UNIT ROOT TESTS, COINTEGRATION, ECM, VECM, AND CAUSALITY MODELS

|

|

|

- Beverly Henry

- 6 years ago

- Views:

Transcription

1 UNIT ROOT TESTS, COINTEGRATION, ECM, VECM, AND CAUSALITY MODELS Compiled by M&B EFA is desroying he brains of curren generaion s researchers in his counry. Please sop i as much as you can. Thank you. The aim of his lecure is o provide you wih he key conceps of ime series economerics. To is end, you are able o undersand ime-series based researches, officially published in inernaional journals 1 such as applied economics, applied economerics, and he likes. Moreover, I also expec ha some of you will be ineresed in ime series daa analysis, and choose he relaed opics for your fuure hesis. As he ime his lecure is compiled, I believe ha he Vienam ime series daa 2 is long enough for you o conduc such sudies. This is jus a brief summary of he body of knowledge in he field according o my own undersanding. Therefore, i has no scienific value for your ciaions. In addiion, researches using bivariae models have no 1 Seleced papers were compiled by Phung Thanh Binh & Vo Duc Hoang Vu (2009). You can find hem a he H library. 2 The mos imporan daa sources for hese sudies can be World Bank s World Developmen Indicaors, IMF-IFS, GSO, and Reuers Thomson. 1

2 been highly appriciaed by inernaional journal s ediors and my universiy s supervisors. As a researcher, you mus be fully responsible for your own choice in his field of research. My advice is ha you should firsly sar wih he research problem of your ineres, no wih daa you have and saisical echniques you know. A he curren ime, EFA becomes he mos supid phenomenon of young researchers ha I ve ever seen in my universiy of economics, HCMC. They blindly imiae ohers. I don wan he series of models presened in his lecure will become he second wave of research ha annoys he fuure generaion of my universiy. Therefore, jus use i if you really need and undersand i. Some opics such as serial correlaion, ARIMA models, ARCH family models, srucural breaks 3, and panel uni roo and coinegraion ess are beyond he scope of his lecure. You can find hem elsewhere such as economerics exbooks, journal aricles, and my lecure noes in Vienamese. The aim of his lecure is o provide you: An overview of ime series economerics The concep of nonsaionary The concep of spurious regression The uni roo ess The shor-run and long-run relaionships 3 My aricle abou hreshold coinegraion and causaliy analysis in growh-energy consumpion nexus ( did menion abou his issue. 2

3 Auoregressive disribued lag (ARDL) model and error correcion model (ECM) Single-equaion esimaion of he ECM using he Engle-Granger 2-sep mehod Vecor auoregressive (VAR) models Granger causaliy ess (boh coinegraed and noncoinegraed series) Esimaing a sysem of ECMs using vecor error correcion model (VECM) Opimal lag lengh selecion crieria ARDL and bounds es for coinegraion Basic pracicaliies in using Eviews and Saa Suggesed research opics 1. AN OVERVIEW OF TIME SERIES ECONOMETRICS In his lecure, we will mainly discuss single equaion esimaion echniques in a very differen way from wha you have previously learned in he basic economerics course. According o Aseriou (2007), here are various aspecs o ime series analysis bu he mos common heme o hem is o fully exploi he dynamic srucure in he daa. Saying differenly, we will exrac as much informaion as possible from he pas hisory of he series. The analysis of ime series is usually explored wihin wo fundamenal ypes, namely, ime series forecasing and dynamic modelling. Pure ime series forecasing, such as ARIMA and ARCH/GARCH family models, is ofen menioned as univariae analysis. Unlike mos oher economerics, in univariae analysis we do no 3

4 concern much wih building srucural models, undersanding he economy or esing hypohesis, bu wha we really concern is developing efficien models, which are able o forecas well. The efficien forecasing models can be empirically evaluaed using various ways such as significance of he esimaed coefficiens (especially he longes lags in ARIMA), he posiive sign of he coefficiens in ARCH, diagnosic checking using he correlogram, Akaike and Schwarz crieria, and graphics. In hese cases, we ry o exploi he dynamic iner-relaionship, which exiss over ime for any single variable (say, asse prices, exchange raes, ineres raes, ec). On he oher hand, dynamic modelling, including bivariae and mulivariae ime series analysis, is mosly concerned wih undersanding he srucure of he economy and esing hypohesis. However, his kind of modelling is based on he view ha mos economic series are slow o adjus o any shock and so o undersand he process mus fully capure he adjusmen process which may be long and complex (Aseriou, 2007). The dynamic modelling has become increasingly popular hanks o he works of wo Nobel laureaes in economics 2003, namely, Granger (for mehods of analyzing economic ime series wih common rends, or coinegraion) and Engle (for mehods of analyzing economic ime series wih ime-varying volailiy or ARCH) 4. Up o now, dynamic 4 hp://nobelprize.org/nobel_prizes/economics/laureaes/2003/ 4

5 modelling has remarkably conribued o economic policy formulaion in various fields. Generally, he key purpose of ime series analysis is o capure and examine he dynamics of he daa. In ime series economerics, i is equally imporan ha he analyss should clearly undersand he erm sochasic process. According o Gujarai (2003), a random or sochasic process is a collecion of random variables ordered in ime. If we le Y denoe a random variable, and if i is coninuous, we denoe i a Y(), bu if i is discree, we denoe i as Y. Since mos economic daa are colleced a discree poins in ime, we usually use he noaion Y raher han Y(). If we le Y represen GDP, we have Y1, Y2, Y3,, Y88, where he subscrip 1 denoes he firs observaion (i.e., GDP for he firs quarer of 1970) and he subscrip 88 denoes he las observaion (i.e., GDP for he fourh quarer of 1991). Keep in mind ha each of hese Y s is a random variable. In wha sense we can regard GDP as a sochasic process? Consider for insance he GDP of $ billion for 1970Q1. In heory, he GDP figure for he firs quarer of 1970 could have been any number, depending on he economic and poliical climae hen prevailing. The figure of $ billion is jus a paricular realizaion of all such possibiliies. In his case, we can hink of he value of $ billion as he mean value of all possible values of GDP for he firs quarer 5

6 of Therefore, we can say ha GDP is a sochasic process and he acual values we observed for he period 1970Q1 o 1991Q4 are a paricular realizaion of ha process. Gujarai (2003) saes ha he disincion beween he sochasic process and is realizaion in ime series daa is jus like he disincion beween populaion and sample in cross-secional daa. Jus as we use sample daa o draw inferences abou a populaion; in ime series, we use he realizaion o draw inferences abou he underlying sochasic process. The reason why I menion his erm before examining specific models is ha all basic assumpions in ime series models relae o he sochasic process (populaion). Sock & Wason (2007) say ha he assumpion ha he fuure will be like he pas is an imporan one in ime series regression. If he fuure is like he pas, hen he hisorical relaionships can be used o forecas he fuure. Bu if he fuure differs fundamenally from he pas, hen he hisorical relaionships migh no be reliable guides o he fuure. Therefore, in he conex of ime series regression, he idea ha hisorical relaionships can be generalized o he fuure is formalized by he concep of saionariy. 2. STATIONARY STOCHASTIC PROCESSES 2.1 Definiion According o Gujarai (2003), a key concep underlying sochasic process ha has received a grea deal of 6

7 aenion and scruiny by ime series analyss is he socalled saionary sochasic process. Broadly speaking, a ime series is said o be saionary if is mean and variance are consan over ime and he value of he covariance 5 beween he wo periods depends only on he disance or gap or lag beween he wo ime periods and no he acual ime a which he covariance is compued (Gujarai, 2011). In he ime series lieraure, such a sochasic process is known as a weakly saionary or covariance saionary. By conras, a ime series is sricly saionary if all he momens of is probabiliy disribuion and no jus he firs wo (i.e., mean and variance) are invarian over ime. If, however, he saionary process is normal, he weakly saionary sochasic process is also sricly saionary, for he normal sochasic process is fully specified by is wo momens, he mean and he variance. For mos pracical siuaions, he weak ype of saionariy ofen suffices. According o Aseriou (2007), a ime series is weakly saionary when i has he following characerisics: (a) (b) (c) exhibis mean reversion in ha i flucuaes around a consan long-run mean; has a finie variance ha is ime-invarian; and has a heoreical correlogram ha diminishes as he lag lengh increases. 5 or he auocorrelaion coefficien. 7

8 In is simples erms a ime series Y is said o be weakly saionary (hereafer refer o saionary) if: (a) Mean: E(Y) = (consan for all ); (b) Variance: Var(Y) = E(Y-) 2 = 2 (consan for all ); and (c) Covariance: Cov(Y,Y+k) = k = E[(Y-)(Y+k-)] where k, covariance (or auocovariance) a lag k, is he covariance beween he values of Y and Y+k, ha is, beween wo Y values k periods apar. If k = 0, we obain 0, which is simply he variance of Y (= 2 ); if k = 1, 1 is he covariance beween wo adjacen values of Y. Suppose we shif he origin of Y from Y o Y+m (say, from he firs quarer of 1970 o he firs quarer of 1975 for our GDP daa). Now, if Y is o be saionary, he mean, variance, and auocovariance of Y+m mus be he same as hose of Y. In shor, if a ime series is saionary, is mean, variance, and auocovariance (a various lags) remain he same no maer a wha poin we measure hem; ha is, hey are ime invarian. According o Gujarai (2003), such ime series will end o reurn o is mean (called mean reversion) and flucuaions around his mean (measured by is variance) will have a broadly consan ampliude. If a ime series is no saionary in he sense jus defined, i is called a nonsaionary ime series. In 8

9 oher words, a nonsaionary ime series will have a ime-varying mean or a ime-varying variance or boh. Why are saionary ime series so imporan? According o Gujarai (2003, 2011), here are a leas wo reasons. Firs, if a ime series is nonsaionary, we can sudy is behavior only for he ime period under consideraion. Each se of ime series daa will herefore be for a paricular episode. As a resul, i is no possible o generalize i o oher ime periods. Therefore, for he purpose of forecasing or policy analysis, such (nonsaionary) ime series may be of lile pracical value. Second, if we have wo or more nonsaionary ime series, regression analysis involving such ime series may lead o he phenomenon of spurious or nonsense regression (Gujarai, 2011; Aseriou, 2007). In addiion, a special ype of sochasic process (or ime series), namely, a purely random, or whie noise, process, is also popular in ime series economerics. According o Gujarai (2003), we call a sochasic process purely random if i has zero mean, consan variance 2, and is serially uncorrelaed. This is similar o wha we call he error erm, u, in he classical normal linear regression model, once discussed in he phenomenon of serial correlaion opic. This error erm is ofen denoed as u ~ iid(0, 2 ). 2.2 Random Walk Process 9

10 According o Sock and Wason (2007), ime series variables can fail o be saionary in various ways, bu wo are especially relevan for regression analysis of economic ime series daa: (1) he series can have persisen, long-run movemens, ha is, he series can have rends; and, (2) he populaion regression can be unsable over ime, ha is, he populaion regression can have breaks. For he purpose of his lecure, I only focus on he firs ype of nonsaionariy. A rend is a persisen long-erm movemen of a variable over ime. A ime series variable flucuaes around is rend. There are wo ypes of rends ofen seen in ime series daa: deerminisic and sochasic. A deerminisic rend is a nonrandom funcion of ime (i.e. Y = A + B*Time + u, Y = A + B*Time + C*Time 2 + u, and so on) 6. For example, he LEX [he logarihm of he dollar/euro daily exchange rae, LEX.wf1, Gujarai (2011)] is a nonsaionary seris (Figure 2.1), and is derended series (i.e. residuals from he regression of log(ex) on ime: e = log(ex) a b*time) is sill nonsaionary (Figure 2.2). This indicaes ha log(ex) is no a rend saionary series. 6 Y = a + bt + e => e = Y a bt is called he derended series. If Y is nonsaionary, while e is saionary, Y is known as he rend (sochasic) saionary (TSP). Here, he process wih a deerminisic rend is nonsaionary bu no a uni roo process. 10

11 Figure 2.1: Log of he dollar/euro daily exchange rae Figure 2.2: Residuals from he regression of LEX on ime. In conras, a sochasic rend is random and varies over ime. According o Sock and Wason (2007), i is more appropriae o model economic ime series as having 11

12 sochasic raher han deerminisic rends. Therefore, our reamen of rends in economic ime series focuses mainly on sochasic raher han deerminisic rends, and when we refer o rends in ime series daa, we mean sochasic rends unless we explicily say oherwise. The simples model of a variable wih a sochasic rend is he random walk. There are wo ypes of random walks: (1) random walk wihou drif (i.e. no consan or inercep erm) and (2) random walk wih drif (i.e. a consan erm is presen). The random walk wihou drif is defined as follow. Suppose u is a whie noise error erm wih mean 0 and variance 2. The Y is said o be a random walk if: Y = Y-1 + u (1) The basic idea of a random walk is ha he value of he series omorrow (Y+1) is is value oday (Y), plus an unpredicable change (u+1). From (1), we can wrie Y1 = Y0 + u1 Y2 = Y1 + u2 = Y0 + u1 + u2 Y3 = Y2 + u3 = Y0 + u1 + u2 + u3 Y4 = Y3 + u4 = Y0 + u1 + + u4 Y = Y-1 + u = Y0 + u1 + + u 12

13 In general, if he process sared a some ime 0 wih a value Y0, we have Y Y0 u (2) herefore, E (Y ) E(Y0 u ) Y0 In like fashion, i can be shown ha Var(Y ) (E Y 0 u 2 0 Y ) (E u 2 ) 2 Therefore, he mean of Y is equal o is iniial or saring value, which is consan, bu as increases, is variance increases indefiniely, hus violaing a condiion of saionariy. In oher words, he variance of Y depends on, is disribuion depends on, ha is, i is nonsaionary. Ineresingly, if we re-wrie (1) as (Y Y-1) = Y = u (3) where Y is he firs difference of Y. I is easy o show ha, while Y is nonsaionary, is firs difference is saionary. And his is very significan when working wih ime series daa. This is widely known as he difference saionary (sochasic) process (DSP). 13

14 Figure 2.3: A random walk wihou drif Figure 2.4: Firs difference of LEX. 14

15 The random walk wih drif can be defined as follow: Y = + Y-1 + u (4) where is known as he drif parameer. The name drif comes from he fac ha if we wrie he preceding equaion as: Y Y-1 = Y = + u (5) i shows ha Y drifs upward or downward, depending on being posiive or negaive. We can easily show ha, he random walk wih drif violaes boh condiions of saionariy: E(Y) = Y0 +. Var(Y) = 2 In oher words, boh mean and variance of Y depends on, is disribuion depends on, ha is, i is nonsaionary. Sock and Wason (2007) say ha because he variance of a random walk increases wihou bound, is populaion auocorrelaions are no defined (he firs auocovariance and variance are infinie and he raio of he wo is no well defined) 7. 7 Corr(Y,Y -1) = Cov(Y,Y ) Var(Y )Var(Y 1 ~ 1 ) 15

16 Figure 2.5: A random walk wih drif (Y = 2 + Y-1 + u) Figure 2.6: Random walk wih drif (Y = -2 + Y-1 + u). 16

17 2.3 Uni Roo Sochasic Process According o Gujarai (2003), he random walk model is an example of wha is known in he lieraure as a uni roo process. Le us wrie he random walk model (1) as: Y = Y-1 + u (-1 1) (6) This model resembles he Markov firs-order auoregressive model [AR(1)], menioned in he basic economerics course, serial correlaion opic. If = 1, (6) becomes a random walk wihou drif. If is in fac 1, we face wha is known as he uni roo problem, ha is, a siuaion of nonsaionariy. The name uni roo is due o he fac ha = 1. Technically, if = 1, we can wrie (6) as Y Y-1 = u. Now using he lag operaor L so ha Ly = Y-1, L 2 Y = Y-2, and so on, we can wrie (6) as (1-L)Y = u. If we se (1-L) = 0, we obain, L = 1, hence he name uni roo. Thus, he erms nonsaionariy, random walk, and uni roo can be reaed as synonymous. If, however, 1, ha is if he absolue value of is less han one, hen i can be shown ha he ime series Y is saionary. 2.4 Illusraive Examples Consider he AR(1) model as presened in equaion (6). Generally, we can have hree possible cases: 17

18 Case 1: < 1 and herefore he series Y is saionary. A graph of a saionary series for = 0.67 is presened in Figure 2.7. Case 2: > 1 where in his case he series explodes. A graph of an explosive series for = 1.26 is presened in Figure 2.8. Case 3: = 1 where in his case he series conains a uni roo and is non-saionary. Graph of saionary series for = 1 are presened in Figure 2.9. In order o reproduce he graphs and he series which are saionary, exploding and nonsaionary, we ype he following commands in Eviews: Sep 1: Open a new workfile (say, undaed ype), conaining 200 observaions. Sep 2: Generae X, Y, Z as he following commands: smpl 1 1 genr X=0 genr Y=0 genr Z=0 smpl genr X=0.67*X(-1)+nrnd genr Y=1.26*Y(-1)+nrnd genr Z=Z(-1)+nrnd 18

19 smpl Sep 3: Plo X, Y, Z using he line plo ype (Figures 2.7, 2.8, and 2.9). plo X plo Y plo Z Figure 2.7: A saionary series 19

20 1.6E E E E E E E E E Figure 2.8: An explosive series Figure 2.9: A nonsaionary series 20

21 3. THE UNIT ROOTS AND SPURIOUS REGRESSIONS 3.1 Spurious Regressions Mos macroeconomic ime series are rended and herefore in mos cases are nonsaionary. The problem wih nonsaionary or rended daa is ha he sandard ordinary leas squares (OLS) regression procedures can easily lead o incorrec conclusions. According o Aseriou (2007), i can be shown in hese cases ha he regression resuls have very high value of R 2 (someimes even higher han 0.95) and very high values of -raios (someimes even higher han 4), while he variables used in he analysis have no real inerrelaionships. Aseriou (2007) saes ha many economic series ypically have an underlying rae of growh, which may or may no be consan, for example GDP, prices or money supply all end o grow a a regular annual rae. Such series are no saionary as he mean is coninually rising however hey are also no inegraed as no amoun of differencing can make hem saionary. This gives rise o one of he main reasons for aking he logarihm of daa before subjecing i o formal economeric analysis. If we ake he logarihm of a series, which exhibis an average growh rae we will urn i ino a series which follows a linear rend and which is inegraed. This can be easily seen formally. Suppose we have a series X, which increases by 10% every period, hus: X = 1.1X-1 21

22 If we hen ake he logarihm of his we ge log(x) = log(1.1) + log(x-1) Now he lagged dependen variable has a uni coefficien and each period i increases by an absolue amoun equal o log(1.1), which is of course consan. This series would now be I(1). More formally, consider he model: Y = β1 + β2x + u (7) where u is he error erm. The assumpions of classical linear regression model (CLRM) require boh Y and X o have zero and consan variance (i.e., o be saionary). In he presence of nonsaionariy, hen he resuls obained from a regression of his kind are oally spurious 8 and hese regressions are called spurious regressions. The inuiion behind his is quie simple. Over ime, we expec any nonsaionary series o wander around (see Figure 3.1), so over any reasonably long sample he series eiher drif up or down. If we hen consider wo compleely unrelaed series which are boh nonsaionary, we would expec ha eiher hey will boh go up or down ogeher, or one will go up while he oher goes down. If we hen performed a regression of one series on he oher, we would hen find eiher a significan posiive 8 This was firs inroduced by Yule (1926), and re-examined by Granger and Newbold (1974) using he Mone Carlo simulaions. 22

23 relaionship if hey are going in he same direcion or a significan negaive one if hey are going in opposie direcions even hough really hey are boh unrelaed. This is he essence of a spurious regression. I is said ha a spurious regression usually has a very high R 2, saisics ha appear o provide significan esimaes, bu he resuls may have no economic meaning. This is because he OLS esimaes may no be consisen, and herefore all he ess of saisical inference are no valid. Granger and Newbold (1974) consruced a Mone Carlo analysis generaing a large number of Y and X series conaining uni roos following he formulas: Y = Y-1 + ey (8) X = X-1 + ex (9) where ey and ex are arificially generaed normal random numbers (as he same way performed in secion 2.4). Since Y and X are independen of each oher, any regression beween hem should give insignifican resuls. However, when hey regressed he various Ys o he Xs as show in equaion (8), hey surprisingly found ha hey were unable o rejec he null hypohesis of β2 = 0 for approximaely 75% of heir cases. They also found ha heir regressions had very high R 2 s and very low values of DW saisics. 23

24 To see he spurious regression problem, we can ype he following commands in Eviews (afer opening he new workfile, say, undaed wih 500 observaions) o see how many imes we can rejec he null hypohesis of β2 = 0. The commands (or smpl 1 1) genr Y=0 genr (or smpl 2 500) genr Y=Y(-1)+nrnd genr X=X(-1)+nrnd sca(r) Y ls Y c X An example of a plo of Y agains X obained in his way is shown in Figure 3.1. The esimaed equaion beween hese wo simulaed series is: Table 3.1: Spurious regression 24

25 Y TOPICS IN TIME SERIES ECONOMETRICS X Figure 3.1: Scaer plo of a spurious regression Granger and Newbold (1974) proposed he following rule of humb for deecing spurious regressions: If R 2 > DW saisic or if R 2 1 hen he esimaed regression mus be spurious. To undersand he problem of spurious regression beer, i migh be useful o use an example wih real economic daa. This example was conduced by Aseriou (2007). Consider a regression of he logarihm of real GDP (Y) o he logarihm of real money supply (M) and a consan. The resuls obained from such a regression are he following: 25

26 Y = M; R 2 = 0.945; DW = (4.743) (8.572) Here we see very good -raios, wih coefficiens ha have he righ signs and more or less plausible magniudes. The coefficien of deerminaion is very high (R 2 = 0.945), bu here is a high degree of auocorrelaion (DW = 0.221). This shows evidence of he possible exisence of spurious regression. In fac, his regression is oally meaningless because he money supply daa are for he UK economy and he GDP figures are for he US economy. Therefore, alhough here should no be any significan relaionship, he regression seems o fi he daa very well, and his happens because he variables used in he example are, simply, rended (i.e. nonsaionary). So, Aseriou (2007) recommends ha economericians should be very careful when working wih rended variables. You can find more such examples in Gujarai (2011, pp ) 3.2 Explaining he Spurious Regression Problem According o Aseriou (2007), in a slighly more formal way he source of he spurious regression problem comes from he fac ha if wo variables, X and Y, are boh saionary, hen in general any linear combinaion of hem will cerainly be saionary. One imporan linear combinaion of hem is of course he equaion error, and so if boh variables are saionary, he error in he equaion will also be saionary and have a well-behaved 26

27 disribuion. However, when he variables become nonsaionary, hen of course we can no guaranee ha he errors will be saionary and in fac as a general rule (alhough no always) he error iself be nonsaionary and when his happens, we violae he basic CLRM assumpions of OLS regression. If he errors were nonsaionary, we would expec hem o wander around and evenually ge large. Bu OLS regression because i selecs he parameers so as o make he sum of he squared errors as small as possible will selec any parameer which gives he smalles error and so almos any parameer value can resul. The simples way o examine he behaviour of u is o rewrie (7) as: u = Y β1 β2x (10) or, excluding he consan β1 (which only affecs u sequence by rescaling i): u = Y β2x (11) If Y and X are generaed by equaions (8) and (9), hen if we impose he iniial condiions Y0 = X0 = 0 we ge ha: u Y 0 e Y1 e Y2... e Yi (X 2 0 e X1 e X2... e Xi ) or u e e (12) i1 Yi 2 i1 Xi 27

28 From equaion (12), we realize ha he variance of he error erm will end o become infiniely large as increases. Hence, he assumpions of he CLRM are violaed, and herefore, any es, F es or R 2 are unreliable. In erms of equaion (7), here are four differen cases o discuss: Case 1: Boh Y and X are saionary 9, and he CLRM is appropriae wih OLS esimaes being BLUE. Case 2: Y and X are inegraed of differen orders. In his case, he regression equaions are meaningless. Case 3: Y and X are inegraed of he same order [ofen I(1)]and he u sequence conains a sochasic rend. In his case, we have spurious regression and i is ofen recommended o re-esimae he regression equaion in he semi-difference mehods (such as he FGLS mehod: Orcu-Cochrane procedure, AR(1), and Newey-Wes sandard error). These mehods did menion in my lecures abou serial correlaion and a brief review of basic economerics. Case 4: Y and X are inegraed of he same order and he u is saionary. In his special case, Y and X 9 Based on he saisical ess such as ADF, PP, and KPSS. 28

29 are said o be coinegraed. The concep of coinegraion will be examined in deail laer. 4. TESTING FOR UNIT ROOTS 4.1 Graphical Analysis According o Gujarai (2003), before one pursues formal ess, i is always advisable o plo he ime series under sudy. Such a plo (line graph of he level) and correlogram [of boh he level (ACF) and he firs difference (ACF and PACF)] gives an iniial clue abou he likely naure of he ime series. Such a inuiive feel is he saring poin of formal ess of saionariy (i.e. choose he appropriae es equaion). 4.2 Auocorrelaion Funcion and Correlogram Auocorrelaion is he correlaion beween a variable lagged one or more periods and iself. The correlogram or auocorrelaion funcion is a graph of he auocorrelaions for various lags of a ime series daa. According o Hanke (2005), he auocorrelaion coefficiens 10 for differen ime lags for a variable can be used o answer he following quesions: (1) Are he daa random? (This is usually used for he diagnosic ess of forecasing models). (2) Do he daa have a rend (nonsaionary)? 10 This is no explained in his lecure. You can make references from eiher Gujarai (2003: ), Hanke (2005: 60-74), or Nguyen Trong Hoai e al (2009: Chaper 3, 4, and 8). 29

30 (3) Are he daa saionary? (4) Are he daa seasonal? Besides, he correlogram is very useful when selecing he appropriae p and q in he ARIMA models and ARCH family models 11. (1) If a series is random, he auocorrelaions (i.e. ACF) beween Y and Y-k for any lag k are close o zero (i.e. he auocorrelaion coefficien is saisically insignifican). The successive values of a ime series are no relaed o each oher (Figure 4.1). In oher words, Y and Y-k are independen. (2) If a series has a (sochasic) rend, successive observaions are highly correlaed, and he auocorrelaion coefficiens are ypically significanly differen from zero for he firs several ime lags and hen gradually drop oward zero as he number of lags increases. The auocorrelaion coefficien for ime lag 1 is ofen very large (close o 1). The auocorrelaion coefficien for ime lag 2 will also be large. However, i will no be as large as for ime lag 1 (Figure 4.2). (3) If a series is saionary, he auocorrelaion coefficiens for lag 1 or lag 2 are significanly 11 See Nguyen Trong Hoai e al, 2009 and my lecure abou ARIMA models. 30

31 differen from zero and hen suddenly die ou as he number of lags increases (Figure 4.3). In oher words, Y and Y-1, Y and Y-2, Y and Y-3 are weakly correlaed; bu Y and Y-k [as k increases] are compleely independen. (4) If a series has a seasonal paern, a significan auocorrelaion coefficien will occur a he seasonal ime lag or muliples of seasonal lag (Figure 4.4). This paern is no imporan wihin his lecure conex. Figure 4.1: Correlogram of a random series 31

32 Figure 4.2: Correlogram of a nonsaionary series Figure 4.3: Correlogram of a saionary series 32

33 Figure 4.4: Correlogram of a seasonal series The correlogram becomes very useful for ime series forecasing and oher pracical (business) implicaions. If you conduc academic sudies, however, i is necessary o provide more formal saisics such as saisic 12, Box-Pierce Q saisic, Ljung-Box (LB) saisic, or especially uni roo ess. 4.3 Simple Dickey-Fuller Tes for Uni Roos Dickey and Fuller (1979, 1981) devised a procedure o formally es for nonsaionariy (hereafer refer o DF es). The key insigh of heir es is ha esing for nonsaionariy is equivalen o esing for he exisence of a uni roo. Thus he obvious es is he following which is based on he following simple AR(1) model: 12 See Nguyen Trong Hoai e al, 2009 and my lecure abou ARIMA models o undersand he sandard error in ime series economerics s.e. = 1/ n. 33

34 Y = Y-1 + u (13) Wha we need o examine here is = 1 (uniy and hence uni roo ). Obviously, he null hypohesis is H0: = 1, and he alernaive hypohesis is H1: < 1 (why?). We obain a differen (more convenien) version of he es by subracing Y-1 from boh sides of (13): Y Y-1 = Y-1 Y-1 + u Y = ( - 1)Y-1 + u Y = Y-1 + u (14) where = ( - 1). Then, now he null hypohesis is H0: = 0, and he alernaive hypohesis is H1: < 0 (why?). In his case, if = 0, hen Y follows a pure random walk (and, of course, Y is nonsaionary). Dickey and Fuller (1979) also proposed wo alernaive regression equaions ha can be used for esing for he presence of a uni roo. The firs conains a consan in he random walk process as in he following equaion: Y = + Y-1 + u (15) According o Aseriou (2007), his is an exremely imporan case, because such processes exhibi a definie rend in he series when = 0, which is ofen he case for macroeconomic variables. The second case is also allow, a non-sochasic ime rend in he model, so as o have: 34

35 Y = + T + Y-1 + u (16) The Dickey-Fuller es for saionariy is he simply he normal es on he coefficien of he lagged dependen variable Y-1 from one of he hree models (14, 15, and 16). This es does no, however, have a convenional disribuion and so we mus use special criical values which were originally calculaed by Dickey and Fuller. This is also known as he Dickey- Fuller au saisic (Gujarai, 2003; 2011). However, mos modern saisical packages such as Saa and Eviews rouinely produce he criical values for Dickey-Fuller ess a 1%, 5%, and 10% significan levels. MacKinnon (1991,1996) abulaed appropriae criical values for each of he hree above models and hese are presened in Table 4.1. Table 4.1: Criical values for DF es Model 1% 5% 10% Y = Y-1 + u Y = + Y-1 + u Y = + T + Y-1 + u Sandard criical values Source: Aseriou (2007) 35

36 In all cases, he es concerns wheher = 0. The DF es saisic is he saisic for he lagged dependen variable. If he DF saisical value is smaller in absolue erms han he criical value hen we rejec he null hypohesis of a uni roo and conclude ha Y is a saionary process. 4.4 Augmened Dickey-Fuller Tes for Uni Roos As he error erm is unlikely o be whie noise, Dickey and Fuller exended heir es procedure suggesing an augmened version of he es (hereafer refer o ADF es) which includes exra lagged erms of he dependen variable in order o eliminae auocorrelaion in he es equaion. The lag lengh 13 on hese exra erms is eiher deermined by Akaike Informaion Crierion (AIC) or Schwarz Bayesian/Informaion Crierion (SBC, SIC), or more usefully by he lag lengh necessary o whien he residuals (i.e. afer each case, we check wheher he residuals of he ADF regression are auocorrelaed or no hrough LM ess and no he DW es (why?)). The hree possible forms of he ADF es are given by he following equaions: 1 p Y Y Y u (17) i 1 i i 13 This issue will be discussed laer in his lecure. 36

37 1 p Y Y Y u (18) i1 1 i p i1 i Y T Y Y u (19) The difference beween he hree regressions concerns he presence of he deerminisic elemens α and T. The criical values for he ADF es are he same as hose given in Table 4.1 for he DF es. According o Aseriou (2007), unless he economerician knows he acual daa-generaing process, here is a quesion concerning wheher i is mos appropriae o esimae (17), (18), or (19). Daldado, Jenkinson and Sosvilla-Rivero (1990) sugges a procedure which sars from esimaion of he mos general model given by (19) and hen answering a se of quesions regarding he appropriaeness of each model and moving o he nex model. This procedure is illusraed in Figure 4.1. I needs o be sressed here ha, alhough useful, his procedure is no designed o be applied in a mechanical fashion. Ploing he daa and observing he graph is someimes very useful because i can clearly indicae he presence or no of deerminisic regressors. However, his procedure is he mos sensible way o es for uni roos when he form of he daa-generaing process is ypically unknown. In pracical sudies, researchers mosly use boh he ADF and he Phillips-Perron (PP) ess. Because he i i 37

38 disribuion heory ha supporing he Dickey-Fuller ess is based on he assumpion of random error erms [iid(0, 2 )], when using he ADF mehodology we have o make sure ha he error erms are uncorrelaed and hey really have a consan variance. Phillips and Perron (1988) developed a generalizaion of he ADF es procedure ha allows for fairly mild assumpions concerning he disribuion of errors. The regression for he PP es is similar o equaion (15). Y = + Y-1 + e (20) While he ADF es correcs for higher order serial correlaion by adding lagged differenced erms on he righ-hand side of he es equaion, he PP es makes a correcion o he saisic of he coefficien from he AR(1) regression (semi-difference mehod) o accoun for he serial correlaion in e. So, he PP saisics are jus modificaions of he ADF saisics ha ake ino accoun he less resricive naure of he error process. The expressions are exremely complex o derive and are beyond he scope of his lecure. Luckily, since mos saisical packages have rouines available o calculae hese saisics, i is good for researcher o es he order of inegraion of a series performing he PP es as well. The asympoic disribuion of he PP saisic is he same as he ADF saisic and herefore he MacKinnon (1991,1996) criical values are sill applicable. 38

39 Figure 4.1: Procedure for esing for uni roos Y Esimae he model T Y 1 p i1 Y i i u = 0? NO YES: Tes for he presence of he rend NO STOP: Conclude ha here is no uni roo is = 0? given ha = 0? NO = 0? YES STOP: Conclude ha Y has a uni roo YES Y Esimae he model Y 1 p i1 Y is = 0? i i u NO STOP: Conclude ha here is no uni roo YES: Tes for he presence of he consan NO is = 0? given ha = 0? NO = 0? YES STOP: Conclude ha Y has a uni roo YES Esimae he model Y Y 1 i1 Y i u is = 0? Source: Aseriou (2007) p i NO YES STOP: Conclude ha here is no uni roo STOP: Conclude ha Y has a uni roo 39

40 As wih he ADF es, he PP es can be performed wih he inclusion of a consan and linear rend, or neiher in he es regression. Dickey-Fuller ess may have low power (H0 of uni roo no rejeced, whereas in realiy here may be no uni roo) when ρ is close o one. This could be he case of rend saionariy (H0). An alernaive es is KPSS (Kwiakowski-Phillips-Schmid-Shin). Is es procedure is briefly summarized as: (1) Regress Y on inercep and ime rend and obain OLS residuals e. (2) Calculae parial sums S = es for all. s1 T 2 S (3) Calculae he es saisic KPSS = T s1 ˆ compare wih criical value. 2 2, and The criical values are rouinely produced by saisical packages such as Saa and Eviews. The null hypohesis is rejeced if he KPSS es saisic is larger han he seleced criical value. 4.5 Performing Uni Roo Tess in Eviews The DF/ADF es Table 4.2: DF/ADF es procedure Sep 1 Open he file ADF.wf1 by clicking File/Open/Workfile and hen choosing he file name from he appropriae pah. 40

41 Sep 2 Le s assume ha we wan o examine wheher he series named GDP conains a uni roo. Double click on he series named GDP o open he series window and choose View/Uni Roo Tes In he uni-roo es dialog box ha appears, choose he ype es (i.e. he Augmened Dickey- Fuller) by clicking on i. Sep 3 We hen specify wheher we wan o es for a uni roo in he level, firs difference, or second difference of he series. We can use his opion o deermine he number of uni roos in he series. However, we usually sar wih he level and if we fail o rejec he es in levels we coninue wih esing he firs difference and so on. Sep 4 We also have o specify which model of he hree ADF models we wish o use (i.e., wheher o include a consan, a consan and linear rend, or neiher in he es regression). For he model given by equaion (17) click on none in he dialog box; for he model given by equaion (18) click on inercep in he dialog box; and for he model given by equaion (19) click on inercep and rend in he dialog box; Sep 5 Finally, we have o specify he number of lagged dependen variables o be included in he model in order o correc he presence of serial correlaion. In pracice, we jus click he auomaic selecion on he lag lengh dialog box. Sep 6 Having specified hese opions, click <OK> o carry ou he es. Eviews repors he es 41

he criical value, and we conclude ha he series is saionary.")

42 saisic ogeher wih he esimaed es regression. Sep 7 We rejec he null hypohesis of a uni roo agains he one-sided alernaive if he ADF saisic is less han (lies o he lef of) he criical value, and we conclude ha he series is saionary. Sep 8 Afer running a uni roo es, we should examine he esimaed es regression repored by Eviews, especially if unsure abou he lag srucure or deerminisic rend in he series. We may wan o rerun he es equaion wih a differen selecion of righ-hand variables (add or delee he consan, rend, or lagged differences) or lag order. Source: Aseriou (2007) Figure 4.2: Illusraive seps in Eviews (ADF) 42

43 Table 4.3: ADF es of GDP series This figure is posiive, so he seleced model is incorrec (see Gujarai (2003)). 43

44 4.5.2 The PP/KPSS es Table 4.4: PP/KPSS es procedure Sep 1 Open he file PP.wf1 by clicking File/Open/Workfile and hen choosing he file name from he appropriae pah. Sep 2 Le s assume ha we wan o examine wheher he series named GDP conains a uni roo. Double click on he series named GDP o open he series window and choose View/Uni Roo Tes In he uni-roo es dialog box ha appears, choose he ype es (i.e. he Phillipd- Perron/Kwiakowski-Phillips-Schmid-Shin) by clicking on i. Sep 3 We hen specify wheher we wan o es for a uni roo in he level, firs difference, or second difference of he series. We can use his opion o deermine he number of uni roos in he series. However, we usually sar wih he level and if we fail o rejec he es in levels we coninue wih esing he firs difference and so on. Sep 4 We also have o specify which model of he hree we need o use (i.e. wheher o include a consan, a consan and linear rend, or neiher in he es regression). For he random walk model click on none in he dialog box; for he random wih drif model click on inercep in he dialog box; and for he random walk wih drif and wih deerminisic rend model click on inercep and rend in he dialog box. 44

45 Sep 5 Finally, for he PP/KPSS es we specify he lag runcaion o compue he Newey-Wes sandard error consisen esimae of he specrum a zero frequency. Sep 6 Having specified hese opions, click <OK> o carry ou he es. Eviews repors he es saisic ogeher wih he esimaed es regression. Sep 7 We rejec he null hypohesis of a uni roo agains he one-sided alernaive if he ADF saisic is less han (lies o he lef of) he criical value, and we conclude ha he series is saionary. Source: Aseriou (2007) Figure 4.3: Illusraive seps in Eviews (PP) 45

46 Table 4.5: PP es of GDP series This figure is posiive, so he seleced model is incorrec (see Gujarai (2003)). Table 4.6: ADF es of log(ex) (LEX.wf1, Gujarai, 2011) Table 4.7: ADF es of log(ex) (LEX.wf1, Gujarai, 2011) 46

47 Table 4.8: PP es of log(ex) (LEX.wf1, Gujarai, 2011) 5. SHORT-RUN AND LONG-RUN RELATIONSHIPS 5.1 Undersanding Conceps In case of bivariae model, you have once known he saic or shor-run causal relaionship beween wo ime series Y and X, where Y is dependen variable and X is independen variable. The OLS regression ofen experiences he serial correlaion, and we perform various remedies such as semi-difference mehods (Cochrane-Orcu, Prais-Winsen, AR(1)), firs difference mehod, and Newey-Wes sandard error. By any way, he purpose of your sudy is jus o know he shor-run slope or elasiciy of Y wih respec o X [Y/Y]. However, he naure of he srucural modeling is o discover he dynamic causal relaionship beween Y and X. In such model, you mus a leas disinguish beween shor-run 47

48 48 and long-run relaionship [slope or elasiciy]. To simplify our analysis, we consider he simple auoregressive disribued lag model [ARDL(1,1)] in he following form: Y = A0 + A1Y-1 + B0X + B1X-1 + u (21) We can analyse boh shor-run and long-run effecs (slopes or elasiciies) as follows: (1) Shor-run or saic effec: 0 B X Y (22) (2) Long-run or dynamic or equilibrium effec: T A 1 B B X Y (23) Proof: 0 B X Y B X Y A X Y = B.B A (why?) ) B A (A.B X Y A X Y (why?) )] B A (A.B X Y A X Y (why?) )] B (A.B A X Y A X Y (why?)

49 If A1 < 1, he cummulaive effec or long-run slope (Slr) will be he sum of all derivaives: 2 Slr B0 [A 1B0 B1] A 1[A 1B0 B1] A 1(A 1.B 0 B1)]... A1(A 1.B 0 B1)] (24) Muliply boh sides of (24) by A1, we have: 2 A1Slr A1B0 A 1[A 1B0 B1] A 1(A 1.B 0 B1)]... A1(A 1.B 0 B1)] (25) By subsrac (25) from (24), we obain: Slr A1Slr = B0 + B1 Slr = B 1 0 B A 1 1 = equaion (23) We can also ake expecaions o derive he long-run relaion beween Y and X: E(Y) = A0 + A1E(Y-1) + B0E(X) + B1E(X-1) E(Y) = A0 + A1E(Y) + B0E(X) + B1E(X) E(Y) - A1E(Y) = A0 + (B0 + B1)E(X) (1-A1)E(Y) = A0 + (B0 + B1)E(X) A0 (B 0 B1) => E(Y) = (E X) 1 A (1 A 1 = α + βe(x) or simply o wrie: Y * = α + βx * (26) Here, β = (B0+B1)/(1-A1) is he long-run effec of a lasing shock in X. And he shor-run effec of a change in X is B0. In he same oken, we can expand he model ARDL(p,q): 1 49

50 (1) Shor-run or saic effec: Y X B 0 (27) (2) Long-run or dynamic or equilibrium effec: YT X B 0 1 A B 1 1 B... B 2 2 A... A q p (28) 5.2 ARDL and Error Correcion Model (ECM) By subsracing Y-1 boh sides of equaion (23), and rearraning, we have: Y Y-1 = A0 + A1Y-1 Y-1 + B0X B0X-1 + B0X-1 + B1X-1 + u Y = A0 (1 A1)Y-1 + B0X + (B0+B1)X-1 + u A = B0X (1 A1) 0 (B 0 B1) Y 1 X1 + u (1 A1) (1 A1) = B0X (1 A1)Y X + u 1 1 = B0X Y X + u (29a) 1 1 = B0X ECT-1 + u (29b) This is applicable wih all ARDL models. Par in brackes of equaion (29a) is error-correcion erm (equilibrium error). Equaions (29a or 29b) are widely known as he error correcion model (ECM). Therefore, ECM and ARDL are basically he same if he series Y and X are inegraed of he same order [ofen I(1)] and coinegraed. In his model, Y and X are assumed o be in long-run equilibrium, i.e. changes in Y relae o changes in X 50

51 according B1. If Y-1 deviaes from he opimal value (i.e. is equilibrium), here is a correcion. Speed of adjusmen is given by = (1-A1), which is beween > 0 and <1. This will be furher discussed laer. 6. ENGLE-GRANGER 2-STEP METHOD OF COINTEGRATION 6.1 Coinegraion According o Aseriou (2007), he concep of coinegraion was firs inroduced by Granger (1981) and elaboraed furher Engle and Granger (1987), Engle and Yoo (1987), Phillips and Ouliaris (1990), Sock and Wason (1988), Phillips (1986 and 1987), and Johansen (1988, 1991, and 1995). I is known ha rended ime series can poenially creae major problems in empirical economerics due o spurious regressions. One way of resolving his is o difference he series successively unil saionary is achieved and hen use he saionary series for regression analysis. According o Aseriou (2007), his soluion, however, is no ideal because i no only differences he error process in he regression, bu also no longer gives a unique long-run soluion. If wo variables are nonsaionary, hen we can represen he error as a combinaion of wo cumulaed error processes. These cumulaed error processes are ofen called sochasic rends and normally we could expec ha hey would combine o produce anoher non-saionary 51

52 process. However, in he special case ha wo variables, say X and Y, are really relaed, hen we would expec hem o move ogeher and so he wo sochasic rends would be very similar o each oher and when we combine hem ogeher i should be possible o find a combinaion of hem which eliminaes he nonsaionariy. In his special case, we say ha he variables are coinegraed (Aseriou, 2007). Coinegraion becomes an overriding requiremen for any economic model using nonsaionary ime series daa. If he variables do no co-inegrae, we usually face he problems of spurious regression and economeric work becomes almos meaningless. On he oher hand, if he sochasic rends do cancel o each oher, hen we have coinegraion. Suppose ha, if here really is a genuine long-run relaionship beween Y and X, he alhough he variables will rise overime (because hey are rended), here will be a common rend ha links hem ogeher. For an equilibrium, or long-run relaionship o exis, wha we require, hen, is a linear combinaion of Y and X ha is a saionary variable [an I(0) variable]. A linear combinaion of Y and X can be direcly aken from esimaing he following regression: Y = β1 + β2x + u (30) And aking he residuals: û Y ˆ ˆ X (31)

53 If û ~ I(0), hen he variables Y and X are said o be co-inegraed. 6.2 An example of coinegraion TABLE14-1.wf1 gives quarerly daa on personal consumpion expendiure (PCE) and personal disposible (i.e. afer-ax) income (PDI) for he USA for he period (Gujarai, 2011: pp.226). Boh graph (Figure 6.1) and ADF ess (Table 6.1) indicae ha hese wo series are no saionary. They are I(1), ha is, hey have sochasic rends. In addiion, he regression of log(pce) on log(pdi) seems o be spurious. Since boh series are rending, le us see wha happens if we add a rend variable o he model. The elasiciy coefficien is now changed, bu he regression is sill spurious (Table 6). However, afer esimaing he regression of log(pce) on log(pdi) and rend, we realize ha he obained residuals is a saionary series [I(0)]. This implies ha a linear combinaion (e = log(pce) b1 b2log(pdi) b3t) cancels ou he sochasic rends in he wo variables. Therefore, his regression is, in fac, no spurious. In oher words, he variables log(pce) and log(pdi) are coinegraed. 53

54 LOG(PCE) LOG(PDI) Figure 6.1: Logs of PDI and PCE, USA Table 6.1: Uni roo ess for log(pce) 54

55 Table 6.2: Uni roo ess for log(pdi) Table 6.3: OLS regression of log(pce) on log(pdi) Table 6.4: Regression of log(pce) on log(pdi) and rend 55

56 Economically speaking, wo variables will be coinegraed if hey have a long-run, or equilibrium, relaionship beween hem. In he presen conex, economic heory ells us ha here is a srong relaionship beween consumpion expendiure and personal disposible income. In he language of coinegraion heory, he equaion log(pce) = B1 + B2log(PDI) + B3T is known as a coinegraing regression and he slope parameers B2 and B3 are known as coinegraing parameers. 6.3 Engle-Granger Tess for Coinegraion For single equaion, he simple ess of coinegraion are DF and ADF uni roo ess on he residuals esimaed from he coinegraing regression. These modified ess by he Engle- Granger (EG) and Augmened Engle-Granger (AEG) ess. Noice he difference beween he uni roo and coinegraion ess. Tess for uni roos are performed on single ime series, whereas simple coinegraion deals wih he relaionship among a group of variables, each having a uni roo (Gujarai, 2011). 6.4 Inerpreaion of he ECM According o Aseriou (2007), he conceps of coinegraion and he error correcion mechanism are very closely relaed. To undersand he ECM, i is beer o 56

57 hink firs of he ECM as a convenien reparamerizaion of he general linear auoregressive disribued lag (ARDL) model (see Secion 6). Consider he very simple dynamic ARDL model describing he behaviour of Y in erms of X as equaion (21): Y = A0 + A1Y-1 + B0X + B1X-1 + u (21) where u ~ iid(0, 2 ). In his model 14, he parameer B0 denoes he shor-run reacion of Y afer a change in X. The long-run effec is given when he model is in equilibrium where: Y * = α + βx * (26) Recall ha he long-run effec (slope oe elasiciy) beween Y and X is capured by β =(B0+B1)/(1-A1). I is noed ha, we need o make he assumpion ha A1 < 1 (why?) in order ha he shor-run model (21) converges o a long-run soluion [equaion (26), see Secion 6]. The ECM is shown in equaion (29a or 29b): Y = B1X Y 1 1 X + u (29a) or Y = B1X ECT-1 + u (29b) According o Aseriou (2007), wha is of imporance here is ha when he wo variables Y and X are coinegraed, 14 We can easily expand his model o a more general case for large numbers of lagged erms [ARDL(p,q)]. 57

58 he ECM incorporaes no only shor-run bu also long-run effecs. This is because he long-run equilibrium [Y-1 α βx-1] is included in he model ogeher wih he shor-run dynamics capured by he differenced erm. Anoher imporan advanage is ha all he erms in he ECM model are saionary and he sandard OLS esimaion is herefore valid. This is because if Y and X are I(1), hen Y and X are I(0), and by definiion if Y and X are coinegraed hen heir linear combinaion [Y-1 α βx-1] ~ I(0). A final imporan poin is ha he coefficien = (1-A1) provides us wih informaion abou he speed of adjusmen in cases of disequilibrium. To undersand his beer, consider he long-run condiion. When equilibrium holds, hen [Y-1 α βx-1] = 0. However, during periods of disequilibrium his erm is no longer be zero and measures he disance he sysem is away from equilibrium. For example, suppose ha due o a series of negaive shocks in he economy in period -1. This causes [Y-1 α βx-1] o be negaive because Y-1 has moved below is long-run equilibrium pah. However, since = (1-A1) is posiive (why?), he overall effec is o boos Y back owards is long-run pah as deermined by X in equaion (26). Noice ha he speed of his adjusmen o equilibrium is dependen upon he magniude of = (1-A1). 58

59 The coefficien in equaion (29a,b) is he errorcorrecion coefficien and is also called he adjusmen coefficien. In fac, ells us how much of he adjusmen o equilibrium akes place each period, or how much of he equilibrium error is correced each period. According o Aseriou (2007), i can be explained in he following ways: (1) If ~ 1, hen nearly 100% of he adjusmen akes place wihin he period 15, or he adjusmen is very fas. (2) If ~ 0.5, hen abou 50% of he adjusmen akes place each period. (3) If ~ 0, hen here seems o be no adjusmen. According o Aseriou (2007), he ECM is imporan and popular for many reasons: (1) Firsly, i is a convenien model measuring he correcion from disequilibrium of he previous period which has a very good economic implicaion. (2) Secondly, if we have coinegraion, ECM models are formulaed in erms of firs difference, which ypically eliminae rends from he variables involved; hey resolve he problem of spurious regressions. 15 Depending on he kind of daa used, say, annually, quarerly, or monhly. 59

60 (3) A hird very imporan advanage of ECM models is he ease wih hey can fi ino he general-o-specific (or Hendry) approach o economeric modeling, which is a search for he bes ECM model ha fis he given daa ses. (4) Finally he fourh and mos imporan feaure of ECM comes from he fac ha he disequilibrium error erm is a saionary variable. Because of his, he ECM has imporan implicaions: he fac ha he wo variables are coinegraed implies ha here is some auomaically adjusmen process which prevens he errors in he long-run relaionship becoming larger and larger. 6.5 Engle-Granger 2-Sep Mehod of Coinegraion Granger (1981) inroduced a remarkable link beween nonsaionary processes and he concep of long-run equilibrium; his link is he concep of coinegraion. Engle and Granger (1987) furher formulized his concep by inroducing a very simple es for he exisence of co-inegraing (i.e. long-run equilibrium) relaionships. This approach involves he following seps: Table 6.5: Engle-Granger 2-Sep Mehod: Sep-by-Sep Sep 1 Tes he variables for heir order of inegraion. The firs sep is o es each variable o deermine is order of inegraion. The Dickey- 60

61 Fuller and he augmened Dickey-Fuller ess can be applied in order o infer he number of uni roos in each of he variables. We migh face hree cases: a) If boh variables are saionary (I(0)), i is no necessary o proceed since sandard ime series mehods apply o saionary variables. b) If he variables are inegraed of differen orders, i is possible o conclude ha hey are no coinegraed. c) If boh variables are inegraed of he same order, we proceed wih sep wo. Sep 2 Esimae he long-run (possible co-inegraing) relaionship. If he resuls of sep 1 indicae ha boh X and Y are inegraed of he same order (usually I(1)) in economics, he nex sep is o esimae he long-run equilibrium relaionship of he form: Y ˆ ˆX û and obain he residuals of his equaion. If here is no coinegraion, he resuls obained will be spurious. However, if he variables are coinegraed, OLS regression yields consisen esimaors for he co- 61

62 inegraing parameer ˆ. Sep 3 Check for (coinegraion) he order of inegraion of he residuals. In order o deermine if he variables are acually coinegraed, denoe he esimaed residual sequence from he equaion by Thus, û. û is he series of he esimaed residuals of he long-run relaionship. If hese deviaions from long-run equilibrium are found o be saionary, he X and Y are coinegraed. Sep 4 Esimae he error correcion model. If he variables are coinegraed, he residuals from he equilibrium regression can be used o esimae he error correcion model and o analyse he long-run and shor-run effecs of he variables as well as o see he adjusmen coefficien, which is he coefficien of he lagged residual erms of he long-run relaionship idenified in sep 2. A he end, we always have o check for he accuracy of he model by performing diagnosic ess. Source: Aseriou (2007) According o Aseriou (2007), one of he bes feaures of he EG 2-sep mehod is ha i is boh very easy o 62

63 undersand and o implemen. However, i also remains some caveas: (1) One very imporan issue has o do wih he order of he variables. When esimaing he long-run relaionship, one has o place one variable in he lef-hand side and use he ohers as regressors. The es does no say anyhing abou which of he variables can be used as regressors and why. Consider, for example, he case of jus wo variables, X and Y. One can eiher regress Y on X (i.e. Y = C + DX + u1) or choose o reverse he order and regress X on Y (i.e. X = D + EY + u2). I can be shown, which asympoic heory, ha as he sample goes o infiniy he es for coinegraion on he residuals of hose wo regressions is equivalen (i.e. here is no difference in esing for uni roos in u1 and u2). However, in pracice, in economics we rarely have very big samples and i is herefore possible o find ha one regression exhibis coinegraion while he oher doesn. This is obviously a very undesirable feaure of he EG approach. The problem obviously becomes far more complicaed when we have more han wo variables o es. (2) A second problem is ha when here are more han wo variables here may be more han one inegraing relaionship, and EG 2-sep mehod using residuals from a single relaionship can no 63

64 rea his possibiliy. So, he mos imporan problem is ha i does no give us he number of co-inegraing vecors. (3) A hird and final problem is ha i replies on a wo-sep esimaor. The firs sep is o generae he residual series and he second sep is o esimae a regression for his series in order o see if he series is saionary or no. Hence, any error inroduced in he firs sep is carried ino he second sep. The EG 2-sep mehod in Eviews The EG 2-sep mehod is very easy o perform and does no require any more knowledge regarding he use of Eviews. For he firs sep, ADF and PP ess on all variables are needed o deermine he order of inegraion of he variables. If he variables (le s say X and Y) are found o be inegraed of he same order, hen he second sep involves esimaing he long-run relaionship wih simple OLS procedure. So he command here is simply: ls X c Y or ls Y c X depending on he relaionship of he variables. We hen need o obain he residuals of his relaionship which are given by: genr res1=resid 64

65 The hird sep (he acual es for coinegraion) is a uni roo es on he residuals, he command for which is: adf res1 for no lags, or adf(4) res1 for 4 lags in he augmenaion erm, and so on. 6.6 Engle-Granger 2-sep Mehod: An Example Use he example in Secion 6.2, we have he following error correcion model: Table 6.6: Error correcion model of LPCE and LPDI All coeeficiens in he able are individually saisically significan a 6% or lower level. The coefficien of abou 0.31 shows ha a 1% increase in log(pdi/pdi-1) will lead on average o a 0.31% increase 65

66 in ln(pce/pce-1). This is he shor-run consumpionincome elasiciy. The long-run value is given by he coinegraing regression (Table 6), which is abou The coefficien of he error-correcion erm of abou suggess ha abou 6% of he discrepancy beween long-erm and shor-erm PCE is correced wihin a quarer (quarerly daa), suggesing a slow rae of adjusmen o equilibrium. 7. VECTOR AUTOREGRESSIVE MODELS According o Aseriou (2007), i is quie common in economics o have models where some variables are no only explanaory variables for a given dependen variable, bu hey are also explained by he variables ha hey are used o deermine. In hose cases, we have models of simulaneous equaions, in which i is necessary o clearly idenify which are he endogenous and which are he exogenous or predeermined variables. The decision regarding such a differeniaion among variables was heavily criicized by Sims 16 (1980). According o Sims (1980), if here is simulaneiy among a number of variables, hen all hese variables should be reaed in he same way. In oher words, hese should be no disincion beween endogenous and exogenous variables. Therefore, once his disincion is abandoned, all variables are reaed as endogenous. This means ha 16 Nobel prize in economics

67 in is general reduced form, each equaion has he same se of regressors which leads o he developmen of he VAR models. VAR is defined as a sysem of ARDL equaions describing dynamic evoluion of a se of variables from heir common hisory (here vecor implies muliple variables involved. The VAR model is defined as follow. Suppose we have wo series, in which Y is affeced by no only is pas (or lagged) values bu curren 17 and lagged values of X, and simulaneously, X is affeced by no only is lagged values bu curren and lagged values of Y. This simple bivariae VAR model is given by: p Y = A1 + B1X + C jy j + D jx j + u1 (32) j1 p p j1 X = A2 + B2Y + E jy j + F jx j + u2 (33) j1 where we assume he u1 and u2 are uncorrelaed whienoise error erms, called impulses or innovaions or shocks in he language of VAR (Gujarai, 2011, pp.266). Noe ha hese equaions are no reduced-form equaions since Y has a conemporaneous impac on X, and X has a conemporaneous impac on Y. p j1 17 Gujarai (2011, pp.266) said ha [from he poin of view of forecasing] each equaion in VAR conains only is own lagged values and he lagged values of he oher variables in he sysem. Similarly, Wooldridge (2003, pp ) said ha wheher he conemporaneous (curren) value is included or no depends parly on he purpose of he equaion. In forecasing, i is rarely included. 67

68 The bivariae VAR ofen has he following feaures (according o Gujarai, 2011, pp.266): (1) Alhough he number of lagged values of each variable can be differen, in mos cases we use he same number of lagged erms in each equaion. (2) The bivariae VAR sysem given above is known as a VAR(p) model, because we have p lagged values of each variable on he righ-hand side. If we have only one lagged value of each variable on he righ-hand side, i would be a VAR(1) model; if wo lagged erms, i would be a VAR(2) model; and so on. (3) Alhough we are dealing wih only wo variables, he VAR sysem can be exended o several variables. (4) In he wo-variable sysem, here can be a mos one coinegraing, or equilibrium, relaionship beween hem. If we have a hree-variable VAR sysem, here can be a mos wo coinegraing relaionships beween he hree variables. Noe ha all variables have o be of he same order of inegraion. The following cases are disinc: (1) All he variables are I(0) (saionary): one is in he sandard case, i.e. a VAR in level. (2) All he variables are I(d) (non-saionary) wih d > 0 (usually d = 1): 68

69 If here are nonsaionary [I(1)] variables, we esimae a VAR using firs differences of variables [ha are I(0)] o remove common rends. The variables are coinegraed: he error correcion erm has o be included in he VAR model. The model becomes a vecor error correcion model (VECM) which can be seen as a resriced VAR. Why (if possible) a VECM insead of a VAR on differenced variables? VECM gives long-run srucural relaions plus informaion on adjusmen, which provides beer insigh in economic processes. The variables are no coinegraed: he variables have firs o be differenced d imes and one has a VAR in difference. According o Aseriou (2007), he VAR model has some good characerisics. Firs, i is very simple because we do no have o worry abou which variables are endogenous or exogenous. Second, esimaion is very simple as well, in he sense ha each equaion can be esimaed wih he usual OLS mehod separaely. Third, forecass obained from VAR models are in mos cases beer han hose obained from he far more complex simulaneous equaion models (see Mahmoud, 1984; McNees, 1986). Besides forecasing purposes, VAR models also provide framework for causaliy ess, which will be presened shorly. 69

70 However, on he oher hand he VAR models have faced severe criicism on various differen poins. According o Aseriou (2007), he VAR models have been criicised by he following aspecs. Firs, hey are a-heoreic since hey are no based on any economic heory. Since iniially here are no resricions on any of he parameers under esimaion, in effec everyhing causes everyhing. However, saisical inference is ofen used in he esimaed models so ha some coefficiens ha appear o be insignifican can be dropped, in order o lead models ha migh have an underlying consisen heory. Such inference is normally carried ou using wha are called causaliy ess. Second, hey are criicised due o he loss of degrees of freedom. Thus, if he sample size is no sufficienly large, esimaing ha large a number of parameers, say, a hree-variable VAR model wih 12 lags for each, will consume many degrees of freedom, creaing problems in esimaion. Third, he obained coefficiens of he VAR models are difficul o inerpre since hey oally lack any heoreical background. 8. VECM AND COINTEGRATION 8.1 Rank of Coinegraing Marix In his secion, we exend he single-equaion error correcion model o a mulivariae one. Le s assume ha we have hree variables, Y, X and W, which can all be 70

71 71 endogenous, i.e. we have ha (using marix noaion for Z = [Y,X,W]) Z = A1Z-1 + A2Z ApZ-p + u (34) A VAR(p) can be reformulaed in a vecor error correcion model as follows: Z = 1 Z Z p-1 Z-p+1 + Z-1 + u (35) where he marix conains informaion regarding he long-run relaionships. We can decompose = β where will include he speed of adjusmen o equilibrium coefficiens, while β will be he long-run marix of coefficiens. Therefore, he β Z-1 erm is equivalen o he error correcion erm [Y-1 α βx-1] in he single-equaion case, excep ha now β Z-1 conains up o (p 1) vecors in a mulivariae framework. For simpliciy, we assume ha p = 2, so ha we have only wo lagged erms, and he model is hen he following: u W X Y W X Y W X Y (33) or u W X Y W X Y W X Y (34)

72 Le us now analyse only he error correcion par of he firs equaion (i.e. for Y on he lef-hand side) which gives: 1Z-1 = ([11β β12][ 11β β22] Y 1 [ 11β β32]) X 1 W 1 (35) Equaion (35) can be rewrien as: 1Z-1 = 11(β11Y-1 + β21x-1 + β31w-1) + 12(β12Y-1 + β22x-1 + β32w-1) (36) which shows clearly he wo co-inegraing vecors wih heir respecive speed of adjusmen erms 11 and 12. Wha are advanages of he muliple equaion approach? (1) From he muliple equaion approach we can obain esimaes for boh co-inegraing vecors (36), while he simple equaion we have only a linear combinaion of he wo long-run relaionships. (2) Even if here is only one co-inegraing relaionship (for example he firs only) raher han wo, wih he muliple equaion approach we can calculae all hree differing speeds of adjusmen coefficiens ( ). (3) Only when 21 = 31 = 0, and only one co-inegraing relaionship exiss, can we hen say ha he muliple equaion mehod is he same (reduces o) as 72

73 he single equaion approach, and herefore, here is no loss from no modelling he deerminans of X and W. Here, i is good o menion as well ha when 21 = 31 = 0, is equivalen o X and W being weakly exogenous. Suppose ha we have k variables in a VECM, he kk marix conains he error correcion erms (linear combinaions of k variables in Z-1 ha are I(0). Table 8.1: Rank of marix and is implicaions Rank of Implicaions r = 0 There is no coinegraion. No sable longrun relaions beween variables. VECM is no possible (only VAR in firs differences). 0 < r < k There are r coinegraing vecors. These vecors describe he long-run relaionships beween variables. VECM is o.k. r = k All variables are already saionary. No need o esimae he model as VECM. VAR on unransformed daa is o.k. 8.2 Johansen s Tes for Coinegraion Tes Procedure According o Aseriou (2007), if we have more han wo variables in he model, hen here is a possibiliy of having more han one co-inegraing vecor. By his we mean ha he variables in he model migh form several equilibrium relaionships. In general, for k number of variables, we can have only up o k-1 co-inegraing 73

74 vecors. To find ou how many coinegraing relaionships exis among k variables requires he use of Johansen s mehodology 18. This mehod involves he following seps: Table 8.2: Johansen s approach Sep 1 Tesing he order of inegraion of all variables. Sep 2 Seing he appropriae lag lengh of he model. Seing he value of he lag lengh is affeced by he omission of variables ha migh affec only he shor-run behavior of he model. This is due o he fac ha omied variables insanly become par of he error erm. Therefore, very careful inspecion of he daa and he funcional relaionship is necessary before proceeding wih esimaion in order o decide wheher o include addiional variables. I is whie common o use dummy variables o ake ino accoun shor-run shocks o he sysem, such as poliical evens ha had imporan effecs on macroeconomic condiions. The mos common procedure in choosing he opimal lag lengh is o esimae a VAR model including all variables in levels (nondifferenced). This VAR model should be 18 Similar o EG approach, he Johansen s approach also requires all variables in he sysem are inegraed of he same order 1 [I(1)]. 74

75 esimaed for a large number of lags, hen reducing down by re-esimaing he model for one lag less unil we reach zero lag. In each of hese models, we inspec he values of he AIC and he SBC crieria, as well as he diagnosics concerning auocorrelaion, heeroskedasiciy, possible ARCH effecs and normaliy of he residuals. In general, he model ha minimizes AIC and SBC is seleced as he one wih he opimal lag lengh. This model should also pass all he diagnosic checks. Sep 3 Choosing he appropriae model regarding he deerminisic componens in he mulivariae sysem. Anoher imporan aspec in he formulaion of he dynamic model is wheher an inercep and/or rend should ener eiher he shor-run or he long-run model, or boh models. The general case of he VECM including all he various opions ha can possibly happen is given by he following equaion: Z = 1 Z k-1 Z-p ( Z 1 1 ) 1 Z u (37) In general five disinc models can be considered. Alhough he firs and he fifh model are no ha realisic, we presen all of hem for reasons of complemenariy. 75

76 Model 1: No inercep or rend in CE (coinegraing equaion) or VAR (1 = 2 = 1 = 2 = 0). Model 2: Inercep (no rend) in CE, no inercep or rend in VAR (1 = 2 = 2 = 0). Model 3: Inercep in CE and VAR, no rend in CE and VAR (1 = 2 = 0). Model 4: Inercep in CE and VAR, linear rend in CE, no rend in VAR (2 = 0). Model 5: Inercep and quadraic rend in CE, inercep and linear rend in VAR. Sep 4 Deermining he rank of or he number of coinegraing vecors. There are wo mehods for deermining he number of co-inegraing relaions, and boh involve esimaion of marix. (1) One mehod ess he null hypohesis, ha Rank() = r agains he hypohesis ha he rank is r+1. So, he null in his case is ha here are coinegraing vecors and ha we have up o r co-inegraing relaionships, wih he alernaive suggesing here is (r+1) vecors. The es saisics are based on he characerisic roos (also called eigenvalues) obained from he esimaion procedure. The es consiss of ordering 76

77 he larges eigenvalues in descending order and considering wheher hey are significanly differen from zero. To undersand he es procedure, suppose we obained n characerisic roos denoed by 1 > 2 > 3 > > n. If he variables under examinaion are no coinegraed, he rank of is zero and all he characerisic roos will equal zero. Therefore, ( 1 ˆ ) will be equal o 1 i and since ln(1) = 0. To es how many of he numbers of he characerisic roos are significanly differen from zero, his es uses he following saisic: r,r 1) T ln(1 ˆ ) (38) max( r 1 As we said before, he es saisic is based on he maximum eigenvalue and because of ha is called he maximal eigenvalue saisic (denoed by max). (2) The second mehod is based on a likelihood raio es abou he race of he marix (and because of ha i is called he race saisic). The race saisic considers wheher he race is increased by adding more eigenvalues beyond he r h eigenvalue. The null hypohesis in his case is ha he number of co-inegraing vecors is less han or equal o r. From he previous analysis, i is clear ha when all ˆ i = 77

78 0, he race saisic is equal o zero as well. This saisic is calculaed by: n race ( r) T ln(1 ˆ r 1) (39) i r 1 Criical values for boh saisics are provided by Johansen and Juselius (1990). These criical values are direcly provided from Eviews afer conducing a coinegraion es. Source: Aseriou (2007) A Numerical Example Remind ha we rejec he null hypohesis ha r, he number of coinegraing vecors, is less han k if he es saisic is greaer han he criical values specified. Table 8.3: Trace es H 0 H 1 Saisic 95% Criical Decision r = 0 r = Rejec H0 r 1 r = Accep H0 r 2 r = Accep H0 r 3 r = Accep H0 We conclude ha his daa exhibis one coinegraing vecor. 78

79 8.2.3 The Johansen approach in Eviews Eviews has a specific command for esing for coinegraion using Johansen approach under group saisics. Consider he file Johansen.wf1, which has quarerly daa for hree macroeconomic variables: X, Y, and Z. Sep 1: Deermine he order of inegraion for he variables. To do his, we apply he uni-roo ess on all hree variables. We apply he Doldado, Jenkinson and Sosvilla- Rivero (1990) procedure for choosing he appropriae model and we deermine he number of lags according o he SBC crierion. Table 8.4: Inegraion of he variables a level 79

80 Table 8.5: Inegraion of he variables a difference 80

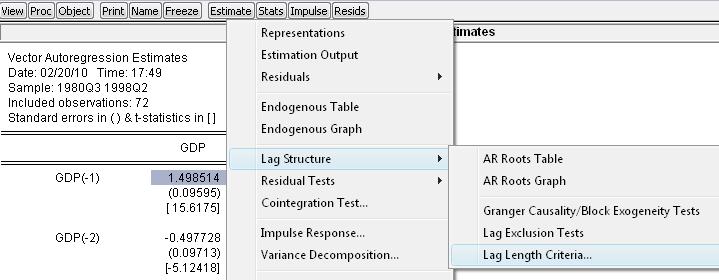

81 Sep 2: Deermine he opimal lag lengh Unforunaely, Eviews does no allow us o auomaically deec he lag lengh (in CE es equaion), so we need o esimae he model for a large number of lags and hen reduce down o check for he opimal value of AIC and SBC. A rule of humb is o choose he lag lengh according o he daa inerval (year, quarer, monh). By doing his, we found ha he opimal lag lengh is 4 lags (quarerly daa). In Eviews, we can auomaically deermine he lag lengh as he following seps. (1) Esimae unresriced VAR (using I(0) variables in he VAR model, i.e. firs differences) wih he defau lag lengh (rouinely 2). (2) A he VAR esimaes, selec View/Lag Srucure/Lag Lengh Crieria 81

82 Figure 8.1: Lag lengh crieria Sep 3: Perform he es equaion for coinegraion wih opimal lag lengh deermined above. We es each one of he models for coinegraion in Eviews by opening Quick/Group Saisics/Coinegraion Tes. Then in he series lis window, we ener he names of he series o check for coinegraion, for example: X Y Z hen press <OK>. The five alernaive models explained in Sep 3 above are given under labels 1, 2, 3, 4, and 5. There is anoher opion (opion 6 in Eviews) ha compares all hese models ogeher. 82

numbers 1 2 for inclusion of wo lags.")

83 Figure 8.2: Johansen es specificaion In our case, we wish o esimae models 2, 3, and 4 (because as noed earlier models 1 and 5 occur only very rarely). To esimae model 2, we selec ha model, and specify he number of lags in he boom-righ corner box ha has he (defaul by Eviews) numbers 1 2 for inclusion of wo lags. We change he 1 2 ro 1 4 for four lags, and click <OK> o ge he resuls. Noe ha here is anoher box ha allows us o include (by yping heir names) variables ha will be reaed as exogenous. Here we usually pu variables ha are eiher found o be I(0) or dummy variables ha possibly affec he behaviour of he model. 83

84 Doing he same for models 3 and 4 (in he uniled group window selec View/Coinegraion Tes) and simply change he model by clicking nex o 3 or 4. We ge he resuls as he following ables. Table 8.6: Coinegraion es resuls (model 2) Table 8.7: Coinegraion es resuls (model 3) 84

85 Table 8.8: Coinegraion es resuls (model 4) Sep 4: Decide which of he esimaed models o choose in esing for coinegraion. We can use Opion 6 in Figure 8.2 o selec he bes model o use in he VECM. Table 8.9: Johansen Coinegraion Tes Summary 85

. 8.")

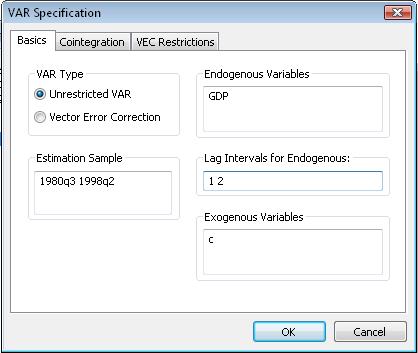

Quick/Esimae VAR (2) In VAR Specificaion, choose Vecor Error Correcion in VAR ype,")

86 From his summary, we see ha Model 4 (Linear, Inercep, and Trend) seems o be he bes model (one coinegraing vecor). 8.3 Esimaion of VECM in Eviews Afer deermining opimal lag lengh, and number of coinegraing vecors, we sar esimaing he VECM: (1) Quick/Esimae VAR (2) In VAR Specificaion, choose Vecor Error Correcion in VAR ype, add all variables in Endogeneous Variables, hen choose Lag Lengh. Figure 8.3: VAR specificaion 86

87 (3) We hen ener number of coinegraing in Coinegraion : Figure 8.4: Coinegraion Table 8.10: VECM esimaes 87

88 9. CAUSALITY TESTS According o Aseriou (2007), one of he good feaures of VAR models is ha hey allow us o es he direcion of causaliy. Causaliy in economerics is somewha differen o he concep in everyday use (ake examples?); i refers more o he abiliy of one variable o predic (and herefore cause) he oher. Suppose wo saionary variables, say Y and X, affec each oher wih disribued lags. The relaionship beween Y and X can be capured by a VAR model. In his case, i is possible o have ha (a) Y causes X (Unidirecional Granger causaliy from Y o X), (b) X causes Y (Unidirecional Granger causaliy from X o Y), (c) here is a bi-direcional feedback (causaliy among he variables), and finally (d) he wo variables are independen. The problem is o find an appropriae procedure ha allows us o es and saisically deec he cause and effec relaionship among variables. Granger (1969) developed a relaively simple es ha defined causaliy as follows: a variable Y is said o Granger-cause X, if X can be prediced wih greaer accuracy by using pas values of he Y variable raher han no using such pas values, all oher erms remaining unchanged. This es has been widely applied in economic policy analysis. 88

89 9.1 The Granger Causaliy Tes The Granger causaliy es for he of wo saionary variables, say, Y and X, involves as a firs sep he esimaion of he following VAR model: p Y = A1 + j1 p X = A2 + j1 C + D + u1 (40) j Y j j Y j p j1 p j X j E + F + u2 (41) j1 j X j where i is assumed ha boh u1 and u1 are uncorrelaed whie-noise error erms, and Y and X are inegraed of order 1. In his model, we can have he following differen cases: Case 1 The lagged X erms in equaion (40) are saisically differen from zero as a group, and he lagged Y erms in equaion (41) are no saisically differen from zero. In his case, we have ha X causes Y. Case 2 The lagged Y erms in equaion (41) are saisically differen from zero as a group, and he lagged X erms in equaion (40) are no saisically differen from zero. In his case, we have ha Y causes X. Case 3 Boh ses of lagged X and lagged Y erms are saisically differen from zero as a group in equaion (40) and (41), so ha we have bi- 89

90 direcional causaliy beween Y and X. Case 4 Boh ses of lagged X and lagged Y erms are no saisically differen from zero in equaion (40) and (41), so ha X is independen of Y. The Granger causaliy es, hen, involves he following procedures. Firs, esimae he VAR model given by equaions (40) and (41). Then check he significance of he coefficiens and apply variable deleion ess firs in he lagged X erms for equaion (40), and hen in he lagged Y erms in equaion (41). According o he resul of he variable deleion ess, we may conclude abou he direcion of causaliy based upon he four cases menioned above. More analyically, and for he case of one equaion (i.e. we will examine equaion (40)), i is inuiive o reverse he procedure in order o es for equaion (41), and we perform he following seps: Sep 1 Regress Y on lagged Y erms as in he following model: Y A p C Y j1 j u j 1 (42) and obain he RSS of his regression (which is he resriced one) and label i as RSSR. Sep 2 Regress Y on lagged Y erms plus lagged X erms as in he following model: 90

91 Y A 1 p C Y j1 j p j DjX j u1 (40) j1 and obain he RSS of his regression (which is he unresriced one) and label i as RSSU. Sep 3 Se he null and alernaive hypoheses as below: H H p 0 : Dj 0 or X does no cause Y j1 p 1 : Dj 0 or X does cause Y j1 Sep 4 Calculae he F saisic for he normal Wald es on coefficien resricions given by: F (RSSR RSSU)/ p RSS /(N k) u where N is he included observaions and k = 2p + 1 is he number of esimaed coefficiens in he unresriced model. Sep 5 If he compued F value exceeds he criical F value, rejec he null hypohesis and conclude ha X causes Y. Open he file GRANGER.wf1 and hen perform as follows: 91

92 Figure 9.1: An illusraion of GRANGER in Eviews 19 Why I use he firs differenced series? 19 However, his is no a good way of conducing Granger causaliy es (why?) 92

proposed an alernaive es for causaliy making use of he fac ha in any general noion of causaliy, i is no possible for he fuure o cause he presen.")

93 Noe ha his lag specificaion is no highly appreciaed in empirical sudies (why?). Table 9.2: A resul of he Granger causaliy ess 9.2 The Sims Causaliy Tes Sims (1980) proposed an alernaive es for causaliy making use of he fac ha in any general noion of causaliy, i is no possible for he fuure o cause he presen. Therefore, when we wan o check wheher a variable Y causes X, Sims suggess esimaing he following VAR model: 93