Inference in Regression Analysis

|

|

|

- Dayna Park

- 6 years ago

- Views:

Transcription

1 ECNS 561 Inference

2 Inference in Regression Analysis Up to this point 1.) OLS is unbiased 2.) OLS is BLUE (best linear unbiased estimator i.e., the variance is smallest among linear unbiased estimators) But, so far, we have not explored the sampling distribution of β j Under our Gauss-Markov assumptions, the sampling distribution can have virtually any shape Conditioning on Xs, our sampling distribution of the OLS estimators depend on the underlying distribution of errors To make the sampling distributions of the β j tractable, we assume the unobserved error is distributed normally.

3 Assumption MLR.6 Normality The population error ε is independent of the right-hand-side variables x 1, x 2,, x k and is normally distributed with zero mean and variance σ 2 : ε ~ Normal(0, σ 2 ) For cross-sectional regressions MLR.1-MLR.6 are called the classical linear model (CLM) assumptions We refer to this as the classical linear model Under the CLM assumptions, the OLS estimators have a stronger efficiency property than under the Gauss-Markov assumptions (MLR.1-MLR.5) It can be shown that the OLS estimators are the minimum variance unbiased estimators We no longer have to restrict our comparison to estimators that are linear in the y i Summarized as y x ~ Normal(β 0 + β 1 x β k x k, σ 2 ) i.e., conditional on x, y has a normal distribution with mean linear in x 1,, x k and a constant variance

4

5 Because ε is the sum of many different unobserved factors affecting y, we can invoke the CLT to conclude that ε has an approximate normal distribution This argument has merit, but also some weaknesses The factors in ε can have very different distributions in the population Normal approximation can be poor depending on how many factors appear in ε and how different their distributions are CLT assumes unobserved factors affect y in a separate, additive fashion. If ε is a complicated function of the unobserved factors, then the CLT argument does not really apply Whether or not the normality assumption is appropriate is very much an empirical question E.g., No theorem says that a variable denoting wages conditional on education, experience, etc. is normally distributed Since wage 0, it cannot have a normal distribution Also, minimum wage laws that create a fraction of the population who earn the exact same wage also violate the assumption of normality We can sometimes use transformations (e.g., log) to get closer to a normal distribution Other applications where the normality assumption clearly fails is when y can only take on a few values We will address these issues further in Ch. 5 We will see that, when N is large, nonnormality of ε is not a serious problem

6 For now, we will make the normality assumption this translates into the following theorem: Under the classical linear model assumptions (i.e., MLR.1- MLR.6), conditional on the sample values of the independent variables, β j ~ Normal(β j, Var( β j )) -subtract off mean and divide by s.d. to obtain a standard normal r.v. β j β j sd( β j ) ~ Normal(0, 1) [show that this holds]

7 The proof that the β j are normally distributed is as follows (remember, we are making the assumption that the errors are normal and we want to show how this assumption implies that the OLS estimates are distributed normal): -Each β j can be written as β j = β j + i 1 n w ij ε i where w ij = r ij SSR j, r ij is the i th residual from the regression of x j on all the other independent variables and SSR j is the sum of the squared residuals form this same regression -Since the w ij depend only on the Xs, they can be treated as fixed -Thus, β j is just a linear combo of the errors of the sample -A linear combo of independent normal random variables is itself normally distributed (see our notes from our review of probability theory) -We can actually go a little further -Any linear combo of the β 0, β 1,, β k -Any subset of the β j has a joint normal distribution These facts are vital to the hypothesis testing we will cover below

8 Hypothesis Testing (single population parameter) For what follows, consider our standard population model under the CLM assumptions y = β 0 + β 1 x β k x k + ε Here, we study how to test hypotheses about a particular β j To conduct hypothesis test, we require the following Under the CLM assumptions MLR.1 MLR.6, β j β j se( β j ) ~ t n-k-1 where k + 1 is the number of unknown parameters in the population model y = β 0 + β 1 x β k x k + ε and n k 1 is the degrees of freedom t distribution comes from the fact that σ in sd( β j ) has been replaced with σ

9 The above theorem allows us to test hypotheses involving the β j. In most applications, our interest is in testing the null H 0 : β j = 0 We can think of this as testing whether x j shares a relationship with y that is statistically distinguishable from zero For example, consider the following equation Crime i = β 0 + β 1 Educ i + β 2 Income i + ε i The null H 0 : β 1 = 0 tests whether, conditional on Income, Educ is statistically significantly related to Crime. The statistic we use to test the above null is the t statistic t β j β j se( β j )

10 Because we are testing H 0 : β j = 0, it make sense to use our unbiased estimate, β j, for guidance. Our question is, how far is β j from zero? A sample value of β j very far from zero provides evidence against the null But, there is a sampling error in our estimate of β j, so the magnitude of the coefficient estimate must be weighed against its sampling error Because the standard error of β j is an estimate of the standard deviation, t β j measures how many estimated standard deviations β j is away from zero. Values of t β j sufficiently far from zero will result in a rejection of the null The exact decision rule depends on the alternative hypothesis and the chosen level of statistical significance

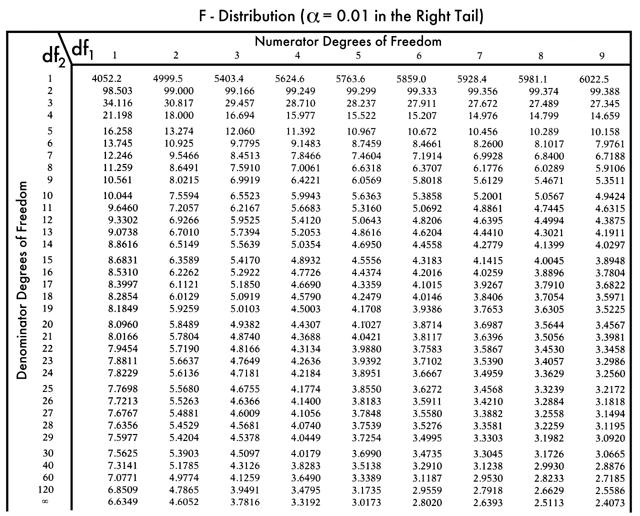

11 Testing against One-Sided Alternatives Consider the following one-sided alternative H 1 : β j > 0 To choose a rejection rule, we first decide on a significance level or the probability of reject H 0 when it is in fact true If we choose the 5% level, we say that we are willing to mistakenly reject H 0 when it is true 5% of the time We are looking for a sufficiently large positive value of t β j in order to reject H 0 : β j = 0 By sufficiently large, we mean the 95 th percentile in a t distribution with n k 1 degrees of freedom we denote this by c (i.e., our critical value) The one-sided rejection rule is that H 0 is rejected in favor of H 1 at the 5% level if t β j > c (see Table G.2 for choosing c)

12 For significance level of 5% and df = 28

13 Two-Sided Alternatives Here, we are interested in testing H 0 : β j = 0 against The rejection rule is H 1 : β j 0 t β j > c For a two-tailed test, c is chosen to make the area in each tail of the t distribution equal to 2.5%. That is, c is the 97.5 th percentile in the t distribution with n k 1 df. When a specific alternative is not stated, it is usually considered twosided. Our default is generally going to be a two-sided alternative tested at the 5% level

14 Testing Other Hypotheses Consider the null H 0 : β j = a j where a j is the hypothesized value of β j Everything is the same as before, we just specify the t stat as t = β j a j se( β j )

15 Computing p-values for t Tests Comparing the t stat to a critical value involves choosing a level of significance If we compute a p-value instead, then we can answer the question, What is the smallest significance level at which the null hypothesis would be rejected? A p-value for testing the null hypothesis H 0 : β j = 0 against the twosided alternative is P( T > t ) where we let T denote a t distributed random variable with n k 1 df

16 In an example where df = 40 and t = 1.85, the p-value is p-value = P( T > 1.85) = 2P(T > 1.85) = 2(.0359) =.0718 where P(T > 1.85) is the area to the right of 1.85 in a t distribution with 40 df If the null is true, we would observe an absolute value of the t stat as large as 1.85 about 7.2 percent of the time So, in this case, we would fail to reject the null at the 5% level, but reject at the 10% level. Weakly statistically significant Statistically significant at conventional levels

17 Remember, when hypothesis testing, don t just get caught up in statistical significance! Statistical significance vs. Economic significance Magnitude of estimate Sign of estimate

18 Confidence Intervals Using the fact that β j β j has a t distribution with n k 1 degrees se( β j ) of freedom, simple manipulation leads to a CI for the unknown β j : a 95% CI, given by β j ± c se β j, where c is the 97.5 th percentile in a t n-k-1 distribution.

19 Problems Ch. 4, #2 Consider an equation to explain salaries of CEOs in terms of annual firm sales, return on equity (roe, in percentage form), and return on the firm s stock (ros, in percentage form): log(salary) = β 0 + β 1 log(sales) + β 2 roe + β 3 ros + ε (i) In terms of the model parameters, state the null hypothesis that, after controlling for sales and roe, ros has no effect on CEO salary. State the alternative that better stock market performance increases a CEO s salary Ans. H 0 : β 3 = 0. H 1 : β 3 > 0

20 log(salary) = β 0 + β 1 log(sales) + β 2 roe + β 3 ros + ε (ii) Using a dataset on firms, suppose the following was obtained via OLS log(salary)= log(sales) roe ros (.32) (.035) (.0041) (.00054) N = 209, R 2 =.283 By what percentage is salary predicted to increase if ros increases by 50 points? Does ros share an economically large relationship with salary? Ans. -Recall, we interpret a log-level model as % y = 100β x (or, e β x 1) -So, a 50 point increase in ros is associated with an increase in salary by 1.2 (e =.012) percent -A 1.2 percent increase in salary that is related to a 50 percent increase in a return on a firm s stock does not seem economically meaningful

21 log(salary)= log(sales) roe ros (.32) (.035) (.0041) (.00054) N = 209, R 2 =.283 (iii) Test the null hypothesis that ros has no effect on salary against the alternative that ros has a positive effect. Carry out the test at the 10% significance level. Ans. The 10% critical value for a one-tailed test, using df = 200, is (table) The t stat on ros is.00024/ =.44, which is well below the critical value. Therefore, we fail to reject H 0 at the 10% significance level and say that the relationship between ros and salary is statistically indistinguishable from zero.

22 log(salary)= log(sales) roe ros (.32) (.035) (.0041) (.00054) N = 209, R 2 =.283 (iv) Would you include ros in a final model explaining CEO compensation in terms of firm performance? Ans. Based on this sample, ros is not a statistically significant predictor of CEO compensation. However, including ros may not be causing harm Q. What does this depend on? -It depends on how correlated it is with the other independent variables

23 Ch. 4, #4 Are rent rates influenced by the student population in a college town? Let rent be the average monthly rent paid on rental units in a college town in the United States. Let pop denote the total city population, avginc the average city income, and pctstu the student population as a percentage of the total population. One model to test for a relationship is log(rent) = β 0 + β 1 log(pop) + β 2 log(avginc) + β 3 pctstu + ε (i) State the null hypothesis that size of the student body relative to the population has no ceteris paribus effect on monthly rents. State the alternative that there is an effect. Ans. H 0 : β 3 = 0. H 1 : β 3 0 (ii) What signs do you expect for β 1 and β 2? Ans. -Ceteris paribus, a larger population increases the demand for rental housing, which should increase rents. -The demand for overall housing is higher when average income is higher, pushing up the cost of housing, including rental rates.

24 (iii) Suppose the following equation is estimated using data for 64 college towns log(rent) = log pop log aveinc pctsu (.844) (.039) (.081) (.0017) N = 64 R 2 =.458 What is wrong with the following statement: A 10% increase in population is associated with about a 6.6% increase in rent? Ans. -Remember a Log-log model is interpreted as % y = β 1 % x. -The coefficient on log(pop) is an elasticity. A correct statement is that a 10% increase in population increases rent by.066(10) =.66% (iv) Test the hypothesis stated in part (i) at the 1% level. Ans. -With df = 64 4, the 1% critical value for a two-tailed test is (table). -The t-stat is about 3.29, which is well above the critical value. -We conclude that β 3 is statistically different from zero at the 1% level.

25 Ch. 4, #5 Consider the estimated equation based on data from 500 college students colgpa = hsGPA +.015ACT.083skipped (.33) (.094) (.011) (.026) N = 500, R 2 =.234 where colgpa is college GPA, hsgpa is high school GPA, ACT is high school ACT score, and skipped is the average number of lectures missed per week (i) Using the standard normal approximation, find the 95% CI for β hsgpa Ans..412 ± 1.96(.094), where 1.96 is the critical value associated with a two-sided test at the 5% level (table). So, the 95% CI is [.228,.596]. (ii) Can you reject the hypothesis H 0 : β hsgpa =.4 against the two-sided alternative at the 5% level? No, because the value.4 is well inside the 95% CI. (iii) Can you reject the hypothesis H 0 : β hsgpa = 1 against the two-sided alternative at the 5% level? Yes, because 1 is well outside of the 95% CI [show regression output in a STATA example]

26 Back to #2 Back to #4 Back to #5

27 Testing Hypotheses about a Single Linear Combination of the Parameters Often we want to test hypotheses involving more than one of the population parameters Consider the following population model from your text that compares the returns to education at junior colleges and four-year colleges (i.e., universities) log(wage) = β 0 + β 1 jc + β 2 univ + β 3 exper + ε where jc = # of yrs. attending a two-year college univ = # of years at a four-year college exper = months in the workforce The hypothesis of interest is whether one year at a junior college is worth one year at a university H 0 : β 1 = β 2

28 What is our alternative of interest? Easy to justify a one-sided alternative hypothesis of interest a year at a junior college is worth les than a year at a university H 1 : β 1 < β 2 Conceptually, construction of the t-stat is the same as before when we write the null as Our t-stat is as follows H 0 : β 1 - β 2 = 0 t = β 1 β 2 se( β 1 β 2 ) Easy to obtain the numerator, but more difficult to obtain the denominator

29 To find the denominator, we first obtain the variance of the difference Var β 1 β 2 = Var β 1 + Var β 2 2Cov( β 1, β 2 ) The standard deviation of the difference between the two coefficient estimates is just the square root of the equation above, and, because [se( β 1 )] 2 is an unbiased estimator of Var( β 1 ), we have se β 1 β 2 = {[se β 1 ] 2 + [se β 2 ] 2 2Cov β 1, β 2 } 1/2 The covariance statistic is generally not reported in your standard regression output. But, most software packages have post estimation commands that allow one to easily test the hypothesis above (which we will see soon once we discuss the F test).

30 Testing Multiple Linear Restrictions: The F Test Suppose we want to test whether a set of variables has no effect on the dependent variable Consider the example from your textbook where we model major league baseball players salaries log(salary) = β 0 + β 1 years + β 2 gamesyr + β 3 bavg + β 4 hrunsyr + β 5 rbisyr + ε where salary is total salary, years is years in the league, gamesyr is average games played per year, bavg is career batting average, hrunsyr is home runs per year, and rbisyr is runs batted in per year. Suppose we want to test the null hypothesis that, conditional on years in the league and games per year, the statistics for performance (i.e., bavg, hrunsyr, rbisyr) have no effect on salary. H 0 : β 3 = 0, β 4 = 0, β 5 = 0 We refer to a test of multiple restrictions as a joint hypothesis test The alternative is that, conditional on years in the league and games played per year, performance measures matter. This can simply be stated as H 1 : H 0 is not true

31 t stat to test the above null doesn t work It puts no restrictions on the other parameters We would have three outcomes to contend with one for each t stat We need a way to test the restrictions jointly Suppose we have data on major league baseball players and we estimate the following log(salary) = years gamesyr bavg (0.29) (.0121) (.0026) (.00110) hrunsyr rbisyr (.0161) (.0072) N = 353, SSR = , R 2 =.6278 We can see that none of the performance measures are individually statistically significant Does this mean we can reject the below null? H 0 : β 3 = 0, β 4 = 0, β 5 = 0

32 To figure this out, we need to derive a test of multiple restrictions whose distribution is known and tabulated here, the SSR is going to come in handy We want to figure out how much the SSR increases when we drop the performance measures from the model B/c OLS estimates are chosen to minimize the sum of squared residuals, the SSR always increases when we drop variables from the regression What we want to know is whether the increase is large enough, relative to the SSR in the regression controlling for all of the variables, to warrant rejecting the null Suppose we estimated the model only controlling for years played and games per year and obtained the following log(salary) = years gamesyr (.11) (.0125) (.0013) N = 353, SSR = , R 2 =.5971

33 We can also derive the test for the general case. Consider the unrestricted model y = β 0 + β 1 x 1 + β 2 x β k x k + ε where the number of parameters in this model is k + 1 Suppose we are interested in testing q exclusion restrictions; i.e, the null that q of the variables in the equation above have coefficients equal to zero. We can state the null as So, our restricted model is H 0 : β k-q+1 = 0,, β k = 0 y = β 0 + β 1 x 1 + β 2 x β k-q x k-q + ε Remember, we want to look at the relative increase in the SSR when going from the unrestricted to the restricted model. The F statistic is defined as F ( SSRr SSRur ) / q SSR / ( n k 1) ur where SSR r is the sum of squared residuals from the restricted model and SSR ur is the sum of squared residuals from the unrestricted model

34 To use the F stat, we must know its sampling distribution under the null so we can choose critical values and form rejection rules. It can be shown that, under H 0, F is distributed as an F random variable with (q, n k 1) degrees of freedom F ~ F q, n-k-1 (see our probability theory notes for more details on the F stat) We will reject the null when F is large enough again, this will depend on our chosen significance level (see Table G.3 for critical values for the F distribution) We reject H 0 in favor of H 1 at the chosen level of significance if F > c

35

36 Back to our baseball example F = (SSR r SSR ur )/q SSR ur /(n k 1) = ( )/ /( ) = 9.55 Critical value for testing joint significance at 1% level is approximately 3.78 (see table) So, we easily reject the hypothesis that bavg, hrunsyr, and rbisyr have no effect on salary Is this outcome surprising due to the fact that none of these variables are individually statistically significant? What is happening is that the two variables hrunsyr and rbisyr are highly correlated, and this multicollinearity makes it difficult to uncover the partial effect of each variable; this is reflected in the individual t stats The F stat tests whether all three variables are jointly significant, and multicollinearity between hrunsyr and rbisyr is much less relevant for testing this hypothesis In general, the F stat is useful for testing exclusion of a group of variables when the variables in the group are highly correlated We can substitute in for SSR (= SST(1 R 2 )) and express our F-stat in terms of R 2 F = (R 2 ur R 2 r )/q (1 R 2 ur )/(n k 1) [Show t-stat in Mata. Show f-stat in canned Stata procedure]

37 F Statistic for Overall Significance of a Regression Consider the null H 0 : x 1, x 2, x k do not help explain y This says is that none of the explanatory variables share a statistically significant relationship with y This is stated in terms of the parameters of our model as H 0 : β 1 = β 2 = = β k = 0 The alternative is that at least one of the betas is different from 0 This implies the restricted model of y = β 0 + ε The F stat for testing the null is thus F = (R 2 )/k (1 R 2 )/(n k 1) here, k = q because the # of restrictions is equal to the # of variables in the population model The restricted R 2 is simply zero because all independent variables have been dropped when estimating the restricted model. If we fail to reject the null, then there is no evidence that any of the independent variables help to explain y This overall significance of the regression is generally reported in regression software (show STATA example)

38 Testing General Linear Restrictions Sometimes we might be interested, for theoretical reasons, in testing a null hypothesis that is more complicated than just excluding some independent variables Consider the following log(price) = β 0 + β 1 log(assess) + β 2 log(lotsize) + β 3 log(sqrft) + β 4 bdrms + ε where price is house price, assess is the assessed housing value before home sold, lotsize is the size of the lot in feet, sqrft is the square footage of the house, bdrms is the number of bedrooms Suppose we want to test whether the assessed housing price is a rational valuation i.e, an X% change in assess should be associated with an X% change in price i.e., β 1 = 1 In addition, the remaining covariates should not help to explain variation in price, conditional on the assessed value Thus, we have the following null H 0 : β 1 = 1, β 2 = 0, β 3 = 0, β 4 = 0

39 Unrestricted model: log(price) = β 0 + β 1 log(assess) + β 2 log(lotsize) + β 3 log(sqrft) + β 4 bdrms + ε (1) Restricted model: log(price) = β 0 + log(assess) + ε which we can rewrite as follows for estimation purposes log(price) - log(assess) = β 0 + ε (2) This is just a model with an intercept, but with a different dependent variable than in the first equation above The procedure for computing the F stat is the same Calculate the SSR r from equation (2) and the SSR ur from equation (1) One point to emphasize here We cannot use the R 2 version of the F stat because the dependent variable is different across the two equations and, thus, the total sum of squares from the two regressions will be different As a general rule, the SSR form of the F stat should be used if a different dependent variable is needed for running the restricted regression [this is easily implemented in STATA show with example]

40 back

41 -finish hypothesis testing with Wald and LR/LM tests

Multiple Regression Analysis: Inference MULTIPLE REGRESSION ANALYSIS: INFERENCE. Sampling Distributions of OLS Estimators

1 2 Multiple Regression Analysis: Inference MULTIPLE REGRESSION ANALYSIS: INFERENCE Hüseyin Taştan 1 1 Yıldız Technical University Department of Economics These presentation notes are based on Introductory

1 2 Multiple Regression Analysis: Inference MULTIPLE REGRESSION ANALYSIS: INFERENCE Hüseyin Taştan 1 1 Yıldız Technical University Department of Economics These presentation notes are based on Introductory

CHAPTER 4. > 0, where β

CHAPTER 4 SOLUTIONS TO PROBLEMS 4. (i) and (iii) generally cause the t statistics not to have a t distribution under H. Homoskedasticity is one of the CLM assumptions. An important omitted variable violates

CHAPTER 4 SOLUTIONS TO PROBLEMS 4. (i) and (iii) generally cause the t statistics not to have a t distribution under H. Homoskedasticity is one of the CLM assumptions. An important omitted variable violates

Multiple Regression Analysis

Multiple Regression Analysis y = β 0 + β 1 x 1 + β 2 x 2 +... β k x k + u 2. Inference 0 Assumptions of the Classical Linear Model (CLM)! So far, we know: 1. The mean and variance of the OLS estimators

Multiple Regression Analysis y = β 0 + β 1 x 1 + β 2 x 2 +... β k x k + u 2. Inference 0 Assumptions of the Classical Linear Model (CLM)! So far, we know: 1. The mean and variance of the OLS estimators

Problem 4.1. Problem 4.3

BOSTON COLLEGE Department of Economics EC 228 01 Econometric Methods Fall 2008, Prof. Baum, Ms. Phillips (tutor), Mr. Dmitriev (grader) Problem Set 3 Due at classtime, Thursday 14 Oct 2008 Problem 4.1

BOSTON COLLEGE Department of Economics EC 228 01 Econometric Methods Fall 2008, Prof. Baum, Ms. Phillips (tutor), Mr. Dmitriev (grader) Problem Set 3 Due at classtime, Thursday 14 Oct 2008 Problem 4.1

Multiple Regression: Inference

Multiple Regression: Inference The t-test: is ˆ j big and precise enough? We test the null hypothesis: H 0 : β j =0; i.e. test that x j has no effect on y once the other explanatory variables are controlled

Multiple Regression: Inference The t-test: is ˆ j big and precise enough? We test the null hypothesis: H 0 : β j =0; i.e. test that x j has no effect on y once the other explanatory variables are controlled

Inference in Regression Model

Inference in Regression Model Christopher Taber Department of Economics University of Wisconsin-Madison March 25, 2009 Outline 1 Final Step of Classical Linear Regression Model 2 Confidence Intervals 3

Inference in Regression Model Christopher Taber Department of Economics University of Wisconsin-Madison March 25, 2009 Outline 1 Final Step of Classical Linear Regression Model 2 Confidence Intervals 3

Solutions to Problem Set 5 (Due November 22) Maximum number of points for Problem set 5 is: 220. Problem 7.3

Maximum number of points for Problem set 5 is: 220. Problem 7.3") Solutions to Problem Set 5 (Due November 22) EC 228 02, Fall 2010 Prof. Baum, Ms Hristakeva Maximum number of points for Problem set 5 is: 220 Problem 7.3 (i) (5 points) The t statistic on hsize 2 is over

Solutions to Problem Set 5 (Due November 22) EC 228 02, Fall 2010 Prof. Baum, Ms Hristakeva Maximum number of points for Problem set 5 is: 220 Problem 7.3 (i) (5 points) The t statistic on hsize 2 is over

ECNS 561 Topics in Multiple Regression Analysis

ECNS 561 Topics in Multiple Regression Analysis Scaling Data For the simple regression case, we already discussed the effects of changing the units of measurement Nothing different here Coefficients, SEs,

ECNS 561 Topics in Multiple Regression Analysis Scaling Data For the simple regression case, we already discussed the effects of changing the units of measurement Nothing different here Coefficients, SEs,

2. (3.5) (iii) Simply drop one of the independent variables, say leisure: GP A = β 0 + β 1 study + β 2 sleep + β 3 work + u.

(iii) Simply drop one of the independent variables, say leisure: GP A = β 0 + β 1 study + β 2 sleep + β 3 work + u.") BOSTON COLLEGE Department of Economics EC 228 Econometrics, Prof. Baum, Ms. Yu, Fall 2003 Problem Set 3 Solutions Problem sets should be your own work. You may work together with classmates, but if you

BOSTON COLLEGE Department of Economics EC 228 Econometrics, Prof. Baum, Ms. Yu, Fall 2003 Problem Set 3 Solutions Problem sets should be your own work. You may work together with classmates, but if you

Problem C7.10. points = exper.072 exper guard forward (1.18) (.33) (.024) (1.00) (1.00)

(.33) (.024) (1.00) (1.00)") BOSTON COLLEGE Department of Economics EC 228 02 Econometric Methods Fall 2009, Prof. Baum, Ms. Phillips (TA), Ms. Pumphrey (grader) Problem Set 5 Due Tuesday 10 November 2009 Total Points Possible: 160

BOSTON COLLEGE Department of Economics EC 228 02 Econometric Methods Fall 2009, Prof. Baum, Ms. Phillips (TA), Ms. Pumphrey (grader) Problem Set 5 Due Tuesday 10 November 2009 Total Points Possible: 160

Econometrics I KS. Module 2: Multivariate Linear Regression. Alexander Ahammer. This version: April 16, 2018

Econometrics I KS Module 2: Multivariate Linear Regression Alexander Ahammer Department of Economics Johannes Kepler University of Linz This version: April 16, 2018 Alexander Ahammer (JKU) Module 2: Multivariate

Econometrics I KS Module 2: Multivariate Linear Regression Alexander Ahammer Department of Economics Johannes Kepler University of Linz This version: April 16, 2018 Alexander Ahammer (JKU) Module 2: Multivariate

Lecture Module 6. Agenda. Professor Spearot. 1 P-values. 2 Comparing Parameters. 3 Predictions. 4 F-Tests

Lecture Module 6 Professor Spearot Agenda 1 P-values 2 Comparing Parameters 3 Predictions 4 F-Tests Confidence intervals Housing prices and cancer risk Housing prices and cancer risk (Davis, 2004) Housing

Lecture Module 6 Professor Spearot Agenda 1 P-values 2 Comparing Parameters 3 Predictions 4 F-Tests Confidence intervals Housing prices and cancer risk Housing prices and cancer risk (Davis, 2004) Housing

Economics Introduction to Econometrics - Fall 2007 Final Exam - Answers

Student Name: Economics 4818 - Introduction to Econometrics - Fall 2007 Final Exam - Answers SHOW ALL WORK! Evaluation: Problems: 3, 4C, 5C and 5F are worth 4 points. All other questions are worth 3 points.

Student Name: Economics 4818 - Introduction to Econometrics - Fall 2007 Final Exam - Answers SHOW ALL WORK! Evaluation: Problems: 3, 4C, 5C and 5F are worth 4 points. All other questions are worth 3 points.

ECNS 561 Multiple Regression Analysis

ECNS 561 Multiple Regression Analysis Model with Two Independent Variables Consider the following model Crime i = β 0 + β 1 Educ i + β 2 [what else would we like to control for?] + ε i Here, we are taking

ECNS 561 Multiple Regression Analysis Model with Two Independent Variables Consider the following model Crime i = β 0 + β 1 Educ i + β 2 [what else would we like to control for?] + ε i Here, we are taking

CHAPTER 7. + ˆ δ. (1 nopc) + ˆ β1. =.157, so the new intercept is = The coefficient on nopc is.157.

+ ˆ β1. =.157, so the new intercept is = The coefficient on nopc is.157.") CHAPTER 7 SOLUTIONS TO PROBLEMS 7. (i) The coefficient on male is 87.75, so a man is estimated to sleep almost one and one-half hours more per week than a comparable woman. Further, t male = 87.75/34.33

CHAPTER 7 SOLUTIONS TO PROBLEMS 7. (i) The coefficient on male is 87.75, so a man is estimated to sleep almost one and one-half hours more per week than a comparable woman. Further, t male = 87.75/34.33

Statistical Inference. Part IV. Statistical Inference

Part IV Statistical Inference As of Oct 5, 2017 Sampling Distributions of the OLS Estimator 1 Statistical Inference Sampling Distributions of the OLS Estimator Testing Against One-Sided Alternatives Two-Sided

Part IV Statistical Inference As of Oct 5, 2017 Sampling Distributions of the OLS Estimator 1 Statistical Inference Sampling Distributions of the OLS Estimator Testing Against One-Sided Alternatives Two-Sided

Multiple Regression Analysis: Further Issues

Multiple Regression Analysis: Further Issues Ping Yu School of Economics and Finance The University of Hong Kong Ping Yu (HKU) MLR: Further Issues 1 / 36 Effects of Data Scaling on OLS Statistics Effects

Multiple Regression Analysis: Further Issues Ping Yu School of Economics and Finance The University of Hong Kong Ping Yu (HKU) MLR: Further Issues 1 / 36 Effects of Data Scaling on OLS Statistics Effects

coefficients n 2 are the residuals obtained when we estimate the regression on y equals the (simple regression) estimated effect of the part of x 1

estimated effect of the part of x 1") Review - Interpreting the Regression If we estimate: It can be shown that: where ˆ1 r i coefficients β ˆ+ βˆ x+ βˆ ˆ= 0 1 1 2x2 y ˆβ n n 2 1 = rˆ i1yi rˆ i1 i= 1 i= 1 xˆ are the residuals obtained when

Review - Interpreting the Regression If we estimate: It can be shown that: where ˆ1 r i coefficients β ˆ+ βˆ x+ βˆ ˆ= 0 1 1 2x2 y ˆβ n n 2 1 = rˆ i1yi rˆ i1 i= 1 i= 1 xˆ are the residuals obtained when

Multiple Regression Analysis: Heteroskedasticity

Multiple Regression Analysis: Heteroskedasticity y = β 0 + β 1 x 1 + β x +... β k x k + u Read chapter 8. EE45 -Chaiyuth Punyasavatsut 1 topics 8.1 Heteroskedasticity and OLS 8. Robust estimation 8.3 Testing

Multiple Regression Analysis: Heteroskedasticity y = β 0 + β 1 x 1 + β x +... β k x k + u Read chapter 8. EE45 -Chaiyuth Punyasavatsut 1 topics 8.1 Heteroskedasticity and OLS 8. Robust estimation 8.3 Testing

Introductory Econometrics Exercises for tutorials (Fall 2014)

") Introductory Econometrics Exercises for tutorials (Fall 2014) Dept. of Econometrics, Uni. of Economics, Prague, zouharj@vse.cz September 23, 2014 Tutorial 1: Review of basic statistical concepts Exercise

Introductory Econometrics Exercises for tutorials (Fall 2014) Dept. of Econometrics, Uni. of Economics, Prague, zouharj@vse.cz September 23, 2014 Tutorial 1: Review of basic statistical concepts Exercise

Model Specification and Data Problems. Part VIII

Part VIII Model Specification and Data Problems As of Oct 24, 2017 1 Model Specification and Data Problems RESET test Non-nested alternatives Outliers A functional form misspecification generally means

Part VIII Model Specification and Data Problems As of Oct 24, 2017 1 Model Specification and Data Problems RESET test Non-nested alternatives Outliers A functional form misspecification generally means

Chapter 3 Multiple Regression Complete Example

Department of Quantitative Methods & Information Systems ECON 504 Chapter 3 Multiple Regression Complete Example Spring 2013 Dr. Mohammad Zainal Review Goals After completing this lecture, you should be

Department of Quantitative Methods & Information Systems ECON 504 Chapter 3 Multiple Regression Complete Example Spring 2013 Dr. Mohammad Zainal Review Goals After completing this lecture, you should be

Multiple Linear Regression CIVL 7012/8012

Multiple Linear Regression CIVL 7012/8012 2 Multiple Regression Analysis (MLR) Allows us to explicitly control for many factors those simultaneously affect the dependent variable This is important for

Multiple Linear Regression CIVL 7012/8012 2 Multiple Regression Analysis (MLR) Allows us to explicitly control for many factors those simultaneously affect the dependent variable This is important for

ECO375 Tutorial 4 Wooldridge: Chapter 6 and 7

ECO375 Tutorial 4 Wooldridge: Chapter 6 and 7 Matt Tudball University of Toronto St. George October 6, 2017 Matt Tudball (University of Toronto) ECO375H1 October 6, 2017 1 / 36 ECO375 Tutorial 4 Welcome

ECO375 Tutorial 4 Wooldridge: Chapter 6 and 7 Matt Tudball University of Toronto St. George October 6, 2017 Matt Tudball (University of Toronto) ECO375H1 October 6, 2017 1 / 36 ECO375 Tutorial 4 Welcome

Introduction to Econometrics. Heteroskedasticity

Introduction to Econometrics Introduction Heteroskedasticity When the variance of the errors changes across segments of the population, where the segments are determined by different values for the explanatory

Introduction to Econometrics Introduction Heteroskedasticity When the variance of the errors changes across segments of the population, where the segments are determined by different values for the explanatory

Multiple Regression. Midterm results: AVG = 26.5 (88%) A = 27+ B = C =

A = 27+ B = C =") Economics 130 Lecture 6 Midterm Review Next Steps for the Class Multiple Regression Review & Issues Model Specification Issues Launching the Projects!!!!! Midterm results: AVG = 26.5 (88%) A = 27+ B =

Economics 130 Lecture 6 Midterm Review Next Steps for the Class Multiple Regression Review & Issues Model Specification Issues Launching the Projects!!!!! Midterm results: AVG = 26.5 (88%) A = 27+ B =

x i = 1 yi 2 = 55 with N = 30. Use the above sample information to answer all the following questions. Show explicitly all formulas and calculations.

Exercises for the course of Econometrics Introduction 1. () A researcher is using data for a sample of 30 observations to investigate the relationship between some dependent variable y i and independent

Exercises for the course of Econometrics Introduction 1. () A researcher is using data for a sample of 30 observations to investigate the relationship between some dependent variable y i and independent

Multiple Regression Analysis: Inference ECONOMETRICS (ECON 360) BEN VAN KAMMEN, PHD

BEN VAN KAMMEN, PHD") Multiple Regression Analysis: Inference ECONOMETRICS (ECON 360) BEN VAN KAMMEN, PHD Introduction When you perform statistical inference, you are primarily doing one of two things: Estimating the boundaries

Multiple Regression Analysis: Inference ECONOMETRICS (ECON 360) BEN VAN KAMMEN, PHD Introduction When you perform statistical inference, you are primarily doing one of two things: Estimating the boundaries

ECO220Y Simple Regression: Testing the Slope

ECO220Y Simple Regression: Testing the Slope Readings: Chapter 18 (Sections 18.3-18.5) Winter 2012 Lecture 19 (Winter 2012) Simple Regression Lecture 19 1 / 32 Simple Regression Model y i = β 0 + β 1 x

ECO220Y Simple Regression: Testing the Slope Readings: Chapter 18 (Sections 18.3-18.5) Winter 2012 Lecture 19 (Winter 2012) Simple Regression Lecture 19 1 / 32 Simple Regression Model y i = β 0 + β 1 x

Section 3: Simple Linear Regression

Section 3: Simple Linear Regression Carlos M. Carvalho The University of Texas at Austin McCombs School of Business http://faculty.mccombs.utexas.edu/carlos.carvalho/teaching/ 1 Regression: General Introduction

Section 3: Simple Linear Regression Carlos M. Carvalho The University of Texas at Austin McCombs School of Business http://faculty.mccombs.utexas.edu/carlos.carvalho/teaching/ 1 Regression: General Introduction

Multiple Regression Analysis. Part III. Multiple Regression Analysis

Part III Multiple Regression Analysis As of Sep 26, 2017 1 Multiple Regression Analysis Estimation Matrix form Goodness-of-Fit R-square Adjusted R-square Expected values of the OLS estimators Irrelevant

Part III Multiple Regression Analysis As of Sep 26, 2017 1 Multiple Regression Analysis Estimation Matrix form Goodness-of-Fit R-square Adjusted R-square Expected values of the OLS estimators Irrelevant

Econometrics Homework 1

Econometrics Homework Due Date: March, 24. by This problem set includes questions for Lecture -4 covered before midterm exam. Question Let z be a random column vector of size 3 : z = @ (a) Write out z

Econometrics Homework Due Date: March, 24. by This problem set includes questions for Lecture -4 covered before midterm exam. Question Let z be a random column vector of size 3 : z = @ (a) Write out z

Answer Key: Problem Set 6

: Problem Set 6 1. Consider a linear model to explain monthly beer consumption: beer = + inc + price + educ + female + u 0 1 3 4 E ( u inc, price, educ, female ) = 0 ( u inc price educ female) σ inc var,,,

: Problem Set 6 1. Consider a linear model to explain monthly beer consumption: beer = + inc + price + educ + female + u 0 1 3 4 E ( u inc, price, educ, female ) = 0 ( u inc price educ female) σ inc var,,,

Problem 13.5 (10 points)

") BOSTON COLLEGE Department of Economics EC 327 Financial Econometrics Spring 2013, Prof. Baum, Mr. Park Problem Set 2 Due Monday 25 February 2013 Total Points Possible: 210 points Problem 13.5 (10 points)

BOSTON COLLEGE Department of Economics EC 327 Financial Econometrics Spring 2013, Prof. Baum, Mr. Park Problem Set 2 Due Monday 25 February 2013 Total Points Possible: 210 points Problem 13.5 (10 points)

Wooldridge, Introductory Econometrics, 4th ed. Chapter 6: Multiple regression analysis: Further issues

Wooldridge, Introductory Econometrics, 4th ed. Chapter 6: Multiple regression analysis: Further issues What effects will the scale of the X and y variables have upon multiple regression? The coefficients

Wooldridge, Introductory Econometrics, 4th ed. Chapter 6: Multiple regression analysis: Further issues What effects will the scale of the X and y variables have upon multiple regression? The coefficients

Hypothesis testing Goodness of fit Multicollinearity Prediction. Applied Statistics. Lecturer: Serena Arima

Applied Statistics Lecturer: Serena Arima Hypothesis testing for the linear model Under the Gauss-Markov assumptions and the normality of the error terms, we saw that β N(β, σ 2 (X X ) 1 ) and hence s

Applied Statistics Lecturer: Serena Arima Hypothesis testing for the linear model Under the Gauss-Markov assumptions and the normality of the error terms, we saw that β N(β, σ 2 (X X ) 1 ) and hence s

Statistical Inference with Regression Analysis

Introductory Applied Econometrics EEP/IAS 118 Spring 2015 Steven Buck Lecture #13 Statistical Inference with Regression Analysis Next we turn to calculating confidence intervals and hypothesis testing

Introductory Applied Econometrics EEP/IAS 118 Spring 2015 Steven Buck Lecture #13 Statistical Inference with Regression Analysis Next we turn to calculating confidence intervals and hypothesis testing

1. The shoe size of five randomly selected men in the class is 7, 7.5, 6, 6.5 the shoe size of 4 randomly selected women is 6, 5.

Economics 3 Introduction to Econometrics Winter 2004 Professor Dobkin Name Final Exam (Sample) You must answer all the questions. The exam is closed book and closed notes you may use calculators. You must

Economics 3 Introduction to Econometrics Winter 2004 Professor Dobkin Name Final Exam (Sample) You must answer all the questions. The exam is closed book and closed notes you may use calculators. You must

Ch 13 & 14 - Regression Analysis

Ch 3 & 4 - Regression Analysis Simple Regression Model I. Multiple Choice:. A simple regression is a regression model that contains a. only one independent variable b. only one dependent variable c. more

Ch 3 & 4 - Regression Analysis Simple Regression Model I. Multiple Choice:. A simple regression is a regression model that contains a. only one independent variable b. only one dependent variable c. more

LECTURE 6. Introduction to Econometrics. Hypothesis testing & Goodness of fit

LECTURE 6 Introduction to Econometrics Hypothesis testing & Goodness of fit October 25, 2016 1 / 23 ON TODAY S LECTURE We will explain how multiple hypotheses are tested in a regression model We will define

LECTURE 6 Introduction to Econometrics Hypothesis testing & Goodness of fit October 25, 2016 1 / 23 ON TODAY S LECTURE We will explain how multiple hypotheses are tested in a regression model We will define

ECON2228 Notes 2. Christopher F Baum. Boston College Economics. cfb (BC Econ) ECON2228 Notes / 47

ECON2228 Notes / 47") ECON2228 Notes 2 Christopher F Baum Boston College Economics 2014 2015 cfb (BC Econ) ECON2228 Notes 2 2014 2015 1 / 47 Chapter 2: The simple regression model Most of this course will be concerned with

ECON2228 Notes 2 Christopher F Baum Boston College Economics 2014 2015 cfb (BC Econ) ECON2228 Notes 2 2014 2015 1 / 47 Chapter 2: The simple regression model Most of this course will be concerned with

Homoskedasticity. Var (u X) = σ 2. (23)

= σ 2. (23)") Homoskedasticity How big is the difference between the OLS estimator and the true parameter? To answer this question, we make an additional assumption called homoskedasticity: Var (u X) = σ 2. (23) This

Homoskedasticity How big is the difference between the OLS estimator and the true parameter? To answer this question, we make an additional assumption called homoskedasticity: Var (u X) = σ 2. (23) This

Applied Quantitative Methods II

Applied Quantitative Methods II Lecture 4: OLS and Statistics revision Klára Kaĺıšková Klára Kaĺıšková AQM II - Lecture 4 VŠE, SS 2016/17 1 / 68 Outline 1 Econometric analysis Properties of an estimator

Applied Quantitative Methods II Lecture 4: OLS and Statistics revision Klára Kaĺıšková Klára Kaĺıšková AQM II - Lecture 4 VŠE, SS 2016/17 1 / 68 Outline 1 Econometric analysis Properties of an estimator

Applied Econometrics (QEM)

") Applied Econometrics (QEM) based on Prinicples of Econometrics Jakub Mućk Department of Quantitative Economics Jakub Mućk Applied Econometrics (QEM) Meeting #3 1 / 42 Outline 1 2 3 t-test P-value Linear

Applied Econometrics (QEM) based on Prinicples of Econometrics Jakub Mućk Department of Quantitative Economics Jakub Mućk Applied Econometrics (QEM) Meeting #3 1 / 42 Outline 1 2 3 t-test P-value Linear

Business Statistics. Lecture 10: Correlation and Linear Regression

Business Statistics Lecture 10: Correlation and Linear Regression Scatterplot A scatterplot shows the relationship between two quantitative variables measured on the same individuals. It displays the Form

Business Statistics Lecture 10: Correlation and Linear Regression Scatterplot A scatterplot shows the relationship between two quantitative variables measured on the same individuals. It displays the Form

Regression Models. Chapter 4. Introduction. Introduction. Introduction

Chapter 4 Regression Models Quantitative Analysis for Management, Tenth Edition, by Render, Stair, and Hanna 008 Prentice-Hall, Inc. Introduction Regression analysis is a very valuable tool for a manager

Chapter 4 Regression Models Quantitative Analysis for Management, Tenth Edition, by Render, Stair, and Hanna 008 Prentice-Hall, Inc. Introduction Regression analysis is a very valuable tool for a manager

Table of z values and probabilities for the standard normal distribution. z is the first column plus the top row. Each cell shows P(X z).

.") Table of z values and probabilities for the standard normal distribution. z is the first column plus the top row. Each cell shows P(X z). For example P(X.04) =.8508. For z < 0 subtract the value from,

Table of z values and probabilities for the standard normal distribution. z is the first column plus the top row. Each cell shows P(X z). For example P(X.04) =.8508. For z < 0 subtract the value from,

Wooldridge, Introductory Econometrics, 4th ed. Chapter 2: The simple regression model

Wooldridge, Introductory Econometrics, 4th ed. Chapter 2: The simple regression model Most of this course will be concerned with use of a regression model: a structure in which one or more explanatory

Wooldridge, Introductory Econometrics, 4th ed. Chapter 2: The simple regression model Most of this course will be concerned with use of a regression model: a structure in which one or more explanatory

7. Prediction. Outline: Read Section 6.4. Mean Prediction

Outline: Read Section 6.4 II. Individual Prediction IV. Choose between y Model and log(y) Model 7. Prediction Read Wooldridge (2013), Chapter 6.4 2 Mean Prediction Predictions are useful But they are subject

Outline: Read Section 6.4 II. Individual Prediction IV. Choose between y Model and log(y) Model 7. Prediction Read Wooldridge (2013), Chapter 6.4 2 Mean Prediction Predictions are useful But they are subject

Mathematics for Economics MA course

Mathematics for Economics MA course Simple Linear Regression Dr. Seetha Bandara Simple Regression Simple linear regression is a statistical method that allows us to summarize and study relationships between

Mathematics for Economics MA course Simple Linear Regression Dr. Seetha Bandara Simple Regression Simple linear regression is a statistical method that allows us to summarize and study relationships between

In Chapter 2, we learned how to use simple regression analysis to explain a dependent

3 Multiple Regression Analysis: Estimation In Chapter 2, we learned how to use simple regression analysis to explain a dependent variable, y, as a function of a single independent variable, x. The primary

3 Multiple Regression Analysis: Estimation In Chapter 2, we learned how to use simple regression analysis to explain a dependent variable, y, as a function of a single independent variable, x. The primary

1 Motivation for Instrumental Variable (IV) Regression

Regression") ECON 370: IV & 2SLS 1 Instrumental Variables Estimation and Two Stage Least Squares Econometric Methods, ECON 370 Let s get back to the thiking in terms of cross sectional (or pooled cross sectional) data

ECON 370: IV & 2SLS 1 Instrumental Variables Estimation and Two Stage Least Squares Econometric Methods, ECON 370 Let s get back to the thiking in terms of cross sectional (or pooled cross sectional) data

Lecture 4: Multivariate Regression, Part 2

Lecture 4: Multivariate Regression, Part 2 Gauss-Markov Assumptions 1) Linear in Parameters: Y X X X i 0 1 1 2 2 k k 2) Random Sampling: we have a random sample from the population that follows the above

Lecture 4: Multivariate Regression, Part 2 Gauss-Markov Assumptions 1) Linear in Parameters: Y X X X i 0 1 1 2 2 k k 2) Random Sampling: we have a random sample from the population that follows the above

5. Let W follow a normal distribution with mean of μ and the variance of 1. Then, the pdf of W is

Practice Final Exam Last Name:, First Name:. Please write LEGIBLY. Answer all questions on this exam in the space provided (you may use the back of any page if you need more space). Show all work but do

Practice Final Exam Last Name:, First Name:. Please write LEGIBLY. Answer all questions on this exam in the space provided (you may use the back of any page if you need more space). Show all work but do

In Chapter 2, we learned how to use simple regression analysis to explain a dependent

C h a p t e r Three Multiple Regression Analysis: Estimation In Chapter 2, we learned how to use simple regression analysis to explain a dependent variable, y, as a function of a single independent variable,

C h a p t e r Three Multiple Regression Analysis: Estimation In Chapter 2, we learned how to use simple regression analysis to explain a dependent variable, y, as a function of a single independent variable,

Statistics II. Management Degree Management Statistics IIDegree. Statistics II. 2 nd Sem. 2013/2014. Management Degree. Simple Linear Regression

Model 1 2 Ordinary Least Squares 3 4 Non-linearities 5 of the coefficients and their to the model We saw that econometrics studies E (Y x). More generally, we shall study regression analysis. : The regression

Model 1 2 Ordinary Least Squares 3 4 Non-linearities 5 of the coefficients and their to the model We saw that econometrics studies E (Y x). More generally, we shall study regression analysis. : The regression

MS&E 226: Small Data

MS&E 226: Small Data Lecture 15: Examples of hypothesis tests (v5) Ramesh Johari ramesh.johari@stanford.edu 1 / 32 The recipe 2 / 32 The hypothesis testing recipe In this lecture we repeatedly apply the

MS&E 226: Small Data Lecture 15: Examples of hypothesis tests (v5) Ramesh Johari ramesh.johari@stanford.edu 1 / 32 The recipe 2 / 32 The hypothesis testing recipe In this lecture we repeatedly apply the

Regression Models - Introduction

Regression Models - Introduction In regression models there are two types of variables that are studied: A dependent variable, Y, also called response variable. It is modeled as random. An independent

Regression Models - Introduction In regression models there are two types of variables that are studied: A dependent variable, Y, also called response variable. It is modeled as random. An independent

Business Statistics. Lecture 10: Course Review

Business Statistics Lecture 10: Course Review 1 Descriptive Statistics for Continuous Data Numerical Summaries Location: mean, median Spread or variability: variance, standard deviation, range, percentiles,

Business Statistics Lecture 10: Course Review 1 Descriptive Statistics for Continuous Data Numerical Summaries Location: mean, median Spread or variability: variance, standard deviation, range, percentiles,

Economics 113. Simple Regression Assumptions. Simple Regression Derivation. Changing Units of Measurement. Nonlinear effects

Economics 113 Simple Regression Models Simple Regression Assumptions Simple Regression Derivation Changing Units of Measurement Nonlinear effects OLS and unbiased estimates Variance of the OLS estimates

Economics 113 Simple Regression Models Simple Regression Assumptions Simple Regression Derivation Changing Units of Measurement Nonlinear effects OLS and unbiased estimates Variance of the OLS estimates

Correlation Analysis

Simple Regression Correlation Analysis Correlation analysis is used to measure strength of the association (linear relationship) between two variables Correlation is only concerned with strength of the

Simple Regression Correlation Analysis Correlation analysis is used to measure strength of the association (linear relationship) between two variables Correlation is only concerned with strength of the

2) For a normal distribution, the skewness and kurtosis measures are as follows: A) 1.96 and 4 B) 1 and 2 C) 0 and 3 D) 0 and 0

For a normal distribution, the skewness and kurtosis measures are as follows: A) 1.96 and 4 B) 1 and 2 C) 0 and 3 D) 0 and 0") Introduction to Econometrics Midterm April 26, 2011 Name Student ID MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. (5,000 credit for each correct

Introduction to Econometrics Midterm April 26, 2011 Name Student ID MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. (5,000 credit for each correct

At this point, if you ve done everything correctly, you should have data that looks something like:

This homework is due on July 19 th. Economics 375: Introduction to Econometrics Homework #4 1. One tool to aid in understanding econometrics is the Monte Carlo experiment. A Monte Carlo experiment allows

This homework is due on July 19 th. Economics 375: Introduction to Econometrics Homework #4 1. One tool to aid in understanding econometrics is the Monte Carlo experiment. A Monte Carlo experiment allows

Multiple Regression Analysis

Chapter 4 Multiple Regression Analysis The simple linear regression covered in Chapter 2 can be generalized to include more than one variable. Multiple regression analysis is an extension of the simple

Chapter 4 Multiple Regression Analysis The simple linear regression covered in Chapter 2 can be generalized to include more than one variable. Multiple regression analysis is an extension of the simple

Regression Analysis. BUS 735: Business Decision Making and Research. Learn how to detect relationships between ordinal and categorical variables.

Regression Analysis BUS 735: Business Decision Making and Research 1 Goals of this section Specific goals Learn how to detect relationships between ordinal and categorical variables. Learn how to estimate

Regression Analysis BUS 735: Business Decision Making and Research 1 Goals of this section Specific goals Learn how to detect relationships between ordinal and categorical variables. Learn how to estimate

Basic Business Statistics 6 th Edition

Basic Business Statistics 6 th Edition Chapter 12 Simple Linear Regression Learning Objectives In this chapter, you learn: How to use regression analysis to predict the value of a dependent variable based

Basic Business Statistics 6 th Edition Chapter 12 Simple Linear Regression Learning Objectives In this chapter, you learn: How to use regression analysis to predict the value of a dependent variable based

Econometrics Review questions for exam

Econometrics Review questions for exam Nathaniel Higgins nhiggins@jhu.edu, 1. Suppose you have a model: y = β 0 x 1 + u You propose the model above and then estimate the model using OLS to obtain: ŷ =

Econometrics Review questions for exam Nathaniel Higgins nhiggins@jhu.edu, 1. Suppose you have a model: y = β 0 x 1 + u You propose the model above and then estimate the model using OLS to obtain: ŷ =

Heteroskedasticity (Section )

") Heteroskedasticity (Section 8.1-8.4) Ping Yu School of Economics and Finance The University of Hong Kong Ping Yu (HKU) Heteroskedasticity 1 / 44 Consequences of Heteroskedasticity for OLS Consequences

Heteroskedasticity (Section 8.1-8.4) Ping Yu School of Economics and Finance The University of Hong Kong Ping Yu (HKU) Heteroskedasticity 1 / 44 Consequences of Heteroskedasticity for OLS Consequences

Trendlines Simple Linear Regression Multiple Linear Regression Systematic Model Building Practical Issues

Trendlines Simple Linear Regression Multiple Linear Regression Systematic Model Building Practical Issues Overfitting Categorical Variables Interaction Terms Non-linear Terms Linear Logarithmic y = a +

Trendlines Simple Linear Regression Multiple Linear Regression Systematic Model Building Practical Issues Overfitting Categorical Variables Interaction Terms Non-linear Terms Linear Logarithmic y = a +

Simple Linear Regression: One Quantitative IV

Simple Linear Regression: One Quantitative IV Linear regression is frequently used to explain variation observed in a dependent variable (DV) with theoretically linked independent variables (IV). For example,

Simple Linear Regression: One Quantitative IV Linear regression is frequently used to explain variation observed in a dependent variable (DV) with theoretically linked independent variables (IV). For example,

Economics 326 Methods of Empirical Research in Economics. Lecture 14: Hypothesis testing in the multiple regression model, Part 2

Economics 326 Methods of Empirical Research in Economics Lecture 14: Hypothesis testing in the multiple regression model, Part 2 Vadim Marmer University of British Columbia May 5, 2010 Multiple restrictions

Economics 326 Methods of Empirical Research in Economics Lecture 14: Hypothesis testing in the multiple regression model, Part 2 Vadim Marmer University of British Columbia May 5, 2010 Multiple restrictions

Multiple Regression Analysis

Multiple Regression Analysis y = 0 + 1 x 1 + x +... k x k + u 6. Heteroskedasticity What is Heteroskedasticity?! Recall the assumption of homoskedasticity implied that conditional on the explanatory variables,

Multiple Regression Analysis y = 0 + 1 x 1 + x +... k x k + u 6. Heteroskedasticity What is Heteroskedasticity?! Recall the assumption of homoskedasticity implied that conditional on the explanatory variables,

Multiple Linear Regression

Multiple Linear Regression Asymptotics Asymptotics Multiple Linear Regression: Assumptions Assumption MLR. (Linearity in parameters) Assumption MLR. (Random Sampling from the population) We have a random

Multiple Linear Regression Asymptotics Asymptotics Multiple Linear Regression: Assumptions Assumption MLR. (Linearity in parameters) Assumption MLR. (Random Sampling from the population) We have a random

Lecture 5: Hypothesis testing with the classical linear model

Lecture 5: Hypothesis testing with the classical linear model Assumption MLR6: Normality MLR6 is not one of the Gauss-Markov assumptions. It s not necessary to assume the error is normally distributed

Lecture 5: Hypothesis testing with the classical linear model Assumption MLR6: Normality MLR6 is not one of the Gauss-Markov assumptions. It s not necessary to assume the error is normally distributed

Simple Regression Model. January 24, 2011

Simple Regression Model January 24, 2011 Outline Descriptive Analysis Causal Estimation Forecasting Regression Model We are actually going to derive the linear regression model in 3 very different ways

Simple Regression Model January 24, 2011 Outline Descriptive Analysis Causal Estimation Forecasting Regression Model We are actually going to derive the linear regression model in 3 very different ways

σ σ MLR Models: Estimation and Inference v.3 SLR.1: Linear Model MLR.1: Linear Model Those (S/M)LR Assumptions MLR3: No perfect collinearity

LR Assumptions MLR3: No perfect collinearity") Comparison of SLR and MLR analysis: What s New? Roadmap Multicollinearity and standard errors F Tests of linear restrictions F stats, adjusted R-squared, RMSE and t stats Playing with Bodyfat: F tests

Comparison of SLR and MLR analysis: What s New? Roadmap Multicollinearity and standard errors F Tests of linear restrictions F stats, adjusted R-squared, RMSE and t stats Playing with Bodyfat: F tests

1 A Non-technical Introduction to Regression

1 A Non-technical Introduction to Regression Chapters 1 and Chapter 2 of the textbook are reviews of material you should know from your previous study (e.g. in your second year course). They cover, in

1 A Non-technical Introduction to Regression Chapters 1 and Chapter 2 of the textbook are reviews of material you should know from your previous study (e.g. in your second year course). They cover, in

Chapter 16. Simple Linear Regression and Correlation

Chapter 16 Simple Linear Regression and Correlation 16.1 Regression Analysis Our problem objective is to analyze the relationship between interval variables; regression analysis is the first tool we will

Chapter 16 Simple Linear Regression and Correlation 16.1 Regression Analysis Our problem objective is to analyze the relationship between interval variables; regression analysis is the first tool we will

The Simple Linear Regression Model

The Simple Linear Regression Model Lesson 3 Ryan Safner 1 1 Department of Economics Hood College ECON 480 - Econometrics Fall 2017 Ryan Safner (Hood College) ECON 480 - Lesson 3 Fall 2017 1 / 77 Bivariate

The Simple Linear Regression Model Lesson 3 Ryan Safner 1 1 Department of Economics Hood College ECON 480 - Econometrics Fall 2017 Ryan Safner (Hood College) ECON 480 - Lesson 3 Fall 2017 1 / 77 Bivariate

Business Statistics. Lecture 9: Simple Regression

Business Statistics Lecture 9: Simple Regression 1 On to Model Building! Up to now, class was about descriptive and inferential statistics Numerical and graphical summaries of data Confidence intervals

Business Statistics Lecture 9: Simple Regression 1 On to Model Building! Up to now, class was about descriptive and inferential statistics Numerical and graphical summaries of data Confidence intervals

Homework Set 2, ECO 311, Fall 2014

Homework Set 2, ECO 311, Fall 2014 Due Date: At the beginning of class on October 21, 2014 Instruction: There are twelve questions. Each question is worth 2 points. You need to submit the answers of only

Homework Set 2, ECO 311, Fall 2014 Due Date: At the beginning of class on October 21, 2014 Instruction: There are twelve questions. Each question is worth 2 points. You need to submit the answers of only

Chapter 7 Student Lecture Notes 7-1

Chapter 7 Student Lecture Notes 7- Chapter Goals QM353: Business Statistics Chapter 7 Multiple Regression Analysis and Model Building After completing this chapter, you should be able to: Explain model

Chapter 7 Student Lecture Notes 7- Chapter Goals QM353: Business Statistics Chapter 7 Multiple Regression Analysis and Model Building After completing this chapter, you should be able to: Explain model

Homework 1 Solutions

Homework 1 Solutions January 18, 2012 Contents 1 Normal Probability Calculations 2 2 Stereo System (SLR) 2 3 Match Histograms 3 4 Match Scatter Plots 4 5 Housing (SLR) 4 6 Shock Absorber (SLR) 5 7 Participation

Homework 1 Solutions January 18, 2012 Contents 1 Normal Probability Calculations 2 2 Stereo System (SLR) 2 3 Match Histograms 3 4 Match Scatter Plots 4 5 Housing (SLR) 4 6 Shock Absorber (SLR) 5 7 Participation

Wednesday, October 17 Handout: Hypothesis Testing and the Wald Test

Amherst College Department of Economics Economics 360 Fall 2012 Wednesday, October 17 Handout: Hypothesis Testing and the Wald Test Preview No Money Illusion Theory: Calculating True] o Clever Algebraic

Amherst College Department of Economics Economics 360 Fall 2012 Wednesday, October 17 Handout: Hypothesis Testing and the Wald Test Preview No Money Illusion Theory: Calculating True] o Clever Algebraic

Econometrics. Week 8. Fall Institute of Economic Studies Faculty of Social Sciences Charles University in Prague

Econometrics Week 8 Institute of Economic Studies Faculty of Social Sciences Charles University in Prague Fall 2012 1 / 25 Recommended Reading For the today Instrumental Variables Estimation and Two Stage

Econometrics Week 8 Institute of Economic Studies Faculty of Social Sciences Charles University in Prague Fall 2012 1 / 25 Recommended Reading For the today Instrumental Variables Estimation and Two Stage

An overview of applied econometrics

An overview of applied econometrics Jo Thori Lind September 4, 2011 1 Introduction This note is intended as a brief overview of what is necessary to read and understand journal articles with empirical

An overview of applied econometrics Jo Thori Lind September 4, 2011 1 Introduction This note is intended as a brief overview of what is necessary to read and understand journal articles with empirical

Lectures 5 & 6: Hypothesis Testing

Lectures 5 & 6: Hypothesis Testing in which you learn to apply the concept of statistical significance to OLS estimates, learn the concept of t values, how to use them in regression work and come across

Lectures 5 & 6: Hypothesis Testing in which you learn to apply the concept of statistical significance to OLS estimates, learn the concept of t values, how to use them in regression work and come across

The general linear regression with k explanatory variables is just an extension of the simple regression as follows

3. Multiple Regression Analysis The general linear regression with k explanatory variables is just an extension of the simple regression as follows (1) y i = β 0 + β 1 x i1 + + β k x ik + u i. Because

3. Multiple Regression Analysis The general linear regression with k explanatory variables is just an extension of the simple regression as follows (1) y i = β 0 + β 1 x i1 + + β k x ik + u i. Because

Intermediate Econometrics

Intermediate Econometrics Markus Haas LMU München Summer term 2011 15. Mai 2011 The Simple Linear Regression Model Considering variables x and y in a specific population (e.g., years of education and wage

Intermediate Econometrics Markus Haas LMU München Summer term 2011 15. Mai 2011 The Simple Linear Regression Model Considering variables x and y in a specific population (e.g., years of education and wage

Ch 7: Dummy (binary, indicator) variables

variables") Ch 7: Dummy (binary, indicator) variables :Examples Dummy variable are used to indicate the presence or absence of a characteristic. For example, define female i 1 if obs i is female 0 otherwise or male

Ch 7: Dummy (binary, indicator) variables :Examples Dummy variable are used to indicate the presence or absence of a characteristic. For example, define female i 1 if obs i is female 0 otherwise or male

Outline. 2. Logarithmic Functional Form and Units of Measurement. Functional Form. I. Functional Form: log II. Units of Measurement

Outline 2. Logarithmic Functional Form and Units of Measurement I. Functional Form: log II. Units of Measurement Read Wooldridge (2013), Chapter 2.4, 6.1 and 6.2 2 Functional Form I. Functional Form: log

Outline 2. Logarithmic Functional Form and Units of Measurement I. Functional Form: log II. Units of Measurement Read Wooldridge (2013), Chapter 2.4, 6.1 and 6.2 2 Functional Form I. Functional Form: log

Lecture 4: Multivariate Regression, Part 2

Lecture 4: Multivariate Regression, Part 2 Gauss-Markov Assumptions 1) Linear in Parameters: Y X X X i 0 1 1 2 2 k k 2) Random Sampling: we have a random sample from the population that follows the above

Lecture 4: Multivariate Regression, Part 2 Gauss-Markov Assumptions 1) Linear in Parameters: Y X X X i 0 1 1 2 2 k k 2) Random Sampling: we have a random sample from the population that follows the above

Chapter 9: The Regression Model with Qualitative Information: Binary Variables (Dummies)

") Chapter 9: The Regression Model with Qualitative Information: Binary Variables (Dummies) Statistics and Introduction to Econometrics M. Angeles Carnero Departamento de Fundamentos del Análisis Económico

Chapter 9: The Regression Model with Qualitative Information: Binary Variables (Dummies) Statistics and Introduction to Econometrics M. Angeles Carnero Departamento de Fundamentos del Análisis Económico

Psychology 282 Lecture #4 Outline Inferences in SLR

Psychology 282 Lecture #4 Outline Inferences in SLR Assumptions To this point we have not had to make any distributional assumptions. Principle of least squares requires no assumptions. Can use correlations

Psychology 282 Lecture #4 Outline Inferences in SLR Assumptions To this point we have not had to make any distributional assumptions. Principle of least squares requires no assumptions. Can use correlations

Eco 391, J. Sandford, spring 2013 April 5, Midterm 3 4/5/2013

Midterm 3 4/5/2013 Instructions: You may use a calculator, and one sheet of notes. You will never be penalized for showing work, but if what is asked for can be computed directly, points awarded will depend

Midterm 3 4/5/2013 Instructions: You may use a calculator, and one sheet of notes. You will never be penalized for showing work, but if what is asked for can be computed directly, points awarded will depend

Regression #8: Loose Ends

Regression #8: Loose Ends Econ 671 Purdue University Justin L. Tobias (Purdue) Regression #8 1 / 30 In this lecture we investigate a variety of topics that you are probably familiar with, but need to touch

Regression #8: Loose Ends Econ 671 Purdue University Justin L. Tobias (Purdue) Regression #8 1 / 30 In this lecture we investigate a variety of topics that you are probably familiar with, but need to touch

Regression with a Single Regressor: Hypothesis Tests and Confidence Intervals

Regression with a Single Regressor: Hypothesis Tests and Confidence Intervals (SW Chapter 5) Outline. The standard error of ˆ. Hypothesis tests concerning β 3. Confidence intervals for β 4. Regression

Regression with a Single Regressor: Hypothesis Tests and Confidence Intervals (SW Chapter 5) Outline. The standard error of ˆ. Hypothesis tests concerning β 3. Confidence intervals for β 4. Regression

THE MULTIVARIATE LINEAR REGRESSION MODEL

THE MULTIVARIATE LINEAR REGRESSION MODEL Why multiple regression analysis? Model with more than 1 independent variable: y 0 1x1 2x2 u It allows : -Controlling for other factors, and get a ceteris paribus

THE MULTIVARIATE LINEAR REGRESSION MODEL Why multiple regression analysis? Model with more than 1 independent variable: y 0 1x1 2x2 u It allows : -Controlling for other factors, and get a ceteris paribus

Introduction to Econometrics Chapter 4

Introduction to Econometrics Chapter 4 Ezequiel Uriel Jiménez University of Valencia Valencia, September 2013 4 ypothesis testing in the multiple regression 4.1 ypothesis testing: an overview 4.2 Testing

Introduction to Econometrics Chapter 4 Ezequiel Uriel Jiménez University of Valencia Valencia, September 2013 4 ypothesis testing in the multiple regression 4.1 ypothesis testing: an overview 4.2 Testing

M(t) = 1 t. (1 t), 6 M (0) = 20 P (95. X i 110) i=1

= 1 t. (1 t), 6 M (0) = 20 P (95. X i 110) i=1") Math 66/566 - Midterm Solutions NOTE: These solutions are for both the 66 and 566 exam. The problems are the same until questions and 5. 1. The moment generating function of a random variable X is M(t)

Math 66/566 - Midterm Solutions NOTE: These solutions are for both the 66 and 566 exam. The problems are the same until questions and 5. 1. The moment generating function of a random variable X is M(t)