FORECASTING WITH REGRESSION

|

|

|

- Scott Fitzgerald

- 6 years ago

- Views:

Transcription

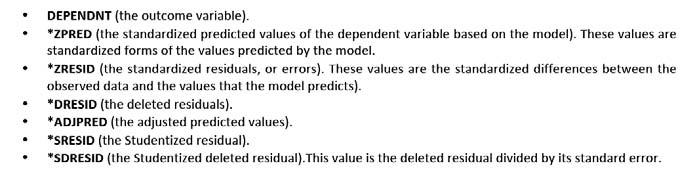

1 FORECASTING WITH REGRESSION MODELS Overview of basic regression echniques. Daa analysis and forecasing using muliple regression analysis. 106 Visualizaion of Four Differen Daa Ses Daa Se A Daa Se B Daa Se C For each daa se: Mean of X = 9.0 Mean of Y = 7.5 Correlaion = 0.82 OLS Regression equaion: Y = X 0.5 Daa Se D All have very similar saisical properies, bu are visually quie differen!!! 107 1

2 Simple Linear Regression Model The populaion regression model: Dependen Variable y Populaion Y inercep i β Populaion Slope Coefficien 0 β 1 Independen Variable x i ε i Random Error erm Linear componen Random Error componen Simple Linear Regression Model Y Y i β 0 β 1 X i ε i Observed Value of Y for x i Prediced Value of Y for x i ε i Random Error for his X i value Slope = β 1 Inercep = β 0 x i X 2

3 Simple Linear Regression Equaion The simple linear regression equaion provides an esimae of he populaion regression line Esimaed (or prediced) y value for observaion i yˆ i Esimae of he regression inercep b 0 b Esimae of he regression slope 1 x i Value of x for observaion i The individual random error erms e i have a mean of zero e i - yˆ ) y ( yi i i -(b0 1 i b x ) The mahemaical form of he regression model The mos basic regression analysis mehod Ordinary Leas Squares (OLS) OLS is referred o in boh Excel and SPSS as "linear regression". The mahemaical form of he regression model is essenially an equaion y f ( x) When building a forecas model, we sar wih a specific equaion. This is called model specificaion. The relaionship could be linear and non linear. Various mahemaical forms could be aemped If he model properies do no work ou when calibraing, i can be respecified by replacing he variables on he righ hand side wih ohers ha seem o provide a more clear explanaion of he forecas variable

4 Ordinary Leas Squares (OLS) Coefficien Esimaors b 0 and b 1 are obained by finding he values of b 0 and b 1 ha minimize he sum of he squared residuals (errors), SSE: min SSE min min min n i1 e 2 i (y yˆ ) i i 2 i [y (b 0 b x )] Differenial calculus is used o obain he coefficien esimaors b 0 and b 1 ha minimize SSE 1 i 2 4

5 OLS Coefficien Esimaors b 1 The slope coefficien esimaor is n i1 (xi x)(yi y) n 2 (x x) i1 i Cov(x, y) s 2 x s r s And he consan or y inercep is b0 y b1x y x where sample correlaion coefficien s sxy r s s sample covariance Cov(x, y) xy x y (x x)(y y) i n 11 i The regression line always goes hrough he mean x, y Muliple Regression Analysis (MRA) a paricular mulivariae echnique MRA incorporaes informaion from several variables o predic he behavior of a given variable. If a researcher is ineresed in predicing he sales of a produc, MRA can be used o develop a model ha would poenially incorporae informaion from oher influenial variables. Once a regression model is developed i can be used o predic he sales ino he fuure if fuure projecions of hese oher influenial variables are available. (such as inernal facors of he firm, economic facors or demographic characerisics) 115 5

6 12.1 The Muliple Regression Model Idea: Examine he linear relaionship beween 1 dependen d (Y) & 2 or more independen d variables ibl (X i ) Muliple Regression Model wih K Independen Variables: Y inercep Populaion slopes Random Error Y β0 β1 X1 β2 X2 βk XK ε Muliple Regression Equaion The coefficiens of he muliple regression model are esimaed using sample daa Muliple regression equaion wih K independen variables: Esimaed (or prediced) value of y yˆ i b 0 Esimaed inercep b 1 x 1i Esimaed slope coefficiens b 2 x 2i b K x Ki 6

7 Regression (e.g., MRA) models developed using cross secional daa are used for predicing saic values or values ha do no have a ime elemen. This means ha values are no generaed for a specific dae and ha ime is irrelevan in predicing values. Wha deermines values for hese models are oher non ime dependen d facors e.g. house sales price=f(house's square fee of living space). 118 MRA models developed using ime series daa, on he oher hand, are used o predic values ha have a ime elemen. In oher words, values are deermined for specific daes since he model is buil by examining he relaionships amongs variables over ime. For example, in a housing sars model, an annual (or monhly) model will be developed by examining he correlaion beween he number of sars and oher facors such as ineres raes or household income for successive years (or monhs). If he model is used o predic fuure values, hen he prediced values are referred o as forecass

8 Three opions o forecas a variable of ineres, e.g. sales 1. Develop a forecas by examining he hisorical paern of sales and hen exend he paern forward o generae a forecas. In his approach, sales is o be forecased by using pas values of his variable. 2. Develop a forecas using a muliple regression model based on "saic" or cross secional informaion from oher variables highly correlaed wih sales. 3. Develop a forecas using a muliple regression model based on boh pas values (ime series) of he variable o be prediced and oher variables highly correlaed wih sales. The seps involved in building models for predicing saic or ime series values are almos idenical. 120 A muliple regression model based on "saic" or cross secional informaion This model would predic he level of sales given for example, he household income, unemploymen rae, and cusomer demographics. Noe ha up o dae cross secional daa on economic variables, such as household income, is difficul o obain. This daa can be compiled from Saisical Absracs as par of he populaion Census, bu his is only underaken every five years. Mos companies do no he have he resources or ime o conduc heir own demographic consumer surveys

9 A muliple regression model based on boh ime series of he variable and oher highly correlaed variables Generaesa a model using ime series daa (annual/quarerly/monhly) for boh sales and oher influencing facors. examine several variables generae a muliple regression model. This ype of daa may be more readily available since a single annual survey can be used o exrapolae informaion for many regions. Daa collecing agencies such as TUİK (Turkish Saisical Insiue), BIST (Borsa Isanbul) generally produce ime series daa 122 Model Building Mehodology The Sages of Saisical Model Building Model lspecificaion i * Coefficien Esimaion Model Verificaion Undersand he problem o be sudied Selec dependen and independen variables Idenify model form (linear, quadraic ) Deermine required daa for he sudy Inerpreaion and Inference 9

10 The Sages of Model Building Model Specificaion Coefficien Esimaion Model lverificaion Inerpreaion and Inference * (coninued) Esimae he regression coefficiens using he available daa Form confidence inervals for he regression coefficiens For predicion, goal is he smalles s e If esimaing individual slope coefficiens, examine model for mulicollineariy and specificaion bias The Sages of Model Building Model Specificaion Coefficien Esimaion Model lverificaion Inerpreaion and Inference * (coninued) Logically evaluae regression resuls in ligh of he model (i.e., are coefficien signs correc?) Are any coefficiens biased or illogical? Evaluae regression assumpions (i.e., are residuals random and independen?) If any problems are suspeced, reurn o model specificaion and adjus he model 10

11 The Sages of Model Building Model Specificaion (coninued) Coefficien Esimaion Model lverificaion Inerpreaion and Inference Inerpre he regression resuls in he seing and unis of your sudy Form confidence inervals or es hypoheses abou regression coefficiens Use he model for forecasing or predicion * A process for regression forecasing preliminary daa screening by graphics Look for rend, seasonal, and cyclical componens, as well as for ouliers. Deermine wha ype of regression model may be mos appropriae (e.g. Linear versus Nonlinear, or Trend versus Causal) generaion of a forecas model by MRA

12 Forecas model evaluaion In sample evaluaion (Rerospecive approach) When he model is evaluaed in comparison wih he daa used in specifying he model, we are deermining how well he model fis he daa. Ou of sample evaluaion When he model is evaluaed by using a holdou period, we can deermine how accurae he model is for an acualforecas horizon. Afer an evaluaion of fi and accuracy, he bes model should be respecified using he enire daa se. 128 Forecasing wih a Simple Linear Trend Example: For DPI daa (given from Jan 1993 hrough Dec 2005), develop a forecas for he las seven monhs of The linear ime rend model for DPI is DPI ˆ b 0 b where T, ime index, is usually se equal o 1 for he firs observaion T 12

13 Sequence char Pronounced rend! A linear rend line would fi he daa well. 130 Run Linear Regression o provide model coefficien esimaes PI ˆ 4542,54 28,91T D

14 Inerpreaion of he coefficien esimaes DPI ˆ 4542,54 28,91T The slope erm ells ha: On average, disposable personal income increased by 28,91 billion dollars per monh 132 Saisical Evaluaion of he regression model Saisical evaluaion suggess ha his linear equaion provides a very good fi o he daa

15 Using he equaion o make a forecas DPI ˆ 4542,54 28,91T forhe las seven monhs of 2005, subsiue he ime index values (T) from 150 o 156. Trend esimaes: June 2005: DPI = 4542,54+28, (150) = 8879,04 July 2005: DPI = 4542,54+28,91 (151) = 8907,95... Dec 2005: DPI = 4542,54+28,91 (156) = 9052, Noe We do no imply any sense of causaliy in such a model. dltime does no cause income orise. Income has increased over ime a a reasonably seady rae for reasons no explained by our model

16 Using a causal regression model o forecas y f ( x) Ina causal model, dl a change in he independen d variable ibl (X) is assumed o cause a change in he dependen variable (Y). Suppose ha a bivariae (simple) regression model will be developed for explaining and predicing he level of jewelery sales. Wha facors do you hink migh have an impac on jewelery sales? Some poenial causal variables: income, ineres raes, he unemploymen rae, so on. A subsanial seasonal aspec o jewelery sales can be expeced. 136 DPI JS? Consider how well jewelery sales (JS) can be forecas on he basisof disposablepersonal l income (DPI), as a measure of overall purchasing power. Develop a forecas of JS for each of he monhs of

17 Before developing a regression forecas model Look a ime paerns of he variables 138 Seasonal decomposiion of JS Deseasonalized JS daa shows he upward rend clearly

18 Look firs a scaer plo of JS and DPI Higher values of JS are associaed wih higher incomes The effec of seasonaliy is seen in a dramaic way. 140 Scaer Plo of seasonally adjused JS and DPI A linear line hrough h hose poins could provide a reasonably good fi o he daa. See also all of hese observaions are well away from he origin!

19 Regression Resuls for Original JS Daa J Sˆ b0 b1 DPI J Sˆ 88,738 0,265 DPI 142 Using he equaion o make a forecas J Sˆ 88,738 0,265 DPI To use his model dlo forecas JS for each monh of 2005, DPI forecass for he same period should be obained. Hol s Exponenial Smoohing forecas for DPI

20 Hol s Exponenial Smoohing forecas for DPI 144 Forecas JS for each monh of 2005 dae DPI esimae JS forecas JAN ,5 2518,66 FEB ,1 2526,23 Mar ,8 2533,84 APR ,5 2541,45 May ,2 2549,05 JUN ,9 2556,66 JUL ,6 2564,26 AUG ,3 2571,87 SEP ,0 2579,47 OCT ,7 2587,08 NOV ,4 2594,68 DEC ,1 2602,29 Upward rend in JS is accouned for by he regression model bu he seasonaliy is no aken ino accoun!! Thus, 2005 forecass are likely o be subsanially incorrec

21 ? How o incorporae seasonaliy in regression modeling 1. Eiher use a model ha can accoun for seasonaliy direcly 2. Or, deseasonalize he daa before developing he regression forecasing model * Developing a model based on seasonally adjused jewelery sales daa (SAJS) and reinroduce he seasonaliy as forecass being developed 146 Regression Model for SAJS Daa S AJS ˆ b0 b1 DPI SAJS ˆ 381,44 0,219DPI

22 SAJS as a funcion of DPI SAJS ˆ 381,44 0,219DPI dae Acual SAJSAJS forecas Error squared JAN , , ,12 FEB , , ,25 Mar , ,11 862,70 APR , ,39 223,42 May , , ,65 JUN , , ,29 JUL , , ,86 AUG , , ,79 SEP , , ,03 OCT , , ,03 NOV , , ,77 DEC , ,68 607,49 MSE= ,40 RMSE= 492, JS Final Forecas for 2005 i. Trend for SAJS is forecased ii. These are muliplied by he seasonal indices o ge he final forecas. reseasonalized dae Acual JS SAJS forecas seasonal indices JS forecas Error squared JAN , ,47 FEB , ,39 Mar , ,14 APR , ,71 May , ,40 JUN , ,65 JUL , ,85 AUG , ,71 SEP , ,91 OCT , ,45 NOV , ,67 DEC , ,34 MSE= ,69 RMSE= 466,

The error erms are random variables wih mean 0 and")

23 Linear Regression Assumpions For a given value of X, he populaion of Y values is normally disribued abou he populaion regression line. The rue relaionship form is linear (Y is a linear funcion of X, plus random error) The error erms are random variables wih mean 0 and consan variance, σ 2 The dispersion of populaion daa poins around he populaion regression line remains consan everywhere along he line. The uniform variance propery is called homoscedasiciy. A violaion of his assumpion is called heeroscedasiciy. The error erms, ε i are independen of each oher. This assumpion implies a random sample of X Y daa poins. When he X Y daa poins are recorded over ime, his assumpion is ofen violaed. Raher han being independen, consecuive observaions are serially correlaed (serial correlaion problem)

24 Basic Diagnosic Checks for Model Evaluaion 1. Ask yourself wheher he sign on he slope erm makes sense. i.e., are coefficien signs correc? Wha if he signs do no make sense? DPI ˆ 4542,54 28,91T J Sˆ 88,738 0,265 DPI SAJS ˆ 381,44 0,219DPI 152 Basic Diagnosic Checks for Model Evaluaion 2. Wheher or no he slope erm is significanly posiive or negaive?

25 Inference abou he Slope: Tes es for a populaion slope Is here a linear relaionship beween X and Y? Null and alernaive hypoheses H 0 : β 1 = 0 (no linear relaionship) H 1 : β 1 0 (linear relaionship does exis) Tes saisic b1 β s b 1 1 where: b 1 = regression slope coefficien β 1 = hypohesized slope s b1 = sandard error of he slope Hypohesis Tes for Populaion Slope Using he F Disribuion F Tes saisic shows he overall qualiy of he model F MSR MSE where MSR SSR k SSE MSE n k 1 where F follows an F disribuion wih k numeraor and (n k 1) denominaor degrees of freedom (k = he number of independen variables in he regression model) 25

26 Hypohesis Tes for Populaion Slope Using he F Disribuion (coninued) An alernae es for he hypohesis ha he slope is zero: H 0 : β 1 = 0 H 1 : β 1 0 Use he F saisic F MSR MSE SSR 2 s e The decision rule is rejec H 0 if F F 1,n 2,α As a general rule of humb, an F Saisic greaer han 4 is accepable and represens a well fied model. However, significanly larger F value readings are preferable. Regression Model for SAJS Daa SAJS ˆ 381,44 0,219DPI P value for he F Tes H 0 : β 1 = 0 H 1 : β 1 0 ( = 0,05) F raio=832,755 (p value=0,000 < α=0,05). There is sufficien evidence ha DPI affecs Seasonally Adjused Jewelery Sales (SAJS) Since P value < α, he esimaed coefficiens, b 0 and b 1, are saisically significan

27 Basic Diagnosic Checks for Model Evaluaion 3. Evaluae wha percen of he variaion (i.e. Up and down d movemen) in he dependen d variable is explained by variaion in he independen variable? R squared: he coefficien of deerminaion 2 2 R r 158 Explanaory Power of a Linear Regression Equaion Toal variaion is made up of wo pars: SST SSR SSE Toal Sum of Squares Regression Sum of Squares Error (residual) Sum of Squares 2 SST (y SSR (y ˆ y) SSE (y y ˆ 2 i y ) where: y i ) = Average value of he dependen variable y i = Observed values of he dependen variable ŷ i = Prediced value of y for he given x i value 2 i i) 27

(coninued) 28")

28 Analysis of Variance (ANOVA) SST = oal sum of squares Measures he variaion of he y i values around heir mean, y SSR = regression sum of squares Explained variaion aribuable o he linear relaionship beween x and y SSE = error sum of squares Variaion aribuable o facors oher han he linear relaionship beween x and y Analysis of Variance (ANOVA) (coninued) 28

29 Coefficien of Deerminaion, R 2 The coefficien of deerminaion is he porion of he oal variaion in he dependen variable ha is explained by variaion in he independen variable The coefficien of deerminaion is also called R squared and is denoed as R 2 R 2 SSR SST regression sum of squares oal sum of squares noe: 0 R 2 1 Examples of Approximae r 2 Values Y r 2 = 1 Y r 2 = 1 X Perfec linear relaionship beween X and Y: 100% of he variaion in Y is explained by variaion in X r 2 = 1 X 29

30 Examples of Approximae r 2 Values Y 0 < r 2 < 1 Y X Weaker linear relaionships beween X and Y: Some bu no all of he variaion in Y is explained by variaion in X X Examples of Approximae r 2 Values Y r 2 = 0 r 2 = 0 X No linear relaionship beween X and Y: The value of Y does no depend on X. (None of he variaion in Y is explained by variaion in X) 30

31 Regression Model for SAJS Daa SAJS ˆ 381,44 0,219DPI 85,4% of he variaion in SAJS is explained by variaion in DPI 166 * Using he sandard error of he esimae s e is a measure of he variaion of observed y values from he regression line Y Y small s s e X large s e X The magniude of s e should always be judged relaive o he size of he y values in he sample daa 31

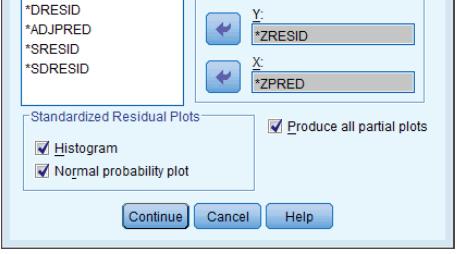

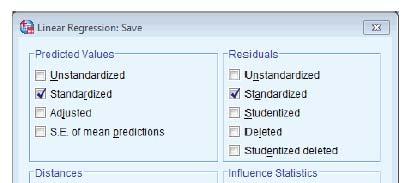

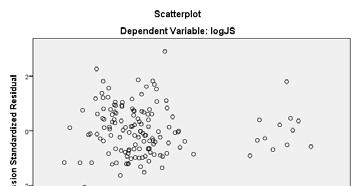

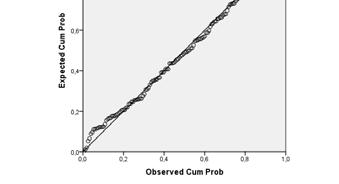

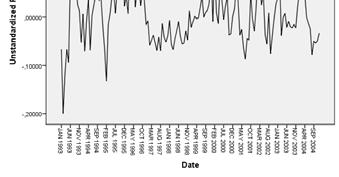

32 Regression Model for SAJS Daa SAJS ˆ 381,44 0,219DPI s e = $109 ($Millions) is moderaely small relaive o SAJS in he $1099 $2572 ($Millions) range 168 Analysis of Residuals Errors (residuals) from he regression model: e i = (y i y i ) < Assumpions: The underlying relaion is linear. The model errors are independen The errors have a consan variance The errors are normally disribued These residual plos are used in muliple regression: Residuals vs. Fied values of y Hisogram of he residuals PP plo for normaliy Residuals vs. ime (if ime series daa) Use he residual plos o check for violaions of regression assumpions

33 Regression plos in SPSS

34 * Serial correlaion also called auocorrelaion Auocorrelaion in he residuals is caused by a couple of reasons: Omission of criical variables from he model: since many economic variables end o exhibi an auocorrelaed paern, if an auocorrelaed explanaory variable has been excluded from he regression model, is influence will be echoed in he residuals. Using he incorrec mahemaical form of he model: if he mahemaical form of he model used is significanly differen from he rue form of he relaionship, li he residual may show he serial correlaion. For example, if a linear model is used insead of a muliplicaive model, he residual may be serially correlaed. 172 Auocorrelaed Errors Independence of Errors Error values are saisically independen Auocorrelaed Errors Residuals in one ime period arerelaed o Residuals in one ime period are relaed o residuals in anoher period 34

35 Auocorrelaed Errors Auocorrelaion violaes a leas squares regression assumpion Leads o s b esimaes ha are oo small (i.e., biased) Thus values are oo large and some variables may appear significan when hey are no (coninued) Auocorrelaion Auocorrelaion is correlaion of he errors ( id l ) i (residuals) over ime Time () Residual Plo Here, residuals show a cyclic paern, no random Residuals Time () Violaes he regression assumpion ha residuals are random and independen 35

36 Residual Analysis for Independence No Independen Independen residuals X res siduals X residuals X The Durbin Wason Saisic The Durbin Wason saisic is used o es for auocorrelaion H 0 : successive residuals are no correlaed (i.e., Corr(ε,ε 1 ) = 0) H 1 : auocorrelaion is presen If auocorrelaion is deeced, he OLS mehod of esimaing he coefficiens canno be used. 36

37 The Durbin Wason Saisic H 0 : ρ = 0 (no auocorrelaion) H 1 : auocorrelaion i is presen The Durbin Wason es saisic (d): d n 2 (e 2 e 1) n 1 e 2 The possible range is 0 d 4 d should be close o 2 if H 0 is rue d less han 2 may signal posiive auocorrelaion, d greaer han 2 may signal negaive auocorrelaion Tesing for Posiive Auocorrelaion H 0 : posiive auocorrelaion does no exis H 1 : posiive auocorrelaion is presen Calculae he Durbin Wason es saisic = d d can be approximaed by d = 2(1 r), where r is he sample correlaion of successive errors Find he values d L and d U from he Durbin Wason able (for sample size n and number of independen variables K) Decision rule: rejec H 0 if d < d L Rejec H 0 Inconclusive Do no rejec H 0 0 d L d U 2 37

38 Negaive Auocorrelaion Negaive auocorrelaion exiss if successive errorsarenegaively correlaed This can occur if successive errors alernae in sign Decision rule for negaive auocorrelaion: rejec H 0 if d > 4 d L ρ 0 ρ 0 Do no rejec H 0 Rejec H 0 Inconclusive Inconclusive Rejec H 0 0 d L d U 2 4 d U 4 d L 4 Tesing for Posiive Auocorrelaion Example wih n = 25: (coninued) Durbin-Wason Calculaions Sum of Squared Difference of Residuals Sum of Squared Residuals Durbin-Wason Saisic Sales y = x R 2 = Time d n 2 (e e n 1 e 2 )

39 Tesing for Posiive Auocorrelaion Here, n = 25 and here is K = 1 independen variable Using he Durbin Wason able, d L = and d U = (coninued) D = < d L = 1.29, so rejec H 0 and conclude ha significan posiive auocorrelaion exiss Therefore he linear model is no he appropriae model o forecas sales Decision: rejec H 0 since D = < d L Rejec H 0 Inconclusive Do no rejec H 0 0 d d U = L =1.29 Esimaion of Regression Models wih Auocorrelaed Errors Suppose ha we wan o esimae he coefficiens of he regression model y β 0 β x 1 1 β 2 x 2 β K x K ε where he error erm ε is auocorrelaed Two seps: (i) Esimae he model by leas squares, obaining he Durbin Wason saisic, d, and hen esimae he auocorrelaion parameer using r 1 d 2 39

40 Esimaion of Regression Models wih Auocorrelaed Errors (coninued) (ii) Esimae by leas squares a second regression wih dependen variable (Y ry 1 ) independen variables (X 1 rx 1, 1 ), (X 2 rx 2, 1 ),..., (X K rx K, 1 ) The parameers 1, 2,..., k are esimaed regression coefficiens from he second model An esimae of 0 is obained by dividing he esimaed inercep for he second model by (1 r) Hypohesis ess and confidence inervals for he regression coefficiens can be carried ou using he oupu from he second model Heeroscedasiciy Homoscedasiciy The probabiliy disribuion of he errors has consan variance Heeroscedasiciy The error erms do no all have he same variance The size of he error variances may depend on he size of he dependen variable value, for example 40

41 Heeroscedasiciy (coninued) When heeroscedasiciy is presen: leas squares is no he mos efficien procedure o esimae regression coefficiens The usual procedures for deriving confidence inervals and ess of hypoheses is no valid Residual Analysis for Homoscedasiciy Y Y x x residuals Non consan variance x residuals Consan variance x 41

42 Tess for Heeroscedasiciy To es he null hypohesis ha he error erms, ε i, all have he same variance agains he alernaive i ha heir variances depend on he expeced values ŷ i Esimae he simple regression e 2 i a 0 a yˆ 1 i Le R 2 be he coefficien of deerminaion of his new regression The null hypohesis is rejeced if nr 2 is greaer han 2 1, where 2 1, is he criical value of he chi square random variable wih 1 degree of freedom and probabiliy of error Generaion of a forecas model by MRA 1. Invesigae all he facors (explanaory variables) ha will influence he dependen variable (e.g. sales) and caegorize he daa by ype. 2. Describe he appropriae mahemaical form of he regression model o use given he available daa ypes. 3. Examine he relaionship beween he explanaory variable and he dependen variables using correlaion marix. 4. Selec he variables for model calibraion and esimae he model. This sep also involves evaluaing he model properies. coninued

43 Generaion of a forecas model by MRA 5. Inerpre coefficiens for explanaory variables, confirming heir saisical significance and raionalizing heir relaive size and sign (posiive/negaive). 6. Tes and evaluae he model. 7. Use he model o generae a forecas, applying he regression equaion o daa beyond ha used o creae he model. 8. Sae conclusions abou he qualiy of he model (e.g., abiliy o predic reliable oucomes). 190 Sep 1: Invesigae all facors influencing he forecas variable MRA involves esimaing he value of one variable based on daa from oher variables. For he jewelery sales (JS) forecas, key influencing facors could be: Disposable personal income (DPI) expeced sign of coefficien is posiive (posiive relaion bw JS and DPI) The unemploymen rae (UR) expeced sign negaive (likely inverse relaion bw JS and DPI) Thus: Dependen variable: JS Independen variables: DPI (in consan 1996 dollars) UR The wo independen variables are boh demand side facors. All hree variables are ime series daa. In considering he se of independen variables o use, we should find ones ha are no highly correlaed wih one anoher (Because of mulicollineariy problem)

. The developer would have o eiher purchase a forecas of DPI and UR from a forecasing agency or develop heir own forecas.")

44 JewelrySales versus Disposable Personal Income and Unemploymen 3 dimenional scaer As UR increases, JS decrease (while DPI is held consan) As DPI increases (while UR is held consan), JS increases. 192 Pracice Noe: Forecasing Explanaory Variables In selecing explanaory variables for a forecas model, a crucial limiaion is ha a forecas of hese variables is required. For insance, if he developer selecs he disposablepersonal l income (DPI) and unemploymen rae (UR) as he explanaory variables for he jewelery sales regression model, hen he developer will need a forecas of hese variables in order o generae a forecas of jewelery sales (JS). The developer would have o eiher purchase a forecas of DPI and UR from a forecasing agency or develop heir own forecas. The regression model specifies he relaionship beween he independen variables and he dependen variable. Therefore, if he fuure values of he independen variables are available hen he relaionship can be used calculae he fuure values of he dependen variable. However, i is imporan ha he forecas of he independen variables be reliable. For his reason, i is good pracice o choose independen variables ha are regularly forecas by an independen saisical agency like TUİK

45 Sep 2: The mahemaical form of he regression model The mos basic regression analysis mehod Ordinary Leas Squares (OLS) OLS is referred o in boh Excel and SPSS as "linear regression". The mahemaical form of he regression model is essenially an equaion y f ( x) When building a forecas model, we sar wih a specific equaion. This is called model specificaion. The relaionship could be linear and non linear. Various mahemaical forms could be aemped If he model properies do no work ou when calibraing, i can be respecified by replacing he variables on he righ hand side wih ohers ha seem o provide a more clear explanaion of he forecas variable. 194 Model specificaion for Jewelery Sales MRA The relaionship iniially examined beween he explanaory variables (DPI, UR) and dependen variable (JS) for our forecas model is: JS β β1 DPI β2 UR 0 For his model, he esimaed equaion would be: J Sˆ b This is a linear model, because all he parameers appear as muliples of he variables or he consan, and are added ogeher. 0 b1 DPI b 2 UR ε

46 Linear Models J Sˆ JSˆ b b Srucural Examples J Sˆ b0 b1 DPI 0 b1 DPI 0 b 1 DPI b 2 b UR 2 DPI 2 Non Linear Models J Sˆ b * DPI J Sˆ 0 b * DPI 0 b 1 b * UR 1 b Modelling Limiaions The model is a simplified represenaion of a real world relaionship. li Jus as archiecs build simplified models of buildings, analyss build simplified models of he world. By necessiy, hese models mus leave ou some informaion, bu hopefully capure he imporan pars of he relaionship

47 Sep 3: Examine he relaionship beween he explanaory variable and he dependen variables Analyze Correlae Bivariae The bes model is one where he explanaory variables are highly correlaed wih he dependen variable, and where he explanaory variables are no relaed o each oher. 198 Sep 4: Selec he variables for model calibraion and esimae he model Model Calibraion To evaluae a regression model, here are hree key saisics o consider: 1. The Durbin Wason (DW) saisic 2. The F saisic 3. The Adjused R 2 Saisics Used in Evaluaing Regression Models

48 Adjused R 2 The adjused R squared is an adjused measure of he coefficien of deerminaion (R 2 ). Adding variables o a regression will almos always increase he R 2, because mos variables will have some correlaion wih he dependen variable, even if ha correlaion is very low. The adjused R 2 is useful in helping he analys achieve he wo objecives in designing a model: Explain as much of he dependen variable as possible. Make he model as simple as possible

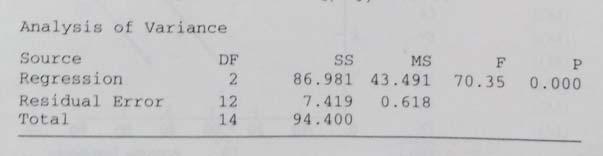

49 Oupus for JS muliple regression model The adjused R Square is quie low. Because many of he daa poins are quie a disance above or below he esimaed regression plane. The regression equaion explains only 7.5% of he variaion in jewelery sales volume. For n=144, α=0,05, k=2 independen variables: d L = 1,63 d U =1,72 (from Durbin Wason able) d L = 1,63 d U =1,72 4 d U = 2,28 4 d L = 2,37 There is no serial correlaion in he regression residuals 202 The ANOVA able shows he F saisic is relaively large and significan (an F Value above 4 is generally considered significan)

50 Sep 5: Inerpreing Coefficiens The unsandardized coefficiens (B): These are he esimaed coefficien values ( ). The value shows he relaionship of he explanaory variable on he dependen variable. The coefficien represens he parial effec of he independen variable on he dependen variable, holding all oher effecs consan. For example, if he variable coefficien is 10, hen a one uni change in he explanaory variable (also called he "regressor") will increase he dependen variable by 10. The sandardized coefficiens (Bea): The Bea value indicaes he relaive imporance of he variable in he model. A high absolue value indicaes ha he variable is very imporan while a low value indicaes ha he variable conribues lile o he model's predicive capaciy. Sd. Error (sandard error): This is he sandard error of he coefficien. This is required o deermine wheher he esimaed coefficien is significanly differen from zero. We usually wan he sandard error of he esimae o be less han half he size of he coefficien. The sandard error is required o calculae he value. The value: The value is calculaed by dividing he coefficien by he sandard error. The saisic deermines if he esimaed coefficien is significanly differen from zero. A value above 2 is considered significan. However, he saisic here can be ignored, because he "Sig" column inerpres is saisical significance for us. Sig. (Significance): The "Sig." column provides he significance level of he coefficien. The lower he Sig. Value, he higher he significance of he variable in he model. Usually, we require a level of significance smaller han 0.05 (95% confidence level), wih his indicaing fair confidence ha he coefficien is no equal o zero. In oher words, we can be quie sure ha his variable has a leas some parial influence on he arge variable, holding oher variables consan. If a variable is found o no be significan by a wide margin, you should srongly consider removing i from he equaion. 204 Sandardized bea (Bea) values are measured in sandard deviaion unis and so are direcly comparable. The "Bea" value is highes for DPI (.275), showing his o be he mos imporan variable in he regression. DPI has more impac in he model, his predicor is making a significan conribuion o he model. UR is insignifican, p value = 0,484 < 0,05. Signs of he coefficiens are esimaed as expeced. As he adjused R Square is quie low, he regression model needs o be improved

51 206 Mulicollineariy Where explanaory variables are relaed o each oher, he model suffers from mulicollineariy. This causes low significance of coefficiens and a high F saisic for he regression, meaning resuls may be unreliable or misleading in predicing he dependen variable

52 Suggesed mehods for removing mulicollineariy for regression esimaion. Remove one of he srongly correlaed explanaory variables from he model building process. If possible, generae a single new variable ha incorporaes informaion from boh correlaed explanaory variables. The variable selecion process should be resriced o explanaory variable ha have zero or only modes amouns of collineariy. Generally, o avoid mulicollineariy, any correlaion over +/ 0.5 should be examined, alhough hese correlaions do no usually creae serious collineariy problems unil hey are over +/ he coefficien able includes wo more columns: Tolerance and VIF. The variable's olerance describes he proporion of variance explained by his one variable ha is no explained by any oher variable. If he olerance is low (less hen 0.3), hen he variable could be deleed from he model wih lile loss of informaion. The VIF is he "variance inflaion facor". I is large if he variable is collinear wih oher variables and small if he variables are independen from one anoher. Ideally, he VIFs will all be less han 3.3 (he olerance and VIF are direcly relaed, wih VIF = 1/Tolerance)

53 Collineariy Saisics for JS regression The collineariy saisics show no evidence of a mulicollineariy problem. VIF=~ 1 < Example of a mulicollineariy problem The above coefficiens able indicaes he presence of mulicollineariy as he VIF value for he T Bill rae and 5 year morgage rae is well above 3.3. The correlaion beween hese variables.is 0.957, hus he T Bill variable is removed and regression model is redeveloped

54 Dummy Variables Accouning for Seasonaliy in a MR model Can be used o measure a qualiaive aribue as seasons, gender, inervenions, i ec

55 Using Regression o forecas seasonal daa 55

56 Time relaed explanaory variables Seasonal dummy variables Assumpion: he seasonal componen is unchanging from year o year D1=1 if hemonh h is January, 0 oherwise; D2=1 if he monh is February, 0 oherwise;.. D11=1 if he monh is November, 0 oherwise. Trading day variaion Assumpion: sales daa ofen vary according o he day of he week T1 = he number of imes Monday occurred in ha monh; T2 = he number of imes Tuesday occurred in ha monh;.. T7 = he number of imes Sunday occurred in ha monh. Time relaed explanaory variables Variable holiday effecs The effec of New Year on monhly sales daa Use seasonaldummy variable for December The effec of Ramadan Bairam I can occur in differen monhs every year V = 1 ifanyparof he Ramadan period falls in ha monh and zero oherwise. Inervenions Can occur when here is some ouside influence a a paricular ime which affecs he forecas variable. E.g. Inroducion of sea bels may have caused he number of road faaliies oundergo a levellshif downward. d To measure he effec of he sea bel inroducion Use a dummy variable consising of 0 s before he inroducion of sea bels and 1 s afer ha monh. 56

adverising expendiure: A1 = adverising expendiure for he previous monh; A2 = adverising expendiure for wo monhs previously;.")

57 Time relaed explanaory variables Adverising expendiure he effec of adverising which lass for some ime beyond he acual adverising campaign. To include several weeks (or monhs) adverising expendiure: A1 = adverising expendiure for he previous monh; A2 = adverising expendiure for wo monhs previously;.. A1 = adverising expendiure for m monhs previously. Improvemens in JS regression model Remember JS ime series is quie seasonal wih some rend. Adding Dummy Variables Accouning for Seasonaliy Seasonal dummy variables for he 11 monhs of each year February hrough December. Effec of 9 Sepember A dummy variable for 911 effec ha equals 1 in Sepember and Ocober

58 Rerunning he regression model 220 Adjused R 2 has increased from 7,5 o 96,6 percen. Sandard Error of regression has fallen TheF saisics has increased Durbin Wason saisics indicaes ha no firs order serial correlaion is presen

59 Model coefficiens have he correc signs and are saisically significan, as indicaed by he high values and he corresponding low Sig. values. Consan erm and 911 effec are no significan and do no conribue o he model. The collineariy saisics show no evidence of a mulicollineariy problem

exhibi")

60 Pu simply, we wan a model where he residuals or errors (he difference beween he acual value of JS and he esimaed value) exhibi a paern ha mees specified crierion or properies. The errors are approximaely normally disribued The errors have no a consan variance!! Use ransformaion for improvemen. 224 Variable Transformaions Four mos common funcions The reciprocal The log (or Ln) The square roo The square

61

62 Sep 6: Use he Model o Generae a Forecas If he esimaed model is valid (boh saisically and hrough judgmen), we can use he resuls o generae a fuure forecas. We would only be comforable using he equaion o produce a forecas if we were fairly sure eiher ha: a. The independen variables acually cause he values of he prediced variable; or b. he relaionship ha shows correlaion beween he variable o be forecas and he variables in he equaion is likely o coninue. 228 Appendix: Correcing Heeroskedasiciy For auocorrelaion funcion: Choose Analyze Forecasing Auocorrelaions i Naural log ransform. For ARIMA: Choose Analyze Forecasing Creae Models. Under "Mehod", choose ARIMA; clickcrieria and selec Naural log ransform under "Transformaion"

Time series Decomposition method

Time series Decomposiion mehod A ime series is described using a mulifacor model such as = f (rend, cyclical, seasonal, error) = f (T, C, S, e) Long- Iner-mediaed Seasonal Irregular erm erm effec, effec,

Time series Decomposiion mehod A ime series is described using a mulifacor model such as = f (rend, cyclical, seasonal, error) = f (T, C, S, e) Long- Iner-mediaed Seasonal Irregular erm erm effec, effec,

Econ107 Applied Econometrics Topic 7: Multicollinearity (Studenmund, Chapter 8)

") I. Definiions and Problems A. Perfec Mulicollineariy Econ7 Applied Economerics Topic 7: Mulicollineariy (Sudenmund, Chaper 8) Definiion: Perfec mulicollineariy exiss in a following K-variable regression

I. Definiions and Problems A. Perfec Mulicollineariy Econ7 Applied Economerics Topic 7: Mulicollineariy (Sudenmund, Chaper 8) Definiion: Perfec mulicollineariy exiss in a following K-variable regression

R t. C t P t. + u t. C t = αp t + βr t + v t. + β + w t

Exercise 7 C P = α + β R P + u C = αp + βr + v (a) (b) C R = α P R + β + w (c) Assumpions abou he disurbances u, v, w : Classical assumions on he disurbance of one of he equaions, eg. on (b): E(v v s P,

Exercise 7 C P = α + β R P + u C = αp + βr + v (a) (b) C R = α P R + β + w (c) Assumpions abou he disurbances u, v, w : Classical assumions on he disurbance of one of he equaions, eg. on (b): E(v v s P,

Solutions to Odd Number Exercises in Chapter 6

1 Soluions o Odd Number Exercises in 6.1 R y eˆ 1.7151 y 6.3 From eˆ ( T K) ˆ R 1 1 SST SST SST (1 R ) 55.36(1.7911) we have, ˆ 6.414 T K ( ) 6.5 y ye ye y e 1 1 Consider he erms e and xe b b x e y e b

1 Soluions o Odd Number Exercises in 6.1 R y eˆ 1.7151 y 6.3 From eˆ ( T K) ˆ R 1 1 SST SST SST (1 R ) 55.36(1.7911) we have, ˆ 6.414 T K ( ) 6.5 y ye ye y e 1 1 Consider he erms e and xe b b x e y e b

ACE 562 Fall Lecture 8: The Simple Linear Regression Model: R 2, Reporting the Results and Prediction. by Professor Scott H.

ACE 56 Fall 5 Lecure 8: The Simple Linear Regression Model: R, Reporing he Resuls and Predicion by Professor Sco H. Irwin Required Readings: Griffihs, Hill and Judge. "Explaining Variaion in he Dependen

ACE 56 Fall 5 Lecure 8: The Simple Linear Regression Model: R, Reporing he Resuls and Predicion by Professor Sco H. Irwin Required Readings: Griffihs, Hill and Judge. "Explaining Variaion in he Dependen

Licenciatura de ADE y Licenciatura conjunta Derecho y ADE. Hoja de ejercicios 2 PARTE A

Licenciaura de ADE y Licenciaura conjuna Derecho y ADE Hoja de ejercicios PARTE A 1. Consider he following models Δy = 0.8 + ε (1 + 0.8L) Δ 1 y = ε where ε and ε are independen whie noise processes. In

Licenciaura de ADE y Licenciaura conjuna Derecho y ADE Hoja de ejercicios PARTE A 1. Consider he following models Δy = 0.8 + ε (1 + 0.8L) Δ 1 y = ε where ε and ε are independen whie noise processes. In

Chapter 15. Time Series: Descriptive Analyses, Models, and Forecasting

Chaper 15 Time Series: Descripive Analyses, Models, and Forecasing Descripive Analysis: Index Numbers Index Number a number ha measures he change in a variable over ime relaive o he value of he variable

Chaper 15 Time Series: Descripive Analyses, Models, and Forecasing Descripive Analysis: Index Numbers Index Number a number ha measures he change in a variable over ime relaive o he value of he variable

ACE 562 Fall Lecture 5: The Simple Linear Regression Model: Sampling Properties of the Least Squares Estimators. by Professor Scott H.

ACE 56 Fall 005 Lecure 5: he Simple Linear Regression Model: Sampling Properies of he Leas Squares Esimaors by Professor Sco H. Irwin Required Reading: Griffihs, Hill and Judge. "Inference in he Simple

ACE 56 Fall 005 Lecure 5: he Simple Linear Regression Model: Sampling Properies of he Leas Squares Esimaors by Professor Sco H. Irwin Required Reading: Griffihs, Hill and Judge. "Inference in he Simple

ECON 482 / WH Hong Time Series Data Analysis 1. The Nature of Time Series Data. Example of time series data (inflation and unemployment rates)

") ECON 48 / WH Hong Time Series Daa Analysis. The Naure of Time Series Daa Example of ime series daa (inflaion and unemploymen raes) ECON 48 / WH Hong Time Series Daa Analysis The naure of ime series daa

ECON 48 / WH Hong Time Series Daa Analysis. The Naure of Time Series Daa Example of ime series daa (inflaion and unemploymen raes) ECON 48 / WH Hong Time Series Daa Analysis The naure of ime series daa

The Simple Linear Regression Model: Reporting the Results and Choosing the Functional Form

Chaper 6 The Simple Linear Regression Model: Reporing he Resuls and Choosing he Funcional Form To complee he analysis of he simple linear regression model, in his chaper we will consider how o measure

Chaper 6 The Simple Linear Regression Model: Reporing he Resuls and Choosing he Funcional Form To complee he analysis of he simple linear regression model, in his chaper we will consider how o measure

Econ Autocorrelation. Sanjaya DeSilva

Econ 39 - Auocorrelaion Sanjaya DeSilva Ocober 3, 008 1 Definiion Auocorrelaion (or serial correlaion) occurs when he error erm of one observaion is correlaed wih he error erm of any oher observaion. This

Econ 39 - Auocorrelaion Sanjaya DeSilva Ocober 3, 008 1 Definiion Auocorrelaion (or serial correlaion) occurs when he error erm of one observaion is correlaed wih he error erm of any oher observaion. This

Comparing Means: t-tests for One Sample & Two Related Samples

Comparing Means: -Tess for One Sample & Two Relaed Samples Using he z-tes: Assumpions -Tess for One Sample & Two Relaed Samples The z-es (of a sample mean agains a populaion mean) is based on he assumpion

Comparing Means: -Tess for One Sample & Two Relaed Samples Using he z-tes: Assumpions -Tess for One Sample & Two Relaed Samples The z-es (of a sample mean agains a populaion mean) is based on he assumpion

Summer Term Albert-Ludwigs-Universität Freiburg Empirische Forschung und Okonometrie. Time Series Analysis

Summer Term 2009 Alber-Ludwigs-Universiä Freiburg Empirische Forschung und Okonomerie Time Series Analysis Classical Time Series Models Time Series Analysis Dr. Sevap Kesel 2 Componens Hourly earnings:

Summer Term 2009 Alber-Ludwigs-Universiä Freiburg Empirische Forschung und Okonomerie Time Series Analysis Classical Time Series Models Time Series Analysis Dr. Sevap Kesel 2 Componens Hourly earnings:

ACE 562 Fall Lecture 4: Simple Linear Regression Model: Specification and Estimation. by Professor Scott H. Irwin

ACE 56 Fall 005 Lecure 4: Simple Linear Regression Model: Specificaion and Esimaion by Professor Sco H. Irwin Required Reading: Griffihs, Hill and Judge. "Simple Regression: Economic and Saisical Model

ACE 56 Fall 005 Lecure 4: Simple Linear Regression Model: Specificaion and Esimaion by Professor Sco H. Irwin Required Reading: Griffihs, Hill and Judge. "Simple Regression: Economic and Saisical Model

Diebold, Chapter 7. Francis X. Diebold, Elements of Forecasting, 4th Edition (Mason, Ohio: Cengage Learning, 2006). Chapter 7. Characterizing Cycles

. Chapter 7. Characterizing Cycles") Diebold, Chaper 7 Francis X. Diebold, Elemens of Forecasing, 4h Ediion (Mason, Ohio: Cengage Learning, 006). Chaper 7. Characerizing Cycles Afer compleing his reading you should be able o: Define covariance

Diebold, Chaper 7 Francis X. Diebold, Elemens of Forecasing, 4h Ediion (Mason, Ohio: Cengage Learning, 006). Chaper 7. Characerizing Cycles Afer compleing his reading you should be able o: Define covariance

1. Diagnostic (Misspeci cation) Tests: Testing the Assumptions

Tests: Testing the Assumptions") Business School, Brunel Universiy MSc. EC5501/5509 Modelling Financial Decisions and Markes/Inroducion o Quaniaive Mehods Prof. Menelaos Karanasos (Room SS269, el. 01895265284) Lecure Noes 6 1. Diagnosic

Business School, Brunel Universiy MSc. EC5501/5509 Modelling Financial Decisions and Markes/Inroducion o Quaniaive Mehods Prof. Menelaos Karanasos (Room SS269, el. 01895265284) Lecure Noes 6 1. Diagnosic

Estimation Uncertainty

Esimaion Uncerainy The sample mean is an esimae of β = E(y +h ) The esimaion error is = + = T h y T b ( ) = = + = + = = = T T h T h e T y T y T b β β β Esimaion Variance Under classical condiions, where

Esimaion Uncerainy The sample mean is an esimae of β = E(y +h ) The esimaion error is = + = T h y T b ( ) = = + = + = = = T T h T h e T y T y T b β β β Esimaion Variance Under classical condiions, where

Vectorautoregressive Model and Cointegration Analysis. Time Series Analysis Dr. Sevtap Kestel 1

Vecorauoregressive Model and Coinegraion Analysis Par V Time Series Analysis Dr. Sevap Kesel 1 Vecorauoregression Vecor auoregression (VAR) is an economeric model used o capure he evoluion and he inerdependencies

Vecorauoregressive Model and Coinegraion Analysis Par V Time Series Analysis Dr. Sevap Kesel 1 Vecorauoregression Vecor auoregression (VAR) is an economeric model used o capure he evoluion and he inerdependencies

Solutions: Wednesday, November 14

Amhers College Deparmen of Economics Economics 360 Fall 2012 Soluions: Wednesday, November 14 Judicial Daa: Cross secion daa of judicial and economic saisics for he fify saes in 2000. JudExp CrimesAll

Amhers College Deparmen of Economics Economics 360 Fall 2012 Soluions: Wednesday, November 14 Judicial Daa: Cross secion daa of judicial and economic saisics for he fify saes in 2000. JudExp CrimesAll

The Multiple Regression Model: Hypothesis Tests and the Use of Nonsample Information

Chaper 8 The Muliple Regression Model: Hypohesis Tess and he Use of Nonsample Informaion An imporan new developmen ha we encouner in his chaper is using he F- disribuion o simulaneously es a null hypohesis

Chaper 8 The Muliple Regression Model: Hypohesis Tess and he Use of Nonsample Informaion An imporan new developmen ha we encouner in his chaper is using he F- disribuion o simulaneously es a null hypohesis

OBJECTIVES OF TIME SERIES ANALYSIS

OBJECTIVES OF TIME SERIES ANALYSIS Undersanding he dynamic or imedependen srucure of he observaions of a single series (univariae analysis) Forecasing of fuure observaions Asceraining he leading, lagging

OBJECTIVES OF TIME SERIES ANALYSIS Undersanding he dynamic or imedependen srucure of he observaions of a single series (univariae analysis) Forecasing of fuure observaions Asceraining he leading, lagging

Distribution of Least Squares

Disribuion of Leas Squares In classic regression, if he errors are iid normal, and independen of he regressors, hen he leas squares esimaes have an exac normal disribuion, no jus asympoic his is no rue

Disribuion of Leas Squares In classic regression, if he errors are iid normal, and independen of he regressors, hen he leas squares esimaes have an exac normal disribuion, no jus asympoic his is no rue

Wednesday, November 7 Handout: Heteroskedasticity

Amhers College Deparmen of Economics Economics 360 Fall 202 Wednesday, November 7 Handou: Heeroskedasiciy Preview Review o Regression Model o Sandard Ordinary Leas Squares (OLS) Premises o Esimaion Procedures

Amhers College Deparmen of Economics Economics 360 Fall 202 Wednesday, November 7 Handou: Heeroskedasiciy Preview Review o Regression Model o Sandard Ordinary Leas Squares (OLS) Premises o Esimaion Procedures

3.1 More on model selection

3. More on Model selecion 3. Comparing models AIC, BIC, Adjused R squared. 3. Over Fiing problem. 3.3 Sample spliing. 3. More on model selecion crieria Ofen afer model fiing you are lef wih a handful of

3. More on Model selecion 3. Comparing models AIC, BIC, Adjused R squared. 3. Over Fiing problem. 3.3 Sample spliing. 3. More on model selecion crieria Ofen afer model fiing you are lef wih a handful of

Regression with Time Series Data

Regression wih Time Series Daa y = β 0 + β 1 x 1 +...+ β k x k + u Serial Correlaion and Heeroskedasiciy Time Series - Serial Correlaion and Heeroskedasiciy 1 Serially Correlaed Errors: Consequences Wih

Regression wih Time Series Daa y = β 0 + β 1 x 1 +...+ β k x k + u Serial Correlaion and Heeroskedasiciy Time Series - Serial Correlaion and Heeroskedasiciy 1 Serially Correlaed Errors: Consequences Wih

Solutions to Exercises in Chapter 12

Chaper in Chaper. (a) The leas-squares esimaed equaion is given by (b)!i = 6. + 0.770 Y 0.8 R R = 0.86 (.5) (0.07) (0.6) Boh b and b 3 have he expeced signs; income is expeced o have a posiive effec on

Chaper in Chaper. (a) The leas-squares esimaed equaion is given by (b)!i = 6. + 0.770 Y 0.8 R R = 0.86 (.5) (0.07) (0.6) Boh b and b 3 have he expeced signs; income is expeced o have a posiive effec on

Forecasting optimally

I) ile: Forecas Evaluaion II) Conens: Evaluaing forecass, properies of opimal forecass, esing properies of opimal forecass, saisical comparison of forecas accuracy III) Documenaion: - Diebold, Francis

I) ile: Forecas Evaluaion II) Conens: Evaluaing forecass, properies of opimal forecass, esing properies of opimal forecass, saisical comparison of forecas accuracy III) Documenaion: - Diebold, Francis

ACE 564 Spring Lecture 7. Extensions of The Multiple Regression Model: Dummy Independent Variables. by Professor Scott H.

ACE 564 Spring 2006 Lecure 7 Exensions of The Muliple Regression Model: Dumm Independen Variables b Professor Sco H. Irwin Readings: Griffihs, Hill and Judge. "Dumm Variables and Varing Coefficien Models

ACE 564 Spring 2006 Lecure 7 Exensions of The Muliple Regression Model: Dumm Independen Variables b Professor Sco H. Irwin Readings: Griffihs, Hill and Judge. "Dumm Variables and Varing Coefficien Models

Financial Econometrics Jeffrey R. Russell Midterm Winter 2009 SOLUTIONS

Name SOLUTIONS Financial Economerics Jeffrey R. Russell Miderm Winer 009 SOLUTIONS You have 80 minues o complee he exam. Use can use a calculaor and noes. Try o fi all your work in he space provided. If

Name SOLUTIONS Financial Economerics Jeffrey R. Russell Miderm Winer 009 SOLUTIONS You have 80 minues o complee he exam. Use can use a calculaor and noes. Try o fi all your work in he space provided. If

Types of Exponential Smoothing Methods. Simple Exponential Smoothing. Simple Exponential Smoothing

M Business Forecasing Mehods Exponenial moohing Mehods ecurer : Dr Iris Yeung Room No : P79 Tel No : 788 8 Types of Exponenial moohing Mehods imple Exponenial moohing Double Exponenial moohing Brown s

M Business Forecasing Mehods Exponenial moohing Mehods ecurer : Dr Iris Yeung Room No : P79 Tel No : 788 8 Types of Exponenial moohing Mehods imple Exponenial moohing Double Exponenial moohing Brown s

4.1 Other Interpretations of Ridge Regression

CHAPTER 4 FURTHER RIDGE THEORY 4. Oher Inerpreaions of Ridge Regression In his secion we will presen hree inerpreaions for he use of ridge regression. The firs one is analogous o Hoerl and Kennard reasoning

CHAPTER 4 FURTHER RIDGE THEORY 4. Oher Inerpreaions of Ridge Regression In his secion we will presen hree inerpreaions for he use of ridge regression. The firs one is analogous o Hoerl and Kennard reasoning

Stationary Time Series

3-Jul-3 Time Series Analysis Assoc. Prof. Dr. Sevap Kesel July 03 Saionary Time Series Sricly saionary process: If he oin dis. of is he same as he oin dis. of ( X,... X n) ( X h,... X nh) Weakly Saionary

3-Jul-3 Time Series Analysis Assoc. Prof. Dr. Sevap Kesel July 03 Saionary Time Series Sricly saionary process: If he oin dis. of is he same as he oin dis. of ( X,... X n) ( X h,... X nh) Weakly Saionary

Properties of Autocorrelated Processes Economics 30331

Properies of Auocorrelaed Processes Economics 3033 Bill Evans Fall 05 Suppose we have ime series daa series labeled as where =,,3, T (he final period) Some examples are he dail closing price of he S&500,

Properies of Auocorrelaed Processes Economics 3033 Bill Evans Fall 05 Suppose we have ime series daa series labeled as where =,,3, T (he final period) Some examples are he dail closing price of he S&500,

Dynamic Econometric Models: Y t = + 0 X t + 1 X t X t k X t-k + e t. A. Autoregressive Model:

Dynamic Economeric Models: A. Auoregressive Model: Y = + 0 X 1 Y -1 + 2 Y -2 + k Y -k + e (Wih lagged dependen variable(s) on he RHS) B. Disribued-lag Model: Y = + 0 X + 1 X -1 + 2 X -2 + + k X -k + e

Dynamic Economeric Models: A. Auoregressive Model: Y = + 0 X 1 Y -1 + 2 Y -2 + k Y -k + e (Wih lagged dependen variable(s) on he RHS) B. Disribued-lag Model: Y = + 0 X + 1 X -1 + 2 X -2 + + k X -k + e

Robust estimation based on the first- and third-moment restrictions of the power transformation model

h Inernaional Congress on Modelling and Simulaion, Adelaide, Ausralia, 6 December 3 www.mssanz.org.au/modsim3 Robus esimaion based on he firs- and hird-momen resricions of he power ransformaion Nawaa,

h Inernaional Congress on Modelling and Simulaion, Adelaide, Ausralia, 6 December 3 www.mssanz.org.au/modsim3 Robus esimaion based on he firs- and hird-momen resricions of he power ransformaion Nawaa,

Vehicle Arrival Models : Headway

Chaper 12 Vehicle Arrival Models : Headway 12.1 Inroducion Modelling arrival of vehicle a secion of road is an imporan sep in raffic flow modelling. I has imporan applicaion in raffic flow simulaion where

Chaper 12 Vehicle Arrival Models : Headway 12.1 Inroducion Modelling arrival of vehicle a secion of road is an imporan sep in raffic flow modelling. I has imporan applicaion in raffic flow simulaion where

Distribution of Estimates

Disribuion of Esimaes From Economerics (40) Linear Regression Model Assume (y,x ) is iid and E(x e )0 Esimaion Consisency y α + βx + he esimaes approach he rue values as he sample size increases Esimaion

Disribuion of Esimaes From Economerics (40) Linear Regression Model Assume (y,x ) is iid and E(x e )0 Esimaion Consisency y α + βx + he esimaes approach he rue values as he sample size increases Esimaion

NCSS Statistical Software. , contains a periodic (cyclic) component. A natural model of the periodic component would be

component. A natural model of the periodic component would be") NCSS Saisical Sofware Chaper 468 Specral Analysis Inroducion This program calculaes and displays he periodogram and specrum of a ime series. This is someimes nown as harmonic analysis or he frequency approach

NCSS Saisical Sofware Chaper 468 Specral Analysis Inroducion This program calculaes and displays he periodogram and specrum of a ime series. This is someimes nown as harmonic analysis or he frequency approach

GMM - Generalized Method of Moments

GMM - Generalized Mehod of Momens Conens GMM esimaion, shor inroducion 2 GMM inuiion: Maching momens 2 3 General overview of GMM esimaion. 3 3. Weighing marix...........................................

GMM - Generalized Mehod of Momens Conens GMM esimaion, shor inroducion 2 GMM inuiion: Maching momens 2 3 General overview of GMM esimaion. 3 3. Weighing marix...........................................

How to Deal with Structural Breaks in Practical Cointegration Analysis

How o Deal wih Srucural Breaks in Pracical Coinegraion Analysis Roselyne Joyeux * School of Economic and Financial Sudies Macquarie Universiy December 00 ABSTRACT In his noe we consider he reamen of srucural

How o Deal wih Srucural Breaks in Pracical Coinegraion Analysis Roselyne Joyeux * School of Economic and Financial Sudies Macquarie Universiy December 00 ABSTRACT In his noe we consider he reamen of srucural

Unit Root Time Series. Univariate random walk

Uni Roo ime Series Univariae random walk Consider he regression y y where ~ iid N 0, he leas squares esimae of is: ˆ yy y y yy Now wha if = If y y hen le y 0 =0 so ha y j j If ~ iid N 0, hen y ~ N 0, he

Uni Roo ime Series Univariae random walk Consider he regression y y where ~ iid N 0, he leas squares esimae of is: ˆ yy y y yy Now wha if = If y y hen le y 0 =0 so ha y j j If ~ iid N 0, hen y ~ N 0, he

Lecture 3: Exponential Smoothing

NATCOR: Forecasing & Predicive Analyics Lecure 3: Exponenial Smoohing John Boylan Lancaser Cenre for Forecasing Deparmen of Managemen Science Mehods and Models Forecasing Mehod A (numerical) procedure

NATCOR: Forecasing & Predicive Analyics Lecure 3: Exponenial Smoohing John Boylan Lancaser Cenre for Forecasing Deparmen of Managemen Science Mehods and Models Forecasing Mehod A (numerical) procedure

Wisconsin Unemployment Rate Forecast Revisited

Wisconsin Unemploymen Rae Forecas Revisied Forecas in Lecure Wisconsin unemploymen November 06 was 4.% Forecass Poin Forecas 50% Inerval 80% Inerval Forecas Forecas December 06 4.0% (4.0%, 4.0%) (3.95%,

Wisconsin Unemploymen Rae Forecas Revisied Forecas in Lecure Wisconsin unemploymen November 06 was 4.% Forecass Poin Forecas 50% Inerval 80% Inerval Forecas Forecas December 06 4.0% (4.0%, 4.0%) (3.95%,

Outline. lse-logo. Outline. Outline. 1 Wald Test. 2 The Likelihood Ratio Test. 3 Lagrange Multiplier Tests

Ouline Ouline Hypohesis Tes wihin he Maximum Likelihood Framework There are hree main frequenis approaches o inference wihin he Maximum Likelihood framework: he Wald es, he Likelihood Raio es and he Lagrange

Ouline Ouline Hypohesis Tes wihin he Maximum Likelihood Framework There are hree main frequenis approaches o inference wihin he Maximum Likelihood framework: he Wald es, he Likelihood Raio es and he Lagrange

Chapter 11. Heteroskedasticity The Nature of Heteroskedasticity. In Chapter 3 we introduced the linear model (11.1.1)

") Chaper 11 Heeroskedasiciy 11.1 The Naure of Heeroskedasiciy In Chaper 3 we inroduced he linear model y = β+β x (11.1.1) 1 o explain household expendiure on food (y) as a funcion of household income (x).

Chaper 11 Heeroskedasiciy 11.1 The Naure of Heeroskedasiciy In Chaper 3 we inroduced he linear model y = β+β x (11.1.1) 1 o explain household expendiure on food (y) as a funcion of household income (x).

Methodology. -ratios are biased and that the appropriate critical values have to be increased by an amount. that depends on the sample size.

Mehodology. Uni Roo Tess A ime series is inegraed when i has a mean revering propery and a finie variance. I is only emporarily ou of equilibrium and is called saionary in I(0). However a ime series ha

Mehodology. Uni Roo Tess A ime series is inegraed when i has a mean revering propery and a finie variance. I is only emporarily ou of equilibrium and is called saionary in I(0). However a ime series ha

Nature Neuroscience: doi: /nn Supplementary Figure 1. Spike-count autocorrelations in time.

Supplemenary Figure 1 Spike-coun auocorrelaions in ime. Normalized auocorrelaion marices are shown for each area in a daase. The marix shows he mean correlaion of he spike coun in each ime bin wih he spike

Supplemenary Figure 1 Spike-coun auocorrelaions in ime. Normalized auocorrelaion marices are shown for each area in a daase. The marix shows he mean correlaion of he spike coun in each ime bin wih he spike

20. Applications of the Genetic-Drift Model

0. Applicaions of he Geneic-Drif Model 1) Deermining he probabiliy of forming any paricular combinaion of genoypes in he nex generaion: Example: If he parenal allele frequencies are p 0 = 0.35 and q 0

0. Applicaions of he Geneic-Drif Model 1) Deermining he probabiliy of forming any paricular combinaion of genoypes in he nex generaion: Example: If he parenal allele frequencies are p 0 = 0.35 and q 0

A Specification Test for Linear Dynamic Stochastic General Equilibrium Models

Journal of Saisical and Economeric Mehods, vol.1, no.2, 2012, 65-70 ISSN: 2241-0384 (prin), 2241-0376 (online) Scienpress Ld, 2012 A Specificaion Tes for Linear Dynamic Sochasic General Equilibrium Models

Journal of Saisical and Economeric Mehods, vol.1, no.2, 2012, 65-70 ISSN: 2241-0384 (prin), 2241-0376 (online) Scienpress Ld, 2012 A Specificaion Tes for Linear Dynamic Sochasic General Equilibrium Models

Hypothesis Testing in the Classical Normal Linear Regression Model. 1. Components of Hypothesis Tests

ECONOMICS 35* -- NOTE 8 M.G. Abbo ECON 35* -- NOTE 8 Hypohesis Tesing in he Classical Normal Linear Regression Model. Componens of Hypohesis Tess. A esable hypohesis, which consiss of wo pars: Par : a

ECONOMICS 35* -- NOTE 8 M.G. Abbo ECON 35* -- NOTE 8 Hypohesis Tesing in he Classical Normal Linear Regression Model. Componens of Hypohesis Tess. A esable hypohesis, which consiss of wo pars: Par : a

Exponential Weighted Moving Average (EWMA) Chart Under The Assumption of Moderateness And Its 3 Control Limits

Chart Under The Assumption of Moderateness And Its 3 Control Limits") DOI: 0.545/mjis.07.5009 Exponenial Weighed Moving Average (EWMA) Char Under The Assumpion of Moderaeness And Is 3 Conrol Limis KALPESH S TAILOR Assisan Professor, Deparmen of Saisics, M. K. Bhavnagar Universiy,

DOI: 0.545/mjis.07.5009 Exponenial Weighed Moving Average (EWMA) Char Under The Assumpion of Moderaeness And Is 3 Conrol Limis KALPESH S TAILOR Assisan Professor, Deparmen of Saisics, M. K. Bhavnagar Universiy,

Biol. 356 Lab 8. Mortality, Recruitment, and Migration Rates

Biol. 356 Lab 8. Moraliy, Recruimen, and Migraion Raes (modified from Cox, 00, General Ecology Lab Manual, McGraw Hill) Las week we esimaed populaion size hrough several mehods. One assumpion of all hese

Biol. 356 Lab 8. Moraliy, Recruimen, and Migraion Raes (modified from Cox, 00, General Ecology Lab Manual, McGraw Hill) Las week we esimaed populaion size hrough several mehods. One assumpion of all hese

Exponential Smoothing

Exponenial moohing Inroducion A simple mehod for forecasing. Does no require long series. Enables o decompose he series ino a rend and seasonal effecs. Paricularly useful mehod when here is a need o forecas

Exponenial moohing Inroducion A simple mehod for forecasing. Does no require long series. Enables o decompose he series ino a rend and seasonal effecs. Paricularly useful mehod when here is a need o forecas

Bias in Conditional and Unconditional Fixed Effects Logit Estimation: a Correction * Tom Coupé

Bias in Condiional and Uncondiional Fixed Effecs Logi Esimaion: a Correcion * Tom Coupé Economics Educaion and Research Consorium, Naional Universiy of Kyiv Mohyla Academy Address: Vul Voloska 10, 04070

Bias in Condiional and Uncondiional Fixed Effecs Logi Esimaion: a Correcion * Tom Coupé Economics Educaion and Research Consorium, Naional Universiy of Kyiv Mohyla Academy Address: Vul Voloska 10, 04070

Modeling and Forecasting Volatility Autoregressive Conditional Heteroskedasticity Models. Economic Forecasting Anthony Tay Slide 1

Modeling and Forecasing Volailiy Auoregressive Condiional Heeroskedasiciy Models Anhony Tay Slide 1 smpl @all line(m) sii dl_sii S TII D L _ S TII 4,000. 3,000.1.0,000 -.1 1,000 -. 0 86 88 90 9 94 96 98

Modeling and Forecasing Volailiy Auoregressive Condiional Heeroskedasiciy Models Anhony Tay Slide 1 smpl @all line(m) sii dl_sii S TII D L _ S TII 4,000. 3,000.1.0,000 -.1 1,000 -. 0 86 88 90 9 94 96 98

GDP Advance Estimate, 2016Q4

GDP Advance Esimae, 26Q4 Friday, Jan 27 Real gross domesic produc (GDP) increased a an annual rae of.9 percen in he fourh quarer of 26. The deceleraion in real GDP in he fourh quarer refleced a downurn

GDP Advance Esimae, 26Q4 Friday, Jan 27 Real gross domesic produc (GDP) increased a an annual rae of.9 percen in he fourh quarer of 26. The deceleraion in real GDP in he fourh quarer refleced a downurn

Smoothing. Backward smoother: At any give T, replace the observation yt by a combination of observations at & before T

Smoohing Consan process Separae signal & noise Smooh he daa: Backward smooher: A an give, replace he observaion b a combinaion of observaions a & before Simple smooher : replace he curren observaion wih

Smoohing Consan process Separae signal & noise Smooh he daa: Backward smooher: A an give, replace he observaion b a combinaion of observaions a & before Simple smooher : replace he curren observaion wih

Kriging Models Predicting Atrazine Concentrations in Surface Water Draining Agricultural Watersheds

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 Kriging Models Predicing Arazine Concenraions in Surface Waer Draining Agriculural Waersheds Paul L. Mosquin, Jeremy Aldworh, Wenlin Chen Supplemenal Maerial Number

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 Kriging Models Predicing Arazine Concenraions in Surface Waer Draining Agriculural Waersheds Paul L. Mosquin, Jeremy Aldworh, Wenlin Chen Supplemenal Maerial Number

Chapter 16. Regression with Time Series Data

Chaper 16 Regression wih Time Series Daa The analysis of ime series daa is of vial ineres o many groups, such as macroeconomiss sudying he behavior of naional and inernaional economies, finance economiss

Chaper 16 Regression wih Time Series Daa The analysis of ime series daa is of vial ineres o many groups, such as macroeconomiss sudying he behavior of naional and inernaional economies, finance economiss

Measurement Error 1: Consequences Page 1. Definitions. For two variables, X and Y, the following hold: Expectation, or Mean, of X.

Measuremen Error 1: Consequences of Measuremen Error Richard Williams, Universiy of Nore Dame, hps://www3.nd.edu/~rwilliam/ Las revised January 1, 015 Definiions. For wo variables, X and Y, he following

Measuremen Error 1: Consequences of Measuremen Error Richard Williams, Universiy of Nore Dame, hps://www3.nd.edu/~rwilliam/ Las revised January 1, 015 Definiions. For wo variables, X and Y, he following

A First Course on Kinetics and Reaction Engineering. Class 19 on Unit 18

A Firs ourse on Kineics and Reacion Engineering lass 19 on Uni 18 Par I - hemical Reacions Par II - hemical Reacion Kineics Where We re Going Par III - hemical Reacion Engineering A. Ideal Reacors B. Perfecly

A Firs ourse on Kineics and Reacion Engineering lass 19 on Uni 18 Par I - hemical Reacions Par II - hemical Reacion Kineics Where We re Going Par III - hemical Reacion Engineering A. Ideal Reacors B. Perfecly

y = β 1 + β 2 x (11.1.1)

") Chaper 11 Heeroskedasiciy 11.1 The Naure of Heeroskedasiciy In Chaper 3 we inroduced he linear model y = β 1 + β x (11.1.1) o explain household expendiure on food (y) as a funcion of household income (x).

Chaper 11 Heeroskedasiciy 11.1 The Naure of Heeroskedasiciy In Chaper 3 we inroduced he linear model y = β 1 + β x (11.1.1) o explain household expendiure on food (y) as a funcion of household income (x).

Explaining Total Factor Productivity. Ulrich Kohli University of Geneva December 2015

Explaining Toal Facor Produciviy Ulrich Kohli Universiy of Geneva December 2015 Needed: A Theory of Toal Facor Produciviy Edward C. Presco (1998) 2 1. Inroducion Toal Facor Produciviy (TFP) has become

Explaining Toal Facor Produciviy Ulrich Kohli Universiy of Geneva December 2015 Needed: A Theory of Toal Facor Produciviy Edward C. Presco (1998) 2 1. Inroducion Toal Facor Produciviy (TFP) has become

DEPARTMENT OF ECONOMICS

ISSN 0819-6 ISBN 0 730 609 9 THE UNIVERSITY OF MELBOURNE DEPARTMENT OF ECONOMICS RESEARCH PAPER NUMBER 95 NOVEMBER 005 INTERACTIONS IN REGRESSIONS by Joe Hirschberg & Jenny Lye Deparmen of Economics The

ISSN 0819-6 ISBN 0 730 609 9 THE UNIVERSITY OF MELBOURNE DEPARTMENT OF ECONOMICS RESEARCH PAPER NUMBER 95 NOVEMBER 005 INTERACTIONS IN REGRESSIONS by Joe Hirschberg & Jenny Lye Deparmen of Economics The

On Measuring Pro-Poor Growth. 1. On Various Ways of Measuring Pro-Poor Growth: A Short Review of the Literature

On Measuring Pro-Poor Growh 1. On Various Ways of Measuring Pro-Poor Growh: A Shor eview of he Lieraure During he pas en years or so here have been various suggesions concerning he way one should check

On Measuring Pro-Poor Growh 1. On Various Ways of Measuring Pro-Poor Growh: A Shor eview of he Lieraure During he pas en years or so here have been various suggesions concerning he way one should check

A Dynamic Model of Economic Fluctuations

CHAPTER 15 A Dynamic Model of Economic Flucuaions Modified for ECON 2204 by Bob Murphy 2016 Worh Publishers, all righs reserved IN THIS CHAPTER, OU WILL LEARN: how o incorporae dynamics ino he AD-AS model

CHAPTER 15 A Dynamic Model of Economic Flucuaions Modified for ECON 2204 by Bob Murphy 2016 Worh Publishers, all righs reserved IN THIS CHAPTER, OU WILL LEARN: how o incorporae dynamics ino he AD-AS model

Final Spring 2007

.615 Final Spring 7 Overview The purpose of he final exam is o calculae he MHD β limi in a high-bea oroidal okamak agains he dangerous n = 1 exernal ballooning-kink mode. Effecively, his corresponds o

.615 Final Spring 7 Overview The purpose of he final exam is o calculae he MHD β limi in a high-bea oroidal okamak agains he dangerous n = 1 exernal ballooning-kink mode. Effecively, his corresponds o

You must fully interpret your results. There is a relationship doesn t cut it. Use the text and, especially, the SPSS Manual for guidance.

POLI 30D SPRING 2015 LAST ASSIGNMENT TRUMPETS PLEASE!!!!! Due Thursday, December 10 (or sooner), by 7PM hrough TurnIIn I had his all se up in my mind. You would use regression analysis o follow up on your

POLI 30D SPRING 2015 LAST ASSIGNMENT TRUMPETS PLEASE!!!!! Due Thursday, December 10 (or sooner), by 7PM hrough TurnIIn I had his all se up in my mind. You would use regression analysis o follow up on your

DEPARTMENT OF STATISTICS

A Tes for Mulivariae ARCH Effecs R. Sco Hacker and Abdulnasser Haemi-J 004: DEPARTMENT OF STATISTICS S-0 07 LUND SWEDEN A Tes for Mulivariae ARCH Effecs R. Sco Hacker Jönköping Inernaional Business School

A Tes for Mulivariae ARCH Effecs R. Sco Hacker and Abdulnasser Haemi-J 004: DEPARTMENT OF STATISTICS S-0 07 LUND SWEDEN A Tes for Mulivariae ARCH Effecs R. Sco Hacker Jönköping Inernaional Business School

THE UNIVERSITY OF TEXAS AT AUSTIN McCombs School of Business

THE UNIVERITY OF TEXA AT AUTIN McCombs chool of Business TA 7.5 Tom hively CLAICAL EAONAL DECOMPOITION - MULTIPLICATIVE MODEL Examples of easonaliy 8000 Quarerly sales for Wal-Mar for quarers a l e s 6000

THE UNIVERITY OF TEXA AT AUTIN McCombs chool of Business TA 7.5 Tom hively CLAICAL EAONAL DECOMPOITION - MULTIPLICATIVE MODEL Examples of easonaliy 8000 Quarerly sales for Wal-Mar for quarers a l e s 6000

Introduction D P. r = constant discount rate, g = Gordon Model (1962): constant dividend growth rate.

: constant dividend growth rate.") Inroducion Gordon Model (1962): D P = r g r = consan discoun rae, g = consan dividend growh rae. If raional expecaions of fuure discoun raes and dividend growh vary over ime, so should he D/P raio. Since

Inroducion Gordon Model (1962): D P = r g r = consan discoun rae, g = consan dividend growh rae. If raional expecaions of fuure discoun raes and dividend growh vary over ime, so should he D/P raio. Since

Nonlinearity Test on Time Series Data

PROCEEDING OF 3 RD INTERNATIONAL CONFERENCE ON RESEARCH, IMPLEMENTATION AND EDUCATION OF MATHEMATICS AND SCIENCE YOGYAKARTA, 16 17 MAY 016 Nonlineariy Tes on Time Series Daa Case Sudy: The Number of Foreign

PROCEEDING OF 3 RD INTERNATIONAL CONFERENCE ON RESEARCH, IMPLEMENTATION AND EDUCATION OF MATHEMATICS AND SCIENCE YOGYAKARTA, 16 17 MAY 016 Nonlineariy Tes on Time Series Daa Case Sudy: The Number of Foreign

Dynamic Models, Autocorrelation and Forecasting

ECON 4551 Economerics II Memorial Universiy of Newfoundland Dynamic Models, Auocorrelaion and Forecasing Adaped from Vera Tabakova s noes 9.1 Inroducion 9.2 Lags in he Error Term: Auocorrelaion 9.3 Esimaing

ECON 4551 Economerics II Memorial Universiy of Newfoundland Dynamic Models, Auocorrelaion and Forecasing Adaped from Vera Tabakova s noes 9.1 Inroducion 9.2 Lags in he Error Term: Auocorrelaion 9.3 Esimaing

Math 10B: Mock Mid II. April 13, 2016

Name: Soluions Mah 10B: Mock Mid II April 13, 016 1. ( poins) Sae, wih jusificaion, wheher he following saemens are rue or false. (a) If a 3 3 marix A saisfies A 3 A = 0, hen i canno be inverible. True.

Name: Soluions Mah 10B: Mock Mid II April 13, 016 1. ( poins) Sae, wih jusificaion, wheher he following saemens are rue or false. (a) If a 3 3 marix A saisfies A 3 A = 0, hen i canno be inverible. True.

STAD57 Time Series Analysis. Lecture 5

STAD57 Time Series Analysis Lecure 5 1 Exploraory Daa Analysis Check if given TS is saionary: µ is consan σ 2 is consan γ(s,) is funcion of h= s If no, ry o make i saionary using some of he mehods below:

STAD57 Time Series Analysis Lecure 5 1 Exploraory Daa Analysis Check if given TS is saionary: µ is consan σ 2 is consan γ(s,) is funcion of h= s If no, ry o make i saionary using some of he mehods below:

Stability. Coefficients may change over time. Evolution of the economy Policy changes

Sabiliy Coefficiens may change over ime Evoluion of he economy Policy changes Time Varying Parameers y = α + x β + Coefficiens depend on he ime period If he coefficiens vary randomly and are unpredicable,

Sabiliy Coefficiens may change over ime Evoluion of he economy Policy changes Time Varying Parameers y = α + x β + Coefficiens depend on he ime period If he coefficiens vary randomly and are unpredicable,

The Effect of Nonzero Autocorrelation Coefficients on the Distributions of Durbin-Watson Test Estimator: Three Autoregressive Models

EJ Exper Journal of Economi c s ( 4 ), 85-9 9 4 Th e Au h or. Publi sh ed by Sp rin In v esify. ISS N 3 5 9-7 7 4 Econ omics.e xp erjou rn a ls.com The Effec of Nonzero Auocorrelaion Coefficiens on he

EJ Exper Journal of Economi c s ( 4 ), 85-9 9 4 Th e Au h or. Publi sh ed by Sp rin In v esify. ISS N 3 5 9-7 7 4 Econ omics.e xp erjou rn a ls.com The Effec of Nonzero Auocorrelaion Coefficiens on he

Cointegration and Implications for Forecasting

Coinegraion and Implicaions for Forecasing Two examples (A) Y Y 1 1 1 2 (B) Y 0.3 0.9 1 1 2 Example B: Coinegraion Y and coinegraed wih coinegraing vecor [1, 0.9] because Y 0.9 0.3 is a saionary process

Coinegraion and Implicaions for Forecasing Two examples (A) Y Y 1 1 1 2 (B) Y 0.3 0.9 1 1 2 Example B: Coinegraion Y and coinegraed wih coinegraing vecor [1, 0.9] because Y 0.9 0.3 is a saionary process

Lecture 4. Classical Linear Regression Model: Overview

Lecure 4 Classical Linear Regression Model: Overview Regression Regression is probably he single mos imporan ool a he economerician s disposal. Bu wha is regression analysis? I is concerned wih describing

Lecure 4 Classical Linear Regression Model: Overview Regression Regression is probably he single mos imporan ool a he economerician s disposal. Bu wha is regression analysis? I is concerned wih describing

RC, RL and RLC circuits

Name Dae Time o Complee h m Parner Course/ Secion / Grade RC, RL and RLC circuis Inroducion In his experimen we will invesigae he behavior of circuis conaining combinaions of resisors, capaciors, and inducors.

Name Dae Time o Complee h m Parner Course/ Secion / Grade RC, RL and RLC circuis Inroducion In his experimen we will invesigae he behavior of circuis conaining combinaions of resisors, capaciors, and inducors.

STRUCTURAL CHANGE IN TIME SERIES OF THE EXCHANGE RATES BETWEEN YEN-DOLLAR AND YEN-EURO IN

Inernaional Journal of Applied Economerics and Quaniaive Sudies. Vol.1-3(004) STRUCTURAL CHANGE IN TIME SERIES OF THE EXCHANGE RATES BETWEEN YEN-DOLLAR AND YEN-EURO IN 001-004 OBARA, Takashi * Absrac The

Inernaional Journal of Applied Economerics and Quaniaive Sudies. Vol.1-3(004) STRUCTURAL CHANGE IN TIME SERIES OF THE EXCHANGE RATES BETWEEN YEN-DOLLAR AND YEN-EURO IN 001-004 OBARA, Takashi * Absrac The

Forecasting. Summary. Sample StatFolio: tsforecast.sgp. STATGRAPHICS Centurion Rev. 9/16/2013

STATGRAPHICS Cenurion Rev. 9/16/2013 Forecasing Summary... 1 Daa Inpu... 3 Analysis Opions... 5 Forecasing Models... 9 Analysis Summary... 21 Time Sequence Plo... 23 Forecas Table... 24 Forecas Plo...

STATGRAPHICS Cenurion Rev. 9/16/2013 Forecasing Summary... 1 Daa Inpu... 3 Analysis Opions... 5 Forecasing Models... 9 Analysis Summary... 21 Time Sequence Plo... 23 Forecas Table... 24 Forecas Plo...

KINEMATICS IN ONE DIMENSION

KINEMATICS IN ONE DIMENSION PREVIEW Kinemaics is he sudy of how hings move how far (disance and displacemen), how fas (speed and velociy), and how fas ha how fas changes (acceleraion). We say ha an objec

KINEMATICS IN ONE DIMENSION PREVIEW Kinemaics is he sudy of how hings move how far (disance and displacemen), how fas (speed and velociy), and how fas ha how fas changes (acceleraion). We say ha an objec

Some Basic Information about M-S-D Systems

Some Basic Informaion abou M-S-D Sysems 1 Inroducion We wan o give some summary of he facs concerning unforced (homogeneous) and forced (non-homogeneous) models for linear oscillaors governed by second-order,

Some Basic Informaion abou M-S-D Sysems 1 Inroducion We wan o give some summary of he facs concerning unforced (homogeneous) and forced (non-homogeneous) models for linear oscillaors governed by second-order,

(10) (a) Derive and plot the spectrum of y. Discuss how the seasonality in the process is evident in spectrum.

(a) Derive and plot the spectrum of y. Discuss how the seasonality in the process is evident in spectrum.") January 01 Final Exam Quesions: Mark W. Wason (Poins/Minues are given in Parenheses) (15) 1. Suppose ha y follows he saionary AR(1) process y = y 1 +, where = 0.5 and ~ iid(0,1). Le x = (y + y 1 )/. (11)