Time Series Econometrics 10 Vijayamohanan Pillai N

|

|

|

- Jason Rice

- 6 years ago

- Views:

Transcription

: LSE Approach Hendry, Pagan and Sargan (984) and Hendry (987).")

and income (Y ) i.e., say C α 0 + α Y () Since his is an equilibrium relaionship, a dynamic adjusmen equaion can be searched by saring firs wih a very general and elaborae specificaion.")

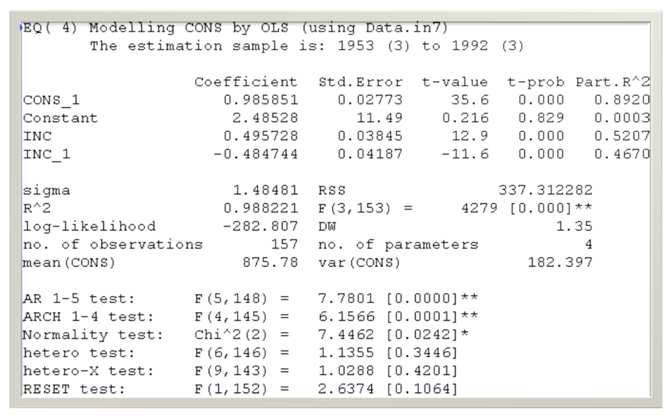

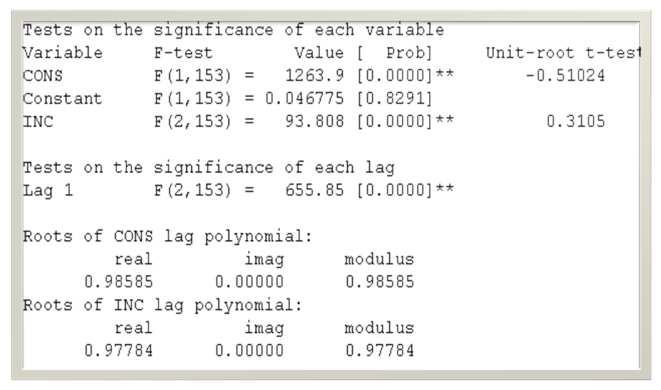

1 Time Economerics 0 Vijayamohanan Pillai N Time Mehodology 7 November 03 Vijayamohan: CDS MPhil: Time 7 November 03 Vijayamohan: CDS MPhil: Time Time : Mehodology Three alernaive approaches: (): general o specific model (GETS): LSE Approach Hendry, Pagan and Sargan (984) and Hendry (987). (): vecor auoregressions model (VAR): Sims (980): dominan approach in he USA; and (3): vecor error correcion model (VECM): Follows he Granger Represenaion heorem (Engle and Granger 987) GETS Approach Suppose, he heory implies ha here is a relaionship beween consumpion (C ) and income (Y ) i.e., say C α 0 + α Y () Since his is an equilibrium relaionship, a dynamic adjusmen equaion can be searched by saring firs wih a very general and elaborae specificaion. This iniial general specificaion is ermed he general unresriced model (GUM). 3 /7/03 0:9:4 AM Vijayamohan: M Phil: Time 4 GETS Approach A good GUM for he consumpion equaion: C αc + β 0 Y + β Y + ε ; where Y (Y, Y,., Y k ), C (α) )C + β 0 Y + ( (β 0 +β )Y +ε ; or C β 0 Y + λ [C k Y ] +ε+ ; where k (β 0 +β )/ ( α) ) and λ (α) GETS Approach A good GUM for he consumpion equaion in general: n βci C i + β yi Y i + λ( C ky ) ε i m C + i Include enough lagged variables so ha here is no serial correlaion in he residuals of he GUM. Finally, a parsimonious version of equaion () is developed, by deleing he insignifican variables and imposing consrains on he esimaed coefficiens. GETS is hus a highly empirical approach. CDS MPhil FQ Vijayamohan 5 CDS MPhil FQ Vijayamohan 6

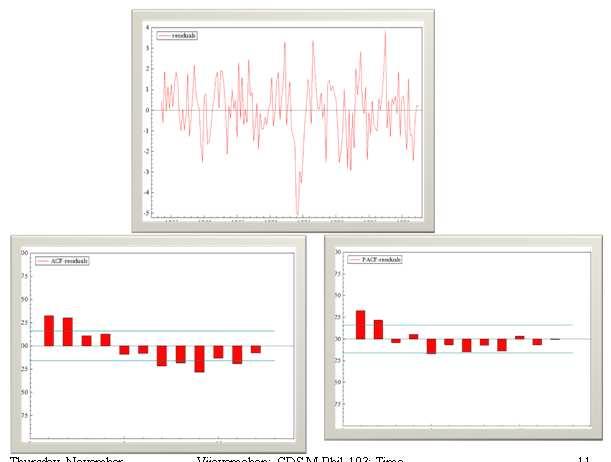

2 Consumpion Income Consumpion Inflaion Income Residual Analysis ACF PACF

3 Consumpion Income Inflaion 3 /7/03 0:9:4 AM Vijayamohan: M Phil: Time PcGive: Tes: Dynamic Analysis PcGive: Tes: Dynamic Analysis CDS MPhil FQ Vijayamohan 7 8 3

, since in equilibrium, equaion () will be 0 0 + 0 + λ(c ky ) + 0 9 C* ky*.")

4 Residual Analysis GETS Approach Noe: he equilibrium heoreical consumpion relaionship can be recovered from equaion() n βci C i + β yi Y i + λ( C ky ) ε i m C + i () by imposing he equilibrium condiion ha all he ACF PACF changes in he variables are zero, i.e., from he erm in he las par in (), since in equilibrium, equaion () will be λ(c ky ) C* ky*. /7/03 0:9:4 AM Vijayamohan: M Phil: Time 0 GETS Approach The expression in he lagged level variables, λ(c ky ) in equaion () n m C β C + β Y + λ ( C ky ) + ε ci i i i yi i is known as he error correcion erm and models ha include i are known as he error correcion models (ECM). I implies ha deparures from he equilibrium posiion in he immediae pas period will be offse in he curren period by λ proporion. Noe ha λ should be negaive. /7/03 0:9:4 AM Vijayamohan: M Phil: Time Developed as an alernaive o he large scale economeric models based on he Cowles Commission approach. Sims (980) argued: The classificaion of variables ino endogenous and exogenous, The consrains implied by he radiional heory on he srucural parameers, and The dynamic adjusmen mechanisms used in he large scale models, are all arbirary and oo resricive. VAR Models Include all variables as endogenous. For a se of n ime series variables y (y,y,...,y a VAR model of order p (VAR(p)) can be wrien as: y VAR Models k )' Ay + Ay Apy p + ε VAR Models Consider a wo-variable VAR() wih k. y z bz + cy + cz by + cy + cz + ε y + ε wih ε i.i.d(, σ ) and cov( ε y, ε z ) 0 i ~ 0 ε i z where he A s i are (n x n) coefficien marices and,,..., )' ε ( ε ε ε k is an unobservable i.i.d. zero mean error erm. In marix form: b b y c z c c c y z ε y + ε z 3 4 4

5 b BX VAR Models b y c z c X c y c z Γ + ε Srucural VAR (SVAR) or he Primiive Sysem ε y + ε z VAR Models y a a y e + z a a z e These error erms are composies of he srucural innovaions from he primiive sysem. To normalize he LHS vecor, we need o muliply he equaion by inverse B: e B ε B ( b b ) b b B BX B Γ X + B ε X + e A X VAR in sandard form (unsrucured VAR: UVAR). e e ( bb ) b b ε y ε z 5 6 e e VAR Models ε y + bε z b ε + ε y E(e z i ) 0 b b E( ε y + bε z ) σ y + bσ z Var(e ) E(e ) ime independen, and he same is rue for he oher one. Bu covariances are no zero: Cov(e,e VAR Models ) E(e e ) E[( ε y + bε z )( ε z + bε y )] ( b y σ z + bσ ) 0 So he shocks in a sandard VAR are correlaed. The only way o remove he correlaion and make he covar 0 is o assume ha he conemporaneous effecs are zero: b b 0 y bz + cy + cz + ε y z by + cy + cz + ε z 7 8 VAR Models Same regressors for all equaions; so model esimaion is sraighforward: ML esimaor OLS esimaor for each equaion. This propery populariy of VAR models. Noe: All variables in he reduced form equaions are endogenous,, and hence he equaions can be seen as he basic ARDL formulaion of a simple VAR model. 9 VAR / GETS / VECM The simple VAR models do no idenify srucural coefficiens (hence Srucural VAR models ) nor do hey ake seriously he relevance of uni roo ess. In GETS, alhough here is some awareness of he uni roo characerisics of he variables, he crucial heoreical relaionship, in he error correcion par, is specified in he levels of he variables. In conras, VECM, like VAR, reas all variables as endogenous, bu limis he number of variables o hose relevan for y a z a a y a z a paricular heory. e + e 30 5

6 VECM This mehod developed by Johansen (988) is undoubedly he mos widely used mehod in applied work. Models using his approach are also known as Coinegraing VAR (CIVAR) models. VECM can be seen as scaled down (reduced form)var model in which he srucural coefficiens are idenified. The heoreical basis of VECM: Granger Represenaion Theorem. 3 VECM Granger Represenaion Theorem (Engle and Granger 987): If a se of variables are coinegraed,, hen here exiss a VARMA represenaion for hem and an error error-correcing mechanism (ECM); for example, If Y and X are boh I() and have consan means and are coinegraed,, hen here exiss an ECM,, (wih he equilibrium error U Y β X ), of he form: Y λ U + lagged{ Y, X } + θ (L)ε, Where θ (L) is a finie polynomial in lag operaor L and ε is a whie noise. 3 VECM In Y λ U + lagged{ Y, X } + θ (L)ε, The equilibraing error in he previous period, U, capures he adjusmen owards long-run equilibrium, and he expeced ve sign error would correc in he long-run run. Noe: No feedback assumed from Y o X. If feedback assumed from Y o X, an addiional equaion: VECM in Saa Saisics > Mulivariae ime series > Vecor errorcorrecion model (VECM) X λ U + lagged{ Y, X } + θ (L)ε, where ε is whie noise. Level variables 33 7 November 03 Vijayamohan: CDS M Phil: Time 7 34 VECM in Saa VECM in Saa provides informaion abou he sample, he model fi, and he idenificaion of he parameers in he coinegraing equaion. The main esimaion able he esimaes of he shor-run parameers, + heir sandard errors and confidence inervals

7 VECM in Saa VECM in Saa. predic ce, ce. line ce ime The second esimaion able he esimaes of he parameers in he coinegraing equaion, + heir sandard errors and confidence inervals. Prediced coinegraed equaion q 960q 970q 980q 990q Vijayamohan: ime CDS M Phil 03: Time 38 VECM Remember: VECM, like VAR, reas all variables as endogenous, bu limis he number of variables o hose relevan for a paricular heory. For example, wih wo variables: Y and X, wo endogenous variables, wo possible CVs; If our equaion of ineres is Y f(x ) only,, ha is, If No feedback assumed from Y o X, or X f(y ), we need o consider and esimae only one, firs, equaion, unlike in VAR. VECM Thus we need o es for direcion of feedback: From X o Y : wheher Y is exogenous o X ; From Y o X : wheher X is exogenous o Y ; Tha is, we need o es for exogeneiy of variables: This exogeneiy es is: Granger non- causaliy es (Granger 969): VECM: Granger non- causaliy es: an Exogeneiy es Consider he following equaions: Y Σα i Y i + Σβ i X i + e, () X Σγ i Y i + Σδ i X i + e, () where he summaions are for some lag lengh k, and e and e are independenly disribued whie noises. () hypohesises ha he curren value of Y is relaed o pas values of Y iself and hose of X, while () posulaes a similar behaviour for X. VECM: Granger non- causaliy es: an Exogeneiy es Y Σα i Y i + Σβ i X i + e, () We have he following implicaion: X does no Granger-cause Y if, and only if, β i 0, for all i, as a group; Thus he measure of linear feedback from X o Y is zero (Geweke 98). Tha is, he pas values of X do no help o predic Y. In his case, Y is exogenous wih (Engle e al. 983). respec o X 4 4 7

8 X Σγ i Y i + Σδ i X i + e, () Similarly, we have he following implicaion: Y does no Granger-cause X, if, and only if, γ i 0 for all i as a group; he measure of linear feedback from Y o X is zero. VECM: Granger non- causaliy es: an Exogeneiy es Tha is, he pas values of Y fail o help predic X. Here X is exogenous wih respec o Y. If he coefficiens, hen Y Σα i Y i + Σβ i X i + e, () X Σγ i Y i + Σδ i X i + e, () lagged erms here direcions. VECM: Granger non- causaliy es: an Exogeneiy es is causaliy have significan or feedback non-zero in boh Granger non- causaliy es in STATA Granger non- causaliy es in STATA In Saa, firs run a VAR model: Saisics > Mulivariae ime series > Vecor auoregression (VAR) Level variables 7 November 03 Vijayamohan: CDS M Phil: Time Granger non- causaliy es in STATA Granger non- causaliy es in STATA

9 In Saa Granger non- causaliy es in STATA Granger non- causaliy es in STATA H 0 : x does no Granger-cause y. Saisics > Mulivariae ime series > VAR diagnosics and ess > Granger causaliy ess H 0 : x does no Granger-cause y. Y X VECM: Granger non- causaliy es: an Exogeneiy es Granger causaliy : concerned wih only shor run forecasabiliy, while Coinegraion: concerned wih long run equilibrium; Error correcion model (ECM) (differen) conceps ogeher. brings he wo Suppose Y and X are boh I() series and hey are coinegraed such ha u Y βx is I(0). VECM: Granger non- causaliy es: an Exogeneiy es This coinegraed sysem can be wrien in erms of ECM as: y λ u + lagged{ y, x } + θ (L)ε, () x λ u + lagged{ y, x } + θ (L)ε, () where θ (L)ε and θ (L)ε are finie order moving averages and one of λ, λ VECM: Granger non- causaliy es: an Exogeneiy es y λ u + lagged{ y, x } + θ (L)ε, () x λ u + lagged{ y, x } + θ (L)ε, () VECM: Granger non- causaliy es: an Exogeneiy es y λ u + lagged{ y, x } + θ (L)ε, () x λ u + lagged{ y, x } + θ (L)ε, () In he ECM, he error correcion erm, U, Granger causes Y or X (or boh). As U iself is a funcion of Y and X, eiher X is Granger caused by Y or Y by X. Tha is, he coefficien of EC conains informaion on wheher he pas values of he variables affec affec he curren values of he variable under consideraion. This hen implies ha here mus be some Granger causaliy beween he wo series in order o induce hem owards equilibrium

10 Granger non- causaliy es: Causaliy - es? Firs suggesed by Wiener (956): More properly called Wiener-Granger non- causaliy es. Economiss (e.g., Zellner 979) and even philosophers (e.g., Holland 986) quesion he very erm causaliy : To mean cause-effec relaionship, when here is only emporal lead-lag relaionship? No causaliy bu precedence as suggesed by Edward Leamer. Unforunaely several sudies o infer cause-effec relaionship! 55 Granger non- causaliy es: Causaliy - es? Adrian Pagan (989) on Granger causaliy: There was a lo of high powered analysis of his opic, bu I came away from a reading of i wih he feeling ha i was one of he mos unforunae urnings for economerics in he las wo decades, and i has probably generaed more nonsense resuls han anyhing else during ha ime. Pagan, A.R. (989), '0 Years Afer: Economerics ,' in B. Corne and H. Tulkens (eds)., Conribuions o Operaions Research and Economerics, The XXh Anniversary of CORE, (Cambridge, Ma., MIT Press). 56 Consider a (linear) filer Y k Φ X k k Consider a (linear) filer Y k Φ X k k The impac muliplier is: Y X k response in he oupu a ime o a uni pulse in he inpu a ime k: one-period muliplier or ransien response or impulse response: Y Y k + X X k 7 November 03 Vijayamohan: CDS MPhil: Time 57 7 November 03 Vijayamohan: CDS MPhil: Time 58 The firs order Auorregresive process AR(): Given he linear filer k Impulse response funcion Y k Φ X k The ime pah of all he periodical impulse responses: ACF ρ k γ k / γ 0 Φ k, k 0,,,.. Impulse responses ACF, as k, since Φ < : Sign of saionariy. +Φ: direc convergence; negaive Φ: oscillaory convergence. Y Y + k X k X 7 November 03 Vijayamohan: CDS MPhil: Time 59 7 November 03 Vijayamohan: CDS MPhil: Time

: 78.333 Vecor AR -5 es: F(45,395) 0.8479 [0.748] Vecor Normaliy es: Chi^(6) 9.045 [0.678] Vecor heero es: F(7,73).88 [0.064] Vecor heero-x es: F(6,695).38 [0.89] sigma 3.")

11 In PcGive Firs run a VAR 6 6 SYS( ) Esimaing he sysem by OLS (using Daa.in7) The esimaion sample is: 953 (3) o 99 (3) URF equaion for: CONS Coefficien Sd.Error -value -prob CONS_ CONS_ INC_ INC_ INFLAT_ INFLAT_ Consan U sigma.877 RSS URF equaion for: INFLAT Coefficien Sd.Error -value -prob CONS_ CONS_ INC_ INC_ INFLAT_ INFLAT_ Consan U sigma RSS URF equaion for: INC Coefficien Sd.Error -value -prob CONS_ CONS_ INC_ INC_ INFLAT_ INFLAT_ Consan U Vecor Pormaneau(): Vecor AR -5 es: F(45,395) [0.748] Vecor Normaliy es: Chi^(6) [0.678] Vecor heero es: F(7,73).88 [0.064] Vecor heero-x es: F(6,695).38 [0.89] sigma RSS Quarerly daa Response of 953 () o 99 (3).0 Shock from 0.5 Consumpion 0.0 Shock from Income Shock from-.5 Inflaion -5.0 Consumpion Income Inflaion CONS (CONS eqn) INC (CONS eqn) INFLAT (CONS eqn) CONS (INC eqn) INC (INC eqn) 0.0 CONS (INFLAT eqn) INFLAT (INC eqn).0 0 INC (INFLAT eqn) INFLAT (INFLAT eqn) Consumpion Income Inflaion 6 cum CONS (CONS eqn) 4 cum INC (CONS eqn) 0.75 cum INFLAT (CONS eqn) Shock from 3 4 Consumpion 0.50 Shock from Income 5-50 Shock from Inflaion cum CONS (INC eqn) 0 cum CONS (INFLAT eqn) -50 Accumulaed Response of 5 0 cum INC (INC eqn) cum INFLAT (INC eqn) cum INC (INFLAT eqn) cum INFLAT (INFLAT eqn)

67 68 var cons")

se(myirf) (file myirf.")

.")

12 In Saa Firs run a VAR or VECM. var cons inc infla, noconsan lags(/) In Saa Firs run a VAR or VECM. var cons inc infla, noconsan lags(/). irf creae order, sep(0) se(myirf) (file myirf.irf creaed) (file myirf.irf now acive) (file myirf.irf updaed). irf graph oirf, impulse(inc) response(cons) order, inc, cons sep 95% CI orhogonalized irf Graphs by irfname, impulse variable, and response variable 7 7

13 . All he series are I(0) Simply model he daa in heir levels, using OLS esimaion.. All he series are inegraed of he same order (e.g., I()), bu no coinegraed. Jus difference (appropriaely)each series, and esimae a sandard regression model using OLS. 3. All he series are inegraed of he same order, and hey are coinegraed. esimae wo ypes of models: (i) An OLS regression model using he levels of he daa. he long-run equilibraing relaionship beween he variables. (ii) An error-correcion model (ECM), esimaed by OLS. he shor-run dynamics of he relaionship beween he variables Finally, Some of he variables in quesion may be saionary, some may be I() and here may be coinegraion among some of he I() variables. ARDL Auoregressive-Disribued Lag. in use for decades, bu in more recen imes provide a very valuable vehicle for esing for he presence of long-run relaionships beween economic ime-series In is basic form, an ARDL regression model : (MARMA model) y β 0 + β y β k y -p + α 0 x + α x - + α x α q x -q + ε where ε is a random "disurbance" erm. "auoregressive y is "explained (in par) by lagged values of iself. "disribued lag" successive lags of he explanaory variable "x". Pesaran MH and Shin Y An auoregressive disribued lag modelling approach o coinegraion analysis. Chaper in Economerics and Economic Theory in he 0h Cenury: The Ragnar Frisch Cenennial Symposium, Srom S (ed.). Cambridge Universiy Press: Cambridge. Someimes, he curren value of x is excluded

14 Bounds Tesing Approaches o he Analysis of Level Relaionships M. Hashem Pesaran, Yongcheol Shin and Richard J. Smih Journal of Applied Economerics 6: (00) a new approach o esing for he exisence of a relaionship beween variables in levels which is applicable irrespecive of wheher he underlying regressors are purely I(0), purely I() or muually coinegraed. Two ses of asympoic criical values : one when all regressors are purely I() and he oher if hey are all purely I(0). These wo ses of criical values provide criical value bounds for all classificaions of he regressors ino purely I(), purely I(0) or muually coinegraed. Accordingly, various bounds esing procedures are proposed The ARDL / Bounds Tesing mehodology of Pesaran and Shin (999) and Pesaran e al. (00) has a number of feaures ha many researchers feel give i some advanages over convenional coinegraion esing. For insance: I can be used wih a mixure of I(0) and I() daa. I involves jus a single-equaion se-up, making i simple o implemen and inerpre. Differen variables can be assigned differen lag-lenghs as hey ener he model. 8 8 A convenional ECM for coinegraed daa : y β 0 + Σ β i y -i + Σγ j x -j + Σδ k x -k + φz - + e ; The ranges of summaion : from o p, 0 o q, and 0 o q respecively. z, he "error-correcion erm", is he OLS residuals series from he long-run "coinegraing regression", Sep : use he ADF/PP/KPSS ess o check ha none of he series are I(). Sep : Formulae he following model: y β 0 + Σ β i y -i + Σγ j x -j + Σδ k x -k + θ 0 y - + θ x - + θ x - + e ; y α 0 + α x + α x + v

15 y β 0 + Σ β i y -i + Σγ j x -j + Σδ k x -k + θ 0 y - + θ x - + θ x - + e ; almos like a radiional ECM. The error-correcion erm, z - replaced wih he erms y -, x -, and x - from y α 0 + α x + α x + v he lagged residuals series would be z - (y - - a 0 - a x - - a x - ), where he a's are he OLS esimaes of he α's. "unresriced ECM", or an "unconsrained ECM". Pesaran e al. (00) call his a "condiional ECM". Sep 3: y β 0 + Σ β i y -i + Σγ j x -j + Σδ k x -k + θ 0 y - + θ x - + θ x - + e ; The ranges of summaion : from o p, 0 o q, and 0 o q respecively Maximum lags are deermined by using one or more of he "informaion crieria" : AIC, SC (BIC), HQ, ec. Remember: Schwarz (Bayes) crierion (SC) is a consisen model-selecor Sep 4: A key assumpion in he ARDL / Bounds Tesing mehodology of Pesaran e al. (00) : The errors of he equaion mus be serially independen. Sep 5: We have a model wih an auoregressive srucure, so we have o be sure ha he model is "dynamically sable". Once an apparenly suiable version of he equaion has been esimaed, use he LM es o es he null hypohesis ha he errors are serially independen, agains he alernaive hypohesis ha he errors are (eiher) AR(m) or MA(m), for m,, 3,... Check ha all he associaed wih he model Sep 6: Now perform he " " y β 0 + Σ β i y -i + Σγ j x -j + Σδ k x -k + θ 0 y - + θ x - + θ x - + e ; Do a "F-es" of he hypohesis, H 0 : θ 0 θ θ 0 ; agains he alernaive ha H 0 is no rue. Sep 6: "Bounds Tesing" y β 0 + Σ β i y -i + Σγ j x -j + Σδ k x -k + θ 0 y - + θ x - + θ x - + e ; As in convenional coinegraion esing, we're esing for beween he variables. This absence coincides wih zero coefficiens for y -, x - and x - in he equaion: H 0 : θ 0 θ θ 0 89 A rejecion of H 0 implies ha we have a long-run relaionship. 90 5

, and he upper bound : all he variables are I().")

16 Exac criical values for he F-es no available for an arbirary mix of I(0) and I() variables. Pesaran e al. (00) supply bounds on he criical values for he asympoic disribuion of he F-saisic. lower and upper bounds on he criical values. he lower bound is based on he assumpion ha all of he variables are I(0), and he upper bound : all he variables are I(). If he compued F-saisic falls below he lower bound conclude : he variables are I(0), so no coinegraion possible, by definiion. If he F-saisic exceeds he upper bound, conclude : we have coinegraion. Finally, if he F-saisic falls beween he bounds, he es is inconclusive. 9 9 Sep 7: If he bounds es proves coinegraion, esimae he long-run equilibrium relaionship beween he variables: y α 0 + α x + α x + v ; as well as he usual ECM: y β 0 + Σ β i y -i + Σγ j x -j + Σδ k x -k + φz - + e ; where z - (y - -a 0 - a x - - a x - ), and he a's are he OLS esimaes of he α's. Sep 8: Exrac" long-run effecs from he unresriced ECM. y β 0 + Σ β i y -i + Σγ j x -j + Σδ k x -k + θ 0 y - + θ x - + θ x - + e ; a a long-run equilibrium, y 0, x x 0, he long-run coefficiens for x -(θ / θ 0 ) and x -(θ / θ ) CDS MPhil FQ Vijayamohan 96 6

17 CDS MPhil FQ Vijayamohan 97 7

Vectorautoregressive Model and Cointegration Analysis. Time Series Analysis Dr. Sevtap Kestel 1

Vecorauoregressive Model and Coinegraion Analysis Par V Time Series Analysis Dr. Sevap Kesel 1 Vecorauoregression Vecor auoregression (VAR) is an economeric model used o capure he evoluion and he inerdependencies

Vecorauoregressive Model and Coinegraion Analysis Par V Time Series Analysis Dr. Sevap Kesel 1 Vecorauoregression Vecor auoregression (VAR) is an economeric model used o capure he evoluion and he inerdependencies

R t. C t P t. + u t. C t = αp t + βr t + v t. + β + w t

Exercise 7 C P = α + β R P + u C = αp + βr + v (a) (b) C R = α P R + β + w (c) Assumpions abou he disurbances u, v, w : Classical assumions on he disurbance of one of he equaions, eg. on (b): E(v v s P,

Exercise 7 C P = α + β R P + u C = αp + βr + v (a) (b) C R = α P R + β + w (c) Assumpions abou he disurbances u, v, w : Classical assumions on he disurbance of one of he equaions, eg. on (b): E(v v s P,

Methodology. -ratios are biased and that the appropriate critical values have to be increased by an amount. that depends on the sample size.

Mehodology. Uni Roo Tess A ime series is inegraed when i has a mean revering propery and a finie variance. I is only emporarily ou of equilibrium and is called saionary in I(0). However a ime series ha

Mehodology. Uni Roo Tess A ime series is inegraed when i has a mean revering propery and a finie variance. I is only emporarily ou of equilibrium and is called saionary in I(0). However a ime series ha

Lecture 5. Time series: ECM. Bernardina Algieri Department Economics, Statistics and Finance

Lecure 5 Time series: ECM Bernardina Algieri Deparmen Economics, Saisics and Finance Conens Time Series Modelling Coinegraion Error Correcion Model Two Seps, Engle-Granger procedure Error Correcion Model

Lecure 5 Time series: ECM Bernardina Algieri Deparmen Economics, Saisics and Finance Conens Time Series Modelling Coinegraion Error Correcion Model Two Seps, Engle-Granger procedure Error Correcion Model

Ready for euro? Empirical study of the actual monetary policy independence in Poland VECM modelling

Macroeconomerics Handou 2 Ready for euro? Empirical sudy of he acual moneary policy independence in Poland VECM modelling 1. Inroducion This classes are based on: Łukasz Goczek & Dagmara Mycielska, 2013.

Macroeconomerics Handou 2 Ready for euro? Empirical sudy of he acual moneary policy independence in Poland VECM modelling 1. Inroducion This classes are based on: Łukasz Goczek & Dagmara Mycielska, 2013.

Dynamic Econometric Models: Y t = + 0 X t + 1 X t X t k X t-k + e t. A. Autoregressive Model:

Dynamic Economeric Models: A. Auoregressive Model: Y = + 0 X 1 Y -1 + 2 Y -2 + k Y -k + e (Wih lagged dependen variable(s) on he RHS) B. Disribued-lag Model: Y = + 0 X + 1 X -1 + 2 X -2 + + k X -k + e

Dynamic Economeric Models: A. Auoregressive Model: Y = + 0 X 1 Y -1 + 2 Y -2 + k Y -k + e (Wih lagged dependen variable(s) on he RHS) B. Disribued-lag Model: Y = + 0 X + 1 X -1 + 2 X -2 + + k X -k + e

A Specification Test for Linear Dynamic Stochastic General Equilibrium Models

Journal of Saisical and Economeric Mehods, vol.1, no.2, 2012, 65-70 ISSN: 2241-0384 (prin), 2241-0376 (online) Scienpress Ld, 2012 A Specificaion Tes for Linear Dynamic Sochasic General Equilibrium Models

Journal of Saisical and Economeric Mehods, vol.1, no.2, 2012, 65-70 ISSN: 2241-0384 (prin), 2241-0376 (online) Scienpress Ld, 2012 A Specificaion Tes for Linear Dynamic Sochasic General Equilibrium Models

Econ107 Applied Econometrics Topic 7: Multicollinearity (Studenmund, Chapter 8)

") I. Definiions and Problems A. Perfec Mulicollineariy Econ7 Applied Economerics Topic 7: Mulicollineariy (Sudenmund, Chaper 8) Definiion: Perfec mulicollineariy exiss in a following K-variable regression

I. Definiions and Problems A. Perfec Mulicollineariy Econ7 Applied Economerics Topic 7: Mulicollineariy (Sudenmund, Chaper 8) Definiion: Perfec mulicollineariy exiss in a following K-variable regression

Unit Root Time Series. Univariate random walk

Uni Roo ime Series Univariae random walk Consider he regression y y where ~ iid N 0, he leas squares esimae of is: ˆ yy y y yy Now wha if = If y y hen le y 0 =0 so ha y j j If ~ iid N 0, hen y ~ N 0, he

Uni Roo ime Series Univariae random walk Consider he regression y y where ~ iid N 0, he leas squares esimae of is: ˆ yy y y yy Now wha if = If y y hen le y 0 =0 so ha y j j If ~ iid N 0, hen y ~ N 0, he

Licenciatura de ADE y Licenciatura conjunta Derecho y ADE. Hoja de ejercicios 2 PARTE A

Licenciaura de ADE y Licenciaura conjuna Derecho y ADE Hoja de ejercicios PARTE A 1. Consider he following models Δy = 0.8 + ε (1 + 0.8L) Δ 1 y = ε where ε and ε are independen whie noise processes. In

Licenciaura de ADE y Licenciaura conjuna Derecho y ADE Hoja de ejercicios PARTE A 1. Consider he following models Δy = 0.8 + ε (1 + 0.8L) Δ 1 y = ε where ε and ε are independen whie noise processes. In

Diebold, Chapter 7. Francis X. Diebold, Elements of Forecasting, 4th Edition (Mason, Ohio: Cengage Learning, 2006). Chapter 7. Characterizing Cycles

. Chapter 7. Characterizing Cycles") Diebold, Chaper 7 Francis X. Diebold, Elemens of Forecasing, 4h Ediion (Mason, Ohio: Cengage Learning, 006). Chaper 7. Characerizing Cycles Afer compleing his reading you should be able o: Define covariance

Diebold, Chaper 7 Francis X. Diebold, Elemens of Forecasing, 4h Ediion (Mason, Ohio: Cengage Learning, 006). Chaper 7. Characerizing Cycles Afer compleing his reading you should be able o: Define covariance

Cointegration and Implications for Forecasting

Coinegraion and Implicaions for Forecasing Two examples (A) Y Y 1 1 1 2 (B) Y 0.3 0.9 1 1 2 Example B: Coinegraion Y and coinegraed wih coinegraing vecor [1, 0.9] because Y 0.9 0.3 is a saionary process

Coinegraion and Implicaions for Forecasing Two examples (A) Y Y 1 1 1 2 (B) Y 0.3 0.9 1 1 2 Example B: Coinegraion Y and coinegraed wih coinegraing vecor [1, 0.9] because Y 0.9 0.3 is a saionary process

14 Autoregressive Moving Average Models

14 Auoregressive Moving Average Models In his chaper an imporan parameric family of saionary ime series is inroduced, he family of he auoregressive moving average, or ARMA, processes. For a large class

14 Auoregressive Moving Average Models In his chaper an imporan parameric family of saionary ime series is inroduced, he family of he auoregressive moving average, or ARMA, processes. For a large class

Exercise: Building an Error Correction Model of Private Consumption. Part II Testing for Cointegration 1

Bo Sjo 200--24 Exercise: Building an Error Correcion Model of Privae Consumpion. Par II Tesing for Coinegraion Learning objecives: This lab inroduces esing for he order of inegraion and coinegraion. The

Bo Sjo 200--24 Exercise: Building an Error Correcion Model of Privae Consumpion. Par II Tesing for Coinegraion Learning objecives: This lab inroduces esing for he order of inegraion and coinegraion. The

Regression with Time Series Data

Regression wih Time Series Daa y = β 0 + β 1 x 1 +...+ β k x k + u Serial Correlaion and Heeroskedasiciy Time Series - Serial Correlaion and Heeroskedasiciy 1 Serially Correlaed Errors: Consequences Wih

Regression wih Time Series Daa y = β 0 + β 1 x 1 +...+ β k x k + u Serial Correlaion and Heeroskedasiciy Time Series - Serial Correlaion and Heeroskedasiciy 1 Serially Correlaed Errors: Consequences Wih

Introduction D P. r = constant discount rate, g = Gordon Model (1962): constant dividend growth rate.

: constant dividend growth rate.") Inroducion Gordon Model (1962): D P = r g r = consan discoun rae, g = consan dividend growh rae. If raional expecaions of fuure discoun raes and dividend growh vary over ime, so should he D/P raio. Since

Inroducion Gordon Model (1962): D P = r g r = consan discoun rae, g = consan dividend growh rae. If raional expecaions of fuure discoun raes and dividend growh vary over ime, so should he D/P raio. Since

How to Deal with Structural Breaks in Practical Cointegration Analysis

How o Deal wih Srucural Breaks in Pracical Coinegraion Analysis Roselyne Joyeux * School of Economic and Financial Sudies Macquarie Universiy December 00 ABSTRACT In his noe we consider he reamen of srucural

How o Deal wih Srucural Breaks in Pracical Coinegraion Analysis Roselyne Joyeux * School of Economic and Financial Sudies Macquarie Universiy December 00 ABSTRACT In his noe we consider he reamen of srucural

Outline. lse-logo. Outline. Outline. 1 Wald Test. 2 The Likelihood Ratio Test. 3 Lagrange Multiplier Tests

Ouline Ouline Hypohesis Tes wihin he Maximum Likelihood Framework There are hree main frequenis approaches o inference wihin he Maximum Likelihood framework: he Wald es, he Likelihood Raio es and he Lagrange

Ouline Ouline Hypohesis Tes wihin he Maximum Likelihood Framework There are hree main frequenis approaches o inference wihin he Maximum Likelihood framework: he Wald es, he Likelihood Raio es and he Lagrange

Econ Autocorrelation. Sanjaya DeSilva

Econ 39 - Auocorrelaion Sanjaya DeSilva Ocober 3, 008 1 Definiion Auocorrelaion (or serial correlaion) occurs when he error erm of one observaion is correlaed wih he error erm of any oher observaion. This

Econ 39 - Auocorrelaion Sanjaya DeSilva Ocober 3, 008 1 Definiion Auocorrelaion (or serial correlaion) occurs when he error erm of one observaion is correlaed wih he error erm of any oher observaion. This

OBJECTIVES OF TIME SERIES ANALYSIS

OBJECTIVES OF TIME SERIES ANALYSIS Undersanding he dynamic or imedependen srucure of he observaions of a single series (univariae analysis) Forecasing of fuure observaions Asceraining he leading, lagging

OBJECTIVES OF TIME SERIES ANALYSIS Undersanding he dynamic or imedependen srucure of he observaions of a single series (univariae analysis) Forecasing of fuure observaions Asceraining he leading, lagging

Stationary Time Series

3-Jul-3 Time Series Analysis Assoc. Prof. Dr. Sevap Kesel July 03 Saionary Time Series Sricly saionary process: If he oin dis. of is he same as he oin dis. of ( X,... X n) ( X h,... X nh) Weakly Saionary

3-Jul-3 Time Series Analysis Assoc. Prof. Dr. Sevap Kesel July 03 Saionary Time Series Sricly saionary process: If he oin dis. of is he same as he oin dis. of ( X,... X n) ( X h,... X nh) Weakly Saionary

Chapter 16. Regression with Time Series Data

Chaper 16 Regression wih Time Series Daa The analysis of ime series daa is of vial ineres o many groups, such as macroeconomiss sudying he behavior of naional and inernaional economies, finance economiss

Chaper 16 Regression wih Time Series Daa The analysis of ime series daa is of vial ineres o many groups, such as macroeconomiss sudying he behavior of naional and inernaional economies, finance economiss

Generalized Least Squares

Generalized Leas Squares Augus 006 1 Modified Model Original assumpions: 1 Specificaion: y = Xβ + ε (1) Eε =0 3 EX 0 ε =0 4 Eεε 0 = σ I In his secion, we consider relaxing assumpion (4) Insead, assume

Generalized Leas Squares Augus 006 1 Modified Model Original assumpions: 1 Specificaion: y = Xβ + ε (1) Eε =0 3 EX 0 ε =0 4 Eεε 0 = σ I In his secion, we consider relaxing assumpion (4) Insead, assume

DEPARTMENT OF STATISTICS

A Tes for Mulivariae ARCH Effecs R. Sco Hacker and Abdulnasser Haemi-J 004: DEPARTMENT OF STATISTICS S-0 07 LUND SWEDEN A Tes for Mulivariae ARCH Effecs R. Sco Hacker Jönköping Inernaional Business School

A Tes for Mulivariae ARCH Effecs R. Sco Hacker and Abdulnasser Haemi-J 004: DEPARTMENT OF STATISTICS S-0 07 LUND SWEDEN A Tes for Mulivariae ARCH Effecs R. Sco Hacker Jönköping Inernaional Business School

Bias in Conditional and Unconditional Fixed Effects Logit Estimation: a Correction * Tom Coupé

Bias in Condiional and Uncondiional Fixed Effecs Logi Esimaion: a Correcion * Tom Coupé Economics Educaion and Research Consorium, Naional Universiy of Kyiv Mohyla Academy Address: Vul Voloska 10, 04070

Bias in Condiional and Uncondiional Fixed Effecs Logi Esimaion: a Correcion * Tom Coupé Economics Educaion and Research Consorium, Naional Universiy of Kyiv Mohyla Academy Address: Vul Voloska 10, 04070

International Parity Relations between Poland and Germany: A Cointegrated VAR Approach

Research Seminar a he Deparmen of Economics, Warsaw Universiy Warsaw, 15 January 2008 Inernaional Pariy Relaions beween Poland and Germany: A Coinegraed VAR Approach Agnieszka Sążka Naional Bank of Poland

Research Seminar a he Deparmen of Economics, Warsaw Universiy Warsaw, 15 January 2008 Inernaional Pariy Relaions beween Poland and Germany: A Coinegraed VAR Approach Agnieszka Sążka Naional Bank of Poland

Økonomisk Kandidateksamen 2005(II) Econometrics 2. Solution

Econometrics 2. Solution") Økonomisk Kandidaeksamen 2005(II) Economerics 2 Soluion his is he proposed soluion for he exam in Economerics 2. For compleeness he soluion gives formal answers o mos of he quesions alhough his is no always

Økonomisk Kandidaeksamen 2005(II) Economerics 2 Soluion his is he proposed soluion for he exam in Economerics 2. For compleeness he soluion gives formal answers o mos of he quesions alhough his is no always

Advanced time-series analysis (University of Lund, Economic History Department)

") Advanced ime-series analysis (Universiy of Lund, Economic Hisory Deparmen) 30 Jan-3 February and 6-30 March 01 Lecure 9 Vecor Auoregression (VAR) echniques: moivaion and applicaions. Esimaion procedure.

Advanced ime-series analysis (Universiy of Lund, Economic Hisory Deparmen) 30 Jan-3 February and 6-30 March 01 Lecure 9 Vecor Auoregression (VAR) echniques: moivaion and applicaions. Esimaion procedure.

ACE 564 Spring Lecture 7. Extensions of The Multiple Regression Model: Dummy Independent Variables. by Professor Scott H.

ACE 564 Spring 2006 Lecure 7 Exensions of The Muliple Regression Model: Dumm Independen Variables b Professor Sco H. Irwin Readings: Griffihs, Hill and Judge. "Dumm Variables and Varing Coefficien Models

ACE 564 Spring 2006 Lecure 7 Exensions of The Muliple Regression Model: Dumm Independen Variables b Professor Sco H. Irwin Readings: Griffihs, Hill and Judge. "Dumm Variables and Varing Coefficien Models

Forecasting optimally

I) ile: Forecas Evaluaion II) Conens: Evaluaing forecass, properies of opimal forecass, esing properies of opimal forecass, saisical comparison of forecas accuracy III) Documenaion: - Diebold, Francis

I) ile: Forecas Evaluaion II) Conens: Evaluaing forecass, properies of opimal forecass, esing properies of opimal forecass, saisical comparison of forecas accuracy III) Documenaion: - Diebold, Francis

Financial Econometrics Jeffrey R. Russell Midterm Winter 2009 SOLUTIONS

Name SOLUTIONS Financial Economerics Jeffrey R. Russell Miderm Winer 009 SOLUTIONS You have 80 minues o complee he exam. Use can use a calculaor and noes. Try o fi all your work in he space provided. If

Name SOLUTIONS Financial Economerics Jeffrey R. Russell Miderm Winer 009 SOLUTIONS You have 80 minues o complee he exam. Use can use a calculaor and noes. Try o fi all your work in he space provided. If

Chapter 5. Heterocedastic Models. Introduction to time series (2008) 1

1") Chaper 5 Heerocedasic Models Inroducion o ime series (2008) 1 Chaper 5. Conens. 5.1. The ARCH model. 5.2. The GARCH model. 5.3. The exponenial GARCH model. 5.4. The CHARMA model. 5.5. Random coefficien

Chaper 5 Heerocedasic Models Inroducion o ime series (2008) 1 Chaper 5. Conens. 5.1. The ARCH model. 5.2. The GARCH model. 5.3. The exponenial GARCH model. 5.4. The CHARMA model. 5.5. Random coefficien

Dynamic Models, Autocorrelation and Forecasting

ECON 4551 Economerics II Memorial Universiy of Newfoundland Dynamic Models, Auocorrelaion and Forecasing Adaped from Vera Tabakova s noes 9.1 Inroducion 9.2 Lags in he Error Term: Auocorrelaion 9.3 Esimaing

ECON 4551 Economerics II Memorial Universiy of Newfoundland Dynamic Models, Auocorrelaion and Forecasing Adaped from Vera Tabakova s noes 9.1 Inroducion 9.2 Lags in he Error Term: Auocorrelaion 9.3 Esimaing

ACE 562 Fall Lecture 4: Simple Linear Regression Model: Specification and Estimation. by Professor Scott H. Irwin

ACE 56 Fall 005 Lecure 4: Simple Linear Regression Model: Specificaion and Esimaion by Professor Sco H. Irwin Required Reading: Griffihs, Hill and Judge. "Simple Regression: Economic and Saisical Model

ACE 56 Fall 005 Lecure 4: Simple Linear Regression Model: Specificaion and Esimaion by Professor Sco H. Irwin Required Reading: Griffihs, Hill and Judge. "Simple Regression: Economic and Saisical Model

ECON 482 / WH Hong Time Series Data Analysis 1. The Nature of Time Series Data. Example of time series data (inflation and unemployment rates)

") ECON 48 / WH Hong Time Series Daa Analysis. The Naure of Time Series Daa Example of ime series daa (inflaion and unemploymen raes) ECON 48 / WH Hong Time Series Daa Analysis The naure of ime series daa

ECON 48 / WH Hong Time Series Daa Analysis. The Naure of Time Series Daa Example of ime series daa (inflaion and unemploymen raes) ECON 48 / WH Hong Time Series Daa Analysis The naure of ime series daa

Distribution of Least Squares

Disribuion of Leas Squares In classic regression, if he errors are iid normal, and independen of he regressors, hen he leas squares esimaes have an exac normal disribuion, no jus asympoic his is no rue

Disribuion of Leas Squares In classic regression, if he errors are iid normal, and independen of he regressors, hen he leas squares esimaes have an exac normal disribuion, no jus asympoic his is no rue

Testing for a Single Factor Model in the Multivariate State Space Framework

esing for a Single Facor Model in he Mulivariae Sae Space Framework Chen C.-Y. M. Chiba and M. Kobayashi Inernaional Graduae School of Social Sciences Yokohama Naional Universiy Japan Faculy of Economics

esing for a Single Facor Model in he Mulivariae Sae Space Framework Chen C.-Y. M. Chiba and M. Kobayashi Inernaional Graduae School of Social Sciences Yokohama Naional Universiy Japan Faculy of Economics

Chapter 2. First Order Scalar Equations

Chaper. Firs Order Scalar Equaions We sar our sudy of differenial equaions in he same way he pioneers in his field did. We show paricular echniques o solve paricular ypes of firs order differenial equaions.

Chaper. Firs Order Scalar Equaions We sar our sudy of differenial equaions in he same way he pioneers in his field did. We show paricular echniques o solve paricular ypes of firs order differenial equaions.

Problem Set 5. Graduate Macro II, Spring 2017 The University of Notre Dame Professor Sims

Problem Se 5 Graduae Macro II, Spring 2017 The Universiy of Nore Dame Professor Sims Insrucions: You may consul wih oher members of he class, bu please make sure o urn in your own work. Where applicable,

Problem Se 5 Graduae Macro II, Spring 2017 The Universiy of Nore Dame Professor Sims Insrucions: You may consul wih oher members of he class, bu please make sure o urn in your own work. Where applicable,

Kriging Models Predicting Atrazine Concentrations in Surface Water Draining Agricultural Watersheds

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 Kriging Models Predicing Arazine Concenraions in Surface Waer Draining Agriculural Waersheds Paul L. Mosquin, Jeremy Aldworh, Wenlin Chen Supplemenal Maerial Number

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 Kriging Models Predicing Arazine Concenraions in Surface Waer Draining Agriculural Waersheds Paul L. Mosquin, Jeremy Aldworh, Wenlin Chen Supplemenal Maerial Number

Robust estimation based on the first- and third-moment restrictions of the power transformation model

h Inernaional Congress on Modelling and Simulaion, Adelaide, Ausralia, 6 December 3 www.mssanz.org.au/modsim3 Robus esimaion based on he firs- and hird-momen resricions of he power ransformaion Nawaa,

h Inernaional Congress on Modelling and Simulaion, Adelaide, Ausralia, 6 December 3 www.mssanz.org.au/modsim3 Robus esimaion based on he firs- and hird-momen resricions of he power ransformaion Nawaa,

1. Diagnostic (Misspeci cation) Tests: Testing the Assumptions

Tests: Testing the Assumptions") Business School, Brunel Universiy MSc. EC5501/5509 Modelling Financial Decisions and Markes/Inroducion o Quaniaive Mehods Prof. Menelaos Karanasos (Room SS269, el. 01895265284) Lecure Noes 6 1. Diagnosic

Business School, Brunel Universiy MSc. EC5501/5509 Modelling Financial Decisions and Markes/Inroducion o Quaniaive Mehods Prof. Menelaos Karanasos (Room SS269, el. 01895265284) Lecure Noes 6 1. Diagnosic

Lecture Notes 2. The Hilbert Space Approach to Time Series

Time Series Seven N. Durlauf Universiy of Wisconsin. Basic ideas Lecure Noes. The Hilber Space Approach o Time Series The Hilber space framework provides a very powerful language for discussing he relaionship

Time Series Seven N. Durlauf Universiy of Wisconsin. Basic ideas Lecure Noes. The Hilber Space Approach o Time Series The Hilber space framework provides a very powerful language for discussing he relaionship

Testing the Random Walk Model. i.i.d. ( ) r

r") he random walk heory saes: esing he Random Walk Model µ ε () np = + np + Momen Condiions where where ε ~ i.i.d he idea here is o es direcly he resricions imposed by momen condiions. lnp lnp µ ( lnp lnp

he random walk heory saes: esing he Random Walk Model µ ε () np = + np + Momen Condiions where where ε ~ i.i.d he idea here is o es direcly he resricions imposed by momen condiions. lnp lnp µ ( lnp lnp

Solutions to Odd Number Exercises in Chapter 6

1 Soluions o Odd Number Exercises in 6.1 R y eˆ 1.7151 y 6.3 From eˆ ( T K) ˆ R 1 1 SST SST SST (1 R ) 55.36(1.7911) we have, ˆ 6.414 T K ( ) 6.5 y ye ye y e 1 1 Consider he erms e and xe b b x e y e b

1 Soluions o Odd Number Exercises in 6.1 R y eˆ 1.7151 y 6.3 From eˆ ( T K) ˆ R 1 1 SST SST SST (1 R ) 55.36(1.7911) we have, ˆ 6.414 T K ( ) 6.5 y ye ye y e 1 1 Consider he erms e and xe b b x e y e b

Distribution of Estimates

Disribuion of Esimaes From Economerics (40) Linear Regression Model Assume (y,x ) is iid and E(x e )0 Esimaion Consisency y α + βx + he esimaes approach he rue values as he sample size increases Esimaion

Disribuion of Esimaes From Economerics (40) Linear Regression Model Assume (y,x ) is iid and E(x e )0 Esimaion Consisency y α + βx + he esimaes approach he rue values as he sample size increases Esimaion

Chickens vs. Eggs: Replicating Thurman and Fisher (1988) by Arianto A. Patunru Department of Economics, University of Indonesia 2004

by Arianto A. Patunru Department of Economics, University of Indonesia 2004") Chicens vs. Eggs: Relicaing Thurman and Fisher (988) by Ariano A. Paunru Dearmen of Economics, Universiy of Indonesia 2004. Inroducion This exercise lays ou he rocedure for esing Granger Causaliy as discussed

Chicens vs. Eggs: Relicaing Thurman and Fisher (988) by Ariano A. Paunru Dearmen of Economics, Universiy of Indonesia 2004. Inroducion This exercise lays ou he rocedure for esing Granger Causaliy as discussed

Modeling and Forecasting Volatility Autoregressive Conditional Heteroskedasticity Models. Economic Forecasting Anthony Tay Slide 1

Modeling and Forecasing Volailiy Auoregressive Condiional Heeroskedasiciy Models Anhony Tay Slide 1 smpl @all line(m) sii dl_sii S TII D L _ S TII 4,000. 3,000.1.0,000 -.1 1,000 -. 0 86 88 90 9 94 96 98

Modeling and Forecasing Volailiy Auoregressive Condiional Heeroskedasiciy Models Anhony Tay Slide 1 smpl @all line(m) sii dl_sii S TII D L _ S TII 4,000. 3,000.1.0,000 -.1 1,000 -. 0 86 88 90 9 94 96 98

Comparing Means: t-tests for One Sample & Two Related Samples

Comparing Means: -Tess for One Sample & Two Relaed Samples Using he z-tes: Assumpions -Tess for One Sample & Two Relaed Samples The z-es (of a sample mean agains a populaion mean) is based on he assumpion

Comparing Means: -Tess for One Sample & Two Relaed Samples Using he z-tes: Assumpions -Tess for One Sample & Two Relaed Samples The z-es (of a sample mean agains a populaion mean) is based on he assumpion

Nonstationary Time Series Data and Cointegration

ECON 4551 Economerics II Memorial Universiy of Newfoundland Nonsaionary Time Series Daa and Coinegraion Adaped from Vera Tabakova s noes 12.1 Saionary and Nonsaionary Variables 12.2 Spurious Regressions

ECON 4551 Economerics II Memorial Universiy of Newfoundland Nonsaionary Time Series Daa and Coinegraion Adaped from Vera Tabakova s noes 12.1 Saionary and Nonsaionary Variables 12.2 Spurious Regressions

GMM - Generalized Method of Moments

GMM - Generalized Mehod of Momens Conens GMM esimaion, shor inroducion 2 GMM inuiion: Maching momens 2 3 General overview of GMM esimaion. 3 3. Weighing marix...........................................

GMM - Generalized Mehod of Momens Conens GMM esimaion, shor inroducion 2 GMM inuiion: Maching momens 2 3 General overview of GMM esimaion. 3 3. Weighing marix...........................................

ACE 562 Fall Lecture 5: The Simple Linear Regression Model: Sampling Properties of the Least Squares Estimators. by Professor Scott H.

ACE 56 Fall 005 Lecure 5: he Simple Linear Regression Model: Sampling Properies of he Leas Squares Esimaors by Professor Sco H. Irwin Required Reading: Griffihs, Hill and Judge. "Inference in he Simple

ACE 56 Fall 005 Lecure 5: he Simple Linear Regression Model: Sampling Properies of he Leas Squares Esimaors by Professor Sco H. Irwin Required Reading: Griffihs, Hill and Judge. "Inference in he Simple

State-Space Models. Initialization, Estimation and Smoothing of the Kalman Filter

Sae-Space Models Iniializaion, Esimaion and Smoohing of he Kalman Filer Iniializaion of he Kalman Filer The Kalman filer shows how o updae pas predicors and he corresponding predicion error variances when

Sae-Space Models Iniializaion, Esimaion and Smoohing of he Kalman Filer Iniializaion of he Kalman Filer The Kalman filer shows how o updae pas predicors and he corresponding predicion error variances when

( ) ( ) if t = t. It must satisfy the identity. So, bulkiness of the unit impulse (hyper)function is equal to 1. The defining characteristic is

( ) if t = t. It must satisfy the identity. So, bulkiness of the unit impulse (hyper)function is equal to 1. The defining characteristic is") UNIT IMPULSE RESPONSE, UNIT STEP RESPONSE, STABILITY. Uni impulse funcion (Dirac dela funcion, dela funcion) rigorously defined is no sricly a funcion, bu disribuion (or measure), precise reamen requires

UNIT IMPULSE RESPONSE, UNIT STEP RESPONSE, STABILITY. Uni impulse funcion (Dirac dela funcion, dela funcion) rigorously defined is no sricly a funcion, bu disribuion (or measure), precise reamen requires

ESTIMATION OF DYNAMIC PANEL DATA MODELS WHEN REGRESSION COEFFICIENTS AND INDIVIDUAL EFFECTS ARE TIME-VARYING

Inernaional Journal of Social Science and Economic Research Volume:02 Issue:0 ESTIMATION OF DYNAMIC PANEL DATA MODELS WHEN REGRESSION COEFFICIENTS AND INDIVIDUAL EFFECTS ARE TIME-VARYING Chung-ki Min Professor

Inernaional Journal of Social Science and Economic Research Volume:02 Issue:0 ESTIMATION OF DYNAMIC PANEL DATA MODELS WHEN REGRESSION COEFFICIENTS AND INDIVIDUAL EFFECTS ARE TIME-VARYING Chung-ki Min Professor

Hypothesis Testing in the Classical Normal Linear Regression Model. 1. Components of Hypothesis Tests

ECONOMICS 35* -- NOTE 8 M.G. Abbo ECON 35* -- NOTE 8 Hypohesis Tesing in he Classical Normal Linear Regression Model. Componens of Hypohesis Tess. A esable hypohesis, which consiss of wo pars: Par : a

ECONOMICS 35* -- NOTE 8 M.G. Abbo ECON 35* -- NOTE 8 Hypohesis Tesing in he Classical Normal Linear Regression Model. Componens of Hypohesis Tess. A esable hypohesis, which consiss of wo pars: Par : a

The Multiple Regression Model: Hypothesis Tests and the Use of Nonsample Information

Chaper 8 The Muliple Regression Model: Hypohesis Tess and he Use of Nonsample Informaion An imporan new developmen ha we encouner in his chaper is using he F- disribuion o simulaneously es a null hypohesis

Chaper 8 The Muliple Regression Model: Hypohesis Tess and he Use of Nonsample Informaion An imporan new developmen ha we encouner in his chaper is using he F- disribuion o simulaneously es a null hypohesis

Wednesday, November 7 Handout: Heteroskedasticity

Amhers College Deparmen of Economics Economics 360 Fall 202 Wednesday, November 7 Handou: Heeroskedasiciy Preview Review o Regression Model o Sandard Ordinary Leas Squares (OLS) Premises o Esimaion Procedures

Amhers College Deparmen of Economics Economics 360 Fall 202 Wednesday, November 7 Handou: Heeroskedasiciy Preview Review o Regression Model o Sandard Ordinary Leas Squares (OLS) Premises o Esimaion Procedures

ACE 562 Fall Lecture 8: The Simple Linear Regression Model: R 2, Reporting the Results and Prediction. by Professor Scott H.

ACE 56 Fall 5 Lecure 8: The Simple Linear Regression Model: R, Reporing he Resuls and Predicion by Professor Sco H. Irwin Required Readings: Griffihs, Hill and Judge. "Explaining Variaion in he Dependen

ACE 56 Fall 5 Lecure 8: The Simple Linear Regression Model: R, Reporing he Resuls and Predicion by Professor Sco H. Irwin Required Readings: Griffihs, Hill and Judge. "Explaining Variaion in he Dependen

Wisconsin Unemployment Rate Forecast Revisited

Wisconsin Unemploymen Rae Forecas Revisied Forecas in Lecure Wisconsin unemploymen November 06 was 4.% Forecass Poin Forecas 50% Inerval 80% Inerval Forecas Forecas December 06 4.0% (4.0%, 4.0%) (3.95%,

Wisconsin Unemploymen Rae Forecas Revisied Forecas in Lecure Wisconsin unemploymen November 06 was 4.% Forecass Poin Forecas 50% Inerval 80% Inerval Forecas Forecas December 06 4.0% (4.0%, 4.0%) (3.95%,

Robert Kollmann. 6 September 2017

Appendix: Supplemenary maerial for Tracable Likelihood-Based Esimaion of Non- Linear DSGE Models Economics Leers (available online 6 Sepember 207) hp://dx.doi.org/0.06/j.econle.207.08.027 Rober Kollmann

Appendix: Supplemenary maerial for Tracable Likelihood-Based Esimaion of Non- Linear DSGE Models Economics Leers (available online 6 Sepember 207) hp://dx.doi.org/0.06/j.econle.207.08.027 Rober Kollmann

Lecture 10 Estimating Nonlinear Regression Models

Lecure 0 Esimaing Nonlinear Regression Models References: Greene, Economeric Analysis, Chaper 0 Consider he following regression model: y = f(x, β) + ε =,, x is kx for each, β is an rxconsan vecor, ε is

Lecure 0 Esimaing Nonlinear Regression Models References: Greene, Economeric Analysis, Chaper 0 Consider he following regression model: y = f(x, β) + ε =,, x is kx for each, β is an rxconsan vecor, ε is

Time series Decomposition method

Time series Decomposiion mehod A ime series is described using a mulifacor model such as = f (rend, cyclical, seasonal, error) = f (T, C, S, e) Long- Iner-mediaed Seasonal Irregular erm erm effec, effec,

Time series Decomposiion mehod A ime series is described using a mulifacor model such as = f (rend, cyclical, seasonal, error) = f (T, C, S, e) Long- Iner-mediaed Seasonal Irregular erm erm effec, effec,

Properties of Autocorrelated Processes Economics 30331

Properies of Auocorrelaed Processes Economics 3033 Bill Evans Fall 05 Suppose we have ime series daa series labeled as where =,,3, T (he final period) Some examples are he dail closing price of he S&500,

Properies of Auocorrelaed Processes Economics 3033 Bill Evans Fall 05 Suppose we have ime series daa series labeled as where =,,3, T (he final period) Some examples are he dail closing price of he S&500,

Monetary policymaking and inflation expectations: The experience of Latin America

Moneary policymaking and inflaion expecaions: The experience of Lain America Luiz de Mello and Diego Moccero OECD Economics Deparmen Brazil/Souh America Desk 8h February 7 1999: new moneary policy regimes

Moneary policymaking and inflaion expecaions: The experience of Lain America Luiz de Mello and Diego Moccero OECD Economics Deparmen Brazil/Souh America Desk 8h February 7 1999: new moneary policy regimes

- The whole joint distribution is independent of the date at which it is measured and depends only on the lag.

Saionary Processes Sricly saionary - The whole join disribuion is indeenden of he dae a which i is measured and deends only on he lag. - E y ) is a finie consan. ( - V y ) is a finie consan. ( ( y, y s

Saionary Processes Sricly saionary - The whole join disribuion is indeenden of he dae a which i is measured and deends only on he lag. - E y ) is a finie consan. ( - V y ) is a finie consan. ( ( y, y s

Vehicle Arrival Models : Headway

Chaper 12 Vehicle Arrival Models : Headway 12.1 Inroducion Modelling arrival of vehicle a secion of road is an imporan sep in raffic flow modelling. I has imporan applicaion in raffic flow simulaion where

Chaper 12 Vehicle Arrival Models : Headway 12.1 Inroducion Modelling arrival of vehicle a secion of road is an imporan sep in raffic flow modelling. I has imporan applicaion in raffic flow simulaion where

(10) (a) Derive and plot the spectrum of y. Discuss how the seasonality in the process is evident in spectrum.

(a) Derive and plot the spectrum of y. Discuss how the seasonality in the process is evident in spectrum.") January 01 Final Exam Quesions: Mark W. Wason (Poins/Minues are given in Parenheses) (15) 1. Suppose ha y follows he saionary AR(1) process y = y 1 +, where = 0.5 and ~ iid(0,1). Le x = (y + y 1 )/. (11)

January 01 Final Exam Quesions: Mark W. Wason (Poins/Minues are given in Parenheses) (15) 1. Suppose ha y follows he saionary AR(1) process y = y 1 +, where = 0.5 and ~ iid(0,1). Le x = (y + y 1 )/. (11)

Physics 235 Chapter 2. Chapter 2 Newtonian Mechanics Single Particle

Chaper 2 Newonian Mechanics Single Paricle In his Chaper we will review wha Newon s laws of mechanics ell us abou he moion of a single paricle. Newon s laws are only valid in suiable reference frames,

Chaper 2 Newonian Mechanics Single Paricle In his Chaper we will review wha Newon s laws of mechanics ell us abou he moion of a single paricle. Newon s laws are only valid in suiable reference frames,

Derived Short-Run and Long-Run Softwood Lumber Demand and Supply

Derived Shor-Run and Long-Run Sofwood Lumber Demand and Supply Nianfu Song and Sun Joseph Chang School of Renewable Naural Resources Louisiana Sae Universiy Ouline Shor-run run and long-run implied by

Derived Shor-Run and Long-Run Sofwood Lumber Demand and Supply Nianfu Song and Sun Joseph Chang School of Renewable Naural Resources Louisiana Sae Universiy Ouline Shor-run run and long-run implied by

STATE-SPACE MODELLING. A mass balance across the tank gives:

B. Lennox and N.F. Thornhill, 9, Sae Space Modelling, IChemE Process Managemen and Conrol Subjec Group Newsleer STE-SPACE MODELLING Inroducion: Over he pas decade or so here has been an ever increasing

B. Lennox and N.F. Thornhill, 9, Sae Space Modelling, IChemE Process Managemen and Conrol Subjec Group Newsleer STE-SPACE MODELLING Inroducion: Over he pas decade or so here has been an ever increasing

Some Basic Information about M-S-D Systems

Some Basic Informaion abou M-S-D Sysems 1 Inroducion We wan o give some summary of he facs concerning unforced (homogeneous) and forced (non-homogeneous) models for linear oscillaors governed by second-order,

Some Basic Informaion abou M-S-D Sysems 1 Inroducion We wan o give some summary of he facs concerning unforced (homogeneous) and forced (non-homogeneous) models for linear oscillaors governed by second-order,

DYNAMIC ECONOMETRIC MODELS vol NICHOLAS COPERNICUS UNIVERSITY - TORUŃ Józef Stawicki and Joanna Górka Nicholas Copernicus University

DYNAMIC ECONOMETRIC MODELS vol.. - NICHOLAS COPERNICUS UNIVERSITY - TORUŃ 996 Józef Sawicki and Joanna Górka Nicholas Copernicus Universiy ARMA represenaion for a sum of auoregressive processes In he ime

DYNAMIC ECONOMETRIC MODELS vol.. - NICHOLAS COPERNICUS UNIVERSITY - TORUŃ 996 Józef Sawicki and Joanna Górka Nicholas Copernicus Universiy ARMA represenaion for a sum of auoregressive processes In he ime

CHAPTER 17: DYNAMIC ECONOMETRIC MODELS: AUTOREGRESSIVE AND DISTRIBUTED-LAG MODELS

Basic Economerics, Gujarai and Porer CHAPTER 7: DYNAMIC ECONOMETRIC MODELS: AUTOREGRESSIVE AND DISTRIBUTED-LAG MODELS 7. (a) False. Economeric models are dynamic if hey porray he ime pah of he dependen

Basic Economerics, Gujarai and Porer CHAPTER 7: DYNAMIC ECONOMETRIC MODELS: AUTOREGRESSIVE AND DISTRIBUTED-LAG MODELS 7. (a) False. Economeric models are dynamic if hey porray he ime pah of he dependen

References are appeared in the last slide. Last update: (1393/08/19)

") SYSEM IDEIFICAIO Ali Karimpour Associae Professor Ferdowsi Universi of Mashhad References are appeared in he las slide. Las updae: 0..204 393/08/9 Lecure 5 lecure 5 Parameer Esimaion Mehods opics o be

SYSEM IDEIFICAIO Ali Karimpour Associae Professor Ferdowsi Universi of Mashhad References are appeared in he las slide. Las updae: 0..204 393/08/9 Lecure 5 lecure 5 Parameer Esimaion Mehods opics o be

Stability. Coefficients may change over time. Evolution of the economy Policy changes

Sabiliy Coefficiens may change over ime Evoluion of he economy Policy changes Time Varying Parameers y = α + x β + Coefficiens depend on he ime period If he coefficiens vary randomly and are unpredicable,

Sabiliy Coefficiens may change over ime Evoluion of he economy Policy changes Time Varying Parameers y = α + x β + Coefficiens depend on he ime period If he coefficiens vary randomly and are unpredicable,

12: AUTOREGRESSIVE AND MOVING AVERAGE PROCESSES IN DISCRETE TIME. Σ j =

1: AUTOREGRESSIVE AND MOVING AVERAGE PROCESSES IN DISCRETE TIME Moving Averages Recall ha a whie noise process is a series { } = having variance σ. The whie noise process has specral densiy f (λ) = of

1: AUTOREGRESSIVE AND MOVING AVERAGE PROCESSES IN DISCRETE TIME Moving Averages Recall ha a whie noise process is a series { } = having variance σ. The whie noise process has specral densiy f (λ) = of

A Dynamic Model of Economic Fluctuations

CHAPTER 15 A Dynamic Model of Economic Flucuaions Modified for ECON 2204 by Bob Murphy 2016 Worh Publishers, all righs reserved IN THIS CHAPTER, OU WILL LEARN: how o incorporae dynamics ino he AD-AS model

CHAPTER 15 A Dynamic Model of Economic Flucuaions Modified for ECON 2204 by Bob Murphy 2016 Worh Publishers, all righs reserved IN THIS CHAPTER, OU WILL LEARN: how o incorporae dynamics ino he AD-AS model

Department of Economics East Carolina University Greenville, NC Phone: Fax:

March 3, 999 Time Series Evidence on Wheher Adjusmen o Long-Run Equilibrium is Asymmeric Philip Rohman Eas Carolina Universiy Absrac The Enders and Granger (998) uni-roo es agains saionary alernaives wih

March 3, 999 Time Series Evidence on Wheher Adjusmen o Long-Run Equilibrium is Asymmeric Philip Rohman Eas Carolina Universiy Absrac The Enders and Granger (998) uni-roo es agains saionary alernaives wih

Zürich. ETH Master Course: L Autonomous Mobile Robots Localization II

Roland Siegwar Margaria Chli Paul Furgale Marco Huer Marin Rufli Davide Scaramuzza ETH Maser Course: 151-0854-00L Auonomous Mobile Robos Localizaion II ACT and SEE For all do, (predicion updae / ACT),

Roland Siegwar Margaria Chli Paul Furgale Marco Huer Marin Rufli Davide Scaramuzza ETH Maser Course: 151-0854-00L Auonomous Mobile Robos Localizaion II ACT and SEE For all do, (predicion updae / ACT),

School and Workshop on Market Microstructure: Design, Efficiency and Statistical Regularities March 2011

2229-12 School and Workshop on Marke Microsrucure: Design, Efficiency and Saisical Regulariies 21-25 March 2011 Some mahemaical properies of order book models Frederic ABERGEL Ecole Cenrale Paris Grande

2229-12 School and Workshop on Marke Microsrucure: Design, Efficiency and Saisical Regulariies 21-25 March 2011 Some mahemaical properies of order book models Frederic ABERGEL Ecole Cenrale Paris Grande

t is a basis for the solution space to this system, then the matrix having these solutions as columns, t x 1 t, x 2 t,... x n t x 2 t...

Mah 228- Fri Mar 24 5.6 Marix exponenials and linear sysems: The analogy beween firs order sysems of linear differenial equaions (Chaper 5) and scalar linear differenial equaions (Chaper ) is much sronger

Mah 228- Fri Mar 24 5.6 Marix exponenials and linear sysems: The analogy beween firs order sysems of linear differenial equaions (Chaper 5) and scalar linear differenial equaions (Chaper ) is much sronger

Time Series Test of Nonlinear Convergence and Transitional Dynamics. Terence Tai-Leung Chong

Time Series Tes of Nonlinear Convergence and Transiional Dynamics Terence Tai-Leung Chong Deparmen of Economics, The Chinese Universiy of Hong Kong Melvin J. Hinich Signal and Informaion Sciences Laboraory

Time Series Tes of Nonlinear Convergence and Transiional Dynamics Terence Tai-Leung Chong Deparmen of Economics, The Chinese Universiy of Hong Kong Melvin J. Hinich Signal and Informaion Sciences Laboraory

Measurement Error 1: Consequences Page 1. Definitions. For two variables, X and Y, the following hold: Expectation, or Mean, of X.

Measuremen Error 1: Consequences of Measuremen Error Richard Williams, Universiy of Nore Dame, hps://www3.nd.edu/~rwilliam/ Las revised January 1, 015 Definiions. For wo variables, X and Y, he following

Measuremen Error 1: Consequences of Measuremen Error Richard Williams, Universiy of Nore Dame, hps://www3.nd.edu/~rwilliam/ Las revised January 1, 015 Definiions. For wo variables, X and Y, he following

Nonstationarity-Integrated Models. Time Series Analysis Dr. Sevtap Kestel 1

Nonsaionariy-Inegraed Models Time Series Analysis Dr. Sevap Kesel 1 Diagnosic Checking Residual Analysis: Whie noise. P-P or Q-Q plos of he residuals follow a normal disribuion, he series is called a Gaussian

Nonsaionariy-Inegraed Models Time Series Analysis Dr. Sevap Kesel 1 Diagnosic Checking Residual Analysis: Whie noise. P-P or Q-Q plos of he residuals follow a normal disribuion, he series is called a Gaussian

The Simple Linear Regression Model: Reporting the Results and Choosing the Functional Form

Chaper 6 The Simple Linear Regression Model: Reporing he Resuls and Choosing he Funcional Form To complee he analysis of he simple linear regression model, in his chaper we will consider how o measure

Chaper 6 The Simple Linear Regression Model: Reporing he Resuls and Choosing he Funcional Form To complee he analysis of he simple linear regression model, in his chaper we will consider how o measure

VAR analysis in the presence of a Changing Correlation in the Structural Errors

VAR analysis in he presence of a Changing Correlaion in he Srucural Errors By Sephen G. Hall Imperial College Business School Naional Insiue of Economic and Social research Absrac In his paper an exension

VAR analysis in he presence of a Changing Correlaion in he Srucural Errors By Sephen G. Hall Imperial College Business School Naional Insiue of Economic and Social research Absrac In his paper an exension

FORECASTING THE DEMAND OF CONTAINER THROUGHPUT IN INDONESIA

[Memoirs of Consrucion Engineering Research Insiue Vol.47 (paper) Nov.2005] FORECASTING THE DEMAND OF CONTAINER THROUGHPUT IN INDONESIA Syafi i, Kasuhiko Kuroda, Mikio Takebayashi ABSTRACT This paper forecass

[Memoirs of Consrucion Engineering Research Insiue Vol.47 (paper) Nov.2005] FORECASTING THE DEMAND OF CONTAINER THROUGHPUT IN INDONESIA Syafi i, Kasuhiko Kuroda, Mikio Takebayashi ABSTRACT This paper forecass

A STRUCTURAL VECTOR ERROR CORRECTION MODEL WITH SHORT-RUN AND LONG-RUN RESTRICTIONS

199 THE KOREAN ECONOMIC REVIEW Volume 4, Number 1, Summer 008 A STRUCTURAL VECTOR ERROR CORRECTION MODEL WITH SHORT-RUN AND LONG-RUN RESTRICTIONS KYUNGHO JANG* We consider srucural vecor error correcion

199 THE KOREAN ECONOMIC REVIEW Volume 4, Number 1, Summer 008 A STRUCTURAL VECTOR ERROR CORRECTION MODEL WITH SHORT-RUN AND LONG-RUN RESTRICTIONS KYUNGHO JANG* We consider srucural vecor error correcion

Stock Prices and Dividends in Taiwan's Stock Market: Evidence Based on Time-Varying Present Value Model. Abstract

Sock Prices and Dividends in Taiwan's Sock Marke: Evidence Based on Time-Varying Presen Value Model Chi-Wei Su Deparmen of Finance, Providence Universiy, Taichung, Taiwan Hsu-Ling Chang Deparmen of Accouning

Sock Prices and Dividends in Taiwan's Sock Marke: Evidence Based on Time-Varying Presen Value Model Chi-Wei Su Deparmen of Finance, Providence Universiy, Taichung, Taiwan Hsu-Ling Chang Deparmen of Accouning

Modeling Economic Time Series with Stochastic Linear Difference Equations

A. Thiemer, SLDG.mcd, 6..6 FH-Kiel Universiy of Applied Sciences Prof. Dr. Andreas Thiemer e-mail: andreas.hiemer@fh-kiel.de Modeling Economic Time Series wih Sochasic Linear Difference Equaions Summary:

A. Thiemer, SLDG.mcd, 6..6 FH-Kiel Universiy of Applied Sciences Prof. Dr. Andreas Thiemer e-mail: andreas.hiemer@fh-kiel.de Modeling Economic Time Series wih Sochasic Linear Difference Equaions Summary:

(a) Set up the least squares estimation procedure for this problem, which will consist in minimizing the sum of squared residuals. 2 t.

Set up the least squares estimation procedure for this problem, which will consist in minimizing the sum of squared residuals. 2 t.") Insrucions: The goal of he problem se is o undersand wha you are doing raher han jus geing he correc resul. Please show your work clearly and nealy. No credi will be given o lae homework, regardless of

Insrucions: The goal of he problem se is o undersand wha you are doing raher han jus geing he correc resul. Please show your work clearly and nealy. No credi will be given o lae homework, regardless of

A generalization of the Burg s algorithm to periodically correlated time series

A generalizaion of he Burg s algorihm o periodically correlaed ime series Georgi N. Boshnakov Insiue of Mahemaics, Bulgarian Academy of Sciences ABSTRACT In his paper periodically correlaed processes are

A generalizaion of he Burg s algorihm o periodically correlaed ime series Georgi N. Boshnakov Insiue of Mahemaics, Bulgarian Academy of Sciences ABSTRACT In his paper periodically correlaed processes are

Simulation-Solving Dynamic Models ABE 5646 Week 2, Spring 2010

Simulaion-Solving Dynamic Models ABE 5646 Week 2, Spring 2010 Week Descripion Reading Maerial 2 Compuer Simulaion of Dynamic Models Finie Difference, coninuous saes, discree ime Simple Mehods Euler Trapezoid

Simulaion-Solving Dynamic Models ABE 5646 Week 2, Spring 2010 Week Descripion Reading Maerial 2 Compuer Simulaion of Dynamic Models Finie Difference, coninuous saes, discree ime Simple Mehods Euler Trapezoid

Chapter 11. Heteroskedasticity The Nature of Heteroskedasticity. In Chapter 3 we introduced the linear model (11.1.1)

") Chaper 11 Heeroskedasiciy 11.1 The Naure of Heeroskedasiciy In Chaper 3 we inroduced he linear model y = β+β x (11.1.1) 1 o explain household expendiure on food (y) as a funcion of household income (x).

Chaper 11 Heeroskedasiciy 11.1 The Naure of Heeroskedasiciy In Chaper 3 we inroduced he linear model y = β+β x (11.1.1) 1 o explain household expendiure on food (y) as a funcion of household income (x).

STRUCTURAL CHANGE IN TIME SERIES OF THE EXCHANGE RATES BETWEEN YEN-DOLLAR AND YEN-EURO IN

Inernaional Journal of Applied Economerics and Quaniaive Sudies. Vol.1-3(004) STRUCTURAL CHANGE IN TIME SERIES OF THE EXCHANGE RATES BETWEEN YEN-DOLLAR AND YEN-EURO IN 001-004 OBARA, Takashi * Absrac The

Inernaional Journal of Applied Economerics and Quaniaive Sudies. Vol.1-3(004) STRUCTURAL CHANGE IN TIME SERIES OF THE EXCHANGE RATES BETWEEN YEN-DOLLAR AND YEN-EURO IN 001-004 OBARA, Takashi * Absrac The

Section 4 NABE ASTEF 232

Secion 4 NABE ASTEF 3 APPLIED ECONOMETRICS: TIME-SERIES ANALYSIS 33 Inroducion and Review The Naure of Economic Modeling Judgemen calls unavoidable Economerics an ar Componens of Applied Economerics Specificaion

Secion 4 NABE ASTEF 3 APPLIED ECONOMETRICS: TIME-SERIES ANALYSIS 33 Inroducion and Review The Naure of Economic Modeling Judgemen calls unavoidable Economerics an ar Componens of Applied Economerics Specificaion

DEPARTMENT OF ECONOMICS

ISSN 0819-6 ISBN 0 730 609 9 THE UNIVERSITY OF MELBOURNE DEPARTMENT OF ECONOMICS RESEARCH PAPER NUMBER 95 NOVEMBER 005 INTERACTIONS IN REGRESSIONS by Joe Hirschberg & Jenny Lye Deparmen of Economics The

ISSN 0819-6 ISBN 0 730 609 9 THE UNIVERSITY OF MELBOURNE DEPARTMENT OF ECONOMICS RESEARCH PAPER NUMBER 95 NOVEMBER 005 INTERACTIONS IN REGRESSIONS by Joe Hirschberg & Jenny Lye Deparmen of Economics The

Lecture 4 Kinetics of a particle Part 3: Impulse and Momentum

MEE Engineering Mechanics II Lecure 4 Lecure 4 Kineics of a paricle Par 3: Impulse and Momenum Linear impulse and momenum Saring from he equaion of moion for a paricle of mass m which is subjeced o an

MEE Engineering Mechanics II Lecure 4 Lecure 4 Kineics of a paricle Par 3: Impulse and Momenum Linear impulse and momenum Saring from he equaion of moion for a paricle of mass m which is subjeced o an

The General Linear Test in the Ridge Regression

ommunicaions for Saisical Applicaions Mehods 2014, Vol. 21, No. 4, 297 307 DOI: hp://dx.doi.org/10.5351/sam.2014.21.4.297 Prin ISSN 2287-7843 / Online ISSN 2383-4757 The General Linear Tes in he Ridge

ommunicaions for Saisical Applicaions Mehods 2014, Vol. 21, No. 4, 297 307 DOI: hp://dx.doi.org/10.5351/sam.2014.21.4.297 Prin ISSN 2287-7843 / Online ISSN 2383-4757 The General Linear Tes in he Ridge