Econ671 Factor Models: Principal Components

|

|

|

- Emery White

- 6 years ago

- Views:

Transcription

1 Econ671 Factor Models: Principal Components Jun YU April 8, 2016 Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

2 Factor Models: Principal Components Learning Objectives 1. Show how models in finance have a factor structure interpretation. 2. Understand principal components. 3. Deriving and interpreting an eigen decomposition. 4. A factor model of the term structure of interest rates. Background Reading 1. Matrices, Handout on course website - especially the section on eigenvalues and eigenvectors. EViews Computer Files 1. yields_us.wf1 2. yields_us_loadings.wf1 3. capm.wf1 Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

3 Introduction An important feature of many asset markets is that key variables (returns, yields, spreads etc) often display similar features. 1. Mean Asset markets tend to move together whereby the spreads between the key variables are stationary, even though these key variables may be nonstationary (cointegration). 2. Variance Periods of turbulence and tranquility tend to coincide across asset markets both locally and internationally, with the global financial crisis representing an example of synchronized turbulence. 3. Dynamics The dynamical behavior within classes of asset markets tend to exhibit very similar autocorrelation patterns. Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

4 Introduction Example (Term Structure of Interest Rates) The term structure of interest rates is the relationship between the yields of a bond for differing maturities The Figure shows that U.S. Treasury yields (%p.a.) for maturities from 1mthh to 10yrs, tend to move together. YIELD_M1 YIELD_M3 YIELD_M YIELD_Y1 YIELD_Y2 YIELD_Y YIELD_Y5 YIELD_Y7 YIELD_Y Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

5 Introduction Suggests that the time series characteristics of many financial variables can be summarized by a small set of factors. To formalise this model consider the following linear regression equation r i,t = α i + β i s t + u i,t where - r i,t is the return on the i th asset - s t is the factor (or set of factors) with parameters (vectors) α i, β i - u i,t is an unknown disturbance term representing idiosyncratic movements in r i,t. It is important to distinguish between two types of factors. 1. Observable s t 2. Unobservable s t Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

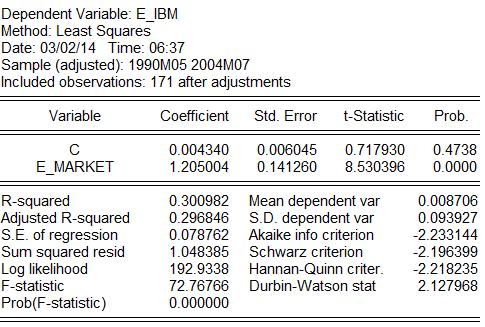

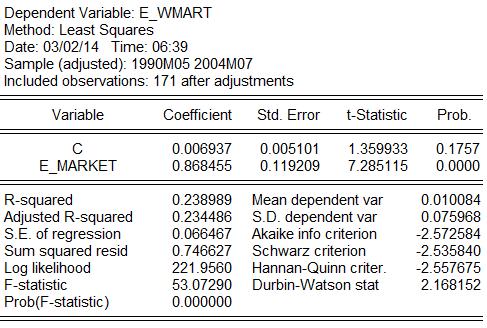

6 Introduction 1. Observable s t Time series are available on s t, whereby the parameter β i is estimated simply by regressing r i,t on s t. Typical examples of this type of model are CAPM, and the Fama-French three-factor model. Example (CAPM) The CAPM r i,t r f,t = α i + β i (r m,t r f,t ) + u i,t is estimated for 6 assets using monthly data for the U.S. beginning May 1990 and ending July The OLS parameter estimates are summarised below. Asset: Exxon GE Gold IBM Microsoft Walmart α i : β i : Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

7 Introduction 2. Unobservable s t Time series are not directly available on s t making the application of least squares to estimate α i and β i unworkable. There are two solutions: (a) Proxy variables A proxy variable is used instead of s t, but this creates errors in variables problems. In fact, this is a common strategy, if adopted only implicitly, with the application of the CAPM being a typical example. (b) Latent variables The statistical solution is to still treat s t as an unobservable variable, but to introduce additional structure on the model thereby providing additional information to enable the parameters to be estimated. This is the main focus of this and the next lecture! Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

8 Introduction If s t is latent it is not immediately obvious how the parameters of r i,t = α i + β i s t + u i,t can be identified when all of the terms on the right hand-side of the equation (i) Parameters : α i, β i (ii) Explanatory variables : s t (iii) Disturbance term : u i,t are unknown. Two broad methods are investigated to show how to address this identification problem. 1. Principal Components (this lecture) 2. Kalman Filter (next lecture) Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

9 The Role of Factors in Finance To motivate the role of factors in finance various models are presented, ranging from theoretical to purely statistical models. An important feature of this discussion is the distinction between factors that are observable and factors that are unobservable, that is latent. The examples consist of 1. Term Structure of Interest Rates 2. Capital Asset Pricing Model (CAPM) 3. Arbitrage Pricing Theory (APT) Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

10 The Role of Factors in Finance Term Structure of Interest Rates Inspection of the U.S. Treasury yields (%p.a.) for maturities from 1 month to 10 years, reveals two important characteristics. 1. The levels of the yields tend to move together. 2. Neighboring yields move together more closely than yields with greater differences in maturities. This latter empirical property of yields is highlighted by the following correlation matrix. corr = 1-mth 3-mth 6-mth 1-yr 2-yrs 3-yrs 5-yrs 7-yrs 10-yrs Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

11 The Role of Factors in Finance Term Structure of Interest Rates These two characteristics suggest that a potential model to explain the term structure of interest rates is given by at least a two-factor model r i,t = α i + β 1,i s 1,t + β 2,i s 2,t + u i,t, i = 1, 2,, 9, where u i,t is the disturbance term and s 1,t and s 2,t are the factors designed to Level factor (s 1,t ) : Slope factor (s 2,t ) : Capture the level of yields Capture the correlation between neighbouring yields As the two factors are implied by the data, they are latent factors. Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

12 The Role of Factors in Finance Capital Asset Pricing Model The CAPM r i,t r f,t = α i + β i (r m,t r f,t ) + u i,t represents a single factor model given by the excess return on the market r m,t r f,t, where the (market) factor is observable. Extending the model to allow for other observable factors including Fama-French factors, momentum, liquidity etc, generates a multi-factor CAPM. From a theoretical point of view, the use of r m,t in the model actually serves as a proxy for the excess return on all invested wealth. As this is an unobservable variable, the excess return on the market portfolio, r m,t r f,t, is essentially serving as a proxy. This suggests that the more theoretically correct CAPM specification is r i,t r f,t = α i + β i s t + u i,t where s t is now a latent factor representing the excess return on all invested wealth. Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

13 The Role of Factors in Finance Arbitrage Pricing Theory This is an alternative form of the CAPM equation where the (unknown) excess return on wealth is extended to the multi-factor version of the CAPM where all factors are unknown r i,t = α i + K j=1 β i,j s j,t + u i,t where there are K latent factors (s 1,t, s 2,t,, s K,t ) and as before u i,t is a disturbance term representing the idiosyncratic factor (risk). This is the arbitrage pricing model (APT) of Ross (1976). The factors and the disturbance term are assumed to have the following properties { 1 : j = k Factors : E [s j,t ] = 0, E [s j,t s k,t ] = { 0 : j = k σ 2 Disturbance : E [u i,t ] = 0, E [u i,t u k,t ] = i : i = k 0 : i = k Covariance : E [u i,t s j,t ] = 0 Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

.")

14 The Role of Factors in Finance Arbitrage Pricing Theory Historical Background: Stephen Ross (1943-) He is the inventor of Arbitrage Pricing Theory and also very well known for his work in finance including the CIR model of interest rates (he is the R ). Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

15 The Role of Factors in Finance Arbitrage Pricing Theory These assumptions imply a decomposition of the covariance matrix of r t = {r 1,t, r 2,t,, r N,t }. In the case of a K = 1 factor model (let β i = β i,1 for simplicity of notation) r i,t = α i + β i s 1,t + u i,t the covariance matrix is of the form (see the next tutorial for the derivation of this result) β σ2 1 β 1 β 2 β 1 β N β 2 β 1 β 2 2 cov(r t ) = + σ2 2 β 2 β N..... β N β 1 β N β 2 β 2 N + σ2 N This result shows that the covariance matrix can be reorganized into a factor structure which may be more informative about the movements in returns. Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

16 Principal Components Specification Consider the following model containing N asset returns r t = {r 1,t, r 2,t,, r N,t } and K N factors s t = {s 1,t, s 2,t,, s K,t } r 1,t r 2,t. α 1 α 2. = β 1,1 β 1,2 β 1,K β 2,1 β 2,2 β 2,K s 1,t s 2,t. + u 1,t u 2,t. r N,t α N β N,1 β N,2 β N,K s K,t u N,t or in matrix notation r t αµ = βs t + u t where - α is a (N 1) vector containing the means of r t. - s t is a (K 1) vector containing the factors. - β is a (N K ) matrix containing the factor loadings. - u t is a (N 1) vector of disturbances. Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

17 Principal Components Specification The vector of latent factors and the disturbance vector have the properties E [u t ] = 0, E [ u t u t ] = Ω E [s t = 0, E [ s t s t ] = I, E [ s t u t ] = 0, where Ω is a (N N) covariance matrix. As E [s t ] = E [u t ] = 0, the mean of the returns is E [r t ] = E [µ + βs t + u t ] = µ + βe [s t ] + E [u t ] = µ The factor equation r t α = βs t + u t shows that r t α can be decomposed into a systematic component (βs t ) and an idiosyncratic component (u t ). Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

18 Principal Components Specification Given the properties of s t and u t, the covariance structure of r t simplifies as cov (r t ) = E [ (r t α) (r t α) ] = E [ (βs t + u t ) (βs t + u t ) ] = βe [ s t s t ] β + βe [ s t u t ] [ + E ut s t ] β + E [ u t u t ] ββ = }{{} Systematic Risk + }{{} Ω Idiosyncratic Risk This equation shows that the covariance matrix can be decomposed in terms of two sources of factors/risks. 1. Systematic risk ( ββ ). 2. Idiosyncratic risk (Ω). Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

19 Principal Components Specification In the special case where the number of variables matches the number of factors (N = K ), there is an exact decomposition of the covariance matrix of r t as Ω = 0 in this case, with the covariance matrix cov (r t ) reducing to cov (r t ) = ββ = β 1 β 1 + β 2 β 2 + β N β N An important property of principal components is that they exhibit the same features as this equation cov (r t ) = λ 1 P 1 P 1 + λ 2 P 2 P λ N P N P N where λ i is the i th eigenvalue with (N 1) orthonormal eigenvector P i, that is, P i P i = 1 and P i P j = 0, i = j. A comparison of these equations suggests that the loading parameter vector β i be chosen as β i = λ i P i, i = 1, 2,, N Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

20 Principal Components Specification Now consider the N variances of r t = {r 1,t, r 2,t,, r N,t }, corresponding to the diagonal elements of cov (r t ) var (r 1,t ) var (r 2,t ). var (r N,t ) = λ 1 P 2 1,1 P 2 2,1. P 2 N,1 + λ 2 P 2 1,2 P 2 2,3. P 2 N,2 + + λ 1 P 2 1,N P 2 2,N. P 2 N,N Given that the eigenvectors are normalized as P i P i = 1, then the sum of the elements of each of the column vectors on the right hand-side all equal unity, that is P1,1 2 + P2 2,1 + + P2 N,1 = 1 P1,2 2 + P2 2,2 + + P2 N,2 = 1... P1,N 2 + P2 2,N + + P2 N,N = 1 Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

21 Principal Components Specification Thus a measure of the total volatility of all asset returns N var (r i,t ) = var (r 1,t ) + var (r 2,t ) + + var (r N,t ) i=1 is achieved by combining all of the variance equations as N ( var (r i,t ) = λ 1 P 2 1,1 + P2, P 2 ) N,1 i=1 ( +λ 2 P 2 1,2 + P2, PN,2 2 ) ( + + λ N P 2 1,N + P2,N PN,N 2 ) Given the normalization of the eigenvectors, this equation simplifies to N N var (r i,t ) = λ 1 + λ λ N = λ i i=1 i=1 That is, the total volatility of all r t equals the sum of all eigenvalues. Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

22 Principal Components Specification Instead of performing an eigen decomposition on the covariance matrix cov (r t ), to circumvent scaling issues when variables are measured in different units for example, the correlation matrix cor (r t ) can be used instead. In this case as the correlation matrix contains unity on the main diagonal by definition, then the sum of correlations becomes N λ i = N i=1 By inspecting the relative magnitude of the largest eigenvalues it is possible to quantify the proportion of the total variance of the data that is explained by K < N principal components. Bai and Ng (2002, Econometrica) propose a formal test of the number of factors based on information criteria. Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

23 The Role of Factors in Finance Specification Historical Background: Karl Pearson ( ) Inventor of Principal Components plus many other well-used and well-loved statistical techniques. Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

24 Principal Components Estimation In practice it is necessary to estimate the eigenvalues and the eigenvectors from the data. As an example consider the following correlation matrix of the 1-month, 1-year and 5-year U.S. Treasury yields given earlier cor (r t ) = The EViews commands to estimate the eigenvalues and eigenvectors of cor (r t ), highlight the 3 series and double click the shaded region and then click Open Group / View / Principal Components... / Calculation For Type: choose Correlation / OK The output is given in the following window. Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

25 Principal Components Estimation Source: EViews yields_us.wf1 Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

26 Principal Components Estimation The estimated eigenvalues and eigenvectors of the correlation matrix are respectively λ = 0.151, P = with the columns of P representing the three eigenvectors P 1 = 0.588, P 2 = 0.299, P 3 = corresponding to the order of the three eigenvalues in λ. The use of the ^ emphasises that the population parameters λ and P are estimated from the data. Jun YU () Econ671 Factor Models: Principal Components April 8, / 59,

27 Principal Components Estimation Recovering the Correlation Matrix from the Decomposition The correlation matrix is recovered as follows: 1. Diagonal elements (ie own correlations) cor (r 1,t ) = (0.581) ( 0.490) (0.649) 2 = cor (r 2,t ) = (0.588) ( 0.299) ( 0.752) 2 = cor (r 3,t ) = (0.563) (0.819) (0.144) 2 = Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

28 Principal Components Estimation 2. Off-diagonal elements cor (r 1,t, r 2,t ) = (0.581) (0.588) ( 0.490) ( 0.299) (0.649) ( 0.752) = cor (r 1,t, r 3,t ) = (0.581) (0.563) ( 0.490) (0.819) (0.649) (0.144) = cor (r 2,t, r 3,t ) = (0.588) (0.563) ( 0.299) (0.819) ( 0.752) (0.144) = Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

29 Principal Components Estimation Properties of the Estimates Some key properties of the parameter estimates are as follows. 1. Normalization of eigenvectors = ( 0.490) 2 + ( 0.299) = Orthogonality of eigenvectors ( 0.752) = P 1 P 2 = ( 0.490) ( 0.299) = 0 P 1 P 3 = ( 0.752) = 0 P 2 P 3 = ( 0.490) (0.649) + ( 0.299) ( 0.752) = 0 Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

30 Principal Components Estimation 3. Eigenvalues As it is the correlation matrix that is being used in the eigen decomposition, the eigenvalues sum to N = 3 The normalized eigenvalues are λ i = = 3 i = = = 1 The first eigenvalue explains 94.6% of the total variance, the second explains an additional 5%, while the contribution of the third and last eigenvalue is 0.4%. Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

31 Principal Components Estimation 4. Factor loadings β 1 = λ 1 P 1 = = β 2 = λ 2 P 2 = = β 3 = λ 3 P 3 = = Intercepts As E [r t ] = α, an estimate of α is given by the sample mean of r t given by α = r = [ ] Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

32 Principal Components Estimation The K = 1 Estimated Factor Model The estimated model is r 1,t = α 1 + β 1,1 s 1,t + û 1,t = s 1,t + û 1,t r 2,t = α 2 + β 2,1 s 1,t + û 2,t = s 1,t + û 3,t r 3,t = α 3 + β 3,1 s 1,t + û 3,t = s 1,t + û 3,t An increase in the factor s 1,t, results in all 3 yields increasing by similar amounts. This suggests that s 1,t is a LEVEL factor. Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

33 Principal Components Estimation As E [ s1,t 2 ] = 1, the systematic risks are ĥ 1 = β 2 1,1 = = ĥ 2 = β 2 2,1 = = ĥ 3 = β 2 3,1 = = The idiosyncratic risks are var (û 1,t ) = var (r 1,t ) ĥ 1,t = = var (û 2,t ) = var (r 2,t ) ĥ 2,t = = var (û 3,t ) = var (r 3,t ) ĥ 3,t = = Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

34 Principal Components Estimation The K = 2 Estimated Factor Model The estimated model is r 1,t = s 1,t 0.190s 2,t + û 1,t r 2,t = s 1,t 0.116s 2,t + û 2,t r 3,t = s 1,t s 2,t + û 3,t An increase in the factor s 2,t, widens the spreads between all 3 yields as r 1,t falls, as does r 2,t but by a smaller amount, whilst r 3,t increases. This suggests that s 2,t is a SLOPE factor as it changes the slope of the yield curve. Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

35 Principal Components Estimation As E [ s1,t 2 ] [ ] = E s 2 2,t = 1, the systematic risks are ĥ 1 = β 2 1,1 + β 2 1,2 = ( 0.190) 2 = ĥ 2 = β 2 2,1 + β 2 2,2 = ( 0.116) 2 = ĥ 3 = β 2 3,1 + β 2 3,2 = = The idiosyncratic risks are var (û 1,t ) = var (r 1,t ) ĥ 1 = = var (û 2,t ) = var (r 2,t ) ĥ 2 = = var (û 3,t ) = var (r 3,t ) ĥ 3 = = Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

36 Principal Components Estimation The K = 3 Estimated Factor Model The estimated model is r 1,t = s 1,t 0.190s 2,t s 3,t r 2,t = s 1,t 0.116s 2,t 0.082s 3,t r 3,t = s 1,t s 2,t s 3,t. There are no idiosyncratic terms in this model as 3 factors perfectly explain the movements of the 3 interest rates. Nonetheless it is sometimes hard to diversify all latent factors! Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

37 Principal Components Estimation As E [ s 2 1,t ] = E [ s 2 2,t ] = E [ s 2 3,t ] = 1, the systematic risks now equal the diagonal components of the correlation matrix as ĥ 1 = β 2 1,1 + β 2 1,2 + β 2 1,3 = ( 0.190) = ĥ 2 = β 2 2,1 + β 2 2,2 + β 2 2,3 = ( 0.116) 2 + ( 0.082) 2 = ĥ 3 = β 2 3,1 + β 2 3,2 + β 2 3,3 = = In which case the idiosyncratic risks are all zero var (û 1,t ) = var (r 1,t ) ĥ 1 = = var (û 2,t ) = var (r 2,t ) ĥ 2 = = var (û 3,t ) = var (r 3,t ) ĥ 3 = = Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

38 Principal Components Factor Extraction Method Since r i,t = α i + β i s 1,t + u i,t, i = 1,..., N, having estimated the factor model, estimates of the vector of factor loadings at time t are obtained as ŝ t = ( β Ω 1 β) 1 β Ω 1 (r t µ) where ŝ t is a (K 1) vector of the estimated factors at time t, β is a (N K ) estimated matrix of factor loadings, Ω is the (N N) covariance matrix of û t, r t is a (N 1) vector of interest rates and µ is a (N 1) vector of sample means corresponding to the vector of interest rates. Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

39 Principal Components Factor Extraction If Ω = σ 2 I, K = 1, then ŝ t = N β i=1 i (r it µ i ). The bigger the factor N i=1 β 2 i loading, the more importance of the variable in determining the factor. This expression shows that the factors at time t are a (weighted) linear function of the actual interest rates at time t. Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

40 Principal Components Factor Extraction EViews Commands The EViews commands to extract the factors, highlight the 3 series and double click the shaded region and then click Open Group / Proc / Make Principal Components... For Scores series names:, write in the window Level Slope Curvature Then click Calculation and for Type: choose Correlation / OK The output will be presented in a spreadsheet. Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

41 Principal Components Factor Extraction Interpretation The three factors are plotted over time. 4 3 LEVEL SLOPE CURVATURE Source: EViews file yields_us.wf1 The results show that: (i) The LEVEL factor dominates the SLOPE and CURVATURE factors. (ii) As the LEVEL factor tracks the three yields this suggests that a 1-factor model suffi ces to explain the three yields. Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

42 A Multi-Factor Model of Interest Rates Consider the N = 9, U.S. Treasury yields (percentage, annualized) from July 2001 to September 2010, presented in the Figure earlier. The N = 9 eigenvalues of the correlation matrix from highest to lowest are λ = {8.2339, , , , , , , , } The proportionate contributions of the first three eigenvalues are λ 1 = = 0.915, λ 2 = = 0.079, λ 3 = This suggest that a K = 3 factor model explains the U.S. term structure with the first three eigenvalues explaining = 0.999, or 99.9% of the total variance/correlation in the yields. = Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

43 A Multi-Factor Model of Interest Rates The estimated factor loadings on the first factor are computed as β 1,1 β 2,1 β 3,1 β 4,1 β 5,1 β 6,1 β 7,1 β 8,1 β 9,1 = = The other factor loadings are computed in a similar way. Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

44 A Multi-Factor Model of Interest Rates The following Figure plots the loadings of the first three factors which are identified respectively as level, slope and curvature LEVEL SLOPE CURVATURE Source: EViews file yields_us.wf1 Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

45 A Multi-Factor Model of Interest Rates Factor Interpretation 1. Level Factor The first factor represents a levels effect as a shock to this factor raises all yields by approximately the same amount. 2. Slope Factor The second factor is a slope factor as a positive shock twists the yield curve by lowering short rates (negative loadings) and raising long rates (positive loadings). 3. Curvature Factor The third factor is a curvature factor which bends the yield curve by simultaneously raising the very short and long rates (positive loadings), while lowering (negative loadings) the intermediate rates at around 2 years (24 months) and 3 years (36 months). Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

46 A Multi-Factor Model of Interest Rates The three factors are plotted over time LEVEL SLOPE CURVATURE During the recent crisis: Source: EViews file yields_us.wf1 (i) The LEVEL factor falls showing that all yields were falling. (ii) The SLOPE factor becomes negative suggesting an inverted yield curve. (iii) The CURVATURE factor becomes negative at the end of 2008, suggesting that short and long yields fall relative to intermediate yields. Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

47 A Latent Factor CAPM The latent multi-factor CAPM is r i,t r f,t = α i + K j=1 β i,j s j,t + u i,t where s j,t are unobserved latent factors. The data are the excess returns on 6 stocks consisting of Exxon, GE, Gold, IBM, Microsoft and Walmart. The data are monthly beginning in April 1990 and ending in July The covariance matrix is cov (r t ) = Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

48 A Latent Factor CAPM The EViews output from the principal components decomposition based on the covariance matrix is Source: EViews file capm.wf1 Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

49 A Latent Factor CAPM The N = 6 eigenvalues of the covariance matrix from highest to lowest are λ = { , , , , , } The total sum of the eigenvalues is = This sum equals the total volatility of all 6 excess returns as given by the sum of their variances = Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

50 A Latent Factor CAPM The proportionate contributions of the first three eigenvalues to total volatility are λ 1 = = λ 2 = = λ 3 = = The first factor explains 51.27% of total volatility (equal to ). - The second factor explains 17.30% of total volatility. - The third factor explains 13.98% of volatility. So the first three factors explain jointly = or 82.55% of total volatility. This suggests that a 1-factor CAPM is potentially inappropriate and there is a need for a 3-factor model (maybe even higher). Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

51 A Latent Factor CAPM To estimate the multi-factor CAPM, the intercepts (α i ) are estimated using the sample means as given by the EViews output. Source: EViews file capm.wf1 Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

52 A Latent Factor CAPM Using the first eigen vector, the K = 1 factor CAPM is estimated as β 1 = λ 1 P 1 = These results show that = (i) Gold moves in the opposite direction to the other assets, which is consistent with the asset representing a hedge stock. (ii) Microsoft has the highest loading, equal to , showing that this asset responds the most to changes in the factor s 1,t, compared to the other stocks. This result is consistent with Microsoft being an aggressive stock at least relative to the other stocks. Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

53 A Latent Factor CAPM Using the sample means and the loadings on the first factor, the estimated K = 1 factor model is then Exxon : r 1,t = s 1,t + û 1,t GE : r 2,t = s 1,t + û 2,t Gold : r 3,t = s 1,t + û 3,t IBM : r 4,t = s 1,t + û 4,t Microsoft : r 5,t = s 1,t + û 5,t Walmart : r 6,t = s 1,t + û 6,t For comparison the OLS estimates of the CAPM with the excess return on the market as the (observable) factor are given below. The beta-risk estimates are very different from the two models. Part of the reason for this is that the variance of s 1,t by construction is normalized to be unity, whereas the variance of the excess return on the market r m,t r f,t, is not. Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

")

54 A Latent Factor CAPM Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

55 A Latent Factor CAPM To make the beta-risk estimates commensurate across the two estimated models the approach is to rescale s 1,t to make it equivalent to the variance of r m,t r f,t. The EViews output of the descriptive statistics of r m,t r f,t shows that the variance is var (r m,t r f,t ) = Series: E_MARKET Sample 1990M M07 Observations 171 Mean Median Maximum Minimum Std. Dev Skewness Kurtosis Jarque Bera Probability Source: EViews file capm.wf1 Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

56 A Latent Factor CAPM Reconsider the 1-factor CAPM r i,t r f,t = α i + β i,1 s 1,t + u i,t Defining σ m as the standard deviation of the excess return on the market, then the model is rewritten as r i,t r f,t = α i + β i,1 σ m σ m s 1,t + u i,t = α i + β i,1 σ m (σ m s 1,t ) + u i,t Here the factor know has a variance equal to the variance of the excess return on the market as [ E (σ m s 1,t ) 2] = σ 2 me [ s1,t 2 ] = σ 2 m 1 = σ 2 m Thus, the rescaled beta-risk estimates are obtained by dividing the loading vector β i,1, by the standard deviation of σ m = r m,t r f,t. Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

57 These rescaled beta estimates are β 1 = β = Interpretation: / / / / / / = (i) GE tracks the market with a beta-risk of (ii) Exxon and Walmart are conservative stocks with estimates between 0 and 1. (iii) The tech-stocks of IBM and Microsoft are aggressive stocks with estimates greater than 1. (iv) Gold is a hedge stock with a beta-risk of Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

58 A Latent Factor CAPM The estimate of the first factor (ŝ 1,t ) is plotted over time (note that the two factors are not scaled to have the same variances) S1T E_MARKET Source: EViews file capm.wf1 These results show that there are some similarities in the two factors as well as some differences. The correlation between the two factors is showing that the first factor is highly correlated with the excess returns on the market. Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

59 End of Lecture Jun YU () Econ671 Factor Models: Principal Components April 8, / 59

R = µ + Bf Arbitrage Pricing Model, APM

4.2 Arbitrage Pricing Model, APM Empirical evidence indicates that the CAPM beta does not completely explain the cross section of expected asset returns. This suggests that additional factors may be required.

4.2 Arbitrage Pricing Model, APM Empirical evidence indicates that the CAPM beta does not completely explain the cross section of expected asset returns. This suggests that additional factors may be required.

Multivariate GARCH models.

Multivariate GARCH models. Financial market volatility moves together over time across assets and markets. Recognizing this commonality through a multivariate modeling framework leads to obvious gains

Multivariate GARCH models. Financial market volatility moves together over time across assets and markets. Recognizing this commonality through a multivariate modeling framework leads to obvious gains

Financial Econometrics Lecture 6: Testing the CAPM model

Financial Econometrics Lecture 6: Testing the CAPM model Richard G. Pierse 1 Introduction The capital asset pricing model has some strong implications which are testable. The restrictions that can be tested

Financial Econometrics Lecture 6: Testing the CAPM model Richard G. Pierse 1 Introduction The capital asset pricing model has some strong implications which are testable. The restrictions that can be tested

Ross (1976) introduced the Arbitrage Pricing Theory (APT) as an alternative to the CAPM.

introduced the Arbitrage Pricing Theory (APT) as an alternative to the CAPM.") 4.2 Arbitrage Pricing Model, APM Empirical evidence indicates that the CAPM beta does not completely explain the cross section of expected asset returns. This suggests that additional factors may be required.

4.2 Arbitrage Pricing Model, APM Empirical evidence indicates that the CAPM beta does not completely explain the cross section of expected asset returns. This suggests that additional factors may be required.

Identifying Financial Risk Factors

Identifying Financial Risk Factors with a Low-Rank Sparse Decomposition Lisa Goldberg Alex Shkolnik Berkeley Columbia Meeting in Engineering and Statistics 24 March 2016 Outline 1 A Brief History of Factor

Identifying Financial Risk Factors with a Low-Rank Sparse Decomposition Lisa Goldberg Alex Shkolnik Berkeley Columbia Meeting in Engineering and Statistics 24 March 2016 Outline 1 A Brief History of Factor

Factor models. May 11, 2012

Factor models May 11, 2012 Factor Models Macro economists have a peculiar data situation: Many data series, but usually short samples How can we utilize all this information without running into degrees

Factor models May 11, 2012 Factor Models Macro economists have a peculiar data situation: Many data series, but usually short samples How can we utilize all this information without running into degrees

Factor models. March 13, 2017

Factor models March 13, 2017 Factor Models Macro economists have a peculiar data situation: Many data series, but usually short samples How can we utilize all this information without running into degrees

Factor models March 13, 2017 Factor Models Macro economists have a peculiar data situation: Many data series, but usually short samples How can we utilize all this information without running into degrees

Regression: Ordinary Least Squares

Regression: Ordinary Least Squares Mark Hendricks Autumn 2017 FINM Intro: Regression Outline Regression OLS Mathematics Linear Projection Hendricks, Autumn 2017 FINM Intro: Regression: Lecture 2/32 Regression

Regression: Ordinary Least Squares Mark Hendricks Autumn 2017 FINM Intro: Regression Outline Regression OLS Mathematics Linear Projection Hendricks, Autumn 2017 FINM Intro: Regression: Lecture 2/32 Regression

Factor Models for Asset Returns. Prof. Daniel P. Palomar

Factor Models for Asset Returns Prof. Daniel P. Palomar The Hong Kong University of Science and Technology (HKUST) MAFS6010R- Portfolio Optimization with R MSc in Financial Mathematics Fall 2018-19, HKUST,

Factor Models for Asset Returns Prof. Daniel P. Palomar The Hong Kong University of Science and Technology (HKUST) MAFS6010R- Portfolio Optimization with R MSc in Financial Mathematics Fall 2018-19, HKUST,

Network Connectivity and Systematic Risk

Network Connectivity and Systematic Risk Monica Billio 1 Massimiliano Caporin 2 Roberto Panzica 3 Loriana Pelizzon 1,3 1 University Ca Foscari Venezia (Italy) 2 University of Padova (Italy) 3 Goethe University

Network Connectivity and Systematic Risk Monica Billio 1 Massimiliano Caporin 2 Roberto Panzica 3 Loriana Pelizzon 1,3 1 University Ca Foscari Venezia (Italy) 2 University of Padova (Italy) 3 Goethe University

ASSET PRICING MODELS

ASSE PRICING MODELS [1] CAPM (1) Some notation: R it = (gross) return on asset i at time t. R mt = (gross) return on the market portfolio at time t. R ft = return on risk-free asset at time t. X it = R

ASSE PRICING MODELS [1] CAPM (1) Some notation: R it = (gross) return on asset i at time t. R mt = (gross) return on the market portfolio at time t. R ft = return on risk-free asset at time t. X it = R

17 Factor Models and Principal Components

17 Factor Models and Principal Components 17.1 Dimension Reduction High-dimensional data can be challenging to analyze. They are difficult to visualize, need extensive computer resources, and often require

17 Factor Models and Principal Components 17.1 Dimension Reduction High-dimensional data can be challenging to analyze. They are difficult to visualize, need extensive computer resources, and often require

Notes on empirical methods

Notes on empirical methods Statistics of time series and cross sectional regressions 1. Time Series Regression (Fama-French). (a) Method: Run and interpret (b) Estimates: 1. ˆα, ˆβ : OLS TS regression.

Notes on empirical methods Statistics of time series and cross sectional regressions 1. Time Series Regression (Fama-French). (a) Method: Run and interpret (b) Estimates: 1. ˆα, ˆβ : OLS TS regression.

Financial Econometrics Short Course Lecture 3 Multifactor Pricing Model

Financial Econometrics Short Course Lecture 3 Multifactor Pricing Model Oliver Linton obl20@cam.ac.uk Renmin University Financial Econometrics Short Course Lecture 3 MultifactorRenmin Pricing University

Financial Econometrics Short Course Lecture 3 Multifactor Pricing Model Oliver Linton obl20@cam.ac.uk Renmin University Financial Econometrics Short Course Lecture 3 MultifactorRenmin Pricing University

Theory and Applications of High Dimensional Covariance Matrix Estimation

1 / 44 Theory and Applications of High Dimensional Covariance Matrix Estimation Yuan Liao Princeton University Joint work with Jianqing Fan and Martina Mincheva December 14, 2011 2 / 44 Outline 1 Applications

1 / 44 Theory and Applications of High Dimensional Covariance Matrix Estimation Yuan Liao Princeton University Joint work with Jianqing Fan and Martina Mincheva December 14, 2011 2 / 44 Outline 1 Applications

Identifying Aggregate Liquidity Shocks with Monetary Policy Shocks: An Application using UK Data

Identifying Aggregate Liquidity Shocks with Monetary Policy Shocks: An Application using UK Data Michael Ellington and Costas Milas Financial Services, Liquidity and Economic Activity Bank of England May

Identifying Aggregate Liquidity Shocks with Monetary Policy Shocks: An Application using UK Data Michael Ellington and Costas Milas Financial Services, Liquidity and Economic Activity Bank of England May

Applications of Random Matrix Theory to Economics, Finance and Political Science

Outline Applications of Random Matrix Theory to Economics, Finance and Political Science Matthew C. 1 1 Department of Economics, MIT Institute for Quantitative Social Science, Harvard University SEA 06

Outline Applications of Random Matrix Theory to Economics, Finance and Political Science Matthew C. 1 1 Department of Economics, MIT Institute for Quantitative Social Science, Harvard University SEA 06

MFE Financial Econometrics 2018 Final Exam Model Solutions

MFE Financial Econometrics 2018 Final Exam Model Solutions Tuesday 12 th March, 2019 1. If (X, ε) N (0, I 2 ) what is the distribution of Y = µ + β X + ε? Y N ( µ, β 2 + 1 ) 2. What is the Cramer-Rao lower

MFE Financial Econometrics 2018 Final Exam Model Solutions Tuesday 12 th March, 2019 1. If (X, ε) N (0, I 2 ) what is the distribution of Y = µ + β X + ε? Y N ( µ, β 2 + 1 ) 2. What is the Cramer-Rao lower

Chapter 4: Factor Analysis

Chapter 4: Factor Analysis In many studies, we may not be able to measure directly the variables of interest. We can merely collect data on other variables which may be related to the variables of interest.

Chapter 4: Factor Analysis In many studies, we may not be able to measure directly the variables of interest. We can merely collect data on other variables which may be related to the variables of interest.

Intro VEC and BEKK Example Factor Models Cond Var and Cor Application Ref 4. MGARCH

ntro VEC and BEKK Example Factor Models Cond Var and Cor Application Ref 4. MGARCH JEM 140: Quantitative Multivariate Finance ES, Charles University, Prague Summer 2018 JEM 140 () 4. MGARCH Summer 2018

ntro VEC and BEKK Example Factor Models Cond Var and Cor Application Ref 4. MGARCH JEM 140: Quantitative Multivariate Finance ES, Charles University, Prague Summer 2018 JEM 140 () 4. MGARCH Summer 2018

This paper develops a test of the asymptotic arbitrage pricing theory (APT) via the maximum squared Sharpe

via the maximum squared Sharpe") MANAGEMENT SCIENCE Vol. 55, No. 7, July 2009, pp. 1255 1266 issn 0025-1909 eissn 1526-5501 09 5507 1255 informs doi 10.1287/mnsc.1090.1004 2009 INFORMS Testing the APT with the Maximum Sharpe Ratio of

MANAGEMENT SCIENCE Vol. 55, No. 7, July 2009, pp. 1255 1266 issn 0025-1909 eissn 1526-5501 09 5507 1255 informs doi 10.1287/mnsc.1090.1004 2009 INFORMS Testing the APT with the Maximum Sharpe Ratio of

VARs and factors. Lecture to Bristol MSc Time Series, Spring 2014 Tony Yates

VARs and factors Lecture to Bristol MSc Time Series, Spring 2014 Tony Yates What we will cover Why factor models are useful in VARs Static and dynamic factor models VAR in the factors Factor augmented

VARs and factors Lecture to Bristol MSc Time Series, Spring 2014 Tony Yates What we will cover Why factor models are useful in VARs Static and dynamic factor models VAR in the factors Factor augmented

Errata for Campbell, Financial Decisions and Markets, 01/02/2019.

Errata for Campbell, Financial Decisions and Markets, 01/02/2019. Page xi, section title for Section 11.4.3 should be Endogenous Margin Requirements. Page 20, equation 1.49), expectations operator E should

Errata for Campbell, Financial Decisions and Markets, 01/02/2019. Page xi, section title for Section 11.4.3 should be Endogenous Margin Requirements. Page 20, equation 1.49), expectations operator E should

Model Mis-specification

Model Mis-specification Carlo Favero Favero () Model Mis-specification 1 / 28 Model Mis-specification Each specification can be interpreted of the result of a reduction process, what happens if the reduction

Model Mis-specification Carlo Favero Favero () Model Mis-specification 1 / 28 Model Mis-specification Each specification can be interpreted of the result of a reduction process, what happens if the reduction

Multivariate Time Series Analysis and Its Applications [Tsay (2005), chapter 8]

![Multivariate Time Series Analysis and Its Applications [Tsay (2005), chapter 8]](/thumbs/77/75858385.jpg "Multivariate Time Series Analysis and Its Applications [Tsay (2005), chapter 8]") 1 Multivariate Time Series Analysis and Its Applications [Tsay (2005), chapter 8] Insights: Price movements in one market can spread easily and instantly to another market [economic globalization and internet

1 Multivariate Time Series Analysis and Its Applications [Tsay (2005), chapter 8] Insights: Price movements in one market can spread easily and instantly to another market [economic globalization and internet

State-space Model. Eduardo Rossi University of Pavia. November Rossi State-space Model Fin. Econometrics / 53

State-space Model Eduardo Rossi University of Pavia November 2014 Rossi State-space Model Fin. Econometrics - 2014 1 / 53 Outline 1 Motivation 2 Introduction 3 The Kalman filter 4 Forecast errors 5 State

State-space Model Eduardo Rossi University of Pavia November 2014 Rossi State-space Model Fin. Econometrics - 2014 1 / 53 Outline 1 Motivation 2 Introduction 3 The Kalman filter 4 Forecast errors 5 State

Econ 423 Lecture Notes: Additional Topics in Time Series 1

Econ 423 Lecture Notes: Additional Topics in Time Series 1 John C. Chao April 25, 2017 1 These notes are based in large part on Chapter 16 of Stock and Watson (2011). They are for instructional purposes

Econ 423 Lecture Notes: Additional Topics in Time Series 1 John C. Chao April 25, 2017 1 These notes are based in large part on Chapter 16 of Stock and Watson (2011). They are for instructional purposes

FE670 Algorithmic Trading Strategies. Stevens Institute of Technology

FE670 Algorithmic Trading Strategies Lecture 3. Factor Models and Their Estimation Steve Yang Stevens Institute of Technology 09/12/2012 Outline 1 The Notion of Factors 2 Factor Analysis via Maximum Likelihood

FE670 Algorithmic Trading Strategies Lecture 3. Factor Models and Their Estimation Steve Yang Stevens Institute of Technology 09/12/2012 Outline 1 The Notion of Factors 2 Factor Analysis via Maximum Likelihood

Sample Exam Questions for Econometrics

Sample Exam Questions for Econometrics 1 a) What is meant by marginalisation and conditioning in the process of model reduction within the dynamic modelling tradition? (30%) b) Having derived a model for

Sample Exam Questions for Econometrics 1 a) What is meant by marginalisation and conditioning in the process of model reduction within the dynamic modelling tradition? (30%) b) Having derived a model for

Multivariate modelling of long memory processes with common components

Multivariate modelling of long memory processes with common components Claudio Morana University of Piemonte Orientale, International Centre for Economic Research (ICER), and Michigan State University

Multivariate modelling of long memory processes with common components Claudio Morana University of Piemonte Orientale, International Centre for Economic Research (ICER), and Michigan State University

14 Week 5 Empirical methods notes

14 Week 5 Empirical methods notes 1. Motivation and overview 2. Time series regressions 3. Cross sectional regressions 4. Fama MacBeth 5. Testing factor models. 14.1 Motivation and Overview 1. Expected

14 Week 5 Empirical methods notes 1. Motivation and overview 2. Time series regressions 3. Cross sectional regressions 4. Fama MacBeth 5. Testing factor models. 14.1 Motivation and Overview 1. Expected

Lecture 6: Univariate Volatility Modelling: ARCH and GARCH Models

Lecture 6: Univariate Volatility Modelling: ARCH and GARCH Models Prof. Massimo Guidolin 019 Financial Econometrics Winter/Spring 018 Overview ARCH models and their limitations Generalized ARCH models

Lecture 6: Univariate Volatility Modelling: ARCH and GARCH Models Prof. Massimo Guidolin 019 Financial Econometrics Winter/Spring 018 Overview ARCH models and their limitations Generalized ARCH models

Introduction to Algorithmic Trading Strategies Lecture 3

Introduction to Algorithmic Trading Strategies Lecture 3 Pairs Trading by Cointegration Haksun Li haksun.li@numericalmethod.com www.numericalmethod.com Outline Distance method Cointegration Stationarity

Introduction to Algorithmic Trading Strategies Lecture 3 Pairs Trading by Cointegration Haksun Li haksun.li@numericalmethod.com www.numericalmethod.com Outline Distance method Cointegration Stationarity

Volatility. Gerald P. Dwyer. February Clemson University

Volatility Gerald P. Dwyer Clemson University February 2016 Outline 1 Volatility Characteristics of Time Series Heteroskedasticity Simpler Estimation Strategies Exponentially Weighted Moving Average Use

Volatility Gerald P. Dwyer Clemson University February 2016 Outline 1 Volatility Characteristics of Time Series Heteroskedasticity Simpler Estimation Strategies Exponentially Weighted Moving Average Use

The Bond Pricing Implications of Rating-Based Capital Requirements. Internet Appendix. This Version: December Abstract

The Bond Pricing Implications of Rating-Based Capital Requirements Internet Appendix This Version: December 2017 Abstract This Internet Appendix examines the robustness of our main results and presents

The Bond Pricing Implications of Rating-Based Capital Requirements Internet Appendix This Version: December 2017 Abstract This Internet Appendix examines the robustness of our main results and presents

Cross-regional Spillover Effects in the Korean Housing Market

1) Cross-regional Spillover Effects in the Korean Housing Market Hahn Shik Lee * and Woo Suk Lee < Abstract > In this paper, we examine cross-regional spillover effects in the Korean housing market, using

1) Cross-regional Spillover Effects in the Korean Housing Market Hahn Shik Lee * and Woo Suk Lee < Abstract > In this paper, we examine cross-regional spillover effects in the Korean housing market, using

Generalized Autoregressive Score Models

Generalized Autoregressive Score Models by: Drew Creal, Siem Jan Koopman, André Lucas To capture the dynamic behavior of univariate and multivariate time series processes, we can allow parameters to be

Generalized Autoregressive Score Models by: Drew Creal, Siem Jan Koopman, André Lucas To capture the dynamic behavior of univariate and multivariate time series processes, we can allow parameters to be

Inference on Risk Premia in the Presence of Omitted Factors

Inference on Risk Premia in the Presence of Omitted Factors Stefano Giglio Dacheng Xiu Booth School of Business, University of Chicago Center for Financial and Risk Analytics Stanford University May 19,

Inference on Risk Premia in the Presence of Omitted Factors Stefano Giglio Dacheng Xiu Booth School of Business, University of Chicago Center for Financial and Risk Analytics Stanford University May 19,

Principal Component Analysis-I Geog 210C Introduction to Spatial Data Analysis. Chris Funk. Lecture 17

Principal Component Analysis-I Geog 210C Introduction to Spatial Data Analysis Chris Funk Lecture 17 Outline Filters and Rotations Generating co-varying random fields Translating co-varying fields into

Principal Component Analysis-I Geog 210C Introduction to Spatial Data Analysis Chris Funk Lecture 17 Outline Filters and Rotations Generating co-varying random fields Translating co-varying fields into

APT looking for the factors

APT looking for the factors February 5, 2018 Contents 1 the Arbitrage Pricing Theory 2 1.1 One factor models............................................... 2 1.2 2 factor models.................................................

APT looking for the factors February 5, 2018 Contents 1 the Arbitrage Pricing Theory 2 1.1 One factor models............................................... 2 1.2 2 factor models.................................................

A Guide to Modern Econometric:

A Guide to Modern Econometric: 4th edition Marno Verbeek Rotterdam School of Management, Erasmus University, Rotterdam B 379887 )WILEY A John Wiley & Sons, Ltd., Publication Contents Preface xiii 1 Introduction

A Guide to Modern Econometric: 4th edition Marno Verbeek Rotterdam School of Management, Erasmus University, Rotterdam B 379887 )WILEY A John Wiley & Sons, Ltd., Publication Contents Preface xiii 1 Introduction

Chapter 5. Classical linear regression model assumptions and diagnostics. Introductory Econometrics for Finance c Chris Brooks

Chapter 5 Classical linear regression model assumptions and diagnostics Introductory Econometrics for Finance c Chris Brooks 2013 1 Violation of the Assumptions of the CLRM Recall that we assumed of the

Chapter 5 Classical linear regression model assumptions and diagnostics Introductory Econometrics for Finance c Chris Brooks 2013 1 Violation of the Assumptions of the CLRM Recall that we assumed of the

Monetary policy at the zero lower bound: Theory

Monetary policy at the zero lower bound: Theory A. Theoretical channels 1. Conditions for complete neutrality (Eggertsson and Woodford, 2003) 2. Market frictions 3. Preferred habitat and risk-bearing (Hamilton

Monetary policy at the zero lower bound: Theory A. Theoretical channels 1. Conditions for complete neutrality (Eggertsson and Woodford, 2003) 2. Market frictions 3. Preferred habitat and risk-bearing (Hamilton

Factor Investing using Penalized Principal Components

Factor Investing using Penalized Principal Components Markus Pelger Martin Lettau 2 Stanford University 2 UC Berkeley February 8th 28 AI in Fintech Forum 28 Motivation Motivation: Asset Pricing with Risk

Factor Investing using Penalized Principal Components Markus Pelger Martin Lettau 2 Stanford University 2 UC Berkeley February 8th 28 AI in Fintech Forum 28 Motivation Motivation: Asset Pricing with Risk

Testing the APT with the Maximum Sharpe. Ratio of Extracted Factors

Testing the APT with the Maximum Sharpe Ratio of Extracted Factors Chu Zhang This version: April, 2008 Abstract. This paper develops a test of the asymptotic arbitrage pricing theory (APT) via the maximum

Testing the APT with the Maximum Sharpe Ratio of Extracted Factors Chu Zhang This version: April, 2008 Abstract. This paper develops a test of the asymptotic arbitrage pricing theory (APT) via the maximum

Multivariate Tests of the CAPM under Normality

Multivariate Tests of the CAPM under Normality Bernt Arne Ødegaard 6 June 018 Contents 1 Multivariate Tests of the CAPM 1 The Gibbons (198) paper, how to formulate the multivariate model 1 3 Multivariate

Multivariate Tests of the CAPM under Normality Bernt Arne Ødegaard 6 June 018 Contents 1 Multivariate Tests of the CAPM 1 The Gibbons (198) paper, how to formulate the multivariate model 1 3 Multivariate

Homoskedasticity. Var (u X) = σ 2. (23)

= σ 2. (23)") Homoskedasticity How big is the difference between the OLS estimator and the true parameter? To answer this question, we make an additional assumption called homoskedasticity: Var (u X) = σ 2. (23) This

Homoskedasticity How big is the difference between the OLS estimator and the true parameter? To answer this question, we make an additional assumption called homoskedasticity: Var (u X) = σ 2. (23) This

How to Run the Analysis: To run a principal components factor analysis, from the menus choose: Analyze Dimension Reduction Factor...

The principal components method of extraction begins by finding a linear combination of variables that accounts for as much variation in the original variables as possible. This method is most often used

The principal components method of extraction begins by finding a linear combination of variables that accounts for as much variation in the original variables as possible. This method is most often used

GMM - Generalized method of moments

GMM - Generalized method of moments GMM Intuition: Matching moments You want to estimate properties of a data set {x t } T t=1. You assume that x t has a constant mean and variance. x t (µ 0, σ 2 ) Consider

GMM - Generalized method of moments GMM Intuition: Matching moments You want to estimate properties of a data set {x t } T t=1. You assume that x t has a constant mean and variance. x t (µ 0, σ 2 ) Consider

Threading Rotational Dynamics, Crystal Optics, and Quantum Mechanics to Risky Asset Selection. A Physics & Pizza on Wednesdays presentation

Threading Rotational Dynamics, Crystal Optics, and Quantum Mechanics to Risky Asset Selection A Physics & Pizza on Wednesdays presentation M. Hossein Partovi Department of Physics & Astronomy, California

Threading Rotational Dynamics, Crystal Optics, and Quantum Mechanics to Risky Asset Selection A Physics & Pizza on Wednesdays presentation M. Hossein Partovi Department of Physics & Astronomy, California

Is there a flight to quality due to inflation uncertainty?

MPRA Munich Personal RePEc Archive Is there a flight to quality due to inflation uncertainty? Bulent Guler and Umit Ozlale Bilkent University, Bilkent University 18. August 2004 Online at http://mpra.ub.uni-muenchen.de/7929/

MPRA Munich Personal RePEc Archive Is there a flight to quality due to inflation uncertainty? Bulent Guler and Umit Ozlale Bilkent University, Bilkent University 18. August 2004 Online at http://mpra.ub.uni-muenchen.de/7929/

Chapter 15 Panel Data Models. Pooling Time-Series and Cross-Section Data

Chapter 5 Panel Data Models Pooling Time-Series and Cross-Section Data Sets of Regression Equations The topic can be introduced wh an example. A data set has 0 years of time series data (from 935 to 954)

Chapter 5 Panel Data Models Pooling Time-Series and Cross-Section Data Sets of Regression Equations The topic can be introduced wh an example. A data set has 0 years of time series data (from 935 to 954)

The Cross-Section of Positively Weighted Portfolios

The Cross-Section of Positively Weighted Portfolios Daniel Niedermayer Heinz Zimmermann January 11, 2007 Abstract This paper examines properties of mean-variance inefficient proxies with respect to producing

The Cross-Section of Positively Weighted Portfolios Daniel Niedermayer Heinz Zimmermann January 11, 2007 Abstract This paper examines properties of mean-variance inefficient proxies with respect to producing

Nowcasting Norwegian GDP

Nowcasting Norwegian GDP Knut Are Aastveit and Tørres Trovik May 13, 2007 Introduction Motivation The last decades of advances in information technology has made it possible to access a huge amount of

Nowcasting Norwegian GDP Knut Are Aastveit and Tørres Trovik May 13, 2007 Introduction Motivation The last decades of advances in information technology has made it possible to access a huge amount of

The Conditional Pricing of Systematic and Idiosyncratic Risk in the UK Equity Market. Niall O Sullivan b Francesco Rossi c. This version: July 2014

The Conditional Pricing of Systematic and Idiosyncratic Risk in the UK Equity Market John Cotter a Niall O Sullivan b Francesco Rossi c This version: July 2014 Abstract We test whether firm idiosyncratic

The Conditional Pricing of Systematic and Idiosyncratic Risk in the UK Equity Market John Cotter a Niall O Sullivan b Francesco Rossi c This version: July 2014 Abstract We test whether firm idiosyncratic

Econometrics of Panel Data

Econometrics of Panel Data Jakub Mućk Meeting # 2 Jakub Mućk Econometrics of Panel Data Meeting # 2 1 / 26 Outline 1 Fixed effects model The Least Squares Dummy Variable Estimator The Fixed Effect (Within

Econometrics of Panel Data Jakub Mućk Meeting # 2 Jakub Mućk Econometrics of Panel Data Meeting # 2 1 / 26 Outline 1 Fixed effects model The Least Squares Dummy Variable Estimator The Fixed Effect (Within

Introduction to Computational Finance and Financial Econometrics Probability Theory Review: Part 2

Introduction to Computational Finance and Financial Econometrics Probability Theory Review: Part 2 Eric Zivot July 7, 2014 Bivariate Probability Distribution Example - Two discrete rv s and Bivariate pdf

Introduction to Computational Finance and Financial Econometrics Probability Theory Review: Part 2 Eric Zivot July 7, 2014 Bivariate Probability Distribution Example - Two discrete rv s and Bivariate pdf

Lecture 13. Simple Linear Regression

1 / 27 Lecture 13 Simple Linear Regression October 28, 2010 2 / 27 Lesson Plan 1. Ordinary Least Squares 2. Interpretation 3 / 27 Motivation Suppose we want to approximate the value of Y with a linear

1 / 27 Lecture 13 Simple Linear Regression October 28, 2010 2 / 27 Lesson Plan 1. Ordinary Least Squares 2. Interpretation 3 / 27 Motivation Suppose we want to approximate the value of Y with a linear

ECON4515 Finance theory 1 Diderik Lund, 5 May Perold: The CAPM

Perold: The CAPM Perold starts with a historical background, the development of portfolio theory and the CAPM. Points out that until 1950 there was no theory to describe the equilibrium determination of

Perold: The CAPM Perold starts with a historical background, the development of portfolio theory and the CAPM. Points out that until 1950 there was no theory to describe the equilibrium determination of

A Non-Parametric Approach of Heteroskedasticity Robust Estimation of Vector-Autoregressive (VAR) Models

Models") Journal of Finance and Investment Analysis, vol.1, no.1, 2012, 55-67 ISSN: 2241-0988 (print version), 2241-0996 (online) International Scientific Press, 2012 A Non-Parametric Approach of Heteroskedasticity

Journal of Finance and Investment Analysis, vol.1, no.1, 2012, 55-67 ISSN: 2241-0988 (print version), 2241-0996 (online) International Scientific Press, 2012 A Non-Parametric Approach of Heteroskedasticity

Announcements (repeat) Principal Components Analysis

Principal Components Analysis") 4/7/7 Announcements repeat Principal Components Analysis CS 5 Lecture #9 April 4 th, 7 PA4 is due Monday, April 7 th Test # will be Wednesday, April 9 th Test #3 is Monday, May 8 th at 8AM Just hour long

4/7/7 Announcements repeat Principal Components Analysis CS 5 Lecture #9 April 4 th, 7 PA4 is due Monday, April 7 th Test # will be Wednesday, April 9 th Test #3 is Monday, May 8 th at 8AM Just hour long

Financial Factors in Economic Fluctuations. Lawrence Christiano Roberto Motto Massimo Rostagno

Financial Factors in Economic Fluctuations Lawrence Christiano Roberto Motto Massimo Rostagno Background Much progress made on constructing and estimating models that fit quarterly data well (Smets-Wouters,

Financial Factors in Economic Fluctuations Lawrence Christiano Roberto Motto Massimo Rostagno Background Much progress made on constructing and estimating models that fit quarterly data well (Smets-Wouters,

Forecasting the term structure interest rate of government bond yields

Forecasting the term structure interest rate of government bond yields Bachelor Thesis Econometrics & Operational Research Joost van Esch (419617) Erasmus School of Economics, Erasmus University Rotterdam

Forecasting the term structure interest rate of government bond yields Bachelor Thesis Econometrics & Operational Research Joost van Esch (419617) Erasmus School of Economics, Erasmus University Rotterdam

Beta Is Alive, Well and Healthy

Beta Is Alive, Well and Healthy Soosung Hwang * Cass Business School, UK Abstract In this study I suggest some evidence that the popular cross-sectional asset pricing test proposed by Black, Jensen, and

Beta Is Alive, Well and Healthy Soosung Hwang * Cass Business School, UK Abstract In this study I suggest some evidence that the popular cross-sectional asset pricing test proposed by Black, Jensen, and

Linear Factor Models and the Estimation of Expected Returns

Linear Factor Models and the Estimation of Expected Returns Cisil Sarisoy a,, Peter de Goeij b, Bas J.M. Werker c a Department of Finance, CentER, Tilburg University b Department of Finance, Tilburg University

Linear Factor Models and the Estimation of Expected Returns Cisil Sarisoy a,, Peter de Goeij b, Bas J.M. Werker c a Department of Finance, CentER, Tilburg University b Department of Finance, Tilburg University

Econometría 2: Análisis de series de Tiempo

Econometría 2: Análisis de series de Tiempo Karoll GOMEZ kgomezp@unal.edu.co http://karollgomez.wordpress.com Segundo semestre 2016 IX. Vector Time Series Models VARMA Models A. 1. Motivation: The vector

Econometría 2: Análisis de series de Tiempo Karoll GOMEZ kgomezp@unal.edu.co http://karollgomez.wordpress.com Segundo semestre 2016 IX. Vector Time Series Models VARMA Models A. 1. Motivation: The vector

Multivariate Statistical Analysis

Multivariate Statistical Analysis Fall 2011 C. L. Williams, Ph.D. Lecture 4 for Applied Multivariate Analysis Outline 1 Eigen values and eigen vectors Characteristic equation Some properties of eigendecompositions

Multivariate Statistical Analysis Fall 2011 C. L. Williams, Ph.D. Lecture 4 for Applied Multivariate Analysis Outline 1 Eigen values and eigen vectors Characteristic equation Some properties of eigendecompositions

Discussion of Bootstrap prediction intervals for linear, nonlinear, and nonparametric autoregressions, by Li Pan and Dimitris Politis

Discussion of Bootstrap prediction intervals for linear, nonlinear, and nonparametric autoregressions, by Li Pan and Dimitris Politis Sílvia Gonçalves and Benoit Perron Département de sciences économiques,

Discussion of Bootstrap prediction intervals for linear, nonlinear, and nonparametric autoregressions, by Li Pan and Dimitris Politis Sílvia Gonçalves and Benoit Perron Département de sciences économiques,

Quaderni di Dipartimento. Estimation Methods in Panel Data Models with Observed and Unobserved Components: a Monte Carlo Study

Quaderni di Dipartimento Estimation Methods in Panel Data Models with Observed and Unobserved Components: a Monte Carlo Study Carolina Castagnetti (Università di Pavia) Eduardo Rossi (Università di Pavia)

Quaderni di Dipartimento Estimation Methods in Panel Data Models with Observed and Unobserved Components: a Monte Carlo Study Carolina Castagnetti (Università di Pavia) Eduardo Rossi (Università di Pavia)

ZHAW Zurich University of Applied Sciences. Bachelor s Thesis Estimating Multi-Beta Pricing Models With or Without an Intercept:

ZHAW Zurich University of Applied Sciences School of Management and Law Bachelor s Thesis Estimating Multi-Beta Pricing Models With or Without an Intercept: Further Results from Simulations Submitted by:

ZHAW Zurich University of Applied Sciences School of Management and Law Bachelor s Thesis Estimating Multi-Beta Pricing Models With or Without an Intercept: Further Results from Simulations Submitted by:

18.S096 Problem Set 7 Fall 2013 Factor Models Due Date: 11/14/2013. [ ] variance: E[X] =, and Cov[X] = Σ = =

![18.S096 Problem Set 7 Fall 2013 Factor Models Due Date: 11/14/2013. [ ] variance: E[X] =, and Cov[X] = Σ = =](/thumbs/82/85647425.jpg "18.S096 Problem Set 7 Fall 2013 Factor Models Due Date: 11/14/2013. [ ] variance: E[X] =, and Cov[X] = Σ = =") 18.S096 Problem Set 7 Fall 2013 Factor Models Due Date: 11/14/2013 1. Consider a bivariate random variable: [ ] X X = 1 X 2 with mean and co [ ] variance: [ ] [ α1 Σ 1,1 Σ 1,2 σ 2 ρσ 1 σ E[X] =, and Cov[X]

18.S096 Problem Set 7 Fall 2013 Factor Models Due Date: 11/14/2013 1. Consider a bivariate random variable: [ ] X X = 1 X 2 with mean and co [ ] variance: [ ] [ α1 Σ 1,1 Σ 1,2 σ 2 ρσ 1 σ E[X] =, and Cov[X]

AMS Foundations

ams-5-sol-04-m.nb AMS 5 - Foundations Factor Models Robert J. Frey Research Professor Stony Brook University, Applied Mathematics and Statistics frey@ams.sunysb.edu Exercises for Class 3. The Chapters

ams-5-sol-04-m.nb AMS 5 - Foundations Factor Models Robert J. Frey Research Professor Stony Brook University, Applied Mathematics and Statistics frey@ams.sunysb.edu Exercises for Class 3. The Chapters

Optimal Investment Strategies: A Constrained Optimization Approach

Optimal Investment Strategies: A Constrained Optimization Approach Janet L Waldrop Mississippi State University jlc3@ramsstateedu Faculty Advisor: Michael Pearson Pearson@mathmsstateedu Contents Introduction

Optimal Investment Strategies: A Constrained Optimization Approach Janet L Waldrop Mississippi State University jlc3@ramsstateedu Faculty Advisor: Michael Pearson Pearson@mathmsstateedu Contents Introduction

Network Connectivity, Systematic Risk and Diversification

Network Connectivity, Systematic Risk and Diversification Monica Billio 1 Massimiliano Caporin 2 Roberto Panzica 3 Loriana Pelizzon 1,3 1 University Ca Foscari Venezia (Italy) 2 University of Padova (Italy)

Network Connectivity, Systematic Risk and Diversification Monica Billio 1 Massimiliano Caporin 2 Roberto Panzica 3 Loriana Pelizzon 1,3 1 University Ca Foscari Venezia (Italy) 2 University of Padova (Italy)

Macroeconometrics. Christophe BOUCHER. Session 4 Classical linear regression model assumptions and diagnostics

Macroeconometrics Christophe BOUCHER Session 4 Classical linear regression model assumptions and diagnostics 1 Violation of the Assumptions of the CLRM Recall that we assumed of the CLRM disturbance terms:

Macroeconometrics Christophe BOUCHER Session 4 Classical linear regression model assumptions and diagnostics 1 Violation of the Assumptions of the CLRM Recall that we assumed of the CLRM disturbance terms:

In modern portfolio theory, which started with the seminal work of Markowitz (1952),

,") 1 Introduction In modern portfolio theory, which started with the seminal work of Markowitz (1952), many academic researchers have examined the relationships between the return and risk, or volatility,

1 Introduction In modern portfolio theory, which started with the seminal work of Markowitz (1952), many academic researchers have examined the relationships between the return and risk, or volatility,

Quantitative Trendspotting. Rex Yuxing Du and Wagner A. Kamakura. Web Appendix A Inferring and Projecting the Latent Dynamic Factors

1 Quantitative Trendspotting Rex Yuxing Du and Wagner A. Kamakura Web Appendix A Inferring and Projecting the Latent Dynamic Factors The procedure for inferring the latent state variables (i.e., [ ] ),

1 Quantitative Trendspotting Rex Yuxing Du and Wagner A. Kamakura Web Appendix A Inferring and Projecting the Latent Dynamic Factors The procedure for inferring the latent state variables (i.e., [ ] ),

ECON 4551 Econometrics II Memorial University of Newfoundland. Panel Data Models. Adapted from Vera Tabakova s notes

ECON 4551 Econometrics II Memorial University of Newfoundland Panel Data Models Adapted from Vera Tabakova s notes 15.1 Grunfeld s Investment Data 15.2 Sets of Regression Equations 15.3 Seemingly Unrelated

ECON 4551 Econometrics II Memorial University of Newfoundland Panel Data Models Adapted from Vera Tabakova s notes 15.1 Grunfeld s Investment Data 15.2 Sets of Regression Equations 15.3 Seemingly Unrelated

Factors that Fit the Time Series and Cross-Section of Stock Returns

Factors that Fit the Time Series and Cross-Section of Stock Returns Martin Lettau Markus Pelger UC Berkeley Stanford University November 3th 8 NBER Asset Pricing Meeting Motivation Motivation Fundamental

Factors that Fit the Time Series and Cross-Section of Stock Returns Martin Lettau Markus Pelger UC Berkeley Stanford University November 3th 8 NBER Asset Pricing Meeting Motivation Motivation Fundamental

FINM 331: MULTIVARIATE DATA ANALYSIS FALL 2017 PROBLEM SET 3

FINM 331: MULTIVARIATE DATA ANALYSIS FALL 2017 PROBLEM SET 3 The required files for all problems can be found in: http://www.stat.uchicago.edu/~lekheng/courses/331/hw3/ The file name indicates which problem

FINM 331: MULTIVARIATE DATA ANALYSIS FALL 2017 PROBLEM SET 3 The required files for all problems can be found in: http://www.stat.uchicago.edu/~lekheng/courses/331/hw3/ The file name indicates which problem

University of Karachi

ESTIMATING TERM STRUCTURE OF INTEREST RATE: A PRINCIPAL COMPONENT, POLYNOMIAL APPROACH by Nasir Ali Khan A thesis submitted in partial fulfillment of the requirements for the degree of B.S. in Actuarial

ESTIMATING TERM STRUCTURE OF INTEREST RATE: A PRINCIPAL COMPONENT, POLYNOMIAL APPROACH by Nasir Ali Khan A thesis submitted in partial fulfillment of the requirements for the degree of B.S. in Actuarial

Ch3. TRENDS. Time Series Analysis

3.1 Deterministic Versus Stochastic Trends The simulated random walk in Exhibit 2.1 shows a upward trend. However, it is caused by a strong correlation between the series at nearby time points. The true

3.1 Deterministic Versus Stochastic Trends The simulated random walk in Exhibit 2.1 shows a upward trend. However, it is caused by a strong correlation between the series at nearby time points. The true

Lecture 8: Multivariate GARCH and Conditional Correlation Models

Lecture 8: Multivariate GARCH and Conditional Correlation Models Prof. Massimo Guidolin 20192 Financial Econometrics Winter/Spring 2018 Overview Three issues in multivariate modelling of CH covariances

Lecture 8: Multivariate GARCH and Conditional Correlation Models Prof. Massimo Guidolin 20192 Financial Econometrics Winter/Spring 2018 Overview Three issues in multivariate modelling of CH covariances

1 Bewley Economies with Aggregate Uncertainty

1 Bewley Economies with Aggregate Uncertainty Sofarwehaveassumedawayaggregatefluctuations (i.e., business cycles) in our description of the incomplete-markets economies with uninsurable idiosyncratic risk

1 Bewley Economies with Aggregate Uncertainty Sofarwehaveassumedawayaggregatefluctuations (i.e., business cycles) in our description of the incomplete-markets economies with uninsurable idiosyncratic risk

Lecture 9: Markov Switching Models

Lecture 9: Markov Switching Models Prof. Massimo Guidolin 20192 Financial Econometrics Winter/Spring 2018 Overview Defining a Markov Switching VAR model Structure and mechanics of Markov Switching: from

Lecture 9: Markov Switching Models Prof. Massimo Guidolin 20192 Financial Econometrics Winter/Spring 2018 Overview Defining a Markov Switching VAR model Structure and mechanics of Markov Switching: from

A new test on the conditional capital asset pricing model

Appl. Math. J. Chinese Univ. 2015, 30(2): 163-186 A new test on the conditional capital asset pricing model LI Xia-fei 1 CAI Zong-wu 2,1 REN Yu 1, Abstract. Testing the validity of the conditional capital

Appl. Math. J. Chinese Univ. 2015, 30(2): 163-186 A new test on the conditional capital asset pricing model LI Xia-fei 1 CAI Zong-wu 2,1 REN Yu 1, Abstract. Testing the validity of the conditional capital

Heteroscedasticity and Autocorrelation

Heteroscedasticity and Autocorrelation Carlo Favero Favero () Heteroscedasticity and Autocorrelation 1 / 17 Heteroscedasticity, Autocorrelation, and the GLS estimator Let us reconsider the single equation

Heteroscedasticity and Autocorrelation Carlo Favero Favero () Heteroscedasticity and Autocorrelation 1 / 17 Heteroscedasticity, Autocorrelation, and the GLS estimator Let us reconsider the single equation

Financial Econometrics

Financial Econometrics Multivariate Time Series Analysis: VAR Gerald P. Dwyer Trinity College, Dublin January 2013 GPD (TCD) VAR 01/13 1 / 25 Structural equations Suppose have simultaneous system for supply

Financial Econometrics Multivariate Time Series Analysis: VAR Gerald P. Dwyer Trinity College, Dublin January 2013 GPD (TCD) VAR 01/13 1 / 25 Structural equations Suppose have simultaneous system for supply

Financial Times Series. Lecture 12

Financial Times Series Lecture 12 Multivariate Volatility Models Here our aim is to generalize the previously presented univariate volatility models to their multivariate counterparts We assume that returns

Financial Times Series Lecture 12 Multivariate Volatility Models Here our aim is to generalize the previously presented univariate volatility models to their multivariate counterparts We assume that returns

An Introduction to Independent Components Analysis (ICA)

") An Introduction to Independent Components Analysis (ICA) Anish R. Shah, CFA Northfield Information Services Anish@northinfo.com Newport Jun 6, 2008 1 Overview of Talk Review principal components Introduce

An Introduction to Independent Components Analysis (ICA) Anish R. Shah, CFA Northfield Information Services Anish@northinfo.com Newport Jun 6, 2008 1 Overview of Talk Review principal components Introduce

Estimation of Vector Error Correction Model with GARCH Errors. Koichi Maekawa Hiroshima University of Economics

Estimation of Vector Error Correction Model with GARCH Errors Koichi Maekawa Hiroshima University of Economics Kusdhianto Setiawan Hiroshima University of Economics and Gadjah Mada University Abstract

Estimation of Vector Error Correction Model with GARCH Errors Koichi Maekawa Hiroshima University of Economics Kusdhianto Setiawan Hiroshima University of Economics and Gadjah Mada University Abstract

Instead of using all the sample observations for estimation, the suggested procedure is to divide the data set

Chow forecast test: Instead of using all the sample observations for estimation, the suggested procedure is to divide the data set of N sample observations into N 1 observations to be used for estimation

Chow forecast test: Instead of using all the sample observations for estimation, the suggested procedure is to divide the data set of N sample observations into N 1 observations to be used for estimation

On Generalized Arbitrage Pricing Theory Analysis: Empirical Investigation of the Macroeconomics Modulated Independent State-Space Model

On Generalized Arbitrage Pricing Theory Analysis: Empirical Investigation of the Macroeconomics Modulated Independent State-Space Model Kai-Chun Chiu and Lei Xu Department of Computer Science and Engineering,

On Generalized Arbitrage Pricing Theory Analysis: Empirical Investigation of the Macroeconomics Modulated Independent State-Space Model Kai-Chun Chiu and Lei Xu Department of Computer Science and Engineering,

Gaussian Slug Simple Nonlinearity Enhancement to the 1-Factor and Gaussian Copula Models in Finance, with Parametric Estimation and Goodness-of-Fit

Gaussian Slug Simple Nonlinearity Enhancement to the 1-Factor and Gaussian Copula Models in Finance, with Parametric Estimation and Goodness-of-Fit Tests on US and Thai Equity Data 22 nd Australasian Finance

Gaussian Slug Simple Nonlinearity Enhancement to the 1-Factor and Gaussian Copula Models in Finance, with Parametric Estimation and Goodness-of-Fit Tests on US and Thai Equity Data 22 nd Australasian Finance

Supply Chain Network Structure and Risk Propagation

Supply Chain Network Structure and Risk Propagation John R. Birge 1 1 University of Chicago Booth School of Business (joint work with Jing Wu, Chicago Booth) IESE Business School Birge (Chicago Booth)

Supply Chain Network Structure and Risk Propagation John R. Birge 1 1 University of Chicago Booth School of Business (joint work with Jing Wu, Chicago Booth) IESE Business School Birge (Chicago Booth)

A Dynamic Model for Investment Strategy

A Dynamic Model for Investment Strategy Richard Grinold Stanford Conference on Quantitative Finance August 18-19 2006 Preview Strategic view of risk, return and cost Not intended as a portfolio management

A Dynamic Model for Investment Strategy Richard Grinold Stanford Conference on Quantitative Finance August 18-19 2006 Preview Strategic view of risk, return and cost Not intended as a portfolio management

Miloš Kopa. Decision problems with stochastic dominance constraints

Decision problems with stochastic dominance constraints Motivation Portfolio selection model Mean risk models max λ Λ m(λ r) νr(λ r) or min λ Λ r(λ r) s.t. m(λ r) µ r is a random vector of assets returns

Decision problems with stochastic dominance constraints Motivation Portfolio selection model Mean risk models max λ Λ m(λ r) νr(λ r) or min λ Λ r(λ r) s.t. m(λ r) µ r is a random vector of assets returns

ON MEASURING HEDGE FUND RISK

ON MEASURING HEDGE FUND RISK Alexander Cherny Raphael Douady Stanislav Molchanov Department of Probability Theory Faculty of Mathematics and Mechanics Moscow State University 119992 Moscow Russia E-mail:

ON MEASURING HEDGE FUND RISK Alexander Cherny Raphael Douady Stanislav Molchanov Department of Probability Theory Faculty of Mathematics and Mechanics Moscow State University 119992 Moscow Russia E-mail:

Regression Analysis. y t = β 1 x t1 + β 2 x t2 + β k x tk + ϵ t, t = 1,..., T,

Regression Analysis The multiple linear regression model with k explanatory variables assumes that the tth observation of the dependent or endogenous variable y t is described by the linear relationship

Regression Analysis The multiple linear regression model with k explanatory variables assumes that the tth observation of the dependent or endogenous variable y t is described by the linear relationship