Simulating Exchangeable Multivariate Archimedean Copulas and its Applications. Authors: Florence Wu Emiliano A. Valdez Michael Sherris

|

|

|

- Darlene Sutton

- 5 years ago

- Views:

Transcription

1 Simulating Exchangeable Multivariate Archimedean Copulas and its Applications Authors: Florence Wu Emiliano A. Valdez Michael Sherris

Sampling from Archimedean Copulas Embrechts, P., Lindskog, and A.")

2 Literatures Frees and Valdez (1999) Understanding Relationships Using Copulas Whelan, N. (2004) Sampling from Archimedean Copulas Embrechts, P., Lindskog, and A. McNeil (2001) Modelling Dependence with Copulas and Applications to Risk Management

to multi-dimensional copulas Presenting an algorithm for generating Exchangeable Multivariate Archimedean Copulas")

3 This paper: Extending Theorem in Nelson (1999) to multi-dimensional copulas Presenting an algorithm for generating Exchangeable Multivariate Archimedean Copulas based on the multi-dimensional version of theorem Demonstrating the application of the algorithm

Copula C is exchangeable if it is associative C(u,v,w) = C(C(u,v),w) = C(u, C(v,w)) for all")

4 Exchangeable Archimedean Copulas One parameter Archimedean copulas Archimedean copulas a well known and often used class characterised by a generator, φ(t) Copula C is exchangeable if it is associative C(u,v,w) = C(C(u,v),w) = C(u, C(v,w)) for all u,v,w in I.

5 Archimedean Copulas Charateristics of the generator φ(t): ϕ(1) = 0 is monotonically decreasing; and is convex (ϕ exists and ϕ 0). If ϕ exists, then ϕ 0 C(u 1,,u n ) = ϕ -1 (ϕ(u 1 ) + + ϕ(u n ))

= - log((e -θt 1)/(e -θ 1) ϕ -1 (t) = - log(1 (1 - e -θ )e -t )")

6 Archimedean Copulas - Examples Gumbel Copula ϕ(t) = (-log(u)) 1/θ ϕ -1 (t) = exp(-u θ ) Frank Copula ϕ(t) = - log((e -θt 1)/(e -θ 1) ϕ -1 (t) = - log(1 (1 - e -θ )e -t ) /log(θ)

7 Theorem Let (U 1,U 2 ) be a bivariate random vector with uniform marginals and joint distribution function defined by Archimedean copula C(u 1,u 2 ) = ϕ - 1 (ϕ(u 1 ) + ϕ(u 2 )) for some generator ϕ. Define the random variables S = ϕ(u 1 )/(ϕ(u 1 ) + ϕ(u 2 )) and T = C(u 1,u 2 ). The joint distribution function of (S,T) is characterized by H(s,t) = P(S s, T t) = s K C (t) where K C (t) = t ϕ(t)/ ϕ (t).

8 Simulating Bivariate Copulas Algorithm for generating bivariate Archimedean copulas (refer Embrecht et al (2001): Simulate two independent U(0,1) random variables, s and w. Set t = K -1 C (w) where K C (t) = t ϕ(t)/ ϕ (t). Set u 1 = ϕ -1 (s ϕ(t)) and u 2 = ϕ -1 ((1-s) ϕ(t)). x 1 = F 1-1 (u 1 ) and x 2 = F 2-1 (u 2 ) if inverses exist. (F 1 and F 2 are the marginals).

9 Theorem for Multi-dimensional Archimedean Copulas (1) Let (U 1,,U n ) be an n-dimensional random vector with uniform marginals and joint distribution function defined by the Archimedean copula C(u 1,,u n ) = ϕ -1 (ϕ(u 1 ) + + ϕ(u n )) or some generator ϕ. Define the n tranformed random variables S 1,,S n-1 and T, where S k = (ϕ(u 1 ) + + ϕ(u k )) / (ϕ(u 1 ) + + ϕ(u k+1 )) T = C(u 1, u n ) = ϕ -1 (ϕ(u 1 ) + + ϕ(u n ))

10 Theorem for Multi-dimensional Archimedean Copulas (2) The joint density distribution for S 1,,S n-1 and T can be defined as follows. h(s 1,s 2,,s n,t) = J c(u 1, u n ) or h(s 1,s 2,,s n-1,t) = s 10 s 21 s 32. s n-2 n-1 ϕ -1(n) (t)[ϕ(t)] /ϕ (t) Hence S 1,,S n-1 and T are independent, and 1. S 1 and T are uniform; and 2. S 2,,S n-1 each have support in (0,1).

11 Theorem for Multi-dimensional Archimedean Copulas (3) Distribution functions for S k: Corollary: The density for S k for k = 1,2, n-1 is given by f Sk (s) = ks k-1, for s (0,1) The distribution functions for S k can be written as: F Sk (s) = s k, for s (0,1) Corollary: The marginal density for T is given by: f T (t) = ϕ -1(n) (t)[ϕ(t)] n-1 ϕ (t) for t (0,1)

12 Algorithm for simulating multidimensional Archimedean Copulas 1. Simulate n independent U(0,1) random variables, w 1, w n. 2. For k = 1,2,, n-1, set s k =w k 1/k 3. Set t = F T -1 (w n ) 4. Set u 1 = ϕ -1 (s 1 s n-1 ϕ(t)), u n = ϕ -1 ((1-s n-1 ) ϕ(t)) and for k = 2,,n, u k = ϕ -1 ((1-s k-1 )Πs j ϕ(t). 5. x k = F -1 k (u k ) for k = 1,,n.

u -(k+1)/ θ Ψ k-1 (u θ ) Ψ k (x) = [θ(x-1) + k] Ψ k-1 (x) - θ Ψ k-1 (x) Recursive with Ψ 0 (x) = 1.")

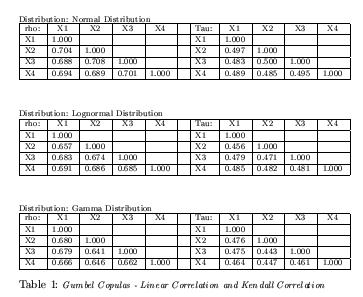

13 Example: Multivariate Gumbel Copula Gumbel Copulas ϕ(u) = (-log(u)) 1/θ ϕ -1 (u) = exp(-u θ ) ϕ -1(k) = (-1) k θexp(-u θ )u -(k+1)/ θ Ψ k-1 (u θ ) Ψ k (x) = [θ(x-1) + k] Ψ k-1 (x) - θ Ψ k-1 (x) Recursive with Ψ 0 (x) = 1.

14 Example: Gumbel Copula (Kendall Tau 0.5, Theta =2)

")

15 Example: Gumbel Copula (3) Normal vs Lognormal vs Gamma

16 Application: VaR and TailVaR (1) Insurance portfolio Contains multiple lines of business, with tail dependence Copulas Gumbel copula distributions have heavy right tails Frank copula lower tail dependence than Gumbel at the same level of dependence Economic Capital: VaR/TailVaR VaR: the k-th percentile of the total loss TailVaR: the conditional expectation of the total loss at a given level of VaR (or E(X X VaR))

17 Application: VaR and TailVaR (2) Density of Gumbel Copulas Density of Frank Copulas

18 Application: VaR and TailVaR (3) Assumptions: Lines of business: 4 Kendall s tau = 0.5 (linear correlation = 0.7) theta = 2 for Gumbel copula theta = 5.75 for Frank copula Mean and variance of marginals are the same

19 Application: VaR and TailVaR (4) Gumbel Frank

20 Application: VaR and TailVaR (5) Gumbel copula has higher TailVaR s than Frank copula for Lognormal and Gamma marginals Lognormal has the highest TailVaR and VaR at both 95% and 99% confidence level.

21 Application: VaR and TailVaR (6) Gumbel 1.4 Frank The Case of LogNormal Distribution The Case of LogNormal Distribution The Case of Gamma Distribution The Case of Gamma Distribution

22 Application: VaR and TailVaR (7) Impact of the choice of Kendall s correlation on VaR and TailVaR

23 Conclusion Derived an algorithm for simulating multidimensional Archimedean copula. Applied the algorithm to assess risk measures for marginals and copulas often used in insurance risk models. Copula and marginals have a significant effect on economic capital

Correlation & Dependency Structures

Correlation & Dependency Structures GIRO - October 1999 Andrzej Czernuszewicz Dimitris Papachristou Why are we interested in correlation/dependency? Risk management Portfolio management Reinsurance purchase

Correlation & Dependency Structures GIRO - October 1999 Andrzej Czernuszewicz Dimitris Papachristou Why are we interested in correlation/dependency? Risk management Portfolio management Reinsurance purchase

Modelling Dependent Credit Risks

Modelling Dependent Credit Risks Filip Lindskog, RiskLab, ETH Zürich 30 November 2000 Home page:http://www.math.ethz.ch/ lindskog E-mail:lindskog@math.ethz.ch RiskLab:http://www.risklab.ch Modelling Dependent

Modelling Dependent Credit Risks Filip Lindskog, RiskLab, ETH Zürich 30 November 2000 Home page:http://www.math.ethz.ch/ lindskog E-mail:lindskog@math.ethz.ch RiskLab:http://www.risklab.ch Modelling Dependent

Correlation: Copulas and Conditioning

Correlation: Copulas and Conditioning This note reviews two methods of simulating correlated variates: copula methods and conditional distributions, and the relationships between them. Particular emphasis

Correlation: Copulas and Conditioning This note reviews two methods of simulating correlated variates: copula methods and conditional distributions, and the relationships between them. Particular emphasis

Modelling Dependence with Copulas and Applications to Risk Management. Filip Lindskog, RiskLab, ETH Zürich

Modelling Dependence with Copulas and Applications to Risk Management Filip Lindskog, RiskLab, ETH Zürich 02-07-2000 Home page: http://www.math.ethz.ch/ lindskog E-mail: lindskog@math.ethz.ch RiskLab:

Modelling Dependence with Copulas and Applications to Risk Management Filip Lindskog, RiskLab, ETH Zürich 02-07-2000 Home page: http://www.math.ethz.ch/ lindskog E-mail: lindskog@math.ethz.ch RiskLab:

Modelling and Estimation of Stochastic Dependence

Modelling and Estimation of Stochastic Dependence Uwe Schmock Based on joint work with Dr. Barbara Dengler Financial and Actuarial Mathematics and Christian Doppler Laboratory for Portfolio Risk Management

Modelling and Estimation of Stochastic Dependence Uwe Schmock Based on joint work with Dr. Barbara Dengler Financial and Actuarial Mathematics and Christian Doppler Laboratory for Portfolio Risk Management

Tail Approximation of Value-at-Risk under Multivariate Regular Variation

Tail Approximation of Value-at-Risk under Multivariate Regular Variation Yannan Sun Haijun Li July 00 Abstract This paper presents a general tail approximation method for evaluating the Valueat-Risk of

Tail Approximation of Value-at-Risk under Multivariate Regular Variation Yannan Sun Haijun Li July 00 Abstract This paper presents a general tail approximation method for evaluating the Valueat-Risk of

Non parametric estimation of Archimedean copulas and tail dependence. Paris, february 19, 2015.

Non parametric estimation of Archimedean copulas and tail dependence Elena Di Bernardino a and Didier Rullière b Paris, february 19, 2015. a CNAM, Paris, Département IMATH, b ISFA, Université Lyon 1, Laboratoire

Non parametric estimation of Archimedean copulas and tail dependence Elena Di Bernardino a and Didier Rullière b Paris, february 19, 2015. a CNAM, Paris, Département IMATH, b ISFA, Université Lyon 1, Laboratoire

Copulas and Measures of Dependence

1 Copulas and Measures of Dependence Uttara Naik-Nimbalkar December 28, 2014 Measures for determining the relationship between two variables: the Pearson s correlation coefficient, Kendalls tau and Spearmans

1 Copulas and Measures of Dependence Uttara Naik-Nimbalkar December 28, 2014 Measures for determining the relationship between two variables: the Pearson s correlation coefficient, Kendalls tau and Spearmans

A Brief Introduction to Copulas

A Brief Introduction to Copulas Speaker: Hua, Lei February 24, 2009 Department of Statistics University of British Columbia Outline Introduction Definition Properties Archimedean Copulas Constructing Copulas

A Brief Introduction to Copulas Speaker: Hua, Lei February 24, 2009 Department of Statistics University of British Columbia Outline Introduction Definition Properties Archimedean Copulas Constructing Copulas

Efficient estimation of a semiparametric dynamic copula model

Efficient estimation of a semiparametric dynamic copula model Christian Hafner Olga Reznikova Institute of Statistics Université catholique de Louvain Louvain-la-Neuve, Blgium 30 January 2009 Young Researchers

Efficient estimation of a semiparametric dynamic copula model Christian Hafner Olga Reznikova Institute of Statistics Université catholique de Louvain Louvain-la-Neuve, Blgium 30 January 2009 Young Researchers

Trivariate copulas for characterisation of droughts

ANZIAM J. 49 (EMAC2007) pp.c306 C323, 2008 C306 Trivariate copulas for characterisation of droughts G. Wong 1 M. F. Lambert 2 A. V. Metcalfe 3 (Received 3 August 2007; revised 4 January 2008) Abstract

ANZIAM J. 49 (EMAC2007) pp.c306 C323, 2008 C306 Trivariate copulas for characterisation of droughts G. Wong 1 M. F. Lambert 2 A. V. Metcalfe 3 (Received 3 August 2007; revised 4 January 2008) Abstract

Lifetime Dependence Modelling using a Generalized Multivariate Pareto Distribution

Lifetime Dependence Modelling using a Generalized Multivariate Pareto Distribution Daniel Alai Zinoviy Landsman Centre of Excellence in Population Ageing Research (CEPAR) School of Mathematics, Statistics

Lifetime Dependence Modelling using a Generalized Multivariate Pareto Distribution Daniel Alai Zinoviy Landsman Centre of Excellence in Population Ageing Research (CEPAR) School of Mathematics, Statistics

Lecture Quantitative Finance Spring Term 2015

on bivariate Lecture Quantitative Finance Spring Term 2015 Prof. Dr. Erich Walter Farkas Lecture 07: April 2, 2015 1 / 54 Outline on bivariate 1 2 bivariate 3 Distribution 4 5 6 7 8 Comments and conclusions

on bivariate Lecture Quantitative Finance Spring Term 2015 Prof. Dr. Erich Walter Farkas Lecture 07: April 2, 2015 1 / 54 Outline on bivariate 1 2 bivariate 3 Distribution 4 5 6 7 8 Comments and conclusions

Explicit Bounds for the Distribution Function of the Sum of Dependent Normally Distributed Random Variables

Explicit Bounds for the Distribution Function of the Sum of Dependent Normally Distributed Random Variables Walter Schneider July 26, 20 Abstract In this paper an analytic expression is given for the bounds

Explicit Bounds for the Distribution Function of the Sum of Dependent Normally Distributed Random Variables Walter Schneider July 26, 20 Abstract In this paper an analytic expression is given for the bounds

Fitting Archimedean copulas to bivariate geodetic data

Fitting Archimedean copulas to bivariate geodetic data Tomáš Bacigál 1 and Magda Komorníková 2 1 Faculty of Civil Engineering, STU Bratislava bacigal@math.sk 2 Faculty of Civil Engineering, STU Bratislava

Fitting Archimedean copulas to bivariate geodetic data Tomáš Bacigál 1 and Magda Komorníková 2 1 Faculty of Civil Engineering, STU Bratislava bacigal@math.sk 2 Faculty of Civil Engineering, STU Bratislava

Tail Dependence of Multivariate Pareto Distributions

!#"%$ & ' ") * +!-,#. /10 243537698:6 ;=@?A BCDBFEHGIBJEHKLB MONQP RS?UTV=XW>YZ=eda gihjlknmcoqprj stmfovuxw yy z {} ~ ƒ }ˆŠ ~Œ~Ž f ˆ ` š œžÿ~ ~Ÿ œ } ƒ œ ˆŠ~ œ

!#"%$ & ' ") * +!-,#. /10 243537698:6 ;=@?A BCDBFEHGIBJEHKLB MONQP RS?UTV=XW>YZ=eda gihjlknmcoqprj stmfovuxw yy z {} ~ ƒ }ˆŠ ~Œ~Ž f ˆ ` š œžÿ~ ~Ÿ œ } ƒ œ ˆŠ~ œ

VaR vs. Expected Shortfall

VaR vs. Expected Shortfall Risk Measures under Solvency II Dietmar Pfeifer (2004) Risk measures and premium principles a comparison VaR vs. Expected Shortfall Dependence and its implications for risk measures

VaR vs. Expected Shortfall Risk Measures under Solvency II Dietmar Pfeifer (2004) Risk measures and premium principles a comparison VaR vs. Expected Shortfall Dependence and its implications for risk measures

Introduction to Dependence Modelling

Introduction to Dependence Modelling Carole Bernard Berlin, May 2015. 1 Outline Modeling Dependence Part 1: Introduction 1 General concepts on dependence. 2 in 2 or N 3 dimensions. 3 Minimizing the expectation

Introduction to Dependence Modelling Carole Bernard Berlin, May 2015. 1 Outline Modeling Dependence Part 1: Introduction 1 General concepts on dependence. 2 in 2 or N 3 dimensions. 3 Minimizing the expectation

On tail dependence coecients of transformed multivariate Archimedean copulas

Tails and for Archim Copula () February 2015, University of Lille 3 On tail dependence coecients of transformed multivariate Archimedean copulas Elena Di Bernardino, CNAM, Paris, Département IMATH Séminaire

Tails and for Archim Copula () February 2015, University of Lille 3 On tail dependence coecients of transformed multivariate Archimedean copulas Elena Di Bernardino, CNAM, Paris, Département IMATH Séminaire

Tools for sampling Multivariate Archimedean Copulas. Abstract

Mario R. Melchiori CPA Universidad Nacional del Litoral Santa Fe - Argentina March 26 Abstract A hurdle for practical implementation of any multivariate Archimedean copula was the absence of an efficient

Mario R. Melchiori CPA Universidad Nacional del Litoral Santa Fe - Argentina March 26 Abstract A hurdle for practical implementation of any multivariate Archimedean copula was the absence of an efficient

Dependence. Practitioner Course: Portfolio Optimization. John Dodson. September 10, Dependence. John Dodson. Outline.

Practitioner Course: Portfolio Optimization September 10, 2008 Before we define dependence, it is useful to define Random variables X and Y are independent iff For all x, y. In particular, F (X,Y ) (x,

Practitioner Course: Portfolio Optimization September 10, 2008 Before we define dependence, it is useful to define Random variables X and Y are independent iff For all x, y. In particular, F (X,Y ) (x,

Sampling Archimedean copulas. Marius Hofert. Ulm University

Marius Hofert marius.hofert@uni-ulm.de Ulm University 2007-12-08 Outline 1 Nonnested Archimedean copulas 1.1 Marshall and Olkin s algorithm 2 Nested Archimedean copulas 2.1 McNeil s algorithm 2.2 A general

Marius Hofert marius.hofert@uni-ulm.de Ulm University 2007-12-08 Outline 1 Nonnested Archimedean copulas 1.1 Marshall and Olkin s algorithm 2 Nested Archimedean copulas 2.1 McNeil s algorithm 2.2 A general

Models for construction of multivariate dependence

Dept. of Math. University of Oslo Statistical Research Report No. 3 ISSN 0806 3842 June 2007 Models for construction of multivariate dependence Daniel Berg University of Oslo and Norwegian Computing Center

Dept. of Math. University of Oslo Statistical Research Report No. 3 ISSN 0806 3842 June 2007 Models for construction of multivariate dependence Daniel Berg University of Oslo and Norwegian Computing Center

Robustness of a semiparametric estimator of a copula

Robustness of a semiparametric estimator of a copula Gunky Kim a, Mervyn J. Silvapulle b and Paramsothy Silvapulle c a Department of Econometrics and Business Statistics, Monash University, c Caulfield

Robustness of a semiparametric estimator of a copula Gunky Kim a, Mervyn J. Silvapulle b and Paramsothy Silvapulle c a Department of Econometrics and Business Statistics, Monash University, c Caulfield

Overview of Extreme Value Theory. Dr. Sawsan Hilal space

Overview of Extreme Value Theory Dr. Sawsan Hilal space Maths Department - University of Bahrain space November 2010 Outline Part-1: Univariate Extremes Motivation Threshold Exceedances Part-2: Bivariate

Overview of Extreme Value Theory Dr. Sawsan Hilal space Maths Department - University of Bahrain space November 2010 Outline Part-1: Univariate Extremes Motivation Threshold Exceedances Part-2: Bivariate

Risk Aggregation. Paul Embrechts. Department of Mathematics, ETH Zurich Senior SFI Professor.

Risk Aggregation Paul Embrechts Department of Mathematics, ETH Zurich Senior SFI Professor www.math.ethz.ch/~embrechts/ Joint work with P. Arbenz and G. Puccetti 1 / 33 The background Query by practitioner

Risk Aggregation Paul Embrechts Department of Mathematics, ETH Zurich Senior SFI Professor www.math.ethz.ch/~embrechts/ Joint work with P. Arbenz and G. Puccetti 1 / 33 The background Query by practitioner

Multivariate survival modelling: a unified approach with copulas

Multivariate survival modelling: a unified approach with copulas P. Georges, A-G. Lamy, E. Nicolas, G. Quibel & T. Roncalli Groupe de Recherche Opérationnelle Crédit Lyonnais France May 28, 2001 Abstract

Multivariate survival modelling: a unified approach with copulas P. Georges, A-G. Lamy, E. Nicolas, G. Quibel & T. Roncalli Groupe de Recherche Opérationnelle Crédit Lyonnais France May 28, 2001 Abstract

2 (U 2 ), (0.1) 1 + u θ. where θ > 0 on the right. You can easily convince yourself that (0.3) is valid for both.

, (0.1) 1 + u θ. where θ > 0 on the right. You can easily convince yourself that (0.3) is valid for both.") Introducing copulas Introduction Let U 1 and U 2 be uniform, dependent random variables and introduce X 1 = F 1 1 (U 1 ) and X 2 = F 1 2 (U 2 ), (.1) where F1 1 (u 1 ) and F2 1 (u 2 ) are the percentiles

Introducing copulas Introduction Let U 1 and U 2 be uniform, dependent random variables and introduce X 1 = F 1 1 (U 1 ) and X 2 = F 1 2 (U 2 ), (.1) where F1 1 (u 1 ) and F2 1 (u 2 ) are the percentiles

Copulas. Mathematisches Seminar (Prof. Dr. D. Filipovic) Di Uhr in E

Di Uhr in E") Copulas Mathematisches Seminar (Prof. Dr. D. Filipovic) Di. 14-16 Uhr in E41 A Short Introduction 1 0.8 0.6 0.4 0.2 0 0 0.2 0.4 0.6 0.8 1 The above picture shows a scatterplot (500 points) from a pair

Copulas Mathematisches Seminar (Prof. Dr. D. Filipovic) Di. 14-16 Uhr in E41 A Short Introduction 1 0.8 0.6 0.4 0.2 0 0 0.2 0.4 0.6 0.8 1 The above picture shows a scatterplot (500 points) from a pair

THIELE CENTRE for applied mathematics in natural science

THIELE CENTRE for applied mathematics in natural science Tail Asymptotics for the Sum of two Heavy-tailed Dependent Risks Hansjörg Albrecher and Søren Asmussen Research Report No. 9 August 25 Tail Asymptotics

THIELE CENTRE for applied mathematics in natural science Tail Asymptotics for the Sum of two Heavy-tailed Dependent Risks Hansjörg Albrecher and Søren Asmussen Research Report No. 9 August 25 Tail Asymptotics

Efficient rare-event simulation for sums of dependent random varia

Efficient rare-event simulation for sums of dependent random variables Leonardo Rojas-Nandayapa joint work with José Blanchet February 13, 2012 MCQMC UNSW, Sydney, Australia Contents Introduction 1 Introduction

Efficient rare-event simulation for sums of dependent random variables Leonardo Rojas-Nandayapa joint work with José Blanchet February 13, 2012 MCQMC UNSW, Sydney, Australia Contents Introduction 1 Introduction

Copulas and dependence measurement

Copulas and dependence measurement Thorsten Schmidt. Chemnitz University of Technology, Mathematical Institute, Reichenhainer Str. 41, Chemnitz. thorsten.schmidt@mathematik.tu-chemnitz.de Keywords: copulas,

Copulas and dependence measurement Thorsten Schmidt. Chemnitz University of Technology, Mathematical Institute, Reichenhainer Str. 41, Chemnitz. thorsten.schmidt@mathematik.tu-chemnitz.de Keywords: copulas,

On the Systemic Nature of Weather Risk

Martin Odening 1 Ostap Okhrin 2 Wei Xu 1 Department of Agricultural Economics 1 Ladislaus von Bortkiewicz Chair of Statistics C.A.S.E. Center for Applied Statistics and Economics 2 Humboldt Universität

Martin Odening 1 Ostap Okhrin 2 Wei Xu 1 Department of Agricultural Economics 1 Ladislaus von Bortkiewicz Chair of Statistics C.A.S.E. Center for Applied Statistics and Economics 2 Humboldt Universität

Contents 1. Coping with Copulas. Thorsten Schmidt 1. Department of Mathematics, University of Leipzig Dec 2006

Contents 1 Coping with Copulas Thorsten Schmidt 1 Department of Mathematics, University of Leipzig Dec 2006 Forthcoming in Risk Books Copulas - From Theory to Applications in Finance Contents 1 Introdcution

Contents 1 Coping with Copulas Thorsten Schmidt 1 Department of Mathematics, University of Leipzig Dec 2006 Forthcoming in Risk Books Copulas - From Theory to Applications in Finance Contents 1 Introdcution

Reducing Model Risk With Goodness-of-fit Victory Idowu London School of Economics

Reducing Model Risk With Goodness-of-fit Victory Idowu London School of Economics Agenda I. An overview of Copula Theory II. Copulas and Model Risk III. Goodness-of-fit methods for copulas IV. Presentation

Reducing Model Risk With Goodness-of-fit Victory Idowu London School of Economics Agenda I. An overview of Copula Theory II. Copulas and Model Risk III. Goodness-of-fit methods for copulas IV. Presentation

Copulas. MOU Lili. December, 2014

Copulas MOU Lili December, 2014 Outline Preliminary Introduction Formal Definition Copula Functions Estimating the Parameters Example Conclusion and Discussion Preliminary MOU Lili SEKE Team 3/30 Probability

Copulas MOU Lili December, 2014 Outline Preliminary Introduction Formal Definition Copula Functions Estimating the Parameters Example Conclusion and Discussion Preliminary MOU Lili SEKE Team 3/30 Probability

Financial Econometrics and Volatility Models Copulas

Financial Econometrics and Volatility Models Copulas Eric Zivot Updated: May 10, 2010 Reading MFTS, chapter 19 FMUND, chapters 6 and 7 Introduction Capturing co-movement between financial asset returns

Financial Econometrics and Volatility Models Copulas Eric Zivot Updated: May 10, 2010 Reading MFTS, chapter 19 FMUND, chapters 6 and 7 Introduction Capturing co-movement between financial asset returns

Estimation of multivariate critical layers: Applications to rainfall data

Elena Di Bernardino, ICRA 6 / RISK 2015 () Estimation of Multivariate critical layers Barcelona, May 26-29, 2015 Estimation of multivariate critical layers: Applications to rainfall data Elena Di Bernardino,

Elena Di Bernardino, ICRA 6 / RISK 2015 () Estimation of Multivariate critical layers Barcelona, May 26-29, 2015 Estimation of multivariate critical layers: Applications to rainfall data Elena Di Bernardino,

Non-parametric Estimation of Elliptical Copulae With Application to Credit Risk

Non-parametric Estimation of Elliptical Copulae With Application to Credit Risk Krassimir Kostadinov Abstract This paper develops a method for statistical estimation of the dependence structure of financial

Non-parametric Estimation of Elliptical Copulae With Application to Credit Risk Krassimir Kostadinov Abstract This paper develops a method for statistical estimation of the dependence structure of financial

Properties of Hierarchical Archimedean Copulas

SFB 649 Discussion Paper 9-4 Properties of Hierarchical Archimedean Copulas Ostap Okhrin* Yarema Okhrin** Wolfgang Schmid*** *Humboldt-Universität zu Berlin, Germany **Universität Bern, Switzerland ***Universität

SFB 649 Discussion Paper 9-4 Properties of Hierarchical Archimedean Copulas Ostap Okhrin* Yarema Okhrin** Wolfgang Schmid*** *Humboldt-Universität zu Berlin, Germany **Universität Bern, Switzerland ***Universität

A simple graphical method to explore tail-dependence in stock-return pairs

A simple graphical method to explore tail-dependence in stock-return pairs Klaus Abberger, University of Konstanz, Germany Abstract: For a bivariate data set the dependence structure can not only be measured

A simple graphical method to explore tail-dependence in stock-return pairs Klaus Abberger, University of Konstanz, Germany Abstract: For a bivariate data set the dependence structure can not only be measured

Behaviour of multivariate tail dependence coefficients

ACTA ET COMMENTATIONES UNIVERSITATIS TARTUENSIS DE MATHEMATICA Volume 22, Number 2, December 2018 Available online at http://acutm.math.ut.ee Behaviour of multivariate tail dependence coefficients Gaida

ACTA ET COMMENTATIONES UNIVERSITATIS TARTUENSIS DE MATHEMATICA Volume 22, Number 2, December 2018 Available online at http://acutm.math.ut.ee Behaviour of multivariate tail dependence coefficients Gaida

Elements of Financial Engineering Course

Elements of Financial Engineering Course Baruch-NSD Summer Camp 0 Lecture Tai-Ho Wang Agenda Methods of simulation: inverse transformation method, acceptance-rejection method Variance reduction techniques

Elements of Financial Engineering Course Baruch-NSD Summer Camp 0 Lecture Tai-Ho Wang Agenda Methods of simulation: inverse transformation method, acceptance-rejection method Variance reduction techniques

VaR bounds in models with partial dependence information on subgroups

VaR bounds in models with partial dependence information on subgroups L. Rüschendorf J. Witting February 23, 2017 Abstract We derive improved estimates for the model risk of risk portfolios when additional

VaR bounds in models with partial dependence information on subgroups L. Rüschendorf J. Witting February 23, 2017 Abstract We derive improved estimates for the model risk of risk portfolios when additional

Elements of Financial Engineering Course

Elements of Financial Engineering Course NSD Baruch MFE Summer Camp 206 Lecture 6 Tai Ho Wang Agenda Methods of simulation: inverse transformation method, acceptance rejection method Variance reduction

Elements of Financial Engineering Course NSD Baruch MFE Summer Camp 206 Lecture 6 Tai Ho Wang Agenda Methods of simulation: inverse transformation method, acceptance rejection method Variance reduction

Operational Risk and Pareto Lévy Copulas

Operational Risk and Pareto Lévy Copulas Claudia Klüppelberg Technische Universität München email: cklu@ma.tum.de http://www-m4.ma.tum.de References: - Böcker, K. and Klüppelberg, C. (25) Operational VaR

Operational Risk and Pareto Lévy Copulas Claudia Klüppelberg Technische Universität München email: cklu@ma.tum.de http://www-m4.ma.tum.de References: - Böcker, K. and Klüppelberg, C. (25) Operational VaR

MODELS FOR CONSTRUCTION OF MULTIVARIATE DEPENDENCE - A COMPARISON STUDY

MODELS FOR CONSTRUCTION OF MULTIVARIATE DEPENDENCE - A COMPARISON STUDY Kjersti Aas & Daniel Berg Abstract A multivariate data set, which exhibit complex patterns of dependence, particularly in the tails,

MODELS FOR CONSTRUCTION OF MULTIVARIATE DEPENDENCE - A COMPARISON STUDY Kjersti Aas & Daniel Berg Abstract A multivariate data set, which exhibit complex patterns of dependence, particularly in the tails,

Nonparametric Estimation of the Dependence Function for a Multivariate Extreme Value Distribution

Nonparametric Estimation of the Dependence Function for a Multivariate Extreme Value Distribution p. /2 Nonparametric Estimation of the Dependence Function for a Multivariate Extreme Value Distribution

Nonparametric Estimation of the Dependence Function for a Multivariate Extreme Value Distribution p. /2 Nonparametric Estimation of the Dependence Function for a Multivariate Extreme Value Distribution

Rearrangement Algorithm and Maximum Entropy

University of Illinois at Chicago Joint with Carole Bernard Vrije Universiteit Brussel and Steven Vanduffel Vrije Universiteit Brussel R/Finance, May 19-20, 2017 Introduction An important problem in Finance:

University of Illinois at Chicago Joint with Carole Bernard Vrije Universiteit Brussel and Steven Vanduffel Vrije Universiteit Brussel R/Finance, May 19-20, 2017 Introduction An important problem in Finance:

On the Estimation and Application of Max-Stable Processes

On the Estimation and Application of Max-Stable Processes Zhengjun Zhang Department of Statistics University of Wisconsin Madison, WI 53706, USA Co-author: Richard Smith EVA 2009, Fort Collins, CO Z. Zhang

On the Estimation and Application of Max-Stable Processes Zhengjun Zhang Department of Statistics University of Wisconsin Madison, WI 53706, USA Co-author: Richard Smith EVA 2009, Fort Collins, CO Z. Zhang

X

Correlation: Pitfalls and Alternatives Paul Embrechts, Alexander McNeil & Daniel Straumann Departement Mathematik, ETH Zentrum, CH-8092 Zürich Tel: +41 1 632 61 62, Fax: +41 1 632 15 23 embrechts/mcneil/strauman@math.ethz.ch

Correlation: Pitfalls and Alternatives Paul Embrechts, Alexander McNeil & Daniel Straumann Departement Mathematik, ETH Zentrum, CH-8092 Zürich Tel: +41 1 632 61 62, Fax: +41 1 632 15 23 embrechts/mcneil/strauman@math.ethz.ch

1 Introduction. Amir T. Payandeh Najafabadi 1, Mohammad R. Farid-Rohani 1, Marjan Qazvini 2

JIRSS (213) Vol. 12, No. 2, pp 321-334 A GLM-Based Method to Estimate a Copula s Parameter(s) Amir T. Payandeh Najafabadi 1, Mohammad R. Farid-Rohani 1, Marjan Qazvini 2 1 Mathematical Sciences Department,

JIRSS (213) Vol. 12, No. 2, pp 321-334 A GLM-Based Method to Estimate a Copula s Parameter(s) Amir T. Payandeh Najafabadi 1, Mohammad R. Farid-Rohani 1, Marjan Qazvini 2 1 Mathematical Sciences Department,

Sum of Two Standard Uniform Random Variables

Sum of Two Standard Uniform Random Variables Ruodu Wang http://sas.uwaterloo.ca/~wang Department of Statistics and Actuarial Science University of Waterloo, Canada Dependence Modeling in Finance, Insurance

Sum of Two Standard Uniform Random Variables Ruodu Wang http://sas.uwaterloo.ca/~wang Department of Statistics and Actuarial Science University of Waterloo, Canada Dependence Modeling in Finance, Insurance

Stochastic orders: a brief introduction and Bruno s contributions. Franco Pellerey

Stochastic orders: a brief introduction and Bruno s contributions. Franco Pellerey Stochastic orders (comparisons) Among his main interests in research activity A field where his contributions are still

Stochastic orders: a brief introduction and Bruno s contributions. Franco Pellerey Stochastic orders (comparisons) Among his main interests in research activity A field where his contributions are still

Risk Aggregation and Model Uncertainty

Risk Aggregation and Model Uncertainty Paul Embrechts RiskLab, Department of Mathematics, ETH Zurich Senior SFI Professor www.math.ethz.ch/ embrechts/ Joint work with A. Beleraj, G. Puccetti and L. Rüschendorf

Risk Aggregation and Model Uncertainty Paul Embrechts RiskLab, Department of Mathematics, ETH Zurich Senior SFI Professor www.math.ethz.ch/ embrechts/ Joint work with A. Beleraj, G. Puccetti and L. Rüschendorf

8 Copulas. 8.1 Introduction

8 Copulas 8.1 Introduction Copulas are a popular method for modeling multivariate distributions. A copula models the dependence and only the dependence between the variates in a multivariate distribution

8 Copulas 8.1 Introduction Copulas are a popular method for modeling multivariate distributions. A copula models the dependence and only the dependence between the variates in a multivariate distribution

Package CopulaRegression

Type Package Package CopulaRegression Title Bivariate Copula Based Regression Models Version 0.1-5 Depends R (>= 2.11.0), MASS, VineCopula Date 2014-09-04 Author, Daniel Silvestrini February 19, 2015 Maintainer

Type Package Package CopulaRegression Title Bivariate Copula Based Regression Models Version 0.1-5 Depends R (>= 2.11.0), MASS, VineCopula Date 2014-09-04 Author, Daniel Silvestrini February 19, 2015 Maintainer

Risk Aggregation with Dependence Uncertainty

Introduction Extreme Scenarios Asymptotic Behavior Challenges Risk Aggregation with Dependence Uncertainty Department of Statistics and Actuarial Science University of Waterloo, Canada Seminar at ETH Zurich

Introduction Extreme Scenarios Asymptotic Behavior Challenges Risk Aggregation with Dependence Uncertainty Department of Statistics and Actuarial Science University of Waterloo, Canada Seminar at ETH Zurich

EVANESCE Implementation in S-PLUS FinMetrics Module. July 2, Insightful Corp

EVANESCE Implementation in S-PLUS FinMetrics Module July 2, 2002 Insightful Corp The Extreme Value Analysis Employing Statistical Copula Estimation (EVANESCE) library for S-PLUS FinMetrics module provides

EVANESCE Implementation in S-PLUS FinMetrics Module July 2, 2002 Insightful Corp The Extreme Value Analysis Employing Statistical Copula Estimation (EVANESCE) library for S-PLUS FinMetrics module provides

Evolution of copulas: Continuous, D Title Application to Quantitative Risk Ma

Evolution of copulas: Continuous, D Title Application to Quantitative Risk Ma Author(s) YOSHIZAWA, Yasukazu Citation Issue 2015-03-20 Date Type Thesis or Dissertation Text Version ETD URL http://doi.org/10.15057/27116

Evolution of copulas: Continuous, D Title Application to Quantitative Risk Ma Author(s) YOSHIZAWA, Yasukazu Citation Issue 2015-03-20 Date Type Thesis or Dissertation Text Version ETD URL http://doi.org/10.15057/27116

CONTAGION VERSUS FLIGHT TO QUALITY IN FINANCIAL MARKETS

EVA IV, CONTAGION VERSUS FLIGHT TO QUALITY IN FINANCIAL MARKETS Jose Olmo Department of Economics City University, London (joint work with Jesús Gonzalo, Universidad Carlos III de Madrid) 4th Conference

EVA IV, CONTAGION VERSUS FLIGHT TO QUALITY IN FINANCIAL MARKETS Jose Olmo Department of Economics City University, London (joint work with Jesús Gonzalo, Universidad Carlos III de Madrid) 4th Conference

A New Family of Bivariate Copulas Generated by Univariate Distributions 1

Journal of Data Science 1(212), 1-17 A New Family of Bivariate Copulas Generated by Univariate Distributions 1 Xiaohu Li and Rui Fang Xiamen University Abstract: A new family of copulas generated by a

Journal of Data Science 1(212), 1-17 A New Family of Bivariate Copulas Generated by Univariate Distributions 1 Xiaohu Li and Rui Fang Xiamen University Abstract: A new family of copulas generated by a

Construction and estimation of high dimensional copulas

Construction and estimation of high dimensional copulas Gildas Mazo PhD work supervised by S. Girard and F. Forbes Mistis, Inria and laboratoire Jean Kuntzmann, Grenoble, France Séminaire Statistiques,

Construction and estimation of high dimensional copulas Gildas Mazo PhD work supervised by S. Girard and F. Forbes Mistis, Inria and laboratoire Jean Kuntzmann, Grenoble, France Séminaire Statistiques,

Copula-based top-down approaches in financial risk aggregation

Number 3 Working Paper Series by the University of Applied Sciences of bfi Vienna Copula-based top-down approaches in financial risk aggregation December 6 Christian Cech University of Applied Sciences

Number 3 Working Paper Series by the University of Applied Sciences of bfi Vienna Copula-based top-down approaches in financial risk aggregation December 6 Christian Cech University of Applied Sciences

Estimation of Operational Risk Capital Charge under Parameter Uncertainty

Estimation of Operational Risk Capital Charge under Parameter Uncertainty Pavel V. Shevchenko Principal Research Scientist, CSIRO Mathematical and Information Sciences, Sydney, Locked Bag 17, North Ryde,

Estimation of Operational Risk Capital Charge under Parameter Uncertainty Pavel V. Shevchenko Principal Research Scientist, CSIRO Mathematical and Information Sciences, Sydney, Locked Bag 17, North Ryde,

On the Choice of Parametric Families of Copulas

On the Choice of Parametric Families of Copulas Radu Craiu Department of Statistics University of Toronto Collaborators: Mariana Craiu, University Politehnica, Bucharest Vienna, July 2008 Outline 1 Brief

On the Choice of Parametric Families of Copulas Radu Craiu Department of Statistics University of Toronto Collaborators: Mariana Craiu, University Politehnica, Bucharest Vienna, July 2008 Outline 1 Brief

GENERAL MULTIVARIATE DEPENDENCE USING ASSOCIATED COPULAS

REVSTAT Statistical Journal Volume 14, Number 1, February 2016, 1 28 GENERAL MULTIVARIATE DEPENDENCE USING ASSOCIATED COPULAS Author: Yuri Salazar Flores Centre for Financial Risk, Macquarie University,

REVSTAT Statistical Journal Volume 14, Number 1, February 2016, 1 28 GENERAL MULTIVARIATE DEPENDENCE USING ASSOCIATED COPULAS Author: Yuri Salazar Flores Centre for Financial Risk, Macquarie University,

Non-Life Insurance: Mathematics and Statistics

ETH Zürich, D-MATH HS 08 Prof. Dr. Mario V. Wüthrich Coordinator Andrea Gabrielli Non-Life Insurance: Mathematics and Statistics Solution sheet 9 Solution 9. Utility Indifference Price (a) Suppose that

ETH Zürich, D-MATH HS 08 Prof. Dr. Mario V. Wüthrich Coordinator Andrea Gabrielli Non-Life Insurance: Mathematics and Statistics Solution sheet 9 Solution 9. Utility Indifference Price (a) Suppose that

Counts using Jitters joint work with Peng Shi, Northern Illinois University

of Claim Longitudinal of Claim joint work with Peng Shi, Northern Illinois University UConn Actuarial Science Seminar 2 December 2011 Department of Mathematics University of Connecticut Storrs, Connecticut,

of Claim Longitudinal of Claim joint work with Peng Shi, Northern Illinois University UConn Actuarial Science Seminar 2 December 2011 Department of Mathematics University of Connecticut Storrs, Connecticut,

Simulation of Tail Dependence in Cot-copula

Int Statistical Inst: Proc 58th World Statistical Congress, 0, Dublin (Session CPS08) p477 Simulation of Tail Dependence in Cot-copula Pirmoradian, Azam Institute of Mathematical Sciences, Faculty of Science,

Int Statistical Inst: Proc 58th World Statistical Congress, 0, Dublin (Session CPS08) p477 Simulation of Tail Dependence in Cot-copula Pirmoradian, Azam Institute of Mathematical Sciences, Faculty of Science,

A measure of radial asymmetry for bivariate copulas based on Sobolev norm

A measure of radial asymmetry for bivariate copulas based on Sobolev norm Ahmad Alikhani-Vafa Ali Dolati Abstract The modified Sobolev norm is used to construct an index for measuring the degree of radial

A measure of radial asymmetry for bivariate copulas based on Sobolev norm Ahmad Alikhani-Vafa Ali Dolati Abstract The modified Sobolev norm is used to construct an index for measuring the degree of radial

Copula methods in Finance

Wolfgang K. Härdle Ostap Okhrin Ladislaus von Bortkiewicz Chair of Statistics C.A.S.E. Center for Applied Statistics and Economics Humboldt-Universität zu Berlin http://ise.wiwi.hu-berlin.de Motivation

Wolfgang K. Härdle Ostap Okhrin Ladislaus von Bortkiewicz Chair of Statistics C.A.S.E. Center for Applied Statistics and Economics Humboldt-Universität zu Berlin http://ise.wiwi.hu-berlin.de Motivation

EXTREMAL DEPENDENCE OF MULTIVARIATE DISTRIBUTIONS AND ITS APPLICATIONS YANNAN SUN

EXTREMAL DEPENDENCE OF MULTIVARIATE DISTRIBUTIONS AND ITS APPLICATIONS By YANNAN SUN A dissertation submitted in partial fulfillment of the requirements for the degree of DOCTOR OF PHILOSOPHY WASHINGTON

EXTREMAL DEPENDENCE OF MULTIVARIATE DISTRIBUTIONS AND ITS APPLICATIONS By YANNAN SUN A dissertation submitted in partial fulfillment of the requirements for the degree of DOCTOR OF PHILOSOPHY WASHINGTON

ISSN Distortion risk measures for sums of dependent losses

Journal Afrika Statistika Journal Afrika Statistika Vol. 5, N 9, 21, page 26 267. ISSN 852-35 Distortion risk measures for sums of dependent losses Brahim Brahimi, Djamel Meraghni, and Abdelhakim Necir

Journal Afrika Statistika Journal Afrika Statistika Vol. 5, N 9, 21, page 26 267. ISSN 852-35 Distortion risk measures for sums of dependent losses Brahim Brahimi, Djamel Meraghni, and Abdelhakim Necir

arxiv: v1 [math.st] 31 Oct 2014

![arxiv: v1 [math.st] 31 Oct 2014](/thumbs/86/93348804.jpg "arxiv: v1 [math.st] 31 Oct 2014") A two-component copula with links to insurance arxiv:1410.8740v1 [math.st] 31 Oct 2014 S. Ismail 1 3, G. Yu 2 4, G. Reinert 1, 5 and T. Maynard 2 5 1 Department of Statistics, 1 South Parks Road, Oxford

A two-component copula with links to insurance arxiv:1410.8740v1 [math.st] 31 Oct 2014 S. Ismail 1 3, G. Yu 2 4, G. Reinert 1, 5 and T. Maynard 2 5 1 Department of Statistics, 1 South Parks Road, Oxford

COPULA FITTING TO AUTOCORRELATED DATA, WITH APPLICATIONS TO WIND SPEED MODELLING

Annales Univ. Sci. Budapest., Sect. Comp. 43 (2014) 3 19 COPULA FITTING TO AUTOCORRELATED DATA, WITH APPLICATIONS TO WIND SPEED MODELLING Pál Rakonczai (Budapest, Hungary) László Varga (Budapest, Hungary)

Annales Univ. Sci. Budapest., Sect. Comp. 43 (2014) 3 19 COPULA FITTING TO AUTOCORRELATED DATA, WITH APPLICATIONS TO WIND SPEED MODELLING Pál Rakonczai (Budapest, Hungary) László Varga (Budapest, Hungary)

Asymptotics for Risk Capital Allocations based on Conditional Tail Expectation

Asymptotics for Risk Capital Allocations based on Conditional Tail Expectation Alexandru V. Asimit Cass Business School, City University, London EC1Y 8TZ, United Kingdom. E-mail: asimit@city.ac.uk Edward

Asymptotics for Risk Capital Allocations based on Conditional Tail Expectation Alexandru V. Asimit Cass Business School, City University, London EC1Y 8TZ, United Kingdom. E-mail: asimit@city.ac.uk Edward

An empirical analysis of multivariate copula models

An empirical analysis of multivariate copula models Matthias Fischer and Christian Köck Friedrich-Alexander-Universität Erlangen-Nürnberg, Germany Homepage: www.statistik.wiso.uni-erlangen.de E-mail: matthias.fischer@wiso.uni-erlangen.de

An empirical analysis of multivariate copula models Matthias Fischer and Christian Köck Friedrich-Alexander-Universität Erlangen-Nürnberg, Germany Homepage: www.statistik.wiso.uni-erlangen.de E-mail: matthias.fischer@wiso.uni-erlangen.de

A novel multivariate risk measure: the Kendall VaR

A novel multivariate risk measure: the Kendall VaR Matthieu Garcin, Dominique Guegan, Bertrand Hassani To cite this version: Matthieu Garcin, Dominique Guegan, Bertrand Hassani. A novel multivariate risk

A novel multivariate risk measure: the Kendall VaR Matthieu Garcin, Dominique Guegan, Bertrand Hassani To cite this version: Matthieu Garcin, Dominique Guegan, Bertrand Hassani. A novel multivariate risk

Bivariate extension of the Pickands Balkema de Haan theorem

Ann. I. H. Poincaré PR 40 (004) 33 4 www.elsevier.com/locate/anihpb Bivariate extension of the Pickands Balkema de Haan theorem Mario V. Wüthrich Winterthur Insurance, Römerstrasse 7, P.O. Box 357, CH-840

Ann. I. H. Poincaré PR 40 (004) 33 4 www.elsevier.com/locate/anihpb Bivariate extension of the Pickands Balkema de Haan theorem Mario V. Wüthrich Winterthur Insurance, Römerstrasse 7, P.O. Box 357, CH-840

Time Varying Hierarchical Archimedean Copulae (HALOC)

") Time Varying Hierarchical Archimedean Copulae () Wolfgang Härdle Ostap Okhrin Yarema Okhrin Ladislaus von Bortkiewicz Chair of Statistics C.A.S.E. Center for Applied Statistics and Economics Humboldt-Universität

Time Varying Hierarchical Archimedean Copulae () Wolfgang Härdle Ostap Okhrin Yarema Okhrin Ladislaus von Bortkiewicz Chair of Statistics C.A.S.E. Center for Applied Statistics and Economics Humboldt-Universität

MULTIDIMENSIONAL POVERTY MEASUREMENT: DEPENDENCE BETWEEN WELL-BEING DIMENSIONS USING COPULA FUNCTION

Rivista Italiana di Economia Demografia e Statistica Volume LXXII n. 3 Luglio-Settembre 2018 MULTIDIMENSIONAL POVERTY MEASUREMENT: DEPENDENCE BETWEEN WELL-BEING DIMENSIONS USING COPULA FUNCTION Kateryna

Rivista Italiana di Economia Demografia e Statistica Volume LXXII n. 3 Luglio-Settembre 2018 MULTIDIMENSIONAL POVERTY MEASUREMENT: DEPENDENCE BETWEEN WELL-BEING DIMENSIONS USING COPULA FUNCTION Kateryna

Multivariate Distribution Models

Multivariate Distribution Models Model Description While the probability distribution for an individual random variable is called marginal, the probability distribution for multiple random variables is

Multivariate Distribution Models Model Description While the probability distribution for an individual random variable is called marginal, the probability distribution for multiple random variables is

Losses Given Default in the Presence of Extreme Risks

Losses Given Default in the Presence of Extreme Risks Qihe Tang [a] and Zhongyi Yuan [b] [a] Department of Statistics and Actuarial Science University of Iowa [b] Smeal College of Business Pennsylvania

Losses Given Default in the Presence of Extreme Risks Qihe Tang [a] and Zhongyi Yuan [b] [a] Department of Statistics and Actuarial Science University of Iowa [b] Smeal College of Business Pennsylvania

Dependence. MFM Practitioner Module: Risk & Asset Allocation. John Dodson. September 11, Dependence. John Dodson. Outline.

MFM Practitioner Module: Risk & Asset Allocation September 11, 2013 Before we define dependence, it is useful to define Random variables X and Y are independent iff For all x, y. In particular, F (X,Y

MFM Practitioner Module: Risk & Asset Allocation September 11, 2013 Before we define dependence, it is useful to define Random variables X and Y are independent iff For all x, y. In particular, F (X,Y

Dependence Patterns across Financial Markets: a Mixed Copula Approach

Dependence Patterns across Financial Markets: a Mixed Copula Approach Ling Hu This Draft: October 23 Abstract Using the concept of a copula, this paper shows how to estimate association across financial

Dependence Patterns across Financial Markets: a Mixed Copula Approach Ling Hu This Draft: October 23 Abstract Using the concept of a copula, this paper shows how to estimate association across financial

GENERAL MULTIVARIATE DEPENDENCE USING ASSOCIATED COPULAS

GENERAL MULTIVARIATE DEPENDENCE USING ASSOCIATED COPULAS YURI SALAZAR FLORES University of Essex, Wivenhoe Park, CO4 3SQ, Essex, UK. ysalaz@essex.ac.uk Abstract. This paper studies the general multivariate

GENERAL MULTIVARIATE DEPENDENCE USING ASSOCIATED COPULAS YURI SALAZAR FLORES University of Essex, Wivenhoe Park, CO4 3SQ, Essex, UK. ysalaz@essex.ac.uk Abstract. This paper studies the general multivariate

Systemic Weather Risk and Crop Insurance: The Case of China

and Crop Insurance: The Case of China Ostap Okhrin 1 Martin Odening 2 Wei Xu 3 Ladislaus von Bortkiewicz Chair of Statistics C.A.S.E. Center for Applied Statistics and Economics 1 Department of Agricultural

and Crop Insurance: The Case of China Ostap Okhrin 1 Martin Odening 2 Wei Xu 3 Ladislaus von Bortkiewicz Chair of Statistics C.A.S.E. Center for Applied Statistics and Economics 1 Department of Agricultural

Bayesian inference for multivariate copulas using pair-copula constructions

Bayesian inference for multivariate copulas using pair-copula constructions Aleksey MIN and Claudia CZADO Munich University of Technology Munich University of Technology Corresponding author: Aleksey Min

Bayesian inference for multivariate copulas using pair-copula constructions Aleksey MIN and Claudia CZADO Munich University of Technology Munich University of Technology Corresponding author: Aleksey Min

Conditional Least Squares and Copulae in Claims Reserving for a Single Line of Business

Conditional Least Squares and Copulae in Claims Reserving for a Single Line of Business Michal Pešta Charles University in Prague Faculty of Mathematics and Physics Ostap Okhrin Dresden University of Technology

Conditional Least Squares and Copulae in Claims Reserving for a Single Line of Business Michal Pešta Charles University in Prague Faculty of Mathematics and Physics Ostap Okhrin Dresden University of Technology

Construction of asymmetric multivariate copulas

Construction of asymmetric multivariate copulas Eckhard Liebscher University of Applied Sciences Merseburg Department of Computer Sciences and Communication Systems Geusaer Straße 0627 Merseburg Germany

Construction of asymmetric multivariate copulas Eckhard Liebscher University of Applied Sciences Merseburg Department of Computer Sciences and Communication Systems Geusaer Straße 0627 Merseburg Germany

Study Guide on Dependency Modeling for the Casualty Actuarial Society (CAS) Exam 7 (Based on Sholom Feldblum's Paper, Dependency Modeling)

Exam 7 (Based on Sholom Feldblum's Paper, Dependency Modeling)") Study Guide on Dependency Modeling for the Casualty Actuarial Society Exam 7 - G. Stolyarov II Study Guide on Dependency Modeling for the Casualty Actuarial Society (CAS) Exam 7 (Based on Sholom Feldblum's

Study Guide on Dependency Modeling for the Casualty Actuarial Society Exam 7 - G. Stolyarov II Study Guide on Dependency Modeling for the Casualty Actuarial Society (CAS) Exam 7 (Based on Sholom Feldblum's

Dependence and VaR Estimation:An Empirical Study of Chinese Stock Markets using Copula. Baoliang Li WISE, XMU Sep. 2009

Dependence and VaR Estimation:An Empirical Study of Chinese Stock Markets using Copula Baoliang Li WISE, XMU Sep. 2009 Outline Question: Dependence between Assets Correlation and Dependence Copula:Basics

Dependence and VaR Estimation:An Empirical Study of Chinese Stock Markets using Copula Baoliang Li WISE, XMU Sep. 2009 Outline Question: Dependence between Assets Correlation and Dependence Copula:Basics

Using copulas to model time dependence in stochastic frontier models

Using copulas to model time dependence in stochastic frontier models Christine Amsler Michigan State University Artem Prokhorov Concordia University November 2008 Peter Schmidt Michigan State University

Using copulas to model time dependence in stochastic frontier models Christine Amsler Michigan State University Artem Prokhorov Concordia University November 2008 Peter Schmidt Michigan State University

ON UNIFORM TAIL EXPANSIONS OF BIVARIATE COPULAS

APPLICATIONES MATHEMATICAE 31,4 2004), pp. 397 415 Piotr Jaworski Warszawa) ON UNIFORM TAIL EXPANSIONS OF BIVARIATE COPULAS Abstract. The theory of copulas provides a useful tool for modelling dependence

APPLICATIONES MATHEMATICAE 31,4 2004), pp. 397 415 Piotr Jaworski Warszawa) ON UNIFORM TAIL EXPANSIONS OF BIVARIATE COPULAS Abstract. The theory of copulas provides a useful tool for modelling dependence

Multivariate Non-Normally Distributed Random Variables

Multivariate Non-Normally Distributed Random Variables An Introduction to the Copula Approach Workgroup seminar on climate dynamics Meteorological Institute at the University of Bonn 18 January 2008, Bonn

Multivariate Non-Normally Distributed Random Variables An Introduction to the Copula Approach Workgroup seminar on climate dynamics Meteorological Institute at the University of Bonn 18 January 2008, Bonn

Probabilistic Engineering Mechanics. An innovating analysis of the Nataf transformation from the copula viewpoint

Probabilistic Engineering Mechanics 4 9 3 3 Contents lists available at ScienceDirect Probabilistic Engineering Mechanics journal homepage: www.elsevier.com/locate/probengmech An innovating analysis of

Probabilistic Engineering Mechanics 4 9 3 3 Contents lists available at ScienceDirect Probabilistic Engineering Mechanics journal homepage: www.elsevier.com/locate/probengmech An innovating analysis of

Tail comonotonicity: properties, constructions, and asymptotic additivity of risk measures

Tail comonotonicity: properties, constructions, and asymptotic additivity of risk measures Lei Hua Harry Joe June 5, 2012 Abstract. We investigate properties of a version of tail comonotonicity that can

Tail comonotonicity: properties, constructions, and asymptotic additivity of risk measures Lei Hua Harry Joe June 5, 2012 Abstract. We investigate properties of a version of tail comonotonicity that can

Convexity of chance constraints with dependent random variables: the use of copulae

Convexity of chance constraints with dependent random variables: the use of copulae René Henrion 1 and Cyrille Strugarek 2 1 Weierstrass Institute for Applied Analysis and Stochastics, 10117 Berlin, Germany.

Convexity of chance constraints with dependent random variables: the use of copulae René Henrion 1 and Cyrille Strugarek 2 1 Weierstrass Institute for Applied Analysis and Stochastics, 10117 Berlin, Germany.

Operational Risk and Pareto Lévy Copulas

Operational Risk and Pareto Lévy Copulas Claudia Klüppelberg Technische Universität München email: cklu@ma.tum.de http://www-m4.ma.tum.de References: - Böcker, K. and Klüppelberg, C. (25) Operational VaR

Operational Risk and Pareto Lévy Copulas Claudia Klüppelberg Technische Universität München email: cklu@ma.tum.de http://www-m4.ma.tum.de References: - Böcker, K. and Klüppelberg, C. (25) Operational VaR