony Tay Slide 1 smpl @all line(m) sii dl_sii S TII D L _ S TII 4,000. 3,000.1.0,000 -.1 1,000 -. 0 86 88 90 9 94 96 98

14 Autoregressive Moving Average Models

14 Auoregressive Moving Average Models In his chaper an imporan parameric family of saionary ime series is inroduced, he family of he auoregressive moving average, or ARMA, processes. For a large class

14 Auoregressive Moving Average Models In his chaper an imporan parameric family of saionary ime series is inroduced, he family of he auoregressive moving average, or ARMA, processes. For a large class

Financial Econometrics Jeffrey R. Russell Midterm Winter 2009 SOLUTIONS

Name SOLUTIONS Financial Economerics Jeffrey R. Russell Miderm Winer 009 SOLUTIONS You have 80 minues o complee he exam. Use can use a calculaor and noes. Try o fi all your work in he space provided. If

Name SOLUTIONS Financial Economerics Jeffrey R. Russell Miderm Winer 009 SOLUTIONS You have 80 minues o complee he exam. Use can use a calculaor and noes. Try o fi all your work in he space provided. If

OBJECTIVES OF TIME SERIES ANALYSIS

OBJECTIVES OF TIME SERIES ANALYSIS Undersanding he dynamic or imedependen srucure of he observaions of a single series (univariae analysis) Forecasing of fuure observaions Asceraining he leading, lagging

OBJECTIVES OF TIME SERIES ANALYSIS Undersanding he dynamic or imedependen srucure of he observaions of a single series (univariae analysis) Forecasing of fuure observaions Asceraining he leading, lagging

Time series Decomposition method

Time series Decomposiion mehod A ime series is described using a mulifacor model such as = f (rend, cyclical, seasonal, error) = f (T, C, S, e) Long- Iner-mediaed Seasonal Irregular erm erm effec, effec,

Time series Decomposiion mehod A ime series is described using a mulifacor model such as = f (rend, cyclical, seasonal, error) = f (T, C, S, e) Long- Iner-mediaed Seasonal Irregular erm erm effec, effec,

Imo Udo Moffat Department of Mathematics/Statistics, University of Uyo, Nigeria

Inernaional Journals of Advanced Research in Compuer Science and Sofware Engineering ISSN: 2277-128 (Volume-7, Issue-8) a Research Aricle Augus 2017 Applicaion of Inerruped Time Series Modelling o Prime

Inernaional Journals of Advanced Research in Compuer Science and Sofware Engineering ISSN: 2277-128 (Volume-7, Issue-8) a Research Aricle Augus 2017 Applicaion of Inerruped Time Series Modelling o Prime

STAD57 Time Series Analysis. Lecture 17

STAD57 Time Series Analysis Lecure 17 1 Exponenially Weighed Moving Average Model Consider ARIMA(0,1,1), or IMA(1,1), model 1 s order differences follow MA(1) X X W W Y X X W W 1 1 1 1 Very common model

STAD57 Time Series Analysis Lecure 17 1 Exponenially Weighed Moving Average Model Consider ARIMA(0,1,1), or IMA(1,1), model 1 s order differences follow MA(1) X X W W Y X X W W 1 1 1 1 Very common model

STAD57 Time Series Analysis. Lecture 17

STAD57 Time Series Analysis Lecure 17 1 Exponenially Weighed Moving Average Model Consider ARIMA(0,1,1), or IMA(1,1), model 1 s order differences follow MA(1) X X W W Y X X W W 1 1 1 1 Very common model

STAD57 Time Series Analysis Lecure 17 1 Exponenially Weighed Moving Average Model Consider ARIMA(0,1,1), or IMA(1,1), model 1 s order differences follow MA(1) X X W W Y X X W W 1 1 1 1 Very common model

R t. C t P t. + u t. C t = αp t + βr t + v t. + β + w t

Exercise 7 C P = α + β R P + u C = αp + βr + v (a) (b) C R = α P R + β + w (c) Assumpions abou he disurbances u, v, w : Classical assumions on he disurbance of one of he equaions, eg. on (b): E(v v s P,

Exercise 7 C P = α + β R P + u C = αp + βr + v (a) (b) C R = α P R + β + w (c) Assumpions abou he disurbances u, v, w : Classical assumions on he disurbance of one of he equaions, eg. on (b): E(v v s P,

A Hybrid Model for Improving. Malaysian Gold Forecast Accuracy

In. Journal of Mah. Analysis, Vol. 8, 2014, no. 28, 1377-1387 HIKARI Ld, www.m-hikari.com hp://dx.doi.org/10.12988/ijma.2014.45139 A Hybrid Model for Improving Malaysian Gold Forecas Accuracy Maizah Hura

In. Journal of Mah. Analysis, Vol. 8, 2014, no. 28, 1377-1387 HIKARI Ld, www.m-hikari.com hp://dx.doi.org/10.12988/ijma.2014.45139 A Hybrid Model for Improving Malaysian Gold Forecas Accuracy Maizah Hura

Chapter 3, Part IV: The Box-Jenkins Approach to Model Building

Chaper 3, Par IV: The Box-Jenkins Approach o Model Building The ARMA models have been found o be quie useful for describing saionary nonseasonal ime series. A parial explanaion for his fac is provided

Chaper 3, Par IV: The Box-Jenkins Approach o Model Building The ARMA models have been found o be quie useful for describing saionary nonseasonal ime series. A parial explanaion for his fac is provided

Forecast of Adult Literacy in Sudan

Journal for Sudies in Managemen and Planning Available a hp://inernaionaljournalofresearch.org/index.php/jsmap e-issn: 2395-463 Volume 1 Issue 2 March 215 Forecas of Adul Lieracy in Sudan Dr. Elfarazdag

Journal for Sudies in Managemen and Planning Available a hp://inernaionaljournalofresearch.org/index.php/jsmap e-issn: 2395-463 Volume 1 Issue 2 March 215 Forecas of Adul Lieracy in Sudan Dr. Elfarazdag

Wisconsin Unemployment Rate Forecast Revisited

Wisconsin Unemploymen Rae Forecas Revisied Forecas in Lecure Wisconsin unemploymen November 06 was 4.% Forecass Poin Forecas 50% Inerval 80% Inerval Forecas Forecas December 06 4.0% (4.0%, 4.0%) (3.95%,

Wisconsin Unemploymen Rae Forecas Revisied Forecas in Lecure Wisconsin unemploymen November 06 was 4.% Forecass Poin Forecas 50% Inerval 80% Inerval Forecas Forecas December 06 4.0% (4.0%, 4.0%) (3.95%,

Chapter 16. Regression with Time Series Data

Chaper 16 Regression wih Time Series Daa The analysis of ime series daa is of vial ineres o many groups, such as macroeconomiss sudying he behavior of naional and inernaional economies, finance economiss

Chaper 16 Regression wih Time Series Daa The analysis of ime series daa is of vial ineres o many groups, such as macroeconomiss sudying he behavior of naional and inernaional economies, finance economiss

Forecasting optimally

I) ile: Forecas Evaluaion II) Conens: Evaluaing forecass, properies of opimal forecass, esing properies of opimal forecass, saisical comparison of forecas accuracy III) Documenaion: - Diebold, Francis

I) ile: Forecas Evaluaion II) Conens: Evaluaing forecass, properies of opimal forecass, esing properies of opimal forecass, saisical comparison of forecas accuracy III) Documenaion: - Diebold, Francis

Lecture 5. Time series: ECM. Bernardina Algieri Department Economics, Statistics and Finance

Lecure 5 Time series: ECM Bernardina Algieri Deparmen Economics, Saisics and Finance Conens Time Series Modelling Coinegraion Error Correcion Model Two Seps, Engle-Granger procedure Error Correcion Model

Lecure 5 Time series: ECM Bernardina Algieri Deparmen Economics, Saisics and Finance Conens Time Series Modelling Coinegraion Error Correcion Model Two Seps, Engle-Granger procedure Error Correcion Model

Chapter 5. Heterocedastic Models. Introduction to time series (2008) 1

1") Chaper 5 Heerocedasic Models Inroducion o ime series (2008) 1 Chaper 5. Conens. 5.1. The ARCH model. 5.2. The GARCH model. 5.3. The exponenial GARCH model. 5.4. The CHARMA model. 5.5. Random coefficien

Chaper 5 Heerocedasic Models Inroducion o ime series (2008) 1 Chaper 5. Conens. 5.1. The ARCH model. 5.2. The GARCH model. 5.3. The exponenial GARCH model. 5.4. The CHARMA model. 5.5. Random coefficien

12: AUTOREGRESSIVE AND MOVING AVERAGE PROCESSES IN DISCRETE TIME. Σ j =

1: AUTOREGRESSIVE AND MOVING AVERAGE PROCESSES IN DISCRETE TIME Moving Averages Recall ha a whie noise process is a series { } = having variance σ. The whie noise process has specral densiy f (λ) = of

1: AUTOREGRESSIVE AND MOVING AVERAGE PROCESSES IN DISCRETE TIME Moving Averages Recall ha a whie noise process is a series { } = having variance σ. The whie noise process has specral densiy f (λ) = of

A Forecasting Model for Monthly Nigeria Treasury Bill Rates by Box-Jenkins Techniques

Inernaional Journal of Life Science and Engineering Vol. 1, No. 1, 2015, pp. 20-25 hp://www.publicscienceframework.org/journal/ijlse A Forecasing Model for Monhly Nigeria Treasury Bill Raes by Box-Jenkins

Inernaional Journal of Life Science and Engineering Vol. 1, No. 1, 2015, pp. 20-25 hp://www.publicscienceframework.org/journal/ijlse A Forecasing Model for Monhly Nigeria Treasury Bill Raes by Box-Jenkins

Econ Autocorrelation. Sanjaya DeSilva

Econ 39 - Auocorrelaion Sanjaya DeSilva Ocober 3, 008 1 Definiion Auocorrelaion (or serial correlaion) occurs when he error erm of one observaion is correlaed wih he error erm of any oher observaion. This

Econ 39 - Auocorrelaion Sanjaya DeSilva Ocober 3, 008 1 Definiion Auocorrelaion (or serial correlaion) occurs when he error erm of one observaion is correlaed wih he error erm of any oher observaion. This

Modeling Rainfall in Dhaka Division of Bangladesh Using Time Series Analysis.

Journal of Mahemaical Modelling and Applicaion 01, Vol. 1, No.5, 67-73 ISSN: 178-43 67 Modeling Rainfall in Dhaka Division of Bangladesh Using Time Series Analysis. Md. Mahsin Insiue of Saisical Research

Journal of Mahemaical Modelling and Applicaion 01, Vol. 1, No.5, 67-73 ISSN: 178-43 67 Modeling Rainfall in Dhaka Division of Bangladesh Using Time Series Analysis. Md. Mahsin Insiue of Saisical Research

Diebold, Chapter 7. Francis X. Diebold, Elements of Forecasting, 4th Edition (Mason, Ohio: Cengage Learning, 2006). Chapter 7. Characterizing Cycles

. Chapter 7. Characterizing Cycles") Diebold, Chaper 7 Francis X. Diebold, Elemens of Forecasing, 4h Ediion (Mason, Ohio: Cengage Learning, 006). Chaper 7. Characerizing Cycles Afer compleing his reading you should be able o: Define covariance

Diebold, Chaper 7 Francis X. Diebold, Elemens of Forecasing, 4h Ediion (Mason, Ohio: Cengage Learning, 006). Chaper 7. Characerizing Cycles Afer compleing his reading you should be able o: Define covariance

ST4064. Time Series Analysis. Lecture notes

ST4064 Time Series Analysis ST4064 Time Series Analysis Lecure noes ST4064 Time Series Analysis Ouline I II Inroducion o ime series analysis Saionariy and ARMA modelling. Saionariy a. Definiions b. Sric

ST4064 Time Series Analysis ST4064 Time Series Analysis Lecure noes ST4064 Time Series Analysis Ouline I II Inroducion o ime series analysis Saionariy and ARMA modelling. Saionariy a. Definiions b. Sric

Chapter 15. Time Series: Descriptive Analyses, Models, and Forecasting

Chaper 15 Time Series: Descripive Analyses, Models, and Forecasing Descripive Analysis: Index Numbers Index Number a number ha measures he change in a variable over ime relaive o he value of he variable

Chaper 15 Time Series: Descripive Analyses, Models, and Forecasing Descripive Analysis: Index Numbers Index Number a number ha measures he change in a variable over ime relaive o he value of he variable

Regression with Time Series Data

Regression wih Time Series Daa y = β 0 + β 1 x 1 +...+ β k x k + u Serial Correlaion and Heeroskedasiciy Time Series - Serial Correlaion and Heeroskedasiciy 1 Serially Correlaed Errors: Consequences Wih

Regression wih Time Series Daa y = β 0 + β 1 x 1 +...+ β k x k + u Serial Correlaion and Heeroskedasiciy Time Series - Serial Correlaion and Heeroskedasiciy 1 Serially Correlaed Errors: Consequences Wih

Smoothing. Backward smoother: At any give T, replace the observation yt by a combination of observations at & before T

Smoohing Consan process Separae signal & noise Smooh he daa: Backward smooher: A an give, replace he observaion b a combinaion of observaions a & before Simple smooher : replace he curren observaion wih

Smoohing Consan process Separae signal & noise Smooh he daa: Backward smooher: A an give, replace he observaion b a combinaion of observaions a & before Simple smooher : replace he curren observaion wih

TÁMOP /2/A/KMR

ECONOMIC STATISTICS ECONOMIC STATISTICS Sonsored by a Gran TÁMOP-4..2-08/2/A/KMR-2009-004 Course Maerial Develoed by Dearmen of Economics, Faculy of Social Sciences, Eövös Loránd Universiy Budaes (ELTE)

ECONOMIC STATISTICS ECONOMIC STATISTICS Sonsored by a Gran TÁMOP-4..2-08/2/A/KMR-2009-004 Course Maerial Develoed by Dearmen of Economics, Faculy of Social Sciences, Eövös Loránd Universiy Budaes (ELTE)

Department of Economics East Carolina University Greenville, NC Phone: Fax:

March 3, 999 Time Series Evidence on Wheher Adjusmen o Long-Run Equilibrium is Asymmeric Philip Rohman Eas Carolina Universiy Absrac The Enders and Granger (998) uni-roo es agains saionary alernaives wih

March 3, 999 Time Series Evidence on Wheher Adjusmen o Long-Run Equilibrium is Asymmeric Philip Rohman Eas Carolina Universiy Absrac The Enders and Granger (998) uni-roo es agains saionary alernaives wih

INVESTIGATING THE WEAK FORM EFFICIENCY OF AN EMERGING MARKET USING PARAMETRIC TESTS: EVIDENCE FROM KARACHI STOCK MARKET OF PAKISTAN

Elecronic Journal of Applied Saisical Analysis EJASA, Elecron. J. App. Sa. Anal. Vol. 3, Issue 1 (21), 52 64 ISSN 27-5948, DOI 1.1285/i275948v3n1p52 28 Universià del Saleno SIBA hp://siba-ese.unile.i/index.php/ejasa/index

Elecronic Journal of Applied Saisical Analysis EJASA, Elecron. J. App. Sa. Anal. Vol. 3, Issue 1 (21), 52 64 ISSN 27-5948, DOI 1.1285/i275948v3n1p52 28 Universià del Saleno SIBA hp://siba-ese.unile.i/index.php/ejasa/index

Distribution of Estimates

Disribuion of Esimaes From Economerics (40) Linear Regression Model Assume (y,x ) is iid and E(x e )0 Esimaion Consisency y α + βx + he esimaes approach he rue values as he sample size increases Esimaion

Disribuion of Esimaes From Economerics (40) Linear Regression Model Assume (y,x ) is iid and E(x e )0 Esimaion Consisency y α + βx + he esimaes approach he rue values as he sample size increases Esimaion

Mean Reversion of Balance of Payments GEvidence from Sequential Trend Break Unit Root Tests. Abstract

Mean Reversion of Balance of Paymens GEvidence from Sequenial Trend Brea Uni Roo Tess Mei-Yin Lin Deparmen of Economics, Shih Hsin Universiy Jue-Shyan Wang Deparmen of Public Finance, Naional Chengchi

Mean Reversion of Balance of Paymens GEvidence from Sequenial Trend Brea Uni Roo Tess Mei-Yin Lin Deparmen of Economics, Shih Hsin Universiy Jue-Shyan Wang Deparmen of Public Finance, Naional Chengchi

Dynamic Models, Autocorrelation and Forecasting

ECON 4551 Economerics II Memorial Universiy of Newfoundland Dynamic Models, Auocorrelaion and Forecasing Adaped from Vera Tabakova s noes 9.1 Inroducion 9.2 Lags in he Error Term: Auocorrelaion 9.3 Esimaing

ECON 4551 Economerics II Memorial Universiy of Newfoundland Dynamic Models, Auocorrelaion and Forecasing Adaped from Vera Tabakova s noes 9.1 Inroducion 9.2 Lags in he Error Term: Auocorrelaion 9.3 Esimaing

Fourier Transformation on Model Fitting for Pakistan Inflation Rate

Fourier Transformaion on Model Fiing for Pakisan Inflaion Rae Anam Iqbal (Corresponding auhor) Dep. of Saisics, Gov. Pos Graduae College (w), Sargodha, Pakisan Tel: 92-321-603-4232 E-mail: anammughal343@gmail.com

Fourier Transformaion on Model Fiing for Pakisan Inflaion Rae Anam Iqbal (Corresponding auhor) Dep. of Saisics, Gov. Pos Graduae College (w), Sargodha, Pakisan Tel: 92-321-603-4232 E-mail: anammughal343@gmail.com

Solutions to Odd Number Exercises in Chapter 6

1 Soluions o Odd Number Exercises in 6.1 R y eˆ 1.7151 y 6.3 From eˆ ( T K) ˆ R 1 1 SST SST SST (1 R ) 55.36(1.7911) we have, ˆ 6.414 T K ( ) 6.5 y ye ye y e 1 1 Consider he erms e and xe b b x e y e b

1 Soluions o Odd Number Exercises in 6.1 R y eˆ 1.7151 y 6.3 From eˆ ( T K) ˆ R 1 1 SST SST SST (1 R ) 55.36(1.7911) we have, ˆ 6.414 T K ( ) 6.5 y ye ye y e 1 1 Consider he erms e and xe b b x e y e b

Institute for Mathematical Methods in Economics. University of Technology Vienna. Singapore, May Manfred Deistler

MULTIVARIATE TIME SERIES ANALYSIS AND FORECASTING Manfred Deisler E O S Economerics and Sysems Theory Insiue for Mahemaical Mehods in Economics Universiy of Technology Vienna Singapore, May 2004 Inroducion

MULTIVARIATE TIME SERIES ANALYSIS AND FORECASTING Manfred Deisler E O S Economerics and Sysems Theory Insiue for Mahemaical Mehods in Economics Universiy of Technology Vienna Singapore, May 2004 Inroducion

Distribution of Least Squares

Disribuion of Leas Squares In classic regression, if he errors are iid normal, and independen of he regressors, hen he leas squares esimaes have an exac normal disribuion, no jus asympoic his is no rue

Disribuion of Leas Squares In classic regression, if he errors are iid normal, and independen of he regressors, hen he leas squares esimaes have an exac normal disribuion, no jus asympoic his is no rue

Modelling Monthly Rainfall Data of Port Harcourt, Nigeria by Seasonal Box-Jenkins Methods

International Journal of Sciences Research Article (ISSN 2305-3925) Volume 2, Issue July 2013 http://www.ijsciences.com Modelling Monthly Rainfall Data of Port Harcourt, Nigeria by Seasonal Box-Jenkins

International Journal of Sciences Research Article (ISSN 2305-3925) Volume 2, Issue July 2013 http://www.ijsciences.com Modelling Monthly Rainfall Data of Port Harcourt, Nigeria by Seasonal Box-Jenkins

Kriging Models Predicting Atrazine Concentrations in Surface Water Draining Agricultural Watersheds

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 Kriging Models Predicing Arazine Concenraions in Surface Waer Draining Agriculural Waersheds Paul L. Mosquin, Jeremy Aldworh, Wenlin Chen Supplemenal Maerial Number

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 Kriging Models Predicing Arazine Concenraions in Surface Waer Draining Agriculural Waersheds Paul L. Mosquin, Jeremy Aldworh, Wenlin Chen Supplemenal Maerial Number

Estimation Uncertainty

Esimaion Uncerainy The sample mean is an esimae of β = E(y +h ) The esimaion error is = + = T h y T b ( ) = = + = + = = = T T h T h e T y T y T b β β β Esimaion Variance Under classical condiions, where

Esimaion Uncerainy The sample mean is an esimae of β = E(y +h ) The esimaion error is = + = T h y T b ( ) = = + = + = = = T T h T h e T y T y T b β β β Esimaion Variance Under classical condiions, where

Quarterly ice cream sales are high each summer, and the series tends to repeat itself each year, so that the seasonal period is 4.

Seasonal models Many business and economic ime series conain a seasonal componen ha repeas iself afer a regular period of ime. The smalles ime period for his repeiion is called he seasonal period, and

Seasonal models Many business and economic ime series conain a seasonal componen ha repeas iself afer a regular period of ime. The smalles ime period for his repeiion is called he seasonal period, and

Exponential Smoothing

Exponenial moohing Inroducion A simple mehod for forecasing. Does no require long series. Enables o decompose he series ino a rend and seasonal effecs. Paricularly useful mehod when here is a need o forecas

Exponenial moohing Inroducion A simple mehod for forecasing. Does no require long series. Enables o decompose he series ino a rend and seasonal effecs. Paricularly useful mehod when here is a need o forecas

Applied Time Series Notes White noise: e t mean 0, variance 5 2 uncorrelated Moving Average

Applied Time Series Noes Whie noise: e mean 0, variance 5 uncorrelaed Moving Average Order 1: (Y. ) œ e ) 1e -1 all Order q: (Y. ) œ e ) e â ) e all 1-1 q -q ( 14 ) Infinie order: (Y. ) œ e ) 1e -1 ) e

Applied Time Series Noes Whie noise: e mean 0, variance 5 uncorrelaed Moving Average Order 1: (Y. ) œ e ) 1e -1 all Order q: (Y. ) œ e ) e â ) e all 1-1 q -q ( 14 ) Infinie order: (Y. ) œ e ) 1e -1 ) e

STRUCTURAL CHANGE IN TIME SERIES OF THE EXCHANGE RATES BETWEEN YEN-DOLLAR AND YEN-EURO IN

Inernaional Journal of Applied Economerics and Quaniaive Sudies. Vol.1-3(004) STRUCTURAL CHANGE IN TIME SERIES OF THE EXCHANGE RATES BETWEEN YEN-DOLLAR AND YEN-EURO IN 001-004 OBARA, Takashi * Absrac The

Inernaional Journal of Applied Economerics and Quaniaive Sudies. Vol.1-3(004) STRUCTURAL CHANGE IN TIME SERIES OF THE EXCHANGE RATES BETWEEN YEN-DOLLAR AND YEN-EURO IN 001-004 OBARA, Takashi * Absrac The

A SEASONAL TIME SERIES MODEL FOR NIGERIAN MONTHLY AIR TRAFFIC DATA

www.arpapress.com/volumes/vol14issue3/ijrras_14_3_14.pdf A SEASONAL TIME SERIES MODEL FOR NIGERIAN MONTHLY AIR TRAFFIC DATA Ette Harrison Etuk Department of Mathematics/Computer Science, Rivers State University

www.arpapress.com/volumes/vol14issue3/ijrras_14_3_14.pdf A SEASONAL TIME SERIES MODEL FOR NIGERIAN MONTHLY AIR TRAFFIC DATA Ette Harrison Etuk Department of Mathematics/Computer Science, Rivers State University

Økonomisk Kandidateksamen 2005(II) Econometrics 2. Solution

Econometrics 2. Solution") Økonomisk Kandidaeksamen 2005(II) Economerics 2 Soluion his is he proposed soluion for he exam in Economerics 2. For compleeness he soluion gives formal answers o mos of he quesions alhough his is no always

Økonomisk Kandidaeksamen 2005(II) Economerics 2 Soluion his is he proposed soluion for he exam in Economerics 2. For compleeness he soluion gives formal answers o mos of he quesions alhough his is no always

1. Joint stationarity and long run effects in a simple ADL(1,1) Suppose Xt, Y, also is stationary?

Suppose Xt, Y, also is stationary?") HG Third lecure - 9. Jan. 04. Join saionariy and long run effecs in a simple ADL(,) Suppose X, Y are wo saionary ime series. Does i follow ha he sum, X Y, also is saionary? The answer is NO in general.

HG Third lecure - 9. Jan. 04. Join saionariy and long run effecs in a simple ADL(,) Suppose X, Y are wo saionary ime series. Does i follow ha he sum, X Y, also is saionary? The answer is NO in general.

Unit Root Time Series. Univariate random walk

Uni Roo ime Series Univariae random walk Consider he regression y y where ~ iid N 0, he leas squares esimae of is: ˆ yy y y yy Now wha if = If y y hen le y 0 =0 so ha y j j If ~ iid N 0, hen y ~ N 0, he

Uni Roo ime Series Univariae random walk Consider he regression y y where ~ iid N 0, he leas squares esimae of is: ˆ yy y y yy Now wha if = If y y hen le y 0 =0 so ha y j j If ~ iid N 0, hen y ~ N 0, he

Lecture 15. Dummy variables, continued

Lecure 15. Dummy variables, coninued Seasonal effecs in ime series Consider relaion beween elecriciy consumpion Y and elecriciy price X. The daa are quarerly ime series. Firs model ln α 1 + α2 Y = ln X

Lecure 15. Dummy variables, coninued Seasonal effecs in ime series Consider relaion beween elecriciy consumpion Y and elecriciy price X. The daa are quarerly ime series. Firs model ln α 1 + α2 Y = ln X

5. NONLINEAR MODELS [1] Nonlinear (NL) Regression Models

![5. NONLINEAR MODELS [1] Nonlinear (NL) Regression Models](/thumbs/88/116431777.jpg "5. NONLINEAR MODELS [1] Nonlinear (NL) Regression Models") 5. NONLINEAR MODELS [1] Nonlinear (NL) Regression Models General form of nonlinear or linear regression models: y = h(x,β) + ε, ε iid N(0,σ ). Assume ha he x and ε sochasically independen. his assumpion

5. NONLINEAR MODELS [1] Nonlinear (NL) Regression Models General form of nonlinear or linear regression models: y = h(x,β) + ε, ε iid N(0,σ ). Assume ha he x and ε sochasically independen. his assumpion

Properties of Autocorrelated Processes Economics 30331

Properies of Auocorrelaed Processes Economics 3033 Bill Evans Fall 05 Suppose we have ime series daa series labeled as where =,,3, T (he final period) Some examples are he dail closing price of he S&500,

Properies of Auocorrelaed Processes Economics 3033 Bill Evans Fall 05 Suppose we have ime series daa series labeled as where =,,3, T (he final period) Some examples are he dail closing price of he S&500,

Nonlinearity Test on Time Series Data

PROCEEDING OF 3 RD INTERNATIONAL CONFERENCE ON RESEARCH, IMPLEMENTATION AND EDUCATION OF MATHEMATICS AND SCIENCE YOGYAKARTA, 16 17 MAY 016 Nonlineariy Tes on Time Series Daa Case Sudy: The Number of Foreign

PROCEEDING OF 3 RD INTERNATIONAL CONFERENCE ON RESEARCH, IMPLEMENTATION AND EDUCATION OF MATHEMATICS AND SCIENCE YOGYAKARTA, 16 17 MAY 016 Nonlineariy Tes on Time Series Daa Case Sudy: The Number of Foreign

STAD57 Time Series Analysis. Lecture 5

STAD57 Time Series Analysis Lecure 5 1 Exploraory Daa Analysis Check if given TS is saionary: µ is consan σ 2 is consan γ(s,) is funcion of h= s If no, ry o make i saionary using some of he mehods below:

STAD57 Time Series Analysis Lecure 5 1 Exploraory Daa Analysis Check if given TS is saionary: µ is consan σ 2 is consan γ(s,) is funcion of h= s If no, ry o make i saionary using some of he mehods below:

GMM - Generalized Method of Moments

GMM - Generalized Mehod of Momens Conens GMM esimaion, shor inroducion 2 GMM inuiion: Maching momens 2 3 General overview of GMM esimaion. 3 3. Weighing marix...........................................

GMM - Generalized Mehod of Momens Conens GMM esimaion, shor inroducion 2 GMM inuiion: Maching momens 2 3 General overview of GMM esimaion. 3 3. Weighing marix...........................................

Generalized Least Squares

Generalized Leas Squares Augus 006 1 Modified Model Original assumpions: 1 Specificaion: y = Xβ + ε (1) Eε =0 3 EX 0 ε =0 4 Eεε 0 = σ I In his secion, we consider relaxing assumpion (4) Insead, assume

Generalized Leas Squares Augus 006 1 Modified Model Original assumpions: 1 Specificaion: y = Xβ + ε (1) Eε =0 3 EX 0 ε =0 4 Eεε 0 = σ I In his secion, we consider relaxing assumpion (4) Insead, assume

Forecasting. Summary. Sample StatFolio: tsforecast.sgp. STATGRAPHICS Centurion Rev. 9/16/2013

STATGRAPHICS Cenurion Rev. 9/16/2013 Forecasing Summary... 1 Daa Inpu... 3 Analysis Opions... 5 Forecasing Models... 9 Analysis Summary... 21 Time Sequence Plo... 23 Forecas Table... 24 Forecas Plo...

STATGRAPHICS Cenurion Rev. 9/16/2013 Forecasing Summary... 1 Daa Inpu... 3 Analysis Opions... 5 Forecasing Models... 9 Analysis Summary... 21 Time Sequence Plo... 23 Forecas Table... 24 Forecas Plo...

Lecture Notes 2. The Hilbert Space Approach to Time Series

Time Series Seven N. Durlauf Universiy of Wisconsin. Basic ideas Lecure Noes. The Hilber Space Approach o Time Series The Hilber space framework provides a very powerful language for discussing he relaionship

Time Series Seven N. Durlauf Universiy of Wisconsin. Basic ideas Lecure Noes. The Hilber Space Approach o Time Series The Hilber space framework provides a very powerful language for discussing he relaionship

Dynamic Econometric Models: Y t = + 0 X t + 1 X t X t k X t-k + e t. A. Autoregressive Model:

Dynamic Economeric Models: A. Auoregressive Model: Y = + 0 X 1 Y -1 + 2 Y -2 + k Y -k + e (Wih lagged dependen variable(s) on he RHS) B. Disribued-lag Model: Y = + 0 X + 1 X -1 + 2 X -2 + + k X -k + e

Dynamic Economeric Models: A. Auoregressive Model: Y = + 0 X 1 Y -1 + 2 Y -2 + k Y -k + e (Wih lagged dependen variable(s) on he RHS) B. Disribued-lag Model: Y = + 0 X + 1 X -1 + 2 X -2 + + k X -k + e

BOOTSTRAP PREDICTION INTERVALS FOR TIME SERIES MODELS WITH HETROSCEDASTIC ERRORS. Department of Statistics, Islamia College, Peshawar, KP, Pakistan 2

Pak. J. Sais. 017 Vol. 33(1), 1-13 BOOTSTRAP PREDICTIO ITERVAS FOR TIME SERIES MODES WITH HETROSCEDASTIC ERRORS Amjad Ali 1, Sajjad Ahmad Khan, Alamgir 3 Umair Khalil and Dos Muhammad Khan 1 Deparmen of

Pak. J. Sais. 017 Vol. 33(1), 1-13 BOOTSTRAP PREDICTIO ITERVAS FOR TIME SERIES MODES WITH HETROSCEDASTIC ERRORS Amjad Ali 1, Sajjad Ahmad Khan, Alamgir 3 Umair Khalil and Dos Muhammad Khan 1 Deparmen of

Identification of Trends and Cycles in Economic Time Series. by Bora Isik

Idenificaion of Trends and Cycles in Economic Time Series by Bora Isik An Honours essay submied o Carleon Universiy in fulfillmen of he requiremens for he course ECON 498, as credi oward he degree of Bachelor

Idenificaion of Trends and Cycles in Economic Time Series by Bora Isik An Honours essay submied o Carleon Universiy in fulfillmen of he requiremens for he course ECON 498, as credi oward he degree of Bachelor

BOX-JENKINS MODEL NOTATION. The Box-Jenkins ARMA(p,q) model is denoted by the equation. pwhile the moving average (MA) part of the model is θ1at

model is denoted by the equation. pwhile the moving average (MA) part of the model is θ1at") BOX-JENKINS MODEL NOAION he Box-Jenkins ARMA(,q) model is denoed b he equaion + + L+ + a θ a L θ a 0 q q. () he auoregressive (AR) ar of he model is + L+ while he moving average (MA) ar of he model is

BOX-JENKINS MODEL NOAION he Box-Jenkins ARMA(,q) model is denoed b he equaion + + L+ + a θ a L θ a 0 q q. () he auoregressive (AR) ar of he model is + L+ while he moving average (MA) ar of he model is

Time Series Models for Growth of Urban Population in SAARC Countries

Advances in Managemen & Applied Economics, vol., no.1, 01, 109-119 ISSN: 179-7544 (prin version), 179-755 (online) Inernaional Scienific Press, 01 Time Series Models for Growh of Urban Populaion in SAARC

Advances in Managemen & Applied Economics, vol., no.1, 01, 109-119 ISSN: 179-7544 (prin version), 179-755 (online) Inernaional Scienific Press, 01 Time Series Models for Growh of Urban Populaion in SAARC

A Specification Test for Linear Dynamic Stochastic General Equilibrium Models

Journal of Saisical and Economeric Mehods, vol.1, no.2, 2012, 65-70 ISSN: 2241-0384 (prin), 2241-0376 (online) Scienpress Ld, 2012 A Specificaion Tes for Linear Dynamic Sochasic General Equilibrium Models

Journal of Saisical and Economeric Mehods, vol.1, no.2, 2012, 65-70 ISSN: 2241-0384 (prin), 2241-0376 (online) Scienpress Ld, 2012 A Specificaion Tes for Linear Dynamic Sochasic General Equilibrium Models

DYNAMIC ECONOMETRIC MODELS vol NICHOLAS COPERNICUS UNIVERSITY - TORUŃ Józef Stawicki and Joanna Górka Nicholas Copernicus University

DYNAMIC ECONOMETRIC MODELS vol.. - NICHOLAS COPERNICUS UNIVERSITY - TORUŃ 996 Józef Sawicki and Joanna Górka Nicholas Copernicus Universiy ARMA represenaion for a sum of auoregressive processes In he ime

DYNAMIC ECONOMETRIC MODELS vol.. - NICHOLAS COPERNICUS UNIVERSITY - TORUŃ 996 Józef Sawicki and Joanna Górka Nicholas Copernicus Universiy ARMA represenaion for a sum of auoregressive processes In he ime

Forecasting with ARMA Models

CS-BIGS 4(): 59-5 00 CS-BIGS hp://wwwbenleyedu/csbigs/vol4-/jaggiapdf Forecasing wih ARMA Models Sanjiv Jaggia California Polyechnic Sae Universiy, San Luis Obispo, CA Increasing awareness and daa availabiliy

CS-BIGS 4(): 59-5 00 CS-BIGS hp://wwwbenleyedu/csbigs/vol4-/jaggiapdf Forecasing wih ARMA Models Sanjiv Jaggia California Polyechnic Sae Universiy, San Luis Obispo, CA Increasing awareness and daa availabiliy

Exponential Weighted Moving Average (EWMA) Chart Under The Assumption of Moderateness And Its 3 Control Limits

Chart Under The Assumption of Moderateness And Its 3 Control Limits") DOI: 0.545/mjis.07.5009 Exponenial Weighed Moving Average (EWMA) Char Under The Assumpion of Moderaeness And Is 3 Conrol Limis KALPESH S TAILOR Assisan Professor, Deparmen of Saisics, M. K. Bhavnagar Universiy,

DOI: 0.545/mjis.07.5009 Exponenial Weighed Moving Average (EWMA) Char Under The Assumpion of Moderaeness And Is 3 Conrol Limis KALPESH S TAILOR Assisan Professor, Deparmen of Saisics, M. K. Bhavnagar Universiy,

State-Space Models. Initialization, Estimation and Smoothing of the Kalman Filter

Sae-Space Models Iniializaion, Esimaion and Smoohing of he Kalman Filer Iniializaion of he Kalman Filer The Kalman filer shows how o updae pas predicors and he corresponding predicion error variances when

Sae-Space Models Iniializaion, Esimaion and Smoohing of he Kalman Filer Iniializaion of he Kalman Filer The Kalman filer shows how o updae pas predicors and he corresponding predicion error variances when

The Effect of Nonzero Autocorrelation Coefficients on the Distributions of Durbin-Watson Test Estimator: Three Autoregressive Models

EJ Exper Journal of Economi c s ( 4 ), 85-9 9 4 Th e Au h or. Publi sh ed by Sp rin In v esify. ISS N 3 5 9-7 7 4 Econ omics.e xp erjou rn a ls.com The Effec of Nonzero Auocorrelaion Coefficiens on he

EJ Exper Journal of Economi c s ( 4 ), 85-9 9 4 Th e Au h or. Publi sh ed by Sp rin In v esify. ISS N 3 5 9-7 7 4 Econ omics.e xp erjou rn a ls.com The Effec of Nonzero Auocorrelaion Coefficiens on he

Volatility. Many economic series, and most financial series, display conditional volatility

Volailiy Many economic series, and mos financial series, display condiional volailiy The condiional variance changes over ime There are periods of high volailiy When large changes frequenly occur And periods

Volailiy Many economic series, and mos financial series, display condiional volailiy The condiional variance changes over ime There are periods of high volailiy When large changes frequenly occur And periods

Wednesday, November 7 Handout: Heteroskedasticity

Amhers College Deparmen of Economics Economics 360 Fall 202 Wednesday, November 7 Handou: Heeroskedasiciy Preview Review o Regression Model o Sandard Ordinary Leas Squares (OLS) Premises o Esimaion Procedures

Amhers College Deparmen of Economics Economics 360 Fall 202 Wednesday, November 7 Handou: Heeroskedasiciy Preview Review o Regression Model o Sandard Ordinary Leas Squares (OLS) Premises o Esimaion Procedures

Chickens vs. Eggs: Replicating Thurman and Fisher (1988) by Arianto A. Patunru Department of Economics, University of Indonesia 2004

by Arianto A. Patunru Department of Economics, University of Indonesia 2004") Chicens vs. Eggs: Relicaing Thurman and Fisher (988) by Ariano A. Paunru Dearmen of Economics, Universiy of Indonesia 2004. Inroducion This exercise lays ou he rocedure for esing Granger Causaliy as discussed

Chicens vs. Eggs: Relicaing Thurman and Fisher (988) by Ariano A. Paunru Dearmen of Economics, Universiy of Indonesia 2004. Inroducion This exercise lays ou he rocedure for esing Granger Causaliy as discussed

Use of Unobserved Components Model for Forecasting Non-stationary Time Series: A Case of Annual National Coconut Production in Sri Lanka

Tropical Agriculural Research Vol. 5 (4): 53 531 (014) Use of Unobserved Componens Model for Forecasing Non-saionary Time Series: A Case of Annual Naional Coconu Producion in Sri Lanka N.K.K. Brinha, S.

Tropical Agriculural Research Vol. 5 (4): 53 531 (014) Use of Unobserved Componens Model for Forecasing Non-saionary Time Series: A Case of Annual Naional Coconu Producion in Sri Lanka N.K.K. Brinha, S.

Types of Exponential Smoothing Methods. Simple Exponential Smoothing. Simple Exponential Smoothing

M Business Forecasing Mehods Exponenial moohing Mehods ecurer : Dr Iris Yeung Room No : P79 Tel No : 788 8 Types of Exponenial moohing Mehods imple Exponenial moohing Double Exponenial moohing Brown s

M Business Forecasing Mehods Exponenial moohing Mehods ecurer : Dr Iris Yeung Room No : P79 Tel No : 788 8 Types of Exponenial moohing Mehods imple Exponenial moohing Double Exponenial moohing Brown s

Predicting Money Multiplier in Pakistan

The Pakisan Developmen Review 39 : (Spring 2000) pp. 23 35 Predicing Money Muliplier in Pakisan MUHAMMAD FAROOQ ARBY The paper has developed ime-series models for he monhly money muliplier and is componens,

The Pakisan Developmen Review 39 : (Spring 2000) pp. 23 35 Predicing Money Muliplier in Pakisan MUHAMMAD FAROOQ ARBY The paper has developed ime-series models for he monhly money muliplier and is componens,

Forecasting models for economic and environmental applications

Universiy of Souh Florida Scholar Commons Graduae Theses and Disseraions Graduae School 008 Forecasing models for economic and environmenal applicaions Shou Hsing Shih Universiy of Souh Florida Follow

Universiy of Souh Florida Scholar Commons Graduae Theses and Disseraions Graduae School 008 Forecasing models for economic and environmenal applicaions Shou Hsing Shih Universiy of Souh Florida Follow

A New Unit Root Test against Asymmetric ESTAR Nonlinearity with Smooth Breaks

Iran. Econ. Rev. Vol., No., 08. pp. 5-6 A New Uni Roo es agains Asymmeric ESAR Nonlineariy wih Smooh Breaks Omid Ranjbar*, sangyao Chang, Zahra (Mila) Elmi 3, Chien-Chiang Lee 4 Received: December 7, 06

Iran. Econ. Rev. Vol., No., 08. pp. 5-6 A New Uni Roo es agains Asymmeric ESAR Nonlineariy wih Smooh Breaks Omid Ranjbar*, sangyao Chang, Zahra (Mila) Elmi 3, Chien-Chiang Lee 4 Received: December 7, 06

Modeling Economic Time Series with Stochastic Linear Difference Equations

A. Thiemer, SLDG.mcd, 6..6 FH-Kiel Universiy of Applied Sciences Prof. Dr. Andreas Thiemer e-mail: andreas.hiemer@fh-kiel.de Modeling Economic Time Series wih Sochasic Linear Difference Equaions Summary:

A. Thiemer, SLDG.mcd, 6..6 FH-Kiel Universiy of Applied Sciences Prof. Dr. Andreas Thiemer e-mail: andreas.hiemer@fh-kiel.de Modeling Economic Time Series wih Sochasic Linear Difference Equaions Summary:

MODELING AND FORECASTING EXCHANGE RATE DYNAMICS IN PAKISTAN USING ARCH FAMILY OF MODELS

Elecronic Journal of Applied Saisical Analysis EJASA (01), Elecron. J. App. Sa. Anal., Vol. 5, Issue 1, 15 9 e-issn 070-5948, DOI 10.185/i0705948v5n1p15 01 Universià del Saleno hp://siba-ese.unile.i/index.php/ejasa/index

Elecronic Journal of Applied Saisical Analysis EJASA (01), Elecron. J. App. Sa. Anal., Vol. 5, Issue 1, 15 9 e-issn 070-5948, DOI 10.185/i0705948v5n1p15 01 Universià del Saleno hp://siba-ese.unile.i/index.php/ejasa/index

How to Deal with Structural Breaks in Practical Cointegration Analysis

How o Deal wih Srucural Breaks in Pracical Coinegraion Analysis Roselyne Joyeux * School of Economic and Financial Sudies Macquarie Universiy December 00 ABSTRACT In his noe we consider he reamen of srucural

How o Deal wih Srucural Breaks in Pracical Coinegraion Analysis Roselyne Joyeux * School of Economic and Financial Sudies Macquarie Universiy December 00 ABSTRACT In his noe we consider he reamen of srucural

Solutions to Exercises in Chapter 12

Chaper in Chaper. (a) The leas-squares esimaed equaion is given by (b)!i = 6. + 0.770 Y 0.8 R R = 0.86 (.5) (0.07) (0.6) Boh b and b 3 have he expeced signs; income is expeced o have a posiive effec on

Chaper in Chaper. (a) The leas-squares esimaed equaion is given by (b)!i = 6. + 0.770 Y 0.8 R R = 0.86 (.5) (0.07) (0.6) Boh b and b 3 have he expeced signs; income is expeced o have a posiive effec on

Forecasting of boro rice production in Bangladesh: An ARIMA approach

J. Bangladesh Agril. Univ. 8(1): 103 112, 2010 ISSN 1810-3030 Forecasing of boro rice producion in Bangladesh: An ARIMA approach N. M. F. Rahman Deparmen of BBA, Mirpur Universiy College, Dhaka Absrac

J. Bangladesh Agril. Univ. 8(1): 103 112, 2010 ISSN 1810-3030 Forecasing of boro rice producion in Bangladesh: An ARIMA approach N. M. F. Rahman Deparmen of BBA, Mirpur Universiy College, Dhaka Absrac

3.1 More on model selection

3. More on Model selecion 3. Comparing models AIC, BIC, Adjused R squared. 3. Over Fiing problem. 3.3 Sample spliing. 3. More on model selecion crieria Ofen afer model fiing you are lef wih a handful of

3. More on Model selecion 3. Comparing models AIC, BIC, Adjused R squared. 3. Over Fiing problem. 3.3 Sample spliing. 3. More on model selecion crieria Ofen afer model fiing you are lef wih a handful of

Outline. lse-logo. Outline. Outline. 1 Wald Test. 2 The Likelihood Ratio Test. 3 Lagrange Multiplier Tests

Ouline Ouline Hypohesis Tes wihin he Maximum Likelihood Framework There are hree main frequenis approaches o inference wihin he Maximum Likelihood framework: he Wald es, he Likelihood Raio es and he Lagrange

Ouline Ouline Hypohesis Tes wihin he Maximum Likelihood Framework There are hree main frequenis approaches o inference wihin he Maximum Likelihood framework: he Wald es, he Likelihood Raio es and he Lagrange

Stability. Coefficients may change over time. Evolution of the economy Policy changes

Sabiliy Coefficiens may change over ime Evoluion of he economy Policy changes Time Varying Parameers y = α + x β + Coefficiens depend on he ime period If he coefficiens vary randomly and are unpredicable,

Sabiliy Coefficiens may change over ime Evoluion of he economy Policy changes Time Varying Parameers y = α + x β + Coefficiens depend on he ime period If he coefficiens vary randomly and are unpredicable,

1. Diagnostic (Misspeci cation) Tests: Testing the Assumptions

Tests: Testing the Assumptions") Business School, Brunel Universiy MSc. EC5501/5509 Modelling Financial Decisions and Markes/Inroducion o Quaniaive Mehods Prof. Menelaos Karanasos (Room SS269, el. 01895265284) Lecure Noes 6 1. Diagnosic

Business School, Brunel Universiy MSc. EC5501/5509 Modelling Financial Decisions and Markes/Inroducion o Quaniaive Mehods Prof. Menelaos Karanasos (Room SS269, el. 01895265284) Lecure Noes 6 1. Diagnosic

2 Univariate Stationary Processes

Univariae Saionary Processes As menioned in he inroducion, he publicaion of he exbook by GEORGE E.P. BOX and GWILYM M. JENKINS in 97 opened a new road o he analysis of economic ime series. This chaper

Univariae Saionary Processes As menioned in he inroducion, he publicaion of he exbook by GEORGE E.P. BOX and GWILYM M. JENKINS in 97 opened a new road o he analysis of economic ime series. This chaper

PROJECTING ECONOMIC ACTIVITY AT THE STATE

FORECASTING STATE LEVEL ECONOMIC ACTIVITY: AN ERROR CORRECTION MODEL WITH EXOGENOUS NATIONAL STRUCTURAL FORECAST COMPONENTS Michael Hicks, Ball Sae Universiy* INTRODUCTION PROJECTING ECONOMIC ACTIVITY

FORECASTING STATE LEVEL ECONOMIC ACTIVITY: AN ERROR CORRECTION MODEL WITH EXOGENOUS NATIONAL STRUCTURAL FORECAST COMPONENTS Michael Hicks, Ball Sae Universiy* INTRODUCTION PROJECTING ECONOMIC ACTIVITY

ACE 562 Fall Lecture 8: The Simple Linear Regression Model: R 2, Reporting the Results and Prediction. by Professor Scott H.

ACE 56 Fall 5 Lecure 8: The Simple Linear Regression Model: R, Reporing he Resuls and Predicion by Professor Sco H. Irwin Required Readings: Griffihs, Hill and Judge. "Explaining Variaion in he Dependen

ACE 56 Fall 5 Lecure 8: The Simple Linear Regression Model: R, Reporing he Resuls and Predicion by Professor Sco H. Irwin Required Readings: Griffihs, Hill and Judge. "Explaining Variaion in he Dependen

Solutions: Wednesday, November 14

Amhers College Deparmen of Economics Economics 360 Fall 2012 Soluions: Wednesday, November 14 Judicial Daa: Cross secion daa of judicial and economic saisics for he fify saes in 2000. JudExp CrimesAll

Amhers College Deparmen of Economics Economics 360 Fall 2012 Soluions: Wednesday, November 14 Judicial Daa: Cross secion daa of judicial and economic saisics for he fify saes in 2000. JudExp CrimesAll

Sample Autocorrelations for Financial Time Series Models. Richard A. Davis Colorado State University Thomas Mikosch University of Copenhagen

Sample Auocorrelaions for Financial Time Series Models Richard A. Davis Colorado Sae Universiy Thomas Mikosch Universiy of Copenhagen Ouline Characerisics of some financial ime series IBM reurns NZ-USA

Sample Auocorrelaions for Financial Time Series Models Richard A. Davis Colorado Sae Universiy Thomas Mikosch Universiy of Copenhagen Ouline Characerisics of some financial ime series IBM reurns NZ-USA

Robust critical values for unit root tests for series with conditional heteroscedasticity errors: An application of the simple NoVaS transformation

WORKING PAPER 01: Robus criical values for uni roo ess for series wih condiional heeroscedasiciy errors: An applicaion of he simple NoVaS ransformaion Panagiois Manalos ECONOMETRICS AND STATISTICS ISSN

WORKING PAPER 01: Robus criical values for uni roo ess for series wih condiional heeroscedasiciy errors: An applicaion of he simple NoVaS ransformaion Panagiois Manalos ECONOMETRICS AND STATISTICS ISSN

Ready for euro? Empirical study of the actual monetary policy independence in Poland VECM modelling

Macroeconomerics Handou 2 Ready for euro? Empirical sudy of he acual moneary policy independence in Poland VECM modelling 1. Inroducion This classes are based on: Łukasz Goczek & Dagmara Mycielska, 2013.

Macroeconomerics Handou 2 Ready for euro? Empirical sudy of he acual moneary policy independence in Poland VECM modelling 1. Inroducion This classes are based on: Łukasz Goczek & Dagmara Mycielska, 2013.